Have Navigating Shipping Fortunes Ever Been Harder?

“Geopolitics, wars, pandemics, financial crises, and regulation have all buffeted shipping over the past 10 years”

—Andy Dacy managing director of the global transportation group at JP Morgan Asset Management

“I’ve rarely seen a year start with more uncertainty”

—Tim Huxley, CEO of Mandarin Shipping

“Regulatory pressures remain a dominant factor shaping operations”

— Emanuele Grimaldi, chairman of the International Chamber of Shipping

“We are not very optimistic for 2025”

— Torbjorn Gjervik, CEO of Western Bulk Chartering

“The shipping industry spends a much smaller portion of its operating costs on training”

— Pradeep Chawla, CEO of

MarinePALS

The site for incisive, exclusive maritime news and views www.splash247.com

EDITORIAL DIRECTOR

Sam Chambers sam@asiashippingmedia.com

CORRESPONDENTS

Adis Adjin adis@asiashippingmedia.com

Bojan Lepic bojan@asiashippingmedia.com

All editorial material should be sent to sam@asiashippingmedia.com

COMMERCIAL DIRECTOR

Grant Rowles grant@asiashippingmedia.com

GENERAL MANAGER

Victor Halder victor@asiashippingmedia.com

Advertising agents are also based in Tokyo, Seoul and Oslo – to contact a local agent please email grant@ asiashippingmedia.com for details.

MEDIA KITS ARE AVAILABLE FOR DOWNLOAD AT WWW.SPLASH247.COM/ADVERTISING

All commercial material should be sent to grant@asiashippingmedia.com or mailed to Asia Shipping Media Pte Ltd, 30 Cecil Street, #19-08 Prudential Tower, Singapore 049712

Although every effort has been made to ensure that the information contained in this review is correct, the publishers accept no liability for any inaccuracies or omissions that may occur. All rights reserved. No part of the publication may be reproduced, stored in retrieval systems or transmitted in any form or by any means without prior written permission of the copyright owner. For reprints of specific articles contact grant@asiashippingmedia.com.

The coming decade

While this magazine is focused on what to expect in the year ahead, we’ve also got another project looking at ship operations further down the line.

Is life at sea set to become easier, safer, and cheaper to manage? That’s sort of the angle posed by 14 questions set by our team alongside our friends at Inmarsat in a new survey seeking reader input on how ship operations will change in the coming decade with results due to be published in Ship Concept 2035, another Splash magazine due for distribution at NorShipping this June.

The questionnaire essentially asks you to ponder how technologies – and by extension, operations – will have evolved onboard by the year 2035?

Ship Concept 2035 will give readers a glimpse of what is realistic for newbuilds coming out of yards 10 years from now with advice from experts in the know from across the world. Taking into account regulations, fuels, information technology, seafaring skills, shipyards and charterers this unique magazine gives a big picture beyond the hype of what is practical for vessels delivering by the middle of the next decade.

Crew numbers, artificial intelligence, bunker selection, reskilling, and automation are some of the topics covered in the survey.

To have your say takes as little as two minutes to vote, and there is no registration required. To vote, follow this QR code.

Ship Concept 2035 Survey

Sam Chambers Editor Splash

The non-boring twenties

Mid-way through the decade, and shipping is proving an industry not for the faint-hearted

Splash turned 10 in March, the site covering one of shipping’s most tumultuous decades on record.

Chinese shipyards going under or restructuring and capes heading for the scrap heap dominated headlines on March 4, 2015 in what was by common consent a far easier time to be covering the shipping and offshore industries, a period where supply and demand statistics were easier to gauge and geopolitics did not weigh so heavily on the sector’s fortunes.

Tim Wilkins, the managing director of INTERTANKO, recounts: “Back in 2015, the industry’s challenges seemed more clearly defined. Issues such as security threats and reducing greenhouse gas emissions were distinct focus areas with well-outlined solutions.”

Wilkins says the “complexity” and sheer volume of challenges have grown significantly, most notably thanks to geopolitics.

“The key change is in shipping’s risk profile: 10 years ago shipping risk was all about safety, oil spills, piracy and ISPS; shipping risk today is about ESG, geopolitics and sanctions,” says Mark Williams, the founder of UK consultancy Shipping Strategy, adding: “The costs

The industry has had to become more transparent

of compliance have risen fast but the costs of non-compliance have risen enormously and can even be existential.”

Michael Grey, one of the most famous editors of shipping titles over the past 50 years, commented on Splash’s anniversary: “It’s been 10 years of huge and increasing challenges to be faced, arising from the green agenda – right or wrong – peak globalisation now facing its own existential threats and growing political instability.”

The news cycle – and by extension shipping cycles – have accelerated and shortened since Splash was created, a viewpoint picked up by Andy Dacy, managing director of the global transportation group at JP Morgan Asset Management.

“Geopolitics, wars, pandemics, financial crises, and regulation have all buffeted shipping over the past 10 years. We’ve seen more of these in a shorter time span than before,” Dacy says.

Discussing the past decade’s “seismic shifts” for shipping, Bjorn Hojgaard, who heads up Anglo-Eastern, the world’s largest shipmanger, says decarbonisation, digitalisation, and

geopolitical changes have rewritten the rulebook.

“The industry has had to become more transparent, more accountable, and more technologically agile than ever before,” Hojgaard says.

Nick Brown, the CEO of Lloyd’s Register, concedes that global trade has been tested by an extraordinary set of challenges over the past decade, listing the likes of the pandemic, sanctions, tariffs, and war, all of which, he says have exposed vulnerabilities in the supply chain and highlight the vital yet under-recognised role of seafarers.

“As we navigate the turbulent waters of today’s world, we must do so with a firm grasp of the challenges facing individual sectors, the industry as a whole, and the broader economic and geopolitical forces at play,” says Emanuele Grimaldi, the chairman of the International Chamber of Shipping. “To succeed, we must ensure that our industry functions in ways that allow us to meet sustainability targets, reap the benefits of technological advancement, and keep trade flowing uninterrupted –even in turbulent waters.”

Navigating EU ETS and FuelEU Maritime

As a global leader in maritime solutions, the Synergy Marine Group is committed to helping shipowners navigate the complexities of the EU Emissions Trading System and FuelEU Maritime regulations. Our expertise in technical management, digitalisation and sustainable ship management practices ensures that your fleet remains compliant and efficient in an ever-evolving regulatory landscape.

Through our innovative decarbonisation arm, Azolla, we offer cutting-edge solutions to reduce greenhouse gas emissions and enhance fuel efficiency. By integrating advanced technologies and sustainable practices, Azolla helps clients achieve their environmental targets while maintaining operational excellence.

Join us in shaping green shipping.

Discover more about our innovative solutions and sustainability efforts:

• Compliance with EU ETS and FuelEU Maritime

• Technical Management Expertise

• Advanced Digital Solutions

• Sustainable Ship Management Practices

Fleet growth

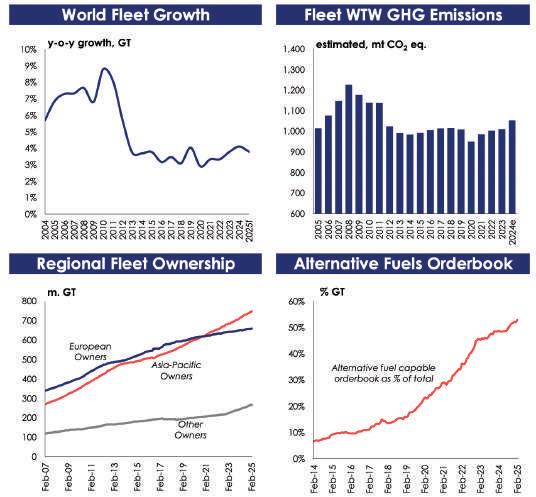

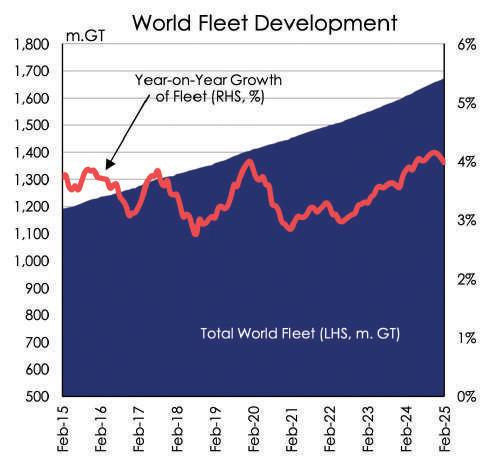

In the past 10 years, according to Dr Martin Stopford, the world’s most famous maritime economist, the shipping fleet in dwt terms has grown by a third, and earnings are up by about 40%.

