Each year, VISIT DENVER compiles this Marke�ng Plan, which contains a thorough study of industry informa�on, customer feedback and consumer sen�ment, as well as a situa�on analysis of local, na�onal and interna�onal trends. Together, this informa�on helps guide VISIT DENVER in developing its 2024 strategies and tac�cs.

THE STATE OF DENVER’S TRAVEL INDUSTRY

Denver’s travel industry is back. It has been several years since such an unequivocal statement could be made about it.

Prior to 2023, growth had been strong but inconsistent, and a myriad of headwinds limited poten�al, everything from lingering concerns about COVID to drama�c increases in travel prices. While there are s�ll several meaningful issues to face, a combina�on of record-breaking 2022 travel results from our partners at Longwoods Interna�onal; favorable industry studies from domes�c and global research partners; and strong internal sales and marke�ng indicators all combine to allow this organiza�on to feel a brisk wind at its back for the first �me in more than three years.

The 2023 version of this report stated that, “There is no new normal.” VISIT DENVER came to that conclusion based on the available informa�on at the �me, no�ng a period of tremendous opportuni�es that were paired with new and rapidly evolving challenges related not only to the pandemic, but also to vola�lity in the global economy, poli�cal upheavals, social jus�ce, changing travel habits and more.

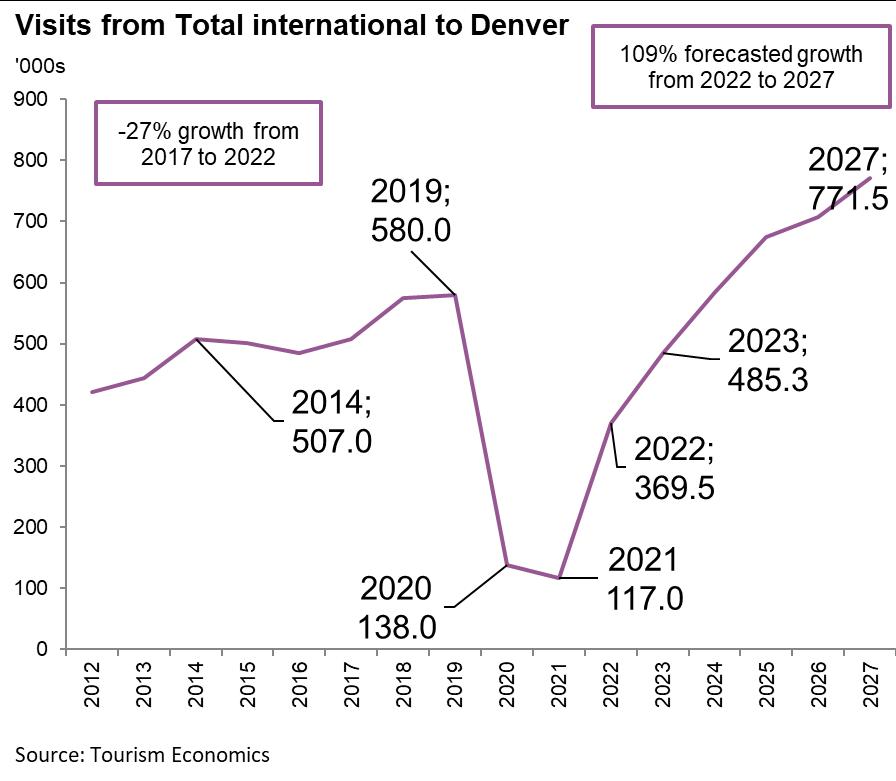

Today, there has been tremendous stabilization across nearly all key sectors that impact the global travel business. Travel demand, particularly from domestic leisure audiences, continues to grow despite continued concerns about travel prices and the looming threat of a recession. Demand in the group market continues to outpace earlier projections, with VISIT DENVER achieving lead volumes that exceed the organization’s 2019 high water mark. The international market has also surged back, particularly from North American and European destinations as all international flights have been restored with more on the way.

In response to these opportunities, VISIT DENVER continues to develop and execute comprehensive sales and marketing strategies that takes advantage of this renewed demand, while also ensuring the organization leans in, and does not put its guard down nor rest on its past successes.

There are innumerable reasons for doing so: Travel remains a highly competitive global business, with domestic visitors experiencing increased demand for international trips, and domestic destinations also putting out savvy marketing messages. The recovery in the meetings market brings with it new demand dynamics that have upended decades of booking patterns. While international demand is rising, few countries have yet to reach their 2019 travel levels.

And the global airline industry continues to wrestle with service and staffing issues that can leave travelers feeling frustrated.

Here in Denver, the travel product itself continues to evolve. Persistent crime and safety issues continue to impact the downtown area in particular, though significant progress has been made. Certain sectors of the industry, such as restaurants, continue to struggle with high food and labor prices and workforce issues, causing many closures. Hotels, which have enjoyed high rates during the peak of the inflationary period, have not yet seen their occupancy return to 2019 levels, primarily due to softness in the transient business market.

Despite these headwinds, and with a new City administration in place, VISIT DENVER’s outlook for 2024 is stronger than it has been in years. The organization retains a commitment to work through all challenges, known and unknown, with the same diligence and professionalism that has marked its stewardship of Denver’s travel industry for 114 years

NATIONAL PERSPECTIVES

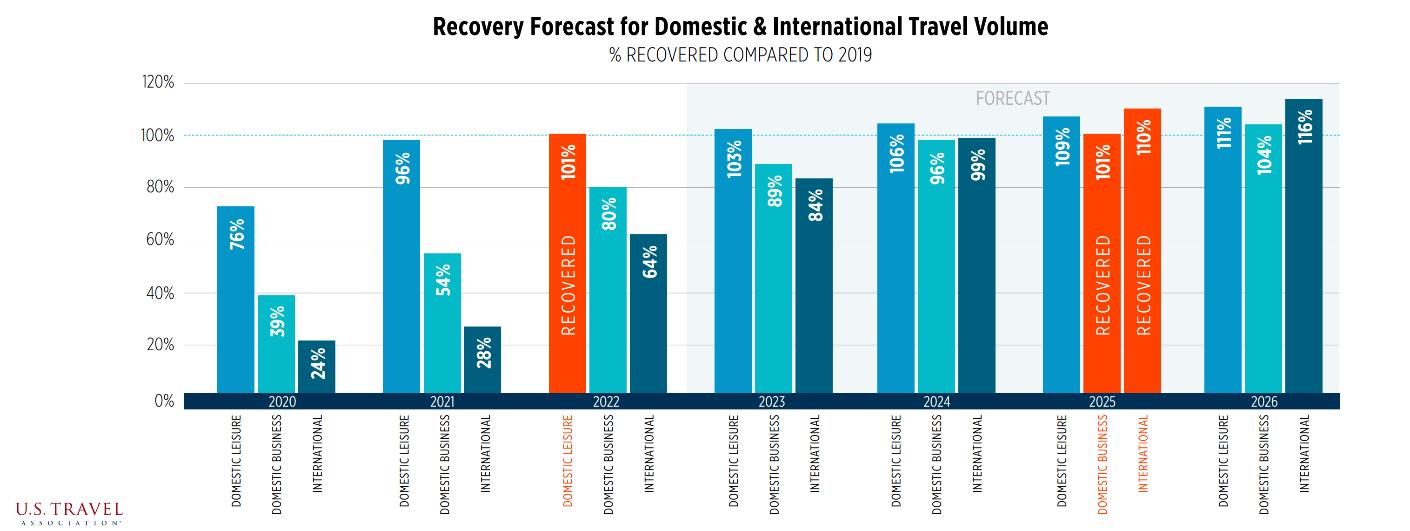

U.S. Travel Forecast for 2023 & Beyond

The U.S. Travel Association (USTA) shows an optimistic outlook for 2023 and beyond in their U.S. Travel Forecast, Summer 2023 edition, with the latest figures available. As they have in past versions of this report, USTA offers their forecast in both a nominal and inflation-adjusted manner to give the industry a truer picture of recovery.

Here are their primary takeaways for 2023 and beyond:

Overall market:

A return to more “normalized” growth of around 2 percent for domestic leisure travel, which will remain resilient despite some headwinds

Rapid 2023 growth in domestic business travel, with a slight slowdown toward the end of the year and into 2024 due to a still-expected mild recession. A full recovery in terms of volume has been pushed to 2025 and inflation-adjusted spending recovery remains beyond the range of the forecast

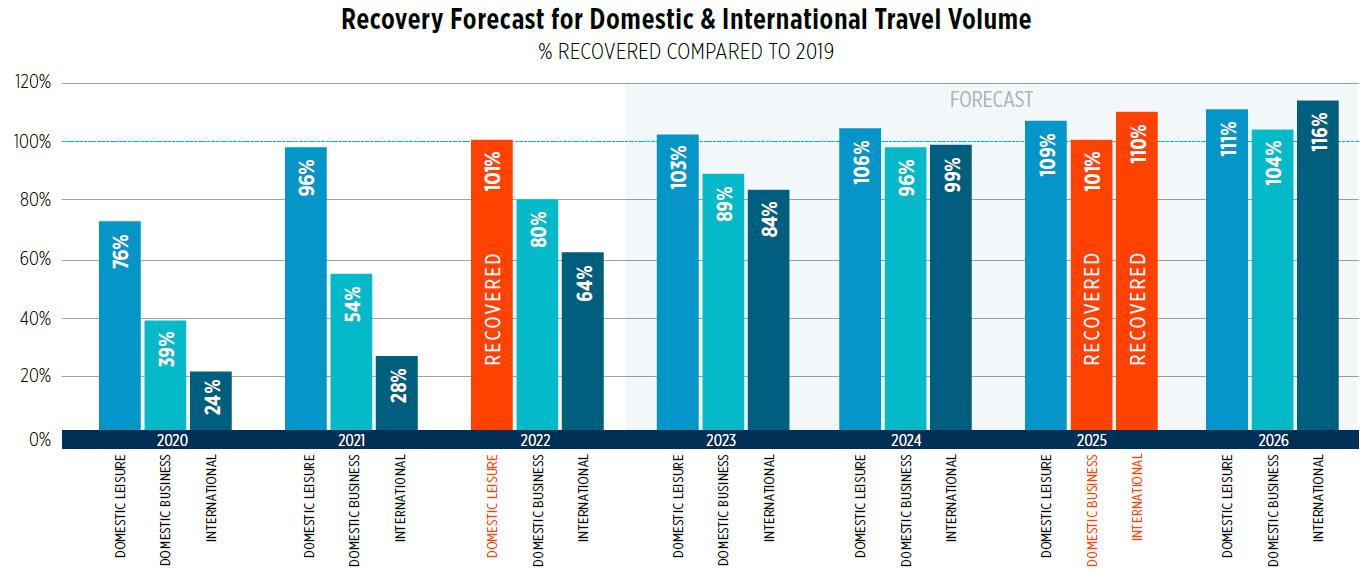

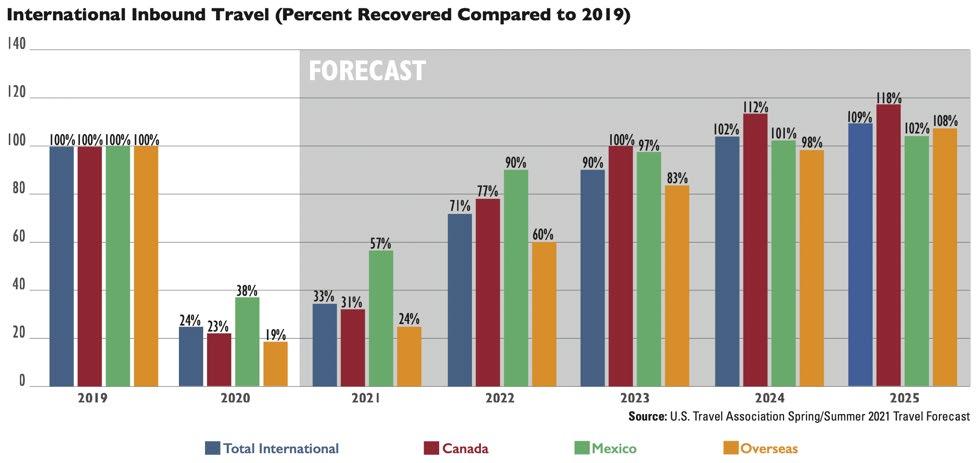

A boost in international visitation. While still far behind, international inbound travel is expected to experience the strongest growth of any segment throughout the range of the forecast, nearing full recovery in 2024 and exceeding it in 2025

