Leo Nolan, Partner

Wyatt Batchelor, Partner

Michael Mulcahy, Partner

Kevin Mulcahy, Partner

Trip Cowin, Partner

MBN Brands

Leo Nolan, Partner

Wyatt Batchelor, Partner

Michael Mulcahy, Partner

Kevin Mulcahy, Partner

Trip Cowin, Partner

MBN Brands

By Paul Marino

The firm maintains a diverse, businessoriented practice focused on investment funds, litigation, corporate, real estate, regulatory and compliance, tax and ERISA.

Drawing on the experience and depth of our lawyers in these distinct areas, we can leverage each lawyer’s industryspecific knowledge to help our clients succeed. This collaborative approach brings to the table a collective insight that contributes to sensible, efficient resolutions, and allows us to remain attentive to the cost and time sensitivities that may be involved.

Sadis’s clients include domestic and international entities, financial institutions, hedge funds, private equity funds, venture capital funds, buyout funds, commodity pools, and numerous businesses operating in various industries around the world.

BY PAUL MARINO

SADIS & GOLDBERG

In early January 2025, the wind was at our backs, the sun was shining on our face; I had so much confidence in the market that I was convinced the market would “rip”; and I was not alone. The University of Michigan Consumer Sentiment Index (“ICS”) consumer sentiment survey was at a near 5 year high (with a 71.70 handle)¹ and the consumer confidence index (“CCI”) was also at a multi-year high (with a 104.1 handle)², small business index (“SBI”) sentiment on the other hand dipped to 62.3

from 69.1 at the end of Q4 2024 (survey results suggested the dip was a result of worry about consumer spending and inflation).³

As I write today in the middle of December, the ICS sits at 51 (20 point drop) and CCI is 11.3 points under water at 88.7. It is not an understatement to say that the foregoing is not good; however, not all is lost. The SBI for Q3 2025 rose to 72 which (as described by the publisher of the report) is an “alltime SBI high”.⁴

So, small business owners are feeling good, consumers are not—what does it mean for M&A professionals? Based on what I am seeing, it seems that 2026 will outstrip 2025 and we will see greater deal volume and more deal activity spread across the deal landscape (e.g., aggregate global M&A value rose (driven by a cluster of mega / >$10B deals) while deal counts fell — i.e., big deals pushed dollar value higher even as overall transaction activity softened (especially in the middle market).⁵

For those of us living in the middle market the last part of the foregoing sentence is painful to read because we lived it; but beneath the headline numbers, dealmaking in the first half of 2025 was slower than expected.⁶ Why did the deal market cool off so much? The talking heads (pick your preferred media platform of choice) would have you believe it was taxes, tariffs, interest rates, global uncertainty, and just about any number of other potential calamities (except for global warming— that one seems to have vanished—at least for now). I posit the real reason deal volume fell, at least to this guy (especially in the middle and lower middle market) is valuation. The spread between the bid and ask is still too high.

Here are some thoughts: First, when deal volume hits a decade low but total deal value is up year over year, that tells me (i) the mega deals that closed in 2025 were really deals that were in the pipeline that didn’t close because of the change from the previous (less accommodative) administration to the new (more accommodative) administration and (ii) irrespective of financing, the mergers created cost cutting to such an extent that cost of financing was out-stripped by valuation created by merger (let’s not forget that publically traded

companies trade at MUCH higher multiples than private companies—and that includes publically traded private equity companies).

Second, combine (i) lofty valuations with (ii) higher interest rates/cost of capital and stricter lending terms and you get (iii) a deal market that failed to launch.⁷ Third, as deal sizes get bigger you run out of chairs (think musical chairs) and when that happens EVERYONE starts to worry about being the guy left standing because you know what they call him: loser. Conversely, if you’re the seller that has held out and didn’t sell because you think your company is worth as much as your friends who sold in 2022 at a 15x EBITDA multiple, you too don’t want to be a loser (and like handicaps, there is a lot of vanity associated with what your business is sold for). In addition to multiples being lower, the “all cash walk away” offer is hard to find, with many buyers wanting additional structure such as rollover equity, earnouts, and/or seller notes to bridge valuation gaps.

In short, many sellers still want the multiples of days past when capital was cheap and plentiful and multiples were high, while buyers are trying to deal with the reality that it is harder to underwrite and hit their needed returns due to the cost of capital and market risk — that disconnect reduced closings.⁸

On the middle and lower middle market deal side: deal activity picked up in the second half of 2025 and should continue to prove both strong and robust.⁹

What’s driving the ascent in the middle/lower middle market?

• Dry powder.10 There remains significant amount of unpaid capital in the system. Many PE funds, family offices and credit providers have undeployed capital waiting for the right moment. The backlog of companies held by funds (due to slower exits) adds urgency.

• Adjustment of Valuations and Leverage. With higher borrowing costs and inflationary pressures, deal multiples have come down.11

• Shift Toward More Creative Structures And Alternative Sponsors. Most limited partners are suffering from illiquidity fatigue and have grown impatient with GPs. The foregoing fact has given rise to continuation vehicles but most of all has created the rush to secondary fund formation. In this liquidity winter, most LPs are looking at DPI as the greatest attribute for any sponsor and as luck would have it, most IS have a great track-record for returning capital in a 4-6 year time period.12

• Exit Backlog & Anticipated Liquidity. With fewer exits in 2022-24, many portfolio companies are “waiting” for the right exit window. As the macro stabilizes, that backlog can release and fuel more deal activity. The fact is that no one likes to give up on their “draft picks”, and the same can be said about GPs. Portfolio companies remain platforms well past their expiration date because GPs don’t want to give up on a trade they may have paid too much for a few years back.13

The foregoing is why Independent Sponsors (“IS”) have taken off in the current investment landscape. Also, the following is a consideration:

• Pick your Platform: The idea of choosing a deal to invest in directly or vis-à-vis a sponsor is greatly appreciated by investors (mostly family offices and HNW individuals who are less enthralled by blind pool funds and like the idea of having more autonomy to choose which deals and which sponsors to back). It means investors get a clear line of sight on the transaction and (more than likely) the exit.

• When You Know, You Know: The ability to direct invest in an area that you know well creates superior alignment between all parties is a great selling point for sponsors. If you deal with a number of family offices you quickly realize that many family offices (especially those run by first and second gen) invest in areas that they know (usually where they made their money). A single platform SPV allows for this type of investment transparency, alignment and commonality. But it’s not just family offices, you also are seeing a huge rise is more institutional investors backing good ISs with good deal.

• People Who Need People: Sellers like to sell to people who understand them and their business. ISs, for the most part, get into the weeds discussing the sellers business. The fact is people like to deal with people who they understand and speak the same language (take note, this isn’t saying sellers will not sell to the highest bidder—they often will but when everything is equal they’ll sell to the group they trust).

The IS model is evolving to one that mirrors what a middle market PE firm used to look like. A few deals with high IRR in narrow sector specific transactions. And what I mean by a few deals is a number of addon/tuck-in business that are in line with or adjacent to the platform.

Of course, there are always headwinds in the middle/lower middle market (and more specifically IS); here are a few:

• Execution Risk: Let’s face it, without having a pool of capital behind you there is always a risk that the deal won’t get done because there isn’t cash available. Execution risk is closely tied to the equity and/or debt fundraising market. In 2026, with a new Fed Chairman coming online, a potential recession on the horizon, and a national election, you can bet that the monetary policy coming out of Washington, D.C., will be accommodative. And this will apply to interest rates but, for example, look for more incentives from the SBA for US manufacturing, etc.

• Competition and Valuations: With PE firms and IS competing for the same quality assets, valuations will be bid up, therefore squeezing returns.

• Capital Stack Complexity: ISs often rely more heavily on custom capital stacks (equity from family offices, debt from specialty lenders, etc). The terms may vary widely, and deal economics/ ownership can become more bespoke.

• Operational Resources: Some ISs may have less scale, fewer in-house operations or integrations teams compared to large funds. To create value, they must be smart about sourcing management talent, leveraging operational expertise, and running effective post-deal playbooks.

The deal environment in 2026 is being shaped not just by macro or capital structure, but also by a few evolving themes — geography, sector, and strategy.

Private equity firms and sponsors are increasingly looking outside their traditional domestic markets for growth or opportunity.

In emerging markets, as interest rates stabilize, and companies seek capital for growth, there are opportunities, though with higher risk. For independent sponsors, cross-border deals may become more viable (e.g., will near shoring and strength of dollar push companies to look at Mexico or Canada…or Argentina).

• Technology / digital transformation: Given that many portfolio companies and targets suffered from outdated technology, sponsors are focusing on value creation via modernization, AI adoption, digital services, SaaS models (although, my guess is SaaS is going to have to adopt to the new AI business order).