Regionally, the epicentre of sea trade has continued its move towards the Pacific. In 2015 Atlantic and Pacific seaborne trade – including imports and exports – were roughly the same – about 45% each. Now the Pacific is about 50%, and the Atlantic about 40%, according to data from Stopford.

China’s share of shipbuilding has jumped from 36% to 51% in the period since Splash started, but sea trade growth has slowed to 1.8% per annum, half the long-term trend of 3-4% per year.

Shipping is necessary due to fundamental geographical dislocations between cargo demand and supply. Exacerbate these via geopolitical tensions and shipping demand, more often than not, goes up.

We can see this in the premium in growth observed for ship demand, incorporating cargo volumes and distances, versus the standalone cargo element, in the 2010s and the 2020s. According to data from Maritime Strategies International, the annual

The next decade will determine the shape of the industry’s long-term sustainability

average difference in growth between ship demand and cargo volumes over the period 2020-2024, has seen ship demand increase by about double the rate of cargo growth on average across the tanker, dry bulk, container, and LNG sectors compared with the period 20102019.

Green transition?

Dr Roar Adland, who heads up research at broker SSY, says of the period since Splash’s debut: “It was the decade when Chinese demand growth finally decelerated, geopolitical drivers came back with a vengeance and the green transition in shipping turned out to be what we all suspected – all talk and no action.”

Guy Platten, secretary-general of the International Chamber of Shipping, hails shipping’s “remarkable transformation” over the past decade, driving progress, resilience, and sustainability on a global scale. Platten takes issue with Adland’s take on the industry’s decarbonisation, claiming shipping is now at the forefront of the energy transition and several steps ahead of regulators.

Johannah Christensen, head of the not-for-profit Global Maritime Forum, agrees with Platten, maintaining that the industry has moved over the past 10 years from being a green laggard to a frontrunner among the hard-to-abate sector.

Among other key changes experienced in the past 10 years has been the global sulphur cap, and the growing regulatory requirements on compliance.

Also of importance, as highlighted by Mikael Skov, who heads up Hafnia, the world’s largest product tanker owner, has been the the entrance – and exit – of private equity in shipping.

Brown, the head of LR, argues that during this time of complex challenges, the sector has reached a turning point in its energy transition, developing a broader shift towards multifuel solutions.

“The next decade will determine the shape of the industry’s longterm sustainability, demanding not just technological advancements but also greater investment in seafarers and human capital, which remain fundamental to creating the long-term change we need,” Brown says.

Can these two men find some middle ground to keep world trade moving?

Shipowners and charterers have little idea what next bombshell out of the White House will impact their businesses

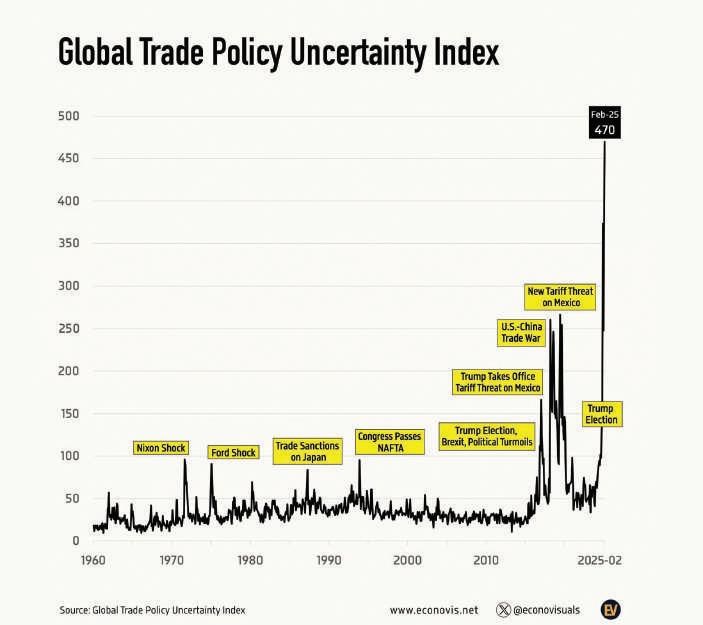

Economists have been left flabbergasted by the opening months of Donald Trump’s return to power in the US, the international rulebook torn up, policies raining in and often being rescinded by the hour. Making a call on how the global economy plays out in the coming months has rarely been more tricky, or down to the whims of one man.

At no point since tracking began on the subject have global trade policies been more uncertain than right now, according to one index developed in the US.

The Trade Policy Uncertainty (TPU) Index developed by four employees at the Federal Reserve Board analyses the frequency of joint occurrences of trade policy and uncertainty terms in major newspapers, firms’ earnings conference calls, and aggregate data on tariff rates in a way that is similar to existing volatility indices in mainstream financial markets, spanning equities and derivatives.

Since Donald Trump returned to the White House on January 20, the index, which goes back to 1960, has spiked to record levels, twice as high as previous peaks registered during Trump’s first term in office.

A paper submitted by the creators of the TPU index documents that increases in trade policy uncertainty reduce investment and activity using both firmlevel and aggregate data.

Trump’s first months back in the White House have dominated shipping headlines for tariffs, a push for peace in Ukraine, a renewed ‘maximum pressure’ strategy on Iran, the creation of a National Energy Dominance Council, and a planned tax on Chinese-built tonnage calling US ports.

The war of tariffs is beginning to make

Credit: FMT

I’ve rarely seen a year start with more uncertainty

its way into the macroeconomic forecasts.

As an example, Goldman Sachs just revised their US Q4 2025 GDP growth downwards from 2.2% to 1.7% whilst at the same time increasing their likelihood for a US recession within 12 months from 15% to 20%.

“As the Trump 2.0 reality show unfolds, as it does daily, often with singular market-moving tweets, we might as well suspend trying to make credible forecasts of future supplydemand balance across shipping sectors. Underwhelming spot earnings render shipping sentiment downbeat while we seek greater clarity on today’s geopolitical, trade and social threats,” notes a recent report from broker Hartland Shipping.

“I’ve rarely seen a year start with more uncertainty,” says Tim Huxley, the veteran

head of Hong Kong shipowner Mandarin Shipping, adding: “Both the US and China want to see growth and they will do everything they can to achieve that. A stronger domestic economy in China will probably see the target of 5% growth met. In the USA, tariffs could lead to inflation and that could preocupy the new administration.”

If shipping markets in the 2020s can be characterised by disruption, then the two decades prior could similarly be defined with one word – China.

Without the growth in Chinese demand for commodities, manufactured exports and shipbuilding capacity witnessed since the start of the millennium, the shipping world would be an entirely different place.

China’s demand has been a solid factor supporting shipping markets amid economic and political upheaval,

PARTNER.SHIP. REDEFINED. marlow-navigation.com

pandemic and war. But this drive was, at least initially, itself a disruptive factor.

The opening of China’s economy, often marked by the country’s accession to the WTO in the early 2000s, changed the shipping game. Since then, the industry has become in large part dependent on ever-expanding Chinese demand.

For large oil tankers and dry bulk

carriers, this is put in stark relief when we consider that Chinese imports of crude oil and iron ore do not just constitute the majority of global incremental import growth in these sectors over the period 2000-2024. Due in part to declines elsewhere, they exceed it.

Could this era of expansion go into reverse? In Maritime Strategies

International’s view, the answer is yes.

There are structural shifts in China’s economy, MSI analysts point out, which will reduce demand for some of the major commodity types it will import. Perhaps the two of the most important of these trends are reduced rates of urbanisation and increased vehicle electrification.

John Michael Radziwill, a high profile owner who chairs Monaco-based C Transport Maritime, concedes that China has domestic challenges to its economy that it must address or risk slowing growth and internal discontent.

“We see the Chinese government as willing to drip feed support without really enacting enough policies that could turnaround the situation quickly,” Radziwill tells Splash.

