HandbookofMetal InjectionMolding

SecondEdition

Editedby

DonaldF.Heaney

An imprint of Elsevier

WoodheadPublishingisanimprintofElsevier TheOfficers’MessBusinessCentre,RoystonRoad,Duxford,CB224QH,UnitedKingdom 50HampshireStreet,5thFloor,Cambridge,MA02139,UnitedStates TheBoulevard,LangfordLane,Kidlington,OX51GB,UnitedKingdom

Copyright © 2019ElsevierLtd.Allrightsreserved.

Nopartofthispublicationmaybereproducedortransmittedinanyformorbyanymeans, electronicormechanical,includingphotocopying,recording,oranyinformationstorageand retrievalsystem,withoutpermissioninwritingfromthepublisher.Detailsonhowtoseek permission,furtherinformationaboutthePublisher’spermissionspoliciesandour arrangementswithorganizationssuchastheCopyrightClearanceCenterandtheCopyright LicensingAgency,canbefoundatourwebsite: www.elsevier.com/permissions.

Thisbookandtheindividualcontributionscontainedinitareprotectedundercopyright bythePublisher(otherthanasmaybenotedherein).

Notices

Knowledgeandbestpracticeinthisfieldareconstantlychanging.Asnewresearchand experiencebroadenourunderstanding,changesinresearchmethods,professionalpractices, ormedicaltreatmentmaybecomenecessary.

Practitionersandresearchersmustalwaysrelyontheirownexperienceandknowledgein evaluatingandusinganyinformation,methods,compounds,orexperimentsdescribedherein. Inusingsuchinformationormethodstheyshouldbemindfuloftheirownsafetyandthesafety ofothers,includingpartiesforwhomtheyhaveaprofessionalresponsibility.

Tothefullestextentofthelaw,neitherthePublishernortheauthors,contributors,oreditors, assumeanyliabilityforanyinjuryand/ordamagetopersonsorpropertyasamatterofproducts liability,negligenceorotherwise,orfromanyuseoroperationofanymethods,products, instructions,orideascontainedinthematerialherein.

LibraryofCongressCataloging-in-PublicationData

AcatalogrecordforthisbookisavailablefromtheLibraryofCongress

BritishLibraryCataloguing-in-PublicationData

AcataloguerecordforthisbookisavailablefromtheBritishLibrary

ISBN:978-0-08-102152-1(print)

ISBN:978-0-08-102809-4(online)

ForinformationonallWoodheadpublications visitourwebsiteat https://www.elsevier.com/books-and-journals

Publisher: MatthewDeans

AcquisitionEditor: ChristinaGifford

EditorialProjectManager: LindsayLawrence

ProductionProjectManager: JoyChristelNeumarinHonestThangiah

CoverDesigner: VictoriaPearson

TypesetbySPiGlobal,India

3.4DifferentMIMpowderfabricationtechniques

4Powder-binderformulationandcompoundmanufacture inmetalinjectionmolding(MIM)57

R.K.Enneti,V.P.Onbattuvelli,O.Gulsoy,K.H.Kate,S.V.Atre

4.1Introduction:Theroleofbinders

4.2Binderchemistryandconstituents

4.3Binderandpowderpropertiesandtheireffectsonfeedstock

D.F.Heaney,C.D.Greene

7Debindingandsinteringofmetalinjectionmolding(MIM)

S.Banerjee,C.J.Joens

7.1Introduction

11Modelingandsimulationofmetalinjectionmolding(MIM)219

T.G.Kang,S.Ahn,S.H.Chung,S.T.Chung,Y.S.Kwon,S.J.Park, R.M.German

12Commondefectsinmetalinjectionmolding(MIM)253

13Qualificationofmetalinjectionmolding(MIM)271

D.F.Heaney

14Controlofcarboncontentinmetalinjectionmolding281 GemmaHerranz

PartFourMetalinjectionmoldingofspecificmaterials407

19Metalinjectionmolding(MIM)oftitaniumandtitaniumalloys431

20Metalinjectionmolding(MIM)ofthermalmanagementmaterialsin microelectronics461 J.L.Johnson

21Metalinjectionmolding(MIM)ofsoftmagneticmaterials499 H.Miura

22Metalinjectionmolding(MIM)ofhigh-speedtoolsteels525 N.S.Myers,D.F.Heaney

23Metalinjectionmolding(MIM)ofheavyalloys,refractory metals,andhardmetals535 J.L.Johnson,D.F.Heaney,N.S.Myers

