Implications and Motivations of Central Bank Digital Currencies on Financial Systems and the Global Economy

BREXIT: AN ECONOMIC FALLOUT

Looking at the economic impacts of BREXIT and what it means for our future

THE EFFECT OF BANK RUNS ON GLOBAL FINANCIAL SYSTEMS

Looking at what Bank Runs are and their effect on Global Financial Systems

MEXICO’S SWEET SOLUTION

Looking at sugar taxes and the issues in Mexico 2014

WHAT’S HAPPENING NEXT

Looking at future events taking place in the college and outside, helping to further your ecnomics knowledge

PG 3

PG 5

PG 9 PG 7

PG 12

PG 15

Photo Taken By Sami Rahman

PRICE DISCRIMINATION:

HAVE YOU EVER WONDERED WHY DIFFERENT PEOPLE GET CHARGED DIFFERING PRICES FOR CONSUMING EXACTLY THE SAME GOOD OR SERVICE? THAT’S PRICE DISCRIMINATION AT WORK.

Whether we pay attention to it or not, this happens in our everyday life. Let's take cinemas for example. As students, we are likely to be charged a higher ticket price than those a few years younger to watch the exact same movie; and often the adult prices are even higher than those of teenagers Additionally, it is much more expensive to travel by tube at certain times of the day, such as during peak hours. A third prominent example is supermarket club cards. Tesco advertises large discounts for users of its Clubcard - because after all ‘every little helps’. But with such significant discounts on targeted items (such as meal deals being over £2 cheaper for Clubcard users than non-users) it leaves us to wonder - is this simply a reward for brand loyalty, or is there a hidden agenda? Why are there discounts on certain items, yet not on all?

Price discrimination means that different customers are charged different prices for the same good, according to demographics or social characteristics such as age, gender, and number of purchases made. Although this may seem as though it was an act of inequality, the main goal of firms is to make increased profit. Firms do not profit from segregation but instead use subtle approaches on how to target certain consumers within the market. It is an act of self-interest, a smart tactic used by firms in order to maximise their revenue (price x quantity) and therefore maximise profits

Price Elasticity of Demand (PED)

The price elasticity of demand is an important calculation that many firms rely on in order to indicate the extent to which they can increase and decrease prices for certain groups. PED is the percentage change in quantity demanded divided by the percentage change in price. The numerical values achieved from this calculation are divided into two key groups: those with elastic and inelastic demand. Groups with an elastic PED (>1) are price sensitive and therefore firms are more likely to keep their prices lower for this certain group in order to increase the quantity demanded by a proportionately larger amount. This will therefore allow firms to maximise their revenue.

However, groups with inelastic demand (<1) are price insensitive which indicates that a change in price will lead to a proportionally lower change in demand. This is why firms are inclined to increase their prices for this certain group in order to increase their revenue and therefore lead to larger profits.

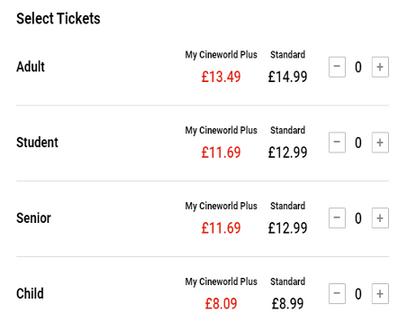

Cinemas

Let's take a certain industry for an example such as cinemas which all have one thing in common; they charge different prices to watch the same movie according to the age of the consumer. An adult is sometimes charged nearly twice as much as a child. The reason for this revolves around each age group's PED, where

Average Cinema Tickets

Taken from a the Cineworld cinema chain with venues across the UK

Figures to Apr 2024

adults tend to have an inelastic PED while children have a more elastic PED.

Degrees of Price Discrimination

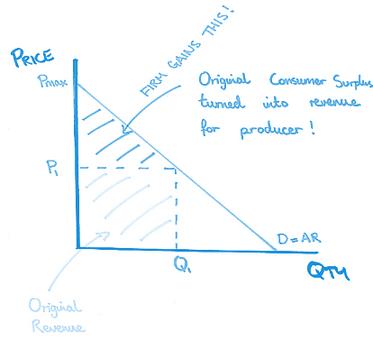

There are three degrees of price discrimination. The first degree of price discrimination - perfect price discrimination - is where consumers are charged the maximum amount that they are prepared to pay for a good. This is how bidding works, in auctions for property or works of art. This degree of discrimination will erode all consumer surplus and turn it into monopoly profits This can be seen on the model (pg 4), where firms will not only gain their original revenue but will also gain the consumer surplus since the firm knows the maximum price (Pmax) that consumers are willing and able to pay for the good.

