As your business grows, so will your healthcare expenses. Customized captive insurance from QBE makes it easier to self-fund your employee healthcare coverage, allowing you to increase transparency and reduce the cost of risk.

Take advantage of QBE solutions like:

• The QBE Captive Curve solution model removes barriers to entry and allows you to move easily to new strategies.

• Agora, an open MSL group captive that makes it simpler to participate in a group program.

Together, we’ll find a solution so no matter what happens next, you can stay focused on your future.

TheTheralded “No Surprises Act” (NSA) became effective in January 2022, with intentions to protect consumers from an unexpected balance bill for the difference between what a provider charged and what their insurance paid. The law prohibits ‘surprise’ billing for some services, and led to the creation of the independent dispute resolution (IDR) process to resolve disputes about how much insurers should pay for out-of-network care.

NSA applies to several classes of out-of-network or otherwise noncontracted medical services, including:

Air ambulance services

Emergency services (except for ground ambulances)

Written By Laura Carabello

Services provided to stabilize a patient post-trauma

Out-of-network services at an in-network facility if the provider didn't notify the patient that the services were out-ofnetwork and obtain patient approval of the same

Administered by The Centers for Medicare & Medicaid Services (CMS), an agency within the Departments of Health and Human Services (HHS), the Federal IDR process represents a systematic way to negotiate payment amounts between providers and insurers. The parties must exhaust the 30-business-day open negotiation period before requesting payment determination through the Federal IDR Process. Both parties present their proposed payment amounts to a certified independent arbitrator, who then makes a binding decision to determine the final payment.

Nine states have adopted their own IDR processes to resolve out-of-network payments: Alaska, Georgia, Maine, Michigan, Nevada, New Jersey, New York, Virginia and Washington.

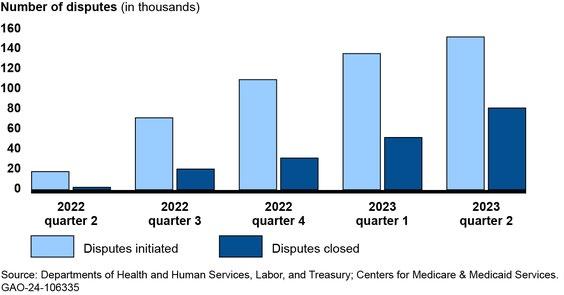

Few predicted the high demand for the federal IDR process, but it is contributing to claim delays, impacting provider cash flow and resulting in a mounting backlog of disputes. According to a December 2023 report from the U.S. Government Accountability Office, officials anticipated approximately 22,000 disputes in 2022. The volume of disputes far outpaced the estimate, with nearly 200,000 disputes initiated before the end of 2022 and another 670,000 submitted during 2023. Despite the fact that cases are getting resolved, the median time to resolve a case in the most recent reported period was 76

days — well above the statutory requirement of 30 days. By the end of 2023, the swollen backlog of disputes had left approximately 590,000 cases unresolved, resulting in delays in payment determinations.

Officials blame this bottleneck on the complexity of determining whether disputes are eligible for the process. The Commonwealth Fund reports that the IDR system continues to endure significant pressure from high caseloads, despite the fact that most claims never enter the IDR process.

Relief is on the way, contends the government agency within HHS that administers the IDR process, as well as new rules for 2025 recently announced by the Federal Hearings and Appeals Services (FHAS). These changes include: Additional Information Sharing, Open Negotiation Requirements, New Batching Provisions and Eligibility Determinations, Direct Administrative Fee Collection and Extending Time Periods Due to Extenuating Circumstances.

Many providers are now preparing for the new requirements, developing strategies and processes within their revenue cycle management to identify, track and dispute low payments from noncontracted payers. Providers feel it is inevitable that there will be lower reimbursement rates and delays in cash receipts as additional requirements and processes are established.

Number of Out-of-Network Disputes in the Federal Independent Dispute Resolution Process by Calendar Quarter, April 15, 2022—June 30, 2023

PASSAGE Safe

We deliver best-in-class solutions that cover your clients and support you with experts in data analytics, underwriting, claim reimbursements, dedicated account management and CompanionCARE SM

With CompanionCARE, you have access to experts in large case management and emerging therapies.

Our stop loss contracts are backed with the strength reflected in our A+ AM Best company rating.

In addition to specific and aggregate stop loss insurance, Companion Life offers an array of innovative products:

UNDERSTANDING THE IDR PROCESSES

Federal and State IDR programs are very similar, with the ultimate outcome measured in terms of benefits to the member (patient) and the provider. Depending on the insurance plan type, each case may follow Federal rules and be facilitated through the Federal portal. However, the case may be required to follow a different process defined by the state in which the health services were rendered.

Industry consultants counsel that states have the primary role in enforcing NSA rules against health providers, with the Federal government providing supplemental support as necessary. Consultants advise that even in states where consumers are covered by a federally regulated health plan, states remain the primary enforcer. Most states are familiar with NSA obligations, as 33 states independently implemented their own balanced-billing laws prior to NSA. New York State serves as an example of how the process works.

Bruce Roffe, CEO, H.H.C. Group, one of five companies that has been approved by New York State as a certified Independent Dispute Resolution Entity

(IDRE), explains, “New York's program is outside of the Federal program, although I’ve been told that the New York program was used as the model for the Federal program. The work that we perform for New York is fairly extensive because it involves so many different characteristics that we have to look at, including Fair Health data. It's not simply looking at the provider charges of $10 and the insurance company paid $2."

Fair Health is an independent, national nonprofit organization known for providing fair and neutral information. They base cost estimates on claims for medical and dental services paid for by private insurance plans, including the country's largest insurers. Their database includes more than 48 billion private health care claim records, and 45 billion Medicare claim records for 10,000 services in all areas of the United States, dating back to 2002. They receive about 2 billion new records each year and use powerful data to create a reliable picture of healthcare costs around the country and locally.

Bruce Roffe

IDR: What's Really Working?

“There are many factors that must be taken into account when performing an independent dispute review -- it's just not a clinical or financial review conducted line-by-line,” continues Roffe, noting that the IDR process in New York State is administered by the New York State Department of Financial Services (NYSDFS). “From what I've been told, the New York program was used as the model for the Federal program.”

Roffe maintains that the work required for the New York program is fairly extensive because it involves so many

different characteristics that need to be identified.

"Interestingly, New York is not backlogged like the Federal program," says Roffe. "If we are behind, it's just a week or two because nobody can really predict how much volume is going to come in over time."

He shares that sometimes when his team does this work, they will scratch their heads and ask themselves: How did the payer come up with their reimbursement rate? Where did they get this from anyway?

"I think the bottom line here is that it really is an objective assessment to determine if the insurance company paid enough or if the provider charged too much," adds Roffe. "I believe it's an objective assessment, and the person who really benefits from this is the patient because they can't be balanced billed."

In his experience, Roffe says that usually, about 49% of the time, the provider prevails, in 20% of the cases the payor wins and 31% are split decisions. Results in the Federal IDR process are somewhat

Protection and peace of mind with Wellpoint Stop Loss

Our highly experienced team can help you customize policies focused on cost control, administrative efficiency, and better employee outcomes.

• Faster reimbursement, with an advance funding option to help with cash flow concerns

• Lower claim costs, with a dedicated team to seek out cost-mitigation opportunities

To learn more about our stop loss offering, contact your WellPoint Stop Loss sales executive. What you can expect

• Solid protection with no surprises, so you can budget with confidence

• Industry leadership, as a top-5 stop loss carrier with our family of companies*

Better outcomes.

Long-term cost savings.

Mayo Clinic Complex Care Program

experienced a change in diagnosis

experienced a change in treatment plan

avoided a locally recommended surgery 23%

Discover how a customizable center of excellence program can help minimize healthcare costs while o ering high-cost, high-risk members exactly the care they need.

The Mayo Clinic Complex Care Program is for a small subset of a population with serious, complex or rare conditions who need subspecialized expertise that may not be available locally.

