Speculative office building in Budapest continues to fall as developers exercise caution in their development strategies. New projects are not being initiated in an uncertain geopolitical environment, with questions over long-term demand, and concerns over the cost and availability of finance. 15

Limited Supply, Upward Pressure on Rents Across CEE

A low development pipeline combined with limited supply, leading to a scarcity of offices that meet tenant and ESG requirements, is the dominant trend across Central and Eastern Europe. 18

Wandering through the streets of Szeged last week, David Holzer spied a lad wearing rolled-up trousers, big boots, and a denim jacket covered in patches. One of these read “Support a Punk, Buy Them a Beer.” Whenever he sees someone dressed punk style, it lifts his spirits, he reports. 29

Three Decades a Charm

DVM group is celebrating the 30th anniversary of its foundation in Budapest in 1995. To mark the occasion, its three managing partners and co-owners, Tibor Massányi, Péter Haberl, and Balázs Czár, discuss the past, present, and future of one of the most consequential providers of integrated building services in Hungary. Discover how the ‘sum of small improvements’ built a ‘deeply exciting’ business. 9

Disappointing Q1 GDP Data Redraws Outlook

The economic performance of the first three months was a massive negative surprise for analysts and the government. Many say it is already questionable whether full-year GDP growth will reach 1%; some are even more pessimistic. 3

German Firms Skeptical of Business Upturn

The Hungarian economy is facing difficult times, as underlined by recent statistical data, and the results of the spring survey of members of the German-Hungarian Chamber of Industry and Commerce. 7

EDITOR-IN-CHIEF: Robin Marshall

EDITORIAL CONTRIBUTORS: Luca Albert, Balázs Barabás, Zsófia Czifra, Kester Eddy, Bence Gaál, Gergely Herpai, David Holzer, Gary J. Morrell, Nicholas Pongratz.

LISTS: BBJ Research (research@bbj.hu)

NEWS AND PRESS RELEASES: Should be submitted in English to news@bbj.hu

LAYOUT: Zsolt Pataki

PUBLISHER: Business Publishing Services Kft.

CEO: Tamás Botka

ADVERTISING: AMS Services Kft.

CEO: Balázs Román

SALES: sales@bbj.hu

CIRCULATION AND SUBSCRIPTIONS: circulation@bbj.hu

Address: Madách Trade Center 1075 Budapest, Madách Imre út 13-14, Building B, 7th floor. Telephone +36 (1) 398-0344, Fax +36 (1) 398-0345, www.bbj.hu

THE EDITOR SAYS

ECONOMIC PLANNING AMID A ‘NEWSNAMI’

A world events podcast I listen to refers to the period since U.S. President Donald Trump returned to the White House as a non-stop “newsnami.” Partly this is a deliberate ploy from the administration to “flood the zone,” a phrase former political adviser Steve Bannon borrowed from the sports field. The strategy is to overwhelm the media and what opposition there is from the Democrats through a tidal wave of moves that make it nigh-on impossible to respond to, well, everything, everywhere, all at once.

BBJ-PARTNERS

Why Support the BBJ?

• Independence. The BBJ’s journalism is dedicated to reporting fact, not politics, and isn’t reliant on advertising from the government of the day, whoever that might be.

• Community Building. Whether it is the Budapest Business Journal itself, the Expat CEO award, the Expat CEO gala, the Top Expat CEOs in Hungary publication, or the new Expat CEO Boardroom meeting, we are serious about doing our part to bind this community together.

• Value Creation. We have a nearly 30-year history of supporting the development of diversity and sustainability in Hungary’s economy. The fact that we have been a trusted business voice for so long, indeed we were the first English-language publication when we launched back on November 9, 1992, itself has value.

• Crisis Management. We have all lived through a once-in-a-century pandemic. But we also face an existential threat through climate change and operate in a period where disruptive technologies offer threats and opportunities. Now, more than ever, factual business reporting is vital to good decision-making.

For more information visit budapestbusinessjournal.com

That explains all those executive orders covering everything from the “war on woke” to “Maintaining Acceptable Water Pressure in Showerheads,” the latter presumably an attempt to make America’s showers great again. But it is not just that. There truly seems to be a lot going on nowadays, whether it is the election of a new pontiff, the on-off application of tariffs, hostage exchanges, and war (and ceasefires, potential or otherwise) in the Middle East, Ukraine, and Kashmir. Somewhere buried in this newsnami is Hungary’s economy and Viktor Orbán’s relationship with the President. While the government is quick to welcome each attempt at negotiating a ceasefire as reflective of its peace policy, it seems less keen to talk about the economic whirlwind we find ourselves in. However close Budapest and Washington might be, trade negotiations within the EU are a matter for the European Commission, not the member states. That means Hungary cannot carve out a tariff discount for itself; it can only get whatever the European Union can achieve as a bloc. That’s bad news at a time when the Hungarian economy is not exactly, as they say, going like gangbusters.

Doubtless, the government will blame the sluggish world economy, more specifically anemic growth in Germany, this country’s largest trade partner. It will probably also throw into the mix the destabilizing factor of a three-year war in the region. Those are, undoubtedly, contributing factors. But that is equally true across Europe. As our Macroscope report on page three makes clear, Hungary’s Q1 GDP figures didn’t just disappoint, they were the worst in the EU at the time of writing (some countries are still to report, but that won’t suddenly make Hungary’s figures markedly better once submitted). Gross domestic product stagnated according to the raw data, and was 0.4% lower according to seasonally- and calendaradjusted data in Q1 2025 than in Q1 2024. Compared to Q4 2024, the economic performance was down by 0.2.

The government predicated the 2025 budget on economic growth of 3.4%. Only a month ago, the Ministry for National Economy lowered that to 2.5%. So far, it hasn’t modified its expectations in light of the fresh data, though it has said it won’t abandon its plan “to achieve the highest possible economic growth, and the economic policy programs for 2025 and 2026 will continue to set this ambitious goal.” It doesn’t have much of a hand to play, and it isn’t apparent how the much vaunted trans-Atlantic friendship can help it in a world where tariffs go as quickly as they come, and it becomes increasingly hard to plan or prepare. If anyone does have an answer, please share it. One of the analysts we spoke to said he had thought growth would be less than 2%; now he says whether the figure will even start with one is questionable.

Robin Marshall Editor-in-chief

THEN & NOW

In the 1959 black-and-white photo from the Fortepan public archive, visitors buy ice cream from a stand at the harbor in Siófok (104 km southwest of Budapest by road, on the southern shore of Lake Balaton). In the background is the motor passenger ship Csobánc, named for a volcanic hill in the Tapolca Basin near the lake. In the modern image from state news wire MTI, ice creams ready for judging are displayed aboard the Szántód ferry during the 12th Balaton Ice Cream competition on May 9, 2025.

Photo by Zsolt Szigetváry / MTI

Photo by Sándor Bauer / Fortepan

Ukraine-Hungary Tensions Rise With Tit-for-tat Expulsions

Relations between Hungary and Ukraine reached a new low last week as the countries each expelled two diplomats from their respective territories, with accusations of espionage on both sides.

Ukraine

Roundup Crisis

of his criticism of language laws “that severely restrict the rights of the Hungarian minority in the country.”

Hungarian Expulsion

“Two Hungarian diplomats must leave our country within 48 hours,” Ukrainian Foreign Minister Andrii Sybiha said on the X social media platform on May 9, after Ukraine’s SBU security services said it had exposed a military intelligence network run by the Hungarian state.

The SBU claimed that it had detained two suspected agents tasked with gathering intelligence about Transcarpathia, which contains a sizable ethnic Hungarian minority. This included information about how well the region was protected by ground and air defenses, and “to study the socio-political views of [the] local population, including scenarios of their behavior if Hungarian troops enter the region,” the security service claimed.

According to the state security agency, it was the first time a Hungarian spy network had been found working against Kyiv’s interests.

“We have just summoned [the] Hungarian Ambassador to MFA [the Ministry of Foreign Affairs of] Ukraine and presented him with the relevant note,” Sybiha wrote in English on X. “We are acting in response to Hungary’s actions, based on the principle of reciprocity and our national interests.” The Hungarian side saw matters in a somewhat different light.

