LOCAL EXPERTISE WITH A GLOBAL PERSPECTIVE

Welcome to the quarterly residential market report of the third quarter of 2023, providing the latest data on the Cyprus real estate market in the reporting period.

Cyprus’s high-end residential property market showed a slight decrease both in terms of volume and value compared with the same period of the last year. The market is stabilizing itself on the back of extremely strong performance in 2022 and first half of 2023. To a certain degree, this is influenced by the latest legislative initiatives: the adjusted regulations for permanent residency by investment in Cyprus and a new law on reduced VAT for first homes. However, we expect the demand to remain quite strong.

Despite occasional fluctuations, the real estate sector, especially its premium end, over the decades has proved to be particularly resilient and a good investment field in our challenging times. As for our company updates, in October Cyprus Sotheby’s International Realty marked a significant four-year milestone of operating in Cyprus.

We have become one of the country’s leading real estate agencies with international recognition. Our team of 30 dedicated professionals acts as ambassadors of the Cyprus lifestyle.

We believe in the stable and sustainable growth of our island, its attractive business environment, and excellent opportunities for life, which will support the local property market going forward.

With gratitude,

Anastasia Yianni Chief Executive Officer Cyprus Sotheby’s International Realty

Anastasia Yianni Chief Executive Officer Cyprus Sotheby’s International Realty

ABOUT INSIGHTS:

Transaction data are provided by Cyprus’ Department of Lands and Surveys, which records all transfers of ownership and registered contracts of sale (including property description, purchase price, date, etc). The data is processed in order to classify each transaction (as some properties are under construction, their description is not exact, or they form part of bigger projects) and are categorised by property type.

The analysis covers the entire area controlled by the Republic of Cyprus, excludes properties sold at auction (foreclosure), and references property values based on the amount declared by the purchaser at the time of the transaction (which excludes any VAT, transfer fees, or other duties levied).

THE REAL ESTATE MARKET

IN CYPRUS

TRANSACTION VOLUME

• Across Cyprus, quarter-on-quarter (Q3 2023 – Q4 2023) transaction volume of houses decreased by 14% (to less than 0.1K) and by 25% (to less than 1.8k) for apartments. Year-on-year (Q4 2022 – Q4 2023) transaction volume of houses decreased by 33% and by 34% for apartments.

• Quarter-on-quarter transaction volume of high-end houses (>€500k) decreased by 23% (to 112) and by 35% (to 525) for high-end apartments (>€200k). Year-on-year (Q4 2022 – Q4 2023) transaction volume of high-end houses decreased by almost 43% and by 44% for high-end apartments.

• Paphos’s year-on-year transaction volume of houses and apartments decreased by 47% (to 228) and 58% (212) respectively.

• Paphos’s quarter-on-quarter transaction volume for houses decreased by 30% and (to 228) and 44% (to 212) decrease in apartment transactions.

PRICES

• Across Cyprus, median prices of houses and apartments decreased in Q4 2023, compared to Q3 2023, at €232k for houses and €150k for apartments. Moreover, year-on-year (Q4 2022 – Q4 2023) median prices decrease by 11% for houses and 5% for apartments.

• Quarter-on-quarter median prices of premium houses (>€500k) decrease by 5% (to €740k) and increase 3% (to €300k) for high-end apartments (>€200k). Year-on-year (Q4 2022 – Q4 2023) median prices decrease by 3% for high-end houses and by 3% for high-end apartments.

OUTLOOK

• The declining trend in prices is expected to reach a point of stabilization in the near future.

• The ongoing conflict between Russia-Ukraine, as well as the persistent geopolitical risk premium associated with Israel-Palestinian war, continue to have an impact on energy prices, causing them to rise. This, in turn, is expected to subsequently affect the construction prices once again.

• Escalating interest rates and rising prices will undoubtedly exert an impact on both the demand of residential properties.

