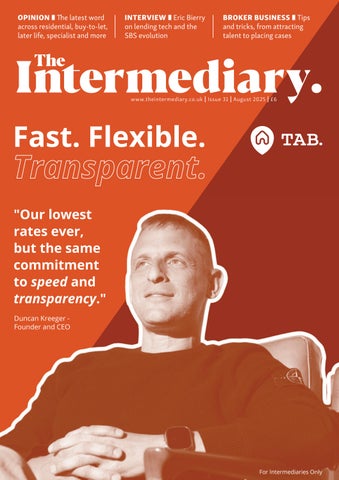

"Our

rates ever, but the same commitment to speed and transparency."

Duncan KreegerFounder and CEO

"Our

rates ever, but the same commitment to speed and transparency."

Duncan KreegerFounder and CEO

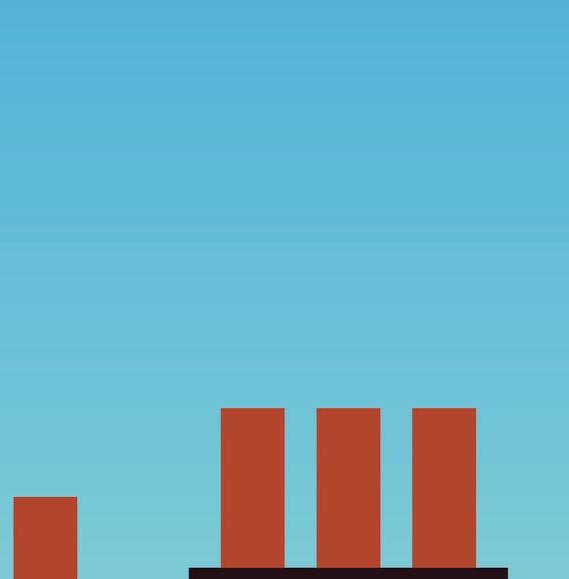

From 7.50% p.a.

Inc. Bank of England base rate

Loan sizes:

£100,000 up to £5,000,000

Up to 75% LTV - Residential Up to 70% LTV - Commercial

2.00% Arrangement fee, 2.00% exit fee ESG discounts available to exit fee

From 8.50% p.a.

Inc. Bank of England base rate

Loan sizes: £100,000 up to £5,000,000 Terms up to 24 months

Up to 75% LTV - Residential Up to 70% LTV - Commercial

2.00% Arrangement fee No exit fee

e latest word across residential, buy-to-let, later life, specialist and more

Bierry on

We’re here to speed things up, not slow things down. Our 100% online application is stripped back to the essentials, offering speed of service, saving time for everyone.

Clear, up front criteria and a straight-talking broker support team. That means no surprises, so you’ll always know where you stand.

Quick, consistent decisions with instant DIPs and desktop valuations for remortgages on standard properties that meet eligibility.

All underpinned by clear criteria so you know where you stand with simple processes for portfolio landlords, no extra forms just a few additional questions to fully understand your application.

As the sun continues to pelt cheerily in through our home office windows – giving us a glimpse of the kind of summer that seemed to pass us by last year – it’s safe to say that the past month has seen hopes and hearts start to li a li le in Ol’ Blighty.

In what I’m sure our readers will agree is equally exciting news, in the weeks just gone we have seen the women bring football home once again in the Euros, and the Monetary Policy Commi ee (MPC) lower the base rate to 4.0%, the lowest level since March 2023. This is the fi h consecutive reduction, and even the most pessimistic among us –among which I usually number – should be about ready to call it a trend.

While my local pub wasn’t replete with screaming fans – and an entire brass band that, impressively, popped up out of nowhere – for the MPC announcement, many of those in the know still felt an upswelling of positive emotion that can be hard to come by in these fraught times.

The move was described by many as a welcome boost for borrowers and the market, and indeed, we’ve seen some immediate results, with lenders reducing and reviewing their rates populating the headlines.

Overall, I dare say the picture is looking quite positive. For the first time since the 2022 miniBudget, average 2-year fixed rate deals have dipped below 5%. Meanwhile, lenders have shown a willingness to expand their mortgage offerings with flexibility around borrowing

capacity in mind. House prices have remained resilient, and improvements in affordability mean that buyers don’t need to wait for an expected – but unlikely – drop to start seeing their dream home become a potential reality.

Of course, the picture gets a li le gloomier when you turn to look at the buy-to-let (BTL) market. The Royal Institution of Chartered Surveyors (RICS) has reported the steepest drop in new rental listings since the Covid-19 lockdown of 2020, pu ing an upward pressure on rents, and no one can have avoided the knowledge that landlords are feeling a squeeze just as much as their tenants.

With the Renters’ Rights Bill rumbling down the track, landlords are also increasingly wary of how this change could make their lives harder. Expert forecasts are predicting a decline in BTL lending through the rest of the year.

Next month, our popular BTL Focus returns to make sense of this turbulent market. It will tackle all the difficult and practical realities our readers need to understand to make sense of the rented sector, and to make the most for their clients, regardless of the storm clouds brewing on the horizon.

Keep an eye out for all the expert insight in that issue. In the meantime, and with lots to discuss across all sectors of the market this month, I think it’s acceptable to take a moment to bask in the warmth. ●

Jessica Bird

@jess_jbird

www.theintermediary.co.uk www.uk.linkedin.com/company/the-intermediary @IntermediaryUK www.facebook.com/IntermediaryUK

Jessica Bird Managing Editor

Jessica O’Connor .................... Deputy Editor

Marvin Onumonu Reporter

Brian West Sales Director (Interim) brian@theintermediary.co.uk

Ryan Fowler Publisher

Felix Blakeston .............. Associate Publisher

Helen Thorne Accounts nance@theintermediary.co.uk

Orson McAleer Designer

Bryan Hay Associate Editor

Subscriptions subscriptions@theintermediary.co.uk

Ahmed Michla | Andy Philo | Averil Leimon

Charlotte Grimshaw | Chris Storey

Christopher Blewitt | Claire Cherrington

Craig Hall | Dan Narwal | Dave Harris

David Fell | David Lownds | Donna Francis

Eric Bierry | Gavin Diamond | Ginny English

Grant Hendry | Gregor Sked | Hamza Behzad

Imran Hussain | Jake Sandford James Armitage

Jed Newton | Jerry Mulle Jonathan Westho

Kate Davies | Laura omas | Lewis Atkinson

Lisa Hodgson | Louisa Ritchie | Louise Pengelly

Mark Harrison | Martese Carton | Matt Kingston

Mel Spencer | Neil Leitch | Paresh Raja

Parik Chandra | Phil Chesham | Rob McCoy

Rob Stanton | Rodney Sloan | Roz Cawood

Sarah Davidson Simon Martin | Stephanie

Dunkley | Steve Goodall | Tippie Malgwi

Vic Jannels | Will Hale

Copyright © 2025 The Intermediary

Cartoons by Fergus Boylan Printed by Pensord Press

Feature 36

BEYOND THE HEADLINES

Jessica O’Connor asks how the estate agency industry can turn a new page

Broker business 72

A look at the practical realities of being a broker, from attracting talent to the monthly case clinic

Local focus 86

This month The Intermediary takes a look at the housing market in Nottingham

On the move 90

An eye on the revolving doors of the mortgage market: the latest industry job moves

SECTORS AT-A-GLANCE

The Interview 24

SBS

Eric Bierry discusses business evolution and the lending tech landscape

Pro le 46

BREEZE CAPITAL

Mark Harrison on the importance of culture in the lender’s success

Q&As 30, 70

CUMBERLAND BUILDING SOCIETY

Lisa Hodgson talks working with intermediaries and the changing holiday let market

LENDERHIVE

James Armitage on how brokering can embrace the modern age

Meet the Broker 74

TRINITY FINANCIAL

Jed Newton gives his view on brokering in the current market

Meet the BDMs 20, 42

AFIN BANK FOUNDATION HOME LOANS

Tippie Malgwi and Ginny English discuss the challenges and opportunities for BDMs

Our recent survey of savers generated a host of insights for anyone with an interest in the housing market.

