Rachael Biddulph & Lisa Young

JUNIOR CYCLE SUCCESS BUSINESS BUSINESS BUSINESS BUSINESS BUSINESS The Ultimate Revision BookSAMPLE

89F Lagan Road, Dublin Industrial Estate, Glasnevin, Dublin 11, D11 F98N, Republic of Ireland. T: ++ 353 1 8081494 - F: ++ 353 1 836 2739 - E: info@4schools.ie

© 2022

ISBN 978-1-907330-44-5

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, including photocopying and recording, without the publisher’s written permission. Such written permission must also be obtained before any part of this publication is stored in a retrieval system of any nature. Permission requests should be directed to 4schools, 89F Lagan Road, Dublin Industrial Estate, Glasnevin, Dublin 11, D11 F98N, Republic of Ireland. or info@4schools.ie

4schools has attempted to contact all proprietors of images, texts and graphics included in this book. Proprietors we could not reach are requested to contact us.

E-BOOK How to claim and access your e-Book

To claim your e-Book

1. Log in to 4schools.examcraftgroup.ie/user/login

2. Activate your e-Book using the code above at 4schools.examcraftgroup.ie/activatecode

3. Download the app at 4schools.examcraftgroup.ie/apps

4. Log in to the app (please use the same login and password you used on the 4Schools website)

5. Download the e-Book

Notes

• Please ensure the email address used to complete the steps above is the email address of the student or teacher who will be using this e-Book.

• If the e-Book code was purchased using another email address, e.g., a parent’s, please register the email address of the e-Book user before completing the steps above. You can register the alternative email address here: 4schools.examcraftgroup.ie/user/register

Online Resources

Get access to exclusive content by scanning the QR code.

Code: https://4schools.examcraftgroup.ie/premium-content/junior-cycle-success-business

Published by 4schools

SAMPLE

Steps to Success

Topic 1

Topic 2

Managing my

Managing my

Topic 3 | The Savvy

Topic 4

Topic 5

Topic 6

Personal Financial Life

Starting an

Topic 7

Topic

Topic 9

Topic 10

Topic

Topic

Topic

Topic

World of

Marketing

The Bookkeeping Cycle

to

1

|

Personal Resources 03

|

Money 11

Consumer 19

| Insurance 27

|

Cycle 33

|

Enterprise 37

|

Work 43

8 |

53

|

59

| Introduction

Economics 73

11 | Demand, Supply and Equilibrium 83

12 | Managing Government Money 93

13 | Economic Performance 101

14 | International Business 113 SAMPLE

QR codes are also used throughout the book. Once scanned, these will allow you access to our bank of online resources to further assist you in your exam preparation.

HUG

Highlight - You should highlight the outcome verb in the question.

Underline - You should underline the key words in the question.

Glance Back - After you have written your answer, you should look back to ensure you have answered the question.

Throughout this book you will encounter the Key to Success information boxes. These boxes contain expert analysis, explanations, hints and tips from the authors that will help you maximise your grade in the examination.

Meet the authors

Lisa is a teacher of Leaving Certificate and Junior Cycle Business and Geography at Salerno Secondary School, Galway. Lisa is the co-author of Enterprise, a Junior Cycle textbook. Lisa has many years of experience teaching Junior Cycle Business Studies as well as providing workshops and seminars in the subject.

Rachael Biddulph

Rachael is a teacher of Leaving Certificate and Junior Cycle Business, Maths and Accounting at Dominican College, Dublin 9. Rachael has examined for the State Examinations Commission at both Leaving Certificate and Junior Certificate Business.

Rachael and Lisa have provided many workshops on teaching and learning methodologies for teachers of the business subjects.

Lisa Young

Lisa Young

2

SAMPLE

THE SAVVY CONSUMER 19 Topic 3 3.1 Definitions and Abbreviations 3.2 The Informed Consumer 3.3 Rights and Responsibilities 3.4 Letters and Emails of Complaint 3.5 Consumer Agencies 3.6 The Ethical Consumer THE SAVVY CONSUMER SAMPLE

3.1

Definitions and Abbreviations

False economy

A person who buys goods and services for their own use.

Buying an item without planning or thinking about the consequences.

Buying goods and services that seem to be good value but turn out to be more expensive in the long term.

Responsible for investigating complaints made by private citizens against government bodies and offices.

A consumer who understands what is right and wrong. They only buy products that are produced in a fair and honest way. They avoid exploitation of people and natural resources.

A balanced approach to buying goods and services which takes the environmental impact into consideration.

