WEST AFRICAN PAPERS

Secretariat

Secretariat

OCTOBER 2024, NO. 45

SAHEL AND Club WEST AFRICA

Secretariat

The West African Papers series explores African socio-economic, political and security transformations, their interactions and their effects. Intended for an audience of experts, researchers and decision makers, they aim to stimulate discussion and inform policy. The papers are available in English and/ or French and can be downloaded from:https://doi.org/10.1787/24142026

Pleasecitethisworkas:

Thériault, V. et al. (2024), ”Diet transformations and changing food environments in the Sahel and WestAfrica,”SahelandWestAfricaClub(OECD/SWAC),WestAfricanPapers,No.45,OECDPublishing, Paris.

Authorcontact:

VéroniqueThériault,MichiganStateUniversity,theria13@msu.edu

JillBouscarat(OECD/SWAC),jill.bouscarat@oecd.org

AlbanMasAparisi(OECD/SWAC),alban.masaparisi@oecd.org

PhilippHeinrigs(OECD/SWAC),philipp.heinrigs@oecd.org

AmidouAssima,amidou.assima@gmail.com

OECD Working Papers should not be reported as representing the officialviews of the OECD or of its member countries. The opinions expressed and arguments employed are those of the authors.WorkingPapersdescribepreliminaryresultsorresearchinprogressbytheauthor(s)andare publishedtostimulatediscussiononabroadrangeofissuesonwhichtheOECDworks.Commentson Working Papers are welcomed and may be sent to OECD/SWAC, 2 rue André-Pascal, 75775 Paris Cedex16.

Co-funded by the European Union. Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union. Neither the European Union nor the grantingauthoritycanbeheldresponsibleforthem.

This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the nameofanyterritory,cityorarea.

AuthorisedforpublicationbySibiriJeanZoundi,Director(Acting),SahelandWestAfricaClub Secretariat(OECD/SWAC).

©OECD/SWAC2024

The use of this work, whether digital or print, is governed by the terms and conditions to be foundat http://www http://www.oecd.or.oecd.or/g/termsandconditions g/termsandconditions/

Abstract:

Over the past two decades, urban population growth and rising incomes in West Africa have increased demand for diverse, convenient, safe and nutritious foods, including processed products. At the same time, urbanisation is changing foods environments —the physical, economic, and informational contexts that influence consumer food choices—with expected implications for nutrition. This paper assesses the current understanding of diets and food environment transformations in the region. Findings indicate a shift towards more nutritious foods, as well as oils, sweets, and high-fat products, with dietary changes varying across income groups. Food environments are growing more complex, with numerous outlets offering diverse products, but with inconsistent proximity and affordability. The rapid pace of these changes emphasizes the need for better data systems to update our understanding of food consumption patterns in the region and to capture their growing complexity.

Key words: food systems, food environment, nutrition, healthy diets, West Africa

JEL classification: Q13, Q18, I18, 055

The Sahel and West Africa Club (SWAC) is an international platform whose Secretariat is hosted by the Organisation for Economic Co-operation and Development (OECD). OECD/SWAC produces and maps data, provides informed analyses and facilitatesstrategic dialogue, to help better anticipate transformations in the region and their territorial impacts. Through its retrospective and prospective approach, it promotes more contextualised policies as levers for regional integration, sustainable development and stability. Its areas of work include food systems, urbanisation,climateandsecurity.

Its Members and financial partners are Austria (Federal Ministry of European and International Affairs/Austrian Development Agency), Belgium (Ministry of Foreign Affairs,Foreign Trade and Development Cooperation), Canada (Global AffairsCanada), CILSS (Permanent Interstate Committee for Drought Control in the Sahel), the ECOWAS (Economic Community of West African States) Commission, the European Union, GIZ (Deutsche Gesellschaft für Internationale Zusammenarbeit), France (Ministry for Europe and Foreign Affairs/Agence française de développement), Luxembourg (Ministry of Foreign and European Affairs, Directorate for Development Cooperation and Humanitarian Affairs), the Netherlands (Ministry of Foreign Affairs), Spain (Spanish Agency for International Development Cooperation), Switzerland (Swiss Agency for Development and Cooperation/Federal Department of Foreign Affairs), the UEMOA (West AfricanEconomicandMonetaryUnion)CommissionandtheUnited States(USAID).

Formoreinformation: https://www https://www.oecd.org/swac .oecd.org/swac

- Diets are diversifying, but not equally across households .........................................................

- Increased demand for convenience foods ....................................................................................

- Importance of food consumed out of the home .................

............

-Physical access: High reliance on a plurality of food outlets, with disparities in proximity ..

- Affordability: Food is expensive, incomes are low, and healthy diets out of reach ................

- Information and food product attributes .........................................................................................

FIGURES

Figure 1.

Number of food groups consumed in rural and urban areas over time .............................

Figure 2.

F ood group frequency consumption (#days/week) ................................................................

Figure 3.

N umber of food groups consumed across expenditure quintiles, 2018-19 .......................

Figure 4.

F ood group consumption across expenditure quintiles, 2018-19 (#days/week) ...............

Figure 5.

Food group frequency consumption in rural and urban areas, 2018-19 (#days/week) ....

Figure 6.

Sources of food items consumed in the previous 7 days, 2018-19 (%) ................................

Figure 7.

Sources of foods purchased by Malian and Senegalese households, 2023 (%) .................

Figure 8.

Share of the budget allocated to food across expenditure quintiles, 2018-19 (%) ............ TABLES

Table 1.

Share of processed food items consumed by households, 2018-19 (%) ..............................

Table 2.

Share of HHs who consumed a meal/snack/drink in the last 7 days, 2018-19 (%) .............

Table 3a.

Food groups utlets in Mali, 2023 (%) .........................................................................................

Table 3b.

Food groups purchasing outlets in Senegal, 2023 (%) ...........................................................

Over the last two decades, West African countries have experienced significantpopulation growth. From 2000 to 2020,thenumberofinhabitantshasincreasedfrom222millionto395million(SWAC/OECD,2024[1]).Thesameperiod sawanevenfasterriseinurbanisation:thepopulationgrewbyafactorof2.4,andurbanresidentsnowmakeuphalf ofthepopulation.Populationgrowthandurbanisationwereaccompaniedbysignificantincreasesinincomesandper capitagrossdomesticproduct(IMF,2021[2]).

Thesepatternshaveconvergedtoboostdemandformorediverse,convenient,saferandnutritiousproducts— including fruits, vegetables and animal-sourced foods (Staatz and Hollinger, 2016[3]). Demand has also risen for processedfoodsandfoodconsumedoutsidethehome(Adeosun,GreeneandOosterveer,2022[₄).Thisshiftindiets, driven by socio-demographic and economic changes, has been referred to as a diet transformation (Worku et al., 2017[5]);(Tschirleyetal.,2015[6]).

