Australian Conveyancer edition 11 - Time To Clean House

Conveyancer.

THE PRACTITIONER’S COMPANION

REAL ESTATE’S MONEY-LAUNDERING WASH CYCLE EXPOSED

AIRING DIRTY LAUNDRY

Lawyers and real estate agents face tough anti-money laundering regulations as Australia closes the loopholes that have allowed criminals to wash cash through property transactions. We examine the extent of the problem and what the changes mean.

From Page 12

STATE’S NEW MINI CITY

NSW has announced the creation of a new mini city in Sydney’s metro area that will go a long way to reaching home building targets aimed at easing the housing crisis.

Page 4

HANDLE WITH CARE

Australian Institute of Conveyancers NSW president Ann BlanninFerguson has been in the industry for decades. The Sydney-based conveyancing boss opens up about challenges and successes.

The December 2025 deadline to open up e-conveyancing to full competition is at risk after the body leading the reform paused its work and called for federal intervention.

Governments have been pushing to deliver greater competition in digital settlements, breaking the monopoly of Commonwealth-bank backed PEXA, which in 2023 completed transactions with a property settlement value of over $814 billion.

However efforts have been delayed, with the Australian Registrars National Electronic Conveyancing Council (ARNECC) pausing the interoperability program, which is leading the reform.

In a June statement, ARNECC said issues raised by the banking industry are “beyond the remit of state and territories to resolve”.

The council, which has representatives from each state and territory, said it would raise the challenges with the federal government and regulators.

However, the federal assistant

NEWSROOM

Stories that moved the dial

minister for competition Andrew Leigh criticised states and territories for the delays, adding the federal government would only intervene once ARNECC used all its available powers.

Under the reforms, lawyers, conveyancers and bankers involved in an e-conveyancing transaction will no longer have to use the same electronic lodgment network operator (ELNO) for property settlements.

Currently customers do not have a choice but to use the PEXA monopoly. The second operating ELNO, Sympli – a joint venture between legal software provider InfoTrack and ASX Ltd – was approved in 2019, but cannot yet seamlessly operate within the existing network platform.

A third player, Lextech, does not yet have approval to operate.

PEXA group advocate Simon Smith said it’s “relieved” the e-conveyancing

INTEROPERABILITY: THE UPSHOT

reforms have been paused, given its longstanding concerns with the interoperability model.

PEXA believes the model designed by regulators is flawed because no single party would be accountable if things went wrong.

“The banks have said that the situation – the absence of oversight on financial settlement – is too risky. And we’ve been saying the same thing,” Smith said.

“It’s just proven to be a massive blowout in time and cost because it was never properly designed in the first place.

“There wasn’t a proper business plan and design done, and so it turned into one of those big tech projects that went off the rails.”

However, rival Sympli disagreed, accusing PEXA of promoting falsehoods to undermine the reforms and protect their monopoly.

For the past decade, conveyancers have used digital provider PEXA to settle properties on behalf of home buyers and sellers.

PEXA operates as a monopoly. A regulator has been established to promote a competitive environment that drives efficiencies, costsavings and innovation in the e-settlement space. Similar approaches are evident in the airline, telecommunication and transport sectors.

ARNECC is the regulator committed to promoting an open network for multiple organisations to seamlessly exchange and use data. By creating this open network, other organisations can enter the e-settlement ecosystem, ensuring conveyancers and their clients have choice for pricing and service quality.

e-conveyancing work paused

“What will happen in an interoperable world, is if there’s any issue that happens in a transaction … then a customer goes to the network they subscribe to, to resolve that problem,” Sympli chief executive Philip Joyce said.

“Unfortunately, I think [PEXA’s] position has scared stakeholders to such a point that we’re going to have federal or some intervention here to clarify this once and for all.”

While Joyce admitted there were challenges, they did not involve financial services.

“We think the incumbent has executed a pretty sophisticated disinformation campaign here,” he said. “Most of the issues affecting the execution of this reform are actually not financial settlement issues – they are actually all about the exchange of information between the counterparties, which is in ARNECC’S wheelhouse.

“We’re determined to stick around and get this reform completed. This reform is really about choice for conveyancers and that choice and competition is really the benefit for them.”

In a recent report, the NSW Productivity Commission noted PEXA’s “very high profits”, with 88 per cent overall market share in 2023.

The commission also said consumers were unlikely to have fully benefited from lower costs through the shift to e-conveyancing, with the estimated $89 million in annual productivity benefits likely flowing to ELNOs via “above-normal profits”.

The commission described

industry regulator ARNECC as under-resourced and lacking power, and recommended that ARNECC, state governments and the federal government consider making the ACCC responsible for overseeing the e-conveyancing market.

However, the ACCC has previously turned down the suggestion it should take on a greater role, in light of its other regulatory responsibilities. While the ACCC said it was aware of ARNECC’s pause in the interoperability program, it “does not have a direct or specific regulatory role in relation to e-conveyancing reforms”.

The regulator has “strongly supported efforts to introduce effective competition into the e-conveyancing market as soon as is practicable” and noted the “effects of uncertainty and further delay on the development of a competitive market”.

The timeline to achieve interoperability has taken much longer than first proposed, with multiple delays to date.

PEXA’s Simon Smith denied it was deliberately stalling the reforms, saying that making e-conveyancing work across different jurisdictions and rules involved great complexity.

“All we’ve been doing is just highlighting the level of detail and matters that need to be resolved if it’s to be done safely,” he said.

The Australian Institute of Conveyancers has previously aired strong concerns about the potential for an ELNO to use its market power to move into the conveyancing market and operate with an unfair competitive advantage.

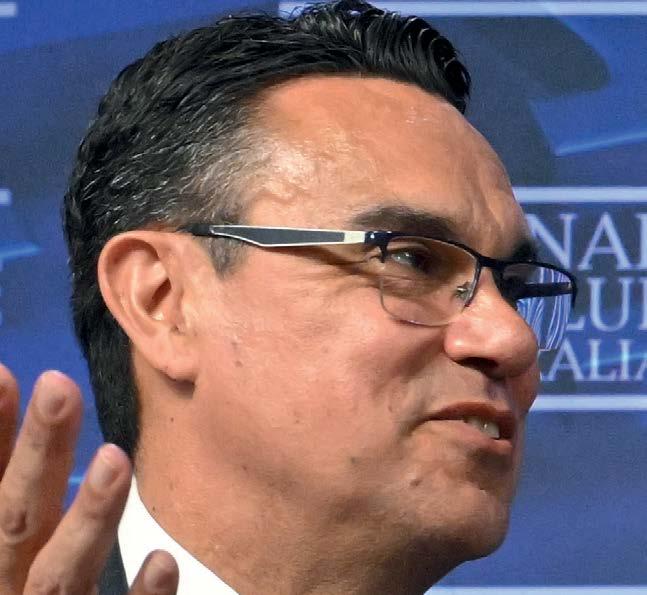

Federal Assistant Minister for Competition Andrew Leigh is critical of the ARNECC delay but says the federal government will not intervene until the state and territories have exhausted their powers.