Travel volume:

Domestic leisure trips recovered in 2022, and are expected to return to more “normalized” rates of growth in 2023 and beyond

Business travel trips are projected to recover in 2025

International visitations are projected to recover in 2024 or 2025

Source: U.S. Travel Association’s U.S. Travel Forecast Summer 2023

Travel spending:

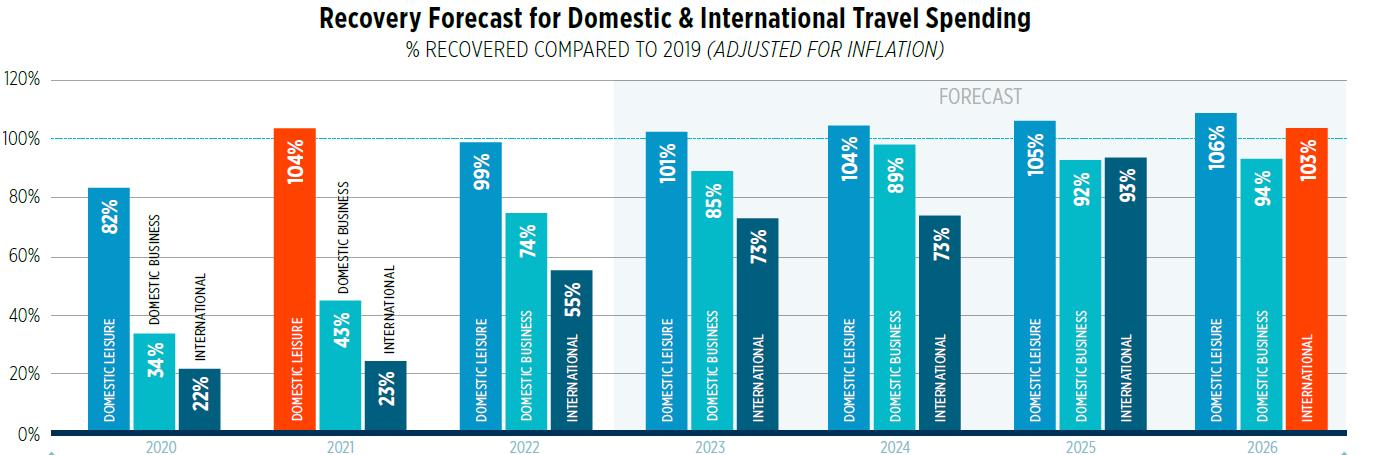

Domestic leisure travel spending recovered in 2021 (though it somewhat regressed in 2022); It is expected to grow more modestly in 2023 and beyond

Business travel spending when adjusted for inflation, is not projected to recover within the range of the forecast, so not before 2027 or even 2028

International visitations are projected to recover only in 2026

U.S.

Economic downturn:

A mild recession is expected in the second half of 2023:

o Although the economy dodged a recession and continued to grow during the first part of the year, thanks to strong consumer spending and a solid jobs market, the risks of a downturn later this year remain significant

o Elevated inflation and interest rates are expected to constrain consumer spending, business hiring and investment in the second half of the year

o Nevertheless, GDP growth for the year is projected to remain positive at 1.3 percent, followed by just 0.4 percent growth in 2024

Source:

Travel Association’s U.S. Travel Forecast Summer 2023

Economic indicators:

MONETARY POLICY: The Fed raised rates by 25 points in May and July, after holding them in June, and policymakers stressed they will resume hiking if inflation proves to be stickier than expected. The Fed is expected to keep interest rates steady for the rest of this year before cutting them in early 2024.

LABOR MARKET: Job growth was strong in April, May and June, countering other signs that the labor market lost some steam. But job gains are expected to ease through the rest of Q2 and payrolls will decline as tight lending standards and the impact of cumulative Fed rate hikes weigh on labor demand and the broader economy.

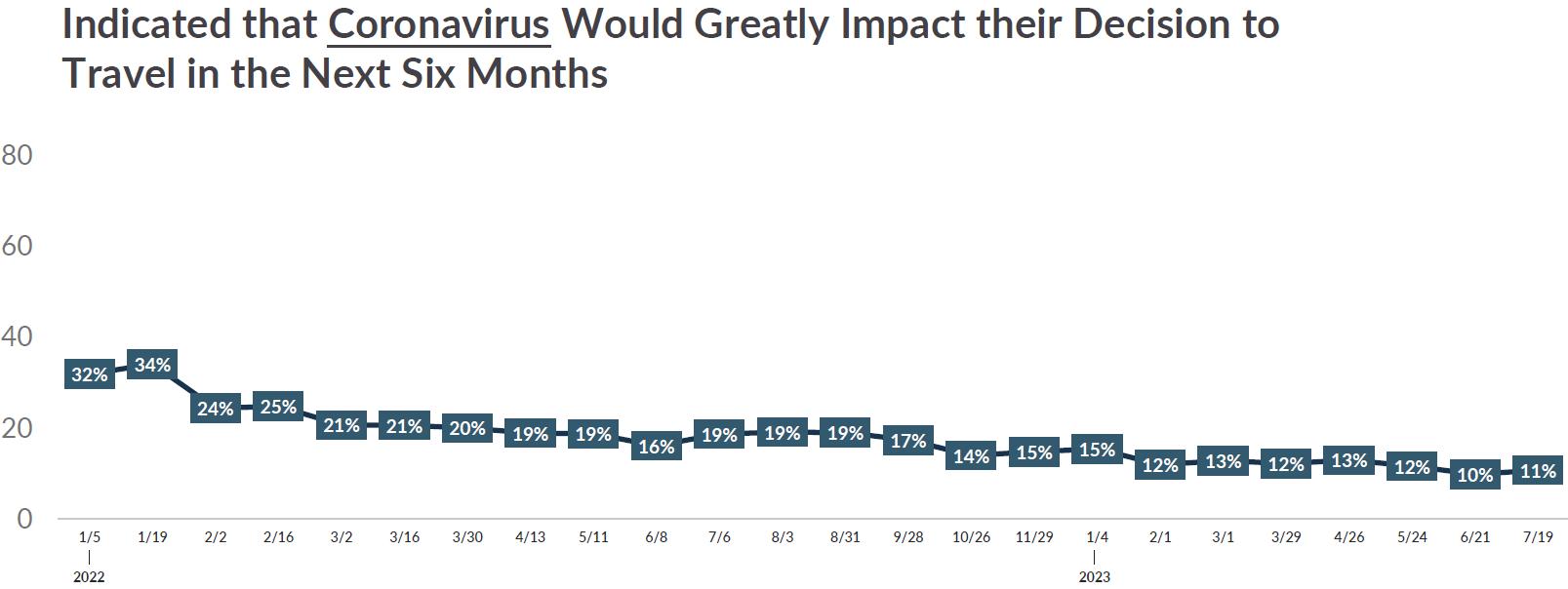

INFLATION: Inflation is expected to soften but remain high through the rest of 2023. The Consumer Price Index is expected to grow by 4.4 percent this year, well above the Fed’s 2 percent inflation target. Travel prices are expected to rise only 0.9 percent in 2023, primarily due to falling motor fuel prices. Inflation Consumer as well as Travel is expected to normalize after 2023.

CONSUMER SPENDING: While consumer spending remained strong through Q1 and into Q2, it will come under pressure due to an expected weakening in job and wage growth. Also, low- and middle-income households have exhausted most of their excess savings.

Source: U.S. Travel Association Travel Forecast, Summer 2023

DENVER’S TRAVEL INDUSTRY

2022 Longwoods Visitor Study

VISIT DENVER has many ways to measure the impact of the travel industry on the city, but none are so eagerly anticipated as the Annual Visitor Profile from Longwoods International. Longwoods surveys domestic visitors 12 months a year and produces for its clients an annual report on visitation, spending, visitor demographics and more. Their methodology is the industry standard for this kind of study, with a high degree of confidence and low margin of error. Longwoods has been researching the Denver visitor market since 1994.

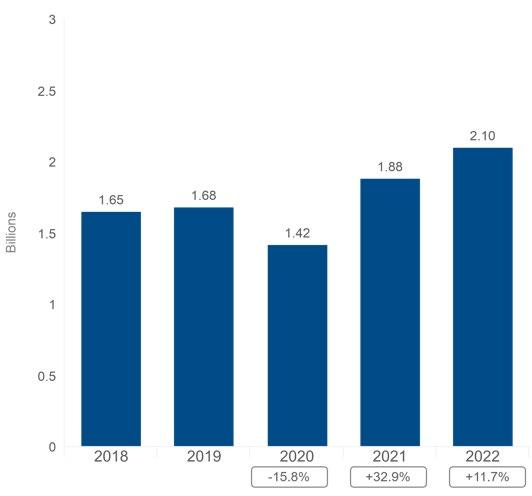

In 2022, the latest figures available, Denver welcomed a record 36.3 million visitors, marking a 15 percent increase over 2021 and surpassing all historic tourism totals by a large margin. A record number of visitors also spent more money in Denver than ever before, generating $9.4 billion in tourism revenue, far beyond the previous record of $7 billion spent in 2019.

Overnight visitors totaled nearly 20 million, a 20 percent rise over the prior year. Growth was particularly strong in the domestic overnight leisure market, which rose by 13 percent over the prior year to a new high of 16.7 million visitors.

Longwoods also studies the impacts of VISIT DENVER’s efforts to target “marketable” visitors, the primary focus of the organization’s promotional efforts. In 2022, these marketable visitors increased by 18 percent over 2021 surpassing eight million for the first time.

Spending by overnight visitors increased in 2022 to $8 billion, a 45 percent increase over 2021. Among all traveler types, marketable leisure visitors spent the most at $229 per day followed by business travelers at $152 per day.

Longwoods International also conducted Return on Investment (ROI) research for VISIT DENVER’s largest advertising campaign of the year, the 2022 summer advertising campaign. The study revealed the strongest ROI numbers VISIT DENVER has ever seen, showing that the campaign generated 1.8 million incremental trips, generating $641 million in incremental visitor spending and $72 million in state and local taxes. Measured against spending, the campaign generated an ROI of $167 in visitor spending and $19 in taxes for every $1 in advertising investment.

Key numbers for 2022 include:

Denver welcomed 36.3 million total visitors in 2022, including 19.9 million overnight visitors and 16.4 million day visitors.

Overnight leisure visitors totaled 16.7 million in 2022, a 13 percent increase over 2021.

There were 8.3 million “marketable” leisure visitors in 2022, an 18 percent increase over 2021. This segment has the most discretion on where to vacation and responds to tourism marketing. This audience is the primary focus of much of VISIT DENVER’s marketing efforts and spends more time and money in-market than any other leisure visitor type.

Denver visitors spent $9.4 billion in 2022, including $8 billion from overnight visitors and an additional $1.4 billion in spending from day visitors. Total spending increased by 42.5 percent over 2021.

Denver overnight visitors spent nearly $2.3 billion on accommodations, and $1.3 billion on food and beverages.

Expenditures by overnight visitors on transportation reached nearly $2.7 billion. Retail purchases were $969 million, while overnight visitors spent nearly $685 million on paid attractions and other recreational and sightseeing activities.

On average in 2022, the biggest spenders were marketable travelers, who spent $229 per day, followed by business visitors, who spent $152 per day. Day visitors spent $88 per day.

Out-of-state overnight leisure travelers comprised 76 percent of visitors.

The top five states sending vacationers to Denver in 2022, apart from Colorado itself, were:

o California

o Texas

o Arizona

o Florida

o Kansas

The top five cities from outside of Colorado sending leisure visitors to Denver in 2022 were:

o Los Angeles, CA*

o Phoenix, AZ*

o Dallas-Ft. Worth, TX*

o Chicago, IL*

o New York City, NY*

*Denotes VISIT DENVER advertising market

DENVER 2022 PRODUCT UPDATE

The following sec�on documents the current state of Denver’s tourism product. It is always important to document the strengths and weaknesses of the city’s infrastructure, since it is an area over which VISIT DENVER has litle control. As is said around the organiza�on on a regular basis, “we own nothing,” meaning that once the sales and marke�ng efforts do their job, it’s up to the business owners to close the deal.

