Associate Director Heritage and Taxation Advisory Service Christie's lromanelli@christies.com +44 (0) 20 7389 2725

Index

1 Editorial Luisa Romanelli

3 The timeless illustrations of Shirley Hughes Luisa Romanelli

4 EU VAT Changes Effective 1 January 2025 Neil Millen

6 The Huguenot Museum, Rochester: The First Ten Years

Tessa Murdoch

11 The Artist’s Estate Alice Julian

14 Making Tax Digital

18

Editorial

In last year’s issue we featured an overview of the National Gallery’s NG200 bicentenary celebrations, and the milestone year has been marked by a number of new acquisitions, including a recently announced offer in lieu shown on our front cover, negotiated by Christie’s Heritage and Taxation Advisory Service. The magnificent King David by Giovanni Francesco Barbieri (1591–1666), known as Il Guercino, was accepted in lieu of Inheritance Tax from Estate of Jacob, 4th Baron Rothschild and has now joined its pendants on display, one of which was previously negotiated by Christie’s to the National Gallery in 2012.

Elsewhere in the museum world, Tessa Murdoch has provided an overview of the first ten years of the Huguenot Museum in Rochester, highlighting a number of recent acquisitions of their own as well as upcoming events that are being held and which serve to demonstrate how the story of the Huguenots continues to resonate in today’s world.

We also feature two articles covering issues that may relate to working artists. Alice Julian of Boodle Hatfield LLP provides a useful overview of the points to consider in relation to IHT planning when dealing with Artists’ Estates. With the upcoming reduction in Business Property Relief, efficient and effective tax planning will become increasingly vital. From an accountancy perspective, Tim Adams of Saffery LLP looks at the imminent introduction of Making Tax Digital, and how this will affect the creative industries, among others. While those working in the tax profession have long been aware of this upcoming change, it will fundamentally alter the Self-Assessment regime, and will no doubt require many clients to alter their behaviour

and record-keeping to ensure that they are able to meet the new reporting requirements.

As an additional technical point, Neil Millen, Christie’s Group Indirect Tax Director, provides an update following legislative developments within the European Union in relation to EU VAT changes which came into effect on 1 January 2025, and which will impact sales and shipments for many clients.

In addition to the aforementioned offer in lieu to the National Gallery, we at Christie’s were also privileged to undertake the offer in lieu of the archive of the author and illustrator Shirley Hughes (1927-2022). I am sure that many readers will be familiar with her work, either from their own childhood memories or through reading with children or grandchildren. We have looked at the many achievements from her lengthy career, and it is wonderful to note that her archive is now available for all at the Bodleian Library, University of Oxford.

Finally, as well as the work undertaken by the Heritage and Taxation Team, we also feature an article from Amelia Walker, Head of Private and Iconic Collections at Christie’s, outlining recent sales of guitar collections from Rock Icons. As you will read, for the past two years in January, Christie’s King Street has been transformed with wall-to-wall displays of guitars from the collections of Mark Knopfler and Jeff Beck, together with spaces to listen to these instruments being played. These sales were tremendously successful, and we very much hope to welcome you to Christie’s for similar events in the future!

Tim Adams

Rock Icons at Christie’s Amelia Walker

Associate Director Heritage and Taxation Advisory Service

Christie's

lromanelli@christies.com

+44 (0) 20 7389 2725

Luisa is an Associate Director in Christie’s Heritage and Taxation Advisory Service and a qualified Chartered Tax Advisor (CTA), specialising in Inheritance Tax, Trusts and Estates. Luisa has worked on a number of Offers in Lieu and Conditional Exemption claims for UK Estates, across multiple artistic specialities. She also provides a range of clients with advice on the tax issues surrounding the acquisition, disposal and inheritance of works of art.

The timeless illustrations of Shirley Hughes

Among the various offers in lieu that Christie’s had the privilege of undertaking in the 202324 financial year, the offer of the archive of the children’s author, Shirley Hughes (1927-2022) was a highlight. It is a pleasure to feature this charming archive of such a well-admired author that now has a permanent home at the Bodleian Library, University of Oxford.

Born in 1927, the art of illustration captured Hughes’ imagination from a young age and as a child she enjoyed spending time drawing and writing stories and plays with her two sisters. This continued through her studies at the Ruskin School of Drawing and Fine Art in Oxford, where Hughes first started working in the picture-book format and where it was suggested that illustration might be the ideal focus for her talents.

In the 1950s, Hughes moved to London, married John Sebastian Papendiek Vulliamy, started a family and began working as a freelance illustrator of the books of other authors. These early works already served to demonstrate her trademark skill in sensitively rendering children’s emotions.

The first book of her own that Hughes wrote and illustrated, Lucy and Tom’s Day, was published in 1960 and subsequently became a series of stories which drew on the everyday experiences of her own young children, and which demonstrated her appeal to readers through the depiction of familiar domestic scenes.

This success was followed by Dogger, which was published in 1977 to international acclaim, and won Hughes her first Kate Greenaway Medal for illustration. This story was inspired by a real-life incident where her son, Ed, lost his own teddy in Holland Park, and again showcased Hughes’ ability to captivate readers with everyday stories, told and illustrated in an imaginative and charming fashion. Hughes was later awarded the ‘Greenaway of Greenaways’ award in 2007 for Dogger: as voted for by the public who chose their favourite of all

the Greenaway Medal-winning works dating from the inception of the prize in 1955.

Alfie, another of Hughes’ best-known characters, made his first appearance in 1981 when the original book, Alfie Gets in First was published. This was to be followed by 25 other titles in the series with the latest released in 2019. These timeless stories depict Alfie and his little sister Annie Rose in day-to-day scenarios such as going to the park, nursery, and spending time with grandparents, and the familiarity of daily life shown through the siblings’ eyes remains part of their continued appeal to many generations of readers.

While Dogger and Alfie are probably Hughes’ most well-known creations, she also wrote over 50 other books of her own, including collaborations with her daughter Clara, and her 2003 book, Ella’s Big Chance, won her a second Greenaway Medal with a retelling of the Cinderella story set in the Jazz Age on the French Riviera.

Hughes’ formidable energy and work ethic saw her working right through her 80s and into her 90s: on her death, in February 2022 at the age of 94, she left an unfinished work-in-progress, entitled Sugar Candy Slippers, and not two years before she had produced Dogger’s Christmas, a sequel to the well-loved work that first brought her work to an international audience.

Such was Hughes’ success, her books sold over ten million copies worldwide across the course of her career and she was appointed OBE in 1999 and CBE in 2017. The archive that was accepted in lieu of Inheritance Tax includes drafts, rough layouts, manuscripts and finalised illustrations covering her lifetime’s work and shows a variety of medium such as pastel, watercolour and gouache. We were delighted to have been instructed to work on this remarkable archive and it is wonderful that these timeless illustrations, familiar to generations of readers around the world, are now available for the public in perpetuity.

Luisa Romanelli

Left: Cover artwork for Dogger by Shirley Hughes (1927-2022), part of the Shirley Hughes Archive

Neil has worked for Christie’s for 16 years and practiced indirect tax for 28 years. Prior to joining Christie’s he originally trained with HM Customs & Excise, and has worked for HMRC, the Bank of England and at City advisory firm. He has been a guest lecture at Christie’s Education, a contributing author of the Art Collecting Legal handbook (3rd ed). Graduating in art history and classical studies, he is an occasional artist.

