Bank nationalisation back in the spotlight

SARB Amendment Bill is likely to have implications for investor confidence

By DEBORAH CARMICHAEL & KATLEHO NTAHALE

ENS

The SA Reserve Bank Amendment Bill of 2018 (SARB Amendment Bill) has again become the subject of a vigorous debate following the public hearing held by SA s parliament on July 2 2025.

In essence, the SARB Amendment Bill proposes to nationalise the South African Reserve Bank (the Bank) by: (i) making the state the sole shareholder of the Bank and (ii) empowering the finance minister (minister) to appoint all directors of the Bank.

A central concern is whether nationalising the Bank would undermine its independence. In this regard, SA’s constitution (the constitution) expressly obliges the Bank to perform its functions independently. This constitutional safeguard is not dependent on who owns the Bank. In fact, the shareholders of the Bankdo not influence the policy, regulatory or supervisory decisions of the Bank. It is therefore crucial to clarify what the shareholders are currently able to do.

The South African Reserve Bank Act of 1989 (the SARB Act) limits the shareholders functions to: (i) considering annual financial statements; (ii) electing half of the nonexecutive directors (the board); and (iii) appointing external auditors. If the minister were to assume all these roles, the practical impact on the Bank should, in theory, be minimal.

First, the minister already has access to the annual financial statements of the Bank. Second, the board (regardless of how it is constituted) must already consult the minister when performing its functions. Last, external auditors are, in any case, required to operate independently and in accordance with international standards.

In this regard, it is crucial to also consider the International Monetary Fund s working paper of 2024 (the IMF Paper), which sets out a new measure of Central Bank independence

The IMF Paper challenges the existing view that a central bank’s board is more independent if appointed by private shareholders, noting that this perspective is no longer fully aligned with current views on central bank independence . At the same time, the IMF Paper cautions against a model in which the board is appointed solely by the state. These guidelines seem to support the SARB Amendment Bill in making the state the sole shareholder of the Bank, while opposing the proposal that the board be appointed solely by the minister.

Contentious aspect

The most contentious aspect of the SARB Amendment Bill is probably the proposal to expropriate all Bank shares without compensation to the existing shareholders. Any such expropriation must be assessed in light of the constitution and the Expropriation Act of 2024. The constitution permits expropriation only if it is: (a) for a public purpose or in the public interest; and (b) subject to compensation, the amount of which and the time and manner of payment of which have either been agreed to by those

affected or decided or approved by a court.”

The Expropriation Act generally aligns with the constitution, except in certain cases involving land expropriation for nil compensation. As the SARB Amendment Bill concerns shares rather than land, the prevailing legal framework in SA would

The Bank is one of only nine central banks that still has private shareholders. Most central banks globally are wholly state-owned

require the state to compensate shareholders for their shares.

The SARB no longer publishes its shareholders register online due to the Protection of Personal Information Act of 2013 (Popi), which came into effect in 2021. The last publicly available shareholders register reflected a diverse mix of local and international investors, which included both organisations and individuals. Some of the most notable names in that register were the Nelson Mandela Children’s Fund, the Anton Rupert Trust and the late former finance minister Tito Mboweni.

Following the Popi Act, anyone wishing to inspect the latest shareholders’ register may do so at the Bank’s head office, subject to prior arrangement.

Another key consideration, especially from the public s perspective, is whether the state can afford to acquire all Bank shares. The market value of Bank shares is not publicly available as they are not listed on a stock exchange and are

traded on an over-the-counter market. However, based on the share price data published by the Bank on July 8 2025, it would cost the state about R20m to acquire all shares in the Bank at value. This suggests that affordability, while a factor, is unlikely to prohibit the state from adopting the SARB Amendment Bill.

Investor confidence

Despite constitutional and legislative protections, the SARB Amendment Bill is likely to have implications for investor confidence. Most investors regard the independence of a central bank as the most crucial safeguard against politically motivated monetary policy. However, as most investors ought to know, nationalising the Bank would not be an anomaly. In fact, the Bank is one of only nine central banks that still has private shareholders. Most central banks globally are wholly state-owned and yet maintain operational independence.

It seems that the most crucial question should not be whether the Bank is owned by the state or by private shareholders, but rather, whether its operational independence is maintained. Provided that constitutional protections are upheld, nationalisation of the Bank should not, in itself, compromise the Bank’s ability to perform its functions.

The IMF Paper challenges the existing view that a central bank’s board is more independent if appointed by private shareholders

Litigation vs arbitration: finality, costs and appeals

By PAUL RUSSELL Nortons Inc

Arbitration is a way of resolving a dispute outside of the court system, known as alternative dispute resolution, and involves the parties to a dispute agreeing to enter into arbitration and be bound by the arbitrator s decision.

Mediation, in contrast, involves a process in which a neutral third party, the mediator, facilitates a negotiation between the parties in order to reach a mutually acceptable settlement of their dispute. Mediation is generally less formal than either court litigation or arbitration and does not involve a binding decision.

Here are some key aspects relating to finality, appeals and costs when considering the arbitration route versus litigation.

Finality and appeals

Arbitration proceedings are not subject to appeal (unless an appeal is provided for in the arbitration agreement), but are, in limited instances, subject to review.

Court litigation caters for an appeal process and judgments in the lower courts may be overturned on appeal.

Costs Court litigation costs usually involve the fees for attorneys, advocates, the sheriff and any additional disbursements. However, the parties are not responsible for the payment of the judicial officer, the preparation of the judgment or the venue. The judicial officer has the discretion to grant a costs order against the unsuccessful party. The costs of an arbitration typically involve the arbitrator’s fee, the costs of the legal practitioners, experts, the venue and catering (where applicable). The parties can agree on how the costs of the arbitration proceedings will be apportioned. The arbitrator s fees are usually agreed between the parties and the arbitrator. The Arbitration Act provides that, unless the arbitration agreement provides otherwise, the award of costs shall be in the discretion of the arbitrator.