• Healthcare / Life Sciences: Aging demographics,

regulatory tailwinds, and innovation mean that healthcare continues to be attractive; HOWEVER, health care is a political football and one has to wonder when “deflate” gate hits the space.

• Infrastructure & Energy Transition: With the globe no longer on death watch (apparently catastrophic climate change has been revised) and sustainability mandates lessened, many funds are moving out of the rent seeking space of climate activism but instead pivoting to the real need for infrastructure development to meet AI energy needs (e.g., data center, etc.)

• Middle-Market/Fragmented Industries: Industries with smaller players (lowermiddle market) where consolidation, digital enablement, and operational improvement can drive outsized returns. ISs are particularly active in this market. Again, look for on or near shoring to have an oversized impact in the middle and lower middle markets.

• SPAC: SPAC’s will make a comeback. You heard (actually read) it here first. The valuations in public markets (albeit volatile) are much higher than private markets and with the dearth of exits in PE (and GP continuation vehicles making up 50p of the secondary market—not a good sign for LPs clamoring for DPI), it is a good time for SPACs.

• Add-On Strategy: Since platform deals are harder to source and will command premium pricing, many sponsors will emphasize add-on acquisitions to build scale and drive value.

• Growth Equity / Minority Investments: Instead of full control LBOs, some sponsors will lean into growth equity, preferred equity, minority stakes with rights — especially where leverage is constrained.

• Co-Investment & Hybrid Capital: To reduce fees and align interests, LPs are co-investing more. Sponsors are offering co-investment opportunities. Bain’s data shows co-investment ratios remain meaningful.

• Alternative Capital Structures: Independent sponsors and smaller funds will use more creative capital stack alternatives (e.g., mezzanine, unitranche, preferred equity, structured equity) to compensate for higher debt cost or limited leverage.

Deal participants need to layer in thematic/sectoral awareness and geographic flexibility into their sourcing and value-creation playbooks. Just doing “generic buyouts” in 2025 is higher risk. Thematic clarity and operational execution matter more than ever.

As Yogi Berra once said, “it’s tough to make predictions, especially about the future.”15

Nonetheless, if you look at 2025 it is a tale of two M&A markets, the first half was tepid at best with movement in the later part of the second quarter driven by massive transactions, likely resulting from

an accommodative regulatory body. The second half saw the aggregate value of deals in the US increasing to $598 billion in the third quarter, which is the highest in four years.16 Sounds awesome, but much like modern box office sales figures, the data is somewhat punk.17

equity, growth equity, structured deals, coinvestments, secondaries. Irrespective of interest rates, the “classic leveraged buyout” may become less dominant. With the rise of DPI as a deal metric, look for sponsors to have a shorter duration.

The total number of deals in the US remained mostly flat during 2025, which means that we are not transacting nearly as much as we have previously done in years past. In fact, according to a survey conducted by Deloitte, the value of US deals in Q3 jumped 56% whereas the volume only increased by 1.6%.18

Here is what I expect to see in 2026:

• Interest Rates Start To Ease (Conditionally): If central banks signal rate cuts, the cost of debt for leveraged deals should decline, unlocking higher leverage and more willing sellers. That could accelerate deal volume.

• Deal Volume Recovery: After a slower 2022-25, we expect deal flow to pick up further in 2026 — especially add-on deals, platform builds, carveouts. The IS model will continue to mature, with more capital providers, more hybrid models (seeded, pledge funds), and more competition.

• More Creative/Alternative Structures: Expect growth in minority investments, preferred

• Value Creation Plays Front And Center: Given exit/ multiple constraints, operational improvement, digital transformation, consolidation strategies will differentiate winners. One question you’re going to hear (even in trade and trade services deals (e.g., HVAC, etc.) is how will artificial intelligence impact this business.

• Fundraising Bifurcation: Top-tier large funds will continue to raise easily; emerging managers will still face headwinds, but independent sponsor pools will open up more. Shorter duration and return of capital are key. Thereby giving IS an advantage.

• Exit Backlog Will Begin To Roll: By 2026, we may see more liquidity events, but the excess will have been “priced in” and value creation from operations will matter more than the multiple arbitrage of earlier years.

• Increased Consolidation In The Sponsor/Fund Industry: Smaller funds may merge, strategic partnerships may form, and competition may thin out.

• If interest rates remain high (or rise), the leverage advantage may be further constrained.

• If macroeconomic growth disappoints (recession,

inflation shock, supply-chain disruption), the deal market could stall.

• Regulatory shocks (e.g., stricter antitrust/FTC rules, geopolitical decoupling) could make crossborder deals riskier.

• Valuation recovery may be uneven: some sectors will bounce, others may lag — sponsors must pick wisely.

• Execution risk remains acute in independentsponsor deals — capital is not committed upfront, and sponsor/backer alignment matters more.

HOW MANY MORE TIMES - What Sponsors/ Investors Can Do To Prepare For 2026

• Build Sourcing Pipelines Now: sponsors with deal flow ready as activity picks up will gain advantage.

• Focus On Operational Playbooks: invest in digital, talent, integration teams, and value creation systems.

• Diversify Deal Strategy: include growth equity, carve-outs, add-ons, and minority deals, international.

• Strengthen LP/Backer Relationships: transparency, alignment, previous execution track-record will matter.

• Stress-Test Exit Assumptions: assume longer holding periods, potential for multiple stagnation, emphasize operational growth.

• Consider Independent Sponsor Structure: If you’re a deal professional outside a large fund, 2026 may be a strong year to launch or scale an IS platform.

For sponsors, investors, and advisors, the message is: “be bold, but be grounded.” The environment for deals is better than 2022-25 in many respects, but the rules have changed. Leverage is more expensive, valuation arbitrage is harder, execution and value creation matter more than ever, and structure matters. Independent sponsors, in particular, have strong tailwinds, but must execute seamlessly and build resilience.

Looking ahead to 2026, those who are ready with a pipeline, aligned capital, operational playbook, and global/sector awareness will likely have the upper hand. The question isn’t just “how many deals can we do” but “how well can we execute, create value, and exit in a more complex environment”.

1. https://ycharts.com/indicators/us_consumer_sentiment_index? (visited, 12/4/2025) 100 being the baseline.

2. https://www.conference-board.org/topics/consumer-confidence/ (visited, 12/4/2025)

3. https://www.uschamber.com/co/run/finance/metlife-small-business-index?utm (visited, 12/4/2025) graded on a scale of 0-100 with 100 being the best.

4. https://www.uschamber.com/sbindex/summary?utm (visited, 12/4/2025)

5. https://dealogic.com/insight/ma-highlights-1h25/?utm (visited, 12/4/2025)

6. https://dealogic.com/insight/ma-highlights-1h25/?utm (The number of transactions has plummeted to a two-decade low, down 16% to 16,663 deals as of 23 June.)

7. Failed to launch like a 28-year man-child who graduated from a top tier liberal arts school, wearing tube socks, in his robe living in his parents basement, listening to sports to talk radio

8. It should be noted that smaller firms (both sell and buy side) are more susceptible to sector-specific headwinds (supply chains, tariffs, demand shifts). https:// www.pwc.com/gx/en/services/deals/trends.html?utm (visited, 12/4/2025)

9. According to the Citrin Cooperman 2025 Independent Sponsor Report: 44% of independent sponsors surveyed in 2025 are targeting companies with EBITDA > $10 million (versus only 4% in 2017) (https://www.citrincooperman.com/Focused-Programs/Independent-Sponsor-Report?utm) (visited, 12/4/2025)

10. Very few words are overused more than “dry powder”; it is in my top 10 least favorite business terms (i) Synergy: The corporate equivalent of “magic happens here;” ; (ii) Value-add: Usually means… nothing was actually added; (iii) Circle back:“I don’t want to deal with this right now;” (iv) Bandwidth: Your calendar isn’t the problem; your willpower is; (v) Low-hanging fruit: The mythical easy tasks no one ever seems to pick; (vi) Move the needle: Because apparently everything is a giant speedometer; (vii) Win-Win: Win-Win: When said, usually means someone is losing; (viii) Take it offline: Corporate for “stop talking about this in front of people;” (ix) Thought Leadership: Often used as a fancy wrapper for basic observations. Honorable Mention: (x) Pivot: Overused since 2020 and still going strong; and (xi) Greenshoots: the most overused word of the GFC.

