Shop a wide variety of ASCPAbranded goodies, as well as fun items for any future CPA in your life!

The ASCPA Store offers a wide range of sizes and styles to suit every preference. With brands like Carhartt, Adidas, Nike, Port Authority, and Bella+Canvas you can’t go wrong. Plus, with every purchase you’re supporting ASCPA’s Educational Foundation and creating a brighter future for the next generation of CPAs. So, start shopping!

2025-26

Paul

Lyndsey

Cathy

Jennifer

Bruce

Matthew

Brian

Jeremy Mosteller

Cam

Sherman

Bradley

Dennis

Jamey

By: James E. Long, Jr. and Bruce P. Ely

From the Pipeline: Job Shadow

Hear from one Alabama student who recently jobshadowed with Huntsville-based BMSS, and learn what surprised her the most.

New Leadership Development Opportunities

Three

to grow your skillsets in

Covering the Bases

Learn more about what the 2025-26 Board will be doing for its members this year.

Should I disclose use of AI?

Should clients be informed about use of generative AI? If so, how?

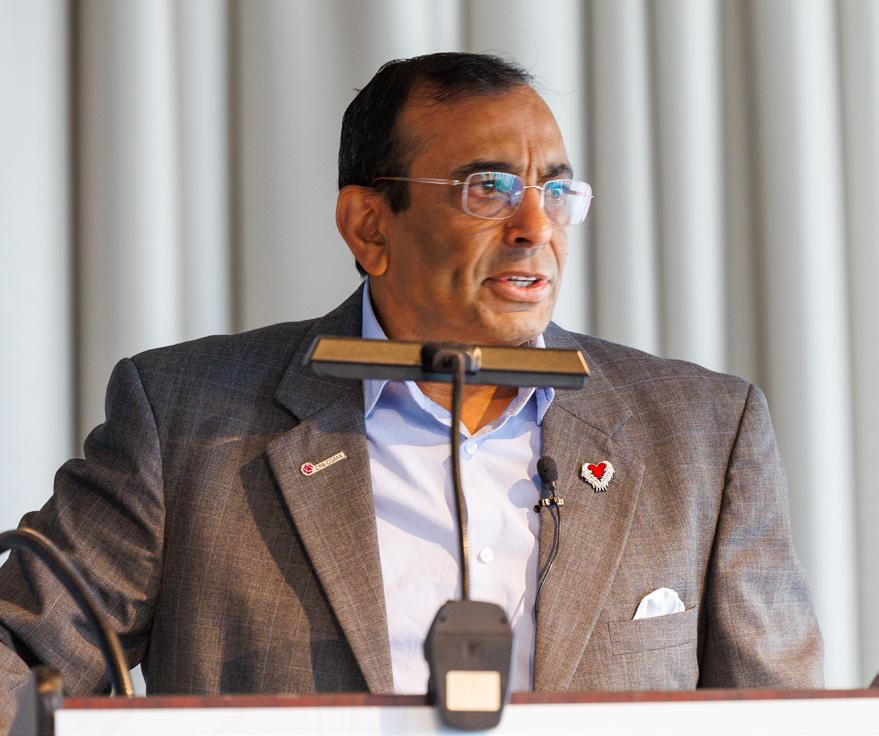

On the Cover

As the 104th ASCPA Board Chair, Paul Perry will lead strategic efforts of ASCPA’s 15-person board to support the profession. He is pictured on the cover with Past Chair Sarah Propper (far left) and Chair-Elect Kendra James (far right). Flip to page 8 to meet Paul.

The Alabama Society of CPAs is more than a membership —it’s your professional home at every stage of your career. From your first accounting class to your final day in the profession and beyond, we are your constant partner in growth, connection, and purpose.

We ignite potential, unlock leadership, and amplify your impact. Whether you are exploring the CPA path, climbing toward leadership, leading an organization, or shaping the future as a mentor — your Society surrounds you with the tools, the people, and the purpose to thrive.

By joining the Alabama Society of CPAs, you don’t just belong to a network — you belong to a movement. One that protects, strengthens, and reimagines the accounting profession for generations to come. Together, we build the future of the profession — one stage at a time.

I hope the newly revised ASCPA Member Value Proposition resonates with you. In that regard, this issue of Connections showcases several ways in which ASCPA supports your growth, professional education and protection.

With so much going on in the advocacy arena, I would like to highlight a couple of important issues. ASCPA leadership recently visited Congress, along with every state society and the AICPA, to discuss issues of importance to include STEM, expansion of 529 plan usage (now included in the comprehensive tax bill that is headed back to the House for final passage), Disaster Relief, and PTET. With each visit, members asked our opinion about various provisions of the federal tax bill. What does that tell us? It tells us that elected officials, whether federal or state, rely on CPAs for support and intelligence as it relates to tax, accounting, business, and economic development.

Each year, at both the state and federal levels, regular discussions occur among politicians, economists, tax practitioners and others about changing state and national tax systems. And each year, our goal is to protect the profession and the public by continuing to share the profession’s message about the importance of good tax policy, our guiding principles. Accountability to taxpayers, appropriate government revenues, certainty, economic growth and efficiency, effective tax administration, fairness and equity, information security, transparency, simplicity, and more are a part of this message. With legislation, sometimes we agree that good tax policy principles are met, and sometimes, we disagree. An example of where we disagree were the original PTET provisions in President Trumps tax bill.

The original PTET language would eliminate the ability of certain pass-through entities, including accounting firms, to take advantage of the state and local tax deduction. Specifically, the proposal newly subjects local entity level taxes to the individual SALT cap. The proposed tax legislation unfairly subjects specified service trades or businesses (SSTBs), such as accountants, doctors, lawyers, dentists, veterinarians, etc., to the individual cap on state and local income tax deductions at the federal level, regardless of partners’/owners’ income level or the state in which they live.

When comparing the tax treatment of state and local taxes for pass-through entities between the TCJA and this proposed bill, the sole change targeted pass-through service providers, who were already substantially limited under the qualified business income (QBI) deduction for SSTBs.

The profession spoke with one voice and was successful in convincing the U.S. Senate to remove the limit on pass-through businesses’ state and local tax (SALT) deductions entirely. We will now do the same in urging the U.S House of Representatives to join their Senate counterparts in preserving this important deduction. Our gratitude to you for answering our request to act and contact your member of Congress to express our concern. As for this writing, the bill passed the House, passed the Senate in the morning hours of July 2, and now moves back to the House for final passage.

One other important piece of news relates to the Uniform Accountancy Act (UAA). The boards of directors of the AICPA and the National Association of State Boards of Accountancy recently approved an expansion of accountancy’s model legislation to include an additional path to

CPA licensure. The approved amendments to the (UAA) add the option to earn CPA licensure with a bachelor’s degree, two years of professional experience, and passage of the CPA Exam.

The UAA will continue to allow CPA licensure with one year of experience, passage of the CPA Exam, and either a bachelor’s degree with 30 additional credit hours or a bachelor’s degree and a master’s degree. All paths require an accounting concentration at either the undergraduate or graduate level.

Other changes to the UAA also include a shift from state-based mobility to an individualbased practice privilege that maintains a CPA’s ability to practice across state lines with one license. (The Alabama State Board of Public Accountancy (ASBPA) already has this language.) The revised UAA also adds safe-harbor language that allows CPAs who were licensed under differing education, experience, and exam requirements as of Dec. 31, 2024, to continue to have practice privileges under mobility.

The ASBPA has begun its process to revise our Alabama law and rules to allow for the new, additional pathway. Our bill will be drafted with sponsors secured before the 2026 Regular Session of the Alabama Legislature commences. This effort will be a top priority of the ASCPA government relations team. To date, there have been sixteen states to pass this legislation with more to follow by the end of the year. As a suggestion to CPAs in public practice, please seek the instructions of any state where you may be working across state lines”. The safest thing may be for you to secure a reciprocal license in that state until we can fully implement the new mobility language across the country.

The UAA, jointly published by the AICPA and NASBA, provides state legislatures and state boards of accountancy with a national model that can be adopted in whole or in part to meet the needs of each individual jurisdiction. The updated UAA, according to the news release, maintains that oversight and disciplinary authority over licensees continues with state boards of accountancy.