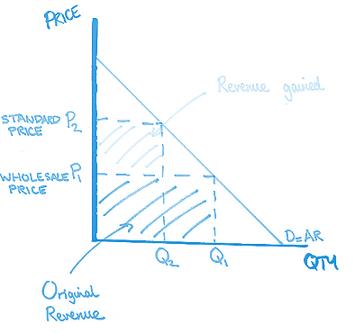

The second degree of price discrimination is used where firms have fixed costs and therefore attempt to leave no capacity idle in order to obtain as much revenue as possible. For example, a hotel, has a certain number of rooms (a fixed capacity) and since these companies have fixed costs it would make sense for them to attempt to fill every last room. This is why we see the prices of hotel rooms fluctuating, where producers may add on last minute deals or discounts to room pricings. This can also apply for products or services that are bought in bulk - the more you buy, the less you pay per unit.

The diagram shows that the firm gains the dark blue shaded area as additional revenue from being able to charge a higher price to those buying smaller quantities. Lastly, the third degree

of discrimination, also the one which is most common amongst producers, is where a company charges different prices to different consumer groups. This is where the cinema example comes into play.

Conclusion

To sum up, price discrimination is an economic tactic that is utilised by firms worldwide to ensure their revenue is at its highest level By being a significant market power move, it simultaneously displays both the significance of marketing as well as the use of PED which helps to make price discrimination a highly impactful method. Many of us, being a part of a consumer-society may dislike this but it would be futile to argue that it is not one of the smartest moves made by firms and businesses. So, the next time you go to scan your club card, tap your Zip card, or buy that extralarge, extra buttery popcorn at the cinemas, because let's be honest what's a movie without a good snack, just keep in mind that each and every one of us is a pawn on a chessboard, buying exactly what they want us to, at the price that gives them the most revenue.

Written by Shreya Kaul

References

https://www.investopedia.com/terms/p/price_discrimination.asp#:~:text=With%20first%2D degree%20discrimination%2C%20the,prices%20for%20different%20consumer%20group s

IMPLICATIONS AND MOTIVATIONS OF CENTRAL BANK DIGITAL CURRENCIES ON FINANCIAL SYSTEMS AND THE GLOBAL ECONOMY

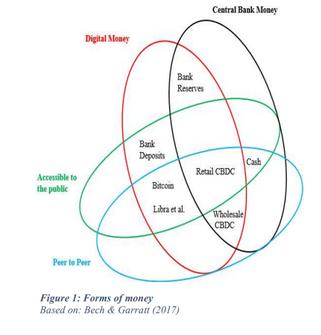

A central bank digital currency (CBDC) is a digital substitute for a nation's traditional currency. The diagram below demonstrates the different forms of money. Unlike cryptocurrencies, like Bitcoin and Ethereum, CBDCs are regulated by a central bank and maintain the same value as broad money.

According to a 2022 survey from the Bank of International Settlements (BIS), 93% of central banks are exploring CBDCs, and 58% report that they are likely or might possibly issue a CBDC in the short to medium term. This clearly indicates the level of high interest on a global scale. Moreover, several central banks are already launching pilot projects in their country.

Why are the Bank of England and other Central Banks considering this?

The main motivation behind the CBDCs could be argued to be anchoring the role of the central bank as the main financial authority, enabling the maintenance of parity between the different forms of money (Pfister, 2019; Villeroy de Galhau, 2023). This would provide a centralised and more stable alternative to cryptocurrencies which should act to increase financial stability and support the digitalisation of assets by enabling seamless transactions in a controlled environment. This should help maintain trust in fiat currency and protect financial systems by adapting to changes in how people pay while striving for increasing efficiency and innovation.

