Why Swiss Banks Fall Short in Portfolio Management

A Timely Look At The History of UK Pension Changes

10 Ways Expats Can Maximise Their Skywards Points

Why Swiss Banks Fall Short in Portfolio Management

A Timely Look At The History of UK Pension Changes

10 Ways Expats Can Maximise Their Skywards Points

Imagine a world where your investments deliver a consistent return, year after year. Argen Capital offers exactly that – a remarkable opportunity to earn an 8% fixed return per annum, designed for those who seek stability and security.

Our innovative approach, developed by Skybound Capital, provides you with the peace of mind that comes with a steady income stream, while also allowing you to take control of your financial future.

Discover how Argen Capital can work for you. Contact us today to learn more about this exclusive investment opportunity and take the first step towards securing your financial future.

Chief Executive Officer

Josh Burton

Chief Financial Officer Mike Coady

Husain Rangwalla

Chief Technology Officer

Peter Gollogly

Regional Director - Europe

Tom Pewtress

Group Head of Proposition

Carlo Casaleggio

Group Head of Compliance

Veronica O’Brien

Group Head of Corporate Affairs

Carla Smart

Group Head of Pensions

Jonathan Lumb

Regional Manager - UAE

Skybound Wealth Management stands as a beacon of excellence in the world of international wealth management. As an independent firm, we pride ourselves on delivering bespoke financial solutions tailored to meet the unique needs of our global clientele. Our innovative approach combines the agility of a boutique firm with the expertise and resources typically associated with a major financial institution.

of client assets under management £1 billion

international clients & growing 5,000 +

Richard Gartland

Regional Manager - Cyprus Ryan Donaldson Regional Manager - Europe

Bryan Bann

Regional Manager - Switzerland

As we step into the final quarter of 2024, it’s clear that this year has been one of significant shifts and opportunities in the global financial landscape. From interest rate movements to geopolitical tensions, markets have remained as dynamic as ever. For expats, it’s more crucial than ever to stay informed, make sound decisions, and be ready to act, especially as we approach the first Budget under the new Labour government in the UK.

At Skybound Wealth, we’ve experienced remarkable growth this year, expanding both our global reach and our capabilities. Our client acquisition has grown by over 38%, while assets under management have surged by 41%—a clear testament to the trust our clients place in us and the expertise of our advisory teams.

We’ve also continued to invest in our technology and digital solutions, ensuring that wherever you are in the world, you can count on our support no matter where your expat journey takes you.

This inaugural edition of Soar, our newly revamped newsletter, reflects all the exciting developments happening across Skybound Wealth. It not only delivers key insights tailored to the global expat community, but also showcases the incredible work that’s been going on behind the scenes, from our enhanced digital solutions to our expanding global presence.

We’re excited to announce the opening of our new office in Cyprus, further enhancing our services across Europe. You’ll also find a timely look at the history of UK pension changes, especially relevant as we approach the Budget, which could have significant implications for expats. We cover important topics like the necessity of keyman insurance for business owners and delve into the crucial importance of having a valid will in the UAE. We also offer some practical tips for expats living in Switzerland, ensuring you’re well-equipped to negotiate the local financial landscape.

As always, our goal remains simple: to help you stay ahead of the curve and ensure your financial future is secure. Thank you for being part of the Skybound Wealth family, and I hope you enjoy this edition.

Mike Coady

Mike Coady Chief Executive Officer

Mike Coady Talks Strategic Asset Allocation for Expats

Announcing New Office in Cyprus to Enhance Our European Services

This location allows us to better serve our European clients with localized expertise and comprehensive financial solutions.

Pilots, Autopilots & Advisers: The Future of Wealth Management 10.

Husain Rangwalla, Chief Technology Officer talks about how we at Skybound Wealth Management see the role of technology in wealth management.

Mike Coady Talks Strategic Asset Allocation for Expats

Following a thought-provoking piece from Skybound Capital, Coady shares expert advice on asset allocation strategies to help you grow and protect your wealth.

Exploring Property Investment: Leverage, Risks, and Strategy 10 Ways Expats Can Maximise Their Skywards Points

Tune in to this insightful episode as Simon Athwal and Tom Pewtress on share their expertise on making the most of property as an investment.

Managing Associate, Thomas Sleep draws on his personal expat experiences to help your finances benefit from the Emirates Skywards Reward Programme

The latest Q3 report from our investment team reviews market trends over the past three months and offers key insights and outlook for Q4.

Skybound Wealth’s Taylor Condon discusses why Swiss Banks fall short when compared to bespoke services in portfolio management.

Carla Smart, Group Head of Pensions at Skybound Wealth takes a look back at the many changes to the UK pension system since 1980.

Should You Run Your Personal

Josh Burton of Skybound Wealth Management explains how expats and business owners can benefit from treating personal finances like a business.

In this spotlight feature, we take a closer look at the career of senior adviser Ryan Donaldson, highlighting his key achievements and contributions over the years.

Christopher Bowler, Financial Adviser at Skybound Wealth covers what you need to know when investing your retirement accounts as a South African Expat.

Bryan Bann, Regional Manager - Europe at Skybound Wealth Management reveals his 10 Essential Financial Tips for Expats in Switzerland

Ben Stockton, Financial Adviser at Skybound Wealth highlights the importance of Keyman Insurance and other essential protections for expat business owners.

Max Gerstein, a financial adviser in the UAE explains the key reasons why having a Will is so crucial for expats living in the Middle East region.