The ASCPA staff and leadership are grateful for your support. If you have questions or if I can be of assistance to you, please feel free to contact me at jbirmingham@alabama.cpa.

Fellow Members,

It is with honor and privilege that I step into this role of Board Chair for the year, following and adding to a remarkable 100+ year legacy of former Chairs. Many of those individuals I have had the pleasure of knowing and learning from, and their wisdom continues to guide and inspire me. To follow in their footsteps and stand on their shoulders is a rare gift that I do not take lightly. Thank you first off to my good friends and immediate Past Chairs, Sarah Propper and James White, Jr. – thank you for showing me how it is done.

As we embark on this next year, I am thrilled with the opportunity to serve our community of CPAs and accounting professionals throughout the State. My commitment to you is one of visibility, understanding, and growth. I believe in the value of our Society (and the profession) and its potential to better each of us today, tomorrow, and years to come. I intend to work diligently, both at the local and national levels, to enhance the branding of our profession and to embody the “service above self” mentality that is so consistently preached by Rotarians.

Connect. Protect. and Educate. Those words hopefully resonate with you in terms of what the Society means to and does for you and your organizations.

Connect. The Society offers opportunities for you to connect with colleagues from all industries and corners of this great State. Whether you are looking for assistance, partnership or employment within the profession, there are a number of events that can help you make those connections that mean the most to you.

Protect. Often overlooked by many is the protection and advocacy purpose and task of the Society. When we are advocating for support and opposition to bills and legislature with the local or national governments, the Society is standing up for what is best for the profession and its members, to help with support, relief and clarity among the laws and regulations that impact our firms, businesses and individuals. When we are administering the peer review process for others, the Society is helping add to the notion of public trust of the profession.

Educate. As noted on page 14, there is a plethora of educational session offerings, taught by some of the most sought-after presenters, throughout each year to help add to your continued development and

knowledge for this ever changing (now more than ever) profession and service to others with the public trust in mind.

Education doesn’t begin once you’re a member. It started long before that. We also recognize the journey of young students applying themselves and garnering every opportunity to be successful. Our Educational Foundation offers scholarships to outstanding students every year, and this year was no different. Flip to page 16 to see the names of students who will fill the halls of your organization one day soon. (Should you be so lucky!)

I am excited about the opportunity to collaborate with Jeannine and her wonderful staff, who have shown continued dedication and support for our mission and values. Together, we will work to continue the significant work in promoting and continuing to elevate our profession.

There is an older country music song lyric that goes, “…sometimes you lead and sometimes you follow.” As Chair, I embrace the duality of this role, recognizing the times to lead with conviction and the moments to follow others. I look forward to the growth and development of the Society that will come from this balance.

Please do not hesitate to reach out if I can ever be of assistance to you and your organization in this, and future, roles. I look forward to meeting each of you at a future event, meeting or social gathering.

Now, “…heads down, pencils up, let’s get to work.”

MESSAGE FROM THE EDITOR

To better align with the evolving needs of our members and ensure we continue delivering the highest quality content, we are transitioning from a bi-monthly publication schedule to a quarterly format—publishing four issues per year instead of six.

Rest assured, each issue will continue to provide the same valuable content you’ve come to expect: timely updates, expert insights, essential resources, and stories that matter to our profession. This new schedule allows us to focus on deeper, more comprehensive coverage while maintaining our commitment to keeping you informed,

Thank you for being part of our community. We look forward to continuing to serve you

Megan G. Hughes, APR CONNECTIONS Editor mhughes@alabama.cpa

A well-run business starts with the right tools.

As a CPA, you know more than anyone how important a banking relationship is to a business. At CB&S Bank, we understand business and provide helpful tools to manage business finances for you and your clients.

Business Borrowing | Business Checking & Savings

Treasury Management Services | Merchant Services

Business Internet & Mobile Banking

Fraud Protection Services | Business Credit Card

When it comes to having helpful tools to manage your business finances, it’s important to have a bank that understands.

Give us a call at 877-332-1710 or scan the QR code for more information.

Meet Paul Perry

2025-2026 ASCPA Board Chair

The Alabama Society of Certified Public Accountants is proud to introduce the 104th Board Chair Paul Perry of Birmingham. As Chair, Perry will lead strategic efforts of our 15-person board to support the profession, and continue working with the Society to move our initiatives forward. Perry will serve a term as Chair for one calendar year, then will move into a past-president role. Dedicated to spending this year working strategically on leadership, growth, talent and technology, Perry has objectives in place and is ready to go to work for all ASCPA Members.

ASCPA: Where did you grow up?

Paul: Born in Clarksville, TN but grew up in Dothan, AL

ASCPA: When did you decide on accounting as a career?

Paul: I took an accounting class in high school and did not miss a single question on a test.

ASCPA: What advice would you give to a smart, driven college student about to enter the “real world”?

Paul: Raise your hand for things that are outside of your comfort zone and take every opportunity you are given. Don’t compare yourself to others but compare yourself to you yesterday.

ASCPA: What prompted you to enter public accounting instead of another sector?

Paul: It was intriguing to work on multiple clients instead of just working for one.

ASCPA: In the last five years, what new belief, behavior, or habit has most improved your life?

Paul: Learning that the answer is already No, so you might as well ask anyway. You will be surprised at the opportunities you are given. Make the most of them and be grateful.

ASCPA: What is one of the best or most worthwhile investments of time, money or energy you’ve ever made?

Paul: While my children would want me to say them (and they are probably right), being a lifelong learner would be the answer. Get every credential that will further

your knowledge and understanding of a subject matter. If you come across a conversation or topic you are unfamiliar with, take the time to read everything you can and become an expert.

ASCPA: When you feel overwhelmed or have lost your focus, what do you do?

Paul: Remind myself of my purpose and try to get back to trusting my process.

ASCPA: What’s your greatest takeaway from 2024-2025 year on the board?

Paul: Experiencing other peoples passion for the profession. When you serve others it is nice to know you are not alone.

ASCPA: What prompted you to become a member of the ASCPA? What benefits have you seen from being a member?

Paul: Once I passed my CPA exam it was just something you did. Benefits are definitely the connections and friendship you make with others in the profession. Also I think learning about the advocacy that goes on behind the scenes for CPAs.

ASCPA: Tell us about your family and life outside of work.

Paul: My wife Hilary and I have been together for more than two decades and have three wonderfully and ambitious children - Mallie Kate (13), David and Madeline (11). Life outside of work includes getting them to the next pageant, dance recital, cheerleading event, random practice, and chess tournament.

SALT CORNER

Alabama’s New Mobile Workforce/Remote Worker Safe Harbor

Alabama recently became the sixth state to enact a mobile workforce safe harbor designed to provide a brightline test and a 30-day safe harbor for employees and their employers when those employees who are not residents of Alabama spend a limited time working in the State. Act 2025-334 (H.B. 379). As we highlighted in our last column, Alabama was one of the many states that could require an employer to withhold tax and a nonresident employee to file a personal income tax return if the employee spent even one day performing services within the state.

Effective for tax years beginning on or after January 1, 2026, Compensation paid to a nonresident individual is not subject to Alabama payroll tax withholding by the employer and the employee is exempt from Alabama’s income tax if the following conditions are satisfied:

• the compensation was for employment duties performed in this state on 30 or fewer days in the calendar year;

• the nonresident individual performed employment duties in more than one state during the calendar year; and

• the nonresident individual’s state of residence either provides a “substantially similar exclusion” or does not impose an individual income tax (e.g., Tennessee, Texas or Florida), or the individual’s income is otherwise exempt from taxation by Alabama law or under the U.S. Constitution or specific federal statute.

Ala. Code § 40-18-2.2(b), added by Act 2025-334. Alabama’s new safe harbor was based on model legislation drafted and supported by the Council On State Taxation (“COST”), the American Institute of Certified Public Accountants (“AICPA”) and other business associations.. Similar to the model legislation, the safe harbor and the exemption from income tax do not apply to three new classes of highly compensated individuals – professional athletes, professional entertainers, and public figures who receive compensation on a per-event basis. Ala. Code § 40-18-2.2(b)(3).