Q4 2023

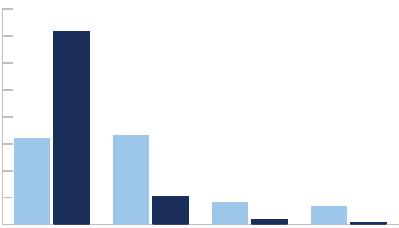

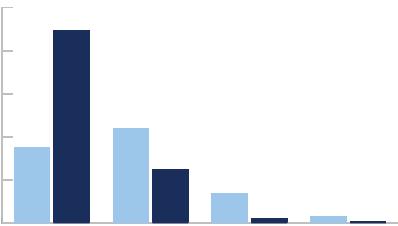

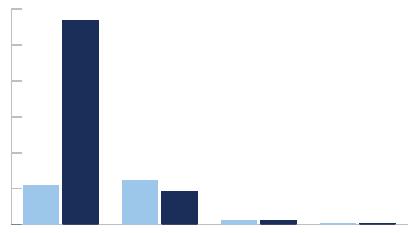

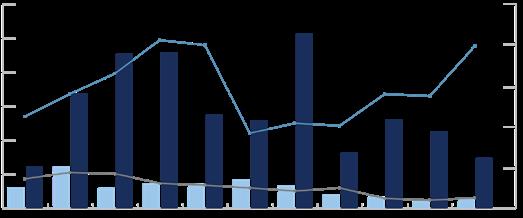

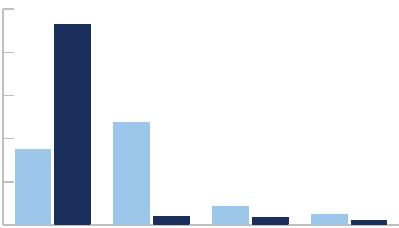

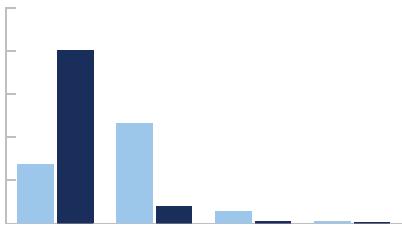

VOLUME OF PREMIUM HOUSES & APARTMENTS

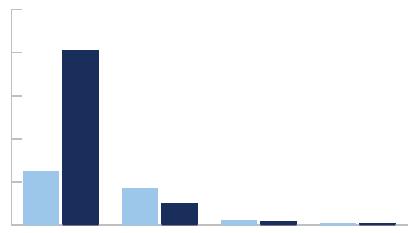

VOLUME OF PREMIUM RESIDENTIAL PROPERTIES BY DISTRICT

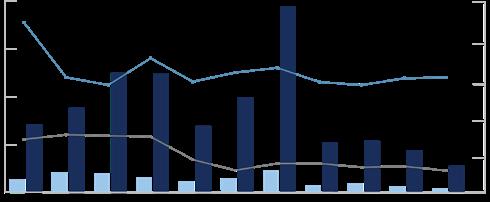

1.1k 1.5k 1.9k 2.1k 1.2k 1.6k 1.0k 0.9k 0.8k 0.5k 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 0.4k 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 0.6k 0.6k 0.4k 0.4k 0.6k 0.6k 0.2k 0.2k 0.1k 0.1k CYPRUS

CYPRUS

Q4 2022

Q4 2023 PREMIUM HOUSES PREMIUM HOUSES PREMIUM APARTMENTS PREMIUM APARTMENTS

–

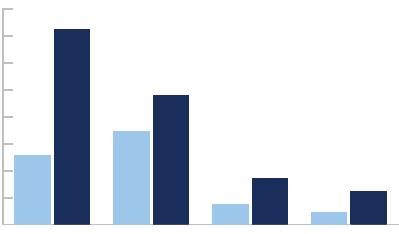

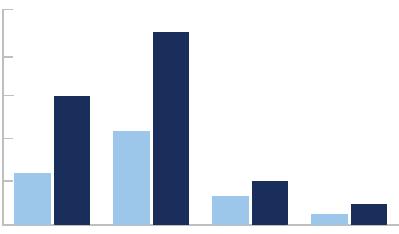

Larnaca Nicosia Famagusta 12% 1% 16% 58% 13% 478 57 672 2377 522 40% 9% 8% 5% 39% 346 69 75 47 338 VOLUME VOLUME 0 0.4bn 0.2bn 0.6bn 0.8 bn 1bn 1.2bn Q1-Q4 2022 Q1-Q4 2022 Q1-Q4 2023 Q1-Q4 2023 0 500 1000 1500 2000 2500 TRANSACTION VOLUME OF PREMIMUM PROPERTIES Apartments Houses TRANSACTION VALUE OF PREMIUM PROPERTIES Apartments Houses