Learn more by calling 507-422-6103 or visit us online at mayoclinic.org/complex-care-program

comparable, as federal agencies report that providers, facilities, or air ambulance providers won about 77% of resolved cases, including a substantial subset of cases where only one party submitted an offer and paid the required fees.

"The New York program allows for a split decision, enabling the arbitrator to look at the bill line by line. Ultimately, it's usually the provider who prevails with the assumption contingent upon the provider supplying all the information necessary and enabling the IDR company to perform the assessment of the charges."

DOES THE PROCESS EVER FAIL?

“No, at least not for us -- we've never failed at it, and I honestly don't intend to," says Roffe. "There's no reason for us to fail since we have so many checks and balances built into this process. In New York, we are also obligated to send the case out to a physician in the same or similar specialty as the physician providing the service that is subject to the dispute. If we're looking at an orthopedic claim, then we'll send the claim to an orthopedic surgeon who's board-certified. If we're

looking at a neurosurgery claim, we'll send it to a neurosurgeon or neurologist."

He comments that when providers don't like the result, they complain.

“If they don’t complain, then we're not doing our job,” he remarks. “Providers might not like the result, but our determinations are evidence-based and built upon multiple factors that go into assessing a claim. Everything is in writing, including how the determination was made and why we selected one rate as opposed to another rate. It's a very laborintensive process that requires extensive training for reviewers."

Beyond RBP — The Power of Care Empowered Pricing

Control Costs with cutting-edge software and best-in-class plan language.

Protect Against Balance Bills with independent legal representation.

Own Your Program with support from industry-leading cost containment experts.

IDR: What's Really Working?

Roffe explains that gaining approval as an approved New York State IDRE required multiple layers of evaluation by the New York State Department of Financial Services,

"IDR work requires in-depth knowledge and understanding about healthcare costs, a capability that the Company developed because we deal with that every day on the cost containment side of our business," says Roffe. "We know about the clinical side of the healthcare environment because we address these issues on the Independent Review Organization side of our organization. Combined with our URAC accreditation, we were in a unique position."

LEGAL CHALLENGES

A federal appeals court states that the government overstepped its bounds when it attempted to dictate how certain factors should be weighed in an IDR process, leading the court to vacate parts of the rule. The 5th U.S. Circuit Court of Appeals ruling upholds a lower court decision in the case, Texas Medical Association et al. v. U.S. Department of Health and Human Services et al. According to reports, The TMA declined to comment on the decision or say whether it plans to appeal. Representatives for HHS and Labor departments also did not respond to requests for comment.

Christine Cooper, founder and CEO, aequum and chair of the Self-Insurance Institute of America, Inc. (SIIA) Price Transparency Committee, provides this guidance.

“The recent decision from the Fifth Circuit Court of Appeals was a big victory for self-funded health plans and insurers,” advises Cooper, who handles claims on behalf of plans. “Providers attacked the methodology for the calculation of the Qualifying Payment Amount (QPA), the median rate paid to in-network physicians, hospitals and others. They did not like that the calculation could include "ghost rates" and could not include single-case agreements, bonuses, retrospective payments or adjustments, or different provider specialties. Allowing and disallowing these items in the QPA calculation will allow for plans to calculate more favorable QPAs.”

Ghost rates are contracted rates that are present in contracts but are never negotiated or used. In healthcare, ghost rates can depress the

QPA for a service. For example, an orthopedic surgeon’s contract might include ghost rates for dermatology services that they never provide.

Cooper also expounds on the lack of compliance with the timelines set forth in the NSA, which she says has been rampant.

“One of the frustrations for plans is the failure of the IDR Entities to comply with their timelines,” she says. “The Fifth Circuit Court of Appeals decision addressed compliance with decision payment timelines. If extrapolated out, all timelines should be followed and this would help alleviate the backlog and the inconsistent decisions coming from the IDR Entities. Hopefully, the Courts will continue to follow this thinking and apply the statutory timelines to all of the key parties.”

One Think Tank, the Niskanen Center, comments on a concerning trend: the type of providers choosing to go to arbitration. They observe that approximately two-thirds of the initiating parties in cases going to arbitration are private equitybacked provider groups with a strong incentive to add revenue to pay down debt quickly and the resources to pay administrative fees and argue their case.

Cooper believes that a positive outcome of the NSA is the effect on some private equity-backed providers.

Christine Cooper

“Private equity's involvement in health care is generally perceived as bad for patients because of the potential for lower quality services and higher cost," she explains. "Private equity's main concern is financial returns on investment and does not seem like it should have a place in healthcare.”

The subject of private equity’s health care acquisitions is generating considerable attention, as Health Affairs recently examined the topic in depth. They point to discussions about their influence on the U.S. health care system and report that policy makers, especially at the state level, are exploring ways to regulate private-equity firms’ involvement in physician practices, hospitals, and nursing homes. Authors continue to question whether private equity’s role in health care is helpful or harmful to patients.

Cooper points to some private equity-backed providers who report taking a hit due to the NSA.

“For example, Envision Healthcare filed bankruptcy, citing the NSA as one of the reasons,” says Cooper. "Envision healthcare is one of the highest utilizers of the IDR process. Prior to the NSA, Envision Healthcare used surprise billing as part of its business model and advocated heavily against NSA enactment.”

“The statistics show that 82% of the decisions go in favor of providers,” she adds. “But that statistic may not be very meaningful since it would include arbitrations where the plans/ insurers do not participate or do not submit the requisite information.”

Eric Hanna, VP of Claim and Access Solutions at Vālenz® Health says that on the surface, the IDR process seems beneficial for members, providing protection against balance-billing and out-of-pocket costs.

“However, providers prevail in 70%+ of payment determinations with steep increases in percent-of-Medicare rates resulting from arbitration, incentivizing continued filings,” says Hanna. “These increases are unsustainable for selfinsured employers, ultimately forcing them to pass these costs to members.

Hanna emphasizes the importance of applying what has been learned from past IDR rulings to subsequent cases, ensuring that each decision point is addressed to increase the likelihood of favorable resolutions.

“While determinations are largely rules-based, we don’t discount the human element, acknowledging with arbitrators that the patients burdened by these crippling costs are parents, children, or siblings, each with their own individual struggles," he continues. “We also

encourage patients to approach healthcare decisions as consumers, with a proactive lens towards understanding their options to help reduce the impact on their wallets. With a model of health literacy and data-driven decision making, we strive to provide access to comprehensive cost and quality data, allowing members to make well-informed decisions about their care.”

THE COST OF WINNING

While providers prevail in most IDR cases, yielding them nearly three times the usual in-network rates offered by payers, the cost implications of these wins are significant.

Many providers still complain about the financial hardships they endure as a result of the NSA, particularly companies providing emergency services, such as physicians groups and air medical transportation companies. Multiple health care provider organizations cite the new law, along with higher costs of debt and unfavorable payer contracts, as contributing factors in their bankruptcy filings. As of November 2023, about 30 public companies named the NSA law as a potential risk to their financial performance.

Payer associations and advocacy organizations estimate that about 80 percent of 10 million out-ofnetwork claims in the first three quarters of 2023 saw initial

Eric Hanna

payments accepted by providers, and fewer than 7% went through IDR.

Original estimates from the Congressional Budget Office (CBO) projected that the NSA would trigger insurance premiums to fall by 0.5 to 1.0 percent. CBO’s estimate was based upon the assumption that the prevailing in-network rate would be a key benchmark for both payers’ initial offers to providers and arbitrators’ payment determinations.

But it appears that the current pattern of payment determinations might lead to higher provider rates in future plan–provider rate negotiations for in-network services. If this trend persists, CBO’s anticipated premium trend reduction may not be achieved.

As the outcomes of ongoing litigation and the reactions of stakeholders are heard, it will be interesting to gauge the cost-containment success of the NSA and IDR.

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com

Legislative/Regulatory Preview for 2025

Written By Chris Condeluci

NowNthat the 2024 elections are in the rear-view mirror, it’s time to look ahead to potential federal legislative/regulatory developments in the coming months.

