ASCPA Connections - October November December 2025

2025-26 ASCPA BOARD OF DIRECTORS

Paul Perry, Chair

Kendra James, Chair Elect

Lyndsey Dixon

Cathy Dover

Jennifer Forrester

Bruce Fryer

Matthew Hilburn

Brian McLeod

Jeremy Mosteller

Cam Pearce

Sherman Pitts

Bradley Rayborn

Dennis Sherrin, AICPA Council Rep

Jamey Carroll, AICPA Council Rep

Sarah Propper, Past Chair

CHIEF EXECUTIVE OFFICER

Jeannine Birmingham, CPA, CAE, CGMA

CONTRIBUTING

Michael Brand, CPA

Boyd Busby, CPA

Bruce Ely

Marc Hamilton

Dustin Hostetler

Karen Miller, CPA

Rob Pearson, CPA

Susanna C. Zoebelein, CPA

Thomas C. Zoebelein, CPA

EDITOR

Megan G. Hughes, APR

Susanna and Thomas Zoebelein, CPAs

ASCPA Member Brian Barksdale and his wife Becky, were recently honored by United Ability at their 2025 Journey of Hope event. Their work with, and support of, the organization is rooted in a true devotion to their granddaughter Caroline. Read their story on page 8.

(Photo courtesy of Bham Now.)

In a profession grounded in integrity, accuracy, and public trust, Certified Public Accountants (CPAs) do not stand alone. Behind the individual licenses, regulated audits, tax prep and advisory services, there exists a powerful collective of state CPA societies - including the Alabama Society of CPAs (ASCPA). ASCPA is more than a professional organization. We are a community of accounting professionals who have a shared purpose. We are the posterprofession for lifelong learning, and we are advocates for excellence.

ASCPA is a professional membership organization that serves licensed CPAs, accounting professionals, CPA candidates, and accounting students. Whether at the state, regional, or national level—ASCPA was formed to elevate the profession, support practitioners, and ensure the highest standards of competence and ethics are maintained.

ASCPA is not a regulatory body, but we work hand-in-hand with the Alabama State Board of Public Accountancy, and other stakeholders such as the National Association of State Boards of Accountancy and the American Institute of Certified Public Accountants, to shape the future of the profession. ASCPA, at its core, provides membership connections, advocacy, education, and opportunities to gain experience and lead.

Membership in the ASCPA deepens that professional identity. Here is how:

1. Professional Development & Education - laws, standards, and technologies change, most often rapidly. CPA societies offer continuing professional education (CPE) through seminars, webinars, conferences, and on-demand learning. These opportunities help members stay ahead of regulatory changes, sharpen their skills, and explore emerging topics such as cybersecurity, ESG reporting, and AI in accounting.

For many members, society-provided education is not just about credit hours— it is about staying relevant and futureready.

2. Networking & Community - being a CPA can sometimes feel solitary, particularly for those in smaller companies or specialized roles. ASCPA can bridge that gap by offering a vibrant professional community. Through events, committees, on-line communities, mentorship programs, and chapter groups, members connect with others who share their challenges, values, and ambitions. These networking events often parlay relationships into career opportunities, client referrals, business partnerships, and lasting friendships.

3. Advocacy & Representation - ASCPA amplifies the voice of the profession. We advocate for sound financial and tax legislation, fair regulation, and policies that support both businesses and the public. Whether it is speaking with lawmakers about tax conformity or protecting the CPA designation from dilution (such as the effort some states have seen in legislation to abandon professional licenses), ASCPA ensures the interests and concerns of Alabama CPAs are heard and respected.

For ASCPA members, this means someone is always looking out for the profession’s long-term health—and their role within it.

4. Ethical Standards & Public Trust - ethics are the backbone of the CPA profession. ASCPA and the ASBPA play a vital role in reinforcing those standards through resources, guidance, and peer support. This dedication not only protects individual reputations but also strengthens public trust in the profession as a whole.

5. Support at Every Stage - whether you are a student exploring accounting as a career, a new CPA navigating the early years, or a seasoned professional transitioning into retirement or advisory work, ASCPA is here for its members with resources tailored to each phase. Scholarships, exam prep, leadership training, succession planning, ASCPA is here for the journey.

As ASCPA and its governing board begin to navigate the bigger picture, we are grateful to each of you who took time to complete the recent ASCPA Membership Survey. We found plenty of nuggets, comments, and suggestions upon which to continue to build our valued programs and services for you.

After taking a deep-dive into the survey data, showcasing the wants-and-needs of our members, we will begin to consider our future. Innovation, standards, technology, alternate practice solutions, the CPA exam, and pipeline are just some of the issues we will continue to address as a valued service for you. ASCPA wants to be the professional organization that does not just adapt to new trends, but helps lead the change.

We are “A Lifelong Professional Home: Advancing You. Elevating the Profession.” But perhaps the most important part of that phrase is You. So, thank you!

As we approach the end of another year (hard to believe) and the start of one of our many “busy seasons” throughout the year (I am talking to the 9/30 and 10/31 period-end people), we hope this Practice Management issue of Connections is helpful to you and your mission. I have the privilege and responsibility to observe the adaptability and resilience that define our profession. Today, the landscape of public accounting is evolving faster than ever, challenging us to not just keep pace, but to lead with thoughtfulness, agility, and care. A favorite TV series quote of mine is “the purpose of looking at the future is to disturb the present” – and in my opinion, is why our profession does so well with change – we anticipate, prepare and adjust accordingly for any and all opportunities to grow.

Rethinking the Pipeline: With Tomorrow in Mind - One of our most pressing concerns is sustaining our pipeline of accounting professionals. With increased competition from other fields and shifting perceptions about the CPA profession, we must become passionate ambassadors for our industry. This means engaging with the future worker at all levels, supporting and revamping internship programs, and making the pathway to licensure attainable and attractive. We must highlight the solid impact CPAs have on businesses and communities, hoping to inspire the next generation to see accounting as not only a rewarding career, but an essential cornerstone of society.

Fostering Growth through Advancement

- In today’s environment, talent development cannot be an afterthought. Firms that thrive are those that recognize and reward growth, providing clear and equitable pathways for advancement. Whether you are a small firm or a large practice, it is vital to establish mentorship programs, encourage continuous education, and promote a culture where achievement is celebrated and all voices are valued. In doing so, you not only retain your best people but build a firm that is resilient and future-ready.

New Staff: Setting the Stage for Success

– As we all look to onboard the future of our Firms during this time – we must remember that the onboarding process is more than a checklist – it is the foundation for a new professional’s career trajectory.

A thoughtful, structured onboarding experience can foster understanding, accelerate learning, and instill your Firm’s values from day one. This includes not only technical training but also opportunities to connect with firm leadership, peers, and clients. In an era when remote and hybrid work arrangements are increasingly common, we must ensure that our onboarding processes are inclusive, flexible, and supportive, bridging the gap between digital and in-person experiences.

Managing Deadlines: Excellence Amidst the Crunch - From September through December, our calendars fill with deadlines – quarterly reports, final tax returns, yearend reviews, tax planning meetings, and more. Managing this workload requires foresight, communication, and teamwork. Embrace technology to automate routine tasks, stay nimble with scheduling, and prioritize wellness initiatives to support your team’s mental and physical health. Remember that efficiency is not just a matter of faster work, but smarter work— setting realistic goals, communicating clearly, and celebrating milestones, even the small ones.

Embracing Today’s Challenges, Preparing for Tomorrow - Beyond the tactical, today’s practice leaders must look ahead to tomorrow’s realities. Cybersecurity, AI, digital assets, regulatory change, and evolving client expectations are not passing trends, but fundamental shifts. Invest in your firm’s technological infrastructure. Stay informed of legislation and standards. Develop flexible policies. And finally, foster a culture of curiosity and lifelong learning – because it is our willingness to adapt that secures our relevance and continued success.

As leaders we all bear a shared responsibility: we are entrusted with the well-being of our teams and the continued trust of our clients and the public. By focusing on talent development, thoughtful onboarding, robust processes, and a forever eye toward the future, we ensure the Alabama CPA community will “endure for millennia” (I like a good pop culture reference in my daily life – I have a passion finding where “life imitates art”, plus I enjoy seeing who is paying attention). Management (at all levels) is definitely not

for those without passion (but as I like to say “if it was easy, anyone could do it.”) Thank you for all you do that continues to prove the passion and dedication of individuals in this profession.