CRU

Definitions Abbreviations

Competition and Consumer Protection Commission

Advertising Standards Authority for Ireland

European Consumer Centre Ireland

Commission for Regulation of Utilities

Topic 3 20

Consumer Impulse buying

Ombudsman Ethical consumer Sustainability

CCPC ASAI ECCI

SAMPLE

3.2

The Informed Consumer

The informed consumer knows their rights and is always careful online.

Is this an impulse buy? Is this a false economy?

Can I afford this?

How do I make a complaint if there is a problem?

Are there any hidden costs? Is this item safe? Is there an ethical cost?

Be Careful Online

public Wi-Fi

using a creditcard or PayPal

Check your bankstatements regularly.

Question A

Damian and Margaret need to buy a washing machine. Their granddaughter Sadie loves the outdoors and often gets mucky, so the washing machine is very busy.

> Option 1 will last for 10 years with light use and cost €200.

> Option 2 should also last 10 years but has more functions including a setting for sports clothes which deals well with muck. It costs €299.

Which option would you recommend? Place a tick beside your chosen option. Give a reason for your answer.

Calculations 200/10 = €20 per year

Option 2 299/10 = €29.90 per year

Option 1 Option 2

Reason I would recommend option 2. It is more expensive per year but meets Damian and Margaret’s needs. Option 1 would be a false economy.

THE SAVVY CONSUMER 21

• Avoid

• Change passwordyourregularly• Use websitesauthentic only • Pay

•

Sample

SAMPLE

3.3 Rights and Responsibilities

Consumers are protected by three pieces of legislation.

Proof of Purchase is required for redress

The Sale of Goods and Supply of Services Act 1990 Goods Services Redress

Goods must: Services must be performed:

> Be of merchantable quality

> Be fit for purpose

> Conform to the sample displayed

> Be as described.

> By a skilled and qualified provider

> Using proper care and diligence

> Using parts and materials of merchantable quality.

Where goods and services do not meet these requirements, consumers are entitled to one of the following forms of redress:

> Repair

> Refund > Replacement.

Sample Question B

State which clause of the Sale of Goods and Supply of Services Act 1990 is broken in each of these scenarios.

Marie bought a waterproof jacket. She wore it out for a walk and her jumper was soaked when she got home.

Goods must be as described.

Damian's new jeans ripped at the seams when he wore them for the first time. Goods must be of a merchantable quality.

Karen bought a new sofa. When it was delivered it was not the same colour as the one they saw in the shop.

Declan’s car was serviced by an unqualified mechanic.

Goods must conform to the sample provided.

Services must be performed by a skilled and qualified provider.

Topic 3 22

SAMPLE

The Consumer Protection Act 2007

> Information about products and services should not be false or misleading and must comply with labelling laws.

> Prices must be displayed including all taxes and charges.

> Sellers cannot put pressure on customers to buy.

> Advertisements cannot mislead consumers or contain false information.

The Competition and Consumer Protection Act 2014

This Act protects the consumer by ensuring they know their rights and by monitoring the market to guarantee fair competition.

SAMPLE

Competition Product safety Enforcement

Makes sure there is competition between businesses which keeps prices low for consumers.

Ensures that producers and manufacturers meet health and safety standards for all products.

Established the CCPC which enforces Competition and Consumer Protection laws in Ireland. They have the power to fine and prosecute a business that breaks consumer law.

THE SAVVY CONSUMER 23

3.4

Letters and Emails of Complaint

Carmel Gray bought a new designer handbag for €300. While she was out with friends the handle ripped away from the bag. She brought it back to the store and was told she was not entitled to redress. Below is the letter of complaint she wrote to the store manager, Bernie Keegan.

Carmel Gray, Mealduin, Dunshaughlin, Co Meath.

10th of January 2024

Bernie Keegan, Designers 4 You, Cabra Road, Dublin 7.

Re: Faulty Handbags

Dear Ms Keegan,

I am writing to you in relation to a handbag purchased in your store on the 8th of December 2023.

I carried the bag for the first time on New Year’s Eve and within an hour of leaving the house the strap had broken off the bag. I returned it to your store on 5th of January 2023. I spoke to your store assistant Frances Kelly and she informed me that I was not entitled to redress. Under the Sale of Goods and Supply of Services Act 1980, the bag is not of Merchantable Quality.

I would like the bag replaced or a full refund of the €300 I paid for the bag. I have enclosed a copy of my receipt as proof of purchase.

Yours sincerely, Carmel Gray

Topic 3 24

SAMPLE

With a few minor changes, this can be changed to an email of complaint.

