Taxmann's Analysis | Fixing Common Ind AS 16 Mistakes

Indian Accounting Standard (Ind AS) 16, Property, Plant, and Equipment, provides a comprehensive framework for the recognition, measurement, and disclosure of tangible fixed assets. Compliance with Ind AS 16 is crucial for ensuring transparency and accuracy in financial reporting. However, several companies have been observed to fall short of the standard’s requirements, leading to non-compliance issues. This article examines key observations reported by the Financial Reporting Review Board of ICAI on Ind AS 16 compliance and related standards concerning Property, Plant, and Equipment (PPE), referencing real-world financial statement examples. It also explores the implications of non-compliance and its impact on financial reporting.

1. Non-Disclosure of Capital Work-in-Progress (CWIP) Movements

1.1 Relevant Provisions

Ind AS 16 Para 73(e) – “The financial statements shall disclose, for each class of property, plant and equipment:

…

(e) a reconciliation of the carrying amount at the beginning and end of the period showing:

(i) additions;

(v) impairment losses recognised in profit or loss in accordance with Indian Accounting Standard 36;

(vi) impairment losses reversed in profit or loss in accordance with Indian Accounting Standard 36;

(ix) other changes.”

Para 74(b) – “The financial statements shall also disclose:

(b) the amount of expenditures recognised in the carrying amount of an item of property, plant and equipment in the course of its construction.”

1.2 Observation

In several cases, companies disclosed Capital Work-in-Progress (CWIP) in their balance sheets but failed to provide detailed movements or reconciliations. For example, a company reported that CWIP was worth Rs. XX million (previous year Rs. YY million) in its balance sheet but did not disclose any reconciliation of the carrying amount at the beginning and end of the period. This omission violates the disclosure requirements of Ind AS 16, as CWIP is considered part of Property, Plant, and Equipment (PPE) and should be treated as such.

It may also be noted that the same view, as to capital-work-in-progress be treated as property, plant and equipment, was taken by the Ind AS Transition and Facilitation Group (ITFG) of ICAI and can be referred from issue number 33 of Compendium of ITFG Clarification Bulletins, December 2018 edition. The relevant extract of the issue number 33 of the compendium is reproduced below:

“…Capital work in progress is in the nature of property, plant and equipment under construction, and accordingly, provisions of Ind AS 16, Property, Plant and Equipment apply to it.”

The company also failed to disclose the amount of expenditures recognised in the carrying amount of PPE during its construction, as required by Para 74(b).

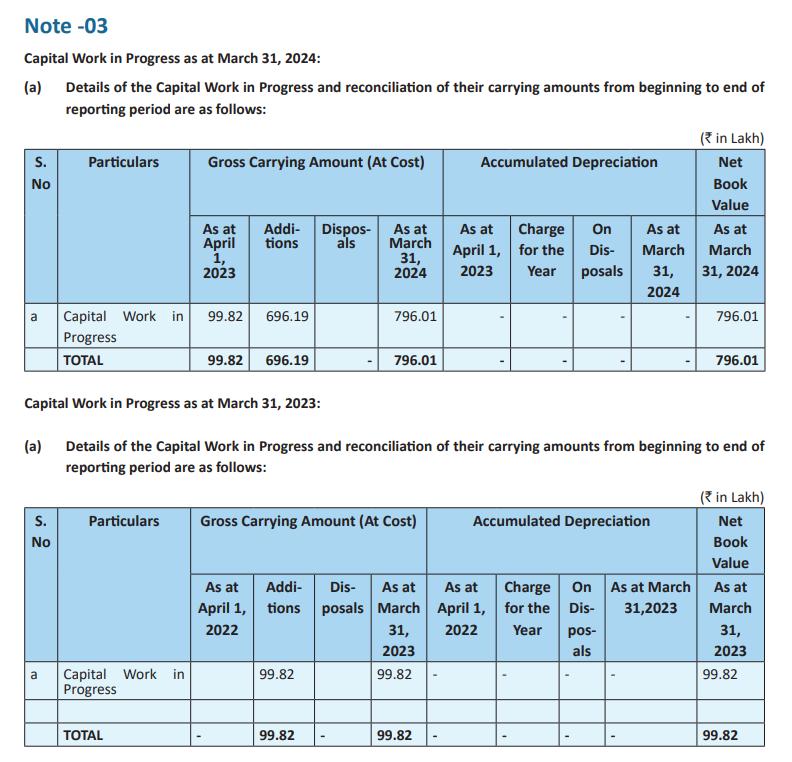

A relevant extract of the notes to the Standalone Financial Statements for the year ended 31st March, 2024 of NBCC Limited reflecting the correct presentation of CWIP is as follows:

1.3 Implication

The non-disclosure of CWIP movements and construction-related expenditures can obscure the true financial position of a company. Stakeholders, including investors and creditors, rely on this information to assess the progress and costs associated with ongoing projects. Without this disclosure, it becomes difficult to evaluate the company’s capital commitments, project timelines, and future cash flows. This lack of transparency can lead to misinterpretation of the company’s asset base and financial health, potentially affecting investment decisions and credit ratings.

