• HUD and Census Bureau Report New Residential Sales in July 2025

• HUD Unveils Exhibitors for the 2025 Innovative Housing Showcase on the National Mall

• HUD Announces Sponsors for the 2025 Innovative Housing Showcase

• ICYMI | HUD Regional Administrator Quinonez on HUD’s Support for Foster Youth in Texas

ARTICLES BY ERIC

• Southern California Rentals in 2025: The Hidden Upside for OC Landlords Amid Supply Constraints

• Insurance & Climate Resilience: The New Hidden Costs of Owning in Orange County

• Days on Market and Negotiation Shifts: How Buyer Leverage Is Evolving in Fall 2025

• How Climate Risks Are Reshaping Insurance, Disclosures & Lending in High-Risk Neighborhoods

• How Retirees Are Reshaping Orange County’s Housing Market

• Market Signals from the Top: What Orange County’s HighEnd Price Adjustments Mean for Everyday Buyers and Sellers

• Equity Through Conversion: How Rezoning and Redevelopment Are Unlocking Hidden Value for Owners

• Micro-Markets That Hold Firm: Which Orange County Neighborhoods Are Winning in 2025

• The Rise of the Hybrid Seller: Balancing Cash Buyers, iBuyers, and Traditional Offers in Orange County

• Mortgage Rates and Buyer Psychology: How Orange County Households Are Adjusting in a 6–7% Rate Environment

• Inventory Squeeze and New Construction Slowdown — Why Orange County Buyers Face Limited Choices in 2025

• California’s 2025 Housing Reforms: How New State Laws Will Reshape Orange County’s Market

Housing is more than just a roof over our heads it is the foundation of family, community, and opportunity. Every month, the U.S. Department of Housing and Urban Development (HUD) plays a critical role in shaping that foundation through its programs, initiatives, and property listings At HUD Magazine, our mission is to make those updates accessible, timely, and meaningful for you whether you are a homebuyer, a housing professional, or a policymaker

I am pleased to welcome you to the October issue of HUD Magazine, an edition filled with important updates and resources that highlight HUD’s continuing work to expand housing access and strengthen communities across the country.

This month’s press releases provide a wealth of insight into the federal government’s housing agenda. You will find updates on affordable housing investments, fair housing enforcement, rental assistance, and disaster recovery efforts Each release reflects HUD’s ongoing commitment to addressing the challenges of affordability, equity, and sustainability in the housing market. For professionals in real estate, mortgage lending, and community development, these announcements serve as both a guidepost and a call to action They remind us that housing policy is not abstract it has a direct and daily impact on the lives of millions of Americans

Alongside these announcements, this issue also features our signature HUD property listings These listings are an invaluable tool for buyers seeking affordable entry points into homeownership and for investors committed to revitalizing neighborhoods. Each property tells its own story: a home in need of a new family, a block awaiting renewal, or a community gaining stability through investment. By publishing these listings, we connect opportunity with action linking available homes to people ready to take the next step in their journey toward ownership

October is a time of reflection and preparation. As the fall season begins, the housing market itself is in transition Rising interest rates, shifting buyer demand, and evolving regulatory frameworks all contribute to a marketplace that requires attention, adaptability, and informed decision-making HUD’s updates this month address these realities head-on, offering clarity at a moment when uncertainty often dominates the headlines.

Eric Lawrence Frazier, MBA - Principal advisor

One of the strengths of HUD Magazine is its ability to bring together national updates and practical resources. Our goal is not only to share what HUD is doing at a policy level but also to provide you with tools you can use today Whether you are a first-time buyer scanning the listings, a housing counselor guiding families, or an investor looking for ways to make a positive impact, the information in these pages was curated with you in mind.

I also want to emphasize that this publication is not meant to be read in isolation. Share these updates with your networks, discuss them within your organizations, and apply them in your communities. Housing is both a personal and collective journey The more we engage with these resources together, the closer we come to ensuring housing stability and opportunity for all.

As you explore this month’s issue, I encourage you to think beyond the listings and announcements. Consider how each piece of information connects to the broader vision of building stronger, more equitable communities. HUD’s mission is not only about homes; it is about creating pathways for families to thrive, for neighborhoods to grow, and for the promise of opportunity to remain within reach for every American.

Thank you for joining us this October. I hope the insights and resources in this issue inform, inspire, and empower you

HAPPY READING

EDITOR IN CHIEF

Eric Lawrence Frazier, MBA

Your trusted advisor in business and wealth www ericfrazier com | www thepowerisnow com | www ericfrazier net NMLS #451807 | CA DRE #01143484

Eric Lawrence Frazier, MBA - Principal advisor

Eric

Eric

Eric Lawrence Frazier, MBA

Lawrence Frazier, MBA

Eric

Eric

Eric

Lawrence Frazier, MBA

Eric

Eric Lawrence Frazier, MBA

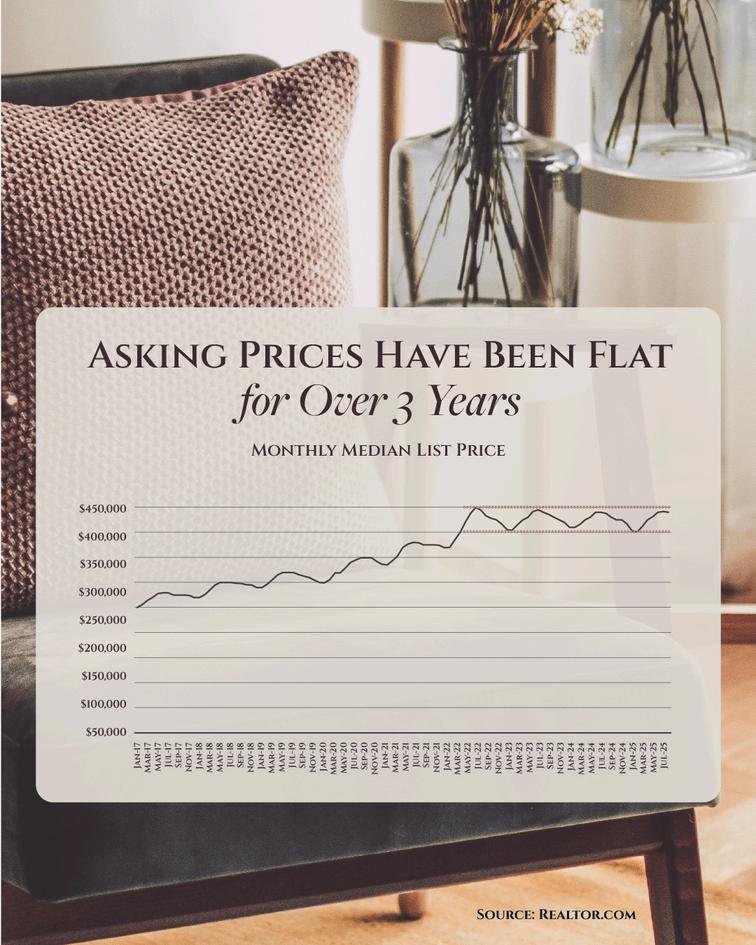

If your listing isn’t getting traction, here's what you need to realize Homes are sitting longer today And one of the reasons why?

Overpricing like it’s 2021 again. Unlike a normal market where list prices keep rising, they’ve actually been flat for over 3 years. And that’s a change worth paying attention to

List prices have leveled off because buyers are being more selective as inventory has grown over the past few years There are more homes on the market, and sellers need to take note.

So, if your home isn’t getting showings or offers, take it as a sign to check in with your agent A small price adjustment could be the move that gets buyers through the door

Because in a market like this you can’t just wait it out and hope for the best. Patience won’t sell your house. But the right price will.