23.1Introduction

23.6Hardmetals

24Metalinjectionmolding(MIM)ofnickel-basesuperalloys575 K.Horke,A.Meyer,R.F.Singer

24.1Introduction

25Metalinjectionmolding(MIM)ofpreciousmetals609 J.T.Strauss

25.1IntroductionpreciousmetalMIM:Preciousmetalsandpowder

Contributors

S.Ahn PusanNationalUniversity,Busan,SouthKorea

S.V.Atre UniversityofLouisville,Louisville,KY,UnitedStates

S.Banerjee DSHTechnologiesLLC,CedarGrove,NJ;HoloInc.,Oakland,CA, UnitedStates

C.Binet AdvancedPowderProducts,Inc.,Philipsburg,PA,UnitedStates

S.H.Chung HyundaiSteelCo.,Incheon,SouthKorea

S.T.Chung CetaTechInc.,Sacheon,SouthKorea

T.Ebel Helmholtz-ZentrumGeesthacht,Geesthacht,Germany

R.K.Enneti GlobalTungstenandPowders,Towanda,PA,UnitedStates

R.M.German SanDiegoStateUniversity,SanDiego,CA,UnitedStates

C.D.Greene TreemenIndustries,Inc.,Boardman,OH,UnitedStates

O.Gulsoy MarmaraUniversity,Istanbul,Turkey

D.F.Heaney AdvancedPowderProducts,Inc.,Philipsburg,PA,UnitedStates

GemmaHerranz UniversityofCastillaLaMancha,INEI-ETSII,CiudadReal,Spain

J.Hidalgo DelftUniversityofTechnology,Delft,TheNetherlands

K.Horke JointInstituteofAdvancedMaterialsandProcesses,Friedrich-Alexander Universit€ atErlangen-N€ urnberg,Germany

K.S.Hwang NationalTaiwanUniversity,Taipei,Taiwan,ROC

C.J.Joens ElnikSystemsLLC,CedarGrove,NJ,UnitedStates

J.L.Johnson ElmetTechnologiesLLC,Lewiston,ME,UnitedStates

T.G.Kang KoreaAerospaceUniversity,Goyang,SouthKorea

K.H.Kate UniversityofLouisville,Louisville,KY,UnitedStates

Y.S.Kwon CetaTechInc.,Sacheon,SouthKorea

H.Lobo DatapointLabs,Ithaca,NY,UnitedStates

M.Martens FormatecCeramics,DVGoirle,TheNetherlands

A.Meyer JointInstituteofAdvancedMaterialsandProcesses,Friedrich-Alexander Universit€ atErlangen-Nurnberg,Germany

H.Miura KyushuUniversity,Fukuoka,Japan

N.S.Myers Kennametal,Inc.,Pittsburgh,PA,UnitedStates

K.Nishiyabu KindaiUniversity,Higashiosaka,Japan

V.P.Onbattuvelli IntelCorporation,SantaClara,CA,UnitedStates

S.J.Park POSTECH,Pohang,SouthKorea

V.Piotter KarlsruheInstituteofTechnology(KIT),Karlsruhe,Germany

G.Schlieper GammatecEngineeringGmbH,Radevormwald,Germany

R.F.Singer NeueMaterialienFurthGmbH,Germany

J.T.Strauss HJECompany,Inc.,Queensbury,NY,UnitedStates

P.Suri HeraeusMaterialsTechnologyLLC,Singapore,Singapore

J.M.Torralba InstituteIMDEAMaterials,UniversidadCarlosIIIdeMadrid, Madrid,Spain

P.Vervoort EisenmannThermalSolutions,Bovenden,Germany

1.3Industrystructure

TheMIMindustrystructureandinteractionsshowsgenerallythatthefirmsfallintoa fewkeyfocalpoints.Everythingrevolvesaroundthecustomfabricators,firmsthat formcomponentstosatisfythespecificationsoftheusercommunity—theusers aregenerallywell-knownfirmssuchasinfirearms(Glock,Colt,Remington),computers(HewlettPackard,Dell,Apple,Seagate),cellulartelephones(Motorola, Samsung,Apple),handtools(Sears,Leatherman,Snap-onTools),industrialcomponents(Swagelok,Pall,LG),andautomotive(Mercedes-Benz,Borg-Warner,Honda, BMW,Toyota,Chrysler).TheleadingconferencefocusedonMIMstartedin1990 andcontinuestoday,whereparticipantsgathertoshareinformationontechnology advances.Attheseconferencestheactorsintheindustrygenerallycomefromone ofthefollowingsectors:

