LOCAL EXPERTISE WITH A GLOBAL PERSPECTIVE

Welcome to the quarterly residential market report for Q1 2024, providing insights into the Cyprus residential real estate landscape.

In this report, we delve into the details of residential property transactions, with a particular focus on property value and price distribution. The term “premium properties” refers to apartments priced above €200,000 and houses above €500,000.

Even though the figures of this period show us a decline in both value and volume of sales, we should consider it in the context of the previous years' steep climb up.

In the last two years (2022-2023) the market was super dynamic due to the geopolitical tension, primarily influenced by the ongoing geopolitical situation that led many families and businesses to relocate to safer countries like Cyprus.

The current situation on the real estate market shows levelling out to the statistics similar to 2021. The figures for Q1 2024 are definitely lower than in 2023, but that was expected as the market stabilises after a strong growth in 2022 and 2023.

We have a moderate outlook for the property market for 2024 and expect a stable demand for residential property from both local and international buyers supported by traditional Cyprus market drivers such as attractive lifestyle and business opportunities with a sunny climate, safety, reasonable cost of living, favourable tax system, the island’s prospects as an international business centre and one of the top investment destinations in Europe.

As we navigate the Cyprus real estate market into 2024, it’s crucial to consider these trends and insights for informed decision-making.

As a company, we continue to have a strong presence in all regions of the island, share our expertise in numerous online and offline events, and support our partners and clients in our common goal of making Cyprus a perfect place for life, business, and well-being.

For personalized assistance and expert guidance in your property searches, you can trust Cyprus Sotheby’s International Realty, a global brand with a local perspective.

With gratitude,

Anastasia Yianni Chief Executive Officer

Anastasia Yianni Chief Executive Officer

Cyprus

Sotheby’s International RealtyABOUT INSIGHTS:

Transaction data are provided by Cyprus’ Department of Lands and Surveys, which records all transfers of ownership and registered contracts of sale (including property description, purchase price, date, etc). The data is processed in order to classify each transaction (as some properties are under construction, their description is not exact, or they form part of bigger projects) and are categorised by property type.

The analysis covers the entire area controlled by the Republic of Cyprus, excludes properties sold at auction (foreclosure), and references property values based on the amount declared by the purchaser at the time of the transaction (which excludes any VAT, transfer fees, or other duties levied).

THE REAL ESTATE MARKET

IN CYPRUS

KEY HIGHLIGHTS

• According to the Cyprus Land Registry, for the first quarter of 2024, the number of sales contracts reached 2,456 with a total value of 585 million euros.

• In the first quarter of 2024, the high-end property market in Cyprus recorded 659 transactions, representing 27% of all deals within this reported period. The total value of these high-end properties reached €290 million, accounting for 49% of the overall market value.

• During this period, the high-end apartment segment recorded 550 transactions, amounting to €190.5 million. The premium housing segment resulted in 109 deals, with a total value of approximately €100 million.

• In Limassol, in Q1 2024, the market registered 635 residential property transactions, 51% (322 properties) of which were from the high-end segment, indicating particularly great demand for premium residential properties in this region. High demand was reported for apartments priced above EUR 200k, with 283 transactions accounting for 51% of the total in Cyprus, and for houses priced above EUR 500k, with 39 transactions representing 36% of the total for Cyprus during the past quarter.

• In Q1 2024, Pafos recorded 469 residential property transactions, with 22% (102 properties) in the high-end segment, underscoring the sustained demand for premium residential properties. During this period, 37 houses priced above EUR 500k were sold, making up 34% of such sales in Cyprus, and 65 apartments priced above EUR 200k were sold, accounting for 12% of the total in Cyprus.

• In Nicosia, in Q1 2024, the residential transactions totaled 705 deals, with 19% (136 properties) in the high-end market segment. The demand for premium residential properties in Nicosia is moderate, as reflected in the sales of 15 houses (14% of the total in Cyprus) and 121 apartments (22% of the total in Cyprus) during the past quarter.

Q1 2024

• In Larnaca, residential transactions totaled 532 in Q1 2024, with only 15% (81 properties) falling into the premium market segment.

• The emerging demand for premium residential properties in Larnaca is reflected in the sale of 10 houses priced above EUR 500k (9% of the total for Cyprus) and 71 apartments priced above EUR 200k (13% of the total for Cyprus) during the reported period.

• In Famagusta, in Q1 2024, the market registered 115 residential property transactions, of which 16% (18 properties) were under the high-end segment.

• The demand for premium residential properties in Famagusta shows potential for growth, as reported by 8 houses (7% of Cyprus's total) and 10 apartments (2% of Cyprus's total) being sold in the premium category over the last quarter.