Denver Tourism Roadmap Update

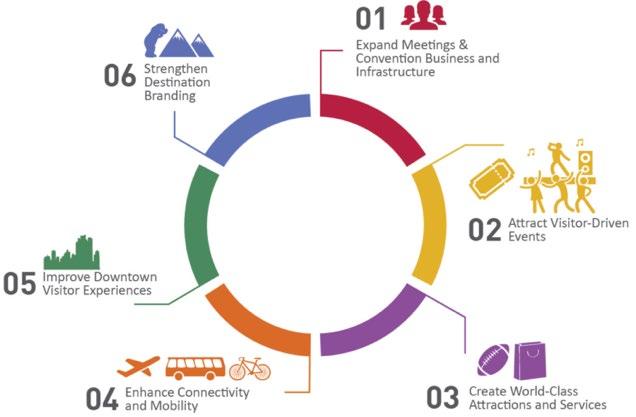

VISIT DENVER’s focus on the Denver Tourism Roadmap, a long-term destination strategic plan, continues to guide the organization and its goals. Despite the pandemic-related disruption to this Roadmap over the last three years, the six goals remain the same. There will also be an opportunity to update the Roadmap with the board and with the new City administration in 2024.

Tourism Improvement District (TID)

The TID was formed in 2017, with the help of the Colorado Hotel & Lodging Associa�on (CHLA), to make sure that Denver had the marke�ng funds available to grow the tourism and conven�on business well into the future. As part of its forma�on, the TID also dedicates funds annually to the City for the expansion of the Colorado Conven�on Center (CCC), and the remaining funds then flow to VISIT DENVER for sales and marke�ng efforts. Past efforts using the TID tax revenue include programs such as the annual Mile High Holidays campaign and the

opera�ons of the Mile High Tree as well as the MLB All-Star Game fes�vi�es. Both programs helped drive overnight business to Denver.

In 2023 the TID remained commited to key strategic areas and its mission of increasing overnight demand by conven�on and mee�ng visitors, as well as leisure visitors to Denver, especially in our low- and off-peak seasons like major holidays and weekends. Specific programs include funding a holiday season marke�ng campaign highligh�ng the Mile High Tree, client concessions to atract mee�ngs and conven�ons in future years, and regional leisure marke�ng.

The TID con�nues to serve a significant role in helping Denver remain compe��ve when atrac�ng conven�ons. While compe�ng ci�es offer conven�on center discounts and financial incen�ves to book citywide business, the TID program has helped atract cri�cal business with a robust economic impact. Addi�onally, there has been increased compe��on from mega-hotels (facili�es so large that the en�re mee�ng can be held in one hotel, elimina�ng the need for a conven�on center), compe�ng for conven�on center business. Since the TID’s crea�on, VISIT DENVER has booked 35 groups with a $539 million economic impact, and $43 million in tax dollars. In 2023, VISIT DENVER has booked nine groups through TID incen�ves, worth $139.4 million in future economic impact which would result in nearly $11.2 million in tax dollars for our city.

Transporta�on & Accessibility

Located almost exactly 1,000 miles from both Chicago and San Francisco, Denver is the most isolated city in North America, 600 miles from the closest city of comparable size and surrounded by minimally populated areas of prairie to the north, east and south, and mountains to the west.

Denver Interna�onal Airport

Denver’s success in the 21st century, both in the leisure and mee�ngs markets, relies heavily on its accessibility, and primarily on the strength of Denver Interna�onal Airport (DEN) to provide convenient air service, and ground transporta�on from the airport to a compact, walkable downtown. DEN is Colorado’s largest economic engine, bringing in $33 billion annually.

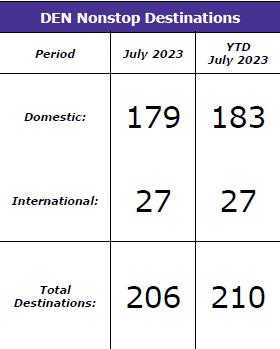

Based on the strength of its domes�c network, DEN outperformed nearly every other airport in the country during and a�er the pandemic on a host of measures. In terms of passenger counts, DEN is the third busiest in the country and seventh busiest in the world (Source: DEN, July 2023 Air Service Profile). In 2022, DEN had 69.3 million passengers, surpassing the previous record set in 2019. Year-to-date in 2023, passenger traffic is up 13.2 percent versus 2019. July 2023 is scheduled to be DEN’s busiest month ever in terms of interna�onal flights and capacity. Compared to July 2019, DEN airlines will offer 10.5 percent more interna�onal flights and 31.9 percent addi�onal capacity.

DEN is also planning for future growth. Vision 100, the airport’s strategic plan, will enable it to prepare for and reach 100 million annual passengers. The strategic plan will serve as a blueprint to align decision-making and enable accountability so DEN can though�ully prepare to serve

100 million passengers in the next 8-10 years. DEN’s strategic plan is centered on the four pillars of Vision 100 and under each pillar are strategic objec�ves:

Powering our people

Growing our infrastructure

Maintaining what we have

Expanding our global connections

The Regional Transporta�on District (RTD) and 16th Street Mall RTD services a population of 3.08 million in a services area of 2,342 square miles and 143 regular fixed routes. With 9,750 average daily active bus stops, RTD maintains the largest fleet of electric buses in the nation (26) to service the 16th Street Mall, and as of 2020, these electric buses had traveled more than 1.2 million miles carrying passengers throughout downtown.

During July and August 2023, RTD offered zero fares across its system as part of the Zero Fare for Better Air initiative. This collaborative, statewide initiative, made possible by Colorado Senate Bill 22-180, in partnership with the Colorado Energy Office, is designed to reduce ground-level ozone by increasing the use of public transit. Current RTD customers also benefitted as they did not have to use or purchase fare products from July 1 – August 31, 2023, during Colorado’s high ozone season.

Built in 1982, the 40-year-old 16th Street Mall is currently undergoing a major restoration. The project will reconfigure the Mall’s layout to create wider sidewalks, a new amenity zone and center-running Free Mall Ride shuttle service. Phased construction began in 2022, starting at Market Street and moving towards Broadway before reaching completion in late 2024.

I-70 Project

Central I-70, between I-25 and Chambers Road, is one of Colorado's economic backbones. It is home to 1,200 businesses, provides the regional connection to DEN and carries upwards of 200,000 vehicles per day. The highway is essential to tourism traffic, both from the airport to downtown and through Colorado from the east to the mountain resorts in the west.

The Central I-70 Project, which was completed as of July 2023, reconstructed a 10-mile stretch of I-70 between Brighton Boulevard and Chambers Road, adding one new Express Lane in each direction, removing the aging 57-year-old viaduct, lowering the interstate between Brighton and Colorado Boulevards, and placing a four-acre park over a portion of the lowered interstate. Tolling of the Express Lanes began on July 11, 2023.

Colorado Conven�on Center Expansion

The expansion of the Colorado Conven�on Center (CCC) remains on track. Voters approved the project in 2015, and in July 2020, the City of Denver selected Hensel Phelps and TVS Design as the design/build team for the project. City Council approved the contract in fall 2020. Construc�on started in June 2021, and a "Raise the Roof" kick-off ceremony and press

conference took place in September 2021. The expansion will be completed by December 2023.

VISIT DENVER has worked closely with ASM Global, Denver Office of Transporta�on and Infrastructure (DOTI) and the contracted team to minimize the impact on exis�ng business, while also con�nuing to book new business during construc�on. Both VISIT DENVER and ASM Global are focused on driving new business to the expansion space beginning April 2024.

Key features of the expansion include:

Multi-function Bluebird Ballroom Space

o The signature feature of the expansion is an 80,000-square-foot, column-free multifunction space that includes 19 subdivisions of varying sizes.

Pre-function Concourse

o The new 35,000 square feet wrap-around, pre-function concourse, which features dramatic views of the Rocky Mountains and is conveniently accessible via the center’s existing street-level lobbies.

Rooftop Terrace

o The 20,000 square-foot rooftop terrace features spectacular views of the Rocky Mountains to the north and west and stunning views of Denver’s skyline to the east.

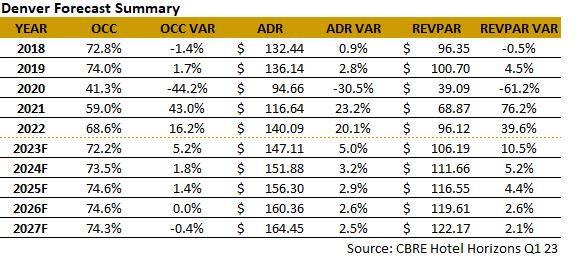

Hotels

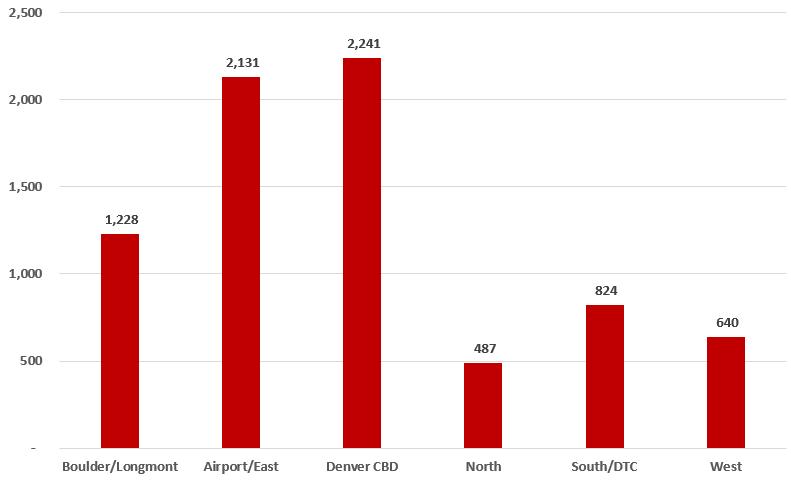

Supply con�nued to grow in Denver even during the pandemic but is leveling off as of August 2023. According to CoStar Group, pipeline proper�es are concentrated in the CBD and East/DEN areas of the Denver metro area.

Pipeline Proper�es Concentrated in Downtown & Airport

1,000 1,500 2,000 2,500

Source: CoStar 2023

There are already more than 12,500 downtown hotel rooms within walking distance of the conven�on center and nearly 52,000 rooms in the metro area, with more on the way. According to CoStar, as of August 2023 there are 2,673 rooms under construc�on and an addi�onal 4,878 rooms in final planning across all Denver submarkets.

In 2022, many downtown Denver hotels celebrated openings, as well as multi-million-dollar

renovations. Here is a shortlist:

Originally set to open in 2021, the Thompson Denver by Hyatt opened in early 2022. Located in the heart of LoDo, the hotel also includes Chez Maggy by Michelin-starred chef Ludo Lefebvre.

The much an�cipated Slate Hotel opened in May 2022 at the historic site of the original Emily Griffith Opportunity School across the street from the Colorado Conven�on Center and many other iconic Mile High atrac�ons. This hotel adds 251 guest rooms to downtown Denver.

In August 2022, Denver’s trendy RiNo Art District welcomed the 140-room Vīb by Best Western Hotels & Resorts. Its ameni�es include mee�ng and event space and an enclosed roo�op bar taking advantage of the views of the Rocky Mountains and Denver’s skyline.

2023 had fewer hotels open:

The Cambria Hotel Denver Downtown, a new 153-room hotel, opened in RiNo in September 2023.

Offering only 18 rooms, the Urban Cowboy Denver will bring a unique new experience to Uptown in late 2023.

And there are more hotels in the works in Denver:

Populus, the 250-room hotel planned adjacent to Civic Center Park, will feature a roof-top terrace. The property will be the first carbon positive hotel in the country and is scheduled to open in spring 2024.

Courtyard by Marriott Denver Stadium will add 118 rooms near Empower Field at Mile High in March 2024.

The Sonder Jefferson Park, a 93-room hotel, will open in December 2024.