Forms of money

Based on: Bech & Garratt (2017)

Key term: Fiat Currency

A fiat currency is a type of currency that is issued by the government and has value only because people have faith in it.. For example today’s US dollar is a fiat currency, whereas in 1971 it was convertible into gold.

To end, I would like to leave you to make your own judgement on whether a new centralized system of transaction is; firstly worthwhile considering the cost, and secondly, the right step forward in preserving stability and trust in the fiat currency.

1. Implementation of Monetary Policy

Central banks have the primary responsibility for formulating and implementing monetary policy, which involves managing the money supply and interest rates to achieve specific economic objectives including price stability and economic growth

Tools of monetary policy include open market operations (buying and selling government securities), setting interest rates (e g , the policy rate), and managing reserve requirements of banks

Central banks adjust these tools to influence borrowing costs, inflation rates and overall economic activity

2. Banker to the Government

Central banks act as the government’s banker by managing the government’s bank accounts, facilitating payments, and helping with debt issuance and management

They often oversee the issuance and redemption of government bonds and treasury bills, helping the government fund its spending and manage its debt. Central banks also provide advice on fiscal and monetary coordination to ensure overall economic stability

3. Banker to the Banks – Lender of Last Resort

Central banks serve as a lender of last resort to financial institutions, especially during times of financial crises or bank runs

In this role, central banks provide emergency funding to banks facing liquidity problems to prevent systemic financial instability

By offering short-term loans (often referred to as the discount window), central banks help maintain confidence in the banking system

4 Regulation of the Banking Industry

Central banks often play a critical role in supervising and regulating the banking sector to ensure its stability and soundness

They set and enforce prudential regulations, including capital adequacy requirements and risk management standards, to prevent excessive risk-taking by banks

Central banks may also conduct regular bank examinations to assess the financial health and compliance of financial institutions with regulatory standards

Key term: Seigniorage

Seniorage is the difference between the f value of money, such as a £10 note and t cost to produce it (likely to be no more th pennies).

https://www.investopedia.com/terms/c/central-bank-digital-currency-cbdc.asp https://mpra.ub.uni-muenchen.de/111006/1/MPRA paper 111006.pdf

https://www imf org/_/media/Files/Publications/FTN063/2023/English/FTNEA2023010 ashx#:~:text =For%20some%20countries%2C%20enhancing%20monetary,%2Dto%2Dperson%20monetary%2 0transfers.

BREXIT: A PERSONAL VIEW THE ECONOMIC CONSEQUENCE

The economy has changed dramatically after the United Kingdom's exit from the European Union in January 2020. This article will explore the different changes and some of the resulting consequences. The lack of workers, wage growth, and overall effects on the UK economy are the three main Brexit-related assumptions that are examined within this article.

A notable and immediate consequence of Brexit has been a labour shortage, especially in sectors like agriculture, hospitality, and healthcare that were significantly dependant on labour from the EU. The Spectator's data indicates a significant fall in the number of workers available in these sectors following Brexit, suggesting a large number of vacancies now exist that the local labour force has found difficult to fill [Labour market].(https://data.spectator.co.uk/labour-market).

Due to a severe staffing crisis, the hospitality industry—which was heavily dependent on EU workers has had to restrict services and operating hours. Nearly 10% of hospitality jobs remained empty in 2022, a considerable rise from pre-Brexit levels, according to the UK hospitality trade organisation. In addition to having an adverse effect on service quality, the inelastic nature of the price elasticity of supply of labour has led to some enterprises temporarily closing or reducing their hours of operation [Labour market](https://data.spectator.co.uk/labourmarket)

The agricultural industry has experienced a decline in the number of seasonal workers required for crop harvesting, which has affected output and raised operating expenses. According to the National producers' Union (NFU), in 2021, a shortage of pickers caused fruit and vegetable producers to abandon produce valued at £60 million to rot in the fields [Labour market] (https://data.spectator.co.uk/labour-market.) This will have contributed to higher food prices for consumers and lower revenues for farmers.

Wages have been directly impacted by the labour shortage. Labour expenses have increased overall because of employers needing to raise wages in order to draw and keep the best local talent The Spectator's analysis indicates that since Brexit, average pay has increased in the industries most impacted by labour shortages.