The initial version of the bill provided for a 24 day threshold (Georgia has a 24 day threshold but it is applied on a quarterly – not annual – basis). Thanks to efforts by COST, the Alabama Society of CPAs, the AICPA, and other business associations, an amendment was adopted in the House Ways and Means Education Committee to increase the threshold to 30 days, in line with the model legislation.

Once the 30 day threshold is exceeded in any given calendar year, however, the employer is required to begin withholding and remit Alabama income taxes for every day (including the first 30 days) the employee performs employment duties in Alabama. Ala. Code § 40-18-2.2(c). Alabama’s safe harbor – like the model legislation –provides for a waiver of interest and penalties for failing to withhold income taxes if the employer meets either of the following conditions:

• reliance on information from a “time and attendance system” that tracks where employees perform services on a daily basis (which is maintained at the discretion of the employer), or

• reliance on the employee’s annual determination of time the employee expects to spend working in Alabama (with appropriate carve-outs for collusion or actual knowledge of fraud on the part of the employee in making such determination).

Finally, another important feature added by a second committee amendment, at the request of the Alabama Society of CPAs, was an exemption for employers who send nonresident employees into Alabama to conduct disaster relief efforts on a temporary basis (regardless of the number of days spent performing services in Alabama). Thanks to the amendment, all nonresident individuals who provide disaster relief services in Alabama will now be covered by the exemption, regardless of the 30-day threshold.

A special thanks to your new Director of Governmental Affairs, Rob Pearson, a Demopolis CPA in his former life, for his diligent efforts in having the 2 critical amendments made to the bill. If a reader has any questions about the new Act, please email us at jelong@bradley.com or bely@bradley.com.

Since 1967, the ASCPA’s Educational Foundation has been providing support to students majoring in accounting at Alabama colleges and universities. Over time the scholarship amounts have grown from $500 to $2,500. The process of selecting scholarship recipients each year is the Foundation’s most visible activity. Each Spring our college and university contacts are asked to share our online application with their students. The application requires the student write an essay and share their journey. Our Educational Foundation and its mission to promote CPA careers through educational scholarships is just as vital now as it was in 1967. Thank you for your continuing support of that mission and in the nurturing of future Alabama CPAs.

Congratulations to all our scholarship winners! Applications are accepted each year for scholarships beginning on December 1. Applications close on March 1 and recipients are typically notified no later than May 1.

RECIPIENTS

Josue Alvarez University of Alabama in Huntsville

Grace Aragon Auburn University at Montgomery

Alden Barentine Troy

Mary Berry University of South Alabama

Shelby Irwin Montevallo

Jimena Lugo Martinez University of Alabama in Huntsville

Kiona McCallister University of West Alabama

Abigail McElwee University of North Alabama

Desiree Moreno Troy

La’Porsha Bowman Auburn University at Montgomery

Alexander Clifton Spring Hill

Aaliyah Daniels Montevallo

Rabia Dewani University of Alabama

Nic Glass University of South Alabama

Jad Hakim University of Alabama at Birmingham

Ryan Mukendi University of North Alabama

Amiah Murry University of Alabama in Huntsville

Khong Nguyen University of Alabama

Riina Niemeyer Athens State University

Pamela Palmer-Wiggins Auburn University at Montgomery

Allison Roberts Huntingdon

Blake Smith Samford

Kaitlin Shook Auburn University

Victoria Speake Auburn University at Montgomery

Mark Swayer Jacksonsville State

with BMSS job SHADOW SHADOW

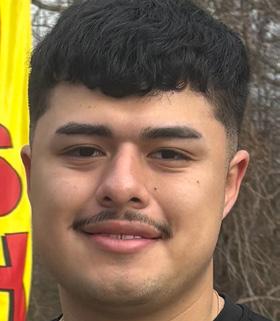

Last year Cheyenne Sandlin, Manager with BMSS in Huntsville, participated in a presentation during Accounting Opportunities Week at a local high school. Angel Garcia, a student who heard Cheyenne’s presentation, reached out after the presentation about setting up a job-shadow experience. Last month Angel spent three days with the Huntsville firm and got an inside look at accounting. ASCPA chatted with Angel after her time “on the job” - check out our conversation!

Q: Where will you attend school in the Fall?

A: I graduated from East Limestone High School this past May and I am going to Calhoun in the Fall.

Q: When did you job shadow and who did you meet while doing so?

A: I job shadowed from June 911. I met a variety of BMSS

members who all brought something to the table. On Monday, I met with members of the audit team and learned about the different auditing tools they use. Tuesday was understanding what CAS and government contracting entailed. Wednesday was everything taxes, which was very interesting.

Q: What was the most surprising thing you learned while “on the job”?

A: There were a variety of personalities in the office. Everyone brings something to the table! I was also surprised how important time management is in this field.

Q: What was your favorite part?

A: It had to be understanding that everyone is on the same boat. If you are stuck on an assignment, there is someone to be a fresh set of eyes and help you.

Q: What was your least favorite part?

A: I was so anxious the first daybut the moment I got out of my head and realized everyone is just trying to make it to the end of the day, I relaxed. I was more receptive to people. Everyone was once an awkward teenager and they were very welcoming.

Q: How did this experience change your opinion of Accounting?

A: I believe the media gives off a very outdated perception of what accounting is. It will never be a glamorous job, but it is much less strict and dull as people make it out to be. I came in with the assumption that I would be dozing off in a cold office next to a stack of binders that were piling up dust. In reality, I was fascinated

by just how much goes into accounting. It was so satisfying being able to understand how they got to a certain result in a project. There are so many tools and programs that I learned about in my time there.

Q: Would you recommend others job shadow as well?

A: Absolutely! Whatever it is that you’re interested in, pursue it. Research and get in contact with someone in the space. I am very reserved and introverted, so job shadowing was something out of my comfort zone. Everyone was so welcoming that dispelled any doubts that I was meant to be in accounting. I couldn’t be more grateful to have experienced this.

Q: What are your plans for the future?

A: I’m hoping to finish Calhoun and transfer to a university to do two more years. I would also like to do an internship at an accounting firm while I’m studying! Hopefully these next few years will be prosperous and full of growth.

Q: What is your hometown?

A: I was born in Huntsville, but I grew up in the Limestone county area.

Do you host students at your organization? Or have a pipeline story you’d like to share? Let us know! Contact CONNECTIONS Editor Megan Hughes at mhughes@alabama.cpa.

Pictured (L-R): Cheyenne Sandlin, Manager; Josh Corbin, Staff B; Andrew Clark, Staff B; Angel Garcia, Job Shadow Student; Madison May, Manager; Jessica Fair, Supervisor.

CPE WITH ASCPA

Welcome back to CPE with the Alabama Society of CPAs!

On the next few pages, you will find a listing of our CPE programming for the remainder of the year, including live webcasts, webinars, in-person events and hybrid events featuring in-person and virtual attendance options.

As you know, we have renewed our partnership with CPA Crossings to bring you ALOnDemand, a platform designed to bring many more On-Demand courses to your fingertips!

We have a list of CPE FAQs on our website which address accessing your ASCPA account, logging into a CPE course, and finding your transcript. There is also a section on surveys, which must be completed within 7 days after a course in order to process CPE certificates. Please read over this short FAQ page, which can be found at alabama.cpa/cpe-faq, to ensure you are ready to conquer the 2025 CPE Season.

New Quality Management Standards: ResourcesExpectations for Firms and Engagement Partners

Virtual

7/8/2025 (12-1 PM)

AICPA Speaker | 1 A&A

S Corporations vs. LLCs and Partnerships: Strengths and Weaknesses

Virtual

7/14/2025 (8:30 AM-12 PM)

Greg Carnes 4 Tax

New Quality Management

Standards: What’s New for Firms’ Monitoring and Remediation Processes

Virtual

7/15/2025 (12-1 PM)

AICPA Speaker | 1 A&A

SQMS Is Here: Are You Ready?

