Your chosen entity will guide business decision-making processes, tax structuring, and other efficiencies, as well as your ability to effectively scale, raise capital, and manage investors. By carefully considering available legal entity types and then choosing the most appropriate one for your current project needs, you can help address liabilities, structure efficient taxation, and launch the business in a favorable form for conducting and financing the enterprise efficiently.

(LLC)

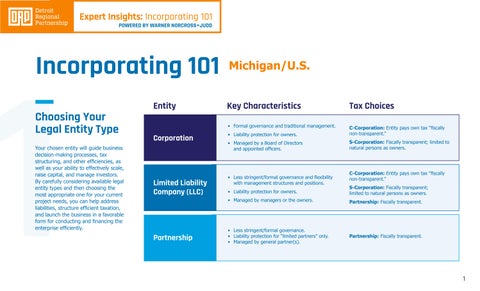

Key Characteristics

• Formal governance and traditional management.

• Liability protection for owners.

• Managed by a Board of Directors and appointed officers.

Tax Choices

C-Corporation: Entity pays own tax “fiscally non-transparent.”

S-Corporation: Fiscally transparent; limited to natural persons as owners.

• Less stringent/formal governance and flexibility with management structures and positions.

• Liability protection for owners.

• Managed by managers or the owners.

C-Corporation: Entity pays own tax “fiscally non-transparent.”

S-Corporation: Fiscally transparent; limited to natural persons as owners.

Partnership: Fiscally transparent.

• Less stringent/formal governance.

• Liability protection for “limited partners” only.

• Managed by general partner(s).

Partnership: Fiscally transparent.

Selecting Where to Form (and Qualify) Your Business

When deciding what state to form your entity in, consider the following.

Foreign Qualification

If your business might have a presence in more than one state, consider whether formally registering in these other states is required. Typically, this is a simple process that involves submitting necessary information/paperwork and paying applicable fees.

Michigan Advantage

Michigan is recognized and often selected as a state of formation for entities conducting business here due to its lack of franchise taxes, nominal filing and administrative fees, limited reporting obligations, and sophisticated corporate statutes and courts.

U.S. entities are formed under state law. This means you can form your entity in any state (even a state where you do not or may not operate) however, your entity will be required to “qualify” in each state that its activities meet the threshold for “doing business” in such state. It is commonplace for Michigan businesses to operate not only within the state but around the U.S. and globally.

Factors

Sophistication and advancement of corporate statutes and courts.

“Friendliness” of courts and state laws to businesses (i.e., protection afforded to your business operations and assets).

Management flexibility as well as shareholder rights (including minority shareholder protections), and other governance-related considerations.

Location(s) of your business activities.

State reporting obligations and administrative complexity.

Implications of state taxes (respect for federal tax elections, state income tax on ownership, etc.)

Future investor expectations.

Franchise taxes and other related fees (varying significantly). Some states have unique “hidden” costs, like publication requirements.

Lender and other business partners’ familiarity with the jurisdiction.

POWERED BY WARNER NORCROSS+JUDD

Defining Your Corporate Governance

Corporate Formalities

When considering your choice of legal entity and state of formation, balancing the desire for oversight against the need for agility and flexibility will be among one of many important decisions for your new business. Corporations generally have greater formal requirements (e.g., annual shareholder meetings, board approvals, etc.), whereas limited liability companies are on the other end of the spectrum with fewer statutory requirements and far more operational flexibility. Michigan’s limited liability company act provides substantial freedom for companies to tailor their governance practices (in an operating agreement or similar document) to align with applicable business needs.

Corporate governance refers to various systems of rules and processes by which a company is operated and controlled, including the basic aspects of a company’s existence, how the company approves actions, and stakeholders’ rights and obligations. Corporate governance is established both by applicable state law and a company’s organizational documents.

Assumed Names

Assumed names (also referred to as doing business as, “DBAs,” or fictitious names) allow a company to conduct business under one or more names that are different from their legal entity name (i.e., the name used in the formation document(s)). Assumed names are frequently used where you want to differentiate your products or offerings for different market segments. Sometimes, assumed names are required in connection with a foreign qualification because your legal entity name is not available in the foreign state.