HERE’S WHAT WE KNOW

We now know that Republicans will control all of Washington, DC, throughout 2025, with (1) Republicans holding on to the majority in the House of Representatives, (2) Republicans re-taking the majority in the Senate, and (3) Former President Trump being elected the 47th President.

We also know that the top 3 policy priorities for Republicans are Taxes, Energy, and Immigration/Border Security.

To get these 3 policy priorities into the law, we know Congressional Republicans are going to use an obscure legislative process called the “Reconciliation Process.”

HERE’S WHAT WE DON’T KNOW

Will Republicans be able to enact their top policy priorities of Taxes, Energy, and Immigration/Border Security into law by the end of 2025?

Will Republicans be able to find an agreement on how to fund the government through the rest of 2025 by March 14, 2025 (when the new deadline for funding the government will expire) without slowing down their efforts to enact their top policy priorities into law?

And will Republicans be able to raise the debt ceiling while also achieving spending reductions through things like entitlement reform (e.g., reforming Medicaid) and streamlining government bureaucracies (through the newly launched “Department of Government Efficiency” or “DOGE,” spear-headed by Elon Musk and Vivek Ramaswamy)?

THE UPCOMING SPENDING FIGHT

As 2024 was drawing to a close, Congress passed, and President Biden signed a short-term spending bill to fund the government through March 14, 2025. Getting the spending bill across the finish line – and avoiding a government shutdown – was not without its drama.

For example, President-elect Trump inserted himself into the debate by telling Congress that in addition to funding the government through 2025, Congress should also raise the debt ceiling so the incoming Trump Administration and Congress would not have to deal with the issue in 2025.

That suggestion was rejected by conservative House Republicans, so President-elect Trump and Republican Leadership had to settle for a “clean” spending bill that was devoid of other spending and nonspending priorities.

This sets up another battle over funding the government during the 1st Quarter of 2025, which will likely have an adverse impact on the speed with which Congressional Republicans will be able to enact legislation on Taxes, Energy, and Immigration/Border Security.

RAISING THE DEBT CEILING AND REDUCING GOVERNMENT SPENDING

Because Congress and the Trump Administration will have to agree on raising the debt ceiling at some point during 2025, the ensuing fight over this issue will also suck the oxygen out of Washington, DC, for a period of time. Conservative House Republicans are already on record

saying that they will refuse to raise the debt ceiling if significant spending reductions are not part of the deal.

This is where DOGE may have its greatest impact on policymaking, although questions remain about whether any recommendations on how to streamline the government and eliminate fraud, waste, and abuse can be memorialized in legislation that Congress can pass.

PASSING REPUBLICAN PRIORITIES THROUGH THE RECONCILIATION PROCESS

As stated, Republicans will have the opportunity to add their top policy priorities to the law through an obscure legislative process called the Reconciliation Process. The Reconciliation Process is an exception to the general rule of legislating in the Senate. Under the general rule, at least 60 votes are needed to pass legislation in the Senate. But legislation that is run through the Reconciliation Process (called a “reconciliation bill”) only requires 51 votes for passage.

However, to take advantage of this 51-vote exception, specific rules dictate what policy changes can be included in an underlying reconciliation bill and what cannot. The most important requirement is that a policy change must have a “direct” impact on (1) government spending or (2) tax revenue. If

Preview for 2025

a policy change has too “indirect” of an impact on spending or taxes, this policy must be removed from the reconciliation bill.

There is no question that Republicans will use the Reconciliation Process to pass an extension of the 2017 Tax Cuts and other tax policy changes promised on the campaign trail. These policies have a “direct” impact on taxes, so they can rightly be included in a reconciliation bill.

Republicans will also use the Reconciliation Process to pass Energy policy changes. Most Energy policies have been found to have a “direct” impact on spending. In addition, a lot of energy policy is run through the Tax Code (e.g., tax credits and even excise taxes), thereby having a “direct” impact on taxes, so these changes can also rightly be included in a reconciliation bill.

Immigration/Border Security, however, is something that will be difficult for Republicans to change through a reconciliation bill. This is because Immigration/Border Security has been found to have

too “indirect” of an impact on spending and taxes, and therefore, these changes cannot be included in a reconciliation bill. But that won’t stop Republicans from still trying.

WHAT ABOUT A HEALTH CARE RECONCILIATION BILL?

No one expects that Republicans will try to “repeal and replace” the Affordable Care Act (ACA) through the Reconciliation Process, but don’t be surprised if you hear certain Republican members of Congress calling for repeal and replace.

Preview for 2025

What most analysts expect is that Republicans will try to reform Medicaid by, for example, adding “work requirements” to Medicaid eligibility and also re-structuring how Medicaid is funded by the government (e.g., Federal “block grants” to States or a percapita spending cap on Medicaid enrollees).

Most also expect that House and Senate Republican Leadership will explore whether they should limit the tax preference for employer-sponsored health coverage (known as the “exclusion”).

Why? Because Republicans will need “offsets” to pay for

things like extending the 2017 Tax Cuts or reforming Medicaid, and limiting the exclusion raises billions of dollars in tax revenue for the government.

Note, efforts to limit the exclusion are not new: Democrats limited the exclusion – through the Cadillac Tax – which was included in the ACA, but ultimately repealed before ever taking effect.

TRUMP ADMINISTRATION REGULATIONS

The first Trump Administration developed regulations (the Hospital Transparency and Transparency in Coverage (TiC) Rules) requiring hospitals and healthcare payers to publicly disclose medical prices on a website through machine-readable files (MRFs).

While the current state of price transparency is still a bit murky – due to non-compliance with the Hospital Transparency Rule and insurance carriers unwilling or unable to disclose “usable” data on the required MRFs – expect a second Trump Administration to double-down on price transparency.

Here, expect regulations calling for increased penalties for noncompliance and routine audits of insurance carriers to make sure their pricing data can be easily consumed by employers, plan service providers, and researchers. Also expect improvements to the MRFs and required, specified methodologies for determining – and then disclosing – a particular price for a particular medical item or service.

Also, although Congress tried to require owners of the provider networks (i.e., insurance carriers) to share health claims data with sponsors of self-insured health plans (through the enactment of the Gag Clause Prohibition at the end of 2020), insurance carriers are still refusing to share the data. Expect the

Trump Administration to clarify how the Gag Clause Prohibition was originally intended to work and even force insurance carriers to share the claims data or face penalties or co-fiduciary liability.

Chris Condeluci serves as SIIA’s Washington Counsel.

NAVIGATING IN THE NEW AGE OF CYBERSECURITY THREATS

Written By Bruce Shutan

PanicPset in at 6 a.m. last July 8 when Phia Group, LLC CEO Adam Russo was contacted by his head of IT, who reported that the healthcare cost-containment firm had been hacked. “The first reaction I had was one of pure despair,” he recalls. “It’s a company I built from scratch. I didn’t know how long we’d be down or if clients would terminate our contracts because they were just nervous about potential liability and breaches down the road.”

His company quickly identified a serious cybersecurity threat and shut down all systems across the entire business within two hours of discovering the hack to limit any potential exposure from stolen data. Clients were immediately informed about the incident and the steps that were taken.

Of course, The Phia Group is not alone in experiencing such a breach. In the past year, 92% of healthcare organizations reported experiencing at least one cyberattack, which was up from 88% in 2023, according to a recent survey by Proofpoint and Ponemon Institute. Of those cyberattacks, 69% reported disruptions to patient care as a direct consequence. Ransomware attacks on this sector rose 128% in 2023, while the April 2024 attack on Change Healthcare compromised information on an estimated 100 million Americans.

Considerable damage has been wrought by large data breaches, which affected more than 167 million Americans in 2023 and set a new record. These large breaches caused by hacking and ransomware skyrocketed 89% and 102%, respectively, since 2019.

