LATER LIFE ▮ e latest from Key Later Life, LiveMore, ERS and more MEET THE BDM ▮HSBC and Lendco take the spotlight in a double-header INTERVIEW ▮Kay Westgarth talks later life lending and innovation Intermediary. The www.theintermediary.co.uk | Issue 3 | April 2023 | £6 PICKING UP THE PIECES

later life lending market post mini-Budget DIGITAL EDITION

The

From the publisher...

And just like that, Q1 2023 is done. It’s amazing how quickly time can pass, as it only feels like a couple of weeks since Christmas. In the first three months of the year, the UK managed to avoid both the recession and the catastrophic house price crash that were predicted by some of the market’s biggest players and institutions.

Indeed, the Bank of England itself was speculating that the UK would be in recession come Q1. That recession, it anticipated, would last for five quarters, with the country set to emerge this time next year. Thankfully for us all, the country has managed to avoid the Old Lady of Threadneedle Street’s predictions for now.

That is despite the best efforts of erstwhile Prime Minister Liz Truss and her Chancellor Kwasi Kwarteng. The human hand grenade, as she was allegedly nicknamed by Boris Johnson, exacerbated the impact of global economic issues on these shores and, in the process, almost tanked the entire economy.

She’s now on a tour of the political speaking circuit, justifying why she was right and why those she refused to listen to, such as pesky economists, the Permanent Secretary to the Treasury, and the Office for Budget Responsibility, to name but a few, were all

The Team

Ryan Fowler Publisher

Felix Blakeston Associate Publisher

Jessica Bird Managing Editor

Jessica O’ Connor Reporter editorial@theintermediary.co.uk

Claudio Pisciotta BDM

claudio@theintermediary.co.uk

Maggie Green Accounts

finance@theintermediary.co.uk

Barbara Prada Designer

Bryan Hay Associate Editor

Lorraine Moore Subscriptions

subscriptions@theintermediary.co.uk

wrong. A er all the fallout, it turns out she was indeed right. Luckily for us, her mooted comeback has gone down like a fart in a li . Hopefully, the duo of Truss and Kwarteng will remain far away from frontline politics in the future.

In this issue, we look at the impact that the pair’s September 2022 mini-Budget had on the later life market in our feature on Page 34. Hannah Smith looks at how the market has been working hard to support borrowers and brokers in a financial world that has changed significantly over the past six months.

We also catch up with Kay Westgarth of Standard Life Home Finance to discuss how the firm is navigating the challenges faced by the later life, and indeed the entire, mortgage sector. You can find that interview on Page 48.

As we look ahead at the coming months, it remains to be seen what impact the banking scare will have and if it is set to turn into a fullon crisis. Bank of England Governor Andrew Bailey thinks not, and has played down talks of a banking crisis in a speech to the IMF.

The question now is if his comments will pave the way for further interest rate rises, in a market already feeling the strain. ●

Ryan Fowler

Contributors

Aaron Scott | Alison Pallett | Amanda Wilson

Andrew Dignum | Andrew Gething | Bill Purves

Damian ompson | Darren Deacon | David Jones | David Kempster | Ellen Fell | Emily Chisnall | Graham Evans | Grant Hendry

Gregor Sked | Hannah Smith | Jacqui Gillies

Jerry Mulle | Jon Dunckley | Jonathan Sealey

Jonathan Stinton | Karen Woodley | Louise

Chapman | Louise Pengelly | Lucy Barrett

Maeve Ward | Mark Blackwell | Mark Gillis

Martese Carton | Matthew Cumber | Matthew

Dilks | Michael Conville | Miranda Khadr

Neal Jannels | Paul Brett | Ranjit Narwal

Richard Rowntree | Robin Johnson | Sam

Simmons | Shaun Almond | Steve Carruthers

Steve Cox | Steve Goodall | Stuart Cheetham

Stuart Law | Tanya Elmaz omas Cantor

Tim Hague | Tom Denman-Molloy | Tom Lee

Tom Rowlands | Tony Marshall | Will Hale

www.uk.linkedin.com/company/the-intermediary @IntermediaryUK www.facebook.com/IntermediaryUK

www.theintermediary.co.uk

Copyright © 2023 The Intermediary Cover illustration by Klawe Rzeczy (Photos ©UK Parliament/Jessica Taylor, HM Treasury Zara Farrar, Adobe, Unsplash) Cartoons by Giles Pilbrow Printed by Pensord Press CBP006075 ▮ latest from Key Later Life, LiveMore, ERS and more ▮ and Lendco take the spotlight in double-header Kay Westgarth talks later life lending and innovation Intermediary. The PICKING UP THE PIECES The later life lending market post mini-Budget April 2023 | The Intermediary 3

Buy-to-let. Better.

Choose Landbay and you’ll find experts at the end of the line, smart technology designed for you, and fast decisions you can count on.

FEATURES & REGULARS

Feature 34

Hannah Smith looks at the challenges faced by the later life lending sector

Local Focus 76

This month The Intermediary takes a look at the housing market in Ipswich

On the Move 94

An eye on the revolving doors of the mortgage market: the latest industry job moves

SECTORS AT-A-GLANCE

Residential 6

Buy-to-let 40

Later Life 52

Specialist Finance 58

Technology 72

Second Charge 80

Protection 84

Local Focus

INTERVIEWS & PROFILES

Meet the BDM 46

LENDCO

Graham Palmer on what makes Lendco stand out from the crowd

The Interview 48

STANDARD LIFE

Standard Life Home Finance’s sales director Kay Westgarth discusses navigating challenges, innovating products, and preparing for Consumer Duty regulations

Q&A 60

SAXON TRUST

Brian West and Andrew Gardiner from development and bridging specialist Saxon Trust speak about the firm’s growth plans

Q&A 86

LV=

Sarah Watts, head of intermediary at LV= General Insurance, reflects on the brand’s first year in the intermediary market

Meet the BDM 18

HSBC UK

Siobhan Moran on the challenges and opportunities facing the mortgage market

The Intermediary | February 2023

Contents

76

Consumer Duty rules shift the goal posts significantly

March is always a busy month for those in finance. The end of the tax year and the Spring Budget can have significant implications for businesses in the mortgage market, and importantly, our customers.

In the longer-term view, though, we have a more pressing issue in the shape of the Consumer Duty, which becomes enforceable from 31st July.

Four outcomes

The rules include: a Consumer Principle that requires firms to act to deliver good outcomes for retail customers; cross-cu ing rules providing greater clarity on the Financial Conduct Authority’s (FCA) expectations under the new Principle and helping firms interpret the four outcomes; and rules relating to the four outcomes the regulator wants to see under the Consumer Duty. These represent key elements of the firmconsumer relationship which are instrumental in helping to drive good outcomes for customers.

These outcomes relate to products and services, price and value, consumer understanding, and consumer support. The la er is particularly relevant if arrears continue to grow.

The FCA requires firms to consider the needs, characteristics and objectives of customers – including characteristics of vulnerability – and how they behave at every stage of the customer journey. As well as acting to deliver good outcomes, firms will need to understand and evidence whether those outcomes are being met.

It’s quite the shi , from suitable product at point of sale within the boundaries laid out by a firm’s

authorisation permissions, to the forward-looking consideration of outcomes.

While my feeling is that all lenders, networks and intermediary firms are supportive of the principle of this regulation, there is distinct nervousness about the process of adhering to it. There is nothing fundamentally new compared with the original regulatory framework in 2004, or the Mortgage Market Review (MMR) in 2014, but the regulator is clearly frustrated about the lack of clarity, and possibly the lip service being paid. So it’s the evidence that is the fundamental shi here.

Where is this duty handed off from one regulated entity to another? Should the process and evidence base be the same for advisers in branch versus independent brokerages? Is the regulatory responsibility held by appointed representative (AR) networks sufficient to cover both lenders and ARs? What is the personal responsibility for this duty of care when it comes to individual advisers?