New Message

To: bernie.keegan@designers4you.ie

From: carmel.gray@gmail.com

Re: Faulty Handbag

Dear Ms. Keegan,

Main body as in the letter above.

Kind regards,

Carmel Gray

> Always quote a piece of consumer legislation.

> Include the date of the purchase and the date you are writing to the provider in the form Day/Month/Year.

> Be clear that you are making a complaint.

> State the type of redress you wish to receive.

> Always provide a copy of your receipt!

Test yourself

> Anne purchased a new oven on the 20th July 2022. She outlined to the sales assistant that it must have a self-clean function. When the oven was delivered and installed in her home, she noticed that it didn’t have the self-clean function.

Write an email of complaint on Anne's behalf to Susan Maguire, the store manager in Electric World.

THE SAVVY CONSUMER 25

Scan for Worked Solution SAMPLE

3.5 Consumer Agencies

There are lots of agencies that help consumers in Ireland:

> Competition and Consumer Protection Commission

> The Advertising Standards Authority of Ireland

> The Small Claims Procedure

> Ombudsman

> Commission for Energy Regulation

> European Consumer Centre Ireland

> Trade Associations

> Commission for Communications Regulations (ComReg)

> Commission for Regulation of Utilities.

You need to be able to explain three of these agencies.

Competition and Consumer Protection Commission (CCPC)

> Enforces consumer and competition law

> Protects consumer interests

> Informs and educates consumers.

> Ensures that all advertisements are legal, decent, honest and truthful

> Offers pre-publication advice

> Deals with complaints about advertisements.

3.6 The Ethical Consumer

> Last resort for consumers seeking compensation up to €2,000

> Judge listens to both sides and makes a decision.

> No solicitor required

The ethical consumer considers the impact of their purchases on the wider world. They ask a set of questions before every single purchase:

> How will this impact the environment? Pollution? Climate change? Natural resources?

> How will this impact people?

Exploitation? Child labour? Human rights?

> Will this purchase impact animals?

Animal testing? Animal cruelty?

> Is this a sustainable purchase? Does this purchase impact future generations?

Topic 3 26

The Advertising Standards Authority of Ireland (ASAI)

The Small Claims Procedure (Court)

SAMPLE

THE BOOKKEEPING CYCLE 59 FinancialStatements ecnalaBlairT regdeL BusinessDocuments Topic 9 9.1 Definitions and Abbreviations 9.2 Business Documents 9.3 Double Entry Bookkeeping 9.4 The Final Accounts 9.5 Test Yourself BOOKKEEPING CYCLE THE SAMPLE

Definitions and Abbreviations

A reduction in price given from one business to the other.

An extra reduction in price to encourage customers to pay in cash rather than using store credit.

The book of account book for all cash transactions. Moneycomingin is on the left, money going out is on the right.

List of balances of all a business’s accounts.

A

Abbreviations

of a business for the previous

Final AICS

Income Statement

Position

Topic 9 60 9.1

summary of all the financial transactions

year. Trade discount Cash discount Analysed cash book Trial balance Final accounts Definitions Value Added Tax Cash with Order Cash on Delivery Errors and Omissions Excepted Credit Transfer VAT CWO COD E&OE CT Business documents Account Analysed Cash Book General Ledger brought down carried down a/c ACB GL b/d c/d Bookkeeping

Statement of Financial

IS SFP

SAMPLE

9.2 Business Documents

There are nine business documents. You should be able to prepare each of these and advise businesses on what they should do with the final version.

Document Explanation

Letter of enquiry

Direction of document

Sent to potential sellers to enquire about the terms of sale and availability Buyer to Seller

Quotation Sent to the seller showing the prices of goods and the terms of sale Seller to Buyer

Order Buyer sends to their chosen seller detailing the items they wish to buy Buyer to Seller

Delivery note Accompanies the goods being delivered and lists the items and quantities

Seller to Buyer

Invoice A request for payment from the seller. It details the quantities and prices of items being sent. Seller to Buyer

Credit note Sent to the buyer to explain a reduction in the amount owed by the buyer Seller to Buyer

Debit note Sent to the buyer to explain an increase in the amount owed by the buyer Seller to Buyer

Statement of account Sent to the buyer to summarise all transactions made between both firms in a period of time Seller to Buyer

Receipt Sent by the seller as proof payment has been received Seller to Buyer

THE BOOKKEEPING CYCLE 61

SAMPLE

Sample Question A

Using the information given in the first line of the table, complete the invoice extract below:

€

Total (excluding VAT) 8,000 Trade Discount (10%) 800 Subtotal 7,200 VAT (23%) 1,656

Total Including VAT 8,856

Trade Discount 8,000 x 10/100 = 800 VAT 7,200 x 23/100 = 1,656

Sample Question B

Using the information given, complete and balance the following extract from the statement of account sent by McDermot Ltd to Norris Ltd.

