Auditing is not just a compliance requirement but a critical safeguard ensuring financial transparency and accountability. Yet, persistent gaps in audit practices continue to threaten the reliability of financial reporting. According to a 2023 global audit study, nearly 30% of audit deficiencies arise from inadequate documentation, improper reliance on management experts, and weak risk assessment methodologies.

Imagine an auditor relying blindly on an expert’s valuation, later finding that flawed assumptions led to a massive financial misstatement. Or consider an inventory audit where third-party stock verification is overlooked, leading to inflated asset values and regulatory penalties. These real-world challenges highlight the need for auditors to strengthen their approach to gathering and evaluating audit evidence.

This article dives deep into key observations from SA 500, Audit Evidence and associated standards, exploring where audits often fall short and how best practices can bridge these critical gaps. By adopting a meticulous and proactive approach, auditors can reinforce their role as financial gatekeepers, ensuring accuracy, credibility, and compliance.

1.1

Management often relies on experts for various financial estimations, such as depreciation, gratuity, and leave encashment liabilities. However, it was observed that auditors, in some cases, did not adequately evaluate these experts’ competence, capability, and objectivity. The reliance on such experts’ reports without due verification led to incomplete or unreliable audit evidence. Additionally, some expert reports lacked transparency regarding the basis of estimation, limitations, or assumptions, raising concerns over their credibility as audit evidence.

SA 500, Audit Evidence States:

“When information to be used as audit evidence has been prepared using the work of a management’s expert, the auditor shall, to the extent necessary, having regard to the significance of that expert’s work for the auditor’s purposes:

(a) Evaluate the competence, capabilities and objectivity of that expert;

(b) Obtain an understanding of the work of that expert; and

(c) Evaluate the appropriateness of that expert’s work as audit evidence for the relevant assertion.” (Para 8)

As per SA 500, when information is to be used as audit evidence and has been prepared using the work of a management expert, the auditor needs to evaluate that expert’s competence, capabilities, and objectivity. The auditor should obtain an understanding of the expert’s work and evaluate the appropriateness of that expert’s work as audit evidence for the relevant assertion. Preparing an entity’s financial statements may require expertise in a field other than accounting or auditing, such as actuarial calculations, valuations, or engineering data. Failure to assess these aspects increases the risk of material misstatements in the financial statements.

An extract from the ONGC Independent Auditor’s Report for the year ended 31st March 2024 that reflects the scrutiny of the report on ‘IT audit and security’ of a third-party expert by the auditor is enclosed below:

