Macro Newsletter

October 2025

Domestic News

Forint Strengthens as Central Bank Holds Rates Steady; Inflation and Wage Growth Show Signs of Stabilization

• The National Bank of Hungary left its key interest rate unchanged at 6 50% for the thirteenth consecutive meeting in October, as widely expected. Headline inflation remained steady at 4.3% for the second consecutive month in August, staying above the central bank’s 2–4% target range. Governmentimposed price caps and delayed service sector price adjustments may trigger a postelection rebound in inflation, posing risks for 2026

• Hungary’s annual inflation rate remained at 4 3% in September 2025, marking the third straight month of stability and slightly below market expectations of 4.4%. Inflation rose for services (5.9%) and consumer durables (2 5%), while easing for food, energy, and tobacco products Core inflation stayed unchanged at 3.9%, its lowest level since August 2021.

• Wage growth continued to moderate: gross wages increased by 8.7% year-on-year in August, down from 9.0% in July. Real wages grew by 4.7%, supported by easing inflation. Both public and private sector wage growth softened, and excluding bonuses, wages rose 8.1% year-on-year. For the January–August period, average gross wages were up 9.1% from the previous year

Source: National Bank of Hungary

Industrial Output Contracts Sharply, but Retail Sales Show Modest

Recovery

• Hungary’s industrial production fell by 7.3% year-on-year and 2.3% month-onmonth in August 2025, marking a broad-based downturn across nearly all manufacturing subsectors. During January–August, industrial output was 3.9% lower than a year earlier. Export sales, which account for 64% of total output, declined 2.4%, while domestic sales dropped 4.1%. Out of thirteen manufacturing branches, production decreased in eleven, led by a 13.3% plunge in electrical equipment manufacturing and a 4.5% drop in transport equipment, the largest subsector. Only computer, electronic and optical products (+9.2%) and wood, paper and printing (+2.6%) registered growth.

• In contrast, retail trade posted moderate gains, with sales up 2.4% year-onyear in August, accelerating from July’s 1.7% growth. The rebound was driven by stronger demand for non-food products (+4.9%), while sales of food, beverages, and tobacco were flat. Over the first eight months of 2025, retail volumes rose 2.8% compared to the same period of 2024.

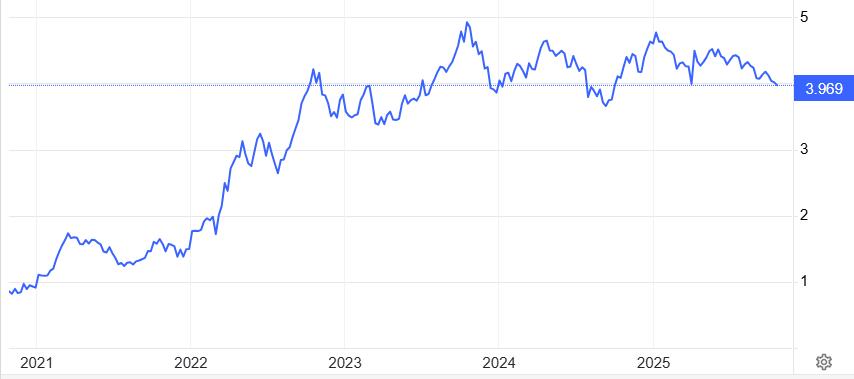

• On the financial side, the forint traded around 389 per euro on October 21, supported by the central bank’s stable policy stance.

• Hungary’s 10-year government bond yield stood at 6.85% on October 25, reflecting steady but cautious investor sentiment

EUR/HUF ex. rate (2020-2025)

Source: Trading economics

Energy market

Energy Prices Ease as Gas Stocks Remain High and Oil Faces Oversupply Pressures

• European natural gas futures held near €32/MWh, supported by strong storage levels and steady supply despite geopolitical risks at the start of the heating season. EU gas reserves stood at 82.9%, with particularly high levels in Italy (93.9%), France (92.7%), and Germany (75.7%), reducing fears of winter shortages. Robust LNG imports and Norwegian pipeline flows continue to offset the loss of Russian gas, while weaker Chinese demand for Arctic LNG 2 volumes has further eased global supply constraints. Although forecasts of colder midOctober weather could temporarily boost demand, global LNG capacity is expected to expand by 60% by 2030, led by the US, potentially creating long-term downward pressure on prices in both Europe and Asia.

• Meanwhile, Brent crude prices declined to around $60.8 per barrel on October 21, extending the recent slide amid concerns over global oversupply and uncertainty surrounding US–China trade talks. A record buildup of crude oil stored at sea has underscored the growing market imbalance and reinforced the prevailing bearish sentiment in global oil markets

Eurozone

Eurozone Inflation Edges Higher as ECB Poised to Hold Rates; German Industry Suffers Sharp Downturn

• The European Central Bank (ECB) is expected to keep its three key interest rates unchanged at the end of October, maintaining the deposit facility at 2.00%, the main refinancing rate at 2.15%, and the marginal lending rate at 2.40%. Markets anticipate that rates will remain stable in the near term, with a potential tightening cycle only resuming in late 2026 if inflationary pressures persist.

• Euro area headline inflation rose to 2 2% in September 2025, up from 2.1% in August. Core inflation, which excludes volatile items such as food, energy, and tobacco, climbed to 2.4%, surpassing preliminary estimates and marking the highest level since April 2025 The uptick reflects ongoing price pressures in services and manufactured goods.

• Meanwhile, Germany’s industrial sector contracted sharply, with output down 4.3% month-on-month in August, following a 1 3% gain in July and significantly underperforming expectations of a 1% drop. This represented the largest decline since March 2022, led by steep falls in automotive production (-18 5%) and machinery manufacturing (-6 2%) Over the June–August period, industrial output was 1.3% lower than in the previous three months, while annual production fell 3.9%, reversing last year’s modest growth

US Inflation Rises to 3% While Manufacturing Shows Mild Recovery

• The US annual inflation rate climbed to 3.0% in September 2025, the highest since January, up from 2.9% in August and below forecasts of 3.1%. Core inflation actually slowed to 3% from 3.1%, with markets expecting it to stay at 3.1%.

• In the real economy, US manufacturing output rose 0.2% month-on-month in August, outperforming forecasts for a decline and rebounding from a 0.2% fall in July. The durable manufacturing index also gained 0.2%, supported by a 2.6% increase in motor vehicle and parts production, while fabricated metal products and machinery registered modest decreases On an annual basis, manufacturing production grew 0.9%, following a downwardly revised 1.3% gain in July.

• In financial markets, the 10-year US Treasury yield hovered around 4% on October 21, stabilizing after a previous dip as investors assessed the potential economic impact of the ongoing government shutdown, trade uncertainties, and the future trajectory of monetary policy.

Forecast- Hungary

Source: Colliers