In conjunction with major socio-economic drivers that have caused these changes, food environments are shaping consumers’ food decisions. Food environments can be described as the physical, economic, political, and sociocultural context in which consumers engage with the food system to make decisions about acquiring, preparing, andconsumingfood(HLPE,2017[7]).

In environments where consumers rely on markets to procure food, consumption choices are influencedby the accessibilityandavailabilityoffoodoutletsandfoodproducts,andconsumers’abilitytotravel.Thequantityandtypes of foods purchased are also extensively determined by food prices and consumer incomes. Information sharing, througheducation,promotionandadvertising,aswellastheattributesoffoodproducts(e.g.theirqualityandsafety) canequallyaffectconsumerpreferencesandtheirperceptionofrisksandbenefitsrelatedtofood.

Urbanisation and rising incomes are also changing food environments. Urbanisation including secondary cities andsmallsettlementsinsemiruralareas isassociatedwithagreaternumberanddiversityoffoodoutlets,whether shops,kiosksorsupermarkets(Laaretal.,2022[8]).Foodsupplypatternsvaryacrossoutlets,forinstanceinthedegree of processing, the availability of perishable food and in food safety levels. Urbanisation is also linked to increased economicinequality,withimplicationsforfoodaffordability(DeBruinetal.,2021[9]).Thiscreatescomplexandevolving foodenvironments.

The transformation in West African diets and food environments has important implications for food and nutrition security. West Africa is transitioning through the so-called “triple burden of malnutrition” where the incidence of overnutrition (overweight and obesity) is growing fast, even while undernutrition (stunting and wasting) and micronutrient deficienciesremain significant.Over 58 million people are classifiedas underweight, and around 52 millionareeitheroverweightorobeseintheregion(SWAC/OECD,2021[10]).

Foodenvironments,whichareamenabletopoliciesandinterventions,canhelpaddressfoodandnutritionsecurityby makinghealthyandnutritiousfoodmoreavailable,accessible,affordable,acceptableandsafeforconsumers.Recent research has demonstrated the important role that food environments play in influencingdiets and nutrition (see Adeosun,GreeneandOosterveer,2022[4]forNigeria;Mockshelletal.,2022[11]forGhana;andIgnowskietal.,2023[12]) andAmbikapathietal.,2021[13])forTanzania).

Improving food and nutrition security in the region requires a grounded understanding of the current state and trendsindietarypatternsandfoodenvironments.Yet,studiesonfoodenvironmentsinWestAfricaandAfricaoverall remainlimited,andmostoftheliteraturefocusesonhigh-incomecountries (Laaretal.,202[4];Toureetal.,2021[14]); Turneretal.,2018[15]).

This paper addresses the gap by reviewing and analysing the literature and datasets available in West Africa. By outlining the shifts in the region on the basis of the latest information available, it aims to identify critical avenues for further data collection and research.

The paper first reviews the data that has been used to identify shifting diets and food environments. Second, it presents key findings about shifts in diet in the region. Third, it presents the state of knowledge on changing food environments. Fourth, it pinpoints areas of research that deserve further attention, to improve understanding of the changes in the way West Africans consume food.

The literature on food environments and diet transformation, with an emphasis on the Sahel and West Africa and more broadly on Africa, is first reviewed to develop a better understanding of how food choices are made and their implications for food and nutrition security.

The paper then explores trends in food consumption and food environments in the Sahel and West Africa through descriptive data analysis, including, in particular, a collection of harmonised surveys on household living conditions in Mali, Nigeria and Senegal (henceforth referred to as LSMS datasets). Although LSMS datasets do not contain panel data, their national-level representation allows for analysis of change over time. Given that comparable data for previous years is not available for Senegal, the temporal descriptive analyses only involve Mali and Nigeria.

The Harmonized Survey on Households Living Standards 2018-19 and the Integrated Agricultural Survey 2014 is used for Mali (UEMOA Commission, 2022[16]); (Cellule de Planification et de Statistiques (CPS), 2020[17]). Approximately 6 600 and 3 800 Malian households were surveyed in 2018-19 and 2014-15, respectively.

The General Household Survey, Panel 2018-2019, Wave 4 and General Household Survey, Panel 20152016, Wave 3 in Nigeria (Nigeria National Bureau of Statistics, 2021[18]); (Nigeria National Bureau of Statistics, 2019[19]) is used for Nigeria. Approximately 4 900 households were surveyed in Nigeria in 2018-19 and and 4 500 in 2015-16, respectively.

The Harmonized Survey on Households Living Standards 2018-19, which included 7 100 households (UEMOA Commission, 2022[16]) is used for Senegal.

Additional data come from household food consumption surveys (henceforth referred to as HFCS datasets) conducted in Mali and Senegal in 2023 (Theriault, 2024a[20]), (Theriault, 2024b[21]). During this project, approximately 400 urban and rural households were interviewed about their food consumption and purchasing habits in the southern regions of Mali and across all regions in Senegal. Information from these surveys is used to describe food market environments.

Similarly, data from an informal food trader survey (henceforth referred to as IFTS datasets) conducted in two secondary cities in Nigeria and three cities in Ghana in 2018, are used to examine key elements of the food market environments in these countries (IFPRI, 2019[22]), (IFPRI, 2020[23]). In these data, over 1 000 informal food retail traders selling either fresh, packaged and/or processed foods were asked about their trading activities, as well as their food purchasing habits.

Dietsarediversifying,butnotequallyacrosshouseholds

WestAfricansareconsumingmorefoodgroups,morefrequently

The number of food groups consumed1 increased in both urban and rural households in Mali and Nigeria between 2014/15-2015/16 and 2018/19 (Figure 1) The increase is limited, however, at between 1 to 2 food groups out of a maximumof12.Thediversificationofdietsisalsobecomingmoreconsistent:overthesameperiodthefrequencyof consumptionwentupfor8outof10foodgroupsinMaliand4outof10foodgroups inNigeria (Figure2).2

Figure1. Numberoffoodgroupsconsumedinruralandurbanareas,2014-15and2018-19

Note: This represents the number of food groups consumed in the last seven days, since information on the previous 24 hours was not available.

Source: Authors’ calculations from LSMS datasets.

Diversification is occurring across food groups typically associated with healthy diets, such as fruits and vegetables. For instance, the frequency of fruit consumption more than doubled in Mali, and consumption of vegetables increased from four to five days per week; but meanwhile, the consumption of oil, fat and sweets also increased by a day per week. The greater diversification does not imply any substitution of staple foods. Diets remain anchored around consumption of cereals — almost daily in Mali and Senegal and five days per week in Nigeria.