To compensate for the workforce shortage, the hotel industry, for instance, has reported salary hikes of up to 10%, which increases the cost of production for these firms. [Workforce market] (https://data.spectator.co.uk/labour-market).

Wages in the logistics and transportation industries have increased because of companies competing for a decreasing pool of skilled drivers, a situation made worse by Brexit. The Road Haulage Association reports that between 2020 and 2022, the average salary for truck drivers rose by 20% The pressing need to close the gap and guarantee the smooth operation of supply chains is reflected in this wage inflation [Labour market](https://data.spectator.co.uk/labourmarket).

Brexit's overall economic effects are unevenly distributed. Positively, higher salaries have raised some workers' standards of living and it may have lessened income disparity in some industries. Furthermore, the need to fill positions has incentivised companies to upskill and train local employees, which could reduce occupational immobility in the UK labour market in the long run as the quality and quantity of labour improve.

Nonetheless, the adverse effects are significant. Inflationary pressures are a result of nominal wage costs reducing aggregate supply and driving costpush inflation as firms pass on increases in their costs.

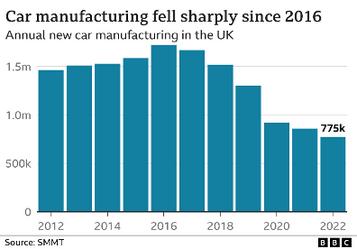

Annual New Car Manufacturing In The UK

BBC News - Business

The Consumer Price Index (CPI) increased by 5.5% in 2021, the biggest increase in almost 30 years, according to The Spectator's economic tracker [Commodities] (https://data.spectator.co.uk/commodities).

This indicates that inflation rates have been rising. Additionally, the decrease in labour availability has limited company operations and growth, especially in industries with intensive labour, by causing

shortages in the workforce needed for production, increasing labour and production costs. This leads to delays in fulfilling orders and scaling up operations. Investor confidence, often referred to as "animal spirits," has been undermined by the uncertainty surrounding trade agreements and regulatory reforms following Brexit As a result, investment in the UK economy has decreased, making it more difficult for firms to conduct business in the post-Brexit environment. Since investment is a key component of aggregate demand (AD), this decline has contributed to a fall in AD. As well as this, statistics from The Spectator's commodities tracker indicate that foreign direct investment (FDI) flows into the UK have decreased, reflecting the cautious attitude of overseas investors [Commodities] (https://data.spectator.co.uk/commodities).

Brexit's impact on supply chains has also had a significant ripple effect. For instance, the paperwork and customs inspections at the crossings have caused major delays and raised expenses for the car industry. Production schedules have been affected, and consumer prices have gone up as a result. According to data from the Society of Motor Manufacturers and Traders (SMMT), the UK's car output decreased by 29% in 2021 compared to pre-Brexit levels, mainly due to these logistical challenges.

The impact of Brexit scenarios paints a complicated picture of the economy. Higher wages because of labour shortages have helped some, but has challenged many enterprises. Brexit looks to have had a more negative overall effect, with significant labour market disruptions and higher operating costs for firms, thus impacting the wider economy

It is critical that politicians address these issues, by isolating labour market inflexibilities, encouraging investment, and assisting the industries most impacted by these changes as the UK continues to adapt to its post-Brexit reality The ability to adjust to the new environment and take advantage of the opportunities presented by this grand shift will determine the UK’s long-term economic sustainability.

Written by Kausic Subaukumar

THE EFFECT OF BANK RUNS ON GLOBAL FINANCIAL SYSTEMS

Bank Runs can have a catastrophic effect on the financial system and the economy as a whole Once one bank fails, it spreads like a contagious disease, causing banks to fail across the financial system. Eventually, banks fail nationwide, causing widespread panic. As the panic sets in, people start cutting spending on goods and services, investment plummets, and markets fall. Aggregate demand takes a nosedive, and the economy heads for a recession. On a whim, the economy could break down at record speed. However, to understand why this could occur, we first need to define what a Bank Run is.

What Is A Bank Run And What Can Cause A Bank Run?