Board of Directors and Officers

As noted, corporations operate within more formal management structures, including a governing board of directors (who are charged with setting overall strategy and overseeing management) and certain officer positions (who are responsible for running day-to-day operations). Generally, corporations must elect at least one director and certain officers on an annual basis (in Michigan, for example, a president, secretary, and treasurer must be appointed). In contrast, limited liability companies can be managed directly by their member(s) without a separate governing board or any officer appointments (though in Michigan, for example, a governing board and officer positions can be designated).

POWERED BY WARNER NORCROSS+JUDD

Considering Tax Matters

Let’s talk about the use of Federal Employer Identification Numbers and initial capitalization.

Federal Employer Identification Number

An Employer Identification Number (EIN), also known as a Federal Tax Identification Number, is a unique nine-digit number assigned by the Internal Revenue Service (IRS) to businesses operating in the United States.

Why It’s Important Tax Purposes

The EIN is used to identify a business entity for federal tax reporting. It is the number used to identify a company in the U.S. tax system and by many other agencies, and frequently, your business partners. When applying for an EIN, the company needs an individual with a U.S. social security number or individual taxpayer identification number. This can be a hurdle for a foreign company setting up in the U.S.

Required For Most Business Activities

You’ll typically need an EIN to:

• Open a business bank account

• Apply for business licenses or permits

• Hire employees (it’s required for payroll tax reporting)

• File federal and state tax returns

Flexibility in Capital Structure

The U.S. allows significant flexibility in how a business is capitalized. Founders can contribute capital in various forms (cash, property, and/or services) and in exchange for:

Equity: Ownership interest (e.g., common or preferred shares).

Debt: Loans from shareholders or third parties.

This flexibility helps companies choose a structure that aligns with their tax planning, investor preferences, and long-term growth strategies.

No Minimal Capital Requirement

Unlike some countries, the U.S. does not require a minimum initial capital to incorporate a business (except in rare, regulated industries such as banking or insurance). This makes entry easier for startups and foreign companies.

Documentation and Transfer Pricing

When funding with intercompany debt:

• You must document the loan terms clearly (interest rate, repayment schedule, etc.).

• Comply with transfer pricing rules to prove that interest rates and terms are at arm’s length (comparable to what independent parties would agree to).

• Improper documentation can lead to reclassification of debt as equity, resulting in denied deductions and potential tax penalties.

Withholding Tax on Interest and Dividend Payments

If a U.S. entity pays interest to a foreign lender (including a parent company) or dividends to a shareholder, the payment will be subject to U.S. withholding tax (typically 30%). Lower rates under an applicable tax treaty may apply.

POWERED BY WARNER NORCROSS+JUDD

Setting the Stage for Successful Contracts

Sales Agent Arrangements

Helping you navigate through the range of options while protecting business interests.

In addition to your other standard contract forms, if your business plans to engage commissioned sales representatives (agents) to help develop and maintain client relationships, you will want to ensure those arrangements are appropriately documented in writing and that both parties are aligned on key commercial terms, including with respect to territory, product and service lines, exclusivity, carveout accounts, commissions and other compensation arrangements, marketing obligations as well as the authority to accept orders, among others. You will also want to be informed regarding applicable state sales representative, sales commission, or similar acts, which could provide for different outcomes than your business otherwise anticipates, and take appropriate steps to help avoid the sales representative being unexpectedly deemed an employee of your business.

Proceed Cautiously When Utilizing Foreign Contracting Templates and Practices

The U.S.’s common law system, which is heavily reliant on court decisions and judicial precedent, can be a startling contrast for those accustomed to transacting in civil law jurisdictions (e.g., Germany, Japan, Mexico, etc.) where more comprehensive legal codes provide a very different framework for commercial contracting. Developing proper standard contract forms or appropriate modifications to existing foreign forms, including terms and conditions, services agreements, and confidentiality agreements, etc., provides a great return on investment for protecting important business interests in the U.S.

Kurt Brauer Partner

kbrauer@wnj.com

313.546.6182 wnj.com

Carlotta C. Gmachl Business Development Executive gmachl@wnj.com