Eric Lawrence Frazier, MBA - Principal advisor

Eric Lawrence Frazier,

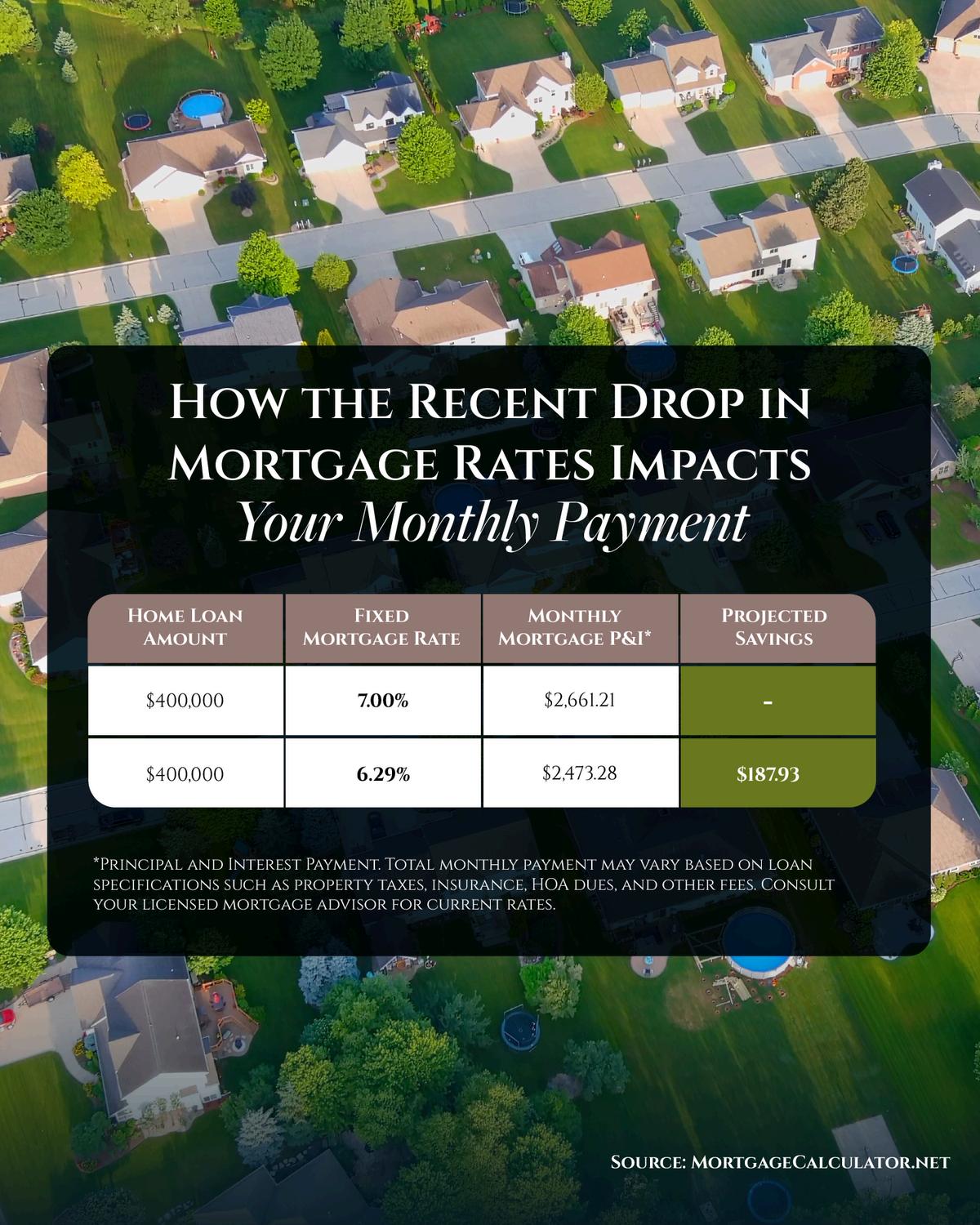

Biggest One-Day Mortgage Rate Drop

Mortgage rates just had their biggest one-day drop in over a year.

They fell to the lowest they've been since last October.

And that shift matters. Compared to when rates were at 7% earlier this year, that could mean your future monthly payment is now about $200 lower

Want to know how much you could save if you’re looking to buy? Message me and let’s talk it over.

Eric Lawrence Frazier, MBA - Principal advisor

mortgage

Eric Lawrence Frazier, MBA - Principal advisor

Eric

Eric Lawrence Frazier, MBA

Eric

Eric Lawrence Frazier, MBA - Principal advisor

Eric Lawrence Frazier,

Eric

About half of homes are selling for under their asking price right now

While that feels very different from the past few years, it’s actually a return to what’s considered normal for the market.

And the sellers who succeed today are the ones who recognize this shift. They price smart from day one, make their home stand out, and stay flexible when buyers ask for give-and-take.

You need to plan for the market we’re in, not the one we saw a few years back. And I can help

Eric Lawrence Frazier, MBA - Principal advisor

Eric Lawrence Frazier,

Eric Lawrence Frazier, MBA

Eric

Eric

Buyers and Sellers Are Here

Reach out today for your digital copies

Your fall move just got easier The Fall Buyer & Seller Guides just dropped

These guides unpack the latest data, forecasts, and strategies you’ll need to make the right move in today’s market.

Find out what’s changing, what’s not, and what it all means for you as a buyer or seller this season

If you want the information serious buyers and sellers are using to stay ahead? DM me and I’ll send the guides your way.

Eric Lawrence Frazier, MBA - Principal advisor

Eric

Eric Lawrence Frazier, MBA

Eric Lawrence Frazier, MBA

Eric

) g , g g y y y That’s a big difference.

So, don’t let the headlines scare you. I’ve got the data that can replace fear with facts. This isn’t a sign of trouble – and we’re nowhere near crash levels, no matter what the headlines seem to say.

Eric Lawrence Frazier, MBA - Principal advisor Real estate & mortgage | business | finance | CA

Eric Lawrence Frazier, MBA

HUD and Census Bureau Report New Residential Sales in July 2025

WASHINGTON (August 25, 2025) - The U.S. Census Bureau and the U.S. Department of Housing and Urban Development jointly announced the following new residential sales statistics for July 2025:

New Home Sales

Sales of new single-family houses in July 2025 were at a seasonally-adjusted annual rate of 652,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 0.6 percent (±15.5 percent)* below the June 2025 rate of 656,000, and is 8.2 percent (±14.0 percent)* below the July 2024 rate of 710,000.

For Sale Inventory and Months' Supply

The seasonally-adjusted estimate of new houses for sale at the end of July 2025 was 499,000. This is 0.6 percent (±1.2 percent)* below the June 2025 estimate of 502,000, and is 7.3 percent (±5.7 percent) above the July 2024 estimate of 465,000. This represents a supply of 9.2 months at the current sales rate. The months' supply is virtually unchanged (±16.7 percent)* from the June 2025 estimate of 9.2 months, and is 16.5 percent (±19.0 percent)* above the July 2024 estimate of 7.9 months.

Sales Price

The median sales price of new houses sold in July 2025 was $403,800.

This is 0 8 percent (±5 9 percent)* below the June 2025 price of $407,200, and is 5.9 percent (±8.5 percent)* below the July 2024 price of $429,000. The average sales price of new houses sold in July 2025 was $487,300. This is 3.6 percent (±8.0 percent)* below the June 2025 price of $505,300, and is 5 0 percent (±8.6 percent)* below the July 2024 price of $513,200.

The August report is scheduled for release on September 24, 2025. View the full schedule in the Economic Briefing Room. The full text and tables for this release can be found here.

EXPLANATORY NOTES

These statistics are estimated from sample surveys. They are subject to sampling variability as well as nonsampling error including bias and variance from response, nonreporting, and undercoverage. Estimated average relative standard errors of the preliminary data are shown in the tables. Whenever a statement such as “2.5 percent (±3.2%) above” appears in the text, this indicates the range (-0.7 to +5.7 percent) in which the actual percent change is likely to have occurred. All ranges given for percent changes are 90-percent confidence intervals and account only for sampling variability. If a range does not contain zero, the change is statistically significant. If it does contain zero, the change is not statistically significant; that is, it is uncertain whether there was an increase or decrease. The same policies apply to the confidence intervals for percent changes shown in the tables. Changes in seasonally adjusted statistics often show irregular movement. It takes 3 months to establish a trend for new houses sold. Preliminary new home sales figures are subject to revision due to the survey methodology and definitions used. The survey is primarily based on a sample of houses selected from building permits. Since a “sale” is defined as a deposit taken or sales agreement signed, this can occur prior to a permit being issued

An estimate of these prior sales is included in the sales figure On average, the preliminary seasonally adjusted estimate of total sales is revised about 3.2 percent. Changes in sales price data reflect changes in the distribution of houses by region, size, etc., as well as changes in the prices of houses with identical characteristics. Explanations of confidence intervals and sampling variability can be found on our website.

The Census Bureau has reviewed SOC monthly and quarterly tables to ensure appropriate access, use, and disclosure avoidance protection of the confidential source data (Disclosure Review Board (DRB) approval number: CBDRBFY25-0286).

API

The Census Bureau’s application programming interface lets developers create custom apps to reach new users and makes key demographic, socio-economic and housing statistics more accessible than ever before.

FRED Mobile App

Receive the latest updates on the nation’s key economic indicators by downloading the FRED App for both Apple and Android devices. FRED, the signature database of the Federal Reserve Bank of St. Louis, now incorporates the Census Bureau’s 13 economic indicators.

* The 90 percent confidence interval includes zero. In such cases, there is insufficient statistical evidence to conclude that the actual change is different from zero.

HUD Unveils Exhibitors for the 2025 Innovative Housing Showcase on the National Mall

Showcase Returns on September 6th-10th to Celebrate 250 Years of the American Home

WASHINGTON - The U.S. Department of Housing and Urban Development (HUD) announced more than 25 exhibitors that will showcase innovative housing and construction technologies on the National Mall during HUD’s annual Innovative Housing Showcase, taking place September 6th-10th.

“HUD is proud to champion public-private partnerships across the nation,” said HUD Secretary Scott Turner. “This year’s Innovative Housing Showcase is historic. We look forward to welcoming thousands of attendees as they join us in celebrating American ingenuity, endurance, and free market innovation to see firsthand how Americans are making housing great again – all as part of the America 250 Initiative.”

This year’s theme, “The American Home Is the American Dream,” spotlights the American Dream of homeownership, the future of housing innovation, and history-defining events in housing. Part of the America 250 Initiative, the showcase commemorates America’s 250th birthday and the American values of independence and opportunity.