Figure 2.

Frequency of consumption (#days/week) of food groups

Note: The frequency of consumption of food groups per week refers to the number of days within a week that the specific food group was consumed.

Source: Authors’ calculations from LSMS datasets.

Diet diversification is limited in poorer and rural households

Diversification of diet is unequal across income levels. Poorer households consume around 8 different food groups, compared to approximately 10 for the wealthiest households (Figure 3). Poor and wealthy households have similar frequencies of consumption for staple foods, such as cereals in Mali and Nigeria, and legumes in Nigeria and Senegal. However, poorer households consume other food groups less frequently. The difference in the frequency of consumption is particularly marked for highly nutritious food groups, such as animal-sourced products, fruits and vegetables (Figure 4). There is a difference in the frequency of food group consumption not only between the poorest and wealthiest households, but also between the poorest (quintile 1) and slightly less poor households (quintile 2).

Figure 3.

Number of food groups consumed across expenditure quintiles, 2018-19

Note: Total household expenditure is used as a proxy for total household income The first income level (expenditure quintile1)representsthepooresthouseholdsandthefifthincomelevel(expenditurequintile5)representsthe wealthiesthouseholds.

Source: Authors’ calculations from LSMS datasets.

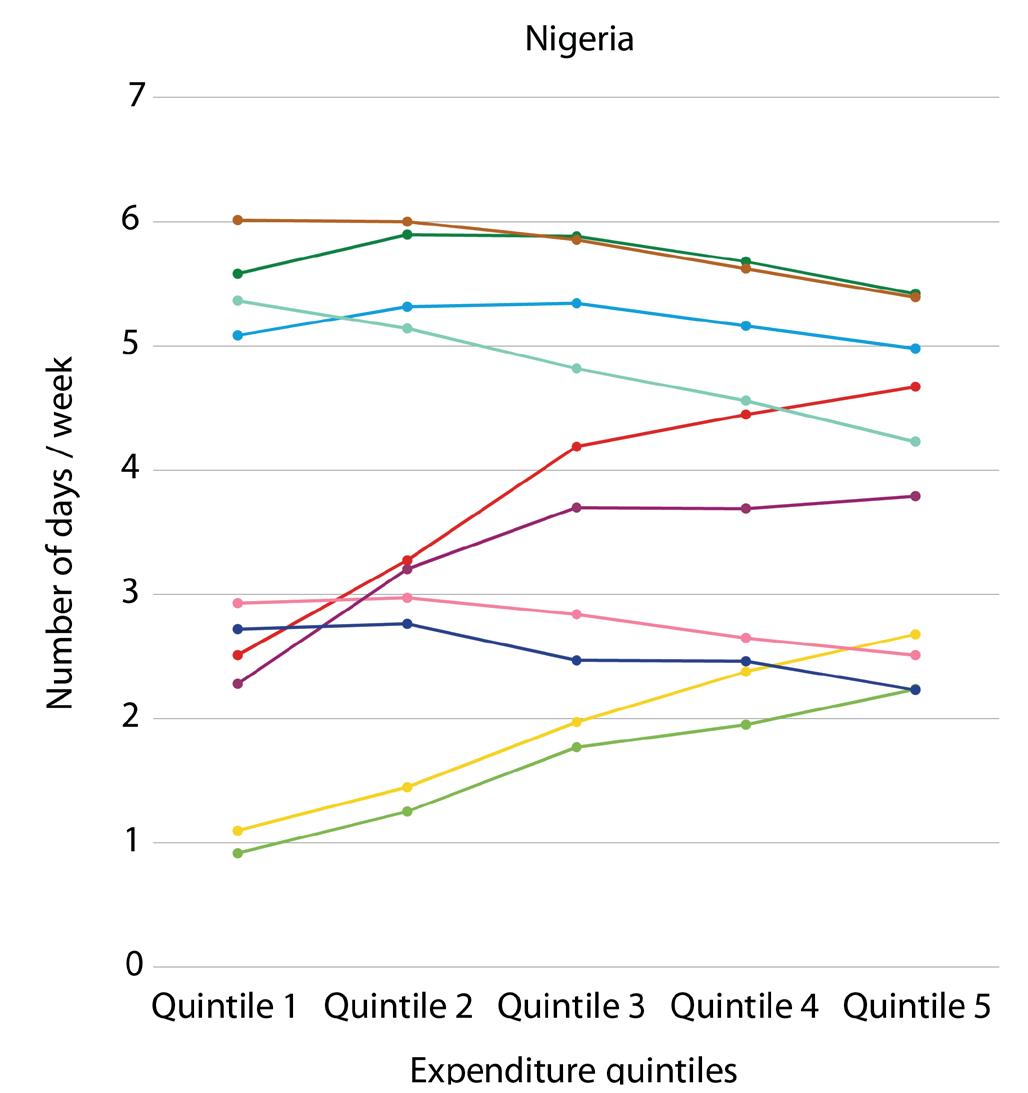

Figure 4.

Frequency of consumption (#days/week) of food groups by expenditure quintiles, 2018-19

Note: Total household expenditure is used as a proxy for total household income. The first income level (expenditure quintile 1) represents the poorest households and the fifth income level (expenditure quintile 5) represents the wealthiest households.

Source: Authors’ calculations from LSMS datasets.

There are notable discrepancies between urban and rural households in frequency of consumption (Figure 5). Urban households consume high-value products more often. These results are aligned with those of (Zhou and Staatz, 2016[24]), who projected that demand for diverse foods would grow more rapidly in cities, especially for animal-based foods. More granular studies also point to differences in urban/rural consumption patterns within food groups. For instance, in the fruits and vegetables group in Senegal, rural households consume more leaves, okra and African eggplant; while urban households consume more fruits, in particular watermelons and bananas (Faye et al., 2023[25]).

Figure 5. Frequency of consumption (#days/week) of food groups in rural and urban areas, 2018-19

Source: Authors’ calculations from LSMS dataset.

Processed and ultra-processed foods3 are widely consumed in Mali, Nigeria and Senegal, accounting for 48%, 40% and48%ofallfooditemsconsumedbyhouseholdsintheprevioussevendaysin2018/19,respectively.Theevidence further points to an increase in the consumption of ultra-processed foods. The share of ultra-processed food items is respectively 25% (Mali), 16% (Nigeria) and 25% (Senegal) (Table 1) Using data from a 24-hour recall, (Kébé et al., 2024[26])estimatedthatinSenegal,30%offoodsconsumedwereultra-processed.