Limassol Pafos

LIMASSOL

Limassol is the business capital of Cyprus and a city of skyscrapers. Relocated international companies are the driving force behind the constant real estate growth in the city.

Residential transactions totalled 700 in Q4 2023, of which 46% (322 properties) were of the premium segment of the market.

Premium residential properties are of particularly high demand in Limassol, indicated by the high percentage of houses (41 properties, 37% of the total for Cyprus) and apartments (281 properties, 54% of the total for Cyprus) transacted over the past quarter.

Since Q4 2022, transaction value of residential properties totalled €2.15bln, of which €1.6bln (76%) was for the premium end of the market. It is worth noting that €1.25bln related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €800k and €313k for apartments in Q4 2023. Compared to Q4 2022, median prices of houses remained almost staple and for apartment decreased by 10.7%.

KEY INDICATORS

LIMASSOL

Value Q3 ‘23 Volume Q3 ‘23 Value Q3 ‘22 - Q3 ‘23 Volume Q3 ‘22 - Q3 ‘23 Residential €256m 700 €2,145m 5,243 Houses €89m 240 €717m 1,691 Apartments €167m 460 €1,428m 3,552 Premium €181m 322 €1,630m 2,723 Houses €41m 41 €377m 346 Apartments €140m 281 €1,253m 2,377

2023

• There have been 26,158 transactions, 8,510 of houses and 17,648 of apartments. Of these, 10,968 (42%) were at the premium end of the market.

• Total transaction value for residential properties stood at €10,6bln of which €7,9bln (75%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 83% of houses under €500k and 46% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for apartments).

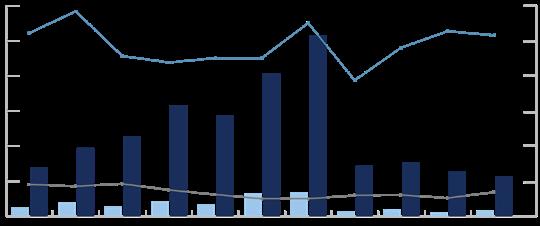

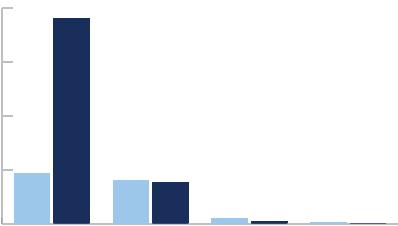

VOLUME AND MEDIAN PRICES OF

PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

Apartments

LIMASSOL

SINCE Q1 2016

€0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ €200 000 0 500 1000 1500 2000 €400 000 €600 000 €800 000 €1 000 000 €1 200 000 NUMBER OF TRANSACTIONS VOLUME MEDIAN PRICES NUMBER OF TRANSACTIONS Transaction

> € 200k Apartments

> € 500k

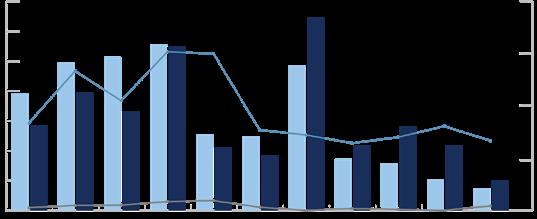

2572 355 893 646 1338 196 299 144 74 7253 3471 4787 740 1723 456 1211 2000 0 6000 8000 4000 900 1500 1200 300 600 0 Q1 - Q4 2023 2016 - 2022 Apartments Houses Apartments Houses 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023

Volume of

Transaction Volume of

Houses Median Prices of > € 500k Houses Median Prices of > € 200k

PAFOS

Pafos is the cultural capital of the island, a city of villas and low-rise buildings, It has traditionally been popular with foreign buyers.