2. Non-Disclosure of Depreciation Methods

2.1

Relevant Provision

Ind AS 16 Para 73(b) – “The financial statements shall disclose, for each class of property, plant and equipment:

(b) the depreciation methods used.”

Part C of Schedule II to the Companies Act, 2013 – “The following information shall also be disclosed in the accounts, namely:

(i) depreciation methods used; and

2.2 Observation

In one instance, a company provided detailed information on the useful lives of its assets but failed to disclose the depreciation methods applied. For example, the company’s accounting policy stated that depreciation is provided on a pro-rata basis for additions and disposals, but it did not specify whether the straight-line method, written-down value method, or another method was used. This omission was viewed as non-compliance with both Ind AS 16 and the Companies Act, 2013.

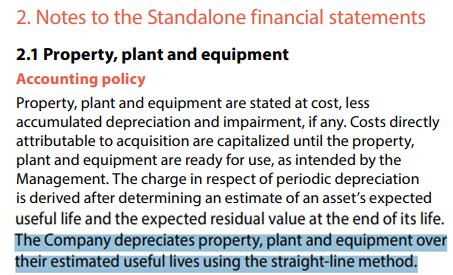

An extract of notes to the Standalone financial statements of Infosys Limited for the year ended 31st March, 2024 reflecting the correct accounting policy related to the depreciation method used is as follows:

2.3 Implication

The depreciation method significantly impacts the carrying amount of assets and the depreciation expense recognised in the profit and loss statement. Without this information, users of financial statements cannot accurately assess the company’s asset utilisation,

future capital expenditures, and the pattern of expense recognition. This lack of disclosure can lead to incorrect assumptions about the company’s financial performance and asset management practices, potentially affecting stakeholder decisions.

3. Non-Disclosure of Charges on PPE for Secured Loans

3.1 Relevant Provision

Ind AS 16, Para 74(a) – “The financial statements shall also disclose:

(a) the existence and amounts of restrictions on title, and property, plant and equipment pledged as security for liabilities.”

Note 6E of General Instructions for Preparation of Balance Sheet (Schedule III to the Companies Act, 2013):

“Borrowings shall further be sub-classified as secured and unsecured. Nature of security shall be specified separately in each case.”

3.2 Observation

In one case, a company had availed secured loans from banks and created charges on its PPE as collateral. However, the financial statements did not disclose this information. For example, the company’s notes to accounts mentioned secured loans from HDFC Bank but did not specify that PPE was pledged as security for these loans. This omission was viewed as non-compliance with Ind AS 16 and Schedule III of the Companies Act, 2013.

3.3 Implication

The non-disclosure of charges on PPE can mislead stakeholders about the company’s financial obligations and the extent to which its assets are encumbered. This lack of disclosure can affect the assessment of the company’s liquidity and solvency, as stakeholders may not be aware of the potential risks associated with the secured loans. It can also lead to a loss of trust in the company’s financial reporting, as stakeholders may question the completeness and accuracy of the information provided.

4. Non-Disclosure of Useful Lives and Depreciation Rates

4.1

Relevant Provision

Ind AS 16, Para 73(c) – “The financial statements shall disclose, for each class of property, plant and equipment:

(c) the useful lives or the depreciation rates used;

4.2 Observation

In one case, a company disclosed that it depreciates its PPE over their useful lives as per Schedule II of the Companies Act but failed to disclose the specific useful lives or depreciation rates applied. For example, the company’s accounting policy stated that depreciation is provided based on internal assessments and independent technical evaluations, but it did not provide the actual useful lives or rates used for different classes of assets.