Founded in 2019 by former HUD Secretary Ben Carson, the showcase will feature a variety of full-scale housing models including manufactured, 3D printed, and modular homes built by American companies from across the nation To view the list of 2025 exhibitors, click here: https://www.huduser.gov/portal/ihs/Exhibitors-2025.html.

More Details About the 2025 Innovative Housing Showcase

A family-friendly event, the showcase is open to the public on the National Mall and expected to attract thousands of attendees, including Members of Congress, industry leaders, and community stakeholders. Visitors can view and enter exhibits on the Mall and attend expert-led panel discussions highlighting housing innovations. The panels are open to the public for in-person or virtual attendance. Register here: https://www.huduser.gov/portal/event/ihs2025.html

To view photos from past showcases, please visit IHS Past Showcases | HUD USER. For more information, please visit the Innovative Housing Showcase webpage.

HUD Announces Sponsors for the 2025 Innovative Housing Showcase

The Historic Showcase Returns to the National Mall September 6th - 10th Highlighting 250 Years of Innovation in American Housing

WASHINGTON - Today the U.S. Department of Housing and Urban Development (HUD) announced the presenting sponsors for the 2025 Innovative Housing Showcase: The International Code Council (ICC), The Manufactured Housing Institute (MHI), The Structural Building Components Association (SBCA), and The Home Depot.

As a proud part of the America 250 Initiative, the showcase will feature the theme, “The American Home Is The American Dream,” celebrating the evolution of homeownership over 250 years and how the American home is representative of the American values of independence, opportunity, and the unshakable drive to build a better life.

“This year’s Innovative Housing Showcase puts the spotlight on American grit and free market innovation - a powerful reminder that free enterprise, not big government, drives the American Dream of Homeownership,” said HUD Secretary Scott Turner. “HUD will continue to spotlight solutions that support quality, affordable homeownership opportunities for hardworking Americans. Together, we will usher in the Golden Age of American Homeownership.”

Founded in 2019 by former HUD Secretary Ben Carson, the showcase will feature a variety of full-scale housing models including manufactured, 3D printed, and modular homes from across the country displayed on the National Mall.

“The International Code Council is committed to supporting and facilitating the innovations necessary to make housing more affordable,” said John Belcik, Chief Executive Officer, International Code Council (ICC). “We are pleased to join HUD and other sponsors to highlight what is currently possible, and the policies, codes and standards that will continue to facilitate future progress.”

“MHI is excited to partner again with HUD to bring the 2025 Innovative Housing Showcase to the National Mall in celebration of the Showcase’s fifth year running and America’s 250th birthday. HUD Code manufactured homes have been bringing quality, attainable homeownership to Americans nationwide for fifty years MHI welcomes the opportunity to demonstrate the beauty and innovation in design, scalability, and efficiency of today’s manufactured homes and the solutions they offer to address the nation’s housing supply needs,” said Lesli Gooch, Chief Executive Officer, Manufactured Housing Institute (MHI).

“SBCA is excited to return to the National Mall as a co-sponsor and exhibitor for HUD’s Innovative Housing Showcase," said Jess Lohse, Executive Director, Structural Building Components Association (SBCA).

“This event is a powerful platform for sharing solutions to the housing challenges our country faces. As the voice of the structural building components industry, SBCA is proud to demonstrate how trusses and wall panels provide scalable, efficient building methods supporting greater housing availability, accessibility, and affordability. We’re honored to join HUD and our fellow co-sponsors in presenting methodologies and technologies that are moving construction and housing forward.”

“We’re proud to sponsor the Department of Housing and Urban Development’s Innovative Housing Showcase,” said Chip Devine, Senior Vice President of Pro Sales, The Home Depot. “At The Home Depot, we’re dedicated to driving growth in the housing industry by equipping professionals with the resources, tools, and partnerships they need to succeed. This event underscores the importance of advancing housing solutions nationwide, and addressing challenges like the skilled trades gap, which continues to be a barrier to progress.”

Additional Details About 2025 Innovative Housing Showcase

A family-friendly event, the showcase is open to the public on the National Mall and expected to attract thousands of attendees, including Members of Congress, industry leaders, and community stakeholders. Visitors can view and enter exhibits on the Mall and attend expert-led panel discussions highlighting housing innovations. In years past, the showcase has attracted thousands of attendees from across the country. To view photos from past showcases, please visit IHS Past Showcases | HUD USER For more information, please visit the Innovative Housing Showcase webpage.

ICYMI | HUD Regional Administrator Quinonez on HUD’s Support for Foster Youth in Texas

HUD Celebrates the Sixth Anniversary of the Foster Youth to Independence Initiative

TEXAS - U.S. Department of Housing and Urban Development (HUD) Southwest Regional Administrator Ashlea Quinonez penned an opinion piece discussing the continued impact of HUD’s investment in youth transitioning out of foster care in Texas. This year marks the sixth anniversary of HUD’s Foster Youth to Independence program, which gives these vulnerable youth the tools and resources they need to achieve success and selfsufficiency as they transition to adulthood.

“[HUD] has delivered more than $5 million in investment nationwide since President Trump returned to the White House,” wrote HUD Southwest Regional Administrator Ashlea Quinonez. “Nearly $250,000 of that investment went to Texas foster youth, providing them with stable temporary housing and supportive services as they build their futures.”

Read the full op-ed below:

Each year, more than 20,000 young Americans transition from foster care, many with no safety net, no stable housing, and no clear path forward. It’s estimated a quarter of them become homeless shortly after leaving the foster care system. For these youth, the transition from foster care to adulthood marks a crossroads one that can either lead to opportunity or derail their chance to achieve the American Dream.

The U.S. Department of Housing and Urban Development (HUD) recognizes that this transition point is critical. It’s a moment when targeted investment can transform futures.

That’s why, in 2019, HUD launched the Foster Youth to Independence (FYI) initiative. FYI provides local public housing authorities funding to help young Americans transitioning from foster care avoid homelessness and begin their new chapters as responsible adults. In addition to temporary rental assistance, the program includes support for services like skills training and job preparation. HUD’s investment in foster youth is equipping them with tools for success so they can enjoy housing stability, dignity, and independence.

This year, we are celebrating the sixth anniversary of this important program, which has delivered more than $5 million in investment nationwide since President Trump returned to the White House. Nearly $250,000 of that investment went to Texas foster youth, providing them with stable temporary housing and supportive services as they build their futures.

As HUD’s Southwest Regional Administrator, I have witnessed firsthand the impact HU

Southern California Rentals in 2025: The Hidden Upside for OC Landlords Amid Supply Constraints

Southern California’s housing market has always been a complex mix of opportunity and challenge. In 2025, that balance is leaning in favor of landlords especially in Orange County. Sales activity has stabilized, home prices continue to edge upward, and rental demand shows no signs of slowing down. While affordability pressures are hitting renters hard, they are also creating an environment where rental properties are increasingly valuable assets.

Orange County landlords today find themselves in a position of strength, supported by low vacancy rates, rising rents, and limited new supply. For investors looking at where to place their capital, Orange County offers both stability and growth potential This article will explore the key drivers shaping this market, including rental demand, supply constraints, affordability challenges, and the implications for landlords and new investors alike.

Rising Rents and Tight Vacancies

Vacancy rates are often the clearest measure of rental market health. As of 2025, Orange County’s multifamily vacancy rate has dropped to 3.6%, a sharp decline from mid2023 levels of 5.4% (Matthews, 2025). Such a low figure indicates that most available rental units are quickly occupied, giving landlords greater leverage in setting prices.

Alongside shrinking vacancies, rents have soared. Average asking rents in Orange County reached $2,730 per month by Q2 2025 representing a 25% jump since late 2019 (Matthews, 2025). This growth not only reflects scarcity but also the enduring appeal of the region, from its economic opportunities to its quality of life. For landlords, this translates into stronger, more reliable income streams.

Home Sales Stability Adds a Safety Net

While affordability challenges make renting more common, the home sales market in Orange County hasn’t weakened it has stabilized. Median listing prices hovered around $1.3 million in late 2024, posting steady year-over-year growth of about 4% (ManageCasa, 2025). Properties still move quickly, often in a matter of weeks, showing that buyer demand remains intact at higher price points.

Statewide, the median home value reached $884,350 in March 2025, up 3.5% from the previous year (ManageCasa, 2025). For landlords, this dual trend of strong sales and persistent affordability barriers creates a “sweet spot”: property values are appreciating, while renters unable to buy ensure a stable tenant base.

Supply Constraints Favor Landlords

Orange County continues to suffer from underbuilding relative to need. Over the past year, 633 apartment units were absorbed, but only 465 new units were delivered to the market (Matthews, 2025) That imbalance keeps vacancy rates tight and demand consistently high.

For landlords, this is a critical factor. Limited new construction means less competition from fresh rental stock. Unlike in some markets where an influx of new units puts pressure on rents, Orange County landlords benefit from a constrained pipeline that helps keep rents climbing and turnover low.

Affordability Pressures Reinforce Renting

Orange County’s affordability challenges are significant, and they feed directly into rental demand. The average renter would now need to earn nearly $55 per hour—more than three times the state’s minimum wage to avoid being cost-burdened (Matthews, 2025).

