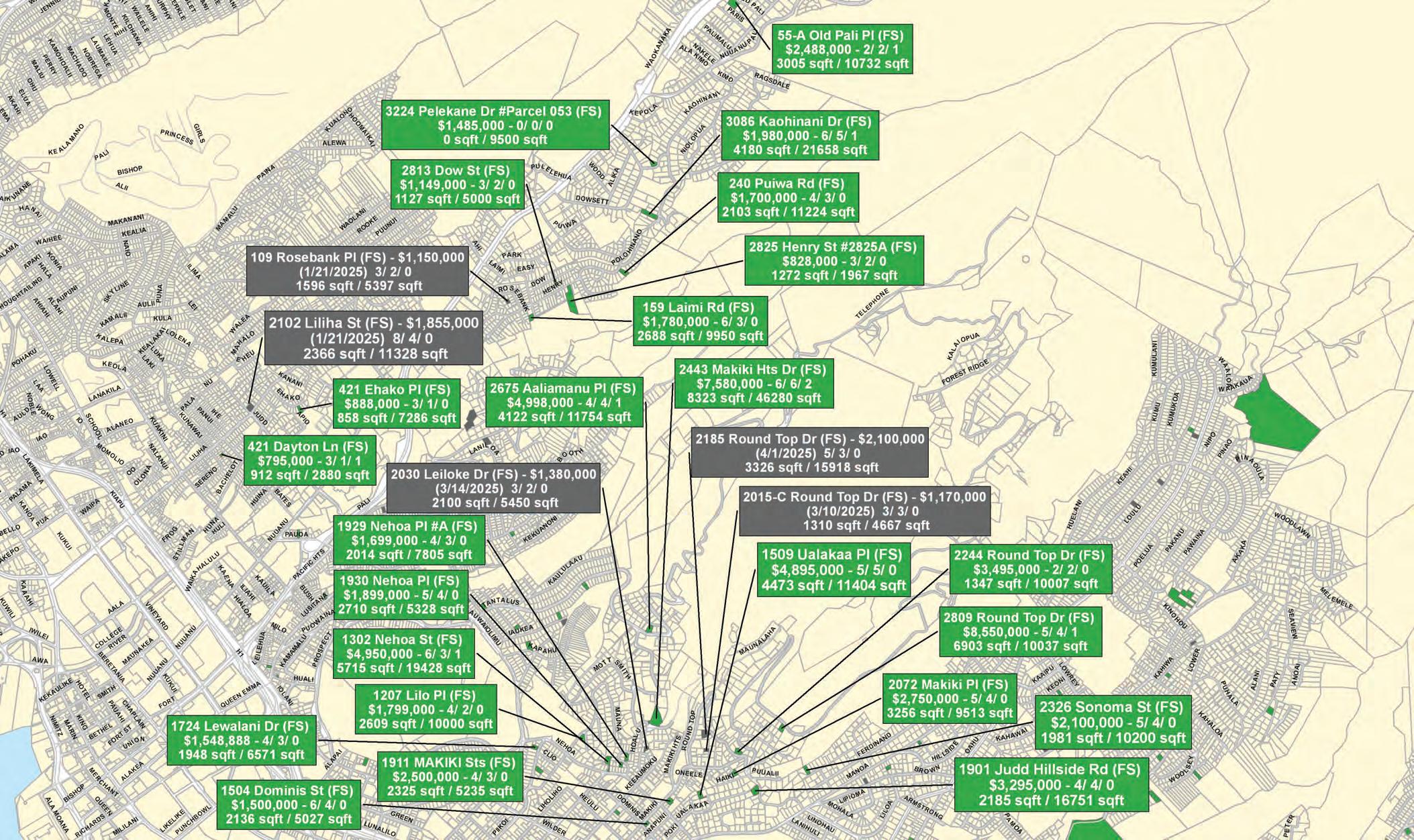

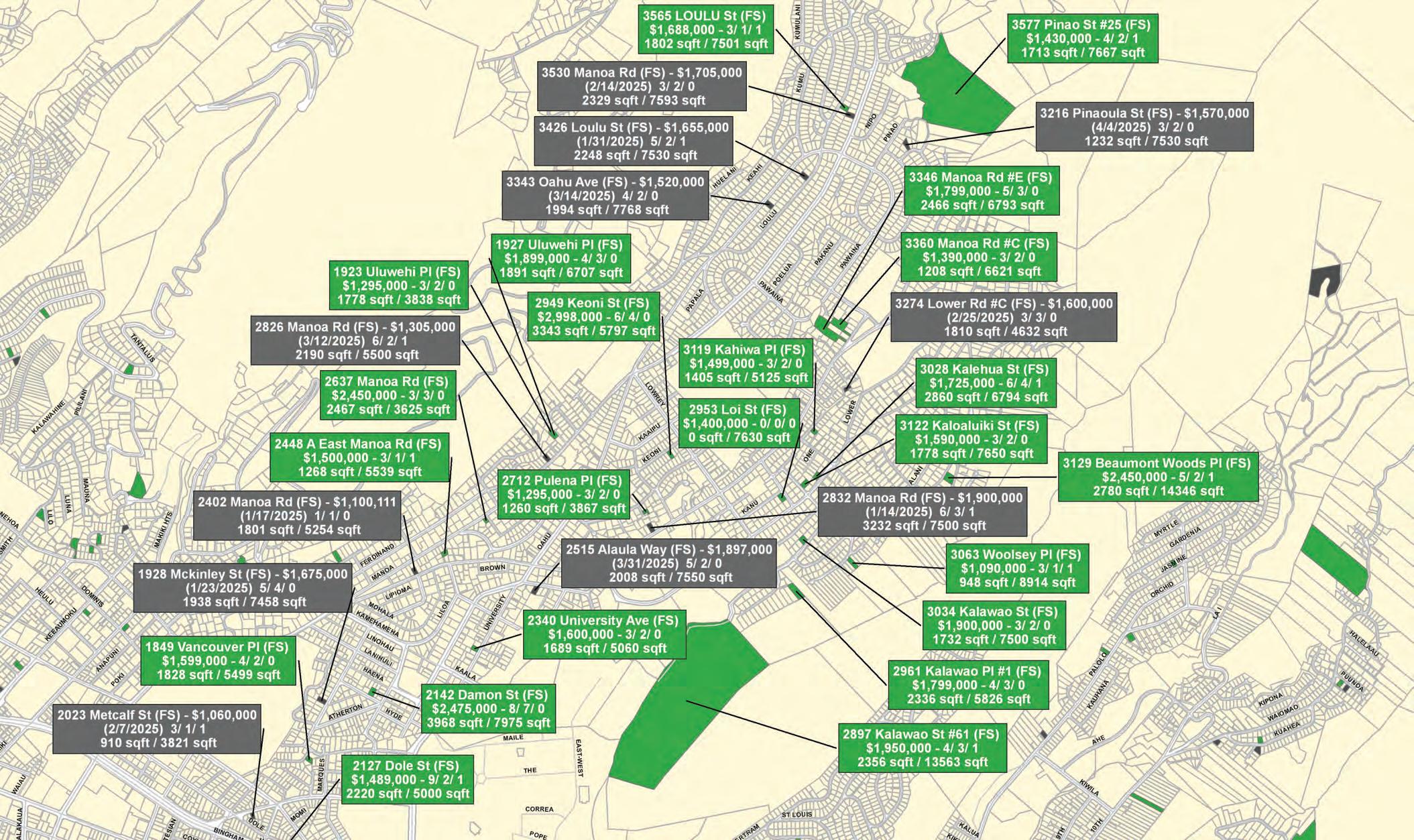

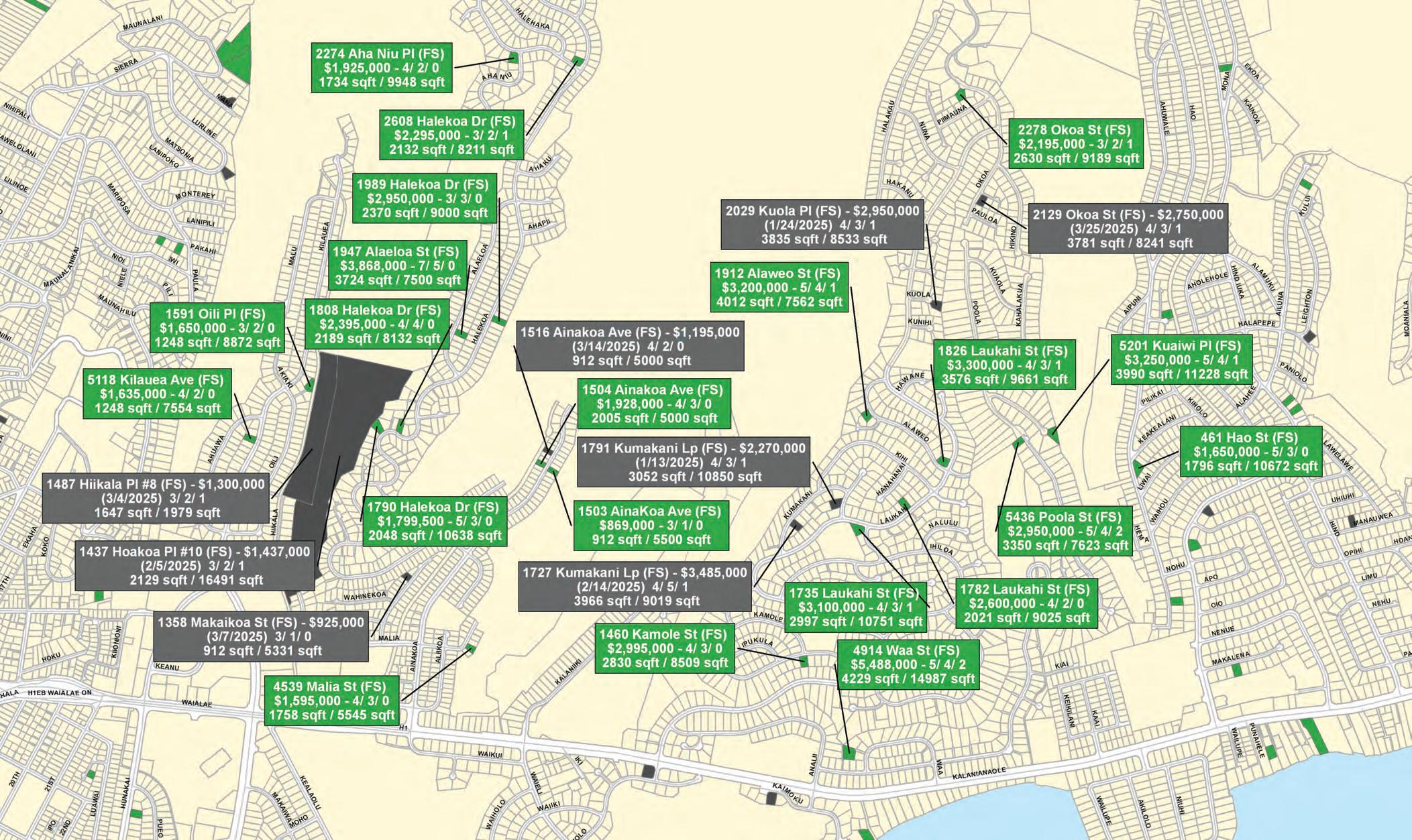

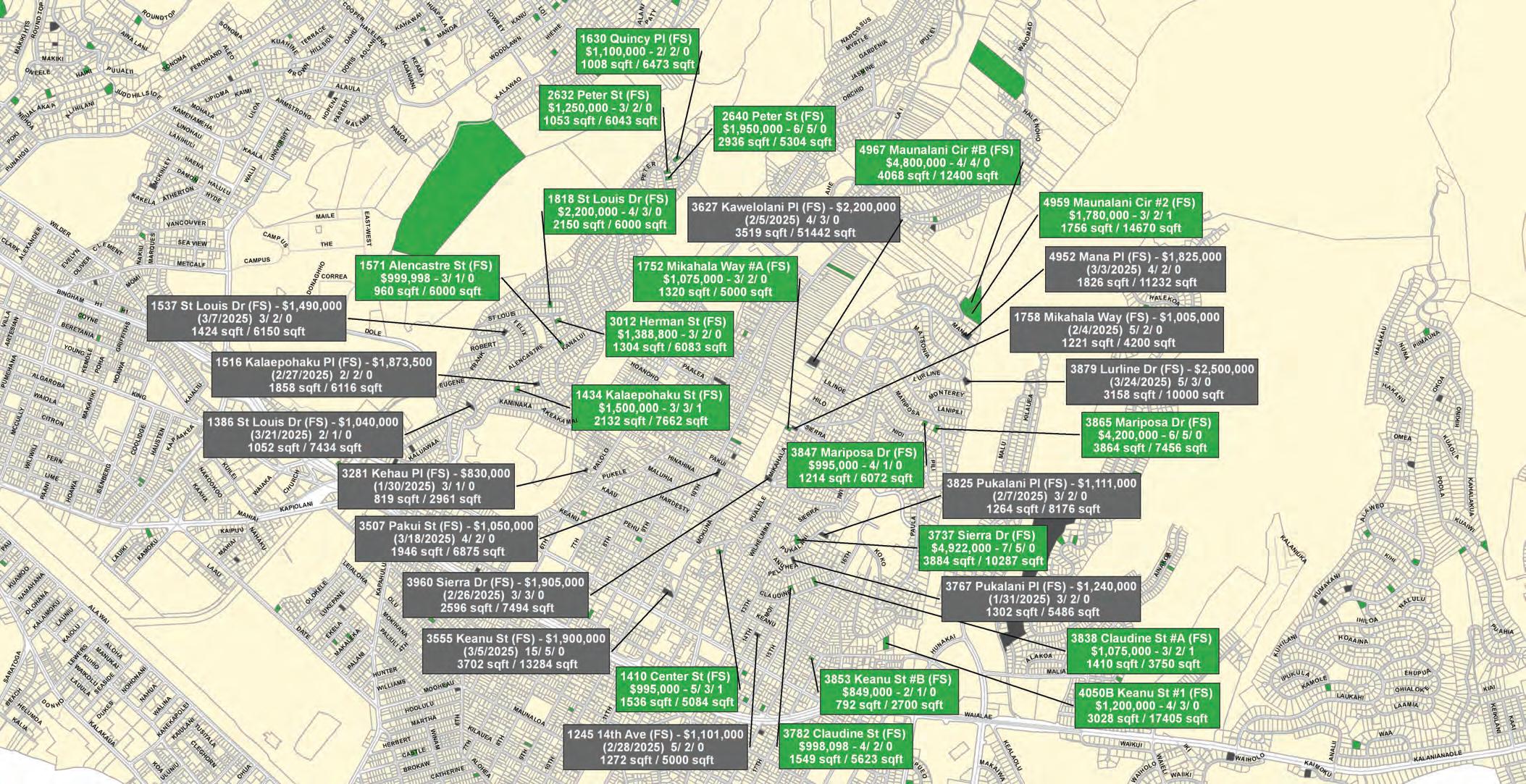