How should lenders, networks and advisers judge vulnerability? How should they document their reasoning? The regulator said Consumer Duty does not remove the responsibility from consumers, but the vulnerable customer tag would certainly imply a higher level of duty.

Where is the line? What constitutes the basis for a legitimate legal challenge that argues an adviser failed in their regulatory obligations?

Ultimately, Consumer Duty requires firms and advisers to ensure they are in no way causing ‘foreseeable harm’ – something that an industry with fewer grey hairs than ever before may find a challenge. ‘How they behave’ is also enshrined into the regulatory wording, but what

does that mean, and how can it be responsibly assessed when people react in individual ways to the stress – or not – of executing a mortgage or remortgage application?

Covering the bases

There is no one straightforward answer, or one process that will allow lenders and intermediaries to ensure they’ve done what’s required. Forms, questionnaires, personal assessments, and customers agreeing to sign confirming they are comfortable with the recommendations – we simply do not know if this will cover all liability bases. In basic terms, it’s impossible to know until it becomes law and there are test cases available for scrutiny. Processes relating to the duty are not going to be perfect on day one.

We cannot know how the regulator will supervise this new regulation until it becomes real. There are things we do know, though. The good old 80:20 rule will inevitably apply. Networks are more likely to be asked to provide examples of how advisers have approached, assessed and executed advice, but the regulator may force lenders and networks to have even closer working relationships, as the former police the la er.

Ensuring the regulation is implemented successfully is going to be a priority for the FCA. Particularly when it shi s the goal posts so significantly. Be assured, there will be a desire to demonstrate the return on investment in developing and delivering these new rules. Enforcement will be the tool, and firms must be ready. ●

Opinion RESIDENTIAL The Intermediary | April 2023 6

TIM HAGUE is managing director of Sagis

Speak to our property finance team today 0344 225 3939 borrow@ccbank.co.uk ccbank.co.uk/mixeduse Help your clients discover new investment opportunities and broaden their property portfolio. With potential for higher yields, longer leases and increased tax benefits, your clients could diversify their property portfolio. For intermediary use only. Cambridge & Counties Bank Limited. Registered office: Charnwood Court, 5B New Walk, Leicester LE1 6TE United Kingdom. Registered number 07972522. Registered in England and Wales. We are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Financial Services Register No: 579415. Our authorisation can be checked at the Financial Services Register at www.fca.org.uk. Up to £15m borrowing per customer Interest only option available Debt service cover of 130% considered from net rental income Your clients can unlock the best of both worlds with our mixed-use loans HADDOCK & SPICE VASE HADDOCK & SPICE VASE ROAST & SPOKE BLACK COFFEE HADDOCK & SPICE VASE ROAST & SPOKE BLUE Fresh GROUND COFFEE TEMPEST BIKES Key highlights: Up to 70% LTV 2 years property investment experience Consider all commercial property types No restrictions on property numbers Get in touch for further details about our lending criteria.

Retaining clients and importance of the advice process

Everyday mortgage brokers help thousands of people onto and up the housing ladder. In fact, 80% of mortgage business is now conducted through a broker.

But despite the valuable role many brokers play in the homebuying journey, our data shows that just over a quarter (26%) of borrowers who were introduced to Coventry Building Society via a broker got back in touch with us directly when looking to remortgage.

With this in mind, it’s key that brokers evaluate their client retention strategies, particularly as the current climate is prompting more borrowers to lock in new deals ahead of any further interest rate rises. So how can brokers improve client retention and avoid losing out on these valuable opportunities for more business?

1 Proactive communication

It is in brokers’ best interests to create and foster a dynamic relationship with clients beyond the mortgage journey. By giving clients regular updates on changes in the market, as well as providing

information during key stages in their mortgage journey – from the initial application to assessment and affordability checks – brokers will keep the line of contact open and ensure they are on the front foot when it comes to securing additional business opportunities. It is also essential to strike the right balance between being overbearing and staying in touch. Ge ing it right will mean clients create new associations in their minds with the broker as someone who always provides the most relevant advice and has their interests at heart.

2 The power of tailored marketing

Making use of a variety of marketing strategies can help brokers to stay in touch with clients during the ‘in-between times’. Content marketing strategies such as newsle ers are a great way of updating clients on what’s happening in the market and why it’s relevant to them. Contact can be tailored to different types of clients – first-time buyers, landlords, downsizers – and cover a range of timely topics to help clients keep up with the evolving market.

Blogs are another good way to share

content with clients whilst improving rankings on Google. A study by HubSpot found that businesses that blog saw their monthly leads rise by 126% against those who don’t blog.

3Engaging through social media

Social media is a useful way to reach multiple clients at once without being overly intrusive. Many brokers are already social media savvy, with a continuous presence on traditional platforms like Twi er, Facebook and LinkedIn.

More recently, short-form video formats like TikTok and Instagram have rapidly increased in popularity, including amongst brokers. Some brokers have already taken their expertise to TikTok, with 10% of brokers revealing they have created a TikTok video for professional use and 36% finding the platform ‘invaluable’. These platforms allow brokers to create distinctive and personable content for a wider audience. By simplifying complex topics and cu ing through technical jargon, brokers can also tap into the Millennial and Generation Z demographics. Whatever their preference, these communication tools provide invaluable opportunities to connect and resonate with clients, pu ing brokers at the forefront of customers’ minds when it comes to future mortgage decisions.

These steps can go a long way in making clients feel that their broker is a real human who understands their issues, and who they can rely on for all their mortgage needs. ●

Opinion RESIDENTIAL The Intermediary | April 2023 8

JONATHAN STINTON is head of intermediary relationships at Coventry for intermediaries

Customer retention: The advice process is more valuable than ever

WE KNOW YOUR CLIENTS WON’T ALWAYS FIT THE MOULD.

— We take into account earned income up to the age of 70, or even 75 if the client is in a non-manual role.

— We’ll consider pension pots, as well as fixed pensions, investment and rental income. Other income can be considered on a case-by-case basis.

— We lend in retirement with higher maximum ages than most lenders.

— We have a common sense approach to lending and use human beings, not robots, to underwrite each case. This means we can tailor our solutions to each of your client’s needs.

US, FLEXIBIL I

I N LA

LIFE

W ITH

TYGETS EASIER

TER

How can we help?

FAMILY BUILDING SOCIETY, EBBISHAM HOUSE, 30 CHURCH ST, EPSOM, SURREY KT17 4NL Family Building Society is a trading name of National Counties Building Society which is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. National Counties is on the Financial Services Register. Firm Reference Number 206080

CALL

OR EMAIL mortgage.desk@familybsoc.co.uk

FIND OUT MORE AND SEE JUST HOW FLEXIBLE WE CAN BE! VISIT intermediaries.familybuildingsociety.co.uk

US ON 01372 744155

THAT’SWHYWEOFFER FLEXIBLE SOLUTIONSFORLATERLIFELENDING.

Intermediaries critical as owners face remortgaging

For many homeowners with a remortgage on the horizon, the outlook could fairly be described as challenging. The

Office for National Statistics (ONS) believes that more than 1.4 million households in the UK face the prospect of an interest rate rise when they renew their fixed rate mortgages this year.

For many, the rates they are offered could be significantly higher this time round. ONS data also finds that 57% of fixed rate mortgages coming up for renewal in 2023 were fixed at interest rates below 2%. But the Office for Budget Responsibility (OBR) forecasts that the Bank Rate will peak at 4.8% towards the end of the year.

That means, according to ONS estimates, that if the interest rate on a £300,000 mortgage increases from 2% to 6%, based on a 25-year capital and repayment mortgage, the monthly mortgage repayment would go up from £1,272 to £1,933 – an increase of 52%.

Repayments shock

It’s not hard to see why figures like that are cause for alarm, especially against the backdrop of the cost-ofliving crisis. Inflation, while forecast to fall over the course of the year, is still eroding spending power and wage growth.