FINDING PHISHING EXPEDITIONS

One huge cybersecurity concern involves phishing, fraudulent emails that appear to be from a legitimate source whose aim is to trick the recipient into providing sensitive personal information that may include passwords or credit-card details by clicking on malicious links to download malware to steal data or money. Scores of employees

have been duped by this popular scam over the years as methods of deception have become increasingly sophisticated.

"They have become so realistic, looking exactly like you're getting emails from Amazon, FedEx, UPS or any of the major companies, especially during the winter holidays," observes Michael Carrara, CEO of Hi-Tech Health. "Someone may unknowingly click on one of these links, and next thing you know, your internal system and network is compromised.”

We Know ... Risk

We study it, research it, speak on it, share insights on it and pioneer new ways to manage it. With underwriters who have many years of experience as well as deep specialty and technical expertise, we’re proud to be known as experts in understanding risk. We continually search for fresh approaches, respond proactively to market changes, and bring new flexibility to our products. Our clients have been benefiting from our expertise for over 50 years. To be prepared for what tomorrow brings, contact us for all your medical stop loss and organ transplant needs.

His firm has a subscription to KnowBe4, which sends out emails with phishing-scam addresses that the company’s internal network is able to detect if employees click on deceptive content. Those random tests are done monthly all year long in addition to a security monitoring report that is reviewed on a weekly basis to detect malicious threats.

It didn't take long for Russo to realize the enormous scope of cybersecurity breaches. "You'd be shocked how sophisticated these criminal enterprises that do phishing are," Russo says. "They are international and earn billions of dollars. The Dark Web has these guys all over the place, and what they do is find just one little crack, and once they’re in, they could potentially have the ability to steal data files with personal health information or literally shut down every single thing in your company from your phone system to your network drives, backups, you name it.”

Amalgamated Life Insurance Company Medical Stop Loss Insurance— The Essential, Excess Insurance

What’s equally surprising is that it isn’t necessarily a random individual on the phone, he explains. It’s an entire industry, complete with a sophisticated call center that has its own hold music. “You’re given a number,” he adds. “They literally treat you as if you’re the client, even though they’re the ones who hacked into your system.”

RESPONSES INSIDE THE BELTWAY

Given that cybersecurity breaches are top of mind for businesses across all industries, legislative and regulatory changes are afoot to address such concerns. For example, the Health Infrastructure Security and Accountability Act,

Mike Carrara

S. 5182, introduced in the U.S. Senate in September and referred to the Committee on Finance, includes several important steps to strengthen healthcare cybersecurity. Chief among them: establishing minimum and enhanced standards as well as incident response and recovery plans, expanding risk analysis requirements, holding C-suite executives accountable for complying with security standards, conducting third-party and annual Health and Human Services audits, and funding rural and urban safety net hospitals to implement better cybersecurity practices.

In addition, the U.S. Department of Health and Human Services (HHS) recently proposed a rule that would modify the Health Insurance Portability and Accountability Act (HIPPA) to require health plans and healthcare clearinghouses, as well as most providers, their business associates and other third parties, to strengthen cybersecurity protections for individuals' protected health information.

In strengthening the cybersecurity of electronically protected health information, HHS notes that group health plan documents would need to be revised to comply with administrative, physical and technical safeguards.

“Payers were always subject to HIPAA security because they handle protected and electronic health information,” explains Greg Garcia, executive director of cyber security for the Health Sector Coordinating Council. “Much of the enhancement references what was published earlier this year as voluntary cyber performance goals, which are now moving to a mandatory status.” He says it’s difficult to predict how a second Trump term would handle enforcement of regulatory action such as this one, particularly as the public comment period was extended 60 days to March 7.

BREACH VS. INCIDENT

Meanwhile, one of the biggest challenges for businesses is determining the difference between a breach and an incident, according to Carrara. Whenever a cyber threat is brought to someone's attention, he says it's often classified as a breach. But if an email was sent internally with some personal health information, "it isn't really a breach," he explains. "It's an incident, and that's confusing to someone like me. When I hear the word breach, I panic, and usually, after troubleshooting, it's found not to be a breach."

There are several steps Carrara’s firm takes once a threat has been identified, which are part of incident-response policies. For example, he says the parties involved may need to be retrained to avoid certain pitfalls or encrypt emails with private health information.

Hi-Tech Health also contracts with a cybersecurity company called Secure Compliance Solutions LLC that filters every transaction that happens on company servers and produces a monthly report. If there are any intermittent or regular attacks that are registered on the server, he says “we might make changes to our firewall policies.”

Self-insured clients might compare their internal IT to what his company is doing and come up with their own set of best practices. Carrara notes that statistics on security flaws in software or hardware that have been assigned a unique identifier, known as Common Vulnerabilities and Exposures or CVEs, define the scope and critical nature of cyber threats in security reports, whether it’s Windows 11, a server, firewall, patch or something similar, and suggest corrective actions. Examples of less-critical vulnerabilities might involve older servers or software whose patches take a little longer to put in place.

Greg Garcia

Each year, attorneys provide Hi-Tech Health staffers updates on HIPPA rules and regulations, including schooling new employees on clean-desk policies and requirements designed to safeguard sensitive personal information that HIPAA places on third-party administrators (TPAs) as well as his own firm. TPAs and some health insurers use the Hi-Tech Health system to process group health insurance claims.

A related issue that’s likely to garner considerable attention is the role of artificial intelligence (AI) in creating more problems as much as solving them. “I think AI is going to present a lot of new challenges for both thieves and the good guys, particularly private information when AI has the ability to reach out and touch so many different sources and pull together that information,” Carrara notes.

His company is exploring AI use for internal customer service for education and training on how to use its proprietary claim system and other issues that don’t necessarily require using employee data or private health information.

PREPARATION BEGETS PROTECTION

As Russo unpacked his cybersecurity breach, he was surprised to learn that only about 10% to 20% of clients had a robust team in place that knew what to do, and most of the bigger companies had actually seen potential breaches on a daily basis.

"What I noticed was across our industry, it's a topic that's almost taboo because so many people don't want to talk about their experience. No one wants to say, 'yeah, we got breached,'" he says, adding that there's no standard checklist on how self-insured employers and their partners should identify and respond to a security breach or notify and communicate with clients.

The same applies to something as simple as deciphering how strong passwords should be and how often they need to be updated. “You got people who haven’t changed their password in three years, and then you have others who’ve chosen a sophisticated phrase with 20 characters, some numbers, letters and symbols,” he notes.

Ironically enough, preparing for a cybersecurity attack was one of Russo’s priorities when he was named chairman of SIIA’s board of directors in 2019. Little did he know at the time that those steps, which included devoting sessions to this emerging topic at the annual national conference, would benefit his own company five years later.

It also helps to have the right insurance coverage in place. For example, Phia Group had every imaginable policy prior to its cybersecurity breach that covered anything from cybersecurity and ransom threats to terrorism and hacking – even bribery. If not for those coverages, the company easily could have incurred several hundreds of thousands of dollars in expenses.

What’s critical is to quickly identify the perpetrator(s), suggests Russo. Some clients told him they work with vendors who experienced similar breaches that were not resolved for as many as six to nine months, whereas his firm had the right forensic team and processes in place to respond, investigate how the breach occurred and prevent it from happening again.

Many people don't realize that a lot of times, it could be an internal person whose need to pay off gambling debts or other personal problems make them susceptible to selling personal information, according to Russo. "So, you look at everything in your hiring process to avoid an inside job," he suggests. For example, reinforcing the need to establish stronger trust with new hires could mean not granting access or permission to certain information until they're on the job for a certain period of time.

One silver lining in the aftermath of his harrowing brush with a cybersecurity hack is how it elevated his company’s standing among prospective clients and

Adam Russo

partners. "We took what would be deemed a negative in our industry and actually have used it as a promotional marketing piece on how fast we were able to eradicate the threat and communicate to our clients," Russo says. "I was very proud of my team and how quickly we're able to identify, respond, and get things back online the way they used to be pre-incident."

Bruce Shutan is a Portland, Oregon-based freelance writer who has closely covered the employee benefits industry for more than 35 years.