In summary, there are a number of significant advantages to arbitration, not least of which are that the process is confidential, can be tailored to suit the particular circumstances of the parties and, provided both parties agree, can be much faster and simpler than court litigation. Arbitration can also help those involved deal with matters with less conflict than protracted litigation and so help to preserve business relationships.

As far as costs are concerned, while it is true that, in the case of arbitration, the parties have to pay the arbitrator s fee and for the venue (which are costs they would not be exposed to in the case of litigation), the fact that arbitration is usually considerably faster and more streamlined generally keeps expenses lower. It can be expensive in litigation to have a hearing cancelled at the last minute after the legal teams have fully prepared (with the result that they will need to spend time refreshing in the future when a hearing is rescheduled).

However, as noted at the outset, not all disputes are suited to arbitration and there may be particular features of a dispute which may make it better suited to court litigation.

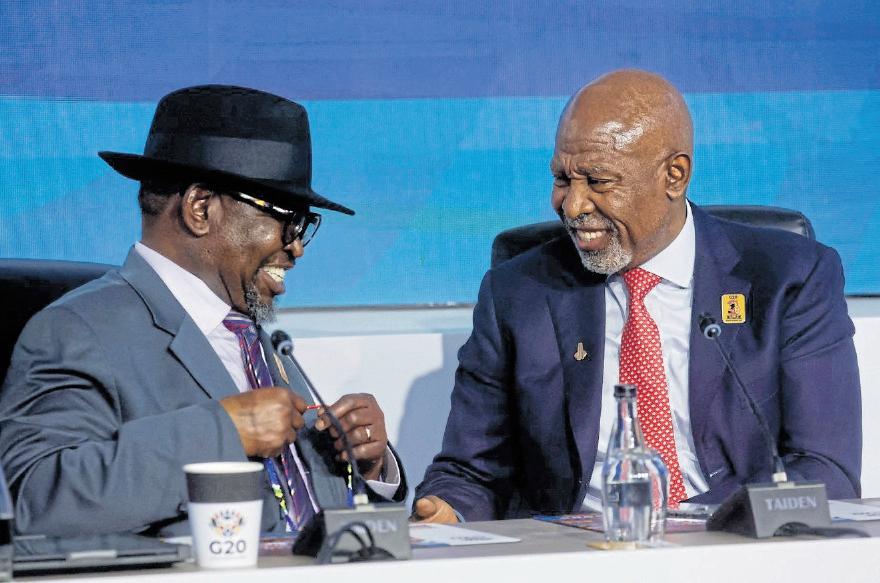

SA finance minister Enoch Godongwana (left) and Reserve Bank Governor Lesetja Kganyago share a moment after the press conference concluding the G20 finance meeting in Durban earlier this month. REUTERS

SA’s Fair Pay Bill may well be a catalyst for change

It

aims to end salary discrimination and promote equal opportunity in the workplace

By NORMA MAZIBUKO & AMANDLA

MAKHONGWANABowmans South Africa

SA may be on the brink of a major shift in how employers handle remuneration matters in recruitment.

The recently introduced Fair Pay Bill (bill) aims to end salary discrimination and promote equal opportunity in the workplace. At its core, the bill seeks to ban employers from asking about a candidate’s previous salary history and requires employers to be upfront about what they are willing to pay for a role.

This is a game-changer for both employers and job seekers and if passed is set to reshape recruitment, pay practices and workplace culture across the country.

How does pay transparency tackle inequality and discrimination? Globally, the practice of asking for salary history has come under scrutiny. The European Union has introduced the Pay Transparency Directive, set to be implemented across member states by June 2026, with the express purpose of standardising pay transparency measures to eradicate causes of pay inequality and close the gender pay gap. Similarly, several US states and cities have enacted laws banning employees from asking candidates about salary history.

The bill is in line with this growing movement towards increased pay transparency. One of the most powerful aspects of the bill is its direct attack on the root causes of wage inequality and workplace discrimination.

While there are good business reasons for seeking pay disclosures in recruitment processes, the impact of this practice is counterintuitive to what the Employment Equity Act, 1998 (EEA) seeks to achieve, and does little to close the gender pay gap. Further, salary history disclosures undermine merit-based pay, as it shifts the focus from the value of the role and the candidate’s qualifications to arbitrary past figures.

Moreover, the bill and the recently proposed pay disclosure provisions of the Companies Act, 2008, as amended, are largely complementary in their aims both seek to promote transparency, accountability and fairness.

● No more asking about salary history. If the bill is passed into law, employers will no longer be permitted to require disclosure of, or even ask candidates about, their current or past pay during recruitment, selection or appointment. The only exception is if an offer has already been made and the candidate themselves requests that their past pay be considered.

● Mandatory pay range disclosure. When advertising a job, and during recruitment, promotion or transfer processes, employers will need to disclose the salary or salary range they expect to pay for the position. This means no more vague market-related offers, as candidates will know upfront what is on the table.

● Open conversations about pay. Employees will have the right to discuss job offers and pay ranges with one another. This is designed to break down

When employees know that pay is determined fairly and transparently, trust in management increases. This can lead to a more positive workplace culture

the secrecy that often surrounds pay and to empower employees to advocate for fair treatment.

● Remuneration transparency. Employers will be required to determine and document pay structures and ranges for each position, making it easier to justify pay decisions and spot any unfair disparities.

For employers, the proposed changes are not only about compliance but also contribute to staying competitive and building a reputation as a fair and attractive place to work. Here is why:

● Attracting top talent. By being transparent about pay, employers can attract candidates who are genuinely interested and qualified, saving time and resources in the hiring process. No more wasted interviews with candidates who walk

away because the offer does not meet their expectations.

● Reducing legal and reputational risk. The days of underpaying employees based on their previous salaries may soon be over. This helps employers avoid claims of unfair labour practices and discrimination, which can be costly and damaging to brand reputation.