PHOTO: MICK TSIKAS

First mini-cities revealed in fasttracked housing plan

TNEWSROOM

Stories that moved the dial

he first planned mini-cities have been unveiled under a signature NSW housing policy a minister insists will enable the state to deliver on ambitious homebuilding goals.

Tens of thousands of homes could be built near four stations as part of a blanket high-density rezoning around those and other transport hubs.

Plans for the initial fast-tracked precincts were revealed recently as part of a strategy the government says will rebalance housing growth around new metro stations and existing train infrastructure.

Kellyville and Bella Vista, in Sydney’s north-west, will be among the fast-tracked precincts as an existing metro line is linked up with a soon-toopen route under the city centre.

More than 20,000 extra homes could be delivered in a rezoning of the area around the two suburban stations. Those houses would be supported by 10,000 additional jobs, and up to 1650 affordable properties could be delivered under the plans.

Similar proposals at Hornsby, north-west of Sydney’s city centre, and Macquarie Park, in the city’s

north, are tipped to provide 5000 and 4600 homes respectively.

The projects are predicted to collectively deliver 30,000 homes, although the housing tally represents only a fraction of the 377,000 extra properties NSW needs to build within five years under its nationally agreed targets.

Planning Minister Paul Scully insisted the state could still hit that number despite approvals and completions consistently lagging the required tally of 75,000 per year.

“About two-thirds of those [377,000] are in the planning system for approval or under construction at some point,” he said.

“We remain confident we’ve set, and through all levels of government agreed on, an ambitious [and] realistic target.”

Scully said the mini-cities represented a blueprint for Sydney’s future based on infill development rather than further sprawl.

But opposition leader Mark Speakman labelled the announcement “density without infrastructure”, arguing facilities such as schools and hospitals were left out of the plan. “If you’re going

to have more density around metro stations you’ve got to provide for schools, hospitals, police, public transport and open space … we’re seeing none of that,” he said.

“In Bella Vista and Kellyville, where there are 20,000 new homes proposed, there’s a proposal for only one extra school and very little in the way of extra open space.”

The fast-tracked precincts will share more than $500 million put aside for road upgrades, transport links, open spaces and other community infrastructure.

They are among eight “priority high-growth areas” earmarked for greater density under the transportlinked housing plan.

Rezoning of the sites, which include locations in Sydney’s inner west and lower north shore, will create capacity for nearly 50,000 homes over 15 years, the government says.

Housing Now chair David Borger said the government’s plan was a great step forward and capitalised on the $21 billion city metro project.

NSW Planning Minister Paul Scully: Believes the state’s Mini-City plan is ambitious but realistic.

PHOTO: BIANCA DE MARCHI

Renter relief finally hits

By POPPY JOHNSTON in Canberra

Clouds are finally starting to part for Australian tenants, with rents in most major cities either falling, stalling or growing at a slower pace.

Low vacancy rates have pushed advertised rents higher for several months running but the latest report from real estate platform Domain shows conditions are improving for renters.

Asking rents for houses fell 1.8 per cent in Hobart in the June quarter and held steady in Sydney and Perth, the report found. Several other cities recorded slower rates of growth over the three months, with the pace of quarterly growth 1.5 times slower than the previous quarter across the combined capitals.

Similarly for units, the pace of growth has halved across the combined capitals in the June quarter compared to the three months prior. Domain chief of research and economics Dr Nicola Powell said rental market conditions would likely

continue to ease, given vacancy rates were moving higher.

Vacancy rates last month in Sydney, Melbourne, Brisbane and Canberra hit six-month highs and in Perth a two-year landmark.

“Secondly, rental demand is easing, as the number of prospective tenants per rental listing has consistently fallen throughout 2024,” Powell said.

This reflected overseas migration likely passing its peak, she said, with further declines expected as the federal government’s immigration strategy worked to ease population growth.

An increase in first-home ownership should further alleviate rental conditions in Australia, Powell said.

Initiatives such as Queensland’s doubled first-home owner grant, the federal Help to Buy shared equity scheme and revised stamp duty concessions in the ACT, South Australia, Western Australia, and Queensland would help more Australians into home ownership.

Home lending slips, still ahead

By POPPY JOHNSTON in Canberra

New home lending remains far ahead of where it was a year ago despite a minor dip in May for property investors and owner-occupiers.

Over the month, the Australian Bureau of Statistics logged a 1.7 per cent fall in all new housing loans, to $28.8 billion, with first-home buyer loans down the most, sinking 2.9 per cent.

Yet over the past 12 months, the value of new commitments was up 18 per cent.

Loans to investors had been growing faster than lending to owner-occupiers in the year to May, said the bureau’s head of finance statistics, Fiona Cotsell.

Investor lending had been moving higher in most states and territories, with the biggest rises in NSW, Queensland and Western Australia.

“In May, the value of new loans to investors in Queensland reached an all-time high of $2.4 billion, exceeding Victoria for the third consecutive month,” Cotsell said.

“This is mainly due to investors taking out larger loans in the Sunshine State compared to this time last year.”

The regional divide in property market performance was still playing out, Oxford Economics Australia senior economist Maree Kilroy said.

The mid-sized capitals – Perth, Adelaide and Brisbane – have been leading the pace of home price growth, which has, overall, proved resilient to higher interest rates.

“At the national level, we expect price momentum to temporarily fade in the back half of 2024,” the economist said.

Yet interest rate cuts, likely in early 2025, along with ongoing housing shortages, would trigger an acceleration in home prices from then, Kilroy said. “However, housing affordability will place a limit on gains.”

RateCity research director Sally Tindall said Australia’s “Teflon property market” continued to rise despite higher interest rates, “dragging the average new loan size along for the ride”.

The size of the average new owner-occupier mortgage in Australia is $626,055 nationally.

FACE-TO-FACE

With Australian Institute of Conveyancers

NSW president ANN BLANNIN-FERGUSON

Handle with care

Ann’s tech-savvy and heartfelt approach to customers.

AICNSW president Ann Blannin-Ferguson: after decades in the business, she still enjoys the black-and-white nature of the profession.

Story: MELISSA IARIA

Photos: JULIAN ANDREWS

“We’ve all become more aware of making sure there’s a balance between work and non-work, and to actually go out and enjoy the sunshine.”