Credit

Balance € 1/1/2022 Balance 2,000 6/1/2022 Invoice No. 220 2,600 4,600 10/1/2022 Payment by CT 3,500 1,100 19/1/2022 Invoice No. 250 820 1,920 25/1/2022 Credit Note No. 3 200 1,720

Topic 9 62

Date Details (-) Debit € (+)

€

SAMPLE

9.3 Double Entry Bookkeeping

The Analysed Cash Book The General Ledger

The Trial Balance

Sample Question C

Cooney Cosmetics have asked for your assistance with bookkeeping. Using the information provided, complete the Analysed Cash Book, General Ledger and Trial Balance of Cooney Cosmetics Ltd for the month of May and balance the account.

1/5/23 Patricia, the owner invested in the business €20,000

3/5/23 Sold goods €15,000 plus VAT@ 21%

10/5/23 Paid wages €3,000

15/5/21 Purchased goods for resale €8,000 plus VAT@ 21%

20/5/21 Paid electricity €680 25/5/21 Paid wages €3,000

Workings

Sales Purchases

15,000 x 21/100 = 3,150 15,000 + 3,150 = 18,150

8,000 x 21/100 = 1,680 8,000 +1,680 = 9,680

THE BOOKKEEPING CYCLE 63

SAMPLE

Analysed

Date Details Bank

1/5/23 Capital

3,150

15,000 3,150 20,000

1/6/21 Balance b/d 21,790

You should add up these columns

post the total to the opposite

of the General Ledger.

the

Topic 9 64

€ Sales € VAT € Capital

20,000 20,000 3/5/23 Sales 18,150 15,000

38,150

cash book of Cooney Cosmetics MoneyIn Balancing

account Balancing 1. Add up the debit bank column. 2. Add up the credit bank column. 3. Calculate the difference between the two. 4. Place the bigger number in both bank columns. 5. Use the balance to bring up the smaller side. 6. Carry down the final balance. DR = 38,150 CR = 16,360 Bal = 21,790

and

side

SAMPLE

MoneyOut

10/5/21 Wages 3,000 3,000

Purchases 9,680 8,000 1,680

Electricity 680 680

Wages 3,000 3,000

Balance c/d 21,790 38,150 8,000 1,680 680 6,000

should add up these

the

the

the General Ledger.

b/d should be on the

of the

the

of

side/bigger side on the first

THE BOOKKEEPING CYCLE 65 Date Details Bank € Purchases € VAT € Electricity € Wages €

15/5/21

20/5/21

25/5/21

31/5/21

1. Dates must contain day, month and year 2. Money in on the Debit Side (left) 3. Money out on the Credit Side (right) 4. All entries must in the Bank column and an analysis column 5. All columns must be totalled 6. Balance c/d should be on the smaller side on

last day

the month 7. Balance

opposite

day

following month after the totals. You

columns and post

total to

opposite side of

SAMPLE

Topic 9 66 Date Details F Bank € Sale € VAT € Capital 38,150 15,000 3,150 20,000 1/6/21 Balance b/d 21,790 Sales account Capital account Purchases account Electricity Wages VAT Date Details Bank € Date Details Bank € 31/5/23 Bank 15,000 Date Details Bank € Date Details Bank € 31/5/23 Bank 20,000 Date Details Bank € Date Details Bank € 31/5/23 Bank 8,000 Date Details Bank € Date Details Bank € 31/5/23 Bank 680 Date Details Bank € Date Details Bank € 31/5/23 Bank 6,000 Date Details Bank € Date Details Bank € 31/5/23 Bank (Purchases) 1,680 31/5/23 Bank (Sales) 3,150 31/5/23 Balance c/d 1,470 3,150 3,150 1/5/23 Balance c/d 1,470 The General Ledger > Ledgers are the individual accounts for each business activity. > Every transaction has a debit entry and a credit entry. Entries appear on the opposite side in the Ledger compared to the Analysed Cash Book. SAMPLE

The Trial

>

>

>

>

>

of

entry must be

the

side to the

be used to provide details.

>

entry from each

> The entry should be on the

side as the balance in the

> The

should balance.