“You cannot believe the Ukrainian regime or its secret service,” László Toroczkai, leader of Hungary’s radical right opposition party Mi Hazánk [Our Homeland], responded. He called for an urgent meeting of Parliament’s national security committee and claimed Ukrainian authorities were making “the same accusations

Meanwhile, the Hungarian government expelled two individuals working at Ukraine’s embassy in Budapest on suspicion of espionage, Minister of Foreign Affairs and Trade Péter Szijjártó said in a video on his Facebook page.

File photo shows László Brenzovics, president of the KMKSz, speaking at the 1st Gala of Excellence of the Carpathian Basin Techniques in Budapest on Jan. 31, 2025. To his right is Minister of Culture and Innovation Balázs Hankó.

of treason and separatism” that they had against ethnic Hungarian community leader László Brenzovics in 2020.

Brenzovics is president of the Hungarian Cultural Association of Transcarpathia (KMKSz). According to Hungary Today, he was forced to flee his homeland after a series of death threats from Ukrainian nationalists. He also “faced harassment from the Ukrainian authorities” because

How the Right Benefits Strategy can Transform the Employee Experience

With 4.7 million workers across 25 sectors and an ever-evolving set of expectations, reaching, motivating, and retaining employees has never been more challenging in Hungary. What sets successful employers apart today is not just what they offer but how those offerings truly resonate with people. The BeneFit Share Conference in Budapest this month will bring together companies that have already cracked the code.

BENCE GAÁL

The BeneFit Share Conference is not just another theoretical HR forum. It’s a practical, insight-

driven gathering of top-performing employers (all of whom have earned the BeneFit Prize) sharing their real-world approaches to compensation, employee retention, and workplace wellbeing.

From their tested benefit systems to the mistakes they’ve learned from, the day promises a deep dive into what actually works in today’s labor market.

The event will explore how benefits can reshape the employee

experience, turning smart ideas into sustainable, value-generating programs. Attendees will hear how top organizations integrate forward-looking trends into their HR strategies and what innovative, people-first decisions have helped them attract and retain talent in a competitive environment.

From flexible work models to well-being programs and beyond, participants will get firsthand accounts of what makes a benefits package

“Anti-Hungarian propaganda in Ukraine is on the rise because we Hungarians want peace and say ‘No’ to war; we have not sent and will not send weapons to Ukraine and [...] will not allow Hungary to be dragged into the war,” Szijjártó insisted.

Additionally, Hungary’s CounterTerrorism Center (TEK) detained a Ukrainian national in downtown Budapest on May 9, who had been banned from entering the country due to espionage activities. TEK said the individual, whose diplomatic status had expired, was questioned and deported overnight because his actions threatened Hungary’s sovereignty.

Amid the heightened tensions, Hungary cancelled a meeting with Ukraine on minority rights scheduled for May 12, Deputy Minister of Foreign Affairs and Trade Levente Magyar said in a statement issued on May 11. Magyar said the meeting in Ukraine was called off because the recent developments would preclude “constructive talks in such an important and sensitive matter as minority rights.”

not just appealing, but meaningful. The speakers are HR professionals with proven track records and practical stories to share, not just consultants with theories.

Prestigious Venue

The full-day event runs from 8 a.m. to 4 p.m. on May 20, in one of the country’s most prestigious venues: the Hungarian Academy of Sciences (MTA), located in the heart of Budapest on the Pest banks of the Danube at District V’s Széchenyi István tér. 9. (Incidentally, the MTA and the Library of the Hungarian Academy of Sciences are celebrating the 200th anniversary of their foundation this year. To mark this milestone, numerous events will take place between this month and December 2026.)

Whether you’re an HR leader looking to refine your strategy, a business owner seeking inspiration, or part of a team aiming to raise the bar, Benefit Share is the place to be. You’ll walk away with tools, insights, and real examples, and maybe even set your own company on the path to becoming the next BeneFit Prize winner.

For more information and registration, visit share.benefitprize.hu (Hungarian-language only).

NICHOLAS PONGRATZ

Photo by Tamás Purger / MTI

East Meets West: Hungary’s Strategic Role in Bridging Global FDI

Hungary’s role as a bridge between continents was the focal point of the “East Meets West” conference held on May 6 at the GermanHungarian Chamber of Industry and Commerce (DUIHK) office in Budapest.

Jointly organized by the DUIHK and EY Hungary, the event gathered business leaders, policymakers, and industry experts to explore how Hungary continues to attract diverse FDI amid global economic and geopolitical shifts.

The opening remarks by András Sávos, the DUIHK president, emphasized the need for ongoing dialogue between East and West to sustain competitiveness.

Tamás Vékási, EY Hungary’s country managing partner, noted Hungary’s reliance on FDI, particularly from Germany and, more recently, Asia.

“There was a time when Japan, then South Korea, and now China emerged as key investors,” he said, stressing the need for resilience amid global disruptions.

Vékási highlighted EY’s role in supporting investment through tax, regulatory, and strategic guidance. He pointed to shifting consumer habits and the broader uncertainty caused by inflation, war, and migration.

“Despite the challenges, we must remain optimistic and proactive,” he concluded.

In the first keynote, Simon Moger, a partner at EY in the United Kingdom and the EMEIA leader for global location services and incentives, examined how geopolitics are reshaping FDI flows. Citing a drop in global FDI from over EUR 1 trillion in 2023 to EUR 900 billion in 2024, Moger warned that national industrial strategies and protectionist policies are becoming the norm. While sectors like semiconductors and data centers are gaining importance, traditional manufacturing investments face tougher scrutiny.

In a follow-up discussion moderated by Barbara Zollmann, CEO of the DUIHK, with Simon Moger and Tamás Szűcs, EY Hungary partner and tax and subsidy expert, both stressed Hungary’s competitiveness in high-value sectors.

Szűcs outlined recent changes in Hungary’s subsidy framework, allowing for more flexible job creation metrics and a shift toward innovation and renewables.

“It’s not just about greenfield anymore,” he said. “Existing investors must demonstrate their strategic value to global headquarters.”

A highlight of the day was the appearance of Joe Wang, managing director of Sunwoda Hungary, who detailed the Chinese battery giant’s EUR 1.5 bln investment in Nyíregyháza. Sunwoda Group/Electronic, which employs more than 50,000 globally, is establishing a European base for EV battery production and automotive electronics in Hungary.

Wang cited incentives, infrastructure, and Hungary’s geographic position as some of the key factors to the investment decision. Construction is underway, with plans to localize the workforce and supply chain in phases.

“We’re not just building a factory,” he said. “We’re relocating a part of our value chain.”

Sunwoda is also partnering with the University of Nyíregyháza to ensure long-term talent development and has established a procurement team in Budapest to scout local suppliers. Wang said that although the EV rollout in the EU is not progressing at a rapid pace, he remains optimistic about future development prospects.

“Clean energy and smart mobility are the future. We’re here for the long run.”

FDI Trends

A central feature of the conference was a roundtable discussion moderated by Róbert Ésik (EY Hungary partner for global location services and

She also encouraged Asian firms to empower local leadership early on: “Once the local team is trusted, the whole company benefits.”

Hu echoed this, stating that Semcorp intends to become a “Hungarian company.” The firm is actively developing local suppliers and exploring automation and AI to remain competitive.

“We must adapt together; building understanding is just as important as building factories,” he said.

The Cultural Iceberg

In the final keynote, Margit Farkas, EY’s people consulting leader for the region, offered a human-centered view on navigating cultural differences in business. Drawing on the “cultural iceberg” model, she explored how unspoken norms, like attitudes toward time, leadership, or risk, shape business outcomes.

During an interactive session, attendees named trust, language, respect, and communication as top cultural concerns. Farkas explained that language barriers go beyond vocabulary.

incentives covering the EMEIA Region), and featuring Melinda Topolcsik (representing Japan’s Bridgestone), István Szászi (for Germany’s Bosch), and Hu Tao (Semcorp, from China).

All three offered insights into FDI trends and emphasized workforce quality and cultural adaptation as keys to success.

Szászi stressed that the growing complexity of automotive technologies requires a skilled, collaborative workforce.

“The first, second, and third factor is competencies,” he said, highlighting Bosch’s collaboration with universities and its R&D hub in Budapest.

Topolcsik described Bridgestone’s Tatabánya plant as a model of automation and continuous reinvestment.

“Our people aren’t just operators; they work with AI and program PLCs,” she said. She underscored the importance of employer branding and performance-driven investment.

