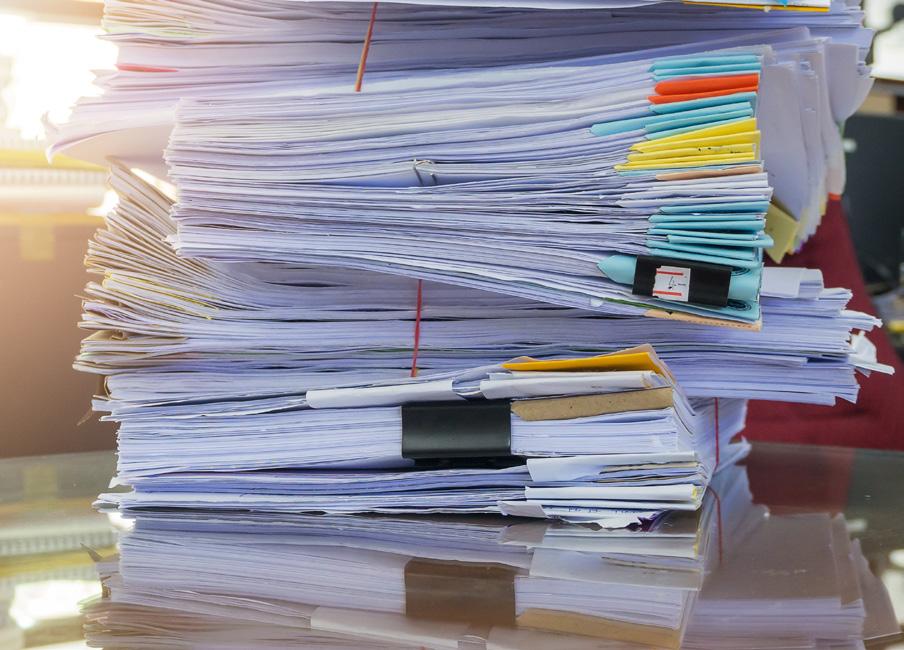

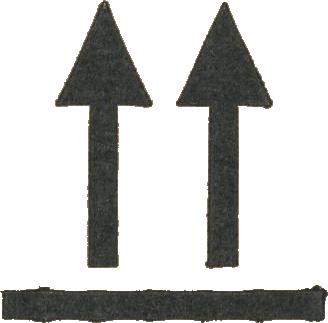

the home-buying process

seller

❱ Comparable Sales Reviewed

❱ Market Analysis Presented

❱ Price Range Established

❱ Listing Agreement Signed

❱ List on MLS

❱ Open Houses (Brokers & Public)

❱ Showings by Appointment

❱ Advertising

❱ Provide Property Disclosures

❱ Facilitate Property Inspections

❱ Inspections & Conditions Removal

buyer

❱ Needs/Wants Discussed

❱ Buyer Agency Agreement Signed

❱ Financial Qualifications Determined

❱ Market Education

❱ View Property

❱ Write O er with Agent

Purchase O er Presented to Seller

Negotiation of Terms

Seller Agent Buyer Agent

Accepted Sales Contract

❱ Open Escrow

❱ Deposit Earnest Money

❱ Disclosure

❱ Inspection

❱ Title Search

❱ Preliminary Title Report

❱ Obtain Necessary Property Inspections

Loan Process

Days

Days ❱ Loan Condition Removal

Additional Negotiation (if necessary)

Seller Agent Buyer Agent

❱ Inspections & Conditions Removal

❱ Recieve Cash Proceeds

❱ Move Out

Closing

❱ Loan Funding

❱ Title Records at City Hall

❱ Utilities O /On

❱ Keys Received

❱ Move In

GUIDING YOU THROUGH THE PROCESS

There are a lot of steps, forms, and considerations involved with a real estate transaction, and timely completion of each is critical. I’ll be your point person in the transaction and will guide you through the process and the contract. I’ll ensure you understand all options, documents, and fees, and will anticipate potential issues before they arise.

Defining your agent relationship

The first step in hiring me is coming to an agreement on the terms of my representation, which is called a Buyer Agency Agreement. This includes key factors like how long you want to work with me, the exclusivity of our relationship, and how I’ll be compensated. This short agreement helps define how our relationship works early on and will give you key insight into my role, adding transparency throughout the process.

Buyer Agency Agreements have not always been required, but have recently been introduced as a mandatory step that is meant to provide you with greater transparency into the process and how I am compensated for our services.

Identifying your goals

After you hire me, my first step will be to get to know you better to understand your situation, needs, and goals for buying a home. We’ll discuss the area(s) that you’re most interested in and why, and I can advise you about the current market there and answer any questions you may have. I’ll also provide you with a checklist to help you identify your wants vs. needs and prioritize which home features and lifestyle goals are most important to you.