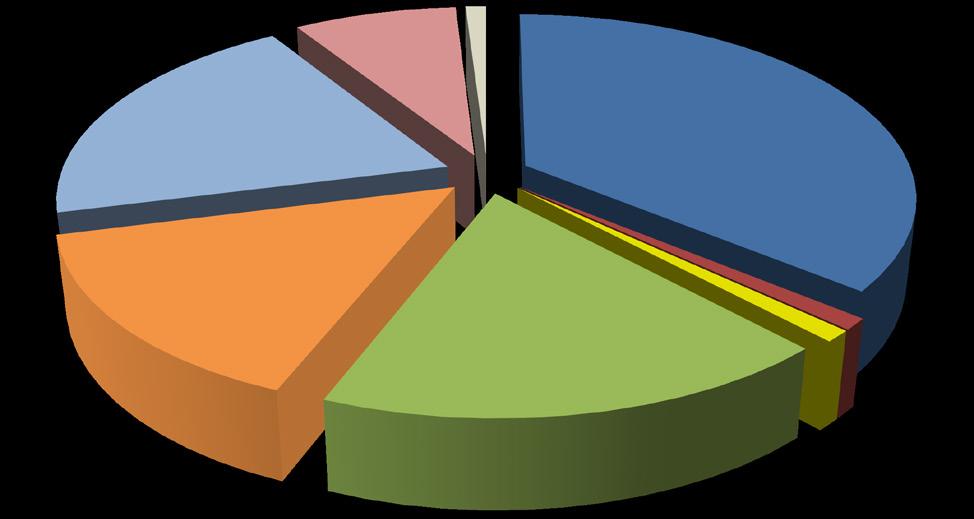

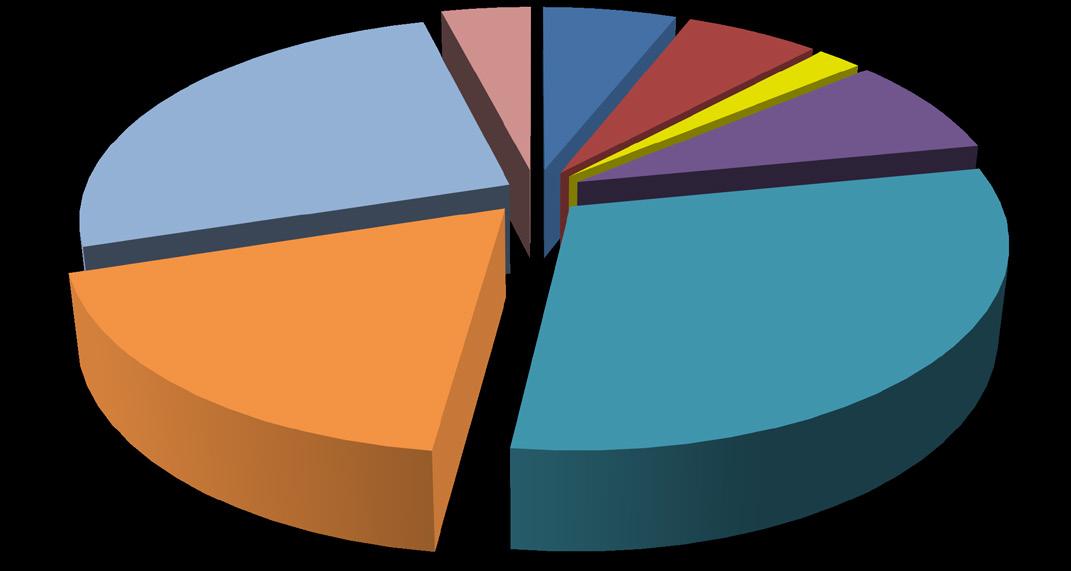

ASCPA FINANCIAL UPDATE

Alabama Society of CPA's Condensed Statement of Position For the Year Ended April 30 Compiled

Alabama Society of CPA's Condensed Schedule of Activities For the Years Ended April 30

Compiled from consolidated audited financial statements

Meet Brian Barksdale

2025 United Ability Journey of Hope Honoree

ASCPA Member Brian Barksdale and his wife Becky, pictured here with their family, were honored by United Ability at their 2025 Journey of Hope event. Brian and Becky are pictured here with their daughter and son-in-law, along with the real star of the show - Brian’s granddaughter Caroline, shinning bright here, far left.

Photo by Cady Metzger, courtesy United Ability.

When Brian’s granddaughter Caroline was born at just 31 weeks, his family’s world shifted overnight. What had been a healthy pregnancy for his daughter Meredith quickly turned into a crisis. One Sunday afternoon, Meredith mentioned she didn’t feel right. The next day, a check-up revealed an emergency: doctors needed to deliver the baby immediately.

Caroline entered the world tiny and fragile, having suffered a stroke in utero. The umbilical cord had been wrapped around her neck, cutting off oxygen. She wasn’t breathing when she was born, and the medical team rushed her to the NICU.

“That night, the doctors told us she probably wouldn’t live through the night,” Brian recalls. “And if she did, they said she’d never walk, talk, feed herself, or do anything independently. It was brutal to hear at two in the morning.”

But later, another doctor—the Chief Neurologist at Children’s of Alabama— offered words that became a lifeline. “Only One knows for sure, and He’s not down here. He’s up there. I think this baby will live.” He also urged the family to find the best early intervention program available.

“That gave us hope,” Brian says. “We went home that night and started Googling, trying to figure out what early intervention even meant.”

Despite a dire prognosis, Caroline not only survived but has grown into a joyful, determined teenager. Now 13, she continues to face challenges—major surgeries, daily therapies, and ongoing medical care—but she does so with remarkable strength.

“She’s the happiest kid I know,” Brian says. “She rolls out of bed every morning just glad to be here. And her hugs—well, you better be ready. She may break your ribs with how strong they are.”

Caroline is nonverbal but communicates through a speech device and sign language. Her talker—an iPad-sized device—speaks aloud when she presses symbols. Over time, she has become skilled at using it to share thoughts, jokes, and greetings. “I’ve always believed she understands more than most people think,” Brian explains. “She just needs a different way to tell us.”

Her resilience shows in everyday moments. As a toddler, fascinated by running water,

she once pulled herself up to the kitchen counter using only her fingertips just to feel it flow. “Most of us couldn’t even do that,” Brian laughs. “But she figured out how.”

Caroline has also endured significant surgeries. One procedure involved breaking and realigning her femurs, bolting them back into her hips, and lengthening her calf muscles so she could place her heels on the ground instead of walking on tiptoes. “She came through it with her usual toughness,” Brian says. “Her arms are so strong, she can climb ladders using just her upper body. She’s tough as nails.”

She also loves football—especially her siblings’ games at Jacksonville State. “Every morning, she signs their team’s motto, ‘Fear the Beak,’” Brian says with pride. “She’s already counting down to the next game.”

As Caroline grew, the family searched for programs to support her development. She began at the Bell Center in Birmingham and later transitioned to United Cerebral Palsy, now known as United Ability.

“At first, I thought it sounded too good to be true,” Brian admits. “My daughter told me about it, and I said, ‘I’ve lived in Birmingham my whole life and never heard of a place with all that.’ But when she toured it, she came back and said, ‘Dad, it’s all real—and more.’”

United Ability quickly became a cornerstone in Caroline’s journey. The nonprofit provides education, therapies, medical clinics, and adaptive technology for children and adults with disabilities. Onsite clinics make it possible for families to schedule multiple appointments—speech therapy, orthotics fittings, dental care— all in one day. “For parents who would otherwise drive all over town, that’s lifechanging,” Brian says.

The environment also fosters inclusion. Children with and without disabilities learn side by side, building friendships without stigma. “To those kids, it’s just normal,” Brian says. “They don’t stare. They don’t see ‘different.’ They just see their classmate. That’s one of the greatest lessons they’ll carry through life.”

He shares one vivid memory: “I once watched a little boy move Caroline’s walker to the bottom of the slide so it would be waiting for her when she came down. Nobody told him to—he just did it. That’s the kind of acceptance that place nurtures.”

Brian became deeply involved, joining United Ability’s board, later serving as chair, and now contributing on the foundation board. “For us, it’s personal,” he says. “Caroline benefits directly, but so do thousands of other families. Supporting it feels like the least we can do.”

Earlier this year, United Ability honored Brian and his wife Becky at the Journey of Hope gala. At first, Brian declined. “I don’t do things for recognition,” he says. “But they convinced me that sharing our story could encourage others to get involved.”

The evening drew more than 800 guests to the Alys Stephens Center. Inclusive circus performers wowed the crowd, half of them living with disabilities themselves. Videos and slideshows highlighted Caroline’s journey, but the most powerful moment came when Caroline took the stage.

“She used her talker to share a message with the audience, then signed ‘thank you,’” Brian remembers. “You could feel the emotion in the room. That moment—that was everything.”

Raising a child with disabilities has opened Brian’s eyes to both the challenges families face and the blessings they receive. Simple logistics—like finding an accessible bathroom or a changing table for a teenager—can be overwhelming. Traveling requires careful planning for elevators, seating, and medical needs.