THE BOOKKEEPING CYCLE 67 Date Details F Bank € Purchases € VAT € Electricity € Wages € 38,150 8,000 1,680 680 6,000 The Trial Balance of Cooney Cosmetics as at 31st of May 2023 Details DR CR Bank 21,790 Sales 15,000 Capital 20,000 Purchases 8,000 Electricity 680 Wages 6,000 VAT 1,470 Total 36,470 36,470

Balance

Dates should be in the form Day/Month/Year and the General Ledger will always be the final day

the month

Only totals from the ACB should be included in

general ledger

Entries in the general ledger should be on the opposite

ACB

Accounts with more than one

balanced

Bank or analysed cash book should

One

account

same

ledger

columns

SAMPLE

9.4 The Final Accounts

The Trial Balance Income Statement Statement of Financial Position

Sample Question D

Use the information in the Trial Balance below to prepare the final accounts of Galligan Website Design Ltd for the year ended 31/12/2022. They have authorised share capital of €300,000.

DR € CR €

Cash purchases and sales 15,000 €20,000

Opening stock 1/1/2022 2,600 Insurance 1,440

Import duty 900 Advertising 1,800 Wages 12,000 Vehicles 25,000 Machinery 36,000 Premises 120,000

Debtors and creditors 2,000 4,240 Cash at bank 2,500

Issued share capital 175,000 Dividends paid 5,000

Reserves 2,500 224,240 224,240

Notes:

1. Stock on the 31/12/2022 will be €6,000.

2. Depreciation on vehicles is charged at 20% and 10% on machinery.

Topic 9 68

SAMPLE

Sample Answer:

1. Mark the location of each item in the Trial Balance. Every item should appear in either the Income Statement (IS) or the Statement of Financial Position (SFP).

2. Calculate the depreciation. Vehicles Machinery 25,000 x 20% = €5,000 (IS) 25,000 – 5,000 = €20,000 (SFP) 36,000 x 10% = €3,600 (IS) 36,000 – 3,600 = 32,400 (SFP)

3. Work your way through the income statement. Words highlighted in red are headings and you must include them in your answer. Be sure to tick things off as you place them in the income statement.

Income Statement of Galligan Ltd for the year ended 31st of December 2022

€ € €

Sales 42,500

Less costs of sales

Purchases 15,000 Opening stock 2,600 Import duty 900 18,500

Less closing stock (6,000) Cost of goods available for sale 12,500 Gross profit 30,000 Less expenses Insurance 1,440 Advertising 1,800 175,000 Wages 12,000

Depreciation: motor vehicles 5,000 Depreciation: machinery 3,600 8,600 23,840

Net profit 6,160

Less dividend paid (5,000) 1,160

Opening reserves 1/1/22 2,500 Closing reserves 31/12/22 3,660

THE BOOKKEEPING CYCLE 69

SAMPLE

4. Prepare the Statement of Financial Position (SFP). Remember items in red are headings and must be included in your own accounts.

Statement of Financial Position of Galligan Ltd as at 31st of December 2022 € € €

Fixed Assets

Vehicles 25,000 5,000 20,000 Machinery 36,000 3,600 32,400 Premises 120,000 120,000 161,000 8,600 172,400

Current Assets

Debtors 2,000 Cash at bank 2,500 Closing stock 6,000 10,500

Current liabilities Creditors 4,240 (4,240)

Working capital 6,260 178,660

Financed by Authorised Issued Share capital 300,000 175,000 175,000 Reserves 3,660 Capital Employed 178,660

Topic 9 70

SAMPLE

Test Yourself

Question 1

Using the information below, complete the Analysed Cash Book, General Ledger and Trial Balance of Conaty Toy Emporium Ltd for the month of May and balance the account.