The shock of an increase in repayments of that size is going to be even more stark for the growing cohort of borrowers on longer fixes. There has been an increase in the popularity of 5-year fixed rate mortgages in recent years. In Q4 2021, UK Finance said that these accounted for the majority (60%) of all fixed rate mortgages taken out by homeowners, up from 42% in Q4 2016.

Historically low interest rates over the past decade will have been a contributing factor to that rise. But the uncertainty caused by Brexit also played a significant part in many people’s decision-making, with many choosing to lock in for a longer period in an a empt to secure some stability during volatile times.

‘Great Resignation’

A further dimension to this trend which should not be overlooked is the number of people currently locked into longer fixed-rate mortgages who will have had a career change in that period, in particular those who have become self-employed.

According to the Association of Independent Professionals and the Self-Employed (IPSE), the self-employed population grew continuously up to 2019. While it dipped slightly during the pandemic, the subsequent ‘Great Resignation’ has seen more people choose to strike out on their own.

It’s reasonable to expect that a decent proportion of those who took out a fixed mortgage five years ago may have done so as a full-time employee, but will now be looking to remortgage as self-employed. We know that this is a segment of the population which can find it harder to secure a mortgage.

Borrower support

Where does all this leave those facing a remortgage over the coming months?

It’s important not to be too alarmist. There are options out there, and as a lender we are ramping up our support to borrowers who be struggling with their repayments.

However, with such a fast-moving – and at times complex – landscape to navigate, I firmly believe that the role of the intermediary

community in supporting borrowers through the process has never been more important.

It’s likely that borrowing over a longer term will become a more popular option as a way of maintaining affordability; however, that will see more people paying back loans into their 60s and 70s.

Likewise, against a backdrop of squeezed affordability, we can expect to see product transfers become a more a ractive option to many – but that won’t necessarily be the best option for everyone.

Holistic approach

These are decisions which should not be taken lightly, and the best way to get a holistic assessment and an impartial recommendation is through an intermediary.

Research from Mintel last year found 85% of people said they would seek mortgage advice for their next mortgage, whether than be a mortgage broker, independent financial adviser (IFA), online broker, or bank or building society adviser. That figure is encouraging.

Through intermediaries, homeowners have the best possible route to ensuring they navigate the options and land on a solution that is right for them. ●

Opinion RESIDENTIAL The Intermediary | April 2023 10

ALISON PALLETT is sales director at Nottingham Building Society

The best way to get a holistic assessment and an impartial recommendation is through an intermediary”

Removing housebuilding targets a backwards step

April sees the Levelling Up Bill reaching its final Parliamentary stages. The Government’s consultation into its proposed planning changes has now closed, and the industry awaits its response with anticipation.

As a result of the new Bill, the Government’s manifesto commitment to build 300,000 new homes each year by the mid-2020s could be confined to the annals of history. Rather than there being a specific Government target for house building, the government wants to make councils responsible for developing local plans for new housebuilding levels.

Everyone agrees that there is no silver bullet when it comes to solving the UK’s housing crisis but nationally set housebuilding targets exist for a reason. Indeed, The Home Builders Federation previously warned that scrapping the 300,000 annual targets could lead to 100,000 fewer homes

each year being built and deprive the economy of £17bn in housebuilding and supply chain output. This is simply unacceptable.

Housing costs are at their most unaffordable level for over a century:

There is li le doubt that home ownership remains the preferred tenure of choice for millions of people. Although demand for housing continues to increase, we are facing a chronic shortage of homes resulting in soaring house prices which drive deposit requirements and mortgages ever higher. This means first-time buyers are finding it harder than ever to get on the ladder and it is now the hardest time to afford a home since our founding year in 1875, a sad reflection of decades of Government inaction to tackle the UK’s housing crisis.

But the longer-term aim for the Government must be to address the drastic shortage in housing. The issues facing homeownership are deeprooted and wide-ranging but building

enough homes to meet demand is the right place to start.

Achieving these targets will be difficult, and it will take all parts of the market to deliver this level of housebuilding, from private developers to housing associations and local government, but with enough political will, a decades-old problem can surely be overcome and would start to deliver on the homeownership aspirations of millions of people.

Through the decades

To understand why we have a chronic shortage of housing it’s worth looking at the history of post-war Government housebuilding strategies in the UK.

There was a huge shortage of housing in post-war Britain – with over half a million properties being destroyed by air raids during the war. It was estimated that around three million new homes were needed immediately and as a result the government aimed to build over 300,000 new homes each year. However, there were shortages of builders, materials, and money.

Many ‘non-traditional homes’ were built using various prefabrication approaches, which pushed up housing output to 354,000 new homes in 1954. As a result of these new building approaches, total annual new housing completions soared, and peaked in 1968 at around 400,000 – the highest ever annual level.

The 1960s was the decade of tower blocks, and the availability of new homes pushed up owner occupation levels still further. The decade saw the largest number of new homes

Opinion RESIDENTIAL The Intermediary | April 2023 12

MARTESE CARTON is director of mortgage distribution at Leeds Building Society

4 3.5 3 2.5 2 1.5 1 0.5 0 1950-59 1960-69 1970-79 1980-89 1990-99 2000-09 2010-19

Number

of houses built each decade (millions)

built at over 3.5 million. Since then, the number of new homes built each decade has declined and the latest figures show that just over 1 million new homes were built in the 2010s –the lowest level since the war.

Despite the continued increase in demand for homes the number of houses built has declined decade upon decade, reducing by 69% since the end of 1960s.

Government housing policy has changed over time. Whereas slum clearance was a key priority in the 1950s and 1960s, it is no longer central to the current Governments housing policy. Post-war Britain saw the large-scale demolition of sub-standard housing. Between 1953 and 1985 over 1.5 million homes were demolished

because of slum clearance – displacing around 3.8 million people.

The removal of so many properties, and the inability to build sufficient homes for a growing and everchanging population has been central to the housing crisis we now see today.

Housing targets help to catalyse supply as well as providing consistency and stability – all things the market desperately needs as we seek to rebalance supply and demand.

Trade-off

We need a national conversation about the reasons why we’re building homes. It’s understandable that people are protective of their communities and don’t want undue disruption or pressure on services and

infrastructure, but the trade-off is between that, and millions of people being blocked from the benefits home ownership brings.

Those supporting the effective removal of the 300,000 housing targets argue they want to put control in the hands of local people. We agree this is an essential component of deciding the development of communities, but this is no reason why the Government should step back from having nationally published housing targets.

With the affordability of home ownership now at its worst point for 150 years and housebuilding levels at post-war lows, it is clear that housing must be a key ba leground at the next General Election. ●

Opinion RESIDENTIAL April 2023 | The Intermediary 13

Housing targets help to catalyse supply as well as providing consistency and stability, all things the market desperately needs as we seek to rebalance supply and demand”

Package cases well so lenders can help you and your client

EMILY CHISNALL is underwriting service optimisation manager at Accord Mortgages

Try to respond to document requests as soon as possible. At Accord, requests for documents are visible as soon as the lending decision –or decision in principle (DIP) – is submi ed, and assessed as soon as they are received. The earlier they are submi ed, the earlier they can be assessed.

Othercommitments

e understand that brokers want to provide the best service possible to clients, giving them the best advice they can, and finding the product to suit their needs.

But once you’ve chosen a product, the speed at which a lender can turn around their offer is out of your control, isn’t it? Well, no. Not completely.

There are actually lots of things brokers can do to help lenders ensure a case goes through as smoothly as possible. Any improvements, however small, will benefit everyone involved – saving time for you, your customer and your lender, with the added bonus of helping to build relationships all round. So, to package a ‘best-in-class’ case, where do you start?

First, it’s a good idea to check whether your chosen lender has any specific advice on how to package a case – each lender might have slightly different requirements, so it’s important to be aware of these.

At Accord, we have a page on our website dedicated to packaging top tips. Here, I will take you through some of the key things to consider.