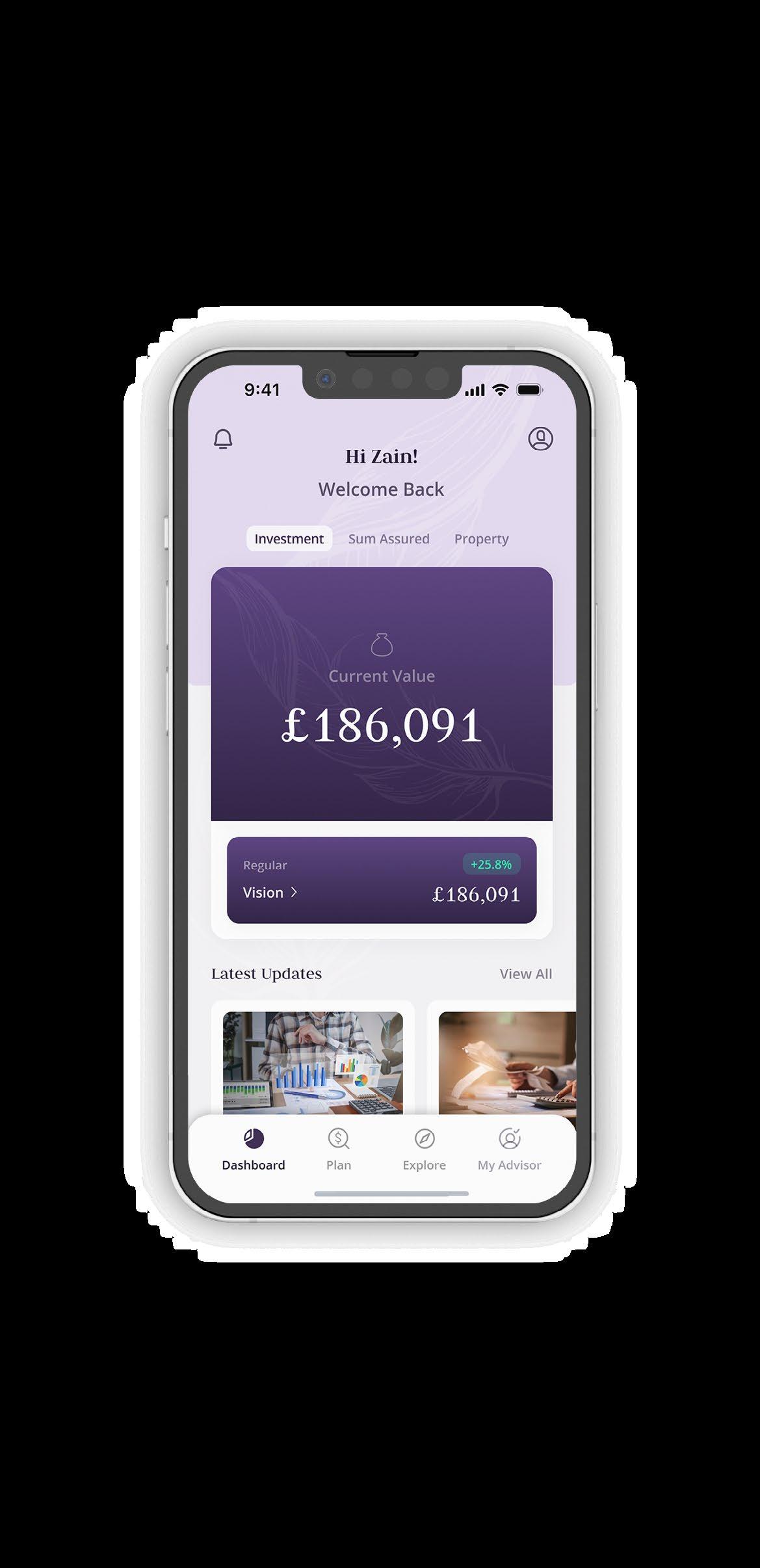

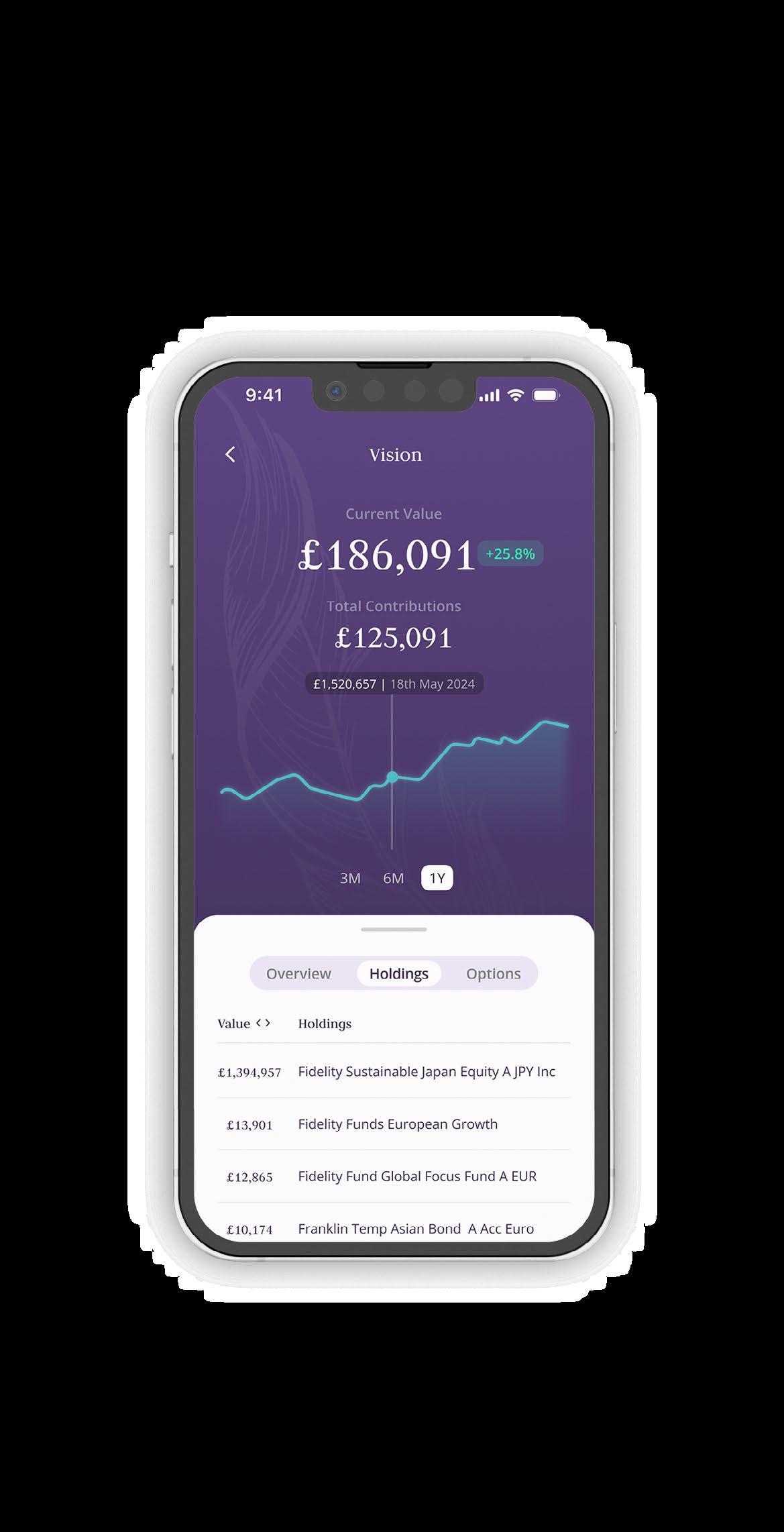

Download the exclusive Skybound Wealth App to help you stay in touch with your Advisor and access your policy information round the clock.

Scan the QR code code or click here to download the app.

Written by Mike Coady

Skybound Wealth Management is thrilled to announce the expansion of our global presence with the opening of a new office in Nicosia, Cyprus. This strategic move highlights our dedication to providing top-tier financial advisory services throughout Europe.

The Cyprus offices is operational and holds regulatory approval from the Cyprus Securities and Exchange Commission (CYSEC), and the Insurance Companies Control Service (ICCS). These licenses enable us to provide a full range of financial wealth and insurance services tailored to the needs of our European based clients.

Skybound Wealth Europe Ltd and Skybound Insurance Brokers Ltd offices are led by five distinguished EU based directors. For Skybound Wealth Europe these are Christos Christou, Petros Hadjipetrou, Andreas Themistokleous, Andreas Savva and for Skybound Insurance Brokers this is Andreas Charalambides. Additionally, Evie Kyprianou heads our compliance operations, ensuring that we maintain the highest standards of regulatory compliance and client satisfaction.

Enhancing Our European Footprint

Peter Gollogly, Regional Director for Europe, stated,

“With these new offices, Skybound Wealth Management strengthens its ability to provide comprehensive, regulated financial advice to clients across Europe to the benefit of our expat-based clients in the likes of Spain, Portugal, France and Belgium etc.

Our expansion into Cyprus allows us to navigate the post-Brexit landscape more effectively, ensuring seamless service continuity for our international clients.

Mike Coady, Chief Executive Officer, added,

“Opening offices in Cyprus was a strategic decision aimed at expanding our footprint in Europe. This location allows us to better serve our European clients with localized expertise and comprehensive financial solutions. We are excited about the opportunities this brings and remain committed to providing top-tier financial advisory services.”

Written by Husain Rangwalla

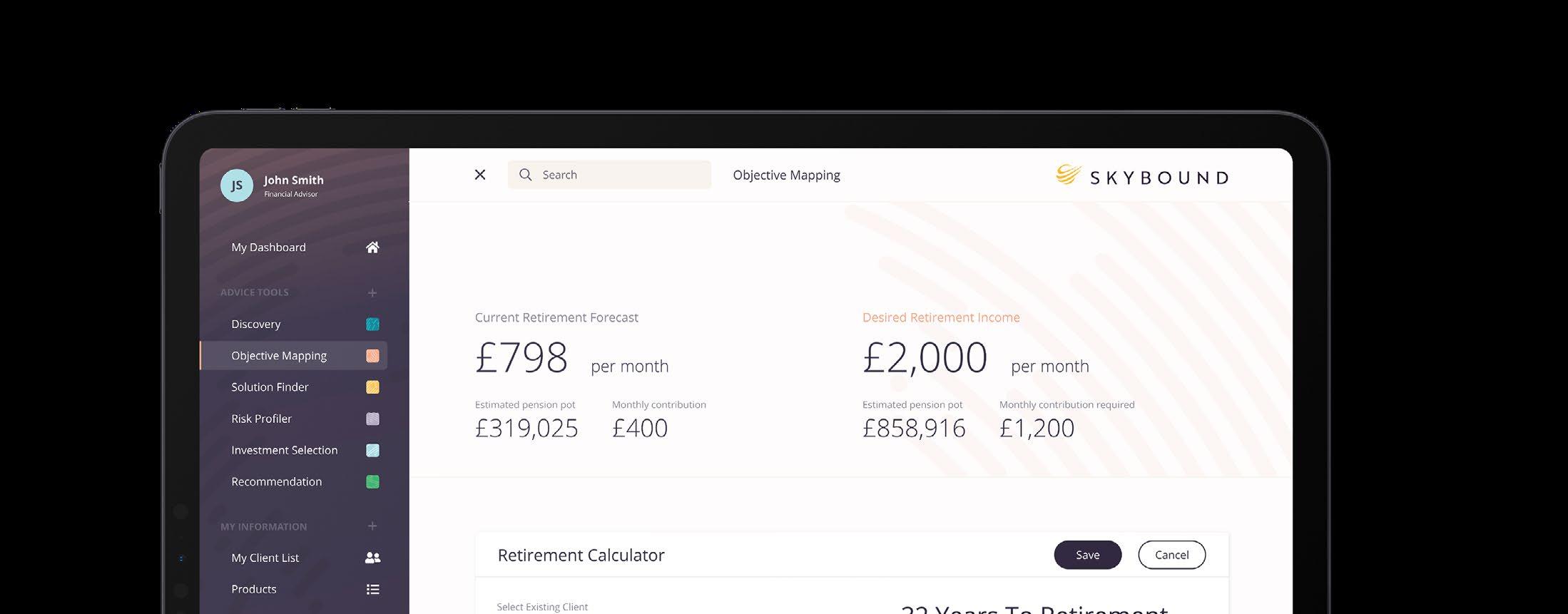

Picture this: You’re flying at 35,000 feet. The autopilot is engaged, guiding the plane steadily, adjusting for turbulence, and processing data in real-time. But while the autopilot ensures smooth sailing, it’s the human pilot’s intuition, judgment, and experience that are indispensable when the unexpected arises. This is how we at Skybound Wealth Management see the role of technology in wealth management. Our proprietary Plume WealthTech serves as the autopilot—handling data, automating routine tasks, and ensuring everything runs smoothly—while our advisers remain at the helm, applying their personal insight to help guide each client through their individual financial journey.

It’s natural to wonder, Can technology really enhance the role of the adviser? The answer lies in what the technology is designed to do. Plume Wealth Tech doesn’t replace advisers—it empowers them. Through tools like automated compliance, realtime data access, and intuitive financial planning software, advisers can focus less on administrative tasks and more on understanding their clients’ unique needs.

For instance, the Plume Client Manager, powered by Salesforce, automates KYC checks and compliance workflows. This streamlining allows advisers to spend more time deepening relationships and delivering highly personalised advice. The tech handles the routine; the adviser brings the human touch.

Amplifying Expertise: Skybound Wealth advisers are highly qualified, and skilled professionals.

Plume Wealth Tech amplifies this expertise by giving them real-time access to client data and advanced insights. Whether it’s analyzing detailed financial histories or accessing real-time market movements, advisers can make informed decisions quicker, and with greater precision.