1/5/23 James, the owner invested in the business €35,000

Scan for Sample Answers

3/5/23 Sold goods €25,000 plus VAT@ 21%

10/5/23 Paid wages €8,000

15/5/21 Purchased goods for resale €15,000 plus VAT@ 21%

20/5/21 Paid electricity €950

25/5/21 Paid wages €8,000

THE BOOKKEEPING CYCLE 71 9.5

SAMPLE

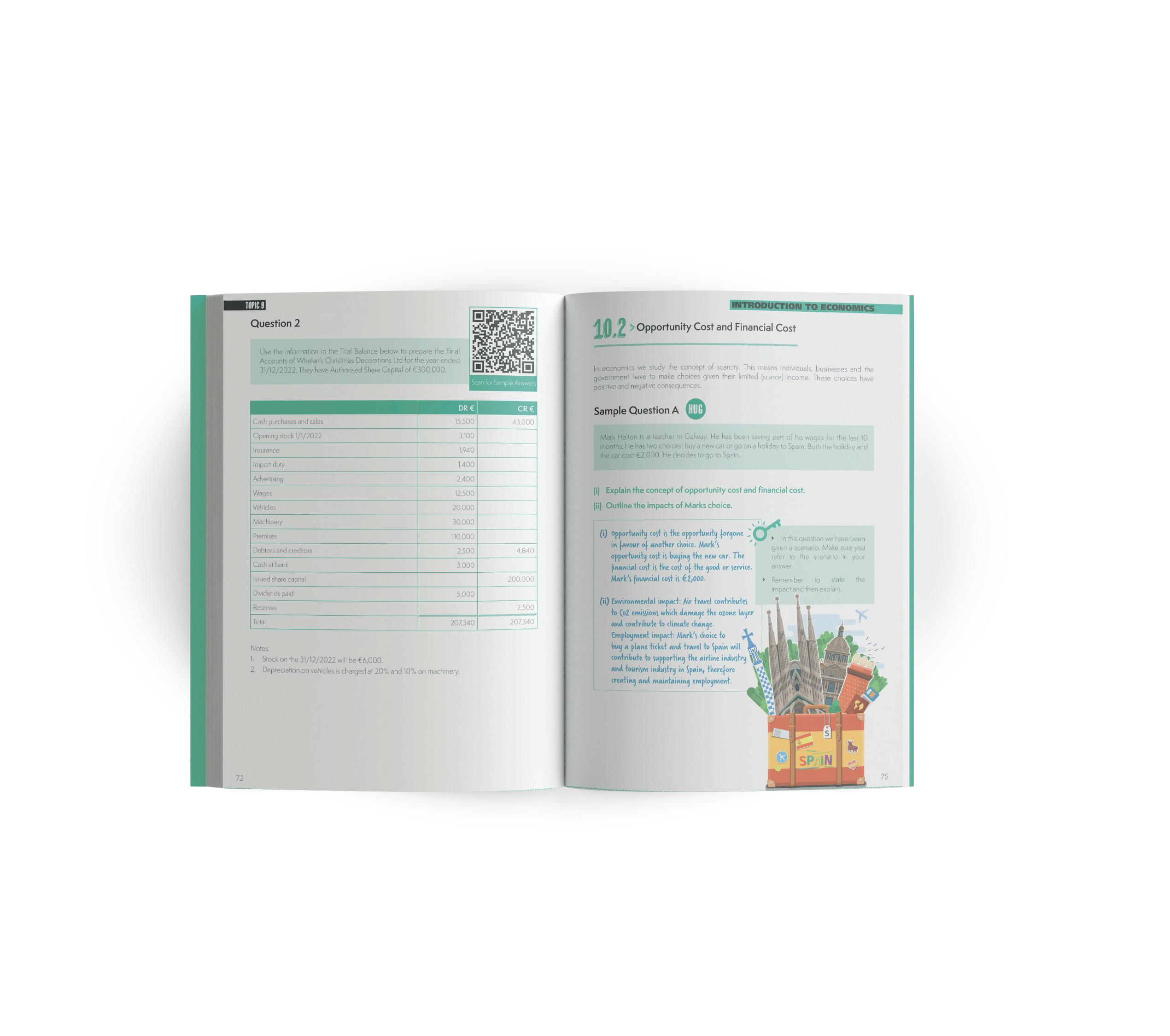

Use the information in the Trial Balance below to prepare the Final Accounts of Whelan’s Christmas Decorations Ltd for the year ended 31/12/2022. They have Authorised Share Capital of €300,000.

Scan

Sample

DR € CR €

Cash purchases and sales 15,500 43,000

Opening stock 1/1/2022 3,100

Insurance 1,940

Import duty 1,400 Advertising 2,400

Wages 12,500

Vehicles 20,000 Machinery 30,000

Premises 110,000

Debtors and creditors 2,500 4,840

Cash at bank 3,000

Issued share capital 200,000

Dividends paid 5,000 Reserves 2,500

Total 207,340 207,340

Notes:

1. Stock on the 31/12/2022 will be €6,000.

2. Depreciation on vehicles is charged at 20% and 10% on machinery.

Topic 9 72 Question 2

for

Answers

SAMPLE

INTRODUCTION TO ECONOMICS 73 Topic 10 10.1 Definitions and Abbreviations 10.2 Opportunity Cost and Financial Cost 10.3 Economic Resources 10.4 Economic Systems and Ireland’s Economy 10.5 The Circular Flow of Income INTRODUCTION TO ECONOMICSSAMPLE

10.1

Definitions and Abbreviations

Economics

A social science which is the study of how individuals, organisations and the government make choices to satisfy their needs and wants given their limited resources.