The World Trade Center complex in Globeville includes plans for a 240-room hotel. Opening date TBD.

Train Denver Bou�que Hotel is coming to Denver’s RiNo Art District. The opening date is TBD.

Restaurants

Denver’s restaurants have always been a key pillar in the city’s reputa�on as a sophis�cated urban des�na�on. Discerning travelers choose des�na�ons in part due to the strength of a city’s culinary offerings. Similarly, they may avoid des�na�ons they don’t feel can provide them with the fresh, crea�ve and adventurous dining op�ons they crave.

This was a vola�le industry even before the pandemic, with razor-thin margins and persistent staffing challenges. COVID then unleashed upon restaurants nothing short of an existen�al crisis as public gathering places became highly restricted, and their in-person workforce went through several cycles of staff reduc�ons and re-hirings.

Add to these challenges the steep rise in food costs that began in early 2022, which persists today, as well as high labor costs due to a �ght job market and Denver’s high minimum wage, and the restaurants must feel they are in the perfect storm.

On the posi�ve side, the introduc�on of a new Colorado program from Michelin, the global leader in restaurant reviews, will significantly raise the profile of the Colorado dining scene in general and Denver in par�cular.

Atrac�ons, Cultural & Mee�ng Facili�es

A�er the devasta�ng effects of the pandemic – the city’s crea�ve community lost nearly 30,000 jobs and more than $1.4 billion in revenue between April 1 and July 31, 2020 – this vital and cri�cal sector of Denver’s tourism product has roared back to life. The author of the previous study, Colorado Business Commitee for the Arts, has not published its follow up, but there is significant evidence of the sector’s rebound.

According to Denver Center for the Performing Arts, in their 2021/2022 Community Report, their programs had the following impact and results:

More than $203 million total economic impact

More than 605,000 tickets distributed

More than 700,000 total guest interactions

World premiere of “Theater of the Mind, ” an immersive production co-created by Talking Heads frontman David Byrne and artist writer Mala Gaonkar

Addi�onally, according to Denver Arts & Venues, the City had a significant impact on residents across the city, including:

More than 1,000 hosted cultural events

2.7 million attendees

350 artists and organizations receiving funding

More than 80 active public art projects

All of this speaks to a city that values culture as one of its defining principles, a quality that is highly visible to visitors who seek to enrich their lives through culture on their visit.

Some other significant cultural developments in the city include:

DENVER WALLS, a major street art festival in the RiNo neighborhood from September 22 –October 2, 2023. DENVER WALLS is tied to the global World Wide Walls event, which joins cities across the globe to beautify and connect local artists with their communities.

The strong return of Denver’s major cultural festivals such as March Powwow, Cinco De Mayo, Juneteenth, PrideFest, Cherry Creeks Arts Festival, Colorado Black Arts Festival and many others. Such a robust festival calendar offers locals and visitors alike multiple opportunities throughout the year to connect with the city’s diverse communities and artists.

The reopening of Denver Art Museum’s Hamilton Building Collection Galleries in May 2023, which included the Arts of Africa, Modern and Contemporary Art and Arts of Oceania galleries.

Sports

The year of 2023 in the sports world was welcomed by most rights holders, a�er a tough three years that seemed like decades in the making. According to Mat Swenson of Connect Sports, “Predic�ng the future is unknown, but it appears safe to say the worst of the pandemic is over. Arenas and stadiums across the country are full again. Generally speaking, Americans are back to many of their old rou�nes. The expecta�on is 2023 will be the closest to the ways things were, albeit with a few twists.”

“We have seen an upward trend in event par�cipa�on for our sport by around 10 percent to 20 percent,” reports Connor Shane, director of na�onal events at USA Racquetball. “Our regional events are coming back online in full force this year a�er almost three years of seeing obstacles from COVID-19.”

Denver was honored to host several events in 2023 that are keeping The Mile High City in the spotlight. Na�onal championships with USA Curling and USA Fencing brought �tle-chasing hopefuls to Denver, while the NCAA once again staged sold-out opening rounds of March Madness at Ball Arena.

This past year also brought another championship to the Kroenke Sports family and a first �tle to long-suffering Denver Nuggets fans everywhere. A�er a 47-year wait, the Denver Nuggets topped the Miami Heat for the NBA World Championship this past June. For the future of spor�ng event recrui�ng, the future looks bright, and the Denver Sports Commission will con�nue to move ahead with evalua�on of all levels of sports tourism.

Fes�vals & Events

2023 continued the trend of in-person events that started in 2022. Denver PrideFest received 550,000 visitors with another record-breaking attendance. Cherry Creek Arts Festival received 150,000 visitors and more than 225 artists, while Denver Day of Rock took place on June 3rd this year (one week later than in 2022). Taste of Colorado was modified this year with the newly created Taste of Colorado at ¡Viva! Streets Denver, across four Sundays throughout the summer, and served as Denver’s first-ever large-scale Ciclovía. The Denver Center for the Performing Arts returned to a full schedule in 2022, which continued in 2023. Red Rocks Amphitheatre maintained its full schedule of events, including Yoga on the Rocks and Film on the Rocks.

Sustainability

Denver’s Office of Climate Ac�on, Sustainability and Resiliency has led the way in decreasing the city’s greenhouse gas emissions and priori�zing a sustainable future for the city. Likewise, VISIT DENVER collaborates with our venues, hotels and other partners to ensure we are offering sustainable op�ons that allow both the community and natural environment to thrive. Below are a few of VISIT DENVER’s sustainability efforts as well as those from our biggest partners:

VISIT DENVER Environmental and Sustainability Industry Recognitions:

o In 2023, VISIT DENVER was recognized as a Silver Level member of the Colorado

Green Business Network (CGBN). This is a voluntary program that encourages, supports and rewards organizations that make the move toward the goal of true, operational sustainability.

o VISIT DENVER is also pursuing certification in the Event Industry Council’s (EIC) Sustainable Event Standards in 2023. These standards replaced the APEX/ASTM Environmentally Sustainable Meeting Standards in 2019, with an updated version released in 2022. VISIT DENVER was previously certified at Level II under the APEX/ASTM standards and had a goal of achieving Silver.

Hotel Sustainability Reports: In 2022, VISIT DENVER surveyed downtown hotels on their sustainability practices, including Waste Management, Energy Conservation, Air Quality and more. The survey provides meeting planners and visitors with comparable information regarding the sustainable practices of Denver hotels.

Green Vendor Directory: VISIT DENVER provides a one-stop resource to showcase vendors’ sustainability practices. The Green Vendor Directory allows visitors to sort businesses by certification type and practice. VISIT DENVER is proud to support and promote partners and their sustainable efforts.

Colorado Convention Center’s commitment to sustainability:

o CCC’s certifications include LEED Existing Building – Operations and Maintenance Level GOLD; ISO Standard 14001 – Environmental Management System. The CCC will be pursuing LEED Gold certification for the new ballroom and rooftop terrace upon completion.

o The CCC’s Waste Management Program, Energy and Water Conservation efforts, Air Quality policies and sustainable catering support the CCC’s commitment to making all events held at the Convention Center sustainable.

Denver International Airport’s dedication to energy efficiency and the environment: The seventh busiest airport in the world holds a strong commitment to sustainability. Programs like the Environmental Management System, wastewater reduction, airport solar program, single-stream recycling and a partnership with the Colorado Green Business Network support the airport’s goals to reduce its impact on the environment. In addition, the RTD A Line offers a “green” way to travel to and from the airport.

Diverse Denver Recap and Statement

VISIT DENVER con�nues to priori�ze the core values of diversity, equity and inclusion (DEI) in all of its opera�ons and sales/marke�ng efforts. The DEI Board Commitee, which was formed in June 2020, provides ongoing input for focus areas of internal policies/prac�ces, community affilia�ons and support, social impact/work force development efforts and marke�ng efforts and programs.

With the engagement of Darrell Hammond, Sr., of Higher Ground Consul�ng, several DEI educa�onal training courses for staff were conducted throughout 2022. All staff members

par�cipated in Outward Mindset workshops to gain more skills for interac�ng with clients, stakeholders and co-workers. In addi�on, staff recruitment efforts have increased the diversity among VISIT DENVER employees.

Based on opportunity areas iden�fied by the 2021 DEI Percep�on Survey, staff-led Impact Teams researched and developed proposals for enhancing internal policies and prac�ces, with the goal of enhancing DEI efforts. VISIT DENVER’s Board and leadership team have consistently embraced and guided this ongoing journey to enhance the organiza�on’s DEI efforts.

The focus on DEI will remain as a constant thread, in 2023 and beyond, woven into the fabric of all things VISIT DENVER. There will be a focus on addi�onal training and opportuni�es to keep an "outward mindset" top of mind through ac�on and conversa�ons, as well as con�nued work with the Board Commitee and the DEI focus areas. This includes the organiza�on’s official Commitment to Diversity, Equity and Inclusion:

At VISIT DENVER, we believe that travel makes the world a smaller and more connected place. It brings people together and fosters interaction among diverse cultures. It builds understanding, appreciation, empathy and respect for one another. This core philosophy is a big part of who we are as a community and why Denver is one of the top destinations in the country to live and to visit.

The Mile High City embraces and celebrates people of all races, ethnicities, abilities, gender identities and sexual orientation. We believe that Black lives matter and we reject any form of racial injustice. We also acknowledge that there remains a long road ahead to achieve true equity for all historically oppressed communities.

With this in mind, VISIT DENVER is pledging a renewed sense of awareness and action to create change, both within our organization and in our city. While VISIT DENVER has consistently supported diversity, equity and inclusion, we also believe that we can, and we must, do better. We are committed to making these core values a way of life for our organization, our partners in the hospitality industry and our visitors