l ingredientsuppliers—polymers,powders,andingredientsforeitherselfmixingorcommercialfeedstockproduction;globallythereareapproximately40firmsthatprovidemostofthe MIMpowders,althoughabout400firmssupplymetalpowdersofvariouschemistries,particlesizes,particleshapes,andpurities;forexample,intitaniumaboutfourcompaniesoutof 40suppliersmakethepowdersusedforMIM;

l feedstockproductionfirms—purchaserawingredientsandformulatemixturesforsalesto moldingfirms;globallythereareusuallyabout12feedstocksuppliers;

l moldingfirms—bothcustomandcaptivemoldersthattotalnearly300MIMoperations; aboutone-thirdarecaptiveandmakepartsforthemselves,butmanyofthecaptivefirms alsoperformcustomfabrication;83%ofallpartsproductioniscategorizedascustom manufacturing;

l thermalprocessingfirms—ownsinteringfurnacesanddebindingequipmentthatprovidetoll services;currentlyonlyahalf-dozenfirmsareactiveinthisareaandmostareassociatedwith furnacesfabricators;afewfirmsprovidetollhotisostaticpressingtoforce100%density whenrequiredinmedicaloraerospacefields;

l designers—largelysystemsdesignfirmsassociatedwithlargemultinationalfirmsthatintersectwiththeMIMindustry;afewindependentdesignersareavailabletohandleadhoc projects;

l equipmentsuppliers—firmsthatdesignandfabricatecustomfurnaces,molders,mixers, debindingsystems,roboticsystems,andothercapitaldevicessuchastestingdevices;the majorityofmoldingmachinesalesarefromsixfirms,furnacesalesarefromeightfirms, mixersalesarefromfourfirms,soabout20firmsconstitutethekeyequipmentsuppliers; Metalpowderinjectionmolding(MIM):Keytrendsandmarkets3

4HandbookofMetalInjectionMolding

l consumablessuppliers—supplyprocessatmospheres,chemicals,molds,polishingcompounds,machininginserts,packagingmaterials,heatingelements,andsinteringsubstrates;

l adjuncts—includingresearchers,instructors,consultants,designadvisors,conferenceorganizers,tradeassociationpersonnel,magazineeditors,andpatentattorneys.

Componentproductionisthecentralactivity.Itissplitbetweeninternalandexternal products,referredtoascaptiveandcustommolders.Likewiseitissupportedbytwo parallelsupplyroutes,dependingonthedecisiontoselfmixortopurchasepremixed feedstock.AnexamplecaptivemolderwouldbeafirearmcompanythatusesMIMto fabricatesomeofthesafety,trigger,orsightcomponents.Ontheotherhand,custom moldersalsocanmakethesesamecomponents,butjustaslikelymaybeinvolvedin severalapplicationareasasdeterminedbytheircustomerbase.

Asoutsourcingincreasesformultinationalfirms,customfabricationgrows. Accordingly,MIMfromfacilitiesownedbylargefirmssuchasRocketdyne,IBM, AMP,andGTEasearlyadopters,shiftedtopurchasingcomponentsfromcaptive moldersfocusedonavarietyofapplicationareas.Someoftheearlycaptiveapplicationsincludedthefollowingexamples:

l dentalorthodonticbracketsmadeoutofstainlesssteelorcobalt-chromiumalloys;

l businessmachinecomponentsforpostagemetersandtypewriters;

l watchcomponentsincludingweights,bezels,cases,bands,andclasps;

l cameracomponentsthatincludedswitchesandbuttons;

l firearmsteelpartssuchastriggerguards,sights,gunbodies,andsafeties;

l carbideandtoolsteelcuttingtoolssuchaswoodrouterbits,endmills,andmetalcutting inserts;

l electronicpackagesforelectronicsystemsusingglass-metalsealingalloys;

l personalcareitemssuchashairtrimmersusingtoolsteel;

l medicalhandtoolsforspecialsurgicaloperations;

l rocketenginesusingspecialtymaterialssuchasniobium;

l automotiveairbagactuatorcomponentsusinghardenablestainlesssteels;

l specialammunitionthatincludedbirdshot,armorpiercingandfrangiblebullets;

l turbochargerrotorsfortrucksandautomobilesformedfromhigh-temperaturestainless steelsornickelsuperalloys.