WChecking personal details

This is a pre y basic one, but you’ll fall at the first hurdle if the personal details are incorrect. Make sure that your client’s name and address are up to date. Proof of identification and inevitable delays may result if not.

Providing documents

Every case will require a certain amount of document submission, so it’s important to provide what’s been requested as soon as you can. Here are some things to bear in mind: Upload your documents at the same time, if you can, so that we have them all at once for when the case is reviewed;

Don’t forget about extra documents which could be required for selfemployed clients or contractors, like business bank statements in addition to personal statements; Don’t send us more than we ask for – if we need something else, we’ll let you know;

It’s possible that further items might be needed later on. Underwriting is pre y fluid, so there could be a request for more information if something else comes to light;

If there are any debts or financial commitments outstanding when we receive the application, it will slow things down if they are not declared, so make sure these are included up front. These include things like: Declaring childcare costs; Including details of debts, however small, like student loans or credit card debt; Details of any other properties if they are to be included in the affordability calculation.

Pay any initial costs to get things moving

This is a simple one, but could easily be forgo en. A valuer will o en be instructed as soon as the valuation fee is paid, if there is one, so ensuring that this is done will help get the ball moving nicely.

It’s a two-way street

Brokers increasingly have direct access to underwriting teams –that’s certainly the case at Accord – so it’s easier than ever to have a two-way conversation. Lenders are always looking for ways to make improvements – it helps you, and us, to do our jobs be er, and helps your clients. That’s ultimately what we’re all here for. ●

Opinion RESIDENTIAL The Intermediary | April 2023 14

Stay ahead with best-in-class packaging

than just the one cherry on top

More products. More opportunities. More “Well, that was easy” moments.

Now that we offer buy-to-let mortgages as well as bridging loans, we will continue to do the extra special but with more solutions and for more of your clients.

For hands-on help with your specialist lending enquiries, get in touch with the team that makes good things happen.

mt-finance.com

FOR INTERMEDIARIES ONLY

Meeting the challenges of climate change

Climate risks are driving significant asset value exposure risks for lenders. It is vital, therefore, that lenders have a clear understanding of how this could affect mortgage offers in the future.

Nevertheless, there is an absence of direction from lenders to their conveyancer panels to verify future risks. This is a big miss, as the data is available and both parties need to be in sync. It’s important that the findings from climate analysis in environmental searches are translated into actionable advice, particularly given the incoming Law Society guidance on climate risks.

Some forward-thinking firms, especially commercial lawyers, are starting to join the dots and see advice on climate risks and use of search report analysis as a way to help discharge their duties. However, it is important that this is not a ‘nice to have’ option for lenders. There are treating customers fairly (TCF) considerations, and lenders have a duty of care to their borrowers.

It’s good that the Law Society is looking to implement guidance on climate due diligence – ge ing on the front foot. Overarching ethical and operational guidance will help conveyancers avoid future litigation exposure. Given their requirements with the Prudential Regulation Authority (PRA), you’d think lenders would be responding similarly.

If lenders want conveyancers to triage risk on their behalf and improve the information flow back to them, they need to admit that and mandate it. They should be specific in their Part 2 and Part 3 instructions. The UK Finance handbook should include climate analysis into the

future in its environmental search due diligence guidance.

We have witnessed a clear acceleration in extreme weather events, driven by human input from greenhouse gas emissions over the past 40 years. As our atmosphere warms, more moisture is created and provides localised, heavier rain. At the start of April, we learned England has endured its we est March in more than 40 years. According to the Met Office, England recorded 111.3mm of rain, almost double the average level. This presents major issues for homebuyers and owners in terms of making their properties more resilient, and investing in measures to mitigate against the risk.

While successive Governments have channelled millions into flood defences to protect priority communities from the river network, there are still thousands of undefended streams. The insurance bill for 2020 floods alone stands at £375m.

Major considerations

The tapering off of Flood Re as a support to the most vulnerable, and high premiums or excesses for those just outside of this extra support, means there are major considerations at play for homebuyers and business owners. Insurers may vary their cover in response, but could lenders offer be er terms for those households that have taken out flood resilience measures as an extra incentive?

As the we er areas get we er, so the drier areas get drier. We have just recorded the driest February since the 1960s. The record-breaking 2022 heatwave brought with it a surge in subsidence claims through clay shrink-swell impacts. Meanwhile, sea levels could rise by as much as 1m in the next century, accelerating coastal

erosion. Whole se lements could be given up to the sea.

Many properties now have a shorter lifespan and will be unmortgageable and uninsurable. Some cash buyers may walk into transactions with eyes wide open, but some will become trapped. Many will end up staring at a total loss on their investment.

Look at buyers in Hemsby, who bought on the understanding that there could be 30 years le . They are now staring at a total loss within five years.

This is only going to be be er understood if the homebuyer, lender and conveyancer benefit from joined up climate predictive analysis.

I want to challenge lenders to step up to the plate. With The Law Society set to issue guidance, lenders must start to insist that their panels manage climate risks in the transaction, and mirror the risk management here in a joined up way.

This joining up should be across the board, not le to individual lenders. A concerted policy decision by the representative bodies is in order. ●

Opinion RESIDENTIAL The Intermediary | April 2023 16

DAVID KEMPSTER is a director of Groundsure

If lenders want conveyancers to triage risk on their behalf and improve the information flow back to them, they need to admit that and mandate it”

Racing you to your customer’s new home

Withautomaticcreditsearches,affordabilitychecksandadynamicrulesengineassessinghow yourcustomerfitsinourresidentialmortgagerange,ourportalisworkingwhileyouaretoget youadealfasterthanaboxonatrolley(wethink,wenevercheckedhowfastshe’smoving).

if you do

Mortgagesmadesimple Search | LendInvest LendInvest Loans Limited is authorised and regulated by the Financial Conduct Authority (FRN:737073). Lendinvest Loans Limited is a wholly owned subsidiary of Lendinvest plc. Borrowing through LendInvest involves entering into a mortgage contract secured against property. Your property may be repossessed

not

Register

repay your mortgage in full.

Meet The BDM

How and why did you become a BDM?

A er being a mortgage and protection manager with HSBC UK for six years, I was approached internally to see if I would be interested in the business development manager (BDM) job because of my knowledge of our products and policies, and the Northern Ireland mortgage market as a whole.

I met with Paul Norgate, head of North Region, and straight away was blown away by his enthusiasm and what an exciting opportunity it would be to get involved in bringing HSBC UK Intermediaries to the Northern Ireland market.

e BDM role is very much relationship-driven and I knew that my already established relationships internally and externally in the Northern Ireland market could bring a lot of value to the BDM role.

What brought you to HSBC UK?

I joined HSBC 12 years ago a er completing a graduate programme with another high street lender. During the graduate programme I carried out various roles, but ultimately it was the mortgage role that appealed the most to me. I found it so rewarding and satisfying, as it provided the opportunity to help people at an important point in their lives.

I became CeMAP qualified during the programme, and I was keen to gain further experience with another high street leader. e timing was perfect, as an opportunity arose within HSBC just as I was finishing.

I have been able to continue to focus on my personal development throughout my career with HSBC.

The Intermediary talks to Siobhan Moran, BDM, Northern Ireland at HSBC UK, about the challenges and opportunities facing

the mortgage market

I am a board member of Women in Banking and Finance, and head up their Personal Excellence programmes for the UK.

What makes HSBC UK stand out from the crowd?

We are constantly listening to feedback from our brokers, and this is reflected in the amount of positive policy changes we have made. is is alongside heavily investing in technology to ensure our broker platform works well.

In addition, we have a fantastic team that enables us to answer thousands of queries a month through our chat facility and our broker support helpdesk.