A Bank Run occurs when a large number of depositors try to withdraw their money from a bank simultaneously, as either cash or transfers to another bank, and the institution cannot meet the demand for withdrawals. Put simply, it's when John, who has deposited his £100 into Santander bank, wants to withdraw his money as he believes Santander bank is insolvent. In a real-life scenario, thousands of depositors are all withdrawing at the same time In such a case, a bank can go into bankruptcy. This wouldn’t have a significant impact on the wider economy if the Bank Run remained isolated to one bank. However, this is not the case.

Financial contagion is when liquidity risk is transmitted from one financial institution to another. In this case, it is when the depositors in Lloyds want to withdraw their money due to the depositors in Santander withdrawing their funds. This can happen when there is an economic link between Santander and Lloyds. This means a Bank Run on Santander can cause a Bank Run on Lloyds. In this effect, it is almost like the plague, spreading to other banks in the domestic economy and overseas. A Bank Run has these contagious effects due to the phenomenon known as herd behaviour. This is when people act irrationally and do what others are doing instead of making their own informed decisions In the case of Bank Runs, it is when I withdraw my deposit in Lloyds because Anthony is withdrawing his funds as well. Was my decision based on information I have collected and verified? No, it was just due to Anthony’s actions. This means when Anthony withdraws, Adrian does too, followed by Jean, and then Jean’s friends. A snowball effect occurs leading to the collapse of multiple banks.

What causes a Bank Run?

The run could be initially caused by a lack of consumer confidence in the bank due to a large shareholder of the bank going bankrupt or even a rumour that spreads inciting people to withdraw funds from their bank. A simple rumour could collapse a bank.

Saliently, technology now accelerates a bank run. In the past, people had to physically visit a branch and queue, one by one, to withdraw funds a slow process. Today, an app on a mobile phone allows customers to move funds immediately, and at the same time as thousands, perhaps millions, of others. This means that a bank might collapse before some people are even aware that it is in difficulties.

How a Bank Run Can Turn a Drama into a Crisis

In 1907, the US economy was booming, and everyone believed there was more growth to come. At the same time, F Augustus Heinze and C.W. Morse were attempting to corner the stocks of United Copper. They planned to do this by buying a majority of the United Copper shares, and then selling those shares at exorbitant prices to those who shorted the stock. However, they made a grave miscalculation in their trade, and ultimately their decision ended up causing Bank Runs on two brokerage banks associated with Heinze and Morse as they used the United Copper shares they bought as a security for loans

Bank Runs started on both of their banks, ultimately lead to the collapse of both banks. Even though their banks were relatively small, the Bank Runs spread to other banks tied to Morse and Heinze. This snowballed into Bank Runs on the third largest trust in New York, and a nearly 50% fall in the stock market. The economy was now headed towards a recession at record speed. The economy was saved due to JP Morgan (among other financiers) who used $20,000,000 (~$700,000,000 in today’s currency) of his private capital to bail out banks that were going bankrupt. The Bank Runs on two relatively obscure banks nearly triggered one of the worst recessions America would have ever experienced.

What Has Been Done To Mitigate The Risks Of Bank Runs?

In response to the American economy nearly collapsing several times due to Bank Runs, the US Congress established the FDIC to insure bank deposits. This means that the bank has to keep a certain amount of their deposits in their liquid reserves. For example, if the reserve rate was 20%, and Joe wants to deposit $100 in the bank, then the bank must keep $20 in the liquid reserves, and they can loan out the $80 This means that banks have greater liquidity in times of high withdrawals.

In addition, the establishment of the Federal Reserve System in the US and the Bank of England in the UK means that in times of very low liquidity in banks, they can bail them out by lending them cash. This is why the central bank is known as the lender of last resort.

The government also provides deposit insurance. In the UK, the Financial Services Compensation Scheme (FSCS) will compensate you with up to £85,000 if the bank fails meaning you won’t lose all of your money This provides confidence to the consumers and keeps the financial system from imploding.

Conclusion

In reality, Bank Runs can occur any day of the week. A slight shift in consumer confidence is all you need to trigger a bank run. You could say many things have been done to mitigate this risk and ensure that this won’t happen again. Ultimately, enough has not been done, as proven time after time, and it seems that the whole financial system is just a house of cards waiting for the next gust of wind to tear itself apart.