11. For instance, Citrin Cooperman notes that the average multiple for emerging sponsors dipped to 8× (versus 9.9× earlier) and that 76% of independent sponsors closed deals at 6× or less in the past year. (visited, 12/5/2025; https://www.citrincooperman.com/In-Focus-Resource-Center/What-To-Expect-in-Private-Equityin-2025?utm)

12. https://www.sadis.com/insights/strengths-and-weaknesses-of-dpi-how-the-distributions-to-paid-in-capital-metric-illuminates-and-obscures-fundperformance

13. Exit windows remain muted — in particular, IPOs and strategic sales are slower compared to the boom years. That leaves many sponsors holding portfolio companies longer, which places pressure on internal rates of return (IRRs). The Harvard Law publication notes that “elevated levels of untapped dry powder” and “long holding periods” are issues for sponsors in 2025. https://corpgov.law.harvard.edu/2025/01/24/private-equity-2024-review-and-2025-outlook (visited, 12/5/2025)

14. For example, the Citrin Cooperman report points out that 43% of PE/VC-owned companies say that outdated tech is their biggest barrier to AI adoption. (https:// www.citrincooperman.com/In-Focus-Resource-Center/What-To-Expect-in-Private-Equity-in-2025) (visited, 12/5/2025)

15. My favorite prognosticator is of course Mr. T in Rocky III, prediction, yeah, I have a prediction, “Pain” (https://www.youtube.com/watch?v=SNguN22of8k&t=5s)

16. https://www.deloitte.com/us/en/what-we-do/capabilities/mergers-acquisitions-restructuring/articles/m-a-trends-report.html?utm (visited, 12/5/2025).

17. In other words, number of movie tickets (in total) is way down but the cost of a movie ticket has dramatically increased in price.

18. https://www.deloitte.com/us/en/what-we-do/capabilities/mergers-acquisitions-restructuring/articles/m-a-trends-report.html?utm (visited, 12/5/2025).

PAUL MARINO Partner

Sadis & Goldberg pmarino@sadis.com

Paul Marino is a partner in the Financial Services and Corporate Groups. Paul focuses his practice in matters concerning financial services, corporate law and corporate finance. Paul provides counsel in the areas of private equity funds and mergers and acquisitions for private equity firms and public and private companies and private equity fund and hedge fund formation.

BY DON LEVY KROLL

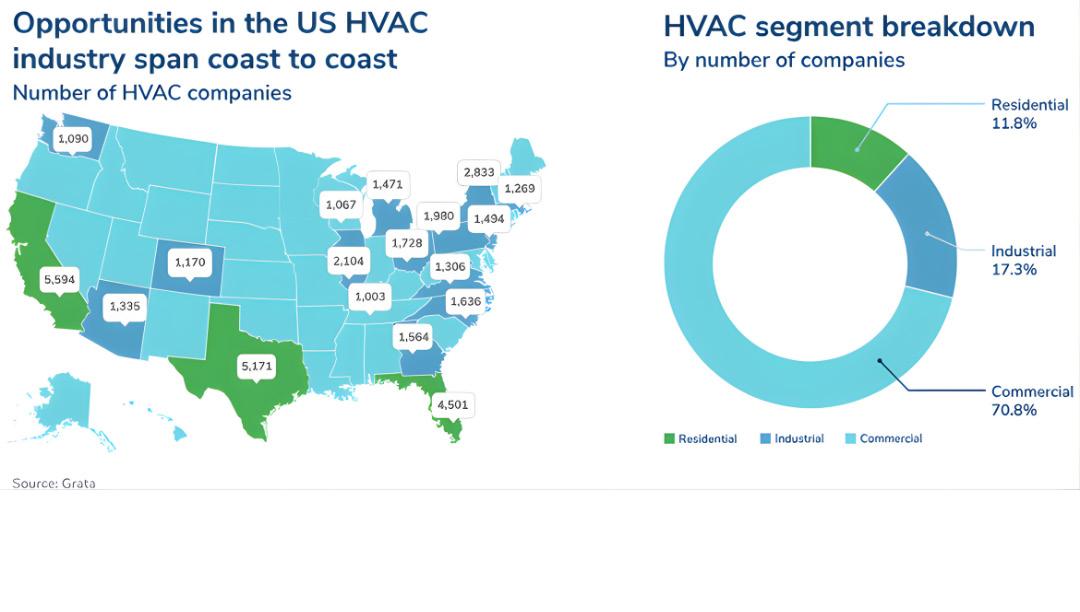

Global HVAC in general, from commercial and residential services to equipment and system manufacturing, remains a large, durable market, estimated in excess of $350 billion in 2025, with mid-single-digit CAGR through the next decade.

More specifically, PE firms remain the dominant buyers of residential HVAC service platforms, executing buy-and-build rollups across various regions in the U.S. Large growth/mega-cap PE and alternative-asset groups (Goldman Sachs Alternatives, General Atlantic, L Catterton, Gryphon, Gamut and various others) are buying sizeable regional platforms, while middle-market PE and strategic consolidators focus on tuck-ins and regional density.

Essential, recurring and locally fragmented, residential/commercial service platforms continue to trade actively. A notable example: Sila Services’

sale from Morgan Stanley’s PE arm to Goldman Sachs Alternatives, reportedly at ~$1.5billion including debt in early 2025. These trends have been strong for the last five plus years and continue into Q4 2025 and 2026, primarily due to the focus on recurring revenue via annual/ periodic maintenance plans, low capital intensity, multitrade bundles (HVAC + plumbing + electrical) and technology-enabled service ops.

• Companies with maintenance plans, membership programs and consistent seasonal service cycles provide investors with predictable revenue and EBITDA, along with a strong base on which to further build and grow.

• The multitrade capabilities keep customers with one family of companies and allow for crossselling opportunities.

• Large platforms, such as Sila Services and Apex Services Partners (an active Alpine Investors platform), have completed numerous add-ons

and created well-oiled corporate development and integration processes and protocols allowing for swift and efficient M&A processes.

• Platforms are also now focusing on businesses with upgraded dispatch, mobile invoicing and various modern diagnostic tools that improve productivity, margins and scalability, which is more attractive to investors.

Deal valuation remains at a premium with PE buyers paying double digit multiples for high quality platforms (mid-teens Enterprise Value/EBITDA), especially those with significant recurring revenue.

From an add-on perspective, many of the smaller tuck-ins, which in many cases are single-digit EBITDA family/founder owned businesses, are trading for multiples generally ranging from three to eight times and in some instances more, to the extent they are larger professionalized companies. Founders who have run these smaller regional residential HVAC businesses for decades are educating themselves on the current M&A boom in residential HVAC services.

They are retaining advisors and seeking M&A, knowing that a significant liquidation event may be in their futures, while many often remain with the company to run the business and retain equity. Earnouts and performance-based consideration are often built into the purchase agreement terms.

Diligence considerations and processes also continue to be rigorous, especially with sophisticated PE platform buyers, where advisors are being retained for various workstreams, including but not limited to financial, tax, employee/HR and benefits, and insurance diligence, among others, as necessary. Buyers will deep dive into the target’s labor model, technician productivity, customer churn and retention, recurring revenue breakdown and integration.

Overall HVAC Industry Outlook: Through 2026, the industry expects active add-ons by PE-backed service platforms, continued trimming of noncore assets by global OEMs (e.g., Carrier’s sale of its fire/security businesses) and fast deal flow in controls/AI and mission-critical cooling. HVAC equipment distribution roll-ups are expected to remain steady as strategics seek to increase market share in growth geographies. With secular tailwinds (electrification, refrigerant transition, AI compute), the sector’s M&A engine appears to be poised for continued activity, even if multiples stay selective and buyer due diligence is rigorous. Further, the residential HVAC M&A outlook is that it may be about halfway through the broader consolidation cycle, but commercial HVAC services have a longer runway, which we will see as we get into 2026.

DON LEVY Managing Director, Transaction Advisory Services

Kroll

Don Levy is a managing director in the New York office of Kroll, and a member of the Transaction Advisory Services team. Don has approximately 22 years of professional experience, encompassing M&A transaction advisory services, management consulting focused on distressed companies, real estate acquisitions analysis and public accounting.

BY DREW BRANTLEY

FRISCH CAPITAL

Afew years ago, we were 10 days before closing. The capital providers were all lined up. Due diligence was complete. Legal docs were almost done other than a few minor points and signatures. Everything was buttoned up and ready to close other than one small item on the list, the background check. Nevertheless, we were not

worried. Before the deal started, the Independent Sponsor had asked the seller, “when we run a background check, is anything going to show up other than a speeding ticket?” and the seller had said, “nothing”.

The background check came back and to say it was

bad is an understatement. Turned out the seller, who was going to be the CEO post close, had spent 5 years in a federal penitentiary for two felony counts of mail fraud and insurance fraud. When our Independent Sponsor client asked the seller why he didn’t tell him about it then when he had asked previously, he told him that he had paid an attorney $20,000 to wipe it off his record.