Behavior-Driven Insights: Our technology doesn’t just react to data; it learns from it. Through behavioural analytics integrated with tools like Microsoft Viva and Azure Analytics, we capture client behaviors and preferences, enabling advisers to adapt their strategies in real-time. This ensures financial plans are not static, rather they evolve as clients’ circumstances do, driven by personalised data.

Purpose-Driven Efficiency: We have moved beyond traditional efficiency claims. By integrating Plume WealthTech with data from multiple channels, our advisers can anticipate client needs, and act accordingly. This allows us to replace unnecessary meetings and generic advice with purposeful client engagement filled with relevant insights and informed advice.

The impact of Plume WealthTech isn’t measured by abstract gains—it’s tangible, and proven in the numbers:

• Time Saved: Our advisers report saving up to 30% of their time on routine tasks, like compliance and onboarding, thanks to automation within the Client Manager.

• Enhanced Engagement: As a result, advisers now engage with clients 20% more frequently, and can focus more on strategic planning rather than routine administrative work.

• Document Handling Efficiency: The time required to prepare and deliver client reports has been cut in half, with secure document vaults ensuring both speed and data protection. These results demonstrate that our approach is not just tech for tech’s sake but a real, measurable improvement in the way our advisers work.

We’re not chasing trends like “ChatGPT integration” for the sake of sounding cutting-edge. Instead, we’re focused on leveraging the wealth of data collected over our four-year track record with Plume Wealth Tech. We’re refining our tools to drive greater efficiency and accuracy, using our proprietary data to ensure that future developments are built on real, client-driven insights.

The next phase of our platform will integrate AI and NLP, not as flashy add-ons, but as finely-tuned enhancements that analyze behavior, predict needs, and help our advisers deliver even more tailored, proactive service.

Whether you’re interested in refining your financial strategy with the latest insights or learning about upcoming features that can enhance your experience, we’re here to guide you. For advisers considering joining us, or clients looking to explore the full potential of our wealth management solutions, now is the perfect time to connect and discuss how we can continue to grow together.

Written by Mike Coady

As an expat, building a solid financial plan goes beyond setting aside money each month. With inflation, fluctuating interest rates, and the complexities of different tax regimes, financial planning becomes a critical task—especially for those living abroad. In this context, understanding strategic asset allocation is key to maximizing long-term financial success.

Skybound Capital, the global asset management company, has recently published a thoughtprovoking piece authored by Karl Engelhard, CFA, and Alexander Engelhard, CFA, exploring how current macroeconomic trends, particularly inflation and interest rates, are impacting asset allocation. Drawing on these insights, alongside my own extensive experience in expat financial planning through Skybound Wealth Management, I aim to dive deeper into how these factors shape the financial future of expats and what steps can be taken to stay ahead.

Historically, financial markets have been driven by two major forces: inflation and economic growth. When inflation is the dominant factor, equities and bonds—typically the foundation of most investment portfolios—tend to move in the same direction, reducing their diversification benefits. As noted by Skybound Capital, in the 1970s, high inflation led to poor performance in both asset classes, with only commodities offering a hedge.

Fast forward to today: inflation has once again at the forefront of market concerns. The pandemic-driven fiscal stimulus packages injected by governments have contributed to a rise in inflation, and global supply chains disruptions also worsened this issue. As a result, many central banks, including the US Federal Reserve and the European Central Bank shifted to a more aggressive stance on interest rates. For expats who often deal with multi-currency exposure, rising interest rates in one region can drastically impact the value of your savings and investments held in another.

For expats, this becomes particularly important when managing investments across jurisdictions. A robust asset allocation strategy that accounts for inflation and currency exposure is crucial for mitigating risks and maximizing long-term growth. At Skybound Wealth Management, we frequently advise our clients on diversifying across asset classes and geographies to help cushion the blow from inflationary pressures.

“With inflation, fluctuating interest rates, and the complexities of different tax regimes, financial planning becomes a critical task...”

One of the most significant changes in the financial environment is the end of the “easy money” era.

As Skybound Capital emphasizes, the near-zero interest rates that dominated the post-2008 period incentivised investors to take on riskier assets in search of yield. With interest rates back above 0% for the first time in over a decade, cash is no longer yielding nothing.

For expats, this is a game-changer. Traditional investment strategies that once emphasised riskier assets such as high-growth equities and longduration bonds may no longer be as attractive. With higher interest rates, bonds and cash now offer more competitive returns. As an expat, this creates a valuable opportunity to reassess your asset allocation strategy. For example, cash or shorter-duration bonds can now play a larger role in portfolios without the same penalty they once carried during the low-interest era.

At Skybound Wealth, we are leveraging Skybound Capital’s institutional expertise to reassess portfolio compositions for our clients. By integrating their insights on global market shifts, we ensure that expats are taking advantage of the current environment while maintaining a long-term vision for wealth preservation and growth.

One of the most fascinating aspects of Skybound Capital’s research is the emphasis on deglobalization as a key factor influencing asset allocation. Deglobalization refers to the reversal of trends that have seen economies becoming more interconnected over the past few decades. With geopolitical tensions rising and many countries looking inward to secure supply chains, we’re witnessing a shift toward regional self-reliance. For expats, this creates both opportunities and risks. On the one hand, deglobalization can lead to inflationary pressures as countries invest in more expensive domestic solutions. On the other hand, it opens up new avenues for region-specific investments, especially in sectors like green energy and technology, where governments are pouring funds into innovation.

For those living and working abroad, understanding how these geopolitical factors affect different regions is critical. At Skybound Wealth Management, we work closely with Skybound Capital’s global team to ensure our clients are positioned to take advantage of regional opportunities while mitigating risks tied to deglobalization. Whether it’s adjusting portfolios to capture growth in emerging markets or restructuring assets to hedge against inflationary pressures in specific regions, strategic asset allocation plays a vital role in securing a prosperous financial future.

The key takeaway from Skybound Capital’s research is clear: today’s financial environment is more complex and interconnected than ever. For expats, this complexity requires a tailored approach to asset allocation, one that considers not just the typical factors like risk tolerance and time horizon but also the macroeconomic drivers such as inflation, interest rates, and regional trends.

At Skybound Wealth, our partnership with Skybound Capital allows us to deliver that expertise to our expat clients. By working together, we bring institutional knowledge to the individual investor, helping expats deal with the complexities of managing wealth across borders.

“As an expat, this creates a valuable opportunity to reassess your asset allocation strategy.”

As expats, we face unique challenges in managing our wealth. From dealing with multiple currencies and tax regimes to understanding how global economic trends affect our portfolios, the complexities can often feel overwhelming. However, with the right advice and a strategic approach to asset allocation, expats can turn these challenges into opportunities.

At Skybound Wealth Management, we are proud to collaborate with Skybound Capital to ensure our clients have access to the latest insights and strategies. Whether you’re looking to safeguard your wealth against inflation, adjust your portfolio in response to potential future reductions in interest rates, or explore new regional opportunities, we’re here to help you across all of your global wealth management needs. Together, we can ensure your financial future is secure— wherever your journey takes you.

In this edition of the Expat Investor Podcast, we’re diving deep into the world of property investment with your host, Tom Pewtress, Global Head of Proposition at Skybound Wealth Management, and special guest Simon Athwal, a seasoned financial adviser with many years of experience in the Middle East.

Join the Conversation

Tune in to this insightful episode as Tom and Simon share their expertise on making the most of property as an investment. Whether you’re a seasoned investor or just starting, their discussion will equip you with the knowledge to navigate the complexities of property investment and integrate it effectively into your broader financial strategy.

In this episode, Tom and Simon tackle one of the most frequently asked questions in the world of wealth management: Why is property such a popular asset class? They explore the tangible allure of real estate, the cultural influences driving property ownership in the UK, and the historical performance that makes property a reliable long-term investment.

Tom and Simon break down the concept of leverage in property investment, illustrating how you can control a large asset with a relatively small capital outlay. They discuss how leveraging can significantly amplify returns and why it’s such a powerful tool for building wealth over time. Using practical examples, they demonstrate how even modest increases in property value can yield substantial returns when leveraged correctly.

Understanding debt is crucial to successful investing. Tom and Simon delve into the differences between good debt and bad debt, particularly in the context of property mortgages. They compare interest-only and capital repayment mortgages, providing insights into which might be best depending on your financial goals and life stage. They also discuss the importance of having a robust financial plan, especially when dealing with leverage and long-term debt.

While property is a strong investment, Tom and Simon caution against over-reliance on any single asset class. They discuss the importance of diversification, explaining how spreading investments across different assets can protect against market volatility, maintenance costs, and rental income fluctuations. The duo also highlights specific risks within the UK property market, such as interest rate fluctuations and tax implications, and how to mitigate these risks.

Off-Plan

Are you considering investing in off-plan properties or completed ones? Tom and Simon explore the pros and cons of each, helping you understand which option might align best with your investment strategy. Whether you’re early in your wealth accumulation journey or looking for immediate rental income, they provide valuable insights to guide your decision-making.

For those planning for retirement, this episode offers essential advice on creating reliable income streams through property investment. Tom and Simon explain how property can serve as a stable source of income that complements other investments, helping to extend the longevity of your retirement savings. They also discuss property as a hedge against inflation, ensuring your income keeps pace with rising costs.

With Tom Pewtress & Guests

In this series, we look at all things investing for those living outside their home country and to help you make the most of your wealth.

Written by Thomas Sleep

As an expat, racking up Skywards points can really level up your travel game, making your journeys more enjoyable and cost-effective.