But Caroline’s presence has been a gift. “She may not communicate like you and me, but she laughs, she loves, she has a sense of humor, and she makes life richer for everyone around her,” Brian says. “If society could see people with disabilities the way those kids at United Ability do—not as different, but simply as friends—we’d all be better off.”

The experience has also strengthened his sense of community. From the doctors who gave hope on the night Caroline was born to the volunteers who support United Ability’s programs, Brian is reminded daily of the power of compassion.

“It really does take a village,” he reflects. “And with a child with disabilities, it takes even more. But the blessings go both ways. Caroline brings joy to everyone she meets. She’s taught me more about resilience, joy, and unconditional love than I ever thought possible. Being her grandfather is one of the greatest gifts of my life.”

Now that the One Big Beautiful Bill Act is Law, How will the States Respond?

By Bruce P. Ely

With

special guest contributor, Karen R. Miller, CPA*

To even begin to answer that question, and it may take several columns to do so, we first must revisit the landmark Tax Cuts and Jobs Act of 2017 (TCJA), which among other things drastically reduced the top federal corporate income tax rate from 35% to 21%, increased certain individual tax credits while reducing personal income tax rates, imposed limitations on business interest deductions, imposed the now infamous “SALT Cap” and made a myriad of other domestic and international tax changes. Most of those changes were scheduled to automatically sunset on December 31, 2025. If Congress hadn’t acted, we would have seen a massive ($4 Trillion plus!) tax increase at the federal level-- plus relatively smaller tax increases at the state level for those states that levy a net income tax.

Although revenue estimates vary—widely—the static cost of OBBBA (or OB3) signed into law on July 4 is predicted to range from $1.4 to $3.4 trillion over the next 10 years, largely driven by: increased bonus depreciation and first year

write-offs for business assets, even for certain new manufacturing facilities; immediate expensing of R&D; increased business interest deductions; the continuance of certain tax benefits relating to pass-through entities (and their owners) including an increased SALT Cap; and novel deductions for overtime pay and tips, among several other business and individual tax goodies.

At the same time, as a partial pay-for, OB3 enacted changes to the Medicaid and SNAP (food assistance) programs that likely will increase state costs by millions of dollars annually by reduced federal funding.

Some states are already responding in panic. For example, the Governor of Colorado called their legislature into special session this month to address what he predicts is a $1.2 Billion revenue hole caused by that state’s automatic conformity with many aspects of OBBBA. We expect several other states to go into special session this Fall.

Like Colorado, Louisiana and Tennessee, and the other “rolling conformity” states, Alabama adopts federal corporate income tax changes automatically-- even the retroactive effective dates of several of the key business tax goodies-- while our individual income tax code provides what can be termed “piecemeal” or “rifle shot” automatic conformity, tied to the cross-reference (specifically or generally) in our statutes to particular IRC sections. For example, Alabama doesn’t recognize the now permanent IRC Section 199A qualified business deduction for PTEs and their owners, simply because our statutes don’t contain that cross-reference. Conversely, the Alabama Legislature in Spring 2021 voted to decouple our corporate income tax code from several of the complex foreign tax changes in TCJA, commonly known as GILTI and BEAT, which we hope will include the substantial amendments to those IRC sections by OB3.

Those states with fixed IRC conformity dates (e.g., cross-referencing to the IRC as in effect on 1/1/24), such as Georgia, South Carolina, North Carolina and Texas, must soon decide which OBBBA changes they wish to adopt. We would expect the business communities in those states to lobby especially hard for conformity with the “Big 3” tax benefits (bonus depreciation, IRC Section 179 expensing, and R&D expensing) as well as several other incentives for expansion and job creation.

As with most states, however, the Alabama Legislature is not slated to convene again until next Spring-- in our case, January 13, 2026 unless

Governor Ivey were to call a special session this Fall. Most political observers doubt that will occur. And remember, next year is an election year. Decoupling from any of the most popular business tax benefits, especially the “Big 3,” would be decried by some as a “tax increase” due to our automatic conformity with those federal changes and their retroactive effective dates.

Thankfully, according to the former Co-Chair of the Legislature’s now expired TCJA Task Force, Senator Dan Roberts, our legislative leadership has swung into action already. We’re also pleased to see the Alabama Department of Revenue taking a lead role, along with the Legislative Services Agency (LSA) formerly known as the Legislative Fiscal Office. Practitioners and leaders of the business community have also offered assistance while seeking guidance from the Department of Revenue initially as to those tax changes that became effective this year and will therefore impact 2025 tax return quarterly and annual filings. ASCPA President and CEO Jeannine Birmingham added that “the State Society is committed to working closely with legislative leadership, the Department of Revenue, LSA, and the business community in determining which tax changes enacted by OBBBA should become a part of the Alabama income tax code.”

The authors of this column are working with several of these groups and are especially grateful that Jeannine has tasked your new Director of Governmental Affairs, Rob Pearson, CPA, to be the Society’s point person along with your State Taxation Committee. Stay tuned and monitor your emails from ASCPA as well as its website for developments along the way. This will be a several month’s long process, stretching into next Spring, that will require the cooperation of all stakeholders.

*Karen is a former partner with PwC and now serves as Director of the nationally recognized MTA Program at the University of Alabama’s Culverhouse School of Accountancy, and as an adviser to and frequent speaker for the ASCPA. She and Bruce served as Technical Advisors to the Legislature’s bipartisan “TCJA Task Force” in 2019--2021.

Bruce P. Ely Karen R. Miller, CPA

Zoebeleins on Tax

“Zoebeleins On Tax” is not a typo it is a reflection of my new reality. Unfortunately, my wife of 52+ years lost her battle with cancer last year. I was fortunate to reconnect with my high school sweetheart, Susanna, who like me was also widowed. Susanna is also a CPA and now my wife so you can imagine how exciting our dinner conversations must be like. Susanna will be assisting in editing my articles (she found many errors I missed in past articles) and thus two Zoebeleins.

Enough about me, now to get on with the purpose of this article. Due to space constraints this article will be in outline form to aide as a reference for your year-end planning under the ” One Big Beautiful Bill Act of 2025.”

1. Individual Provisions

• Tax Rates/Standard Deduction

The individual tax rates under TCJA due to expire 1/1/26 are made permanent. After 2025 there will be an inflation adjustment for the brackets 10%, 12% & 22% increasing the upper income cutoff for each bracket.

The Standard deduction is increased retroactively to 1/1/25

Single filers from $14,600 to $15,750

Head of Household from $21,900-$23,625

Married filing jointly from 29,200-$31,500

• Seniors 65 and older (by 12/31 of the filing year) now get an AGI deduction of $6,000 per taxpayer for tax years 2025-2028. That deduction phases out beginning at MAGI of $75,000 for Single and $150,000 for MFJ.

• The child tax credit is increased to $2,200 for 2025 and indexed for inflation after 2025. The refundable portion of the child credit is made permanent at $1,400. The income phaseout of the credit is made permanent.

− Other dependent nonrefundable credit will remain at $500.

• The qualified business deduction, “QBI”, is made permanent at 20%. New for 2025 is a minimum $400 deduction for material participation where QBI income of at least $1,000 (inflation adjusted after 2025).

SSTB phaseout thresholds are increased to $75,000 single and $150,000 for MFJ.

Threshold for limitations is now indexed for inflation (2025 threshold is $394,600 for married and $197,500 for single).

• Charitable Deduction for Nonitemizers allows an above the line deduction of up to $1,000 for single and up to $2,000 for married filing jointly starting in 2026.

• No Federal “Income” Tax on Overtime & Tips-Tax Years 2025-2028

Cash Tips receive an above the line tax deduction up to $25,000 (itemizers & nonitemizers per return) for those individuals working occupations in which tipping is customary. The IRS is to publish a list of occupations where tipping is the norm. Now includes workers in the beauty industry and independent contractors.

The service industries limited for the QBI deduction are excluded from the tip exclusion (sorry fellow accountants). Employers don’t forget the tip credit which is not impacted by this new provision but a good starting point to breakout tip income.

− Overtime-pay up to $12,500 per individual and $25,000 for MFJ will get an above the line deduction. Overtime is limited to pay differential under the fair labor standards act (the 1/2 in time and 1/2). Overtime pay for exempt employees are excluded.

• Phaseout begins at MAGI of $150,000 ($300,000 MFJ) for both deductions.

• Forms W-2 and 1099 must indicate the amount of tip/overtime. Note tip and overtime deduction is not available when filing married filing separate.

• Up to a $10,000 annual deduction for new car loan interest 2025-2028

Must be interest on a new car assembled in the US for personal use (not business)

Loan interest must be on the purchase of the new vehicle with the new vehicle as collateral (lien). Note this is a yearly deduction over the life of the loan for 2025-2028. If refinanced by the taxpayer, the new loan can qualify up remaining balance secured by the vehicle (related party debt does not qualify).