SinceeachoftheseMIMoperationshadasinglefieldoffocus,littlewasdonetogrow thatportionoftheindustry.However,inmorerecentyearsgrowthinMIMhascome withtheshifttocustommoldingwhichservicesawidevarietyofapplications.The custommoldingfirmshavejoinedtogetherineffortstoadvancetheindustry,viacollaborativemarketingefforts,promotionofmaterialstandards,publicitythrough annualawards,andsharingofbusinessdata.Althoughdeclining,captivemoldingstill remainsanimportantpartoftheMIMindustry.Althoughthesalesgrowthvariesyear toyear,inmostrecenttimes,theglobalsalesgainhasbeensustainedat14%peryear.

1.4Statisticalhighlights

MeasuresoftheMIMgrowtharepossiblethroughseveralparameters,includingthe following.

l Patents:SincethestartofMIMthetotalpatentgenerationislarge,exceeding300bytheyear 2000,butinmorerecentyearstherateofpatentgenerationhasslowedandtherearetoday about200currentlyactivepatents.

l Powdersales:In2010,morethan8000tonsofmetalpowderwereconsumedgloballyby MIM,withagrowthrateinpowdertonnageuseapproachingabout20%peryear,but duetopricereductionthevalueincreasesabout14%peryear.

l Feedstockpurchase:Thetwooptionsofself-mixingorpurchasingfeedstockseemtobeof equalmerit.Ofthetopfirms,71%formtheirownfeedstock,whichisalmostthesameratio forallcompaniesindependentofsize,suggestingpurchasedfeedstockisneitheranadvantagenordisadvantage;however,self-mixingdoesprovidegreatermanufacturingflexibility.

l Mixing:Forthosefirmsmixingtheirownfeedstock,in2011,theygenerate $1.8millionin salespermixer,butthetop20firmsthatmixtheirownfeedstockareat $7millioninsalesper mixerperyear.

l Salespermolder:Inmanycountries,especiallywhenanoperationisatahighutilization,the moldingmachinegeneratesatleast $1millioninsalesperyear.Acrosstheindustrythemean salespermolderis $536,000,whiletheleadingfirmshave $1.5millioninsalespermolder peryear.

l Salesperfurnace:Furnacescomeinmanydifferentsizesanddesigns,butacrosstheindustry salesaverageabout $1millionperfurnaceperyear;forthetopMIMoperations(withlarger andcontinuousfurnaces)thesalesaverage $3.2millionperfurnaceperyear.

l Continuousfurnaces:In2011,theinstalledcapacityofhigh-volumecontinuoussintering furnacesreached4500tonsofproductsperyear;theseareinstalledwithabreakdownof 38%Asia,47%Europe,and15%NorthAmerica.

l Captiveversuscustomproduction:Aboutathirdofthefirmsarecaptive,butonly21%ofthe firmshavemorethan50%oftheirsalesinternally.Thebestestimateisthat17%oftheproductionvaluein2011isforinternaluse.

l Salesperkg:AcrosstheMIMindustrytheaverageisabout $125insalesperkgofpowder consumed,rangingfromhighsof $10,000perkgforjewelry,cuttingtips,andprecisionwire bondingtoolsto $16perkgforcastingrefractories.Thelargestceramicapplicationisin aerospacecastingcores,andthetypicalis $1000perkg.Likewise,formetals,thestainless steelorthodonticbracketcontributesnearly $100millioninannualsalesatanaveragenear $650perkg.Thelowtolerancetungstencellphoneeccentricweightssellforaverylow price,inthe $60perkgrange.

l Salesperpart:Acrosstheindustry,thetypicalpartsalepriceisbetween $1and $2each,but valuesrangefrom5centcellphonevibratorweightsto $35solenoidbodiesand $400knee implants.