EU VAT Changes Effective 1 January 2025

Introduction

The European Union (EU) enacted several significant changes to its VAT rules that came into effect on 1 January 2025. These changes impact the art sector in three significant ways. Firstly, the EU has allowed member states to choose to expand the application of the reduced rate of VAT to almost all supplies of works of art, antiques and collectors’ items, if they so wish (expansion of the reduced rate is not compulsory). Secondly, as a result of the expansion of the reduced rate, the eligibility of businesses to sell goods under VAT margin scheme rules has effectively been tightened. Finally, the interaction of these two changes has the potential to shift many businesses in the art sector towards invoicing outside of the margin scheme rules, and as a consequence, towards more complex intra-EU place of supply considerations. The latter were already in place prior to 2025, but the art sector was previously largely shielded from the exposure due to extensive use of the VAT margin scheme.

Expansion of the Reduced Rate of VAT for Works of Art

Historically, VAT rates applied to supplies of works of art, antiques and collectables have varied significantly across the EU, normally in line with the standard VAT rate of a particular EU state. Application of the reduced rate specifically, was mostly restricted to imports into the EU of works of art, antiques and collectors’ items. As of 1 January 2025, the EU has thrown open the gates to allow members states to expand the scope of the reduced VAT rate to all supplies

of works of art, antiques and collectors’ items, with the exception of sales offered under VAT margin scheme rules (the standard VAT rate will still apply to any taxable margin).

It should be noted that member states have a choice as to whether to expand the reduced rate for the art market or not. Leading the way was France with the expansion of its 5.5% VAT rate. In comparison, the Netherlands has made no such legislative changes at the time of writing. As a result of this patchwork quilt of reduced and standard rates, the EU art market now has an even starker variation of VAT rates across member states than it did previously for domestic supplies. The impact of which will not only require more caution on the pricing structure of individual deals, but also a consideration of the broader perception of the commercial viability of the art sector within each EU state.

Use of the VAT margin scheme

In the new EU VAT landscape, the VAT margin scheme itself is not dead. It is still available for consignments from private sellers into the trade. It is also still available for any consignment acquired by the trade that qualifies under the margin scheme specifications of each state’s rules (basic rules on margin scheme eligibility should still all be aligned). As said, the VAT extracted from any taxable margin must be that of the standard VAT rate, it cannot be the reduced VAT rate, even if such a rate applies to non-margin scheme transactions within a state.

Neil Millen Group Indirect Tax Director Christie’s

The new restriction on margin scheme eligibility applies when a trade client acquires a work of art, antique or collectors’ item at the reduced rate of VAT. Where this has occurred at the point of acquisition/consignment, the gallery, dealer or auction house must offer the item for any onward sale under non-margin scheme rules i.e. with VAT on the full price to the buyer at the applicable rate. In consequence the VAT rate applicable to the art market in the member state in question becomes an even more important commercial consideration when the margin scheme cannot be used.

This change is a departure from the rules that were extant before. Previously, a VAT registered business in France could import a work of art, pay the reduced rate of French import VAT, and then choose to sell on the piece under margin scheme rules. As of 2025, a VAT registered business in France importing an art work at the reduced rate will be required to make any onward sale under standard VAT rules, albeit at the newly expanded reduced VAT rate. One advantage will be the option of VAT recovery (subject to the usual rules) on the import VAT incurred, which would otherwise be blocked under margin scheme rules.

Intra-EU shipping consideration

With both the restriction on margin scheme access, and, for any states that have enacted the option, the expansion of the reduced rate of VAT for non-margin scheme sales, it is likely that the number of margin scheme sales within the EU will drop. This has a knock-

on effect to the application of the place of supply rules that determine in which EU state a transaction is taxable for VAT purposes.

Margin scheme sales, if taxable, are taxable in the EU state of the supplier, not the customer. This is true even if the goods are shipped to another EU state by either the customer or the supplier themselves. In contrast, sales outside of the margin scheme may have a place of supply in the location of the buyer, when shipped to a different EU state from the seller. This will be dependent on both the VAT status of the buyer and the shipping arrangements. If a buyer is VAT registered in another EU state, the buyer will reverse charge themselves at the acquisition rate of VAT of their home EU state. However, if the buyer in another EU state is not VAT registered, then the place of supply question becomes more complicated. If the private buyer collects the goods in person from the supplier’s EU state, then the place of supply will remain that of the supplier. This is also the case if the buyer sends in their own shipping agent. However, if the supplier facilitates delivery to the buyer’s EU state, the supplier will have an obligation to invoice the VAT rate of the buyer’s EU state, if over the applicable threshold. This is in contrast to the margin scheme which remains taxable for intra-EU sales in the EU state of the supplier.

Conclusion

EU consumers will need to be mindful of the VAT rate applicable to the art market in their home EU state, and if purchasing a non-margin

scheme item from a different EU state with a lower VAT rate, consider the method of delivery and which VAT rate they will be charged.

EU businesses facilitating shipment of nonmargin scheme sales to private buyers in different EU states will find themselves having to both expand their invoicing capability to bill for multiple different VAT rates and think carefully about the pricing structure of their deals. If they wish to avoid this obligation, then they may have to decline to facilitate shipment to private buyers in different EU states, but this in turn would of course impact on the buyer experience. Thankfully, the EU will not require multiple VAT registrations, as an EU OSS VAT registration will allow declaration of the VAT of all EU states, when imposed on such intraEU sales, to be declared on one VAT return and filed in the EU state of the supplier.

A final word of caution is needed, the EU is taking a very broad view on what it views as ‘facilitation’ when it comes to intra-EU shipment. As ever, a clear and complete audit trail across all the variables should be maintained to ensure VAT compliance.

Tessa is currently Vice-chair of the Acceptance in Lieu Panel. She previously worked at the Museum of London from 1981-1990 and at the V&A from 1990-2021. Her most recent book, Europe Divided: Huguenot Refugee Art and Culture was published by the V&A, November 2021. Tessa advises the National Trust and the National Heritage Memorial Fund, is a Board Member of the Idlewild Trust, and Chair of Trustees of the Huguenot Museum, Rochester.

The Huguenot Museum, Rochester: The First Ten Years

The Huguenot Heritage Centre, opened in 2015 by Princess Alexandra, cares for the historic collections of the French Hospital known by Huguenot communities in the British Isles since the 1720s as La Providence. That affectionate name derives from the seal designed by the Huguenot jeweller Pierre Marchant in 1718, the year that the French Hospital was awarded a royal charter by King George I. The seal shows Elijah being fed by the ravens and has the motto Dominus Providebit (God will Provide).

The charity was founded by bequest from Jacques de Gastigny, a Huguenot soldier who left France on the Revocation of the Edict of Nantes, when Protestantism was outlawed and settled in The Netherlands. Gastigny followed William of Orange to England and fought for the Protestant cause at the Battle of the Boyne. He had already been appointed Master of the King’s Buckhounds, a position which he enjoyed until 1698 (this ancient office was established at the English Court during the reign of Edward III in the 14th century) and William III’s passion for hunting meant that Gastigny enjoyed the monarch’s favour. On Gastigny’s death in 1708, six years after his monarch, he bequeathed £1,000 to acquire and adapt a building to provide shelter and care for Huguenot refugees who could not earn a living. That sum is equivalent to £200,000 today.

The French Hospital’s portrait of Gastigny is attributed to Pierre Mignard so was painted in Paris before Gastigny left for the Netherlands. The sitter is shown in armour in a late 17th century frame. As a royal servant, Gastigny might have featured in the exhibition at Kensington Palace in 2024 Untold Lives but

his portrait is not yet sufficiently well known.

The museum was founded through the vision of the then Deputy Governor of the French Hospital, Peter Duval, whose ancestors had been jewellers to Catherine the Great in St Petersburg. He was supported by Leslie Du Cane, whose forbears were merchants and directors of the Bank of England and by the Huguenot scholar Randolph Vigne, who co-authored The French Hospital in England: Its Huguenot History and Collections, published in 2009.