Virtual

7/15/2025 (8:30 AM-12 PM)

Jim Martin 4 A&A

50 Reasons to Fire a Client

Virtual

7/15/2025 (1-4:30 PM)

Jim Martin 4 Other

K2’s Microsoft 365/Office 365All the Things You Need to Know

Virtual

7/15/2025 (9 AM-4:30 PM)

K2 Speaker | 8 Other

A&A Update

Virtual

7/16/2025 (8:30 AM-12 PM)

Mike Brand | 4 A&A

K2’s Excel Charting and Visualizations

Virtual

7/17/2025 (9 AM-12:30 PM)

K2 Speaker | 4 Other

K2’s Best Word, Outlook, and PowerPoint Features

Virtual

7/17/2025 (1-4:30 PM)

K2 Speaker | 4 Other

2025 Summer Education Conference In-Person

7/20-7/25/2025 (8-11:40 AM)

Various | 4 Tax, 10 A&A, 6 Other

New Quality Management

Standards: Bringing It All Together- Exploring All Components of a Quality Management System

Virtual

7/22/2025 (12-1 PM)

AICPA Speaker | 1 A&A

Domicile or Disaster?

Navigating Tax Risks When Moving Before a Big Payday + Handling Your Remote Workers.

Virtual

7/23/2025 (10-10:50 AM)

Bruce Ely & Will Thistle | 1 Tax

What’s Changing in A&A for Governmental Entities

Virtual

7/29/2025 (8:30 AM-12 PM)

Melisa Galasso 4 A&A

K2’s Microsoft Teams

Virtual

7/29/2025 (9 AM-12:30 PM)

K2 Speaker 4 Other

K2’s Artificial Intelligence for Accounting and Financial Professionals

Virtual

7/29/2025 (1-4:30 PM)

K2 Speaker 4 Other

GPT and Prompt Engineering for CPAs

Virtual

7/30/25 (8:30-10:10 AM)

Marc Hamilton | 2 Other

K2’s Advanced QuickBooks Tips and Techniques

Virtual

7/30/2025 (9 AM-12:30 PM)

K2 Speaker 4 Other

International Tax Primer Series: Individuals Living/Investing Outside the US

Virtual

7/30/2025 (10-11:40 AM)

Alex McGowin | 2 Tax

Excel CoPilot for Financial Automation and Reporting

Virtual

7/30/25 (10:20 AM - 12:10 PM)

Marc Hamilton | 2 Other

Power Query: Automating Data Cleanup and Report Preparation

Virtual 7/30/25 (1-2:40 PM)

Marc Hamilton | 2 Other

Power Automate for Accounting Workflows

Virtual 7/30/25 (2:50-4:30 PM)

Marc Hamilton | 2 Other

Accounting for Difficult Transactions: Deferred Taxes, Pensions, and Accounting Changes & Errors

Virtual 7/31/2025 (8:30 AM-12 PM)

Josh McGowan | 4 A&A

How to Make Your Clients’ Financial Statements Come Alive Virtual

8/5/2025 (10-11:40 AM)

Ruth King | 2 A&A

Taxation of Real Estate Transactions Virtual 8/6/2025 (8:30 AM-12 PM)

Greg Carnes | 4 Tax

Lisa McKinney’s Tax Update

Virtual 8/6/2025 (8:30 AM- 12 PM)

Lisa McKinney 4 Tax

Common Misappropriation and Fraud in Financial Reporting Schemes Virtual 8/7/2025 (8:30 AM-12 PM)

Jim Martin | 4 A&A

Success Skills Series: Team Collaboration and Leadership Virtual 8/7/2025 (1-2:40 PM)

Joel Hughes | 2 Other

City Visit: Birmingham In-Person 8/13/2025 (8:30 AM-4 PM)

Josh McGowan | 8 A&A

City Visit: Tuscaloosa In-Person 8/14/2025 (8:30 AM-4 PM)

Josh McGowan | 8 A&A

Internal Control Best Practices

Virtual

8/14/2025 (8:30-10:10 AM)

Melisa Galasso | 2 A&A

Topic 842: Implementing Leases Workshop

Virtual

8/14/2025 (8:30-10:10 AM)

Melisa Galasso | 2 A&A

SAS 145: Risk Assessment

Virtual

8/14/2025 (1-1:50 PM)

Melisa Galasso | 1 A&A

Treasury Management for CPAs: Enhancing Liquidity and Risk Control

Virtual

8/19/2025 (8:30-10:10 AM)

Marc Hamilton | 2 A&A

Forecasting and Cash Flow Modeling with Excel and AI

K2’s Excel Tips, Tricks, and Techniques for Accountants

Virtual

8/20/2025 (9 AM-4:30 PM)

K2 Speaker | 4 Other, 4 A&A

Private Equity and the Accounting Industry

Virtual

8/20/2025 (10-11:40 AM)

Josh McGowan | 2 Other

B&I Roundtable Series: Update On All Things Technology

Virtual

8/20/2025 (12-1 PM)

Paul Perry | 1 Other

2025 Prep, Comp & Review (SSARS) Update for the Local Firm

Virtual

8/21/2025 (8:30 AM-12 PM)

Jim Martin | 4 A&A

K2’s QuickBooks for Accountants

Virtual

8/21/2025 (9 AM-4:30 PM)

K2 Speaker | 4 Other

Auburn Sip & CPE In-Person

8/21/2025 (3-5 PM)

Amanda Senn | 2 Ethics

Common Peer Review Issues: Learn from Others

Virtual

8/22/2025 (8:30 AM-12 PM)

Jim Martin | 4 A&A

Lessee Implementation Issues for Operation Leases: The Questions Some Are Having

Virtual

8/22/2025 (1-4:30 PM)

Jim Martin | 4 A&A

QM Standards Update

Virtual

8/25/2025 (10-11:40 AM)

Mike Brand | 2 A&A

City Visits: Huntsville In-Person

8/25/2025 (8:30 AM- 4 PM)

Mike Brand | 8 A&A

Sales and Use Tax Workshop

Virtual

8/26/2025 (1 PM-4:30 PM)

Bruce Ely, Will Thistle | 4 Tax

International Tax Primer Series: Correcting Delinquent International Information Reporting

Virtual

8/27/2025 (10-11:40 AM)

Alex McGowin | 2 Tax

2025 AICPA Regulatory Ethics Update

Virtual 9/11/2025 (3:30-5:10 PM)

Melisa Galasso | 2 Ethics

Cybersecurity and Data Protection for CPAs

Virtual 9/16/2025 (8:30-10:10 AM)

Marc Hamilton | 2 Other

City Visits: Decatur In-Person

8/27/2025 (8:30 AM- 4 PM)

Mike Brand | 8 A&A

City Visits: Florence In-Person

8/28/2025 (8:30 AM- 4 PM)

Mike Brand | 8 A&A

City Visits: Mobile In-Person

9/10/2025 (8:30 AM- 4 PM)

Josh McGowan | 8 A&A

City Visits: Montgomery In-Person

9/11/2025 (8:30 AM- 4 PM)

Josh McGowan | 8 A&A

2025 Governmental Auditing Update: Yellow Book & Uniform Guidance

Virtual

9/11/2025 (8:30-11:10 AM)

Melisa Galasso | 3 A&A

2025 Not-For-Profit Accounting & Auditing Update

Virtual

9/11/2025 (12:30-3:10 PM)

Melisa Galasso | 3 A&A

Mastering Microsoft 365 for CPA Efficiency

Virtual 9/16/2025 (10:20 AM-12 PM)

Marc Hamilton | 2 Other

Practical Applications of AI in CPA Workflows

Virtual 9/16/2025 (1-2:40 PM)

Marc Hamilton | 2 Other

Internal Controls for Small Organizations

Virtual 9/16/2025 (2:50-4:30 PM)

Marc Hamilton | 2 A&A

Lisa McKinney’s Tax Update

Virtual 9/17/2025 (8:30 AM-12 PM)

Lisa McKinney | 4 Tax

Ethics: A Cornerstone for Accounting

Virtual 9/17/2025 (10-11:40 AM)

Mike Brand | 2 Ethics

2025 Real World Ethics Update for All Practitioners

Virtual 9/18/2025 (1-2:40 PM)

Jim Martin | 2 Ethics

CPE WITH ASCPA

Montgomery Sip & CPE

In-Person

9/18/2025 (3-5 PM)

Amanda Senn | 2 Ethics

2025 Real World Ethics: Statements on Standards for Tax Services

Virtual

9/19/2025 (1-2:40 PM)

Jim Martin | 8 A&A

A&A for Tax People Who Absolutely Detest A&A

Virtual

9/22/2025 (8:30 AM-4:30 PM)

