Buying a home is an exciting journey and a major life milestone. As you begin this process, we’re looking forward to providing all the services and solutions you need for a smooth, enjoyable, and rewarding homebuying experience.

The biggest contributor to a successful home purchase is preparation. In this booklet, you’ll find

Sincerely,

Your Money Store Mortgage Team

an introduction to our team and company as well as useful information and advice on the home financing process. Please review these materials so you can be prepared for the steps ahead.

Don’t hesitate to contact any member of our team with your questions or concerns at any time. We look forward to helping make your homeownership goals a reality!

The Money Store has been a trusted mortgage brand since 1972. We are a family-owned, privately held lender that serves homebuyers and homeowners from coast to coast. Our mission is to help people achieve their homeownership goals while saving them time, money, and stress. We provide a first-class home financing experience and proudly maintain a 98% customer satisfaction rating.1

☐ Mortgages are 100% of our business

☐ Highly competitive rates and fees

☐ Wide range of flexible loan options

☐ Timely and transparent in-house loan processing

☐ We service the majority of our loans

☐ A+ Better Business Bureau rating

1. Based on client reviews from Experience.com for 8/1/2023 through 8/1/2024. Source: https://www.experience.com/reviews/company/the-money-store-47994

NMLS ID # 1098662

Mortgage Loan Originator

925-914-9631

sceja@themoneystore.com

themoneystore.com/lo/stephanie-ceja

8290 Brentwood Boulevard

Brentwood, CA 94513

Stephanie Ceja is a seasoned mortgage professional with more than 20 years of industry experience. As your partner on your home financing journey, Stephanie will listen to your needs and goals, tailor a mortgage solution specifically for you, and advise and guide you from start to finish. She is passionate about going above and beyond to deliver the service and results you deserve.

925-315-5047

jmalfitano@themoneystore.com

Julianna works directly with Stephanie to gather the necessary initial documentation from you, and she will stay in contact with you throughout the process to ensure everything runs smoothly.

DRE. 02206035

Realtor

603-261-1945

jacob.alley@fastagents.com fastagents.com/agents/jacob-alley

2603 Camino Ramon, Suite 200 San Ramon, CA 94583

Jacob Alley, a native of the Bay Area, brings a deep-rooted understanding of the local market to his role as a young entrepreneur and Team Fast eXp Realtor. With his finger on the pulse of the real estate scene, Jacob provides his clients with exclusive access to hundreds of off-market homes, ensuring they have an edge in finding their dream property. His dedication, coupled with his innovative approach, makes him a valuable

DRE. 02134236

Realtor

415-756-1695

otis@fastagents.com fastagents.com/agents/otis-white-jr

2603 Camino Ramon, Suite 200 San Ramon, CA 94583

Born and raised in the mission district of San Francisco, Otis White Jr. has been around a wide range of diversity growing up. Since childhood, his ability to connect with pretty much anyone has been something that’s helped him stand out. He is a father to three beautiful children and a devoted husband to his wife. Otis is simply a family man who enjoys helping connect. He brings strong communication skills, seasoned negotiating tactics, and the ability to work with just about anyone to the table.

Stephanie made the process efficient and easy.

Stephanie and her team worked very hard to make my homebuying process a dream come true. She is very responsive and knowledgeable in her expertise. She answered all my questions with patience and grace.

— JANET T.

Loved working with Stephanie!

It was such a smooth and easy experience. Stephanie made it so simple for us. Glad to have chosen her and definitely will be recommending her to anyone I know that will be looking for a house in the future.

— KARINA L.

Fast Real Estate was FANTASTIC. They made the house buying process so easy! They kept in communication with us every step of the way and answered any question we had.

— ATHENA H.

Otis did an excellent job.

He helped us to get our dream home. He was always positive and willing to do the best for us. I’ll truly recommend Otis to my friends and family to be their agent.

— MIGUEL J.