The book illustrates the establishment of the charity in its purpose-built premises in Finsbury, where the Petites Maisons catered for those suffering from mental illness. Early residents admitted in this category included Jacques Ray, who entered in 1737, a goldsmith associate of Paul de Lamerie, who was likely suffering from mercury poisoning. 25 years later Anthony Teulon, a milliner from Greenwich, was admitted with similar health problems caused by exposure to mercury in the felting process involved in making hats.

In 1865, La Providence moved to Victoria Park, Hackney, into a sophisticated building designed by an architect of Huguenot descent, Robert Lewis Roumieu. Today this building houses the Mossbourne Victoria Park Academy. In the 1940s, after World War II, the French Hospital was relocated to Compton’s Lea, Sussex but moved to Rochester at the suggestion of then Bishop of Rochester, Christopher Chavasse (also of Huguenot origin) in 1959.

The French Hospital has attracted Trustees who are proud of their Huguenot descent. From the

Dr Tessa Murdoch FSA

late 18th century, the position of Governor has been held by successive Earls of Radnor but in 2016, the present Earl of Radnor (a former Christie’s furniture expert) was succeeded by Lord Chartres, whose Huguenot ancestors settled in Cork, Ireland in the late 17th century.

Christie’s Ceramics expert, Anthony Houssemayne du Boulay, became a director of the French Hospital in 1985 and took a keen interest in the Huguenot Museum during his lifetime.

The Huguenot Museum was delighted to receive on loan from du Boulay in 2020 a silver tea caddy set made by Eliza Godfrey, Huguenot woman silversmith, daughter of Simon Pantin, originally from Rouen. The set is contained in a contemporary shagreen case and the three silver caddies were made in collaboration with Thomas Heming, who became goldsmith to George III. Eliza Godfrey, married to her father’s apprentice Abraham Buteux, remarried Benjamin Godfrey on the death of her first husband and when widowed for a second time, registered

her own maker’s mark at Goldsmiths Hall. The tea caddies (figure 1) were allocated to the Huguenot Museum through the Acceptance in Lieu scheme in 2023 and are now on display.

After his death du Boulay’s ceramics collection was also allocated to the Ashmolean, the Winchester College Museum and the Huguenot Museum through the Acceptance in Lieu scheme. The acquisition includes porcelain made in London at the Chelsea Manufactory founded by Huguenot jeweller Charles Gouyn with Catholic goldsmith Nicholas Sprimont and a later carnelian seal set in porcelain made by Charles Gouyn at the St James’s Manufactory. These items are being conserved thanks to a grant from the Leche Trust and will be displayed in Rochester later this year.

Recent gifts to the Huguenot Museum include portraits of the goldsmith John Jacob (figure 2), who came from Metz to London via Paris and married as his second wife Anne Courtauld, the daughter of Augustine Courtauld.

Augustine was the first of three generations of practising goldsmiths in that family. John Jacob is associated with the production of silver baskets and a fine example of his work is currently on loan to the Huguenot Museum from a private collection. Both John and Anne Jacob’s portraits were painted in their maturity; Anne is dressed as a widow.

The portraits were conserved in 2022 through a grant from the Idlewild Trust, founded by Huguenot Peter Minet. The work was undertaken by Ukrainian refugee professional paintings conservators and the portraits were unveiled in June 2023 in the presence of the Deputy Mayor of Medway, whose Ukrainian wife was able to address the conservators in their mother tongue.

In 2024 the Huguenot Museum acquired an ivory figurative group Susanna and the Elders by David Le Marchand (figure 3), a sculptor from Dieppe, who settled first in Edinburgh but moved to London circa 1700. Le Marchand carved medallion portraits of leading contemporaries including Sir Isaac Newton and Sir Christopher Wren. His figure carvings are rare. By 1726, no longer able to work, Le Marchand was admitted to the French Hospital in February where he died just six weeks later.

The Huguenot Museum also acquired an ivory portrait medallion of Russian Admiral Apraksin (figure 4), celebrated for his victory against Sweden in 1713. This was carved by Salomon

Gouin, Charles Gouin’s great uncle, also from Dieppe. Salomon was recorded in Moscow by 1704 and moved to St Petersburg five years later where he became Master of the Mint to Peter the Great. Examples of Gouin’s work can be seen in the British Museum and the Moscow State Historical Museum. Following the diaspora from Louis XIV’s France, Huguenots also settled in Russia where, as in the British Isles, French was the fashionable language and French fashions dictated court culture. It is salutary to remember that Fabergé was also of Huguenot descent.

In 2023 the Huguenot Museum was awarded a National Lottery Heritage Fund resilience grant: The Huguenot Museum: A New Future.

This has funded our present exhibition, of Sarah Lethieullier’s 1730s Dolls’ House on loan from the National Trust at Uppark (figure 5) until December 2026. This miniature NeoPalladian town mansion contains 700 fixtures and fittings including four state beds, a silver chandelier, tea service and dinner service made by specialist David Clayton. The exhibition has attracted international interest and inspired the 2025 Furniture History Symposium ‘The Art of the Dolls’ House’ held in March at the V&A with talks about earlier dolls’ houses in Nuremberg, Amsterdam and Utrecht as well as the Nostell Dolls’ House, Queen Mary’s Dolls’ House at Windsor Castle and the range of dolls’ houses preserved at the Young V&A.

The Huguenot Museum is situated in the heart of Rochester in a building which provides access to the High Street from the Railway Station. Until April 2024, the ground floor hosted Medway Council’s Visitor Information Centre but this closed due to financial cutbacks. The Huguenot Museum is planning to purchase the freehold from the French Hospital and create a craft centre in association with Cockpit Arts in Bloomsbury and Deptford. The Museum will work with City of London Livery Companies and other charitable foundations and the architect John Simpson to realise this plan by 2027. The craft centre will celebrate many of the skills which the Huguenots brought to the British Isles and provide opportunities for college graduates to establish their own businesses in an environment where technical assistance and mentoring for marketing and business skills are available. The Huguenot Museum is forming a committee to advise and promote this scheme including former Rochester alumni, designer Zandra Rhodes and goldsmith Ray Walton, and Kent-based ceramicist Kate Malone.

The Huguenot Museum is open Tuesday through Saturday 11.00 a.m. to 4.00 p.m. Special events this summer include a tenth anniversary Refugee Week presentation Child Migrant Voices introduced by Amber Butchart and Eithne Nightingale at Rochester Cathedral that will benefit Kent Refugee Action Network, linking the history of the Huguenot diaspora with current challenges faced by displaced young people aged 16 to 24.

Child Migrant Voices - Refugee Week 2025

Tickets, Fri, Jun 20, 2025 at 6:00 PM | Eventbrite

In addition for Friends and Houblon Circle Members, a tenth anniversary garden party will be held in July. Details of events, including a seminar on historic ivories (4 June) and membership, are on the museum website www.huguenotmuseum.org

Huguenots left France for freedom offered by the British Isles over two hundred years ago. In 1550 their first church was founded in the City of London’s Threadneedle Street under the young King Edward VI. Huguenots introduced the word ‘refugee’ (from the French refugier) to the English language. Those who settled here encouraged other family members and contacts back in France to join their communities established across the country. The Huguenot determination to create a new life in their adopted country, through aspiration, assimilation, endurance, faith and resilience continues to resonate in today’s world.

The Artist's Estate

The artist's estate presents a particular challenge: how to deal with an artistic legacy within the context of an artist's overall estate planning? In the ordinary way an artist will wish to provide for their family after they die, but most will also be very focused on their artistic legacy. This gives rise to a number of challenges and questions which need to be addressed.