Nevertheless, the deal died that day, on the “one yard line”. It was a painful lesson learned.

Even though this is an extreme story, it is a true story. However, it is not the only time that we have had surprises show up on background checks that have impacted a capital providers’ view on a deal. Independent Sponsors have a lot on their plates when doing a deal. Especially managing costs and broken deal expenses. To this point, most Independent Sponsors prioritize due diligence costs that are both cost efficient, and may provide greater certainty to close and comfort around buying the business. Take it from us, it can come back to bite you in the long run if you don’t do a simple background check.

In many cases, the easy thing that can be done even before you sign the Letter of Intent (LOI) is to have a conversation with the seller. When you talk to them, we would encourage you to tell them that you are going to run a background check on them and key management (CEO, CFO etc.). Then ask them if there is anything that will come up that we need be aware of, other than speeding tickets. When we ask the questions, we list the

following specific items: judgments, bankruptcies, felonies, jail time, criminal charges, indictments, outstanding legal cases (personal or business), etc. that we need to be aware of and will show up on a background check?

Most of the time when you ask this question, with the follow-up that you will be doing a thorough background check, people will be open and forthright with you about anything in their background that might come up on a background check. This is the ideal scenario. If they bring something up, ask for the details, and then you and your capital providers can figure out if it’s a “Show stopper” or something you can live with. When you run the actual background check, it can then confirm what you heard.

When you get a background check back and there is something other than a speeding ticket, typically capital providers are looking for two types of items. The first is a major item such as a felony, jail time, bankruptcy. Things that would be either headline risks for them as an investor or might shape your view of them in a certain role. For example, if a CFO has filed for personal bankruptcy and there is not a good reason as to why, this might make you question if they will be a good steward of the company’s money and finances if they were not good stewards of their own money and finances.

The second items capital providers are looking for on a background check is a pattern of behavior. If someone has a myriad of smaller items either the same or different that come up in a background

check, does it point to a potential pattern of behavior or the character of that individual. For example, lets say an entrepreneur has started multiple companies in their lifetime, and a background check reveals a single judgment from a previous business. If they can provide you with the information, and that judgment was settled and the story around why, there are plenty of reasons

where you could get comfortable that this was a one-time isolated incident. However, if that same person’s background check came back and there were 11 judgments and they could not provide you with details of each judgment and the receipts showing they were settled, then that begins to look like a pattern of behavior that would cause one to question that person’s judgment and their ability to

be a good partner.

Everyone’s story is different. And there are plenty of items that will come up on background checks that do not raise a red flag for capital providers and Independent Sponsors. What you hope for is that the person is open about what the item is and can provide the necessary supporting information to confirm their story. People being transparent goes a long way. It’s when people hide things, or intentionally mislead you, that a small thing becomes a big problem.

Keep in mind that each capital provider is different. And just because an Independent Sponsor doesn’t think something is an issue, doesn’t mean that a capital provider will have the same view. And just because one capital provider takes a certain stance on an item, doesn’t mean another capital provider will have that same stance. You have to talk to everyone and understand that each capital provider is different.

So back to the original point, a background check

is arguably one of best “bang for your buck” due diligence items an Independent Sponsor can do, and the earlier the better. It is so impactful that we, Frisch Capital, now request that when we engage with a new Independent Sponsor client, that it is the first thing they do before we go to market to raise the capital for their transaction. If a skeleton is going to come out of the closet we want to know that as soon as possible, and not 10 days before closing as we did on that previous deal years ago.

There are a lot of options for background checks out there, and we do not endorse one firm over another. There are a lot of options, and some more cost effective than others. We have found that there are some good high level background checks that are very cost effective that will flag any major items in someone’s background. And then if you need or want to do a more in-depth background check later you can.

Regardless of which background check firm you choose to work with, or how much money you spend, do it early in the deal. Learn from our experience, do not wait to get the background check results right before closing.

DREW BRANTLEY

Managing

Director

Frisch Capital Partners drew@frischcapital.com 706-227-4144

Drew is a serial entrepreneur having started 5 businesses, sold a few and still owns some. He knows what it’s like to be in your shoes. He sees the Independent Sponsor model as the method executives and industry experts can take to own and run already established businesses. He now dedicates his career to helping individuals buy companies, find greater success and live life on their own terms.

BY HARRIS ADAM WITHUM

The One Big Beautiful Bill Act (“OBBBA”) introduces some of the most consequential depreciation changes in recent years, creating new planning opportunities for businesses investing in equipment, machinery, and certain real property. Building on the existing bonus depreciation regime, OBBBA not only restores 100% bonus depreciation but also expands the concept of immediate expensing to areas that historically received far more limited deductions.

This article provides a deeper look at the key changes, how they apply in practice, and what taxpayers need to consider as they plan capital expenditures over the next several years.

Under prior law, bonus depreciation was being phased down from 100% (in place from 2017–2022) to 80% in 2023, 60% in 2024, and ultimately 0% for property placed in service after 2026. OBBBA removes this phase-down and permanently reinstates 100% bonus depreciation for qualified assets placed in service after January 19, 2025.

Qualified property generally includes:

• Tangible personal property with a recovery

period of 20 years or less;

• Machinery and manufacturing equipment;

• Computers, servers, and technology equipment;

• Furniture and fixtures;

• Certain qualified film, TV, and live theatrical productions; and

• Water utility property.

This makes full expensing available for most capital investments that businesses routinely make.

Bonus depreciation depends on when an asset is acquired, not only when it’s placed in service.

Acquisition is determined by:

• The date the taxpayer enters a binding written

contract to acquire or construct the property; or

• The date construction begins (for selfconstructed property).

If a binding contract existed before certain key dates, the asset might be ineligible for 100% expensing. This is especially relevant for equipment purchased through long-term supply contracts, or for property with long lead times such as custom fabrications, turbines, vessels, or sophisticated machinery.

OBBBA retains two important taxpayer elections:

1. Electing out of bonus depreciation for an entire

class of property; and 2. Electing partial depreciation (40% or 60%) instead of 100%.

Taxpayers may use these elections to manage taxable income, preserve NOLs, or coordinate with state nonconformity.

Perhaps the most significant expansion in OBBBA is the introduction of Qualified Production Property (“QPP”), a new category that allows certain real property used in manufacturing or production to be fully expensed in Year 1.

This is a groundbreaking shift. Before OBBBA, commercial buildings were generally depreciated over 39 years, with no bonus depreciation. Now, portions of manufacturing facilities may qualify for immediate expensing.

QPP generally includes nonresidential real property used:

• For manufacturing;

• For production or processing;

• For refining or other industrial operations; and

• As an integral part of producing tangible goods.

To meet the definition, the property must be directly involved in production. Portions of a building that do not qualify are office space; administration; marketing; human resources; and storage not part of production.

complexity. A single facility may include both QPP-qualifying areas and non-qualifying areas, requiring a detailed cost-segregation-level analysis to allocate costs appropriately.

To be eligible for 100% expensing as QPP:

• Construction must begin between January 20, 2025 and December 31, 2028;

• The property must be placed in service by January 1, 2031; and

• “Original use” must begin with the taxpayer (i.e., it must be newly constructed or first used by the business)

These windows create an incentive for manufacturers to accelerate project planning and construction scheduling.

Long-term operational planning is critical, if QPP ceases to be used in production during a specified recapture period (likely 10 years):

• The taxpayer may be required to recapture part or all of the expensed amount;

• Repurposing, selling, or converting the building may trigger recapture; and

• Changes in production lines or redesign of a facility could unintentionally jeopardize qualification.

This distinction creates opportunities and

This may:

Immediate expensing dramatically reduces taxable income in the year of acquisition or completion. For large capital projects, this can create millions of dollars of near-term tax savings. Many companies will now find it more cost-effective to:

• Modernize production lines;

• Replace aging machinery;

• Expand capacity; and

• Build new manufacturing or processing facilities.

It is essential that Businesses carefully document the following:

• Construction start dates;

• Contract execution dates;

The return of 100% bonus depreciation and the introduction of QPP may fundamentally change how businesses plan investments, especially in sectors like manufacturing, logistics, industrials, and data-center operations.

• Original-use determinations;

• In-service dates; and

• Allocation of building components between QPP and non-QPP

Businesses operating in many jurisdictions will need to project state-by-state impacts, as not all states conform to federal bonus depreciation, and fewer still are likely to adopt QPP rules immediately.

HARRIS ADAM Senior Manager, Advisory Services Withum

• Reduce the benefit in nonconforming states;

• Create deferred-tax liabilities; and

• Increase compliance complexity.