Written by Kishon Kathirgamanathan

Ideas for further reading

Northern Rock was a UK-based mortgage lender based in Newcastle upon Tyne that experienced the first bank run in the UK since the nineteenth century. The bank was nationalised by the UK government in 2008, after experiencing a run by savers on their deposits that led to more than £3 billion being withdrawn in 48 hours.

Northern Rock had become heavily reliant on shortterm wholesale funding to finance its ambitious and fast-growth mortgage lending, and when the global credit markets froze in the credit crunch of the summer of 2007, it was unable to refinance its short-term debt, causing severe liquidity problems.

The government intervened by guaranteeing all deposits, providing a loan facility to Northern Rock, and later nationalising the bank. The bank was split into two parts: the "good bank" was sold to Virgin Money in 2012 and the "bad bank" was retained by the government to manage the remaining assets and liabilities.

Brown, M., Trautmann, S. T., & Vlah, R. (2021). Understanding Bank-Run Contagion Mooman, M. (2021). Understanding Bank Run, Consequences for Economy Behavioural Economics. (2021). Herd Behaviour Gotham Center. (2021). The Panic of 1907: How JP Morgan Took Over Wall Street Federal Reserve History. (2021). The Panic of 1907

MEXICO’S SWEET SOLUTION: HOW A SUGAR TAX TRANSFORMED PUBLIC HEALTH

a sugar tax on sugar-sweetened beverages. This government intervention aimed to combat the nation’s alarming rates of obesity and high prevalence of diabetes With Mexico being the number one consumer of sugary drinks globally, the tax imposed sought to reduce the consumption of sugar and so encourage healthier dietary choices amongst society. It also sought to fix one of Mexico’s largest problems, a workforce experiencing a large decline in productivity as obesity reached 70% of adults and 30% of children.

In 2012 the workforce was declining, and Mexico had to pour millions of pesos into its healthcare system to try and address this problem. With 6.2% of GDP alone having to be contributed to healthcare in 2013 it showed just how dire of a situation Mexico was in, and how public health needed a large reformation.

Before this tax was imposed, sugary drinks were, surprisingly, often cheaper than bottled water in Mexico. Major beverage companies implemented strategies such as intensive marketing and promotional campaigns, making their products highly attractive and accessible. On top of this, many sugary drinks were produced and distributed in larger quantities than bottled water. Due to this alarming uptake in sugary drinks, firms were seeing a much greater profit, and this allowed them to subsequently lower cost per unit as production increased.

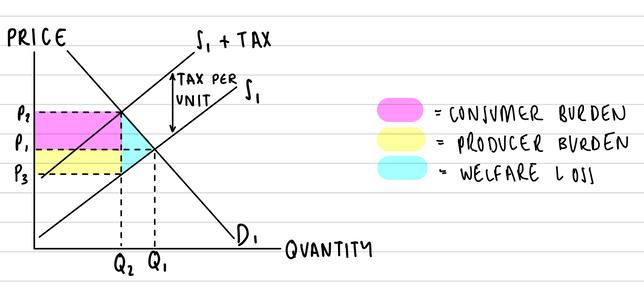

In 2014, Mexico took a significant step towards improving public health policy by implementing With potential for problems to exacerbate even further, Mexico elected to implement an indirect tax sooner rather than later, to avoid a widespread health/economic/moral good of the world epidemic. So in 2014, an indirect tax (a tax on consumption, directly increasing the price of fizzy drinks) affecting all drinks, from flavoured waters and teas to energy drinks. The imposition of this tax, set at one peso per litre, led to a 10% price increase in taxed beverages, and consequently led to a reduction in consumption of taxed sugary drinks by around 7.6% during 2014 and 2015.

The sugar tax imposition will increase the cost of production for drinks manufacturers. Due to a reduced profit incentive, some firms might choose to leave the market. Thus, the number of sellers falls, causing supply to shift inwards and leftwards from S1 to S1+TAX. This suggests that as the price of sugar-sweetened beverages increases from P1 to P2, quantity demanded will fall substantially, from Q1 to Q2. As a result, the sugar tax would ideally reduce consumption of these unhealthy drinks whilst simultaneously increasing demand for healthy substitutes, as the price elasticity of demand should be elastic. This has the positive effect of improving the health of the population, so, over time, less money need be spent on healthcare as fewer people suffer from obesity related diseases such as coronary heart disease. This reduces/minimises any opportunity cost, the best alternative option forgone, as the money being spent treating obesityrelated illnesses is “freed up” to spend on other public services, once demand for sugary drinks declines/the need to treat obesity-related illnesses falls .