The full ramifications for how relations between China and the US, the world’s two largest economies, will develop between Trump and his counterpart, Xi Jinping, still remain unclear.

“While we are all kept guessing as to what Mr Trump has in mind for US-China relations, let’s consider the Chinese astrological Snake: it is wise, mysterious and thoughtful,” says Mark Williams, who heads up consultancy Shipping Strategy. “Snakes like big ideas and understanding how things work. In this Year of the Snake, we could all do with some of these characteristics if we are to come out the other side in better shape.”

Snakes like big ideas and understanding how things work

Stay ahead with what it is driving today’s Chinese shipping markets via our dedicated coverage

The regulatory year ahead

The 2020s were always going to be a decade where the welter of regulations would buffet shipping like never before. Nevertheless, the speed with which they are raining in this year and next has put many on notice that perhaps this is an industry to exit.

The decade’s regulatory changes began on day one with the global sulphur cap, also known as IMO2020, one of the largest regulatory adjustments in a generation, and a good heads-up of what was to follow.

This year started with FuelEU Maritime with experts warning the penalties the European Union could dish out could send some companies bankrupt.

The rules mandate stringent greenhouse gas (GHG) emission intensity requirements for ships over 5,000 gt transporting cargo or passengers for

commercial purposes in the EU. FuelEU Maritime compels shipowners, managers, and charterers to hasten the adoption of renewable and low-carbon fuels in their vessels’ operations. The FuelEU Maritime regulation includes several provisions that incentivise the use of onshore power supplies or alternative zero-emission technologies while ships are at berth.

The regulations aim to reduce the carbon intensity of bunker fuels used by ships calling at European Union ports, with a 2% reduction by 2025, followed by an exponential increase every five years – 6% by 2030, 14.5% by 2035, 31% by 2040, 62% by 2045, and 80% by 2050. GHG emissions are calculated from a well-to-wake perspective. In addition to emissions from onboard combustion, this calculation also includes emissions related to the extraction, cultivation, production, and transport of the fuel.

has had to become more

The regulation includes provisions for crediting ships using wind-assisted propulsion.

“The FuelEU Maritime regulation will significantly impact the shipping industry, even more so than the EU Emissions Trading System (EU ETS),” says Nicholas Fell, chair of BIMCO’s documentary committee.

Non-compliance with FuelEU Maritime will mean fines much higher than those incurred from the EU ETS, with a penalty of €2,400 ($2,536) per tonne VLFSO energy equivalent.

Clear signals needed

“Regulatory pressures remain a dominant factor shaping operations,” Emanuele Grimaldi, the chairman of the International Chamber of Shipping, tells Splash, adding: “They demand significant investment and innovation, something that requires clear signals from policymakers to enable businesses to

We help reduce your carbon footprint.

BSM‘s emission management services include:

• Enhancing vessel performance

• Ensuring compliance with CII, EU ETS, FuelEU Maritime and more

• Reducing OPEX and emission costs

Want to find out more? www.bs-shipmanagement.com/footprint

make the long-term investment decisions needed.”

“Geopolitics, wars, pandemics, financial crises, and regulation have all buffeted shipping over the past 10 years. We’ve seen more of these in a shorter time span than before,” says Andy Dacy, managing director of the global transportation group at JP Morgan Asset Management.

Bjorn Hojgaard, who heads up AngloEastern, the world’s largest shipmanger, reckons decarbonisation, digitalisation, and geopolitical changes have rewritten the rulebook.

“The industry has had to become more transparent, more accountable, and more technologically agile than ever before,” Hojgaard says.

April’s MEPC gathering

The 18th Intersessional Working Group on Greenhouse Gases (GHG) concluded in late February at the International Maritime Organization with the GHG levy in combination with a global fuel standard as the most favoured candidate mid-term measure for reducing GHG emissions from shipping.

Analysis of the participation at the

Regulatory pressures remain a dominant factor shaping operations

meeting carried out by UCL Energy Institute showed that 66% of MARPOL signatories now support a levy, which will be decided upon when member states meet up in April for the 83rd gathering of the Marine Environment Protection Committee (MEPC).

Other important regulations happening in 2025 include the International Maritime Organization’s Energy Efficiency Design Index (EEDI) Phase 3. Phase 3 requires a reduction of at least 30% compared with the initial baseline.

Elsewhere, from May 1, the Mediterranean will become an emissions control area while the following month sees the Hong Kong International Convention for the Safe and Environmentally Sound Recycling of Ships enter into force ensuring that ships, when recycled after reaching the end of their operational lives, do not pose unnecessary risks to human health, safety, or the environment.

Andrew Sillitoe, head of regulatory affairs at Lloyd’s Register, notes how around 10 years ago, IMO agreed that

SOLAS amendments should be packaged together to come into force once every four years, to help manage the flow of regulatory change and its impact on industry.

“It’s probably fair to say that this wellintentioned change has been overtaken by events for shipping companies on the receiving end of changes across all of IMO’s conventions,” he says.

Trump to the fore

Beyond the IMO, regional requirements are undeniably high-impact this year and directly driving the day-to-day and strategic decisions of shipowners and operators keeping their fleet compliant and competitive, something that is being felt all of a sudden in the US where Donald Trump’s return to the White House has seen tariffs, and a planned tax on Chinese-built tonnage calling at American ports rock the industry.

If 2025 looks like a busy one on the regulatory agenda, a glance at what’s incoming for 2026 looks daunting.

Red Sea and red ink

Of all shipping sectors, predicting liner fortunes in the Trump 2.0 era is the hardest by some distance

The opening months of 2025 have been marked by a continuous decline in container spot rates, yet more orders being placed, and a constant stream of newbuilds entering service.

As of the end of February, the overall Shanghai Containerized Freight Index (SCFI) comprehensive index was down 40% compared to the peak in the first week of January 2025. However, it is 47% higher than before the beginning of the Red Sea crisis, but lower than at any point during 2024.

For context it should also be noted that the current level is still higher than at any point in the 10 years before the pandemic, except for a few brief weeks in October 2009.

“Carriers face an uphill battle to reverse the recent rate slide with cargo volumes still muted after the strong January cargo rush that had set new throughput records at key ports,” consultants at Linerlytica noted in a recent market report.

However, there is cause for some optimism, helping to explain why carriers

continue to order new ships in such huge numbers.

A recent report from freight rate platform Xeneta indicates that long-term container freight rates are on the rise, with seven out of nine major fronthaul routes experiencing increases compared to contracts from a year ago. Despite these gains, new long-term rates are still lagging behind spot market levels.

“The fact that longer-term contracts are securing solid rates should provide operators with greater confidence for a more stable market outlook over the long run,” broker Braemar noted.

As neatly surmised by Maersk in its annual report published in February, liner profits in 2025 are on a knife edge, largely out of the carriers’ control - what happens in the Middle East ought to dictate the difference between red and black ink. But then, this is the 2020s, the decade that has kept on giving unexpected bonuses for liner shipping, whether it be the pandemic, or canal closures, or, quite possibly, Donald Trump.

Maersk reported its third-best financial year ever in February with an EBIT for 2024 of $6.5bn. The Danish carrier forecasted global container volume growth in 2025 will be around 4%. However, the very big dividing line between profit and loss this year, according to Maersk, will centre around the Red Sea.

The Houthis of Yemen have put their campaign against merchant shipping on hold, with no attacks reported in 2025 so far, as Israel and Hamas take steps toward peace. The situation remains tense however with very few liners returning to take the Suez route between Asia and Europe.

Maersk’s EBIT forecast for 2025 ranges from zero to $3bn, depending on whether the Red Sea opens in the middle of the year or the end of the year. The company added its outlook for 2025 is subject to “considerable macroeconomic uncertainties” impacting container volume growth and freight rates.

Suez Canal transits last year for the container sector as a whole were down

MOMENTUM WHERE IT MATTERS

Building from a one-country operation at the Port of Manila in the Philippines, ICTSI has pressed forward across 36 years. On six continents, currently in 19 countries, we continue developing ports that deliver transformative benefits.

All across our operations, we work closely with our business and government partners, with our clients and host communities: to keep building momentum where it matters, in and through ports that keep driving sustainable growth.