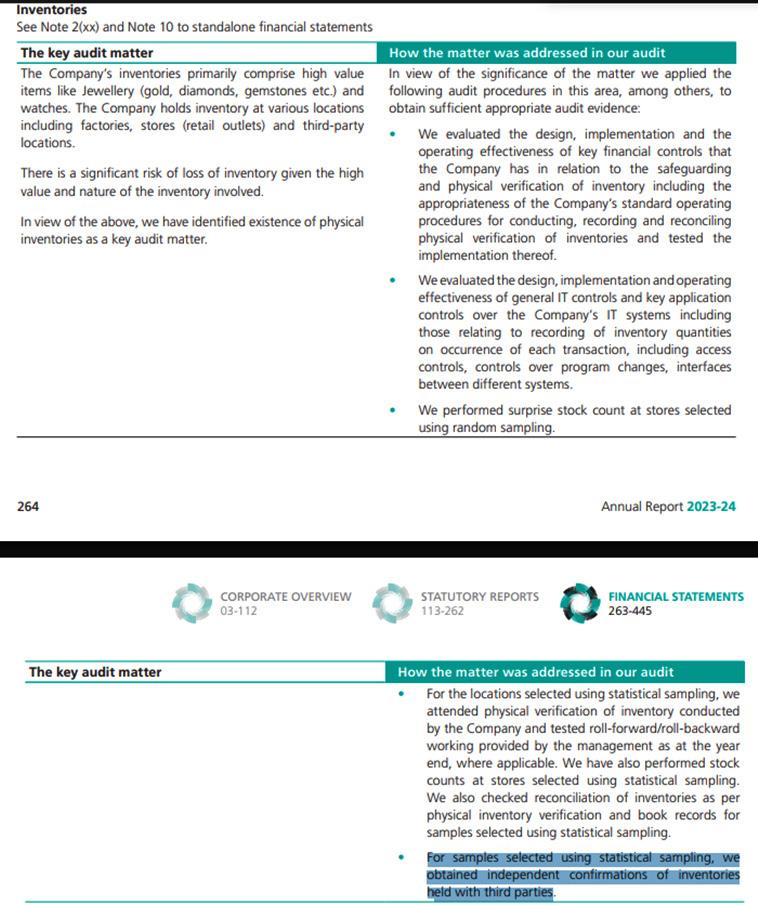

There were instances where auditors did not obtain sufficient documentation for inventory held by third parties. The audit files lacked evidence of confirmations being sent to third parties or alternative procedures to verify the stock’s physical existence. In cases where inventory was material to the financial statements, this lack of confirmation increased the audit risk.

SA 501, Audit Evidence—Specific Considerations for Selected Items States:

“When inventory under the custody and control of a third party is material to the financial statements, the auditor shall obtain sufficient appropriate audit evidence regarding the existence and condition of that inventory by performing one or both of the following:

(a) Request confirmation from the third party as to the quantities and condition of inventory held on behalf of the entity or

(b) Perform inspection or other appropriate audit procedures.” (Para 8)

SA 501 requires the audit firm to confirm significant inventory held by third parties at the physical inventory date. In addition to confirmation, the audit firm may also consider

performing additional procedures depending on the nature of the inventory and other circumstances. These procedures may include attending or arranging for another auditor to attend the third party’s physical counting of inventory, obtaining another auditor’s report on the adequacy of internal controls, inspecting documentation such as warehouse receipts, or requesting confirmation from third parties when inventory has been pledged as collateral.

An extract from the Titan Company Limited Independent Auditor’s Report for the year ended 31st March 2024 that reflects the independent confirmation obtained of inventories held with a third party by the auditor is enclosed below:

3.1 Observation

In several cases, audit firms did not document procedures for verifying opening balances when appointed as new auditors. This raised concerns regarding the accuracy of financial data carried forward from prior periods. Additionally, there was inadequate evidence of reviewing previous audit work or assessing whether prior period misstatements had a continuing impact.

SA 510, Initial Audit Engagements – Opening Balances States:

• “The auditor shall obtain sufficient appropriate audit evidence about whether the opening balances contain misstatements that materially affect the current period’s financial statements.” (Para 3)

• “The auditor shall determine whether the prior period’s closing balances have been correctly brought forward to the current period or, when appropriate, any adjustments have been disclosed as prior period items in the current year’s Statement of Profit and Loss.” (Para 6(a))

SA 510 describes the additional procedures that an auditor should perform when engaged to audit an entity’s financial statements for the first time. In an initial audit engagement, the auditor should determine the appropriateness of the opening balances and assess whether accounting policies applied in prior periods have been consistently applied in the current period. The auditor must obtain sufficient appropriate audit evidence about whether the opening balances contain misstatements materially affecting the current period’s financial statements.

4.1 Observation

Audit documentation often lacked clarity on the rationale behind sample selection, the methodology used, and whether the selected sample size adequately addressed audit

risks. In certain cases, auditors did not document considerations for determining sample sizes, nor did they justify why specific items were included or excluded from the sampling process.