Financing your home is faster and easier with The Money Store’s digital mortgage experience. Through our website or mobile app, you can securely and conveniently navigate your home financing journey from your smartphone, tablet, or computer.

☐ Apply in 10 minutes or less

☐ Get preapproved fast

☐ Scan and upload your documents

☐ Access mortgage and real estate tools

☐ Switch between the app and website at any time

☐ E-sign your forms

☐ Track your loan status

☐ And more!

1. Visit the link below, or scan the code with your phone’s camera.

2. Follow the prompts to create your account and start your application.

3. Download the app when prompted, or continue using your web browser.

You’ll select a real estate agent to work with and plan your home search.

We’ll review your basic qualifications and preapprove you for your home financing.

You and your agent will browse home listings and tour properties to find the right home for you.

You and your agent will make an offer on a home and negotiate a price and contract.

Apply for a Mortgage

You’ll apply for your loan and provide required documentation, and we’ll process your application.

Licensed professionals will assess the home’s condition and value.

Our underwriter will review your application and request any additional items required from you.

If everything is in order, we’ll give the final approval for your loan.

You and your agent will walk through the home again to ensure it’s in the same condition as before.

You’ll sign your final documents, pay your closing costs, and receive the keys to your new home. Congrats!

This is a general overview of a typical homebuying process. The exact steps and order may vary based on various factors and events. Mortgage programs are subject to approval based on program guidelines, borrower’s credit and underwriting approval, acceptable appraisal, and clear title. Rates, terms, and conditions may apply. Programs are subject to change at any time. This is not a commitment to lend. Contact your MLD Mortgage, Inc. dba The Money Store mortgage loan originator for full program details and requirements.

Don’t let an innocent mistake put your mortgage in jeopardy! To help keep your home financing on track, here are some important dos and don’ts to follow until your loan has closed.

☐ Do have easy access to all your pay stubs, bank statements, and other financial documents.

☐ Do continue to make all your bill payments on time.

☐ Do notify us immediately if you experience or expect any changes to your employment.

☐ Do notify us if you plan to receive gift funds for closing.

☐ Do provide your earnest money deposit from your own personal bank account or acceptable gift funds.

☐ Do ask any and all questions you may have throughout the process.

☐ Don’t fail to make any of your bill payments on time.

☐ Don’t change jobs, become selfemployed, or quit your job.

☐ Don’t make any major purchases, such as a car or furniture.

☐ Don’t open, close, cosign, or increase any liabilities, such as credit cards or loans.

☐ Don’t make any large deposits or withdrawals other than automated payroll.

☐ Don’t open or close any asset accounts or move money between accounts.

Your credit and other qualifications will be checked again before your loan closes, so it’s essential to follow these guidelines until after your closing. If you have or expect to have any difficulty upholding these guidelines, please contact us immediately.

Please be prepared to provide copies of the following documents for your mortgage application. Submitting these items promptly is important for keeping your financing on schedule.

If multiple people will be listed on your new mortgage, please provide these items for each person if applicable.

Unless instructed otherwise, all pages for every document must be provided, even if blank. Additional documents may be required in some circumstances.

☐ Current and previous addresses for the last 2 years and duration of residence at each location

☐ Names, addresses, and dates of employment for all employers within the last 2 years

☐ Letter/email explaining any gaps in your employment within the last 2 years

☐ Pay stubs for the most recent 30 days

☐ W-2 and/or 1099 forms for the most recent 2 years*

You may submit your documents through The Money Store mobile app or website (which have their own interactive checklist), email, regular mail, or in person.

☐ Personal federal income tax returns for the most recent 2 years* (not required in all cases)

☐ Most recent 2 monthly or quarterly statements for banking, investment, and retirement accounts

☐ Current mortgage statement, property tax bill, homeowners insurance declaration, and HOA dues statement (if applicable) for all properties owned

* Some mortgage programs require fewer or more years of documentation.