Emirates Skywards, the loyalty programme from Emirates Airlines, has plenty of ways for you to earn and spend these points. Here’s how you can make the most out of it.

Skywards points are like a special currency within the Emirates Skywards programme. You can earn and use these points for a bunch of things beyond just flights—think upgrades, hotel stays, car rentals, and even unique experiences. The trick is knowing how to gather these points efficiently and use them smartly.

One of the easiest ways to earn Skywards points is with an Emirates co-branded credit card. These cards let you earn points on every purchase, with extra points for spending on Emirates flights and other partners. Plus, you can even use your credit card to fund investments and other big expenses, helping you accumulate points faster.

Remember to use credit cards responsibly. Always pay off your balance in full each month to avoid high interest charges and maintain a good credit score.

Using Your Credit Card to Fund Investments

Using your credit card for investments as an expat can be a strategic move to earn more Skywards points. Here’s how to do it effectively:

• Direct Investment Platforms: Some investment platforms allow you to fund your account with a credit card. This is an easy way to earn points on significant transactions.

“The trick is knowing how to gather these points efficiently and use them smartly.”

• Property Investments: When purchasing property, check if any part of the transaction can be done via credit card. This could include paying for services like property management or even the deposit.

• Recurring Investments: Set up recurring investments in mutual funds or retirement accounts using your credit card. This ensures regular point accrual while you build your investment portfolio.

Important: Ensure you manage your spending and avoid carrying a balance on your credit card to prevent high-interest charges. This strategy is most beneficial when you can pay off your card in full each month.

“Consider using points for upgrades, as they often offer better value compared to free flights. Also, check out Emirates’ Mix & Match option, allowing you to use a combination of cash and points for bookings.”

When you’re booking flights, these tips will help you maximise your Skywards points:

• Book Directly with Emirates: You’ll often get more points booking directly with Emirates rather than through third-party sites, plus you can take advantage of special promotions.

• Fly with Partner Airlines: Emirates partners with airlines like Qantas, Japan Airlines, and Alaska Airlines, so you can earn points on those flights too. Just make sure to enter your Skywards number when booking.

• Class of Service: Higher fare classes (like Business and First Class) earn more points than Economy. For example, Business Class can get you up to 175% of the miles flown in points, while Economy can earn between 25% to 100% depending on the fare type.

Skywards Everyday is an app that lets you earn points on your daily purchases. Link your Emirates Skywards account with the app and earn points at partner outlets for dining, retail, wellness, and more.

• Dining: Earn points at participating restaurants, cafes, and even with delivery services.

• Retail: Points are up for grabs at fashion outlets, electronics stores, and supermarkets.

• Wellness: Earn points at gyms, spas, and wellness centres.

Emirates frequently offers promotions that can give you bonus Skywards points. Keep an eye on the Emirates Skywards website and sign up for their newsletter to stay in the loop.

• Double or Triple Points: These promotions can give you double or triple points for booking certain routes or during promotional periods.

• Bonus Points for New Routes: Sometimes Emirates offers bonus points to encourage travel on new routes.

Earn Skywards points by shopping with Emirates’ retail partners, both online and offline. This includes luxury brands, car rentals, and even financial services.

• Emirates High Street: Shop online and earn points on a wide range of products, from electronics to home goods.

• Partner Retailers: Earn points at select stores in malls and shopping centres, such as luxury boutiques and high-end department stores.

You can earn points for every stay at Emirates’ partner hotels, which include luxury chains like Hilton, Marriott, and more.

• Booking.com and Agoda.com: Book your stay through these platforms and earn points. Sometimes there are special promotions that offer additional points for bookings made through these sites.

• Hotel Loyalty Programs: Link your hotel loyalty programmes with Emirates Skywards to double dip on points, earning both hotel points and Skywards points for the same stay.

When renting cars, pick Emirates’ partner companies like Hertz, Avis, and Sixt to earn additional points on your rentals. Look out for promotions that offer bonus points for renting cars for longer durations or booking higher-end models.

If you travel for work, make sure your employer signs up for the Emirates Business Rewards programme. This lets you earn both individual Skywards points and Business Rewards points for the company.

• Corporate Travel: Employees can rack up points for business trips, which can be redeemed for future corporate travel or personal use.

• Small and Medium Enterprises: SMEs can earn points on business travel expenses.

Emirates lets you buy, gift, or transfer Skywards points, which is handy if you’re just short of the points needed for a reward.

• Buy Points: Top up your account when you’re close to a reward. Emirates often has promotions where you can buy points at a discount or get bonus points.

• Gift Points: Share the benefits with family and friends, especially if they are close to reaching a reward.

• Transfer Points: Pool points with family members to reach rewards faster. This is perfect for families travelling together or planning a big trip.

Maximising your Skywards points as an expat requires some planning and savvy usage of available resources. By following these tips, you can make the most of your Emirates Skywards membership and enjoy more rewarding travel experiences. Start implementing these strategies today and watch your Skywards points accumulate faster than ever before.

Lastly, redeem your points smartly to get the most value. Consider using points for upgrades, as they often offer better value compared to free flights. Also, check out Emirates’ Mix & Match option, allowing you to use a combination of cash and points for bookings.

• Upgrades: Use points to upgrade from Economy to Business Class or Business to First Class for a more luxurious travel experience.

• Special Offers: Look for redemption specials, where Emirates offers discounted rates on certain routes or services.

• Emirates Skywards & flydubai: Use your points across both airlines for more flexibility and redemption options.

Since 2003, GC Partners have been helping private & corporate clients across the UAE with their foreign currency and money transfer needs.

Q3 2024 Review & Q4 2024 Outlook

Written by Jabir Sardharwalla

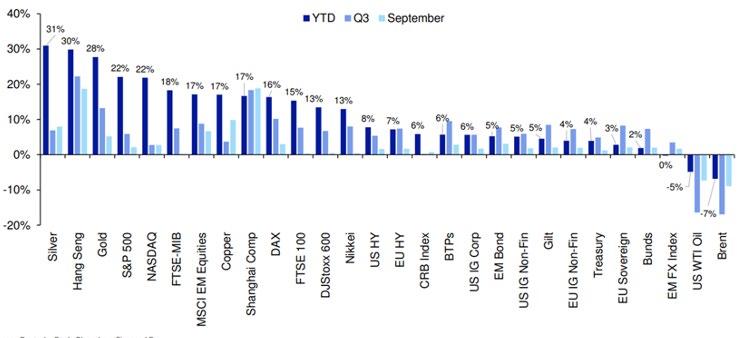

With Q3 just ended, the table below sets out performance by various asset classes / styles:

Q3 delivered good returns giving the perception of calm markets. This was simply not the case. The Quarter was characterised by three features: (1) Two main bouts of volatility – the first starting end of July and peaking first week of August and the second into September. Both had very little to do with fundamentals (more on this later); (2) The muchawaited Fed rate cut of -0.50%. The size of the rate cut alone signalled a strong message to markets - though it remains to be seen whether markets have understood the rationale behind it (again, more on this later) and (3) the substantial stimulus package in China. Global REITs was the top performer delivering over +16% on the Quarter to stand at +21.5% for the year. This is no surprise given the interest rate sensitivity

of this sector. The sector has been trading on very cheap valuations and there is an expectation amongst investors that this marks a turnaround. The latter is debatable given the still large and persistent property overhang. Rate cuts simply help to reduce the discounts to NAV – they do not eradicate them entirely; only an improvement in fundamentals can do that. Vast amounts of Office property remain at distressed levels. Sellers are still reluctant to sell – buyers are still bargainhunting. Value and small cap sectors enjoyed a bounce as sector rotation continued from growth. In terms of highlights, consider the chart on the following page:

Source: Bloomberg Finance LP, Deutche Bank

“Sellers are still reluctant to sell – buyers are still bargainhunting”

• The first bout of volatility was fuelled by incorrect perceptions around the US job market, specifically the weekly jobless numbers which had been rising. Economists became particularly concerned about a slowing job market and its potential implications of a recession. This resulted in a second bout of volatility in September also to do with jobs but specifically around job openings. In both cases, markets overlooked two sides of the equation – job layoffs/ discharges remain low as ever implying companies are focused on retaining workers while reducing the emphasis on hiring (costly and time-consuming). Also, fears generated by recession-talk likely meant fewer people were quitting their jobs which meant less need for companies to hire! Investigations into Nvidia for alleged antitrust violations by the DoJ and late filings by Super Micro sent jitters throughout the tech sector – explaining the substantial rotation from growth stocks into value.

• The rate cut was well-received and reverberated across all sectors. It was also a boost to Fixed Income markets with the Barclays Global Aggregate index returning 7.0% in the quarter. Government and corporate bonds both fared very well – while EM bonds rallied over 6% on the quarter. There has been a marked shift in where markets perceive rates to land. At the end of Q2, they saw it at 4.4% by mid-2025. Now, it is expected to be 3.2%.

• The Chinese Central bank (PBoC) delivered a raft of stimulus packages (monetary, property and market-related) to shore up sentiment. Time will tell how this plays out but it was quite a fillip. Chinese markets were up over 10% in one week alone! If this spreads to the retail investors, an even bigger rise is in store.

• As referenced above, Chinese markets performed very well. The Hang Seng is +30% ( US$ terms) putting on almost +20% in Q3. The Shanghai Composite is up +16.7% YTD (also US$ terms) with nearly all of that coming in September.

• Tech was rather lacklustre by its own standards with the Mag-7 gaining “only” +5.4% in the Quarter. Contrast that with the S&P 500 which gained +5.9% over the same period – only a bit more than the Mag-7. The strong sector rotation alluded to above saw Utilities pile on +19.4% to become the best performing sector.