ARGENTINA AUSTRALIA BRAZIL CAMEROON CHINA COLOMBIA DR CONGO CROATIA ECUADOR GEORGIA HONDURAS IRAQ INDONESIA

MADAGASCAR

MEXICO

NIGERIA

PAPUA

PHILIPPINES

POLAND

90% from 2023, according to data from Jefferies, an investment bank.

The main economic impact of the Red Sea routes’ potential reopening would be to return capacity to the container shipping system, equivalent to around 6% to 8% of existing vessels due to faster sailing, according to data from S&P Global. At the same time, new container vessels adding nearly 24% of new capacity are coming, launching over the next three years.

“Container shipping faces the headwinds of a large orderbook being delivered, the potential impact of trade wars and tariffs, and increased capacity being available through the hoped for cessation of Houthi hostilities and a return to normal Suez operation,” says Tim Huxley, who runs Hong Kong shipowner Mandarin Shipping. “The past few years have provided plenty of surprises that have avoided any pronounced downturn, so we might

The past few years have provided plenty of surprises that have avoided any pronounced downturn

get lucky again,” he says with a hint of optimism.

How seriously tariffs alter trade flows has been brought into question. Tariffs have been a feature of Trump’s first administration as well as by his successor, Joe Biden and yet data from Linerlytica shows loaded container imports into the US outpaced exports by 2.4 times in 2024, a statistic that analysts at Linerlytica said in a weekly report provides “clear evidence that import tariffs imposed since 2018 have been completely ineffective” in reducing the US trade imbalance.

Total laden imports grew by 24% between 2017 and 2024, the Linerlytica data shows, while laden exports shrunk by 8% over the same period, driving a 54% increase in the number of empty containers repositioned out of the US.

There’s then the potential issue of proposed US fees on China-built containerships importing goods into the US, something that may have unintended

consequences, including port congestion, increasing freight rates and shifts in global trade patterns.

“Ocean container carriers will take action to avoid the fees, such as calling at fewer ports, which could cause major congestion and delays in the US,” says Peter Sand, chief analyst at Xeneta.

The global fully cellular container ship fleet is now 30.65m teu while the orderbook has breached the 9m teu level. Deliveries this year so far total more than 300,000 teu. Liner companies can point to the trend in freight rates during the 2020s: earnings per teu have far surpassed expectations even as the fleet has grown by a quarter in five years.

“Overall, we expect liners to remain profitable in 1H 2025, but the underlying demand-supply balance points to a prolonged downcycle for container shipping beyond the current situation,” warned HSBC in a report from early March.

Unrivalled

Mirroring 2023?

The opening months of this year suggest rates could follow the path of the year before last

After a typically sluggish start in the opening couple of months of the year, there have been signs that dry bulk markets – led by capes –are picking up finally. 2025 to date is replaying 2023 which started weakly but ended strongly.

Alexis Ellender, the lead analyst covering dry bulk for Kpler, says a seasonal improvement in cargo availability should support a firming in dry bulk markets come Q2.

Ellender is bullish on the outlook for Brazilian soybean exports, forecasting shipments to be up near 3% year-onyear in Q2. Higher vessel demand, plus associated port congestion, should boost panamax/kamsarmax earnings, he says.

As for cape rates, while expecting them to be firmer in Q2, Ellender says earnings will likely be more in the region they were back in 2023, not last year.

There are downside risks to the demand outlook for geared vessels, Ellender warns. China and India are expected to import less seaborne coal this year than last, with a drop of around 60m tonnes year-on-year anticipated across the two countries combined, Kpler is

forecasting.

Meanwhile tariffs and trade barriers are set to slow the trade in steel products, Ellender cautions. Both of these would hit Pacific demand hardest, with Indonesia coal and Chinese steel product shipments likely to be affected.

“We are not very optimistic for 2025, especially in the first half and especially in the sub-cape sector,” says Torbjorn Gjervik, the CEO of Western Bulk Chartering.

Supply growth will outpace demand growth by a margin, Gjervik reckons as the orderbook has grown significantly, and tonne-mile-adjusted demand lacks the support it had from a disrupted Panama Canal in the first half of 2024. A potential normalisation of the Suez Canal traffic is also weighing in as a potential negative factor later on this year, he warns.

John Michael Radziwill, a high profile owner who heads up Monaco-based C Transport Maritime, agrees with his Norwegian counterpart, anticipating softening rates for much of 2025 with the panamax and supramax sectors being more impacted as they have higher fleet

growth in the range of 3.5% to 4.5% against demand growth that he expects to be quite flat or only slightly accelerating. Capes have a better supply picture, he argues, with very limited growth which will help them navigate 2025 better.

Bauxite

China’s remarkable thirst for bauxite to manufacture aluminium has helped prop up cape rates considerably in recent years. Now for the first time, the capesize fleet was seen carrying more bauxite than coal at the start of the year, according to broker Arrow.

China imported 159m tonnes of bauxite last year, up by 18m tonnes over 2023’s total, with 77% of all shipments carried out on capes, according to AXS data.

Volumes from Guinea have surged, whilst panamaxes have been cannibalising capesize coal cargoes “Infrastructure improvements in West Africa, led by Guinea and including Ivory Coast, Sierra Leone, and Ghana, are expected to drive further increases

in supply for the seaborne market, and especially supply for China,” predicted broker BRS who is forecasting exports of the mined product from West Africa to China to increase by another 20m tonnes this year.

“Beijing’s continuous promotion of the ‘New Three’ (namely electric vehicles, lithium batteries, and solar panels) is significantly boosting the demand for aluminium products,” BRS pointed out.

“Considering the longer voyage distances, the bauxite market is expected to exert an increasing influence on the capesize segment via heightened volatility in the fronthaul route,” BRS maintained.

Slowing down

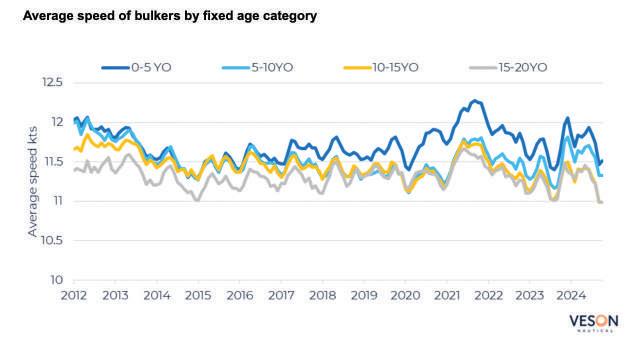

The global bulker fleet is facing a significant slowdown, driven by a combination of factors that are not only causing a decline in average speeds, but also setting the stage for the emergence of what analysts at Veson Nautical believe is a two-tier market.

The impact of an ageing fleet in the era of efficiency means that ageing vessels, stricter emissions regulations, and evolving market dynamics are all factors in the lower average speeds being witnessed.

A recent report from Veson Nautical cited data that suggests that older vessels, particularly those built before the Energy Efficiency Design Index (EEDI) criteria was enforced in 2013, have seen a noticeable decrease in speeds, relative to newer vessels and that this is the single largest contributory factor to the slowdown of the global bulker fleet.

“We can conclude that a surplus of older, inefficient vessels in the fleet, which are now penalised by efficiency regulations for sailing at higher speeds, are a driving factor in declining average speed overall,” said report author Oliver Kirkham, senior valuation analyst at Veson Nautical. “However, the decline in average speeds is not just a matter of operational efficiency; it’s a sign of a deeper shift in the bulker market, where modern, compliant vessels are set to command a premium as older ships struggle to keep pace.”

The report added that the massive

Ageing vessels will be pushed into niche markets while newer vessels will dominate more profitable routes

expansion of the bulker fleet during the mid-2000s, spurred by China’s economic growth, has left a large portion of the fleet increasingly inefficient. These vessels are now struggling to meet modern efficiency standards, creating a growing divide between newer, more efficient vessels and older ships that are nearing the end of their operational lives.

“The difference in terms of efficiency between new bulker vessels and vessels even from five years ago is significant as improved design, fuel efficiency and compliance with green regulations really start to make an impact,” Kirkham said. “These modern vessels are expected to command a premium especially in markets such as the US and Europe that have stringent age restrictions and carbon regulations.”

