Exciting news! BPC introduces the SmartVista Fraud Management Newsletter — a concise, expert-packed digest for elevating your fraud prevention game. In this Issue #3 expect the latest product updates, consultancy insights, success stories, and market trends.

Product Update

We are excited to share with you our latest product planned updates on SmartVista Fraud Management solution.

Name: Profiling Release Plan: Available Now

Statistics profiles allow the assessment of a specific entity’s behaviour. The product enables the user to configure the calculation of statistical profiles and to view and reference previously calculated profiles.

We value your feedback please fill out the survey here to get started and rate your experience using SmartVista.

Product Update

We are excited to share with you our latest product planned updates on SmartVista Fraud Management solution.

Name: Profiling Release Plan: Available Now

Profiling, whether it’s behaviour profiling, statistical profiling, historical profiling, or simply ‘profiling,’ is a powerful tool in combating fraud. Fraudsters can easily steal static data such as names, addresses, card/ account details, and passport or driving licence information. Through generative AI, they can even replicate voices and faces. While biometric authentication is useful in preventing fraud, it does not necessarily detect it.

What is it?

Statistics profiles allow the assessment of a specific entity’s behaviour. The product enables the user to configure the calculation of statistical profiles and to view and reference previously calculated profiles. By default, the product only calculates statistics for request messages, but may be configured so that other messages are included in the statistics calculation.

Profiles serve two main functions: Use in statistical checks - that allow users to access a specific profile node, retrieve one of its measures and compare it against a user-defined value.

Biometric profiling is gaining traction as a valuable type of profiling but is mostly limited to mobile device usage. Although mobile devices represent a significant interaction channel, focusing solely on one channel is less effective than comprehensive monitoring across all channels.

The SmartVista Fraud Management product supports omni-channel profiling of entities and objects, offering a robust solution for preventing and detecting fraud. This article will explore the functionalities available within this product and how they can be utilised to enhance fraud prevention and detection.

A profile is a collection of summarised transactional data, related to a specific entity type instance such as card, account, customer, device or merchant - that defines its behavioural model. A profile is organised as a single hierarchical tree where each node contains data related to a specific transaction attribute.

Use for the behaviour risk scoring. The total risk score that is assigned to a transaction after checking it against an appropriate profile, this can be used in rules checks and displayed in the user interface.

A profile update procedure is run at regular intervals (for example every 5 seconds) to account for behavioural changes in the near-online mode. However, SmartVista Fraud Management only updates a profile if it receives a new incoming transaction that affects this profile since the last time the procedure was run. If fraud or genuine transaction flags are used in profiles, then after a flag is set for a transaction, the profile for the involved entity will be re-calculated. Decisions taken on cases after analysis is done can also be accounted for and used in behaviour profiles, thus feeding analytical models.

Profiles are updated according to the profiling settings that are defined in template profiles.

Statistics profiles page

The Statistics profiles page allows you to view up-to-date profiles, built for entity type instances such as cards, merchants, accounts, devices and so on.

You can view a profile’s hierarchy (tree structure) in the Profile tab. Each node in the tree contains the summarised transactional data associated with instances of a particular entity type.

Using an entity type instance profile, the product can determine if a transaction deviates from the normal behavioural model of the entity type instance and score the risk associated with the transaction accordingly.