The consumption of processed and ultra-processed foods is not an urban phenomenon. The share of these foods consumed by rural and urban households is comparable in Mali and Senegal, whereas it is slightly lower in rural households(38%)thanurbanhouseholds(43%)inNigeria(LSMSdatasets).Thepenetrationofprocessedfoodshas been observed in Mali, where (Smale, Theriault and Vroegindewey, 2020[27]) estimated the share of the total food budgetspentonhighlyprocessedfoodsas15%and7%inurbanandruralareasofMali,respectively.

Table1.

Shareofprocessedfooditemsconsumedbyhouseholds,2018-19(%)

Source: Authors’ calculations from LSMS datasets.

Although ultra-processed food consumption is widespread in the region, the evidence available suggests it is correlated with income levels. In Nigeria, 22% of the food consumed by the wealthiest households was ultra-processed, compared to 10% for the poorest (LSMS datasets). Another study conducted in Nigeria, Tanzania and Uganda estimated that the consumption of ultra-processed foods accounted for about 12% in value of the food consumption of the poor, compared to 20% and 32% for the lower and upper middle classes (Dolislager et al., 2022[28]). This relationship between the share of purchased (ultra) processed foods, in value terms and income was also found in Tanzania (Sauer et al., 2021[29]).

InMali,NigeriaandSenegal,aboutthree-quartersormoreofhouseholdshaveatleastonememberwhoconsumes a meal, snack and/or beverage away from home on a weekly basis (Table 2). The share of households consuming foodawayfromhomedropstolessthanone-quarterinMaliandlessthanhalfinSenegalwhenconsideringtwoor more household members consuming foods outside the home together (LSMS datasets). Between 40% to 50% of households, in all three countries, had at least one member consuming a snack (i.e. any food consumed between meals)intheprevioussevendays

Overall,theconsumptionoffoodoutsidethehomehasspreadtobothruralandurbanareas,butishigherinurban areas (Table 2) and increases with income. About 90% or more of wealthier households (quintile 5) reported that at leastonehouseholdmemberhadconsumedfoodsoutsidethehomeintheprevioussevendays,comparedto63%, 75%and53%ofthepooresthouseholds(quintile1)inMali,NigeriaandSenegal,respectively(LSMSdatasets).

Table 2. Households(%)consumingameal/snack/drinkoutsidethehomeinpast7days,2018-19

Note: One or more household members reported as having consumed foods outside the home. Source: Authors’ calculations from LSMS datasets.

Overall, the evidence available indicates that poorer households, as well as wealthier households in both rural and urban areas of Mali and Nigeria, have experienced noticeable changes in their eating habits. Their diets have diversified, and their consumption of processed foods has increased. Consumption of food away from home by at least one household member is relatively widespread, and on average, urban and higher-income households consume more animal-based and nutrient-dense foods and more foods outside the home. In Nigeria, ultraprocessed foods account for a higher percentage of the food consumed by wealthier households.

Food environments play a crucial role in consumers’ decisions about procuring, preparing and consuming food. Improved physical and economic access to diversified, healthy and safe food products enables consumers to make food choices to support a healthy and nutritious diet, as do information and education. The literature presents different characterisations of the food environment, depending on the research emphasis. This paper definesthe food environment as being composed of four dimensions: physical access; affordability; promotion, advertising and information(henceforthinformation);andquality/safety(henceforthfoodproductattributes)(HLPE,2017[7]).

Physical access refers to the presence and accessibility (e.g. proximity) of food products and locations for food procurement. Affordability refers to the price of food relative to a household’s income and purchasing power Promotion,advertisingandinformationsharinginfluencefoodpurchasingdecisions.Foodqualityandsafetyreferto attributesoffoodproductsthatmakethemmore(orless)valuable,acceptableandsafetoconsume.Giventhelimited literatureanddataavailableonthelasttwoelements,thispaperchieflydiscussesphysicalaccessandaffordability.

This dimension addresses the availability and accessibility of food outlets and products to consumers in time andspace,relativetotheirmobilityandaccesstotransport.

In West Africa, one of the central drivers of changing food environments is households’ increasing reliance on markets to meet their food requirements. Over 90% of food in West African cities, and over half in rural areas, is purchasedinmarkets(SWAC/OECD,2021[2]).Thisrelianceonmarketsalsoappliestolocallyproducedfoods.InMali, Nigeria, and Senegal, households purchase approximately 45%, 50% and 75% of their maize (Figure 6). As for millet and sorghum, regional staples that are typically associated with own consumption, their market purchase share ranges between approximately two-fifths to three-quarters and one-third to one-half across all three countries (Figure6).

This high reliance on markets is true not only for cities but also in rural areas. Rural households source a higher share of their food from their own production, but their market purchases are significant. In rural Mali and Nigeria, betweenone-thirdandone-halfofthemaize,milletandsorghumconsumedarepurchased(LSMSdatasets).Inrural Senegal,purchasesofmaize,milletandsorghumaccountforone-thirdtotwo-thirdsofconsumption(LSMSdataset). Thisrelianceonmarketsisalsotrueforhouseholdsofdifferentincomelevels.Forinstance,over30%ofthepoorest householdsdependonmarketstosourcemilletinMaliandNigeriaandnear60%inSenegal(LSMSdatasets).

These findings are aligned with (Smale, Theriault and Vroegindewey, 2020[27]), who found that own production accounted for 25% to 34% of the food consumed by Malian rural households during the lean and harvest seasons. Examining rural household food consumption across several countries in sub-Saharan Africa, (Dzanku, Liverpool-Tasie and Reardon, 2024[30]) alsofound that households met the majority of their food needs through the market. This includes basic staples and spanned different income brackets, agro-ecological zones and countries.

Figure 6.

Sources of food items consumed in the previous 7 days, 2018-19 (%)

Note: Quantities of food items consumed and reported in kilogrammes. The “Others” category includes gifts and donations.

Source: Authors’ calculations from LSMS datasets.

Consumers rely on a great diversity of outlets to purchase their food. Urbanisation is expanding consumer choice in retail food outlets, which include traditional open-air markets, street vendors, stores, independent and chain supermarkets, bakeries and restaurants.

Open-air markets still dominate food environments, accounting for approximately 50% and 60% of food items purchased by households in Senegal and Mali (Figure 7). However, other retail outlets, such as stores and street vendors, account for approximately 30% and 5%-15% of purchased food items in both countries (HFCS datasets).

Figure 7

Sources of foods purchased by Malian and Senegalese households, 2023 (%)

Note: The “Others” category includes supermarkets, bakeries, restaurants and any other types of food outlets. Source: Authors’ calculations from HFCS datasets (2024).

Supermarket chains have not yet been introduced in every country in the region (Barrett et al., 2022[31]). Independent and chain supermarkets continue to be exclusively located in large cities. Supermarkets’customers are mostly composed of a minority of higher-income households (Hannah et al., 2022[32]) For instance, only 7% and 1% of Senegalese and Malian households report purchasing food at supermarkets (HFCSdatasets).

