Foundations of Financial Management 15th Edition Block

Full download at:

Solution Manual:

https://testbankpack.com/p/solution-manual-for-foundations-of-financialmanagement-15th-by-block-hirt-danielsen-isbn-00778616129780077861612/

Test bank:

https://testbankpack.com/p/test-bank-for-foundations-of-financialmanagement-15th-by-block-hirt-danielsen-isbn-00778616129780077861612/

Chapter 09

The Time Value of Money

True / False Questions

1. An amount of money to be received in the future is worth less today than the stated amount.

True False

2. Discounting refers to the growth process that turns $1 today into a greater value several periods in the future.

True False

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-1

3. Compounding refers to the growth process that turns $1 today into a greater value several periods in the future.

True False

4. The interest factor for the future value of a single sum is equal to (1 + n)i

True False

5. The time value of money is not a useful concept in determining the value of a bond or in capital investment decisions.

True False

6. If a single amount were put on deposit at a given interest rate and allowed to grow, its future value could be determined by reference to a "future value of $1" table.

True False

7. The time value of money concept is fundamental to the analysis of cash inflow and outflow decisions covering multiple periods of time.

True False

8. The future value is the same concept as the way money grows in a bank account.

True False

9. Cash flow decisions that ignore the time value of money will probably not be as accurate as those decisions that do rely on the time value of money.

True False

10. The present value of a positive future inflow can become negative as discount rates become higher and higher.

True False

11. The interest factor for a future value (FVIF) is equal to (1 + i)n

True False

12. The formula PV = FV(1 + n)i will determine the present value of $1.

True False

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-2

13. In determining the interest factor (IF) for the present value of $1, one could use the reciprocal of that IF for the future value of $1 at the same rate and time period.

True False

14. To determine the current worth of four annual payments of $1,000 at 4%, one would refer to a table for the present value of $1.

True False

15. As the interest rate increases, the interest factor (IF) for the present value of $1 increases.

True False

16. The interest factor for the present value of a single amount is the reciprocal of the future value interest factor.

True False

17. The interest factor for the present value of a single sum is equal to (1 + i)/i.

True False

18. Higher interest rates (discount rates) reduce the present value of amounts to be received in the future.

True False

19. In determining the future value of an ordinary annuity, the final payment is not compounded at all.

True False

20. The future value of an ordinary annuity assumes that the payments are received at the end of the year and that the last payment does not compound.

True False

21. The future value of an annuity table provides a "shortcut" for calculating the future value of a steady stream of payments, denoted as A. The same value can be calculated directly from the following equation:

True False

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-3

22. The present value of an annuity table provides a "shortcut" for calculating the future value of a steady stream of payments, denoted as A. The same value can be calculated directly from the following equation:

True False

23. The amount of annual payments necessary to accumulate a desired total can be found by reference to the present value of an annuity table.

True False

24. If an individual's cost of capital were 6%, the person would prefer to receive $110 at the end of one year rather than $100 right now.

True False

25. In evaluating capital investment projects, current outlays must be judged against the current value of future benefits.

True False

26. The farther into the future any given amount is received, the larger its present value.

True False

27. The interest factor for the future value of an annuity is simply the sum of the interest factors for the future value using the same number of periods.

True False

28. An annuity is a series of consecutive payments of equal amount.

True False

29. Using semi-annual compounding rather than annual compounding will increase the future value of an annuity.

True False

30. When the inflation rate is zero, the present value of $1 is identical to the future value of $1.

True False

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-4

31. The amount of annual payments necessary to repay a mortgage loan can be found by reference to the present value of an annuity table.

True False

32. In paying off a mortgage loan, the amount of the periodic payment that goes toward the reduction of principal increases over the life of the mortgage.

True False

33. The time value of money concept becomes less critical as the prime rate of lending increases.

True False

34. Discounted at 6%, $1,000 received three years from now is worth less than $800 received today.

True False

35. Discounted at 10%, $1,000 received at the end of each year for three years is worth less than $2,700 received today.

True False

36. When adjusting for semi-annual compounding of an annuity, the adjustments include multiplying the periods and annuity payment amount by 2.

True False

37. Calculation of the yield of an investment provides the total return over multiple years.

True False

38. To calculate Future or Present Values of an "Annuity Due," we must assume that payments happen twice as often.

True False

Multiple Choice Questions

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-5

39. Under what conditions must a distinction be made between money to be received today and money to be received in the future?