• The Yen had its strongest Quarter vs the US$ (since Q4 2008) gaining 12% fuelled by a combination of rate hike talk in Japan and further rate cuts in the US. A lot of the Yen rally is fuelled by a reversal of the “carry trade” which essentially happens when volatility spikes (risk-off). It has nothing to do with economic fundamentals – it’s entirely around underlying technicals. It’s why the Yen is perceived to be a “safe haven” FX.

• True safe haven assets such as Gold gained over 13% in US$ terms, its strongest Quarter since Q1 2016 as markets priced in faster rate cuts.

• The real surprise is Oil (Brent and Crude) which has declined over the month, the Quarter and YTD. This has been a huge reason for the decline in headline inflation and the slower decline in core inflation.

• We have had a lot of noise which has resulted in sell the rumour and subsequently buy the fact around the misinformation & misinterpretation of data, especially jobs data!

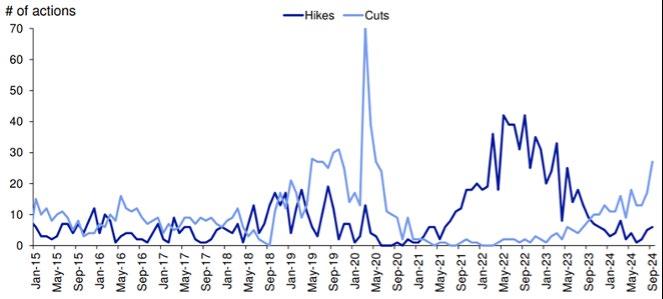

• We have witnessed the start of rate cuts - sizeable ones in the US and China. Rate cuts have not been limited to just these two nations – the Euro-area has also cut its rates.

• Economic activity remains mixed: services activity in developed countries remains in expansion (i.e. over 50) while manufacturing (a smaller component of their economies) in contraction (less than 50 but not massively so).

• Headline Inflation continues its downward trend aided strongly by falling fuel costs. There is a real chance these lower fuel costs could come back to spur headline inflation.

• Retail spending remains well-buoyed as do consumer savings ratios.

• The main concern is the rise in geopolitical risk. Even at the time of writing, the Middle east has erupted again with Israel bombing sites in Lebanon (Hezbollah targets) and elimination the Hezbollah leadership and now targeting Iran following the latter’s missile attack on 1st October.

The following factors will be key during Q4 and define market trajectory:

• Geopolitics: as referenced in the last point on the page before, how far the Middle East escalates will determine geopolitical risk and subsequently energy prices. The latter, in turn, will drive inflation. Iran produces almost 4 million barrels of oil per day (mbpd) accounting for about 4% of global production. Given several cuts in production by OPEC recently, this shortfall could be absorbed (to the delight) of other oil producers for a higher price. Oil prices have tumbled and crude prices sit in the low-$70 end. The likes of Saudi need an oil price closer to $100 pb to breakeven on its domestic budget. Even given the current flareup in the Middle East, it’s

hard to see oil reaching such heights. It would take something far wider - such as blocking off the Straits of Hormuz – to cause contagion. It’s not impossible!

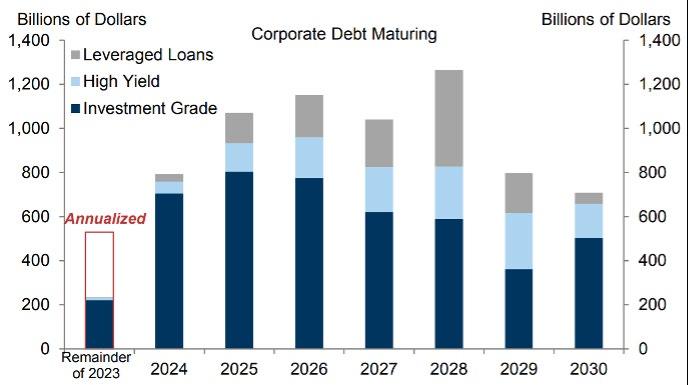

• Interest rates: why did the Fed cut so aggressively? The US economy has not displayed signs of weakness that warrants such an aggressive cut (some would say ant rate cut at all!). Furthermore, the consumer savings and investment ratio remain healthy as does retail spending. There is no imminent risk to the mortgage market with overall, weighted-average mortgage rate still low (albeit higher vs a year ago). So why did the Fed go so deep? I think the answer rests in next year’s maturing Global corporate debt wall which then peaks into 2026.

Two things to note – the US dominates (though Europe is not far behind) and the non-Investment Grade (IG) portion rises materially. Now look specifically at the US corporate maturity wall breakdown:

“Time will tell but rate cutting now far exceeds rate hiking around the globe”

If US companies had to refinance at today’s loan rates, they would suffer higher loan rates in the order of 2% (the exact amount is hard to say as there would be some mitigation from things like interest rate hedging). This higher level – which affects the non-IG companies even more – would result in cost savings which typically come from shedding labour and reduced investment. If this were to happen, then there really would be a labour market problem and an inflation would loom! If correct, the Fed needs to cut by somewhere between 1.5% to 2.0% between now and say middle of 2025. It has already done 0.50% of this! Time will tell but rate cutting now far exceeds rate hiking around the globe:

Source: Haver Analytics, Deustche Bank

US election: It’s going to be a very tight race. VP Harris has narrowed the gap and, depending on which poll ones looks at, leads over Trump. Some suggest she even has a very narrow lead in the critical swing states. ALL polls and their findings are well within the margin or error depending on the pollster and the state in question. Two factors distinguish the candidates – VP Harris wants to provide a big boost to housing by offering $25,000 assistance in downpayments for people to buy homes; Former President Trump wants to cut inflation by effectively flooding the market with cheap oil. The former often results in a housing bubble while the latter is inflationary (services inflation). Both should raise GDP. The bigger impact will be foreign policy and (re)shaping geopolitics – not just towards the Middle East but also China and Russia.

Europe: The European political landscape has changed. The recent Parliamentary elections have given rise to a large Far-Right vote (Italy, France, Germany, Poland, Holland). Together, they account for some one-third of the Parliamentary makeup, significantly higher vs the previous, outgoing Parliament. Then, more recently in Germany, two major state elections saw the Far-Right (the AfD) win in Thuringia and come a close second in Saxony. Things look very bleak for the coalition government of the centre-right. Generally, these Far-Right groups have a softer stance towards Putin, Russia’s position on Ukraine and are more resisting towards the EU as it currently stands. The latter does not mean the EU is set to implode – just that it’s headed for a major restructuring.

Thank you for your continuing support as always – we really value it and please reach out to us if you have any questions.

In the world of wealth management, Switzerland has long been synonymous with excellence. Its robust financial sector, renowned for its stability and discretion, has attracted investors from around the globe seeking to safeguard and grow their wealth.

However, beneath this reputation lies a cost conundrum that savvy investors should be aware of: the expense of portfolio management through traditional banking channels compared to bespoke financial services.

Written by Taylor Condon

Swiss banks have historically been the preferred choice for many investors, offering a comprehensive suite of financial services under one roof. From asset allocation to investment advice, these institutions provide a one-stop solution for managing wealth. Yet, this convenience often comes at a steep price.

One of the primary drawbacks of relying on banks for portfolio management is the high fee structure they impose. These fees can eat into investment returns significantly over time, eroding the potential growth of a portfolio. While banks justify these fees by pointing to the expertise and personalized service they provide, the reality is that many investors end up paying for services they may not fully utilize or need.

Moreover, the inherent conflict of interest within traditional banking models cannot be overlooked. Banks often promote their proprietary products or in-house funds, which may not always align with the best interests of the client. This lack of independence can limit the universe of investment options available to investors, potentially hindering portfolio diversification and performance.

In contrast, bespoke financial services offer a compelling alternative for investors seeking more cost-effective and tailored solutions. These independent wealth managers operate with a fiduciary duty to act in the best interests of their clients, free from the conflicts often present in traditional banking relationships.

By leveraging their expertise and network of external specialists, bespoke financial advisers can construct customized investment portfolios designed to meet the unique objectives and risk profiles of their clients. Furthermore, these advisers typically operate on a fee-based model rather than earning commissions on financial products sold, aligning their interests with those of the investor.

In Switzerland, where the financial landscape is characterized by its sophistication and discerning clientele, the demand for bespoke financial services is on the rise. Investors are increasingly recognizing the value proposition offered by independent advisers, who provide transparency, flexibility, and a more intimate client-advisor relationship.

While Swiss banks undoubtedly continue to play a pivotal role in the financial ecosystem, investors are becoming more discerning in their choices, weighing the costs and benefits of traditional banking versus bespoke financial services. In an era where cost efficiency and performance are paramount, the allure of personalized, cost-effective portfolio management is undeniable.

In conclusion, while Swiss banks have long been synonymous with wealth management excellence, the high costs associated with their services are prompting investors to explore alternatives. Bespoke financial services offer a compelling solution, providing tailored portfolio management at a fraction of the cost, and with a focus on independence and transparency. As investors seek to optimize their wealth management strategies in Switzerland, the choice between traditional banking and bespoke financial services has never been clearer.

Meet Ryan Donaldson, a key leader at Skybound Wealth and an integral part of our team for over a decade. Ryan’s journey with Skybound began in 2014 when he joined as a Paraplanner in the Middle East. His unwavering dedication and talent quickly stood out, leading to his transition to Financial Adviser in Europe in 2018—one of the industry’s most demanding markets.

Recognised for his professionalism and expertise, Ryan was awarded Best Newcomer Adviser early in his advisory career. His success continued, and by 2021, he was promoted to Regional Manager for Switzerland. In this role, Ryan played an instrumental part in expanding Skybound Wealth’s reach across Europe. His leadership skills were further recognised when he moved to London to collaborate with Peter Gollogly and Bryan Bann, laying the foundation for our European team’s continued growth.