CYPRUS

RESIDENTIAL PROPERTY SALES DISTRIBUTION PER REGION

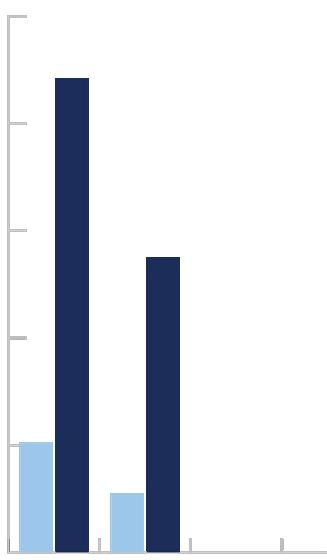

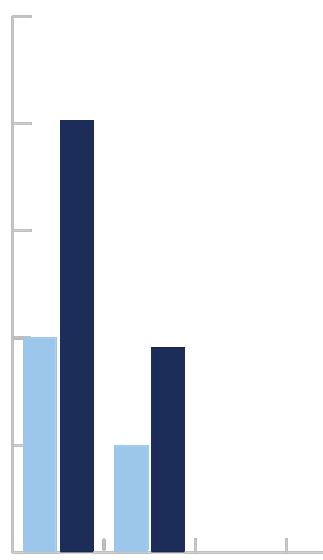

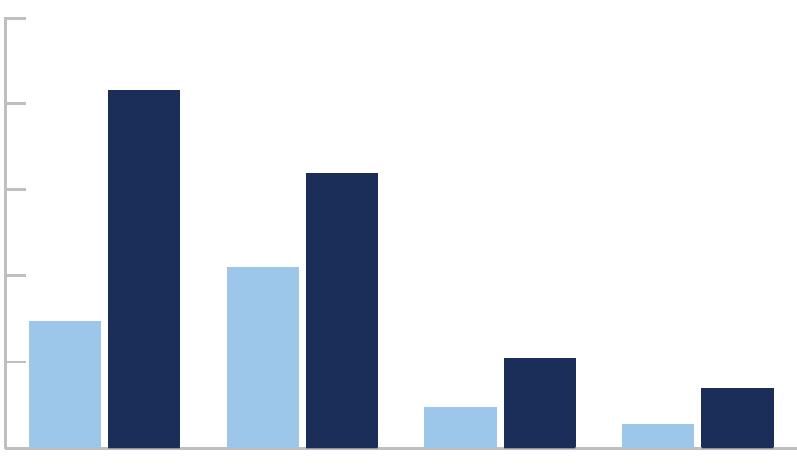

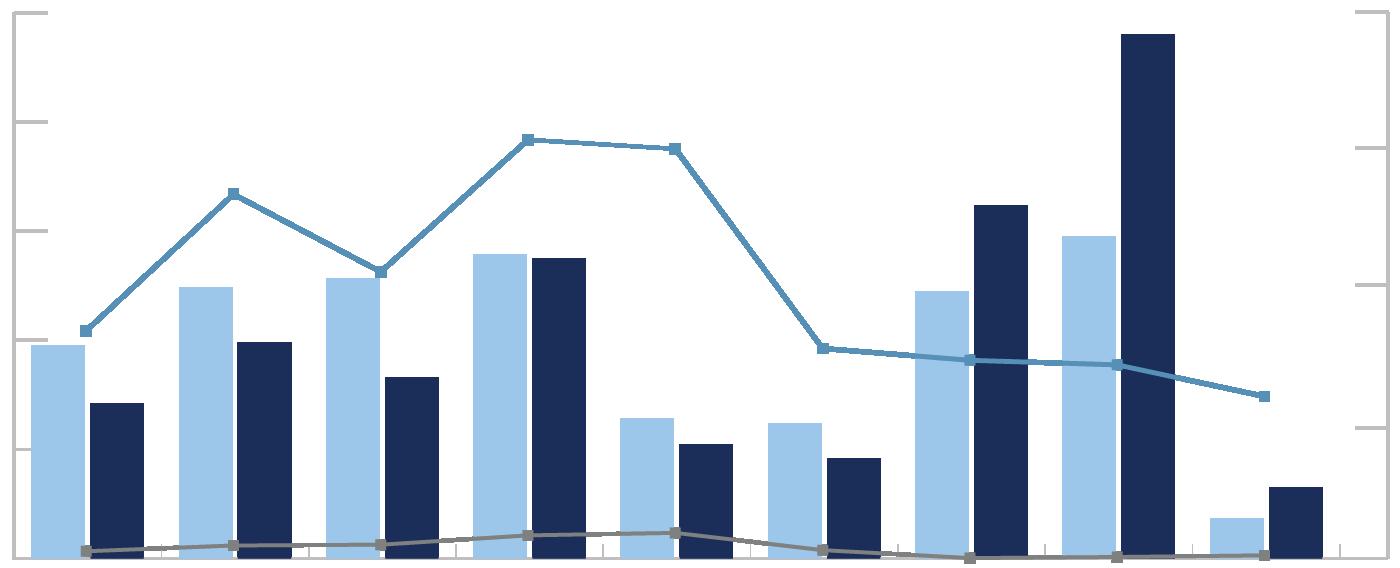

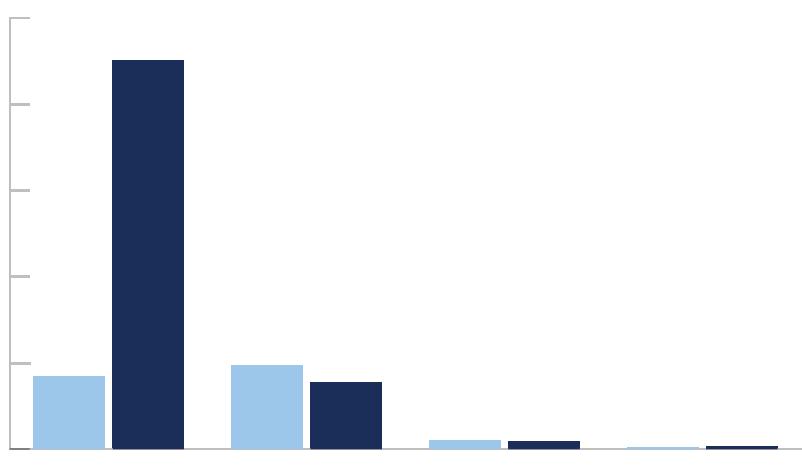

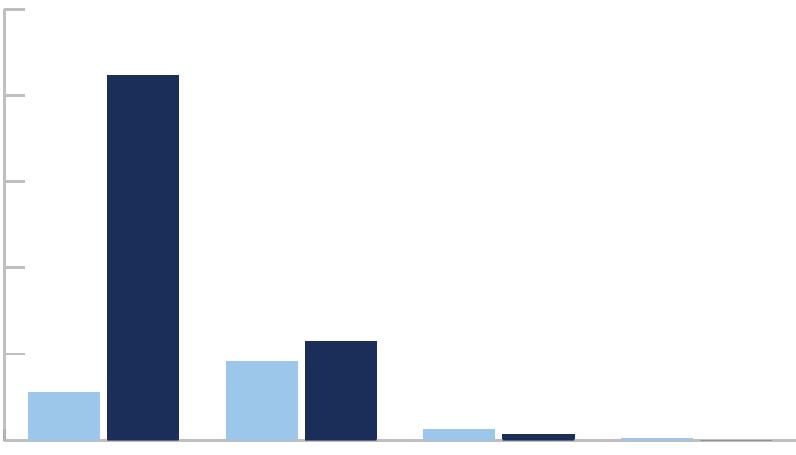

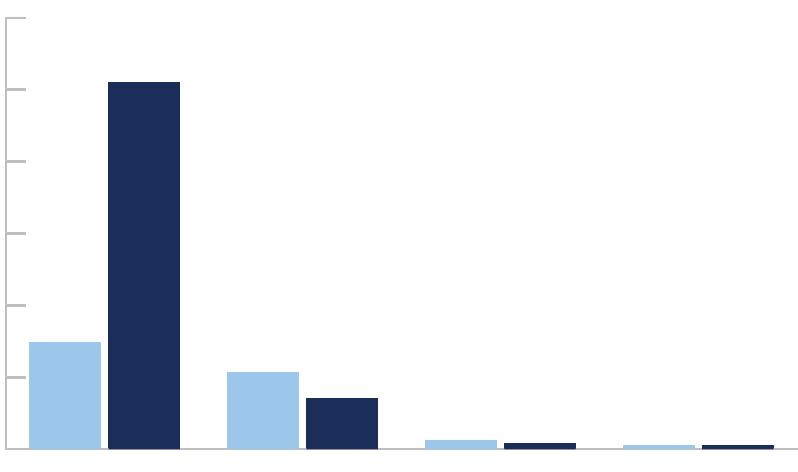

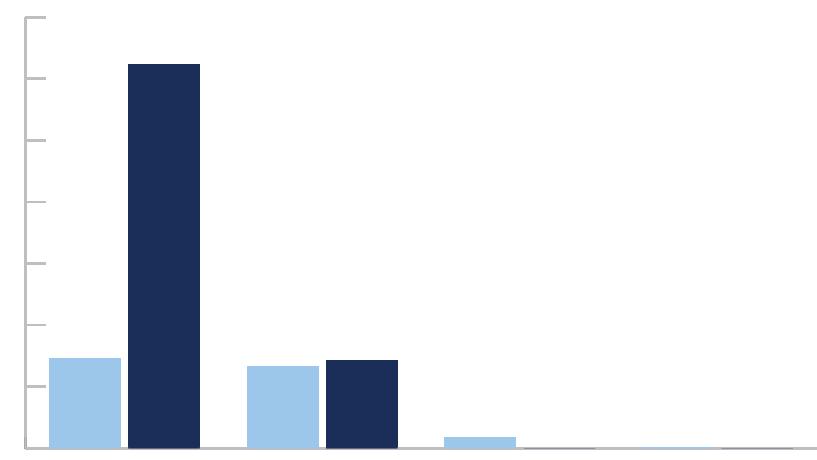

VOLUME OF PREMIUM HOUSES & APARTMENTS

CYPRUS

CYPRUS 3608 1075 1492 1937 2105 1248 1649 3127 550 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024 422 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024 569 583 358 414 598 626 759 109 VOLUME VOLUME VOLUME OF PREMIUM RESIDENTIAL PROPERTIES BY DISTRICT Q1 2024 PREMIUM HOUSES PREMIUM HOUSES PREMIUM APARTMENTS PREMIUM APARTMENTS