● Boosting employee engagement and retention. When employees know that pay is determined fairly and transparently, trust in management increases. This can lead to higher engagement, better retention and a more positive workplace culture.

● Aligning with global best practice. SA is joining a global movement. Irrespective of whether the bill is ultimately enacted, adopting the practices it proposes reflects a proactive approach to fostering an equitable workplace, and signals to employees and stakeholders that the organisation values transparency and nondiscrimination.

To get ahead of the curve, employers can:

● Conduct pay equity audits. Regularly review pay structures to identify unjustified disparities, benchmark salaries across roles, genders and demographics, and document legitimate pay differentiators such as skills, experience and performance. Consider using technology to automate EEA reporting requirements, simulate the impact of pay adjustments and monitor compliance with sector targets.

● Develop a transparent remuneration policy. Set out clear pay structures and grading systems, and objective criteria for salary increases and bonuses. Communicate these policies openly with staff.

● Review and update recruitment policies. Remove any requests for salary history from application forms and interview scripts. Make sure job advertisements include clear pay ranges.

● Train managers and HR teams. Ensure everyone involved in hiring and pay decisions understands the new practices and the reasons behind them.

If passed into law, the bill will be more than merely a legal requirement. It will provide an opportunity for employers to modernise their approaches to pay, attract the best talent and build fairer and more inclusive workplaces.

Case brings ‘who owns data’ into question

By WILMARI STRACHAN ENS

The concept of “data ownership” is complex, with a fundamental legal question remaining unresolved: can data be owned?

A recent Supreme Court of Appeal (SCA) judgment highlighted the critical importance of properly defining and describing data, as well as the return of data upon termination of an agreement. In Inzalo Enterprise Management Systems (Pty) Ltd v Chief Albert Luthuli Municipality ZASCA 85 (June 11 2025), the SCA was faced with a dispute arising from an agreement that regulated the installation and management of designated software and hardware by Inzalo for the municipality. The services included managing the municipality s financial accounting, project management, treasury and cash management, valuation roll management, land use, human resource and payroll management, building control management and revenue management.

Dispute

On termination of the agreement, the municipality requested all data files and documents on the Inzalo EMS Financial System from Inzalo. A dispute arose between the parties, and the municipality brought an urgent application to the high court to obtain its data.

The high court found that Inzalo was not entitled to the municipality s data and nothing in the agreement provided otherwise. It therefore ordered Inzalo to hand back all data files to the municipality.

On appeal, the Supreme Court found that the order granted by the high court did not make any effort to differentiate the types of data to which the municipality and Inzalo may have a claim. The court found that, for instance, some of the data claimed by the municipality, such as “Applications”, “Operating System files and configurations and perhaps all full backups that were run on the FMS system include the intellectual property (IP) of Inzalo.

The court found that the agreement vests no proprietary claim in the municipality to such property. On the contrary, it specifies that Inzalo is the sole proprietor of the IP attaching to data embodied in the designated software. The Supreme Court found that the high court order was “overbroad”

The matter was remitted back to the high court to determine what data, if any, the municipality is entitled to.

Lack of specificity

The appeal court highlighted the relevant agreement was conspicuously silent or ambiguous on the scope of captured data . It did not define precisely what fell within captured data , nor did it specify in any detail how data should be delivered back after the contractual relationship ended. The lack of specificity in the contract gave rise to factual disputes that the appeal court found significant enough to remit the issue back to the high court for oral evidence.

The judgment underscores the fundamental principle that rich detail in data clauses and IP clauses is essential to avoid this sort of conflict. If an agreement is silent or poorly drafted, the supplier may unwittingly commit to hand over assets it never intended to transfer, particularly technology, software configurations and related proprietary materials.

Likewise, the customer may be placed in the vulnerable position of being unsure about whether they can retrieve or continue to use data if the contract is terminated.

Financial regulators bare teeth against Viceroy

Viceroy Research, the controversial short seller, may have met its match as SA regulators bare their teeth. Writing a report high on speculation (while benefiting as share prices plunge) is unlikely to be as easy an opportunity in SA markets anymore, as a fine of R50m may cause some of these researchers to rethink their analysis and tactics before hitting the send button.

Viceroy is, of course, also in the news in international media after taking a short position against Indian miner Vedanta, with global investors struggling to work out which side is up for the share price.

I recall a 2018 incident in SA when Viceroy targeted the property sector, resulting in substantial losses on the stock exchange. I had to advise one of the companies on the hit list at the time, and I must say it is not a fun time to be on the receiving end. Which is not to say these types of research reports do not play an important role in markets when they are based on accurate research, as with Steinhoff. It s a very challenging time for everyone concerned, especially when a company

falls under scrutiny indirectly, as mine did in the property matter, and it can take more than a year to undo the damage in the public eye.

Several companies in the property sector were targeted at the time, and two other adverse analyst reports (neither rated nor mainstream) also targeted the industry. But this was enough to cause panic selling and much consternation. The selling of Resilient’s shares and those of its related companies, including Nepi Rockcastle, Fortress Income Fund and Greenbay Properties, seemed to go on forever.

The speculation, fuelled by rumours and reports, also caused a significant drop in the South African Listed Property Index, with more than R100bn in market capitalisation lost.

Resilient then hired former auditorgeneral Shauket Fakie to conduct an independent investigation into allegations of illicit share dealing. Fakie s report found no evidence of market manipulation” and “no evidence of any insider trading”. It took some time for sanity to prevail, and the matter was only closed after a Financial Sector Conduct Authority (FSCA) investigation, allowing the dust

to settle but it was a rough ride, as it was not until September 2019 that it was finally closed.

In January 2018, Viceroy Research had also just released a report accusing Capitec Bank of being a “wolf in sheep’s clothing” and a “loan shark” with understated loan defaults. This again led to fast losses and the need for damage control. The FSCA has had to step in again to finally settle the matter this time with a hefty penalty.