What do you think are the main challenges facing BDMs right now?

e first challenge is acclimatising to life back on the road and having face-to-face meetings, whilst also handling high volumes of emails and calls. Having said that, we have a brilliant broker support team to help us and also our chat facility gives brokers quick access to a member of our experienced UK-based broker support team who are always happy to help with quick queries, and can also provide case updates.

e second challenge is the downturn in the mortgage market when we still want to increase our market share. Buyer interest is low, reflecting low levels of

The Intermediary | April 2023 18

house purchase activity seen in recent months. With this downturn and borrowing becoming more expensive, many prospective buyers are now priced out of homes they could previously afford. With demand shrinking, sellers are being forced to drop the asking price. ird, due to the increased cost of living, affordability has tightened. We have to work even closer with our broker partners to maximise affordability to help get cases over the line.

Finally, interest cover ratio (ICR) is a big challenge currently for bringing in buy-to-let (BTL) business. Any existing BTL mortgages are likely to increase once their current rate comes to an end, and with an everincreasing emphasis on stress rates and ICR, landlords are faced with some real challenges to meet the current market condition.

Now more than ever, it is really important for BDMs to keep up to date with rate and policy changes to stay ahead of the game.

What are the opportunities?

2023 is going to be a record year for product maturities. ere are £370bn of product maturities in 2023, £35bn more than 2022, so the total refinance market is set to grow this year. 2023 is therefore a massive opportunity for brokers and their customers to review their remortgage and product transfer needs. Year on year we have seen growth in the total number of product transfers, and more importantly the share of broker product transfers has gone up from 27% in 2018 to 40% last year in the residential space.

With stress testing being based on a lender’s standard variable rate (SVR), an increase in the Bank of England base rate could impact what financial institutions can lend. For those on variable or tracker rates, there will be many households that can’t afford an increase in their monthly mortgage payment.

is is the perfect opportunity for our broker partners to reach out to their customers and really make the most of the substantial remortgage and product transfer opportunity.

Brokers have such an important role to play during the cost-ofliving crisis in order to get the best deals for their customers and their individual circumstances.

e evolving landscape means that there is more of an incentive to look at a full remortgage rather that a product transfer for further funds in order for customers to restructure debts. is is another area where broker advice becomes invaluable across the coming year, and HSBC UK is very much here to support these opportunities.

How do you work with brokers to ensure the best outcomes for borrowers?

Communication and visibility are vital, especially in the current climate and the uncertainty with the Bank of England and the increased cost of living. Collaborating and building knowledge to ensure brokers are up to date on our products, key lending criteria and the economy as a whole, is a priority for us.

I organise regular events where a local economist presents to my brokers about trends specifically relating to the Northern Ireland economy. Richard Beardshaw, head of intermediary sales at HSBC UK has also been invaluable by attending these events and providing HSBC UK’s thoughts on the economy, how we decide to price, and our predictions for the mortgage industry.

I also regularly hold mortgage workshops and online masterclasses in order to educate brokers on our criteria and any policy enhancements. ese sessions, combined with our economy updates, provide my brokers with the confidence to use HSBC UK as their lender of choice, as well as the confidence to have quality conversations with their customers.

What advice would you give potential borrowers given the current climate?

e main thing is to act rather than be passive. Falling onto a lender’s SVR will almost certainly be more expensive than a new deal. e broker is more important than ever.

While house price growth may be slowing, inflation and interest rates are still high. is, combined with limited wage growth, means the affordability gap is widening. Moving onto or up the property ladder remains a significant challenge. Although rates have reduced in recent weeks, people are finding it increasingly difficult to choose the right mortgage deal.

Experts expect prices to continue to fall throughout 2023, and given the impact this could have on current and future finances, it’s wise to explore various options. A broker can consider unique personal circumstances, including current and future affordability, as well as the whole market, securing a competitive deal.

Brokers can help customers avoid unnecessary marks on their credit by matching them with the right mortgage lender to meet their needs, first time. ●

HSBC UK

Established 1865

Products

Residential Buy-to-let

International Residential

Additional Borrowing

Foreign nationals

Overseas customers

Foreign currency Let-to-Buy

Siobhan Moran

Email: siobhan.moran@hsbc.com

Telephone: 07795 676 861

April 2023 | The Intermediary 19 MEET THE BDM

Tracker mortgages mainstream again? Not likely

The mortgage market tends to go in cycles: if you stick around long enough, you’ll see the same trends reappear and then disappear again from time to time.

One of the more recent has been the supposed re-emergence of the tracker, which at one point could quite rightly claim to be the UK’s mortgage of choice.

Younger brokers may find it difficult to get their heads around just how popular the humble tracker was.

Roll back the clock to 2009 and they accounted for nearly seven in 10 new mortgages, according to the FCA.

However, for most of the 2010s swap rates were very low by historical standards, boosting the a ractiveness of fixed rate mortgages, which came to dominate.

Today fixed rates are so dominant, in fact, that they accounted for more than nine in 10 new mortgages at the end of last year.

So, why the sudden media interest in trackers? And does it mean they are once again set to become a mainstream mortgage option for the masses?

To answer the first part of that question, we are hearing more about this once-popular mortgage option because of our obsession with predicting ‘peak’ base rate.

Borrowers are being bombarded with headlines on a daily basis about how the peak base rate is in sight –and how rates may actually fall in the coming months.

For example, just last month Barclays predicted that base rate would peak at 4.5% and would fall by to around 3.5% by the end of 2024.

When borrowers read this, it’s natural they will ask whether it is worth taking a gamble on a tracker

now in the hope of lower monthly repayments in the future.

However, I find these days most people soon back away from the idea of a tracker when you outline the pros and cons.

Firstly, trackers no longer have much of a price advantage over fixed rates, which severely dents their appeal among borrowers.

Data from Moneyfacts shows the average 2-year tracker is currently 4.84% – just 0.48% lower than the average 2-year fixed rate.

Keen pricing

If the BoE does increase rates one or perhaps two more times, that miniscule rate advantage is gone.

Clearly, that can change quickly if lenders decide to price their tracker ranges more keenly, but at the moment that’s not the case.

Let’s not forget, also, that the BoE may take us all by surprise and increase rates much higher than expected.

A er all, it is adamant it will keep increasing rates until inflation falls consistently.

This is a key point. For all of the headlines we read about ‘peak’ interest rates, the reality is none of us really know what will happen to the cost of borrowing.

All it takes is worse-than-expected inflation data and the new ‘peak’ may be higher than we expected. Conversely, if inflation plummets, rates may be much lower in the medium-term. We just don’t know.

The reality is, the vast majority of borrowers prize security above anything else, even if it means locking in at a slightly higher rate today.

Recent data from LMS, the conveyancer, confirms this. It revealed that 54% of its clients who

LUCY BARRETT is managing director of Aria Finance

remortgaged in February opted for a 5-year fixed rate.

Of those, nearly two-thirds said they did so because they wanted security over their monthly repayments. Fixed rates have ruled the roost for so long that that mindset is baked into borrowers these days.

It’s worth noting also that when trackers were at their peak, in 2009, the regulatory landscape was very different to what it is today. This was pre-Mortgage Market Review and an era when non-advised sales were still permi ed. Back then, borrowers could walk into a branch and walk away with a tracker mortgage having gone through nothing more than a decision tree with a salesperson.

These days most borrowers must take advice. And most advisers would quite rightly point out that trackers are not suited as a mass-market product for the reasons I’ve outlined above. Therefore, it is no coincidence that trackers went out of fashion the same time that brokers came to dominate the marketplace.

I want to stress, though, that while I don’t think trackers will come to emulate their glory days, they do have a place in the market.

If the outlook for interest rates becomes clearer, they may well become more popular among certain types of borrowers, such as high-networth individuals who can afford to take the risk.