Hu outlined Semcorp’s expansion, noting that Hungary was chosen for its proximity to customers and costefficiency. The company aims to localize

of its workforce by year-end and is building European supplier partnerships. “Hungary is our best location globally,” he said.

In terms of competition from Asian investors, panelists were primarily positive. Szászi saw it as a catalyst for innovation and stressed the need for ecosystem thinking, integrating startups, universities, and SMEs.

“Traditional supplier hierarchies no longer work,” he said. “We need new models of partnership, even between competitors.”

Topolcsik acknowledged the challenge posed by Chinese tire makers but emphasized internal improvement.

“The same word can mean different things based on tone or timing,” she noted, and urged leaders to embrace behavioral diversity and avoid stereotyping.

“We must adapt together; building understanding is just as important as building factories.”

Using personal and professional examples, Farkas described how Hungary’s position between Western and Eastern values allows it to serve as a cultural connector. She outlined three key strategies for success: fostering cultural safety, balancing difference and unity, and encouraging inclusive mindsets.

“Treat others how they want to be treated,” she advised, advocating what she called the “platinum rule” of leadership.

She concluded with a personal story about her early international assignments, beginning not in Singapore, as she once hoped, but in Slovakia.

“From there, I ended up working in 90 countries. It starts with openness, and it grows with curiosity.”

As the formal section closed, moderator Robin Marshall, editor-inchief of the Budapest Business Journal, thanked speakers and organizers and invited attendees to stay for networking.

“Perhaps as important as the knowledge we’ve shared today is the chance to make connections,” he said, encouraging participants to keep the dialogue going.

GERGELY HERPAI

East Meets West Roundtable discussion. From left, moderator Róbert Ésik (EY Hungary), Hu Tao (Semcorp), István Szászi (Bosch), and Melinda Topolcsik (Bridgestone).

Tenant Competition Heats Up for Limited Quality Office Space

Despite current low development levels, Budapest is the second largest office market in the region after Warsaw and, therefore, plays a significant role as a near-shoring hub. In per capita terms, it has one of the lowest stocks in the region, and there is, therefore, growth potential. That said, the limited pipeline means companies looking to move to new quality space in 2026 have few choices, comments Valter Kalaus, managing partner of Newmark VLK Hungary.

There are slight signs of a recovery in the office investment market with CA Immo selling its assets following its decision to exit the country. Trophy buildings in good locations will always remain good targets, although office buildings are not the most attractive asset type for investors these days.

The 14.1% overall vacancy rate identified by the Budapest Research Forum (BRF) could be misleading as it spans a range from 27% in the periphery to 7.8% for Central Buda. This makes clear that few companies wish to relocate to the outskirts of the city and that demand in the Váci Corridor, South Buda and Inner Buda is still very strong. The Central Business District is also attracting particular types of tenants.

“Companies that move are obviously looking to relocate to more modern

in Brief News

MNB Sees Stabilization in Commercial Property Market

The decline in valuations in Hungary’s commercial property market ended in the second quarter of 2024, and the market’s cyclical outlook showed signs of improvement, according to the “Commercial Real Estate Report” of the National Bank of Hungary (MNB), published on April 24. Although weaker-thanexpected GDP growth in the second half of the year dampened momentum in the rental and investment segments, the report said a rebound in GDP in 2025 and a recovery in the European market could ease cyclical risks. Presenting the findings, MNB director Tamás Nagy said the outlook depends heavily on a recovery in Hungary’s industrial sector. He noted that

and well-located office buildings,” says Kalaus. “It will be interesting to see what owners will do with the around 200,000 sqm of space that will become available in the near future with the relocation of governmental bodies to new buildings specifically constructed for them,” he notes. With regard to existing stock, landlords need to look at the feasibility of an office building within its location. If a large tenant relocates from an asset, the owner must consider the feasibility of firstly repositioning it, secondly, repurposing the building for use as a hotel, hostel, private school, private health center or even residential, for example.

Moving Back to the Office?

Offices are not currently considered the most attractive asset class by investors and financiers. However, usage is increasing with companies

financing should remain accessible as banks do not foresee tightening lending criteria for commercial real estate projects. Nagy highlighted continued uncertainty in the office market due to the persistence of hybrid work post-pandemic. He also noted that several office buildings have been converted into hotels and projected that upcoming completions could push the office vacancy rate to a “critical” 15% in 2025.

BIF to Pay HUF 10/share Dividend From 2024 Earnings

Shareholders of property developer Budapest Ingatlan Hasznosítási és Fejlesztési (BIF) approved a HUF 10-per-share dividend on 2024 earnings at its annual meeting, according to the AGM resolutions published on the website of the Budapest Stock Exchange. The total dividend fund amounts to HUF 2.8 billion. Shareholders

looking to bring staff back to the office. IT working practices are for one to two days in the office a week, but there is a labor shortage in the sector and staff, therefore, have a greater ability to dictate their work patterns. Hybrid work in general is here to stay, with the average being three days a week in the office, although a number of companies are looking to step up to four days a week, Kalaus explains.

In terms of requirements, he sees flexibility as key with regard to the length of leases, for example. Location remains essential, with good public

rejected an alternative proposal to pay a HUF 6 bln dividend, which corresponds to the minimum payout level required of BIF as a local real estate investment trust. BIF reported retained earnings of HUF 10.8 bln in 2024.

DH Shareholders Approve

HUF 750 mln Dividend

Shareholders of listed real estate broker Duna House approved a HUF 750 million dividend on ordinary shares at its annual meeting, according to a release published on the website of the Budapest Stock Exchange. The dividend amounts to HUF 21.8 per share, and the board has been authorized to distribute it in multiple installments. Earlier in April, the board proposed paying the HUF 750 mln dividend at the AGM and an interim dividend of the same amount at an extraordinary meeting to comply with Italian regulations. DH explained that, under Italian law, parent

This article is supported by:

Real Estate Matters

A biweekly look at real estate issues in Hungary and the region

“Companies that move are obviously looking to relocate to more modern and well-located office buildings. It will be interesting to see what owners will do with the around 200,000 sqm of space that will become available in the near future with the relocation of governmental bodies to new buildings specifically constructed for them.”

transport and car access. Services must include restaurants/cafes, fitness and wellness, bicycle storage facilities and EV chargers.

All market players need to work together with regard to ESG, including financiers, developers, constructors, landlords and office operators. Energy efficiency is crucial to building operations. Offices will need to provide flexibility, sustainability, smart systems and an employee-centric environment.

Landlords are increasingly open to incorporating a serviced office element in their buildings, as these are seen not just as tenants in their own right but also as a service to other tenants, providing temporary yet immediate space solutions, Kalaus concludes.

companies may not consider dividends declared by subsidiaries before the reporting date when setting their own dividend. Including HUF 124 mln paid on employee shares, the total dividend approved by shareholders amounts to HUF 874 mln.

Graphisoft Park

Shareholders Approve EUR 0.71 Dividend per Share

Shareholders of Graphisoft Park, which owns and operates an eponymous business park in the north of Budapest, approved the payment of a EUR 0.71-per-share dividend on last year’s earnings at an annual meeting on April 29, according to a release published on the website of the Budapest Stock Exchange. The dividend will be paid in euros. As the local form of a real estate investment trust, the company must pay 90% of its pro forma earnings as a dividend.

Valter Kalaus, managing partner of Newmark VLK Hungary

GARY J. MORRELL

2 Business German Companies Skeptical of Hungarian Business Upturn

The Hungarian economy is facing difficult times, as underlined by recent statistical data, and also reflected in the results of the spring survey of members of the GermanHungarian Chamber of Industry and Commerce (DUIHK). The subdued sentiment is visible in poor business expectations for 2025 but also in views of the overall investment climate.

With Germany being Hungary’s most significant trade partner, the views of German companies in the country give a prominent insight into its economic prospects. Numerous Hungarian and other foreign companies also participated in the survey; the results thus provide a reasonable cross-section of investor and business sentiment.

The latest DUIHK spring survey, based on responses from 236 firms, suggests that the climate for doing business is deteriorating. The chamber says that the declining confidence among foreign investors should be viewed as a red flag for Hungary’s long-term competitiveness.

Summing up this year’s findings, the chamber’s president, András Sávos, concludes: “There is no drama, but certain negative trends have become entrenched.”