Jim Martin | 8 A&A

Ethical Failures: 2025 Edition

Virtual

9/22/2025 (10-11:40 AM)

Josh McGowan | 2 Ethics

2025 A&A Update for the Real World

Virtual

9/23/2025 (8:30 AM-4:30 PM)

Jim Martin | 8 A&A

K2’s Next Generation Excel Reporting

Virtual

9/23/2025 (9 AM-4:30 PM)

K2 Speaker | 8 A&A

Success Skill Series: Resilience and Stress

Virtual

9/23/2025 (1-2:40 PM)

Joel Hughes | 2 Other

Hobby v. Business: What Your Clients with Small Businesses Need to Know

Virtual

9/24/2025 (10-11:40 AM)

Jim Martin | 2 Tax

New Tax Acts in 2025

Virtual

9/24/2025 (1-2:40 PM)

Jim Martin | 2 Tax

K2’s Mastering Advanced Excel Functions

Virtual

9/24/2025 (9 AM-12:30 PM)

K2 Speaker | 4 Other

K2’s Implementing Internal Controls in QuickBooks Environments

Virtual 9/24/2025 (1-4:30 PM)

K2 Speaker | 4 A&A

Int’l Tax Primer Series: U.S. Taxation on Foreign Investment/Immigration to U.S.

Virtual

9/25/2025 (10-11:40 AM)

Alex McGowin | 2 Tax

2025 Financial Accounting & Auditing Conference

Hybrid

9/26/2025 (10-11:40 AM)

Various | 8 A&A

Income of Trusts and Estates

Virtual 9/29/2025 (8:30 AM-12 PM)

Greg Carnes 4 Tax

CPE at Sea In-Person

10/11- 10/19/2025

Various | 8 A&A, 12 Other

Spiirall Leadership Program In-Person

11/3-11/4/2025 (8 AM- 4:30 PM)

Erin Crowley 16 Other

Sales & Use Tax Workshop

Virtual

11/5/2025 (10-11:40 AM)

Bruce Ely, Jimmy Long, and Will Thistle | 2 Tax

K2 AI Conference

Virtual 11/7/2025 (8:30 AM-4:30 PM)

Various | 8 Other

2025 Alabama Federal and State Tax Institute

Hybrid

11/12-11/14/2025 (8:30 AM-12 PM)

Various | 20 Tax

2025 Federal and State Tax Update for Local Practitioner

Virtual 11/18/2025 (8:30 AM-4:30 PM)

Jim Martin | 8 Tax

K2 Technology Conference

Virtual

11/18-11/19/2025 (8:30 AM-4:30 PM)

Various | 16 Various

K2 Excel Conference

Virtual

12/3/2025 (8:30 AM-4 PM)

Various | 8 Other

2025 Governmental Accounting & Auditing Forum

Hybrid

12/8-12/10/2025

Various | 8 A&A, 2 Ethics, 2 Tax, 4 Other

ALOnDemand

ASCPA is continuing its partnership with CPA Crossings to offer an ondemand learning solution called ALOnDemand. More than 140 curated courses are available covering a wide range of topics in accounting and auditing, tax, technology and more. A subscription is available to ASCPA members that provides unlimited access to all ALOnDemand courses during the calendar year and unlimited CPE credits. To learn more visit alabama.cpa/ALOnDemand.

Whether you call them “soft” skills, success skills, or leadership development skills, ASCPA has a host of offerings to help members and

non-members alike become more efficient and effective professionals. Register today at alabama.cpa/leadership.

Success Skills Series

Live Webcasts from 1-2:40 PM offering 2.0 Personal Development CPE

Led by Joel Hughes, Troy University

August

7:

Team Collaboration & Leadership

This presentation explores the concept of teamwork, emphasizing the transition from individual focus “ME” to collective success “WE”. The journey from individual achievement to interdependence is crucial for effective team dynamics. The presentation dives into Tuckman’s Model of Group Development, outlining the four stages of group development to achieve optimal performance. the presentation emphasizes the shift from individualism to teamwork, illustrating how collaboration and interdependence are key to a team’s growth and success.

September 23: Resilience & Stress

This course provides a comprehensive exploration of stress, its causes, symptoms, and the stages it goes through, along with effective techniques for managing and reducing stress in both personal and professional life. Additionally, this course empowers you to develop techniques of resiliency in effort to grow the ability to adapt and better understand stress, recognize its early signs, and apply effective techniques for managing it in a healthy way.

The Human Ledger: Spiirall’s 2-Day Leadership Skills Series

The Human Ledger is a high-impact, 16.0 CPE-certified two-day experience designed specifically for accounting professionals who want to sharpen their communication, elevate their leadership, and finally learn how to delegate without breaking into a sweat.

Across two interactive, immersive days, we’ll explore the real blocks behind your technical success. Can your team speak up without fear? Do you build trust or just expect it? Do you create a flow of work or take it all on yourself? Are you leading, or are you micromanaging in a spreadsheet costume?

This program brings the “soft skills” to life with real talk, real tools, and a dash of weird that makes it all stick. We’ll explore concepts like:

• Psychological safety (why silence might be your biggest liability)

• Trust as a formula (yes, there’s an actual equation)

• Delegation that doesn’t boomerang

• Managing your energy like a true professional

• Giving feedback that actually gets heard (without a compliment sandwich)

WHAT TO EXPECT

• Laughs. Lessons. A few uncomfortable but growth-filled moments.

• Highly interactive sessions with smallgroup work, personal reflection, and practical frameworks.

• Tangible takeaways you’ll use right away—no fluff, no filler.

WHO THIS IS FOR

Senior associates, managers, and anyone else tired of the phrase “just give them feedback” with no roadmap for how. You’ve already mastered the technical. Let’s master the human.

ASCPA Leadership Development Academy

Fast Track Your Future-Ready Leaders! The Alabama Society of CPAs has partnered with the AICPA to introduce the ASCPA Leadership Development Academy.

This is a dynamic and customizable 18.0 CPE leadership program designed to empower professionals with 2-7 years of experience in Accounting or Finance who are ready to lead with purpose. This Academy offers a proven framework to enhance your personal strengths, develop high-performing teams, and lead your organization with strategic vision.

The program is structured into three levels:

• High Potential Staff: for new professionals eager to accelerate their growth

• Talented Managers: for team leaders ready to expand their leadership impact

• Experienced Leaders: for senior professionals preparing for executive roles

Each level includes industry-recognized tools like StrengthsFinder, DISC assessment, emotional intelligence training, and moreall facilitated by top AICPA thought leaders and tailored to meet your specific goals.

Key focus areas include:

• Self-awareness and personal leadership development

• Engaging and motivating highperforming teams

• Strategic Thinking

• Business Development

• Innovation

What you receive:

• 7 interactive online webcasts

- 10AM-12:30 PM, 2.0 CPE each webcast

- September 3, 5, 10, 12, 17, 19, and 24

- Each webcast subject matter is available online

• Final session will be held in person at the Alabama Society of CPAs September 30, 9 AM - 3 PM

- Graduation ceremony and certificate

- Individual headshot and group picture with all graduates

- ASCPA Leadership Development

COVERING

Meet the TEAM leading you HOME this year, and learn about

THE BASES

new initiatives and strategies they’ll be PUTTING INTO PLAY.

ASCPA’s Bold Game Plan: A

Three-Year Strategy to Hit It Out of the Park for the Profession

The Alabama Society of CPAs (ASCPA) has developed a forward-thinking three-year strategic plan that aims to strengthen the CPA profession in Alabama while creating a meaningful, lifelong professional home for its members. Built around growth, connection, leadership, and innovation, the plan is centered on addressing the evolving needs of CPAs across every stage of their careers.

Shifting Membership Needs: From Compliance to Connection

ASCPA’s members are transforming. Historically, the typical member has been a mid-to-late career CPA, primarily motivated by continuing education and licensure requirements. However, the profession is changing, and so are its members. The next generation of CPAs, now in their early to mid-careers, values leadership development, mentorship, networking, and societal impact just as much as technical competence.

Recognizing this, ASCPA’s value proposition is clear:

“A Lifelong Professional Home: Advancing You. Elevating the Profession.”