An economic concept according to which individuals, organisations or the government want more than they can have because their resources, such as income, are limited.

Something which we cannot live without, e.g. food.

Something we would like to have but which is not necessary for survival, e.g. a holiday.

The opportunity missed in favour of another choice.

The amount of money paid for a good or service.

The ways in which individuals, organisations and the government produce goods and services in the economy. Also knows as the factors of production. There are four – Land, Labour, Capital and Enterprise.

The methods which a government uses to produce and distribute the factors of production. We will study three – Centrally planned economy, Mixed economy and Free enterprise.

The selling of state-owned enterprises to the private sector.

The section of the economy where individuals set up their own businesses. How money flows through an economy.

Topic 10 74

Scarcity Needs Wants Opportunity cost Financial cost Economic

resources

Economic systems Privatisation Private

sector

Circular

flow of

income

Definitions

Abbreviations

Factors of ProductionFOP

Public

Private PartnershipPPP

SAMPLE

10.2 Opportunity Cost and Financial Cost

In economics, we study the concept of scarcity. This means individuals, businesses and the government have to make choices given their limited (scarce) income. These choices have positive and negative consequences.

Sample Question A

HUG

Mark Halton is a teacher in Galway. He has been saving part of his wages for the last 10 months. He has two choices; buy a new car or go on a holiday to Spain. Both the holiday and the car cost €2,000. He decides to go to Spain.

(i) Explain the concept of opportunity cost and financial cost.

(ii) Outline the impacts of Mark's choice.

(i) Opportunity cost is the opportunity forgone in favour of another choice. Mark’s opportunity cost is buying the new car. The financial cost is the cost of the good or service. Mark’s financial cost is €2,000.

(ii) Environmental impact: Air travel contributes to Co2 emissions which damage the ozone layer and contribute to climate change. Employment impact: Mark’s choice to buy a plane ticket and travel to Spain will contribute to supporting the airline industry and tourism industry in Spain, therefore creating and maintaining employment.

> In this question we have been given a scenario. Make sure you refer to the scenario in your answer.

> Remember to state the impact and then explain.

INTRODUCTION TO ECONOMICS 75

SAMPLE

10.3

Factors of Production

Explanation

Economic Resources

Economic resources are factors used in producing goods or providing services.

There are four economics resources (also known as the factors of production).

Anything supplied by nature that helps in the production of goods and services, e.g. land, sea, forestry and gas.

The human effort in the production process, e.g. factory workers.

Anything manufactured that helps in the production

process, e.g. machinery and equipment.

The person who takes the personal and financial risk to set up a business in the hopes of making a profit. They combine the other factors of production.

Reward Rent Wages Interest Profit/loss

Example Supermac’s purchases the meat for their burgers, vegetables and salads from local farmers around Co. Galway.

SAMPLE

Supermac’s has over 4,000 employees across Ireland. These include chefs and service staff.

Supermac’s has tills for taking money, deep fat fryers for cooking food and drinks dispensers.

Pat McDonagh is the owner of Supermac’s.

The economic resources are scarce. Individuals, businesses and the government must make choices and those choices have consequences.

Topic 10 76

Land Labour Capital Enterprise

Sample Question B

HUG

Ireland’s fast food franchise, Supermacs announce the implementation of self-checkouts which will result in job losses

(i) Explain the possible opportunity cost of Supermac’s decision to invest in selfcheckout counters.

(ii) Explain one impact of this investment.

(iii) Fill in the missing factors in the box below.

(iv) Explain one of the factors of production.

(i) Opportunity cost is the opportunity forgone in favour of another choice. Supermac’s opportunity cost is job losses.

(ii) Unemployment impact: Supermac’s decision to invest in self-checkouts has meant there is less need for staff and will lead to job losses. This will result in increased demand for social welfare.

(iii)

Land Labour Capital Enterprise Factors of Production

(iv) Land: Anything supplied by nature that helps in the production of goods and services, e.g. land, sea, forestry and gas.

INTRODUCTION TO ECONOMICS 77

SAMPLE

10.4

Economic Systems and Ireland’s Economy

There are many economic systems in operation all over the world. An economic system is the methods a country’s government uses to produce and distribute the factors of production available to them. We will look at three examples of economics systems.