The Artistic Estate

Depending on the artist, the estate might include sketches, casts, maquettes, notebooks, catalogues, a workshop, the finished works themselves and associated intangible assets such as copyright and artist’s resale rights (together in this article called “the Artistic Estate”). The starting point is to understand what will make up the Artistic Estate, including identifying which works the artist owns, where copyright and entitlement to the Artist's Resale Rights sit and which other assets the artist might wish to be treated as part of their artistic legacy.

Once the Artistic Estate has been identified, thought can be given as to how the constituent parts will be dealt with on the artist's death. It might be that the artist is happy for the Artistic Estate to be exploited purely for the benefit of their family, descendants and other beneficiaries, but there can be a tension between providing for those individuals and the cost of curating the work of the artist in accordance with his or her wishes.

Questions to consider when formulating a plan include: should one individual take on responsibility for and benefit from the Artistic Estate (or part of it), or should it be held and administered by trustees for a class of beneficiaries for the long term? Does the artist wish for the Personal Representatives to add to the Artistic Estate by repurchasing works so that they can be managed together? Should a catalogue raisonné be prepared and if so, who will undertake that? Copyright and Artist's Resale Rights may become valuable, so who should control and benefit from those rights over the 70 years of their existence? Is any of the Artistic Estate earmarked for charity?

Who and How

If the artist's Executors are to be tasked with managing the Artistic Estate, then selecting the appropriate people for the role is key. The default position is that Executors must make decisions unanimously, so they should be individuals who will work well together, even if each may have a slightly different focus on the estate; one might be a family member (or appointed for their knowledge of the artist’s family, their financial needs and the artist’s wishes in this respect) and another ideally somebody who knew or worked with the artist professionally, understands the artist’s wishes for the Artistic Estate and has the expertise to implement them.

Alice Julian Senior Associate Boodle Hatfield LLP

Alice is a senior associate in the private client department at Boodle Hatfield LLP. She advises on all aspects of private client work, with a particular focus on landed estates and associated art and heritage matters.

Once the artist has an idea of how they wish for the whole of their estate to be dealt with, then a Will can be prepared to provide the legal framework to facilitate the plan, covering both the management of the Artistic Estate and provision for the artist's family or other beneficiaries. This might be achieved by the creation of separate trusts, or a combination of specific legacies and trusts. In most cases, financial constraints are likely to mean that the two are dealt with together in some form of compromise. If there is no Will, then the artist's estate will pass under the rules of intestacy and be administered (usually) by surviving family members who benefit under the estate.

The Will governs the legal devolution of the artist's estate, but then in a letter of wishes the artist can explain the thinking behind this, including (if relevant) how provision for family and other beneficiaries will be balanced against promotion of the artistic legacy. Detailed guidance as to the management of the Artistic Estate can be set out in a letter to the relevant person, be it the Executors (who in due course may become the trustees of any trust created under the Will) or the individual beneficiary who is to inherit the Artistic Estate. The letter might address the questions listed above and also cover practical matters such as recommendations for storage, insurance and conservation during the administration of the estate and suggested

arrangements for selling works. Ideally the artist will have discussed these ideas with the relevant person or people during their lifetime, so that the letter is a useful reminder of earlier conversations rather than wholly new information.

Managing Inheritance Tax

Inheritance Tax (IHT) will be payable in the usual way at 40% on the value of all the assets in an artist’s estate, subject to available exemptions and reliefs. So if everything passes to a spouse, then the spouse exemption will be available on the first death and, depending on ages and timings, it might be that the spouse is able to implement tax planning in his or her lifetime, with the benefit of knowledge of the artist’s wishes. Otherwise thought will need to be given as to how to meet the IHT liability on the whole estate whilst preserving the Artistic Estate intact insofar as possible. There may be an imbalance in values between the Artistic Estate and the rest of the estate, so the Executors will need to decide which assets will fund the tax (a decision that will be informed by the artist's overall wishes). Options for managing the liability include:

Business Property Relief

Depending on how the artist’s business is structured, it might attract Business Property Relief (BPR). For many years BPR has offered 100% relief from IHT on the value of an individual's ‘trading’ business (i.e. a business

that is not one of mainly making or holding investments). The government announced in the October 2024 budget that BPR will be restricted with effect from 6 April 2026 so that the relief will be available at 100% on £1,000,000 of qualifying property and at 50% on the balance. This change significantly impacts the value of the relief, so that for many working artists, other options for meeting the IHT liability on the Artistic Estate now need to be considered too.

The same BPR rules apply to an artist’s business as to any other, so thought should be given during the artist's lifetime as to how to structure the business in order to secure the relief (and the position kept under review). It is possible that artists will continue working to some degree throughout their lives, which is helpful in ensuring that the business is still trading at their death. One important aspect is to ensure that artworks created by the artist are not treated as excepted assets for BPR purposes (which means that any value attributable to them is not eligible for the relief). To avoid that, the artworks must be treated as and qualify as trading stock used for the purposes of the business and be required for future use for those purposes at the date of death.

Charitable exemption and charitable foundations

The charitable exemption from IHT is unlimited in value. Some artists may wish to leave part

of their Artistic Estate to a charity, either to enable the charity to sell artworks and apply the proceeds in furthering the charity’s objects, or to support the work of the charity in another way – for example, a gift of an archive to an educational charity or artworks to a gallery. Often artists will have discussed this with the charity during their lifetime.

Many artists like the idea of their Artistic Estate passing to a foundation, so that it can be managed as one entity in perpetuity. There is then the question of whether a charitable foundation is appropriate. For the most eminent artists, it might be possible to establish a new charity whose objects include the promotion of the artist’s work and legacy. Part of the Artistic Estate could then be donated to that charity. The objects of the charity must be to advance a charitable purpose (as set out in section 3 of the Charities Act 2011) for the public benefit, so it might be that they cover the advancement of the arts and the advancement of education – see for example the objects of the Bridget Riley Art Foundation. The Charity Commission will be particularly concerned to see that no private benefit is conferred by the charity if it is set up during the artist's lifetime.

The constraint of donating all or part of the Artistic Estate to charity is that once assets have been given away, they can only be applied

in furtherance of the charity’s objects; it is the charity trustees who will have control of these elements of the Artistic Estate. It might be possible for the artist’s family to be represented on the board of trustees, or for a relative to have power to appoint trustees, but the charity trustees will have to act independently and only in the best interests of the charity. The charity trustees will be obliged to exploit the works and any rights they own as much as possible for the benefit of the charity, which approach might be at odds with the artist’s wishes.

Acceptance in Lieu

The advantages of this scheme are well-known, enabling taxpayers to transfer artworks into public ownership in lieu of paying IHT and with the financial benefit of the douceur. In order to qualify, the submitted works must be designated as "pre-eminent" in their national, scientific, historic or artistic importance, so this is likely to be available only to a small number of artists' estates. If available, this is an attractive option for meeting the IHT whilst ensuring that an artist's work is transferred into public ownership.

Conditional Exemption

In a similar vein some works might qualify for conditional exemption from IHT, so that no tax is payable on the death, provided the Executors (or other relevant persons) give undertakings to HMRC to preserve the works, keep them in

the country and allow reasonable public access to them. It is this last element which can often present difficulties, but it might be possible for the Executors to come to an arrangement with a gallery which worked with the artist in his or her lifetime to provide the required public access.

Sales

If there is insufficient liquidity in the estate to meet the IHT liability then artworks will likely need to be sold in order to fund the tax. Most successful artists will have developed relationships with a number of galleries and dealers during their careers, who will be well-placed (along with the auction houses) to assist with a sale.

Conclusion

There is no one size fits all approach for dealing with an artist's estate; the answer in each case will be informed by the nature of the artist's work, their attitude to their artistic legacy and their wishes for their family and other beneficiaries. The same issues arise for many artists, however, and they are not straightforward, so it is advisable that they start considering and discussing these with those affected as early as possible in order to achieve what is wanted in terms of providing for their dependants and securing their artistic legacy.