Ryan’s impact at Skybound extends far beyond his leadership roles. He is known for hosting some of our most successful seminars, where his depth of knowledge in financial planning, investments, and pensions shines through. A Level 6 Chartered Member of the Chartered Institute for Securities & Investment (CISI), Ryan’s expertise ensures his clients receive personalised financial strategies that align with their long-term goals.

Beyond his own achievements, Ryan is also deeply invested in developing the next generation of financial professionals. His mentorship of new advisers and contributions to our Graduate Academy have helped shape the future talent at Skybound, ensuring that our clients receive the highest level of service.

Ryan’s extensive experience in the UK, Europe, and Switzerland makes him uniquely positioned to offer expatriate clients tailored financial planning advice. Whether it’s retirement planning, diversifying portfolios, or navigating the complexities of international investments, Ryan is dedicated to ensuring his clients’ financial ambitions become a reality.

Ryan Donaldson’s decade-long journey with Skybound is a testament to his passion, expertise, and commitment to professional excellence. He continues to set an example for both new and experienced advisers, making him an invaluable part of our leadership team.

This tax break can not be carried forward or applied retrospectively, if you do not take steps before the middle of December they are lost forever.

Speak to us now to find out how to reduce your Swiss tax liabilities

Having lived and worked as a financial adviser in Switzerland for many years, I’ve gained a deep understanding of the unique financial challenges and opportunities that expats face here. Switzerland is an exceptional place to live and work, with its high salaries, stable economy, and outstanding quality of life.

Written by Bryan Bann

However, making the most of your financial situation as an expat requires more than just enjoying the benefits—it’s about smart, strategic planning. Here are ten essential tips based on my first-hand experience advising expats like you.

When I first moved to Switzerland, the threepillar pension system seemed complex, but understanding it will play a big part in securing your financial future.

• Pillar 1: This state pension is mandatory, funded by contributions from both employees and employers.

• Pillar 2: The occupational pension is also mandatory and is key to maintaining your lifestyle in retirement.

• Pillar 3: A voluntary private pension that allows you to boost your savings with attractive tax benefits.

For expats, particularly those who might not retire in Switzerland, it’s essential to understand how these pillars work together. I’ve helped many clients understand this system to ensure their longterm plans are put in place, even if their time in Switzerland is temporary.

One of the first pieces of advice I give my expat clients is to fully utilise their Pillar 3a contributions. These contributions are tax-deductible up to a certain limit, and the investment growth is tax-free. This provides a dual benefit: immediate tax savings and long-term financial gain. Whether you’re here for a few years or planning a longer stay, maximising your Pillar 3a is a no-brainer for securing both your financial present and future.

“Switzerland is an exceptional place to live and work, with its high salaries, stable economy, and outstanding quality of life.”

4

Consider Using a Vested

Leaving Switzerland before retirement? You don’t want to leave your pension behind. I often recommend transferring your Pillar 2 pension savings into a vested benefits account. These accounts frequently offer better interest rates, investment options and tax advantages upon exit, especially in tax-friendly cantons like Schwyz or Zug. It’s about ensuring that your hard-earned money continues to work for you, even after you’ve moved on.

Swiss pension conversion rates have been decreasing in recent years, something I monitor closely for my clients. This decline means that the income your retirement savings will generate could be less than expected. It’s a critical factor to consider when planning your retirement, and in some cases, you may need to adjust your savings strategy or explore alternative investments. My role is to ensure you’re aware of these changes and help you adapt your plan to maintain your desired retirement lifestyle.

5

6

“One of the biggest risks for expats earning in Swiss francs but spending or investing in other currencies is exchange rate fluctuations. These can have a substantial impact on your finances if not managed properly.”

Diversification is a key principle in managing risk, particularly in a high-cost environment like Switzerland. I’ve seen the benefits of a welldiversified portfolio time and again with my clients. By spreading investments across different asset classes and geographic regions, you can achieve greater financial stability. Together, we can build a portfolio that aligns with your goals, ensuring you’re prepared for whatever the market throws your way.

If you’re living in France or Germany but working in Switzerland, you’re dealing with cross-border taxation, which can be a minefield. Your income is taxed at source in Switzerland, but you’ll also have tax obligations in your country of residence. Double taxation treaties can be beneficial, but the details can be complicated. I specialise in helping expats deal with these challenges, ensuring compliance while minimising tax burdens. 3

7 8

Banking fees in Switzerland can be surprisingly high, especially for non-residents. Selecting the right bank can make a big difference in how much of your money stays in your pocket. Over the years, I’ve helped many expats choose banks that offer favourable terms, avoiding unnecessary fees and ensuring their banking experience is as seamless as possible.

9 10

For those of you living in France but working in Switzerland, the French wealth tax can be a significant consideration, particularly if you own real estate. It’s a tax that can catch you off guard if you’re not prepared. It’s important that you are aware of the relevant thresholds and rates of tax to ensure you don’t get caught out later down the line.

One of the biggest risks for expats earning in Swiss francs but spending or investing in other currencies is exchange rate fluctuations. These can have a substantial impact on your finances if not managed properly. Hedging against currency risk is something I often recommend to my clients. By using tailored strategies, we can protect your wealth and ensure that currency movements don’t undermine your financial goals, whilst keeping in mind any planned future moves or change of preferred retirement location.

For me, taking the time to consult with a financial adviser is a non-negotiable for expats in Switzerland. Of course, you could say that being a financial adviser I am biased, but working with a professional can help you understandable the complexities of the Swiss financial landscape is key to ensuring your financial strategies are optimised for tax efficiency, investment growth, and long-term security.Whether you’re planning for retirement, managing cross-border taxation, or protecting your wealth from currency fluctuations, a financial adviser can provide personalized advice to help you achieve your financial goals. Don’t wait—seek expert guidance to secure your financial future.

Living and working in Switzerland as an expat is an incredible opportunity, but to truly make the most of it, you need expert financial advice. As someone who’s been through this journey myself, I understand the challenges and the opportunities that lie ahead. Let’s work together to build a financial plan that secures your future, optimises your investments, and gives you peace of mind.

Written by Maximillian Gerstein

As an expat living in the UAE, securing your financial future and protecting your loved ones should be a top priority. Without proper legal documentation, your assets might not be distributed according to your wishes, leading to unintended and potentially devastating consequences for your family.

Max Gerstein, a UAE based financial adviser at the award winning Skybound Wealth Management, explores the critical importance of having a will, naming beneficiaries, and ensuring all legal matters are in order for expatriates in the UAE.

Local Laws And Sharia Application:

In the UAE, if an expatriate dies without a will, their estate will be subject to Sharia law. This dictates specific inheritance shares that may not align with your wishes. For instance, male heirs typically receive double the share of female heirs, and the distribution is strictly regulated. This means your spouse and children won’t receive the assets you intended for them. Imagine your family being forced to leave their home because the property has been allocated to other heirs. Your wife and children facing eviction, causing them to move area, maybe even country.

Complexity Of Foreign Wills:

A will from your home country is not guaranteed to be recognised or enforced in the UAE. The local courts prioritise UAE laws, and proving the validity of a foreign will can be a lengthy and complex process. This delay can cause immediate financial uncertainty and hardship for your loved ones during an already difficult time. For example, without access to your bank accounts, your family will struggle to pay for daily expense. Imagine your partner looking into their wallet and realising that the cash they have on hand is all they can use to support the family until the courts decide what to do. How long can they last?

Register A Will Locally:

Non-Muslim expatriates can register their wills in Dubai and Abu Dhabi. This ensures that your assets are distributed according to your wishes and bypasses default Sharia inheritance rules. Without a locally registered will, your wife and children could lose their home if the property is allocated to other heirs who might not honour your intentions. This will result in your family facing the emotional trauma of relocating during a period of grief, disrupting their lives further.

Appoint Guardians For Minor Children:

Imagine your children ending up with distant relatives or strangers. If you don’t have a guardian appointed, this is what reality could look like. Is this something you want? Without appointing a guardian in your will, the local courts will decide on guardianship. Not you and not your partner.

Understand The Freezing Of Assets:

Upon an expatriate’s death, bank accounts and other assets are typically frozen until the local courts issue a Succession Certificate. This will lead to significant financial strain for surviving family members, as they won’t able to access necessary funds for daily living expenses, education, or emergencies if they don’t have their own account. Imagine your family not being able to pay for groceries, utilities, or school fees, this will force your spouse to take on multiple jobs or make drastic lifestyle changes to make ends meet.

Naming Beneficiaries:

“Without a locally registered will, your wife and children could lose their home if the property is allocated to other heirs who might not honour your intentions.”

Ensure all your assets and investments, have clearly named beneficiaries. This helps streamline the transfer process and reduces potential legal disputes. If you don’t, your assets will be distributed according to default legal rules, which won’t reflect your true intentions and could lead to disputes among your family. Such disputes can tear families apart and drain resources through prolonged legal battles. In the UAE, you can’t name beneficiaries on bank accounts, so it’s crucial to have separate accounts with money in them for each family member. If beneficiaries aren’t clearly stated for your other assets, they can go to whoever and not your intended. While your family is mourning, do you want them fighting over ownership while trying to survive?

Written by Carla Smart

As we’ve all seen in recent times with the changes to the lifetime allowance (LTA), pension reforms remain a constant feature in UK fiscal policy. The decision to abolish the LTA in the 2023 Budget was framed as a way to encourage experienced professionals to stay in the workforce longer. However, it also highlights the ongoing tug-of-war between pension flexibility and tax revenue generation.

