© All rights reserved

Price : ` 995

Tenth Edition : May 2025

Applicable for Assessment Year 2025-26

Published by :

Taxmann Publications (P.) Ltd.

Sales & Marketing :

59/32, New Rohtak Road, New Delhi-110 005 India

Phone : +91-11-45562222

Website : www.taxmann.com

E-mail : sales@taxmann.com

Regd. Office :

21/35, West Punjabi Bagh, New Delhi-110 026 India

Printed at :

Tan Prints (India) Pvt. Ltd.

44 Km. Mile Stone, National Highway, Rohtak Road Village Rohad, Distt. Jhajjar (Haryana) India

E-mail : sales@tanprints.com

Disclaimer

Every effort has been made to avoid errors or omissions in this publication. In spite of this, errors may creep in. Any mistake, error or discrepancy noted may be brought to our notice which shall be taken care of in the next edition. It is notified that neither the publisher nor the author or seller will be responsible for any damage or loss of action to any one, of any kind, in any manner, therefrom. It is suggested that to avoid any doubt the reader should cross-check all the facts, law and contents of the publication with original Government publication or notifications.

No part of this book may be reproduced or copied in any form or by any means [graphic, electronic or mechanical, including photocopying, recording, taping, or information retrieval systems] or reproduced on any disc, tape, perforated media or other information storage device, etc., without the written permission of the publishers. Breach of this condition is liable for legal action.

For binding mistake, misprints or for missing pages, etc., the publisher’s liability is limited to replacement within seven days of purchase by similar edition. All expenses in this connection are to be borne by the purchaser. All disputes are subject to Delhi jurisdiction only.

Chapter

Chapter

Chapter

Chapter

Chapter

Chapter

PART II

TAX DEDUCTION AND COLLECTION AT SOURCE

Q1. Explain the applicability of the provision relating to the deduction of tax at source in the following transactions:

(

i) Max Limited pays ` 1.20 lakhs to Mini Limited, a resident contractor who, under the contract dated 15th October, 2023, manufactures a product according to specification of Max Limited by using materials purchased from Max Limited.

(ii) A company operating a television channel makes payment of ` 5 lakhs to a former cricketer for making running commentary of a one-day cricket match.

(iii) EL Ltd., a foreign company, pays outside India, salary to its employee, Mr. Raghavan, a foreign national and a non-resident, for services rendered in India. [CA Final May 2010] [6 Marks] Ans.

in the case of CIT v. Eli Lilly & Co. (India) P. Ltd.

Q2. Bharathi Cements Ltd., the assessee, purchases jute bags from Raj Kumar & Co. The latter has to supply the jute bags with the logo and address of the assessee, printed on it. From 01.09.2023 to 20.03.2024, the value of jute bags supplied is ` 8,00,000, for which the invoice has been raised on 20.03.2024. While effecting the payment for the same, is the assessee bound to deduct tax at source, assuming that the value of the printing component involved is ` 60,000. The assessee has not sold any material to Raj Kumar & Co. and the latter has to manufacture the jute bags in its plant using raw materials purchased from outsiders. [CA Final May 2010] [2 Marks]

Q3. R Limited transferred a building worth ` 25 lakhs to the Chief Executive Officer, Mr. Mohan Lal, a resident individual on his retirement under an agreement for not carrying on any activity related to its business

for a period of five years. In course of assessment u/s 143(3), the A.O. found that no tax had been deducted at source by R Limited and on that ground, he disallowed 30% of the expenditure by invoking the provision of section 40(a)(ia). Examine the correctness of the action of the Assessing Officer. [CA Final Nov. 2010] [6 Marks]

Ans.

Q4. Maya Bank credited ` 73,50,000 towards interest on the deposits in a separate account for macro-monitoring only by using Core-branch Banking Solutions (CBS) software. No tax was deducted at source in respect of interest on deposits so credited even where the interest in respect of some deposits exceeded the limit of ` 40,000. The Assessing Officer disallowed the entire interest expenditure where the interest on time deposits credited exceeded the limit of ` 40,000 and also levied penalty under section 271C. Decide the correctness of action of the Assessing Officer. [CA Final May 2011] [4 Marks]

Ans. Explanation

Explanation to section 194A will not apply

Q5. What are the consequences of not collecting tax at source (TCS) in respect of sale of scrap by a manufacturing company? State the circumstances under which the TCS provisions are not applicable in the above case. [CA Final May 2012] [5 Marks] Ans. inter alia

Q6. Amisha Hotels and Resorts Ltd. is engaged in business of owning, operating and managing hotels. The tips are paid by the guests by way of charge to the credit cards in the bills. The company disburses the same to the employees at periodic intervals. Explain with reasons whether the company is responsible for deducting tax at source from disbursement of tips to its employees. [CA Final Nov. 2012] [4 Marks] Ans.

ITC Ltd. v. CIT (2016)

Q7. Discuss the liability for deduction of tax at source in the following cases:

(i) Mr. A has been running a sole proprietary business having total turnover of ` 1.5 crore in the immediately preceding financial year. He pays a monthly rent of ` 15,000 for the office premises to Mr. X, the landlord besides, he also pays service charge of ` 10,000 per month to Mr. X towards the use of furniture and fixtures.

