CYPRUS RESIDENTIAL MARKET OVERVIEW Q1 2023 QUARTERLY REPORT

Welcome to the first quarterly residential market report of 2023, providing the latest data on the Cyprus real estate market. We would like to note that at this time the data is incomplete and may not fully represent the actual volume of transactions due to technical issues at the Land Registry. The numbers will be revised and adjusted shortly to account for the delayed contract registration.

In this report, we are introducing a new feature—a comprehensive overview of the finest projects in each area of Cyprus. Our team of experts has carefully selected the most captivating developments on the island, showcasing the very best the market has to offer. We are also thrilled to announce the opening of our new office in Limassol, the business capital of Cyprus, in addition to our established headquarters in Pafos. Situated on the seafront in one of Limassol’s most prestigious areas, this modern space is ready to welcome partners and clients. Expanding our presence is a testament to our unwavering belief in the future of the Cyprus property market.

Within this report, we delve into the details of residential property transactions, with a particular focus on property value and price distribution. In this report, the term “premium properties” refers to apartments priced above €200,000 and houses above €500,000. We take pride in representing the world’s leading luxury real estate brand in Cyprus and being a beacon of knowledge, innovation, and trust in the local market.

With gratitude,

Anastasia Yianni Chief Executive Officer Cyprus Sotheby’s International Realty

Anastasia Yianni Chief Executive Officer Cyprus Sotheby’s International Realty

Transaction data are provided by Cyprus’ Department of Lands and Surveys, which records all transfers of ownership and registered contracts of sale (including property description, purchase price, date, etc). The data is processed in order to classify each transaction (as some properties are under construction, their description is not exact, or they form part of bigger projects) and are categorised by property type.

The analysis covers the entire area controlled by the Republic of Cyprus, excludes properties sold at auction (foreclosure), and references property values based on the amount declared by the purchaser at the time of the transaction (which excludes any VAT, transfer fees, or other duties levied).

• Across Cyprus, quarter-on-quarter (Q4 2022 – Q1 2023) transaction volume of houses decreased by 35% (to 864) and by 35% (to 1.6k) for apartments. Year-on-year (Q1 2022 – Q1 2023) transaction volume of houses decreased by 31% and by 22% for apartments.

• Quarter-on-quarter transaction volume of high-end houses (>€500k) decreased by 34% (to 118) and by 40% (to 493) for high-end apartments (>€200k). Year-on-year (Q1 2022 – Q1 2023) transaction volume of high-end houses decreased by almost 2% and by 8% for high-end apartments.

• Famagusta’s year-on-year transaction volume of houses decreased by 43% (to 46) and Nicosia by 44% (to 154) for apartments.

• Paf os’ quarter-on-quarter transaction volume for both houses and apartments decreased by 40%, to 239 and 285, respectively. Limassol was next in line with a 45% decrease in apartment transactions.

• Across Cyprus, median prices of both houses and apartments decreased in Q1 2023, compared to Q4 2022, at €245k for houses and €150k for apartments. However, year-on-year (Q1 2022 –Q1 2023) median prices slightly increased by 7% for houses, while for apartments by 9%.

• Quarter-on-quarter median prices of premium houses (>€500k) decreased by 14% (to €652.5k) and remained stable (to €310k) for high-end apartments (>€200k). Year-on-year (Q1 2022 – Q1 2023) median prices decreased by 13% for high-end houses and increased by 3% for high-end apartments.

The volume of sales for residential properties in 2023 reached nearly € 4 bln, with Limassol accounting for nearly half of the amount. Year-on-year we have witnessed a 30% increase in the total property sales volume. In some areas of the island, like Limassol and Pafos, the sales increase reached 40 and 58%. The sales to foreign buyers were even higher, they increased by 61% in total, 78 and 79% respectively in Limassol and Pafos.

Limassol is the business capital of Cyprus and a city of skyscrapers. Relocated international companies are the driving force behind the constant real estate growth in the city.

Residential transactions totalled 658 in Q1 2023, of which 47% (311 properties) were of the premium segment of the market.

Premium residential properties are of particularly high demand in Limassol, indicated by the high percentage of houses (45 properties, 38% of the total for Cyprus) and apartments (266 properties, 54% of the total for Cyprus) transacted over the past quarter.

Since Q1 2022, transaction value of residential properties totalled €1.9bln, of which €1.4bln (74%) was for the premium end of the market. It is worth noting that €1.1bln related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €715k and €362.5k for apartments in Q1 2023.