The Gauteng division of the High Court recently ruled that the FSCA, a juristic person established by section 56 of the Financial Sector Regulation Act 9 of 2017, may impose administrative penalties on foreign residents if notice is delivered electronically and the conduct has a sufficient connection to SA.

Earlier, a majority decision by the Financial Services Tribunal had held that the FSCA lacked jurisdiction over three foreign respondents (partners Perring, Lau and Bernarde) in imposing an administrative penalty of R50m. The penalty stemmed from a 2018 report published by Viceroy Research Partnership LLC which falsely claimed that Capitec Bank was insolvent, causing a 20% drop in its share price and a R25bn loss in market capitalisation. The report caused waves at the time, including allegations of reckless lending practices and potential overvaluation of Capitec’s loan book. The decision will be music to the ears of the financial services sector, notably as Viceroy had gone as far as recommending that the Reserve Bank place Capitec into curatorship, indicating a lack of confidence in Capitec’s financial health and the SA Viceroy had gone as far as recommending the Reserve Bank place Capitec into curatorship

Reserve Bank’s regulatory oversight.

The FSCA found the respondents violated section 81 of the Financial Markets Act by making misleading statements. The tribunal then ruled that while the FSCA had jurisdiction over the conduct, it lacked jurisdiction over the foreign respondents persons, as they were peregrini (foreign residents) and had not been served in SA. The key issue here is that the writers of these reports have taken a short position in the targeted company and benefit as the negative news hits the airwaves and leads to losses. Vedanta’s share price, for instance, suffered close to 10% losses when the report was published (as short positions are heavily geared, this leads to significant profits for those who shorted the stock). Vedanta has since pared some of those losses, but the outcome of that matter remains uncertain. Fortunately, in SA we have more clarity and business certainty after this important ruling. The tribunal’s majority decision was set aside. The matter was referred back to the tribunal for a merits-based reconsideration.

PICKWORTH

123RF DMITRYDEMIDOVICH

PETER BLANCKENBERG COLUMNIST

Right to receive reasons for a judgment

It is generally presumed by the public that when a judgment is handed down in a court of law, the judgment must be accompanied by full reasons for the conclusion reached by the court, including, inter alia, findings on the facts, findings on the law and, finally, the application of the law to the facts.

This would seem to be an exercise of common sense: notwithstanding, judicial decisions do occasionally slip through without proper explanation, particularly when such decisions deal with matters which are not central to a case but nevertheless are a part of the fabric of the case, and relevant to its outcome.

In a recent unanimous Constitutional Court judgment (Prithilal v Akani Egoli (Pty) Ltd & another (CCT290/24) [2025] ZACC 5 (24 April 2025)), the court referred favourably to an earlier constitutional court judgment (Mphahlele v First National Bank of South Africa Limited [1999] ZACC 1). In the Prithilal judgment, the constitutional court reaffirmed that the judiciary was bound by the rule of law, a founding value proclaimed in Section 1 of the constitution.

Section 1 of the constitution provides, inter alia, that: “The Republic of South Africa is one sovereign democratic state founded on the following values: Supremacy of the constitution and the rule of law ...

In Mphahlele (quoted in approval by the constitutional court in Prithilal), the constitutional court held, in respect of Section 1(c), as follows (the paragraphs and numbering are the writer s): The rule of law undoubtedly requires judges not to act arbitrarily and to be accountable.

The manner in which [judges] ordinarily account for their decisions is by furnishing reasons. This serves a number of purposes:

● It explains to the parties, and to the public at large which has an interest in courts being open and transparent, why a case is decided as it is.

● It is a discipline which curbs arbitrary judicial decisions.

● It is essential for the appeal process, enabling the losing party to make an informed decision as to whether or not to appeal or, where necessary, seek leave to appeal.

● It assists the appeal court to decide whether or not the order of the lower court is correct.

● And finally, it provides guidance to the public in respect of similar matters.

Where decisions are made which are considered inappropriate, the body making such decision may be requested to supply detailed written reasons

Although all of the above may appear somewhat obvious in respect of the rule of law and its proper application, it bears repeating whenever possible. All too often, particularly in lower courts (and here I include regional and magistrates courts, and administrative tribunals and other administrative decision making bodies), the above principles are inadequately applied, if at all.

The fact that a dispute or an application for instance, the grant or refusal of a liquor licence or a rezoning application in a town planning matter, or an objection to an environmental authorisation, to give three examples of the many administrative opportunities available to the public does not come before a high court or the Supreme Court of Appeal or the constitutional court, does not necessarily lessen the importance of the outcome of a decision by an official body before which such matter is heard.

Generally, where decisions are made by official bodies (which are not recognised as courts in the ordinary sense), provision is made in the relevant supporting legislation of such bodies for written decisions to be issued by such bodies upon request by the interested parties. It is important the public is aware of this right and that where decisions are made which are considered inappropriate, the body making such decision may be requested to supply appropriately detailed written reasons. In this regard, it should be noted that interested parties frequently are limited by a time period during which such request must be made.

In essence, the rule of law requires a high degree of transparency in the decision-making process of all relevant bodies. It is a constitutional right.

-Peter Blanckenberg is a Director at Blanckenberg & Associates Inc.

Joining forces to deter cross-border crimes

By TENDAI JANGARA & HILARY CHAPFUWA ENS

The African Continental Free Trade Area (AfCFTA) presents a transformative opportunity for enhanced commercial integration among African states.

However, its implementation also prompts scrutiny regarding financial crimes such as fraud, corruption and money laundering. These concerns arise both from increased opportunity and volume of cross-border transactions and from the heightened complexity in regulatory oversight when trade barriers are reduced.

The AfCFTA Agreement does not address financial crime risks. To safeguard the integrity of the AfCFTA framework, it is crucial that member states, financial institutions and all private sector participants adopt robust preventative and enforcement mechanisms to mitigate these risks.