OBBBA delivers a powerful combination of incentives: the return of full bonus depreciation and a completely new opportunity to expense qualifying real property used in production. For many businesses, especially manufacturers, this represents a substantial reduction in the after-tax cost of capital investment.

However, eligibility hinges on the specific facts of a project, and the rules contain a number of technical requirements, timing windows, and potential clawbacks. Companies should begin reviewing their planned capital expenditures now, map out project timelines, and evaluate whether construction or acquisition plans can be structured to qualify.

With thoughtful planning and careful documentation, businesses can capture significant benefits from the new law, potentially accelerating investment, improving competitiveness, and enhancing cash flow for years to come.

Withum is a forward-thinking, technology-driven advisory and accounting firm, helping clients to Be in a Position of Strength in today’s modern business landscape.

Wyatt Batchelor and Kevin Mulcahy, partners at MBN Brands, were recently interviewed by Paul Marino of Sadis & Goldberg. The MBN team has built a diversified operating and investment platform focused on acquiring, building, and scaling lower middle market businesses. MBN was formed with the goal of creating best-in-class platforms rather than one-off transactions, emphasizing long-term ownership, operational rigor, and disciplined capital deployment. Over time, the firm has expanded into multiple verticals, with a concentration in consumer and franchised businesses.

MBN Brands typically partners with founder- and family-owned companies that are at an inflection point—where professionalization, scale, and institutional processes can unlock the next phase of value creation. Rather than relying on financial engineering alone, the team focuses on building durable operating platforms through disciplined acquisitions, organic expansion, and selective partnerships. This approach has allowed MBN to assemble portfolios that benefit from shared infrastructure and experienced operating leadership.

In the lower middle market, the firm sees its role as helping entrepreneurs transition from founder-led operations to professionally managed

organizations. That often means upgrading systems, formalizing reporting, and strengthening management teams. MBN’s patient capital orientation gives operators the flexibility to reinvest cash flow into people, technology, and brand development, rather than prioritizing short-term outcomes.

Alignment with partners and operators is a core principle of MBN’s strategy. The firm structures its investments so that incentives remain longterm and management teams retain meaningful ownership. This partnership-first mindset fosters trust and accountability, allowing MBN to work closely with leadership teams as they navigate acquisitions, integrations, and multi-year growth plans.

With experience across a range of operating environments and a disciplined approach to platform building, MBN Brands continues to see opportunity in fragmented markets where scale and professionalization can drive value. As many founders seek thoughtful succession solutions, MBN is positioned to provide both capital and stewardship to businesses entering their next chapter.

For an in-depth exploration of Wyatt Batchelor and Kevin Mulcahy’s business insights, please watch the full video interview at SADIS.com

BY THOMAS SHEFFIELD & HUB INTERNATIONAL THOMAS CLARO STABLE ROCK SOLUTIONS

Private equity is built on the art of calculated risk: acquiring, growing, and exiting businesses to drive returns for investors.

But when an unexpected lawsuit hits, a tax position collapses post-close, or a cyberattack slows or shutters operations, even the best planned investment strategies can unravel. These risks— often invisible at first—can cost sponsors millions,

threaten IRR targets, and derail exits.

Enter insurance—not just as a passive requirement to close a deal, but as an active risk transfer mechanism that protects both the fund and its portfolio companies. For private equity firms and independent sponsors, engaging with an experienced insurance broker is no longer a backoffice function. It’s a strategic partnership that

helps identify, quantify, and offload risk at every stage of the investment lifecycle. Understanding “risk transfer” and the insurance that can be used to soften negotiation positions and manage unknown transactional liabilities is increasingly essential.

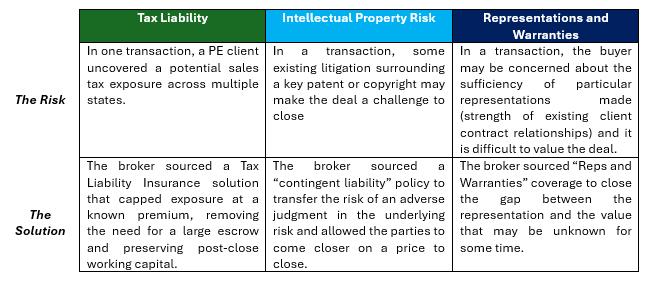

The world of private equity presents a unique set of exposures – the fund itself, its partners, and its GPs can be targeted by litigation or regulatory actions. Portfolio company boards (often with sponsor representation) can face personal liability. Even with planning, acquisitions can carry latent liabilities like unpaid taxes, cyber vulnerabilities, or undisclosed environmental contamination. Additionally, operational risks—like employment practices lawsuits or product liability—can sink performance or disrupt add-on integration.

Each of these risks can be addressed—or in some cases, fully transferred—through targeted insurance solutions. However, risk transfer isn’t just about “buying a policy.” It’s about examination and structuring comprehensive, customized coverage that fits within the PE firm’s investment strategy and financial model. Insurance brokers— in tandem with other consulting enterprises, have emerged as key partners in this process and help to identify risk and resources to help companies exit or build strategic value in the mergers and acquisitions process.

The insurance broker is far more than an intermediary. For private equity firms, a specialized broker acts as a transactional advisor, diligence consultant, underwriter liaison, and strategic risk partner. The process typically unfolds in four key phases:

Every deal begins with risk diligence. While sooner is always better in the deal, this sometimes begins only after being triggered by some key risk element or at the recommendation of one of the various advisors on the deal. Alongside legal, accounting, and tax advisors, the insurance broker advises on risks and risk transfer. The broker reviews deal documents, financials, and operational reports to uncover insurable risks. This includes:

• Reviewing the target’s historical claims, policy coverage, and uninsured exposures.

• Assessing corporate governance and board composition to identify D&O coverage needs.

• Flagging transaction-specific issues (e.g., pending litigation, tax uncertainties, environmental liabilities) that could become a problem postclose.

Review of portfolio company benefits program with eye on saving money for employees and broadening offerings.

Early engagement allows the broker to flag risks that can be insured and advise whether that insurance can be bound in time for closing. For example:

Once risks are identified, the broker works with the sponsor and legal team to build a bespoke insurance program which includes the following:

Transactional Risk Products:

• Representations and Warranties Insurance (RWI) to protect against breaches of reps in the purchase agreement.

• Tax Liability Insurance for uncertain or disputed tax positions.

• Contingent Liability Insurance for known but lowprobability litigation or regulatory exposures.

Operational Insurance for the portfolio company:

• Directors & Officers (D&O) Insurance, often a must-have at both fund and company levels.

• Cyber Liability Insurance, especially critical in healthcare, SaaS, or e-commerce investments.

• Employment Practices Liability (EPL) and Errors

& Omissions (E&O) coverage, depending on industry.

Fund-Level Insurance:

• Dedicated GP/Fund D&O policies to protect the management entity, partners, and advisors.

• Crime, fiduciary, and cyber policies for backoffice risk.

The broker’s job is to structure these layers so they complement each other—avoiding duplication or dangerous gaps. For example, a broker may negotiate coordinated D&O policies that specifically allow some coverage when insureds sue other insureds and shared retention limits to streamline claims if both the fund and a portfolio company are named in a lawsuit. This is a key risk in the PE space and one that has to be carefully addressed to get coverage.

Employee Benefits:

• Human Capital Management Program

• Health and Welfare

• Retirement/Wealth Management

With the program designed, the broker solicits quotes from top insurance carriers. In the world of private equity, this process is often bespoke and fast-moving. The broker plays a critical role in this process and acts as the advisor in the process.

Considerations for engaging the marketplace and underwriting process:

• Positioning the risk favorably: Preparing a detailed submission that highlights strong controls, governance, and sponsor experience.

• Negotiating policy terms: Beyond price, the broker advocates for key terms like policy limits, exclusions, tail coverage, and notice provisions.

• Managing underwriting calls: For RWI and specialty policies, the broker coordinates diligence Q&As and underwriter meetings, ensuring consistency with the deal team’s narrative.

In fast-paced auction environments, brokers can pre-negotiate “stapled” RWI policies to ensure that the buyer can close quickly without compromising protection.

The insurance relationship doesn’t end at binding.

A true PE-specialist broker will stay involved to help with various ongoing risk management considerations. Examples of what a broker will help

a client with post-binding their insurance program include:

• Coordinating add-on acquisitions into the existing insurance program.

• Monitoring claims, advocating on behalf of the sponsor, and managing coverage disputes.

• Adjusting limits and structures as portfolio companies scale.

• Aligning policy renewals with board meetings and financial reporting cycles.

Over time, the broker becomes a strategic advisor to both the deal team and the operating partners, offering portfolio-wide insights and cost efficiencies.