l Componentsize:ThemosttypicalMIMpartmassisinthe6–10grange.Themassrangeis frombelow0.02gtoover300g,butthemeanisunder10g.ThelargestMIMpartsareheat dissipatersforthecontrolsystemsinhybridelectricvehiclesat1.3kgandsomeaerospace superalloybodiesthathavesimilarmassanddimensionsreach200mm.Agrowingaspectof MIMisthemicrominiaturecomponentswherefeaturesareinthemicrometerrangeandthis approached $68millionperyearinsalesfor2010.

l Employment:Nearly8000peopleareemployedinPIMglobally,ofwhichnearly7000peopleareemployedinMIM,givinganaverageof21peopleperoperationandamedianofjust 16peopleperMIMfacility.Thelargerfirmsreachupwardsto300–800people;thelargest ceramicinjectionmoldingfirmoncereachedemploymentnear800people.

Historically,about80%ofthePIMfieldisformetalliccomponents,orMIM.Inrecent times,thathasincreasedtonearly90%metallic.Ofthe366firmsthatcurrently Metalpowderinjectionmolding(MIM):Keytrendsandmarkets5

6HandbookofMetalInjectionMolding

Table1.1 SummarystatisticsonPIM

PercentageofPIMfirmsinNorthAmerica31

PercentageofPIMfirmsinEurope28

PercentageofPIMfirmsinAsia37

PercentageofPIMfirmsinrestofworld4

LargestconcentrationoffirmsUSA,China,Germany,Japan

Percentageoffirmsprimarilycaptive33

LargestPIMfirmsIndia,USA,Germany,Japan

TotalPIMsales2010

$1.1billion

TotalPIMfirms366

TotalPIMemployment8000

TypicalR&Dstaff2

Typicalprofitas%ofsales11

Salesperfull-timeemployee

Salespermoldingmachine

Salesperproductionfurnace

$126,000

$538,000

$980,000

Percentoffirmsself-mixing72

Totalinstallednumberofmixers380

Totalinstallednumberofmoldingmachines1750

Totalinstallednumberoffurnaces850

Percentofindustryusingthermaldebinding49

Percentofindustryusingsolventdebinding26

Percentofindustryusingcatalyticdebinding14

Percentofindustryusingotherdebinding11

Medianpartsize(g)6

practicePIM,themajorityislocatedinAsia.TheleadingcountriesintermsofPIM weretheUSAwith106operations,Chinawith69(althoughexpansionisrapidin China),Germanywith41,Japanwith38,Taiwanwith17,Koreawith14,andSwitzerlandwith12.Thenumberofoperationsisnotnecessarilyindicativeoffinancial size,sinceoneofthelargestMIMfacilitiesisinIndia,acountrywhichonlyhasfive MIMoperations,whiletheUSAhasthemostfirms,buttheytendtobesmaller. Table1.1 providesasummaryofthePIMactivities.TheUSAandChinahavethe mostfirmswhilethelargestfacilityisinIndia.

ThePIMfieldisapproximatelyone-thirdcaptiveandtwo-thirdscustomproduction.Examplecaptiveoperationsincludeceramiccastingcoreproduction,orthodontics,surgicaltools,medicalimplants,andfirearms.

PIMincludesmetals,ceramics,andcarbides.Togetherthesematerialsamountto salesfor2010thatreached $1.1billion,withabout $1billioninmetalcomponents. Table1.2 providesasummaryontheglobalsalesperformance.In2011,ofthe366 firmspracticingPIM,somedomultiplematerials.Acrosstheindustryover80%of

Table1.2 SummaryofPIMglobalsales

Metalpowderinjectionmolding(MIM):Keytrendsandmarkets7

Table1.3 TypicalunitmanufacturingcellinmetalPIM Mixers1 Molders4 Debindingreactors2

Sinteringfurnaces2

Typicalnumberofemployeespercell20

Table1.4 Typicalproductivityratios

Meansalesperemployee

$125,000

Medianemployeespermoldingmachine5

Meanemployeespermoldingmachine4.2

Meanemployeesperproductionfurnace9

Medianemployeesperproductionfurnace6.7

Meansalespermoldingmachine

Mediansalespermoldingmachine

Meansalesperfurnace

Mediansalesperfurnace

Meansalespermixer(ifinstalled)

Mediansalespermixer(ifinstalled)

$536,000

$400,000

$976,000

$667,000

$1.8million

$1.0million

Mediangrowthpercentageinsales11

thefirmsproducemetalliccomponents,20%practiceceramicPIM,4%practice cementedcarbideinjectionmolding,andlessthan1%practicecompositeproduction (mostlyinjection-moldedsiliconcarbidethatisinfiltratedwithaluminumtoform Al-SiC).Obviously,about5%ofthefirmssupplyamixtureofmaterialtypes.