Tim Adams is Private Client partner at Saffery LLP (www. saffery.com/our-people/ tim-adams/). He advises individual and trustees on all aspect of their financial and tax affairs and helps his clients achieve their personal and financial objectives.

Making Tax Digital for income tax: Considerations for the creative industries

With less than a year to go until the biggest change to income tax compliance in a generation, it’s important to understand what Making Tax Digital (MTD) for income tax is, who it applies to and how those affected should prepare.

The basics

MTD is part of the UK government’s plan to modernise the tax system and improve the accuracy of information provided by taxpayers to HM Revenue & Customs (HMRC). MTD for income tax is being introduced in phases from 6 April 2026, and by 6 April 2028 will affect all sole traders and landlords with annual gross business and/or property income over £20,000.

Those required to use MTD for income tax will have to keep digital records of income and expenses and submit quarterly updates to HMRC. They will also have to make an end of year submission (equivalent to the current personal tax return). So instead of having to submit one annual tax return, those affected will have to make (at least) five submissions a year, and all submissions must be made using MTD-compatible software.

MTD for income tax is a reporting requirement and does not change the timing of income tax and National Insurance contributions. These will still be due in January and July each year. Once up and running, it would not be surprising if the tax payment dates were aligned with MTD reporting at some point in the future.

MTD for income tax does not change VAT filing and reporting obligations for those who are also VAT registered. However, those VAT registered artists and landlords will already be used to some of the MTD record keeping requirements as they’ve had to adopt similar rules for the preparation of their VAT returns. It would be an obvious simplification if MTD for income tax and VAT reporting were combined, but that may still be a few years away.

For those in the creative industries, where income can often be sporadic, particular attention will need to be paid to ensure timely registration for MTD for income tax, as it may not be as obvious when their income reaches the relevant threshold. Those with irregular income required to use MTD for income tax should also consider whether sustained periods of low income would allow them to claim an exemption from MTD for income tax. Artists will still be able to claim to average their profits over two consecutive years to smooth out their tax and National Insurance payments through their end of year submission.

Each of these issues is considered further below.

Who does MTD for income tax apply to and from when?

MTD for income tax will apply:

• From 6 April 2026, for those with gross self-employment and/or property income of more than £50,000 a year,

Tim Adams Partner Saffery LLP

• From 6 April 2027, for those with such income of more than £30,000 a year, and

• From 6 April 2028, for those with such income of more than £20,000.

When considering the threshold, it is gross income (or turnover), not profit, that matters, and if a person has multiple sources of income – such as a trade and a rental property – it is the combined income that is considered when working out whether the income threshold is met.

Certain people will not need to file under MTD for income tax, including (but not limited to) the digitally excluded, people without National Insurance numbers, and non-resident entertainers.

Practicalities of deciding who has to use MTD for income tax

Whether and when a person needs to comply with MTD for income tax will be based on the gross income included in their most recent tax return filed before the relevant start date. For example, a person must comply with MTD for income tax from 6 April 2026 if their combined trade and property income in their 2024-25 tax return is more than £50,000. HMRC plan to send letters to taxpayers it considers need to use MTD for income tax before April 2026, but it is the taxpayer’s responsibility to sign-up.

Once a taxpayer is within MTD for income tax, they will remain in MTD until they stop their business, even if their income drops below the relevant threshold. However, a taxpayer can claim an exemption from MTD for income tax from the fourth year if their qualifying income for each of the previous three years is below the relevant threshold for that year.

For example, let’s consider an artist, who in 202425 sold a painting for £45,000 and prints for £15,000, and then in each of the years 2025-26, 2026-27 and 2027-28 only sold prints for £15,000.

The individual will be required to use MTD for income tax from 6 April 2026 as they met the £50,000 income threshold for 202425. They will have to remain in MTD until 2028-29, by which time they can claim an exemption because in each of the three previous years their turnover was below the relevant thresholds of £30,000, £20,000 and £20,000.

Given the sometimes widely fluctuating nature of creative artists’ profits, there is a relief allowing a person’s profits to be averaged over two consecutive years in order to smooth their taxable income and reduce their overall liability to income tax and National Insurance contributions. Averaging claims do not affect the amount of a person’s trading income for the purposes of the MTD for income tax thresholds.

Digital record keeping

A taxpayer within MTD for income tax must keep digital records for each business transaction. This must include the amount, date and the category of the transaction. The categories will match those on the current tax return and separate records must be kept for each business. Digital records must either be kept in MTD-compatible software or on spreadsheets with the information reported to HMRC through bridging software.

Quarterly updates

From the digital records a person must submit quarterly updates of their income and expenses to HMRC for each type of activity, e.g. where a selfemployed individual also has a rental property, they will need to submit one set of updates for the rental activity and one for their business.

The updates are cumulative for the tax year, and do not need to include any accounting or tax adjustments, although they can if applicable.

Quarterly reports will have to be made through ‘MTD-compatible software’, with digital links between the underlying records and the software making the submissions.

End of year submission

Once a person’s fourth quarterly update has been submitted, the software will show their self-employment and property income and

expenses for the whole of the tax year, for each of their businesses. At this stage any accounting and tax adjustments will need to be made, such as for disallowable expenses and to claim any reliefs and allowances. This is when any profit averaging will be reported.

Once a person’s taxable profit or loss from each business has been calculated, their income tax position for the year should be finalised. This will be done through an end of year submission which will replace the current self-assessment tax return. It will include reporting any nonbusiness income sources that HMRC has not already pre-populated. As with the current tax return, the person will need to declare that the information provided is correct and complete and that their income tax position for the tax year is finalised. This must be done by 31 January following the end of the relevant tax year (i.e. the same deadline as applies now for returns submitted electronically).

Tips to get ready for MTD for income tax reporting

1. Ensure you understand how the MTD for income tax rules might apply to you.

2. Identify when you will be required to start filing the new returns.

3. Watch out for regular HMRC and Saffery updates highlighting the taxpayers likely to be affected, and with information about the changes. HMRC have promised more announcements and resources to aid the transition.

4. If you are not already using digital accounting or record keeping software, discuss with your accountant the practicalities of choosing software, digital record-keeping, quarterly reporting and end of year submissions. We encourage clients to keep digital records well ahead of being required to do so.

5. If you are already using digital accounting or record keeping software,

speak with your software providers about MTD for income reporting.

6. For artists and taxpayers with fluctuating income, consider how changes in your gross income will affect your MTD obligations.

7. Consider whether you would like to be part of the MTD reporting pilot scheme (we note that HMRC has begun contacting taxpayers it expects to be required to use MTD for income tax from April 2026, based on their income from 2023-24, and asking them to consider being part of the pilot).

MTD for income tax reporting is a major change in the way self-employed and rental income is reported. You need to start thinking about it now.

If you have any queries on the areas discussed, please get in touch on tim.adams@saffery.com +44 (0)20 7841 4104 or alternatively, visit www.saffery.com

London | 1 July 2025 EXHIBITION

26 June – 1 July 2025

33⅞ x 54⅜ in. (86 x 138.1 cm.)

Estimate on request

Amelia has over 18 years of experience in the organisation and sale of multi-category private, iconic and country house collections. Since joining in 2006, Christie's has sold countless Iconic, Royal, Aristocratic and Connoisseur collections including those of Mark Knopfler, The Princess Margaret, the Earl Spencer, Sting, Audrey Hepburn, Margaret Thatcher, Roger Federer, Charlie Watts, the Rothschild family, and many more. Amelia is interested in all aspects of collecting, both ‘fine’ and decorative art, from antiquity to the contemporary and has had privileged access to some of the world's most wonderful works of art. She loves nothing more than meeting collectors, researching and valuing their collections and unearthing the provenance and story behind each object, picture, or piece of memorabilia.