Ann Blannin-Ferguson

Ann Blannin-Ferguson was elected Australian Institute of Conveyancers NSW president a year ago, bringing four decades of expertise to her significant advocacy role.

During the course of her career, she has witnessed many changes, recalling a Monday morning in the late 1980s when the solicitor she worked with brought in a computer and handed over an instruction book, telling her and other staff members to “turn it on and see what you can do”.

Today, Ann embraces technology as the way of the future, but one thing has remained steadfast: the trust clients invest in her to handle what’s often their biggest asset.

“I’d say at least a third of my job is psychology, trying to keep people on track and not too stressed,” she quips.

From her conveyancing practice on Sydney’s lower north shore, Ann has counted generations of the same family among her clientele.

After decades in the industry, she still finds her work satisfying and enjoys the black and white nature of her profession.

Her achievements on the AICNSW board have been a source of pride and she enjoys meeting other conveyancers and hearing ideas about how the sector can be improved. Australian Conveyancer sat down with Ann to learn more about the well-regarded industry leader and how she copes with her busy roles in these changing times. >>

CONTINUED FROM PAGE 7

AUSTRALIAN CONVEYANCER: What are some practical challenges you face in your own firm?

AB-F: Not having enough hours in the day when it gets really busy. You end up doing stuff in the middle of the night, sending off emails at 11pm.

A small business’s workflow also ebbs and flows.

Sometimes we’re really busy, other times we’re scratching for things to do. At what point do you bite the bullet and put someone else on? As soon as you organise it, work suddenly drops off and you’re considering updating the archives or cleaning out the cupboards.

Then suddenly, you’re busy again and could do with an extra pair of hands. I find that side of things difficult.

AC: What obstacles do technology advances bring and how do they affect your workflow?

AB-F: I have a really good IT bloke who answers my most basic questions. I’m sure I’m the reason why he drinks and swears as well. You’ve got to ensure you’re protected and your whole system is not going to fall over. That’s a challenge, but I’ve met all of them over the years.

There are days I think I’d like a typewriter, some carbon paper and to be able to put a letter in the mail. To not have to respond to something immediately, and have more time to consider options. But on the whole, I try to grab technology and run with it.

When electronic conveyancing was coming in, people were saying, “Oh, I’m not doing that until I have to.” I thought that was really dumb. You’ve got to get your head around it because this is the way of the future and there’s no use denying it.

We’ve got PEXA and possibly some more ELNOs coming on track soon. I use the TriConvey system and I find that’s really good. I also quite often do Zoom meetings if clients can’t pop in or or I can’t see them somewhere convenient. That’s really helpful, especially if we’ve got a very complex contract. I’ll make sure they’ve got the contract in front of them and we’ll go through it.

AC: How do you ensure your practice is as profitable as it needs to be?

AB-F: We don’t waste money. I have some very strong Scottish heritage with a dash of Jewishness in there, so we are minimalist and try to keep it as simple as we can. We’ve just got a couple of computers and an old client gave us a really good photocopier, which was very kind. That’s been a godsend. I work mainly from my sunroom or pop up to my Newport office to see people there as well.

“You’ve got to ensure you’re protected and your whole system is not going to fall over. That’s a challenge, but I’ve met all of them over the years.”

Ann Blannin-Ferguson

AC: How do you cope with industry changes?

AB-F: As soon as something happens, we make sure we’ve got our heads around it. We discuss any changes in legislation or what Revenue NSW or Land Registry Services is doing at great length.

For many things, you don’t have a choice as to whether you’re going to do it or not. But you really need to understand what you’re doing, and how and why you’re doing it, and incorporate that into your daily work.

AC: How do you deal with increased obligations around data security and legal compliance?

AB-F: We’ve discussed at great length things like identity verification, where we must keep people’s private information for a long period before it can be destroyed.

I encourage my clients to use the Australia Post system for doing their verifications; that way it can sit there on their cloud rather than mine. As long as I tick the boxes, I’m fine. We get all that done very early in the matter.

All my paper files also get digitised and come back on a thumb drive, so if TriConvey goes down, I have another way of finding old files. But once they’re archived, they’re archived.

In terms of other financial security, I’m the only person with control over the trust account.

For cybersecurity, I don’t give out account details to anyone in the body of an email and if I’ve got clients transferring money into my trust account, I always ask them to double check account details. I haven’t had any real problems. There’s no money going astray and I haven’t had any cybercrime issues, which is good.

AC: How do you ensure work-life balance?

AB-F: I do my best to make time for myself. Often I’ll move things around if I want to go to lunch with a friend or have an extra long weekend. Sometimes if you’ve gone away for the weekend, you have to take the laptop in case there’s a settlement on a Friday afternoon. I’ve done settlements from all sorts of places.

There’s always something to do, to be honest, and you could sit here and work seven days a week, but sometimes you’ve just got to say enough’s enough.

I don’t answer the phone to clients on a Sunday. That’s my day that absolutely nothing happens. Quite often on a Saturday if clients have gone to an auction, they might need to talk to me about something, so I’m happy to talk to them on a Saturday. Sometimes if clients have to sign something in ink, rather than through Docusign, I’ll see them on a Saturday morning.

You’ve got to be flexible with people. Not everyone can come to see you between nine and five. >>

CONTINUED FROM PAGE 9

AC: How do you retain and develop staff?

AB-F: I like to maintain flexibility. My other staff member Julian’s just only recently got his full licence and he likes that I’m very flexible in what hours he works. If he can work from home, that’s fine. He does things other than conveyancing, so he always makes up the time. It’s a give and take situation.

AC: What do you think of the industry trend of larger conveyancing firms acquiring smaller practices?

AB-F: There are pros and cons. If they’re gobbled up by extremely large corporations, clients lose a lot of that oneon-one with a practitioner. In some very large companies, like legal firms, practitioners also get pigeonholed. You might do one little section of a matter, but not the whole matter, and you’re stuck doing very repetitive work.

In a small practice like this, we do something different every day and it gives us broader expertise.

I can see the pluses and the minuses of acquisitions, but it’s not for me. It’s not my plan to sell the practice to a larger conglomerate, but I won’t say won’t, in case they want to offer me a large amount of money.

AC: What are the risks to the industry’s profitability?

AB-F: The more staff you’ve got, the more supervision is needed to ensure everyone’s pulling their weight.

That can bring certain problems as well, like in-house politics of who does what and when, which is something we don’t have here, and something I don’t miss.

Having worked in larger firms, I’ve had people who look busy but aren’t actually achieving anything. They’re hurrying here or there, but when you look at their billings, they’re not actually getting anywhere fast.

AC: How is the current property environment and interest rate uncertainty impacting the sector?