EMPLOYERS SHOULD EXPECT GROWING FOCUS ON MALE FERTILITY BENEFITS

Written By Laura Carabello

OnceOa taboo subject relegated to whispers in the workplace, male infertility is now generating open discussion among employers and employees alike. While much attention gravitates toward the female experience, new research and medical insights highlight the significant role that men play in a couple’s family-forming journey. Infertility is common, affecting millions of couples worldwide, with some estimates that men contribute up to 50% of cases.

“Male reproductive health merits increased attention and greater understanding of the issues that impact male Infertility,” says David Adamson, MD, founder and CEO, ARC Fertility. “While either one or both of the partners may contribute to the reproductive challenges of the couple, male infertility, like female infertility, is a clinical diagnosis that can only be determined after formal assessment and testing. Approximately one-third of infertility is attributed to the

female partner, one-third attributed to the male partner, and onethird is caused by a combination of problems in both partners or is unexplained.”

According to the World Health Organization and the International Committee Monitoring Assisted Reproductive Technologies (ICMART), failure to get pregnant is defined as clinical infertility if pregnancy is not established after 12 months or more of regular unprotected sexual intercourse. Factors that impact male infertility include abnormal semen parameters or function; anatomical, endocrine, genetic, functional or immunological abnormalities of the reproductive system; chronic illness; and sexual conditions incompatible with the ability to deposit semen in the vagina.

“Male infertility is more common in environments with high levels of environmental pollution, including water contaminants, pesticides and herbicides,” explains Dr. Adamson. “Some recent population studies have suggested that sperm counts have been declining universally even though infertility has not been increasing substantially.” He points out that in at least half of male infertility cases, doctors cannot identify an exact cause. “

For the remaining cases, infertility is either due to male reproductive system functional or anatomic abnormalities, environmental, genetic or other identifiable factors,” explains Dr. Adamson. “Not all male infertility is permanent or untreatable, and it is not uncommon for men to treat infertility through one or a combination of actions.”

Do you aspire to be a published author?

We would like to invite you to share your insight and submit an article to The Self-Insurer! SIIA’s official magazine is distributed in a digital and print format to reach 10,000 readers all over the world.

The Self-Insurer has been delivering information to top-level executives in the self-insurance industry since 1984.

Articles or guideline inquires can be submitted to Editor at Editor@sipconline.net

The Self-Insurer also has advertising opportunties available. Please contact Shane Byars at sbyars@ sipconline.net for advertising information.

Common environmental causes of male infertility:

• Excess heat, for example due to the male’s occupation, such as truck drivers, welders, or firefighters, or habits, such as excessive use of the hot tub or tight clothing.

• Drugs, including certain antibiotics and prescription medicines, anabolic steroids, alcohol, and marijuana.

• Toxicants, such as pesticides, herbicides, heavy metals, lead, mercury, or paint

• Stress

• Excess exercise, including bicycling

• Chronic disease, such as anemia, malnutrition, cancer, neurological disease, or diabetes

• Dietary deficiencies, such as zinc, vitamin C, and folic acid

• Varicocele, a condition in which the veins enlarge inside the scrotum

• Diseases of the male genital tract, including infection, cancer, trauma, or retrograde ejaculation

• Surgery on the male genital tract, such as for the treatment of an undescended testicle, or hernia

• Obesity

Genetic Causes of Male Infertility

• Mutations inside the genes that determine the male sex, called the Y-chromosome

• Other irregular changes in the genes. For instance, some men have a condition called Klinefelter's XXY syndrome, in which they have an extra copy of the female-sex determining genes (the X chromosome)

• Hormonal issues, such as: diabetes, high levels of the milk-producing hormone prolactin, or problems with the hormone-producing organs like the thyroid or adrenal gland.

Source: 2024 ARC Fertility

Skyrocketing prices. Administrative challenges. Shock claims. Aging workforces. At Amwins Group Benefits, we’re here to answer the call. We provide solutions to help your clients manage costs and take care of their people. So whether you need a partner for the day-to-day or a problem solver for the complex, our goal is simple: whenever you think of group benefits, you think of us. We help you win.

UNDERSTANDING MALE INFERTILITY

While either one or both of the partners may contribute to the reproductive challenges of the couple, male infertility, like female infertility, is a clinical diagnosis that can only be determined after formal assessment and testing.

According to the American Urological Association, evaluation of the male is important to most appropriately direct therapy and is necessary to adequately determine the management of the patient and the couple. Without an adequate male partner workup, the female partner may pursue unnecessary, costly, timeconsuming, and invasive treatment options.

They advise that some male factor conditions are treatable with medical or surgical therapy, and others may require donor sperm or adoption, as appropriate. They emphasize that some conditions are life-threatening, while others have health and genetic implications for the patient and potential offspring.

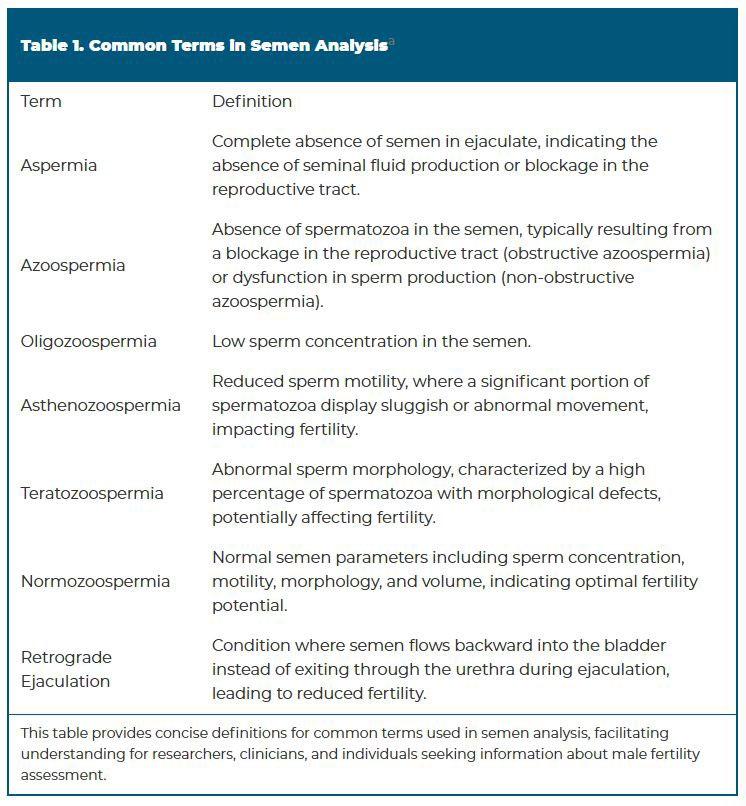

Male infertility is typically diagnosed by one or more factors that may include abnormal semen quality or sperm functional parameters; anatomical, endocrine, genetic, functional, or immunological abnormalities of the male reproductive system; or sexual conditions incompatible with the ability to deposit semen in the vagina.

The common terms of semen analysis (SA) are defined in the chart on the left.

Source: The Journal of Urology; https://www.auajournals.org/doi/10.1097JU.0000000000004180#:~:text=In%202023%20the%20 American%20Urological,partner%20in%20an%20infertile%20couple

University Hospital recommends that when selecting a men’s fertility doctor, individuals should try to see a urologist who has done specialty training in fertility. They explain that these doctors took one to two years after their urology training to learn specialized care for men with infertility. They also suggest that men invite their wives or partners to the appointment since “ pregnancy is a team sport, and this is an important process for both!”

Among the tips to prepare for a first appointment, clinicians advise men to bring all their medical records, including previous surgeries and a current medication list, as well as a wife/partner’s medical records, especially her workup or treatments for infertility.

The initial visit may be lengthy, beginning with a detailed medical history that goes back to childhood, including surgeries or conditions during childhood. Interestingly, many men have had surgeries as a baby that their parents never told them about, so they advise talking to parents to find out if anything was done. Also, inquire if there is a family history of fertility problems, as some of these issues could be passed down from generation to generation.

