ENGINEERING ECONOMIC ANALYSIS

NEWNAN JONES

WHITTAKER

ESCHENBACH

LAVELLE

OXFORD UNIVERSITY PRESS

OxfordUniversityPressisadepartmentoftheUniversityofOxford. ItfurtherstheUniversity'sobjectiveofexcellenceinresearch,scholarship, andeducationbypublishingworldwide.Oxfordisaregisteredtrademarkof OxfordUniversityPressintheUKandincertainothercountries.

Publishedin Canadaby

OxfordUniversityPress

8SampsonMews,Suite204, DonMills,Ontario M3COHSCanada www.oupcanada.com

Copyright©OxfordUniversityPressCanada2018

Themoralrightsoftheauthorshavebeenasserted DatabaserightOxfordUniversityPress(maker)

FirstCanadianEditionpublishedin 2006

SecondCanadianEditionpublishedin 2010

ThirdCanadianEditionpublishedin 2014

OriginaleditionpublishedbyOxfordUniversityPress,Inc., 198MadisonAvenue,New York,N.Y. 10016-4314,USA. Copyright©2012,2009,2004byOxfordUniversityPress,Inc.

Allrightsreserved.Nopartofthispublicationmaybereproduced,storedin aretrievalsystem,ortransmitted,inanyformorbyanymeans,withoutthe priorpermissioninwritingofOxfordUniversityPress,orasexpresslypermitted bylaw,bylicence,orundertermsagreedwiththeappropriatereprographics rightsorganization.Enquiriesconcerning reproduction outsidethescopeofthe aboveshouldbesenttothePermissionsDepartmentattheaddressabove orthroughthefollowingurl: www.oupcanada.com/permission/permission_request.php Everyefforthasbeen madetodetermineandcontactcopyrightholders. In thecaseofanyomissions,thepublisherwillbepleasedtomake suitableacknowledgementinfutureeditions.

LibraryandArchivesCanadaCataloguinginPublication

Newnan, DonaldG.,author

EngineeringeconomicanalysisI DonaldG. Newnan,JohnJones,John Whittaker,TedG.Eschenbach,JeromeP.Lavelle. - Fourth Canadianedition. Includesbibliographicalreferencesandindex. Issuedinprintandelectronicformats.

ISBN 978-0-19-902511-4(hardcover).-ISBN 978-0-19-902522-0(PDF) 1.Engineeringeconomy-Textbooks. 2.Textbooks. I.Jones,John(John Dewey),author II.Whittaker,J. D.,author III.Eschenbach,Ted,author IV.Lavelle,JeromeP.,author V.Title.

TA177.4.N4862018 658.15 C2017-905532-l C2017-905533-X

Coverimage:© RavilSayfullin/123RF Coverandinteriordesign:SherillChapman OxfordUniversityPressiscommittedto our environment. Whereverpossible,ourbooksareprintedonpaperwhichcomesfrom responsiblesources.