A. A period of recession

B. When idle money can earn a positive return

C. When there is no risk of nonpayment in the future

D. When current interest rates are different from expected future rates

40. As the compounding rate becomes lower and lower, the future value of inflows approaches

A. 0.

B. the present value of the inflows.

C. infinity.

D. More information is needed.

41. If you invest $10,000 today at 10% interest, how much will you have in 10 years?

A. $13,860

B. $25,940

C. $3,860

D. $80,712

42. In determining the future value of a single amount, one measures

A. the future value of periodic payments at a given interest rate.

B. the present value of an amount discounted at a given interest rate.

C. the future value of an amount allowed to grow at a given interest rate.

D. the present value of periodic payments at a given interest rate.

43. The concept of time value of money is important to financial decision making because

A. it emphasizes earning a return on invested capital.

B. it recognizes that earning a return makes $1 worth more today than $1 received in the future.

C. it can be applied to future cash flows in order to compare different streams of income.

D. All of these options

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-6

44. As the discount rate becomes higher and higher, the present value of inflows approaches

A. 0.

B. minus infinity.

C. plus infinity.

D. More information is needed.

45. How much must you invest at 8% interest in order to see your investment grow to $8,000 in 10 years?

A. $3,070

B. $3,704

C. $3,105

D. None of these options

46. An annuity may best be defined as

A. a payment at a fixed interest rate.

B. a series of payments of unequal amount.

C. a series of yearly payments, regardless of amount.

D. a series of consecutive payments of equal amounts.

47. You are to receive $12,000 at the end of five years. The available yield on investments is 6%. Which table would you use to determine the value of that sum today?

A. Present value of an annuity of $1

B. Future value of an annuity of $1

C. Present value of $1

D. Future value of $1

48. As the interest rate increases, the present value of an amount to be received at the end of a fixed period

A. increases.

B. decreases.

C. remains the same.

D. Not enough information is given to tell.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-7

49. As the time period until receipt increases, the present value of an amount at a fixed interest rate

A. decreases.

B. remains the same.

C. increases.

D. Not enough information is given to tell.

50. To find the yield on investment that requires the payment of a single amount initially, and which then return a single amount some time in the future, the most efficient table one could use is

A. the present value of $1.

B. the future value of an annuity of $1.

C. present value of an annuity of $1.

D. None of these

51. Ali Shah sets aside $2,000 each year for five years. He then withdraws the funds on an equal annual basis for the next four years. If Ali wishes to determine the amount of the annuity to be withdrawn in years 6 through 9, he should use the following two tables in this order:

A. present value of an annuity of $1; future value of an annuity of $1

B. future value of an annuity of $1; present value of an annuity of $1

C. future value of an annuity of $1; present value of $1

D. future value of an annuity of $1; future value of $1

52. To save for her newborn son's college education, Lea Wilson will invest $1,000 at the beginning of each year for the next 18 years. The interest rate is 12%. What is the future value?

A. $7,690

B. $34,931

C. $63,440

D. $62,440

53. If you were to put $1,000 in the bank at 6% interest each year for the next 10 years, which table would you use to find the ending balance in your account?

A. Present value of $1

B. Future value of $1

C. Present value of an annuity of $1

D. Future value of an annuity of $1

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-8

54. The interest factor (IF) for the future value of an ordinary annuity is 4.641 at 10% for four years. If we wish to accumulate $8,000 by the end of four years, how much should the annual payments be?

A. $2,500

B. $2,000

C. $1,724

D. None of these options

55. Mr. Blochirt is creating a college investment fund for his daughter. He will put in $1,000 per year for the next 15 years beginning one year from now and expects to earn a 6% annual rate of return. How much money will his daughter have when she starts college?

A. $11,250

B. $12,263

C. $24,003

D. $23,276

56. Mr. Nailor invests $5,000 in a money market account at his local bank. He receives annual interest of 8% for seven years. How much total return will his investment earn during this time period?

A. $2,915

B. $3,570

C. $6,254

D. $8,570

57. Lou Lewis borrows $10,000 to be repaid over 10 years at 9%. Repayment of principal in the first year is ______.

A. $1,558

B. $658

C. $742

D. $885

58. Sharon Smith will receive $1 million in 50 years. The discount rate is 14%. As an alternative, she can receive $1,000 today. Which should she choose?

A. The $1 million dollars in 50 years.

B. $2,000 today.

C. She should be indifferent between the two choices.

D. More information is needed.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-9

59. Pedro Gonzalez will invest $5,000 at the beginning of each year for the next nine years. The interest rate is 8%. What is the future value?

A. $58,471

B. $62,440

C. $67,435

D. $72,435

60. Ambrin Corp. expects to receive $2,000 per year for 10 years starting one year from now, and $3,500 per year for the next 10 years at the end of each year. What is the approximate present value of this 20-year cash flow? Use an 11% discount rate.

A. $19,034

B. $27,870

C. $32,389

D. None of these options

61. Dr. J. wants to buy a Dell computer that will cost $3,000 three years from today. He would like to set aside an equal amount at the end of each year in order to accumulate the amount needed. He can earn an 8% annual return. How much should he set aside beginning a year from now?

A. $879

B. $627

C. $924

D. $1,243

62. Mr. Fish wants to build a house in eight years. He estimates that the total cost will be $150,000. If he can put aside $10,000 at the end of each year, what rate of return must he earn in order to have the amount needed?

A. Between 17% and 18%

B. Between 15% and 16%

C. 12%

D. None of these options

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-10

63. Babe Ruth Jr. has agreed to play for the Cleveland Indians for $3 million per year for the next 10 years. What table would you use to calculate the value of this contract in today's dollars?