A principal method for addressing these concerns is through the harmonisation of anticorruption and anti-money laundering (AML) standards across jurisdictions. Many African countries have domestic legislation targeting corruption and money laundering, which are often based on international instruments such as the Financial Action Task Force (FATF) Recommendations and the United Nations Convention Against Corruption (UNCAC), and there are African Union (AU) instruments such as the African Union Convention on Preventing and Combating Corruption (AUCPCC). By integrating these established standards into the AfCFTA framework, signatory states can ensure that foundational principles of transparency, due diligence and accountability are embodied throughout interjurisdictional transactions and contractual relationships.

Such harmonisation can be further bolstered through regional collaborations and peer review mechanisms aimed at evaluating compliance and

fostering remedial action where necessary.

It is, however, challenging to harmonise laws across African jurisdictions due to historical, legal, political and socioeconomic factors. African countries inherited different legal systems and, post-independence, continue to protect their autonomy as they collaborate with other countries. The process of harmonising laws requires strong institutions, technical expertise and resources. While there are regional organisations, such as the African Union (AU), the Economic Community of West African States (Ecowas) and the Southern African Development Community (SADC), that promote legal harmonisation, progress is often slow. Differences in member states commitment, legal traditions and political will can adversely affect the adoption and implementation of harmonised laws.

Beyond legislative harmonisation, the efficacy of any anticorruption or AML regime depends heavily on institutional capacity within AfCFTA member states. Governments and regulatory authorities must be able to conduct comprehensive investigations with definitive outcomes, impose sanctions on violators and provide a robust institutional structure for prosecutorial bodies, law enforcement agencies and judiciary.

In addition to this, it is important to have specialised training programmes that enhance the skill sets of investigators, prosecutors and customs officials who will be assigned to address corruption and money laundering matters. This capacity-building is particularly significant in harmonised trade regimes, as the movement of goods and flow of funds can involve multijurisdictional parties and syndicates.

It is also crucial for AfCFTA member states to focus on corporate compliance. Entities operating within or across AfCFTA borders must adopt effective internal policies designed to detect and

prevent fraudulent or corrupt activities. In practice, this means robust “know your customer” (KYC) and transaction analysis processes, thorough third-party due diligence, compliance audits and the consistent training of employees on how to recognise and address potential noncompliance and illegal activity.

Effective whistleblowing procedures, supported by legal protections for the individuals who report wrongdoing, can also serve as a powerful tool for the detection and deterrence of illegal activities.

Another key factor that serves to deter crossborder financial crimes is joint enforcement and information-sharing initiatives among African countries. Bilateral and multilateral agreements on mutual legal assistance and extradition are especially valuable, as they help ensure that individuals or entities engaging in illicit activity cannot opt to operate in jurisdictions with weaker investigative and law enforcement capabilities. Such cooperation can be enhanced by the adoption and use of shared digital platforms designed for real-time information exchange, enabling both governmental bodies and private organisations to identify suspicious or high-risk transactions at an early stage.

In summary, while the AfCFTA holds the promise of boosting economic growth and prosperity across the continent, it will require a focused and multijurisdictional effort by member states to address the potential fraud, corruption and money laundering risks. Success in this regard depends on harmonised legislation, strengthened institutions, corporate compliance, joint enforcement and specialised training.

By embedding these elements within its institutional framework, the AfCFTA can ensure its foundational goals namely economic development, sustainable growth and crossborder collaboration are achieved without being undermined by illegal financial activity.

Protecting confidential information: lessons from the chicken coop

Case underlines how failure to safeguard company IP can hamper business operations

By CRAIG SHAPIROENS

Heat It Manufacturing (Pty) Ltd is a company specialising in high-quality heating systems for the poultry industry. Stavrakis Michaelides was a former employee of the company.

The company relied heavily on detailed technical drawings to produce its heating systems. Michaelides, who had resigned from the company, was accused of taking these drawings with him, leading to a significant dispute.

The conflict began when Michaelides resigned from the company on April 1 2025. Following his departure, the company alleged that Michaelides had taken a USB drive containing essential and sensitive drawings, effectively the blueprints required to manufacture their heating systems. These drawings were not only critical to the operation of the company’s laser cutting machines but also represented a significant competitive advantage in the market.

Upon realising the loss, the company s director, Mr Vorster, contacted Michaelides, who agreed to return the USB. However, the returned device allegedly contained only the original, outdated drawings, not the updated versions developed over the previous year. Further investigation suggested that the updated drawings had been removed from the company s systems and copied onto a USB, rendering the company’s machinery inoperable without extensive reconfiguration.

Michaelides, in his defence, claimed that he had no intention of using or disclosing the applicant s information. He stated that any files in his possession were received in the ordinary course of his duties and that he had deleted all such materials from his devices and messaging platforms after the dispute arose.

The company filed an application requesting the immediate return of the drawings and the USB containing them. Additionally, they sought an order prohibiting Michaelides from using, copying or distributing the drawings in any manner.

The primary legal issues in Heat It Manufacturing (Pty) Ltd v Michaelides revolved around:

● Ownership and confidentiality whether the manufacturing drawings constituted confidential information belonging to the company, and whether Michaelides had unlawfully retained or misused this information.

● Interdictory relief whether the applicant was entitled to an urgent interdict restraining Michaelides from using, copying or distributing the drawings, and compelling the company to destroy any remaining copies.

● Appropriate remedies and costs whether the relief sought was too broad, and how costs should be apportioned given the conduct of both parties.

Court findings

The court held that the drawings were indeed confidential and critical to the applicant’s business operations. It was not seriously contested that the applicant had invested in the development and improvement of these drawings, and that their unauthorised use or disclosure could cause significant harm.