Printedand boundin Canada 1 2 3 4-21 20 19 18

Preface and Acknowledgements ix

1 Economic Decisions, EngineeringCosts, and Cost Estimating 2

ASea of Problems 4

Simple Problems 4

IntermediateProblems 4

Complex Problems 4

The Role of EngineeringEconomicAnalysis 5

Examplesof Engineering Economic Analysis 5

The Decision-MakingProcess 6

Rational Decision Making 6

Ethics 12

Ethical Dimensionsin EngineeringDecision Making 12

Importanceof Ethicsin Engineeringand Engineering Economy 14

EngineeringDecisionMakingforCurrentCosts 14

EngineeringCosts 17

Fixed,Variable,Marginal,and Average Costs 17

Sunk Costs 19

Opportunity Costs 20

Recurringand Non-RecurringCosts 21

Incremental Costs 21

CashCostsversus BookCosts 22

Life-Cycle Costs 22

CostEstimating 23

Typesof Estimate 23

Difficultiesin Estimation 24

EstimatingModels 25

Per-Unit Model 25

Segmenting Model 25

Cost Indexes 25

Power-SizingModel 27

Triangulation 28

Improvementandthe Learning Curve 28

EstimatingBenefits 31

Cash Flow Diagrams 31

Categoriesof Cash Flow 32

Drawinga Cash Flow Diagram 32

Summary 32 Problems 34

2 Accountingand Engineering Economy 50

The Role ofAccounting 52

Accountingfor BusinessTransactions 52

TheBalanceSheet 53

Assets 53

Liabilities 54

Equity 54

FinancialRatiosDerivedfromBalanceSheetData 55

The Income Statement 55

FinancialRatiosDerivedfromIncomeStatementData 57

LinkingtheBalanceSheet.IncomeStatement.andCapitalTransactions 57

Traditional CostAccounting 59

Directand IndirectCosts 59

IndirectCostAllocation 59

ProblemswithTraditionalCostAccounting 59

OtherProblemstoWatchFor 61

Summary 61

Problems 62

3 Interest and Equivalence 66

Computing Cash Flows 67

TimeValueofMoney 69

SimpleInterest 70

CompoundInterest 70

RepayingaDebt 71

Equivalence 73

Single-PaymentCompoundInterest Formulas 75

Nominaland EffectiveInterest 79

ContinuousCompounding 83

SinglePaymentInterestFactors:ContinuousCompounding 83

EquivalenceandSustainability 86

Summary 86

Problems 87

4 Equivalence for Repeated Cash Flows 94

UniformSeriesCompound Interest Formulas 96

CashFlowsThatDoNotMatchBasicPatterns 102

RelationshipsbetweenCompound Interest Factors 106

The Interest RateViewedasFog 107

ArithmeticGradient 108

DerivationofArithmeticGradientFactors 108

RealityandtheAssumed Uniformityofa, G, andg 114

Geometric Gradient 115

WhenCompounding Periodand Payment Period Differ 118

UniformPaymentSeries:ContinuousCompoundingat

NormalRaterperPeriod 120

Summary 122

Problems 125

5 Present Worth Analysis 140

AssumptionsinSolvingEconomicAnalysisProblems 142

End-of-YearConvention 142

ViewpointofEconomicAnalysisStudies 142

BorrowedMoneyViewpoint 143

IncomeTaxes 143

EffectofInflationandDeflation 143

EconomicCriteria 143

PresentWorthTechniques 143

1.UsefulLivesEqualtotheAnalysisPeriod 144

2.UsefulLivesDifferentfromtheAnalysisPeriod 145

3.InfiniteAnalysisPeriod:CapitalizedCost 148

MultipleAlternatives 151

BondPricing 153

FutureWorthAnalysis 154

Summary 156

Problems 156

6 Annual Cash Flow Analysis 176

AnnualCashFlowCalculations 178

ConvertingaPresentCosttoanAnnualCost 178

TreatmentofSalvageValue 179

AnnualCashFlowAnalysis 182

Analysis Period 182

AnalysisPeriodforaCommonMultipleofAlternativeLives 183

AnalysisPeriodforaContinuingRequirement 183

InfiniteAnalysisPeriod 184

SomeOtherAnalysisPeriod 185

MortgagesinCanada 186

BuildinganAmortizationSchedule 187

TypesofMortgageAvailable 188 Equity 188

MortgageInterestRate 188

Summary 189

Problems 189

7 Rate of Return Analysis 200

MinimumAttractiveRateofReturn 202

InternalRateofReturn 203

CalculatingRateofReturn 204

PlotofNPWversusInterestRatei 207

InterestRatesWhenThereAreFeesorDiscounts 209

IncrementalAnalysis 212

AnalysisPeriod 216

SensitivityAnalysis 217

ASecondPitfall 220

Summary 223

Problems 224

8 Benefit-Cost Ratio and Other AnalysisTechniques 242

PublicSectorInvestmentObjectives 244

ViewpointforAnalysis 245

SelectinganInterestRate 247

NoTime-Value-of-MoneyConcept 247

Cost-of-CapitalConcept 247

Opportunity-CostConcept 247

RecommendedConcept 248

TheBenefit-CostRatio 248

IncrementalBenefit-CostAnalysis 249

ElementsoftheIncrementalBenefit-CostRatioMethod 249

OtherEffectsof Public Projects 252

ProjectFinancing 252

DurationofProject 253

QuantifyingandValuingBenefitsandCosts 254

ProjectPolitics 255

PaybackPeriod 257

Summary 262

Problems 262

9 Selection of a Minimum Attractive Rate of Return 272

SourcesofCapital 275

MoneyGeneratedfromtheFirm'sOperations 275

ExternalSourcesofMoney 275

ChoiceofSourcesofFunds 275

CostofFunds 276

CostofBorrowedMoney 276

CostofCapital 276

InvestmentOpportunities 277

OpportunityCost 277

ChoosingaMinimumAttractiveRateofReturn 280

Adjusting MARRtoAccountforRiskandUncertainty 281

RepresentativeValuesofMARR UsedinIndustry 281

CapitalBudgeting.orSelectingtheBestProjects 282

Summary 284

Problems 285

10 Uncertainty in Future Events 292

Break-EvenAnalysis 295

OptimisticandPessimisticEstimates 296

Probability 298

JointProbabilityDistributions 301

ExpectedValue 303

Economic DecisionTrees 305

Risk 311

RiskversusReturn 313

Simulation 315 Summary 318

Problems 319

11 Income, Depreciation, and Cash Flow 330

Taxation 332

BasicAspectsof Depreciation 333

DeteriorationandObsolescence 333

DepreciationandExpenses 334

TypesofProperty 335

CostBasis 336

CalculatingDepreciation 336

DepreciationMethods 337

Straight-LineDepreciation 337

Sum-of-Years'-DigitsDepreciation 339

Declining-BalanceDepreciation 341

Unit-of-ProductionDepreciation 342

DepreciationforTax Purposes-CapitalCostAllowance 343

The50%Rule,orHalf-YearConvention 344

AcceleratedCCA-50%Straight-Line 344

CalculatingtheCCA-Schedule8 347

CalculatingtheCCAandtheUCC(withoutUsingSchedule8) 351

DepreciationandAssetDisposal 351

NaturalResourceAllowances 353

PercentageDepletion 353

CostDepletion 355

Summary 355

Problems 356

12 After-TaxCash Flows 366

A PartnerintheBusiness 369

CalculationofTaxableIncome 369

TaxableIncomeofIndividuals 369

CorporateIncomeTaxes 373

UsingCCAtoCalculateNetProfit 375

AccountingandEngineeringEconomy 376

CalculatingNetCashFlow 379

AcquiringandDisposingofAssets 381

NetSalvageofLand-CapitalGain 381

NetSalvage-Books-ClosedAssumption 382

CapitalTax FactorsandBooksOpen 383

CalculatingAfter Tax PresentWorth 385

WorkingCapitalRequirements 388

InitialWorkingCapital 389

IncreasingWorkingCapitalRequirement 389

LoanFinancing 390

LoanwithEqualPrincipalRepayment 391

LoanwithEqualAnnualRepayment 392

EstimatingtheAfter-TaxRateofReturn 393

Summary 394

Problems 395

13 ReplacementAnalysis 408

TheReplacementProblem 410

ReplacementAnalysisFlow Chart 411

Minimum-CostLifeofaNewAsset TheChallenger 412

Defender'sMarginalCostData 414

ReplacementAnalysisTechnique 1: DefenderMarginalCostsCanBeComputedandAre Increasing 416

ReplacementRepeatabilityAssumptions 417

ReplacementAnalysisTechnique 2: DefenderMarginalCostsCanBeComputedandAre NotIncreasing 418

ReplacementAnalysisTechnique 3: WhenDefenderMarginalCostDataAre Not Available 422

ComplicationsinReplacementAnalysis 422

Defining DefenderandChallenger FirstCosts 422

RepeatabilityAssumptions NotAcceptable 424

ACloser Lookat Future Challengers 425

After-TaxReplacementAnalysis 426

Marginal CostsonanAfter-Tax Basis 426

Minimum-CostLife Problems 428

SpreadsheetsandReplacementAnalysis 430

Summary 432

Problems 433

14 Inflationand Price Change 444

MeaningandEffectofInflation 446

HowDoesInflation Happen? 446

Hyperinflation 447

DefinitionsforConsideringInflationinEngineeringEconomy 447

AnalysisinReal DollarsversusActualDollars 454

PriceChangewithIndexes 456

WhatIsaPriceIndex? 456

CompositeversusCommodityIndexes 458

Howto UsePriceIndexesinEngineeringEconomicAnalysis 459

Cash FlowsThat InflateatDifferentRates 461

DifferentInflationRatesper Period 463

EffectofInflationonAfter-TaxCalculations 464

InflationandtheBuy/Lease Decision 467

InflationandtheCostofBorrowedMoney 470

Summary 471

Problems 472

15 Introductionto Project Management 482

ScientificManagement 483

TheGanttChart 484

CriticalPathMethod(CPM) 487

CPMandPERT 491

The MethodsofOperationsResearch 498

LinearProgrammingandtheSimplex Method 498

Queuing Theory 499

Summary 499

Problems 500

Glossary 504

References 508

Index 510

Preface and Acknowledgements

Engineeringistheapplicationofknowledgetodeveloppracticalandeconomicalsolutions to the problems that confront ourcivilization.Canada,withanareaof 9,984,670 km2 , isthe second-largest countryin the world. But withapopulation ofabout35,300,000, Canadahas less than0.5% ofthe world's people. In populationdensitywe rankabout 230th,with3.9peoplepersquarekilometreoflandarea.Becausemuchofthecountryis acoldandunforgivingplace,Canadianshaveneededalltheengineeringskillstheycould musterinordertoexistinthisformidableenvironmentand,indoingso,toconsistently achieveapositioninthetopfiveontheUnitedNationslistofthebestcountriestolivein.

Thehistoryofthiscountryisahistoryofengineeringinnovationandadaptability.The ingeniousdesignofthebirchbarkcanoeenabledFirstNationspeopletotravelthousands ofkilometresanddeveloptradingroutesthatspannedthecountry.Inthe1800s,engineersfromBritaintaughtushowtoconstructcanalstocircumventrapids;webuiltonthat knowledge,andwiththeopeningoftheStLawrenceSeawayin1959,ocean-goingshipsof commercewereabletobypassevensogreatanobstacleasNiagaraFallsandpenetratethe heartofthecontinent.