Final assembly must be in the US. Final assembly means assembling parts necessary for mechanical operation of the vehicle. Check the new vehicle sticker for where final assembly took place.

Leased vehicles do not qualify

No golf carts even if street legal

First use is with the taxpayer (no used vehicles)

Gross weight is under 14,000 (car, minivan, SUV pickup truck or motorcycle)

Available for both itemizers and nonitemizers must include VIN to claim the deduction. Phases out for taxpayer with MAGI over $100,000 ($200,000 MFJ).

Lenders will be required to file information returns and furnish info for borrowers

• Child & Dependent Care Provisions

• Employee pre-tax dependent care exclusion is increase from $5,000 to $7,500

• Adoption credit now is refundable up to $5,000.

• Child and dependent credit increase from 35% to 50% of expenses for taxpayers with AGI of $15,000 or less. Over $15,000 is reduce 1% for each $2,000 over but cannot go below 35%. The credit is further reduced 1% for each $2,000 over AGI of $75,000 and 1% for each $4,000 over $150,000 for MFJ.

• Trump Accounts are savings accounts for children under 18 in the tax year beginning 7/03/26. Up to $5,000 can be contributed a year will be in the form of a traditional IRA. Children born between 1/1/25 & 12/31/28 can get a $1,000 tax credit for opening a Trump Account. Certain qualifying children without a Trump account Treasury may set one up $1,000 Trump account. Employers with a qualified plan will be able contribute to an employee’s child’s Trump account. Tax exempts may also contribute to Trump accounts. Treasury guidance will be forthcoming before 1/1/26.

• §529 Plans expands to included elementary & secondary education. Now includes postsecondary credentialing. This would include credentialing where college degree is not required such as the construction trades certification, insurance broker, realtors/real estate brokers and any other similar industrial business certifications.

2. Itemized Deduction Changes

• SALT Cap is raised for 2025 from $10,000 to $40,000 (MFS limit is 1/2 the cap for each return). 2026 the cap is $40,400 after 2026 it is increased 1% per year. Deduction is decrease 30% for income over $500,000 ($250,000 for MFS) but not below $10,000. The $500,000 is increase by 1% for tax years after 2026. Pass-through entity tax payments not impacted by the new provision.

• Casualty Loss deduction limits are made permanent. New for 2026 is casualty loss will include both federal and state declared disasters.

• Gambling Loss deduction now limited to 90% of gambling losses. Breakeven gamblers will find they are now taxed on 10% of winnings. Includes professional gamblers.

• Limit on Itemized Deductions starting in 2026 for those in the 37% bracket will be limited to 35% benefit.

• Mortgage Interest Cap stays at $750,000 for acquisition debt. No equity loan interest if not used for improvements.

• Charitable Contribution Deduction allowed only when in excess of 1/2 of 1% of the charitable contribution base beginning in 2026.

3. Other Miscellaneous Provisions

• Credit for Donations to a Scholarship Granting Organization up to $1,700. Scholarship Granting Organization should be similar to the Alabama AAA.

• Estate & Gift Tax Exemption is raised to $13,990,000 for single $27,980,000 for married couples in 2025. Increases to $15,000,000 for single and $30,000,000 for married couples for 2026 and is indexed after 2026.

• Alt Min Tax Exclusion made permanent with phase out at $500,000 for single and $1 million for married. Phase out increased to 50% of overage above threshold.

• Math Error Authority for the IRS to make changes to the taxpayers return for IRS perceived errors for math and other errors it believes are on the return to change the taxpayers tax return. Taxpayer has 60 days to respond before change is made permanent leaving Tax Court or Taxpayer Advocate. Unlike past notices the new notices do not provide guidance as how to respond to the notice during the 60 days.

• Sunset of Green Incentives some of which will have expired by the time this article is published. Here are the incentives and expiration sunset dates:

• June 30, 2025 used clean vehicle credit, clean vehicle credit, and commercial clean energy vehicles

• September 30, 2025 for sustainable aviation fuel credit

• December 31, 2025 energy efficient home improvements, and deductions for qualified clean energy facilities, property and technology

• June 30, 2026 alternative vehicle refuel credit, energy efficient commercial building deduction, and new energy-efficient home credit

• December 31, 2027 clean energy production credit for wind and solar.

• January 1, 2028 clean hydrogen production credit

• December 31, 2029 clean fuel production credit

4. Business Provisions

• 100% Bonus is made permanent for property acquired after 1/19/2025 (inauguration day forward). Permanent is permanent until an administration change and or shift in control of Congress.

• §179 Expensing Limits increase to $2.5 million with reduction now starting at $4 million.

• Domestic Research and Development Expense Capitalization is eliminated for tax years beginning after 12/31/2024. Unamortized capitalized research expenses can be taken as a deduction either 100% in 2025 or 50% in 2025 & 2026.

• Small Business (Average Gross Receipts of $31 Million or Less) the elimination of required capitalization is applied retroactively to costs incurred after 12/31/2021. This will allow small business to elect to amend 2022-2024 tax return to reverse the R & D capitalization.

• Fiscal files can amend using the effective date.

• 1099-K Reporting de minimis reporting for 2025 is changed to $20,000 on 200 separate transactions. The $20,000 will be indexed for inflation in the future.

• Business Interest Deduction Limitation returns the add back to testing income threshold for interest limitation for depreciation amortization

and depletion. Floor plan interest deduction will now include trailers and campers in the definition of motor vehicle.

• §1202 Stock new for corporate stock issued after 07/04/2025 the exclusion is increased from $10 million to $15 million (1/2 for MFS) or if greater 10 times of the aggregate stock basis. Current law there is a 5-year holding period to obtain the exclusion. Under OB3 there is a tiered phase in 50% if held 3 years, 75% if held 4 years, and 100% if held 5 years.

• Qualified Transportation Fringe gone for bike commuting and adds another year of inflation adjustment for transportation fringe other than bicycles.

• Noncorporate Business Loss Limitation is made permanent. The threshold amounts for 2025 is $313,000 ($616,000 married).

• Special Depreciation Deduction for Qualified Production Property is provided a 100% writeoff in the year placed in service before 1/1/2031. Qualified production activity is manufacturing, production (agriculture, chemical), refining of tangible personal property. There must be a substantial transformation of the property comprising a product excludes production in retail establishments such as a restaurant. There is a ten-year recapture rule on the deduction for change in qualified use.

• The property must be used in qualified production facility engaged in a qualified production activity

• Construction must begin after 1/1/19/2025 and before 1/1/2029.

• Must be in the US or a US territory

• Original use must be with the taxpayer

• Taxpayer must elect to take the deduction

• Portions of the property for nonproduction use are excluded from the deduction. Excluded areas include the items below:

Office space

Admin space

− Parking

Sales activities

Lodging

R&D activities

Software development

• Paid Family & Medical Leave made permanent and allows employers to claim a credit for a portion of paid family leave insurance, makes the credit available in all state, and lowers minimum employment time to six months

• Employer Provided Child Care Credit is expanded 40% of qualifying expenses up to a credit maximum of $500,000 (small business $600,000). Allows pooling or resources and the use of third-party intermediary for their program. The changes are effective for tax years after 12/31/2025.

• Business Meals Deduction no change to the 50% limitation except for business meals for fishing boats and fishing facilities which will be 100% deductible 1/1/2026 and thereafter.

• Opportunity Zones Extended beginning 1/1/27. The changes are numerous and beyond the scope of this article.

• International and Administration provisions are beyond the scope of this article.

We hope you find this to be of some help in this year-end tax planning. Keep in mind the business interest limitation and or the business loss limitation when assessing the taking of some of the benefits of the above tax changes.

Susanna and I wish you all the best for the upcoming holiday season and a very Happy and Blessed New Year.

Thomas C. Zoebelein, CPA Tax Consultant

Susanna C. Zoebelein, CPA Shareholder, Jessup and Associates, P.A.

Member Benefit Provider

CPACharge has made it easy and inexpensive to accept payments via credit card. I’m getting paid faster, and clients are able to pay their bills with no hassles.

Trusted by accounting industry professionals nationwide, CPACharge is a simple, web-based solution that allows you to securely accept client credit and eCheck payments from anywhere. – Cantor Forensic Accounting, PLLC

increase in cash flow with online payments of consumers prefer to pay electronically of bills sent online are paid in 24 hours

Get started with CPACharge today

The Impact of AI in Accounting: Uses and Automation Benefits

By: Gabriela Jhean

Artificial intelligence (AI) is no longer a distant concept but a present-day reality for industries worldwide. And while its adoption varies across sectors, there’s often one shared goal in mind: to increase productivity.