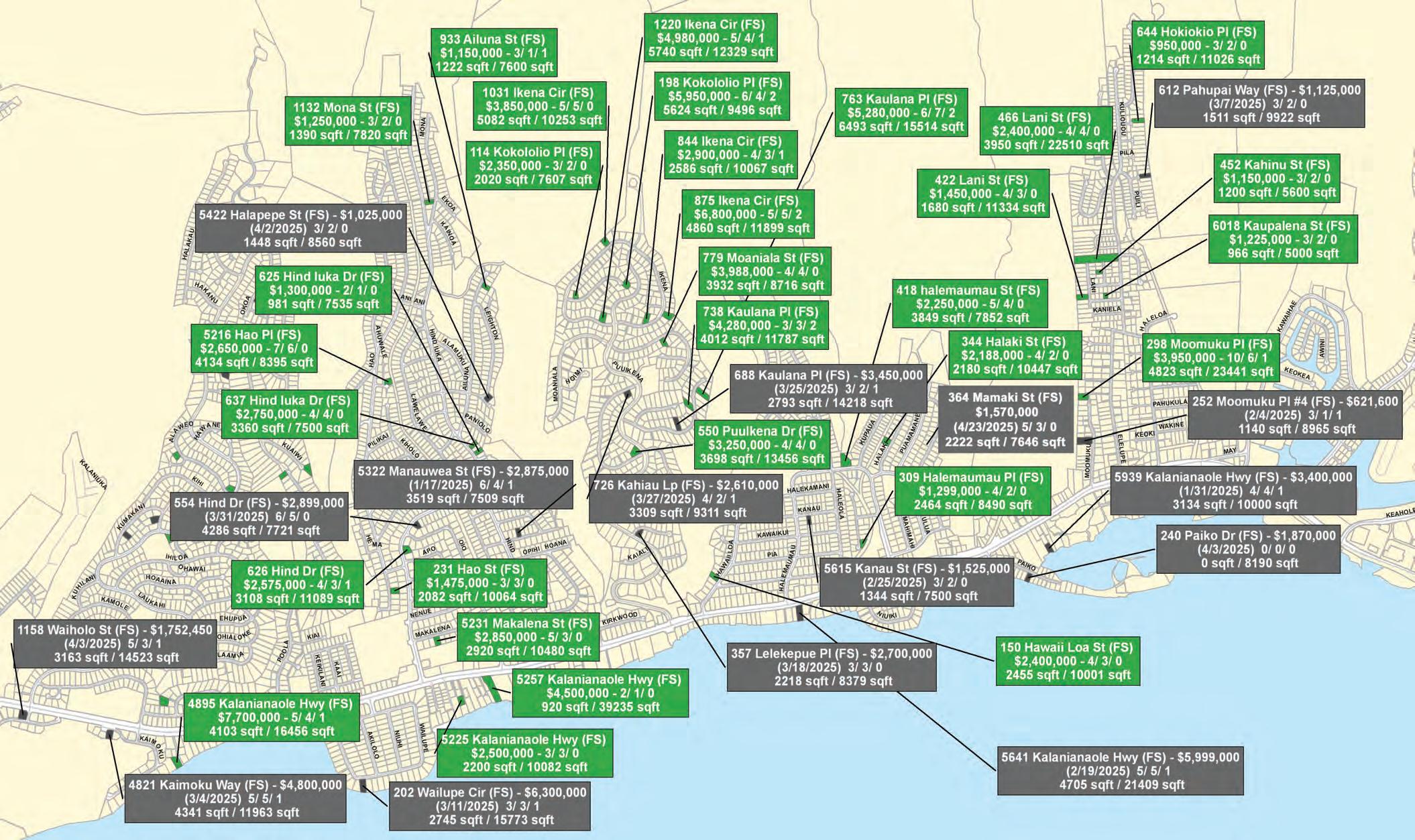

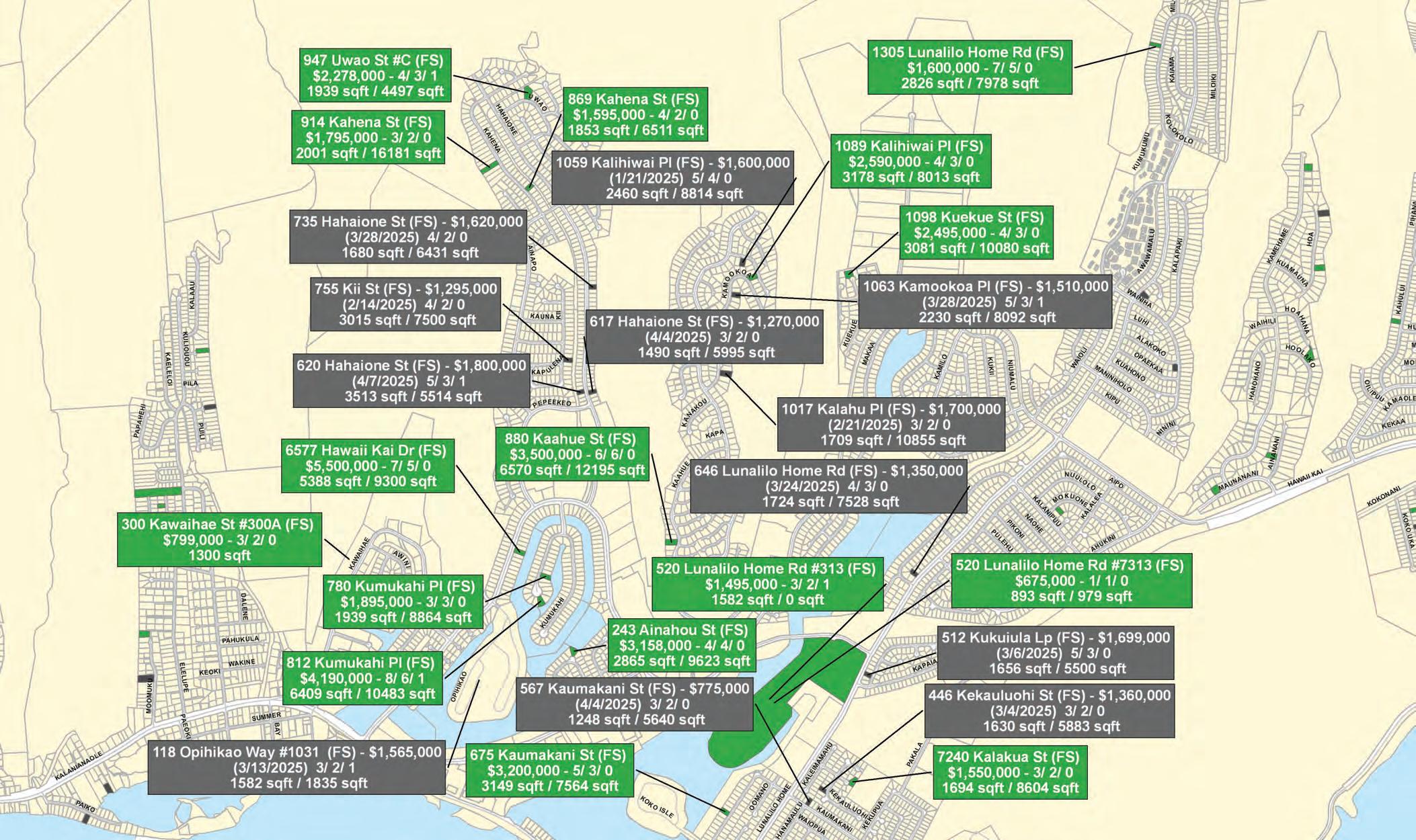

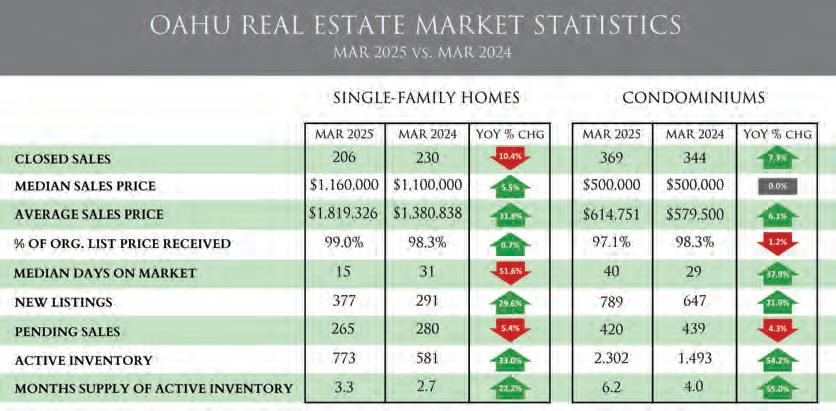

As we close out the first quarter of 2025, Oʻahu’s housing market reflects a shift in pace, with diverging trends between the singlefamily and condominium sectors. Although prices remain resilient, the overall landscape points to growing inventory, lengthier days on the market for condos, and cautious buyer sentiment.

In March 2025, single-family home sales dropped 10.4% yearover-year, with just 206 homes closing escrow compared to 230 in March 2024. Despite fewer transactions, home values continued their upward trajectory, with the median sales price climbing 5.5% to $1,160,000.