A. Present value of an annuity

B. Present value of a single amount

C. Future value of an annuity

D. None of these options

64. Football player Walter Johnson signs a contract calling for payments of $250,000 per year, to begin 10 years from now and then continue for five more years. To find the present value of this contract, which table or tables should you use?

A. The future value of $1

B. The future value of an annuity of $1 and the future value of $1

C. The present value of an annuity of $1 and the present value of $1

D. None of these options

65. Mike Carlson will receive $12,000 a year from the end of the third year to the end of the 12th year (10 payments). The discount rate is 10%. The present value today of this deferred annuity is ______.

A. $61,450

B. $42,185

C. $55,379

D. $60,909

66. The shorter the length of time between a present value and its corresponding future value,

A. the lower the present value, relative to the future value.

B. the higher the present value, relative to the future value.

C. the higher the interest rate used in the discounting to the present value.

D. None of these options

67. A dollar today is worth more than a dollar to be received in the future because

A. a stated rate of return is guaranteed on all investment opportunities.

B. the dollar can be invested today and earn interest.

C. inflation will increase the purchasing power of a future dollar.

D. None of these options

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-11

68. The higher the interest rate used in determining the future value of a $1 annuity,

A. the smaller the future value at the end of the period.

B. the greater the future value at the end of a period.

C. the greater the present value at the beginning of a period.

D. None of these options. The interest has no effect on the future value of an annuity.

69. Mr. Darden is selling his house for $200,000. He bought it for $164,000 10 years ago. What is the annual return on his investment?

A. 2%

B. Between 3% and 5%

C. 10%

D. None of these options

70. Increasing the number of periods will increase all of the following except

A. the present value of an annuity.

B. the present value of $1.

C. the future value of $1.

D. the future value of an annuity.

71. Joe Nautilus has $210,000 and wants to retire. What approximate return must his money earn so he may receive annual benefits of $30,000 for the next 10 years?

A. 12%

B. Between 12% and 13%

C. About 7%

D. Greater than 15%

72. You will deposit $2,000 today. It will grow for six years at 10% interest compounded semiannually. You will then withdraw the funds annually over the next four years at the end of each year. The annual interest rate is 8%. Your annual withdrawal will be approximately ______.

A. $2,340

B. $4,332

C. $797

D. $1,085

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-12

73. Carol Thomas will pay out $6,000 at the end of year 2, $8,000 at the end of year 3, and receive $10,000 at the end of year 4. With an interest rate of 13%, what is the net value of the payments versus receipts in today's dollars?

A. $7,326

B. $10,242

C. $16,372

D. $4,112

74. John Doeber borrowed $150,000 to buy a house. His loan cost was 6% and he promised to repay the loan in 15 equal annual payments. How much are the annual payments?

A. $3,633

B. $9,250

C. $13,113

D. $15,445

75. John Doeber borrowed $150,000 to buy a house. His loan cost was 6% and he promised to repay the loan in 15 equal annual payments. What is the principal outstanding after the first loan payment?

A. $143,555

B. $134,560

C. $141,200

D. None of these options

76. A home buyer signed a 20-year, 8% mortgage for $72,500. Given the following information, how much should the annual loan payments be?

Present value of $1 PVIF = .215

Future value of $1 FVIF = 4.661

Present value of annuity PVIFA = 9.818

Future value of annuity FVIFA = 45.762

A. $1,584

B. $7,384

C. $15,555

D. $15,588

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-13

77. A retirement plan guarantees to pay to you or your estate a fixed amount for 20 years. At the time of retirement, you will have $73,425 to your credit in the plan. The plan anticipates earning 9% interest. Given the following information, how much will your annual benefits be?

Present value of $1 PVIF = .178

Future value of $1 FVIF = 5.604

Present value of annuity PVIFA = 9.129

Future value of annuity FVIFA = 51.16

A. $1,435

B. $13,070

C. $8,043

D. $13,102

78. After 10 years, 100 shares of stock originally purchased for $500 were sold for $900. What was the yield on the investment? Choose the closest answer.

A. 19%

B. 2.5%

C. 8.5%

D. 6%

79. Dr. Stein has just invested $10,000 for his son (age 7). The money will be used for his son's education 15 years from now. He calculates that he will need $100,000 for his son's education by the time the boy goes to school. What rate of return will Dr. Stein need to achieve this goal?

A. Between 9% and 10%

B. Between 16% and 17%

C. Between 10% and 11%

D. Between 15% and 16%

80. The future value of a $500 investment today at 10% annual interest compounded semiannually for five years is ______.

A. $805

B. $814

C. $750

D. $923

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-14

81. Dan would like to save $1,500,000 by the time he retires in 25 years and believes he can earn an annual return of 8%. How much does he need to invest in each of the following years to achieve his goal?

A. $20,518

B. $40,850

C. $18,900

D. $58,000

E. $25,304

82. Sydney saved $10,000 during her first year of work after college and plans to invest it for her retirement in 40 years. How much will she have available for retirement if she can make 8% on her investment?

A. $596,250

B. $453,000

C. $345,100

D. $217,250

83. Luke believes that he can invest $5,000 per year for his retirement in 30 years. How much will he have available for retirement if he can earn 8% on his investment and begins investing one year from now?