2024 Convention & Tourism: SWOT

Strengths, Weaknesses, Opportunities & Threats

STRENGTHS

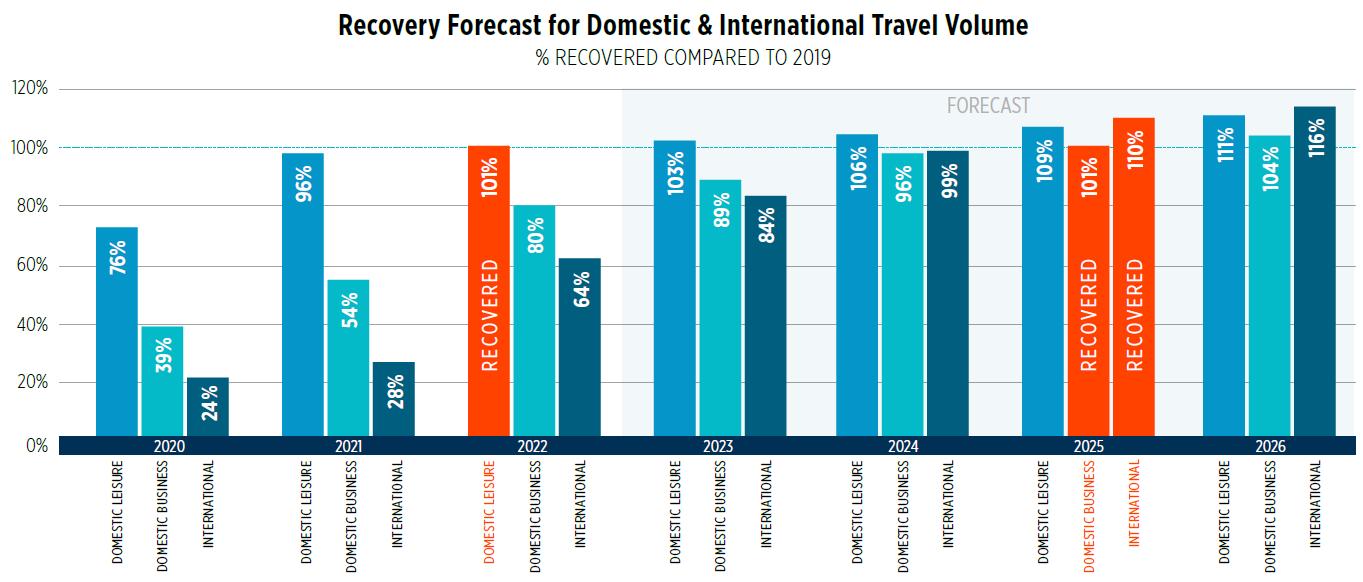

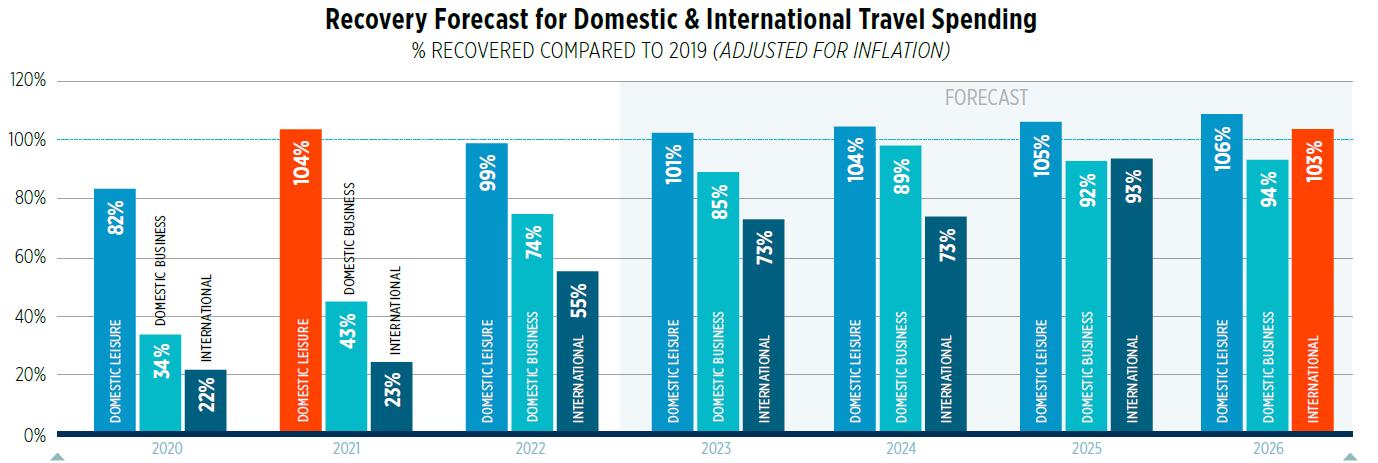

The pandemic era appears to be over, at least for now Infection rates are low and concerns about the virus have largely receded, particularly as a barrier to travel. As proof of this, travel volumes and travel spending have recovered, in many cases surpassing the record levels set in 2019. Domestic leisure travel volume reached 101 percent of 2019 in 2022 and is expected to hit 103 percent by the end of this year (U.S. Travel Association).

The Denver brand, which recently received a major refresh, provides VISIT DENVER a strong platform from which to market the city, both from tourism and convention standpoints, positioning Denver as “uplifting by nature,” an outdoor city full of urban exploration and sophistication. As budgets exceed 2019 levels, VISIT DENVER will expand its sales and marketing presence in both leisure and convention segments.

Smart use of marketing funds in annual regional and national tourism promotional campaigns, including advertising, public relations, social media and search marketing, will keep Denver top-of-mind for the nearly recovered domestic leisure travel market. This includes expanded national advertising in the first and fourth quarters, which are historically soft times for visitation from these segments.

The Denver Tourism Roadmap, launched in 2016 with input from more than 1,000 stakeholders, continues to guide the development of Denver’s tourism product for future years and help VISIT DENVER focus on the top priorities before, during and after the pandemic. This plan will be updated in 2024.

The Tourism Improvement District (TID), launched in 2017, continues to add funds to help complete the expansion of the Colorado Convention Center (CCC), as well as attracting meeting business and marketing initiatives. A fully recovered TID budget is expected to be available in 2024.

Denver has a mild year-round climate, 300 days of sunshine and easy access to outdoor activities, both in the city and the nearby Rocky Mountains. This will be an important part of the brand in attracting visitors in the post-pandemic rea with people who are seeking outdoor and less-populated areas to visit.

Denver has a compact, walkable and vibrant downtown that is easily accessible through a variety of means and includes a wide array of amenities that are attractive to residents and visitors alike, including many options for entertainment, arts and culture, sports, dining, nightlife, retail and outdoor activities. All of this is true despite current challenges related to crime and safety, as well as the reconstruction of the 16th Street Mall.

New hotel product continues to be added to Denver’s supply and Denver has been a leader in supply percentage growth for the last decade. There are more than 6,500 properties in planning, or some phase of construction concentrated in the downtown and airport submarkets

Denver is a central location for meetings, just 340 miles from the exact center of the Continental United States. Denver’s effective status as a regional capital gives the city a leadership position in many areas, including dining, retail, arts and culture and sports, as well as with business, medicine, technology and financial services.