The report concluded that a declining number of transactions of modern bulker vessels in the sales and purchase market is evidence that new bulker vessels are providing commercial advantage and emissions compliance which enables owners to command a premium for their charter. However, some markets are still open to ageing

vessels, especially when transporting cargoes with negligible time constraints.

“As emissions regulations continue to tighten globally it is clear that ageing vessels will be pushed into niche markets while newer vessels will dominate more profitable routes,” Kirkham maintained.

“However, the shipping industry as a whole is currently lacking a standardised and transparent system to offer precise and conclusive proof of a vessels’ fuel and carbon efficiency, and this will need to be resolved as the market evolves.”

Getting older

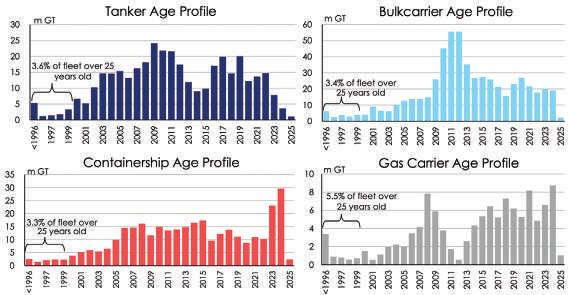

A year is a long time in shipping as new data on global fleet ages clearly shows.

Greek broker Xclusiv Shipbrokers has some sobering statistics on the growing vintage state of the global dry bulk fleet.

As of today, 13% of the total bulk carrier fleet is aged 21 years old or older, a 12% increase compared to the similar period of 2024. The 16 to 20-year-old age dry bulk group now accounts for 16% of the total bulk carrier fleet, a huge 29% increase compared to January 2024.

In rude health

Changes in trade flows ought to be constructive for VLCCs

Why could 2025 be a banner year for hauling oil?

The tanker sector entered 2025 on a high note, with predictions of a healthy outlook. However, a number of challenges have surfaced that may cause uncertainty and impact future market dynamics.

The gradual easing of Red Sea-related trade flow shifts, the complexities stemming from the impact of US and EU sanctions on trade activities and charter rates and a push for peace in Ukraine have been identified as some of the factors that are likely to influence the direction of the tanker market in the near term.

The Houthi group in Yemen has pledged to halt attacks on shipping should the ceasefire in Gaza hold, which may result in the return of tanker transits across the Red Sea region, affecting seaborne trade patterns and lowering tanker tonne-mile demand.

In January, the US issued a fresh list of 180 sanctioned vessels involved in the

Russian oil trade, the largest to date. This was followed by what was described as “maximum pressure” campaign against Iran in a bid to reduce its oil exports, the majority of which went to China. The EU also applied further pressure on Russia’s shadow fleet, expanding the list of sanctioned ships to more than 150.

The US tariffs on China, Canada, and Mexico have also joined the list of various current issues impacting global trade. This, and avoiding sanctioned tankers has led China to import oil from other sources and along with Beijing’s retaliatory tariffs on US crude subsequently reshaped global trade flows. Traders and analysts expect more shipments from different regions in the future given the tariffs and risks and uncertainty over sanctioned oil.

Analysts at Gibson find that the tanker market outlook will very much be influenced by decisions made in the US and Moscow on ending the war in

Ukraine.

“How long this might take, and what that might look like remains unclear, but given how impactful the war has been for the tanker market, it is arguably the most critical factor impacting the mediumterm outlook,” the UK shipbroker said, adding that the rise of crude tanker tonne miles in the past two years was mostly attributed to the war in Ukraine, particularly in 2023.

Aframaxes, followed by suezmaxes, were the greatest beneficiaries of the conflict, while VLCCs lost market share due to Russian port restrictions. Nevertheless, VLCC owners see these new trade flow shifts from a positive side as the largest crude importer could seek shipments via the compliant fleet, boosting this segment.

Gibson notes that any increase in Indian or Chinese buying from outside Russia is likely to benefit VLCCs more than other sizes, given the cargoes are

Never again will change happen so slowly.

In a world where change is accelerating at such pace, there is only one course to take: be par t of that change.

As a stable actor in the shipping industry since 1872, we stand ready to face the future - together with you at all times.

likely to originate from the segment’s key markets in West Africa, the Americas, or the Middle East.

“We expect changes in trade flows to be constructive with the VLCC sector looking to be an asset class in high demand. This development comes at a time when the dynamics of our market increasingly are becoming a robust supply story, with a benign orderbook of new ships, a rapidly aging fleet and a string of sanctions making it increasingly challenging to trade ships in the shadow fleet,” VLCC specialist DHT said.

With challenges on the horizon, limited global crude tanker fleet expansion, expectations of accelerated oil supply growth in 2025 mostly out of the US, Guyana, Canada, and Brazil as well as the growing number of sanctioned

vessels, promise a good year for VLCCs.

Meanwhile, Teekay Tankers, whose fleet counts around 40 ships in the suezmax and aframax segment, reckons that at this stage it is difficult to predict how all these factors will unfold during 2025, what their impact will be on the tanker market, or if there will be additional geopolitical events. However, the company said that: “Geopolitical uncertainty, and changes to seaborne oil trade patterns, typically lead to increased tanker market volatility.”

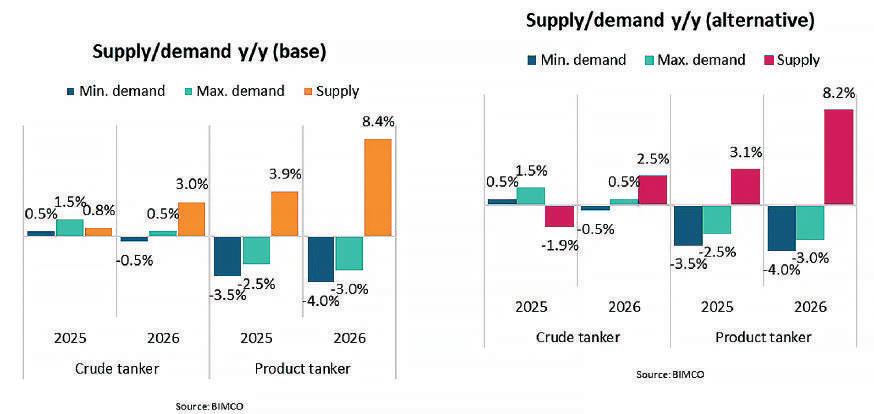

In its latest tanker market outlook, BIMCO forecasts crude tanker tonne miles demand growth of 0.5-1.5% in 2025 and between -0.5% and 0.5% in 2026.

“Expectations for greater volumes support demand but shorter sailing

distances due to the assumed return to the Red Sea and Suez Canal routings temper tonne miles growth,” the world’s largest shipping association said.

The crude tanker supply is estimated to grow 0.8% in 2025 and 3.0% in 2026. BIMCO’s alternative scenario, however, assumes that if sanctioned ships leave the active fleet, it will further lower the supply growth.

Claire Grierson, head of tanker research at shipbroker SSY, finds that other broader factors that will direct the tanker market include slowing growth in global oil consumption, the OPEC+ crude supply, increasing non-OPEC Atlantic crude production, refinery closures in Europe and the US, as well as rising tanker deliveries in the products segment.

Our staff experience covers some 80 bulk vessels ranging in size from small multipurpose bulkers through Handysize, Supramax, Ultramax, Panamax to Capesize vessels trading regionally and worldwide

Our newbuild team project experience is based on various shipping and offshore newbuild projects over a 7 year track record

Our staff experience covers some 30 vessels ranging in size from 1,100teu to 3,500teu, geared and gearless, reefer fitted, running on intensive scheduled services regionally within Asia, North/South America, Europe, Australia and New Zealand

Our staff experience includes full management of STS/Lightering vessel / Terminal for eight years Offloading Capesize, Panamax and Ultramax vessels with the industrial high-cycling Tsuji cranes, then transferring from storage holds via EMS-TECH high spread conveyor and 75meter boom to shallow draft tug & barge trains

Our staff experience covers some 26 units including Dive/ROV Support vessels, AHTS, Heavy Lift Shear Leg barges, Jack-ups, Drillships, SemiSubmersible Drilling units and FSO projects

Our staff experience covers several RoRo, Pure Car Carrier and RoPax vessels supported by long experienced colleagues in Europe, China and Japan, RoRo and RoPax sectors

Not so productive

Why we ought to be cautious about product tanker sentiment in the months ahead

As the US moves to broker a peace deal between Russia and Ukraine and tanker owners wait for clarity to emerge before fully digesting the ramifications for the market, various industry experts began the year anticipating a less-than-rosy outlook for the products sector earnings compared to 2024.