Perhaps what shone through most was just how important the Lifetime ISA (LISA) is to potential homebuyers. Almost all LISA-holders we spoke with – a whopping 98% – said they were reliant to some degree on the cash bonus that comes with the accounts in order to purchase a home. Almost half said they were ‘very reliant’ on the 25% bonus of up to £1,000 paid each year.

That’s an enormous proportion of aspiring homeowners who are playing their part, in terms of putting money aside where possible, but who remain aware that without a helping hand from the Government, their saving efforts may be frustrated by persistent house price growth.

While recent weeks have seen plenty of speculation about ISA limits being scaled back, savers are calling for it to be made more, not less, generous.

Almost half of those we spoke to wanted to see the annual limit for Lifetime ISAs, which currently stands at £4,000, to be increased.

There was similar appetite for the 25% redemption charge – which is levied on Lifetime ISAs if they are used for purposes other than property purchase or for retirement – to be lowered or removed entirely.

Earlier this year, the Treasury Select Committee announced an investigation into the Lifetime ISA, questioning whether it was fit for purpose in its current form.

It noted the frequent complaints about the level of penalty fees being

levied on savers, as well as the fact that the rules around the products have not been updated since 2017.

These products can only be put towards purchases of properties costing less than £450,000, and given the house price growth we have seen in recent years, that means buyers are being frozen out of using their Lifetime ISA savings towards purchasing in certain areas, particularly in the South East.

Our research shows the Lifetime ISA is playing a big role in the purchasing plans of would-be buyers. But it could play an even more impactful role if it was brought up to date, with more generous caps in place.

While it would be welcome for the Lifetime ISA to be updated and improved, as an industry we also need to consider other ways to support would-be buyers who have struggled to save a mammoth deposit.

High loan-to-value (LTV) lending is obviously a good place to start, providing borrowers with more options at 95% LTV or higher. The situation here has greatly improved of late, with data from Moneyfacts showing that in July there were around 447 products available at 95% LTV, compared with 361 a year ago and just 188 the year before. There have been similarly encouraging improvements in the number of 90% LTV products on the market, too.

While these products will always be in the minority compared to those open to borrowers with larger deposits, any measures which make it easier for lenders to provide high LTV mortgages should be welcomed.

That’s why the new, permanent Mortgage Guarantee Scheme announced by the Government is

CHRIS STOREY is chief commercial o cer at Atom bank

Measures which make it easier for lenders to provide high LTV mortgages should be welcomed”

such a positive – and will hopefully result in more substantial options for aspiring homeowners.

The changes made to the high loan-to-income (LTI) caps should also prompt lenders to go a little further in providing funding which will truly make a difference to those potential first-time buyers.

Regulators and the Government are removing those potential barriers and hurdles which may have caused some lenders to be a little more cautious about providing more generous funding.

The onus is now on lenders to step up and respond.

The path to homeownership isn’t an easy one currently. Aspiring buyers need all the help they can get, and not just from the Government. Lenders must be serious about providing true support, and that means higher LTVs, a more flexible approach to LTI, and catering for those who may have the odd black mark in their credit history.

Focusing on family support and the ‘Bank of Mum and Dad’ risks freezing out whole swathes of younger people from homeownership. Lenders must step up and deliver the support that buyers so desperately need. ●

The UK labour market is no longer defined by the nine-to-five. From public sector shift workers to university lecturers and contractbased professionals, working patterns are increasingly fluid. While the job may be constant, the way it’s delivered and remunerated often isn’t.

This isn’t a new trend. Health and social care workers have long relied on flexible schedules, from core contracted hours to top-up shifts known as bank work. In higher education, academics routinely blend salaried teaching with consultancy, examining duties or research fellowships. For brokers, this creates a growing client base whose income can be steady in total but complicated in form.

A payslip with five components shouldn’t raise flags if those components are consistent, proven and part of the professional role. Shift allowances, night duty payments, overtime and bonuses may not be classed as ‘basic salary’, but they are expected, and in many cases contractual.

Many clients in the public sector are doing vital, high-demand work. Their earnings may fluctuate slightly, but their profession does not. For lenders, the real challenge isn’t risk. It’s recognition.

Standardised lending models often fail to account for this. A teacher working regular overtime for afterschool tuition, a police officer rotating between day and night shifts, or a nurse topping up with weekend bank hours aren’t outliers. They’re examples of how the world of work really functions. The potential clients

being turned away are those who power the nation’s infrastructure.

Where a track record exists of typically six months or more, there is little justification for excluding these income elements. In fact, failing to do so can unfairly penalise some of the most stable and employable individuals in the market.

Allowances, overtime, shift uplifts, and income from bank or locum work are the norm in professions such as midwifery or firefighting.

There’s also a need for flexibility around contract types. Many bank workers are technically on zero-hours arrangements, yet work as frequently and earn as much as full-time peers. The distinction is technical, not financial. With many NHS departments advertising shifts well in advance, the income can be consistent, even predictable.

It’s important that lenders can distinguish between gig economy unpredictability and structured, professional flexibility. The former might carry risk. The latter does not. Especially when underpinned by professional registration, skills shortages and public funding.

Another area to consider when working with these clients is whether a lender can accept applications from overseas customers. Skilled worker visa holders and those on ancestry or British National Overseas (BNO) visas are critical to staffing key sectors like education and healthcare. Provided they have a right to reside and a proven employment record, their applications warrant the same level of consideration.

It matters that underwriting teams have the experience and training to understand these sectors. Manual

underwriting, collaboration with broker-facing teams, and internal training can all contribute to better decision-making. It’s not about making exceptions. It’s about building policy around how modern professional life actually works.

A lender’s role isn’t to standardise borrowers. It’s to make intelligent, case-by-case decisions. It’s important they look beyond the contract type or payslip format and understand what the income really represents.

This approach ultimately benefits brokers. It extends the product options available for clients who might otherwise be underserved. It enables cases to be placed more smoothly and more often. It helps to build long-term relationships with clients who value understanding over box-ticking.

Key workers and other professionals remember the lenders and brokers who treated them fairly and offered them choice. Particularly when they’ve experienced rejection elsewhere. A wider product armoury today builds the client bank of tomorrow.

In a market where real-world understanding is in short supply, brokers who work with lenders willing to go further can position themselves not only as solutionfinders but as advocates. That’s where progress lies. Not in relaxing risk criteria, but in recognising that some of the UK’s most valued professionals don’t fit neatly into a standard model. They work differently, earn differently and deserve to be assessed accordingly. ●

hat do we mean by value in today’s market?

Perhaps more importantly, what will we mean by value tomorrow?

Accurately assessing lenders’ capital valuation exposure increasingly requires more than an understanding of market sentiment and liquidity.

While buyer demand and funding availability remain fundamental for loan-to-value (LTV) purposes, they provide only a partial view of the underlying risk.

Lenders must account for a broad spectrum of variables that can materially impact asset performance and, ultimately, resale value.

This includes:

ɐ The property's physical condition;

ɐ Its age, build type, warranties, management charges and incentives;

ɐ Exposure to environmental risks such as flood, subsidence or contamination;

ɐ Current and historical land use and designation under new green, brown and grey belt definitions;

ɐ Tenure, including ongoing leasehold complexities;

ɐ The integrity and durability of construction type and fabric.

Evolving legislative frameworks – such as building safety or net zero mandates

– and uncertainties surrounding future planning or land-use policy also matter and are hard to quantify. Legal title issues, restrictive covenants, easements or absent documentation can cause costly delays on sale. Where legal or historical data is incomplete, latent risk is inbuilt. How, then, can lenders address these issues in a way that is

both comprehensive and commercially viable? At e.surv we have an answer to this question – one we hope to share later this year. It comes down to access to comprehensive datasets that provide enough nuance to be materially useful. It’s a matter of scale.