However, with such large reductions in quantity demanded, consumers had to look at available alternatives, aside from sugar-sweetened beverages, substitutes mainly included water and natural juices which are typically more expensive and less desirable to consumers, so wouldn’t act as such a simple substitute

With potential for problems to exacerbate, an indirect tax had to be implemented sooner rather than later, to avoid a widespread health/economic/moral good of the world epidemic So in 2014,

However, it is assumed that a large increase in price leads to a reduction in quantity demand, as consumers look for alternatives. Substitutes include water and natural juices. However, these may not be close substitutes because they are more expensive and less desirable to consumers. Furthermore, consumers are irrational and so, due to their habitual behaviour and Mexico’s particular reliance on sugary drinks (formerly being the number one consumer of sugary

drinks before 2014), people may still continue to buy unhealthy drinks. This demanded further action Drinks firms were co-opted into reformulating their drinks recipes and reducing their sugar content. This helped play a crucial part in transforming public health. This meant that they could continue to sell their drinks at a similar price to before the tax, but with a combination of a reduced sugar content and smaller quantity in each bottle allowed public health to improve.

In many other economies sugary drinks tend to be price elastic, however, this wasn’t the case for Mexico. Price elasticity of demand is the responsiveness of quantity demand relative to a change in price. With their negative PED, the sugary drinks follow the idea that a small change in price will lead to a large change in quantity demanded. This is due to the usual large number of substitutes for fizzy drinks such as Pepsi being an alternative for Coca-Cola, providing a similar utility, satisfaction gained from the consumption of a good or service.

The Mexican sugar tax served as a pioneering model for global health policy due to its significant impact on public health. With its success, it led to countries including the United Kingdom and France, both introducing their own versions of sugar taxes. Research showed a 7.6% reduction in the first year, followed by an 8% decrease again in the following year. Mexico’s success in avoiding an epidemic inspired similar initiatives across the globe, paving the way for other LatinAmerican countries to adopt similar measures like their own sugar taxes.

Written by Erin Williams

What’shappening?

UPCOMING TALKS & LECTURES

Degree Apprenticeships With Vishmi Sapukotanage:

- Wednesday, 26 June 2024 at 1.30pm

Vishmi, a former St Doms student, is currently undertaking a degree apprenticeship with the Bank of England

Her talk will last for about for about one hour, and explore her career/degree choices and experiences

Vishmi will look at why she chose the apprenticeship route, rather than undertake the more traditional university degree course

Vishmi will also discuss how she is finding her degree studies, particularly balancing them with working full-time

Economics Debate - “Should the government increase taxes on wealthier individuals to reduce income inequality”

- Tuesday, 2 July 2024 3:15pm

A chance to test your public speaking skills in front of fellow peers Showcase your skills, share your thoughts, and connect with peers in a supportive setting

What went wrong with capitalism?

- Wednesday, 3 July 2024 6.30pm to 8.00pm

- Hosted by the London School of Economics and. ------Political Science

A talk to be delivered by Ruchir Sharma, Chairman of Rockefeller International and Founder and Chief Investment Officer of Breakout Capital, an investment firm focused on emerging markets

The LSE’s website states “The now widely accepted narrative is that four decades of downsizing government - cutting taxes, spending, and regulations - left the financial markets free to run wild, fuelling inequality, slowing growth - and alienating much of the population. Sharma exposes the story of shrinking government as a myth...”

Learn more about the talk at the LSE’s Public Events web page

St Dominics UCAS Event

- Friday, 5 July 2024 Throughout The School Day

A chance to talk to professionals and advisors on the next steps after A-Levels with lots of visitors coming to speak to students about the university admissions process as well as other options that are available.

IF YOU WOULD LIKE TO CONTRIBUTE AN ARTICLE TO A SUBSEQUENT EDITION OF THIS MAGAZINE, PLEASE FEEL FREE TO SUGGEST YOUR IDEA AT A FORTHCOMING PLANNING MEETING.