A. $566,400

B. $681,550

C. $150,000

D. $162,000

84. Ian would like to save $2,000,000 by the time he retires in 40 years. If he believes that he can achieve a 7% rate of return, how much does he need to deposit each year, starting one year from now, to achieve his goal?

A. $12,065

B. $37,500

C. $5,790

D. $10,018

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-15

85. Jeff believes he will need a $60,000 annual income during retirement. If he can achieve a 6% return during retirement and believes he will live 20 years after retirement, how much does he need to save by the time he retires, assuming he'll start drawing his money out one year after his retirement?

A. $724,055

B. $1,600,000

C $688,200

D. $209,320

86. If Allison has saved $1,000,000 upon retirement, how much can she live on each year if she can earn 6% per year and will end with $0 when she expects to die 25 years after retirement?

A. $295,334

B. $20,953

C. $70,952

D. $78,229

87. Kathy has $50,000 to invest today and would like to determine whether it is realistic for her to achieve her goal of buying a home for $150,000 in 10 years with this investment. What return must she achieve in order to buy her home in 10 years?

A. About 12%

B. About 13%

C. About 9%

D. About 10%

88. If Gerry makes a deposit of $1,500 at the end of each quarter for five years, how much will he have at the end of the five years assuming a 12% annual return and quarterly compounding?

A. $40,305

B. $30,000

C. $108,078

D. $161,220

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-16

89. Sara would like to evaluate the performance of her portfolio over the past 10 years. What compound annual rate of return has she achieved if she invested $12,000 10 years ago and now has $25,000?

A. Between 8% and 9%

B. Between 10% and 11%

C. Between 9% and 10%

D. Between 7% and 8%

Matching Questions

90. Match the following with the items below:

1. yield

2. discount rate

3. annuity

4. future value of an annuity

5. future value

6. semi-annual compounding

7. interest factor (IF)

8. present value

Essay Questions

The payment of an equal stream of cash into a fund that increases in size (depending on the interest rate received) up to a future point in time.

The interest or return is accumulated every six months.

The discounted value of a future sum or annuity as of today's value.

A series of consecutive payments or receipts of an equal amount.

The percentage rate at which future sums or annuities are brought back to their present value.

The future value of a single amount or annuity when compounded at a given interest rate for a specified period of time.

It is based on the number of periods (n) and the interest rate (i) and whether or not there is more than one cash flow.

The interest rate that equates a future value of an annuity to a given present value.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-17

91. You have an opportunity to buy a $1,000 bond that matures in 10 years. The bond pays $30 every six months. The current market interest rate for similar bonds is 8%. What is the most you would be willing to pay for this bond?

92. In January, 2000, Harold Black bought 100 shares of Country Homes for $37.50 per share. He sold them in January 2010 for a total of $9,715.02. Calculate Harold's approximate annual rate of return.

93. Samuel Johnson invested in gold U.S. coins 10 years ago, paying $216.53 for one-ounce gold "double eagle" coins. He could sell these coins for $734 today. What was his annual rate of return for this investment?

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-18

94. Gary Kiraly wants to buy a new Italian sports car in three years. The vehicle is expected to cost $80,000 at that time. If Gary should be so lucky as to find an investment yielding 12% over that three-year period, how much would he have to invest now in order to accumulate $80,000 at the end of the three years?

95. Mr. Sullivan is borrowing $2 million to expand his business. The loan will be for 10 years at 12% and will be repaid in equal quarterly installments. What will the quarterly payments be?

96. Marcia Stubern is planning for her golden years. She will retire in 20 years, at which time she plans to begin withdrawing $60,000 annually. She is expected to live for 20 years following her retirement. Her financial advisor thinks she can earn 9% annually. How much does she need to invest at the end of each year before she retires, to prepare for her financial needs after her retirement?

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-19

97. Sara Shouppe has invested $100,000 in an account at her local bank. The bank will pay her a constant amount each year for six years, starting one year from today, and the account's balance will be 0 at the end of the sixth year. If the bank has promised Ms. Shouppe a 10% return, how much will they have to pay her each year?

98. Kimberly Ford invested $10,000 10 years ago at 16%, compounded quarterly. How much has she accumulated?

99. Sponge Bob will receive a payment of $5,000 per year for seven years beginning three years from today. At a discount rate of 9%, what is the present value of this deferred annuity?