Prior to further geopolitical tensions, most of this came on the back of the tonnage influx the sector is about to experience in the coming years.

Deliveries of newbuild product tankers will hit a 16-year high in 2025, according to international shipping organisation BIMCO. 2025 will see about 12m dwt delivered, up 256% compared to last year’s deliveries, and the second highest on record, chief shipping analyst at BIMCO Niels Rasmussen noted. Numbers vary, but around 150 new vessels dominated by MRs and LR2s are set to enter the market.

BIMCO expects product tanker supply growth to be 3.9% in 2025 and 8.4% in 2026.

“Challenges such as tonnage supply growth and the impact of newbuild programs commencing the second half -2025 are key factors to monitor,” says Mikael Skov, chief executive of product tanker giant Hafnia, adding that although the company believes 2025 holds strong potential for profitability, several factors beyond its control will influence market sentiment.

“Newbuilding delivery schedules have a degree of predictability attached, but we can’t predict the market,” points out Mark Cameron, executive vice president and chief operating officer at product tankers specialist Ardmore - in addition to the sector overlap of the bigger size vessels encroaching into smaller size vessel trades.

Analysts at Drewry believe that the

Deliveries of newbuild product tankers will hit a 16-year high in 2025

resolution of geopolitical issues is the biggest wildcard for product tanker earnings, which was supported by tight tonnage amid stretched voyages last year.

“A resolution of the Red Sea crisis will restore the transit via the conventional Suez Canal route, negatively impacting product tanker tonne-miles and putting pressure on rates, given recent fleet expansion,” Drewry noted ahead of the Gaza ceasefire deal in January, and that any disruption to traffic transiting the Strait of Hormuz would also have serious consequences for the product tanker market.

For BIMCO, the gradual return to normal routings would see product tanker tonne miles fall between -3.5% and -2.5% in 2025, followed by a further fall of between -4% and - 3% in 2026.

As for the market movements, lower product tanker export volumes from Japan, South Korea and Europe are expected, countered by export growth from the Middle East. Imports to Europe are projected to slow down but increase in Asia.

A potential end of the Russia-Ukraine conflict is also one of the key factors that could switch trade patterns back to short-haul routes, softening rates.

The impact of peace in Ukraine could be arguably more significant than for the crude sector, Gibson stressed. LR2s and MRs witnessed the strongest increase in tonne miles as Europe sought to replace Russian supplies in 2023 with cargoes from the Middle East, India, the Far East and the US, while Russian products found new markets in Latin America,

Africa and Asia.

In the event that Russian supplies return to Europe, analysts estimate MRs will face less harm from reversing trade flows since they may be redeployed on Russian trades, while MRs in the US Gulf will regain some market share in Latin America.

However, for LR2s it is difficult to find a positive outlook, Gibson warned, noting that Europe’s imports from East of Suez would also decline, with LR2s on the losing end.

SSY’s Grierson outlined that scrapping could pick up if older ships come under pressure from the newbuilding arrivals, the increased sanctions and regulatory changes.

“Rising EU ETS costs and the introduction of FuelEU may favour modern ships on some routes, while the Mediterranean will introduce an Emission Control Area (ECA),” she said.

Hafnia’s Skov agrees that decarbonisation initiatives and stricter environmental regulations will likely phase out older and less efficient vessels, however, warns that the simultaneous growth of the dark fleet “could offset these reductions”.

For Ardmore’s Cameron, whether you are a “black swan or pink flamingo pragmatist”, the Trump presidency will have some impact on global trade flows and thereby breed a level of unpredictability with it.

“You can read any number of different outlooks depending on what you want to be influenced by, but I do think AI will help us, provided you ask the right questions,” he asserts.

The US is expected to add the largest new production volumes in 2025

Has the LNG sector passed rock bottom?

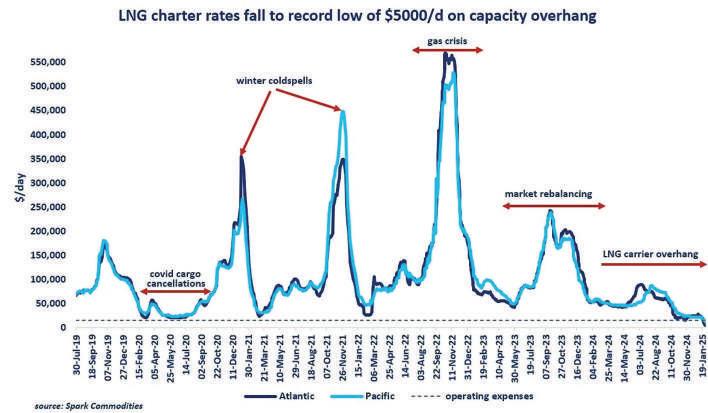

No shipping sector has started 2025 more bleakly than LNG with rates for some older tonnage even entering negative territory for the first time ever. Maritime CEO assesses if the gas shipping segment has bottomed out

No deep dive into any industry or sector should start with a downer. However, there are no two ways about it – the LNG shipping sector has been in freefall of late and nothing earth-shattering has happened in the first two months of this year to convince people that it will improve drastically. But, there might be some normalisation, if not recovery, on the horizon if certain factors align properly.

First, the situation is bleak. According to Clarksons’ weekly report from February 21, LNG carrier spot rates are still close to record lows which were seen at the beginning of the month.

The average spot rate assessment for a 174,000 cu m unit increased to $9,250 per day which is down 83% from the 2024 average. This means that you can hire a 174,000 unit for 10 days and still pay less than one night for the most

expensive hotel room in Las Vegas.

On their own, albeit bad, these numbers only provide the real picture when put into context. In November 2023, LNG spot rates were in the $200,000 per day region just to fall to an average of $50,000 per day in 2024. The nosedive is even more emphatic if we look at the daily rates in 2022 which went easily over $500,000 at a certain point.

So, now that the numbers painted a grim image it is important to understand why are these things happening and how is any of this going to get better. And, most importantly, when.

The growth of the LNG fleet far outpaced the growth in LNG trade in 2024 which took a toll on charter rates. This was not even fully offset by the need for longer journeys as the Suez Canal was almost unusable due to the

permanent threat of Houthi attacks. In 2024, 62 new LNG vessels were delivered to operators while another 68 orders were placed during the year.

At the beginning of this year, several new vessels hit the water and capacity overhang increased, resulting in rates dropping to historic lows. These drops also mean that many vessels are sailing at rates below the operating expense of LNG vessels estimated at around $15,000 per day.

UK consultancy Drewry reported that 96 more LNG carriers are scheduled to be delivered next year, aggravating the oversupply situation, which is also a cause for concern.

They also believe that most shippers will continue to avoid the Suez Canal and go around the Cape of Good Hope which will partially improve the situation. However, if the truce in Gaza lasts and

Houthis refrain from attacking vessels and keep the Red Sea calm, a return to the Suez could put even more pressure on already weak rates.

Another issue could be a possible escalation in the Iran-Israel conflict and the closing of the Strait of Hormuz. Regional exports, which account for 21% of the global LNG supply, could be blocked.

But it is not all bad. Even though this year will be a tough one by all accounts, experts do agree it will be at least stable. The UP World LNG Shipping Index (UPI), which comprises 19 companies and partnerships worldwide and represents around two-thirds of the world’s LNG carrier fleet, said in a recent report that the future of LNG shipping is, in a word, optimistic.

“LNG is now a crucial global commodity, and its importance is still rising. The third wave of development is now running, but the construction of new liquefied capacities is a bit late. On the other hand, the shipbuilders are on time, so the vessels are oversupplied now,” the report stated.

They predict that a near rise of capacity in Qatar and other countries will add about 200m tonnes per annum and that shipping companies will be prepared for this rise. UPI also emphasised that that was not the case in the second wave of development. However, experts are pointing out that this would have more results from 2026-2028 than any immediate impact.