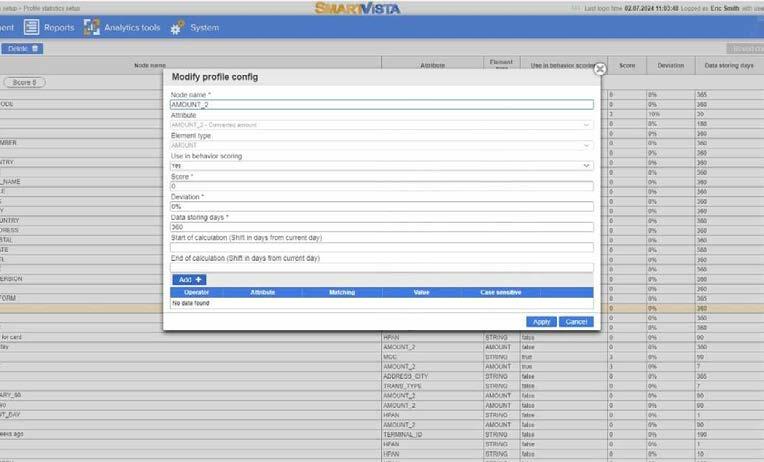

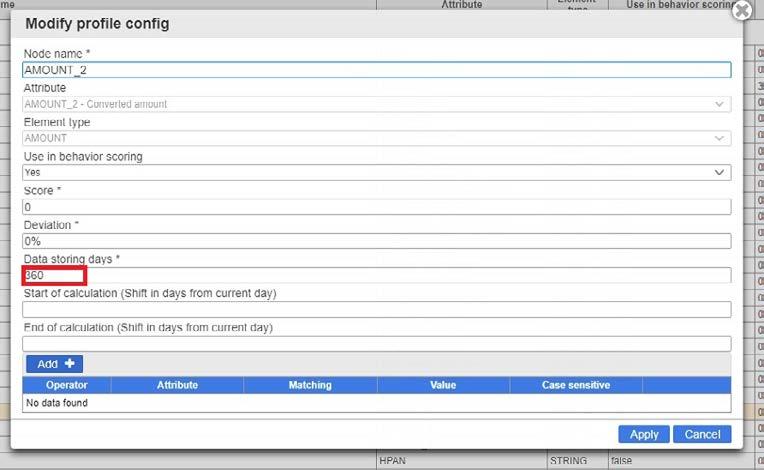

To enable profiling for an entity type, you must create and configure a dedicated profile template - on the Profile statistics setup page.

Profile Template

A profile template is a set of profiling settings and rules that the product uses to build profiles for a specific entity type. A profile template defines the following:

Entity type

Data to be collected for the profiles

Collected data used to update the profiles

Data structure of the profiles

Transaction risk scoring parameters of the profiles

A profile template is organised as a hierarchical tree that is nested under the node named Statistics configuration that stores profile templates.

Nodes

Nodes that are nested under the root node are called child nodes. Users can restrict the data that is collected by a node by configuring its filter. A node filter is a set of logical conditions to be fulfilled by the attributes of a transaction message, in order for its data to be added to the transactional data of the node.

Each node has a configurable data retention period that defines the period of time that it stores the collected transactional data. Transactional data whose age exceeds this period will be deleted automatically. Retention period of statistics is different from retention period of transactions configured in the system.

Risk Thresholds and behaviour profile score

Depending on the data type that is stored, values may represent either a quantity or an amount.

Using risk thresholds, SmartVista Fraud Management can determine whether a transaction is low, medium or high-risk. Risk thresholds are limits against which the total risk score of a transaction is compared. This risk is calculated as per the sum of risks of all triggered rules. Rules consist of multiple checks, including transaction risk calculated based on behaviour profiles and scores from Machine Learning models.

Four default profile templates are built into SmartVista Fraud Management – for cards, merchants, customers, and accounts.

The profile score (risk) for a transaction is calculated against the behaviour profile and this value is stored separately and can be used in rule checks.

Risk thresholds are configured on the Profile statistics setup page and are applied to all profiles in SmartVista Fraud Management.

Penalty points

You can assign penalty points to the root node of a profile template and to every child node and this will be used in behaviour transaction scoring. These penalty points are awarded to a transaction that is associated with an entity that does not yet have a statistical profile in the product or deviates from the calculated profile.

The absence of the profile indicates that SVFM has never received transactions associated with this entity before. Using this feature, you can track the first use of a card, a terminal, a device or any other entity. Another use case can be deviation from the behaviour seen before, for example transaction amount can exceed 40% of average amount stored in related profile. This affects the results profile score of a transaction that differs from rules risk score, and machine learning score as well.

How to create a profiling template

To create a profile template

To create a profile template, select the Statistics configuration node – on the Profile statistics setup page – and click ‘Add’, specify the node parameters and then configure any required filter(s).

1 3 2 4

If you want to restrict the transactional data that is collected by a profile template node, you must configure a filter. A node filter is a set of logical conditions that must be fulfilled by the attributes of an incoming transaction message in order for its data to be included in the transactional data of the node.

Each node of a profile template has the data maturity period that defines the node transactional data that must be used to update profiles. By default, the data maturity period is the same as the data retention period.

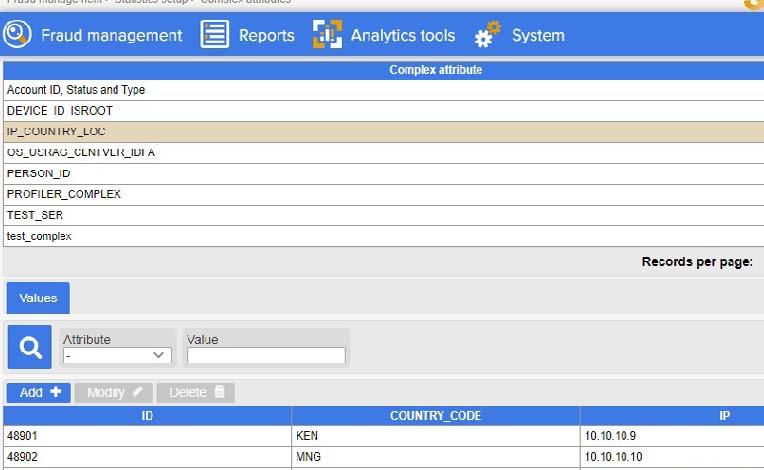

Complex attributes provide a way to merge several attributes (usually received from different channels) into one, for omnichannel profiling. Attribute values coming from different channels contribute to a profile.