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-20

Chapter 09 The Time Value of Money Answer Key

True / False Questions

1. An amount of money to be received in the future is worth less today than the stated amount.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Basic Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

2. Discounting refers to the growth process that turns $1 today into a greater value several periods in the future.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

3. Compounding refers to the growth process that turns $1 today into a greater value several periods in the future.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

4. The interest factor for the future value of a single sum is equal to (1 + n)i

FALSE

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-21

5. The time value of money is not a useful concept in determining the value of a bond or in capital investment decisions.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

6. If a single amount were put on deposit at a given interest rate and allowed to grow, its future value could be determined by reference to a "future value of $1" table.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

7. The time value of money concept is fundamental to the analysis of cash inflow and outflow decisions covering multiple periods of time.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

8. The future value is the same concept as the way money grows in a bank account.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

9. Cash flow decisions that ignore the time value of money will probably not be as accurate as those decisions that do rely on the time value of money.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

9-22

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

10. The present value of a positive future inflow can become negative as discount rates become higher and higher.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

11. The interest factor for a future value (FVIF) is equal to (1 + i)n

TRUE

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

12. The formula PV = FV(1 + n)i will determine the present value of $1.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

13. In determining the interest factor (IF) for the present value of $1, one could use the reciprocal of that IF for the future value of $1 at the same rate and time period. TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

14. To determine the current worth of four annual payments of $1,000 at 4%, one would refer to a table for the present value of $1.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-03 The present value is based on the current value of funds to be received

15. As the interest rate increases, the interest factor (IF) for the present value of $1 increases.

FALSE

AACSB: Analytic

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-23

Blooms: Understand

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

16. The interest factor for the present value of a single amount is the reciprocal of the future value interest factor.

TRUE

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

17. The interest factor for the present value of a single sum is equal to (1 + i)/i.

FALSE

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

18. Higher interest rates (discount rates) reduce the present value of amounts to be received in the future.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate Learning Objective: 09-03 The present value is based on the current value of funds to be received.

19. In determining the future value of an ordinary annuity, the final payment is not compounded at all.

TRUE

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

20. The future value of an ordinary annuity assumes that the payments are received at the end of the year and that the last payment does not compound.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

9-24

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

21. The future value of an annuity table provides a "shortcut" for calculating the future value of a steady stream of payments, denoted as A. The same value can be calculated directly from the following equation: FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

22. The present value of an annuity table provides a "shortcut" for calculating the future value of a steady stream of payments, denoted as A. The same value can be calculated directly from the following equation:

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

23. The amount of annual payments necessary to accumulate a desired total can be found by reference to the present value of an annuity table. FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

24. If an individual's cost of capital were 6%, the person would prefer to receive $110 at the end of one year rather than $100 right now. TRUE

PV = FV × PVIF (App. B: 6%, 1 period) = $110 × 0.943 = $104

AACSB: Analytic

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-25

TRUE

Blooms: Apply

Difficulty: Basic

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

25. In evaluating capital investment projects, current outlays must be judged against the current value of future benefits. TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

26. The farther into the future any given amount is received, the larger its present value. FALSE

Time amplifies the growth of money. Consequently, to achieve a certain future value, more time means that you can start with less.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

27. The interest factor for the future value of an annuity is simply the sum of the interest factors for the future value using the same number of periods.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

28. An annuity is a series of consecutive payments of equal amount. TRUE

If even ONE of a stream of payments is not the same, we cannot use the "shortcut" of annuity tables and calculations.

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

9-26

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

29. Using semi-annual compounding rather than annual compounding will increase the future value of an annuity.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-05 Compounding or discounting may take place on a less than annual basis such as semi-annually or monthly.

30. When the inflation rate is zero, the present value of $1 is identical to the future value of $1.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Challenge

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

31. The amount of annual payments necessary to repay a mortgage loan can be found by reference to the present value of an annuity table.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

32. In paying off a mortgage loan, the amount of the periodic payment that goes toward the reduction of principal increases over the life of the mortgage.

TRUE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

33. The time value of money concept becomes less critical as the prime rate of lending increases.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-27

34. Discounted at 6%, $1,000 received three years from now is worth less than $800 received today.

FALSE

PV = FV × PVIF (App. B: 3 periods, 6%) = $1,000 × .840 = $840

AACSB: Analytic Blooms: Apply

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

35. Discounted at 10%, $1,000 received at the end of each year for three years is worth less than $2,700 received today.

TRUE

PVA = A × PVIFA (App. D: 3 periods, 10%) = $1,000 × 2.487 = $2,487

AACSB: Analytic Blooms: Apply

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

36. When adjusting for semi-annual compounding of an annuity, the adjustments include multiplying the periods and annuity payment amount by 2.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-05 Compounding or discounting may take place on a less than annual basis such as semi-annually or monthly.

37. Calculation of the yield of an investment provides the total return over multiple years.

FALSE

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

9-28

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

38. To calculate Future or Present Values of an "Annuity Due," we must assume that payments happen twice as often.

FALSE

Annuities Due simply move TVM calculations back to the beginning of a year, rather than the end.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Multiple Choice Questions

39. Under what conditions must a distinction be made between money to be received today and money to be received in the future?