While Michaelides denied ongoing possession of the materials, the court noted that, at the time the application was launched, he still had access

to the files on his personal devices and had only deleted them after being served with the application. The court found that the requirements for an interdict had been met: the company had a clear right to the information, faced irreparable harm without protection, and had no adequate alternative remedy.

However, the court also noted that the relief sought in the notice of motion was overly broad and that both parties bore some responsibility for the escalation of the dispute. The applicant could have sought undertakings from Michaelides before launching urgent proceedings, while Michaelides should have promptly returned or destroyed all confidential materials. As a result, the court ordered each party to bear its own costs.

The final order prohibited Michaelides from using, copying or distributing the company s drawings in any way and required Michaelides to destroy any remaining copies in his possession.

By understanding and implementing these lessons, businesses can better protect their IP and navigate the complexities of legal disputes.

The case serves as a critical reminder of the importance of protecting IP and the legal

Key learnings

Importance of confidentiality agreements. Ensure that all employees sign comprehensive intellectual property (IP) and confidentiality agreements that clearly outline their obligations regarding proprietary information. This can provide a strong legal basis for action if such information is misappropriated.

Immediate legal action. In cases of IP theft or misappropriation, swift legal action is crucial. Delays can exacerbate the impact on business operations and complicate the recovery of stolen information.

Employee exit protocols. Implement thorough exit protocols for departing employees, including the return of all company property and a review of any confidential information they had access to. This can help prevent potential disputes and protect sensitive information.

Legal remedies and enforcement. Be aware of the legal remedies available for IP disputes. Courts can issue orders for the return of stolen information and prohibit its use, providing significant protection for businesses.

Proactive measures. Regularly review and update your IP protection strategies. This includes training employees on the importance of confidentiality and the legal implications of misappropriating proprietary information.

mechanisms available to enforce such protection. For businesses, it highlights the need for robust confidentiality agreements, proactive measures and swift legal action in the face of IP disputes.

What tariff shifts mean for businesses in SA

By BRENDAN ROBINSON PKF SA

In an era of intensifying global trade protectionism, the jury may still be out on the full extent of tariffs facing SA, but the warning signs are flashing.

South African exporters and importers alike must prepare for a world where regulatory costs and complexity are rising and where agility, data and strategic foresight will define who wins and who falls behind.

From evolving US trade policy to domestic tariff reforms, South African companies are finding themselves in the crosshairs of shifts in global commerce. The good news? With the right approach, local industries can mitigate risk and even unlock new competitive advantages.

Now is the time to double down on localisation, build consumer trust and promote SA quality

Tariff risk on the rise: eyes on the US

While a final decision has not yet been made, the US is reviewing SA s eligibility for duty-free access under trade agreements, such as the African Growth and Opportunity Act (Agoa). Political and policy developments could lead to punitive tariffs being imposed on a range of South African exports in the coming months. If implemented, these measures would impact sectors such as steel, aluminium and potentially automotive components all of which depend heavily on global market access.

There are nuances, however.

Industries such as precious metals are not only exempt from proposed tariffs but are also currently benefiting from a surge in global demand and prices. The copper industry is another example despite facing a proposed 50% tariff, strong global copper prices are acting as a buffer, aiding South African producers profitability in the short term.

For others, such as automotive players including Volkswagen SA, the exposure is limited. Their leading export destination is the EU, not the US, highlighting the importance of diversified markets and tailored trade strategies.

Domestic tariff reform: closing the loopholes

Even closer to home, SA is making bold moves to protect its own industries, most notably textiles and apparel.

Until recently, large online retailers such as Temu and Shein took advantage of a 2007 concession that allowed them to pay a flat 20% duty on clothing imports with declared values under R500. These imports were also often misdeclared or undervalued, giving foreign players a tax advantage over local retailers and manufacturers.

In a landmark change, the SA Revenue Service (Sars) has moved to impose a more appropriate 45% import duty in addition to 15% VAT on these products. While full implementation was delayed due to the complexity of systems integration, interim measures are now in place.

A simplified clearance process, aligned with the World Customs Organisation framework, was rolled out earlier this year to enhance compliance and enforcement. This is more than just tax reform it’s industrial strategy in action. By

levelling the playing field, the government aims to support job creation, revitalise local manufacturing and nudge consumers back toward South African-made goods.

The road ahead: how businesses should respond

With both global and domestic tariff regimes in flux, the message to SA companies is clear: stay vigilant, stay agile. Here’s how local businesses can adapt:

● Understand your exposure. Companies must map out their supply chains and export markets to determine where tariff risks exist and how they could escalate.

● Scenario plan around policy changes. From Agoa revisions to domestic tariff shifts, businesses must build flexible strategies that can withstand shocks or seize sudden openings.

● Engage with regulators. Proactive engagement with Sars and customs bodies is essential to ensure compliance, advocate for fair treatment

and stay ahead of rule changes.

● Invest in technology and data. In retail, for example, local players will need to sharpen their e-commerce and pricing strategies as online giants adjust to new import costs. Digitisation and real-time data insights are no longer a luxury, they re a business imperative.

● Reposition for local value. Whether you re a manufacturer, exporter or retailer, now is the time to double down on localisation, build consumer trust and promote SA quality.

Turning challenge into competitive edge Tariffs and trade policy are no longer the domain of policy wonks alone they are now boardroom issues. SA companies must view this evolving landscape not as a threat, but as an opportunity to modernise, innovate and take control of their competitive futures. In a world of shifting rules, it s not just about avoiding penalties it’s about positioning your business for long-term resilience and relevance.