AB-F: It impacts us greatly. If they were to keep interest rates on hold for another six months or more, we’d probably expect to be very busy. Actually, we expected to not be very busy over the COVID years and were flat out. I just worked my little self into the grave during COVID, there was so much property changing hands. I was quite amazed at that.

AC: How do compliance obligations affect the industry?

AB-F: Compliance obligations are increasing, with something different every year.

This year we’ve had additional cyber security requirements and questionnaires about electronic conveyancing.

We have to comply with all sorts of things just to get our professional indemnity insurance.

The insurer will look at your risk management and any cyber problems and bill you accordingly, and the insurance seems to go up and up. But it’s whole industry coverage and covers you after you’ve retired.

We also must update our education and pass an exam each year to stay licensed.

Compliance is part of the job and there’s not much wiggle room to be different to everybody else.

We’ve all got to make sure the forms are correct and the clients are advised accordingly, whether you’re buying into a retirement village or a two-bedroom unit down the road.

AC: What are the risks and rewards of using AI in workflows?

AB-F: It’s a bit early to implement AI and I don’t actually know anyone who’s gone down that road yet.

We often get ads offering contract reviews, but I don’t feel confident AI could do it properly at the moment.

If I’m reviewing a contract for a client, the things I’m looking for could be different from what the AI has been set up to do. You’d have to set it up to your individual needs, and then it could assess a property as being prone to flooding, or bushfire, for example.

AC: How is the sector helping staff achieve work-life balance?

AB-F: Fifteen years ago, people were literally working themselves into an early grave, but today everyone I know in the industry seems to consciously try and make their life well balanced.

We’ve all become more aware of making sure there’s a balance between work and non-work, and to actually go out and enjoy the sunshine. We’ll often go out and just sit in the park at the end of the street that overlooks the harbour and have lunch, which is very nice.

“Compliance obligations are increasing, with something different every year. There’s no wiggle room ….”

Ann Blannin-Ferguson

Australia shuts the laundry door

SPECIAL INVESTIGATION

By SAM McKEITH and LEWIS PANTHER

Lawyers and real estate agents face tough anti-money laundering regulations under plans to tighten the regime in Australia.

Up to 100,000 individuals and businesses will need to meet significant reporting obligations under so-called Tranche 2 measures currently being discussed by the government.

They would extend Know Your Customer (KYC)style steps that banks were forced to adopt after the Commonwealth Bank was exposed and fined $700 million for allowing criminals to funnel tens of millions of dollars through its smart ATMs.

Since 2015, when Australia was labelled a soft target, akin to countries like Haiti, Madagascar, China and the US, there have been ongoing calls to extend these KYC steps to the property sector where the vulnerability is described as “very high”.

Given that the real estate sector is worth $10.4 trillion – three times that of the Australia stock market – it is understandable that the government is under pressure to act.

Much of that pressure has come from the global Financial Action Task Force (FATF), of which Australia was a founding member. But while it has toughened anti-money laundering and counter-terrorism financing measures since being shamed in 2015, it is a “matter of concern” that risks still exist.

“Australia is still falling short of meeting all standards set to help combat criminal abuse of our financial system,” said Attorney-General Mark Dreyfus after the latest FATF report in March.

He echoed these comments at the launch of the latest government risk assessment, where he highlighted that property was a main target for money launderers.

“These criminals are constantly looking for new ways to exploit our systems and launder the proceeds of their crime through Australian real estate and our economy more generally,” he said.

“It’s a matter of concern that since 2015, Australia has failed to comply with key FATF standards, including extending the AML/CTF regime to Tranche 2 entities, which

Of the $1.1 billion of criminals’ assets seized by AFP between July 2019 and June 2024, more than $720 million involved real estate.

“Australia’s strong and liquid property market makes it an attractive destination for criminals to both store value and enjoy the fruits of their illicit activity.”

Australian Federal Police

include lawyers, accountants, real estate agents and dealers in precious metals and stones.

“Australia is now one of only five jurisdictions out of more than 200 that do not regulate Tranche 2 entities, placing Australia at risk of being ‘grey-listed’ by the FATF, which could result in significant harm to our economy.”

His latest comments came at the launch of a 120-page National Risk Assessment by AUSTRAC – the Australian Transaction Reports and Analysis Centre – which has repeatedly noted that property is a soft target.

In fact, it is one of only a few areas deemed to pose a “very high and stable money laundering vulnerability”, according to the new report.

“The actual value of money laundering through Australia’s real estate market is difficult to estimate,” the report notes.

But it is one of the commonly identified asset types in criminal confiscation investigations, and Australia is one of the most attractive real estate markets globally, says the report, which warns: “Real estate will continue to pose a very high money laundering vulnerability over the next three years, driven largely by the market’s stability and high value.”

Of the $1.1 billion criminals assets seized by the Australian Federal Police (AFP) between July 2019 and June 2024, more than $720 million involved real estate. More than 370 residential and commercial properties were seized over the same period.

“Australia’s strong and liquid property market makes it an attractive destination for criminals to both store value and enjoy the fruits of their illicit activity,” an AFP spokesperson said.

“Tranche 2 aims to improve the transparency of the Australian real property sector and bring visibility of suspicious transactions to regulators and the police, thereby reducing its exploitation by money launderers.”

The Tranche 2 measures that are certain to be implemented will have a significant impact on the property sector, according to practitioners.

Queensland Law Society chief executive Matt Dunn told Australian Conveyancer that the reforms would have significant workload and ethical challenges for the industry, saying they were one of the biggest issues facing the industry.

Australia airs its dirty laundry

By SAM McKEITH

Australian law enforcement agencies say the nation’s real estate sector has become a key target for getting dirty money into Australia, making the federal government’s plan for stricter antimoney laundering laws a non-negotiable for the sector.

Real estate was increasingly a money laundering option of choice due to Australia’s financial sector and banks getting harder to exploit, the Australian Federal Police (AFP) said.

Australia’s highly regulated financial sector forced “criminals to find alternate means of trying to legitimise their money”, an AFP spokesperson told Australian Conveyancer.

“They can’t just deposit large sums of money into bank accounts and transfer it overseas without attracting the attention of law enforcement and other government agencies.”

On the extent of the problem, the spokesperson described money laundering as “one of the most prevalent crime types for asset confiscation, accounting for more than 30 per cent of all asset restraints made by the (AFP’s) Criminal Assets Confiscation Taskforce”.

Putting the problem in context, the AFP seized $1.1 billion in criminal assets between July 2019 and June 2024, with more than $720 million involving real estate, according to AFP data obtained by this news service.

More than 370 residential and commercial properties were seized over the same period.