ThepromiseofatranscontinentalrailwaywaswhatbroughtBritishColumbiaintothe CanadianConfederation, andagaintheengineersresponded,completing the projectin 1885andopeningthewesternprovincestosettlementanddevelopment.

Canoesworkwellinthesummer,butwintertravelposesspecialchallenges.JosephArmandBombardierattachedaFordenginetoasleigh,which,withcontinuingengineeringrefinements,evolvedintotheirsnowmobile,theSkidoo,anditsinventor'scompany becametheaircraftandlight-rail-transitmanufacturerBombardier,Inc.

TheneedtocommunicatewithnorthernsettlementsledCanadianengineerstodevelop theAnikcommunicationssatellite.And our need tocommunicate,wherever we happentobe,ledaUniversityofWaterlooengineeringstudent,MikeLazaridis,todevelop theBlackBerryandcreatethecompanyResearchInMotion(RIM).

Engineeringhasalwaysbeenamixtureofneed,practicality,andeconomics.Theconceptsofethics,sustainability,andenvironmentalstewardshiparenowbeingaddedtothat mix.This book introduces theeconomicdecisionsthataccompanyengineeringdesign, butitalsoincludesquestionsthatexplorethoseotheraspects.Eachchapterbeginswith avignettedescribingaCanadianengineeringchallengeandinvitingthereadertothink aboutthebroaderimplicationsofengineeringdecisions.

Changes to the Fourth Edition

This edition hassignificantimprovements in organization andcoverage.Before going chapterbychapter,we'dliketopointoutafewglobalchangesmadetokeepthistextthe mostcurrentandmostusefulintoday'scourses:

• Anewdiscussionontheenvironmentalimpactsofengineeringprojectshasbeen added.

• AdditionalCanadianexamplesareincludedthroughout.

• AllunitsarenowinSI.

• Wehaveexpandedcoverageofmoney,inflation,andtheBankofCanada.

• The majority ofin-chapter Excel explanationshave been removed and placed online.

x PrefaceandAcknowledgements

Numerousimprovementstothecontentandwordinghavebeenmadethroughoutthe text.Thetexthasbeencondensedandsomeprintmaterial,suchasthecompoundinterest tables,hasbeenplacedonline.

Changesfromthethirdeditionincludethefollowing:

• Chapters1and2havebeencombinedandcondensedintoonechapter.

• Chapter8hasbeeneliminated,andsomematerialhasbeendistributedinother chapters(informationonincrementalanalysistoChapter7,futureworthcontent toChapter5,benefit-costratiotoChapter8,sensitivityandbreak-evencontent toChapter10).

• Chapter17hasbeenmoveduptobecomeChapter2.

• Chapter16hasbeenmoveduptobecomeChapter8.

• Anewchapteronprojectmanagementhasbeenadded.

• InChapter 12,theexplanationforcalculationoftaxesforindividualshasbeen revisedforclarity,andthecalculationofafter-taxcashflowshasbeenrevised.

Icons

Thesemarginaliconsappearthroughoutthetexttohighlightimportant keyconcepts.

TheseiconsappearintheProblemssectionattheendofeachchaptertosignifythat theanswertotheproblemcanbefoundonthecompanionwebsite:www.oupcanada .com/Newnan4Ce

A Special Word on Spreadsheets

Inthisedition,theauthorshavedeliberatelyomittedanydiscussionofhowtouseanyform ofspreadsheetsoftware.Sincetherearemanyspreadsheetprogramsavailable,andsince theirdetailschangefrequently,thesedetailsare better obtainedfromonline documentation.Studentswillnoticeratherquicklythattheuseofasuitablespreadsheetprogram cangreatlyreducethelabourinvolvedinsolvingeconomicproblems,andtheyshouldbe encouragedtodothis.

Acknowledgements

Thistextbookistheresultofthehardworkofalotofpeopleforover35years.I,along withOxfordUniversityPressCanada,wouldliketogratefullyacknowledgethefollowing reviewers,aswellasthosewhowishedtoremainanonymous:

SohaEidMoussa,UniversityofGuelph

TiffanyBayley,UniversityofWaterloo

ScottFlemming,DalhousieUniversity

MichaelBennett,UOIT

JuanPernia,LakeheadUniversity

MichaelH.Wang,UniversityofWindsor

NadineIbrahim,UniversityofToronto

Theirthoughtfulcommentsandsuggestionshavehelpedtoshapethefourthedition ofthistext.

For the fourth Canadian edition, I would like to thank all the people at OUP Canada-includingMegPatterson,LaurenWing,SuzanneClark,andLianaSpada-and DougLinzeyofAgricolaCommunications.Finally,Iwanttothankmywife,Joan,andmy daughterandeditorialcriticAli.

JohnJones

SimonFraserUniversity,2017

Alternative Futures

Economic Decisions, Engineering Costs, and Cost Estimating

There is no better place to start an engineering economics text than with a discussion of the future of the car, for that question embodies many of the technology and economic factors involved. Hybrids, plug-in electrics, turbocharged diesels, and advanced gasoline engines all compete for the buyer's (and driver's) attention. In 2016 the lineup included the following sedans:

sjo/iStock Photo

Choosing the rightvehicle is a complex problem, and evaluating the choices requires much more information than the price and fuel mileage. Willyou bedriving in the country or city, or a mix? How far doyou drive in ayear? What will the future price of energy (gas. diesel. electricity) be? Howlongwillyou keepthecarbeforeyou sellit? Whatwilltheresalevalue be? Whatfinancing termsdothesellersoffer?

Electricvehicletechnologyhas beenslowlyimproving. Since2012. the UniversityofWaterloo has been challenging teams of high-school students to design and build all-electric vehicles to compete in a 12-volt and a 24-volt endurance race. In the first yearof the competition. Bluevale Secondary School won the 12-volt and 24-volt races. with 41 and 61 laps, respectively. In 2013, theywerenarrowlyedgedoutoffirstplace in the12-voltrace byResurrection Catholic Secondary School, who completed 51.9 laps, but retained first place in the 24-volt race with an impressive 95 laps.

Butthegasoline and dieselengineershavenotbeenstanding still. Futuredriverswillcontinue to beoffered an arrayoftechnologies and will haveto useengineering economicanalysistofind thecorrectchoices.

QUESTIONS TO CONSIDER

1. What marketplace dynamics stimulate or suppress the development of alternative-fuel vehicles? What role. ifany,doesgovernmenthaveinthesedynamics? What additional responsibilitiesshould government have?

2. Developalistofconcernsand questionsthatconsumersmighthaveabouttheconversiontoalternative-fuel vehicles. Which areeconomicfactors. andwhich are non-economic?

3. Some environmentalists have proposed producing bio-fuels from crops as an alternative to fossil fuels. What ethical questions might this involve?

4. Power companies have a lot of extra capacity at night, and so there is a possibility of their offering off-peak power at a reduced cost. This could be used by people with plug-in hybrids. How much investment would a power company have to make in smart circuits for a time-variable pricing policyto be possible?