The doctor will also inquire about all medications and lifestyle habits, including smoking, alcohol and drug use – including the use of testosterone products or anabolic steroids, as these can affect fertility.

a Leading National TPA

Innovative solutions, built around you.

How we do it:

People

Specialized, in-house teams

Partnerships

Strategic point solutions

Programs

Full-service concierge and member advocacy

Technology

Next-generation navigation tools

Creating solutions for better healthcare outcomes is at the heart of everything we do.

That’s the HPI difference. hpiTPA.com

Following a review of the results of all testing, coupled with personal history and a physical exam, the doctor asses individual fertility. Sometimes, the recommendations will come at the initial visit, and other times, it will be after the results come back from blood tests. The doctor will also discuss lifestyle modifications, medications, or procedures that may improve the chances of having a baby.

EMPLOYERS OFFER SUPPORT

According to a recent Mercer report, 35% of employers offer men’s fertility testing, while 13% are considering offering men’s sexual health benefits. Analysts observe that as plan designs related to fertility become more inclusive, they are also seeing access to fertility preservation become inclusive, with 20% of employers indicating that sperm freezing is covered.

The business impact of male infertility is measurable, as one study shows that men struggling with fertility issues often report higher levels of stress and anxiety, leading to reduced productivity and engagement at work. Additional studies demonstrate that infertility can lead to depression, as patients can also experience stigma and reduced self-esteem.

“There can be a sense of inadequacy and shame when men are experiencing infertility,” says Lauren Meyer, LPC, ACS, manager of Health Psychology Operations, MINES and Associates, Inc. “Because of societal expectations and gender norms, it can be difficult for men to express their feelings or seek therapy.”

Related to this, Meyer explains that men are reluctant to share with friends or family about their struggles, which can lead to feeling isolated.

"Since anger is a more socially acceptable emotion for men to express, the entire fertility experience can put a strain on relationships -- romantic or otherwise,” she explains. “Unfortunately, it can be hard to find therapists who have this specialty or identify as infertility being a part of their lived experience.”

IMPACT ON BUSINESS

Furthermore, a lack of fertility support can lead to higher employee turnover, with research showing that 88% of people would consider changing jobs to access fertility benefits. Employees facing fertility issues are more likely to seek employment with businesses offering more comprehensive health benefits.

Analysts counsel that companies that neglect men’s fertility issues risk reputational damage. They advise that modern employees, particularly millennials and

corporatesolutions.swissre.com/esl

Gen Z, are paying close attention to businesses’ commitment to comprehensive health and wellbeing policies.

Dr. Adamson reflects that there has been a significant uptick in interest in male fertility among employers and brokers who want to enhance reproductive health programs.

“Including men in the fertility process is important since one in six heterosexual couples have difficulty conceiving," he explains. “As many as 2% of all men will exhibit suboptimal sperm parameters, resulting from one or a combination of low sperm concentration, poor sperm motility or abnormal morphology.”

He emphasizes the importance of empowering people with education, information and options that help both males and females overcome family-forming challenges.

“Male fertility treatments should be a high priority,” he continues. “Employers should look for care models with comprehensive reproductive health benefits that include services performed by urology networks and at-home sperm testing.”

AT-HOME MALE FERTILITY TESTING

Today, employers can offer their male employees and health plan members a seamless fertility testing experience from the comfort and privacy of their homes. The Sapyen at-home fertility test provides a unique, accessible and discreet option for male fertility testing, and an important step forward in addressing reproductive challenges early on to minimize costs and provide more opportunities to explore options on the path to parenthood.

Male Infertility Algorithm

One year of failure to conceive if female partner is <35 years old or 6 months of failure to conceive if female partner is > 35 years old

Male and female evaluated in parallel including male reproductive history

At least one abnormal semen analysis or abnormal male reproductive history

NO YES

Primary evaluation/ management of female partner

Initial hormonal evaluation (FSH, T)

Further male evaluation and management.

Consider IUI or IVF+ICSI

IUI: Intrauterine Insemination

IVF: In Vitro Fertilization

ICSI: Intracytoplasmic Sperm Injection

RPL: Recurrent Pregnancy Loss

FSH: Follicle-Stimulating Hormone

T: Testosterone

CF: Cystic Fibrosis

Failed IUI or IVF + ICSI or RPL

Complete male evaluation with: - History - Physical Exam

Semen Analysis

Treatment of abnormal factors or management with IUI or IVF + ICSI

Genetic testing (karotype and Y chromosome microdeletion)

Option for microTESE and IVF + ICSI

Categorize azoospermia with FSH, exam and T

Genetic (CF) testing for congenital cases of obstruction

Sperm retrieval or microsurgical reconstruction

Consider diagnostic and/or therapeutic biopsy if FSH & testicular volume normal but no clinical evidence of obstruction

The Sapyen at-home male fertility Test Kit allows men to conduct the most comprehensive, clinical-grade semen analysis from the comfort of their homes or any other convenient location. Priced at $149, this innovative solution eliminates the need for clinic visits, providing privacy and convenience while delivering accurate results through certified laboratory analysis—all at a cost lower than traditional in-lab testing. The test kit includes a patent-pending sperm stabilization medium (SPX72) that maintains semen viability for up to 72 hours, allowing the sample to be mailed and ensuring high-quality analysis.

Ashwin Ramachandran, founder and CEO, Sapyen, explains, “Our advanced at-home male fertility Test Kit offers an unprecedented level of convenience and accuracy, empowering more men to take the crucial first step in understanding their fertility health. "Within 72 hours, members receive a personalized report with detailed fertility insights, actionable next steps and customized recommendations that address a critical need in reproductive health, empowering employees to make well-informed choices for any potential treatments required.”

Oligozoospermia Normozoospermia Azoospermia

Depend on Sun Life to help you manage risk and help your employees live healthier lives

By supporting people in the moments that matter, we can improve health outcomes and help employers manage costs.

For over 40 years, self-funded employers have trusted Sun Life to help them manage financial risk. But we know that behind every claim is a person facing a health challenge and we are ready to do more to help people navigate complicated healthcare decisions and achieve better health outcomes. Sun Life now offers care navigation and health advocacy services through Health Navigator, to help your employees and their families get the right care at the right time – and help you save money. Let us support you with innovative health and risk solutions for your business. It is time to rethink what you expect from your stop-loss partner.

Ask your Sun Life Stop-Loss Specialist about what is new at Sun Life.

For current financial ratings of underwriting companies by independent rating agencies, visit our corporate website at www.sunlife.com. For more information about Sun Life products, visit www.sunlife.com/us. Group stop-loss insurance policies are underwritten by Sun Life Assurance Company of Canada (Wellesley Hills, MA) in all states, except New York, under Policy Form Series 07-SL REV 7-12 and 22-SL. In New York, Group stop-loss insurance policies are underwritten by Sun Life and Health Insurance Company (U.S.) (Lansing, MI) under Policy Form Series 07-NYSL REV 7-12 and 22-NYSL. Policy offerings may not be available in all states and may vary due to state laws and regulations. Not approved for use in New Mexico.

A Harvard Business Review article outlined strategies for employers who want to support an employee’s fertility journey, pointing out that fertility-friendly policies and benefits—such as financial support, access to counseling and flexible work and career-planning options— can help provide couples with peace of mind. Authors stress the importance of including fertility coverage for both male and female fertility diagnostics and procedures.

They also recommend providing managers with guidance on how to better work with employees experiencing physical and scheduling impacts. Workplace guidance, supplemented by social and perhaps professional support, could enable couples to more easily navigate their fertility journeys.

EMPOWER MEN WITH CURRENT INFORMATION

IMPACT OF TESTOSTERONE TREATMENT ON MALE FERTILITY

As testosterone replacement therapy (TRT) continues to rise in popularity, many men are accessing this therapy to enhance vitality, athletic performance and sexual health. However, experts advise

Advocacy in Action

Resolution

On average, aequum resolves claims within just 244 days of placement.

Unmatched Savings

aequum has achieved a remarkable 95.6% savings off disputed charges for self-funded plans.