4.2 Relevant Provision

SA 530, Audit Sampling States:

• “The auditor shall determine a sample size sufficient to reduce sampling risk to an acceptably low level.” (Para 7)

• “The auditor shall select items for the sample in such a way that each sampling unit in the population has a chance of selection.” (Para 8)

SA 530 requires the auditor to design an audit sample considering both the purpose of the audit procedure and the characteristics of the population from which the sample is drawn. The auditor should determine a sample size sufficient to reduce sampling risk to an acceptable level and ensure that items arto provideat provides a representative view of the population.

5.1 Observation

Auditors failed to document procedures to identify subsequent events that may require adjustments or disclosures in the financial statements. This lack of documentation raises concerns about whether all subsequent events were properly accounted for.

5.2 Relevant Provision

SA 560, Subsequent Events States:

• “The auditor shall perform audit procedures designed to obtain sufficient appropriate audit evidence that all events occurring between the financial statements and the date of the auditor’s report that require adjustment of, or disclosure in, the financial statements have been identified.” (Para 6)

SA 560 requires auditors to understand any procedures management has established to ensure that subsequent events are identified. Auditors should inquire with management and those charged with governance, review meeting minutes, and examine the entity’s latest subsequent interim financial statements. If a subsequent event requiring adjustment or disclosure is identified, the auditor should determine whether it is appropriately reflected in the financial statements.

Audit evidence is the cornerstone of financial statement credibility. The abovementioned observations underscore the need for auditors to adhere strictly to SA 500 and related auditing standards. By implementing proper verification procedures, ensuring expert evaluation, and maintaining robust documentation, auditors can enhance audit quality and mitigate financial misstatement risks. Ensuring compliance with SA 500 will improve financial transparency and reinforce trust in audit processes among stakeholders.

Founded 1972

Evolution From a small family business to a leading technology-oriented Publishing/Product company

Expansion

Launch of Taxmann Advisory for personalized consulting solutions

Aim

Achieve perfection, skill, and accuracy in all endeavour

Growth

Evolution into a company with strong independent divisions: Research & Editorial, Production, Sales & Marketing, and Technology

Future

Continuously providing practical solutions through Taxmann Advisory

Editorial and Research Division

Over 200 motivated legal professionals (Lawyers, Chartered Accountants, Company Secretaries)

Monitoring and processing developments in judicial, administrative, and legislative fields with unparalleled skill and accuracy

Helping businesses navigate complex tax and regulatory requirements with ease

Over 60 years of domain knowledge and trust

Technology-driven solutions for modern challenges

Ensuring perfection, skill, and accuracy in every solution provided

Income Tax

Corporate Tax Advisory

Trusts & NGO Consultancy

TDS Advisory

Global Mobility Services

Personal Taxation

Training

Due Diligence

Due Dilligence

Advisory Services

Assistance in compounding of offences

Transactions Services

Investment outside India

Goods

Transaction Advisory

Business Restructuring

Classification

Due Diligence

Training

Advisory

Trade Facilitation Measures

Corporate

Corporate Structuring

VAT Advisory

Residential Status

Naveen Wadhwa

Research and Advisory [Corporate and Personal Tax]

Chartered Accountant (All India 24th Rank)

14+ years of experience in Income tax and International Tax

Expertise across real estate, technology, publication, education, hospitality, and manufacturing sectors

Contributor to renowned media outlets on tax issues

Vinod K. Singhania Expert on Panel | Research and Advisory (Direct Tax)

Over 35 years of experience in tax laws

PhD in Corporate Economics and Legislation

Author and resource person in 800+ seminars

V.S. Datey Expert on Panel | Research and Advisory [Indirect Tax]

Holds 30+ years of experience

Engaged in consulting and training professionals on Indirect Taxation

A regular speaker at various industry forums, associations and industry workshops

Author of various books on Indirect Taxation used by professionals and Department officials

Manoj Fogla Expert on Panel | Research and Advisory [Charitable Trusts and NGOs]

Over three decades of practising experience on tax, legal and regulatory aspects of NPOs and Charitable Institutions

Law practitioner, a fellow member of the Institute of Chartered Accountants of India and also holds a Master's degree in Philosophy

PhD from Utkal University, Doctoral Research on Social Accountability Standards for NPOs

Author of several best-selling books for professionals, including the recent one titled 'Trust and NGO's Ready Reckoner' by Taxmann

Drafted publications for The Institute of Chartered Accountants of India, New Delhi, such as FAQs on GST for NPOs & FAQs on FCRA for NPOs.