☐ Landlord’s name, email, and phone to verify last 12 months of rental history (if currently renting)

☐ Award letter and copy of most recent check for retirement, Social Security, or disability income (if using such income to qualify)

☐ Social Security card (if applying for an FHA loan)

☐ DD Form 214 (if applying for a VA loan)

☐ Proof of residency, such as a resident alien or visa/EAD card (if a foreign citizen)

☐ Homeowners association bylaws and contact info

☐ Divorce decree and settlement agreement

☐ Business federal income tax returns for the most recent 2 years, signed and dated

☐ K-1 forms

☐ Child support documentation

☐ Mortgage modification documentation

☐ Foreclosure documentation

☐ Bankruptcy papers, including discharge

☐ Tax lien payment plan

☐ Names of people who are not on the mortgage application but will be on the title

☐ Trust documents for a property held in trust

☐ Copy of note and mortgage on existing secondary financing that will be subordinating

☐ Year-to-date profit and loss statement and current balance sheet, signed and dated

☐ Your and the seller’s real estate agents’ contact info

☐ Your and the seller’s attorneys’ contact info (if applicable)

☐ Homeowners insurance quote or insurance agent’s name, phone, and email

☐ Home purchase contract (final version with all addendums)

☐ Home sale contract and Closing Disclosure (CD) for any recently sold home

☐ Proof of payment of earnest money (updated bank statement or a daily summary showing 4 digits of account number and earnest money check(s) or wire(s) clearing the account)

Credit scores are 3-digit numbers that assess your likelihood of repaying borrowed money on time. Every person with a credit history typically has three credit scores – one for each major credit bureau: Experian, TransUnion, and Equifax.

There are also multiple credit score models, which are different ways of calculating your three scores. Mortgage lenders use specific versions of the FICO Score model to assess the creditworthiness of mortgage applicants.

Your credit scores help determine which mortgage options and interest rates you qualify for. Generally, if you have high scores, you’ll qualify for more loan options and a lower interest rate than if you had lower scores.

When you apply for a mortgage, all three of your credit scores are considered, and the lowest middle score of all applicants on the loan is typically used. Because lenders use specific FICO Score models, the scores used on your application may differ slightly from the numbers you’ve seen when checking your own scores.