According to the DUIHK survey, only 14% of firms expect an improvement in Hungary’s overall economy in the next 12 months, while 44% see it worsening. In recent years, only 2020 (COVID) and 2022 (Russia’s full-scale invasion of Ukraine) saw a similarly negative view.

Companies generally rate their own business prospects somewhat better than those of the rest of the economy. This was the case in this year’s poll, too, but even so, the balance between optimistic and pessimistic answers was close to zero, the lowest since 2012.

This “flat” outlook is linked to the projections for total (and export-) revenues, which proved similarly weak. According to the DUIHK, this is related to the strong dependence of Hungary on the German economy: current projections for zero growth in Europe’s largest economy do not justify buoyancy for companies here.

These bleak expectations are also reflected in the assessment of key risk factors: Nearly three out of four respondents named a lack of demand as a threat to their own business.

Uncertain Outlook

In reaction to the uncertain market outlook, the investment intentions of the companies surveyed have dropped sharply. Only 16% plan to increase capital expenditure, half the figure seen last year. Meanwhile, 30% are considering a reduction in investment outlays. This translates into a negative net balance of 14 percentage points, the weakest result since 2010.

Hiring plans follow a similar pattern. The share of companies that plan to expand headcount is nearly the same as those considering a reduction, with industrial firms and highly export-oriented businesses expressing particular caution.

Labor shortages started to become one of Hungary’s most urgent economic bottlenecks around 2016-2017. This year, companies reported easing pressure regarding the availability of skilled labor, even in above-average critical areas such as blue-collar workers in production, IT experts or R&D personnel.

According to the report’s author, Dirk Wölfer, this aligns with the economic prospects, which reduce the overall labor demand. This, along with falling inflation rates, has a dampening effect on wages. This year, the managers surveyed anticipate a rise in labor costs of 7%, down sharply from last year’s 11%. At the same time, satisfaction with the vocational training system and with higher education has improved. Altogether, the quality of the labor market again puts Hungary above the average of 16 other countries in Central and Eastern Europe, where German chambers produce similar surveys.

Although the DUIHK noted that the Hungarian incentive schemes for investments are seen as an advantage for attracting new FDI, and Hungary continues to score well in infrastructure and supplier networks, policy and regulatory environment evaluations are slipping.

Member ratings for legal certainty, procurement transparency, and corruption control have all worsened in recent years. An improving trend had started around 2012, but that came to a halt around 2020 and has gradually deteriorated since then. Here, Hungary performs below the (already weak) regional average.

The DUIHK’s Investor Sentiment Index

(BHI) dropped from +3 to -4 in 2025, reinforcing the message that foreign investors are increasingly uneasy.

The DUIHK survey includes a telling question: “Would you choose Hungary again as your investment location?” This year, 78% of companies answered “Yes,” down from 88% four years ago. While this number still signals strong support, the 10-point drop reflects deeper concerns.

Clear Implication

The implications are clear: while foreign companies are not planning to pull out, they are unlikely to channel new investments into Hungary under current conditions, the chamber says.

The reasons for this shift are multifaceted. International dynamics, such as supply chain diversification, rising protectionism, and internal corporate restructuring, certainly play a role. But domestic challenges, including rising costs, regulatory complexity, and political risk, are becoming harder to overlook.

Notably, export-oriented manufacturers, Hungary’s traditional FDI drivers, are more skeptical than companies serving the local market. Their exposure to international competition makes them particularly sensitive to Hungary’s relative competitiveness.

Hungary is not alone in facing weaker investor sentiment. Across the CEE region, expectations for growth and investment are down. However, Hungary’s results consistently fall slightly below the CEE regional average.

The DUIHK says foreign-owned companies remain indispensable to Hungary’s economy. They create jobs, drive exports, and lead technological advancement. But this latest survey makes it clear that their confidence is slipping.

Hungary must act swiftly to restore trust among international investors, the chamber argues. This includes strengthening the rule of law, reducing bureaucratic uncertainty, and ensuring transparent, predictable policymaking. Failure to do so could delay new investments and prompt global companies to shift future growth elsewhere.

The complete analysis is available in Hungarian on the DUIHK webpage (duihk.hu); an English version will follow soon.

German Companies: A Cornerstone of Hungary’s Economy

Over the past three decades, foreign investors have played a pivotal role in Hungary’s transformation into a regional manufacturing and logistics hub. German-owned companies alone employ nearly 230,000 Hungarians. They contribute about 11% to the value added in the total corporate sphere of the country. During the last decade, they have invested EUR 2 bln-3 bln annually into their Hungarian units, more than investors from any other country. German firms’ presence is outstandingly strong in the

automotive sector. German OEMs and suppliers generate about 60% of the industry’s total value added, and provide jobs to nearly 50,000 employees. However, German companies are also active in many other areas, such as telecommunications, machinery and electrical equipment manufacturing, retail trade, and energy. As a result, Germany is responsible for onequarter of Hungarian exports and imports, making the Hungarian economy quite dependent on German business cycles.

DUIHK president András Sávos.

Generative AI and Business: Massive Potential, Many Pitfalls

In a joint presentation to the British Chamber of Commerce in Hungary on April 30, Andrea Belényi and Endre Várady, partners at law firm VJT & Partners, outlined the many positive areas of usage of generative AI, along with the equally many dangers.

tool into your system, you can become a developer, and this would add a new layer of compliance obligations,” Várady warns.

This vast minefield of potential disaster means companies are well advised to establish wellthought-out AI policy guidelines and governance structures in good time.

The power of generative AI, using software tools such as ChatGPT and Microsoft Copilot, is truly vast, but as an example by Andrea Belényi illustrates, the possibilities of embracing disaster, however unwittingly, are very real.

Without revealing names, she related the story of an employee at a law firm who, while researching legal rulings using generative AI, discovered a seemingly relevant court case, complete with a decision, that the employee later cited in court to buttress a case of their own.

Sadly, what the employee did not know, nor check, was that the entire case was fictitious: it had been created by the generative AI tool.

“That’s why it’s very important to double-check what generative AI produces, [...] it can give you different answers to the same question. [...] Our colleague used this case without checking, which was a huge mistake,” she said.

(Although Belényi kept this incident strictly anonymous, a simple Google search for “fictitious AI court rulings” reveals several such cases, with at least one involving a major U.S. law firm.)

Regardless of such “hallucinations,” as these fictitious inventions are termed in generative AI-speak, the new technology is here to stay and is increasingly being taken up by businesses seeking to enhance productivity.

Indeed, generative AI is a “hot topic today,” Belényi declared, and with good reason.

“It’s a top priority of all businesses. It’s very easy to accept generative AI, it’s very easy to use, and it has really huge power, which is why the vast majority of businesses and companies have already started using it in their operations,” she said.

However, all too often, like the U.S. law firm, companies begin using the new technology unaware of the many issues and risks involved. To explain these risks, Endre Várady turned to the European Union’s AI Act, which will come into force in August next year.

“The purpose of the AI Act is very clear, it aims to regulate AI, to handle risks, to protect fundamental rights and values and at the same time it has also evolved to promote innovation,” Várady said.

Fit for Purpose?

To the layperson, this is all very reassuring, although, as he added, there is considerable debate as to whether the act is up to fulfilling its broad goals, since it is so detailed that efforts are already being made to simplify it.

Nonetheless, according to Várady, it forms a good basis for introducing the challenges because “without understanding the basic concepts, we cannot really talk about applying AI user policy management in a meaningful way.”

In essence, the act takes a very logical, risk-based approach, with a structure of use-cases ranging from a prohibited category through high and limited risk, to low risk.

The prohibited AI categories are formally banned under the AI Act, which sets out a list of practices that are simply not permitted.

“Users should exercise great caution to ensure they avoid these

use cases,” Várady warns, citing as some of the key examples AI systems that infer emotions of a natural person in sensitive contexts such as the workplace or education, and any systems that use subliminal techniques to manipulate human behavior or that exploits vulnerabilities of children, persons with disabilities, or otherwise disadvantaged individuals.

He also highlights “social scoring” as another no-go area, “Not only in the sense of state surveillance, as seen in China, but also private-sector scoring, such as banks using AI to assess creditworthiness based on social media profiles.”

Understandably, businesses keen to gain a commercial advantage by using AI must study the act carefully to ensure they are not merely overstepping ethical norms, but also potentially committing a criminal act.