A. A period of recession

B. When idle money can earn a positive return

C. When there is no risk of nonpayment in the future

D. When current interest rates are different from expected future rates

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

40. As the compounding rate becomes lower and lower, the future value of inflows approaches

A. 0.

B. the present value of the inflows.

C. infinity.

D. More information is needed.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-29

41. If you invest $10,000 today at 10% interest, how much will you have in 10 years?

A. $13,860

B. $25,940

C. $3,860

D. $80,712

FV = PV × FVIF (App. A: 10%, 10 years) = $10,000 × 2.594 = $25,940

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

42. In determining the future value of a single amount, one measures

A. the future value of periodic payments at a given interest rate.

B. the present value of an amount discounted at a given interest rate.

C. the future value of an amount allowed to grow at a given interest rate.

D. the present value of periodic payments at a given interest rate.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

43. The concept of time value of money is important to financial decision making because

A. it emphasizes earning a return on invested capital.

B. it recognizes that earning a return makes $1 worth more today than $1 received in the future.

C. it can be applied to future cash flows in order to compare different streams of income.

D. All of these options

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-30

44. As the discount rate becomes higher and higher, the present value of inflows approaches

A. 0.

B. minus infinity.

C. plus infinity.

D. More information is needed.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate Learning Objective: 09-03 The present value is based on the current value of funds to be received.

45. How much must you invest at 8% interest in order to see your investment grow to $8,000 in 10 years?

A. $3,070

B. $3,704

C. $3,105

D. None of these options

PV = A × PVIF (App. B: 8%, 10 periods) = $8,000 × 0.463 = $3,704

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate Learning Objective: 09-03 The present value is based on the current value of funds to be received.

46. An annuity may best be defined as

A. a payment at a fixed interest rate.

B. a series of payments of unequal amount.

C. a series of yearly payments, regardless of amount.

D. a series of consecutive payments of equal amounts.

AACSB: Reflective Thinking Blooms: Remember

Difficulty: Basic

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-31

47. You are to receive $12,000 at the end of five years. The available yield on investments is 6%. Which table would you use to determine the value of that sum today?

A. Present value of an annuity of $1

B. Future value of an annuity of $1

C. Present value of $1

D. Future value of $1

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

48. As the interest rate increases, the present value of an amount to be received at the end of a fixed period

A. increases.

B. decreases.

C. remains the same.

D. Not enough information is given to tell.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

49. As the time period until receipt increases, the present value of an amount at a fixed interest rate

A. decreases.

B. remains the same.

C. increases.

D. Not enough information is given to tell.

AACSB: Analytic Blooms: Understand

Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-32

50. To find the yield on investment that requires the payment of a single amount initially, and which then return a single amount some time in the future, the most efficient table one could use is

A. the present value of $1.

B. the future value of an annuity of $1.

C. present value of an annuity of $1.

D. None of these

AACSB: Analytic Blooms: Understand

Difficulty: Challenge

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

51. Ali Shah sets aside $2,000 each year for five years. He then withdraws the funds on an equal annual basis for the next four years. If Ali wishes to determine the amount of the annuity to be withdrawn in years 6 through 9, he should use the following two tables in this order:

A. present value of an annuity of $1; future value of an annuity of $1

B. future value of an annuity of $1; present value of an annuity of $1

C. future value of an annuity of $1; present value of $1

D. future value of an annuity of $1; future value of $1

AACSB: Analytic Blooms: Understand

Difficulty: Challenge

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

52. To save for her newborn son's college education, Lea Wilson will invest $1,000 at the beginning of each year for the next 18 years. The interest rate is 12%. What is the future value?

A. $7,690

B. $34,931

C. $63,440

D. $62,440

FVA = A × FVIFA (App. C: 12%, 18 + 1 = 19 periods) = $1,000 × (63.440 - 1) = $62,440

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

9-33

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

53. If you were to put $1,000 in the bank at 6% interest each year for the next 10 years, which table would you use to find the ending balance in your account?

A. Present value of $1

B. Future value of $1

C. Present value of an annuity of $1

D. Future value of an annuity of $1

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

54. The interest factor (IF) for the future value of an ordinary annuity is 4.641 at 10% for four years. If we wish to accumulate $8,000 by the end of four years, how much should the annual payments be?

A. $2,500

B. $2,000

C. $1,724

D. None of these options (App. C: 10%, 4 periods)

A = $1,724

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

9-34

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

55. Mr. Blochirt is creating a college investment fund for his daughter. He will put in $1,000 per year for the next 15 years beginning one year from now and expects to earn a 6% annual rate of return. How much money will his daughter have when she starts college?

A. $11,250

B. $12,263

C. $24,003

D. $23,276

FVA = A × FVIFA (App. C: 6%, 15 periods) = $1,000 × 23.276 = $23,276

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

56. Mr. Nailor invests $5,000 in a money market account at his local bank. He receives annual interest of 8% for seven years. How much total return will his investment earn during this time period?

A. $2,915

B. $3,570

C. $6,254

D. $8,570

FV = PV × FVIF (App. A: 8%, 7 periods) = $5,000 × 1.714 = $8,570

$8,570 - Initial investment of $5,000 = $3,570

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

9-35

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

57. Lou Lewis borrows $10,000 to be repaid over 10 years at 9%. Repayment of principal in the first year is ______.

A. $1,558

B. $658

C. $742

D. $885 (App. D: 9%, 10 periods)

A = $1,558 annual payment less interest in year 1 ($10,000 × 9%) = $658

AACSB: Analytic Blooms: Apply Difficulty: Challenge

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

58. Sharon Smith will receive $1 million in 50 years. The discount rate is 14%. As an alternative, she can receive $1,000 today. Which should she choose?