LEARNING OBJECTIVES

Thischapterwillhelpyou

• describetheeconomicdecision-makingprocess

• chooseappropriate economiccriteria fordifferentproblems

• describe common ethical issues in engineering economic decisions

• definevariouscostconcepts

• providespecificexamplesofhowandwhythese engineeringcostconceptsare important

• defineengineeringcostestimating

• explain thethreetypesofengineering estimates.aswellas common difficultiesencountered in making them

• useseveralcommon mathematicalestimating models incostestimating

• discuss theeffectofthelearningcurveoncostestimates

• drawcash flowdiagramstoshowprojectcostsand benefits

KEYTERMS

averagecost bookcost cashcost cashflowdiagram estimating byanalogy fixedcost forgoneopportunity incremental cost learningcurve

A Sea of Problems

learning curvepercentage learningcurverate life-cyclecosting marginalcost model building non-recurringcost opportunitycost out-of-pocketcost overhead

per unit model power-sizing model recurringcost segmenting model shadow price sunkcost triangulation variablecost

Thisbookisaboutmakingdecisions.Itdevelopsthetoolsforanalyzingandsolvingeconomicproblemscommonlyfacedbyengineers. Our emphasis is on solving problems that confrontfirms in the marketplace, but manyexamplesareproblemsstudentsfaceindailylife.Letusstartbylookingatsomeof theseproblems.

Simple Problems

Manyproblemsaresimple,andgoodsolutionsdonotrequiremuchtimeoreffort.

• ShouldIpaybycashorcreditcard?

• DoIbuyasemesterparkingpassorusetheparkingmeters?

• Shouldwereplaceaburned-outmotor?

• Ifweusethreecratesofanitemaweek,howmanycratesshouldwebuyatatime?

Intermediate Problems

Atthemiddlelevelofcomplexity,wefindproblemsthatareprimarilyeconomic.

• ShouldIbuyorleasemynextcar?

• Whichpiecesofequipmentshouldbechosenforanewassemblyline?

• Shouldourofficeupgradetothenewestversionofourprojectmanagementsoftware?

• ShouldIbuyaone-ortwo-semesterparkingpass?

• Shouldwebuyalow-costpressrequiringthreeoperators,oramoreexpensiveone requiringonlytwooperators?

Complex Problems

Complexproblemsrepresentamixtureofeconomic,political,andsocialandethicalelements.

• ThequestionofbuildingpipelinestoexportAlbertanoiloverseasisanexample ofacomplexproblem.Pipelinessuchas theproposedNorthernGatewayfrom AlbertatoKitimat,BC,willbenefittheAlbertaneconomyandcreatejobsinthe Albertanoilindustry.Ontheotherhand,someenvironmentalistsbelievethatthe riskofoilspillswillendangerFirstNationslandsandtheBCcoastline.Globally,

burningAlberta'soilwillincreaseglobalwarming,withpossibleadverseconsequencesworldwide.

• Thechoiceofagirlfriendoraboyfriend(whomaylaterbecomeaspouse)isobviouslycomplex.Economicanalysiscanbeoflittleornohelp.

• Theannualbudgetof acorporationisanallocation of resources,andall projectsareevaluatedeconomically.Thebudgetprocessisalsoheavilyinfluencedby non-economicforcessuchaspowerstruggles,geographicalbalancing,andeffects onindividuals,programs,andprofits.

The Role of Engineering Economic Analysis

Engineeringeconomicanalysisismostsuitableforintermediateproblemsandtheeconomicaspectsofcomplexproblems.Suchproblemshavethefollowingcharacteristics:

1. Theproblemisimportantenoughtojustifyseriousthoughtandeffort.

2. Theproblemcan'tbeworkedoutinone'shead-thatis,acarefulanalysisrequires thatweorganizetheproblemandallthevariousconsequences.

3. Theproblemhaseconomicaspectsthatareimportantinreachingadecision.

Vastnumbersofproblemshavingthese threecharacteristicsareencounteredinthe businessworldandinpeople'spersonallives,soengineeringeconomicanalysisisoften required.

Examplesof Engineering EconomicAnalysis

Engineeringeconomicanalysisfocusesoncosts,revenues,andbenefitsthatoccuratdifferenttimes.Forexample,whenanuclearengineerdesignsareactor,theconstructioncosts occurinthenearfuture;benefitstotheusersbeginonlywhenconstructionisfinished,but continueforalongtime.

Engineeringeconomicanalysisisusedtoanswermanydifferentquestions.

• Whichengineeringprojectsareworthwhile?Hastheminingorpetroleumengineershownthatthemineraloroildepositisworthdeveloping?

• Whichengineeringprojectsshouldhaveahigherpriority?Hastheelectricalengineershownthatreplacingtheplant'sstep-downtransformerismore urgentthan upgradingthepowersupplytothemachineshop?

• Howshouldtheengineeringprojectbedesigned?Has the mechanical engineer chosenthemosteconomicalsizeofmotor?Hasthesoftwareengineercalculated thedevelopmenttimeforwritingthenextreleaseofthesoftware?Hastheaeronauticalengineermadethebesttrade-offsbetween(1)lightermaterialsthatare expensivetobuybutresultinaplanethatischeapertoflyand{2)heaviermaterialsthatarecheaptobuybutresultinaplanethatismoreexpensivetofly?

Engineeringeconomicanalysiscanalsobeusedtoanswerquestionsthatarepersonallyimportant.

• Howtoachievelong-termfinancialgoals:Howmuchshouldyousaveeachmonth tobuyahouse,retire,orfundatriparoundtheworld?Isgoingtograduateschool agoodinvestment?

• Howtocomparedifferentwaystofinancepurchases:Isitbettertofinanceyour carpurchasebyusingthedealer'slow-interestloanorbytakingtherebateand borrowingmoneyfromyourbankorcreditunion?

• Howtomakeshort-andlong-terminvestmentdecisions:Shouldyoubuyaone-or two-semesterparkingpass?Isahighersalarybetterthanstockoptions?

The Decision-Making Process

Decisionmakingrequiresthattherebeatleasttwoalternatives.Ifonlyonecourseofaction isavailable,thereisnodecisiontomake.Doesdecisionmaking,then,consistofchoosing fromamongalternativecoursesofaction?Considerthefollowingsituation:

Ataracetrack,abettorwasuncertainwhichhorsetobetoninthenextrace.He closedhiseyesandpointedhisfingeratthelistofhorsesprintedintheracing program.Uponopeninghiseyes,hesawthathewaspointingtohorsenumber4. Hehurriedofftoplacehisbetonthathorse.

Doestheracehorseselectionrepresentaprocessofdecisionmaking?Clearly,itwasa processofchoosingamongalternatives.Butthisprocessseemsinadequateandirrational. Wewanttodealwithrationaldecisionmaking.