As ever, the devil is in the details, or perhaps more immediately, the misconceptions that have already grown around them, as Várady was at pains to point out.

“First, there is often a misconception that the AI Act is only about developers. This is not true, it applies to business users: Any business user who uses AI tools, including generative AI, is considered a user under the AI Act,” he emphasized.

Beware the Naïve Defense

Another is often taken by, as Várady put it, those who naïvely comfort themselves with the thought, “I do not select high-risk use-cases. I use ChatGPT just for everyday work, so why should I care?”

The partner cautions, “Maybe today you do not fall under the high-risk category, but you can fall tomorrow. Think about job screening or employee monitoring or talent management: these sound very familiar, I guess, to all businesses, but access an AI tool and you can immediately change into the highrisk category.”

Similarly, any idea of simply remaining a user is also fraught with obscured danger. “As soon as you add some fine tuning, with specific data or integrate an AI

“On one hand, this means we have a clear structure. For example, it has to be very clear what the scope of the AI policy is, to whom it applies, whether just to employees or also outside partners, plus what devices are under the scope of the AI usage policy, and how we define the AI tools. All this is very important for employees to understand the unauthorized AI apps,” he suggests.

Companies also need to specify crystal clear processes, such as who grants approvals and who assesses risks.

“The user policy must be a very simple one, with clear boundaries, what is allowed and what is not [...] so that employees can easily understand what their roles are, and what they shouldn’t do,” Varady stressed.

If this all appears to be a mammoth task, it becomes even more of a concern considering the “new mindset” needs to be ready for action when the AI Act comes into force in a little more than a year.

However, “AI governance is the thing which makes AI usage policy into a living part of an organization,” he said, on a more optimistic note.

The alternative, as illustrated by Várady, is even more frightening: “We need governance, because without governance, the AI usage policy is like driving a car without a steering wheel,” he said, by way of an analogy. “You will drive it, but you don’t know where you will go.”

KESTER EDDY

Andrea Belényi

Endre Várady

DVM at 30: How the ‘Sum of Small Improvements’

Built a ‘Deeply Exciting’

Business

This year, DVM group marks the 30th anniversary of its foundation in Budapest in 1995. To mark the occasion, the Budapest Business Journal sat down with its three managing partners and co-owners, Tibor Massányi, Péter Haberl, and Balázs Czár, to discuss the past, present, and future of one of the most consequential providers of integrated building services in Hungary.

naturally, had its ups and downs. It had some very uplifting and also some very difficult human moments. These have stayed with me more than the professional and business successes.

BBJ: How has the market in Hungary changed in that time?

BCz: The Hungarian property market has changed as Hungary has, in economic, social, and technical terms. The players, the companies, the professionals, the clients, and the designers are all much better prepared than they were 30 years ago. At the same time, everything has become more complex: the legal and business environment, the technical systems and regulations, and the needs of the customer. Overall, I feel that we have a more challenging job today than we did a few decades ago.

BBJ: Looking back, is there anything you would change or do differently?

BCz: I’m sure there would be if I started thinking about it, but I don’t want to!

BBJ: What role did international projects play in the last 30 years, or was the focus on Hungary?

BCz: Most of our work is in Hungary, but almost every year we have also performed some design or project management projects abroad. Many of our clients are international companies, for whom we have worked in other countries on many occasions. This is something we would like to develop naturally, and we are currently in the process of some promising negotiations.

BBJ: How many people are employed by DVM today? What business lines do you operate?

BBJ: What are the most significant projects you have worked on recently?

PH: Following the recent completion of the five-star W Hotel within the historic Drechsler Palace, our team is currently engaged in developing another five-star establishment, the St. Regis Hotel in the Klotild Palace. This project is scheduled for completion by the end of this year. Both properties

are part of Marriott’s portfolio of luxury brands; thus, the standards and expectations are equally exacting. In both instances, our task involves the integration of a contemporary, fivestar luxury hotel within the framework of a nationally protected, iconic heritage building in Budapest.

BBJ: How did DVM come to be formed? Balázs Czár: DVM was founded by the late Attila Kovács, and it’s now no secret that it was 30 years ago; the original company name was DVM Design Kft. At the beginning, the company was mainly engaged in office and interior design, which was our principal profile. A few years later, in 2001, DVM Construction Ltd. was established, specifically to carry out construction work.

BBJ: What have been the company highlights from the past three decades?

BCz: It is difficult to highlight certain things. For me, the last three decades have been more about steady, consistent work and company building that has,

Péter Haberl: DVM group currently employs a team of 150 professionals, the majority of whom are engineers, complemented by specialists in key support functions such as finance, human resources, legal, and administration.

In addition to our core organization, we also operate joint venture companies established either on a project-specific basis, such as the DVM-MAN partnership for the Klotild Palace development, or focused on specific industry segments, such as DVM Greenfield, which specializes in the construction of industrial facilities.

DVM has long been recognized for its dual strength in both design and construction, a reputation that is particularly evident in our design and build projects. This integrated capability was a hallmark of our early fit-out operations and continues to characterize our current activities across office, hospitality, residential, and industrial developments.

BALÁZS CZÁR earned his civil engineering degree from the Technical University of Budapest in 1996, but had already gained professional experience at various major Hungarian companies during his academic years. He started his career as a technical surveyor of gas station installations, and later managed large-scale construction projects for Kész Ltd. In 2000, he served as technical and planning coordinator of power plants completed in the United States, and liaised between Kész and the

Dutch NEM group. That same year, he joined DVM Construction Ltd., where he is now managing partner, technical director, and head of construction projects. Czár is also co-owner and managing partner of Horizon Development, the premium real estate development company founded by Attila Kovács in 2006, whose projects include commercial and residential properties such as Eiffel Square, Eiffel Palace, Váci 1, Promenade Gardens, the Szervita Square Building and ParkSide Offices.

ROBIN MARSHALL

more efficient working methods, and planning and executing projects more consciously. We must focus even more on environmental awareness and recognize the responsibility we bear in shaping our surroundings.

It’s often the sum of small improvements that results in truly great outcomes. These “small things” are what make our work better and more meaningful. So, while I don’t have grand new business plans to announce, I believe it’s these detailed, thoughtful improvements, born from the engineering mindset, that hold the real value. I hope this doesn’t sound discouraging, because engineering is a deeply exciting and motivating field.

BBJ: Developing that thought, if you cast forward another three decades, what do you think the DVM of the future will look like? How will it be different from today?

TM: One thing is certain: at DVM group’s 60th anniversary celebration,»I would much rather attend as a guest at age 77 than be the one giving the speech! Jokes aside, I believe that during its first 30 years, DVM group always recognized market shifts and emerging demands at the right time. We’ve always approached our work with humility and professionalism, investing all our energy into what we do. That’s the key to our success. These values won’t change as long as Balázs, Péter, and I are involved in the company’s daily operations.

“DVM group always recognized market shifts and emerging demands at the right time. We’ve always approached our work with humility and professionalism, investing all our energy into what we do. That’s the key to our success. These values won’t change […]. And I hope that, just as in the first 30 years, we’ll continue to deliver remarkable projects.”

And I hope that, just as in the first 30 years, we’ll continue to deliver remarkable projects that make our colleagues, and me, proud. In the next 30 years, the nature of our work will likely change significantly due to technological advancements, and as a result, our team structure will evolve too. But that’s how we’ll continue to uphold the standard of engineering excellence we’re known for today.

“Today, in addition to fitout, we are active in base building projects, as well as in the hotel, residential, and industrial sectors. Despite this diversification, the original commitment to quality, our meticulous approach, and an unwavering attention to detail continue to define our work.”

BBJ: We constantly hear how AI and digitization will change our future. Are you already seeing signs of that today? What might the next significant trend look like for the construction industry?

TM: Digitalization has been present in the construction industry for many years. The supporting technologies are constantly evolving, and new solutions regularly appear that promise greater efficiency. Identifying the right tools, integrating them into workflows, educating users, and convincing them that these tools genuinely support their work must be a priority. There is no room for hesitation or postponement in adopting these technologies. Anyone who avoids them will inevitably fall behind and lose their competitive edge.

Although I would currently place AI in a separate category within construction, the same principle applies: we must actively explore and understand its potential. We need to identify where it can be integrated into workflows and how it can increase efficiency. There are already countless promising applications out there today.