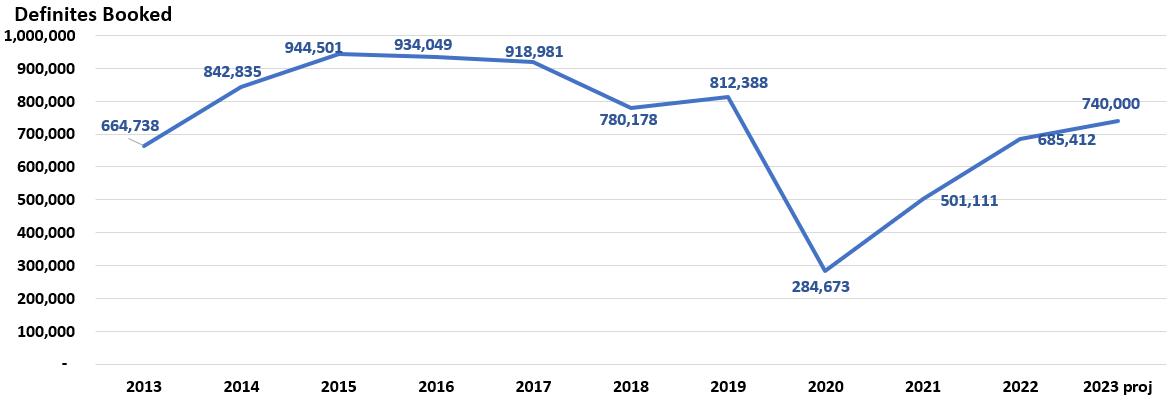

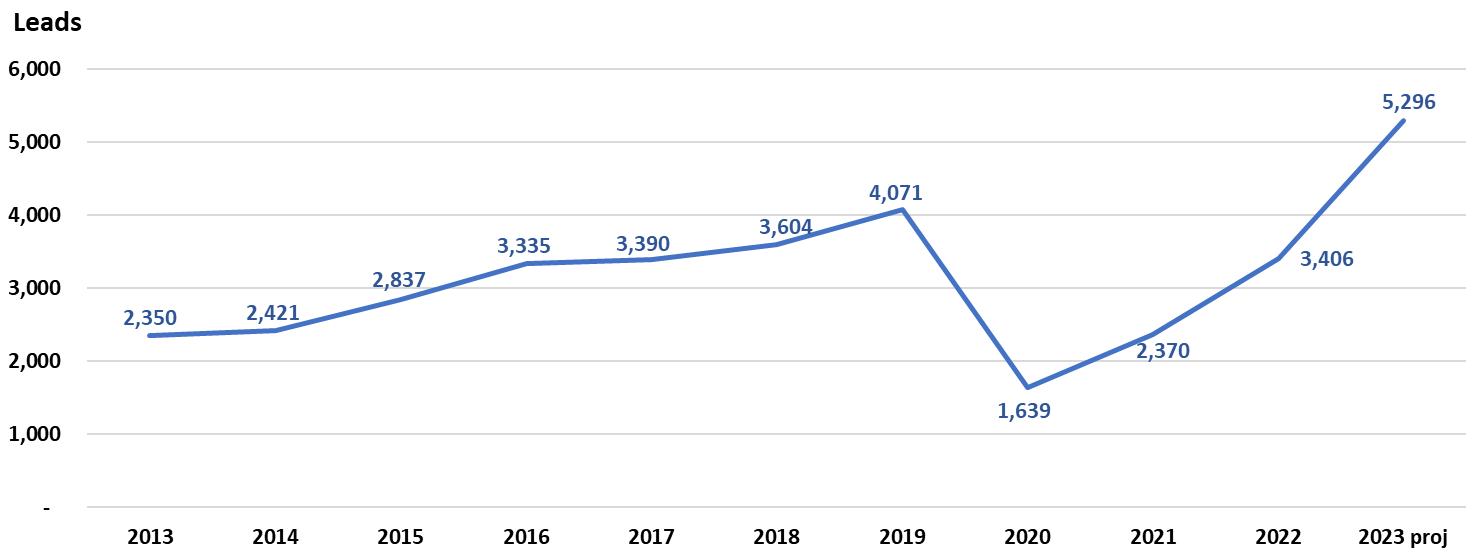

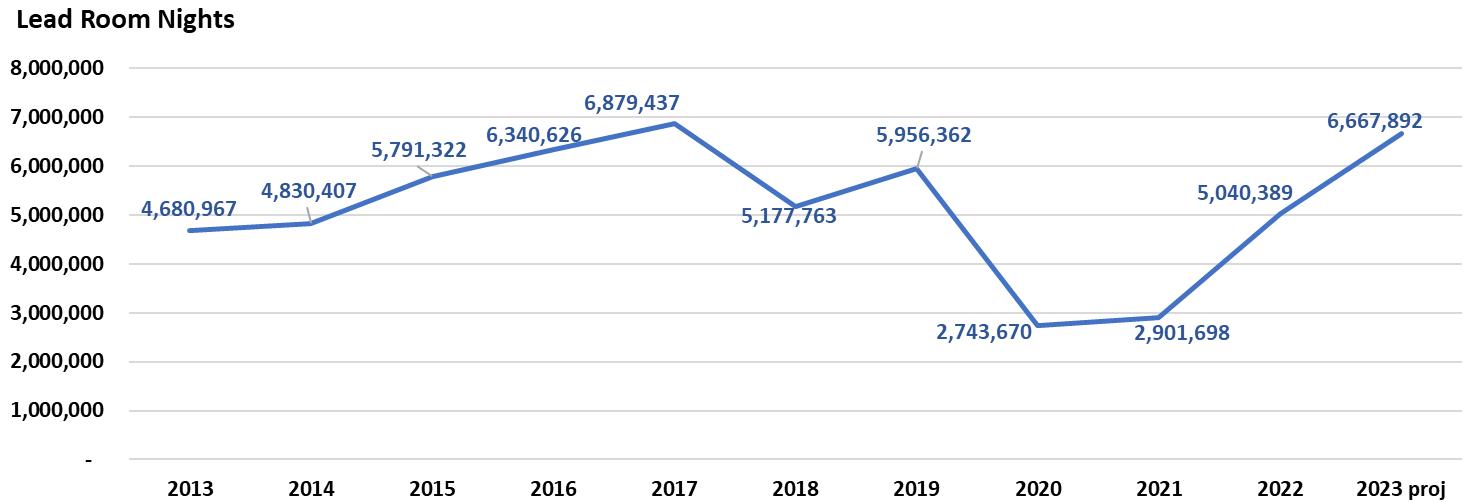

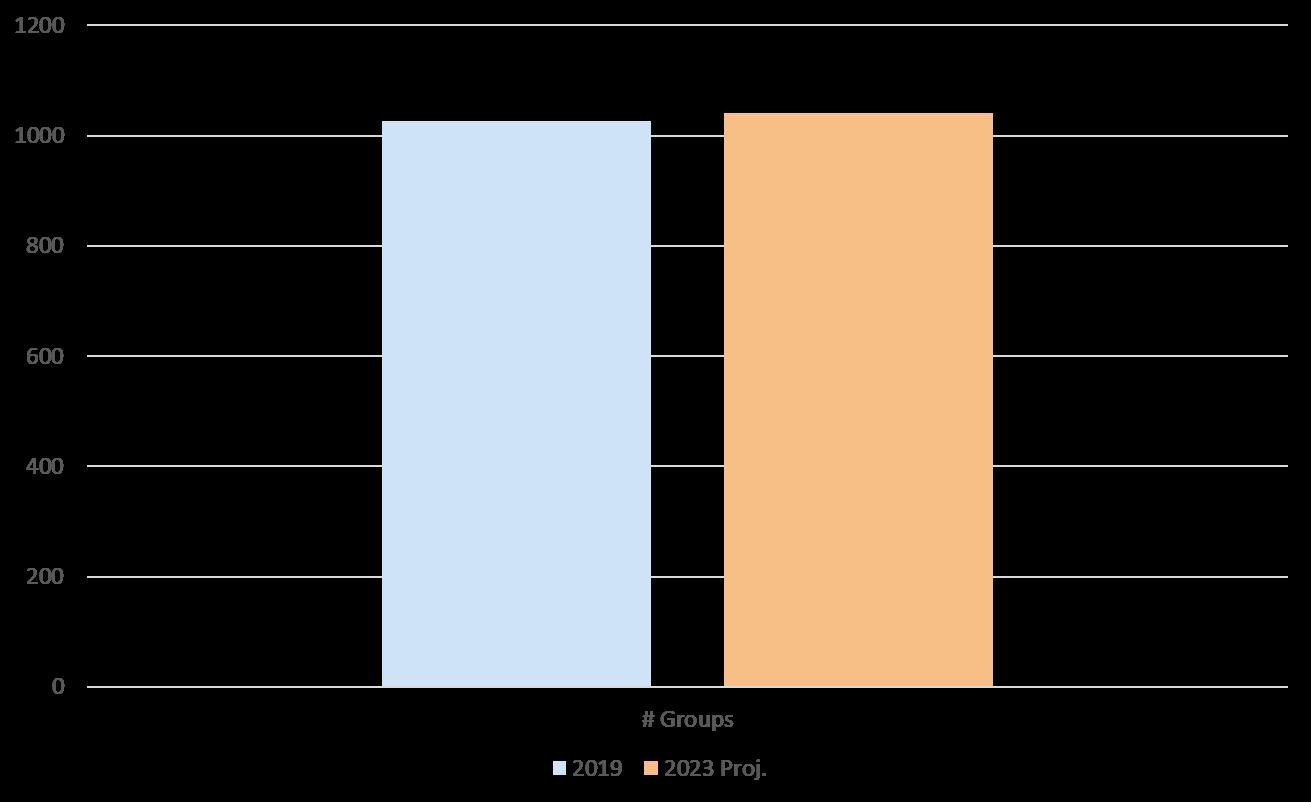

Denver’s long-term prospects in the conventions market remain strong. Meeting lead volume now exceeds 2019.

The CCC already has a strong reputation among clients that will only improve upon the completion of the center’s expansion in late 2023.

Denver International Airport (DEN) remains a central component of Denver’s success in both the leisure and meeting sectors. DEN is currently ranked as the third busiest airport in U.S. and the seventh busiest in the world, due in large part to its strong domestic network and connections. Additionally, DEN has seen the third-fastest recovery of any U.S. airport, with passenger volume through April 14 percent higher than the same period in 2019 (latest figures available).

The recently completed 39-gate expansion has also greatly enhanced DEN’s competitiveness and made the city more attractive, particularly to meeting planners.

The A Line train from DEN to Denver Union Station, which launched in April 2016, provides an efficient option for transportation between the airport and downtown for both meeting planners and leisure travelers, and addressed one of the main complaints from meeting planners.

All international flights to DEN have returned in 2023, including United’s nonstop flight from Tokyo. Additional international nonstop flights are expected to be announced in the coming months.

Denver continues to maintain its position as a top city for “green” meetings and has won many awards and recognition for sustainability.

Denver has a highly regarded medical and bio-science campus at Anschutz Medical Campus, which enhances the city’s reputation as a center for medical meetings and serves as a pool from which VISIT DENVER can recruit ambassadors to assist in the sales process, as well as provide experts and speakers for related groups.

Denver City Council’s 2016 approval of regulations and a taxing mechanism for short-term

rental properties (e.g. Airbnb and VRBO) opened the door for partnerships with these providers and generated additional Lodger’s Tax.

The city’s many tourism, sports, entertainment and cultural-related organizations have been very successful in the last several years in attracting high-demand events, exhibitions and festivals, though some continue to experience limited capacity and visitation during COVID. VISIT DENVER’s continued role in this process will be an ongoing asset.

Denver has a growing reputation for its arts and cultural scene with world-class museums, performance venues such as the Denver Performing Arts Complex, blockbuster exhibitions and annual festivals like the Denver Film Festival, all of which were incorporated into the City’s IMAGINE 2020 Cultural Plan. In addition, there are hundreds of arts and cultural organizations bringing creativity to the city and its neighborhoods, thanks in large part to the unique Scientific & Cultural Facilities District (SCFD) funding that was renewed in 2016 for 10 more years. Innovations like art installations in alleyways and non-traditional, immersive programming by Denver Center for the Performing Arts also represent new ways to appeal to visitors.

The opening of the 90,000-square-foot Meow Wolf in September 2021 and the $150 million renovation of the Denver Art Museum’s Martin Building and Sie Welcome Center and the return of a robust performing arts schedule from Denver Center for the Performing Arts will all keep Denver’s cultural scene on firm footing as 2023 approaches. Notable in 2023 the reopening of Denver Art Museum’s Hamilton Building Collection Galleries that include some of their most inclusive collections, including Arts of Africa, Modern and Contemporary Art and Arts of Oceania.

Denver celebrates its rich ethnic diversity, including its Black heritage, increasing Hispanic/Latino population, Indigenous communities and its engaged LGBTQ+ community, as well as a new focus on people with disabilities, through a wide variety of events, attractions and restaurants.

VISIT DENVER’s board committee on Diversity, Equity and Inclusion continues to evaluate VISIT DENVER’s practices, from hiring to staffing to marketing, in an ongoing effort to ensure the city’s wide diversity is always represented. A consultant hired in 2021 continues to drive this process.

VISIT DENVER’s website, which relaunched in December 2021 with a fresh design, will allow the Bureau to effectively reach visitors across devices and with timely, engaging content, including up-to-date information about navigating the city during COVID. An expanded social media effort, including enhanced social media advertising and increased use of video, is also crucial in communicating with visitors.

Visitors to Denver now have two attraction passes offering discounted admissions to top attractions. The Denver CityPASS launched in 2018, offering tickets to three, four or five of

the eight participating attractions, and the Mile High Culture Pass, a three-day pass providing admission to seven of Denver’s top cultural attractions. The Mile High Culture Pass was relaunched in 2022, and both are selling well.

Denver has a robust culinary reputation that was strengthened in 2023 with the announcement of the Michelin program. Michelin is the global standard of restaurant reviews, and the launch of Denver’s program will immediately elevate the reputation of the city’s dining scene with domestic visitors, meeting planners and international travelers. The program has a three-year contract term with an option for two additional years.

Denver is known as the country’s leading craft brewing city with more than 150 breweries metro-wide. Additionally, the city is becoming increasingly known for its burgeoning craft distilling culture and innovative wineries.

The Denver metro area has extensive parks and open spaces, nearly 80 golf courses and more than 850 miles of bike paths, underscoring the city’s outdoor brand.

Denver has six professional sports teams and modern facilities.

The strength of the Denver Sports Commission in identifying, securing and servicing highvalue, high-impact sporting events, both professional and amateur, puts Denver in good position to grow its sporting event footprint, despite the fact that Denver was not chosen as a host city for the 2026 FIFA World Cup. This reputation was further enhanced by Denver’s successful hosting of the 2021 MLB All-Star Game and Concacaf Nation’s League Finals in 2021, as well as the Denver Nugget’s successful NBA championship run and subsequent parade and rally that was attended by an estimated 750,000 people.

Red Rocks Park & Amphitheatre held a full calendar of concerts, films and fitness events in 2023, extending its season into November and reinforcing the city’s reputation for live music, culture and fitness.

Live music in Denver continues to achieve national awareness with the continued success of the Mission Ballroom in RiNo, the impressive (and largely free) concert calendar at Levitt Pavilion, as well as other smaller venues, especially outdoor ones like Number 38. The success of Denver-based bands OneRepublic, the Lumineers, Nathaniel Rateliff & the Night Sweats and others, as well as strong local festivals, including the Underground Music Showcase and Westword Music Showcase, also aid in this effort.

Denver has a rich Western heritage that is associated with the Rocky Mountain West and anchored by one of the world’s most prestigious livestock shows, the National Western Stock Show & Rodeo. In 2015, voters approved funds for a new development called the National Western Center, which is expected to be completed in 2024 and is intended to be a year-round destination that will engage local visitors and promote out-of-state tourism in collaboration with partners such as Western Stock Show Association, Colorado State

University System, the Denver Museum of Nature & Science and History Colorado.

Denver has a variety of authentic, lively and growing neighborhoods filled with unique restaurants, shops, cultural/historical attractions and parks. Shopping at local merchants is particularly important to international visitors.

Denver’s outdoor brand is supported by the continued development and activation at Civic Center Park, including concerts, events and the Civic Center EATS food truck roundup.

The Amtrak Winter Park Express ski train offers seasonal, weekend rail service from Denver Union Station to Winter Park Resort, creating an option for skiers to stay at least one night in Denver. The service returned to a full January-April schedule in 2023 and is expected to return in 2024.

The introduction of the Rocky Mountaineer luxury train from Denver to Moab, Utah adds another high-demand, rail-based option for visitors to experience the West by train. The train is having its second full year of service in 2023, running trains weekly from AprilOctober.

Denver offers a wide variety of pre- and post-convention vacation opportunities, as well as leisure day trips in the nearby Rocky Mountains, a concept that VISIT DENVER markets under the “Basecamp Denver” brand.

Denver has a growing inventory of innovative tours, such as culinary, brewery and walking tours, as well as new virtual options, which increases Denver’s appeal to leisure travelers, both domestically and internationally.

The City, the Downtown Denver Partnership and other stakeholders have implemented several safety and security plans in the downtown area in 2022 and 2023. There is also a focus on working alongside the provider community to assist individuals who are experiencing homelessness or are in need of specialized services.

In 2023, the city elected a new Mayor, City administration and City Council that appears to support tourism, tourism funding, international marketing and air service development.

On July 1, 2021, the State of Colorado kicked off an incentive program for meetings and events. The program provides a 10 percent cash rebate against eligible hard costs for hosting meetings and events in Colorado. Initially, the meetings had to take place from July 1, 2021 through Dec. 31, 2022; however, in late 2021, the State extended the deadline to June 30, 2024. The minimum rebate is $3,500 and the maximum rebate is $100,000. The program’s goal is to increase tourism recovery by incentivizing meeting and event planners to book new meetings and events in Colorado, rather than in a competing state.

WEAKNESSES

Denver is one of the most geographically isolated major cities in America, with a relatively small population within a 600-mile radius, thus generating less drive traffic for tourism and conventions.

Denver is overly dependent on air traffic, with 41 percent of tourists arriving by air (according to 2022 data), significantly higher than the national average of 25 percent. This makes the city particularly vulnerable during this period with high gas prices that may cause people to travel closer to home.

There is a misconception that Denver is cold, snowy and has unpredictable weather.

Denver is not as well-known as some major U.S. cities with more long-standing tourism brands.

Denver currently has less recognition for offering unique regional cuisine or specialty cooking than other cities.

The number of office workers downtown is still only around 60 percent of pre-pandemic numbers, which impacts the viability of supporting local businesses and the overall vitality of downtown.

Visitors and meeting planners continue to share safety concerns on and around the 16th Street Mall and surrounding areas, noting multiple closed businesses and boarded-up storefronts, aggressive panhandling, people experiencing homelessness and intrusive solicitation by nonprofit groups.

Downtown Denver lacks major retail on or near the 16th Street Mall, a trend that was further exacerbated by COVID-era closures.

Denver has fewer nonstop international flights compared to many other large U.S. cities, though that number has increased substantially in recent years.

Traffic congestion issues exist on I-70 to and from the mountains, especially on weekends.

There is limited public transportation to many of the city’s top neighborhoods, attractions and shopping centers.

There are negative perceptions of Denver’s elevation, including that it can adversely impact a visitor’s stay.

Construction on I-70 and at DEN is greatly increasing traffic congestion from the airport to downtown and creating longer wait times to check in. Construction downtown, including the 16th Street Mall renovation, also impacts traffic flow in the city’s core.