AMIMorPIMfacilitybasicallyrequiresmixing,molding,debinding,andsintering capabilities.Overtheyears,atypicalratiooftheseproductiondeviceshasemerged. Someoftheindustryunitmanufacturingcellratiosarecapturedin Table1.3.Notethat eachdeviceisaninteger(oneortwoorthreemixers)soforthemeanthevaluecanbe noninteger,butforthemedianonlyintegervaluesareallowed.

Anothermetriccomesfromtheproductivity,usuallymeasuredintermsofsalesor peremployee. Table1.4 givesseveralstatisticalproductivitymeasuresfortheglobal PIMindustry.Inthistable,theemploymentcountisbasedonfull-timeequivalent (FTE),sinceseveralfirmshavesignificantpart-timeemployment.Hence,thetypical PIMindustry(metals,ceramics,carbides,andcomposites)seemstobeastabulated.

1.5Industryshifts

ThekeytrendsinMIMonaglobalbasisareevidentbycomparingyear2000withyear 2010.Formanyyears,theMIMfieldsustainedcompoundannualsalesgrowthat22% peryearwitha34%peryearincreaseinthenumberofoperations.Inrecentyears,the

growthrateshavebecomemoremodestandhavestabilizednear8%peryearinNorth America,butcontinueata30%peryearpaceinAsia.Globallytheoverallaverageis 14%peryearforrecentyears.

Onthebasisofsomeimportantstatistics,herearethechangesfromyear2000to year2010forMIM:

l numberofMIMoperationsdecreased34%;

l globalsalesincreased100%;

l employmentincreased100%;

l installedmoldingcapacityincreased79%;

l installedsinteringcapacityincreased86%.

Thesestatisticsindirectlyindicateincreasedconcentrationofthebusinessintothe handsoffewerfirms.AlthoughalargenumberofcompaniesareactiveinMIM,at anyonetimesomearesimplyinanevaluationmode,andthiswasespeciallytrue in2000.Thesecharacteristicallyconsistofasmallteam(twoorthreepeople)and oneortwomoldingmachines,usuallypurchasedfeedstock,andmightevenrely ontollsintering.Afterinitialexploration,manysucheffortsareterminatedorproductionistransferredtoanoutsidevendor.Thisisevidentbythedecreaseinnumberof MIMfirmsfrom2000to2010whiletheoverallfieldgrew.Today,largeactorsconsist ofwellover20moldingmachines.

1.6Salessituation

Salesstatisticswerefirstgatheredinthemiddle1980s.Significantgrowthhasproducedindustrymaturation.ThemetalPIMprocessisnowacceptedbyseveralsophisticatedcustomers,suchasBosh,Siemens,Chrysler,Honeywell,Volkswagen, MercedesBenz,BMW,Chanel,AppleComputer,PrattandWhitney,Samsung,Texas Instruments,GeneralElectric,Nokia,Motorola,RollsRoyce,Continental,Stryker, LG,Sony,Philips,Seagate,Toshiba,Ford,GeneralMotors,IBM,Hewlett-Packard, Seiko,Citizen,Swatch,andsimilarfirms.