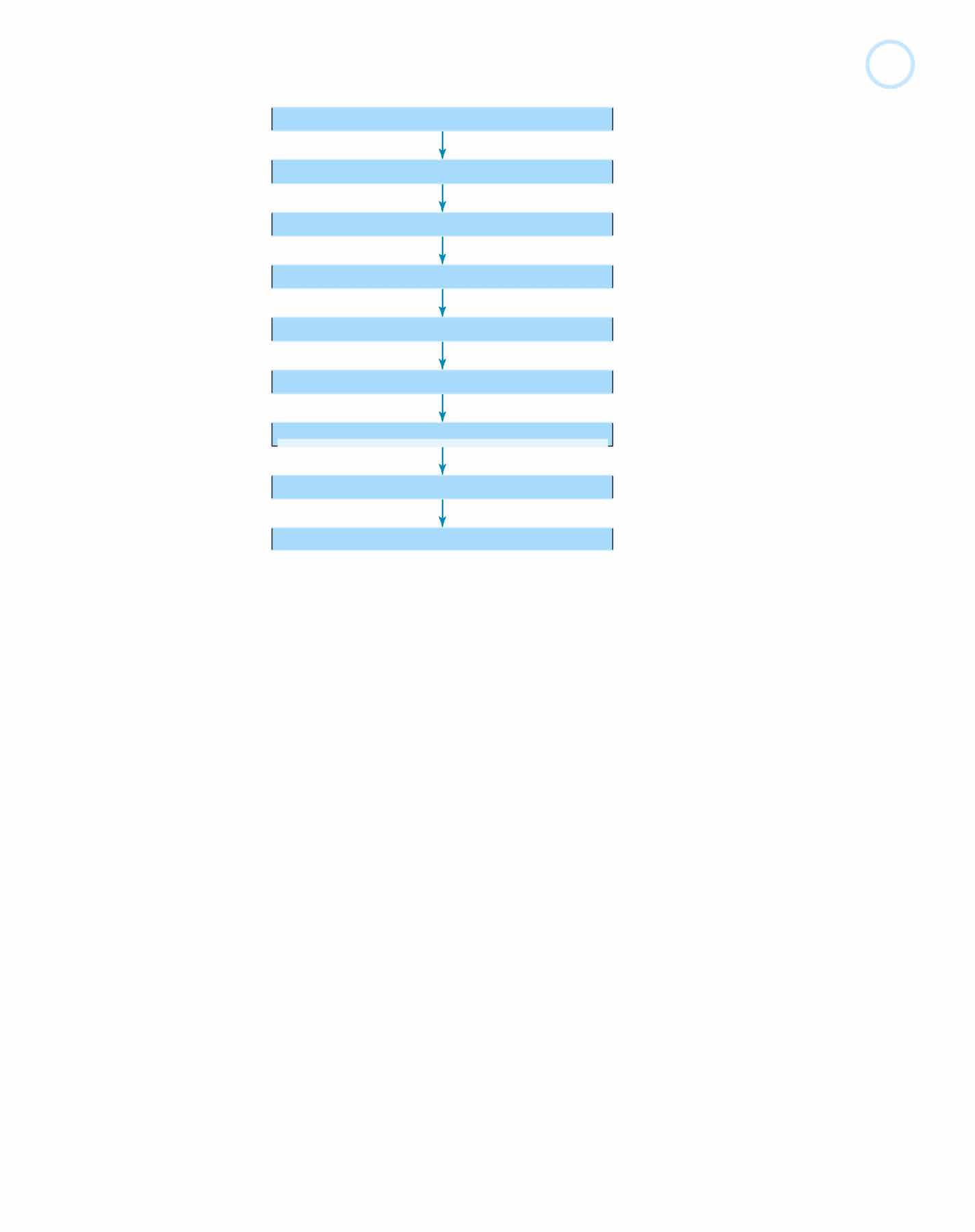

Rational Decision Making

Rational decisionmakingcanbeacomplexprocess.Onepossiblesystematicapproach to this processisshowninFigure 1-1. Although the steps areshownsequentially, itis commonforadecisionmakertorepeatsteps,takethemoutoforder,anddosomesteps simultaneously.Forexample,whenanewalternativeisidentified,moredatawillberequired.Or when theoutcomesaresummarized,it maybecomeclearthat theproblem needstoberedefinedornewgoalsestablished.ThefollowingsectionsdescribetheelementslistedinFigure1-1.

1.RecognizetheProblem

Thestartingpointinrationaldecisionmakingisrecognizingthataproblemexists.

Someyearsago,forexample,itwasdiscoveredthatseveralspeciesofoceanfishcontainedsubstantial concentrations of mercury.The decision-making processbeganwith thisdiscovery,andtherushwasontodeterminewhatshouldbedone.Researchrevealed thatfish takenfrom the ocean decades beforeandpreservedinlaboratoriescontained similarconcentrationsofmercury.Thustheproblemhadexistedforalongtimebuthad notbeenrecognized.

Inmanysituations,recognitionisobviousandimmediate.Acaraccident,acheque thatbounces,aburned-outmotor,anexhaustedsupplyofpartsallproducetherecognitionofaproblem.Onceweareawareoftheproblem,wesolveitasbestwecan.

2.DefinetheGoalorObjective

Thegoalcanbeagrand,overallgoalofapersonorafirm.Forexample,apersonalgoalcould betoleadapleasantandmeaningfullife,whereasafirm'sgoalisusuallytooperateprofitably. Butanobjectiveneednotbethegrand,overallgoalofabusinessoranindividual.It maybenarrowandspecific:"IwanttopayofftheloanonmycarbyMay"and"Theplant mustproduce300golfcartsinthenexttwoweeks"aremorelimitedobjectives.

2. Definethegoalorobjective

3. Assemblerelevantdata

4 Identifyfeasiblealternatives

5.Selectthecriteriatodeterminethebestalternative

6. Constructamodel

7.Predicttheoutcomesorconsequencesforeachalternative

8. Choosethebestalternative

9. Audittheresults

FIGURE1·1 One possibleflowchartofthedecision-making process.

3.AssembleRelevantData

To makeagood decision, youmustassemblegoodinformation.Inadditionto all the publishedinformation,avastquantityofinformationisnotwrittendownanywherebut is stored as individuals'knowledge and experience. There is also information thatremainsungathered.Aquestionlike"Howmanypeopleinyourtownwouldbeinterestedin buyingapairofleft-handedscissors?"cannotbeansweredbyexaminingpublisheddata orbyaskinganyoneperson.Marketresearchorotherdatagatheringwouldberequiredto obtainthedesiredinformation.

Onepartofthedatathatmustbeassembledisthetimehorizonoftheproblem.How longwillthebuildingorequipmentlast?Howlongwillitbeneeded?Willitbescrapped, sold,orshiftedtoanotheruse?Insomecases,suchasaroadoratunnel,thelifemaybe centurieswithregularmaintenanceandoccasionalrebuilding.However,ashorterperiod, suchas50years,maybechosenasthetimehorizonsothatdecisionscanbebasedonmore reliabledata.

Inengineeringdecisions,animportantsourceof dataisafirm's own accountingsystem.Thesedatamustbeexaminedcarefully.Thatisbecauseaccountingdata focus on pastinformation,whereas engineeringjudgment must oftenbeapplied to estimate current and futurevalues. For example, accounting records canshow the pastcostofbuyingcomputers,butengineeringjudgmentisrequiredtoestimatetheir futurecost.

Financialandcostaccountingaredesignedtoshow theflowofmoney-specifically costsandbenefits-inacompany'soperations.Whencostsaredirectlyrelatedtospecific operations,thereisnodifficulty;butthereareothercostsunrelatedtospecificoperations. Theseindirectcosts. oroverhead.areusuallyallocated to acompany's operationsand

productsbysomesemi-arbitrarymethod.Theresultsaregenerallysatisfactoryforcostaccountingpurposesbutmaybeunreliableforuseineconomicanalysis.