Residential transactions totalled 440 in Q4 2023, of which 20% (87 properties) were of the premium segment of the market.

Premium residential properties are of particularly high demand in Paphos, indicated by the high percentage of houses (37 properties, 33% of the total for Cyprus) and apartments (50 properties, 10% of the total for Cyprus) transacted over the past quarter.

Since Q4 2022, transaction value of residential properties totalled €1.064bl, of which €508m (48%) was for the premium end of the market. It’s worth noting that €320m related to houses, as this in the main premium product of the district.

The median transaction price for premium houses was €700k and €325k for apartments in Q4 2023. Compared to Q4 2022, median prices of houses decreased by 3%, and increased by 7% for apartments.

KEY INDICATORS

2023

PAFOS

Value Q3 ‘23 Volume Q3 ‘23 Value Q3 ‘22 - Q3 ‘23 Volume Q3‘22 -Q3 ‘23 Residential €120m 440 €1,064m 4,128 Houses €79m 228 €693m 1,871 Apartments €42m 212 €371m 2,257 Premium €58m 87 €508m 860 Houses €34m 37 €320m 338 Apartments €24m 50 €188m 522

• There have been 19,623 transactions, 9,408 of houses and 10,215 of apartments. Of these, 3,435 (18%) were at the premium end of the market showing the district’s appeal as a destination for more affluent buyers.

• Total transaction value for residential properties stood at €5.4bln of which €2.9bln (54%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 82% of houses under €500k and 83% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for houses).

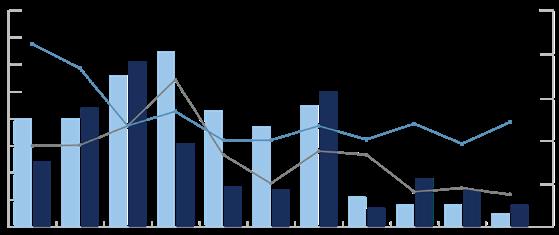

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

Transaction Volume of > €

Apartments

Transaction Volume of

Houses

Median Prices of > € 200k Apartments

Houses

PAFOS

Q1

SINCE

2016

200k

> € 500k

€ 500k

Median Prices of >

€0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ 3202 526 1340 569 370 205 30 49 8 7167 3294 1042 807 199 666 59 1000 0 6000 5000 4000 3000 2000 7000 8000 0 300 600 900 1200 1500 Q1 - Q4 2023 2016 - 2022 0 50 100 150 200 250 300 350 €300 000 €600 000 €900 000 €1 200 000 €1 500 000 Apartments Houses Apartments Houses VOLUME MEDIAN PRICES NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023

NICOSIA

Nicosia, the capital of Cyprus, is a unique and attractive place. Commercial and long-term rental properties drive the market here.

Residential transactions totalled 803 in Q4 2023, of which 16% (127 properties) were of the premium segment of the market.

Premium residential properties are of particularly medium demand in Nicosia, indicated by the percentage of houses (15 properties, 13% of the total for Cyprus) and apartments (112 properties, 21% of the total for Cyprus) transacted over the past quarter.

Since Q4 2022, transaction value of residential properties totalled €808m, of which €279m (35%) was for the premium end of the market. It is worth noting that €213m related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €715k and €269k for apartments in Q4 2023. Compared to Q4 2022, median prices decreased by almost 36.7% of houses and increased by 8.2% for apartments.

KEY INDICATORS

2023

NICOSIA

Value Q3 ‘23 Volume Q3 ‘23 Value Q3‘22 - Q3 ‘23 Volume Q3 ‘22 - Q3 ‘23 Residential €151m 803 €808m 4,247 Houses €51m 200 €279m 1,074 Apartments €100m 603 €529m 3,173 Premium €49m 127 €279m 747 Houses €11m 15 €66m 75 Apartments €38m 112 €213m 672

• There have been 21,725 transactions, 5,749 of houses and 15,976 of apartments. Of these, 2,981 (14%) were at the premium end of the market.