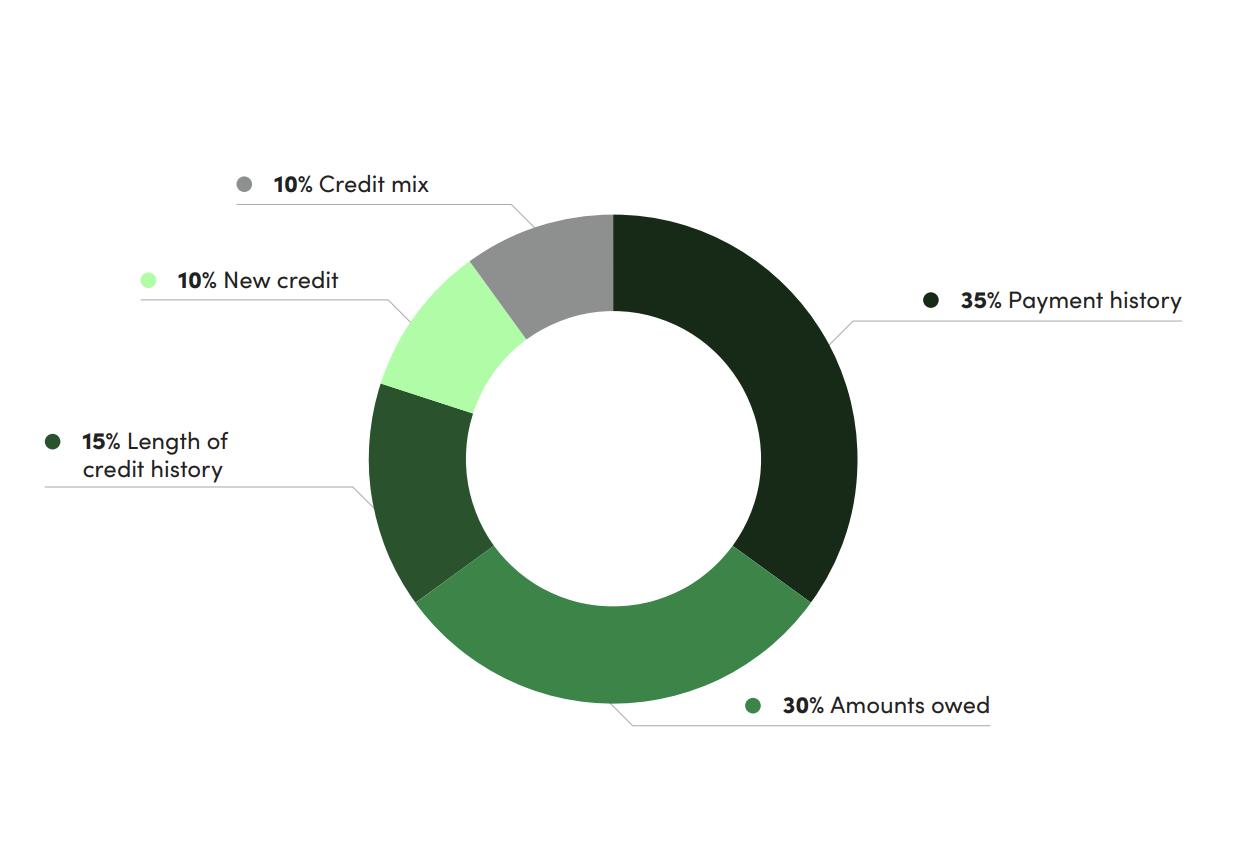

FICO Scores use a scale from 300 to 850, with higher scores being better. Your scores are based on your credit history, which is recorded in a separate credit report at each of the three credit bureaus. FICO Scores are calculated using the following five aspects of your credit history:

☐ 35% Payment history: on-time payments are best

☐ 30% Amounts owed: low utilization of credit limits is best

☐ 15% Length of credit history: a long history is best

☐ 10% New credit: minimal recently opened credit is best

Note: The percentages above are subject to change.

☐ 10% Credit mix: a mix of credit types is best (e.g., credit cards and installment loans)

MLD Mortgage, Inc. dba The Money Store and its employees do not provide credit advice. This material has been prepared for general informational purposes only and is not intended to provide and should not be relied on for such advice. Do not act or refrain from acting on the basis of this material without first consulting a qualified professional for advice.

This glossary defines some of the common terms you may encounter during your mortgage process.

A mortgage with an interest rate that remains constant for an initial fixed period of time and then adjusts at a prearranged frequency

A monthly repayment schedule in which a loan is repaid in fixed payments of principal and interest

The annual cost of a loan, expressed as a yearly rate that reflects interest, discount points, lender fees, and mortgage insurance, thus being slightly higher than the interest rate on the loan

An initial statement of personal and financial information required to approve a mortgage loan

A written estimate of a property’s current market value, based on recent sales information from similar properties and the current condition of the property

Limits on changes in adjustable-rate mortgage (ARM) interest rates or monthly payments, either in an adjustment period or over the life of the loan

A form that accompanies a revised Loan Estimate (LE) and details what has changed on the revised LE

Expenses paid by the borrower and/ or seller during the closing, which can include the loan origination fee, discount points, attorney’s fees, title insurance, appraisals, etc.