Malaysia’s top shipping line, MISC,

revealed a similar prediction in its latest financial report where it said that LNG rates are expected to remain soft in 2025 driven by the continued influx of new vessels and delays in additional supply from new LNG liquefaction projects. However, it expects LNG rates to recover post-2026, driven by the gradual increase in LNG supply as the delayed projects become operational.

In 2025, an additional 42m tonnes per annum of new capacity will enter the fray but Drewry believes that it would be insufficient to balance the fleet growth.

The US is expected to add the largest new production volumes in 2025, with the start of key projects such as Plaquemines LNG with 13.3m tonnes per annum, and Corpus Christi LNG Phase 3 with 10m tonnes per annum while Canada LNG will contribute another 13m tonnes per annum.

There is also a political side to this. US president Donald Trump lifted a moratorium on new US licenses to export LNG, making good on his campaign promise. Former president Joe Biden banned LNG export licensing in January 2024, but a federal judge lifted the freeze in July last year.

There was a catch though. The Energy Department was not required to approve permits and no permit was granted until mid-February when Trump’s administration awarded a conditional export authorisation for the 9.5m tonnes per annum Commonwealth LNG project in Louisiana.

This also enables other multi-billion-

dollar export projects like Venture Global’s Calcasieu Pass LNG project and Energy Transfer’s Lake Charles LNG to apply for export permits and continue development. Trump’s re-election will probably see final investment decisions for US projects accelerate towards the second half of 2025 and peak in 2026. If we add to this Trump’s desire to increase oil and gas drilling, LNG might be one of the sectors to profit from the current US administration.

Steam LNG carriers are also a considerable problem and need scrapping to restore the supply-demand balance. Most of them are on old long-term contracts and as soon the charters of the steamships are finished, they will become uncompetitive. Scrapping of these vessels has already begun on a very small scale but Drewry believes that between 30 and 40 carriers must be scrapped to balance the fleet and stabilise rates.

LNG is now a crucial global commodity, and its importance is still rising, according to UPI. This year may be challenging for spot rates but if no significant geopolitical changes occur, they expect to see improvements by the end of 2025.

Drewry on the other hand expects a boost in Asian LNG demand next year that will further improve US-Asia trade, with the Cape of Good Hope still being the preferred route. These two factors, the consultancy believes, will act as a “silver lining” for LNG shipping, but will probably be insufficient to absorb the newly built vessels.

The dawn of the roboship

What will be the big tech breakthroughs shipping can expect soon?

We create soft ware solutions for the shipping industry to optimize vessel performance and voyage planning in order to maximize profit and minimize CO2 emissions.

Coach Solutions is created by Danish naval architects and commercial shipping experts, who together with highly skilled soft ware engineers work on making shipping smarter.

For Mikael Skov, who heads up Hafnia, the world’s largest product tanker owner, artificial intelligence, emissions reduction and autonomous vessels are likely going to be the biggest tech breakthroughs in general in the industry due to their direct impact on both operational costs and environmental sustainability.

“These advancements are not only technologically disruptive but also essential in addressing global challenges like climate change and maritime safety,” Skov tells Splash.

AI is not just optimising routes or scheduling but actively driving carbon footprint reductions, he says. The potential to cut annual emissions through AI-powered navigation optimisation is a “game-changer”, aligning with global sustainability goals. By integrating with carbon-neutral initiatives, shipping companies can meet stringent environmental regulations while lowering costs, he maintains.

The maritime industry must first address underlying challenges such as data standardisation, cybersecurity risks, and the need for skilled personnel

“One of the significant trends in 2025 and beyond will likely be the integration of AI into the day-to-day operations of vessels,” says Tim Ponath, CEO of German owner NSB Group, a company that like Hafnia is carrying out various pilot projects in this area.

“Most tech decisions and investments will focus on AI’s potential, including vessel hardware,” says Arthur English, CEO of Norwegian shipowner G2 Ocean.

It’s not just owners interviewed for this magazine who see AI’s growing importance. AI is seen by Splash readers as the technology having the most significant impact on maritime operations in the coming 10 years in an ongoing survey being carried out in association with Inmarsat.

AI beat out other tech making plenty of shipping headlines such as blockchain, Big Data analytics and Internet of Things in the survey that seeks to identify how ships will operate 10 years from now.

“While AI presents huge opportunities, the maritime industry must first address underlying challenges such as data standardisation, cybersecurity risks, and the need for skilled personnel to manage AI-driven systems,” urges Niall Jack, director of product development at software provider Shipnet.

The industry must fully embrace digital transformation – not just AI solutions – by investing in high-quality data infrastructure and cultural shifts toward digitisation, Jack argues.

“Overpromising AI’s capabilities without resolving these foundational challenges may lead to suboptimal implementations and rejection of further new developments because of this,” Jack says.

Beyond all the AI hype, Christian Råe Holm, the CEO of software provider Coach Solutions, cautions: “There is still a lot of talk around AI and machine learning, but apart from optimising

manual internal processes, I do not see it replacing expert human advisory yet. Rather, I see the need for human expert support as even more important with the advent of AI, as it takes deep knowledge to see through the sometimes doubtful results coming out of the black box.”

Proactive maintenance

“In 2025, technological advancements will continue to shape the industry, with AI maintaining its prominence as market-ready solutions for predictive maintenance,” says Vikrant Gusain, CEO of Dockendale Ship Management, who points out that proactive maintenance technologies, such as drones, reduce the need for enclosed space entries, improving safety standards.

Additionally, Gusain reckons sensor-

Overpromising

AI’s capabilities without resolving foundational challenges may lead to suboptimal implementations

based monitoring of emissions will gain traction, driven by the EU emissions trading system (EU ETS), as the industry intensifies efforts to ensure regulatory compliance.

Blockchain adoption is something else Hafnia’s Skov reckons will accelerate this year, offering the promise of a tamper-proof, transparent, and decentralised systems that can revolutionise how shipping contracts, payments, and cargo tracking are handled. If widely adopted, blockchain could eliminate inefficiencies, reduce fraud, and foster greater trust across the global supply chain.

Internet of Things (IoT) is also evolving from basic tracking to realtime, end-to-end visibility of the supply chain, improving reliability and customer experience.

With all the increased availability and flow of data brought about by the likes of Starlink over the past year, cyber security measures will call for much more attention in the year to come, says Morten Lind-Olsen, the CEO of Norwegian software firm Dualog, who also warns about the “huge gap” between management expectations to what can be done and what is in place on the IT integration side.

“We believe that digitalisation remains a dominant trend in the maritime industry while areas relevant to cybersecurity are important to ensure operations are conducted under a safe environment,” says Niraj Nanda, chief commercial officer at shipmanager Anglo-Eastern. “New technologies will continue to evolve alongside increased connectivity to allow safer and more How do you see ships evolving in

efficient operations.”

Green tech

Haakon Lenz, the new CEO at Wilhelmsen Ship Management, has been following the development of ammonia engines with great interest. A first ammonia dual-fuel engine may be delivered this year, something Lenz is eagerly looking out for.

“If safety risks are addressed, this technology has the potential to revolutionise the maritime industry’s journey toward decarbonisation,” Lenz maintains.

Shipping spends a much smaller portion of its operating costs on training

Mark Cameron, chief operating officer at Ardmore Shipping, thinks wind will start to put forward some better qualified validation figures this year. Installations are now starting to provide some qualified data to help interpret specific routes, times of the year and vessel types.

Cameron describes himself as a “net believer” in wind assist but reckons there are still too many variables.

“Data will help to qualify reality versus beliefs,” Cameron says, suggesting the different types of wind assist technology will begin to delineate into different markets and price points as experience matures.

Hull coatings are also back in vogue, Cameron reckons, while Andrew Airey, head of Thai manager Highland Maritime, believes we will see continued advances in carbon capture solutions for existing vessels as retrofitting carbon capture systems will, he says, become mandatory in the near future for most existing and new vessels still using fossil fuels.

“The quicker government and private sector drive the incentive and investment in the necessary shore-based recycling plants the quicker we can all cut emissions by 80%, almost overnight,” Airey says.