Take automated valuation models (AVMs). Data comes from across the market. It must be timely, real-time and of a scale that eliminates the deviation that single anomalies can create. People need to be involved to ensure the validity and integrity of that data. In future, AVM services will unite automation, remote digital valuations and proprietary insight.

Seamless application programming interface (API) integration offers fast and scalable deployment into various business workflows. Data must be improved, checked and auditable. Ensuring it comes from one place keeps third-party risk to a minimum, giving regulators confidence and lenders security.

This approach is true of developing markets. The creation of new towns as well as large scale, often multiple, developments that can double or even triple the population of previously smaller towns and villages have massive implications for the value of existing homes, as well as posing all of the usual challenges new-build comes with.

The number of lenders using our new-build hub to gain intelligence has grown at pace since the Chancellor’s announcement on housing, now more than a year ago. Lenders can track their volume and concentration risk across more than 16,000 new-build developments in real-time, allowing for smarter origination strategies based on quantifiable facts.

Specialist markets are equally important. On 17th July, the Government published an update on the next phase of its Remediation Acceleration Plan, first announced in December 2024. The legislation, set to be brought forward “as soon as Parliamentary timetable allows,” will require landlords of buildings 18 metres or more in height with unsafe cladding to complete remediation by the end of 2029, and landlords of buildings 11 to 18 metres in height to complete remediation by the end of 2031.

Those who fail to comply without reasonable excuse could face unlimited fines or imprisonment. New legislation will also give named bodies, such as Homes England and local authorities, powers to remediate buildings with unsafe cladding if the landlord fails to do so.

Understanding progress and exposure will be crucial for lenders –with very real financial implications inevitably hitting in the next few years.

Getting a grip on back books now is imperative to manage refinancing decisions, and up to date information is now an absolute necessity.

My final point to illustrate the breadth of challenges facing lenders is about dealing with customers who are coming to the end of their product terms. The Financial Conduct Authority’s (FCA) July policy statement, PS25/11 Mortgage Rule Review: First steps to simplify our rules and increase flexibility, introduces a new rule into the MCOB Handbook “to clarify that firms must deal fairly with customers whose

mortgage terms have expired.”

This states: “Firms must not take repossession action unless all other reasonable attempts to resolve the position have failed. These requirements are supported by the Consumer Duty.”

While not a significant change to previous expectations put on lenders in this scenario, putting this responsibility into regulation more permanently strengthens the need for lenders to calibrate their own capital risk exposure.

Whether these properties remain on their back books or are, eventually, repossessed and sold, accurate valuation matters. This is perhaps particularly true for building societies in the mid-tier, whose liquidity is under constant watch by the Prudential Regulation Authority (PRA).

For lenders, developing a multidimensional understanding of all these factors are critical. It enables more accurate pricing of risk, betterinformed lending decisions, and improved resilience of the back book in the face of ongoing market and regulatory shifts. ●

Thousands of borrowers are still trapped on skyhigh standard variable rates (SVRs) in closed mortgage books, many of which are held by investors outside of the UK.

The story of their plight has been in and out of the news for almost 18 years, following the 2007 Credit Crunch and 2008 financial crash.

While their numbers have dwindled since then as loans redeem or homes are repossessed, it’s estimated there are still around 47,000 mortgage prisoners unable to refinance onto a new contract with an active lender.

This contingent of borrowers are those who took out mortgages at up to 125% loan-to-value (LTV), who self-certified their incomes and took interest-only loans and have no means to repay the outstanding balance.

While borrowers in this position with an active mortgage lender can move to a more affordable rate under Financial Conduct Authority (FCA) rules, those in closed books held by investors that lack the permissions to originate mortgage contracts are stuck. Often, they’re paying standard variable rates up to 15% – which is, frankly, scandalous when the UK base rate is 4%.

You’d think this is a clear breach of the Consumer Duty rules. These are vulnerable borrowers. The outcomes they face are entirely predictable to most reasonable people – and they’re not good. The products are outrageously priced, the value is abysmal, even detrimental, and the support these borrowers are given is being told, for the most part, tough luck.

The kicker is that the FCA can do nothing about it where the investors operate outside their purview. US pension funds, insurance companies, private equity funds – they are free to ignore the Consumer Duty to their hearts’ content.

This leaves the UK market with a conundrum, however. The borrowers are in the UK and ought to be protected by UK law. They are not.

Contractually, bondholders who have invested in securitised UK mortgages must appoint a fully regulated third-party administrator or servicer – and they are on the hook with the FCA.

This is causing an almighty scrum in the market – investors care about their returns. Legal contracts that govern securitised assets and the returns promised therein are extremely difficult to alter years down the line. The only player in the chain with a reason to care about this conflict is the administrator.

To complicate matters further, some administrators hold permissions to originate new mortgage contracts – something that is required to take a mortgage prisoner off SVR and onto a new fixed rate. Other administrators do not.

There’s a ruckus over whether origination permissions make the servicer a ‘co-manufacturer’ of mortgage contracts. The majority of servicers want absolutely nothing to do with this responsibility. Legally, this side argues, they have no role in setting the criteria or pricing of that loan and are simply carrying out the contract’s obligations on behalf of the investor.

The other side takes a contrary view – they’re the only ones with the power to apply the Consumer Duty rules for borrowers trapped in these mortgage books. If they do not take responsibility, who will?

We’re at an absolute stalemate at the moment – and it doesn’t look like things are going to resolve any time soon. In a review of the number of people affected in 2021, the FCA estimated that there were 195,000 mortgages held in closed mortgage

SARAH DAVIDSON is head of research at WPB

books with inactive lenders – 2.3% of the total number of residential mortgages.

In 2019, it estimated that there were 250,000. The longer this goes on, the more of these mortgages are repaid – at however extortionate a rate – or properties repossessed and sold. The theory is that eventually securities will redeem, and the problem will have gone by default.

Except there’s a really big fly in this ointment: there’s more than one kind of mortgage prisoner.

First you have the credit and/or affordability prisoners whose financial circumstances, credit rating, loan-toincome (LTI) ratio, age or repayment strategy renders them unable to remortgage.

Then you’ve got the property prisoners, where cladding, fire safety, energy efficiency and flood risk make the property unmortgageable. Finally, the contract prisoners, those unfortunates who bought leaseholds with onerous service charges and doubling ground rents.

Many thousands of these mortgages have also been securitised or sold as a whole loan book to investors outside of the FCA’s jurisdiction. Sorry folks, but this isn’t a problem that is going away for many decades to come.

There is no easy answer to this – it’s a nightmare scenario where everybody and nobody is right and wrong.

Expect the plight of these borrowers to come sharply into focus if interest rates move against them. ●

With the cost of everyday life climbing and property prices still daunting, it’s little wonder that many aspiring homeowners are starting to ask, “Is it still worth it?”

The dream of owning a home has always required a degree of sacrifice, but in today’s climate, it’s not just about cutting out coffees, avocados or holiday plans. For many, it’s about stretching deposits to their limit and making long-term financial commitments in a world that feels anything but predictable.

Despite all this, the aspiration for homeownership endures. That’s why the industry, lenders, brokers, and policymakers alike, must continue on its quest to find meaningful, practical answers for those questioning whether the sacrifices are really worth it.

One of those answers lies in the availability of high loan-to-value (LTV) lending, which continues to be a vital route onto the property ladder for thousands of first-time buyers.

The cost-of-living crisis, wage stagnation, and rising house prices have made saving a substantial deposit increasingly difficult. The recent Stamp Duty changes – which reduced the nil-rate threshold for first-time buyers from £425,000 to £300,000 – have further compounded affordability pressures. Purchases between £300,001 and £500,000 now face a 5% charge, and relief has been removed entirely for homes priced above £500,000.