ASCPA is committed to supporting its members from their first accounting class to retirement and beyond. This commitment positions the Society not just as a service provider but as a vital career partner.

The Five Strategic Goals Driving ASCPA’s Future

1. Strengthen Career-Stage Relevance and Retention

To ensure members find consistent value throughout their careers, ASCPA will develop tailored programs for each career stage. This includes a structured onboarding journey, student summits, legacy roundtables, and targeted retention efforts, aiming for a 25% increase in overall retention.

2. Expand Leadership Development and Mentorship

ASCPA will become the leading hub for leadership growth by launching a mentorship initiative and a career-stage

leadership track, and creating a “Lead to Legacy” speaker bureau. These efforts will connect over 500 members annually through leadership and mentoring activities.

3.

Deepen Member Belonging and Community Connection

The Society plans to design a 90-day new member onboarding experience and host an annual “Society Day” for over 1,000 members. By focusing on increasing community connection, ASCPA aims to significantly improve its…..

4. Champion the Pipeline and the Profession’s Public Policy Voice

ASCPA will continue to strengthen its advocacy by growing student outreach, expanding its CPA Exam candidate pipeline, and increasing member participation in public policy initiatives. The Society will publish a quarterly CPA Public Impact Report to elevate the profession’s public presence.

5. Cultivate Thought Leadership and Innovation

ASCPA will position itself as a thought leader by launching a digital hub featuring original content, a new Government Relations podcast producing annual “State of the Profession” reports, and developing an Innovation Lab that fosters collaboration between students and mid-career professionals.

A Focused One-Year Launch Plan for 2025-2026

The Society’s first year of implementation will prioritize four key initiatives:

• Firm Membership Model: A new structure allowing firms to enroll all employees under a bundled membership, starting with a pilot group of firms.

• New Revenue Sources: Diversifying income beyond CPE and dues, including launching 1-2 new revenue-generating initiatives.

• Career-Stage Branding: Tailoring communication and services to five distinct career stages, from students to retired professionals.

• Member and Non-Member Survey: Capturing feedback to inform future strategies and ensure ASCPA remains aligned with member needs.

Each initiative is supported by clear metrics to track progress and ensure accountability.

A Society for the Future

Through this strategic plan, ASCPA is preparing to lead the profession into a new era. By focusing on relevance, leadership, connection, advocacy, and innovation, the Society is creating a more inclusive, engaging, and future-ready community for Alabama CPAs.

In doing so, ASCPA is not just responding to change — it is shaping the future of the profession.

The Alabama Society of CPAs (ASCPA) has laid out a focused, action-driven roadmap for the next year, designed to expand value for members, grow revenue opportunities, and strengthen the Society’s position as a lifelong professional home. This oneyear plan is centered on four key goals, each carefully structured to deliver measurable results and meaningful impact.

Goal 1: Launch a Firm Membership Model

ASCPA is working to create a firm-based membership option that will allow entire accounting firms to enroll all of their employees under one bundled membership. This new structure is designed to make it easier for firms to provide professional development opportunities and support to their entire teams, not just individuals. By streamlining the membership process and offering pricing tiers that fit firms of different sizes, ASCPA can encourage broader participation and create deeper, more meaningful relationships with accounting firms across Alabama. This model will be piloted with a small group of firms first, and based on their feedback, the Society will fine-tune the program before rolling it out to the wider membership base. The goal is to build stronger firm engagement, improve member retention, and ultimately grow the Society’s reach.

Goal 2: Identify and Recommend New Revenue Sources

To ensure long-term financial health and reduce reliance on traditional income streams like dues and continuing professional education (CPE) fees, ASCPA is actively looking to develop new revenue opportunities. This process will begin with a thorough financial review and an analysis of how similar organizations generate additional revenue. The team will brainstorm a variety of creative options, carefully evaluate each for profitability and alignment with ASCPA’s mission, and select the most promising ideas to pilot. These new revenue sources could include partnerships, events, sponsorships, or innovative member services. The ultimate aim is to create a more sustainable financial foundation that can support the growth and future initiatives of the Society.

Goal 3: Develop a Career-Stage Branding Strategy

ASCPA recognizes that its members have different needs, goals, and challenges depending on where they are in their professional journeys. To better serve its diverse membership, ASCPA plans to create a tailored branding and communication strategy that is

customized by career stage. This means understanding and addressing the unique interests of students, early-career professionals, mid-career CPAs, firm leaders, and retirees. By developing segmented messaging and targeted campaigns, ASCPA can offer more personalized support, provide relevant resources, and ensure that members see the value of the Society at every phase of their careers. This strategy will help deepen engagement and build a stronger sense of community.

Goal 4: Conduct a Member and Non-Member Survey

ASCPA is committed to listening to the accounting profession and staying attuned to its evolving needs. To support this, the Society will conduct a comprehensive survey of both members and non-members. The goal is to capture a wide range of perspectives on what professionals value most, what gaps exist, and how ASCPA can better serve its community. By gathering data from a broad, diverse group of respondents, the Society can make more informed decisions and design programs that truly reflect the needs of its members and the larger profession. The survey results will directly inform ASCPA’s strategic planning for future years and help generate new ideas for member services and engagement.

The survey will launch in late August, remain open for roughly three weeks, and close mid-September. Watch for email communication from ASCPA regarding how to participate in the survey in the coming weeks.

Aug. 27 Sept. 3 Sept. 16 Sept. 19

Meet the 2025-26 ASCPA Board of Directors. (Back Row, L-R) Chair Paul Perry, Jamey Carroll, Bradley Rayborn, Brian McLeod, Chair-elect Kendra James, Sherman Pitts, Past Chair Sarah Propper. (Front row, L-R) Matthew Hilburn, Jennifer Forrester, Lyndsey Dixon, Cathy Dover. Not pictured: Bruce Fryer, Jeremy Mosteller, Cam Pearce, and Dennis Sherrin.

“

Should I disclose my use of gen AI to clients?

The use of generative AI by accountants is increasing and leading to questions such as, “Should we inform our clients about our use of generative AI? If so, how?”

By CNA Accountants Risk Control

In today’s rapidly evolving technological landscape, the use of generative AI is gaining currency in the accounting profession. Not only are CPA firms integrating generative AI into administrative workflows, but a growing number of firms are investigating how deploying generative AI can help them more efficiently deliver solutions to clients. Generative AI options range from publicly available platforms to custom-built systems and include essential programs that also make use of generative AI, such as technical research software. Regardless of the platform or software, CPAs are increasingly asking, “Should we inform our clients about our use of generative AI, and if so, how?“

Legal and Ethical Compliance

The analysis starts with assessing whether compulsory requirements exist. The current legal environment is disjointed, and no specific federal law or professional standard applicable to CPAs mandates disclosure when generative AI is used or if client data is used within it. Consider this patchwork of laws, to name a few:

• The Gramm-Leach-Bliley Act, through the Federal Trade Commission’s Privacy Rule and Safeguards Rule, requires “financial institutions” — which includes CPA firms — to safeguard nonpublic personal information and take steps to ensure that their affiliates and service providers safeguard customer information in their care;

• Some states, including California and Utah, have enacted laws that require some level of disclosure around the use of generative AI;

• Existing state consumer/data privacy laws may apply to client data used in generative AI models; and

• Firms that are subject to the European Union’s General Data Protection Regulation may need to consider the recently enacted EU Artificial Intelligence Act.

On the ethics side, outside of the “Confidential Client Information Rule” included in the AICPA Code of Professional Conduct (the Code), tax preparers subject to AICPA Statements on Standards for Tax Services must also comply with Section 1.3, Data Protection, and make reasonable efforts to protect taxpayer information

shared with others.

The legal landscape will likely continue to shift, and future legislation and/or standards may address the disclosure question. Unless a firm’s offices and/or clients are 100% intrastate, it is unlikely that one single disclosure rule will apply. Consequently, as part of ongoing diligence, firms should periodically engage legal counsel to identify laws that may require disclosure to clients, and then ensure any disclosure is compliant.

Trust and Transparency

If, after consultation with an attorney, a CPA determines there is no disclosure requirement, consider the utility of a transparent, voluntary disclosure that tells clients when and how generative AI is used. Being transparent can engender a client’s trust when the CPA is willing to be upfront about how they use generative AI to deliver services and how the firm protects client information — both important to most clients.