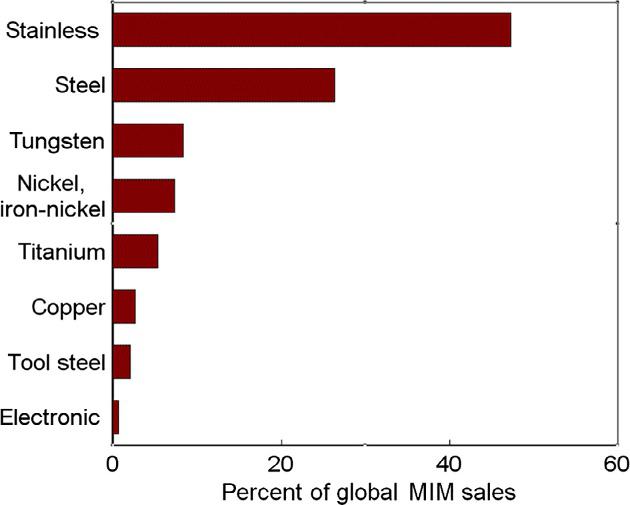

MostofthecommonengineeringmaterialsareavailableinMIM,butasillustrated in Fig.1.1,basedonsales,stainlesssteelsaredominant.Theglobalmaterialsales (value,nottonnage)areasfollows—53%stainlesssteels,27%steels,10%tungsten alloys,7%iron-nickelalloys(mostlymagneticalloys),4%titaniumalloys,3%copper,3%cobalt-chromium,2%toolsteels,2%nickelalloys(superalloys),and1%electronicalloys(KovarandInvar).Onatonnagebasis,thestainlesssteelportionof powderconsumptionislarger,reachingupwardsto60%–65%ofpowderconsumption,andbecauseofthatlargeconsumptionthepowderpriceislower,furtherfueling theuseofstainlesssteel.Someofthemetalpowdersaremuchhigherpriced,suchas titanium,sothesalespartitionbasedontonnageversusdollarsisskewedduetoawide rangeinmaterialcosts.

ThemetalPIMsalesfor2010wereintheneighborhoodof $1billiondollars.Independentreportsfor2010giveestimatesfrom $955to $984million.Somedifficulty existsingatheringaccurateinformationsinceamajorityofthefirmsareprivatelyheld anddonotmakeannualreports.Further,currencyexchangerateschangeovertheyear

leadingtoinaccurateestimates.For2010,thebestestimateonPIMsalesis $1.1billion andMIMsalesis $955million.ThePIMestimatefor2009was $920million,soPIM grewfrom2009to2010byalmost20%,largelyinMIM,andwasaheadofthegeneral economicrecovery.

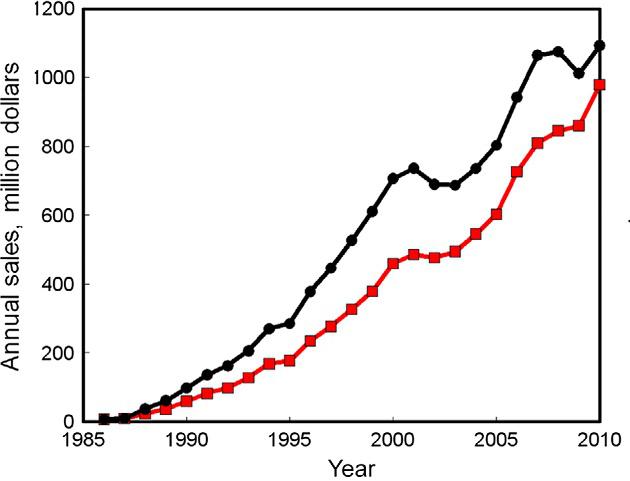

Fig.1.2 plotssalesgrowthgloballysincefirstrecordedat $9millionfor1986.This plotshowsthattheceramicbusinesscontractedwhileMIMexpanded,largelydueto theaerospaceslowdowns.

Fig.1.1 MIMsalesgloballybymainmaterialcategory.Thisplotisbasedpercentofglobal sales,whileotherstudiesreportbasedontonnageofpowderconsumed.

Fig.1.2 Annualsales,inmillionsofUSdollars,forMIMasthelowercurveandallofPIMas theuppercurveplottedagainstyear. Metalpowderinjectionmolding(MIM):Keytrendsandmarkets9

10HandbookofMetalInjectionMolding

Table1.5 SummaryglobalMIMstatistics

2009totalMIMsales

2010totalMIMsales

$860million

$955million

Typicalprofitas%ofsales9 %MIMsalesfromself-mixing63

InstallednumberofMIMmixers290

InstallednumberofMIMmoldingmachines1450

1.7Marketstatistics

ThelargestmarketforMIMhashistoricallybeenindustrialcomponents,including pumphousings,solenoids,handles,plumbingfixtures,andfitting.Thisstillamounts to20%ofglobalsales(moreinJapanandlessinEurope).Thisisbasedoncomponent sales,notnumberofpartsorfirmsortonsofpowder,asisreportedinotherstudies. AutomotivecomponentsarethesecondlargestmarketforMIMat14%ofglobalvalue (ontonnagebasisitismuchhigherinEuropeandlowerinNorthAmerica).Consumer productsarethethirdlargestmarketat11%oftheMIMsales,andthesearedominated byAsia(cellphone,consumer,andcomputerparts).Nextarethedental,medical, electronic,andfirearmapplications,eachat7%–9%oftheglobalMIMproductvalue, withNorthAmericabeingthelargestactor.Othercontributionscomefromcomputers,handtools,luggagetrimmings,cosmeticcases,robots,sportingdevices, andwatchcomponents.