Following this announcement – and in the subsequent months – data from Twenty7tec shows that 90%-plus loan-

to-value (LTV) borrowing among firsttime buyers increased from 48.84% to 49.49%, with nearly half now relying on high LTV mortgages to get on the ladder. These products are now suggested to account for over 22% of all borrowing, reflecting the financial stretch many are making just to take that first step onto the ladder.

For lenders, the challenge lies in balancing risk with support. While lending at higher LTVs naturally requires robust underwriting and careful pricing, it’s an area in which smaller, more agile mutuals can make a meaningful difference. Our close alignment with borrower needs –combined with a flexible, innovative approach, manual underwriting, and a strong commitment to responsible lending – puts us in an excellent position to provide targeted support.

But we also need support in ensuring that our product offering reaches the right type of borrower. In today’s environment, the role of the mortgage intermediary has never been more critical. As product types diversify and economic conditions evolve, borrowers increasingly need tailored advice to help them navigate a market full of options, many of which they don’t even realise exist.

This is especially true in the high LTV space, where mortgages often involve stricter affordability assessments, risk-based pricing, longer terms and even financial support from family members. Here, advisers play a vital role in educating borrowers on the implications of stretching their deposit and in helping them choose a structure that supports long-term financial resilience.

Affordability remains front and centre in borrowers’ minds. Following the aforementioned Stamp Duty changes, first-time buyer activity saw

DAVID LOWNDS is head of products and marketing at Hanley

Economic Building Society

a notable shift, with a drop in search volumes and a shift toward properties priced below the £300,000 threshold. However, there are signs of resilience in the market.

Rightmove’s latest data shows that while average asking prices dipped by 1.2% in July, the largest July drop in over two decades, the number of property sales agreed was 5% higher than this time last year.

Simultaneously, lower mortgage rates have improved buyer affordability. A 2-year fixed rate now averages 4.53%, down from 5.34% last year, saving borrowers almost £150 a month on average.

However, high LTV lending isn’t just about numbers, it’s about opportunity. It’s about giving younger buyers, single-income households, and regional renters a realistic path to homeownership. While it must be delivered sensibly and sustainably, especially in light of regulatory considerations, it deserves a place in every responsible lender’s toolkit.

As affordability remains under pressure and homeownership aspirations persist, it is essential that lenders continue to develop innovative products backed with responsible underwriting.

It’s equally vital that brokers remain confident and equipped to guide borrowers through what is often the biggest financial decision of their lives.

For many, owning a home still matters. If we can offer the right support – through a combination of products, advice, and accessibility –then maybe, just maybe, the sacrifices won’t feel quite so steep after all. ●

Andy Reid Sales Director

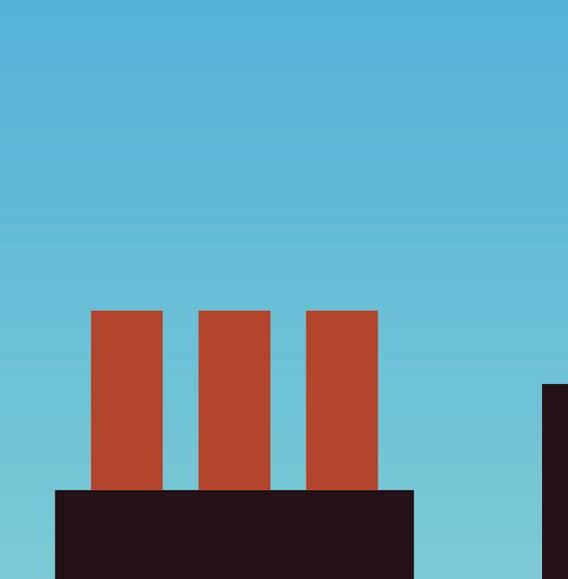

From 7.50% p.a.

Inc. Bank of England base rate

Loan sizes:

£100,000 up to £5,000,000

Up to 75% LTV - Residential Up to 70% LTV - Commercial

2.00% Arrangement fee, 2.00% exit fee ESG discounts available to exit fee

Bridge From 8.50% p.a. Inc. Bank of England base rate

Loan sizes: £100,000 up to £5,000,000 Terms up to 24 months

Up to 75% LTV - Residential Up to 70% LTV - Commercial

2.00% Arrangement fee No exit fee

As the summer holidays draw to a close and September approaches, it seems a good time to take stock of the second half of the year. Back to school and back to work always heralds a bump in mortgage activity, and we expect no difference this year.

The market outlook

Setting to one side politics – so consistently changeable it seems pointless to dwell too long on it – the outlook for the housing market in the UK is relatively benign.

Consumer price inflation rose by 3.6% in the 12 months to June 2025, up from 3.4% in the 12 months to May, according to the Office for National Statistics (ONS). On a monthly basis, the consumer price index (CPI) rose by 0.3% in June 2025, compared with a rise of 0.1% in June 2024.

Over the past year, the rate of inflation has fallen a lot, and the Bank of England is on record saying “inflationary pressures have eased enough” to allow for four rate cuts over the past 12 months.

We saw a further quarter point cut announced at August’s Monetary

Policy Committee meeting, taking the base rate down from 4.25% to 4.00%.

If price pressures continue to ease, the Bank of England governor has said there should be room to reduce interest rates further over time.

When and by how much depends on how the economy bears up under ongoing global trade negotiations, geopolitics and domestic confidence levels.

Whether we see another cut before 2025 is up, mortgage rates are already very competitive, with the lower end of the risk curve priced significantly below base. Multiple high street lenders are already operating with sub-4% rates, with best buys likely to drop further in September if the Bank does bring rates down. The usual burst of September activity across both purchase and remortgage will also put pressure on lenders to keep pricing down.

For those buying, it’s a keen market. House prices have eased in many parts of the country, with some attractive opportunities now a realistic prospect for those hoping to get onto the ladder for the first time.

Rightmove’s July index showed the average price of property coming to the market for sale dropped by 1.2%

CRAIG HALL is director, strategic partnerships, nancial services at LSL Property Services

(-£4,531) that month, to £373,709. The number of available homes is still at a decade-high level, and agents told the property platform that summer sellers are pricing even more competitively to attract buyer interest.

London has been the biggest regional driver of new seller asking price falls, down 1.5% and led by inner London, which saw asking prices down 2.1% on average.

Rightmove’s analysis shows that improving buyer affordability is stimulating stronger activity. The number of sales being agreed is 5% higher than at this time last year, while the number of potential future buyers contacting estate agents about homes for sale is 6% higher than last year.

The Government has committed to a permanent Mortgage Guarantee Scheme, providing lenders with a Government-backed guarantee against a fixed proportion of any potential losses made on eligible loans, continuing to support the 95% loan-to-value (LTV) end of the market. Along with the Prudential Regulation Authority’s (PRA) loanto-income (LTI) capital ratio review and interim suspension of the current 15% threshold on 4.5-times income cap, affordability prospects are good. This followed the previous relaxing of stress-testing, with several lenders stating that this would increase average borrowing capacity by £30,000 to £35,000.

Labour and protection

Protection will be vitally important as people re-finance and buy to protect against tightening labour market.

In September, we’re also expecting a sizable refinancing boost, providing intermediaries with the opportune moment to broach the subject with clients.

As affordability eases and monthly payments are likely to come down on remortgage, the argument for directing some of those savings towards income protection or other relevant cover is stronger than it has been for some time.

It may be time for brokers to rethink whether to look at new markets.

The new-build sector is going to be a key business stream for mortgage intermediaries over the next four years. We know that support for new-build is significant, with £16bn of new public investment destined to fund 500,000 new homes, at the same time unlocking over £53bn of private investment, according to Government estimates.

The bulk of Labour’s focus is in supporting affordable homes, with Shared Ownership housing provision an important part of that. This market is undoubtedly more specialist, but it does represent a strong growth opportunity, and is perhaps worth a

second look. One person’s challenge is another’s opportunity, and so it is in the buy-to-let (BTL) market at the moment.