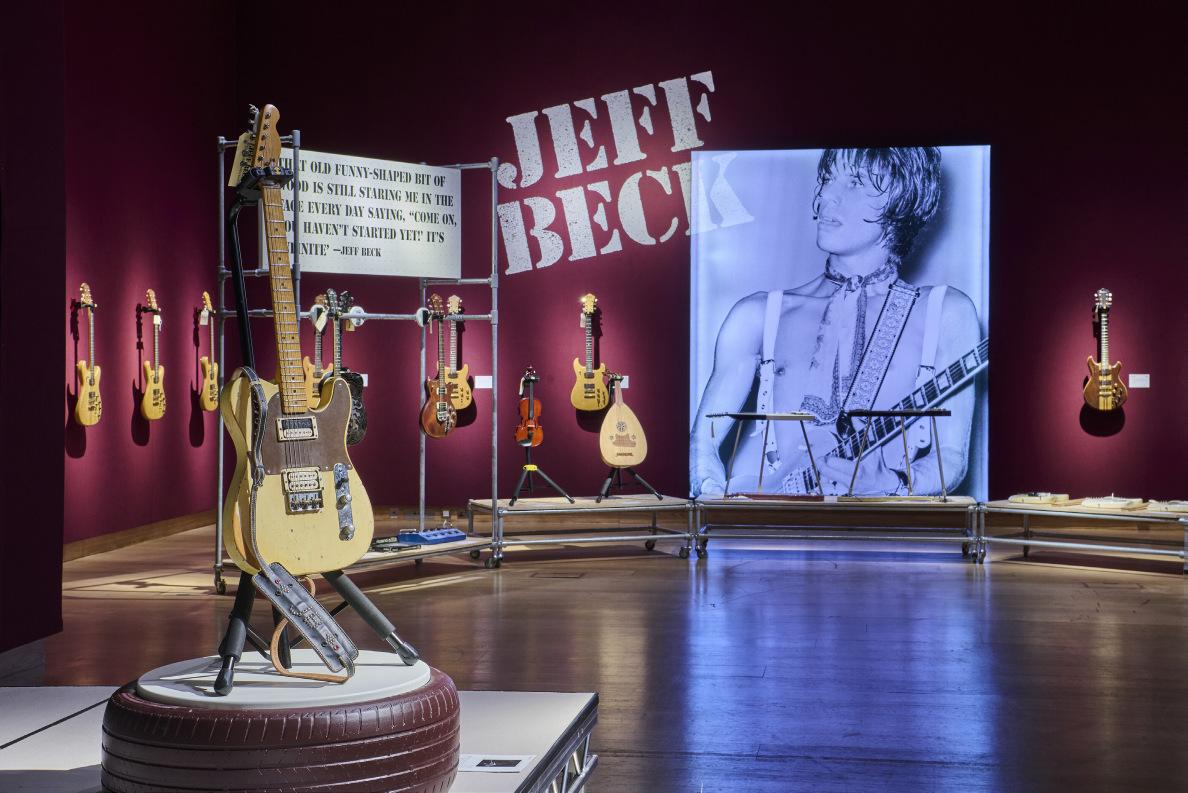

Rock Icons at Christie’s

For two successive years, Christie’s Private & Iconic Collections department in London has transformed Christie’s King Street into a mecca for Rock & Roll fans from around the world, staging The Mark Knopfler Guitar Collection on 31 January 2024 and Jeff Beck: The Guitar Collection on 22 January 2025. These two auctions were the latest in a series of high-profile Rock & Roll collections to come to the market over the last 25 years, a market in which Christie’s is the undisputed leader.

Christie’s pioneered the phenomenon of the celebrity guitar auction with a selection of Eric Clapton’s guitars offered for sale in June 1999 in New York. That incredibly successful auction saw 105 lots sell for just over $5 million, over 566% of the pre-sale low estimate, establishing a new world auction record for a guitar with Clapton’s 1956 Fender Stratocaster known as ‘Brownie’, which sold for $497,500. In 2004, a second sale of guitars from Eric Clapton’s collection, also benefitting his Crossroads Centre, saw records broken again, with 88 lots selling for a combined $7.2 million and with Clapton’s main 1956/7 Stratocaster, known as ‘Blackie’, selling for just under $1 million and breaking ‘Brownie’s’ record.

Since these inaugural single-owner auctions, Christie’s has enjoyed continued and consistent success with both the private collections of celebrated musicians and individual iconic guitars. Christie’s is the only international auction house with a team dedicated to the staging of Private & Iconic Collections, whose expertise in understanding and researching

these music legends and their instruments, as well as staging a global promotional campaign, is fundamental to their success.

Each musician is unique and has distinct appeal amongst fellow players and collectors for the influence they have had on music and culture. Their collections are all different, although the motivations for guitarists amassing their ‘collections’ are manifold and often overlap: most have accumulated guitars in the pursuit of a particular sound or look, with a specific genre or song in mind; some are ‘collectors’, influenced by the rarity, craftsmanship and beauty of a particular maker and/or period – the guitars treasured as works of art in themselves; and to others they are quite simply the ‘tools’ through which they create and express their art, with the scars to prove it. Each instrument is different and the guitars themselves all tell a different story, have captured a different sound and some can be inextricably linked to a particular period in an artist’s career or even to a specific song. These guitarists and their instruments therefore each represent something different to the many collectors, players and legions of devoted fans who all clamour to take part in these unique auction events. Christie’s expertly harnesses all these elements when presenting their collections for sale, and partners with the artists and their teams to maximise the appeal of each and every instrument. Whilst some artists choose to part with their guitars in their lifetime, others are sadly no longer with us; whatever the reason for selling, each collection and auction holds its own unique appeal.

Amelia Walker Director, Specialist Head of Private & Iconic Collections Christie’s