Compared to Q1 2022, median prices of houses increased by 20%, and by 16.3% for apartments.

This exclusive resort, Limassol’s high-end seafront property, is designed in cooperation with the famous Philippe Starck. It boasts a selection of apartments and villas and welcomes the residents to indulge in the Resort’s many unique facilities, icluding Spa, gym, cinema, kids club, business centre, cigar lounge, yacht club, mini golf, tennis court, water sports etc. The services include 24 hour concierge and security, domestic management, pharmacy and medical center, dry cleaning, shops, bakery, limousine services, to name just a few.

€ 1 454 000 + VAT

The villas are located within the new Golf Resort on the western outskirts of Limassol, close to the new Casino Resort, the shopping mall, the hospital, the water park, schools, and Lady’s Mile beach. The resort amenities include an 18-hole championship golf course, commercial facilities, a SPA and wellness centre, a fitness area, yoga and meditation lawns, tennis and basketball courts, kids’ playgrounds, an herb garden, and much more.

• There have been 22,101 transactions, 7,284 of houses, and 14,817 of apartments. Of these, 8,763 (40%) were at the premium end of the market.

• Total transaction value for residential properties stood at €8.750bln of which €6.408bln (73%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 84% of houses under €500k and 49% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the market’s premium segment (particularly for apartments).

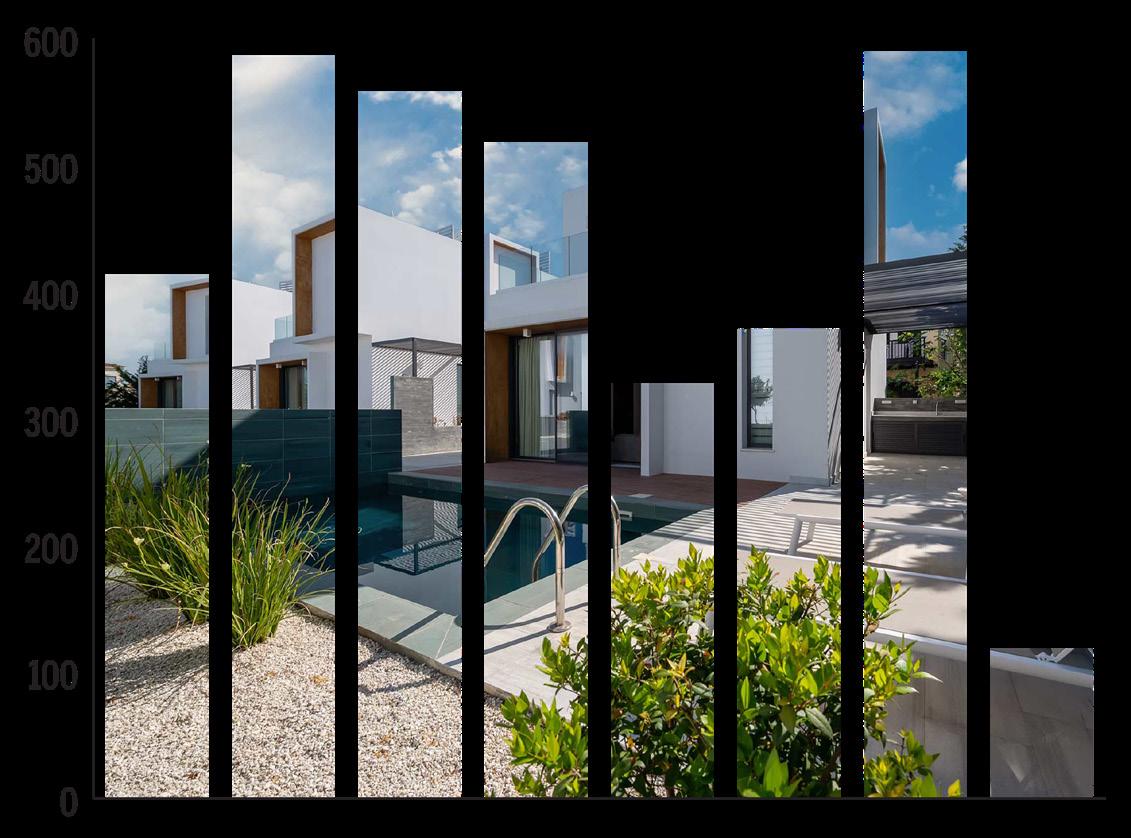

VOLUME AND MEDIAN PRICES OF PREMIUM HOUSES AND APARTMENTS

MEDIAN PRICES FOR HOUSES INCREASE BY 20.4%

Pafos is the cultural capital of the island, a city of villas and low-rise buildings, It has traditionally been popular with foreign buyers.