OPPORTUNITIES

The plan to expand the CCC, which will open in late 2023, and rebuild the National Western Center will allow Denver’s convention and exhibition facilities to stay competitive for years to come. The creation of the TID will bridge the CCC expansion funding gap and, when the industry recovers, provide additional marketing funds, further ensuring the competitiveness of the city in both leisure and meetings markets.

The project to update the 16th Street Mall broke ground in April 2022, with an expected completion date in late 2024. The new Mall will be a focal point for visitors and residents alike, with wider sidewalks, more and larger outdoor patios, an expanded tree canopy and a more consistent bus configuration.

In 2017, the City approved $937 million GO Bonds, which include funding for a number of tourism-related projects, including upgrades to the 16th Street Mall, enhancements of citywide mobility projects, funding for key cultural partners and support for downtown parks.

City-wide infrastructure developments like the addition of protected bike lanes, enhancements to downtown parks and the proposed creation of a 5280 Loop will create additional amenities that will benefit both locals and visitors.

In November 2018, Denver voters approved measure 2A, a 0.25 percent sales tax increase to be specifically dedicated to acquiring, operating and maintaining open space. The fund is generating about $37 million annually and guided by a five-year strategic plan.

The renovation at DEN of the Great Hall, ticketing and security areas will improve safety, make the airport more efficient and elevate the passenger experience when complete.

VISIT DENVER will continue to work with DEN to maintain existing air service and pursue additional nonstop flights to tap unserved destinations in target markets including Europe, Asia, Oceania and South America. The new Air France flight from Paris maintains a key route to a very important international market that serves as an additional flight for the rest of Europe. New international flights from Munich (United Airlines) and London (United Airlines) strengthen connections in these important overseas markets.

VISIT DENVER’s already strong track record in promoting the city’s inclusive communities to diverse audiences will be strengthened in 2024 with the continued operation of the Diversity, Equity and Inclusion committee formed in 2020. This committee, along with a newly hired consultant and extensive activities at the staff and operational level, will help the organization improve several internal practices, from website content, hiring policies and training to promotions and partnerships.

On-going marketing initiatives, particularly around the Basecamp Denver initiative that encourages people to “play in the mountains, stay in the city” are poised to take advantage

of the consistent interest in outdoor experiences that Colorado brings, coupled with Denver’s urban appeal.

Temporary exhibitions at Denver’s cultural attractions have continued throughout the pandemic and provide time-specific marketing opportunities while also enhancing Denver’s reputation as a city that embraces arts and culture. Exhibitions like Desert Rider, Amoako Boafo: Soul of Black Folks and All Stars: American Artists from the Phillips Collection at Denver Art Museum; Bugs and After the Asteroid: Earth’s Comeback Story at Denver Museum of Nature & Science; and Awful Bigness at Clyfford Still Museum will continue to highlight the arts and culture scene into 2024.

The City’s IMAGINE 2020 Cultural Plan provides a framework for future cultural tourism development and the Bureau’s Denver365 events calendar is a key resource and promotional platform within the plan

Brand USA’s website content and cooperative advertising and marketing programs offer ways to reach travel trade and consumers in international markets in a cost-effective way.

VISIT DENVER will continue to leverage the hosting of IPW 2018, and the possibility of hosting it again in the near future, to bring more international visitors to the city, despite the COVID-related slowdown in international travel to the U.S.

U.S. Travel Association’s continued advocacy around visas and improvements to the entry process for international travelers improves perceptions of the U.S. as a travel destination

Strong leadership at the City’s Office of Special Events helps ensure that large events are handled smoothly with more streamlined processes.

To attract more meeting business, the State implemented the Meeting and Events Incentive, which provides pre-approved applicants with a 10 percent rebate of up to $100,000 against the eligible hard costs of hosting meetings and events that take place between July 1, 2021 and July 30, 2024.

The Colorado Tourism Office (CTO) Tourism Recovery Marketing Grant will distribute $1.85 million in matching grants to tourist destinations still in pandemic recovery. Eligible projects are city, county or regional tourism marketing and promotional campaigns overseen by nonprofit organizations promoting tourist destinations, this federal funding allows the Colorado Tourism Office to focus on two areas important to pandemic recovery in tourism destinations: providing the Tourism Marketing Recovery Grant directly to the communities still recovering and attracting high-value international tourists back to Colorado. In October, VISIT DENVER was awarded a $500,000 grant to improve international marketing in 2023 and 2024.

The Michelin program will give VISIT DENVER an expanded platform to market its culinary scene to domestic and international visitors, as well as meeting planners and attendees.

The Downtown Denver Partnership’s retail strategy for the 16th Street Mall could provide a big boost to the area’s shopping amenities.

Denver’s overall mild climate could be an asset in coming years when compared to other parts of the west where extreme heat is becoming more regular.

Denver and Colorado’s central role in vital water issues in the U.S., and particularly the west, could create opportunities for hosting new conferences and businesses related to this critical topic.

THREATS

The impact of COVID on the global tourism and meeting industries cannot be overstated, and while a rebound is certainly underway, continued uncertainty due to the possibility of future variants will remain a threat in the coming years.

The short- and medium-term prospects of a recession/economic downturn could negatively impact tourism in all markets. The recession is expected to be mild and short, and the impacts on the industry is widely expected to be minor, but the prospect alone is enough to be cautious.

The entire hospitality industry is struggling to fill open positions. Prior to COVID, the industry’s workforce issues were a result of historically low unemployment rates, coupled with a relatively weak perception of the industry as a long-term career choice. What has emerged during the pandemic are a host of headwinds that combine to make it difficult to find qualified workers, including competitiveness with other industries, reputational issues with the leisure & hospitality sector, health and safety concerns, childcare issues and affordable housing

University-level leisure & hospitality programs are experiencing lower enrollment across the country, which could lead to future issues in filling key industry workforce roles.

Work-from-home policies have led to a slower-than-expected return of the downtown Denver workforce, which has contributed to the shutting of many downtown businesses that serve this market, including food service and retail. VISIT DENVER is part of several initiatives with the City, local businesses and related agencies like Downtown Denver Partnership to try and address these issues on multiple fronts.

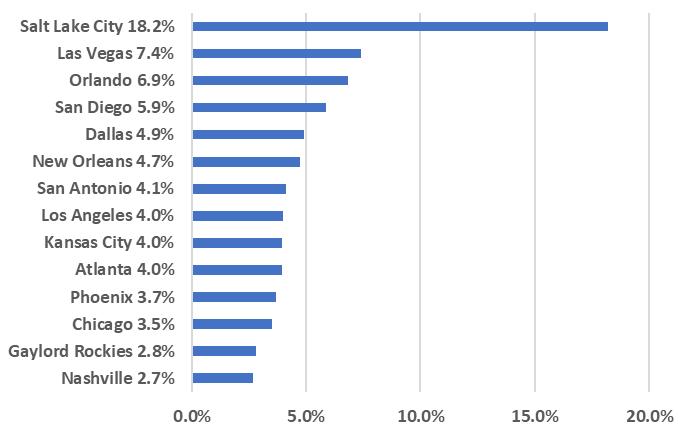

The 1,500-room Gaylord Rockies in Aurora is a top source of lost business for Denver over the long term.

New hotel supply coming online in the metro area will slow the pace of recovery, especially

in the meeting and convention sector.

Perceptions of the impacts of construction and traffic congestion, by both locals and visitors, could negatively impact the city’s appeal

Despite some gains, there are continued safety issues on and near the 16th Street Mall that create an ongoing possibility for negative press, as well as the potential for lost business as more high-profile incidents become public.

Once frequently cited by U.S. News as a top place to live (#14 last year), Denver’s ranking slid to #99 this year in large part due to the lack of affordable housing, a statistic that could cast the city in an unfavorable light. Other issues cited include crime, long commutes and air quality.

Increased competition exists from a variety of traditional web, mobile and social media sources within both the leisure and meetings outlets.

Online booking options enable meeting delegates to easily find lower rates and book outside the block, and new options like short-term rentals further erode hotel room blocks

Ongoing competition from third-party travel and meeting planning websites challenges the relevance of DMOs.

There is always potential for new local, statewide or national legislation or ballot initiatives that could have a negative impact on tourism.

Denver residents’ frustration with growth and traffic could be transferred to anti-tourism feelings, leading to a reduction in local and state tourism marketing dollars.

VISIT DENVER’s success is tied to measurement programs that may not truly reflect business. Convention room blocks are decreasing due to delegates booking outside the block, so attendee counts and room nights booked are frequently lower than actual numbers. New measurements may be needed to accurately provide a picture of tourism business in the 21st century.

Climate changes in general, and worsening fire conditions across the west in particular, could make wildfires and wildfire-related poor air quality conditions a more frequent issue for the state as a whole and Denver in particular.

Meow Wolf, which opened as a successful Convergence Station in 2021, announced the opening of two locations in Texas in coming years, which may reduce the attraction’s regional appeal.

VISIT DENVER: Positioning & Messaging

Denver’s appeal rests on a strong brand foundation that combines outdoor adventure and urban amenities. This section will explore how the current brand positioning was developed, and how it will be deployed in 2024 and beyond.

Denver Brand Positioning & Brand Pillars

VISIT DENVER regularly conducts brand awareness research to gauge the current perceptions of the Denver brand in key regional and target markets.

The 2023 research was conducted by Denver-based BrandJuice, the same firm that conducted earlier studies in 2005 and 2013 from which the previous brand positioning was derived, providing continuity for the development of Denver’s brand.

The research showed a significant expansion of positive brand attributes, as well as some unexpected findings, which has provided the basis for VISIT DENVER’s campaigns for 2024 and beyond

In conducting post-COVID-era research, it became clear that, while travel continued to be a very sought-after activity, the reasons for doing so shifted fairly dramatically as people looked to meet up with loved ones to a much higher degree than pre-COVID. Rather than escape or adventure as primary motivators, travel in 2023 was defined by the idea of reconnecting, and to do so in new places.

Campaigns that will be implemented in 2024 will take advantage of this trend, as well as the trend to make Denver generally more welcoming and inclusive, by continuing the current tagline, “All Ways Welcome.” The line lives on two levels: describing the wide variety of activities in the Denver area, while also signaling to travelers of all types that they will find a warm welcome here.

Brand Highlights:

A strong correlation exists between Denver and the Rocky Mountains in the minds of many respondents, often referred to as “Denver’s Duality. ” The single most important icon for Denver is the Rocky Mountains; the city and its mountain backdrop are inextricably linked.

Denver’s urban qualities were put into a new perspective, with particular emphasis on the previous use of the phrase, “urban adventures,” which was somewhat off-putting and not believable, particularly among long-haul audiences and residents of larger cities like New York and Los Angeles.

Denver’s welcoming and open-minded spirit was reinforced as a key brand differentiator.

Denver’s western history was highlighted, but also brought into current times with qualities of entrepreneurship and collaboration.

Brand Positioning

Uplifting by Nature

Denver is a vibrant outdoor city at the base of the Rocky Mountains with natural energy that heightens every moment.

Known for crisp mountain air, sunshine and expansive blue skies, it’s a des�na�on of discovery that thrives in the beauty of every season offering an escape that upli�s and invigorates travelers with every visit.

Brand Pillars

1. Vibrant, contemporary atmosphere with an open-minded community that embraces visitors

2. 300+ days of sunshine to enjoy panoramic natural beauty and the allure of every season

3. Exciting array of attractions and activities for visitors of all ages (arts, culture, shopping)

4. Creative, contemporary dining scene (including fine dining, “foodie” hangouts, craft breweries, cocktail lounges and urban wineries)

5. Walkable, safe environment that encourages exploration and discovery of eclectic neighborhoods

6. Outdoor activities and adventures, both in the city and the nearby mountain playground

7. Welcoming city for family-friendly fun, providing a variety of opportunities for education and play

8. Dynamic destination for all types of events and entertainment in one-of-a-kind venues

Key Research Findings

DIFFERENTIATING DRAW

Travelers who have been to Denver agree that there are a combination of factors that make the city great, but they struggle to articulate one singular selling point.

Defining clear differentiation from this kaleidoscope of elements can ensure Denver’s appeal as a standout destination is more immediately recognized and understood.