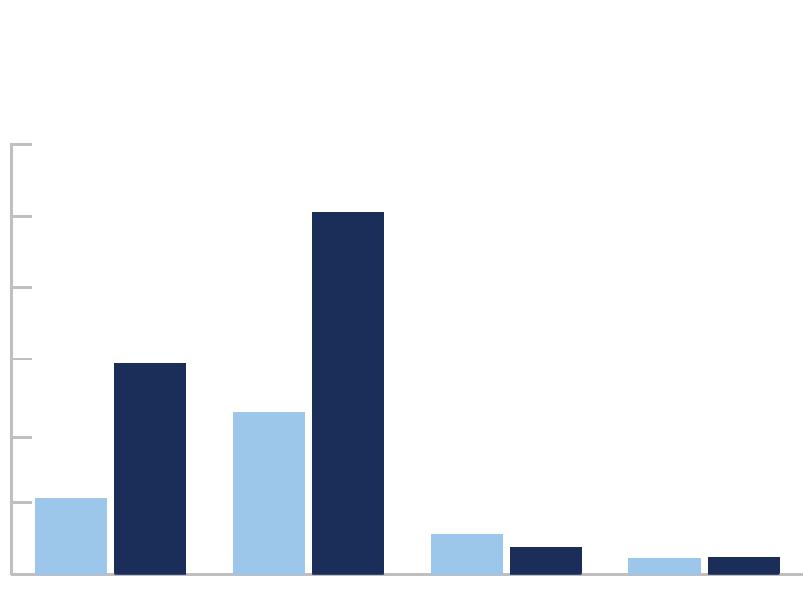

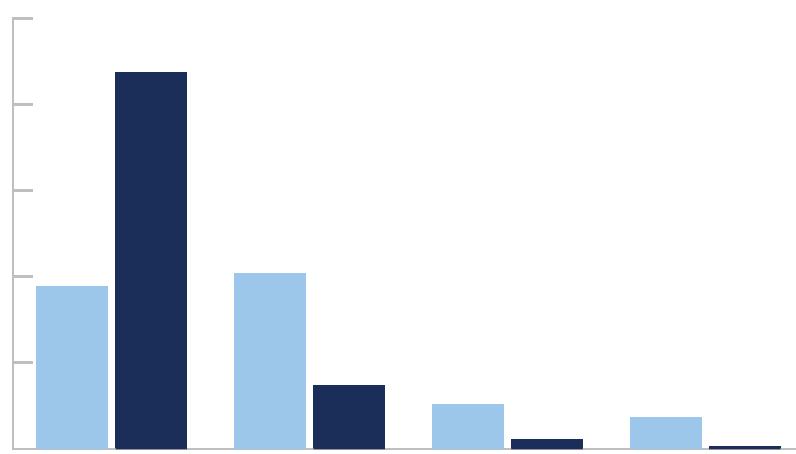

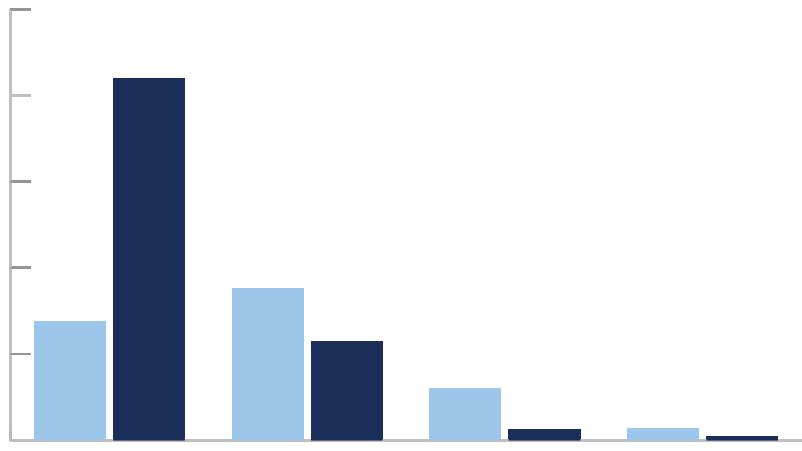

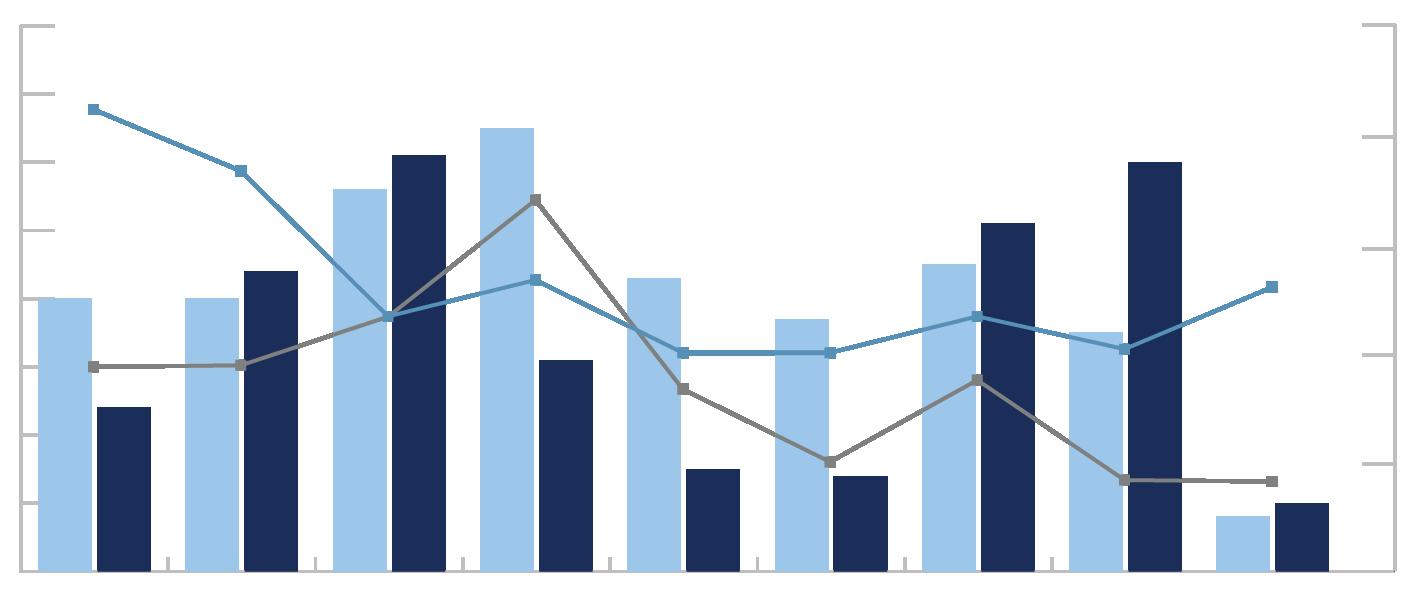

Pafos Larnaca Nicosia Famagusta 13% 2% 16% 56% 13% 528 70 684 2331 545 38% 9% 9% 5% 38% 334 81 78 43 332 1000 500mln

VOLUME OF PREMIMUM PROPERTIES

Limassol

TRANSACTION

VALUE OF PREMIUM PROPERTIES

Houses Q1 2023 Q1 2024 0 200 400 600 800 0 100mln 200mln 300mln 400mln Q1 2023 Q1 2024

Apartments Houses TRANSACTION

Apartments

2 Bedroom Villa in Tsada

Discover a stunning two-bedroom villa nestled in the renowned Minthis golf resort, just moments from Pafos. With panoramic mountain vistas, this property boasts a spacious open-plan layout flooded with natural light. Enjoy modern living with an immaculate kitchen, outdoor entertaining space, and a refreshing plunge pool. Retreat to the serene master suite with a contemporary en-suite. Expansive verandas offer tranquil outdoor living.

With flexible payment options available, make this your dream Mediterranean home and savvy investment today.

PROJECTS

Available for sale € 850.000 + VAT Bedrooms 2 2 176 m2 10 m2 166 m2 388 m2 Covered Bathrooms Covered Area Covered Verandas Internal Area Plot Area Parking

Paphos

LIMASSOL

Limassol is the business capital of Cyprus and a city of skyscrapers. Relocated international companies are the driving force behind the constant real estate growth in the city.

Residential transactions totalled 635 in Q1 2024, of which 51% (322 properties) were of the premium segment of the market.