Amid scaremongering headlines in the national media, the truth is that the commercials in the private rented sector are very strong for landlords prepared to manage portfolios as a sustained business concern.

Rental growth is very strong and shows no sign of abating. The selloff in properties by smaller portfolio landlords is seemingly continuing, yet with rates lower and prices down, buying opportunities are everywhere.

Landlords continue to wait for the outcome of the Minimum Energy Efficiency Standards consultation and confirmation of when and if this will come to bear. This may trigger landlords to rebalance portfolios along with carrying out necessary retrofit requirements.

When you stand back and look at how well the market is performing, it is even more extraordinary given the prevailing economic uncertainty.

But that is the truth of the moment we are in, and we should all grasp it while it lasts. ●

Here at Equifinance, we are totally committed to the intermediary sector as our distribution channel. As a result of the relationships we have put together over time, our business has flourished. The professionalism and support of our partners has meant that we have built up a strong reserve of trust over the quality – and quantity –of the applications we receive.

While it is early days, I am not sure whether fellow mortgage practitioners have had a chance yet to digest the news that the regulator is considering limiting the requirement to give advice during client conversations in favour of more execution-only solutions.

Under consultation paper (CP25/11), the Financial Conduct Authority (FCA) would seem to be flagging the possibility of undoing and unpicking its existing guidance on mortgage advice, which culminated in the adoption of Consumer Duty just last year, and its insistence on making sure that properly considered customer outcomes are the ultimate focus for all advisers.

The layers of regulation – from Treating Customers Fairly (TCF) to Consumer Duty – have reinforced the importance of clients receiving proper advice based around a comprehensive fact-find, followed by a recommendation predicated on extensive research.

Doesn’t it seem an odd time for the regulator to be talking about the possibility of extending the use of execution-only as a viable alternative to proper advice? The whole thrust of advice has been to help ensure that consumers have protection from the lazy option of ‘selling’ a single product or one from a suite of products.

Everything about advice has been geared to trying to reach an equitable lending solution for clients based on

the gathering of their personal and financial details.

Execution-only flies in the face of giving customers a professional service, and definitely contradicts the canon of consumer protection which has been built up over many years.

If adopted, the losers would be the customers who continue to rely on advice and receiving a recommendation from a whole-ofmarket practitioner. Being left to navigate everything from affordability and lender criteria, as well as finding out about legal representation and the whole valuation process, could potentially put clients at risk through lack of vital information.

Of course, it can be argued that not everyone requires advice. Those with a greater knowledge of finance and who are aware of the potential pitfalls do not necessarily require the help. But, for those of us wanting to understand the ins and outs of mortgage finance, we need to know that the multitude of possible solutions have been sifted through to ensure that any recommendation is a valid choice that meets our particular requirements.

The regulator is seeking feedback from the industry based on a desire to help encourage consumer choice and greater convenience. A laudable

LAURA THOMAS is regional sales manager at Equi nance

Advisers should pat themselves on the back for giving peace of mind to so many new borrowers”

ambition, but while this is just a consultation, there is no indication that this more than an old fashioned fishing expedition to get the result that they want.

If I was being cynical, and execution-only was expanded, the main winners would be those high street lenders that have always disliked their reliance on intermediary business because procuration fees cut into profits. An expansion of execution-only would mean an increase in direct business from consumers and a reduction in the cost of procuration fees.

I think that everyone would agree that the mortgage process can be a long one. However, how much of that is down to money laundering legislation and lender caution in assessing individual risk from clients?

The consultation paper states that 97% of new mortgages have been advised since 2015, which in my eyes is something to be proud of. Advisers should pat themselves on the back for giving peace of mind to so many new borrowers.

We don’t want to see the positive results of proper qualified advice diluted in favour of what effectively is a cut price service under execution-only. ●

HAMZA BEHZAD is business development director at Finova

As predicted by UK Finance in December last year, 2025 has been characterised by a strong performance in remortgage volumes. Data from Legal & General shows a significant increase in remortgaging activity in the UK housing market, with figures for Q1 2025 showing that broker searches for remortgage products soared 34% since Q4 2024.

With the changes to Stamp Duty that came in April, March saw a surge in activity and September is set for another big bump in volumes. There are several reasons to expect this positive trend to continue.

Mortgage rates have become even more competitive. Lenders have been pushing the lower loan-to-value (LTV) deals below 4% for months now, illustrating just how tough the game is proving to retain customers coming up to refinance.

While the summer months have seen a slight so ening, typical for this time of year, a large tranche of fixed rates is due to end as we move into the Autumn. According to UK Finance, roughly 1.8 million fixed rate mortgages are set to reach maturity in 2025, up from around 1.6 million in 2024. A further 1.9 million fixed rate deals expire in 2026.

While there remains a swathe of borrowers coming up to the end of very low 5-year fixes, the majority of those refinancing over the next 18 months will be facing the prospect of their monthly repayments falling.

According to research from Compare the Market – based on data from a Freedom of Information request to the Financial Conduct Authority (FCA) and data from the Bank of England – around 940,000

homeowners are coming off 2-year fixed rates in 2025.

Moneyfacts data showed average fixed mortgage rates fell for the fi h consecutive month at the start of July, with the average 2-year fixed mortgage dropping to 5.09%, its lowest point since September 2022 when rates hovered around 4.24%.

Similarly, typical 5-year fixed prices dipped to 5.08% and were last lower in October 2024 at 5.07%. It’s likely that we’ll see rates come down further as lenders vie for the best customers.

Product transfer volumes, supported for several years by borrowers’ need to avoid lengthy affordability checks on much larger mortgage payments, have seen a drop in popularity this year. This is hi ing lender margins – remortgage origination is more expensive to underwrite and source. It is this that is driving such fierce rate competition. But lenders’ desire to maximise customer retention using pricing has also encouraged more borrowers to switch.

At the start of the year, remortgaging to another lender triggered a full reunderwrite of a borrower’s affordability. While there are always those willing to go through the admin this presents, the majority of people will trade a couple of basis points for an easy life.

That dynamic has shi ed. In July, the Financial Conduct Authority (FCA) published the first in a series of measures expected in the coming months, designed to make the process of remortgaging easier.

The requirement for a full affordability assessment when reducing the term of a mortgage has now been removed, though the

FCA still expects firms to consider affordability in line with their responsible lending policy and the Consumer Duty. In addition, the modified affordability assessment has been amended to include new mortgage contracts with new lenders where it is more affordable than either the customer’s current mortgage, or a new mortgage product that is available to that customer from their current lender.

While the changes are permissible rather than mandatory, we expect to see more lenders allow borrowers on lower LTVs, particularly where outstanding balances are small, to forgo a full underwrite.

This is likely to further incentivise intermediaries to source deals from alternative lenders when clients approach their refinancing deadlines, and it’s this that should be concerning for lenders that have been relying on the market to support their retention business. It won’t be enough in this new environment.

Borrowers in a strong position no longer face a stark choice between hassle or no hassle. The FCA’s rule changes will make pricing even keener and the importance of service critical. Where lenders do not have the cost of funds needed to compete with the high street banks on price, borrowers will need the offer of something else worth their while if they are to accept a slightly higher rate. This is where the process of retention really ma ers – certainly for direct to customer remortgaging, but crucially, also for brokers. Lenders in this bracket tend to rely heavily on intermediaries –making their remortgage applications as headache-free as possible is set to be the gamechanger from now on. ●

Affordability assessments can be one of the main barriers facing would-be homeowners who may be restricted by their salary and loan-to-income (LTI) ratios, but following recent clarification from the Financial Conduct Authority (FCA) about stress-testing rules, a number of lenders have made changes to the way they assess a borrower’s affordability.

Previous high loan-to-income limits were restricting many lenders’ ability to support aspiring homeowners and the UK growth agenda. But the refreshed guidance from the FCA clarified how to incorporate future interest rate movements into stresstesting. It emphasised that banks and building societies have flexibility in choosing a suitable stress rate, linking to reversion rates or future product rates, rather than applying a fixed margin above current standard variable rates.