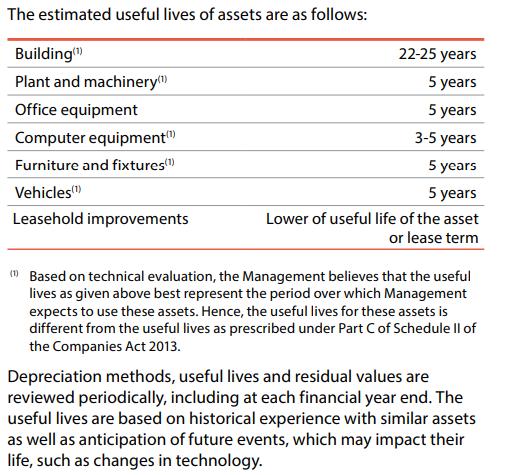

An extract of notes to the Standalone financial statements of Infosys Limited for the year ended 31st March, 2024 reflecting the correct presentation of useful life of assets is as follows:

4.3 Implication

The useful life and depreciation rate are critical for understanding the pattern of asset consumption and the timing of future capital expenditures. Non-disclosure of this information can lead to incorrect assumptions about the company’s asset management practices and the timing of asset replacements. This lack of transparency can affect stakeholder decisions, particularly those related to long-term investments and financial planning.

5. Inconsistencies in Carrying Amounts of PPE

5.1 Relevant Provision

Ind AS 16, Para 73(e) – Requires a reconciliation of the carrying amount of PPE at the beginning and end of the period, including additions, disposals, and other changes.

5.2 Observation

In one instance, a company’s financial statements showed inconsistencies in the carrying amounts of PPE at the beginning and end of the period. For example, the gross block at the beginning of the year did not match the gross block at the end of the previous year. Similarly, there were discrepancies in the accumulated depreciation figures. Such inconsistencies raise concerns about the accuracy of the financial statements.

5.3 Implication

Inconsistencies in carrying amounts can undermine the reliability of financial statements. Stakeholders may question the integrity of the financial reporting process, leading to a loss of trust in the company’s management. This can also result in regulatory scrutiny and potential penalties.

6. Non-Disclosure of Borrowing Costs

Capitalised

6.1 Relevant Provision

Ind AS 23, Para 26 – “An entity shall disclose: (a) the amount of borrowing costs capitalised during the period; and (b) the capitalisation rates used to determine the amount of borrowing costs eligible for capitalisation.”

6.2 Observation

In one case, a company capitalised borrowing costs related to qualifying assets but failed to disclose the amount capitalised or the capitalisation rate used. For example, the company added a significant amount to CWIP, including borrowing costs, but did not provide the required disclosures under Ind AS 23.

6.3 Implication

The capitalisation of borrowing costs affects the carrying amount of PPE and the interest expense recognised in the profit and loss statement. Non-disclosure of this information can lead to an incomplete understanding of the company’s financing activities and their impact on financial performance.

7. Incorrect Capitalisation of Borrowing Costs

7.1 Relevant Provision

Ind AS 23, Para 8 – “An entity shall capitalise borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset as part of the cost of that asset. An entity shall recognise other borrowing costs as an expense in the period in which it incurs them.”

7.2 Observation

In one case, a company capitalised borrowing costs for all constructed assets, regardless of whether they met the definition of a qualifying asset. For example, the company’s accounting policy stated that borrowing costs incurred for constructed assets were capitalised up to the date the asset was ready for use without distinguishing between qualifying and non-qualifying assets.

7.3 Implication

Incorrect capitalisation of borrowing costs can overstate the carrying amount of PPE and understate interest expenses, leading to a misrepresentation of the company’s financial position and performance. This can mislead stakeholders and result in regulatory noncompliance.

8. Use of Incorrect Terminology for PPE

8.1 Relevant Provision

Ind AS 16, Para 73 – Requires disclosure of information related to “Property, Plant, and Equipment.”

8.2 Observation

In one case, a company used the term “Tangible Assets” instead of “Property, Plant, and Equipment” in its financial statements. For example, the company’s note on tangible assets did not align with the terminology used in Ind AS 16, which specifically refers to PPE.

8.3 Implication

The use of incorrect terminology can create confusion among stakeholders and may lead to misinterpretation of the financial statements. It also indicates a lack of alignment with the terminology prescribed by Ind AS 16.

9. Conclusion

Compliance with Ind AS 16 is essential for ensuring the accuracy and transparency of financial statements. The observations highlighted in this article underscore the importance of adhering to the disclosure requirements related to PPE, CWIP, depreciation methods, borrowing costs, and other critical aspects. Non-compliance not only violates accounting standards but also undermines the credibility of financial reporting, potentially leading to regulatory scrutiny and loss of investor confidence. By addressing these common non-compliance issues, companies can enhance the quality of their financial reporting and build trust with stakeholders. It is imperative for companies to regularly review their accounting policies and disclosures to ensure full compliance with Ind AS 16 and other relevant standards.