Residential transactions totalled 524 in Q1 2023, of which 20% (103 properties) were of the market’s premium segment.

Premium residential properties are of particularly high demand in Paphos, indicated by the high percentage of houses (43 properties, 36% of the total for Cyprus) and apartments (60 properties, 12% of the total for Cyprus) transacted over the past quarter.

Since Q1 2022, the transaction value of residential properties totalled €936m, of which €418m (45%) was for the premium end of the market. It’s worth noting that €286m is related to houses, as this is the main premium product of the district.

The median transaction price for premium houses was €655k and €317.5k for apartments in Q1 2023.

Compared to Q1 2022, median prices of houses increased by 20.4%, and by 15.0% for apartments.

KEY INDICATORS 2023

This mixed use development is set in a prime location only 150m from the nearest beach, bringing together sophisticated residences and the facilities of the superior 4-star boutique hotel. Large rooms with spacious balconies and beautiful views, superior leisure facilities, gastronomy and services are at your disposal all year round. Among the many hotel facilities are 3 restaurants, kids’ playground, lobby & pool bar, tennis court, 24-hour reception, gym and 3 pools.

This luxury resort destination in Tsada, Pafos, offers a new way of living focused on wellness, adventure, and nature. With openplan living areas, outdoor pool terraces, and authentic natural materials, these homes embody the true Mediterranean living. The resort boasts a championship-level golf course, clubhouse, village square with social venues and dining options, a world-class wellness center, and more.

• There have been 16,604 transactions, 8,010 of houses, and 8,594 of apartments. Of these, 2,755 (17%) were at the premium end of the market showing the district’s appeal as a destination for more affluent buyers.

• Total transaction value for residential properties stood at €4.539bln of which €2.418bln (53%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 82% of houses under €500k and 85% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for houses).

Nicosia, the capital of Cyprus, is a unique and attractive place. Commercial and long-term rental properties drive the market here.

• There have been 18,494 transactions, 4,918 of houses, and 13,576 of apartments. Of these, 2,352 (13%) were at the premium end of the market.

• Total transaction value for residential properties stood at €3.226bln of which €963m (30%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 94% of houses under €500k and 85% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium end of the market (particularly for apartments).

Residential transactions totalled 648 in Q1 2023, of which 19% (121 properties) were of the market’s premium segment.

Premium residential properties are of particularly medium demand in Nicosia, indicated by the percentage of houses (11 properties, 9% of the total for Cyprus) and apartments (110 properties, 22% of the total for Cyprus) transacted over the past quarter.

Since Q1 2022, the transaction value of residential properties totalled €785m, of which €263m (32%) was for the premium end of the market. It is worth noting that €185m is related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €587k and €254.5k for apartments in Q1 2023.

Compared to Q1 2022, median prices of houses decreased by almost 16.5% and remained stable for apartments.

2023

Larnaca is one of the oldest cities in Cyprus with lots of history and class, yet the recent years’ development gave it a modern sparkle, and the best is yet to come.

Residential transactions totalled 530 in Q1 2023, of which only 13% (69 properties) were of the market’s premium segment.

Premium residential properties are of low demand in Larnaca, indicated by the percentage of houses (15 properties, 13% of the total for Cyprus) and apartments (54 properties, 11% of the total for Cyprus) transacted over the past quarter.

Since Q1 2022, the transaction value of residential properties totalled €550m, of which €130m (24%) was for the premium segment of the market. It is worth noting that €93m is related to apartments, as this is the main premium product of the district.

The median transaction price for premium houses was €650k and for apartments €300k, in Q1 2023.

Compared to Q1 2022, median prices of houses increased by 16%, while for apartments by 18%.

2023

Contemporary. Luxurious. Comfortable. This new residential development is located in one of the most popular areas of Larnaca –Mackenzie, close to the sandy beaches and the Salt Lake. The energy-efficient luxury apartments have large living areas and balconies along with spacious bedrooms including en–suite shower rooms and walkin wardrobes, offering optional space, privacy and stunning views.

€ 700 000 + VAT

An exclusive collection of beachfront villas within a peaceful gated community is located on the east coast of Cyprus, in Pervolia, conveniently situated close to the International Airport and Larnaca city centre. Careful planning provides comfortable accommodation offering a wealth of living space and ample entertaining areas, not to mention their landscaped gardens with magnificent private swimming pools.