Accounting is no exception. CPAs are exploring new ways to leverage AI in accounting and streamline their workflows. Furthermore, firms are discovering how to use AI in accounting to increase their bottom line and drive long-term growth.

This article explores how AI can automate tasks, deliver insights, and help you provide more value to clients.

AI’s role in accounting

According to KarbonHQ’s State of AI in Accounting Report 2025, 85% of accounting professionals are excited or intrigued by AI’s potential. However, only 37% of firms are investing in AI training for their employees.

This gap presents a significant opportunity for your firm to gain a competitive edge. By learning how to use AI in accounting, you can streamline your firm’s operations, enhance client services, and drive sustainable growth.

Will AI replace accountants?

AI can indeed automate many accounting tasks and quickly analyze large amounts of data—but that doesn’t mean accountants will become obsolete.

Accounting involves more than just crunching numbers. It requires critical thinking, ethical judgment, and strong client relationships. And while AI excels at processing information, it can’t replicate the human ability to understand complex financial situations or provide personalized advice.

Instead, AI serves as a powerful tool that enhances an accountant’s capabilities, freeing them to focus on strategic planning and building deeper client connections. It’s about working together—not replacing human expertise.

The benefits of AI for accounting firms

Accounting and AI converge, with clear benefits: increased efficiency, improved client service, and significant cost savings.

Boosted efficiency and accuracy

Using AI in accounting boosts efficiency by automating or speeding up routine tasks like

data entry. This allows accountants to focus on higher-value work. AI also minimizes the risk of human error by reducing the need for manual input, leading to more reliable financial reporting in less time.

CPAs can also use accounting AI tools to analyze large datasets quickly and identify trends or anomalies. This allows for faster, more informed decision-making.

Better client intake and client service

AI improves client intake and ongoing service by streamlining communication and accelerating response times. AI-powered tools can automate the initial stages of client onboarding by collecting essential information and writing accounting proposals. This not only reduces the administrative burden on accounting staff but also provides smooth first interactions with new clients.

For existing clients, AI enables faster, more efficient communication. Chatbots and virtual assistants can handle routine inquiries, schedule appointments, and provide instant answers to common questions—enhancing client satisfaction and allowing accountants to dedicate their time to more complex work.

Improved time and cost savings

One of the most compelling benefits of AI in accounting is the time and cost savings it offers. Automating repetitive tasks like invoice processing, expense tracking, and basic data entry ultimately translates into lower labor costs and increased productivity.

AI’s ability to minimize errors and streamline processes reduces the need for costly rework and corrections. This improved accuracy leads to better compliance and fewer financial discrepancies, saving the firm both time and money.

Common tasks that AI can simplify for accountants

Accounting professionals can rely on AI for a wide range of tasks, including:

• Invoicing and Expenses: AI reduces manual work and improves accuracy. It can process invoices by extracting key details, matching receipts to transactions, flagging discrepancies, and generating accurate reports to help firms save time and reduce costs.

• Data Analysis and Forecasting: AI transforms financial data into actionable insights and accurate forecasts—enabling predictive analytics, detecting fraud, and streamlining budgeting to save time and enhance accuracy.

• Tax Compliance and Preparation: AI automates document collection, tax calculations, and return preparation. It also helps accountants navigate complex tax codes by quickly accessing relevant information and updates.

How to implement AI into your accounting firm

To leverage AI effectively, you need an accounting firm strategy that incorporates its implementation. Let’s explore how you can align AI-powered technologies with your firm’s goals to ensure a seamless integration.

Identify key tasks and build an AI roadmap

Begin by pinpointing specific tasks where you could increase efficiency. You can draw inspiration from the examples of AI in accounting that we discussed in the previous section. Once identified, create a clear AI roadmap outlining implementation timelines and resource allocation. This approach will help you stay on track as you introduce AI tools and update workflows at your firm.

Research and demo AI technology

Research various accounting AI tools to identify solutions that align with your firm’s needs. Request live demos to understand how these tools address your pain points and improve workflows.

Train employees on new AI systems

Don’t underestimate the importance of employee training when introducing AI systems. It’s not enough to just give your team the tools; they need to understand how to use them effectively and securely. Investing in training programs ensures your staff can confidently navigate the new AI landscape, maximizing its potential while minimizing security risks.

Monitor AI performance

Continuously monitor the performance of your AI systems to ensure they’re delivering the expected results. Track key metrics such as task completion times and goal attainment to assess the effectiveness of AI integration. Regular evaluations allow for adjustments and optimizations, ensuring AI consistently contributes to improved efficiency and productivity.

Boost cash flow and productivity with 8am™ CPACharge

Structuring your workflow is essential to maximizing revenue and productivity. CPACharge complements AI-powered processes by automating traditionally manual aspects of billing and payments. To see how CPACharge can integrate with your AI-driven workflow, schedule a demo at www.cpacharge.com/alcpa.

Gabriela Jhean is a Content Writer for 8am™, the trusted solutions provider for legal professionals ready to simplify operations, ensure compliance, and deliver world-class outcomes for clients.

/ November / December

CPE WITH ASCPA

As you know, we have renewed our partnership with CPA Crossings to bring you ALOnDemand, a platform designed to bring many more On-Demand courses to your fingertips!

We have a list of CPE FAQs on our website which address accessing your ASCPA account, logging into a CPE course, and finding your transcript. There is also a section on surveys, which must be completed within 7 days after a course in order to process CPE certificates. Please read over this short FAQ page, which can be found at alabama.cpa/cpe-faq.

Sales & Use Tax Workshop

Virtual 11/5/2025 (10-11:40 AM)

Bruce Ely, Jimmy Long, and Will Thistle | 2 Tax

K2 AI Conference

Virtual 11/7/2025 (8:30 AM-4:30 PM)

Various | 8 Other

2025 Alabama Federal and State Tax Institute

Hybrid

11/12-11/14/2025 (8:30 AM-12 PM)

Various | 20 Tax

2025 Federal and State Tax

Update for Local Practitioner

Virtual

11/18/2025 (8:30 AM-4:30 PM)

Jim Martin | 8 Tax

ALOnDemand

K2 Technology Conference

Virtual 11/18-11/19/2025 (8:30 AM-4:30 PM)

Various | 16 Various

K2 Excel Conference

Virtual 12/3/2025 (8:30 AM-4 PM)

Various | 8 Other

2025 Governmental Accounting & Auditing Forum

In-Person

12/8-12/10/2025

Various | 8 A&A, 2 Ethics, 2 Tax, 4 Other

ASCPA is continuing its partnership with CPA Crossings to offer an on-demand learning solution called ALOnDemand. More than 140 curated courses are available covering a wide range of topics in accounting and auditing, tax, technology and more. A subscription is available to ASCPA members that provides unlimited access to all ALOnDemand courses during the calendar year and unlimited CPE credits. To learn more visit alabama.cpa/ALOnDemand.

CPE Deadline Is Here: What’s Next?

It will be the responsibility of each CPA to log in to their dashboard and download their Certificates of Completion and Transcripts, check for accuracy, and submit to the State Board of Accountancy. Watch for an email from the Alabama Society of CPAs with helpful steps to follow to access your transcript. If you have any questions about extensions or CPE requirements, contact the Alabama State Board of Public Accountancy at 334-242-5700 or visit https://www.asbpa.alabama.gov/contact.aspx.