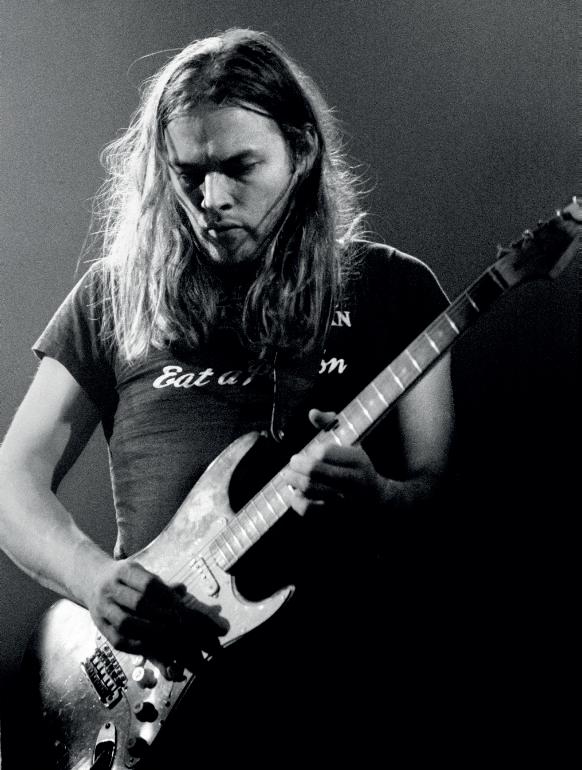

David Gilmour

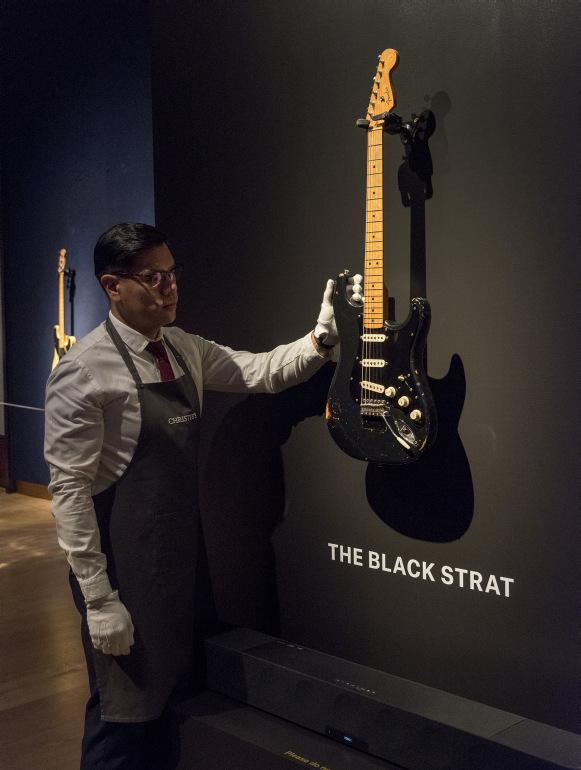

The avid demand for iconic instruments was most notably demonstrated in June 2019 with the sale of guitars from the collection of legendary Pink Floyd guitarist, David Gilmour. Comprising 120 guitars, amps and other instruments, with a pre-sale estimate of $1-1.6 million, the auction attracted unprecedented global attention, with intense competitive bidding driving the final figure to $21.5 million, which benefitted Gilmour’s chosen charity, ClientEarth. ‘The Black Strat’, David Gilmour’s famous 1969

Fender Stratocaster, soared past its pre-sale estimate of $100,000-150,000 to achieve $3,975,000, establishing a new world auction record for any guitar. The undeniable power of the Gilmour name and the cult following of Pink Floyd meant that every single lot, expertly researched and beautifully presented by Christie’s, far exceeded its pre-sale expectations.

Demand for guitars with celebrated histories has continued to grow, including during the Covid-19 Pandemic which saw outstanding results

achieved at Christie’s for Gibsons, Rickenbackers and Fenders, including the ES-355 formerly owned by Blues Legend B.B. King, the ‘Ricky’ bass customised by the iconoclastic bass player from The Clash, Paul Simonon, and, owned by the godfather of the solid-body electric guitar, Les Paul’s own ‘No. 1’ Goldtop Gibson Les Paul. In December 2021 a selection of guitars from the collection of super-producer and Chicfrontman Nile Rodgers achieved two and a half times their pre-sale estimate, raising over $1.6 million for his We Are Family Foundation.

David Gilmour playing 'The Black Strat' with Pink Floyd live at The Rainbow Theatre, London, 4 November 1973. Courtesy of Jill Furmanovsky Archive.

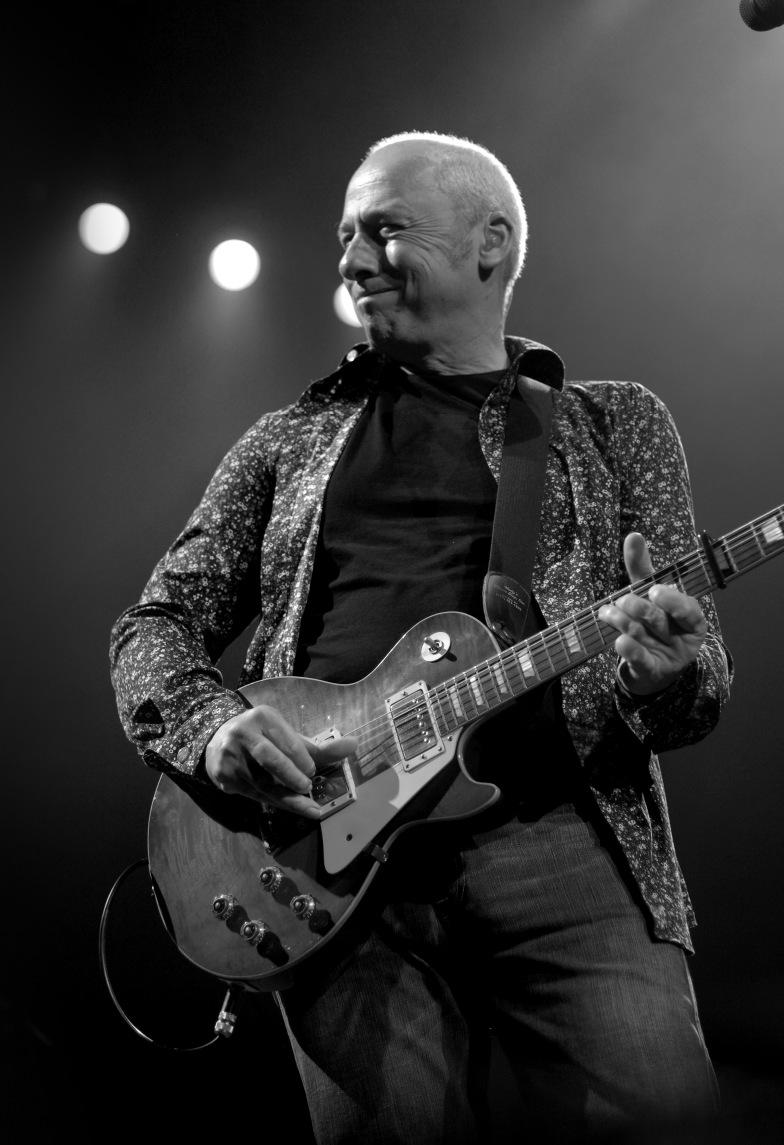

Mark Knopfler

Whilst undoubtedly initially driven by demand in the U.S. for what are mostly American-made instruments, the market for iconic guitars has grown to be truly international. This was reflected in Christie’s decision to hold the next major iconic guitar auction in London as opposed to New York – a hugely successful as well as logical step, given both the increasing dominance and convenience of online bidding, as well as the spread of that particular artist’s fanbase and market.

On 31 January last year, Christie’s offered for sale guitars from the personal collection of music legend Mark Knopfler, the celebrated singer-songwriter, guitar hero and frontman of the iconic British band, Dire Straits. Presenting fans with more than 120 guitars and amps, the collection spanned the 50-year career of one of the world’s most influential musicians and chronicled the diverse array of guitars Knopfler used to write, record and perform an extensive catalogue of compositions for Dire Straits, as

well as multiple successful solo albums and film soundtracks. Renowned for his distinct and virtuoso finger-picking style, Knopfler chose each instrument for its individual sound and tone, assembling a wide-ranging archive including not only world-famous names such as Fender, Gibson, Gretsch and Martin but also custombuilt models by Rudy Pensa and John Suhr, as well as bespoke instruments crafted by luthiers from across the globe. Mark Knopfler expressed that he didn’t set out to be a guitar collector, but

that he had always been obsessed with guitars and somewhat accidentally accumulated a mouth-watering collection of instruments, all in pristine condition, including some exceptionally rare vintage examples alongside icons like the 1983 Gibson ’59 Reissue Les Paul Standard used to write, record and perform ‘Money For Nothing’ and played on stage at Live Aid.