With home values averaging over $1.6 million and rents topping $3,000 per month, the region ranks among the most expensive places to live in the country.

These pressures force many households, including middle-income earners, to remain renters longer than they might prefer. For landlords, this reality ensures a steady pipeline of demand across income brackets. The rental market has become less of a stepping stone to ownership and more of a long-term housing solution for a growing segment of the population.

Why Landlords and Investors Should Pay Attention

Several key advantages stand out for landlords and new investors entering the Orange County rental market in 2025:

Predictable income: Low vacancies and rising rents guarantee more reliable monthly cash flow.

Asset appreciation: With steady home price growth, property owners benefit from equity gains in addition to rental income

Limited competition: Tight supply keeps market conditions favorable, ensuring less downward pressure on rents.

Investment opportunities: New investors can still find strong returns by targeting smaller multifamily properties or strategically located single-family rentals that remain in high demand.

The combination of rental demand and limited supply creates a market where landlords can maintain strong performance even in an environment marked by affordability stress.

The Southern California rental market in 2025 offers clear advantages for Orange County landlords. Home prices continue to rise, sales remain stable, and vacancies are at their lowest levels in years. While affordability pressures create challenges for renters, those same pressures reinforce long-term demand for rentals.

For existing landlords, the environment promises sustained income and appreciation. For new investors, opportunities still exist for those who recognize the strength of this market and are prepared to act. In short, 2025 may be remembered as a year when affordability constraints turned into hidden upside for Orange County property owners.

If you’re considering how these trends could benefit your real estate portfolio, expert guidance can make all the difference. Let’s talk strategy, explore opportunities, and position you for success in today’s market

Eric Lawrence Frazier, MBA - Principal advisor

Insurance & Climate Resilience: The New Hidden Costs of Owning in Orange County

Homeownership in Orange County has long been a symbol of stability sunlit neighborhoods, strong community ties, and a landscape that draws in families and professionals alike. But beneath the serene surface, a complex financial burden is quietly growing Rising insurance premiums, expanding wildfire and flood risks, and shifting state regulations are imposing hidden costs that buyers and sellers must now factor into every deal. The stakes are especially high in Orange County, where high-value coastal and inland properties face escalating environmental threats.

In this article, I’ll explain how three major forces insurance cost hikes, heightened climate risk, and evolving regulations—are reshaping ownership expenses in Orange County. I’ll break down what each trend means for both sellers and buyers and offer practical strategies to navigate these challenges. Let’s get into it.

1. Rising Insurance Premiums Through a Financial Lens

Home insurance rates across California, including Orange County, are climbing sharply. A new regulatory shift permits insurers to use forward-looking catastrophe models incorporating wildfire, flood, and other climate data to set premiums more precisely. Companies like CSAA have already filed for rate increases around 6.9% citing wildfire severity and inflation.

Further pressure comes from allowing insurers to pass their own reinsurance costs to consumers. Analysts estimate potential premium increases of up to 40%, especially in high-risk areas. The FAIR Plan California’s insurer of last resort is stretched thin, pushing more homeowners toward expensive and limited statewide coverage

2. Escalating Wildfire and Flood Risks

Orange County properties are increasingly exposed to wildfire risk and, in some coastal pockets, flood hazard. California’s Sustainable Insurance Strategy addresses this by requiring insurers who use catastrophe models to commit to writing policies in high-risk zones closing gaps in coverage but also paving the way for targeted rate increases. Before this, many insurers withdrew from high-risk markets entirely.

While these models help insurers price risk more precisely, they also mean homeowners living in vulnerable areas now face sharply higher costs driven by real risk, not just market corrections.

3. New State Regulations and the Financial Impact

California’s Insurance Commissioner, Ricardo Lara, has launched a Sustainable Insurance Strategy that integrates catastrophe modeling and mandates increased policy writing in wildfire-prone areas up to 85% of an insurer’s market share in those zones. The goal is to restore access to private insurance, reducing reliance on the FAIR Plan. But the tradeoff is clear: homeowners may bear higher premiums in exchange for coverage availability.

While these reforms aim for long-term market stability, the short-term impact is rising costs for homeowners, especially those unwilling or unable to invest in home-hardening and mitigation

4. Strategies for Buyers and Sellers

Homeowners and buyers can take concrete steps:

Invest in wildfire and flood mitigation like fire-resistant materials or improved drainage to qualify for discounts under new insurer programs. Shop multiple insurers and compare policies carefully coverage, rates, and mitigation credits vary widely.

For coastal or inland flood-prone properties, consider supplemental flood insurance beyond standard home policies.

Sellers should:

Disclose known rising insurance costs and climate risk implications to set realistic expectations.

Highlight any home-hardening improvements as selling points mitigation measures can attract more buyers and help secure better rates.

Owning property in Orange County today means weighing more than just location and design Rising insurance premiums, driven by climate-informed risk modeling and shifting state regulation, are quietly elevating ownership costs. At the same time, increasing wildfire and flood threats make mitigation an essential investment not a luxury.

Buyers and sellers who understand these financial forces and take proactive steps can better manage costs and maintain property value in a changing landscape. The key is staying informed, acting strategically, and treating resilience as both a shield and a selling point.

Let’s navigate these challenges together. As your trusted advisor in business and wealth, I’m here to help you understand the financial landscape of real estate with clarity and confidence.

Eric Lawrence Frazier, MBA - Principal advisor Real estate

mortgage

Days on Market and Negotiation Shifts: How Buyer Leverage Is Evolving in Fall 2025

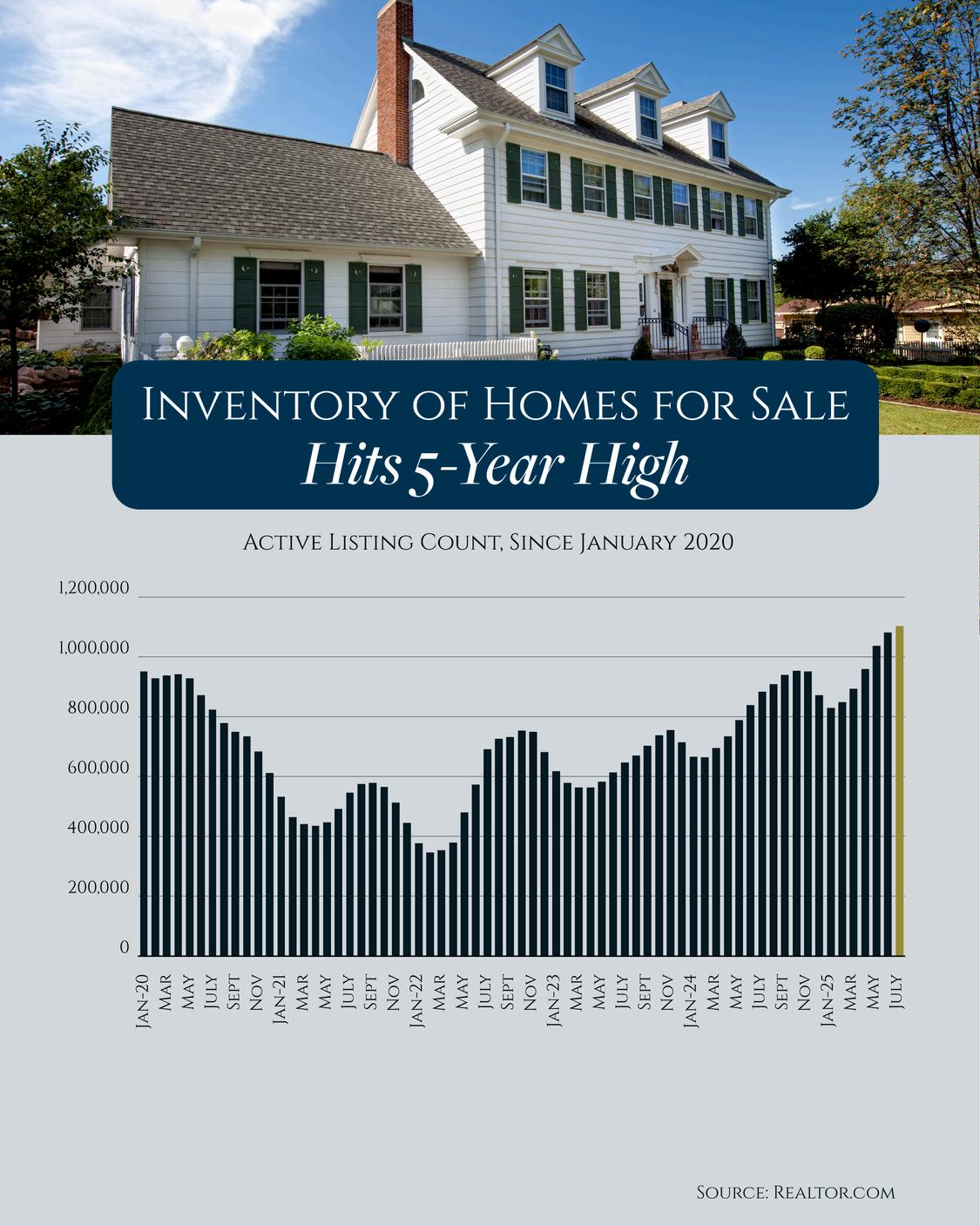

In many counties across the country, a subtle but meaningful shift is underway in residential real estate. Homes that once sold within days are now sitting longer Buyers who once felt squeezed by bidding wars are increasingly able to make contingent offers or ask sellers to cover closing expenses. These evolving conditions matter not just to realtors or investors, but to anyone buying or selling a home in 2025.