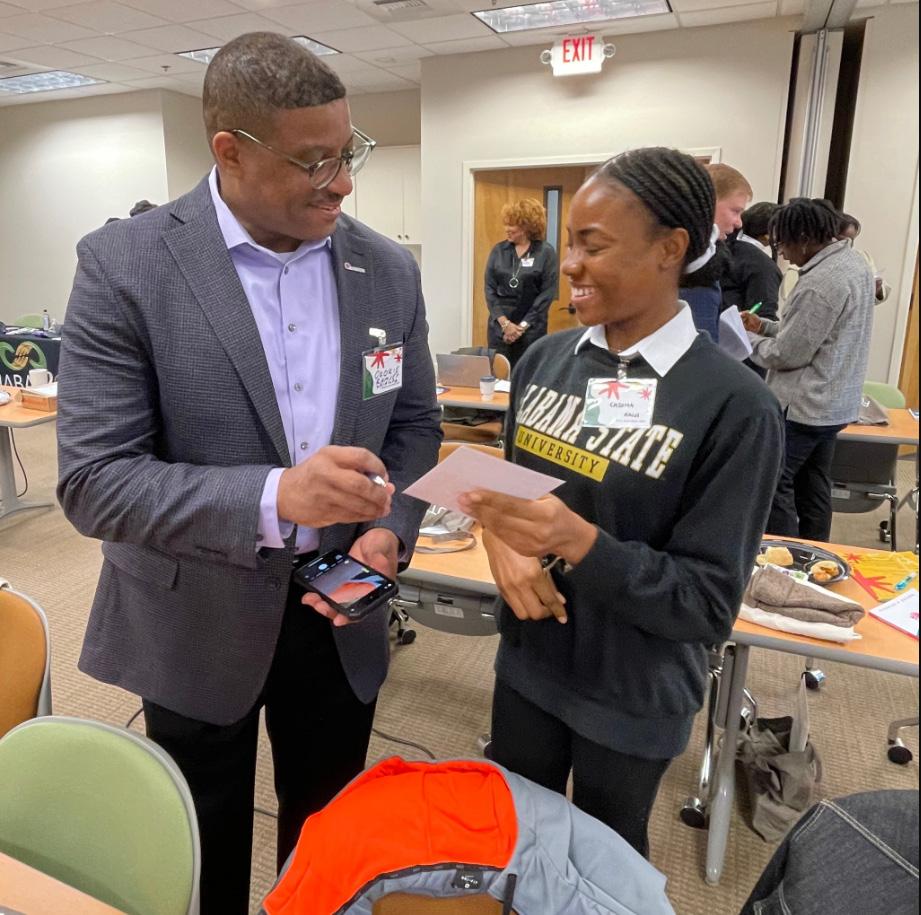

In just two short years, the Alabama Society of CPAs’ Balance Sheet Bash has become a signature event for promoting diversity and inclusion in the accounting profession. Since its launch in 2024, the Bash has welcomed more than 300 students across Alabama, connecting them with leading firms, professional associations, and mentors who are committed to building a stronger, more representative pipeline of future CPAs.

Hosted in Birmingham, Montgomery, and Huntsville, the event features a powerful mix of networking, professional development, and speed mentoring. Students engage directly with representatives from top organizations. This year sponsorship committments have already poured in from Deloitte, Kaiser Permanente, NASBA, and Okorie Ramsey. Sponsors and exhibitors consistently say this event allows them to build relationships and offer practical advice to students that extend beyond the event.

The Balance Sheet Bash returns in 2026 with three dynamic stops:

• Huntsville — January 20

• Birmingham — January 21

• Montgomery — January 22

The event’s continued growth is only possible through the support of sponsors and exhibitors who host interactive tables, share their expertise, and participate in guided mentoring sessions. Each partnership helps ensure that students leave

inspired, informed, and connected. Registration for student participants will open in early November, so be sure to monitor alabama.cpa for its launch!

Whether you are a student ready to step into the profession or an organization eager to make an impact, the Balance Sheet Bash offers a meaningful way to be part of Alabama’s accounting future.

For sponsorship opportunities, contact: Florene Holland, EdD Director, Career Pathways and Talent Engagement fholland@alabama.cpa

Important Developments in Pathways to CPA Licensure

For more than a century, the Certified Public Accountant (CPA) credential has been synonymous with competence, professionalism, and public trust. In Alabama, our commitment to protecting the public and upholding the integrity of the CPA designation has remained steadfast. As the accounting profession evolves and our licensure pathways adapt, it is essential that we thoughtfully preserve the rigor and standards the public expects and deserves.

In response to growing challenges—ranging from the rising cost of education to the recruitment and retention of qualified professionals—the Alabama State Board of Public Accountancy (ASBPA) voted to support a statute change in the current pathways for CPA licensure. This legislative change will be led by the Alabama Society of CPAs. The three pathways below reflect emerging national models under consideration in several jurisdictions.

Proposed Pathways to CPA Licensure

ASBPA intends to maintain the requirement that all candidates must pass the Uniform CPA Examination and complete relevant experience. Once the legislation successfully passes, candidates will become eligible for licensure through one of three pathways:

1. Pathway 1 - The Baccalaureate Degree Plus Two Years of Experience

• A baccalaureate degree from a four-year college or university accredited by a regional accreditation board.

• The total education program shall include an accounting concentration as defined by board rule.

• To obtain licensure, these candidates must complete two years of qualifying supervised experience as defined by board rule.

• This option recognizes that professional experience can further develop core competencies when pursued alongside continuing education.

2. Pathway 2 - The Graduate Degree Plus One Year of Experience

• A graduate degree in addition to a baccalaureate degree from a four-year college or university accredited by a regional accreditation board.

• The total education program shall include an accounting concentration as defined by board rule.

• To obtain licensure, these candidates must complete one year of qualifying supervised experience as defined by board rule.

3. Pathway 3 - The Baccalaureate Degree Plus 30 Hours Plus One Year of Experience

• A baccalaureate degree plus an additional 30 semester credit hours at a four-year college or university accredited by a regional accreditation board.

• The total education program shall include an accounting concentration as defined by board rule.

• To obtain licensure, these candidates must complete one year of qualifying supervised experience as defined by board rule.

Rationale and Safeguards

These pathways recognize the profession’s changing educational and economic realities, while preserving the high standards that have always defined the CPA designation. Several safeguards will remain firmly in place:

• The Uniform CPA Examination continues to serve as the definitive benchmark of professional competence.

• All experience must be verified as defined by board rule.

• Ethical conduct requirements and continuing professional education obligations remain unchanged.

Maintaining the Public Trust

While these pathways create flexibility, our foremost responsibility is to protect the public. Any candidate, regardless of pathway, must demonstrate the knowledge, skills, and ethical judgment necessary to serve clients and employers with distinction.

Next Steps

ASBPA supports these changes and supports the Alabama Society of CPAs as they lead the effort in the 2026 Alabama Legislative Session.

Conclusion

ASBPA appreciates the thoughtful engagement of our stakeholders as we support the ASCPA in their efforts and the future of CPA licensure. Our mission remains unchanged: to ensure that the CPA credential continues to symbolize excellence, integrity, and service to the public for generations to come.

For more information or to provide input, please visit our website or contact the ASBPA office directly.

Sincerely

D. Boyd Busby, CPA Executive Director, Alabama State Board of Public Accountancy

Football, Rural Hospital Tax Credit and Other Cool Things

Happy football season to all who celebrate! Since serving as team waterboy in 2nd grade (over 40 years ago), my fall Friday nights have included being drawn to stadium lights like a moth. These days, I serve as the radio voice of the Demopolis Tigers. My good friend and fellow CPA, David Grizzard, serves as our statistician and analyst. I’m told the players, parents and community appreciate our broadcast, but we do it because it’s a blast. If you are a footballloving CPA, your local team needs you! Statisticians, chain-gang crew, public address spotters, concessions, gate workers, even over-exuberant “homer” radio announcers, there is no shortage of roles to fill. If you don’t have a team, become a referee or clock operator (it’s way better than you might believe). Football is yet another example of how CPAs have immeasurable value in and out of the office.

Rural Hospital Investment Tax Credit

Beginning January 2026, your donation to support Alabama Rural Hospitals could earn you a dollar-for-dollar state tax credit thanks to new legislation sponsored by Rep. Terri Collins. Act 2025-404, signed on May 14th, provides a lucrative incentive meant to supplement the operations of rural hospitals in dire need of financial support.

The Act was modeled after an established program in Georgia and has proven to be effective in creating community support of and engagement with participating rural hospitals. The Act also created the Rural Hospital Investment Board to oversee the credit, on which I serve as the Board’s Chair.

There are a couple of details that are relevant as you advise both rural hospitals and potential donors about the new state credit:

• The Credit will be administered by the Alabama Department of Revenue (ALDOR). They have already created a web page (https://www.revenue.alabama.gov/tax-incentives/ rural-hospital-investment-tax-credit/) with links to the Act and the Program Manual for participating hospitals.

• Hospitals must comply with the provisions outlined in the program manual by November 1st to be eligible for the 2026 tax year.

• The Board will publish, through ALDOR’s website, a list of participating hospitals ranked in order of need by December 1st.

• In order to take the tax credit, donors must log in to ALDOR’s MyAlabamaTaxes site and “reserve” their credit for that tax year. The reservation process will include the donation/ credit amount and the hospital(s) receiving the donation. Yes, taxpayers will be able to designate multiple hospitals at the same time.

• The reservation process is expected to go live on January 2, 2026, for the 2026 tax year. Upon completion of the reservation process, taxpayers will have 30 days to send the donation to the hospital designated. The hospital will then have 30 days to confirm receipt of the donation. Failure to meet these deadlines will forfeit the reservation.

• Taxpayer donations/credits are limited. I’ll refer to the ALDOR website on limits for taxpayers since they range from $15,000 for single individuals to $500,000 for C-Corporations.

• Each hospital’s credit-eligible donations cannot exceed $750,000 in 2026.

• And then there’s an overarching limitation of $20,000,000. Regardless of who gives and gets what, the entire program cannot exceed this amount in 2026. That limit increases by $5,000,000 in each of the following two years.

• If you think the $20,000,000 cap will be met within a matter of days, I agree with you. The early birds will get the worms.