The sale was 100% sold, realising a total of £8,840,160 and was led by Knopfler’s 1959 Sunburst Gibson Les Paul Standard which sold for £693,000, setting a new world auction record for the model (‘Bursts’ from 1959 specifically are regarded by many as the ‘holy grail’ of vintage guitar collecting). Further new world auction records were set including for the purple PensaSuhr guitar which Knopfler had used to record and perform ‘So Far Away’ and for a Schecter Telecaster used to record and perform ‘Walk of Life’. Music aficionados, fans and collectors from 61 countries registered to bid, with phenomenal levels of competition resulting in the auction lasting over six hours. 25% of the total hammer price was divided equally and donated to charities that Mark Knopfler has supported for many years: The British Red Cross, Tusk and Brave Hearts of the North East. 100% of the funds raised from the final lot were donated to Teenage Cancer Trust. In addition, Christie’s contributed a further £50,000 to each of the four charities. After the auction Mark Knopfler himself said, “This auction has been an incredible journey and I am so pleased that these much loved instruments will find new players and new songs as well as raising money for charities that mean a lot to me. All Christie’s staff have been hugely impressive in every respect. It has been heart-warming to witness how much these guitars mean to so many people and I am also pleased that they will continue to give joy to many through the songs recorded over the years with me. To you fellow players, enthusiasts and collectors, I wish you all good things.”

Almost exactly a year later, Christie’s was honoured to bring to auction guitars from the collection of trailblazing guitar icon Jeff Beck (1944-2023) in a landmark sale in London in January 2025. Comprising 128 guitars, amps, pedals and 'tools of the trade', Jeff Beck: The Guitar Collection included most of the instruments which the late, great guitar legend played through his almost six-decade-long career, from joining The Yardbirds in March 1965 to his last tour in 2022. The ultimate guitarist’s guitarist, Jeff Beck was a rock pioneer whose influence on his peers was unmatched. A multi-Grammy award-winning artist – twice inducted into

the Rock & Roll Hall of Fame – his inimitable sound led to collaborations with countless internationally renowned musicians and friends including: Jimmy Page, Jimi Hendrix, Ronnie Wood, Rod Stewart, Stevie Wonder, Steven Tyler, Joe Perry, Billy Gibbons, Jan Hammer, Eric Clapton, David Gilmour, Tina Turner, Nile Rodgers, Mick Jagger, BB King, Buddy Guy, Carlos Santana, Imelda May and Johnny Depp, amongst many others. From the outset, Jeff Beck was a sonic innovator; a maverick and mercurial virtuoso who blazed the trail for musical genres as diverse as Psychedelia, Heavy Metal and Jazz-Rock Fusion, and who embraced a wide range of influences from the

Blues, Rockabilly and Rock & Roll to Indian sitar music, Bulgarian Folk, Techno, and Opera. A maestro of his trade, Jeff could make just about any sound possible with a guitar and an amp.

With the exception, perhaps, of Jeff Beck’s vintage Gretsch guitars – inspired by his idol Cliff Gallup of Gene Vincent’s Blue Caps – guitars truly were ‘tools’ to Jeff Beck, extensively modified to suit his needs and in some cases played almost to destruction. Christie’s sold-out catalogue detailed the blood, sweat and tears which covered their surfaces and told the stories of each and every one – from the Gibson Les Pauls, including the ‘Yardburst’ which Jeff bought in

London in 1966 and which was played by both Jimmy Page and Jimi Hendrix, and the iconic ‘Oxblood’ depicted on the cover of his seminal debut solo instrumental album Blow By Blow, to the Fender Teles and Strats which were his ‘workhorses’, describing the latter with which his playing became synonymous as: “My Strat is another arm, it’s part of me. It doesn’t feel like a guitar at all. It’s an implement which is my voice.”

A testament to the legacy of a genius and a globally revered true rock legend, the sale was 100% sold, realising an outstanding total of £8.7 million, more than eight times the pre-sale low estimate. The auction welcomed bidders from 40 countries, who competed fiercely throughout, resulting in the sale lasting almost seven hours. Having opened with a bang, there was intense competition from lot 1, which sold for more than 10 times its pre-sale estimate, swiftly followed by the ‘Yardburst’ which realised £403,200. The top lot was Jeff Beck’s iconic 1954 ‘Oxblood’ Gibson Les Paul, which doubled its pre-sale high estimate, selling for £1,068,500, after a bidding battle that lasted over four minutes, establishing a new world auction record for any Gibson Les Paul.

Several further new world auction records were achieved, including for Jeff Beck’s pink Jackson guitar, also known as ‘Tina’, signed by Tina Turner, the queen of Rock & Roll herself, which sold for over 36 times its pre-sale high estimate realising £441,000. Jeff Beck’s main stage pedalboard, which comprised the arrangement used on his last tour in 2022, sold for £126,000, establishing a new auction record. His Fender Custom Shop Stratocaster known as ‘Anoushka’ (it had once borne the signature of sitar virtuoso Anoushka Shankar) was almost certainly the instrument that fans would have seen him wield more than any other, having been his main stage and recording guitar from 1998 to 2014. Paying tribute to the power and magnetism of his live performances, the guitar achieved a

world record breaking £1,008,000. Jeff Beck supported many charities throughout his life, and 100% of the hammer price of the final four lots in the sale benefitted Folly Wildlife Rescue in Tunbridge Wells, a charity proudly supported by Jeff Beck alongside his wife Sandra and close friend Johnny Depp, who continue to act as patrons. After the auction, Sandra Beck stated, “I am so happy that Jeff 's guitars have been so popular amongst his fans and friends. Thank you so much for your belief in Jeff's legacy.”

As the guitar heroes of the ’60s and ’70s approach their twilight years it is perhaps unsurprising that collections such as those of Gilmour, Knopfler and Beck should come to the

market. However, it is important to note that the phenomenon of record-breaking prices for guitars is not limited to that generation or driven solely by their fans and guitar collectors, many of whom happen to be a similar age. Breaking The Black Strat’s world record just one year after it was set, the top price (and second highest price) ever paid for a guitar at auction is now held by an instrument played by the Nirvana frontman Kurt Cobain, who died in 1993 at the age of just 27. The power of music to inspire passion and devotion has a direct correlation to the value of iconic guitars, and, for the most era-defining musicians in each and every musical genre, there is no doubt that their instruments will continue to increase in desirability and value.

Christie’s Heritage and Taxation Advisory Service has over 50 years of experience in undertaking offers in lieu of inheritance tax and is extremely experienced in this highly specialised field.

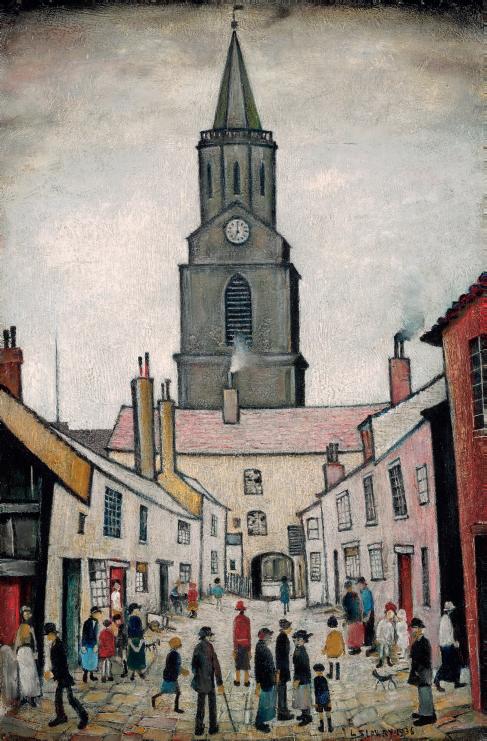

LAURENCE STEPHEN LOWRY, R.A. (1887-1976)

Old Berwick signed and dated ‘L.S. Lowry 1936’ (lower right) oil on panel 21 x 13 ¾ in. (53.3 x 35 cm.)

Accepted by HM Government in lieu of Inheritance Tax and temporarily allocated to Northumberland County Council for display at Berwick Museum and Art Gallery. christies.com