“Australia’s strong and liquid property market makes

Laundering money through real estate

1 Illegal funds are obtained through fraud, corruption, etc.

2 Property is purchased with the illegal funds.

it an attractive destination for criminals to both store value and enjoy the fruits of their illicit activity,” the AFP spokesperson said.

“Tranche 2 aims to improve the transparency of the Australian real property sector and bring visibility of suspicious transactions to regulators and the police, thereby reducing its exploitation by money launderers.”

The tougher regime would help protect Australia’s real estate sector, which remained vulnerable to infiltration from high-level organised crime syndicates involved in drug trafficking, cybercrime and human trafficking, according to the federal agency.

At present, the property market could be exploited by money launderers in several ways, including via “complex ownership structures to obfuscate true ownership”, concealing illicit money flows as rental income, and investing illicit cash into property improvement, it said.

“Criminal groups may use professional facilitators – such as real estate agents, accountants, and solicitors – to give illegal cash the appearance of legitimacy through the purchase of assets, such as property,” the AFP spokesperson said.

AUSTRAC, the federal government’s financial intelligence agency, said criminals were exploiting conveyancers to give the appearance of legitimacy to illegal dealings.

The agency, which oversees the country’s money laundering and counter-terrorism financing regime, pointed to a 2023 operation, known as Steelers. It saw more than $47 million seized, including around $43.5 million in real estate - around 60 properties.

3 Property is sold, creating legitimate income.

2017 Commonwealth Bank fined $700m for AML breaches.

2022 Eight properties in the ACT worth $10m were seized during a money laundering investigation.

2023 the AFP seized homes and luxury cars from a Melbourne gang suspected of laundering $223m over three years.

2023 Money launderers suspected of funnelling $10bn had properties, offices and land worth $109m in Sydney seized.

The operation, which hit locations in Melbourne and regional Victoria, was aimed at a large Middle Eastern organised crime syndicate, AUSTRAC said.

“A number of these restrained properties are suspected to be under the effective control of criminals charged with drug trafficking offences, including the suspected syndicate head,” an AUSTRAC spokesperson told Australian Conveyancer.

The agency was confident the new rules, which include a mandate that conveyancers report suspicious matters and cash transactions of $10,000 or more to AUSTRAC, would assist in the nation’s fight against money laundering.

“AUSTRAC and our law enforcement partners know real estate and high-value goods, including precious metals and stones, are attractive to criminals who seek to legitimise the profits from illicit drugs and other criminal activity,” the AUSTRAC spokesperson said.

“The proposed anti-money laundering reforms will equip businesses with the tools to protect themselves against criminal misuse.

“This (new) reporting drives AUSTRAC’s ability to develop actionable financial intelligence that helps law enforcement and other agencies protect the community from social harms.”

The agency said it would take a partnership approach to the looming regulation.

“We look forward to working with conveyancers and building that partnership throughout the development and implementation of the proposed reforms.”

“We’re committed to regulating Tranche 2 entities to prevent further abuse of our financial system. We are also committed to simplifying the regime to make it easier for business.”

Mark Dreyfus

SPECIAL INVESTIGATION

How politicians are driving overdue change

Reforms to Australia’s anti-money laundering and counter-terrorism financing regime are long overdue, politicians say, after years of legislative inaction on the issue.

First proposed 16 years ago, the long-awaited reforms will finally bring Australia into line with global standards adopted by nearly 200 other jurisdictions globally. Alongside Australia, China, Haiti, Madagascar and the US are among the few nations yet to adopt Tranche 2.

The lack of progress has led to Australia’s property sector lagging global peers and becoming an easy target for criminals looking to launder money, according to Australian academics.

The Australian Greens, who were part of a 2022 parliamentary inquiry that looked into Tranche 2, said both the previous coalition government and current Labor government were slow to act, despite “clear recommendations” from inquiries and the Financial Action Task Force, an intergovernmental organisation that fights money laundering.

”The lack of political will and competing priorities have contributed to Australia lagging in implementing these crucial anti-money laundering and counterterrorism financing reforms,” Senator Barbara Pocock, Greens spokesperson on finance, the public service and employment, told Australian Conveyancer

“While the [previous] Coalition government bears significant responsibility for the initial delays, the Labor government has also failed to act with the urgency that this issue demands.

“Labor had an election commitment to implement a register of ultimate beneficial ownership, yet they have not addressed Tranche 2 of the AML-CTF Act.”

It was “deeply concerning and frankly embarrassing”

Australian Greens Senator Barbara Pocock says the lack of political will to address the issue has contributed to the laundering problem.

that Australia was on a list of outlier nations like Haiti and Madagascar in the area, the senator said.

”It underscores the need for urgent action to bring our laws in line with international standards and ensure we are no longer seen as a money laundering haven.”

Attorney-General Mark Dreyfus did not respond to a request for comment but has described the real estate sector as part of a “disturbing but inescapable fact” that Australia is at “serious risk of exploitation by criminals seeking to launder illicit funds”.

PHOTO: LUKAS COCH

“We’re committed to regulating Tranche 2 entities to prevent further abuse of our financial system. We are also committed to simplifying the regime to make it easier for business,” Dreyfus said in a National Press Club address on July 9.

The government urgently needed to modernise the regime to “ensure it keeps pace with the increasingly digital instant nature of our global financial system, closing the gaps that we know increasingly sophisticated professional criminal organisations can exploit,” he told the event in Canberra, speaking alongside AUSTRAC chief executive Brendan Thomas.

While Australia has been slow to act, the government recently committed $166.4 million in budget funds to help educate the professions that fall under the Tranche 2 laws.

Along with real estate agents, lawyers and conveyancers, the new laws will apply to accountants, trust and company service providers, and dealers in some metals and stones.

Anti-corruption group Transparency International Australia said domestic legislators were finally catching up after years of being off the global pace.

Citing its 2024 report into money laundering, the group said regulatory gaps could be allowing millions of dollars of dirty money from Asia to enter Australia’s real estate sector.

For instance, in the case of Cambodia, the group estimates that between 2019 and 2023, 118 properties worth $110 million were settled in Australia by Cambodian nationals, with “the value of money flowing from Cambodia to Australia vastly disproportionate to Cambodia’s wealth”.

“Lawyers, accountants and real estate agents, sometimes unknowingly, enable money laundering by criminals through the setting up of opaque corporate structures, facilitating payments, or simply turning a blind eye,” the group’s chief executive Clancy Moore said.

“We welcome the government’s announcement of new funding in the federal budget to work with these high-risk professions to combat money laundering and terrorism financing.”

Australian Attorney General Mark Dreyfus says the real estate sector is at serious risk of exploittation.

PHOTO: LUKAS COCH

Lawyers: It’s time to clean up the mess

Lawyers and property professionals say they welcome moves to curb tainted cash flowing into real estate, but worry about the industry impact amid a lack of detail on the proposed reforms.