• If the taxpayer just can’t decide who to give their donation to, there will be an option to make an “undesignated” donation to all eligible rural hospitals. ALDOR’s website will have more information on that option as it becomes available.

I urge you to stay informed about this credit by visiting ALDOR’s website and help spread the word. This is a win-win for taxpayers and rural hospitals!

Other Cool Things

• I’m proud of the AICPA and their efforts related to the One Big Beautiful Bill Act. In particular, CPA firms (and many others) dodged a bullet related to the Pass-Through Entity Tax. Early versions of the OBBBA would have disallowed a deduction for PTET at the federal level for specified service businesses, but AICPA led efforts to inform and advise legislators on the fairness (or lack thereof) of this provision.

• The AICPA also led efforts to expand qualifying expenses paid from Sec. 529, Education Savings Accounts. Costs related to CPA exam preparation and fees now qualify. That’s a good win for our pipeline initiatives.

• OBBBA also affected many of our tax provisions here in Alabama, some of which may require adjustments to our tax code. With challenges come opportunities, and we stand ready to assist with these adjustments.

• Alabama’s CPA Pathways Bill is coming! We’re thankful to Rep. Kerry “Bubba” Underwood, CPA from Tuscumbia, for offering to sponsor this legislation coming in 2026. We have already begun working with legislators to inform and educate them on the need for the additional pathway to CPA.

As always, please reach out to me via email at rpearson@alabama.cpa if you have any questions, concerns, or just to talk football!

Rob Pearson, CPA Director, Government Affairs Alabama Society of CPAs rpearson@alabama.cpa

The Little Things Really are the Big Things

By Dustin Hostetler

When I was asked recently if I’d like to write an article for the Alabama Society of CPAs, two things crossed my mind. First, yes, I love giving back to the profession I’ve been part of for over 20 years now. Second, I knew exactly the topic I would write on. College football season is back! That means I spend way more time this time of year listening to college sports talk and as I was listening to a program on SiriusXM a few weeks ago I was reminded of a famous Nick Saban mindset: the little things lead to the big things. While I was born and raised in Ohio, graduated from Ohio State, and am one of the biggest Buckeye fans now living in SEC country (please don’t stop reading), I admire and respect Nick Saban and those great Alabama teams of the past decade. And his coaching philosophy on the process and little things speaks right to me as a process improvement and transformation leader in the CPA profession.

In the most successful CPA firms, much like the most successful college football programs, a focus on process and doing the little things right is a big driver of success. Somewhere along the way though I think many organizations have forgotten about this. It’s easy to let the little things slip. It’s easier to focus on the big, new, shiny object (e.g. the latest and greatest technology) and mandate it from on high in lieu of putting in the work to master the small stuff first. “We don’t have time for that”, many believe. But here’s the ugly truth: you’ll either invest time on the front end to build a strong foundation, or you’ll waste time later trying to navigate through chaos. And to be the best for our clients, be the true advisors our clients expect of us as CPA firms, we have to start getting back to the basics.

That doesn’t mean that we lose sight of the big picture. It doesn’t mean that we don’t innovate and continuously improve what and how we do things to better serve our clients. It just means that to be the best we can be now and into the future for our clients, we need to understand we can’t just jump to the outcome. We must embrace the process. Because as Nick Saban has masterfully demonstrated, the process leads to the outcomes. We can’t just focus on the outcomes. This is where so many CPA firms get things wrong. They go to that industry conference, they attend “best practice” roundtables. They hear what so-and-so firm is doing and then come back and say we must do this too. Do you see how that’s jumping to the outcome without first mastering the basics? And then when that new shiny object gets deployed, it’s usually met with resistance, confusion, apathy and generates results well below what was expected.

This is where the Lean Six Sigma process improvement methodology and mindset comes into play. It’s a powerful 5-step process improvement tool that focuses on understanding root causes and core issues, so you focus your improvements where it matters most. Not just solving yesterday’s problem or someone else’s problem. But solving your unique problems and building a strong foundation of the “little things” that add up to success with the big thing. DMAIC (Define, Measure, Analyze, Improve and Control) is a mindset as much as a toolkit. It gets firms to focus on defining the core issues and aligning around future goals and objectives (Define), understanding the current state and the truth of today (Measure), identifying what is limiting your growth and future opportunity (Analyze), and then and only then do you start dabbling in the solutions (Improve

and Control). The beauty is in its simplicity – you must do your homework and build a foundation of what matters. This is what leads to the accomplishment of the big things.

Let’s get more specific and look at an example. There’s no doubt AI is here, it’s coming in hot, and it’s going to disrupt what and how we do things in CPA firms. It’s still in the infant and toddler phase though. The key is we need to understand the trend and use it to help us predict and navigate the future. If firms just jump in sporadically and without any clear strategy or plan as to what they’re trying to solve, how it benefits clients, and how it will position the firm to be in a better spot 3-years, 5-years from today as it relates to servicing clients, you’ll just be introducing more chaos. Instead, slow down to go fast as we always like to say. You first need to think about where you want to be as it relates to servicing your clients in the future. Align and define on your future objectives. Then, focus inward on making your foundation as strong as possible. You must create processes that can start doing the little things right before you’re ready for the big thing. For example, you’re not going to automate something in your process that is utterly inconsistent and riddled with personal preferences. You must get that right, you must focus on the basics of blocking and tackling (standardizing some basics), before you’re ready for the big stuff. If you jump to the big stuff, you’ll lose. If you start with the big stuff, you’ll be like that gimmicky offense that looks good against Directional State University but when you face a defense with a pulse you sputter.

The DMAIC mindset is a game-changer. And the thing I like about it perhaps the most is that there are so many applications of it. What Nick Saban and his program at Alabama did is proof of this. It truly shows us that the little things matter. By building a disciplined organization that can masterfully handle the little things, it enables us to fully adapt and accomplish the big things. That’s how we need to be managing and guiding our firms in this age of transformation. Stop chasing the shiny object. Invest in the process.

The accounting profession is in a pivotal transition. Artificial intelligence (AI) is no longer theoretical—it is embedded in the daily platforms CPAs already use. From Microsoft 365 to Adobe Acrobat to enterprise APIs, the shift is not optional. CPAs in public practice, business and industry, government, and nonprofit sectors must now grapple with how to responsibly harness AI without undermining the very assurance their profession is built on.

The profession has always adapted to new standards: from paper to spreadsheets, from manual reconciliations to ERP systems. AI is the next standard. The risk is not adoption itself but failing to adopt with professional guardrails. Research shows that technology-mature firms produce up to 39% more revenue per employee—an unmistakable signal that modernization is now tied directly to firm economics. The critical question is: how do CPAs embrace these tools while ensuring independence, objectivity, and trust remain intact?

What’s Changed Recently: Adoption Guidance AI is already in the tools we use every day. The question is how to move forward with confidence. Start with the short list below: it’s the most current, credible guidance for turning curiosity into governed practice—policies you can defend, workpapers you can audit, and outcomes you can improve.

Responsible AI Implementation Checklist (aligned with ISO/IEC 42001)

Why it matters: Turns “AI governance” into a CPAready control set (roles, human oversight, data classification, documentation) mapped to a globally recognized standard.

Use now: Make this your firm’s AI control baseline; require an AI workpaper (prompt, model/version, inputs, validations, reviewer sign-off) for any AIassisted deliverable; map your policy to the checklist headings.

AI Risk Management Framework (AI RMF 1.0) + Playbook

Why it matters: The U.S. government’s voluntary framework widely adopted across industries. Its Govern --> Map --> Measure --> Manage structure is practical and auditable. The Playbook provides copyready actions.

Use now: Treat any new agent or automation as an RMF deployment with defined risks, success criteria, monitoring, and rollback. Tie your AI workpaper to RMF outcomes (e.g., validation evidence under “Measure”).

AI Management System (AIMS)

Why it matters: The first management-system standard for AI—familiar to CPAs who use ISO-style quality systems. It gives a certifiable structure (policy, objectives, controls, continual improvement) for responsible AI use.

Use now: Borrow the clause structure to formalize your AI policy (scope, leadership, planning, support, operations, performance evaluation, improvement). For larger firms, consider certification to signal maturity to clients and insurers.

“Spotlight: Generative AI in Audits and Financial Reporting” (July 2024)

Why it matters: Not a standard—but a clear signal of regulator expectations: documentation, supervision, and professional skepticism when AI aids audit or financial-reporting work.

Use now: In audit/attest, label preview tools as pilotonly, keep human-in-the-loop, and retain prompts/ outputs/tie-outs in workpapers; ensure partner-level supervision over any AI-assisted procedures.