Quality of work product

For some clients, expected use of generative AI by their CPA will be a given. Other clients may fully reject its use either on privacy or quality grounds. Regardless of client preference, the limitations of generative AI are such that no CPA should blindly rely on its outputs. This conclusion is echoed in the American Bar Association (ABA) Formal Opinion on Generative Artificial Intelligence Tools (July 29, 2024) (the ABA Opinion), which states that a lawyer’s reliance on a generative AI tool’s output without independent verification or review could violate the duty of competent representation. The lack of an authoritative, generative AI-specific standard applicable to CPAs is not likely to help defend a negligence assertion that the work was not properly reviewed prior to delivery to the client.

Data protection

CPAs using generative AI can anticipate clients inquiring about a number of areas, including how their information is stored; whether their data is used to further train the generative AI model; who has access; whether their data is shared outside of your organization; how data is retained, by both the firm and any external provider(s); and whether the generative AI has deidentification procedures for stored information. Before you pay to license any

generative AI software or major application utilizing generative AI, ask the provider about how they protect client information, understand the contract terms (especially risk transfer and data ownership), review the provider’s responsibilities in the event of a data security incident, and make sure your questions are answered to your and/or your IT professional’s satisfaction.

If a firm develops its own generative AI, consider the topics above both from an operational risk perspective and possibly from a buyer’s perspective. Although internally developed generative AI may appear to lack third-party disclosure concerns, firms may wish to monetize their investment in internally developed technologies and may ultimately choose to license or sell their generative AI. Or they may simply be the target in a CPA firm mergers-and-acquisitions transaction. Client data used in creating generative AI platforms raises unique intellectual property questions, and these and other questions about future transactions involving internally developed generative AI are novel.

Risks

when transparency is lacking

With any new, cutting-edge technology, there is a level of wariness until it is understood and accepted. If a CPA overrelies on generative AI output and that overreliance is coupled with a failure to disclose generative AI use upfront, the client may interpret this as an intentional deception. In the event of a loss, the combination of new tech distrust and suboptimal work product may result in a plaintiff’s argument that the CPA lacked subject matter competence or, in the extreme, the CPA fraudulently misrepresented their service capabilities.

Both quality and data concerns should prompt CPAs to consider what happens to client trust if the client learns that generative AI was part of their service without their knowledge or their data was used in generative AI without their explicit consent. It may be worth erring on the side of caution through client disclosure and consent. Disclosure gives the client the ability to make an informed decision on whether they want to proceed with services that use generative AI, and consent gives them control over their information shared with the model.

Creating Disclosure and Consent

In the absence of a controlling professional standard, CPAs who opt to create disclosures and consents may wish to consider the guidance included in the ABA Opinion. The ABA Opinion requires a generative AI-use consent be an informed consent, and explicitly notes that “merely adding general, boiler-plate provisions to engagement letters purporting to authorize the lawyer to use generative AI is not sufficient.” The difference between consent and informed consent perhaps can be best understood by comparatively examining the descriptions of general and specific consent found in ET Section 1.110.010, Conflicts of Interest for Members in Public Practice, paragraph .13 of the Code. Specific consent is deemed to be sufficient to enable the client to make an informed decision with respect to a matter, whereas general consent is not. The language included in the Code and related to specific consent — an explanation of the situation and any planned safeguards — is more consistent with the ABA Opinion, which lists several indicators of informed consent, including the extent of and specific information about the risk of generative AI usage and informing the client of the professional’s best judgment on why generative AI is being used.

When creating a disclosure and/or consent, consult with legal counsel to draft a clear and comprehensive document that accurately reflects the firm’s generative AI use and policies, and adheres to applicable laws, regulations, and professional standards. Use straightforward language to help clients easily understand what generative AI the firm uses, whether the firm is creating its own generative AI from existing client data, and how generative AI will be used in furtherance of the services provided. In addition to describing how generative AI will be used, a disclosure and consent will also likely address:

• The firm’s quality control procedures to be followed prior to final delivery of the work product;

• The client’s consent to the disclosure of confidential information to third parties in support of the firm’s services;

• The firm’s responsibility to prevent unauthorized release of the client’s confidential information; and

A request for the client’s consent to engagement performance under those conditions.

If the disclosure/use involves tax return information, consider Regs. Sec. 301.7216-2 and assess if the disclosure/use requires consent in the format required by Sec. 7216 and Regs. Sec. 301.7216-3.

Regular review and updates to the disclosure and consent and firm policies to reflect any changes in generative AI usage or data security practices, as well as any changes to laws and regulations, is recommended. Training of employees on the importance of disclosure and consent is also suggested. This helps promote a culture of transparency and trust within the firm.

The Original ‘New Normal’

In the Information Age, consumers have become attuned to which businesses misuse client data and which do not. Some businesses understand that being transparent enhances both client trust and their public reputation, and some businesses have yet to learn this lesson. Transparency also empowers clients to make informed decisions. Increasingly, clients want to know who has access to their data and how their data is protected. Whether a CPA uses client data in generative AI for professional services, marketing, or administrative tasks, upfront disclosure can acknowledge clients’ concerns about their sensitive information.

To read the full article, and find more resources, visit alabama.cpa/disclose-ai.

Anglin Reichmann Armstrong

Anglin Reichmann Armstrong is pleased to announce that Steve Sledge, CPA, has joined the firm as an Audit Partner in the Huntsville, Alabama office, bringing over31 years of experience in audit, financial reporting, and technical accounting. His extensive leadership background and dedication to quality client service make him a valuable addition to the firm’s growing audit and assurance practice.

Steve joins Anglin following a distinguished 31-year career at KPMG LLP, where he advanced through professional roles, ultimately serving as an Audit Partner for most of his career. He has extensive experience in financial statement audits, risk assessments, and integrated audit strategies, leading engagements for clients across various industries including healthcare, manufacturing, commercial, and consumer markets. His work has supported both public and private companies including private equity ownership structures. In addition to client service, Steve has served a pivotal role in talent recruitment and development. He has mentored emerging professionals, led technical training programs at both local and national levels, and contributed to internal quality assurance initiatives.

BMSS Advisors & CPAs

Summer Leadership ProgramZebraFest

2025

We spent the day welcoming our committed Spring 2026 interns to the BMSS family & showing them the BMSS way of good food and fun. Looking forward to having this group back in our offices in January!

Spring Serve Day

Throughout the month of May, employees from the BMSS Family of Companies participated in our firm-wide Serve Day, continuing a long-standing tradition of partnering with local charitable organizations to make a meaningful impact in their communities.

Success Season Cookout/Fiesta

In celebration of a successful tax season, our team gathered for a festive April 15th meal!

As a respected leader in the accounting profession, Steve has served on multiple advisory boards and co-authors a long-standing accounting and auditing column for The Tennessee CPA publication. He has been recognized for his contributions to the field, including receiving the University of Alabama Culverhouse School of Business Accounting Alumni Leadership Award in 2023.

WellStone’s Beacon of Hope Celebration

“We are thrilled to welcome Steve to our team,” said Brandon Smith, Managing Partner at Anglin. “His depth of experience and leadership in audit and advisory services will further enhance our ability to serve clients with technical excellence and strategic insight.”

We are honored to be a sponsor in Wellstone’s annual Beacon of Hope celebration!

Annual Promotions

Steve holds a B.S. in Accounting from the University of North Alabama and a Master of Accountancy from the University of Alabama. He is a Certified Public Accountant licensed in Alabama and Tennessee and is actively involved in the American Institute of Certified Public Accountants and the Tennessee Society of Certified Public Accountants, where he currently serves as Chair of the Audit Committee.

Anglin Reichmann Armstrong continues to expand its talent and service offerings to support clients’ evolving needs. With Steve’s leadership in the Huntsville office, the firm strengthens its commitment to delivering high-quality audit and advisory services while fostering professional growth within its team.

July 1st is promotions day at BMSS and we celebrated with sweet treats at each of our offices! Congratulations to our newly promoted team members; thank you for your excellent work!