Premium residential properties are of particularly high demand in Limassol, indicated by the high percentage of houses (39 properties, 36% of the total for Cyprus) and apartments (283 properties, 51% of the total for Cyprus) transacted over the past quarter.

Since Q1 2023, transaction value of residential properties totalled €2.00bln, of which €1.51bln (75%) was for the premium end of the market. It is worth noting that €1.15bln related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €740k and €297k for apartments in Q1 2024. Compared to Q1 2023, median prices of houses and for apartments decreased by 4.6% and 14.2% respectively.

KEY INDICATORS

LIMASSOL

2024 Value Q1 ‘24 Volume Q1 ‘24 Value Q1 ‘23 - Q1 ‘24 Volume Q1 ‘23 - Q1 ‘24 Residential €217m 635 €2,002m 5,075 Houses €86m 205 €675m 1,589 Apartments €131m 430 €1,327m 3,486 Premium €151m 322 €1,506m 2,665 Houses €42m 39 €352m 334 Apartments €109m 283 €1,154m 2,331

• There have been 27,408 transactions, 8,842 of houses and 18,566 of apartments. Of these, 11,324 (42%) were at the premium end of the market.

• Total transaction value for residential properties stood at €11,1bln of which €8.2bln (74%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 83% of houses under €500k and 46% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for apartments).