DENVER’S DUALITY PERSISTS

Denver is “the best of both worlds,” offering the amenities of the city with the outdoor setting of a mountain town.

While the idea of an “Outdoor City” resonates, more can be done to define what it means to get outdoors within city limits.

365 DAYS OF DENVER

Denver’s 300 days of sun are a surprise to travelers who often associate the city with winter.

To sway winter-weary travelers, the brand should explore interesting ways to position the city as a year-round destination.

AFFORDABILITY ATTRACTS

The rising cost of living and proximity to expensive resorts has created a perception that Denver is an expensive destination, but visitors don’t find this to be true.

In terms of cost, the brand must show the value it offers to help attract new visitors.

AMBIGUITY OF URBAN ADVENTURE

Travelers, at best, believe the phrase “Urban Adventure” makes sense paired with “Outdoor City” but, at worst, don’t believe it is a true (or desirable) description of Denver compared to other cities.

Removing “Urban Adventure” from the strategy is the first step to repositioning Denver as a destination.

CULTURAL AUTHENTICITY

To deliver on travelers’ desires to experience new places and different cultures in a unique way, the brand should consider leaning into the spirit of Denver’s wild west roots to create an authentic sense of local culture within the city.

ATTRACTIONS FOR ALL AGES

Former Denver visitors believe that the city has something for everyone while those unfamiliar think of it as an adult-only destination.

To deliver on Denver being a destination for groups of all ages, the brand pillars and messaging should reference more family-friendly attractions.

EVENTS KNOW NO BOUNDARIES

Red Rocks and four major sports teams make Denver an event destination for both regional and national travelers to get away for a long weekend.

The brand should further leverage the appeal of Denver’s events to attract travelers from across markets and spur repeat visits.

Tourism Campaigns and Messaging

Attracting tourists to visit Denver for their vacation – whether as a stand-alone Denver trip or as part of a larger Colorado visit – requires a combination of tactics. Regardless of whether the visitor is from a long-haul target market (Chicago, New York or Los Angeles), a regional market (Phoenix, Cheyenne or Albuquerque) or international markets, the decision to come to Denver begins with the city’s brand appeal.

Visitors may make their final decision to come to Denver based on a variety of factors, including short-term exhibitions, special events or the use of Denver as a base for day trips, but the choice to spend time in the city depends first and foremost on the emotional appeal created by exposure to Denver’s brand.

As the brand research study confirmed, Denver’s appeal as an active, vibrant outdoor city drives interest to visit, and likely precedes investigation of specific things to do.

Post-COVID, the Bureau will expand its advertising focus well beyond historical spring/summer and winter holiday periods. The year-round popularity of the city, combined with an evergrowing list of festivals, events, exhibitions and performances throughout the year, allows marketing campaigns to promote the city 12 months a year. All campaigns have the same goal: to bring more visitors to Denver. Specific tactics and markets change with the individual campaign. Here is a summary of 2023 national and regional campaigns, which are discussed in more detail in the Tourism section of this report.

Always-on Regional

o Geographic focus: Colorado (excluding Denver metro) and regional markets

o Main goal: retail, based on availability of events, exhibitions and performances

o Timing: February - October

Spring/Summer

o Geographic focus: large target markets (Chicago, New York and Los Angeles) with smaller test markets (Atlanta, Minneapolis, Dallas, Houston and others), national overlay

o Main goal: create inspiration through branding; encourage further research

o Timing: April - August

Mile High Holidays

o Geographic focus: Colorado (including Denver metro) and regional markets

o Main goal: retail, based on availability of events, exhibitions and performances related to winter holidays including the Mile High Tree

o Timing: November - December

Basecamp Denver

o Geographic focus: National; audience is behavioral as well as geographic, focusing on interest in outdoor activities

o Main goal: establish Denver as a home base that visitors can use to explore everything Colorado has to offer, but to continue to stay overnight in the city

o Timing: January-March, October-December

Of the campaigns above, the spring/summer campaign is normally the largest in terms of budget and reach; has traditionally been responsible for driving new business to the city; and is designed to deliver on brand attributes, create inspiration and encourage further research.

Convention Messaging

In 2017, VISIT DENVER staff and agency, along with feedback from the Customer Advisory Board, developed a new convention brand: “Different on Purpose.”

It speaks to the way the city delivers a unique experience, both for the planners working with VISIT DENVER and their attendees.

The brand is supported by three core pillars:

People: The friendliness, professionalism, and uniqueness of Denver’s engaged population. This extends beyond the usual service experiences into unexpected places (e.g. neighborhoods) and with unexpected people, namely Denver’s colorful residents and the “makers” of the city who are creating hand-crafted, quality products and services.

Place: The way the city welcomes guests and makes them feel immediately at home. While this occurs in many core places downtown, it also shows in Denver’s diverse neighborhoods and unexpected places.

Partnership: The way planners have come to see VISIT DENVER as a trusted resource and a premier destination marketing organization, one that is committed to client success and willing to go to great lengths to ensure an unmatched meeting experience.

Campaigns targeted to the conventions market are described in more detail in the Conventions Situation Analysis section of this report.

Denver’s Meeting Appeal

Many meeting planners consider Denver to be a top-tier convention city because it has the functional attributes they need: excellent meeting facilities and hotels, good accessibility and affordability, service and safety.

Knowing that, the sales team can consistently communicate those details, the goal of the convention marketing efforts towards meeting professionals – and the decision makers within their organizations – is to focus on Denver’s attributes as an exciting city that offers destination appeal.

In the convention market, studies show that “destination appeal” and the ability to attract attendees are some of the most important factors meeting professionals consider when choosing a destination. Furthermore, busy meeting professionals have limited time to receive destination updates, so the convention marketing strategy, brand and tactics have been retooled to deliver destination updates in ways that clients are asking for: short, informative, visually interesting and, often, delivered digitally or in unique offline ways.

Therefore, Denver’s advertising messages in the convention market strive to establish an emotional connection with the customer. The city’s “functional meeting attributes” are reinforced, especially in interactions with salespeople and in collateral; however, it is critical to create a balance between emotional appeal and functional attributes.

The following pillars are used to support the Denver Convention advertising campaign:

Accessibility

Affordability

Meeting Facilities

Hotel Packages

Service

Sustainability Destination Appeal/Safety

The conventions message also has a campaign dedicated to the expansion of the Colorado Convention Center.

Denver: Awards & Accolades

We are a SOUGHT-AFTER DESTINATION: Travelocity cited Denver as one of the top five most popular family vaca�on des�na�ons for spring and summer travel and TODAY echoed the sen�ment, declaring Denver in the top five sought-a�er des�na�ons from July through September in June 2023. Travel + Leisure proclaimed Denver among the “The 18 Cheapest Places to Travel in 2023.” We also can’t forget TravelPulse named Denver one of the top “3 Best U.S. Des�na�ons for 2022” thanks to our metropolitan offerings – from fine dining to cultural experiences – as well as our 300 annual days of sunshine and proximity to the Rocky Mountains. Addi�onally, the Colorado Division of Aeronau�cs Awards Program named Denver Interna�onal Airport (DEN) the 2023 Colorado Airport of the Year as one of the busiest airports in the world with over 69 million passengers traveling through the airport in 2022.

We are CULTURED AND CREATIVE: With a robust arts and culture scene, Denver is earning more acclaim as a des�na�on for the arts. In December 2022, Clever ranked Denver among the top 20 best ci�es in America for its unique culture and iden�ty. Esteemed architecture also makes Denver stand out as a des�na�on with loca�ons like Union Sta�on, which was ranked No. 9 by Time Out’s list of "The 21 most beau�ful train sta�ons in the U.S." in April 2023. Denver also ranked No. 10 in the 2023 USA TODAY 10Best Readers' Choice travel award contest for Best City for Street Art in June 2023. Denver con�nues to be a top loca�on for musicians and music lovers with hundreds of venues across the city. The iconic Rolling Stone Magazine noted Red Rocks Park and Amphitheatre as the No. 1 "Hotest Music Venue in the Country” in April 2023.

We are a CONVENTION CITY: With four hotels on Cvent’s Top 100 Mee�ng Hotels list and more than 14,000 hotel rooms downtown, Denver is a top �er conven�on city. Cvent also ranked Denver No. 10 in the “Top 50 Mee�ng Des�na�ons in North America” in 2023, no�ng the des�na�on as a top choice for event planners worldwide. Mee�ngSource.com con�nues to rank Denver among the “Top 25 Conven�on Ci�es in the USA” based on walkability, affordability, tourism appeal, ease of access, weather and safety.

We are a SPORTS CAPITAL: Denver is home to six professional sports teams and countless personal spor�ng and recrea�on opportuni�es. Following the success of The Colorado Avalanche in 2022 winning the NHL Stanley Cup, The Denver Nuggets won their first NBA Final in 2023 led by Nikola Jokić. Denver was a proud host of rounds one and two of the 2023 NCAA March Madness tournament, the 2023 Na�onal Cycling League Cup Series, the USGA U.S. Amateur Championship, the 2023 USGAA Finals and more.

We are HEALTHY & FIT: Denver is commonly known for its healthy mindset and exercise culture, and The Mile High City consistently earns high rankings as a top healthy city due, in part, to its temperate climate as well as the city’s loca�on with easy access to all the recrea�onal fun of the Rocky Mountains. Rocket Mortgage named Denver the eighth least stressed city in the U.S. in

August 2022, ci�ng the city's abundance of outdoor spaces, wellness establishments and mental health providers. Similarly, the American College of Sports Medicine ranked Denver No. 9 on their 2023 American Fitness Index.

In January 2023, WalletHub ranked Denver among the top 10 U.S. ci�es for ac�ve lifestyles as well. A study from the Bankers Life Center for a Secure Re�rement also noted Denver as the third best city in America for a healthy re�rement. With extensive miles of paved urban bike trails, metro Denver is a haven for cycling enthusiasts. Any�meEs�mate.com ranked Denver No. 6 on its “most bike-friendly” list because of the number of bike trails and bike shops per capita in The Mile High City. LawnStarter put Denver at No. 7 on its “Best Biking Ci�es in the U.S.” list for similar reasons, but also factored in bike meetups, weather and more.

We are a CULINARY DESTINATION:

Domes�c and interna�onal travelers can find top culinary spots in Denver. In June 2023, The MICHELIN Guide made Denver and Colorado its newest des�na�on. Colorado will be North America’s eighth Guide des�na�on. In addi�on to stars, MICHELIN Guide also awards restaurants The Bib Gourmand award. In the U.S., a three-course meal at a Bib Gourmand restaurant must be under $50. State selec�ons will be made later in 2023.

Colorado as a state is among the top 10 in breweries per capita and one of the top five states with the most cra� dis�lleries. In 2021, Esquire named Colorado, “one of the foremost states when it comes to cra� whiskey,” ci�ng two Denver dis�lleries, Stranahan’s and Leopold Bros., as top op�ons (even naming the later its No. 8 dis�llery in the country). This sen�ment was echoed by Travel + Leisure, which ranked Leopold Bros. sixth in the country.

We love our ENVIRONMENT: From priori�zing green spaces to encouraging the use of electric vehicles and alternate fuel sources, The Mile High City does its part for the planet. Denver ranked No. 1 on Architectural Digest's 2023 list of the “Top 50 Most Climate Resilient Ci�es” due to factors including fewer threats of extreme weather damage and city-level ini�a�ves to support clean energy Denver is the only U.S. city included on Na�onal Geographic’s list of “Eight Sustainable Des�na�ons for 2021 and beyond,” thanks to the city’s goal of achieving 100 percent renewable electricity by the end of 2023, and 125 miles of new bike lanes and solar gardens planned throughout the city. Online insurance marketplace Policygenius echoed this sen�ment, naming Denver as the tenth-best city to live in by 2050 for climate change. Denver’s climate and mindset are conducive to enjoying the great outdoors, whether hiking, biking, running or walking. In August 2023, Denver Interna�onal Airport’s (DIA) fleet opera�ons was recognized for its sustainable management as the number three fleet in North America by the Na�onal Associa�on of Fleet Administrators (NAFA). The annual ranking recognizes peakperforming opera�ons and honors enhanced prac�ces making a posi�ve impact on the environment and improvements within the fleet industry.