Real Estate Institute of NSW chief executive Tim McKibbin said the potential negative effect of the reforms was a concern, but it was hard to assess given the changes remained unclear.

In May, the federal government announced a second stage of industry consultation on the reforms, following feedback from an initial consultation round in 2023.

“We’ve had the benefit of a presentation from the Attorney-General’s department but that presentation indicated that they were still in consultation,” McKibbin told Australian Conveyancer.

“They are certainly trying to minimise the impost both from an administrative commitment and costs, nonetheless there will still be a significant burden.”

McKibbin said one aspect was clear – property professionals would need to get across a range of new terms that would accompany the extra obligations on the sector.

He pointed to terms such as client due diligence (CDD), verification of identity (VOI), know your client (KYC), anti-money laundering (AML) and counter-

terrorism financing (CTF). “We do know that people will have to comply with all of those obligations and there’s going to be overlap,” he said. “What we are hoping to be able to do is to work with other service providers in the property transaction so there is not a doubling up of costs.”

Even so, he forecast big set-up costs for businesses in getting compliant.

“I am concerned, based on what New Zealand real estate agents have been through,” McKibbin said, referring to the introduction of stricter AML/CTF laws there.

When Tranche 2-style reforms were introduced in New Zealand, they required many real estate agents to hire extra staff, with additional costs said to reach $NZ100,000.

While most mid-size and large businesses in New Zealand were able to cope with the extra costs, some smaller players were hit hard, according to McKibbin.

“Some of the smaller offices over there found the burden too onerous and as a consequence they closed the business or merged with other businesses.”

Lawyers, too, are worried about the burden of the new laws, especially at small firms.

Indeed, the Law Council of Australia, in its submission to an inquiry into the reforms, said it was key

“What we are hoping to be able to do is to work with other service providers in the property transaction so there is not a doubling up of costs.”

Tim McKibbin

that sole practitioners and small practices, particularly in regional and remote areas, were not burdened with excessive AML/CTF obligations.

The small end of town also needed expert support to get its existing risk management practices up to speed with best practice, the legal peak body said.

David Chung, founding director of Brisbane-based Creo Legal, said he was worried about the impact of the changes on small firms.

“The Tranche 2 reforms make sense on paper, but my concern as a boutique law firm principal is the cost and burden of compliance,” Chung told Australian Conveyancer. “Before my firm grew, I was a sole practitioner and any sole practitioner would have a hard time with the additional admin and reporting involved.”

In Chung’s view, it was likely that small firms would “simply stop offering certain services that trigger the Tranche 2 rules” once the tougher laws took effect.

The alternative was for lawyers to charge more for impacted services.

“Our clients ultimately are the ones who bear the cost of the legislative changes,” he said. “Lawyers already use their common sense and notify the authorities of any suspected criminal behaviour. There is no incentive for lawyers to facilitate the crimes of their clients.”

Who’s

who in the AML picture

International, federal and state agencies have roles in Australia’s anti-money laundering and counter-terrorism financing regime. Here are four of the main players:

AUSTRALIAN FEDERAL POLICE

The AFP investigates and prosecutes money laundering that affects the Commonwealth. These crimes are connected with serious and organised crime and can include the illegal drug trade, crime syndicates like mafias, and outlaw motorcycle gangs.

Operation Avarus is the AFP’s antimoney laundering strategy, which guides the work of investigation and intelligence teams. The AFP is headed by Commissioner Reece Kershaw.

AUSTRAC (Australian Transaction Reports and Analysis Centre)

AUSTRAC is Australia’s anti-money laundering and counter-terrorism financing regulator and financial intelligence unit. The federal agency uses financial intelligence and regulation to disrupt money laundering, terrorism financing and other serious crime. The agency is responsible for supervising compliance with anti-money laundering regime requirements and for collecting and analysing financial intelligence.

In the dual roles, AUSTRAC oversees compliance of thousands of Australian businesses and provides intelligence to domestic and international agencies in law enforcement, national security, human services, and revenue. AUSTRAC’s chief executive is Brendan Thomas.

AUSTRALIAN CRIMINAL INTELLIGENCE COMMISSION

The Australian Criminal Intelligence Commission provides intelligence in a bid to combat threats to Australia from transnational serious and organised crime, including from money laundering. It has been involved in joint money laundering operations with state police.

Part of the Attorney-General’s portfolio and a member of the international Five Eyes Law Enforcement Group, the commission analyses and disseminates intelligence information and advice at all levels of government. ACIC’s chief executive is Heather Cook.

FINANCIAL ACTION TASK FORCE

FATF is an inter-government body that sets global standards on anti-money laundering and counter-terrorism financing. Its international standards promote effective implementation of legal, regulatory and operational measures to combat money laundering, terrorist financing and other financial financial threats. FATF President is Mexico’s Elisa de Anda Madrazo.

Reece Kershaw

Brendan Thomas

Heather Cook

DECEMBER 2022

AUSTRAC applies for civil penalty orders against casino SkyCity Adelaide for alleged serious and systemic noncompliance with AML-CTF laws. In June 2024, a court orders SkyCity to pay an $67 million penalty.

MARCH 2022

AUSTRAC applies for civil penalty orders under the AML-CTF Act against casinos Crown Melbourne Ltd and Crown Perth. In July 2023 a court orders Crown to pay an $450 million penalty.

TIMELINE OF DECEPTION,

2023

AFP reportedly arrested seven people in Melbourne and seized $50 million of luxury cars and property from an alleged moneylaundering gang linked to a retail money-transfer firm police claim helped criminals launder almost $223 million in three years.

2023

AFP said it charged nine members of an alleged international money laundering organisation and seized more than 20 properties in Sydney, including commercial buildings in Sydney’s CBD, two houses in Sydney worth more than $19 million, and land near the site of Sydney’s second international airport worth $47 million.

NOVEMBER 2019

AUSTRAC applies for a civil penalty order under the AML-CTF Act against Westpac for serious alleged breaches of the AML-CTF Act. In September 2020, AUSTRAC and Westpac agree in court documents to a proposed civil penalty of $1.3 billion.

AUGUST 2017

AUSTRAC applies for a civil penalty order under the AML-CTF Act against the Commonwealth Bank. In June 2018, a court orders CBA to pay a penalty of $700 million.

AFP said it restrained more than $10 million dollars in assets, including eight ACT properties and four high-end vehicles amid an international money laundering investigation, charging one man based in the ACT as a result.

2019

A Chinese National reportedly purchased six houses in Sydney worth $37 million without living in any of them. He also bought $1.2 billion of hotel, apartment, and retail developments in Sydney and in Queensland.