That said, I’d like to highlight a shocking, and perhaps alarming, statistic: by 2030, the energy required for data processing (primarily driven by AI) is projected to equal the entire energy demand of the steel, cement, and other energy-intensive goods combined in the United States. This means that, by 2030, AI-related energy consumption will quadruple.

From this forecast, two things are clear: 1) If AI continues to evolve at its current pace, it will permeate every aspect of our lives by 2030, including construction. 2) It is critically important to approach new technologies with conscious caution and to ensure proper regulation.

Future trends in construction will be more technology-driven than ever. On the software side, AI will become increasingly common. On the implementation side, I believe prefabrication will gain ground, especially in markets that demand high-volume, standardized production, something that suits ongoing

TIBOR MASSÁNYI received his degree in civil engineering from the Ybl Faculty of Szent István University in Budapest in 2000. As head of design and project management at Arkon Inc. between 2000 and 2004, he worked with clients such as Nokia, Vodafone and T-Mobile (now Magyar Telekom). He joined WS Atkins Hungary Ltd. in 2002 as lead architect and gained invaluable professional experience in

technological development. With the global and Hungarian decline in the number of engineers, technological progress is key to maintaining and improving efficiency in construction. In that sense, it could also help balance the growing energy demands of AI, at least in our industry.

BBJ: Do you ever worry about the future of the firm, or the industry in general, or are you positive about the resiliency of (and need for) the business TM: As a leader, it’s natural to sometimes worry about the future.

the international business environment. He developed his leadership skills as the managing director of Pozitan Ltd. between 2004 and 2006. Since 2006, he has been a managing partner of DVM Design Ltd. (renamed DVM group Ltd. in 2021) and the operational director of the design, architectural visualization, project management, environmental consulting and marketing communication departments.

But I also believe in staying optimistic about change and spotting emerging trends and opportunities before they fully materialize. While concern is part of leadership, it’s our ability to recognize and respond thoughtfully to change that helps shape a more secure and positive future. In my view, it’s the leader’s vision that defines the direction of progress. Without vision, there’s no promising future, only aimless drifting. And without a compelling vision, there’s no talented, motivated team to turn that into reality.

Cetin Hungary Marks 5 Years with Major Network and AI Upgrade

Cetin Hungary, which describes itself as the country’s first and largest independent mobile telecommunications infrastructure provider, is marking its fifth anniversary this summer by completing a nationwide modernization project worth more than HUF 102 billion.

concluded in December 2024, included a complete upgrade of radio equipment, antennas, power supply systems, and passive infrastructure such as towers and support structures. By the end of last year, 23% of Cetin’s base stations were already operating with 5G capabilities.

In just five years, the company has transformed Hungary’s mobile backbone, introduced AI-powered operations, and delivered the country’s first multioperator 5G indoor coverage. The Budapest-based infrastructure specialist was formed in July 2020 during the legal separation of Yettel Hungary (formerly Telenor), when it took over the operator’s active and passive network elements.

Since then, Cetin has grown rapidly, both in size and strategic scope, becoming a critical enabler of next-generation mobile services across Hungary. With a workforce of approximately 230 professionals and a customer base exceeding 50

telcos and enterprise clients, the company closed 2024 with revenue of HUF 73.6 bln, a significant increase from HUF 22.2 bln in 2020.

“The separation of end-user mobile services and the underlying infrastructure is a global trend. Cetin Hungary was the first in the country to adopt this model,” says CEO Judit Kübler-Andrási. “We now operate one of the most extensive telecom infrastructure networks in Hungary.”

Over the past five years, the firm has built up and now manages approximately 4,050 base stations and the optical and radio transmission backbone that connects them. The modernization drive,

Alongside physical upgrades, the company has increasingly embedded artificial intelligence into its operational model. According to Kübler-Andrási, Cetin monitors network health through around 200 key performance indicators and uses AI tools to continuously analyze and optimize network parameters.

“We use AI to identify the 100 weakestperforming cells on a weekly basis and automatically adjust their configurations,” she says. “This approach has delivered measurable improvements in quality and performance.”

Predictive Maintenance

Cetin’s AI solutions also support maintenance by analyzing traffic trends and quality metrics in real time. The platform compares live data with predictive models, enabling engineers to detect anomalies or service degradations within minutes.

“This level of insight allows us to respond before users even notice an issue,” Kübler-Andrási adds.

The company’s commitment to AI doesn’t stop there. More than 60%

of its

employees now use AI tools in their daily work, and Cetin is developing specialized AI agents to support engineers in radio planning and network operations. The goal is to integrate corporate knowledge and technical

The Allee project exemplifies Cetin’s broader strategy of supporting digital infrastructure not just for mobile carriers but for the entire ecosystem of data-dependent businesses. In addition to wireless infrastructure, the company provides SD-WAN, leased line, and cybersecurity services and operates mission-critical data centers throughout Hungary.

The business is not resting on its laurels, however. After completing its four-year modernization program, the company is already preparing for further investments in 2025 and beyond.

Kübler-Andrási confirmed it plans “significant new development projects” to meet future traffic growth and customer demands.

While Cetin’s origins are firmly rooted in supporting Yettel’s operations, the company has diversified steadily. Today, it operates entirely independently, offering infrastructure services across the market. This positioning is key in an era when connectivity is essential not only for communication but also for productivity, logistics, and automation.

experience into an intelligent platform that enhances efficiency and decisionmaking across departments.

Another area where AI plays a growing role is energy optimization. The firm’s energy efficiency program uses machine learning to dynamically scale capacity in line with fluctuating traffic demand, maintaining user experience while minimizing power consumption.

The company’s expertise has made it a sought-after partner not just for telcos, but also for property developers. Cetin has pioneered the deployment of operator-neutral indoor antenna systems in buildings where traditional radio signals are obstructed. This includes high-density commercial properties, residential complexes, office buildings, hotels, factories, sports centers, and urban transit hubs. These indoor systems are vital in modern buildings, where environmentally efficient construction materials often block mobile signals. Cetin offers its solutions as a turnkey infrastructure service to real estate developers, ensuring reliable voice and data connectivity in so-called “radio blackspots.”

In late 2024, Cetin commissioned Hungary’s first indoor antenna system capable of delivering 5G services from all three major mobile operators (Telekom, Yettel, and One) inside the Allee shopping center in Budapest.

Engineering Milestone

“It’s a milestone that showcases our engineering capabilities and commitment to multi-operator solutions,” says Kübler-Andrási. “We believe this model will become standard across high-traffic indoor environments.”

The firm’s proactive approach has also earned its main customer highprofile accolades. Thanks in part to Cetin’s 5G-ready infrastructure, Yettel was named the fastest mobile network in Hungary in the second half of 2024 by Ookla Speedtest.

“We use AI to identify the 100 weakestperforming cells on a weekly basis and automatically adjust their configurations. This approach has delivered measurable improvements in quality and performance.”

National measurements by the Hungarian Media and Communications Authority also confirmed that Yettel had the best 4G and 5G download and upload speeds during the same period.

“Such recognition reflects our shared commitment to excellence,” notes Kübler-Andrási. “Our goal is not only to enable fast and reliable networks but to make sure they’re sustainable, intelligent, and future-proof.”

Cetin’s recent collaborations with Hungarian universities, including Széchenyi István University in Győr, Óbuda University, and the University of Pécs, further demonstrate its longterm investment in talent and innovation. The company also supports youth STEM programs and is exploring partnerships in the construction industry, notably with BudaPart and Skanska Hungary.

GERGELY HERPAI

From left, Judit Kübler-Andrási, CEO of Cetin Hungary, and Zsolt Kozma, director of regulatory and PR.

Hungary’s Corporate Landscape Split Between Competitive Winners, Struggling Laggards

The Hungarian economy has become a tale of two worlds, with some businesses flourishing, while others fall further behind, according to the latest research by the Corvinus University of Budapest’s Competitiveness Research Center.

Companies have distinctly different perceptions of the country’s political and economic conditions, with the more competitive firms generally seeing the environment as supportive, while lagging firms consider it an obstacle.

However, both groups have learned to adapt to the system, and most feel at home within the framework of Hungary’s current political and economic structure, commonly referred to as “NER” (National Cooperation System).

The latest report on Hungary’s corporate competitiveness by Corvinus University reveals a stark divide between high-performing and underperforming businesses. This divide is not only a matter of economic success but also shapes how companies experience the country’s political landscape.