About Us

Founded 1972

Evolution From a small family business to a leading technology-oriented Publishing/Product company

Expansion

Launch of Taxmann Advisory for personalized consulting solutions

Our Vision

Aim

Achieve perfection, skill, and accuracy in all endeavour

Growth

Evolution into a company with strong independent divisions: Research & Editorial, Production, Sales & Marketing, and Technology

Future

Continuously providing practical solutions through Taxmann Advisory

Our Strength

Core

Editorial and Research Division

Team

Over 200 motivated legal professionals (Lawyers, Chartered Accountants, Company Secretaries)

Expertise

Monitoring and processing developments in judicial, administrative, and legislative fields with unparalleled skill and accuracy

Impact

Helping businesses navigate complex tax and regulatory requirements with ease

Taxmann Today

Legacy Innovation Commitment

Over 60 years of domain knowledge and trust

Technology-driven solutions for modern challenges

Ensuring perfection, skill, and accuracy in every solution provided

Our Core Domain Areas

Income Tax

Corporate Tax Advisory

Trusts & NGO Consultancy

TDS Advisory

Global Mobility Services

Personal Taxation

Training

Due Diligence

Foreign Exchange Management Laws

Due Dilligence

Advisory Services

Assistance in compounding of offences

Transactions Services

Investment outside India

Your Partners for Frictionless Advice

Goods

Transaction Advisory

Business Restructuring

Classification

Due Diligence

Training

Advisory

Trade Facilitation Measures

Corporate

Corporate Structuring

VAT Advisory

Residential Status

A Glimpse of the People Behind Taxmann

Naveen Wadhwa

Research and Advisory [Corporate and Personal Tax]

Chartered Accountant (All India 24th Rank)

14+ years of experience in Income tax and International Tax

Expertise across real estate, technology, publication, education, hospitality, and manufacturing sectors

Contributor to renowned media outlets on tax issues

Vinod K. Singhania Expert on Panel | Research and Advisory (Direct Tax)

Over 35 years of experience in tax laws

PhD in Corporate Economics and Legislation

Author and resource person in 800+ seminars

V.S. Datey Expert on Panel | Research and Advisory [Indirect Tax]

Holds 30+ years of experience

Engaged in consulting and training professionals on Indirect Taxation

A regular speaker at various industry forums, associations and industry workshops

Author of various books on Indirect Taxation used by professionals and Department officials

Manoj Fogla Expert on Panel | Research and Advisory [Charitable Trusts and NGOs]

Over three decades of practising experience on tax, legal and regulatory aspects of NPOs and Charitable Institutions

Law practitioner, a fellow member of the Institute of Chartered Accountants of India and also holds a Master's degree in Philosophy

PhD from Utkal University, Doctoral Research on Social Accountability Standards for NPOs

Author of several best-selling books for professionals, including the recent one titled 'Trust and NGO's Ready Reckoner' by Taxmann

Drafted publications for The Institute of Chartered Accountants of India, New Delhi, such as FAQs on GST for NPOs & FAQs on FCRA for NPOs.

Has been a faculty and resource person at various national and international forums

the UAE

Chartered Accountant (All India 36th Rank)

Has previously worked with the KPMG

S.S. Gupta Expert on Panel | Research and Advisory [Indirect Tax]

Chartered Accountant and Cost & Works Accountant

34+ Years of Experience in Indirect Taxation

Bestowed with numerous prestigious scholarships and prizes

Author of the book GST – How to Meet Your Obligations', which is widely referred to by Trade and Industry

Sudha G. Bhushan Expert on Panel | Research and Advisory [FEMA]

20+ Years of experience

Advisor to many Banks and MNCs

Experience in FDI and FEMA Advisory

Authored more than seven best-selling books

Provides training on FEMA to professionals

Experience in many sectors, including banking, fertilisers, and chemical

Has previously worked with Deloitte

Contact Us

Taxmann Delhi

59/32, New Rohtak Road

New Delhi – 110005 | India

Phone | 011 45562222

Email | sales@taxmann.com

Taxmann Mumbai

35, Bodke Building, Ground Floor, M.G. Road, Mulund (West), Opp. Mulund Railway Station Mumbai – 400080 | Maharashtra | India

Phone | +91 93222 47686

Email | sales.mumbai@taxmann.com

Taxmann Pune

Office No. 14, First Floor, Prestige Point, 283 Shukrwar Peth, Bajirao Road, Opp. Chinchechi Talim, Pune – 411002 | Maharashtra | India