Over the past few years, low inventory and high demand gave sellers commanding control But by fall 2025, that balance is tilting. Many listings are stretching past the 30- to 60-day mark. Sellers are more willing to offer concessions Contingent offers once seen as weaker are becoming more common. In this blog post, we’ll review the data trends behind these shifts, explore exactly what’s changing in negotiation practices, and offer actionable strategies both buyers and sellers can use to stay ahead in this transition.

The Changing Numbers: Longer Market Time, More Concessions, Rising Contingency

1. Days on Market (DOM) is increasing

Across many markets, the median days on market have ticked upward. Where once homes might move in a week or two, many now spend a month or more before going under contract In some regions, the median has climbed to 50-70 days or beyond well above previous norms. This signals that sellers can’t expect instant offers just because supply remains constrained. More listings competing for attention means pricing needs to be sharper, marketing more aggressive, and patience more realistic.

For Sellers: Defend Your Position Responsibly

Price sharply from the start. When DOM is rising, an overpriced home sticks out. An accurate initial price avoids the need for later, painful cuts.

Build in flexibility. Be ready to grant modest concessions or credits rather than assuming every buyer will waive closing cost help

Limit exposure to weak offers. Ask for stronger earnest money, shorter contingency windows, or prequalification documentation to reduce risk.

Stage decisively and market broadly. In a slower environment, quality listing photos, virtual tours, and wide exposure become even more critical

Use upgrades or warranties as sweeteners, not purely price cuts. Offering home warranties, prepaying a portion of HOA fees, or handling repairs can add perceived value without directly reducing your net proceeds.

As fall 2025 unfolds, the advantage is quietly shifting toward buyers Longer days on market, a surge in seller concessions, and greater acceptance of contingent offers all point to a more balanced (or slightly buyer-leaning) climate. But this shift doesn’t mean buyers can be careless, nor does it force sellers into panic reductions.

The key for both sides is preparation, flexibility, and knowing how to negotiate from an informed position Buyers can protect themselves through savvy contingencies and cost requests. Sellers can defend against lowball offers by pricing correctly and maintaining selective negotiating power.

Whether you’re planning to buy or sell in the coming months, watch local DOM trends, monitor how many offers sellers are receiving, and use that data to guide your decisions Adaptability will be your greatest strength in this evolving landscape.

How Climate Risks Are Reshaping Insurance, Disclosures & Lending in High-Risk Neighborhoods

When a home sits near a fire-prone ridge, a coastal bluff, or a floodplain, the number on the price tag is just part of the story. In recent years, insurance premiums, loan qualification criteria, and legal disclosure rules have all begun to adjust more sharply to climate risk What used to be a niche concern for buyers and sellers in extreme zones is becoming central to real estate deals in many markets

Rising costs from wildfires, flooding, and coastal storm surge are pushing insurers to tighten underwriting or exit markets altogether. Lenders now demand more rigorous risk-proofing or may refuse financing in areas of extreme exposure. On the legal side, sellers are under increasing pressure to inform buyers about climate vulnerabilities, sometimes under new statutory regimes

In this article, I explain how these pressures play out in practice: how climate risk is altering insurance costs and availability, how lenders now assess properties in risk zones, and what disclosure obligations buyers and sellers must navigate. My goal is to help you enter a real estate transaction in a higher-risk neighborhood with eyes wide open financially, legally, and strategically.

Insurance in Risk Zones: Costs, Capacity, and Coverage

Escalating Premiums & Restricted Coverage

Insurance is the first front line when climate risk hits home Because insurers are dealing with more frequent, correlated losses across large regions (e g , during wildfire seasons or major storms), they must recalculate pricing and exposure. Many are increasing premiums sharply, imposing stricter deductibles, or declining new business in extreme-risk areas Some insurers have simply pulled out of highly exposed zones. Analysts describe this as a form of “insurance desert” where coverage is unavailable or unaffordable.

In wildfire-prone regions, for instance, nonrenewals of existing policies have risen, pushing homeowners into higher-cost options or state-run “last resort” insurers. The diminished availability itself becomes a signal to buyers: if you can’t insure it, you probably can’t finance or sustain it

Underinsurance & Gaps in Coverage

Even where insurance exists, it may not be enough. Many policies exclude damage from slow degradation (e.g., chronic flooding or saltwater intrusion), leave out certain perils, or impose sublimits.

As climate risks intensify, those gaps can bite hard A property might be insured for structural damage but not for mold, or exclude flood losses if flood insurance is handled separately Buyers should scrutinize exactly what the policy covers and consider supplemental coverage.

Lending in High-Risk Areas: Stricter Criteria & Higher Hurdles

Risk-Based Lending Criteria

Lenders have always weighed property condition, location, and insurability. Today, they increasingly incorporate climate risk into their underwriting models Properties in flood zones, for example, often require mandatory flood insurance when loans are federally backed or regulated. Lenders may also require structural adaptations (e.g., elevation, improved drainage, fire-resistant materials) before approving a loan.

There is empirical evidence that lenders adjust terms such as loan-to-value ratios or interest rates for high-risk properties, or in extreme cases, refuse to originate mortgages at all. One study finds that in the 500-year flood zone (a lowerthreat band), borrowers are not required to have flood insurance, but the public signal of risk nonetheless plays into lending decisions

Portfolios’ Risk Exposure

Lenders and banks face portfolio-level risks too. A large number of defaulted mortgages in a region hit by wildfire or flood could hit balance sheets hard Some banking regulators now require stress testing for climate exposure across loan portfolios. This means lenders may act conservatively when appraising or extending credit in vulnerable zones, even if individual properties seem marginally acceptable

Disclosures & Legal Obligations: What Buyers Need to Know

Statutory Disclosure Laws

Many jurisdictions now require sellers or agents to disclose whether a property lies in a mapped hazard zone such as floodplains, wildfire buffer areas, or coastal storm surge zones Disclosure may include past claims history, premium amounts for hazard insurance, or documented past damage events. In some states, disclosure is mandatory at the offer stage or even earlier in marketing materials

However, flooding disclosure laws vary widely across states; some require no disclosure at all, leaving buyers vulnerable to surprises. When laws are weak, courts may still hold sellers liable under general duty-of-disclosure or fraud theories if known risks were concealed.

Evolving Regulatory Pressures

As climate risk becomes more central, regulators are pushing for tighter disclosure standards Some states are proposing or enacting rules that force sellers to share more granular climate projections or require disclosures of future flooding risk. Market and regulatory pressure may also demand independent risk assessments or resilience certifications as part of property sales

Sellers should proactively gather as much climaterelated documentation as possible (insurance loss history, elevation data, flood maps, fire buffer studies) and share them transparently. Buyers should request these disclosures and, where permitted, obtain independent climate-risk reports before closing

Examples & Practical Tips

Flood Zone Example: A homeowner in a FEMAdesignated 100-year flood zone must carry flood insurance if the loan is federally backed. Lenders must inform buyers of this requirement before closing

Wildfire Area Example: In regions with recent large wildfires, insurance carriers may decline to renew policies. Prospective buyers may find few viable options for coverage, which may scare off lenders.

Coastal Storm Surge Example: Rising sea levels push some properties into newly mapped hazard zones, triggering retroactive insurance reassessments or disclosure obligations

Practical advice for buyers and sellers:

1 Obtain a climate-risk assessment early in planning.

2.Ask for full insurance claims history and premium trends.

3.Include contingency clauses for insurability or loan approval.

4 Engage legal counsel with climate-disclosure experience

5 If possible, insist on structural mitigations (e g , raising the house, fire-safe landscaping, waterproofing) before finalizing a deal.

In high-risk areas facing wildfire, flood, or coastal threats, real estate deals involve more than just price Insurance may be costly or unavailable, financing harder to secure, and disclosure rules are changing Buyers and sellers must be financially, legally, and practically prepared.

How Retirees Are Reshaping Orange County’s Housing Market

In Orange County, properties priced above the $3 million mark are increasingly acting like early warning lights for the broader real estate landscape Over recent months, these ultra-luxury homes have lingered longer on the market, and many sellers have resorted to more frequent and steeper price reductions. What may appear to be isolated highend softness is in fact loaded with implications for mid-range buyers and sellers because trends in the luxury segment often precede shifts in more accessible tiers

Understanding the trajectory of this luxury cooling matters For everyday buyers, it can hint when negotiation leverage might rise. For sellers, it can signal when to set expectations or adjust pricing. In this article, we’ll examine recent data from Orange County’s $3 million+ market tracking days on market, price cuts, and inventory growth and explain how those movements can serve as a forecast for what lies ahead in the mainstream market Ultimately, you’ll walk away with clear insights on how to interpret these “top-tier” signals and what actions to consider in your own segment.