Example: One sponsor rolled up four service businesses into a single platform over 18 months. The broker created a “master” insurance program with consolidated limits and risk engineering services, saving over 20% in annual premiums while improving coverage breadth.

RWI in Action

In a platform acquisition, the buyer relied on seller-provided financials showing no pending litigation. Months later, an ex-employee brought a whistleblower lawsuit alleging financial misconduct during the seller’s ownership period. Because RWI had been secured and properly tailored to include this type of claim, the insurer reimbursed the buyer for legal defense costs and the eventual

settlement—avoiding a direct hit to the company’s balance sheet.

A mid-market sponsor faced a shareholder suit after a disappointing exit. The plaintiff claimed the fund breached its fiduciary duties by pushing an undervalued sale. Thanks to a tailored D&O policy that included “Side A” coverage and defense outside limits, the fund’s legal defense costs were fully covered, and partner reputations were preserved.

In today’s environment of high valuations, tight

regulatory scrutiny, and compressed hold periods, PE firms and independent sponsors cannot afford surprises. Insurance is no longer just a compliance checkbox—it’s a powerful tool to preserve value, unlock efficiencies, and make deals more competitive.

But the value of insurance is only as good as the strategy behind it. That’s why partnering with an experienced insurance broker who understands the pace, complexity, and nuance of private equity is critical. The right broker not only helps you transfer risk—they help you turn insurance into a strategic advantage.

THOMAS SHEFFIELD Executive Vice President Hub International

Thomas Sheffield currently serves as Executive Vice President & ProEx (Professional & Executive Risk) Leader of HUB International Northeast. Specializing in working with both Financial Institutions, specifically commercial and investment banks and Private Equity sponsors his focus is on helping clients mitigate exposure through development of comprehensive risks management programs and transferring risk through the use of insurance.

THOMAS CLARO Managing Director Stable Rock Solutions

Tom Claro is a licensed Attorney and Insurance Broker working with business owners, executives and other professionals to ensure efficient risk management solutions for companies.

Managing Director

Stable Rock Solutions

Tom Claro is a Managing Director at Stable Rock Solutions, where he leads the firm’s Insurance Services practice, providing business and personal insurance solutions. Tom brings more than two decades of experience across insurance, legal, and advisory roles, having held senior positions at USI Insurance Services, Marsh, Arthur J. Gallagher & Co., Swiss Re Corporate Solutions, and AIG, where he focused on complex claims, property and casualty risk, and client advisory services. He previously served as a Law Clerk at the National Football League.

In addition to his professional work, Thomas is the Head Football Coach at Chaminade High School. Earlier in his career, he was a player for 3 years in the National Football League, competing with the Arizona Cardinals, New England Patriots, Jacksonville Jaguars, and the Barcelona Dragons.

BY FRANK BUKOWSKI

GROUP

According to Novogradac (2025), the most recent data on the total number of Qualified Opportunity Funds (QOFs) tracks at approximately 7,800 funds with an estimated current value around $112 Billion. The most recent fund raising by the top 50% of QOFS accounts for $42.48 Billion of the equity raised.

OZ tax incentives made permanent

New rules should increase rural investment and raise awareness of the positive impacts of OZ, but will restrict the areas that qualify.

Ever since the creation of Opportunity Zones (OZ) as part of the Tax Cuts and Jobs Act of 2017¹, there has been a necessary push for extension of OZ tax incentives, as well as proposals for improvements such as impact reporting and increased incentives for rural zones². On July 4th, 2025, proponents got

their wish as a new version of OZ was contained within the One Big Beautiful Bill Act³ (OBBBA).

Opportunity Zones have driven billions of dollars of investment⁴ to underinvested areas throughout the country, with one study⁵ estimating that "the OZ incentive has roughly doubled the number of new housing units" in these areas. This new version comes with changes that are likely to affect which communities receive OZ investment and the form that investment takes.

One element of the OBBBA that could inspire a big sigh of relief is that it made Opportunity Zones tax incentives permanent. This not only eliminates the original sunset date at the end of 2026, but also means stakeholders won't have to worry about any other sunset date in the future.

Changes to OZ tax incentives

The original OZ tax incentives came in three forms⁶:

1. Deferral of tax on realized capital gains invested in a Qualified Opportunity Fund (QOF) by December 31st, 2026.

2. Exemption of tax on capital gains realized upon exit from a QOF if held at least 10 years.

3. 10% step-up in basis for capital gains invested by December 31st, 2021, and held for at least five years, with an additional 5% step-up in basis after seven years.⁷

The new version contains similar incentives, slightly tweaked:

1. Deferral of capital gains taxes for five years or when the investment is sold, whichever is earlier.

2. Exemption of tax on capital gains realized upon exit if held for at least 10 years. If the investment is held 30 years or more, the basis will be set at the 30-year mark.

3. The 10% step-up in basis at the five-year mark is now permanent, but the additional 5% at the 7-year mark was eliminated.

Deferral of tax on realized gains invested in a QOF for up to five years.

Exemption of tax on capital gains realized upon exit from a QOF if held at least 10 years.

10% step-up in basis for capital gains invested by December 31st, 2021, and held for at least five years.

Additional 5% step-up in basis after seven years.

Deferral of tax on realized gains invested in a QOF for up to five years.

Same exemption, but if investment is held 30 years or more, basis will be set at 30-year mark.

10% step-up in basis after five years is now permanent. Sevenyear step-up in basis is eliminated.

The return of the 10% step-up in basis should encourage more investors to take part, but some critics worry the elimination of the 7-year benefit will drive investors toward the types of shorterterm real estate projects⁸ that dominated the early years of the program⁹, rather than operating businesses10 that can drive long-term job creation.

Opportunity Zones direct investment toward lowincome communities. For OZ 2.0, the definition

of "low-income community" has become more restrictive, limited to census tracts where the median family income is less than 70% of the metropolitan area's median family income (for non-metropolitan areas, the standard will be the state median family income). This is reduced from 80% in the original OZ definition.

A tract can also qualify if it has "a poverty rate of at least 20 percent" AND the median family income "does not exceed 125 percent of the metropolitan area median family income" for those tracts within metropolitan areas, or "of the statewide median family income" for those tracts not in metropolitan areas.

As EIG notes11, this 125% cap "closes a statistical loophole that allowed a small number of highincome census tracts to qualify for OZ status." One of the biggest complaints about the original zones was that they included some areas that were already improving economically before OZ began12 This change will ensure OZ investment is directed toward the communities of greatest need, as was the original intent.

The OBBBA created the Qualified Rural Opportunity Fund (QROF). A QROF is any QOF "that holds at least 90 percent of its assets" in rural OZs. The definition for "rural" excludes any "city or town that has a population of greater than 50,000" and "any urbanized area contiguous and adjacent to" such a city or town.

incentives for investors: the 10% step-up in basis after five years is increased to 30% for QROFs. This is a big win for rural communities, as an extra 20% will surely be enough to draw the attention of investors.

While the OBBBA included much of what industry stakeholders were looking for, some things were missing, such as eligibility for non-capital gains or Fund of Funds structures. There were also changes some may find disappointing: the 7-year step-up in basis was eliminated, and the tax exclusion on new capital gains is now capped at 30 years.

One rule eliminated was that which allowed for the inclusion of non-low-income tracts if they were contiguous to designated Opportunity Zones. The repeal of this rule may benefit the legitimacy of OZ by making it less likely for OZ investment to end up in areas that don't need it, but it also means there will be fewer places where QOFs can invest, effectively shrinking the OZ map.

Also repealed was the special rule for Puerto Rico that designated all low-income tracts on the island as QOZs. This will mean fewer opportunities within Puerto Rico, as its zones will be selected based on the same procedure as those in the 50 states.

Rural areas have found it difficult to attract OZ investment13, and OZ 2.0 solves this with greater

JTC has been among many voices advocating for impact reporting requirements14 to help investors

select the best projects and to aid in improving OZ as a whole. OZ 2.0 includes two types of reporting requirements, those for the Secretary of the Treasury to supply regarding OZ's overall impact and those for individual QOFs to supply both to the Secretary and to their investors.

The Secretary's report must include information such as the number of QOFs, "the percentage of population census tracts designated as qualified opportunity zones that have received qualified opportunity fund investments," and "the aggregate approximate number of residential units resulting from investments made by qualified opportunity funds in real property."

The Secretary's report must also include impact measurements based on "economic indicators, such as job creation, poverty reduction, new business starts, and other metrics." Every five years, the report must include a comparison with a control group, using metrics such as unemployment rate, household poverty rate, and rates of affordable housing and home ownership. This should go a long way toward getting an accurate picture of how OZ is performing and how it can be improved.