A survey of informal food vendors in Nigeria, defined as those who sell food products in open-air markets and the streets nearby, reveal that 90% or more regularly source foods from other street or market vendors (IFTS datasets). This compares to 60%-70% who regularly source from shops and kiosks, and less than 15% who source from supermarkets (Resnick, 2018[33]). Among all food-retailing outlets (excluding restaurants), market stalls were by farthemostprevalenttypeofoutletsinallneighbourhoodssurveyedinthecityofZiguinchorinSenegal,whichhad no supermarket (GRDR, 2023[34]) Only one out of 668 (<1%) low- and middle-income households surveyed in Accra,Ghana,reportedsourcingfoodfromsupermarkets(Tuholskeetal.,2020[35]).

The type of food products supplied varies across outlets and neighbourhoods. Wealthier neighbourhoods tend to have a better supply of fresh and perishable products – especially animal-sourced products, which are more expensive and require an effective cold chain to ensure food safety. For instance, a greater selection of dairy products is available in supermarkets and in high-income urban neighbourhoods of Mali (Theriault et al., 2018[36]). Of all food groups, milk and milk products were also the most regularly sourced from supermarkets rather than other food retailing outlets in Nigeria (Resnick, 2018[33]). In the city of Ziguinchor in Senegal, fish is available in 30% of food-retailing outlets in wealthier neighbourhoods, compared to 10% in the least wealthy ones (GRDR, 2023[34]).

Among food vendors in Nigeria and Ghana, the most common food products sold are vegetables (36% and 35%), followed by dried/smoked fish (23% and 13%), and then roots and tubers (22%) in Nigeria and meat (10%) in Ghana (IFTS datasets). Only about 7% and 16% of Nigerian and Ghanaian traders indicated selling any other fresh food products (IFTS datasets).

The product differentiation for food outlets also goes beyond the fresh/non-fresh divide. For instance, more rural and urban households in Mali reported purchasing eggs, milk/dairy products and sugar/sweets in stores than in open-air markets (HFCS datasets). Fruit is the most common food group purchased from street vendors in Mali and Senegal (HFCS datasets) (Table 3).

Table 3a.

Food group purchase value, by purchasing outlets in Mali, 2023 (%)

Note: The “Others” category includes supermarkets, bakeries, restaurants and any other types of food outlets.

Source: Authors’ calculations from HFCS datasets (2024)

Table 3b.

group purchasing outlets in Senegal, 2023

Note: The “Others” category includes supermarkets, bakeries, restaurants and any other types of food outlets. Source: Authors’ calculations from HFCS datasets (2024).

The further a household is from food retailing options, the greater the opportunity cost for purchasing food, due to transport and time. In addition, the opportunity cost of time increases with income, which makes proximity to food retailing outlets increasingly valuable. For instance, urban consumers in Abidjan, Côte d’Ivoire, indicated a preference for purchasing food based on the retailer’s proximity over food price and quality (Balineau et al., 2021[37]). The relative importance of the retailer’s proximity, compared to food accessibility and quality, also varies from place to place (Balineau et al., 2021[37]).

In Mali, 22% and 5% of households in urban neighbourhoods and rural villages reported that walking to markets was the main mode of transport, compared to 32% and 22% of urban neighbourhoods and rural villages in Nigeria, and 64% to 47% of urban neighbourhoods and rural villages in Senegal (LSMS datasets). This means that a majority of households depend on transportation, public or private, for access to open-air markets, with implications in terms of inequality of mobility and opportunity cost for the foods purchased in these markets. For those who selected walking as their primary mode of transport, the median time to market is 35 minutes in Mali, compared to 20 minutes in Nigeria and 15 minutes in Senegal (LSMS datasets). In comparison, (Anderson et al. 2024[4]) estimated that approximately 60% of the population in Accra, Ghana, lives in an area at least 30 minutes by foot from a market (food or otherwise).

Despite the limited accessibility of food markets, many households can purchase food close to their home, particularly in stores and from street vendors. On average, 95% of food purchases in the previous seven days were made within 1 kilometre of the households in urban areas, compared to 89% in rural areas in Senegal (HFCS datasets). By comparison, 85% of food purchases by urban Malian households in the previous seven days were made within 1 kilometre of their home (HFCS datasets). In both countries, urban households had to travel the greatest distance, on average, to purchase foods from a supermarket and the shortest distance to purchase foods from stores and street vendors. A recent study in peri-urban Dar es Salaam showed that 50% of households had access to over 800 formal and informal food vendors within a 1-kilometre radius of their household (Ambikapathi et al. 2021[13]).

Economic access concerns both the prices and the affordability of food. While prices refer to the cost of food products, affordability is a function of food prices and household purchasing power (Turner et al., 2018[15]).

Lowincomeandhighfoodpriceslimithouseholds’purchasingpower

Foodaffordabilityisamajordeterminantoffoodchoices.InWestAfrica,foodpricesare30%to40%higherthanfood pricesinothercountrieswithsimilarpercapitaincome(Allen,2017[38]).

WestAfricansthusallocate,onaverage,alargeshareoftheirincometofood;at56%,65%and49%inMali,Nigeria andSenegal,respectively(LSMSdatasets).Theshareofincomespentonfoodissomewhatlowerinurbanareasthan inruralareas,whichisprimarilyafunctionofthehigherincomesinurbanareas(LSMSdatasets).Foodisexpensive, incomesarelowandhealthydietsareoutofreach(Figure8).Despitethis,theshareallocatedtofoodremainshigh even for the wealthiest households (quintile 5) in Mali, Nigeria and Senegal. In this context, even small food price increasescanleadtoareductioninthehouseholdconsumptionofmoreexpensivefoods,whichoftentendtobethe mostnutritious(e.g.fruits,vegetables,legumes,nutsandseedsoranimal-sourcedfoods)(Baietal.,2023[39]).

Figure8

Shareofthebudgetallocatedtofoodacrossexpenditurequintiles,2018-19(%)

Source: Authors’ calculations from LSMS datasets.

Healthydietsremainoutofreachforalargeshareofthepopulation

Thecostofahealthydiet⁴exceedsaveragefoodexpenditurelevelsforallWestAfricancountriesexceptCaboVerde, Guinea-Bissau,NigeriaandSenegal(Baietal.,2023[39]).Thiscosthascontinuedtoriseinrecentyears,fromaregional average of 3.2 to 3.7 PPP dollars per person per day between 2017 and 2021 (FAO, IFAD, UNICEF,WFP and WHO, 2023[40]).