At Leeds, we’ve just reduced stress testing rates by up to 1.24%, meaning that a borrowers can now access more lending, and we have lowered the minimum household income needed to borrow more than 4.5-times annual income.

mortgage, a borrower on an income of £30,000 would be able to purchase a property worth up to £173,000, compared to £141,000 before.

Well first, as a lender, this is hugely positive news and allows us to deliver on our purpose of putting homeownership within reach of more people, generation after generation. The rule clarification means that we can confidently lend more to our members and support their homeownership dreams, while continuing to assess affordability in a responsible way, using a range of criteria and underwriting checks to ensure prudent lending.

We are mindful of balancing more generous a ordability with responsible lending”

MARTESE CARTON is director of mortgage distribution

at Leeds Building Society

news for brokers. It means that intermediaries can say ‘yes’ to more clients, and revisit affordability on cases where applications previously fell short.

This is a great opportunity for brokers to engage with clients and educate them on what the changes could mean for their case. Brokers can re-run affordability checks, and we have recently updated our improved affordability calculator to facilitate this.

Historically, stress-testing requirements have unduly held some borrowers back from achieving their homeownership aspirations, so we are pleased to be able to lend more to our customers as a result of these changes in affordability assessments.

single applicants earning £30,000 for a mortgage. This is down

the housing market for

Clearly, the changes benefit borrowers by unlocking more lending to allow them to step onto or climb up the property ladder. Reduced stress buffers also benefit those who are looking to remortgage. Clients coming to the end of fixed rates can now access a wider range of deals and switch lenders more easily without triggering

Despite increased flexibility, both borrowers and brokers can be confident that lenders will still apply robust affordability checks and underwriting. A lower stress rate allows lenders to factor in a more a realistic cushion above a borrower’s expected monthly costs.

expected monthly costs.

Thanks to the changes, joint or single applicants earning £30,000 per year will now be able to apply for a mortgage. This is down from £40,000 annual income and significantly broadens access to the housing market for many creditworthy borrowers. With a 95% loan-to-

lenders more easily without triggering income limits.

value (LTV)

Avoiding unnecessarily restrictive affordability tests, particularly in a falling interest rate

restrictive affordability environment, is also great

Like all lenders, we are mindful of with responsible lending – balancing to help more people achieve their homeownership dreams and support the Government’s plan for growth.

Like all lenders, we are mindful of balancing more generous affordability with responsible lending – balancing growth and protecting our members. We welcome the clarification on lending rules which will allow us to help more people achieve their homeownership dreams and support the Government’s plan for growth.

We will continue to update our affordability models to align with market conditions and regulatory expectations. continue to seek the best outcomes

We will continue to update our stress rate assumptions and affordability models to align with market conditions and regulatory expectations. In collaboration with our intermediary partners, we’ll continue to seek the best outcomes for borrowers, as we have done for 150 years.

150 years. ●

At Magnet Capital, we’re always looking for ways to help your clients level up. That’s why we’ve enhanced our development finance offering, including increasing our LTV to up to 70%. That means more flexibility, more support, and even more power to get your clients’ projects off the ground.

We’re still the same expert team with the same straight-talking approach - just with more powerful funding that stacks up exactly how you need it to.

Ready to level up your client’s next project? Let’s talk.

Product Features:

LTV Day 1: 70%

• Loans from £250k - £4m

• Gross LTGDV: up to 65%

• 100% of development costs funded Max number of units: 20

hello@magnetcapital.co.uk

020 8075 3255

The Intermediary speaks with Tippie Malgwi, business development director at A n bank

How and why did you become a BDM?

I have over 15 years of banking, lending and wealth management experience, within the UK and in Africa. My experience spans specialist lending, high net worth (HNW) banking, and nancial planning, working with brokers, client advisers and direct clients. I was recognised by the Africa Business Chamber (AFBC) as a 2024 Top 100 African Business professional in the UK. I was also

awarded the Chartered Bankers Institute UK young banker of the year (2020), for my award-winning proposal focused on creating a nancial solution for vulnerable individuals living with life-changing conditions. I believe that I have a duty. Banks – and by extension bankers – have great power, but with that power comes responsibility. It is our collective responsibility, as frontline representatives, to actively champion positive societal change, and being a business development manager (BDM) within a bank like A n Bank enables me to do that.

I am passionate about nancial empowerment and providing innovative banking solutions to underserved segments of society, and A n Bank’s proposition of ‘mortgages for all’ focusing on the underserved self-employed, and the diaspora population living and working in the UK via the visa system, truly resonates with me. I look forward to supporting this vibrant diaspora – our doctors,

engineers, healthcare workers, IT workers, and the various other professionals who add so much societal value and now call the UK home, achieve their vision of UK homeownership.

A n Bank is a new digital bank, speci cally built to empower underserved communities, especially those contributing to the UK’s growth and diversity. Financial empowerment is our raison d’etre, and all our products, systems and distribution partners feed into this purpose. is is evident in how we tailor our products to support our target market. Examples include a minimum six months if UK residency required for visa holders, acceptance of complex or forecasted income for self-employed borrowers, and enhanced loan-to-incomes (LTIs) and loan-to-values (LTVs) for professionally quali ed clients.

Our aim at A n Bank is to deliver a seamless mortgage journey uniquely tailored to our client’s needs.

A wise banker once said, “appetite and policy can be two di erent things.” ere are several instances where published criteria and credit appetite di er; this could be very challenging and frustrating for BDMs. At A n Bank, we have the appetite to support our core clientele of employed visa holders and selfemployed clients, with our policies speci cally created to support them on their home buying journey.

e opportunities are endless! A n Bank is launching with a suite of xed and variable rate residential and buy-to-let (BTL) mortgage

products for visa holders and selfemployed borrowers. is is just the starting blocks on our roadmap towards nancial empowerment. We are equally as excited about our upcoming product pipeline aiming to support HNW borrowers, expatriate clients, and an expanded product range – watch this space!

ensure the best outcomes for borrowers?

Earlier this year, we commissioned two research studies to uncover the attitudes and pain points of our priority audiences, the African diaspora and the self-employed.

92% of the Africa diaspora feel underserved by UK banks, with the main pain points being visa status, nationality and lack of UK credit history. 76% of self-employed workers also feel underserved by UK banks, with their pain points being complex or multiple income, and thin credit history. e banking industry is failing these non-standard applicants, with brokers facing signi cant challenges supporting these diverse borrowers.

A n Bank seeks to remedy that by introducing greater exibility and understanding as part of our mortgage range. Brokers can introduce their diaspora clients of all nationalities, on several visa types, with thin or no UK credit records to A n. For self-employed borrowers, projected income is considered together with net retained pro ts and director’s loan accounts.

Our broker partners have welcomed our new proposition, and we look forward to further re ning our o ering with their support.

advice would you give potential borrowers in the current climate?

I had a recent conversation with a surgeon of West African origin, currently working within the NHS.

92% of the Africa diaspora feel underserved by UK banks”

Despite having a good income and a healthy deposit saved, they have been declined a mortgage by their high street bank due to their nationality and visa status. is is prevalent across the UK within the professional services sector – scores of doctors, nurses, accountants, lawyers, and engineers nd themselves stuck in the rental spiral solely for the reason of systemic mortgage barriers.

A n Bank is here to change that narrative and, together with our broker partners, right these wrongs to this underserved segment of society, who contribute signi cantly to the UK’s growth and diversity.

My advice to potential borrowers caught within this rental spiral –come to A n Bank.

What would you like people to know about you outside of work?