• Total transaction value for residential properties stood at €3,9bln of which €1,2bln (31%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 94% of houses under €500k and 84% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium end of the market (particularly for apartments).

VOLUME AND MEDIAN PRICES

HOUSES AND APARTMENTS

1500 NICOSIA

Q1 - Q4 2023 2016 - 2022

Q1

TRANSACTIONS’ PRICE DISTRIBUTION

SINCE

2016

PREMIUM

€0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ 2148 11372 2460 1813 243 209 56 66 373 1978 411 481 49 9 48 7 Transaction Volume of > € 200k Apartments Transaction Volume of > € 500k Houses Median Prices of > € 500k Houses Median Prices of > € 200k Apartments 2000 0 0 4000 6000 500 8000 10000 12000 1000 2000 0 100 200 300 400 500 600 €200 000 €300 000 €400 000 €500 000 €600 000 €700 000 €800 000 VOLUME MEDIAN PRICES NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS Apartments Houses Apartments Houses 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023

OF

LARNACA

Larnaca is one of the oldest cities in Cyprus with lots of history and class, yet the recent years’ development gave it a modern sparkle, and the best is yet to come.

Residential transactions totalled 617 in Q4 2023, of which only 14% (88 properties) were of the premium segment of the market.

Premium residential properties are considered to be of low demand in Larnaca, indicated by the percentage of houses (14 properties, 13% of the total for Cyprus) and apartments (74 properties, 14% of the total for Cyprus) transacted over the past quarter.

Since Q4 2022, transaction value of residential properties totalled €706m, of which €203m (29%) was for the premium segment of the market. It is worth noting that €141m related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €995k and for apartments €251k, in Q4 2023. Compared to Q4 2022, median prices of houses increased by 24.4%, while for apartments decreased by 16%.

KEY INDICATORS

2023

LARNACA

Value Q3 ‘23 Volume Q3 ‘23 Value Q3 ‘22 - Q3 ‘23 Volume Q3 ‘22 - Q3 ‘23 Residential €115m 617 €706m 3,992 Houses €53m 201 €277m 1,140 Apartments €61m 416 €429m 2,852 Premium €35m 88 €203m 547 Houses €14m 14 €61m 69 Apartments €21m 74 €142m 478

• There have been 16,986 transactions, 5,350 of houses and 11,636 of apartments. Of these, 1,946 (11%) were at the premium end of the market.

• Total transaction value for residential properties stood at €2.97bln of which €982m (33%) were for the premium end of the market.

• The overall breakdown of residential transactions across the market was 94% of houses under €500k and 86% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for high-end apartments).

VOLUME AND MEDIAN PRICES

TRANSACTIONS’ PRICE DISTRIBUTION

LARNACA

Q1 2016

SINCE

OF PREMIUM HOUSES

500 0 1000 1500 2000 €0-200k €200-500k €500k-1m €1m+ 461 1907 398 378 49 20 14 2 €0-200k 2000 8000 10000 0 4000 6000 €200-500k €500k-1m €1m+ 2479 8118 1677 984 193 79 140 87 Transaction Volume of > € 200k Apartments Transaction Volume of > € 500k Houses Median Prices of > € 500k Houses Median Prices of > € 200k Apartments 0 50 100 150 200 250 300 €200 000 €400 000 €600 000 €800 000 €1 000 000 €1 200 000 Q1 - Q4 2023 2016 - 2022 NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS Apartments Houses Apartments Houses VOLUME MEDIAN PRICES 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023

AND APARTMENTS

FAMAGUSTA

APARTMENT PRICES REMAINED STABLE

The Eastern part of Cyprus is a famous tourist destination. With the vibrant Ayia Napa and quiet Protaras, this area offers mostly holiday oriented properties.

Residential transactions totalled 198 in Q4 2023, of which 7% (13 properties) were of the premium segment of the market.

Premium residential properties are of particularly low demand in Famagusta, indicated by the low percentage of houses (5 properties, only 7% of the total for Cyprus) and apartments (8 properties, only 2% of the total for Cyprus) transacted over the past quarter.