(ii) By virtue of an agreement with a nationalized bank, a catering organization receives ` 50,000 per month towards supply of food, snacks, etc. during the office hours to the employees of the bank.

(iii) A notified infrastructure debt fund eligible for exemption u/s 10(47) of the Income-tax Act, 1961 pays interest of ` 5 lakhs to a company incorporated in USA. The US Company incurred expenditure of ` 12,000 for earning such interest. The fund also pays interest of ` 3 lakhs to Mr. X, who is a resident of a notified jurisdictional area. Discuss the liability for deduction of tax at source.

[CA Final May 2013] [8 Marks]

Ans.

land, building furniture, fittings

Q8. Explain in the context of provisions contained in Chapter XVII of the Act and also work out the amount of tax to be deducted by the payer of income in the following cases:

(i) Payment of ` 5 lakhs made by JCP & Co. to Pingu Events Co. Ltd. for organization of a debate competition on the subject “Preservation of Rural Heritage of Rajasthan”.

(ii) “Profit Commission” of ` 1 lakh paid by a re-insurance company to the insurer company after the expiry of the term of insurance where there was no claim during the treaty.

(iii) KD, a part time director (non-executive) of DAF Pvt. Ltd. was paid an amount of ` 2,25,000 as fees which was actually in the nature of commission on sales for the period 01.07.2024 to 30.09.2024.

[CA Final Nov. 2013] [6 Marks]

Q9. Discuss whether tax has to be deducted under the provisions of the Income-tax Act, 1961 in the following situations:

(i) M/s. Shiva & Co., partnership firm, pays a sum of ` 43,000 as interest on loan borrowed from Indian branch of a foreign bank.

(ii) Above firm has paid ` 14,000 as interest on capital to partner Mr. Vishnu, a resident in India and ` 22,000 as interest on capital to partner Mr. Brahma, a non-resident.

(iii) Above firm has paid ` 45,000 being share of profit of partner Mr. Brahma, a non-resident. [CA Final May 2014] [6 Marks]

Ans.

i As per Sec. 195, any person responsible for paying to a non-resident or a foreign company other than interest u/s 194LB or 194LC or 194LD any other sum chargeable under this Act (other than salary) at the time of credit or payment whichever is earlier at the rates in force.

However, the foreign banking company may make an application in Form No. 15C to the A.O. for grant of a certificate if the foreign banking company

AUTHOR’S NOTE:

tax is not required to be deducted from interest credited or paid to any banking company to which the Banking Regulation Act, 1949 applies A foreign bank operating in India is governed by the Banking Regulation Act.

Q10. A foreign company seconded some employees to the assessee, an Indian collaborator. The assessee had not deducted tax on the home salary/special allowance or allowances (education allowance or retention allowance) payments made by foreign company/HO to its employees (expatriated to India) outside India in foreign currency. The Revenue authorities, holding the assessee as an ‘assessee-in-default’ u/s 201 of the Income-tax Act, 1961, levied interest and penalty on it. Is the same justified? [CA Final May 2014] [4 Marks] Ans.

in the case of CIT v. Eli Lilly & Co.(India) (P.) Ltd.

such payment would certainly come u/s 192(1) of the Income-tax Act.

bona fide

Q11. Discuss and compute the liability for deduction of tax at source, if any, in the cases stated hereunder, for the financial year ended 31st March, 2025.

(i) Mr. X, a resident, acquired a house property at Mumbai from Mr. Y for a consideration of ` 90 lakhs (stamp duty value is ` 80 lakhs), on 20.6.2024. On the same day, Mr. X made two separate transactions, thereby acquiring an urban plot in Kolkata from Mr. C for a sum of ` 49,50,000 (stamp duty value is ` 48 lakhs) and rural agricultural land from Mr. D for a consideration of ` 60 lakhs (stamp duty value is ` 65 lakhs).

(

ii) A commission of ` 50,000 was retained by the consignee ‘ABC Packaging Ltd.’ and not remitted to the consignor ‘XYZ Developers’, while remitting the sale consideration on 16/07/2024. Examine the obligation of the consignor to deduct tax at source.

(

iii) Raj is working with AB Ltd. He is entitled to a salary of ` 50,000 per month w.e.f. 1.4.2024. He has a house property which is selfoccupied. He paid an interest of ` 80,000 on loan, during the previous year 2024-25. The loan was taken for construction of house. He has notified his employer AB Ltd. that there will be a loss of ` 80,000 in respect of this house property for financial year ended 31.3.2025. Ignore 115BAC.