• There have been 13,829 transactions, 4,441 of houses, and 9,388 of apartments. Of these, 1,384 (10%) were at the premium end of the market.

• Total transaction value for residential properties stood at €2.263bln of which €659m (29%) were for the premium end of the market.

• The overall breakdown of residential transactions across the market was 95% of houses under €500k and 88% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for high-end apartments).

The Eastern part of Cyprus is a famous tourist destination. With the vibrant Ayia Napa and quiet Protaras, this area offers mostly holiday oriented properties.

Residential transactions totalled 108 in Q1 2023, of which 6% (7 properties) were of the premium segment of the market.

Premium residential properties are of particularly low demand in Famagusta, indicated by the low percentage of houses (four properties, only 3% of the total for Cyprus) and apartments (three properties, only 1% of the total for Cyprus) transacted over the past quarter.

Since Q1 2022, transaction value of residential properties totalled €204m, of which €52m (26%) was for the premium end of the market. It is worth noting that €38m related to houses, as this is the main premium product of the district.

The median transaction price for premium houses was €596k and €301k for apartments in Q1 2023. Compared to Q1 2022, median prices of houses decreased by almost 22% and remained stable for apartments.

2023

2 Bedroom Apartment in Protaras

Discover the true meaning of Eden in this remarkable residential development rising just 400 meters away from the pristine waters of the Protaras seashore. This private, gated complex boasts only the most premium in-house amenities that include a concierge service, a fitness center, a luxurious communal pool, and private underground parking with direct access to each floor.

€ 600 000 + VAT

Located on a man-made island, these villas directly overlook the marina and feature walk-out access to secure docks. Residents of these exclusive villas enjoy elegant interiors, private berths, lavish open-plan living areas and infinity edge pools. The lifestyle-centred project offers concierge and security services, fitness and wellness centres, SPA, shopping and dining, swimming pools, gardens, child care, serviced beaches and much more.

• There have been 4,803 transactions, 2,302 of houses and 2,501 of apartments. Of these, 509 (11%) were at the premium end of the market.

• Total transaction value for residential properties stood at €1.183bln of which €494m (42%) was for the premium end of the market.

• The overall breakdown of residential transactions across the market was 87% of houses under €500k and 92% of apartments under €200k. This apportionment has remained broadly stable throughout, indicating the attractiveness of the premium segment of the market (particularly for high-end apartments).

Fully Licensed Real Estate Advisors

Experts in Real Estate Transactions

Complete Range of Services

Property Portfolio Management

International Rules and Standards

Advantages of the Sotheby’s Brand

© 2023 Cyprus Sotheby’s International Realty. All rights reserved. Cyprus Sotheby’s International Realty® and the Sotheby’s International Realty Logo are service marks licensed to Sotheby’s International Realty Affiliates LLC and used with permission. ONE Sotheby’s International Realty fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each franchise is independently owned and operated. Any services or products provided by independently owned and operated franchisees are not provided by, affiliated with or related to Sotheby’s International Realty Affiliates LLC nor any of its affiliated companies. The information contained herein is deemed accurate but not guaranteed.

Data provided by Cyprus’ Department of Lands and Surveys; data processing and analysis carried out by WiRE (Wire Services Ltd, Wire Wind Ltd, and Wire Valuations LLC, collectively WiRE). Cyprus Sotheby’s International Realty and WiRE make no representations or warranties concerning the report or the content and disclaim all such representations and warranties as to the condition, quality, accuracy, suitability, fitness for purpose, or completeness. Nothing in this report shall be regarded as providing financial advice, and you acknowledge that the content of this presentation is not suitable for this purpose. Neither Cyprus Sotheby’s International Realty or WiRE nor any of their directors, employees, or other representatives will be liable for damages arising from or in connection with the use of this report. This is a comprehensive limitation of liability that applies to all damages of any kind, including (without limitation) compensatory, direct, indirect, or consequential damages, loss of data, income or profit, loss of or property damage, and claims of third parties. All material in this report is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in this report constitutes professional and/or financial advice, nor does any information include a comprehensive or complete statement of the matters discussed or the law relating thereto. Information in this report may not be accurate or current. In particular (but without limitation), information may be rendered inaccurate by changes in applicable laws and other regulations. No action should be taken or omitted to be taken in reliance upon data in this report.