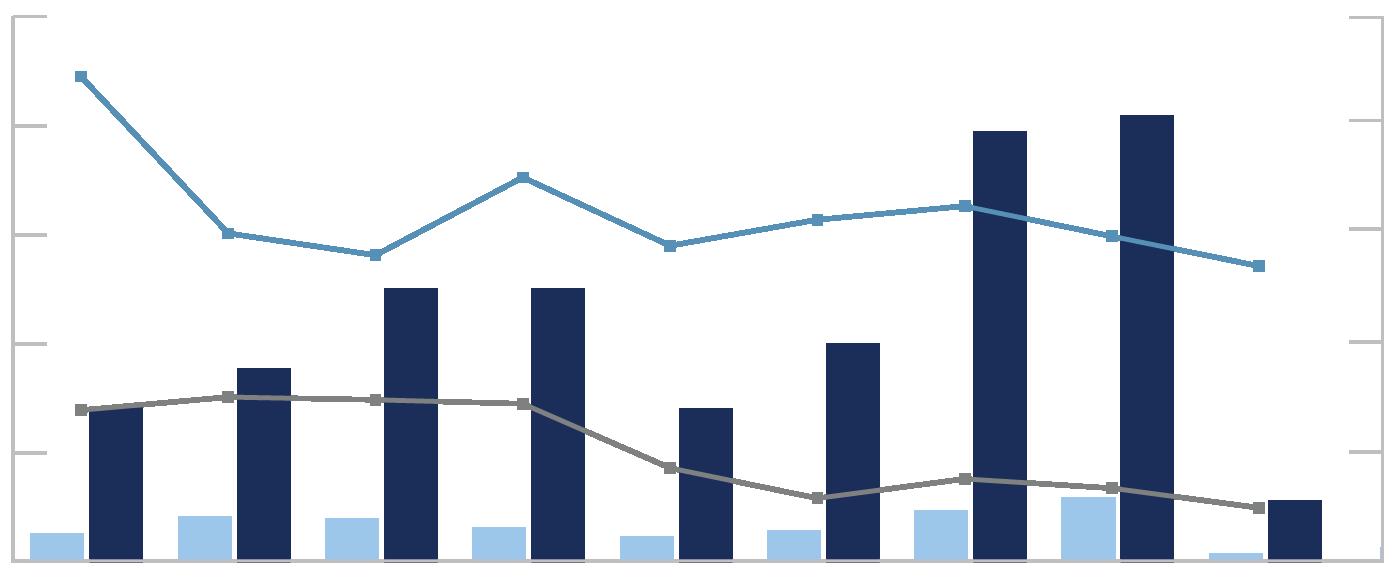

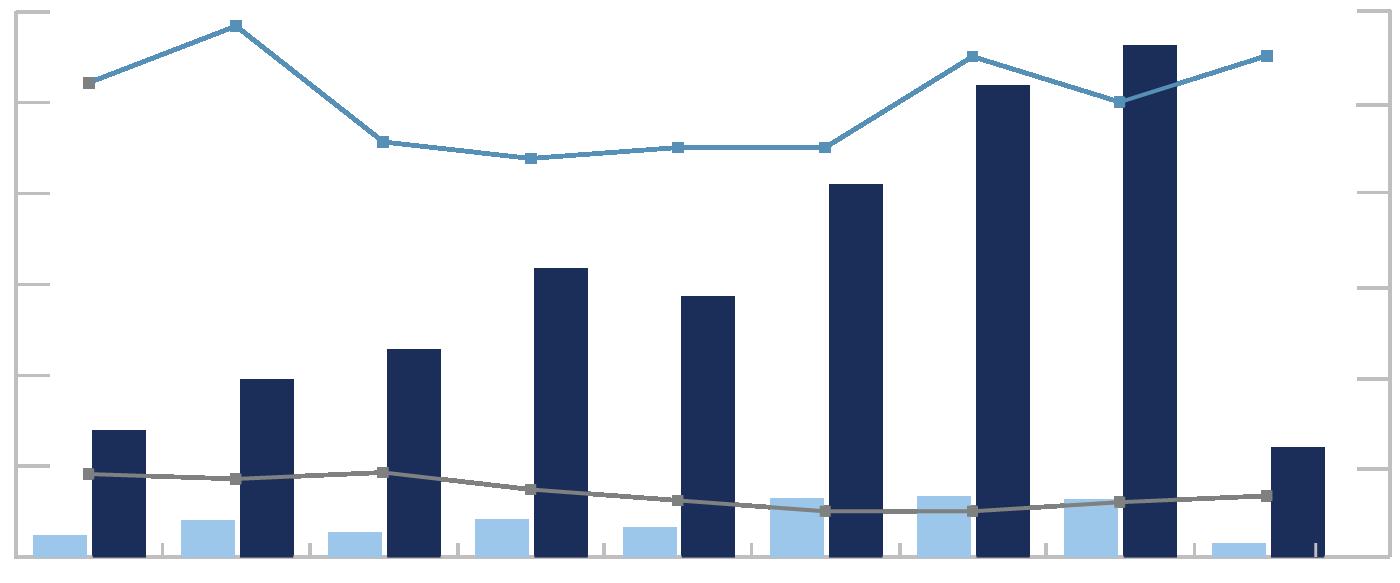

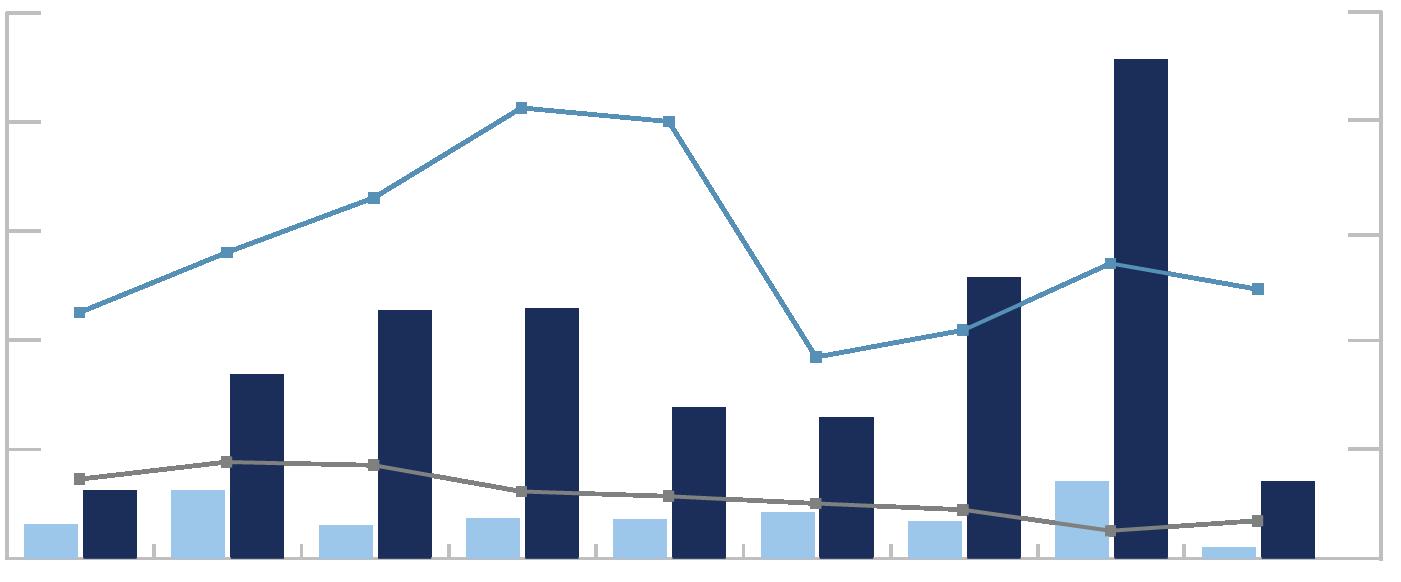

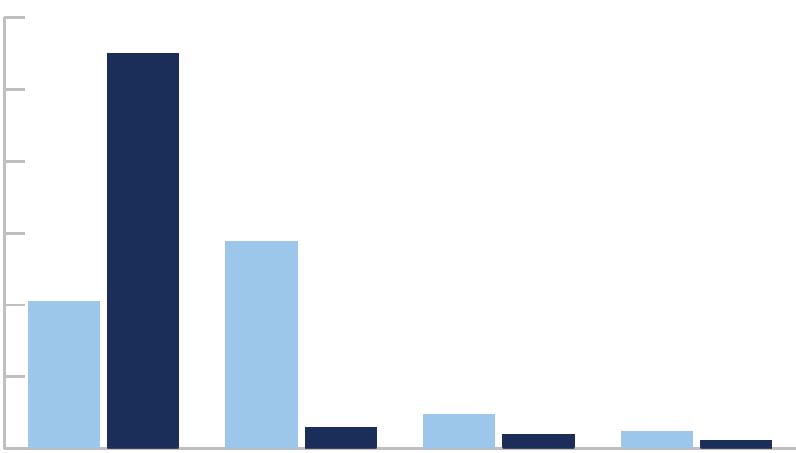

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

Houses Median Prices of > € 200k Apartments

LIMASSOL

SINCE Q1 2016

€0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ €200 000 0 500 1000 1500 2000 2500 €400 000 €600 000 €800 000 €1 000 000 €1 200 000 NUMBER OF TRANSACTIONS VOLUME MEDIAN PRICES NUMBER OF TRANSACTIONS

> € 200k

500k

2948 53 147 113 252 28 19 12 11 8305 4196 6374 951 2077 542 1380 2k 0 6k 8k 10k 4k 150 250 300 200 50 100 0 Q1 2024 2016 - 2023 Apartments Houses Apartments Houses 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024

Transaction Volume of

Apartments Transaction Volume of > €

Houses Median Prices of > € 500k

PAFOS

Pafos is the cultural capital of the island, a city of villas and low-rise buildings. It has traditionally been popular with foreign buyers.

Residential transactions totalled 469 in Q1 2024, of which 22% (102 properties) were of the premium segment of the market.

Premium residential properties are of particularly high demand in Pafos, indicated by the high percentage of houses (37 properties, 34% of the total for Cyprus) and apartments (65 properties, 12% of the total for Cyprus) transacted over the past quarter.

Since Q1 2023, transaction value of residential properties totalled €1.059bln, of which €501m (47%) was for the premium end of the market. It’s worth noting that €308m related to houses, as this in the main premium product of the district.