Tocreateameaningfuleconomicanalysis,wemustdeterminethetruedifferencesbetweenalternatives,andthatmightrequiresomeadjustmentofcost-accountingdata.The followingexampleillustratesthissituation.

EXAMPLE 1-1

Thecost-accountingrecordsofalargecompanyshowtheaveragemonthlycostsforthethree-person printingdepartment.Thewagesandbenefitsof thedepartmentmakeup thefirstcategoryofdirect labour.Thecompany'sindirectoroverheadcosts-suchasheat,electricity,andemployeeinsurancemustbedistributedtoitsvariousdepartmentsinsomemannerand,likemanyotherfirms, thisone usesfloorspaceasthebasisforitsallocations.

Directlabour(includingemployeebenefits)

Materialsandsuppliesconsumed

Allocatedoverheadcosts:

Theprintingdepartmentchargestheotherdepartmentsforitsservicestorecoverits$18,000monthly cost.Forexample,thechargetorun1,000copiesofanannouncementis

Theshippingdepartmentcheckswithacommercialprinterthatwouldprintthesame1,000copiesfor $22.95.Althoughtheshippingdepartmentneedsonlyabout30,000copiesprintedamonth,itsforeman decidestostopusingtheprintingdepartmentandhavetheworkdonebytheoutsideprinter.Theinhouseprintingdepartmentobjectstothis.Asaresult,thegeneralmanagerhasaskedyoutostudythe situationandrecommendwhatshouldbedone.

SOLUTION

Muchoftheprintingdepartment'soutputrevealsthecompany'scosts,prices,andotherfinancialinformation.Thecompanypresidentconsiderstheprintingdepartmentnecessaryinorderto prevent disclosingsuchinformationtopeopleoutsidethecompany.

Areviewofthecost-accountingchargesrevealsnothingunusual.Thechargesmadebytheprinting departmentcoverdirectlabour,materialsandsupplies,andoverhead.Theallocationofindirectcosts isacustomaryprocedureincost-accountingsystems,butitmaybemisleadingfordecisionmaking,as thefollowingdiscussionindicates.

Theshippingdepartmentwouldreduceitscostfrom$793to$688byusingtheoutsideprinter.Inthat case,byhowmuchwouldtheprintingdepartment'scostsdecline?Wewillexamineeachofthecost components:

1. DirectLabour.Iftheprintingdepartmenthadbeenworkingovertime,thentheovertimecould bereducedoreliminated.But,assumingtherewasnoovertime,howmuchwouldthesaving be?Itseemsunlikelythataprintercouldbefiredorevenputonlessthana40-hourwork week.Thus,althoughtheremightbea$228saving,itismuchmorelikelythattherewillbeno reductionindirectlabour.

2. MaterialsandSupplies.Therewouldbea$294savinginmaterialsandsupplies.

3. AllocatedOverheadCosts.Therewillbenoreductionintheprintingdepartment'smonthly $5,000overhead,becausetherewillbenoreductionindepartmentfloorspace.(Thoughthere maybeaslightreductioninthefirm'spowercostsiftheprintingdepartmentdoeslesswork.) Furthermore,thefirmwillincuradditionalexpensesinpurchasingandaccountingtodeal withtheoutsidefirm.

Thefirmwillsave$294inmaterialsandsuppliesandmayormaynotsave$228indirectlabourif theprintingdepartmentnolongerdoestheshippingdepartment'swork.Themaximumsavingwould be$294+228 = $522.Butiftheshippingdepartmentobtainsitsprintingfromtheoutsideprinter, thefirmmustpay$688.50amonth.Thesavingfromnotdoingtheshippingdepartmentworkinthe printingdepartmentwouldnotexceed$522,anditwouldprobablybeonly$294.Theresultwouldbea netincreaseincosttothefirm.Forthisreason,theshippingdepartmentshouldbediscouragedfrom sendingitsprintingtotheoutsideprinter.

Gathering cost data presents other difficulties. One way to look at the financial consequences-costsandbenefits-ofvariousalternativesisasfollows:

• Market Consequences. These consequences have an established price in the marketplace.We can quickly determineraw material prices,machinerycosts, labourcosts,andsoforth.

• Extra-MarketConsequences.Thereareotheritemsthatarenotdirectlypricedin themarketplace.Butbyindirectmeans,apricemaybeassignedtotheseitems. (Economists callthesepricesshadowprices.)Examplesmightbethecostofan employee'sinjuryorthevaluetoemployeesofgoingfromafive-daytoafour-day 40-hourweek.

• IntangibleConsequences.Numericaleconomicanalysisneverfullydescribesthe differencesbetweenalternatives.Wearetemptedtoleaveoutconsequencesthat donothaveasignificanteffectontheanalysisitselforontheconversionofthe finaldecisionintoitscashequivalent.Howdoesoneevaluatethepotentiallossof workers'jobsbecauseofautomation?Whatisthevalueoflandscapingarounda factory?Theseandsimilarfactorsmaybeleftoutofthenumericalcalculations, buttheyshouldbeconsideredinconjunctionwiththenumericalresultsinreachingadecision.

4. IdentifyFeasibleAlternatives

It should bekept in mind thatunlessthebestalternativeisconsidered, the resultwill alwaysbelessthanideal.Twotypesofalternativesaresometimesignored.First,inmany situationsa"do-nothing"alternativeisfeasible.Second,thereareoftenfeasible(butunglamorous)alternatives,suchas"Patchitupandkeepitrunningforanotheryearbefore replacingit."

Thereisnofoolproofwaytoensurethatthebestalternativeisamongtheonesbeing considered.Youshouldensurethatallconventionalalternativeshavebeenlistedandthen strivetosuggestinnovativesolutions.Sometimesitcanbeusefulforagrouptoconsider alternativesinaninnovativeatmosphere, thatis,bybrainstorming.Evenimpracticalalternativesmayleadtoabetterpossibility.

5.SelecttheCriteriaforDeterminingtheBestAlternative

Tochoosethebestalternative,wemustdefinewhatwemeanbybest.Theremustbeatleast onecriterion,orasetofcriteria,toevaluatewhichalternativeisbest-or,insomeunfortunatecases,theleastbad.Hereareseveralpossiblecriteria:

• Createminimaldisturbancetotheenvironment.

• Improvethedistributionofwealthamongpeople.

• Minimizetheexpenditureofmoney.

• Ensurethatthebenefitstothosewhogainfromthedecisionaregreaterthanthe lossesofthosewhoareharmedbythedecision.1

• Minimizethetimeneededtoaccomplishthegoalorobjective.

• Minimizeunemployment.

• Maximizeprofit.

Selectingthecriteriabywhichtochoosethebestalternativewillnotbeeasyifdifferentgroupssupportdifferentcriteriaandhencedesiredifferentalternatives.Orthecriteria mayconflict.Forexample,minimizingunemploymentmayincreasetheexpenditureof money. Minimizingenvironmental disturbancemayincreasethe timeto complete the project.Disagreementsbetweenmanagementandlabourmayreflectdisagreementsover thecriteriaforchoosingthebestalternative.