National Expertise

aequum has successfully handled claims in all 50 states.

that one critical factor often overlooked is TRT’s potential impact on fertility—a vital consideration for those looking to start a family.

While TRT was originally designed to treat medical conditions such as hypogonadism, it is now marketed more broadly to healthy men experiencing normal age-related declines in energy, libido and muscle mass. Despite its benefits, TRT raises significant concerns about longterm reproductive implications, particularly regarding sperm production.

Synthetic testosterone can significantly reduce sperm production, often bringing sperm count close to zero, making conception difficult for couples. This creates not only physical challenges but also emotional stress for those hoping to build a family. Men seeking testosterone therapy should be fully informed about these potential fertility risks. Education and transparency are essential to ensure employees understand all aspects of TRT before starting treatment.

MALE CONTRACEPTIVE GELS

Recent news may be reaching the desktops of employers and employees: Contraline, a medical device company, shared promising data from a clinical trial for its male contraceptive gel, Adam. This nonhormonal hydrogel, often dubbed the "IUD for men," has shown effectiveness in blocking sperm

HEALTH COST IQ EXISTS TO HELP SELF-INSURED ENTITIES SAVE MONEY WITHIN THEIR HEALTH PLANS

Leveraging its proprietary HealthAnalytIQ software platform, HCIQ can:

Identify problematic utilization patterns and risk trends

Forecast future healthcare costs

Predict potentially high-use, high-cost members

Identify medical claims payment irregularities and pharmacy utilization inefficiencies

flow to the vas deferens. With over 20 successful implantations and no reported adverse events, Adam presents a potential game-changer in the realm of male contraception, although continued clinical trials are still underway, and regulatory approval will be required. The product will potentially be available by 2026-2027.

ADDRESSING MALE FERTILITY: A CRITICAL STEP IN FAMILY PLANNING

“Today, 1 in 6 couples struggle to conceive, and male factors contribute to 50% of these cases,” states Pamela Pure, CEO, Posterity Health, a company that works in partnership with ARC Fertility and other reproductive health organizations, the only virtual-first Center of Excellence focused on male fertility, offering a comprehensive, technology-enabled, and expert-driven approach to reproductive health. “The traditional process, focused primarily on evaluating the female, leaves men on the sidelines. As a matter of fact, men aren't evaluated until 22 months into the fertility journey, delaying the family planning journey.”

Pure emphasizes that infertility is a couple issue, best addressed by evaluating both partners simultaneously. Understanding the fertility status of both partners will help every couple determine the most effective path to pregnancy.

“Including male evaluations early on provides essential benefits,” she continues. “Many male infertility factors are correctable, potentially allowing for natural conception and helping avoid unnecessary female treatments. Early evaluation can also uncover underlying health issues—such as hormonal imbalances—that impact broader aspects of a man's wellbeing, including energy levels, weight, and behavior. Common factors like obesity, marijuana use, medications, and untreated health conditions can also influence male fertility and require personalized support.”

Pure established the company to provide comprehensive male fertility care that engages men in their reproductive health from the start.

“We make it easy for males to complete a preconception consult to

identify any potential male factor issues at the beginning of the process,” she explains. “If a male factor exists, our team provides immediate access to expert care. They then create a complete treatment plan, incorporating at-home diagnostics, virtual visits, in-person consultations, procedures and ongoing hormone management care – including LGBTQ+ family-building support. For employers, this approach results not only in better care but also saves costs.”

“By actively diagnosing and treating male fertility issues, we reduce the need for expensive female fertility treatments,” says Pure. “For employers, this means a new opportunity to offer employees comprehensive fertility support while lowering costs associated with prolonged or unnecessary procedures.”

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com

Pam Pure

STOP LOSS INSURANCE WE’LL HELP MANAGE THE RISK.

Prudential’s Stop Loss insurance helps reduce unpredictable risks from self-funded medical plans. This way you can focus on giving your employees the coverage they deserve, while helping to reduce your worries about the increased frequency of catastrophic claims.

Get Stop Loss insurance from a partner you can rely on:

• A highly rated, experienced carrier recognized for nearly 150 years for strength, stability, and innovation

• Efficient, responsive service with streamlined processes across quoting, onboarding, and reimbursements

• A dedicated distribution team that works hand-in-hand with your existing relationships

• Flexible policy options so we can build a coverage plan that meets the unique needs of your organization

Did you know, 1% of people account for a quarter of healthcare spending in the U.S.* See how Prudential can help you manage the risk from your self-funded medical plan.

For more information, contact us at stoploss@prudential.com or visit our website: www.prudential.com/stoploss

CHANGES TO EMPLOYER REPORTING REQUIREMENTS UNDER THE ACA

Written By Alston & Bird, LLP Health Benefits Practice

TheTnew year is off to a good start for plan sponsors required to distribute Forms 1095-B and 1095-C under the Affordable Care Act (ACA). Congress passed two new laws – the Paperwork Burden Reduction Act and the Employer Reporting Improvement Act – which together ease compliance burdens for plan sponsors. These changes include:

• Alternative manner of furnishing Forms 1095-B and 1095-C to employees upon request: Entities required to furnish Forms 1095-B and 1095-C to employees may now provide these statements upon request only. These statements no longer have to be furnished to employees automatically.

• Statutory changes to electronic delivery of Forms 1095-B and 1095-C: The duration of consent to electronic delivery of statements lasts until the employee revokes consent in writing. Regulations require the consent to state the scope and duration of consent, but this statutory change allows the consent to be valid until withdrawn in writing.

• More time to respond to penalty assessment letters from the IRS: Certain large employers now have more time – 90 days rather than 30 days – to respond to letters from the IRS that propose to assess an employer shared responsibility payment (ESRP).

• Fixed statute of limitations for ESRP assessments under Code Section 4980H: Congress set a sixyear statute of limitations for the IRS to assess the ESRP penalty.

• Codifies the birthdate substitution for TINs: Congress made the flexibility for using a full name and birthdate instead of the taxpayer identification number (TIN) on Forms 1095-B and 1095-C a statutory provision rather than just regulatory provision.

We focus on what these changes mean under the ACA for large employers, which typically file and furnish Form 1095-C to report information on employer-provided health insurance offerings and coverage. However, these changes also apply to reporting entities for Forms 1095-B (e.g., insurers and employers sponsoring self-insured plans).

CURRENT LAW

Under the ACA, applicable large employers (ALEs) – or large employers who have employed an average of at least 50 full-time equivalent employees in the prior year – are required to provide Form 1095-C to all full-time employees. Employers of all sizes with self-insured plans must also provide the form to all employees enrolled in the employer’s health plan, regardless of full-time status. Although employers have the option to either mail these statements or furnish them electronically, employers must distribute them automatically.

Electronic delivery requires employee consent, and one of the consent requirements is to define the scope and duration of the consent. This can result in the employee limiting the consent to, for example, only the upcoming Form 1095-C or to a span of 12 months. The difficulty of managing the consent requirements (e.g., different durations for each employee) has resulted in many ALEs choosing to mail these forms to their employees. In either case, automatic distribution must be done by January 31 each year (or March 1 if using an extension).

ALEs also send these Forms 1095-C to the IRS, which in turn uses some of that information to determine whether to assess an ESRP penalty against the employer. If that happens, the IRS sends a letter to the ALE informing the employer of the potential penalty (these are called 226-J letters). These letters usually include a response form that must be returned to the IRS within 30 days, which can be a tight turnaround time if the letter takes a while to move through the employer’s organization and get into the hands of someone authorized to reply. Failure to respond by the deadline could result in the IRS assessing the penalties against the employer. Although the IRS grants extensions for these responses when the request is made within the 30-day period, employers are at risk of not getting an extension for requests made after the 30-day deadline.

ALEs also never know when they may receive a 226-J letter from the IRS for a given year proposing an ESRP assessment because, according to the IRS, there is no statute of limitations for assessing the ESRP. Not knowing when an assessment of ESRP may be proposed from a prior year can affect the employer’s standard record retention policies and procedures.