The survey, which included 335 responses from medium- and large-sized Hungarian companies, 90% of which are domestically owned, revealed that competitive companies are increasingly accustomed to navigating the NER rules, while struggling firms often face more challenges in doing so.

The Corvinus findings show that the corporate landscape in Hungary is now clearly split into two distinct camps. The competitive companies, 175 of the total that responded, outperform their counterparts in almost every aspect, from productivity and profitability to adaptability and market share.

These companies reported more favorable conditions regarding access to capital, the regulatory environment, and overall economic performance. Despite the obstacles posed by factors like inflation, supply chain disruptions, and geopolitical tensions, competitive firms view the Hungarian political system as stable and predictable.

According to Attila Chikán Sr., director of the Competitiveness Research Center, “The Hungarian business environment

has become something of a known entity for many companies. While some may find it challenging, most have adapted to the system and now view it as a reliable platform for their operations.”

This sentiment reflects the growing confidence among firms in navigating the complexities of Hungary’s economic policies.

Taking Advantage

A significant percentage of companies in this group have not only managed to thrive under the NER system but have also learned how to take advantage of the opportunities it offers, such as access to government-backed grants, favorable tax policies, and a relatively stable currency.

These companies focus on maintaining high levels of operational efficiency and are more inclined to innovate in response to consumer demand, Corvinus finds.

In stark contrast, the

companies

categorized as lagging behind face a far more difficult environment. These firms are predominantly based in regions outside the central and capital areas, with a large portion operating in the manufacturing and logistics industries.

For these companies, the political environment is perceived as a significant hindrance to growth, with frequent regulatory changes and an unpredictable policy landscape creating challenges in decision-making.

The struggle for these companies is compounded by factors such as rising inflation, high energy costs, and ongoing supply chain disruptions caused by the ongoing conflict in Ukraine.

Many of these firms find themselves squeezed by rising operational costs and decreasing demand, making it challenging to remain competitive. According to the report, while many of these companies acknowledge the stability of the Hungarian political system, they view the current economic climate as highly unfavorable for survival.

Interestingly, these companies also report greater difficulties securing financing and credit, with many excluded from more lucrative government programs. The economic pressures have led to worsening payment discipline, as these firms struggle to collect payments from clients while facing increasing operational costs.

The division between competitive and lagging companies is more than just an economic issue; it’s also profoundly political. While the competitive firms primarily view NER as an advantageous system that supports their business models, lagging companies feel marginalized. These businesses face significant hurdles in accessing the same growth opportunities, often struggling to keep up with larger, more politically connected firms.

“While the political and economic systems are often seen as stable, they are not always seen as fair,” said Chikán. “There’s a growing sense that the most competitive companies are able to leverage the system for their benefit, while those at the bottom are left to contend with a much more challenging environment.”

Innovation Slowing

Despite the divide, the report also shows that many companies, regardless of their competitiveness, focus on adapting to the changing environment through innovation and digital transformation. However, the survey found that innovation has slowed significantly since the onset of the COVID-19 pandemic, with many firms now focusing more on maintaining operational stability than pursuing groundbreaking innovations.

In particular, Hungarian companies are placing greater emphasis on sustainability and meeting the demands of increasing regulatory pressure. However, this shift is more a response to tightening regulations than a proactive drive toward long-term sustainable development.

“Many businesses are ‘greening’ their operations […] to avoid penalties, not because they genuinely see sustainability as a long-term strategy,” noted Chikán. In terms of financial strategies, the report highlights a growing willingness among competitive companies to invest in their operations, with a particular focus on technology development and innovation. The ability to secure financing and invest in future growth has been crucial for maintaining competitiveness, especially as the global economy continues to face challenges. Interestingly, more companies are taking out loans and engaging in public funding programs than in previous years. Despite this, the rise in debt is accompanied by a decrease in payment discipline, with late payments and cash flow issues becoming more common among struggling firms.

The report also notes that nearly 50% of the surveyed companies have won grants for technological advancements and energy efficiency upgrades, indicating that public funding continues to play a critical role in supporting innovation.

Looking ahead, the outlook for Hungarian businesses remains uncertain. The report emphasizes that while the most competitive companies are in a strong position to weather storms, lagging firms face significant challenges. These include navigating political uncertainties, coping with rising inflation, and responding to an increasingly complex regulatory environment.

The division within Hungary’s corporate sector will likely continue, with competitive companies increasingly leading the charge regarding innovation, investment, and sustainability. On the other hand, lagging companies may continue to struggle unless they can adapt more rapidly to the changing landscape and secure better access to capital and growth opportunities.

GERGELY HERPAI

From left: Attila Chikán Sr., director of the Corvinus Competitiveness Research Center; Erzsébet Czakó, co-director; and research director Dávid Losonci.

Income Inequality and High Deficit Slow Business in Hungary

Inflation, dragging GDP growth, and an excessive budget deficit; economic and financial hardships go hand-in-hand for the Hungarian population and government.

With a prolonged recession last year, the Hungarian government announced a comprehensive program in October 2024 to reignite the economy this year. Prime Minister Viktor Orbán promised that results would be visible as early as the first quarter, with annual GDP growth of at least 3%, possibly even 6%.

While GDP did manage to break the 0% barrier in Q4 2024, the data for Q1 2025 proved a cold shock to economic governance: -0.4%. This figure not only contradicted the Prime Minister’s promise of spectacular growth but also challenged this year’s forecasts. The full-year growth of 3.4% projected in the budget now appears unrealistic; perhaps even 2.5% may be out of reach.

This is bad news for a government preparing for elections in 2026, in a country with a history of generous preelection spending. Before the 2022 elections, the Orbán cabinet spent HUF 1 trillion across various social groups. Back then, more than 5%

GDP growth provided the necessary fiscal space. This year, however, the situation is different.

GDP growth is not only an electoral issue. A low growth rate means that businesses have limited scope for wage increases, which, when combined with accelerating inflation, erodes real incomes. Given the government’s visibly constrained ability to stimulate growth, its only remaining lever is tackling inflation, which stood at 4.7% in March.

To address this, the cabinet chose an instrument previously shown to be of limited effectiveness, albeit now in a revised form. Instead of capping product prices directly (as happened when inflation peaked alarmingly during the economic shock that followed in the wake of Russia’s full-scale invasion of Ukraine), the new measure targets profit margins, setting a maximum of 10% on 30 essential items.

Some Progress

April’s inflation data showed some progress, with the rate easing to 4.2%, the lowest since November last year, though still not back within the official 2-4% target range of the National Bank