Determining your search area

Fair Housing law prohibits me from providing you with certain information about neighborhoods, such as demographics, crime rates, child-friendliness, etc. But you can find a wealth of information online and at your local library, including census data, local schools information, and police records to help you decide where to focus your home search.

HOW WE’LL STAY CONNECTED

Effective communication is imperative for ensuring a smooth and successful process from start to finish. From day one, we’ll establish a clear communication schedule that keeps you fully informed about every aspect of our work together, from major milestones to the smallest details. This structured approach ensures you’re never left wondering about progress, next steps, or important updates, allowing you to stay focused on achieving your goals with complete confidence and clarity.

The best way that you can help is to tell me any time you have questions or concerns, no matter how small. Informed clients make the best decisions, and I’m here to help you do just that. If your needs or timeline ever change in the course of your home search, please let me know right away so we can pivot as needed.

It’s also important for us to keep in close touch about properties you’re interested in and homes you tour. I have tools designed to make that easy and convenient, like my personalized Search app, but I always tailor my communication methods to your preferences.

Loan preapproval

Before you start house-hunting, you need to get preapproved for a loan so you know your budget and sellers will know that you’re prepared to make a serious offer. I can refer you to a mortgage consultant I trust who can help you determine how much you can afford for a down payment and monthly payment, and discuss which type of loan is right for you.

There are several factors that lenders assess when determining your eligibility for financing, including:

❱ Income

❱ How much monthly income goes toward debt (debt-to-income ratio or DTI)

❱ Employment status

❱ Assets

❱ Credit score and history

Prior to your mortgage consultation, be sure to get your finances in order and review your credit score and history to address any issues. Your mortgage consultant will let you know what documentation they will need from you, which may include recent bank statements, pay stubs, W-2 forms, and tax returns.

MISTAKES TO AVOID AFTER PREAPPROVAL

Being preapproved doesn’t guarantee funding. The following can jeopardize your financing even after preapproval:

1. Large cash or credit purchases

2. Quitting or changing jobs

3. Unpaid bills or late payments

4. Opening new credit cards or bank accounts, or co-signing a loan

5. Paying off significant loans or debt

6. Making large deposits

Always consult with your lender before making any significant financial decisions or changes during your home search.

The search

I will create a list of homes matching your criteria that we can tour together, and I’ll keep sending you new listings and checking in with you regularly throughout your home search. When we find a home that interests you, I’ll answer your questions and research the home more if needed.

I subscribe to the Multiple Listing Service and tour new listings in our area every week. Please send me any listings you may find and give me feedback on any homes you view on your own. I recommend that you take notes about the pros and cons of each home you view, as it can become difficult to remember after seeing several listings. We can also use my personalized Search app to communicate and share listings and notes, and you can create a saved search on Windermere.com to be notified automatically anytime a new listing that meets your criteria comes to market.

LOOK BEYOND APPEARANCE

When viewing homes, try not to judge them based on appearance and features you can easily change later. Homes in need of cosmetic updates are often more affordable than ones that are fully updated, and making those changes yourself (or with the help of a hired professional) can be more cost-effective and suit your needs better in the long run. The most important goals are to make sure the home is in good physical condition and to determine the ballpark costs of any repairs and upgrades that are needed.

WINDERMERE REAL ESTATE

Offer & negotiation

When you’re ready to make an offer on a home, we’ll strategize to determine the best offer price by reviewing similar homes and market data in the area. We’ll also discuss your preferred timing, any appliances and other items in the home that you want included in the sale, your preferred method of and availability for signing documents, contingencies, and more. Then we’ll create a purchase and sale agreement outlining the details of your offer, which I’ll send to the seller’s agent. The seller can either accept it, reject it, or make a counteroffer. I will negotiate with the seller on your behalf to get you the home you want with the best terms possible, including, if you so desire, requesting that the seller pay buyer agency fees or provide other concessions.

Earnest money

Earnest money is a “good faith” deposit that you typically submit around the time you make an offer on a home to show that you are seriously interested. Although there’s no rule specifying how much earnest money you should put down, the amount can sometimes make a difference in the negotiation process.

Earnest money eventually goes toward your down payment or closing costs, or it gets returned to you if contractual contingencies are not met.

HOME WARRANTY

Homeowners insurance typically covers damage to or loss of your home and its contents from sudden, unexpected events like fires or break-ins, but not problems resulting from normal wear and tear.

For that, you may consider purchasing a home warranty, which is an annual service plan that can provide peace of mind by covering repairs and replacements of your home’s major systems and appliances. But home warranties differ and don’t always cover regular maintenance or conditions that existed before you bought the home. If you’d like to learn more, I’ll recommend a reputable home warranty company to discuss your options.