The median transaction price for premium houses was €655k and €306k for apartments in Q1 2024. Compared to Q1 2023, median prices of houses decreased by 4.4%, and 1.3% for apartments.

PAFOS

KEY

2024

INDICATORS

Value Q1 ‘23 Volume Q1 ‘23 Value Q1 ‘23 - Q1 ‘24 Volume Q1 ‘23 - Q1 ‘24 Residential €117m 469 €1,059m 4,147 Houses €70m 194 €675m 1,829 Apartments €47m 275 €384m 2,318 Premium €55m 102 €501m 877 Houses €32m 37 €308m 332 Apartments €23m 65 €194m 545

SINCE

• There have been 20,603 transactions, 9,809 of houses and 10,794 of apartments. Of these, 3,655 (18%) were at the premium end of the market showing the district’s appeal as a destination for more affluent buyers.

• Total transaction value for residential properties stood at €5.6bln of which €3.0bln (54%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 82% of houses under €500k and 83% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for houses).

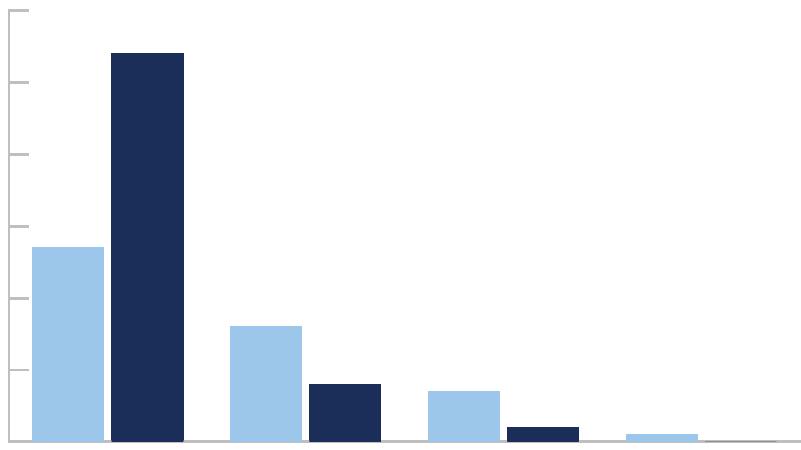

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

Transaction Volume of > € 200k Apartments

Transaction Volume of > € 500k Houses

Median Prices of > € 200k Apartments

Median Prices of > € 500k Houses

PAFOS

Q1

2016

€0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ 3778 69 210 88 57 30 6 7 2 8737 4066 1483 1044 231 727 68 0 6k 4k 2k 8k 10k 0 50 100 150 200 250 Q1 2024 2016 - 2023 0 100 200 300 400 500 €300 000 €600 000 €900 000 €1 200 000 €1 500 000 Apartments Houses Apartments Houses VOLUME MEDIAN PRICES NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024

NICOSIA

Nicosia, the capital of Cyprus, is a unique and attractive place. Commercial and long-term rental properties drive the market here.

Residential transactions totalled 705 in Q1 2024, of which 19% (136 properties) were of the premium segment of the market.

Premium residential properties are of particularly medium demand in Nicosia, indicated by the percentage of houses (15 properties, 14% of the total for Cyprus) and apartments (121 properties, 22% of the total for Cyprus) transacted over the past quarter.

Since Q1 2023, transaction value of residential properties totalled €807m, of which €277m (34%) was for the premium end of the market. It is worth noting that €217m related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €751k and €267k for apartments in Q1 2024. Compared to Q1 2023, median prices increased by almost 15.4% for houses and decreased by 16.0% for apartments.

KEY INDICATORS

NICOSIA

2024 Value Q1 ‘24 Volume Q1 ‘24 Value Q1‘23 - Q1 ‘24 Volume Q1 ‘23 - Q1 ‘24 Residential €133m 705 €807m 4,257 Houses €43m 161 €269m 1,047 Apartments €90m 544 €538m 3,210 Premium €47m 136 €277m 762 Houses €11m 15 €60m 78 Apartments €36m 121 €217m 684

• There have been 22,686 transactions, 5,966 of houses and 16,720 of apartments. Of these, 3,156 (14%) were at the premium end of the market.

• Total transaction value for residential properties stood at €4,07bln of which €1,28bln (31%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 94% of houses under €500k and 83% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium end of the market (particularly for apartments).

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

- 2023

300 NICOSIA

Q1 2024

2016

SINCE Q1 2016

€0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ 2534 13517 2910 2325 297 262 64 72 55 423 91 114 13 2 7 0 Transaction Volume of > € 200k Apartments Transaction Volume of > € 500k Houses Median Prices of > € 500k Houses Median Prices of > € 200k Apartments 3k 0 0 6k 100 9k 12k 15k 200 400 500 0 100 200 300 400 500 600 €200 000 €300 000 €400 000 €500 000 €600 000 €700 000 €800 000 VOLUME MEDIAN PRICES NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS Apartments Houses Apartments Houses 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024

LARNACA

Larnaca is one of the oldest cities in Cyprus with lots of history and class, yet the recent years’ development gave it a modern sparkle, and the best is yet to come.

Residential transactions totalled 532 in Q1 2024, of which only 15% (81 properties) were of the premium segment of the market.

Premium residential properties are considered to be of low demand in Larnaca, indicated by the percentage of houses (10 properties, 9% of the total for Cyprus) and apartments (71 properties, 13% of the total for Cyprus) transacted over the past quarter.

Since Q1 2023, transaction value of residential properties totalled €733m, of which €226m (31%) was for the premium segment of the market. It is worth noting that €157m related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €693k and for apartments €269k, in Q1 2024. Compared to Q1 2023, median prices of houses increased by 14.5%, while for apartments decreased by 11%.