Police take hold of a luxury Sydney property.

Police seize this prime

CBD Sydney property in King Street.

Biggest challenge in a decade for lawyers

Lawyers involved in conveyancing will need to ask “uncomfortable questions” of their clients under new anti-money laundering measures.

Queensland Law Society chief executive Matt Dunn said the Tranche 2 reform of Australia’s AML legislation was one of the biggest challenges for the profession in a decade.

Under the changes, tens of thousands of property professionals will be required to find out much more about their clients in future – and be prepared to blow the whistle on suspicious investors.

“Compliance with the Tranche 2 anti-money laundering reforms is one of the biggest challenges we have faced in a decade,” he told Australian Conveyancer

Question marks on how soon the measures come into force and the fine details are being worked out, but he acknowledges there will be significant ethical and workload challenges.

“You’ve got to do all sorts of things, including making reports on suspicious matters to the regulator,” he added.

“In the conveyancing space, it will force us to ask a lot more questions about clients and do a lot more KYC due diligence than we’ve ever done – really understanding where the client’s money is coming from.

“Asking lots of questions will be uncomfortable and, in some cases, not met well by clients.

“It is going to be a really big and difficult transition for the profession to make – and it will cost a lot too –because that will be a lot of additional work that will need to be done and it’s got to be paid for somehow.”

Training staff and setting up systems to recognise the

dangers around money laundering threats is just one of the requirements.

“It is really going to take people time, effort and energy to focus on and think about risk assessments and the basic plans,” he said.

“It’s not a case of buying a subscription to an AML service and then suddenly everything you need to do is magically fixed.

“Firms are going to have to turn their minds to transactions and be conscious of what’s going on in the transactions that they’re facilitating – what is suspicious and what isn’t.”

Queensland Law Society chief executive Matt Dunn says reforms will be biggest challenge in a decade for the industry.

PHOTO: DAN PELED

AML risk specialist’s view

Anti-money laundering experts support Australia’s move to bolster laws aimed at curbing the flow of dirty money into real estate, saying collaboration is key to help the sector adjust.

The federal government’s strengthening of financial crime laws has been broadly welcomed by local AML experts, who claim the current regime has become unfit for purpose.

Specifically, they pin some of the blame for highprofile money laundering cases on the cohort of professionals, including conveyancers, that is exempt from the financial crime laws that govern Australian banks and lenders.

Ches Rafferty, the chief executive of digital verification technology company Scantek, is an industry expert who echoes the widely held view that the changes are needed.

“There’s no doubt they (Tranche 2) will have an effect,” Rafferty told Australian Conveyancer. “Obviously the rest of the world has already done this.

“This is already required if you’re in a bank, or financing, or money lending or money transfer, so it’s already being done here in Australia,” he said.

According to Rafferty, claims that stepped-up compliance will hit the property sector hard may be overblown given the experience of sectors already under stricter rules.

He said while “some industries have understandable concerns about how this will impact their day-to-day operations I really don’t think that’s going to be the case”.

“I think that if you have good partners, good

1 Enrolling with AUSTRAC

technology providers that can do the heavy lifting for you … I think that’s really important.

“With that in place, from an actual business perspective it’s not going to be particularly difficult in conveyancing.”

He said another positive was the sector’s existing high level of professionalism, which would likely make the transition easier.

“It’s already an industry of such high standards and professionalism already with the number of checks that need to be conducted,” the Perth-based expert said.

“If there’s any industry that’s already prepared for this it’s probably the conveyancing sector compared to some of the sectors that certainly aren’t at that level currently.

“There are already requirements in the conveyancing sector where most of it is outsourced already to key partners to provide that outcome, I feel this would be the same.”

KordaMentha, the Australian advisory and investment firm, agreed that the federal government’s toughening of AML laws around real estate is overdue.

“This is of particular significance given Australia’s real estate sector is worth three times the Australian stock market and is currently not subject to any AMLCTF obligations,” the firm said in a recent report that examined vulnerabilities in the current regime.

“Effective and pragmatic AML-CTF regulation and supervision of Australia’s real estate sector needs to be initiated.” Lawyers and those in property face these key obligations under the Tranche 2 reforms.

2 Developing an AML-CTF program to mitigate risks. That means developing training programs and having internal controls and risk management practices.

3 Conducting enhanced customer due diligence – akin to the Know Your Customer regime that banks currently abide by.

4 Monitoring customer behaviour and updating their risk rating, including transaction monitoring.

5 Reporting Threshold Transactions (above $10,000) and Suspicious Matters to AUSTRAC.

6 Making and keeping specified records.

Those failing to abide by these incoming rules fines of up to $6 million for individuals and $30 million for companies.

24 • TIME TO CLEAN HOUSE

Attorney General Mark Dreyfus says Australia’s money-laundering laws need an urgent overhaul.

PHOTO: LUKAS COCH

Dirty cash flow into Australia risks global reputation

By DOMINIC GIANNINI, ANDREW BROWN and KAT WONG in Canberra

Asian connections have made Australia a prime target for dirty cash, the regulator warns as the government is chided for failing international standards on countering money laundering and terrorism financing.

Drug trafficking and money laundering were being utilised by “large and highly functional” criminal organisations with one even running an underground bank, AUSTRAC chief executive Brendan Thomas said.

“Australia’s extensive economic relations and trade with Asian markets also provide legitimate financial pathways that can mask illicit transfers,” he told the National Press Club recently.

An “underground bank” that was dismantled by the Australian Federal Police in Australia said it could transfer large amounts of cash anywhere in the world within 24 hours, Mr Thomas said.

“It even set its own exchange rates,” the regulator added.

“The organisation effectively operated as an underground bank with global reach.”

“What this says internationally is that our anti-money laundering systems are on a list alongside Yemen, Democratic Republic of Congo, Syria and South Sudan. That is not where we want our economy to be.”

Australia’s extensive international trade, especially in Asia, was subject to vulnerabilities that could be exploited to launder money, Thomas said.

“Large volumes of global trade flows provide opportunities to obscure individual illicit transactions, especially when combined with foreign exchange transactions or diverse trade financing arrangements,” he said.

“Money laundering enables crime by allowing criminals to profit from their offending.”

Mark Dreyfus

Australia’s general money-laundering laws needed an urgent overhaul to stop illicit funds flooding into the country, Dreyfus said.

Drug traffickers and terrorists are exploiting real estate, banks and casinos to profit from their crimes, he said in a joint address with the regulator.

The address marked the release of AUSTRAC’s national risk assessments that revealed bad actors who use established, legal channels to launder their funds in Australia, such as cash, luxury goods, domestic banks, real estate and casinos.