Splash has all the latest ship

news here

Celebrating 10 years of incisive, exclusive maritime news and views

This year will see fewer but better hires in commercial shipping

Paul Ratcliffe provides readers with highlights from Ignition Global’s latest commercial shipping leaders survey

Hiring in commercial shipping should be getting easier. The talent war of 2021–22 has ended, and dry bulk bonuses are cooling. Inflation has eased, remuneration policies have adjusted, and salary expectations have mellowed—making compensation easier to manage. And yet 40% of leaders say hiring is harder than ever.

Why? Because the challenge isn’t just about filling roles anymore. It’s about making the right hires in an industry that’s transforming faster than ever.

For the first time, shipping leaders say finding people with the right attitude is harder than finding technical skills.

A chartering director put it bluntly to me the other day: “I can teach a smart hire the market. I can’t teach them to stop waiting for an email and actually pick up the phone.”

Many leaders are trying to hire younger versions of themselves. Those professionals exist, but they are few and far between—and likely to have already been moulded in another company’s culture.

Junior hires will never join as the finished article. The best young professionals need training, coaching,

and investment. If you want them to succeed, you have to develop them— attitude and skills.

Hiring a ‘safe’ candidate is often a smart move—but sticking to the same talent strategy just because it’s familiar is a risk. In an industry undergoing regulatory, technological, and commercial transformation, firms that don’t adapt will be left behind.

Permanent hiring is more selective and interim specialists are on the rise. In this market, every hiring decision matters more.

With dry bulk struggling, tankers coming off a high, and gas and container facing a wave of newbuilds, firms are becoming more cost-conscious about who they hire.

We’re seeing a shift toward quality over quantity—fewer hires, but more strategic ones. Complementing the high calibre carefully selected future leaders, interim specialists are delivering critical expertise exactly when it’s needed.

Our survey shows widespread openness to interim hires for highly specialised roles including digitalisation, decarbonisation, and regulatory experts. We are also seeing more demand for

interim technical and commercial management leaders—companies looking for deep expertise without committing to a permanent hire.

In our survey, 86% of leaders believe AI will transform shipping in the next five years.

AI is changing what top performers bring to the table. The best people won’t be replaced. They’ll adapt and work differently.

AI-driven analytics will make decision-making more data-heavy— meaning firms need people who can interpret, challenge, and act on AI-driven insights.

Automation will reshape the skill sets needed in chartering, operations, and commercial decision-making.

The best hires will know the market, adapt to change, and keep learning to stay ahead.

Some firms are adapting— hiring fewer, but better people and supplementing their leadership teams with interim specialists. Others are waiting for things to go back to normal. They won’t. How companies hire today will determine who leads shipping tomorrow.

In tech we trust?

The relationship between shipowners and tech providers must be fixed to save shipping’s decarbonisation ambitions, writes WinGD’s Benny Hilström

Shipowners and operators need technology providers that keep their promises in order to avoid frustration, disruption and delay. That applies in day-to-day operations and is even more critical when promises are made around new technologies that require significant investments.

As someone who has worked on both sides of the technology provider/ shipowner relationship, I see worrying signs that this essential trust is being eroded – and putting commercial and environmental sustainability at risk. Our industry needs to move forward with bold decisions and commitments to our decarbonisation ambitions, but this can only happen from a foundation of trust.

As a shipowner, you spend upfront based on assurances of future performance. So when technology underperforms, is unreliable, or fails to meet initial claims, trust erodes. The problem is compounded when suppliers shift blame, revise earlier performance guarantees or deliver slow, costly resolutions. This undermines confidence not just in the technology but in the providers themselves.

This erosion of trust becomes even more significant when it comes to decarbonisation investments. With soaring stakes and mounting carbon costs, shipowners are hesitant to commit, often due to overpromised claims or technologies abandoned when challenges arise. This cycle of disappointment only slows decision-making, making it harder to take the bold steps needed.

No doubt, supplying innovative technologies is tough. Suppliers invest upfront in the solutions they think customers will need only to find the wind has changed – this fuel is out of fashion, that regulation throws a curveball, someone else has gotten there first. The pressure to go to market first and to sell in volume is enormous to recoup research and development spending,

including all those dead ends.

The trust of customers cannot be sacrificed to market pressures. Unlike consumer goods, maritime technology failures come with significant long-term costs. For the supplier, this means taking responsibility, delivering fast and costeffective solutions, and fostering genuine collaboration.

Meaningful partnership, mutual transparency and aligned interests are the key to a supplier-customer relationship in shipping. Those ideas are often touted but seldom deployed. Across my experience spanning both ship technology and shipowning, the partnerships maintained on this basis have been successful. Having the owner fully engaged from the very start –whether you are designing a new engine or trialling a new service concept –

happens to be the best way to deliver a solution the shipowner needs in a way the technology company can manage.

The technical challenges facing shipping are extreme as we grapple with climate ambitions, the optimisation potential of digitalisation and a trade outlook that is increasingly volatile. Even the biggest companies – including the ones I have worked for – cannot do it alone. Trusted partnerships are the only solution both to those challenges and to more successful day-to-day ship operations.

By prioritising trust and accountability, the industry can overcome technical challenges, optimise operations and realise its decarbonisation ambitions. Without it, the path to a sustainable maritime future remains in jeopardy.

What we can learn from aviation when it comes to all things digital

Julian Panter, the CEO of SmartSea, on why maritime must embrace digital transformation to stay afloat in the 21st century

The maritime industry is under threat of long-term risks such as operational inefficiencies and regulatory non-compliance due to some companies clinging to outdated and legacy practices.

A rapidly evolving technological landscape presents unprecedented opportunities as well as challenges for the maritime industry. While some companies are actively adopting digital solutions, many still remain hesitant to use newer and innovative technologies that have the potential to completely reshape operations.

Companies can also be slow to invest in new opportunities because they can struggle to see the overall picture past the initial investment cost. A study by McKinsey & Company* last year estimated that global shipping companies could reduce operational costs by as much as 15-25% through the implementation of digital technologies. While the initial investment in digital technologies may seem substantial, not just in terms of cost but also implementation, the long-term savings are undeniable.

For example, digitalisation streamlines complex maritime operations by automating manual processes and enabling real-time data analysis. Technologies such as the Internet of Things (IoT), Artificial Intelligence (AI), and blockchain are facilitating better fleet management, route optimisation, and cargo tracking. Companies like OneLink, for example, are already helping

and security solutions.

Predictive analytics can also forecast maintenance needs, reducing downtime and costs associated with unexpected equipment failures. Smart sensors on vessels provide real-time data about engine performance, fuel consumption, and weather conditions, allowing operators to make informed decisions that save time and resources. Additionally, AI-driven voyage optimisation leverages real-time data and machine learning to determine the most efficient routes, factoring in variables like weather patterns, sea currents, and port congestion, further enhancing operational efficiency.

Maritime is light years behind the aviation industry, and we really must not shy away from data sharing and sharing best practices to progress.

Digital transformation of the industry also has the potential to enhance workforce productivity and safety. By using tools like AI-driven voyage optimisation this not only minimises wastage and resource, it could also attract the seafarers of tomorrow, making the industry more appealing to a younger, technology-driven talent.

Added to this, the maritime industry is facing increasingly stringent environmental and safety regulations, such as the International Maritime Organisation’s (IMO) 2023 guidelines for carbon intensity reduction.

With the recent Fuel EU regulations now being implemented, advanced emissions monitoring systems, such as EmissionLink, can track and report their findings in real-time, helping companies comply with environmental standards. By resisting the advances in adopting a digital approach, companies could face some severe legal and financial liabilities. If this wasn’t proof enough of the value of integrating digital solutions to their business, companies that fail to integrate also risk losing vital market share to competitors. Early adopters of digital transformation are already reaping the benefits of improved operational efficiency, enhanced decision-making, and better customer experiences. Digitalised fleets and smart ports also outperform traditional systems in terms of cost, efficiency, and reliability.

The path to digital transformation is not without its challenges. It requires significant investment, a cultural shift within organisations, and a willingness to embrace change. However, the risks of not transforming far outweigh the costs of doing so.

The maritime industry really must embrace digital transformation to remain competitive and sustainable. SmartSea is powered by SITA, the global leader in technology for the air transport industry. Aviation is estimated to be 10-15 years ahead in terms of technology adoption. As such, the benefits of digital innovation are too significant to ignore.

numerous vessels with state-of-the-art shipping monitoring support services