Sadly, appeal court encourages legalese

It is a pity to see the Supreme Court of Appeal encouraging the use of the word shall which is a lawyer s main resort to legalese and obscurity. In a judgment at the end of May 2025, the court, with little qualification, said that the use of the word shall in the language of the contract signified that the requirement of the contract was peremptory and provided no scope for the exercise of a discretion. This is especially unfortunate in an age in which consumers are looking for clear language, and AI is showing how it can be done. The court was interpreting an agreement known as a common terms agreement. Though the judgment does not say so, these agreements stretch to

hundreds of pages. A word search of a common terms agreement will reveal hundreds of examples of the use of the word shall where most of them do not signify a peremptory meaning equivalent to “must”. The word is used as the equivalent of “must”, “will”, may , should , is and more. The internet is full of articles pointing out the ambiguity of the word. Bryan Garner of the US, who is the author of the authoritative Black’s Law Dictionary and has written widely on legal writing, has correctly recommended for years that we should delete all our “shalls” in favour of a more precise word.

Precision is what lawyers should be seeking to achieve. If you look at many standard form loan agreements or lease agreements, for instance, you will find

PATRICK BRACHER COLUMNIST

the word “shall” appearing dozens of times, and seldom more than a quarter of them intend a mandatory term imposing a duty. The so-called boilerplate clauses at the beginning and end of many contracts have been downloaded an inestimable number of times where the word shall is used in all its many possible ambiguous forms. The translators in the EU, where

legislation has to be rendered into 24 languages, have complained for years that a document drafted by an English lawyer leaves them to make up their mind in the translation whether the word “shall” is used by the author in a mandatory or other sense.

Because the word is ambiguous, it is up to anyone drafting a precise document to say what they mean. If they mean “must”, then use the word. The scattering of the word “shall” indiscriminately can create a peremptory obligation for the client which was never wanted by the client. Legalese, like other professional writing, is used for what was once called job reservation. Lawyers are aware of the need to write precisely. But somehow they come out of university thinking that the word

“shall” is part of the necessary jargon that is specific to legal drafting. In this cut-and-paste age, it is easy to perpetuate imprecision in this way. As it happens, the decision of the appeal court referred to is correct in the context as to whether arbitration was compulsory, but the breadth of the court s endorsement of shall is regrettable. The legal profession is under threat from AI which is demonstrating how complex language dealing with far less complex obligations can be boiled down to fewer and finer plain words. Until drafters of legal documents learn to do the same, or learn to use AI to do so, real and artificial intelligence will be in opposition instead of on the same side.

123RF MIKE107

123RF SINENKIY

Company obligations for staff incarceration

Employers cannot dismiss employees without following a fair process and considering all relevant circumstances

By JONATHAN GOLDBERG & JOHN BOTHA Global Business Solutions

When an employee is incarcerated, employers are confronted with a challenging situation that invokes a range of rights and obligations.

The Draft Code of Good Practice on Dismissal provides clear guidance to ensure both procedural and substantive fairness in handling such cases are maintained.

Procedural fairness step-by-step

obligations

Employers must follow a series of procedural steps before considering dismissal because of incarceration. These steps are designed to protect the rights of employees while balancing the operational needs of the business.

● Confirm incarceration. Employers should verify the employee s incarceration status, duration and the reason for their incarceration using official documentation where possible.

● Assess incapacity. It is crucial to determine whether the incapacity is temporary or permanent. Estimate the likely period of absence.

● Communication. Employers must attempt to contact the employee or their representative to inform them of the process and seek their input.

● Allow representation. Employees have the right to be assisted by a trade union representative or a fellow employee in any proceedings.

● Investigate alternatives. All possible alternatives to dismissal such as unpaid leave, temporary replacement or adapting duties must be explored and documented.

● Assess impact. The operational impact of the absence should be evaluated, considering the nature of the job and business needs.

● Consider the employee s circumstances. Factors such as length of service, disciplinary record and personal circumstances must be taken

into account.

● Consistency check. Employers are required to ensure that similar cases have been treated consistently in the past.

● Consultation. If the employee is a union member, the union should be consulted before any decision is made.

● Opportunity to respond. Employees must be given a reasonable opportunity to make representations, either directly or through a representative.

● Document process. Employers should keep detailed records of all steps taken, communication and decisions.

● Decision and notification. Any decision must be based on the above considerations, and the employee must be notified in writing, with reasons provided.

● Right of appeal. Employees should be informed of their right to challenge or appeal the decision via appropriate channels.

Substantive fairness key considerations

Substantive fairness focuses on whether the dismissal is justified in the circumstances.

● Nature and duration of incapacity. Employers must consider if the incarceration is temporary or permanent, and whether the absence is unreasonably long.

● Impact on business operations. The effect of the absence on business operations must be evaluated, including whether the position can be temporarily filled or if the absence creates undue hardship.

TAXING MATTERS

● Possibility of alternatives. Dismissal should only be considered if there are no reasonable alternatives, such as temporary replacement or adapting duties.

● Reason for incarceration. It is important to assess whether the incarceration is related to misconduct affecting the workplace or if it is unrelated to the employee’s work.

● Effect on employment relationship. The employment relationship must be assessed to determine if it has become intolerable or if continued employment is feasible.

● Appropriateness of dismissal. Dismissal is only appropriate if no reasonable alternatives exist and the absence is incompatible with operational needs.

● Nondiscrimination. Decisions must not be based on automatically unfair grounds, such as discrimination or union activities.

Balancing rights and responsibilities

The Draft Code makes clear that employers cannot simply dismiss employees owing to incarceration without following a fair process and considering all relevant circumstances. This approach balances the rights of the employee with the legitimate interests of the employer, thus ensuring that dismissals are both procedurally and substantively fair.

Employers are urged to treat each case on its merits, document their processes thoroughly and always provide employees with the opportunity to respond. This not only protects the rights of employees but also shields employers from potential legal challenges.

Selling your business? How to minimise trouble

By MARCO CLAASSEN AJM

Embarking on the journey of selling your business demands more than mere intention. It requires a strategic approach to ensure the process runs smoothly.

One of the first challenges you will face after deciding to sell your business is, of course, identifying a willing and able buyer. Depending on the nature of the industry and the health of the economy, this can be a notoriously tricky exercise.