He was speaking a day after the intergovernmental watchdog Financial Action Task Force gave Australia a zero mark for its oversight of so-called gatekeeper professions.

Gatekeepers are those employed as lawyers, accountants and real estate agents, and other professions known to be used by organised criminal networks to launder cash and finance terrorism.

They are also referred to as Tranche 2 entities.

Australia got a zero score for its compliance with oversight recommendations for gatekeepers, nearly 10 years after being told to comply with the global watchdog’s standards.

Australia is “at risk of being grey-listed by the Financial Action Task Force for failing to meet minimum global standards,” Attorney-General Mark Dreyfus said at the press club event.

Being “grey-listed” is something Australia should definitely avoid, Fiona David, architect of the Global Slavery Index and founder of Fair Futures, told AAP.

Laundering was not a victimless crime with proceeds going back into funding illegal activities including terrorism, Dreyfus said. “Money laundering enables crime by allowing criminals to profit from their offending. This is profit that can then be reinvested to finance future crime.”

More than 240 convictions for money-laundering offences have been recorded by the Commonwealth director of public prosecutions over the past four years, Dreyfus said, without giving earlier figures.

The AFP seized more than $350 million in criminal assets last year, up $214 million from the previous year.

Almost two-thirds of assets were real estate.

One operation by the AFP and Victoria Police resulted in 52 people being charged with money laundering and proceeds of crime offences, seizing more than $47 million in assets, including 60 properties.

A separate investigation led to the seizure of more than 3000 hectares of Tasmanian farmland purchased by Chinese nationals through the proceeds of crime, Dreyfus said.

The coast is also a clear favourite

NSW

While Sydney’s outlying suburbs to the north-west continue their relentless sales surge, it seem property buyers are finding their little pieces of paradise on the central coast, Wyong and the Manning Riverland town of Taree.

e is no denying the appeal of price and Marsden Park, Rouse Hill, entworthville and Penrith.

Transport improvements and affordability keep the city’s fringe locations firmly planted in the top 10.

The convenience of Marsden Park brought the area almost double the sales of second placed Rouse Hill during June. The rush is on and showing no signs of slowing. But savvy buyers in NSW have shifted their gaze away from Central Coast regions.

The Entrance and Wyong, which is just a tad further away from Sydney’s CBD, were also top pics last month. The space, serenity and convenient linkage via the M1 freeway makes it a viable proposition for buyers. An intriguing entry into the sales Top 10 for June was Taree – a few hours up the road from Sydney and not too far north of Newcastle.

For those who don’t know, Taree is a major service centre idyllically located at a point where the Manning River is wide and deep The town is 16 kilometres from the mouth of the Manning River and is surrounded by rich rural farmland where dairying, beef cattle and the timber industry still prosper. Tourism websites describe the town as an ideal place to stop and take a leisurely walk along the river or have a picnic in the riverside parklands.

According to the sales statistics made available to Australian Conveyancer almost 1800 sales in that area landed in June.

Time on Market

The average time a property spends in market before being sold, compared to the same time last year, including advertising.

June 2024

First-home buyer activity

many first-homebuyers entered the market in June 2024, compared to same time last year.

Overseas investment

Residents of which countries invested in the Australian property market for the first time in May 2024.

Marsden Park

Victorian buyers target Tarneit, a suburban gem

VICTORIA

If you’re reading this and live outside of Victoria, you may be forgiven for being familiar with the Melbourne suburb of And this month you ma yourself why.

Tarneit rocketed to the top of the sales charts during June at a time when inner city living in the southern capital seemed to be all the rage Not that Tarneit is a long way from anywhere.

The Melbourne suburb is just 25 kilometres west of the CBD. In June it accounted for 16 per cent of Victorian sales.

So why is it attractive? A little desktop research tells you “it’s a gem” within range of all things Melbourne, and is known for its “beautiful landscapes, a blend of modern and spacious properties, and excellent amenities"

It is touted as having the best of both worlds: space when you need it, the city buzz when you want it. Other Victorian locations offering similar vibes –Hawthorn, Brunswick, and Reservoir rounded out the top 10 of sales in the state last month.

In Queensland,

QUEENSLAND

The push for

buyers north of Brisbane to the suburb of Morayfield. Just as it has done consistently for months, Morayfield drew more home buyers to the area than any other location in Queensland last month. And it wasn’t by just a little bit , by the way. According to Australian Conveyancer sales statistics, the suburb that is nestled 44 kilometres up the road from the sunshine state capital accounted for 23 per cent of sales in Queensland. It’s convenience. It’s space. It’s price. And it continues to shine.

Morayfield is a mostly residential suburb, consisting mainly of low-set brick homes and some semi-rural acreage. The main commercial area is concentrated along Morayfield Road and includes the Morayfield Shopping Centre. The suburb is situated in the Burpengary Creek catchment area.

The outlying areas continue to shine in Queensland when it come to sales, but let’s not neglect to mention the inner-city vibe of Fortitude Valley was the seventhmost-attractive place for buyers in the state last month.

Redcli e

Rockbank

Tarneit

Point Cook

Werribee

Marketing 101

World-renowned management guru Peter Drucker once said the aim of marketing is to know and understand the customer so well, the product or service sells itself.

Marketing makes customers aware of your services, helps your business to engage with, attract and retain customers, and drives profit and growth. In other words, marketing plays an integral role in transforming your business into a success, so it pays to get the basics down pat.

CREATE A PLAN

Creating a marketing plan is one of the most important things you can do for your business, as it helps you identify your target market and how to attract new and existing customers. Mapping this out before designing a website or creating content, will provide a guide on how to reach your target audience.

CREATE A DIGITAL PRESENCE

Building your online presence starts with a website, which should be seen as your digital storefront. It’s often the first thing people see when they search for your business and also your point of contact.

If done well, visitors will naturally convert into customers. Then, consider creating social media pages for your business, like Facebook, LinkedIn and Instagram.

These basic steps will help your brand growing organically.

Once you’ve created your website, research how to maintain and grow its organic search health. Search Engine Optimisation is the best way to do this.

Regular website updates are important because customers want to know you’re providing the market the most current and relevant information.

Your business’s reputation will slowly build if you offer regular website updates and a solution for your target audience.

DIGITAL MARKETING AND ADVERTISING

Also consider paid advertisements through Google or social media. This involves:

• Choosing a headline or message;

• Selecting imagery;

• Selecting your target audience;

• Creating a “call to action” that drives people to a phone number or contact form;

• Allocating a budget and time frame for your ads to run.

Importantly, one unsuccessful campaign ad does not mean they will all fail. Good marketing practice involves re-evaluating performance and direction, to improve or target a different audience next time. For more, visit Google Marketing Platform.