Risk Management Considerations

Insurers are actively recalibrating how AI risk is treated across Cyber, Tech/Professional E&O, Media, EPL, and D&O coverages—and the fine print matters. In 2024, W. R. Berkley introduced an “Artificial Intelligence Exclusion — Absolute” endorsement for certain liability lines; its broad “arising out of” language can sweep in losses linked to the use, development, or deployment of AI (even alleged use), so renewals should be reviewed for similar forms. At the same time, major brokers emphasize that most AI events still flow through existing policies, but with growing reliance on exclusions (or, in some markets, affirmative AI endorsements) and tighter underwriting questions about how firms govern, validate, and document AI-assisted work. In other words, the market is moving from “silent AI” (ambiguity) toward explicit terms—good for clarity, risky if you don’t read the endorsements.

For CPA firms, the play is to treat AI like any material operational risk: (1) Pre-read forms and endorsements at renewal for AI-related language across all lines, watching for “absolute” AI exclusions or broad “actual or alleged use” phrasing; (2) arrive “underwriter-ready” with an AI inventory, your policy spine (e.g., AICPA/ISO/NIST mapping), and sample AI workpapers that show human-in-the-loop review, validation/tie-outs, logging, and rollback plans; (3) align engagement letters and client communications with how you actually use AI (and what you do not

do), since brokers report questionnaires now probe disclosures and controls; and (4) map likely scenarios (model error, data leakage, IP/media claims, bias/ discrimination) to the policies that would respond and the exclusions that might limit recovery. The goal is simple: no surprises at claim time—clear coverage intent, documented controls, and evidence you ran AI in a defensible, supervised way.

AI Tools: A Rapidly Evolving Landscape

If your company or firm runs on Microsoft 365, AI now lives inside the tools you already open every day—Word, Excel, Outlook, and Teams—as Microsoft 365 Copilot. In practice, Copilot drafts and rewrites text in Word and Outlook, summarizes long threads and documents, and answers questions using your Microsoft 365 SharePoint content (subject to your IT permissions). In Excel, Copilot helps you explore a workbook in natural language, propose formulas, and generate explanations or summaries for the ranges you select. For production work, always confirm whether a feature is General Availability (GA) or preview using Microsoft’s official release notes; train staff on GA only and treat preview as pilot-only with added review controls.

For PDF-heavy work, Adobe Acrobat AI Assistant brings summarization and data extraction into Acrobat. Companies can enable admin controls and review the product’s security posture (processing/ caching behavior, model providers) before allowing client data. This keeps PDF review inside governed tools rather than ad-hoc uploads.

Many firms also use research assistants for external lookups and drafting. If you choose to deploy them, prefer enterprise offerings with contractual data protections—e.g., ChatGPT Enterprise (admin controls, SSO/SCIM, no training on your business data by default) and Perplexity Enterprise Pro (answers with cited sources, enterprise controls). Use these for research and first drafts; keep client-identifiable data within governed environments.

From “AI That Writes” to “AI That Helps You Work”

Most of us first met AI as a good drafter—it helps write emails, tidy memos, and summarize long threads. The next step is AI that helps your work move, still under your approval. This is often called agentic AI (supervised, task-capable AI that only acts within guardrails you set): the AI proposes sensible next steps, your workflow tool prepares them, and you decide whether anything is actually sent or posted.

In Microsoft 365, that looks like a Power Automate flow—“when an invoice arrives, save the PDF, extract key fields, draft a reply, post a summary to Teams”— with a pause for approval before any change to a system. When an update is needed, it goes through an API (Application Programming Interface— a secure, rules-based doorway that lets systems exchange data or perform actions with permissions and audit logs). If nothing is approved, nothing happens; every

step is logged.

This approach fits CPA work because it reuses controls you already value—review before release, clear evidence, and reversibility. Each run leaves a short AI workpaper (inputs, model/version, actions taken, outputs, validations/tie-outs, preparer/ reviewer, dates). As features evolve, treat GA (generally available) capabilities as production-ready and preview as pilot-only with added review.

If you’re new to this, the on-ramp is simple: pick one routine task, add a single supervised step (e.g., have the AI draft the message you already send), attach the workpaper, and measure minutes saved. When your comfortable, add one approved API action (for example, create a “to-review” item—not a journal entry). The goal isn’t to automate everything at once; it’s to learn in small, safe steps that compound over time, keeping assurance intact while curiosity grows.

Curiosity Prompts

Quick wins in daily work

• What standard memo or email (client update, variance note, engagement recap) could be safely AI-drafted if a reviewer signs off?

• If Copilot could turn meeting notes into next-step checklists, where would that save you the most time?

Close and reconciliations

• What would a “to-review” queue look like if an API could add invoice candidates but never post to the ledger?

• Which data in your reconciliation workbook always lead to exceptions—and how could AI presort or identify them?

Supervised automations (agentic flows)

• If a Power Automate flow paused for approval before any send or write-back, which task would you automate first?

• Where would a “draft --> approve --> send” pattern prevent rework or mis-sends in your team?

Marc Hamilton, CPA, CGMA

Read the full article, and access digital resources from this article, by visiting alabama.cpa/Hamilton.

The Countdown to SQMS Compliance: Are You Ready for December 2025?

By Michael Brand, CPA

It is hard to believe that the time is almost here for firms to implement the AICPA’s Statements on Quality Management Standards (SQMS). Maybe it is not too hard to believe due to the fact that we have been talking about those standards since 2022. However you might feel, the fact is that by December 15, 2025, firms are required to have their system in place and ready to go. SQMS-1 and SQMS2 were issued in 2022, and those standards focus on a risk-based approach for firms to manage their accounting and auditing practice. The SQMS require a fundamental change from a rules-based standard to a system where firms design and tailor policies and procedures that are specific to the risks that are specific to their firm. In essence, it is going from a system where firms could basically “set it and forget it” to a system where the firm will continuously monitor the effectiveness of their risk assessment and the effectiveness of the responses to those risks. The standards require more thought and analysis to design, implement and monitor quality management.

First of all, let us look at the new standards:

Statement on Quality Management Standards 1, A Firm’s System of Quality Management, provides standards and guidelines for firms to design, implement, and monitor a system of quality management that is tailored to the firm’s accounting and auditing practice and to individual engagements.

Statement on Quality Management Standards 2, Engagement Quality Reviews, provides standards and guidelines for firms to establish policies regarding when to perform an engagement quality review, how and when to perform the review, and the qualifications for who will perform these reviews.

Statement on Auditing Standards 146, Quality Management for an Engagement Conducted in Accordance with Generally Accepted Auditing Standards, provides standards and guidelines for engagement partners and their engagement teams to maintain audit engagement quality.

Statement on Standards for Accounting and Review Services 26, Quality Management for an Engagement Conducted in Accordance with Statements on Standards for Accounting and Review Services, provides standards and guidelines for engagement partners and their engagement teams to maintain engagement quality for reviews and accounting services, similar to the guidelines in SAS 146.

Statement on Quality Management Standards 3, Amendments to Quality Management Section 10, A Firm’s Quality Management, and twenty, Engagement Quality Review, revises certain definitions related to referred -to auditors to conform to SAS 149.

What are the key changes?

• Focus on quality management, not quality control.

• Customize and tailor, the system of quality management to the nature and circumstances of the firm and the engagement it performs.

• Focus on achieving quality objectives through identifying quality risks and responding to quality risks.

• More robust leadership and governance requirements

• Modernization: technology, networks, and external service providers

• Improved information and communication

• Enhanced monitoring and remediation process

The Risk Assessment Process

SQMS 1 requires a risk-based approach to designing, implementing, monitoring, and updating a system of quality management. If you are a CPA who performs audits, the risk-based approach should be a familiar concept. Even if you are a firm that does not perform audits, but does perform other attestation engagements, the concept of a risk-based approach should be a familiar one. Firms should design their system to reduce risk to an acceptable level. This requires professional judgement instead of just relying on rules or a non-tailored checklist approach. For me, this just makes sense as the circumstances within the firm and external to the firm affect engagement quality differently for different firms.

So how do you start the risk assessment process? Firms should first determine what their quality management goals are. For example, with regard to relevant ethical requirements, the firm’s objective

would be to maintain independence when performing non-attest services for attest clients. Risks are what can go wrong at either the quality management level or the engagement level; for example, if an engagement partner’s bonus to obtain additional services leads the firm to perform so many non-attest services that it could impair the firm’s independence for the attest work it performs. The firm should use professional judgment to consider conditions, circumstances, events, and actions/inactions that could drive quality risk. Firms will consider the likelihood and magnitude of the risk of not meeting their quality objectives. The firm should then design and implement responses to address quality risks. For significant risks, the firm should design responses to reduce those risks to an acceptable level. For the example above, the firm might implement responses that require safeguards to be put in place to satisfactorily reduce risk to an acceptable level. This thought process is done for each component of the system of quality management.