The affordability of healthy food is a constraint. Most households cannot afford to spend more on food than they currently do. Limited purchasing power explains, in part, why healthy foods are unaffordable for many households Inefficiencyin the supply and distribution segments of the agri-food value chains, along with low productivity and limitedregionaltrade,alsocontributetoperenniallyhighfoodprices(Allen,2017[38]).Thesehavebeenincreasedby the inflationary pressures of the post-COVID recovery and of the wars in Ukraine and the Middle East on imported food, energy and fertiliser prices, as well as macro-economic challenges linked to exchange rate policies and the strengtheningoftheUSdollar(GlauberandLabordeDebucquet,2023[41]);WorldBank,2024b,2024a[42]).

Consumers’accesstoinformationaboutfood,throughpromotion,advertising,educationorsocio-culturalinteractions, caninfluencetheirdecisionsonwhattopurchase.

Media and marketing have had a strong impact on food choices in high-income countries by influencingproduct placement in supermarkets, as well as consumer preferences and perceptions of risks and benefits associated with foods (Briones Alonso, Cockx and Swinnen, 2018[43]) Most food advertising, worldwide, has been found to focus on promoting ultra-processed, packaged foods and beverages that are high in calories and low in nutrients, as demonstrated by (Santana et al., 2020[44]) for Brazil; (Abrahams et al., 2016[45]) for South Africa; (Allemandi et al., 2017[46]) for Argentina, and (Fagerberg et al., 2019[47]) for Sweden. Information campaigns have also been initiated to encourage healthy food consumption habits, with mixed findingson their effectiveness(Luo, Maafs‐Rodríguez andHatfield,2024[48]) Nutritionlabelscanhelptoaddressmalnutritionbyinforminganddirectingconsumersaway from unhealthy,ultra-processed foods (Reardon et al., 2021[49]); (Hawkes et al., 2015[50]). Despite the evidence that informationcaninfluencefoodchoice,literatureonthetopicisalmostnonexistentforWestAfrica.

One strand of the literature focuses on the willingness to pay for better quality and safer food products In Mali, (Vroegindewey et al., 2021[51]) found that urban consumers’ and retailers’ preferences and willingness to pay for ingredient labelling, product safety certificationand packaging of dairy products were aligned. In Senegal, both consumersandtradersexhibitedawillingnesstopayahigherpricefordriedmaize(Prietoetal.,2021[52]).InNigeria, poultry farmers, feed millers and maize traders also indicated a willingness to pay a higher price for aflatoxin-safe maize(Sanouetal.,2021[53]);(Johnsonetal.,2019[54]).

Another strand of the literature examines the perception of food quality and safety by consumers and the physical environment surrounding food handling and preparation along agri-food value chains. A review of studies on foodbornepathogensinsevensub-SaharanAfricancountriesindicatesahigherprevalenceofmajorpathogensforanimalbasedfoodproductsandforready-to-eatfoods,includingstreetfoodsandbeverages(Paudyaletal.,2017[55]).

Intheabsenceoflabellingandcertification,consumersoftenrelyonwhattheycanobservetojudgethequalityand safetyoffoodproducts,forinstance,presence/absenceofstagnantwater,trashandinsectsatthefoodretailoutlets. Forinstance,consumers’perceptionsofhowfoodsafetymeasureswerefollowedbyfarmers,processersandtraders offruitsandvegetablessoldinopen-airmarketsinfluencedhowtheyhandledandpreparedfoodsathomeinGhana (Lagerkvist,Amuakwa-MensahandTeiMensah,2018[56]).

This note identifies several findings that highlight the links between changing diets and shifts in food environments, and their importance for understanding nutritional outcomes in West Africa.

First, evidence from Mali, Senegal and Nigeria shows that food consumption is diversifying. Cereal products are still firmly at the centre of West Africans’ diets, but consumption of nutritious products (both fruits and vegetables) is growing, as is consumption of sweets, oils and fats. Food products that are easy to prepare and ready to eat are in high demand, and consumption of processed and ultra-processed foods and food consumed outside the home is widespread in rural and urban areas. Diet transformations are happening unequally, but consumption differs more widely across income groups than between rural and urban areas.

Second, the evidence points to complex food environments. A multiplicity of food outlets sell different types of products, with uneven levels of proximity and affordability. These differences play an important role in shaping consumers’ food choices, based on what is available, accessible and affordable. Given the importance of markets in food access, it becomes critical to understand how food environments shape consumption decisions.

Assessments of food market environments in the Sahel and West Africa remain scarce, due, in part, to limited data. Better-quality data, ideally nationally representative and over time, are needed. Data collection efforts should focus on documenting (1) the availability, affordability and quality of various food products across food outlets; (2) the hygienic/ sanitary aspects of diverse food retailing outlets; and (3) the extent of advertising promoting the consumption of unhealthy food products. Given that both urban and rural households rely heavily on the markets to meet their food needs, food market environment assessments should cover both urban and rural settings.

The current transformations in West African diets and food environments also need to be better reflected in food and nutrition security policy. The analysis underlines the significance of monitoring prices beyond traditional markets, and also of covering a greater variety of products. Food and nutrition security policies should consider not only the availability of cereals but market-based consumption of non-staples, processed and ultra-processed food. Key policy questions include: What food is supplied in what outlets, in what quantities and at what prices? How does the proximity, density and type of food retail outlets affect food availability and affordability? How does this, in turn, shape dietary and nutritional outcomes? How do advertising, promotional campaigns and socio-cultural preferences shape consumption patterns? How far are consumers willing to pay more for a higher quality of food?

¹ Following the guidelines of Kennedy et al. (2013) for measuring household dietary diversity, we used these 12 food groups: 1) cereals, 2) vegetables, 3) fruits, 4) eggs, 5) meats, 6) fish and seafood, 7) milk and milk products, 8) white tubers and roots, 9) legumes, nuts and seeds, 10) oils and fats, 11) sweets and 12) spices, condiments and beverages.

² The number of food groups was reduced to 10, rather than 12 (as in the previous figures). The number of food groups was changed because the survey question aggregated them differently. In the question about frequency of consumption, meat was added to fish and seafood, and eggs were added to milk and milk products.

³ This analysis relies on the NOVA classification system (Monteiro et al., 2019). The first level, unprocessed or minimally processed foods, refers to foods that have not undergone any alterations or that were minimally altered (e.g. milled, dried, shelled, fermented and pasteurised) and did not include multiple ingredients: eggs, fruits and vegetables. The second level is for processed culinary ingredients, which refers to products used for seasoning and cooking, such as oils, fats, salt and sugar. The third level, processed foods, refers to foods that are manufactured by combining culinary ingredients (level 2) with unprocessed or minimally processed foods (level 1), for instance fresh bread or dried fish. The fourth and last level, ultra-processed foods, refers to industrial formulations in which unprocessed/minimally processed foods (level 1) are added in small proportion or not at all, for instance breakfast cereals or sweetened juices.