[CA Final Nov. 2014] [6 Marks]

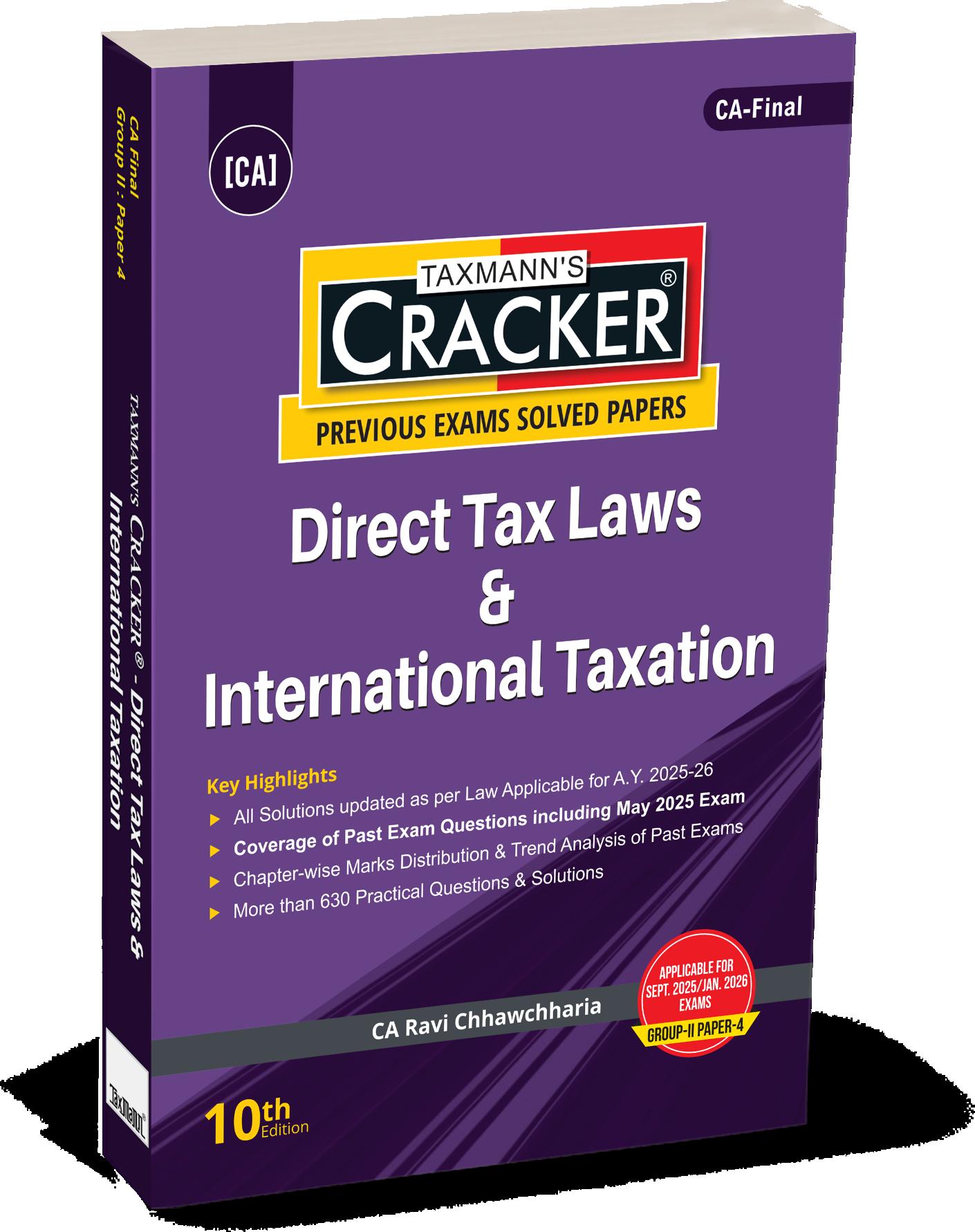

Direct Tax Laws & International Taxation (DT) | A.Y. 2025-26 | CRACKER

AUTHOR : RAVI CHHAWCHHARIA

PUBLISHER : TAXMANN

DATE OF PUBLICATION : MAY 2025

EDITION : 10TH EDITION

ISBN NO : 9789364553889

NO. OF PAGES : 772

BINDING TYPE : PAPERBACK

Direct Tax Laws & International Taxation | CRACKER is a comprehensive study companion for CA-Final Group II – Paper 4. Updated for A.Y. 2025–26, it combines solved past exam papers, chapter-wise analysis, and over 630 practical questions, all geared to help students master both Direct Tax Laws and International Taxation.

The Present Publication is the 10th Edition for the Sept. 2025/Jan. 2026 Exams. This book is authored by CA. Ravi Chhawchharia, with the following noteworthy features:

• [Updated as per A.Y. 2025-26] Reflects all recent amendments and provisions

• [Past Exam Coverage] Includes questions/solutions up to May 2025

• [Chapter-wise Marks Distribution & Trend Analysis] Highlights crucial topics and recurrent patterns

• [630+ Practical Questions] Comprehensive practice with step-by-step solutions

• [Focus on New Topics] Covers Tax Audit & Ethical Compliances and Latest Developments in International Taxation

• [User-friendly Presentation] Clear headings, bullet points, and systematised solutions

• [Ideal Exam-prep Tool] Consolidates trends, analytics, and question banks for targeted revision