Luxury Inventory Swells and Slower Sales

One of the most telling shifts in the ultra-luxury market is the increase in inventory relative to demand In Orange County, listings in the high end have been piling up faster than they are being absorbed. In general county statistics, homes in the $2 million+ bracket already take closer to 52 days on market versus roughly 33 for under-$1 million properties. This gap underscores the cooling at the top (OC Real Estate Report)

In fact, a broader market metric shows that expected market time across all segments has stretched to about 95 days, compared with only 67 days just a year earlier suggesting that the momentum is softening across the board (Tim Smith Real Estate Group)

As luxury homes linger, sellers are pressured to lower expectations or offer concessions. That shift often first appears in the most expensive listings, because those buyers tend to be more rateinsensitive but also selective and value-conscious.

Price Cuts Rise, Marking a Transition in Negotiation Power

When luxury listings stall, sellers often respond with price reductions to stimulate interest In those upper tiers, a property may receive multiple cuts before securing a buyer That signals a move away from a seller’s market toward a more balanced or buyer-friendly posture.

Once that adjustment begins at the top, it tends to percolate down In the mid-market, where margins are tighter and buyers more price-sensitive, sellers may soon feel compelled to reduce asking prices or accept stronger negotiating offsets (repairs, closing costs, credits). In other words, high-end price cuts are an early version of what lower-segment sellers will likely face

What Luxury Cooling Suggests for Mid-Range Segments

1. Negotiation leverage will shift.

As luxury buyers grow pickier and sellers become more realistic, the same behavior tends to migrate downward Mid-tier buyers may find that contingencies, inspections, and seller concessions (closing credits, repair allowances, faster response time) become more common and acceptable.

2. Comps may adjust downward.

Data from high-end sales ultimately feed into comparable sales (comps) used in appraisals If luxury homes begin to soften in price, those comps may erode the benchmark values that mid-level sellers rely on to justify aggressive pricing

3. Patience may improve.

Mid-market listings may remain on the market a bit longer, especially if over-priced or lacking standout features Sellers might need to reconsider staging, marketing refreshes, or periodic price adjustments to avoid items becoming stale.

4. Timing opportunities emerge for buyers.

For buyers waiting on the sidelines, watching luxury trends gives hints about when offers may gain traction. If luxury offers begin to close below list prices or with stronger concessions, mid-range buyers may be less pressured to overbid

Real-World Example: Orange County in 2025

By mid-2025, Orange County began registering flat to slightly declining median prices in some segments. In August, the median slipped from about $1 23 million to $1 175 million in one month (Onyx Homes) Meanwhile, the lower end was still moving relatively quickly, but even there, days on market crept upward (Southern California Homes)

The wealthy buyer class especially in coastal enclaves has shown more patience. As more luxury listings are priced unsustainably, they stay unsold. When those get marked down, they pull the upper end comps downward, tightening margins for sellers in lower tiers

These movements do not always translate immediately, but over time, they foreshadow more balanced negotiation dynamics across all segments.

Conclusion

Luxury market activity in Orange County especially longer time on market and more frequent price cuts in $3 million+ listings serves as an early warning system for the broader real estate environment Those top-tier shifts often foreshadow weakening seller dominance, rising buyer negotiating power, and moderated pricing even in more affordable segments. For sellers, the lesson is to stay realistic, monitor comp behavior, and be ready to adjust strategies. For buyers, calibration and timing matter: what starts at the top tends to ripple downward

If you’re thinking of buying or selling, keeping an eye on the luxury trends is a smart move It offers you a window into where the market may be headed and a chance to act before the pressure fully reaches your price range.

Market Signals from the Top: What Orange County’s High-End Price Adjustments Mean for Everyday Buyers and Sellers

In Orange County, properties priced above the $3 million mark are increasingly acting like early warning lights for the broader real estate landscape. Over recent months, these ultra-luxury homes have lingered longer on the market, and many sellers have resorted to more frequent and steeper price reductions. What may appear to be isolated high-end softness is in fact loaded with implications for mid-range buyers and sellers because trends in the luxury segment often precede shifts in more accessible tiers.

Understanding the trajectory of this luxury cooling matters For everyday buyers, it can hint when negotiation leverage might rise. For sellers, it can signal when to set expectations or adjust pricing. In this article, we’ll examine recent data from Orange County’s $3 million+ market tracking days on market, price cuts, and inventory growth and explain how those movements can serve as a forecast for what lies ahead in the mainstream market. Ultimately, you’ll walk away with clear insights on how to interpret these “top-tier” signals and what actions to consider in your own segment.

Luxury Inventory Swells and Slower Sales

One of the most telling shifts in the ultra-luxury market is the increase in inventory relative to demand. In Orange County, listings in the high end have been piling up faster than they are being absorbed In general county statistics, homes in the $2 million+ bracket already take closer to 52 days on market versus roughly 33 for under-$1 million properties. This gap underscores the cooling at the top (OC Real Estate Report)

In fact, a broader market metric shows that expected market time across all segments has stretched to about 95 days, compared with only 67 days just a year earlier suggesting that the momentum is softening across the board. (Tim Smith Real Estate Group)

As luxury homes linger, sellers are pressured to lower expectations or offer concessions That shift often first appears in the most expensive listings, because those buyers tend to be more rateinsensitive but also selective and value-conscious.

Price Cuts Rise, Marking a Transition in Negotiation Power

When luxury listings stall, sellers often respond with price reductions to stimulate interest In those upper tiers, a property may receive multiple cuts before securing a buyer. That signals a move away from a seller’s market toward a more balanced or buyer-friendly posture.

Once that adjustment begins at the top, it tends to percolate down. In the mid-market, where margins are tighter and buyers more price-sensitive, sellers may soon feel compelled to reduce asking prices or accept stronger negotiating offsets (repairs, closing costs, credits). In other words, high-end price cuts are an early version of what lower-segment sellers will likely face.

What Luxury Cooling Suggests for Mid-Range Segments

1. Negotiation leverage will shift.

As luxury buyers grow pickier and sellers become more realistic, the same behavior tends to migrate downward. Mid-tier buyers may find that contingencies, inspections, and seller concessions (closing credits, repair allowances, faster response time) become more common and acceptable.

2. Comps may adjust downward.

Data from high-end sales ultimately feed into comparable sales (comps) used in appraisals. If luxury homes begin to soften in price, those comps may erode the benchmark values that mid-level sellers rely on to justify aggressive pricing

3. Patience may improve.

Mid-market listings may remain on the market a bit longer, especially if over-priced or lacking standout features Sellers might need to reconsider staging, marketing refreshes, or periodic price adjustments to avoid items becoming stale.

4. Timing opportunities emerge for buyers.

For buyers waiting on the sidelines, watching luxury trends gives hints about when offers may gain traction. If luxury offers begin to close below list prices or with stronger concessions, mid-range buyers may be less pressured to overbid.

Real-World Example: Orange County in 2025

By mid-2025, Orange County began registering flat to slightly declining median prices in some segments. In August, the median slipped from about $1 23 million to $1 175 million in one month (Onyx Homes) Meanwhile, the lower end was still moving relatively quickly, but even there, days on market crept upward. (Southern California Homes)

The wealthy buyer class especially in coastal enclaves has shown more patience As more luxury listings are priced unsustainably, they stay unsold. When those get marked down, they pull the upper end comps downward, tightening margins for sellers in lower tiers.

These movements do not always translate immediately, but over time, they foreshadow more balanced negotiation dynamics across all segments.

Conclusion

Luxury market activity in Orange County especially longer time on market and more frequent price cuts in $3 million+ listings serves as an early warning system for the broader real estate environment Those top-tier shifts often foreshadow weakening seller dominance, rising buyer negotiating power, and moderated pricing even in more affordable segments. For sellers, the lesson is to stay realistic, monitor comp behavior, and be ready to adjust strategies For buyers, calibration and timing matter: what starts at the top tends to ripple downward

If you’re thinking of buying or selling, keeping an eye on the luxury trends is a smart move. It offers you a window into where the market may be headed and a chance to act before the pressure fully reaches your price range.

Equity Through Conversion: How Rezoning and Redevelopment Are Unlocking Hidden Value for Owners

In many cities, the built environment hides untapped potential. Underused lots, aging commercial buildings, and obsolete structures sit idle not because they lack value, but because existing zoning or development rules prevent more productive uses. Yet, across the country, state incentives and local zoning reforms are changing that Increasingly, owners, small-scale investors, or even homeowners are being given new pathways to unlock hidden value by converting or redeveloping underused parcels into housing

This shift matters deeply As housing shortages tighten across many regions, governments are looking to creative solutions to both grow supply and produce more equitable outcomes. By adjusting zoning rules, offering tax credits, or streamlining permits, they can encourage private actors to transform existing assets rather than clearing new land. For owners, these changes can translate into new revenue streams or capital appreciation

In this article, I’ll explore how rezoning and redevelopment policies are creating opportunities for equity through conversion. I’ll look at the types of state and local incentives in play, explain how owners can identify viable conversion projects, and suggest practical strategies for navigating the regulatory and financial challenges. By the end, you’ll see how even modest properties might hold surprising potential when the rules shift

The Policy Shift: Incentives and Zoning Reform

State and Federal Incentives

Governments at various levels are increasingly embracing adaptive reuse and conversion Federally, new programs now allow greater flexibility in funding commercial-to-residential conversion projects, including enhanced access to block grants and low-interest financing to support housing transformations In some instances, existing grant programs have been updated to broaden eligibility for conversion efforts.