⁴ FAFH = food away from home.

5 The cost of a healthy diet represents “the cost of the least expensive locally available foods to meet requirements for energy and food-based dietary guidelines (FBDGs) for a representative person within an energy balance of 2 330 kcal/ day” (FAO et al., 2023:199).

Abrahams, Z. et al. (2016), “A Study of Food Advertising in Magazines in South Africa”, Journal of Hunger and Environmental Nutrition, Vol. 12/3, pp. 429-441.

Adeosun, K.P., M. Greene and P. Oosterveer (2022), “Informal Ready-to-Eat Food Vending: A Social Practice Perspective on Urban Food Provisioning in Nigeria”, Food Security, Vol. 14, pp. 763-780.

Allemandi, L. et al. (2017), “Food Advertising on Argentinean Television: Are Ultra-Processed Foods in the Lead?”, Public Health Nutrition, Vol. 21/1, pp. 238-246.

Allen, T. (2017), “The cost of high food prices in West Africa”, West African Papers, No. 8, OECD Publishing, Paris, September, http://dx.doi.org/10.1787/c2db143f-en.

Alonso, Cockx, and J. Swinnen (2018), “Culture and Food Security”, Global Food Security, Vol. 17, pp. 113-127.

Anderson, B. et al. (2024), “Accessibility for all to unlock sustainable mobility: A gendered approach.The case of Accra and Kumasi in Ghana”, Sahel and West Africa Club (SWAC/OECD), West African Papers,forthcoming, OECD Publishing, Paris.

Ambikapathi, R. et al. (2021), “Informal Food Environment Is Associated with Household Vegetable Purchase Patterns and Dietary Intake in the DECIDE Study: Empirical Evidence from Food Vendor Mapping in Peri-urban Dar es Salaam, Tanzania”, Global Food Security, Vol. 28, p.100 474.

Bai, Y. et al. (2023), “Healthy Diets, Costs, and Food Policies in the Sahel and West Africa”, West African Papers, Vol. No. 40 , OECD Publishing, Paris.

Balineau, G. et al. (2021), “Food Systems in Africa. Rethinking the Role of Markets”, Africa Development Forum Series, a co-publication of the Agence francaise de développement and The World Bank, Paris/Washington DC.

Barrett, C.B. et al. (2022), “Agri-Food Value Chain Revolutions in Low- and Middle-Income Countries”, Journal of Economic Literature, Vol. 60/4, pp.136<?>-1 377.

Cellule de Planification et de Statistiques (CPS) (2020), Enquête Agricole de Conjoncture Intégrée (ECAI) 2014. Ref. MLI_2014_EACI_M_v03_M., World Bank Databank (database), https://doi.org/10.48529/qqam-mn86

Dzanku, F.M., L.S.O. Liverpool-Tasie and T. Reardon (2024), “The Importance and Determinants of Purchases in Rural Food Consumption in Africa: Implications for Food Security Strategies”, Global Food Security, Vol. 40, p. 100 739

De Bruin, Sophie; Dengerink, Just; van Vliet, Jasper (2021), “Urbanisation as driver of food system transformation and opportunities for rural livelihoods”, Food Security, Vol.13, pp 781-798.

Dolislager, M. et al. (2022), “Consumption of Healthy and Unhealthy Foods by the African Poor: Evidence from Nigeria, Tanzania, and Uganda”, Agricultural Economics, Vol. 53, pp. 870-894.

Fagerberg, P. et al. (2019), “Ultra-processed Food Advertisements Dominate the Food Advertising Landscape in Two Stockholm Areas with Low vs High Socioeconomic Status. Is It Time for Regulatory Action?”, BMC Public Health, Vol. 19, p. 1 717.

FAO, IFAD, UNICEF, WFP and WHO (2023), “The State of Food Security and Nutrition in the World 2023. Urbanization, Agrifood Systems Transformation, and Healthy Diets across the Rural-Urban Continuum”, Food and Agriculture Organization, Rome.

Faye, N.F. et al. (2023), “Consumption of Fruits and Vegetables by Types and Sources across Urban and Rural Senegal”, Journal of Agribusiness in Developing and Emerging Economies, https://doi.org/10.1108/ JADEE-05-2022-0090.

Glauber, J. W., & Laborde Debucquet, D. (2023). How will Russia's invasion of Ukraine affect global food security?.

Groupe d’experts de haut niveau sur la sécurité alimentaire et la nutrition (HLPE) (2017), Nutrition and food systems A report by the High-Level Panel of Experts on Food Security and Nutrition of the Committee on World Food Security.

Hawkes, C. et al. (2015), “Obesity 2. Smart Food Policies for Obesity Prevention”, Lancet, Vol. 385<?>, pp. 2 410-2 421.

Hannah, C., Davies, J., Green, R., Zimmer, A., Anderson, P., Battersby, J.,& Evans, T. P. (2022). Persistence of openair markets in the food systems of Africa's secondary cities. Cities, 124, 103608.

HLPE (2017), “Nutrition and food systems. A report by the High-Level Panel of Experts on Food Security and Nutrition of the Committee on World Food Security”, High-Level Panel of Experts, Rome.

Hollinger, F. and Staatz, J. (2015), “Agricultural Growth in West Africa”, Market and Policy Drivers, African Development Bank and the Food and Agriculture Organization, Rome.

Ignowski, L. et al. (2023), “Dietary Inadequacy in Tanzania Is Linked to the Rising Cost of Nutritious Foods and Consumption of Food-Away-from-Home”, Global Food Security, Vol. 37, p. 100 679.

International Food Policy Research Institute (IFPRI), 2019), “Informal Food Retail Trade in Nigeria’s Secondary Cities”, Harvard Dataverse, V1, UNF:6:KuMQKbcis/5/ma2hoNUwlA== [fileUNF], accessed on 12 February 2024, https://doi.org/10.7910/DVN/F2PKSE.

International Food Policy Research Institute (IFPRI), (2020), “Informal Food Retail Trade in Ghanaian Cities”, Harvard Dataverse, V1, UNF:6:MHOn0SY6U5fvHyKjak26tQ== [fileUNF], https://doi.org/10.7910/DVN/DKDUU9.

International Monetary Fund (IMF), (2021), Real per Capita GDP Growth. https://www.imf.org/external/ datamapper/NGDPRPC_PCH@AFRREO/SSA/OEXP/OIMP/ECOWAS.

Johnson, A.M. et al. (2017), “Willingness to Pay of Nigerian Poultry Producers and Feed Millers for Aflatoxin-Safe Maize”, Agribusiness, 2019, pp. 1-19.