Since Q4 2022, transaction value of residential properties totalled €234m, of which €66m (28%) was for the premium end of the market. It is worth noting that €43m related to houses, as this is the main premium product of the district.

The median transaction price for premium houses was €725k and €223k for apartments in Q4 2023. Compared to Q4 2022, median prices of houses and apartments decreased by 8% and 54% respectively.

KEY INDICATORS

2023

FAMAGUSTA

Value Q3 ‘23 Volume Q3 ‘23 Value Q3 ‘22 - Q3 ‘23 Volume Q3 ‘22 - Q3 ‘23 Residential €35m 198 €234m 1,098 Houses €23m 101 €158m 536 Apartments €11m 97 €76m 562 Premium €6m 13 €66m 104 Houses €4m 5 €43m 47 Apartments €2m 8 €22m 57

• There have been 5,772 transactions, 2,782 of houses and 2,990 of apartments. Of these, 644 (11%) were at the premium end of the market.

• Total transaction value for residential properties stood at €1.44bln of which €609m (42%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 87% of houses under €500k and 90% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for high-end houses).

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

Transaction Volume of > € 200k Apartments

Transaction Volume of > € 500k Houses

Median Prices of > € 200k Apartments

Median Prices of > € 500k Houses

FAMAGUSTA

SINCE Q1 2016

€0-200k 500 0 1000 1500 2000 2500 €200-500k €500k-1m €1m+ 871 2323 1179 104 210 79 115 79 272 164 29 18 4 3 2 46 0 100 200 300 400 500 €0-200k €200-500k €500k-1m €1m+ 0 10 20 30 40 50 60 70 80 0 €300 000 €600 000 €900 000 €1 200 000 €1 500 000 Q1 - Q4 2023 2016 - 2022 NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS Apartments Houses Apartments Houses VOLUME MEDIAN PRICES 2016 2017 2018 2019 2020 2021 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023

Two Bedroom Luxury House in Minthis Golf Resort

This lovely two-bedroom villa with breathtaking views of the mountains, greets you with a generously proportioned flowing open-plan layout living space featuring a dining area and two bedrooms, all filled with natural light through floor-toceiling windows. The villa has expansive verandas that add to the overall tranquility and create cozy shaded areas for outdoor entertaining.

€ 850.000 + VAT

PROJECTS

Registration No.: 1013 | License No.: 517/E.

CYPRUS

© 2024 Cyprus Sotheby’s International Realty. All rights reserved. Cyprus Sotheby’s International Realty® and the Sotheby’s International Realty Logo are service marks licensed to Sotheby’s International Realty Affiliates LLC and used with permission. ONE Sotheby’s International Realty fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each franchise is independently owned and operated. Any services or products provided by independently owned and operated franchisees are not provided by, affiliated with or related to Sotheby’s International Realty Affiliates LLC nor any of its affiliated companies. The information contained herein is deemed accurate but not guaranteed.

Data provided by Cyprus’ Department of Lands and Surveys; data processing and analysis carried out by WiRE (Wire Services Ltd, Wire Wind Ltd, and Wire Valuations LLC, collectively WiRE). Cyprus Sotheby’s International Realty and WiRE make no representations or warranties concerning the report or the content and disclaim all such representations and warranties as to the condition, quality, accuracy, suitability, fitness for purpose, or completeness. Nothing in this report shall be regarded as providing financial advice, and you acknowledge that the content of this presentation is not suitable for this purpose. Neither Cyprus Sotheby’s International Realty or WiRE nor any of their directors, employees, or other representatives will be liable for damages arising from or in connection with the use of this report. This is a comprehensive limitation of liability that applies to all damages of any kind, including (without limitation) compensatory, direct, indirect, or consequential damages, loss of data, income or profit, loss of or property damage, and claims of third parties. All material in this report is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in this report constitutes professional and/or financial advice, nor does any information include a comprehensive or complete statement of the matters discussed or the law relating thereto. Information in this report may not be accurate or current. In particular (but without limitation), information may be rendered inaccurate by changes in applicable laws and other regulations. No action should be taken or omitted to be taken in reliance upon data in this report.