KEY INDICATORS

LARNACA

Value Q1 ‘23 Volume Q1 ‘23 Value Q1 ‘23 - Q1 ‘24 Volume Q1 ‘23 - Q1 ‘24 Residential €93m 532 €733m 4,048 Houses €36m 149 €285m 1,142 Apartments €58m 383 €448m 2,906 Premium €27m 81 €226m 609 Houses €8m 10 €69m 81 Apartments €19m 71 €157m 528

2024

• There have been 17,858 transactions, 5,590 of houses and 12,268 of apartments. Of these, 2,093 (12%) were at the premium end of the market.

• Total transaction value for residential properties stood at €3.14bln of which €1.03bln (33%) were for the premium end of the market.

• The overall breakdown of residential transactions across the market was 94% of houses under €500k and 86% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for high-end apartments).

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS Transaction Volume of > €

TRANSACTIONS’ PRICE DISTRIBUTION SINCE

Apartments

Apartments

LARNACA

Q1 2016

200k

500k

> € 500k

200k

0 100 200 300 400 500 €200 000 €400 000 €600 000 €800 000 €1 000 000 €1 200 000 VOLUME MEDIAN PRICES 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024 €0-200k €0-200k €200-500k €200-500k €500k-1m €500k-1m €1m+ €1m+ NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS 2964 73 312 66 71 9 0 0 1 10216 2134 1413 248 166 95 90 2k 0 6k 8k 10k 12k 4k 150 250 300 350 200 50 100 0 Q1 2024 2016 - 2023 Apartments Houses Apartments Houses

Transaction Volume of > €

Houses Median Prices of

Houses Median Prices of > €

FAMAGUSTA

The Eastern part of Cyprus is a famous tourist destination. With the vibrant Ayia Napa and quiet Protaras, this area offers mostly holiday oriented properties.

Residential transactions totalled 115 in Q1 2024, of which 16% (18 properties) were of the premium segment of the market.

Premium residential properties are of particularly low demand in Famagusta, indicated by the low percentage of houses (8 properties, only 7% of the total for Cyprus) and apartments (10 properties, only 2% of the total for Cyprus) transacted over the past quarter.

Since Q1 2023, transaction value of residential properties totalled €222m, of which €69m (31%) was for the premium end of the market. It is worth noting that €41m related to houses, as this is the main premium product of the district.

The median transaction price for premium houses was €780k and €246k for apartments in Q1 2024. Compared to Q1 2023, median prices of houses increased by 29% and for apartments decreased by 51%.

KEY INDICATORS

FAMAGUSTA

2024 Value Q1 ‘23 Volume Q1 ‘23 Value Q1 ‘23 - Q1 ‘24 Volume Q1 ‘23 - Q1 ‘24 Residential €25m 115 €222m 1,050 Houses €15m 51 €142m 489 Apartments €10m 64 €81m 561 Premium €10m 18 €69m 113 Houses €7m 8 €41m 43 Apartments €3m 10 €28m 70

SINCE

• There have been 5,990 transactions, 2,878 of houses and 3,112 of apartments. Of these, 679 (11%) were at the premium end of the market.

• Total transaction value for residential properties stood at €1.49bln of which €632m (42%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 87% of houses under €500k and 90% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for high-end houses).

VOLUME AND MEDIAN PRICES

OF PREMIUM HOUSES AND APARTMENTS

TRANSACTIONS’ PRICE DISTRIBUTION

Transaction Volume of > € 200k Apartments

Transaction Volume of > € 500k Houses

Median Prices of > € 200k Apartments

Median Prices of > € 500k Houses

FAMAGUSTA

Q1 2016

€0-200k 0.5k 0 1k 1.5k 2k 2.5k 3k €200-500k €500k-1m €1m+ 1023 2748 1443 147 239 97 122 27 54 16 8 7 2 1 0 56 0 10 20 30 40 50 60 €0-200k €200-500k €500k-1m €1m+ 0 10 20 30 40 50 60 70 80 0 €300 000 €600 000 €900 000 €1 200 000 €1 500 000 Q1 2024 2016

2023 NUMBER OF TRANSACTIONS NUMBER OF TRANSACTIONS Apartments Houses Apartments Houses VOLUME MEDIAN PRICES 2016 2017 2018 2019 2020 2021 2022 2023 Q1 2024

-

Registration No.: 1013 | License No.: 517/E.

CYPRUS

© 2024 Cyprus Sotheby’s International Realty. All rights reserved. Cyprus Sotheby’s International Realty® and the Sotheby’s International Realty Logo are service marks licensed to Sotheby’s International Realty Affiliates LLC and used with permission. ONE Sotheby’s International Realty fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each franchise is independently owned and operated. Any services or products provided by independently owned and operated franchisees are not provided by, affiliated with or related to Sotheby’s International Realty Affiliates LLC nor any of its affiliated companies. The information contained herein is deemed accurate but not guaranteed.

Data provided by Cyprus’ Department of Lands and Surveys; data processing and analysis carried out by WiRE (Wire Services Ltd, Wire Wind Ltd, and Wire Valuations LLC, collectively WiRE). Cyprus Sotheby’s International Realty and WiRE make no representations or warranties concerning the report or the content and disclaim all such representations and warranties as to the condition, quality, accuracy, suitability, fitness for purpose, or completeness. Nothing in this report shall be regarded as providing financial advice, and you acknowledge that the content of this presentation is not suitable for this purpose. Neither Cyprus Sotheby’s International Realty or WiRE nor any of their directors, employees, or other representatives will be liable for damages arising from or in connection with the use of this report. This is a comprehensive limitation of liability that applies to all damages of any kind, including (without limitation) compensatory, direct, indirect, or consequential damages, loss of data, income or profit, loss of or property damage, and claims of third parties. All material in this report is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in this report constitutes professional and/or financial advice, nor does any information include a comprehensive or complete statement of the matters discussed or the law relating thereto. Information in this report may not be accurate or current. In particular (but without limitation), information may be rendered inaccurate by changes in applicable laws and other regulations. No action should be taken or omitted to be taken in reliance upon data in this report.