A. The $1 million dollars in 50 years.

B. $2,000 today.

C. She should be indifferent between the two choices.

D. More information is needed.

PV = FV × PVIF (App. B: 14%, 50 periods) = $1,000,000 × 0.001 = $1,000

AACSB: Analytic Blooms: Apply Difficulty: Basic Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-36

59. Pedro Gonzalez will invest $5,000 at the beginning of each year for the next nine years. The interest rate is 8%. What is the future value?

A. $58,471

B. $62,440

C. $67,435

D. $72,435

FVA = A × FVIFA (App. C: 8%, 9 + 1 = 10 periods) = $5,000 × (14.487 - 1) = $67,435

AACSB: Analytic Blooms: Apply

Difficulty: Challenge

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

60. Ambrin Corp. expects to receive $2,000 per year for 10 years starting one year from now, and $3,500 per year for the next 10 years at the end of each year. What is the approximate present value of this 20-year cash flow? Use an 11% discount rate.

A. $19,034

B. $27,870

C. $32,389

D. None of these options

PVA = A × PVIFA (App. D: 11%, 10 periods) = $2,000 × 5.889 = $11,778

PVA = A × PVIFA (App. D: 11%, 10 periods)

= $3,500 × 5.889 = $20,612 × PVIF (App. B: 11%, 10 periods)

PVIF = $20,612 × (.352) = $7,255

$11,778 + $7,255 = $19,034 OR

PVIFA(11%, 20 periods) minus PVIFA (11%, 10 periods) = PVIFA years 11 through 20

7.963 - 5.889 = 2.074 × $3,500 = $7,259

PLUS PVIFA (11%, 10 periods) 5.889 × $2,000 = $11,778

TOTAL of present values of both cash streams: $11,778 + $7,259 = $19,037 (some rounding)

AACSB: Analytic Blooms: Apply

Difficulty: Challenge Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-37

61. Dr. J. wants to buy a Dell computer that will cost $3,000 three years from today. He would like to set aside an equal amount at the end of each year in order to accumulate the amount needed. He can earn an 8% annual return. How much should he set aside beginning a year from now?

A. $879

B. $627

C. $924

D. $1,243 (App. C: 8%, 3 periods)

A = $924

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

62. Mr. Fish wants to build a house in eight years. He estimates that the total cost will be $150,000. If he can put aside $10,000 at the end of each year, what rate of return must he earn in order to have the amount needed?

A. Between 17% and 18%

B. Between 15% and 16%

C. 12%

D. None of these options

FVIFA = FVA (App. C: 8 periods)/A

FVIFA = $150,000/10,000 = 15.0 Rate of return = approx. 17.5%

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-38

63. Babe Ruth Jr. has agreed to play for the Cleveland Indians for $3 million per year for the next 10 years. What table would you use to calculate the value of this contract in today's dollars?

A. Present value of an annuity

B. Present value of a single amount

C. Future value of an annuity

D. None of these options

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

64. Football player Walter Johnson signs a contract calling for payments of $250,000 per year, to begin 10 years from now and then continue for five more years. To find the present value of this contract, which table or tables should you use?

A. The future value of $1

B. The future value of an annuity of $1 and the future value of $1

C. The present value of an annuity of $1 and the present value of $1

D. None of these options

AACSB: Analytic Blooms: Understand

Difficulty: Challenge

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

65. Mike Carlson will receive $12,000 a year from the end of the third year to the end of the 12th year (10 payments). The discount rate is 10%. The present value today of this deferred annuity is ______.

A. $61,450

B. $42,185

C. $55,379

D. $60,909

PVA = A × PVIFA (App. D: 10%, 10 periods)

= $12,000 × 6.145 = $73,740

PV = FV × PVIF (App. B: 10%, 2 periods)

= $73,740 × .826 = $60,909

AACSB: Analytic Blooms: Apply

Difficulty: Challenge

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

9-39

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

66. The shorter the length of time between a present value and its corresponding future value,

A. the lower the present value, relative to the future value.

B. the higher the present value, relative to the future value.

C. the higher the interest rate used in the discounting to the present value.

D. None of these options

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

67. A dollar today is worth more than a dollar to be received in the future because

A. a stated rate of return is guaranteed on all investment opportunities.

B. the dollar can be invested today and earn interest.

C. inflation will increase the purchasing power of a future dollar.

D. None of these options

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-01 Money has a time value associated with it; therefore; a dollar received today is worth more than a dollar received in the future.

68. The higher the interest rate used in determining the future value of a $1 annuity,

A. the smaller the future value at the end of the period.

B. the greater the future value at the end of a period.

C. the greater the present value at the beginning of a period.

D. None of these options. The interest has no effect on the future value of an annuity.

AACSB: Analytic Blooms: Understand

Difficulty: Basic

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

9-40

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

69. Mr. Darden is selling his house for $200,000. He bought it for $164,000 10 years ago. What is the annual return on his investment?