Has been a faculty and resource person at various national and international forums

the UAE

Chartered Accountant (All India 36th Rank)

Has previously worked with the KPMG

S.S. Gupta Expert on Panel | Research and Advisory [Indirect Tax]

Chartered Accountant and Cost & Works Accountant

34+ Years of Experience in Indirect Taxation

Bestowed with numerous prestigious scholarships and prizes

Author of the book GST – How to Meet Your Obligations', which is widely referred to by Trade and Industry

Sudha G. Bhushan Expert on Panel | Research and Advisory [FEMA]

20+ Years of experience

Advisor to many Banks and MNCs

Experience in FDI and FEMA Advisory

Authored more than seven best-selling books

Provides training on FEMA to professionals

Experience in many sectors, including banking, fertilisers, and chemical

Has previously worked with Deloitte

Taxmann Delhi

59/32, New Rohtak Road

New Delhi – 110005 | India

Phone | 011 45562222

Email | sales@taxmann.com

Taxmann Mumbai

35, Bodke Building, Ground Floor, M.G. Road, Mulund (West), Opp. Mulund Railway Station Mumbai – 400080 | Maharashtra | India

Phone | +91 93222 47686

Email | sales.mumbai@taxmann.com

Taxmann Pune

Office No. 14, First Floor, Prestige Point, 283 Shukrwar Peth, Bajirao Road, Opp. Chinchechi Talim, Pune – 411002 | Maharashtra | India

Phone | +91 98224 11811

Email | sales.pune@taxmann.com

Taxmann Ahmedabad

7, Abhinav Arcade, Ground Floor, Pritam Nagar Paldi

Ahmedabad – 380007 | Gujarat | India

Phone: +91 99099 84900

Email: sales.ahmedabad@taxmann.com

Taxmann Hyderabad

4-1-369 Indralok Commercial Complex Shop No. 15/1 – Ground Floor, Reddy Hostel Lane Abids Hyderabad – 500001 | Telangana | India

Phone | +91 93910 41461

Email | sales.hyderabad@taxmann.com

Taxmann Chennai No. 26, 2, Rajan St, Rama Kamath Puram, T. Nagar

Chennai – 600017 | Tamil Nadu | India

Phone | +91 89390 09948

Email | sales.chennai@taxmann.com

Taxmann Bengaluru

12/1, Nirmal Nivas, Ground Floor, 4th Cross, Gandhi Nagar

Bengaluru – 560009 | Karnataka | India

Phone | +91 99869 50066

Email | sales.bengaluru@taxmann.com

Taxmann Kolkata Nigam Centre, 155-Lenin Sarani, Wellington, 2nd Floor, Room No. 213

Kolkata – 700013 | West Bengal | India

Phone | +91 98300 71313

Email | sales.kolkata@taxmann.com

Taxmann Lucknow

House No. LIG – 4/40, Sector – H, Jankipuram Lucknow – 226021 | Uttar Pradesh | India

Phone | +91 97924 23987

Email | sales.lucknow@taxmann.com

Taxmann Bhubaneswar

Plot No. 591, Nayapalli, Near Damayanti Apartments

Bhubaneswar – 751012 | Odisha | India

Phone | +91 99370 71353

Email | sales.bhubaneswar@taxmann.com

Taxmann Guwahati

House No. 2, Samnaay Path, Sawauchi Dakshin Gaon Road

Guwahati – 781040 | Assam | India

Phone | +91 70866 24504

Email | sales.guwahati@taxmann.com