On the state level, incentives can include tax credits (for example, credits tied to rehabilitating existing structures), grants for redevelopment in underserved areas, or subsidies that help cover the costs of bringing older buildings up to code These measures aim to reduce the financial burden and risk of conversion projects.

Zoning Reform and Local Adjustments

Beyond financial incentives, the crux of change often lies in zoning adjustments Local governments are increasingly revising their rules to allow higher density, permit accessory dwelling units (ADUs), reduce parking requirements, or grant density bonuses when affordable units are included. Jurisdictions are also offering fast-track review or waiving impact fees for qualifying conversion projects The result: parcels once limited to low-density or single-use zoning can now support multi-unit housing

This kind of reform is often coupled with efforts to promote equity targeting conversions in neighborhoods historically excluded from investment or prioritizing affordable housing outcomes through inclusionary zoning or incentives tied to affordability.

Identifying and Structuring Conversion Opportunities

Spotting the Right Candidate Properties

A property’s viability for conversion depends on several factors. First, it must have zoning or regulatory “upside” for instance, areas where upzoning is underway or local plans encourage housing growth. Commercial buildings with large floor plates, older offices with high vacancy, or underutilized parking lots are prime candidates in many urban areas

Another indicator is proximity to infrastructure being near transit, utilities, or amenities increases appeal and feasibility. Also, owners should check for "zoning arbitrage" potential: situations where the current use is conservative relative to what future zoning or redevelopment plans enable

Financial and Legal Structuring

Once a candidate is identified, the next step is mapping cash flows, costs, and regulatory pathways The cost of structural adjustments, code compliance, and permitting must be weighed against projected rental income or resale value Because conversion often carries more risk than ground-up construction, stacking incentives such as combining tax credits, grants, and fee waivers can be essential.

Owners or small investors should collaborate early with architects, planners, and legal counsel familiar with local zoning and building codes In many cases, creative structuring (for instance, turning part of a parcel into an ADU or subdividing lots) can make a conversion more viable. Engagement with local planning offices is also key: early feedback or pre-applications can reveal necessary adjustments or constraints, avoiding costly missteps

Real-World Examples and Lessons

Cities across the U S are embracing “office-to-anything” conversion models, offering tax incentives and targeted zoning amendments to repurpose vacated commercial space into housing or mixed uses. In one recent example, a 12-story office building was converted into over 200 housing units, supported by local zoning changes and incentives.

Elsewhere, municipal programs encourage homeowners to add basement apartments or accessory units, turning unused space into safe, rentable housing often without altering a building’s external footprint. These smaller scale efforts can provide steady income for residents while helping address housing demand

From these cases, a few lessons emerge: conversion is rarely easy, but when public policy aligns with private opportunity, hidden value can be unlocked Further, timely coordination with local authority, and careful financial planning, determine which projects succeed and which stall.

Micro-Markets That Hold Firm: Which Orange County Neighborhoods Are Winning in 2025

Across Orange County, the broad real estate trends in 2025 show signs of moderation: inventory is gradually loosening, buyer caution is creeping in, and price growth is no longer uniformly aggressive Yet within this shifting environment, certain submarkets are outperforming the broader county. For buyers, sellers, and investors alike, those micro-markets give you clues about where demand remains resilient, where values are holding, and why. In this article, I’ll highlight specific communities whether Irvine villages, coastal enclaves, or strong inland family neighborhoods that are defying broader softening Along the way, I’ll use MLS and market-report data to show which areas are holding their ground and explore the factors behind their durability.

Coastal

Strength: Laguna Niguel, Huntington Beach (92649), and Newport Coast

Coastal enclaves remain among the strongest performers in 2025. In Laguna Niguel, average home values have appreciated year over year and homes go pending rapidly, indicating strong demand Homes in Laguna Niguel typically go under contract in about three weeks, and the median sold price remains near or slightly above asking in many segments. (Data from mid-2025 reports.)

Meanwhile, in Huntington Beach especially zip code 92649 in the southeast region prices continue to tick upward even as countywide medians drift downward In the latest reports, 92649 showed steady appreciation close to 5%, even while the broader county median slipped. That tells us that beachfront or near-shore access continues to command premium pricing and buyer interest

In Newport Coast, the luxury coastal tier resists softening because of severe supply constraints and the prestige of ocean views Though data for luxury coastal segments often lags, anecdotal MLS reports show that high-end homes there still spend very little time on market.

Why they hold up: Scarcity of land, prestige, view premiums, and buyer willingness to pay in luxury coastal corridors When supply is constrained and demand remains for lifestyle, coastal markets tend to outperform.

Irvine Villages: Woodbury, Portola Springs, Great Park, Orchard Hills

Within Irvine, not all neighborhoods are created equal and even in a cooler market, some villages are showing strong resilience. Irvine overall is leaning toward a neutral market, with homes taking longer to sell, and more properties experiencing price reductions (Average days on market climbed to 59 in early 2025 in some reports.)

Meanwhile, in Huntington Beach especially zip code 92649 in the southeast region prices continue to tick upward even as countywide medians drift downward In the latest reports, 92649 showed steady appreciation close to 5%, even while the broader county median slipped. That tells us that beachfront or near-shore access continues to command premium pricing and buyer interest.

In Newport Coast, the luxury coastal tier resists softening because of severe supply constraints and the prestige of ocean views. Though data for luxury coastal segments often lags, anecdotal MLS reports show that high-end homes there still spend very little time on market

Why they hold up: Scarcity of land, prestige, view premiums, and buyer willingness to pay in luxury coastal corridors When supply is constrained and demand remains for lifestyle, coastal markets tend to outperform.

Irvine Villages: Woodbury, Portola Springs, Great Park, Orchard Hills

Within Irvine, not all neighborhoods are created equal and even in a cooler market, some villages are showing strong resilience. Irvine overall is leaning toward a neutral market, with homes taking longer to sell, and more properties experiencing price reductions. (Average days on market climbed to 59 in early 2025 in some reports )

But in certain Irvine enclaves, the story is more optimistic. Neighborhoods like Woodbury, Portola Springs, and Great Park tend to see better absorption because of strong school districts, planned amenities, and access to new employment nodes. The master-planned character and relatively newer inventory help these villages maintain buyer interest. Orchard Hills, with its higher-end product mix and scenic surroundings, also does relatively well compared to older parts of Irvine

As one housing report indicates, Irvine’s supply (measured in months of inventory) stretched to about 2.83 months in early 2025, suggesting the market is still in seller’s territory but with more pressure than earlier years. In those conditions, the better positioned Irvine villages can continue to outperform weaker nodes

Inland Family Neighborhoods: Rancho Santa Margarita, Mission Viejo, Tustin

Not all inland areas are under pressure. Some family-oriented suburbs continue to show strength as buyers look away from coastal price shocks. Mission Viejo, for example, retains a seller’s tilt in 2025; the median sold price showed a year-over-year gain and many homes still sell within 30 days (Some reports show up to 65% of homes in Mission Viejo sold inside a month.)

Tustin is another intriguing case In March 2025, Tustin had among the fastest absorption times and showed a sold-to-list price ratio above 100%. Homes essentially were still trading strongly even as inventory started to loosen. That kind of performance suggests segments in Tustin remain “hot” relative to the broader region

Rancho Santa Margarita also deserves attention its balance of affordability, access to good schools, and lifestyle amenities (nature trails, open space) helps insulate it from sharp corrections Buyers priced out of coastal zones often look inland, and certain inland parts of Orange County are benefiting.

What Makes These Micro-Markets Resilient

Several recurring factors help explain why these neighborhoods hold up while others lag:

1.Supply constraints and limited new development: Coastal zones and highamenity Irvine villages often have tight land availability, limiting new competition.

2.Premium locational attributes: Proximity to ocean, views, walkability, master amenities, strong school reputations, and commute advantages matter more in a softening market.

3.Buyer segmentation: In luxury coastal zones, buyers are less rate-sensitive. Inland family zones attract move-up buyers, not just entry buyers, offering stability.

4.Inventory and absorption dynamics: Even as inventory loosens, these micro-areas still enjoy faster absorption and fewer price reductions, which maintains negotiating power.

5.Psychology and perception: Buyers tend to anchor to “best neighborhoods” and are more willing to tolerate higher pricing or wait. That effect helps reinforce resilience.

Conclusion

While the broader Orange County market in 2025 shows signs of cooling, micro-markets in coastal enclaves (Laguna Niguel, Huntington Beach’s 92649, Newport Coast), select Irvine villages (Woodbury, Great Park, Orchard Hills), and strong inland family suburbs (Mission Viejo, Tustin, Rancho Santa Margarita) are outperforming They benefit from constrained supply, premium location, and more stable demand For homeowners, sellers, and investors, success in 2025 is likely to come not from broad bets across the county, but from choosing the right submarkets. If you’re considering entering the Orange County real estate space, paying attention to these resilient micro-markets and understanding their underlying fundamentals can make all the difference.