CHANGES IN 2025

Under the newly enacted laws, ALEs have a substantially reduced burden for distributing Form 1095-C to employees and have much more breathing room to respond to 226-J letters from the IRS. Changes include:

• Alternative manner of furnishing statements: ALEs now have an alternative to automatically providing Form 1095-C to employees by January 31. Instead of automatically furnishing the statement, either by mail or electronic delivery (if consent has been obtained), ALEs can now provide the statement upon request. ALEs will be treated as providing the Form 1095-C timely so long as:

o The employer “provides clear, conspicuous, and accessible notice” to employees entitled to receive the Form 1095-C that they can request a copy of it.

Isaac Leanos Member Advocate

o The employer satisfies the request for the statement no later than the later of:

January 31 of the year following the calendar year for which the return was required to be made or

30 days after the date of the request.

The ALEs would still have to mail the Form 1095-C to the employee requesting the statement unless the employee consented to electronic delivery.

Effective date: This alternative manner of furnishing statements is available for statements for returns for calendar years after 2023, which includes 2024 Forms 1095-C. Although Congress deferred the time and manner of the required notice to the Secretary of the Treasury, a good-faith compliance standard would likely apply until further guidance is provided.

Practice Pointer: Until the IRS provides further guidance on the time and manner of notice, ALEs wishing to use this alternative manner for distributing their 2024 Forms 1095-C may want to look at regulations for similar notice provisions for guidance. For ALEs with self-insured plans, the IRS already provides an alternative manner of furnishing Form 1095-C to covered non-employees and covered employees who were not full-time employees at any time during the year. Under those regulations, the notice requirement is met if the reporting entity posts the notice prominently in a location on its website that is reasonably accessible to all individuals entitled to receive the form stating that they may receive a copy upon request. The notice must include an email address and a physical address to which a request may be sent, as well as a telephone number for questions. The regulations also require the notice to be retained in the same location on the ALE's website through October 15 following the calendar year to which the statements related (or the first business day after October 15 if October 15 is not a business day).

• Proper electronic consent is valid until it is revoked: Under the current regulations, consent from employees for electronic distribution of the Form 1095-C must state the scope and duration of the consent. Under the new statutory provision, an individual is deemed to have consented to receive the Form 1095-C in electronic form if they have affirmatively consented “at any prior time” to the employer (or to the entity required to provide the Form 1095-C). The consent is valid until the individual revokes the consent in writing.

Effective date: This change applies to Forms 1095-C due after December 31, 2024.

• More time to respond to ESRP assessment letters: ALEs now have 90 days, instead of just 30 days, to respond to the “first letter” (i.e., the 226-J letter) from the IRS proposing an assessment of the ESRP against the employer. The new law does not indicate whether an ALE can still request an extension beyond 90 days.

Effective date: This change applies to assessments proposed in taxable years beginning after December 23, 2024.

• Six-year statute of limitations ESRP assessments under Code Section 4980H: Congress added a six-year statute of limitations on assessments of the ESRP under Code Section 4980H. The sixyear period begins on the due date for filing the return or, if later, the date the return was filed for the calendar year for which the ESRP penalty is determined.

Effective date: This change applies for returns due after December 31, 2024. Note that this change does not necessarily affect the IRS’s position on the statute of limitations for prior years.

• Codifies the birthdate substitution for TINs: Congress made the flexibility for using a full name and birthdate instead of the TIN on Forms 1095-B and 1095-C a statutory provision rather than just a regulatory provision. Regulations already permit the birthdate rather than the TIN to be used if “reasonable efforts” have been made to obtain the TIN. The statutory language states that if the person required to make a return “is unable to collect information on the TINs,” the Secretary of the Treasury “may allow” the individual’s full name and birthdate to be substituted for the TIN. It is unclear whether Congress intended to solely codify into statute the ability to use the date of birth when the employer could not collect the TIN of the dependent or to provide relief from the solicitation requirements applicable to TINs; however, since the statute does not amend IRC Section 6724, which sets forth the applicable solicitation requirements that must be followed to avoid penalties for failing to collect the dependent's TIN, it is likely that the solicitation requirements still apply. Additional guidance from the IRS will be helpful, especially since the solicitation requirements applicable to dependents enrolled in health insurance aren’t clear.

Effective date: This statutory change applies for returns with due dates after December 31, 2024, although technically, it is already permitted under the regulations.

If you have any questions about these changes, contact your employee benefits counsel.

Attorneys John Hickman, Ashley Gillihan, Steven Mindy, Amy Heppner, Laurie Kirkwood, and Bria Smith provide the answers in this column. John is partner in charge of the Health Benefits Practice with Alston & Bird, LLP, an Atlanta, New York, Los Angeles, Charlotte, Dallas and Washington, D.C. law firm. Ashley and Steven are partners in the practice; Amy and Laurie are senior members in the Health Benefits Practice; Bria Smith is an associate in the Employee Benefits Practice. Answers are provided as general guidance on the subjects covered in the question and are not provided as legal advice to the questioner's situation. Any legal issues should be reviewed by your legal counsel to apply the law to the particular facts of your situation. Readers are encouraged to send questions by EMAIL to John at john.hickman@alston.com.

HIGH-COST MEDICAL CLAIMS REQUIRE HIGH-POWERED NEGOTIATIONS & REPRICING

Lower your expenses on in- and out-of-network claims with savings as high as 90%

Our expert negotiating team will help you avoid overpayment and achieve exceptional savings on the highest cost treatments.

H.H.C. Group is your trusted partner to verify costs, ensure billing accuracy and reprice claims. 301.960.7092 | sales@HHCGroup.com

NEWS FROM SIIA MEMBERS

2025 FEBRUARY MEMBER NEWS

Provided below are news highlights from these upgraded members. News items should be submitted to membernews@siia.org.

All submissions are subject to editing for brevity. Information about upgraded memberships can be accessed online at www.siia.org.

If you would like to learn more about the benefits of SIIA’s premium memberships, please contact Jennifer Ivy at jivy@siia.org.

East Coast Underwriters Announces Key Promotions as Part of Leadership Restructuring

East Coast Underwriters, LLC (ECU) has announced the promotion of Jonathan Socko to President and Kody Parker to Senior Vice President of Sales. ECU's former President, Aaron Wilkie, will be shifting to the role of CEO. Aaron had previously served as ECU's President since 2002. Jonathan, who previously served as ECU's Senior Vice President of Sales, has been with the organization since 2012. Kody Parker, who previously served as a Sales Director for ECU, has been with the organization since 2017. Aaron will continue to be a part of East Coast Underwriters; however, daily leadership responsibilities will shift to Jonathan, effective immediately.

"We're pleased to announce the leadership changes at ECU,” said Aaron. “Our company has continued to achieve our goals of ‘smart growth,’ and we are positioned very well with the tremendous staff we have in place.”

Per Jonathan, "ECU has grown by over 40% since 2021. I attribute our success to Aaron's vision for our organization, and I look forward to carrying the torch. We are absolutely blessed to have the staff, carrier partners and clients, many of whom have been with us for nearly 10 years or more. To say that I'm excited about our organization's future would be understated."

Kody added - "I am incredibly grateful for this opportunity and the responsibility that comes with it. I am excited to step into this role and work even closer with our exceptional team to continue to drive growth, maintain and build relationships, and achieve our shared vision of success. We are all looking forward to the continued success and smart growth with our carrying partners and valued clients that we will continue to hold close.”

Jonathan Socko East Coast Underwriters, LLC (ECU)

Kody Parker East Coast Underwriters, LLC (ECU)

Thomas Conde Joins Crum & Foster

Crum & Forster announced that Thomas Conde has joined its A&H Division as Vice President, ESL Programs for the Medical Business Unit (MBU). In this new role, Conde will be responsible for the portfolio management, product development, financial planning and strategic development of Employer Stop Loss, Medical Excess and Ancillary insurance and reinsurance products.

Trustmark Announces Leadership Transition