But like most trends, I think the current fixation with trackers in the press and among borrowers will be fleeting and normal order will soon return. ●

Opinion RESIDENTIAL The Intermediary | April 2023 20

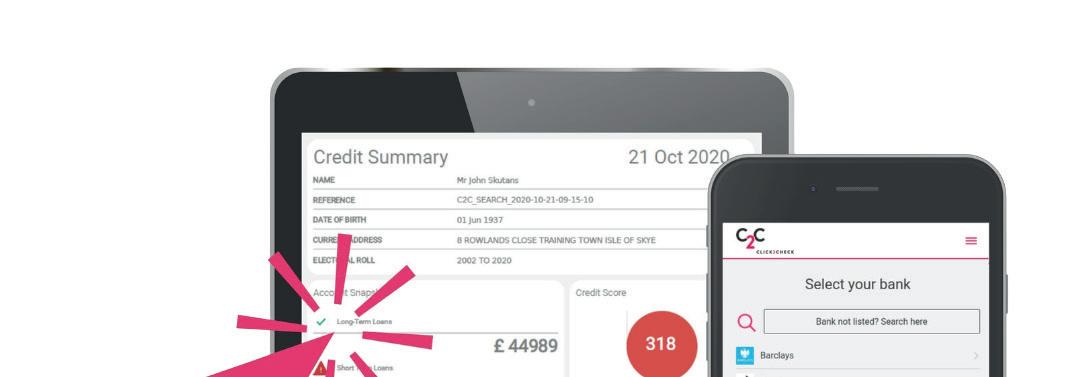

Seewhat Lenderssee beforethey seeit. Asingleviewofcustomer financialdatainreal-time C2Cpulls3sourcesof datatogethersupplying theadviserwithasingle viewinjustONECLICK AML Credit report Open Banking C2C reducestheworkloadandtimetaken byadvisers toprocessmortgageapplicationsbydeliveringa singleviewcreditsummary attheclickofabutton. Enablingadvisersto delivertherightloansolution to satisfiedcustomers–fast! SavesAdvisers£150perapplication Real-timeInformation Increasescompletionby107% www.click2check.com Call01932548888oremail sales@click2check.comfor moreinformation FCANumber:FRN775110

How do you define the ‘cheapest’ deal?

Logic tells us that if two loaves of bread of the same quality are priced so that loaf A is cheaper than loaf B, then clearly loaf A is the one we should buy. Indisputable fact. We can make the same case in an infinite number of examples. The key considerations are that there be no material difference in the makeup of the object or the impact the purchase will have on the person buying the product.

When assessing which mortgage is the most suitable for customers, having chosen candidates from the broadest selection of suitable alternatives that could match the borrower’s needs and individual circumstances, advisers then run into a kno y issue. Namely, the definition of which is cheapest.

The best mortgage

If we accept, without further scrutiny, that the best mortgage among those options which fulfil our customers’ needs is the one which has the lowest rate at outset, then are we really providing our customers with the ‘cheapest’ or just ticking a box and in fact not doing the job we are being asked to undertake?

Understandably, the regulator wants the best outcomes for customers and sees cost as the key determinant in assessing the right mortgage or lending arrangement to recommend. However, the obsession with ‘the cheapest’ has led to a skewing of the meaning. For advisers who use sourcing systems every day, the default se ing, a er all the data has been fed in, provides a list of lender products in order of headline rate cost – i.e. the cheapest available monthly payment at the start of the mortgage.

Job done? Hardly. What we should be ensuring is that the definition of ‘cheapest’ also pays a ention to value. Mortgages which have a notional

term of 25 years might have fixed or discounted rates over a set period within that notional term.

While a diligent mortgage adviser would ensure that their client remortgages before the SVR becomes applicable, the fact remains that just because a mortgage has the cheapest 2-year fixed rate at outset for example, it does not mean that it represents the best value for a customer who may not expect his or her mortgage to be the only mortgage they have in their lifetime and therefore look to pay it off early.

Headline rate

Let’s also not forget that comparing like for like can throw up anomalies that nullify the argument that the cheapest headline rate is, therefore, the best for the customer. What are the charges being levied associated with the mortgage with the cheapest headline rate?

How about the penalties for early redemption and particularly at this time when lenders are struggling to cope with the post national lockdown and stamp duty holiday housing market boom? Will the cheapest mortgage still be available when required and can it be processed in time to complete?

As an industry, we need to work with the regulator to clarify what ‘cheapest’ means to customers, so that the future definition reflects the actual value of our recommendation and mitigates any risk that we become glorified price comparison websites. The Mortgage Market Review demonstrated that the real value to customers lies in the advice that complements the product recommendation. The regulator’s investigation into the GI market and the disparity of pricing to new and existing customers provided evidence that headline rates do not necessarily offer a true reflection of the value of advice.

ALMOND is managing director of HL Partnership

With Consumer Duty around the corner, measuring outcomes replaces the ‘best intentions’ of treating customers fairly and as I have said before, being able to get a client a mortgage will be just the start of a process that measures a successful transaction not by achieving a mortgage offer and subsequent completion, but because it can be proven to be truly in the client’s best interests and most closely matches their needs. On top of that, there is a need to collate the transaction and client communication both during and a er the initial deal.

So, what if the deal is the ‘cheapest’ on paper if it loads the client up with unnecessary cost, for example in the case of using a remortgage for capital raising when the rate of interest charged for the remortgage is significantly higher than leaving the original mortgage in place and doing a second charge for the capital raising. And let’s not forget any ERCs! ●

Opinion RESIDENTIAL The Intermediary | April 2023 22

SHAUN

The regulator wants the best outcomes for customers and sees cost as the key determinant in assessing the right mortgage or lending arrangement to recommend”

Consumer Duty: The sourcing of vulnerability data

Vulnerability guidance raised the need to assess and consider the vulnerability of consumers.

Consumer Duty regulations have added the need to evidence this assessment, and show that we can monitor vulnerabilities over the lifetime of products.

For years, brokers have considered the situation of the consumer and taken into account any issues that have come to light. Most of this has been subjective and rarely documented, but all with good intentions. Consumer Duty comes into force from July, so we must now formalise this – just as fact-finds moved from a subjective, informal approach to a formal, documented process. But where do we get the data on vulnerability?

Many have searched for databases of ‘vulnerable people’, but unfortunately these simply do not exist. True, there is socio-economic data, which identifies cohorts of consumers, but this is generally at a postcode level, rather than a personal one. There is also credit data, which is personal, but this is limited to financial vulnerability and affordability.

Consumer Duty has expanded the scope of the vulnerabilities firms need to consider, monitor and evidence. While financial vulnerabilities are still important factors, firms now need to review all potential issues – including health and lifestyle, domestic abuse, divorce, and learning difficulties, to name just a few.

Larger tech firms use artificial intelligence (AI) to interpret and assess their voice and text interactions with consumers. This can certainly be useful for large lenders – to pick up complaints, for example – but it is limited to those consumers we

already communicate with, where the product is already in place. To meet the Consumer Duty’s requirements, we must assess vulnerability prior to onboarding new customers.

The Financial Conduct Authority’s (FCA) Financial Lives survey identified that around 50% of all consumers are vulnerable, but just who are they in any given group? The only practical and workable way to definitively locate that 50% is to screen all consumers.

Direct assessment

In practice, the only robust approach is to assess all consumers directly, at the point of sale, and to continue to do so on an ongoing basis. For mortgage brokers, this becomes an integral part of the sales process, just like the factfind. The next big challenge is how to be consistent in the assessment, so others can understand vulnerability data today and in the future.

Companies training front-line staff have quickly found that everyone’s interpretation of vulnerability is different. It’s a bit like everyone deciding who is ‘rich’ or ‘poor’ –without guidance you simply end up with multiple answers, based on differing subjective viewpoints. The more we understand about the considerable variations of health and lifestyle issues, the cost overhead of training becomes prohibitive.

A far be er approach is to use an assessment tool which encompasses an objective and consistent way of measuring vulnerability. For example, the MorganAsh Resilience System (MARS) generates a MARS Resilience Rating – this is much like a credit score, but for client vulnerability.

Brokers don’t need to remember the specific level of vulnerability which applies to, for example, domestic

abuse, heart a ack or divorce, because these are all embedded within the tool. Furthermore, MARS includes different options to gather information – either by broker assessment or by the consumer completing an online assessment.