Kebe, S.D. et al. (2024), “Assessment of Ultra-processed Foods Consumption in Senegal: Validation of the NOVAUPF Screener”, Archives of Public Health, Vol. 82/4.

Laar, A.K. et al. (2022), “Perspective: Food Environment Research Priorities for Africa- Lessons from the Africa Food Environment Research Network”, Advances in Nutrition, Vol. 13/3, pp. 739-747.

Lagerkvist, C.J., F. Amankwa-Mensah and J.T. Mensah (2018), “How Consumer Confidence in Food Safety Practices along the Food Supply Chain Determines Food Handling Practices: Evidence from Ghana”, Food Control, Vol.13/3 93, pp. 265-273.

Luo, Y., A.G. Maafs-Rodriguez and D.P. Hatfield (2024), “The Individual-Level Effects of Social Media Campaigns Related to Healthy Eating, Physical Activity, and Healthy Weight: A Narrative Review”, Obesity Science and Practice, Vol. 10/1, pp. e731.

Mockshell, J. et al. (2022), “How Healthy and Food Secure Is the Urban Food Environment in Ghana?” World Development Perspectives, 26:100427. https://www.sciencedirect.com/science/article/pii/S2452292922000352.

Nigeria National Bureau of Statistics (2021), General Household Survey, Panel (GHS-Panel) 2018-2019, World Bank Databank (database), www.microdata.worldbank.org on 3 October 2023.

Nigeria National Bureau of Statistics (2019), General Household Survey, Panel (GHS-Panel) 2015-2016. Ref. NGA_2015_GHSP-W3_v02_M. World Bank Databank (database), www.microdata.worldbank.org on 3 October 2023.

Paudyal, N. et al. (2017), “Prevalence of Foodborne Pathogens in Food from Selected African Countries: A Metaanalysis”, Food Control, Vol. 249, pp. 35-43.

Prieto, S. et al. (2021), “Incomplete Information and Product Quality in Rural Markets: Evidence from an Experimental Auction for Maize in Senegal”, Economic Development and Cultural Change, Vol. 69/4, pp.1 351-1 377.

Reardon, T. et al. (2021), “The Processed Food Revolution in African Food Systems and the Double Burden of Malnutrition”, Global Food Security, Vol. 28, p. 100 466.

Resnik, D. et al. (2018), “The Enabling Environment for Informal Food Traders in Nigeria’s Secondary Cities”, IFPRI Strategy Support Program. Working Paper 59, Washington DC.

Sanou, A. et al. (2021), “Introducing an Aflatoxin-safe Labeling Program in Complex Food Supply Chains: Evidence from a Choice Experiment in Nigeria”, Food Policy, Vol. 102/5, p. 102070.

Santana, M.O. et al. (2020), “Analysing Persuasive Marketing of Ultra-Processed Foods on Brazilian Television”, International Journal of Public Health, Vol. 65/7, pp. 1 067-1 077.

Sauer, C. et al. (2021), “Consumption of Processed Food and Food Away from Home in Big Cities, Small Towns, and Rural Areas of Tanzania”, Agricultural Economics, Vol. 52, pp. 749-770.

Smale, M., V. Theriault and R. Vroegindewey (2020), “Nutritional Implications of Dietary Patterns in Mali”, African Journal of Agricultural and Resource Economics, Vol. 15/3, pp.177-193.

SWAC/OECD (2022), Africapolis (database), accessed on 10 October 2023.

OECD/SWAC (2024), Africapolis (database), www.africapolis.org.

Theriault, V., M. Sissoko and A. Assima (2024a), “Feed the Future Innovation Lab for Legume Systems Research”, Cowpea Household Consumption Survey in Mali (dataset).

Theriault, V. et al. (2024b), “Feed the Future Innovation Lab for Legume Systems Research”, Cowpea Household Consumption Survey in Mali (dataset).

Theriault, V. (2018), “Retailing of Processed Dairy and Grain Products in Mali: Evidence from a City Retail Outlet Inventory”, Urban Science, Vol. 2/24, pp.1-17.

Toure, D. et al. (2021), “An Emergent Framework of the Market Food Environment in Low- and Middle-Income Countries”, Current Developments in Nutrition, Vol. 5/4.

Tschirley, D. et al. (2015), “The Rise of a Middle Class in East and Southern Africa: Implications for Food System Transformation”, Journal of International Development, Vol. 27/5, pp. 628-646.

Tuholske, C. et al. (2020), “Comparing Measures of Urban Food Security in Accra, Ghana”, Food Security, Vol. 12, pp. 417-431.

Turner, C. et al. (2018), “Concepts and Critical Perspectives for Food Environment Research: A Global Framework with Implications for Action in Low- and Middle-Income Countries”, Global Food Security, 18:93-11.

UEMOA Commission (2022), “Harmonized Survey on Households Living Standards, Mali 2018-2019”, Ref. MLI_2018_EHCVM_v02_M, Dataset downloaded from www.microdata.worldbank.org on 3 October 2023

UEMOA Commission (2022b), “Harmonized Survey on Households Living Standards, Senegal 2018-2019”, Ref. SEN_2018_EHCVM_v02_M. Dataset downloaded from www.microdata.worldbank.org on 3 October 2023.

Vroegindewey, R. et al. (2021), “Consumer and Retailer Preferences for Local Ingredients in Processed Foods: Evidence from a Stacked Choice Experiment in an African Urban Dairy Market”, Food Policy, Vol. 103/C, p. 102 106.

World Bank. (2023). Africa's Pulse, No. 27, April 2023: Leveraging Resource Wealth During the Low Carbon Transition. The World Bank (update 2024).

Worku, I.H. et al. (2017), “Diet Transformation in Africa: The Case of Ethiopia”, Agricultural Economics, Vol. 48(S1), pp. 73-86.

Zhou, Y. and J. Staatz (2016), “Projected Demand and Supply for Various Foods in West Africa: Implications for Investments and Food Policy”, Food Policy, Vol. 61, pp. 198-212.

Over the past two decades, urban population growth and rising incomes in West Africa have increased demand for diverse, convenient, safer, and nutritious foods, including processed products. The changing food environments—encompassing the physical, economic, and informational contexts influencingconsumer food choices—are expected to significantlyimpact diets and nutrition. This paper evaluatesthecurrentunderstandingofdietandfoodenvironmenttransformations intheregion.Findingsindicateashifttowardsmorenutritiousfoods,aswellasoils, sweets, and fatty products, with dietary changes varying across income groups. Food environments are growing more complex, with numerous outlets offering diverse products, but with inconsistent proximity and affordability. The rapid pace of these changes highlights the lack of detailed data, emphasising the need for better data systems to capture the complexity of food consumption patterns and trendsintheregion.