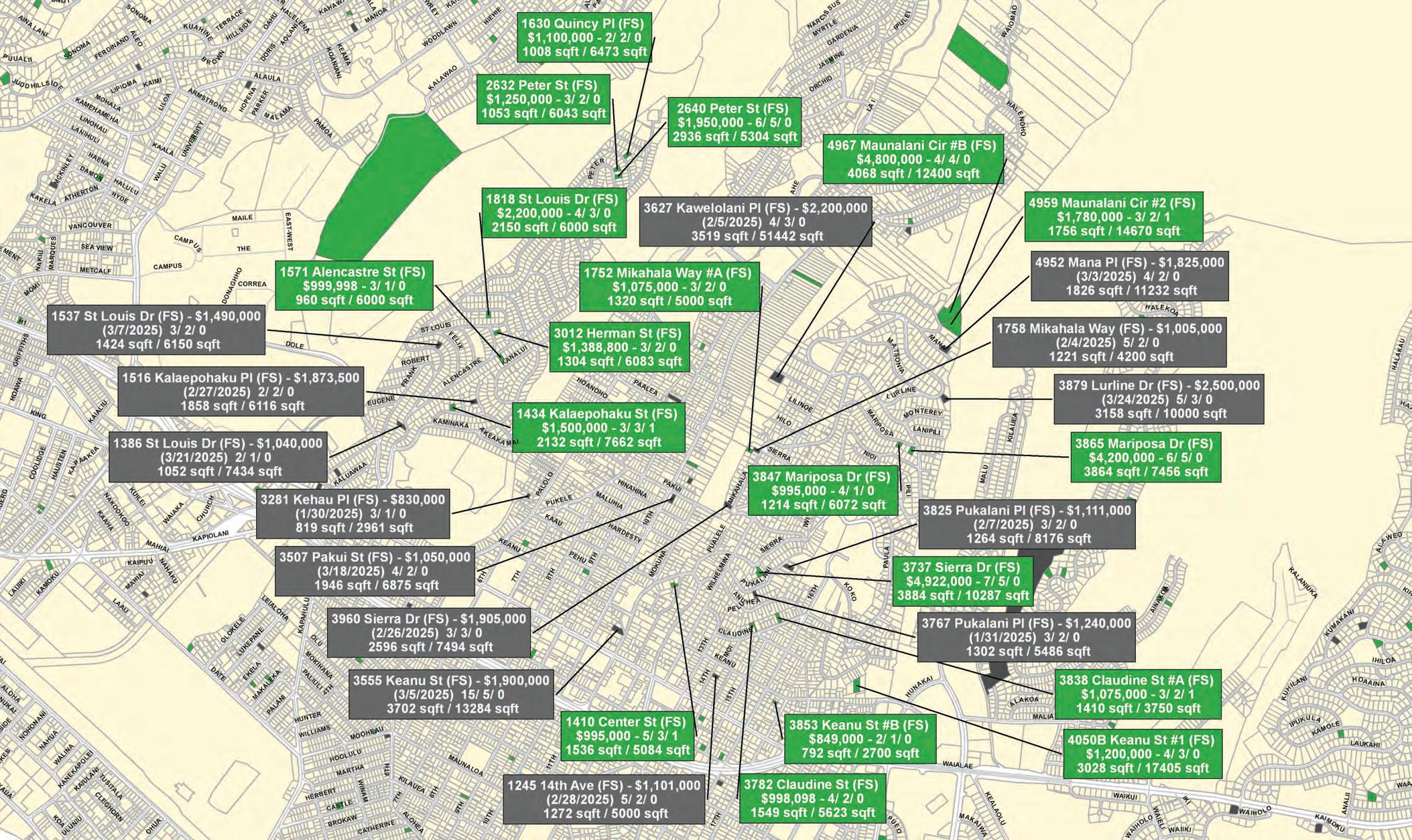

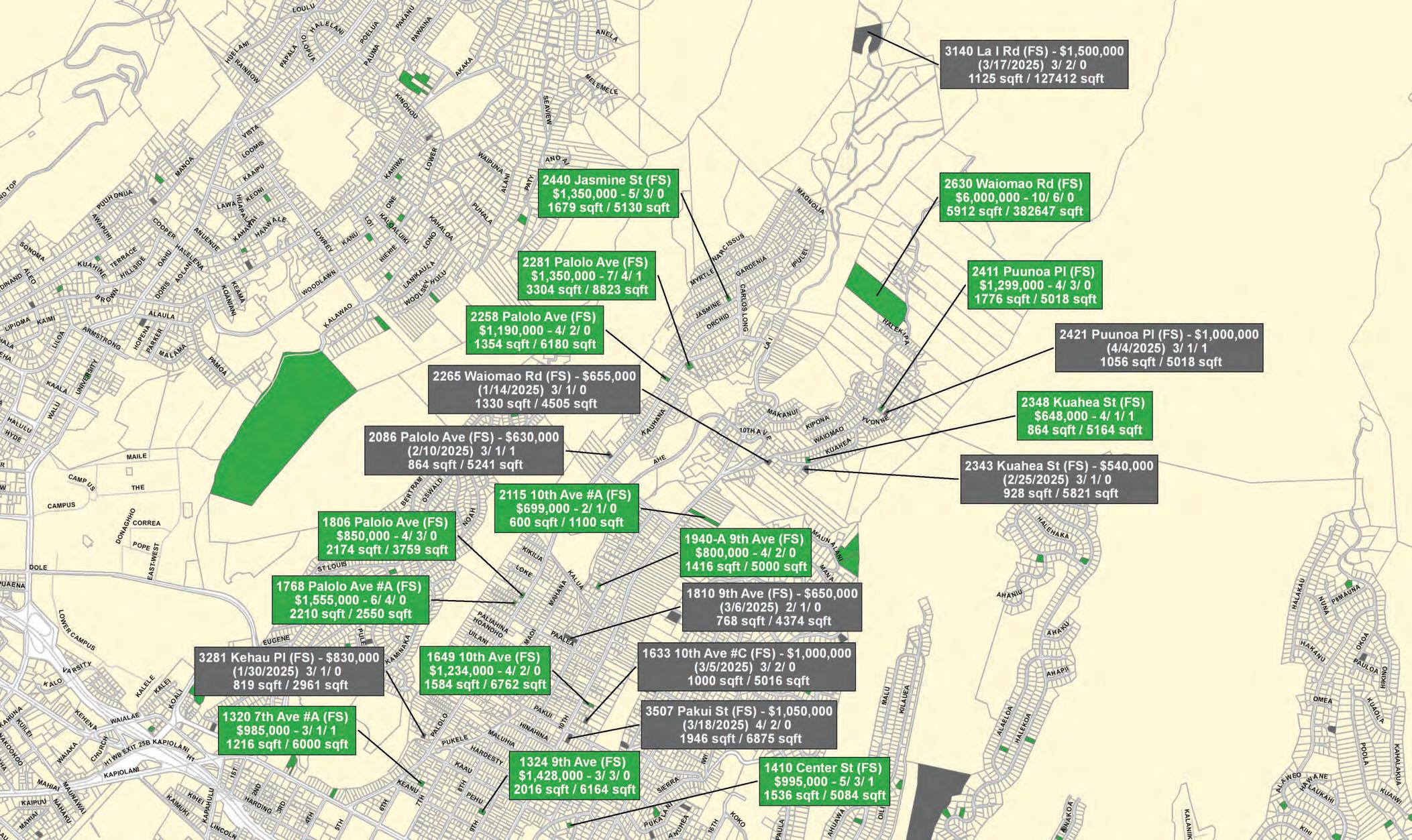

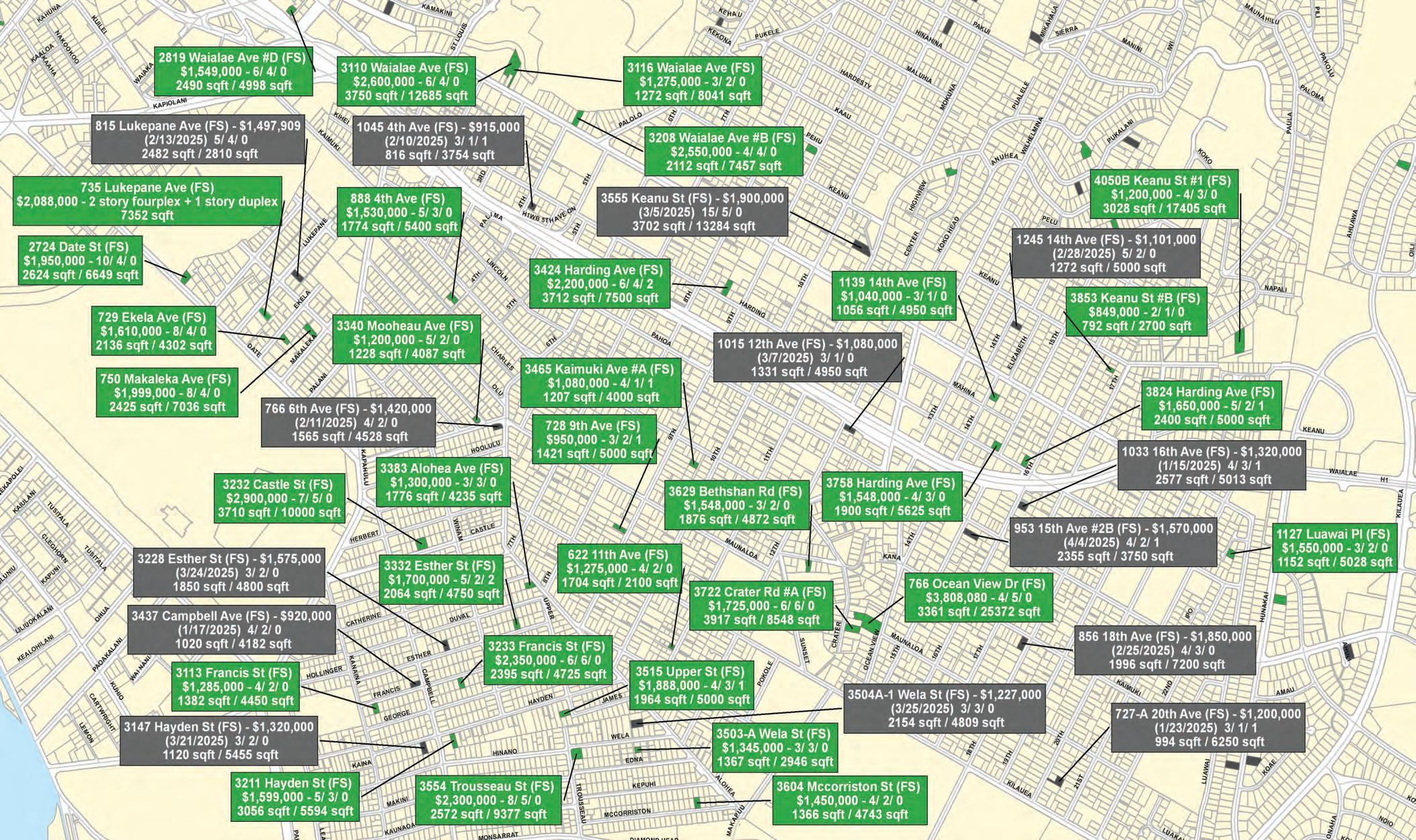

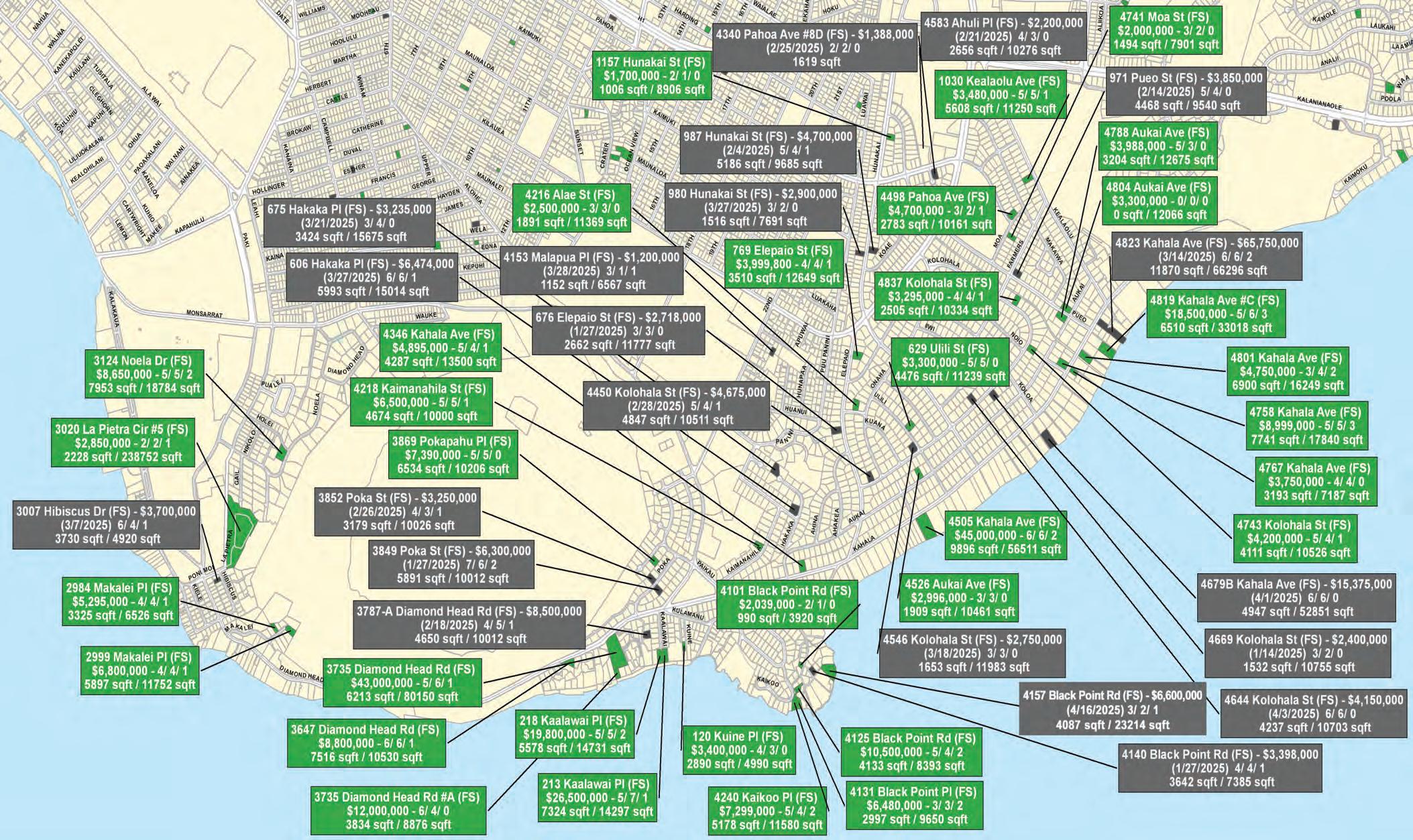

The average sales price reached $1,819,326—heavily influenced by a $65.75 million transaction in Kāhala —excluding this sale results in an adjusted average of $1,507,469 and no change to the median sales price. Days on market improved to a median of 15 days, down from 31 days a year ago, and 99.0% of homes sold received at or near their list price, a slight increase from 98.3% in March 2024. New listings surged nearly 30% to 377, while pending sales fell 5.4% to 265. Active inventory climbed significantly—up 33.0% to 773 homes—giving buyers more options. Months of supply increased to 3.3 months from 2.7 months, suggesting a shift toward a more balanced market.

The condo market showed a modest uptick in activity, with closed sales up 7.3% year-over-year to 369 units. The median price remained steady at $500,000, while the average price jumped 6.1% to $614,751.