QOFs must provide information on the location and value of assets held by the fund, a list of their investors, and “other information as the Secretary may require.” In addition, employment information must also be reported, including the number of monthly full-time employees and “such other indication of the employment impact of such trades or businesses as determined appropriate by the Secretary.”

Zones15, we at JTC believe this commitment to impact reporting will provide a substantial benefit to the Opportunity Zone community. Job creation data can help investors identify which funds and projects have the greatest impact, allowing the funds fulfilling OZ's legislative intent to stand out and potentially attract greater investment.

New Opportunity Zones will be designated July 1st, 2026. OZ 2.0 tax incentives begin six months later, on January 1st, 2027. This gives stakeholders plenty of time to evaluate the new map and encourage governors to choose tracts in an equitable manner. It also gives fund managers and investors plenty of time to evaluate the new zones and begin 2027 with a full understanding of the new rules.

EIG's analysis includes a note that "The current OZ map will remain in effect through the end of 2028, meaning that it will overlap with the new round of designations for two years." This extension ensures that those currently planning projects in tracts that will not be part of OZ 2.0 won't have the rug pulled out from under them, and has significance for how 2026 may look for the industry.

There is every reason to believe OZ will see an increase of investors once rural zones and updated tax incentives kick in. There will be plenty that investors, fund managers, and communities looking for investment can do during the next year to position themselves for what should prove to be an exciting environment under OZ 2.0.

As leaders in impact reporting for Opportunity

For a fund manager, the OZ 2.0 bill opens up

new pathways for impactful investments. It not only provides enhanced incentives and clearer guidelines, but also increases transparency and confidence in Opportunity Zones. With these improvements, funds can drive meaningful returns for their investors while actively contributing to the revitalization of local communities, a win-win for responsible capital and sustainable growth.

JTC Plc (“JTC”) is a global provider of fund, corporate and private client services. JTC administers more than $410 billion in assets and employs more than 2,300 people worldwide. JTC currently administers 72 Opportunity funds with an approximate AUA of $10 Billion. A leader in specialty financial

1. https://www.congress.gov/115/bills/hr1/BILLS-115hr1enr.pdf

administration, JTC serves markets characterized by high administrative complexity, elevated transaction security needs and challenging compliance requirements.

JTC does not provide legal, tax or investment or other professional advice and, whilst it may review and report upon such advice received, JTC does not give, accept or endorse and should not be understood to be giving, accepting or endorsing such advice.

2. https://www.jtcgroup.com/insights/changes-coming-to-oz-proposed-new-opportunity-zones-legislation/

3. https://www.congress.gov/bill/119th-congress/house-bill/1/text

4. https://www.jtcgroup.com/insights/opportunity-zones-have-done-what-they-were-created-to-do-will-that-be-enough/

5. https://eig.org/opportunity-zones-housing-supply/

6. https://www.jtcgroup.com/insights/opportunity-zones-5-year-basis-benefit-set-to-expire/

7. https://www.irs.gov/credits-deductions/opportunity-zones-frequently-asked-questions

8. https://www.dailyjournal.com/mcle/1727-joint-ventures-in-opportunity-zones-what-the-new-rules-mean-for-investors-and-developers

9. https://www.jtcgroup.com/insights/what-critics-of-the-opportunity-zones-initiative-get-wrong/

10. https://www.jtcgroup.com/insights/why-operating-businesses-are-key-to-the-long-term-success-of-opportunity-zones/

11. https://eig.org/opportunity-zones-2-0-where-things-stand/

12. https://www.jtcgroup.com/insights/how-to-get-opportunity-zone-investment-to-the-places-that-need-it-most/

13. https://www.jtcgroup.com/insights/how-opportunity-zones-can-be-used-to-revitalize-rural-communities/

14. https://www.jtcgroup.com/insights/why-the-impact-act-is-exactly-what-opportunity-zones-need-and-now/

15. https://www.jtcgroup.com/insights/best-practices-in-opportunity-zones-fund-administration-measuring-social-impact/

FRANK BUKOWSKI Senior Director -Institutional Capital Services

JTC Group

JTC Group (“JTC”) is a global provider of fund, corporate and private client services. JTC administers more than $410 billion in assets and employs more than 2,300 people worldwide. JTC currently administers 72 Opportunity funds with an approximate AUA of $10 Billion. A leader in specialty financial administration, JTC serves markets characterized by high administrative complexity, elevated transaction security needs and challenging compliance requirements.

As a leading global fund administrator with c.$410bn in assets under administration, including c.$54bn in real estate funds, we deliver seamless, end-to-end support at every stage of the fund lifecycle. With genuine real estate experience and a global reach, we go far beyond traditional fund administration. Let our expertise unlock the full potential of your real estate investments.

Find out more at jtcgroup.com/realestate

ISAE 3402 Certified

Listed on FTSE 250 c.$410 Billion USD Group AUA c. 2,300 People Global Platform

BY PAUL MARINO

SADIS & GOLDBERG

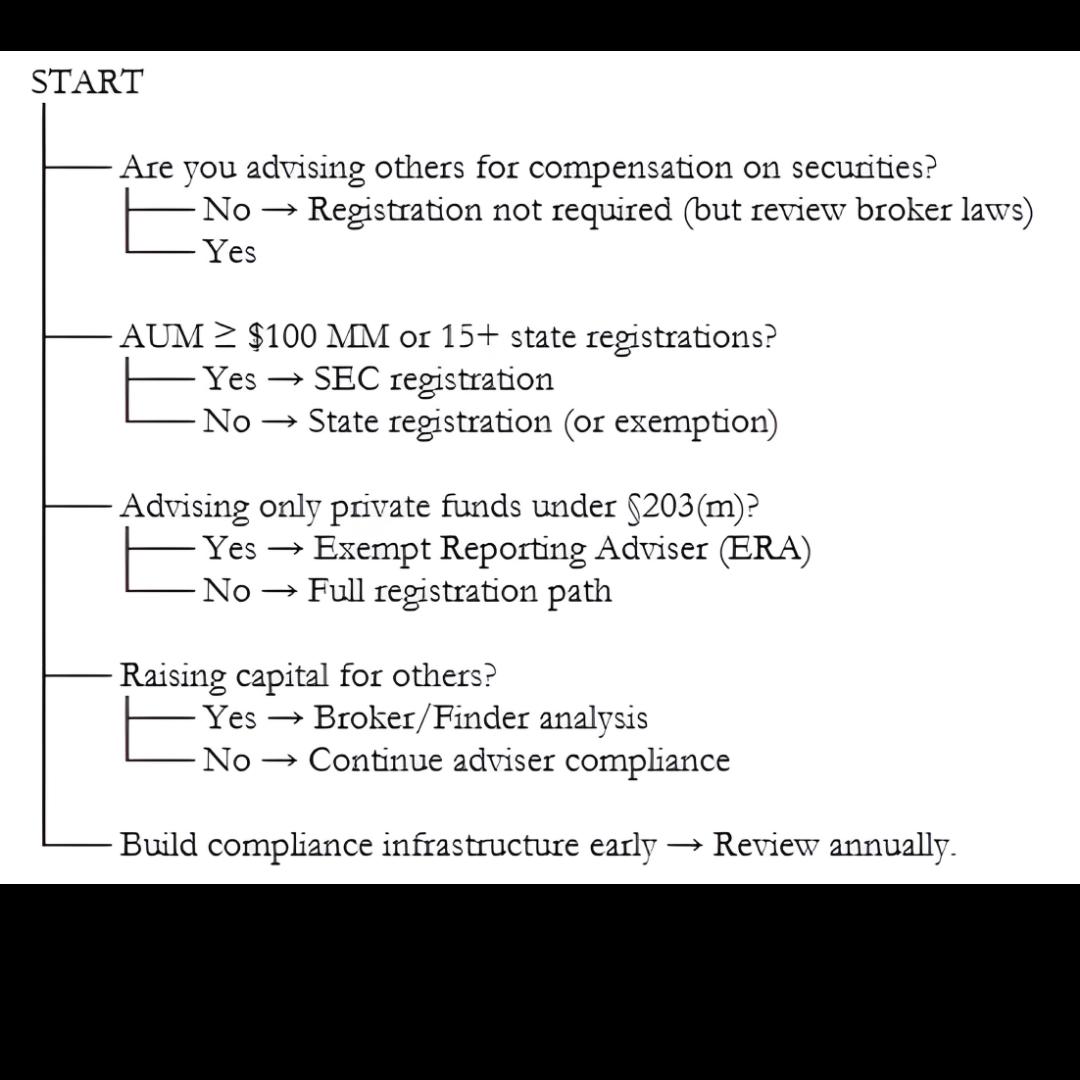

For Independent Sponsors (“IS”), the regulatory question of registration often falls into a zone of ambiguity. Unlike more traditional private equity fund managers, IS operate deal-by-deal or with minimal committed capital. The question of whether an IS’s activities will require the IS to register as an investment adviser (IA) or a brokerdealer can become a strategic cost and structuring hurdle.