A. 2%

B. Between 3% and 5%

C. 10%

D. None of these options

PVIF = PV (App. B: 10 periods)/FV = $164,000/$200,000 = 0.82; Return = 2%

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

70. Increasing the number of periods will increase all of the following except

A. the present value of an annuity.

B. the present value of $1.

C. the future value of $1.

D. the future value of an annuity.

AACSB: Analytic Blooms: Understand

Difficulty: Intermediate

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

71. Joe Nautilus has $210,000 and wants to retire. What approximate return must his money earn so he may receive annual benefits of $30,000 for the next 10 years?

A. 12%

B. Between 12% and 13%

C. About 7%

D. Greater than 15%

PVIFA = PVA (App. D: 10 periods)/A = $210,000/$30,000 = 7.0; Return = 7%

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-41

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

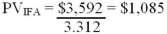

72. You will deposit $2,000 today. It will grow for six years at 10% interest compounded semiannually. You will then withdraw the funds annually over the next four years at the end of each year. The annual interest rate is 8%. Your annual withdrawal will be approximately ______.

A. $2,340

B. $4,332

C. $797

D. $1,085

FV = PV × FVIF (App. A: 5%, 12 periods)

= $2,000 × 1.796 = $3,592

A = PVA (App. D: 8%, 4 periods)

AACSB: Analytic Blooms: Apply

Difficulty: Challenge

Learning Objective: 09-02 The future value is based on the number of periods over which the funds are to be compounded at a given interest rate.

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

73. Carol Thomas will pay out $6,000 at the end of year 2, $8,000 at the end of year 3, and receive $10,000 at the end of year 4. With an interest rate of 13%, what is the net value of the payments versus receipts in today's dollars?

A. $7,326

B. $10,242

C. $16,372

D. $4,112

PV = FV × PVIF (App. B: 13%, 2 periods)

= $6,000 × .783 = $4,698

PV = FV × PVIF (App. B: 13%, 3 periods)

= $8,000 × .693 = $5,544

PV = FV × PVIF (App. B: 13%, 4 periods)

= $10,000 × .613 = $6,130

Net Value of Payments = ($4,698) + ($5,544) + $6,130 = $4,112

AACSB: Analytic Blooms: Apply

Difficulty: Challenge

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-42

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

74. John Doeber borrowed $150,000 to buy a house. His loan cost was 6% and he promised to repay the loan in 15 equal annual payments. How much are the annual payments?

A $3,633

B. $9,250

C. $13,113

D. $15,445

PVA = A × PVIFA (App. D: 6%, 15 periods)

A = PVA/PVIFA = $150,000/9.712 = $15,445

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

75. John Doeber borrowed $150,000 to buy a house. His loan cost was 6% and he promised to repay the loan in 15 equal annual payments. What is the principal outstanding after the first loan payment?

A. $143,555

B. $134,560

C. $141,200

D. None of these options

PVA = A × PVIFA (App. D: 6%, 15 periods)

= $150,000/9.712 = $15,445

Annual Payment - Interest = Amount to be applied to principal

$15,445 - (.06 × $150,000) = $6,445

Outstanding principal at end of year 1 = Loan - Payment to principal

= $150,000 - $6,445 = $143,555

AACSB: Analytic Blooms: Apply Difficulty: Challenge

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

9-43

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

76. A home buyer signed a 20-year, 8% mortgage for $72,500. Given the following information, how much should the annual loan payments be?

Present value of $1 PVIF = .215

Future value of $1 FVIF = 4.661

Present value of annuity PVIFA = 9.818

Future value of annuity FVIFA = 45.762

A. $1,584

B. $7,384

C. $15,555

D. $15,588

$72,500/9.818 = $7,384.

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

77. A retirement plan guarantees to pay to you or your estate a fixed amount for 20 years. At the time of retirement, you will have $73,425 to your credit in the plan. The plan anticipates earning 9% interest. Given the following information, how much will your annual benefits be?

Present value of $1 PVIF = .178

Future value of $1 FVIF = 5.604

Present value of annuity PVIFA = 9.129

Future value of annuity FVIFA = 51.16

A. $1,435

B. $13,070

C. $8,043

D. $13,102

$73,425/9.129 = $8,043.

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-03 The present value is based on the current value of funds to be received.

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

9-44

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

78. After 10 years, 100 shares of stock originally purchased for $500 were sold for $900. What was the yield on the investment? Choose the closest answer.

A. 19%

B. 2.5%

C. 8.5%

D. 6%

PVIF = PV/FV (App. B: 10 periods) = $500/$900 = 0.555 Yield = approx 6%

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

79. Dr. Stein has just invested $10,000 for his son (age 7). The money will be used for his son's education 15 years from now. He calculates that he will need $100,000 for his son's education by the time the boy goes to school. What rate of return will Dr. Stein need to achieve this goal?

A. Between 9% and 10%

B. Between 16% and 17%

C. Between 10% and 11%

D. Between 15% and 16%

PVIF = PV/FV (App. B: 15 periods) = $10,000/$100,000 = 0.10 Return: between 16% and 17%

AACSB: Analytic Blooms: Apply

Difficulty: Intermediate

Learning Objective: 09-04 Not only can future value and present value be computed; but other factors such as yield (rate of return) can be determined as well.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

9-45