Outside of work, you will nd me getting my hands dirty in the garden, getting my feet dirtier running a Tough Mudder obstacle course, or cleaning up a er my two rambunctious little daughters – I wouldn’t have it any other way! ●

A n bank

Established 2021 (VOP in 2024)

Mortgage and buy-to-let products, specialising in visa holders and selfemployed borrowers

Contact Tippie.Malgwi@A nbank.com 07353 963884

In today’s market, brokers are on the front line of helping first-time buyers navigate a path to homeownership – a path increasingly obstructed by rising house prices, deposit shortfalls, and affordability challenges. That’s why the Chancellor’s Mansion House speech and subsequent commitment to a permanent Government-backed Mortgage Guarantee Scheme is a welcome step forward, providing it is done in a sensible and prudent way that supports customers, particularly when times are hard.

Supporting first-time buyers into homeownership is at the heart of what we do in the mutual sector, and this measure is a vital step in helping those with smaller deposits access the market.

The housing challenge in the UK is not just about supply, it’s about affordability. Many would-be homeowners, especially younger people and those affected by economic instability, have been locked out of the market due to rising house prices and deposit shortfalls. Underwriting more higher loan-to-value (LTV) mortgages through this scheme provides an important lifeline and helps shi the balance for those on lower incomes.

We’re also supportive of the Bank of England’s recommendation to allow a higher mortgage lending limit over 4.5-times income, alongside the Financial Conduct Authority’s (FCA) work to simplify remortgaging rules. These reforms reflect a broader willingness to engage with the realities faced by today’s first-time buyers.

For our part, we must continue to ensure that the mortgages people take on are right for their circumstances, especially if times become hard. These initiatives must also go hand in

hand with be er financial education and long-term saving incentives that support deposit-building, including the preservation and promotion of the Cash ISA.

Delaying potential plans to cut Cash ISA limits, and being willing to take more time to consult with industry experts as well as listening further to the public, is a positive step forward.

In the lead up to the Mansion House speech there was significant pushback from customers, the press, and the financial services sector, and we applaud the Treasury’s willingness to engage meaningfully with our industry to explore other possible solutions.

As advocates for responsible saving, we remain firm in our commitment to promoting Cash ISAs as an accessible and impactful tool for financial empowerment. For many of our customers, particularly those saving for a deposit on their first home, Cash ISAs provide a tax-efficient way to grow savings without undue complexity or risk.

For the moment, the Cash ISA and its existing limits are safe, but reform of this savings product may still come, with more details expected to be confirmed in the Autumn budget.

Many customers choose Cash ISAs as they simply cannot afford to risk losing their hard-earned capital investing in stocks and shares. For those that can, access to low-cost financial advice remains a barrier, with less than 9% of the UK population receiving financial advice last year.

Too many people remain unsure of how or where to invest their money, particularly those from underserved communities or younger savers navigating the financial

JONATHAN WESTHOFF is chief executive at West Brom Building Society.

Many would-be homeowners [...] have been locked out of the market”

landscape for the first time. If we want people to invest, we need more initiatives to bridge the ‘advice gap’. We also welcome the FCA’s current consultation to provide a simpler regulatory framework in this area.

The Chancellor also confirmed that there will be a marketing campaign to inform customers of the merits of investing in the Stock Market and how this could further benefit customers’ long-term savings. Any messaging to customers that reinforces and raises awareness of these established savings products – and the importance of savings – is a positive, providing the risks are also made clear.

Empowering people with access to trusted, affordable financial advice is not only key to increasing engagement and building trust with financial providers, but also vital to improving confidence and outcomes in long-term investment. By investing in tools, platforms, and education initiatives that demystify financial planning, the Government and financial sector can encourage a broader culture of investment, ultimately strengthening economic resilience and social mobility across the UK.

As a mutual, we want our customers to build a secure future for themselves and their families, and as such would welcome any strategies or initiatives the Government introduces which helps us and brokers achieve this. ●

made simple with

made simple with

made simple with Afin

made simple with Afin

Empowering underserved borrowers with tailored mortgage solutions and a human touch.

Empowering underserved borrowers with tailored mortgage solutions and a human touch.

Empowering underserved borrowers with tailored mortgage solutions and a human touch.

Empowering underserved borrowers with tailored mortgage solutions and a human touch.

At Afin Bank, we believe everyone deserves the opportunity to build their dream home and financial future. That’s why we specialise in helping borrowers who are often overlooked by traditional lenders, including diaspora communities, selfemployed professionals, and those with unique financial circumstances.

At Afin Bank, we believe everyone deserves the opportunity to build their dream home and financial future. That’s why we specialise in helping borrowers who are often overlooked by traditional lenders, including diaspora communities, selfemployed professionals, and those with unique financial circumstances.

At Afin Bank, we believe everyone deserves the opportunity to build their dream home and financial future. That’s why we specialise in helping borrowers who are often overlooked by traditional lenders, including diaspora communities, selfemployed professionals, and those with unique financial circumstances.

At Afin Bank, we believe everyone deserves the opportunity to build their dream home and financial future. That’s why we specialise in helping borrowers who are often overlooked by traditional lenders, including diaspora communities, selfemployed professionals, and those with unique financial circumstances.

Why Choose Afin Bank?

Why Choose Afin Bank?

Why Choose Afin Bank?

Why Choose Afin Bank?

Tailored lending solutions

Tailored lending solutions

Tailored lending solutions

Support for Diaspora clients

Tailored lending solutions

Support for Diaspora clients

Support for Diaspora clients

Flexible options for professionals

Support for Diaspora clients

Flexible options for professionals

Flexible options for professionals

Self-employed friendly

Flexible options for professionals

Self-employed friendly

Self-employed friendly

Human expertise meets technology

Self-employed friendly

Human expertise meets technology

Human expertise meets technology

Human expertise meets technology

For professional intermediary use only

For professional intermediary use only

For professional intermediary use only

For professional intermediary use only

Find out more about us

Find out more about us

Find out more about us

Find out more about us

Jessica Bird speaks with Eric Bierry, CEO at SBS, about the evolution of the business and the lending tech landscape

Global fintech company SBS services more than 1,500 institutions across 80 countries, including the likes of Santander, Société Générale, and Kensington Mortgages. It provides a cloud-native, API-first platform that supports core banking and lending, payments, compliance and digital engagement.

In almost 28 years in fintech, CEO Eric Bierry has seen this market go through many stages of evolution – experience that he brought with him when he joined the firm in 2016, going on to lead the merger between Sopra Banking Software and Axway in late 2024.

e Intermediary sat down with Bierry to understand SBS’ recent evolution, and how tech is shaping the future of financial services.

To stay at the crest of the wave, four years ago the business made the decision to transform from a service-focused firm to a software company. This meant moving away from a model of bespoke tailoring for each new client, to focusing on creating an optimised product.

Bierry says: “Our heritage is that we were tailoring a lot of solutions for our clients, which was seen at that time as a benefit for them as we were doing exactly what they were expecting. But when we looked at the speed of the banking market, especially, the ability to go super fast is critical; when everything has been done very specifically for the client, the ability to move fast becomes very difficult.

“We wanted to rationalise the way we were going to market, and which products have to be, let’s say, ‘protected’ for the future.”

This was not a change that happened easily or overnight, he adds: “It took us nearly three years to pilot the company within that new strategy, and ensure that our clients were not only following our strategy, but accepting the plan to standardise a lot more.”

The rationale to make this change, in the first instance, was to improve business outcomes for clients, but it also had the added benefit of allowing SBS to reduce costs and improve its own business performance.

In the UK, SBS has a particularly strong grounding in providing software solutions for the building society market, numbering 21 clients in that sector alone. The willingness of building societies to engage with modern technology strategies might surprise some, considering their lower profit margins and physical roots in both communities and historical processes.

For Bierry, the two are not mutually exclusive, particularly as SBS respects the traditions that underpin the mutual model.

He explains: “There is a very strong competitive advantage that building societies have in the market, which is the ability to really engage physically, closely with their members.

“Of course, many other big financial players are compensating for their inability to be

close to their clients by enabling more digital options. That has been the reality of the past six to eight years. But the role of these building societies to address the market in their own way is crucial.”