A form that provides final details about a mortgage loan, such as loan terms and projected monthly payments and closing costs, and must be provided to the borrower by the lender at least three days before the loan closes

Any additional borrowers whose names appear on the loan documents

A property being financed that a borrower offers to a lender to secure a loan

A condition that must be satisfied before a contract is legally binding and a sale can close

A mortgage that is not guaranteed or insured by any government agency

Total monthly debt payments (including projected payments for a new mortgage) divided by monthly income

The government agency that manages benefits and other issues for Veterans of the military

Discount Points

See: Points

The portion of a home purchase price that is paid upfront at the closing of the purchase, which is the difference between the purchase price and the loan amount

A deposit made by a buyer in evidence of good faith when the purchase agreement is signed

Federal law requiring creditors to make credit equally available without discrimination based on race, color, religion, national origin, age, sex, marital status or receipt of income from public assistance programs

The percentage of a property’s value held by the owner, which is the difference between the property’s value and the amount owed on the mortgage

The neutral third party that holds money and/or documents until the escrow instructions are fulfilled

The law that protects consumers through federal regulations on the total interest paid over the life of a loan and procedures to repair errors on a person’s credit report

A government-sponsored enterprise that buys and sells conventional mortgages

A division of Housing and Urban Development (HUD) that insures residential mortgage loans and sets standards for underwriting

A loan insured by the Federal Housing Administration

A mortgage with an interest rate that doesn’t change for the life of the loan

A government-sponsored enterprise that purchases conventional mortgages

The government corporation that purchases conventional mortgages from HUD-approved bankers

Insurance that covers an individual’s home against damages to the home or possessions in the home as well as accidents in the home or on the property

A U.S. government agency established to implement federal housing and community development programs and that oversees the Federal Housing Administration

A benchmark rate used to determine the rate on an adjustable-rate mortgage (ARM) after the initial rate expires

The amount charged, expressed as a percentage of principal, by a lender to a borrower for the use of assets

A mortgage larger than the conforming loan limits set by the Federal Housing Finance Agency (FHFA)

A form that provides important details about a loan and must be provided to the borrower by the lender within three days of the lender receiving the loan application

The percentage of a property’s value that is borrowed

A lender’s guarantee of an interest rate for a set period of time

The amount of percentage points, or spread, added to an index to determine the rate an adjustable-rate mortgage will charge after each adjustment

Mortgage

A document that creates a lien on a property as security for the payment of a debt

An insurance premium that a borrower is required to pay on an FHA loan

The financial institution or entity that is responsible for collecting payments on a mortgage

A provision of a homeowners insurance policy that protects the lender (the mortgagee) from losses incurred due to damage to the insured property

An acronym used to describe monthly housing expenses: principal, interest, taxes, and insurance

Funds paid at closing to the lender, with one point equal to 1% of the loan amount

A preliminary approval from a lender to loan a borrower a specific amount of money

A charge for paying off a loan prior to the end of the prepayment penalty period (certain loan types only)

A basic review by a lender determining the loan amount for which a borrower may qualify

The amount of debt on a loan that does not include interest

Insurance that a borrower is typically required to purchase on a conventional loan with an LTV above 80%

The process of paying off one loan with the proceeds from a new loan secured by the same property

A 3-day waiting period after signing the closing documents granted to the borrower on a refinance transaction of

their primary residence to allow them to cancel if they so choose

A subordinate mortgage made in addition to a first mortgage

The number of years until a loan is due to be paid in full

A rule that consolidates four existing disclosures, applicable to most closedend borrower credit transactions secured by real property, into two forms: the Loan Estimate (LE) and the Closing Disclosure (CD)

A document that gives evidence of ownership of a property as well as rights of ownership and possession

Insurance that protects the lender (lender’s policy) or buyer (owner’s policy) against loss due to disputes over property ownership

The process of verifying data and evaluating a loan application for approval

A home loan available to eligible military Veterans and surviving spouses with little or no down payment and guaranteed by the Department of Veterans Affairs (VA)

The fee financed or paid upfront associated with a VA loan

A document signed by the borrower’s bank or other financial institution that verifies the borrower’s account balance and history

A document signed by the borrower’s employer that verifies the borrower’s position and salary