In practice, those firms using the training approach typically only identify a small proportion of vulnerable customers – usually in single figures. In contrast, those using MARS report vulnerability levels at around 50% – in line with the FCA’s findings. Such a clear disparity shows that it will be tough for many firms to ensure fair value or that products meet clients’ needs – key areas of focus set out by the FCA.

Monitoring is a vital part of the duty. Firms are expected to evidence and stand behind customers’ outcomes. Not surprisingly, the FCA’s recent multi-firm review identified that investing in technology and data strategy is a key priority.

Whether as a standalone system, or integrated into an existing customer relationship management (CRM) system, technology can now not only mitigate the challenges of collecting vulnerability data, but help deliver a competitive advantage. ●

Opinion RESIDENTIAL April 2023 | The Intermediary 23

ANDREW GETHING is managing director of MorganAsh

Firms are expected to evidence and stand behind customers’ outcomes”

A huge opportunity to

Given the rise in the base rate from its December 2021 low of 0.1% to its current 4.25%, the corresponding rise in mortgage rates is unsurprising. That does not mean that borrowers have planned for it, though. More than a decade of mortgage rates that were unbelievably cheap, when viewed within a historical context, has changed borrowers’ expectations.

Adding real value

The scale of the challenge for homeowners, and the opportunity for brokers to add some real value, is clear. The Office for National Statistics (ONS) put a figure on it at the start of the year. More than 1.4 million households in the UK face the prospect of a significant interest rate rise when they renew their fixed rate mortgages in 2023. By the ONS’ summation, 57% of fixed rate mortgages in the UK coming up for renewal in 2023 were fixed at interest rates below 2%.

While many borrowers will cope, for some this is going to be a very challenging period.

In the first quarter of this year, 353,000 fixed rate mortgages will have to be renewed, and borrowers will inevitably see their mortgage rates more than double, with monthly repayments rising by hundreds of pounds for many.

Monthly increase

Looking at different indicative amounts le to repay on mortgages from £100,000 to £500,000, ONS analysts said that, should the interest rate on a £100,000 mortgage increase from 2% to 6%, assuming a 25-year capital and repayment mortgage, the monthly repayment on the same mortgage would increase by £220, from £424 to £644.

Assuming the same increase on a £300,000 mortgage, monthly repayments would rise by £661, from £1,272 to £1,933.

You don’t need me to tell you how serious this is. For borrowers who

have high loan-to-values (LTVs) and are facing remortgage this year, it’s extremely worrying for their personal finances and general health. The volume of unhelpful doom-mongering headlines does not help. Thankfully, some rational and expert help is at hand. For brokers, this is both a challenge and an opportunity. Brokers have a chance to once again illustrate the true value

The Intermediary | April 2023 8

MICHAEL CONVILLE is chief customer officer at Newcastle Building Society

Opinion RESIDENTIAL

help customers

they offer borrowers, and lenders need to step up and play their part in supporting them.

In a bull market, with competitive rates and high LTVs abounding, it’s easy to get a mortgage, provided you have your deposit and a job.

In the market we face today, however, it is much, much harder. Borrowers have been scared out of their wits by unhelpful national newspaper headlines spelling out the absolute worst-case scenario as though it were inevitable and unavoidable.

Hugely misleading

This is what I mean when I say that the pervading sense for many is that it’s impossible to get a mortgage or remortgage. This is hugely misleading. As we all begin to understand the real risks and consider affordability in its real light, I believe

there will be increasing room for lending. The headlines always tend to generalise, especially when writing about a market that is so incredibly diverse. It’s impossible to render its subtleties into headline-worthy words or numbers accurately.

This is why we must remember that this is a market of infinite nuance. Not everyone is in dire straits. In fact, the majority of homeowners with a mortgage are going to weather this period of economic hardship just fine. The majority of homeowners will be able to remortgage, they just won’t achieve it simply by searching the best buy tables or hi ing the ‘renew’ bu on online.

Value of expertise

This is why broker advice is going to be so critical in the coming months. It is always valuable, but in this market

the value of experience and expertise is almost unquantifiable.

When things are uncertain, people’s reflex reaction is to avoid the unknown. That’s when the reassurance that a broker can offer is at its most valuable and appreciated.

Make things work

For brokers, this is also when the ability to pick up the phone to speak to an underwriter, a person with their own financial responsibilities, is the difference between sending a client away and finding a way to make things work.

This year isn’t going to be plain sailing. But that’s when common sense, pragmatic thinking and business comes into its own – and that’s something I and the team here at Newcastle Intermediaries believe in very strongly. ●

April 2023

Opinion RESIDENTIAL

London’s key role in levelling up

Levelling up A favourite phrase among Conservative politicians who insist it is what they will deliver, and the opposition who claim Government cannot. Personally, I take a more pragmatic stance.

I was interested, therefore, in the Budget announcement earlier in March, when the Chancellor reaffirmed previous premier Liz Truss’ promise to create 12 new regional industry-focused hubs.

Albeit a watered down version, Jeremy Hunt honoured that vision –and honestly, it is an admirable one. We do not know as yet which areas specifically will benefit from the funding, for which they must bid, but we do know that the very process should act as a catalyst for further regional investment.

The funding up for grabs is £80m per site, split ‘flexibly’ between investment and tax incentives.

Priority sectors

The binding aim is that each site aligns itself with academic centres of research focused on the Government’s stated priority sectors, which include digital, tech, advanced manufacturing, green and clean, life sciences and the creative industries.

It is a laudable endeavour. I hope, sincerely, that it does come to spur the economic growth so needed within the UK at the moment.

Hunt’s March Budget also acknowledged the considerable wider economic challenge facing the UK economy.

The Office for Budget Responsibility (OBR) published forecasts coinciding with Hunt’s statement that the UK will avoid recession this year and that inflation will plummet from over 10% to under 3% by the year end.

This may be so. I hope it is. A stable economy will be extremely good news for everyone.

However, I am also acutely aware that forecasts rely on historical data. Did anyone foresee the crippling rise in the cost of living that followed the hundreds of billions of Government bailout support packages? If they did, they were not heard. Everyone else was living in the present. Focused on survival now, not on double-digit inflation on the price of milk.

This reminds me to think of the future in terms of the present. Yes, also with reference to the past.

I do not doubt that everyone living in the UK hopes Government promises to level up industrial and commercial opportunity will come to fruition.

Wouldn’t a renewed financial services hub thriving on cu ing edge technology – be it in Edinburgh, Leeds, Manchester or Teeside – be welcomed by everyone?

Those there already,and others encouraged to move with the offer of prosperous employment, would boost the local economy considerably.

Multiply that effect beyond financial services and into all of those potential growth sectors named by the Chancellor in his speech, and yes, the effect on GDP growth could be huge. I really hope it is.

Experience tells me, though, that these things take decades to deliver. While this is all the more reason to invest in them, it is just as compelling a reason not to rely on them for immediate economic relief.

Levelling up cannot be a ‘Robin Hood’ policy that neglects the cashcow of London and the South East. We will need to balance the act of redistribution more carefully.

In prosperous times when there is money going begging for investment opportunities, more risk is tolerable. I am not wholly convinced this is where we sit currently. We all fervently hope inflation subsides this year – though we must recognise that its effects over the past 12 months have inflicted damage on household

ROBIN JOHNSON is managing director of Kinleigh Folkard & Hayward Professional Services

finances that will not be repaired by a future fall in the consumer price index (CPI).

Healthy economy

This brings me back to London, and just how central it is for the health of the UK economy, and most importantly, its ability to thrive in challenging circumstances. It may sound like a cliché, but when London suffers we all do. It is for this reason that Government will divert just as much a ention and funding into rebuilding the capital and its economy, perhaps more.

Consider the relaxation of rules governing companies listing in London. Consider, too, the advantageous capital relief on offer to companies in the UK, the focus on research and development, and the £27bn tax cut for business through ‘radical’ full expensing announced by Hunt in March.