The Immediate Benefits for you

Identifying transactions

Identifying transactions through various parameters: Identify non-typical transactions by time, type, amount or beneficiary through customer profiling. By creating detailed profiles of customer behaviour, financial institutions can quickly spot deviations that may indicate fraudulent activity.

Detection of patterns

By continuously monitoring and analysing spending behaviours, institutions can identify unusual activities that may signify fraud.

Here are several benefits provided through the profiling capability, in the area of electronic payments and digital banking:

Detect new devices & abnormal GEO locations

Detection of new devices, IPs, and abnormal GEO locations. Profiling can flag transactions made from unfamiliar devices, IP addresses, or unexpected geographic locations.

Cooling-off period for new customers and suspicious activity detected

Implementing a cooling-off period allows for additional scrutiny of new accounts and transactions flagged as suspicious. understanding and alignment on goals and strategies.

The power of profiling

Profiling is a hugely useful and powerful capability, for use in support of preventing and detecting fraud and money laundering. If you are not already using this, we highly recommend that you do, as part of ensuring maximum effectiveness and benefit, from the product.

Talk to your Account Manager or Project Manager, if you want to discuss this further – or alternatively, feel free to contact the Product Team directly. Refer to the chapter on “Statistics Setup”, with the SmartVista Fraud Management User Guide, for more detailed information.

Lets start the conversation and discover together!

Survey

Share with us your experience about SmartVista Fraud Management through the below 5 minutes survey.

Your feedback will help us improve the solution, while your suggestions will help us to enhance Fraud Management functionality and plan updates which are important for you and your business. Customer Survey

From one Expert to Another

USEFUL TIPS

#1: Refined use of fraud Types within Case Classification

We have spoken before about the importance of classifying fraud cases, within SmartVista – and in a future edition, we will dive into the details of using Case Management.

In advance of this, we wanted to talk about the refined use of fraud types, during classification, using Case Management.

Suggestion: Keep your types up-to-date

As they say “knowledge is power”, so arming yourself with this extra piece of information – can really help.

By keeping these fraud types up-to-date, you may also determine new or growing fraud threats and attack vectors – allowing you to take early action against them.

BPC encourage you to leverage this valuable feature, in helping to maximise the benefit the product delivers.

#2: Always maintain & refresh rules

Remaining vigilant goes beyond just having the latest software version; it involves the continuous evaluation and enhancement of your fraud, risk, and AML rules. Utilising the available data through reports and dashboards is essential for keeping these rules up to date and effective in detecting and preventing fraudulent activities.

Why is it important?

Simply having the latest software is not sufficient if your rules remain stagnant. Fraudsters can exploit outdated rules over time, necessitating a constant evolution in your detection methods. With fraud tactics constantly evolving, your rules must adapt accordingly to maintain their efficacy.

Suggestion: Regularly refresh your rules

To stay ahead of the curve, it’s imperative to regularly refresh your rules to cover all aspects of fraud, risk, and AML.

Under the menu option “Fraud management -> Case management -> Settings” under the “Fraud Types” tab it is possible to define, in considerable detail – and in hierarchical form – the various fraud types encountered by your organisation.

Why is it important?

It is worth ensuring that this is configured to allow a set of fraud types, which are as refined – and up-to-date, as possible. This allows your monitoring and reporting to be much more accurate. By doing so, you are able to have a better view of the fraud you are encountering and ensure that the SmartVista Fraud Management system is setup to counter these threats.

It may be that with added detail, you can determine potential “gaps” in your fraud detection and prevention –where additional rules, for example, may be required.

A recently updated set of rules will invariably outperform older versions, ensuring better efficiency and effectiveness in fraud detection and prevention.

If you haven’t already, it’s critical to ensure you’re operating on the latest version of the SmartVista Fraud Management (SVFM) product and/or Risk-based Authentication (RBA). Reach out to your Account Manager or Regional Director without delay to initiate discussions, gather information, and make necessary plans and allocations. The latest available version, offers enhanced capabilities to combat evolving threats.

Additionally, establish a robust process for regularly reviewing and refreshing your fraud rules. Monthly reviews are recommended, with quarterly reviews being the minimum requirement, and weekly reviews for those with sufficient resources. Remember, BPC is your partner in this ongoing battle against fraud, and we are committed to providing support and guidance whenever needed. Take action now to fortify your defences, as waiting only plays into the hands of criminals.

MarketWatch

Fraud Prevention in real-time payment systems

Dive deep into our comprehensive white paper to gain vital knowledge and strategies to navigate the complex landscape of realtime payment fraud and how to protect against it

How to protect your mobile wallet against payments fraud?

Mobile wallets, essential for ease, speed, and security, will handle $25 trillion in transactions by 2027. However, rising usage has increased fraud by over 60%. Learn about phishing, malicious apps, weak authentication, and public Wi-Fi risks, and how to protect your transactions.

Did You Miss Issue #2 of our NEW RiskSheild Fraud Newsletter?

Dive into it now and catch up on all the essential insights by simply clicking the link below. Don’t let the opportunity pass you by - stay informed and empowered!