Best Places to Work

We are thrilled to be named the #1 Best Place to Work in the extralarge category by the Birmingham Business Journal. At the BMSS Family of Companies, our goal is to provide a workplace that values character, family, and a life/work balance while creating a professional environment where each individual is treated with respect

Sledge

Golf Tournament

Our BMSS team had a fantastic day at the 36th Annual Greer’s/Goodwill Gulf Coast Golf Tournament, held at the beautiful Robert Trent Jones Golf Trail at Magnolia Grove! Representing BMSS on the course was senior manager, Todd Martin IV, joined by Todd Martin III (Southland Capital Realty Group), Walter Brand (ServisFirst Bank), and Wesley Williams (Wiltew). It’s always a pleasure to support a great cause and spend the day with friends and community partners!

Brews & Schmooze

After Success Season each year, we host our clients and firm friends for our annual Brews & Schmooze event in Birmingham, Gadsden, and Huntsville. We enjoyed gathering at Back Forty Beer Company in each location

New Trussville Office

We celebrated the kick-off of our new BMSS Family of Companies Trussville office with a ribbon-cutting ceremony with the Trussville Area Chamber of Commerce! We’re thrilled to serve the Trussville community from our new space.

Jackson Thornton, a certified public accounting and consulting firm headquartered in Montgomery, AL, is pleased to announce that one of its principals has recently been honored by the National Association of Certified Valuators and Analysts® (NACVA®).

Ashley S. Taylor, a principal in the firm’s Business Valuation & Litigation Consulting Group (BVLC), has been elected Chairperson of the NACVA® Litigation Forensics Board (LFB). The Board oversees certification criteria related to NACVA’s Master Analyst in Financial Forensics® (MAFF®) designation. In addition, the LFB has the responsibility of evaluating the content of NACVA’s litigation and forensicsrelated curriculum to provide assurance that course content remains objective, technically and fundamentally sound, and presents information in a proper perspective necessary to the creation and development of a wellrounded and substantive training program.

“The Litigation Forensic Board provides the Association with critical guidance and important oversight,” said NACVA’s Chief Executive Officer, Parnell Black, MBA, CPA, CVA.

“We are very pleased that Ashley has agreed to chair the Board, share her insight with us, and help the Association as we assist thousands of members keep up with the demand for financial forensics and obtain the necessary training,

certification, and credibility so they grow and thrive in their practice and strengthen brands.”

Taylor has been with Jackson Thornton since 2008 and with the BVLC group since 2009. In 2022, she assumed responsibility for the firm’s Refunding Verification and Arbitrage Rebate practice. Taylor also serves as Director of Campus Recruiting for Jackson Thornton.

Taylor received her Bachelor of Science in Business Administration and Master of Business Administration from Auburn University Montgomery. She is a graduate of the Emerge Montgomery Torchbearers Leadership Class IV and the Leadership Montgomery Legacy Class XXXVII. She served on the inaugural Junior Executive Board for Child Protect Children’s Advocacy Center, is a past president of Jackson Thornton Young Professionals, and a past president of Emerge Montgomery. In addition to the NACVA® Litigation Forensics Board, Taylor currently serves as board secretary for the Kiwanis Club of Montgomery. She was named as Emerge Montgomery’s 2015 Young Professional of the Year, Auburn University Montgomery’s College of Business 2017 Outstanding Young Alumni, “Top 40 Under 40” (Class 2023) by CentrAL INC and named to Troy University School of Accounting’s Hall of Honor in 2023.

Jackson Thornton is also pleased to announce that one of its tax associates has recently been honored by Auburn University Montgomery (AUM).

Emma Gunter, a Senior Tax Associate, has been recognized as the 2025 Young Alumna by Auburn University Montgomery. This award recognizes outstanding achievements and contributions in business, as well as dedication to AUM and the College of Business.

“Gunter’s accomplishments have inspired many and exemplify the spirit of excellence that the AUM College of Business strives to uphold, “ said Dr. Daewoo Park, Dean & Professor, College of Business, Auburn University Montgomery. The award was presented during AUM’s 2025 College Honors Day.

Gunter received both her graduate and undergraduate degrees from AUM and has been with Jackson Thornton since 2022. She holds professional membership in the American Institute of Certified Public Accountants (AICPA), the Alabama Society of Certified Public Accountants (ASCPA) and serves on the Educational Foundation Board for the ASCPA. In addition, she is a member of the Jackson Thornton Young Professionals group and assists with campus recruiting, intern training and tax software implementations for the firm.

Jackson Thornton Wealth Management (JTWM) is pleased to announce that it has been named to the 2025 Accounting Today Wealth Magnets list.

The recently released list ranked CPA firm financial

Taylor

Gunter

planning practices by assets under management (AUM) and featured 200 firms throughout the U.S. JTWM ranked 39th on the list and is the largest CPA firm financial planning practice based in Alabama. The firm has been featured in the rankings since 2021.

“We’re honored to be included in this listing of top firms from around the country,” commented Shaw Pritchett, a financial advisor and president of JTWM. “We’re deeply grateful to the clients who have believed in us and partnered with us for more than 25 years.”

Leading accounting and advisory firm Mauldin & Jenkins is honored to be recognized once again as one of the Birmingham Business Journal’s 2025 Best Places to Work.

Now in its 20th year, the Best Places to Work program celebrates companies in the Birmingham area that go above and beyond to foster exceptional work environments and positive employee experiences. The annual awards are based on confidential employee feedback gathered from a survey that evaluates workplace culture, trust in leadership, benefits, and overall satisfaction.

Bill Curtis, Birmingham Practice Leader, shared, “We are proud to be recognized as a Best Place to Work, which reflects the positive and engaging culture we’ve built as a Firm. Our people are our greatest asset, and we remain dedicated to providing an environment that supports their professional growth and long-term success.”

With a long-standing commitment to employee well-being, career development, and community engagement, Mauldin & Jenkins invests in initiatives such as flexible working arrangements, leadership development opportunities and mentorship programs, wellness resources, and team-driven volunteer efforts that contribute to a positive and engaging workplace.

Warren Averett CPAs and Advisors is pleased to announce two promotions:

Birmingham’s Conrad Wiley, CPA, was promoted to Senior Manager in the firm’s Audit Division. Conrad primarily focuses on building client relationships, providing quality service, improving efficiencies in the audit process, training and promoting staff development, as well as planning and conducting financial statement audits and reviews.

Birmingham’s Eric Byron, CPA, was promoted to Senior Manager in the firm’s Tax Division. He is an expert in managing client interactions to ensure their tax and consulting requirements are met. His daily responsibilities include compliance, financial statement compilations and reviews, as well as consulting on specific client issues.

We first introduced you to Emma in October 2023, when she was featured in our #HeyHeyCPA campaign. Check it out by visiting alabama.cpa/MissAlabama.

Send

Congratulations to the new Miss Alabama, Emma Terry!

Emma, a graduate of The University of Alabama at Birmingham with degrees in accounting, bested 42 other contestants to win the 2025 state title.

Wiley Byron

SELLING YOUR FIRM IS COMPLEX. LET US MAKE IT SIMPLE.

Accounting Biz Brokers knows your market. Contact us TODAY to receive a free market analysis.

For Sale:

• Jackson County, MS Gulf Coast $275k

• MS Gulf Coast $625k

Sold!

• North Metro Atlanta Area $2.55M

• Huntsville $1.2M

• Chattanooga, TN $2.115M

• Western Knoxville, TN $435k

For more information contact Kathy Brents, CPA, CBI at 866.260.2793 or Kathy@AccountingBizBrokers.com. Visit us online at www.AccountingBizBrokers.com .

YOUR PRACTICE WANTED

Thinking about selling your practice? Accounting Practice Sales delivers results, bringing you the best price, optimal terms and a buyer who represents an ideal fit for your clientele. Contact us today for a confidential discussion.

PRACTICES FOR SALE:

• Tuscaloosa CPA grossing $225K *New*

• Montgomery assurance practice grossing $265K *New*

• Dyersburg, TN area CPA grossing $320K *Available*

• Jackson/Humboldt, TN area EA grossing $150K *New*

• Clarksville, TN area EA grossing $650K *New*

• West of Nashville EA grossing $750K *New*

For more information on these listings or to sell your practice, contact Lori Newcomer, CPA and Tim Price, CPA at (888) 5531040 or PNgroup@APS.net, or visit www.APS.net.