While building societies have tended to maintain their physical local presence, they are still investing in automation and digital processes to support efficiency and growth. Most of this, Bierry explains, has happened in ways that those outside the institutions might not see or be aware of.

While building societies might still be seen as “more old-school” when it comes to the digital perspective, this is largely due to the focus of tech advancement being in the back office, where other financial institutions prioritise customer-facing tech.

Looking ahead, however, Bierry warns that this model must change.

He says: “That model is not going to be enough for building societies. Many of them, when they have less than £3bn or £4bn assets under management will start to be too small to stay independent.

“They have two options to stay independent – to modernise and diversify to engage with a larger client base and with more services, or continuing to reduce their costs.

“Of course, many of the CEOs of building societies are more business developers than people aiming to just reduce costs. Also, just reducing costs is going to put them on the menu for consolidation.

“We don’t see the building society market growing by itself – we see there being more consolidation, because of the margins. But we do also see that they are keen to find ways to grow and diversify.

“That’s an opportunity for us to bring what we are doing with banks across Europe and give them that support.”

A factor further shaping the use of tech in the building society market is that these lenders are “not as much in competition as others,” and while competition can spark innovation, this allows them to “share many things” rather than view progress as something to be coveted.

Looking beyond building societies to the UK financial services market at large, Bierry sees many opportunities for greater digital adoption. He says: “Compared to European markets, the UK market has a bigger appetite for digital and the adoption of new models.

“When looking at the complexity of mortgage business, the UK is the most advanced mature

market compared to many other countries in Europe, so that appetite to move forward and take risk is stronger. That’s a very important differentiator.”

This could, in part, be due to the UK model of shorter terms meaning a greater need for tech and efficiency as people engage with their mortgage provider, and potentially change lender, more regularly. Bierry also adds that the regulatory environment has a lot to do with it.

“The regulated approach is not seen as the first driver for moving things forward in the UK, unlike many other countries,” he explains.

“For example, faster payments has not been a regulatory decision, and it worked here a lot earlier than in other countries in Europe. In the UK, we see the ability of the market to move itself without waiting for the Government to make the decision.”

Whether a building society with 200 years of history in a local area, or large financial institutions with vast embedded systems, the challenge is always going to centre around how to evolve and adapt without taking a toll on daily operations.

This is particularly the case when it comes to processing platforms, says Bierry, as engagement platforms tend to be less reliant on legacy systems.

He continues: “On the processing side, it’s very difficult for a bank or financial institution to see the benefit and support the risk of migration. That’s the first blocking factor.

“Their core business is not going to change, so why take the risk and put so much money on the table to make that move?”

Another hindrance to progress is the fact that, historically, many financial institutions felt they were differentiated in the way they were going about providing mortgages and savings products. This meant having systems that were tailored to their business down to the minute specifics. That, Bierry says, no longer makes sense.

He says: “They must accept standardisation – processing is processing, we can spend tonnes of hours and not find anything that really differentiates one brand from the other. The differentiation comes in the way they originate, engage, design the products, and drive aftercare.

“There are many ways for financial institutions to differentiate themselves, but processing alone is not one of them.”

Of course, whether or not it is the right move to standardise, migrating legacy systems is still →

a hard task for many, not least when this might be seen as a hygiene factor – shifting in order to continue functioning smoothly, rather than to create any clear business or profit gain.

To make this transition easier, Bierry says: “Those legacies can stay, but they can stay with conditions – adopting a standard, opening up those legacy systems and adopting all the necessary APIs, and bringing down the time to market expected by financial institutions.”

He adds: “We are already seeing the benefit for 18 or 19 of the building societies we work with today, which have adopted these standardised systems. Then, they can focus on the product catalogue and how they engage with clients.”

Standardisation is also a benefit for those smaller businesses that may not have the resources adopt the most advanced, bespoke technology. Instead, without having to invest in tailored specifics, smaller businesses are better able to compete and focus on growth, which has a broader positive effect on the health of the overall market, through better competition.

Bierry says: “This is not an easy decision to make at first, but once made it is an easy execution. A building society with less than £1bn of assets under management cannot afford to do a two-year IT programme, so their only way to survive is to stay focused on growth and business development, how they want to be seen as different as a niche player, rather than spending money and time on IT and back office processes.”

Any discussion of the tech underpinning the modern lending landscape inevitably rolls around to artificial intelligence (AI), either with excitement for its capabilities, or trepidation about the brave new world it heralds.

For Bierry, the discussion is moot until financial services gets better at leveraging data.

He says: “Historically, financial institutions don’t like to use the data they already have. It comes from their DNA – a history where people were coming to their bank in person to deposit physical money is still part of their processes.

“So, the first step is accepting the use of data – with or without the use of AI.”

When it comes to the dawning use of AI in financial services, whether a reality or a a future discussion, the biggest fear tends to be around the safety of customer data. This is not unfounded, and the growing conversation around public large language models (LLMs) is fuelling this concern. However, not all systems are created equal, and SBS has its own

proprietary AI system, allowing it to be used locally by a lender, without either pulling in unvetted external data or allowing internal data to be dispersed elsewhere or “exposed to the public cloud.”

While this format is more limited in scope than LLMs such as ChatGPT, it is about finding systems and tools that are fit for purpose and work with the “real use cases lenders are expecting to deliver to the market.”

With the realities of audit trails, GDPR compliance and Consumer Duty requirements pressing heavily on all financial services businesses, those in this market that do not enter into the tech and AI conversation are not just going to struggle to compete, but may face nasty compliance shocks along the way.

When it comes to this progress, Bierry adds: “For those of our clients that have not yet matured into using these systems, it’s not because of privacy concerns, it’s because they need to have the right data. They need to decide the way they want to leverage that data, and they need to decide what kind of use case they would like to go to the market.”

Naysayers in all markets will warn against the use of AI, of course. Bierry notes that often this is about a misunderstanding of the solutions out there, and a lack of awareness that closed systems do exist.

On the subject of growing this awareness, he says: “This is going to take years. And the speed of the market is not going to allow for the fact that teaching people is going to take years.”

Part of the solution to this is transparency and communication, not least because AI comes in various diverse forms, many of which the average person interacts with throughout their day without even realising.

For example, it is important to distinguish between generative and predictive AI.

Predictive AI is widely used – from making shopping recommendations to risk modelling and identifying suspicious patterns in fraud detection. Generative AI, meanwhile, is the “next stage” in the evolution. This is centred around the actual creation of content, from personalised marketing through, potentially, to mortgage agreements and KFI documents.

The vast majority of the use cases in financial services at this stage are predictive. Bierry points to the use, for example, in preventing or anticipating defaults.

He says: “It’s a lot better to engage with your client three months before a default, proposing something to help them, rather than waiting for the default and then entering into a very difficult conversation.”

As it stands, “nothing is missing” to implement these systems, which can provide a net positive for both the lender and the consumer. Bierry explains: “If you have two or three years’ experience with the client, plus their profile, some evidence of events that might trigger something, you can run your model and find that there is an 80% chance they are going to face a problem in three months. Then, the person taking care of the client can make the decision to engage with and assist them.

“That client is going to be more loyal longterm, and if you explain that usage to clients, no one is going to think it’s dangerous. Everyone benefits – the risk to the bank is reduced and the client feels well-served.”

This will become easier with younger generations, who arguably are less focused on the theoretical risk, and have already proven more willing to engage with systems like Open Banking. Indeed, the next generation will likely move elsewhere if the use of tech does not fit their standards.

To help bring others on the journey who might still be reluctant, Bierry says: “It’s the responsibility of the financial institutions to clearly publish the way they are using the data of their client. They are more or less already obliged to do that. Then, engage with some use cases and be super transparent.”

Despite being cautious to engage in too much prophesying, Bierry paints an interesting picture of the future. In five years, he says, the next generation may go through the mortgage process having never engaged with someone from the bank.