In an ideal world, diverting more of the UK’s wealth to areas outside of London will help our domestic economy in the more immediate term, and consequently, our international clout longer-term.

In practice, the easier and more reliable win is to shore up London and its hugely profitable professional and financial service sectors. It will have implications for the value of property in these localities – implications we shall be watching for expectantly. ●

Opinion RESIDENTIAL The Intermediary | April 2023 26

Reality bites: Chancellor does not hold Aces

The Budget delivered on 15th March was long-awaited, with Chancellor Jeremy Hunt under considerable pressure to reassure markets that the UK is back to being run with a steady hand.

A er a year of turmoil in Whitehall, Hunt’s job was even harder following the backlash that former Chancellor Kwasi Kwarteng’s miniBudget precipitated, crashing the bond market, the pound, and international confidence in the UK.

There was much emphasis placed on stability in Hunt’s speech, and on reliability, emphasised by the instruction that the Office of Budget Responsibility (OBR) publish its projections on the same day.

While there were welcome announcements on pensions, though, there was li le to please first-time buyers or homeowners.

The housing market has had an unusual few years, largely as a consequence of the pandemic. The total freeze in transactions that ensued following the announcement of the first lockdown was the trigger for then Chancellor Rishi Sunak to implement the Stamp Duty holiday.

Forced into an early introduction following a leak to the media, the tax break had an enormous effect on both the housing market and the economy. The desired effect – restarting transactions – was swi , and there’s no doubt the policy did provide much needed support at a difficult time. Yet, as with almost all short-term fiscal incentives, it has also distorted the market significantly.

Not only did the tax break encourage activity, it pushed house prices up at an alarming rate. This was exacerbated – and perhaps enabled –

by the simultaneous cut in the base rate to 0.1%.

Mortgages had never been cheaper and people rushed to secure a home while the sun shone. The race for space, changes in working and living priorities, and access to cheaper finance converged to push prices up.

Clickbait headlines

Things have changed since then. House price inflation – running over 10% – has fallen back as the Bank of England steadily hiked the base rate. However, we should also remember that annual price inflation recorded by the Office for National Statistics (ONS) remained at 9.8% in December – hardly the crash that clickbait headlines would have us fear. Our own House Price Index – which includes cash and mortgage transactions –reveals that from the start of the pandemic in March 2020 to January 2023, prices rose by some £64,900, or nearly 21%, which contrasts with the increase in general inflation including housing of 14.9% over the same period. Property prices have thus risen in real terms. Our market is clearly more nuanced.

Boosting homeownership and house prices is always a political win – it’s a quintessential British dream for those hoping to be er their financial situation, and for those already on the ladder, rising values are a welcome salve as we all fork out hundreds of pounds more on energy and the weekly food shop.

While we might think housing is due a new support scheme – the Stamp Duty holiday ended 18 months ago, Help to Buy on 31st March, and with onerous mortgage rates, existing and would-be homeowners are not having a great time – it does not present a systemic risk.

The Government is in a tricky position. Voters are under significant financial pressure. The red wall that put the Conservatives back in power is increasingly dissatisfied. Younger voters face high and rising rents, receeding opportunities to buy, and uncertain job prospects.

We knew the economy would suffer in the wake of the pandemic, but the reality of high inflation resulting from the hundreds of billions of pounds in support packages, combined with an energy crisis, has been more painful than many taxpayers have experienced before.

The available options to please voters were few.

Though unexciting, the pensions giveaway is a significant boost for older voters and for the public sector –those already weathering the costof-living storm without too much trouble. This is the Conservative Party’s heartland, and its safe policy. Pu ing the bellows under housing, less so.

Millions are facing considerable payment rises when they remortgage. Millions more are likely to require lenience from their lender to get through. For individuals, it will not be comfortable, but for the economy and broader inflation, there is sense in not launching another stimulus scheme.

The Bank of England’s monetary policy specifically puts the breaks on housing. Undermining that through fiscal policy would be an odd decision, given the threat inflation continues to pose.

It may not be the news we were all hoping for, but this Budget was always going to be a large dose of reality. This might be what returning to an economy built on work, not money printing, looks like. ●

Opinion RESIDENTIAL April 2023 | The Intermediary 27

STEVE GOODALL is managing director of e.surv

Improving the homebuying experience

Over the years we have heard plenty about how to improve the homebuying journey, but where do we currently stand?

A er the chaos of the early pandemic, where the housing market effectively shut down for a short time, we saw a landslide of purchase business across the residential and buy-to-let (BTL) markets.

Buyer demand

This chain of events placed huge additional burdens on surveyors, lenders, intermediaries and conveyancers. Much of this stemmed from pent-up buyer demand, and a Stamp Duty holiday which further accelerated appetites and served to increase both demand and house prices across much of the UK.

This was also a time when many firms and lending institutions across the mortgage market were still ge ing to grips with a new set of working conditions in the wake of Covid-19, and the difficulties this generated from a service, delivery and scalability perspective. The result was a rise in the prominence of – and reliance on – a range of online tools, systems and solutions throughout the homebuying journey.

Faster and more accurate

Having said that, the need for remote valuations was evident way beyond this period, as pressure on the industry was already growing to improve offer times without compromising quality, accuracy or integrity.

Moving forward, the ability to collate as much property-related information as possible, allowing purchasers to make more informed decisions earlier in the process, is

key to any ongoing improvement. As such, there is a constant appetite to explore how to deliver a faster, more accurate and lower risk remote valuation model.

This is one of the reasons why we initially developed PropertyFact, which has since evolved from a desktop-based tool into a more risk-based decision-making model, using data and information to help determine the best approach for an individual valuation.

World-leading market

From a speed, efficiency and data perspective, the Land Registry will play a vital role in elevating the homebuying experience. So, in August 2022, it was encouraging to see the non-ministerial Government department outline its strategy to enable a world-leading property market. This was a bold statement, as we are talking about a transaction which, as outlined in the report, can o en be viewed as unnecessarily complicated, opaque, stressful and susceptible to failure.

This strategy centres around five pillars:

Providing secure and efficient land registration;

Enabling property to be bought and sold digitally;

Providing near real-time property information;

Providing accessible digital register data;

Leading research and accelerating change with property market partners.

Some of the highlights within these pillars include the introduction of automation and digital services that integrate with conveyancing, making its data more accessible, interoperable

MATTHEW CUMBER is managing director of Countrywide Surveying Services

with other data, and reusable to increase its wider value, and working in partnership with others in the sector to build a shared vision for the property market.

There are many other commitments within these pillars, but I’m sure that these examples offer a flavour of both the aims and the challenges for a Land Registry which is looking to move to real-time or near-time registration of transactions with only the most complex cases requiring additional time and manual checking.

Streamlining information

As a business, we also have an important role to play in improving the homebuying experience. We need to educate more consumers, streamline the information required to buy and sell a home, develop innovative products, and deliver the service standards that homebuyers need and deserve.

This is an experience which we are fully commi ed to enhancing. ●

Opinion RESIDENTIAL The Intermediary | April 2023 28

The ability to collate as much property-related information as possible, allowing purchasers to make more informed decisions earlier in the process, is key to any ongoing improvement”

Control your uncertainties

he only certainty is that nothing is certain.” If ever a quote sums up the property market this is it.

The industry mostly uses historical trends and data to predict the future of property prices, and whilst useful, it’s rather crude. Every event that impacts pricing is different, with various sectors being winners and losers on each occasion.

12 months ago, both the commercial and residential markets were bouncing with confidence. Then came the appalling events in Ukraine, which impacted the economy as energy prices increased and inflation took hold. We all know what then happened on 23rd September 2022.

The total number of company insolvencies registered in England and Wales for 2022 was 22,109, the highest number since 2009, and 57% higher than 2021. Pre y grim reading.

However, the first months of 2023 have put a li le more bounce in our