Thelastcriterion-maximizeprofit-istheonenormallyselectedinengineeringdecisionmaking.

6. ConstructaModel

Atsomepointinthedecisionmaking,thevariouselementsmustbebroughttogether. The objective, relevant data,feasible alternatives, and selection standards must be merged.

Constructingtherelationshipsbetween thedecision-makingelementsisfrequently calledmodelbuilding.Toanengineer,amodelmaybeaphysicalrepresentationofthe realthingorasetofequationsdescribingthedesiredrelationships.Ineconomicdecision making,themodelisusuallymathematical.

Itishelpfultomodelonlythatpartofthesystemimportanttotheproblemathand. Thusthemathematicalmodelofthestudentcapacityofaclassroommightbe

1 ThisistheKaldorcriterion.

where

l = lengthofclassroom,inmetres

w=widthofclassroom,inmetres

k = classroomarrangementfactor

Theequationforstudentcapacityofaclassroomisaverysimplemodel,yetitmaybeadequatefortheproblembeingsolved.

7. PredicttheOutcomesforEachAlternative

Amodeland thedataare usedto predict theoutcomesforeachfeasiblealternative.As suggestedearlier,eachalternativemightproduceavarietyofoutcomes.Choosingamotorcycleratherthanabicycle,forexample,maymakethefuelsupplierhappy,theneighbours unhappy,theenvironmentmorepolluted,andtheowner'ssavingsaccountsmaller.But,to avoidunnecessarycomplications,weassumethatdecisionsarebasedonasinglecriterion formeasuringtherelativeattractivenessofthevariousalternatives.Ifnecessary,onecould deviseasinglecompositecriterionthatistheweightedaverageofseveraldifferentcriteria.

Tochoose thebestalternative,theoutcomesforeachalternativemustbestatedina comparableway.Usuallytheconsequencesofeachalternativearestatedintermsofmoney. Theconsequencescanbecategorizedasfollows:

• Marketconsequences-whereestablishedmarketpricesareavailable

• Extra-marketconsequences-nodirectmarketprices,sopricedindirectly

• Intangibleconsequences-valuedbyjudgment,notmonetaryprices

Inthefirstproblemsthatwewillexamine,thecostsandbenefitsoccuroverashort periodandcanbeconsideredtooccuratthesametime.Morecommonly,thevariouscosts andbenefitstakeplaceoveralongerperiod.Wewillrepresenttheseasacashflowdiagram toshowthetimingofthevariouscostsandbenefits.

For these longer-term problems, acommon mistake is to assume thatthe current situationwillbeunchangedifthedo-nothingalternativeischosen.Forexample,current profitsmayshrinkorvanishasaresultoftheactionsofcompetitorsandtheexpectations of customers.Asanotherexample,trafficjams normallyincreaseover theyearsasthe numberofvehiclesincreases.

8.ChoosetheBestAlternative

Earlierwesaidthatchoosingthebestalternativemaybesimplyamatterofdeterminingwhich bestmeetstheselectioncriterion.Butthesolutionstomostproblemsineconomicshavemarket consequences,extra-marketconsequences,andintangibleconsequences.Sincetheintangible consequencesofpossiblealternativesareleftoutofthenumericalcalculations,theyshouldbe introducedintothedecisionmakingatthispoint.Therightchoiceistheonethatbestmeets thecriteriaafterwehaveconsideredboththenumericalandintangibleconsequences.

Duringthedecisionmaking,certainfeasiblealternativesareeliminatedbecausethey aredominatedbyother,betteralternatives.Forexample,shoppingforacomputeronline mayallowyoutobuyacustom-configuredcomputerforlessmoneythanastockcomputer inalocalstore.Buyingatthelocalstoreisfeasible,butdominated.

Havingexaminedthestructureofthedecision-makingprocess,wecanask:When isthedecisionmade,andwhomakesit?Ifonepersonperformsallthestepsindecision making, thensheisthedecisionmaker. Whenshemakesthedecisionisless clear.The selectionofthefeasiblealternativesmaybethecrucialstep,withtherestoftheanalysisa methodicalprocessleadingtotheinevitabledecision.

9.AudittheResults

Anauditoftheresultsisacomparisonofwhathappenedagainstthepredictions.Dothe resultsofadecisionanalysisreasonablyagreewithitsprojections?Ifanewmachinetool waspurchasedto save labourandimprovequality, didit?Ifthesavingsarenotbeing obtained,whatwasoverlooked?Theauditmayhelpensurethattheprojectedoperating advantagesareultimatelyobtained.Ontheotherhand,theeconomicanalysisprojections mayhavebeenundulyoptimistic.Wewanttoknow this,too,sothatthemistakes that led to the inaccurate projectionarenot repeated. An effectiveway topromoterealistic economicanalysiscalculationsisforallpeopleinvolvedtoknowthattherewillbeanaudit oftheresults.

Ethics

Youmustbemindfuloftheethicaldimensionsofengineeringeconomicanalysisandof yourengineeringandpersonaldecisions.Thistextcanonlyintroducethetopic,whichwe hopeyouwillexploreingreaterdepth.

Ethicscanbedescribedasdistinguishingrightandwrongwhenmakingdecisions. Thismayinclude establishingsystemsof beliefs and moral obligations, definingvalues andfairness,anddeterminingdutiesandguidelinesforconduct.Ethicaldecisionmaking requiresan understanding ofthecontextoftheproblem, thepossiblechoices,and the outcomesofeachchoice.

Ethical Dimensions in Engineering Decision Making

Ethicalissuescanariseateverystageofthedecision-makingprocess.Ethicsissuchan importantpartofprofessionalandbusinessdecisionsthatethicalcodesorstandardsof conductexistforprofessionalengineeringsocietiesandsmallandlargeorganizations,to guideindividualandcorporatebehaviour.Writtenprofessionalcodesarecommoninthe engineeringprofession,wheretheyserveasareferencefornewengineersandabasisfor legalactionagainstengineerswhoviolatethecode.

In Canada, provincial and territorial associations of professional engineers are responsiblefor the regulation of the practice of engineering.Thefederationof theseorganizationsiscalledEngineersCanada.ThisistheEngineersCanadacode ofethics:

Registrants shall conduct themselves withintegrityandin anhonourableand ethicalmanner.Registrantsshallupholdthevaluesoftruth,honesty,andtrustworthinessandsafeguardhumanlifeandwelfareandtheenvironment.Inkeepingwiththesebasictenets,registrantsshall

1. holdparamountthesafety,health,andwelfareofthepublicandtheprotectionof theenvironment,andpromotehealthandsafetywithintheworkplace;

2. offerservices,adviseonorundertakeengineeringassignmentsonlyinareasof theircompetence,andpractiseinacarefulanddiligentmannerandincompliancewithapplicablelegislation;

3. act as faithful agents of their clients or employers, maintain confidentiality, andavoidconflictsofinterest,but,wheresuchconflictarises,fullydisclosethe circumstanceswithoutdelaytotheemployerorclient;

4. keepthemselvesinformedinordertomaintaintheircompetence,andadvance theirknowledgeinthefieldwithinwhichtheypractise;