Unlike single-family homes, condos experienced a longer selling cycle, with a median of 40 days on the market—up from 29 days in March 2024. The share of condos selling at or above asking price dipped to 97.1%, compared to 98.3% last year.

New condo listings rose 21.9% to 789, and pending sales dropped 4.3% to 420. Active inventory expanded 54.2% year-overyear to 2,302 units, the largest increase in recent memory. Months of supply increased to 6.2 months from 4.0 last March.

This increase in condo inventory and longer days on market may be a result of the difficulty in condos obtaining adequate hurricane insurance which has led to a lack of available bank financing for purchases and higher maintenance fees.

Buyers: Inventory growth is creating more breathing room and expanding choices, especially in the condo sector. Those waiting on the sidelines may find better negotiating power than a year ago.

Sellers: Homes and condos are still commanding strong prices, but with more competition and longer days on the market, strategic pricing and preparation are critical.

Investors: The cooling in pending sales and increased inventory may signal an opportunity to re-enter the market as it becomes less overheated, potentially creating room for value-based acquisitions.

As Q2 begins, the outlook on the market is somewhat uncertain as the geopolitical and economic issues (such as the tariffs and interest rates) will have a future impact on real estate in Hawaii. Whether you’re buying, selling, or investing, staying informed and working with an experienced real estate professional is your best advantage.

Single-Family Homes:

• Total Q1 sales: 569 (down 4.0%)

• Median price: $1,150,000 (up 7.5%)

• Average price: $1,531,743 (up 11.2%). Heavily influenced by the $65,000,000 Kahala sale.

• Pending sales: 707 (down 8.1%)

Condominiums:

• Total Q1 sales: 974 (up 0.4%)

• Median price: $510,000 (up 1.0%)

• Average price: $625,004 (up 6.9%)

• Pending sales: 1,158 (down 3.9%)

{SOURCE: HONOLULU BOARD OF REALTORS 2025}