Contingencies

A contingency is a condition that must be removed before a contract can be enforced. During the contingency period, the buyer can typically renegotiate or exit the deal with their earnest money if they discover information about the property that is unacceptable or they cannot in good faith fulfill another contingency. Contingencies protect the buyer but can also make an offer look weaker in the eyes of sellers, so I’ll help you strategize based on the current market’s intensity. Common contingencies include:

❱ Appraisal contingency: the buyer can back out if the property is appraised at an amount lower than they’ve specified.

❱ Inspection contingency: the buyer is allowed to get a professional inspection of the property, and if problems are found that the seller is unwilling to repair or negotiate about, the buyer can walk away.

❱ Financing/Mortgage contingency: gives the buyer the right to back out of the deal if they are unable after reasonable efforts to secure a mortgage on the property within a specified timeframe.

Offer acceptance

When your offer is accepted and both parties have signed the agreement, I’ll provide a detailed summary of the timing, tasks, and deadlines you’ll need to meet. Then I’ll coordinate with you through each step to make sure all goes smoothly and on time.

Financing

After your offer is accepted, the next step is to get final loan approval. During this process, your lender will decide if they’re willing to approve your mortgage based on your creditworthiness, the home’s appraisal, its title history, and other factors. A title company will provide a title report for you and your lender detailing the history of the home and ensuring that there are no legal barriers to purchasing it.

Insurance

After completing a title report on the property, the title company will provide a quote for title insurance based on the findings of the report. Title insurance protects both the buyer and lender against any legal disputes and liens on the property that the title search may not have found or resolved, and lenders require title insurance before issuing a mortgage. This one-time charge protects you and the lender from unknown issues that may have already happened.

Lenders also require homeowners insurance before they will finance a property to protect you and the lender from what might happen to the home in the future. If you’d like to learn more, I am happy to make recommendations.

Inspection

When making an offer on a home, I may recommend making it contingent on a professional inspection to assess the home’s condition. Not only does this inform you of any needed repairs, which we may want to negotiate with the seller about, but it also helps you understand the home’s systems and ongoing maintenance needs. Depending on the property, I may advise getting additional inspections like sewer, well, or septic, and can recommend local inspectors I know and trust to do thorough work.

Escrow

When the seller accepts your offer, that’s our cue to begin the escrow process. Escrow is a legal arrangement for temporarily holding the funds in a real estate transaction and making sure they are distributed properly when the deal goes through. The funds, property, and documents are held by a neutral third party “in escrow” until the terms of the agreement have been filled. You’ll meet with the escrow agent to sign the final documents a few days before closing.

!WAIVING INSPECTION

In a highly competitive market, buyers sometimes opt to waive a home inspection contingency in order to make their offer stronger in the eyes of the seller. If you consider this option, for your own protection, you should still reserve the right to conduct an inspection for the purposes of gathering information. You may also consider a limited inspection contingency, such as only for major issues like mold or a faulty foundation, or one that waives repairs of less than $1,000.

Closing

The closing process finalizes the terms of the agreement, leading to the transfer of the property’s title (and keys!). This comes with its own set of costs. I can help you understand what fees each party will pay and receive, and your escrow agent will coordinate with you to schedule the signing appointment and provide instructions for payment of the final funds due for closing. They will then deliver the funds and signed loan documents to the lender, and transfer the title and keys to you when the lender releases the funds to the seller and documents are recorded with the county.

THE BUYER RECEIVES

❱ Credit toward buyer closing costs or the purchase price for any earnest money deposited

EXAMPLES OF WHAT A BUYER MIGHT PAY

❱ One-half of escrow or legal fees paid to the attorney or escrow company for preparing the closing (In California, the party paying escrow fees varies from county to county)

❱ Document preparation fees, if applicable

❱ Recording and notary fees, if applicable

❱ Title search and title insurance*

❱ Local transfer taxes*

❱ Loan fees

❱ Appraisal fees

❱ Credit report fees

❱ Home Owners Association fees, if applicable*

*Paid by either the seller or the buyer

Ongoing support

My service doesn’t end when you get your keys. I can connect you with local service providers, community resources, and more. I will also stay in touch in the years to come to provide helpful home information and be of service any time you have questions about real estate or our area. Regardless of your need, I’ll be ready to help.

SIX TO EIGHT WEEKS BEFORE

Use up things that may be difficult to move, such as frozen food.

Get estimates from professional movers or truck rental companies if you’re moving yourself.

Once you’ve selected a mover, discuss insurance, packing, loading and delivery, and the claims procedure.

Sort through your possessions. Decide what you want to keep, sell, and donate to charity.

Record serial numbers on electronic equipment, take photos (or video) of all your belongings and create an inventory list.

Change your utilities, including phone, power, and water, from your old address to your new address.

Fill out a change-of-address form with the postal service and update your address with creditors and other relevant parties.

Discuss tax-deductible moving expenses with your accountant and begin keeping accurate records.