5. conduct themselves with integrity, equity, fairness, courtesy, and good faith towardclients,colleagues,andothers,givecreditwhereitisdue,andaccept,as wellasgive,honestandfairprofessionalcriticism;

6. presentclearlytoemployersandclientsthepossibleconsequencesifengineering decisionsorjudgmentsareoverruledordisregarded;

7. reporttotheirassociationorotherappropriateagenciesanyillegalorunethical engineeringdecisionsorpracticesbyengineersorothers;

8. beawareofandensurethatclientsandemployersaremadeawareofsocietaland environmentalconsequencesofactionsor projects,andendeavour tointerpret engineeringissuestothepublicinanobjectiveandtruthfulmanner;

9. treatequitablyandpromotetheequitabletreatmentofpeopleandinaccordance withhumanrightslegislation;

10. upholdandenhancethehonouranddignityoftheprofession.(CCPE2012)

In addition, each provincial and territorial associationhasa code of ethicsforits members.Mostengineeringorganizationshavesimilarwrittenstandards.Forallengineers,difficultiesarisewhentheiractionsarecontrarytothesewrittenorinternalcodes.

The Environment We Live In

Thedecisionmakermustaskwhoincursthecostsfortheprojectandwhoreceivesthe benefits.Ethicalissuescanbe particularly difficultbecausethereareoftenstakeholders withopposingviewpoints,andsomeofthedatamaybeuncertainandhardtoquantify.

Thefollowingareexamplesofdifficultchoices:

• Protectingthehabitatofanendangeredspeciesversusflood-controlprojectsthat protectpeople,animals,andstructures

• Meeting the needfor electrical power when every means of generation causes someenvironmentaldamage:

• Hydroelectric-lossoflandandhabitattoreservoir

• Coal-dangertoworkersfromundergroundmining,damagetohabitatfrom open-pitmining,airpollutionfromburningthecoal,andanincreasedrate ofglobalwarmingbecauseofthereleaseofcarbondioxidetotheatmosphere.

• Nuclear-disposalofradioactivewaste

• Fueloil-airpollutionandeconomicdependenceonforeignsources

• Wind-visualpollutionofwindfarms, killingofbirdsandbatsbywhirling blades

• Determiningstandardsforpollutants:Is1partpermillionacceptable,oris1part perbillionnecessary?

Safety and Cost

Someofthemostcommonandmostdifficultethicaldilemmasinvolvetrade-offsbetween safetyandcost.Ifaproductis"toosafe,"itwillbetooexpensiveanditwillnotbeused. Andsometimesthecostisbornebyonepartyandtheriskbyanother.

• Should the oil platform be designed for the 100-year, SOO-year, or 1,000-year hurricane?

• Shouldtheautomanufactureraddrun-flat tires,stabilitycontrol, side-cushion airbags,andrear-seatairbagstoeverycar?

• Arestainlesssteelvalvesrequired,orisiteconomicallybettertouseless-corrosionresistantvalvesandreplacethemmoreoften?

EmergingIssuesand"Solutions"

BreachesofthelawbythecorporateleadersofEnron,Tyco,andotherfirmsledtoattempts bygovernmentstoprevent,limit,andexposefinancialwrongdoingwithincorporations. OnepartoftheAmericanresponsehasbeentheSarbanes-OxleyActof2002,whichimposedrequirementsonexecutivesandauditingfirms,andpenaltiesforviolations. Globalizationisanotherareaofincreasingimportanceforethicalconsiderations.One reasonisthatdifferentcountriesandregionshavedifferentethicalexpectations.Asecond reasonisthatjobsmaybemovedtoanothercountrybecauseofdifferencesincost,productivity,environmentalstandards,andsoon.WhatmayfromaCanadianperspective beasweatshopmayfromtheperspectiveofalessdevelopednationbeanopportunityto supportmanyfamilies.

Importanceof Ethics In Engineering and Engineering Economy

Frequently,thoughengineersandfirms trytoactethically,mistakesaremade-thedata werewrong, the designwaschanged, or the operatingenvironmentwasdifferent than expected.Butinothercases,suchastheChallengerlaunchdecision,achoicewasmadeto placeexpediencyaboveethics.Undersuchcircumstances,itistheengineers'dutytospeak out,withinandifnecessarybeyondtheircompany,toprotectthesafetyofthepublic. Often,recentengineeringgraduatesareasked,"Whatisthemostimportantthingyou wantfromyoursupervisor?"Themostcommonresponseismentoringandopportunities tolearnandprogress.When employeeswith5, 15,25, ormoreyearsofexperienceare askedthesamequestion,themostcommon responseisintegrity.Thisiswhatyoursubordinates,peers,andsuperiorswillexpectandvaluethemostfromyou.Integrityisthe foundationforlong-termcareersuccess.

Engineering Decision Making for Current Costs

Someoftheeasiestkindsofengineeringdecisionsdealwithproblemsofalternativedesigns, methods,or materials.If theresultsofthedecisionappearinaveryshorttime,onecan quicklyaddupthecostsandbenefitsforeachalternative.Then,byusingsuitableeconomic standards,onecanidentifythebestalternative.Threeexamplesillustratethesesituations.

EXAMPLE 1-2

Aconcreteaggregatemixmustcontainatleast31%sandbyvolumeforproperbatching.Onesourceof material,whichhas25%sandand75%coarseaggregate,sellsfor$3.00percubicmetre(m3). Another source,whichhas40%sandand60%coarseaggregate,sellsfor$4.40/m3 • Determinetheleastcostper cubicmetreofblendedaggregates.

SOLUTION

Theleastcostofblendedaggregateswillresultfrommaximumuseofthelower-costmaterial.Thehighercostmaterialwillbeusedtoincreasetheproportionofsanduptotheminimumlevel(31%)specified.

Letx=Portionofblendedaggregatesfrom$3.00/m3 source

1-x=Portionofblendedaggregatesfrom$4.40/m3 source

SandBalance

x (0.25) + (1 + x)(0.40) = 0.31

0.25x + 0.40 - 0.40x = 0.31

0.31 - 0.40 -0.09 x= 0.25 - 0.40 -0.15 =0.60

Thustheblendedaggregateswillcontain

60%of$3.00/m3material

40%of$4.40/m3 material

Theleastcostpercubicmetreofblendedaggregatesis 0.60($3.00) + 0.40($4.40) = 1.80 + 1.76 = $3.56/m3

EXAMPLE 1·3

Amachinepartismanufacturedataunitcostof404formaterialand15<1:fordirectlabour.Aninvestmentof$500,000intoolingisrequired.Theordercallsfor3millionpieces.Halfwaythroughtheorder, anewmethodofmanufacturecanbeputintoeffectthatwillreducetheunitcoststo344formaterial and10<1:fordirectlabour-butitwillrequire$100,000foradditionaltooling.Thistoolingwillnotbe usefulforfutureorders.Othercostsareallocatedat2.5timesthedirectlabourcost.What,ifanything, shouldbedone?

SOLUTION

Sincethereisonlyonewaytohandlethefirst1.5millionpieces,ourproblemconcernsonlythesecond halfoftheorder.

AlternativeA:ContinuewithPresentMethod