Centrally planned Mixed economy Free enterprise

Explanation

The government controls all of the factors of production and makes all of the decisions about economic activity.

Advantages Provision of services: Essential products and services will be provided for all citizens, e.g. healthcare.

There is a mix of privately owned and state-owned businesses operating.

Most businesses are privately owned and there is little state intervention.

Disadvantages Government control: Government controls almost all aspects of life. Quality of goods and services: Due to lack of competition, standards of products and services may be poor.

Taxation

Provision of services: loss making services which may not be provided by entrepreneurs will be provided by the state, e.g. certain rail routes.

More choice: The provision of products and services by both state and private enterprise means there is more choice for the consumer.

Poor management: businesses run by the government do not have profit motive and so maybe less efficient.

SAMPLE

Competitive prices: Due to competition between firms for market share.

Encourages entrepreneurship: High profits encourage more entrepreneurs to enter the market. This leads to greater choice for consumers.

Emphasis on profit: with profit making motive, the welfare and the consumer may be compromised.

The government may impose higher taxes to cover the debts of loss-making businesses.

No profit motive: Government run businesses do not have a profit motive. This may make them uncompetitive and inefficient.

Uneven distribution of wealth: There is a large gap between the rich and the poor. Lack of regulation: Lack of government regulation could lead to environmental issues.

Topic 10 78

Example China Ireland USA

Ireland has a mixed economy meaning there are different sectors operating in the economy.

Sector Explanation Example

Public sector The government owns and operates businesses. These are known as state sponsored bodies

If the government owns part of the business it is knows as a semi state body. The government employs managers to run the business for them.

Private sector Individuals set up and run their own business.

Voluntary sector Businesses which are set up but are not for profit They may be voluntary organisations or social enterprises.

Sample Question C

HUG

Irish government sell their stake in Aer Lingus

(i) Outline why the Irish government owns businesses in the economy.

(ii) Describe the term privatisation.

(iii) Explain why the Irish government privatise businesses.

(i) Provision of services: Some services are loss making and so private entrepreneurs may not supply the service. These would leave people without an essential service, e.g. bus routes to and from remote areas.

Promotion: Some businesses are set up to promote certain aspects of the Irish economy, e.g. Fáilte Ireland promotes tourism both at home and abroad, while Board Bia promote Irish food.

(ii) Privatisation is the selling of state-owned enterprises to the private sector.

(iii) Source of finance: the government may need the money for something else, such as servicing the national debt, and so they sell the state body to get access to the finance. Loss making: The state body may be loss making due to lack of incentives or poor decision making. The government will have to cover the costs of a loss-making business: selling it will get rid of that burden.

INTRODUCTION TO ECONOMICS 79

SAMPLE

10.5

The Circular Flow of Income

The circular flow of income shows how money flows through the economic system. It can be shown in a diagram.

For this step, let's assume that there are only two elements: businesses and households. Businesses pay individuals for the work done (income) and the household spends their income on the goods and services sold by the business.

We know that households do not spend all of their income. They save some in financial institutions, e.g. banks. The financial institutions provide finance for businesses in the form of loans.

We also know that households and businesses have to pay taxes such as PAYE, VAT, etc. These taxes are paid by the households to the government. As well as paying taxes, businesses also receive finance from the government in the form of grants.

So far, we have looked at a closed economy. However, Ireland is an open economy. Households buy goods and services from other countries (imports). Irish businesses also sell their goods and services on the international market (exports).

Topic 10 80

SAMPLE

INTRODUCTION TO ECONOMICS 81 Buy goods and services Provide fee Income Loans Saving s G rants TaxE x port s Imp o r t s Government International trade SAMPLE

Notes 82 SAMPLE

Morning of&night before

• Before you finish your study, check that you have everything you need ready for the following morning, exam number, pens, etc.

• Don’t sit up cramming, make sure you get a good night’s sleep.

• Eat well before the exam to keep up your stamina.

• Give yourself plenty of time to make sure you arrive on time.

• When you get to school, avoid conversations with others about what they have revised, it might only increase your stress.

• Read the paper very carefully.

• Always start with your strongestquestion.

• Make sure to give yourself timeat the end of the exam to re-readover your answers and check them.

Once in the exam Keepandcalm succeed

SAMPLE

89F Lagan Road, Dublin Industrial Estate, Glasnevin, Dublin 11, D11 F98N, Republic of Ireland. T: ++ 353 1 8081494 - F: ++ 353 1 836 2739 - E: info@4schools.ie - W: www.4schools.ie Junior Cycle Success - Business BUSINESSSAMPLE