• Sponsors should be aware of the investment adviser registration requirements under federal laws as well as the states in which they operate.

• Sponsors who manage a single platform over $150mm or multiple platforms that exceed a combined asset value of $150mm or more may be required to register with the SEC.

In this article we unpack the regulatory frameworks, map the “when,” explore the “why,” and provide practical considerations as to whether IS should register as investment advisers or a broker dealer.

The article focus primarily on the investment adviser registration question (which is often relevant for sponsors), and then touches on broker-dealer/ finder issues.

We will also examine state vs. federal registration issues and related exemptions from registration.

Since IS often form transaction vehicles (SPVs, LLCs, single-asset acquisitions) and raise capital on a deal-by-deal basis, it’s critical to determine whether the IS entity is acting in the capacity of an

investment adviser to those vehicles (which may trigger registration above certain asset threshold) or is simply acting as a principal/investor/operator who does not provide investment advice relating to securities (which likely would not trigger any registration obligations).

Under the Investment Advisers Act of 1940 (the “Advisers Act”), an investment adviser (an “Adviser”) is defined broadly to include any person who, for compensation, engages in the business of advising others as to the value of securities or as to the advisability of investing in, purchasing or selling securities.

Key federal triggers:

• Advisers who manage $100 million (or $25 million if the adviser has a place of business in New York) unless an exemption is available. Advisers who manage exclusively private-funds can typically take advantage of exemptions from registration upon filing as an “exempt reporting adviser” (“ERA”). An ERA exemption allows advisers to avoid full SEC registration, but they still must file a partial Form ADV, disclosing key info and adhering to anti-fraud rules, acting as a lighter regulatory

touch for smaller, specialized advisors. In the case of private equity funds, advisers will lose this exemption and must register with the SEC upon achieving “$150 million RAUM” (regulatory assets under management) threshold (post-Dodd-Frank). Advisers who manage exclusively venture capital funds may take advantage to this exemption without regard for RAUM¹

State regime: State investment adviser statutes and notice filings

• Unless an adviser is registered with the SEC as an “RIA”, advisers will be subject to potential registration obligations under state laws. Each U.S. state sets its own rules for Adviser registration as well as exemptions.²

• Many states have a “de minimis” exemption (e.g., fewer than certain number of clients, no physical office).³ For example, in New York: if you are an Adviser to less than six New York clients, the adviser is exempt from registration as an investment adviser with the state of New York. Based on principles provided under federal law, notably, a private fund is considered one client – and each investor in the private fund is not counted as a “client” for these registration purposes.

• States may also have certain exemptions for exempt reporting advisers (“ERAs”), similar to the federal ERA, based on model rules developed by the North American Securities Administrators Association (“NASAA”). Specific adoption, as well

as requirements to secure this exemption, will vary on a state-by-state basis.

• If required, state registration typically involves filing Form ADV via the IARD system

Which registration path generally applies to independent sponsors?

Given the frameworks above, what should independent sponsors consider?

States registration?

If the independent sponsor:

i. Is not registered as an investment adviser with the SEC (even if exempt as a federal ERA), for example, the independent sponsor has assets under management below the dollar threshold required for registration with the SEC,

ii. State law does not provide for a registration exemption.

then it may be possible that state registration or a state law exemption from registration is required..⁴

Federal (SEC) registration?

If the independent sponsor’s adviser entity:

i. Exceeds $100 million of RAUM ($25 million if sponsor has a place of business in New York) and manages both private funds and separately managed accounts or exceeds the $150 million

of RAUM and manages exclusively private funds, or

ii. advises a registered investment company or business development company, or

iii. has a multi-state footprint (and is required to register as an investment adviser in 15 or more states),then

federal registration via the SEC may be required or advisable. Below the thresholds mentioned above, independent sponsors will typically secure exemptions from registration by filing an abrieviated Form ADV as an ERA under federal and state laws.

Both state and federal?

Once an adviser is registered with the SEC, state registration is preempted—but there may still be state notice-filing requirements (so while full registration may not be necessary, some administrative state compliance remains).

The adviser still must be mindful of state antifraud statutes, solicitation laws, and state-level conduct rules (even if registered only federally). The preemption is registration—not conduct regulation.⁵

Thus, in practice, “both” can mean federal registration + state notice filings, but full dual registration is not required for advisers once federally registered; however, state-level issues (particularly broker-deal registration, capital raising,

securities offerings) remain. Of note, any time an independent sponsor receives “transaction based compensation” in connection with the offering of interests in a SPV or other entity, broker-dealer registration will typically be required under both federal and state laws.

Specific considerations for independent sponsors

Drawing from the regulatory roadmap above, here are topics especially relevant to independent sponsors in the middle/low-middle market (which is your practice focus) — and how you might advise clients or position your own activities.

1. Vehicle structure and the “adviser” role

If the sponsor is organizing and directing the assets (for example, making decisions in respect of the SPV) then adviser registration may be required. Conversely, if the sponsor plays a limited role (e.g., sources the deal, arranges capital, takes board seat, but the capital provider has full control over the investment decisions) then the adviser’s registration risk may be lower.

Capital-raising

The capital-raising component of independent sponsorship introduces a separate dimension: the issuer of the SPV is offering securities to investors, typically under a private placement (e.g., Regulation D). The sponsor must consider state securities (blue sky) requirements, broker-dealer regulation, and whether the sponsor’s services (arranging capital and sourcing deals) trigger broker-dealer registration or finder regulation under federal and

state securities laws.

Thus, independent sponsors often need to coordinate adviser registration (if relevant) with securities-offering regulation and broker/finder compliance.

In your focus area of middle/lower-middle market M&A (say transactions in the $5mm-$50mm EBITDA range), independent sponsors may start with smaller investor pools and limited AUM, which helps reduce the regulatory burden.

For example, a single platform transaction will likely reduce or eliminate filings for state security laws (of course depending on the structure of the deal and location of both the investors and the independent sponsor); however, growth in investor count, crossstate solicitation, or larger capital pools may shift the registration calculus quickly.

Since many independent sponsors intend to evolve (for instance, raise a micro-fund, launch a multideal platform, convert to a traditional private equity fund) your registration strategy should anticipate “what happens when we scale.”

Key considerations:

• If you anticipate surpassing the $150 million AUM mark (or whichever threshold applies) you may decide to register with the SEC proactively rather than scramble later. Remember, however, that registration with the SEC is typically only permitted once an adviser has at least $100

million of RAUM.

• If you are currently registered or are required to register multiple states (15+ states) your analysis may shift toward federal registration (some rules permit advisers required to register in 15 or more states to register with SEC instead).

• Your vehicle structure will matter: if you begin managing multiple SPVs or pooled vehicles (rather than deal-by-deal), the “adviser” function may become more central and therefore subject to more scrutiny. Also, for purposes of the private adviser or ERA exemptions for registration, SPVs with a single investor are considered a SMA, causing the sponsor to lose the ERA exemption and likely requiring registration under federal or state laws.

Costs of registration include:

• Preparation of Form ADV (and amendments)

• Compliance program implementation (written policies & procedures, code of ethics, chief compliance officer)

• Possible state-level reporting/filing fees and annual renewals.

• Ongoing examination risk (by SEC or states).

• Operational burden of tracking AUM, client count, cross-state activity.

Benefits of registration include:

• Enhanced investor confidence (especially institutional/private-fund investors) who may prefer working with registered advisers.

• Pre-empting state registration burdens if

federally registered (one umbrella).

• Clearer regulatory regime and avoidance of inadvertent non-compliance.

• Better positioning if scaling up to larger deal sizes, pooled funds or more complex vehicles.

Risks of not registering when required:

• Civil penalties for non-compliance, including possible disgorgement of advisory fees charged to private funds under management. The MVA memo warns of “regulatory landmines” for noncompliance.

• Reputational risk with investors.

• State securities regulators may assert jurisdiction and impose headaches.

Finally, the question an adviser role sufficiently limited and the investor base sufficiently small/ controlled that we can remain under state registration (or even exempt) until a threshold is surpassed; and then build in triggers for migrating to SEC registration once scaling thresholds are crossed.

1. Generally, if an adviser manages $100 million or more in regulatory assets, registration with the SEC will be required (subject to various exceptions).

2. See, New York State Attorney General https://ag.ny.gov/investment-advisers-faq?utm_source=chatgpt.com

3. See, https://www.investopedia.com/ask/answers/09/series63-050509.asp (visited 11/18/2025)