ThestatisticalprofileforMIMfirmsshowsthatabouthalfoftheglobalactorsare tiny,beingunder $1millioninannualMIMsales;sometimesthesearelocatedaspilot effortsinlargecompaniesormorecommonlyreflectingprivateownership. Table1.5 givesanindustrysummaryforMIM.About32%oftheoperationshavecaptiveproducts,butonly18%oftheindustrysalesareprimarilycaptive.FollowingthePrado Principle,inMIMthelargest20%offirmscontrol80%ofsales.Moreover,the top10%ofMIMfirmscontrolover60%ofsales,average $25millionperyearturnoverandrunwith20ormoremoldingmachinesandanaverageof120employees.The top10%oftheMIMindustryaveragefiveemployeesforeachmolder,ninepeopleper furnace,turnover $1.5millionpermoldingmachineeachyear, $3.2millionperfurnaceeachyear,and70%self-mix.

1.8MetalPIMmarketbyregion

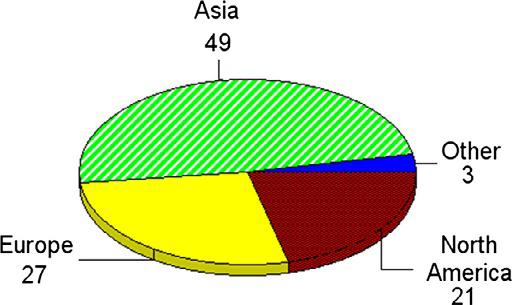

Asshownin Fig.1.3,theprimarysalesandgrowthinMIMisinAsia,buttheUSA remainsoneofthelargestusersandproducersofceramicPIMcomponents. Table1.6 summarizestheregionalstatisticsforPIMinmillionsofdollarsfor2009,thelastyear whereconsolidateddataarereported.Forreference,NorthAmericanMIMwas $186 millionin2009outofthe $316milliontotal.Ofthat $32millionwascaptiveMIM.In NorthAmerica,captiveMIMisfrequentlyusedfororthodonticbracketsandfirearms,

Metalpowderinjectionmolding(MIM):Keytrendsandmarkets11

Fig.1.3 Salespartitionbasedonmajor geographicregion.

Table1.6 SummaryofregionalsalesforPIM

RegionTotalPIM($ million)

butisalsousedformedicalapplications.Thevaluationofthoseproductsisdifficult, sincethedistributedcost(whenthebracketissoldtothedentist)isprobably $100 million,butthetradecost(bulkinternaltransfercost)ismoremodest.For2009,in Europe,thedominantcaptiveMIMapplicationswerewatchesandsimilardecorative componentssuchasspecialtyluggagefasteners.In2009,theSwisswatchindustrydid about $12billioninwatchsales,atanaveragetransactionof $566perwatch.Notall watchesuseMIM,butthosethatdohaveatypicalMIMcontentinthe $1–$8range,so the21millionwatcheswouldfitwiththe $32millioncaptiveEuropesales.InAsia,the captiveMIMismostlyforthe“3Cs”—productsforcomputers,cellulartelephones, andconsumerelectronics—attheassemblyhousessuchasFoxconn.

1.9MetalPIMmarketbyapplication

Inpriorreportsfromsomeofthetradeassociations,suchastheMetalPowderInjectionMoldingAssociationin2006,themedicalcomponentsalesconstituted36%of MIM,theautomotivecomponentwas14%ofsales,andhardwarewas20%ofsales. Inthe2007survey,theMIMmarketwaspartitionedasgivenin Table1.7 interms ofpercentageofsalesineachgeographicregion.Morerecently,anexpandedsetof applicationgroupsisusedtoreflectaddedeffortsinsporting,jewelry,handtools, aerospace,andsuch.Further,consumerproductswereseparatedfromwatchessince watchproductionwasnotgrowing,butusesforlatches,eyeglasses,andluggage claspswasgrowing.Accordingly,the2010industrypartitionedbyapplicationarea