With this backdrop of frequent pension policy changes, and the first Labour government Budget for 14 years on the horizon, it’s worth taking a look at some of the more historic shifts in pensions.

From Margaret Thatcher’s reforms in 1979 to more recent developments under successive governments. These shifts have often mirrored the political and economic ideologies of the time, influencing how we plan for retirement.

“These shifts have often mirrored the political and economic ideologies of the time, influencing how we plan for retirement.”

When Margaret Thatcher took power in 1979, her government implemented key reforms that reflected her economic philosophy of reducing the state’s involvement in welfare.

Linking State Pensions to Inflation (1980):

Thatcher’s government indexed state pension increases to the retail price index (RPI) instead of average earnings. This change controlled state spending but over time, significantly reduced the real value of the state pension as wage growth outpaced inflation.

Promotion of Personal Pensions (1986):

The introduction of portable personal pensions allowed workers, especially those changing jobs, more control over their retirement savings. While this helped some, it also shifted the risk from the state and employers to individuals.

Reforms to Occupational Pensions:

The Social Security Act 1986 introduced stricter regulations, such as inflation-linked revaluation for early leavers, which helped protect deferred pensions from inflation.

Blair’s government, focused on modernising the UK’s welfare system, introduced significant pension reforms.

Restoring the Earnings Link (1997):

Blair’s government restored the link between the basic state pension and average earnings to ensure pensions kept pace with living costs.

Auto-Enrolment and the Pensions Commission (2002–2012):

In response to the growing number of workers without private savings, Labour established the Pensions Commission. This led to auto-enrolment, ensuring employees were automatically enrolled into workplace pensions, significantly boosting pension savings.

Raising the State Pension Age:

Labour also introduced phased increases to the state pension age through the Pensions Acts of 2007 and 2008, reflecting longer life expectancies.

The coalition government (2010–2015) between David Cameron and Nick Clegg, followed by the Conservative government, made further significant pension reforms.

Raising the State Pension Age:

The coalition government accelerated the rise in the state pension age, with plans to equalise it at 65 for men and women by 2018, and increase it further to 66 by 2020.

The Triple Lock Guarantee (2010):

To protect pensioners from falling living standards, the coalition introduced the triple lock, ensuring state pensions rise by the highest of inflation, average earnings, or 2.5% each year.

Auto-Enrolment (2012):

Building on Labour’s earlier reforms, the coalition fully rolled out auto-enrolment into workplace pensions, ensuring millions more workers contributed to a pension scheme.

Pension Freedoms (2015):

After the 2015 election, the Conservative government introduced pension freedoms, allowing individuals over 55 with defined contribution pensions to withdraw their savings flexibly, giving them more control but also increasing the responsibility on individuals to manage their retirement funds.

QROPS Changes (2017):

In 2017, significant changes were made to Qualifying Recognised Overseas Pension Schemes (QROPS), used by UK expats to transfer their pensions abroad. A 25% tax charge was introduced on QROPS transfers unless specific conditions were met, such as the transfer being made within the European Economic Area (EEA). These changes were intended to reduce tax avoidance while maintaining QROPS as a legitimate option for expats.

“After the 2015 election, the Conservative government introduced pension freedoms, allowing individuals over 55 with defined contribution pensions to withdraw their savings flexibly”

As history has shown, pensions frequently find themselves on the agenda when there is a change in government or ideology. Whether driven by fiscal concerns, demographic shifts, or political priorities, these reforms are often framed as necessary adjustments for long-term sustainability. However, the specifics of what changes—if any—lie ahead remain uncertain at this moment. What is clear in my experience however is that fiscal events like these often serve as a ‘jolt,’ prompting many to reassess their financial plans. Yet, waiting until after these changes are implemented often means reacting and being punished in some way. Staying ahead of the curve, reviewing your finances proactively, and seeking expert advice can help you make the most of these shifts while protecting yourself against future uncertainties.

Staying on top of how your pension works and any shifts in legislation is not just a matter of convenience; it’s a necessity for safeguarding your financial future.

• What If I Am Overseas When I Draw Income From My UK Pension?

• How Much Tax Do I Pay?

• Know Your Tax Code

• What Tax Code Will Your SIPP Provider Use?

• Understanding Your Tax Bill

• How Do I Claim Back Any Tax That Has Been Overpaid?

Scan the QR code code or click here to download the e-guide.

Or contact your Skybound Wealth Financial Adviser today for more information.

Written by Josh Burton

As a Chartered Accountant, and Chief Financial Officer of an award winning financial advice company, Josh Burton has seen firsthand the profound impact diligent financial management can have on both businesses and individuals. One of the key practices that can make a significant difference in personal finance is treating it with the same rigour and discipline as you would a business.

Wealthy and successful individuals often use the same methods to assess their personal finances.

So, let’s look at why running your personal finances like a business is crucial and how you can get started.

A business uses financial reporting in three ways:

• To look back at historic financial performance to better understand future requirements

• To assess its current balance sheet and understand its financial strength

• To forecast and budget for the future

Clarity and Control

Just as businesses need to know their financial health to plan for the future, so do individuals. Having a clear picture of your income, expenses, assets, and liabilities, is essential for making informed decisions and gives you clarity and control over your financial situation. Achieving clarity allows absolute control over your financial life and can help to relieve anxiety you might have about the future.

Goal Setting and Tracking

Businesses set financial goals and track their progress towards achieving them. This practice is equally beneficial in personal finance. By setting clear financial goals, such as saving for a home, retirement, or a holiday, you can create a roadmap. More importantly, you can measure your progress regularly.

Your goals might include traveling the world, giving time to charitable causes, securing the next generation of your family’s future, or a combination of all these ambitions. Realising these ambitions in the future requires structured planning and ongoing assessment in the present.

“While investing entails risks, informed decision-making, diversification, and a long-term approach can help navigate challenges and optimize investment returns.”

Drawing on his many years of experience, Josh has compiled an 8-point checklist to help you achieve your financial goals.

1. Create Financial Statements

Start by creating your personal financial statements:

• Profit & Loss / Income Statement: Track your income sources and expenses to determine your net income.

• Balance Sheet / Statement of Financial Position: List your assets (e.g., savings, investments, property) and liabilities (e.g., loans, credit card debt) to calculate your net worth.

2. Set Financial Goals

Define your short-term and long-term financial goals.

Short-term goals might include saving for a vacation or paying off credit card debt, while long-term goals could involve buying a house, funding your children’s education, or retirement planning.

3. Develop a Budget

Create a monthly budget that outlines your expected income and expenses. Categorize your expenses (e.g., housing, utilities, groceries, entertainment) and allocate funds accordingly. Review your budget regularly and adjust as needed to stay on track.

This should hopefully leave you with a surplus budget each month. If it doesn’t, you need to answer to the fact you are most probably living beyond your means. This is a common problem that expatriates find themselves with, but is usually easily resolved.

4. Monitor Cash Flow

Track your actual income and expenses against your budget. A simple excel spreadsheet can be used to do this. Regularly monitoring your cash flow helps you identify areas where you can cut costs or increase savings.

5. Build an Emergency Fund

Aim to save at least three to six months’ worth of living expenses in an easily accessible account. This fund acts as a financial cushion, providing peace of mind and security in case of unexpected events

6. Invest Wisely

Just as businesses invest to grow, consider investing your savings to build wealth over time. Diversify your investments across different asset classes (e.g., stocks, bonds, real estate) to manage risk and achieve your financial goals.

7. Seek Professional Guidance

Consulting with a financial professional can provide you with tailored advice and strategies to optimize your personal finances. They can help you navigate complex financial decisions, consider future tax consequences, ensure you’re on track to meet your goals, and provide support in creating and maintaining a comprehensive financial plan.

8. Review and Adjust Regularly

Conduct regular reviews of your financial situation, at least quarterly. Assess your progress towards your goals, analyse your spending patterns, and make necessary adjustments to your budget and financial plans.

• Improved Financial Health: By understanding and managing your finances better, you can improve your overall financial health and stability.

• Reduced Stress: Knowing where you stand financially reduces anxiety and helps you make confident financial decisions.

• Increased Savings: Effective budgeting and expense management lead to higher savings, enabling you to achieve your financial goals faster.

• Better Preparedness: An emergency fund and wise investments ensure you’re prepared for the future, no matter what it holds.

• Expert Guidance: Professional financial advice can optimize your financial strategy, offering insights and recommendations tailored to your unique situation.

Running your personal finances like a business might seem daunting at first, but the benefits are well worth the effort. By applying the principles of business accounting to your personal finances, you gain clarity, control, and confidence, setting yourself up for a secure and prosperous future. Start today by setting up your personal financial statements, creating a budget, and setting clear financial goals. And remember, consulting with a financial professional can provide you with the expertise and support needed to make the most of your financial journey. Your financial future is in your hands—manage it wisely.

Sometimes life gets in the way of us looking at things as important as this or we are just too anxious to start. Just as a business operates with a Finance Director or Chief Financial Officer, its often so beneficial to operate with a financial mentor for your personal life. If you’re unsure where to start, want guidance on the basics or some more unique financial matters applicable to your circumstances – please reach out for a complimentary introductory session.

Written by Chris Bowler

There are several dedicated retirement structures available to South African expats. Navigating these options and deciding which suits you best, along with how to invest these assets, hinges on several critical questions that need answering before making any decisions:

• Where do you plan to retire?

• What currency will you spend in retirement?

• What is your risk tolerance?

• What is your time horizon for withdrawing funds?

• What income level do you need from your investments?

• Do you prefer a lump sum or regular income withdrawals?