Let us assume you have identified a buyer who has expressed genuine interest in your business. What often follows involves lengthy negotiations between the seller and the potential buyer, often involving legal counsels and other advisers. Additionally, the buyer typically demands a due diligence investigation into the target business s financial, legal and other affairs before agreeing to buy it.

Whether or not your business is ready for sale will most likely be disclosed during the due diligence investigation by the buyer and its advisers. Therefore, as the seller, you need to ensure that the items to be covered in the due diligence investigation meet the required standards.

This article outlines the key considerations and steps to help you prepare your business for sale, minimise trouble during the due diligence stage and ensure a smooth transaction. Admittedly, however, the sale of a business is seldom a smooth transaction.

Subject matter of the sale Before delving into specific considerations, which must be in order on the seller’s side, it is prudent to take a moment to consider the identity of the seller and the subject matter of the

transaction. The seller can be a company, a close corporation, a partnership, an individual or a trust.

The subject matter of the sale can be, among others, shares in a company, a member s interest in a close corporation, assets only, or the entire business. Depending on the structure of the sale, the transaction will have distinct legal and tax implications. Each option has its advantages and challenges. For example, an asset sale allows the buyer to avoid inheriting the seller’s liabilities; however, it may require renegotiation of contracts and payment of transfer duty and transfer costs (where fixed property is involved). A share sale, by contrast, is often more straightforward from a contractual perspective but could expose the buyer to unforeseen liabilities, the so-called skeletons in the closet”, as legal practitioners commonly warn. It is essential to carefully consider these factors and consult with tax and legal advisers to determine the most advantageous structure for your unique situation. You may have initially considered selling just the business, but it could turn out that a full company sale (for example, a share sale), which includes the business, is more beneficial for both parties. However, the sale of the business will be the focus in this article.

Key considerations

The initial phase in readying your business for sale entails ensuring the accuracy and completeness of its financial and operational records.

Prospective buyers will want to review correct and up-to-date financial statements, including audited accounts, tax returns and management accounts. These documents should accurately present the business s financial position and performance. This is especially important given that the prospective buyer would want to value the business to get an idea of what a

fair purchase price would be.

Of course, as the seller, you need to present evidence to support the price you desire. It is highly encouraged to engage your accountants to prepare accounts that reflect the state of the business as of the effective date of the sale. Alternatively, the latest set of financial statements can be adjusted for transactions and movements from the date of the statements to the effective date of the sale. A transparent and accurate overview of the financial statements, adeptly prepared by accountants, serves as the cornerstone for effective and fair negotiations, and fostering trust with potential buyers.

Moreover, a comprehensive compilation of all legal and contractual documents related to the business will

As the seller, you need to ensure the items to be covered in the due diligence investigation meet the required standards

avoid unnecessary delays. This includes leases, supplier and customer contracts, employment agreements, intellectual property registrations and any other agreements that may affect the sale. If any of these agreements requires third-party consent for the transfer of rights or obligations, it is essential to address this early in the process. A buyer would be highly disappointed to learn after the sale has been concluded that the supplier may cancel the supply agreement because of the operation of a change-of-control clause, for example.

Addressing liabilities and encumbrances associated with the business is equally pivotal, as it facilitates a seamless transfer of

ownership. Buyers are typically reluctant to assume liabilities unless explicitly agreed upon. Therefore, you should ensure that all liabilities arising before the effective date of the sale are clearly identified and, where possible, resolved. The sale of business agreement must specifically list the liabilities that the purchaser will assume and identify the excluded liabilities, which will remain with the seller. Examples include obligations to employees, creditors and other stakeholders.

If the business assets are subject to encumbrances, arrangements should be made to release these encumbrances before the sale is completed. An example is where immovable property is disposed of as part of the transaction, which is subject to a mortgage bond. The parties will need to engage the mortgagee, cancel the bond and register a new one after the transfer is registered. It’s important to know that a myriad costs are involved when fixed property (whether encumbered or not) is transferred. Be sure to understand the costs and taxes involved beforehand to avoid any surprises.

The strategic allocation of the purchase price to different assets can profoundly impact the seller s tax liability. Therefore, tax planning is another essential component of the sale and acquisition process. For instance, allocating a higher portion of the purchase price to goodwill rather than trading stock may reduce your tax exposure. It is also imperative to consider the tax implications of any capital gains and recoupments of past allowances following the sale. Furthermore, it is wise to be open to the buyer’s structuring suggestions in addition to your own, as they may also face significant tax implications. Consulting your tax and transaction advisers early in the sale process is therefore prudent, as it helps you identify the relevant taxes at play and save where possible, within the bounds

of the law, thereby maximising your after-tax returns upon exit.

During the period between signing the sale agreement and completing the transaction, it is crucial to continue operations as usual (or even better than normal) to maintain the business’s value. Purchasers may require clauses in the agreement that prevent you from taking actions that could deteriorate the business's financial position and operational performance. This includes refraining from entering new contracts, incurring additional liabilities or making significant changes to the workforce without the buyer s consent. Ensuring that the business continues to operate smoothly during this period will help preserve its value and avoid unnecessary disputes. As an additional measure of protection, not only for the buyer but also for the seller, you may include a clause requiring the purchase price to be adjusted for events that occur after the signature date.

Regulatory landscape

Finally, it is crucial to understand the regulatory landscape both prior to and throughout the journey across the legal minefield toward a successful exit. If employees are transferred to the new employer, you must comply with labour laws governing the transfer of employment contracts, such as section 197 of the Labour Relations Act. Additionally, if the sale is not advertised and creditors are not notified, the buyer may be held liable for the seller’s debts under the Insolvency Act. Ensuring compliance with these and other regulatory requirements will help avoid legal complications and protect the interests of both parties.

Selling a business is a complex process that demands strategic foresight and meticulous execution. Engaging your trusted advisers from the outset is essential in navigating the complexities inherent to this multifaceted transaction.

123RF DOGBONE66