Finance

Matters

A monthly look at financial issues in Hungary and the region

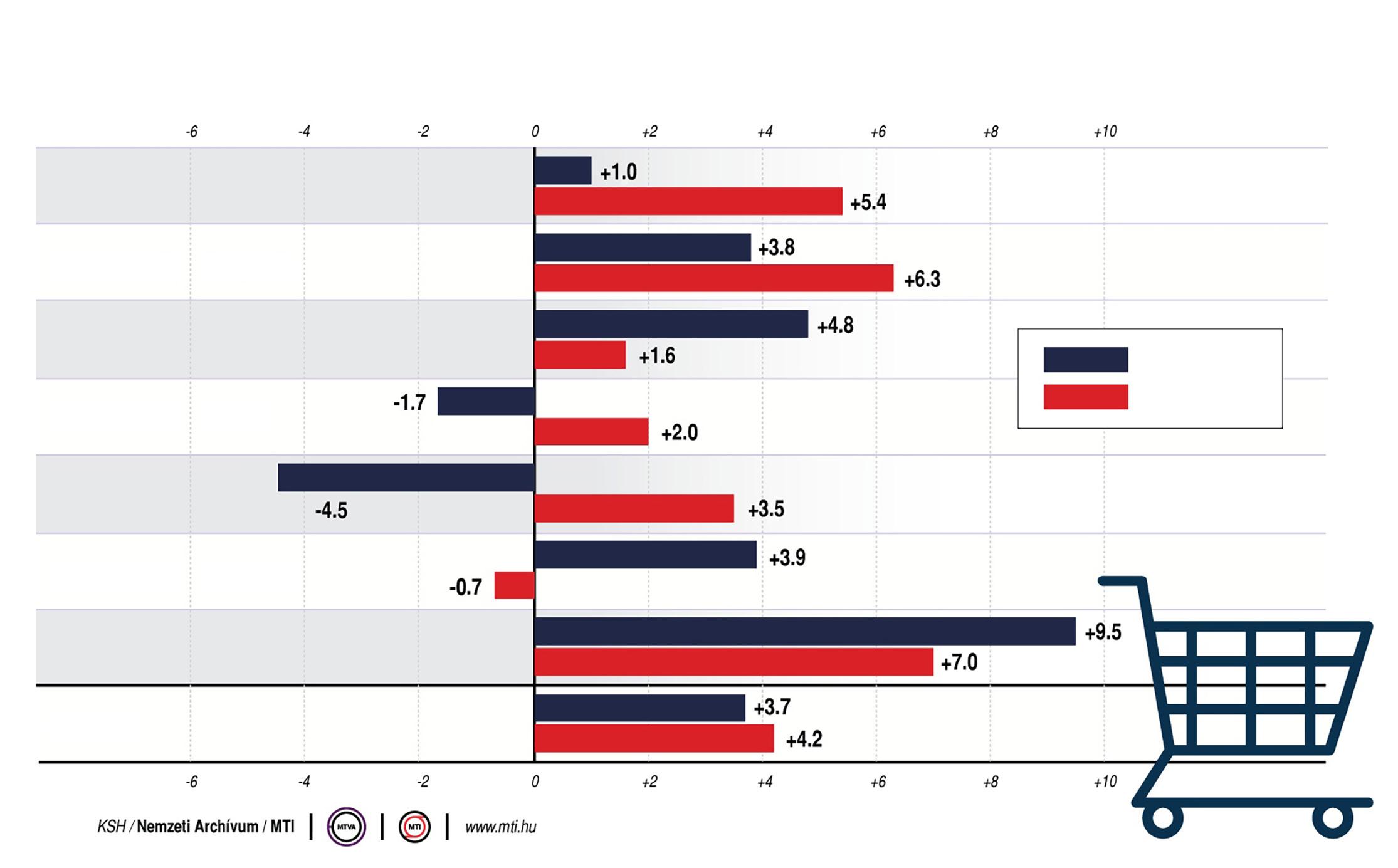

Change in Consumer Prices in Hungary (April 2024-April 2025)

Compared to the same period of the previous year; percent

Source:

of Hungary (MNB). Year-on-year, food prices in April rose 5.4%, services by 7%, alcoholic beverages and tobacco by 6.3%, and household energy by 3.5%. Compared to March, food prices were actually down by 1.3%. This suggests that the profit margin cap may be helping to reduce prices. Fuel prices also contributed, with petrol down 7.1% yearon-year and 1.4% month-on-month.

However, according to sales data, consumers remain unmoved by the modestly improved prices. The Central Statistical Office (KSH) reported on May 7 that retail sales in March were down 0.4% from February, and only

higher

than in March 2024. Péter Virovácz, an analyst at ING, commented: “Looking at the retail data from the first three months of this year, after a spike in January, the sector has failed to stabilize.” Consumer confidence remains far below the highs of 2018-2019, and saving clearly takes precedence over spending.

“The most surprising thing is that the profit margin cap introduced in mid-March has been unable to reignite the retail sector,” Virovácz added.

Income inequality is also hindering the recovery in consumption. Market research institute GKI analyzed KSH data and found that a worrisome twothirds of Hungarian employees earn less than the gross average wage.

According to GKI, the bottom 10% of earners account for just 3.5% of total income, while the top 10% receive 28.1%, an eightfold disparity. In fact, the top 10% of full-time employees collectively

earn more than the entire bottom 50%. This also helps explain weakerthan-expected consumer spending.

“A fundamental principle in economics is that lower-income individuals tend to spend a greater proportion of their income, while higher earners are more likely to save. As a result, widening income inequality can have a negative impact on retail turnover and other consumption indicators,” GKI noted.

According to GKI, the bottom 10% of earners account for just 3.5% of total income, while the top 10% receive 28.1%, an eightfold disparity. In fact, the top 10% of full-time employees collectively earn more than the entire bottom 50%.

Compared to 2023, the lowest earners saw their gross monthly income rise by HUF 29,500, while those at the top gained HUF 166,600 per month.

Dampening Effect

“Beyond questions of social fairness, income inequality dampens domestic consumption, as a smaller share of income goes to those most likely to spend it,” GKI concluded.

Meanwhile, consumers are increasingly turning to credit. In March, families took out personal loans totaling more than HUF 90 billion, an unprecedented figure, according to Bank360. The average value per loan contract rose to HUF 3.3 million.

Mortgage lending reached HUF 137 billion in March, the highest in three years, with an average contract value of HUF 19.9 million. This indicates a rise in property prices. In January-February 2024, the average mortgage contract value was

HUF 14.6 mln, suggesting that borrowers are seeking higher loans to keep pace with housing costs. As the MNB is not expected to reduce its base rate any time soon, loan interest rates, which currently range from 6.18% to 7.99%, are likely to increase further.

While households may feel secure in managing loan repayments, the government is facing mounting fiscal difficulties. By April, the general budget deficit had already reached 71% of the annual target. With consumer spending low, VAT revenues are lagging. Nevertheless, Minister for National Economy Márton Nagy recently claimed that “Budget revenue rose in line with expectations, supported by increasing consumption, even as GDP underperformed.”

On May 13, Nagy confirmed that Hungary had requested the activation of an EU “escape clause” to allow for greater fiscal flexibility in defense spending, effectively permitting a higher deficit.

BALÁZS BARABÁS

3 Special Report

Real Estate: Offices

Low Levels of Speculative Development in Budapest

Speculative office building in Budapest continues to fall as developers exercise caution in their development strategies. New projects are not being initiated in an uncertain geopolitical environment, with questions over long-term demand, and (critically, when it comes to speculative builds), concerns over the cost and availability of finance.

“Financing is crucial, and most banks require a 45% to 50% prelease for an office development. Securing sufficient preleases for each phase is crucial to avoid financial strain,” comments Valter Kalaus, managing partner of Newmark VLK Hungary.

Prelease requirements are expected to remain high, maybe as much as 60% to 70%, according to Mátyás Gereben, country manager at CPI Hungary.

The Budapest office market has expanded by 750,000 sqm over the past five years, much of which is the work of a relatively small number of established Hungarian and regional developers.

Total Budapest office stock stands at around 4.42 million sqm of space, according to the Budapest Research Forum (which comprises CBRE, Colliers, Cushman & Wakefield, Eston International, iO Partners and Robertson Hungary). Of this, 3.57 million sqm consists of speculative class “A” and “B” space.

speculative basis, so we expect these projects to commence after a reasonable level of preletting or owner-occupation,” says CBRE.

Vacancy Rising

Overall vacancy is expected to rise to 15% by year-end, with further pressure on overall vacancy rates as public sector authorities vacate around 225,000 sqm of older stock, in the view of the consultancy. Regarding demand, Budapest has demonstrated a strong recovery with leasing activity growing 8% year-on-year for 2024, exceeding 500,000 sqm, the fourth successive year of growth. Budapest continues to attract and retain occupiers despite broader global market shifts, says Cushman & Wakefield. The BRF has traced lease renewals as representing 45% of total demand in the first quarter of the year.

Cushman has traced 17 office projects due to be delivered by

2027,

with only three going ahead on a speculative basis by established Budapest office market developers: Skanska, GTC, and Atenor. This year, we will see a sharp drop in speculative development, with only 42,000 sqm slated for delivery.

The low speculative office pipeline will likely result in a limited supply of quality, well-located offices that conform to ESG expectations and regulations, despite rising overall vacancy rates heading towards the 15% mark. Indeed, a gap is evident between well-located high-end offices and class “B,” noncentrally located and non-ESG compliant space; availability is significantly higher in the latter category.

The total speculative office pipeline, excluding on-hold projects, through to the end of 2027, amounts to 84,100 sqm, with the Váci Corridor (including the second phase of the H2Offices project and Centerpoint III) accounting for the largest share, at 59,200 sqm.

Colliers says the remaining projects are relatively small in scale and scattered across the city. In the current uncertain economic environment, developers require a substantial prelease before proceeding with a development.

The top six landlords in the Budapest office market are CPI, OTP Real Estate Investment Fund, Erste Real Estate Fund, GTC, CA Immo, and Wing, according to Cushman & Wakefield.

New Blood Welcome