Retirement Annuities, Provident Funds, and Preservation Funds are examples of onshore retirement accounts offered by South African institutions.

When considering these provisions, the pivotal question remains: How do you want to invest your assets? It’s your money, and many expats may have never revisited their initial asset allocation or fund choices since setup.

• Are your investments still aligned with your goals?

• Do they meet your growth expectations?

• Are you invested in sectors and companies you prefer?

In 2023, amendments to the Pensions Fund Act, known as Regulation 28, aimed to safeguard wealth by reshaping how South African expats manage their retirement funds – a positive step forward.

What is Regulation 28?

Regulation 28, part of the Pension Funds Act, protects investors from poorly diversified portfolios, ensuring prudent investment before retirement to avoid excessive risk exposure. Supporters argue it shields pension funds from high-risk ventures, though critics suggest it limits long-term returns. Recent adjustments to Regulation 28 provide more flexibility to expat investors, but is it sufficient?

“In simpler terms, South Africa’s Equity market currently equates to roughly 1.05% of the global market.”

Regulation 28 applies to approved funds like pensions, provident plans, preservation, and retirement annuities, regulating their allocation across asset classes including equities, property, and foreign investments. Approved funds meet SARS criteria under the Income Tax Act.

Current Limits

Recent updates to Regulation 28 raised the cap on foreign asset exposure to 45%, allowing expat investors to diversify globally. This shift enables exploration of offshore opportunities beyond South Africa’s market limitations:

• 75% in equities (local and foreign)

• 25% in property

• 15% in private equity

• 10% in commodities

• 10% in hedge funds

• 2.5% in other excluded assets

Additionally, no more than 25% of fund assets can be in any single entity.

Regulation 28 amendments prohibit investments in cryptocurrencies due to their volatility and lack of regulation. Retirement fund trustees have a fiduciary duty to the fund and its members, and exposing retirement fund assets to cryptocurrencies is not considered in the best interest of fund members.

Although the offshore limit has been increased to 45%, 55% of retirement fund capital must be invested in South African assets. This can be challenging given the shrinking number of listed companies on the JSE, limiting local investment choices.

The JSE (Johannesburg Stock Exchange) currently has 442 listed companies. With a total market cap (all the companies share value combined) of $1.3 Trillion USD – when comparing this to the global market cap (total global equity market) – which at the time of writing this - currently stands at $123.5 Trillion USD.

In simpler terms, South Africa’s Equity market currently equates to roughly 1.05% of the global market, yet South African based Equity Retirement Funds generally hold 45-60% allocation to this 1.05%. In keeping with the 55% regulated allocation to SA assets.

If we look at the sector analysis of South African companies, the vast majority of the equity is comprised of financial based companies (97 total), think Standard Bank, Investec and Capitec. Industrials (46 companies) – Bidvest and Barloworld. And, finally Commodity based “Basic Materials” companies (45 total) – Anglo American, BHP and Glencore.

Traditionally, these can be volatile sectors when considering global economics, fluctuating material prices and interest rates, all the while facing the challenge of an ever increasingly turbulent ZAR valuation.

Over the last 15+ years we have witnessed the domination of US focused tech companies, most recently, Nvidia, but not excluding the other superpowers of The States such as Amazon, Apple and Alphabet (Google). These sectors have been the driving force of portfolios globally for more than a decade.

With Section 28 amendments increasing the available allocation to international equities, is it still enough? Surely limiting investors to ‘keep things in house’ in SA, an emerging market with numerous social, political and economic issues, we are still enforcing a restriction in how South African nationals, expat or not, can manage their future.

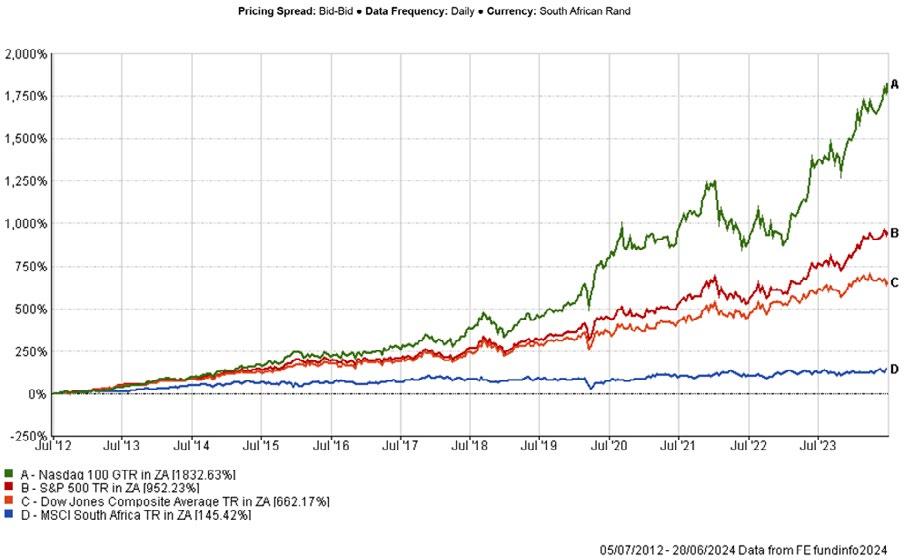

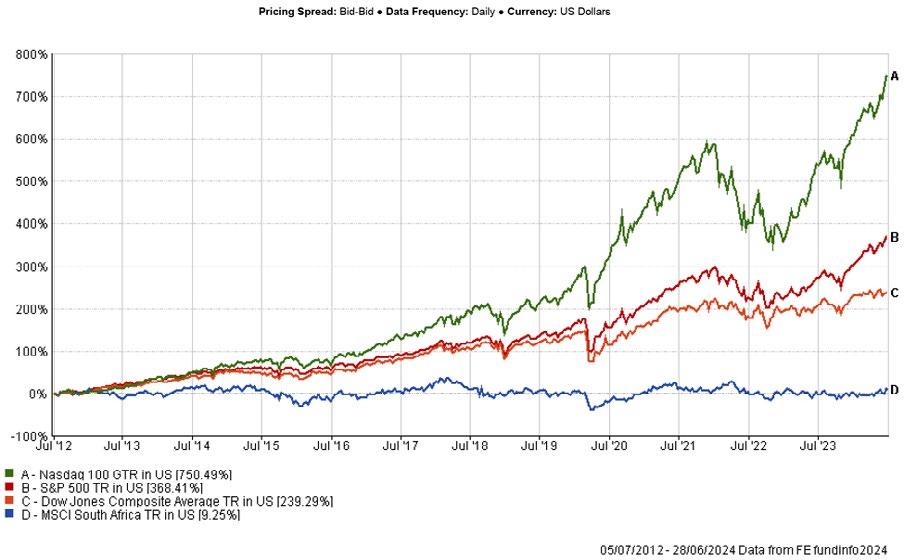

These two charts below, one reporting in USD and the other in ZAR, shows the relative growth rate of major US indexes in comparison the total South African equity market.

Firstly, in ZAR.

In the last 20 years, in relative ZAR terms, the South African Equity market has grown by +145.42% - fantastic right?

In comparison, the most diverse US index, the S&P500 has achieved relative growth of 952.23%. This includes both the devaluation of the ZAR in comparison to the USD but also the exponential growth of US listed companies.

“Over the last 15+ years we have witnessed the domination of US focused tech companies, most recently, Nvidia...”

Critics suggest early withdrawal to invest in diversified portfolios with greater offshore exposure. However, you must consider significant tax implications and fees associated with early retirement fund withdrawals.

Christopher Bowler and Skybound Wealth Management specialize in guiding South African expats through offshore investment strategies. Expats can explore flexible investment and currency options for optimal growth and tax efficiency.

For personalized advice on managing your assets and exploring offshore investment opportunities, arrange a complimentary consultation with Christopher Bowler and the Skybound Wealth Management team today.

Why Choose Skybound Wealth Insurance?

• Comprehensive coverage for expats and their families

• Tailored policies that fit your lifestyle, whether home or abroad

• Peace of mind with flexible life, health, and critical illness cover

• Expert advice to ensure your loved ones are fully protected ACT NOW

Safeguard your future today—speak to an adviser about a bespoke insurance plan.

Scan the QR code code or click here to request your free quote.

Or contact your Skybound Wealth Financial Adviser today.

Written by Ben Stockton

Imagine that a critical employee in your business suddenly becomes incapacitated or passes away, leaving your company reeling from the loss of their skills and expertise. Would your business be able to survive?

For expatriate business owners, this is a crucial question. That’s where a key man insurance policy comes into play. Ben Stockton from Skybound Wealth Management highlights the importance of this strategy and other essential protections for expat business owners.

Running a business as an expatriate comes with its own set of challenges and risks. Two vital strategies to mitigate these risks and ensure the stability and continuity of your business are Key Man Insurance and Shareholder Protection. Here’s why these are essential considerations for expatriate business owners.

Key Man Insurance is a life insurance policy taken out by a business on its most valuable employees— the “key” individuals whose loss would significantly impact the company’s operations. These individuals could be founders, executives, top salespeople, or anyone whose expertise, skills, or reputation are crucial to the business’s success.

Financial Stability in Times of Crisis

The death or incapacitation of a key person can lead to financial instability. Key Man Insurance provides a financial cushion, ensuring the business has the resources to continue operations, recruit a replacement, or cover lost revenue.

Ensuring Business Continuity with Key Man Insurance

It ensures the smooth running of business operations during the transition period after losing a key person, which is vital for maintaining business stability.

Enhancing Creditworthiness for Your Expat Business

Banks and investors often view businesses with Key Man Insurance more favourably, as it indicates prudent risk management and enhances the company’s creditworthiness.