The Rise of the Hybrid Seller: Balancing Cash Buyers, iBuyers, and Traditional Offers in Orange County

The past few years have reshaped how homes are sold in Orange County. Sellers now have more routes than ever beyond simply placing their home on the Multiple Listing Service (MLS) in an effort to gain speed, certainty, and competitive pricing. In many cases, homeowners are combining traditional offers with instant-cash or iBuyer shortcuts, becoming what we might call “hybrid sellers ”

What’s driving this shift? High interest rates, softer buyer demand, and increasing inventory are making timing and certainty more important than ever. Some sellers would prefer a faster sale with less risk, even if it means accepting a bit less. Others are still chasing maximum market value and are willing to wait A hybrid approach allows sellers to hedge between those goals.

In this article, we’ll explore how hybrid selling works in Orange County today We’ll compare the benefits and drawbacks of cash buyers, iBuyers, and typical MLS listings. Most importantly, we’ll look at how real estate agents can help guide clients into strategies that optimize for speed, certainty, or sales price (or a balance of all three).

Understanding the Three Main Paths

Cash Buyers (“We Buy Houses” Investors)

How it works: A local or regional investor offers to purchase your home outright, often “as-is,” with a quick closing timeline.

Pros:

Fast transaction, sometimes in a week or two

No need for repairs, staging, or multiple showings

Certainty of deal (no financing fall-through)

Cons:

Offers tend to be discounted (sometimes 30–70 % of full value)

Very little room for negotiation

Some risks of shady operators, so vetting is essential In Orange County, a number of firms advertise cash‐buyer services daily. Some offer multiple competing bids to try to push offers upward. But often the trade-off is steep: speed and certainty come at a price.

iBuyers

How it works: Technology-driven firms (like Opendoor or smaller local alternatives) provide near‐instant offers based on algorithms and local comps. The seller may have flexibility in closing date.

Pros:

Convenience: many steps are automated or remote

Predictability in timing

Selling “as-is” becomes easier, as some iBuyers handle repairs in-house

Cons:

Fees and margins are higher, reducing the net to the seller

Strict eligibility criteria (e.g. property condition, lot size, age)

Sometimes the “final offer” changes after inspections

iBuyers are gaining ground in Orange County. As noted in analyses of iBuyer pitfalls, sellers must weigh the convenience against potentially higher transaction costs and lower pricing.

Traditional MLS / Agent‐Mediated Offers

How it works: List the property via an agent on the MLS, host showings, negotiate offers, and close in the typical 30–60-day window (or more).

Pros:

Maximum exposure to buyers, often driving bidding wars

Opportunity to push price via competition

Professional guidance, staging, marketing, and negotiation

Cons:

Time risk (days on market)

Uncertainty (appraisals, financing rescission)

Costs: commissions, repair contingencies, and staging costs

In Orange County’s current environment where inventory is growing and days on market are rising traditional listings may need more finesse around pricing and marketing to remain effective.

The Hybrid Seller Strategy

A hybrid seller does not commit entirely to one approach. Instead, they may:

1.Request backup offers: accept a near-instant bid from a cash buyer or iBuyer as a fallback

2.Short-term MLS listing: list on MLS for a short period (e.g. 7–10 days) to attract competing offers, with the understanding that if nothing acceptable arrives, the off-market bid is activated.

3 Simultaneous paths: market traditionally while collecting cash offers behind the scenes.

This strategy hedges risk: if the MLS process drags or fails, the seller still has a safety net. If market demand surges, the traditional process can extract premium pricing.

How Agents Should Guide Clients

Clarify Seller Goals

Speed vs. price vs. certainty: Some clients are under a deadline (job move, financial need), others want maximum long-term return. Discuss how much discount the seller is willing to accept for a sure, quick sale.

Do the Math

Compare net proceeds (after commission, repairs, fees) across three scenarios. Use local comps and adjust for discount rates in cash and iBuyer offers.

Set Clear Parameters

If taking a fallback offer, set a “trigger” (e.g. no solid MLS offer within 14 days). Build in thresholds (lowest acceptable offer, required guarantee) so you don’t accept a bait offer.

Vet the Buyers

Confirm legitimacy of cash buyers (references, track record, proofs of funds)

Review the iBuyer contract carefully for repair deductions, cancellation clauses, or re-appraisal risk

Market Strategically

Even if going hybrid, don’t half-market. Professional photos, targeted ads, open houses, and staging can help bring serious offers in the MLS window. Leverage digital tools to gather multiple cash/iBuyer bids simultaneously to create pressure.

Communicate Frequently

Keep the seller in the loop as offers come in.

Reassess strategy in real time (e g extend listing window, decline weak bids).

Conclusion

Hybrid selling is fast becoming a go-to strategy for homeowners in Orange County who want to balance competing priorities: price, certainty, and speed. Rather than choosing one path exclusively, savvy sellers and the agents who represent them can layer approaches: market traditionally, collect backup cash bids, and pivot if necessary. The key is informed decision-making. Agents must help clients quantify tradeoffs, vet buyers carefully, and remain flexible When executed properly, hybrid selling can offer the best of both worlds: the chance at top dollar with insurance against the unpredictability of the market

If you’re contemplating a sale in Orange County and weigh those options, begin by exploring both MLS and cash/iBuyer paths then let smart strategy chart your course.

Mortgage Rates and Buyer Psychology: How Orange County Households Are Adjusting in a 6–7% Rate Environment

Over the past few years, California homebuyers have grown accustomed to ultra-low mortgage rates, but the current reality looks very different In Orange County, where home prices already test affordability, mortgage rates holding in the 6 % to 7 % range are causing ripples across buyer behavior, financing strategies, and market dynamics. For many homeowners and prospective buyers alike, decisions that once felt straightforward now come with much more deliberation.

In this environment, some potential buyers are pausing or scaling back expectations, while others are getting creative in order to make a purchase still work. The higher rates reshape not just what households can afford, but how they think about their options. In this article, I’ll explore how mortgage rates in the 6–7 % ballpark are altering affordability, buyer demand, and strategy across income brackets in Orange County. I’ll also cover loan programs and creative financing tools agents can highlight to help clients stay competitive even with the headwinds of higher borrowing costs

How 6–7 % Rates Reshape Affordability

Declining Buying Power Across Income Bands

When mortgage rates creep into the 6–7 % range, the same monthly payment supports a smaller loan amount. For instance, a household that might have qualified for a $1.3 million mortgage with a 3–4 % rate may now only qualify for $1.1 million or less. That means many buyers must scale back their search to smaller homes or more outlying neighborhoods

For lower- to moderate-income households, the squeeze is most severe. These buyers may have already been pushing limits on housing cost ratios; the uptick in rates forces them into more constrained choices or to remain renters longer.

Middle-income buyers often have some flexibility but still feel the pinch: they may forgo certain upgrades or accept longer commutes to stay within budget

Higher-income buyers, especially those with strong cash reserves or investment flexibility, feel the constraint less acutely. Some may pay more cash down or opt for jumbo loans, absorbing the rate premium more easily

The Lock-In Effect and Supply Consequences

One psychological and market effect that shows up strongly in Orange County is the “lock-in effect.” Many homeowners locked into low-rate mortgages from earlier years are reluctant to sell and give up their favorable rates, because replacing that with a 6–7 % mortgage would raise their housing costs. As a result, the inventory of existing homes for sale shrinks. In Orange County, turnover rates have declined, with homeowners holding onto their properties longer rather than trading up. (See the housing indicators showing lower homeownership turnover in recent years.)

Reduced supply intensifies competition among buyers still active, which in turn dampens downward movement in home prices even though affordability is strained The result can feel paradoxical: fewer sales but steadier pricing because supply is constrained.

In neighborhoods where sellers held out for higher prices, homes sit longer data from Orange County shows that more than 60 % of recent sales have closed below original asking price, and time on market has stretched. But well-priced, well-presented homes continue to attract buyer interest.

Buyer Psychology and Demand Shifts

Increased Caution, Delay, and Trade-Offs

Higher rates provoke more internal debate from buyers. Some may delay purchasing, expecting rates to drop. Others might accept compromises smaller square footage, fewer luxury features, or longer commutes Many are more risk-averse, asking more questions about longterm resale, tax impacts, and market stability.

In Orange County’s affluent market, status signaling still matters: buyers often prioritize aesthetic finishes, community prestige, and perceived social value. But under rate pressure, some of these preferences soften buyers might trade off some finishes or opt for less glamorous locations to maintain affordability.

The Return of Bidding Discipline

In the frenzy-era with 3–4 % rates, many buyers would stretch into bidding wars. Now, buyers are more disciplined. They set firm limits, walk away more readily, and pay closer attention to comparable sales and financing cost calculations. Agents who educate clients on effective underwriting, stress-test scenarios, and “what-if rate bumps” foster more confidence.

Creative Tools and Loan Programs to Help Clients Compete