Michael Kornman & Grant Kornman

Partners

Align Collaborate

Michael Kornman & Grant Kornman

Partners

Align Collaborate

By Paul Marino

Marino By Seth Lebowitz

By Ronald J. Sylvestri

By Robert Geitz & Greg Jacobs

The firm maintains a diverse, businessoriented practice focused on investment funds, litigation, corporate, real estate, regulatory and compliance, tax and ERISA.

Drawing on the experience and depth of our lawyers in these distinct areas, we can leverage each lawyer’s industryspecific knowledge to help our clients succeed. This collaborative approach brings to the table a collective insight that contributes to sensible, efficient resolutions, and allows us to remain attentive to the cost and time sensitivities that may be involved.

Sadis’s clients include domestic and international entities, financial institutions, hedge funds, private equity funds, venture capital funds, buyout funds, commodity pools, and numerous businesses operating in various industries around the world.

BY PAUL MARINO SADIS & GOLDBERG

Same as the old boss. The classic line from the Who’s, “Won’t Get Fooled Again,” is what many M&A professionals are thinking as it comes to Trump 2.0 . But in 2024 are we similarly situated as we were in 2016?

Some things are similar inasmuch as we came out of the GFC with tepid growth and that continued for about 5 years. Recently, we came out of the pandemic with tepid growth that continued (and continues); and both exogenous events caused a massive updraft in federal deficits. However, after the GFC interest rates were 0 (one of the greatest moments of my young adult life was when my 5/1 ARM adjusted and the notification letter said my interest rate was zero) and inflation was at or near the two percent target (in fact there was great concern that we would move towards some type of Japanese stagflation or deflation). Of course, not everything was tied to accommodative interest rates, there were other factors as well: the fracking boom took full effect and lowered energy costs, cheap goods from overseas (mostly China) flowed into the USA and

the American consumer (and Wal-Mart) was the greatest beneficiary of those cheap goods.

Nonetheless, while history does not repeat itself, it does tend to resemble other parts of the timeline (especially the older you get); however, as John Kenneth Galbraith once said: “We have two kinds of forecasters, the ones who don’t know and the ones who don’t know they don’t know.” I aspire to be neither. Instead I’d like to briefly discuss some data points on what really moves individuals to buy, sell or hold: sentiment.

According to the latest data as of the end of the third quarter 2024, the consumer confidence index (“CCI”) stood at 98.7. That’s a slight downward tick from Q2 of 2024 which was 100.4; and further it is a large gap from the prepandemic reading of 132.6 in February of 2020.

While the CCI is hovering around neutral (100 handle), the Michigan Small Business Owners survey has surged to a nearly 3 ½ year high. The National Federation of Independent Business (NFIB) said on Tuesday its Small Business

Optimism Index jumped 8.0 points to 101.7 last month, the highest level since June 2021. Now, while this survey is somewhat skewed because a majority of small business owners lean/vote Republican (and in case you hadn’t heard Donald Trump won the race for the White House and the GOP will control Congress), it is a good indication of what to expect in 2025 as perception becomes reality. For example, according to the survey, “the share of small business owners expecting the economy to improve increased by 41 points, to 36% of all respondents (basically nearly 1/3 of all small business owners are highly optimistic) the largest since June 2020” and to hammer home how sentiment can drive transactions (i.e., M&A, capital expansion, etc.), the number of small business owners expect to increase capital expansion is at an almost 3-1/2 year high. Conversely, the “uncertainty index” dropped 12 points from a record high of 110 in October. Lastly, there was a marked increase in respondents who expect higher sales growth and decrease in respondents believing inflation is the top issue. (As an aside, as one can tell from parsing through the data, sentiment numbers have been low/negative for some time so any move upward (or to say in a positive direction) is going to appear amazing (like going from 0 to 1 you’ve doubled output)—reminds me of the Doors lyric: “I’ve been down so very damn long—it looks like up to me.”)

To be fair, all is not rosy, especially if you look at the direction of the country poll. As I write today (12/10), according to the Real Clear Politics poll the direction of the country has a negative thirty-six handle (-36). Concededly, the polling for direction of country is done from likely and/or registered voters so a lot is dependent upon who answers the call (I guess you can say that for any poll but when you’re dealing

with likely voters often it’s whomever has a home phone and who answers that phone in the middle of the day—generally older citizens (if I could drop a meme in here it would be Grandpa Simpson: Old Man Yells at Cloud). Nonetheless, anecdotally it appears direction of the country polls will start to trend in a positive direction provided that inflation (especially fuel) stays at or goes down from where it is currently. And, not that this dovetails with how main street feels about the country, the stock market is usually a leading indicator and as such it appears that Wall Street believes the country is heading in the right direction.

Lastly, according to Jeffries bank lending standards remain tight but have likely peaked. What this means is simple, banks start lending to companies which will spur expansion, which will create competition for loans and push the cost of commercial loans down. In tandem with commercial credit, private credit will (likely) start to expand and rates/fees compress as competition starts to swing leverage to the borrower.

To that extent, some fund sponsors such as Dustin Martelo of Groverton, a real estate and private fund partnership, believes the real catalyst for the loosing of lending standards is as follows: (i) rates decreasing, (ii) loosing of internal underwriting criteria; and (iii) accommodative regulations (i.e., a thawing of the current regulatory regime). Hard to counter the foregoing positions, especially a more accommodative regulatory body but how long will it take to reverberate through the economy is the question.

So what does all of this mean for corporate and M&A, private equity and independent sponsors?

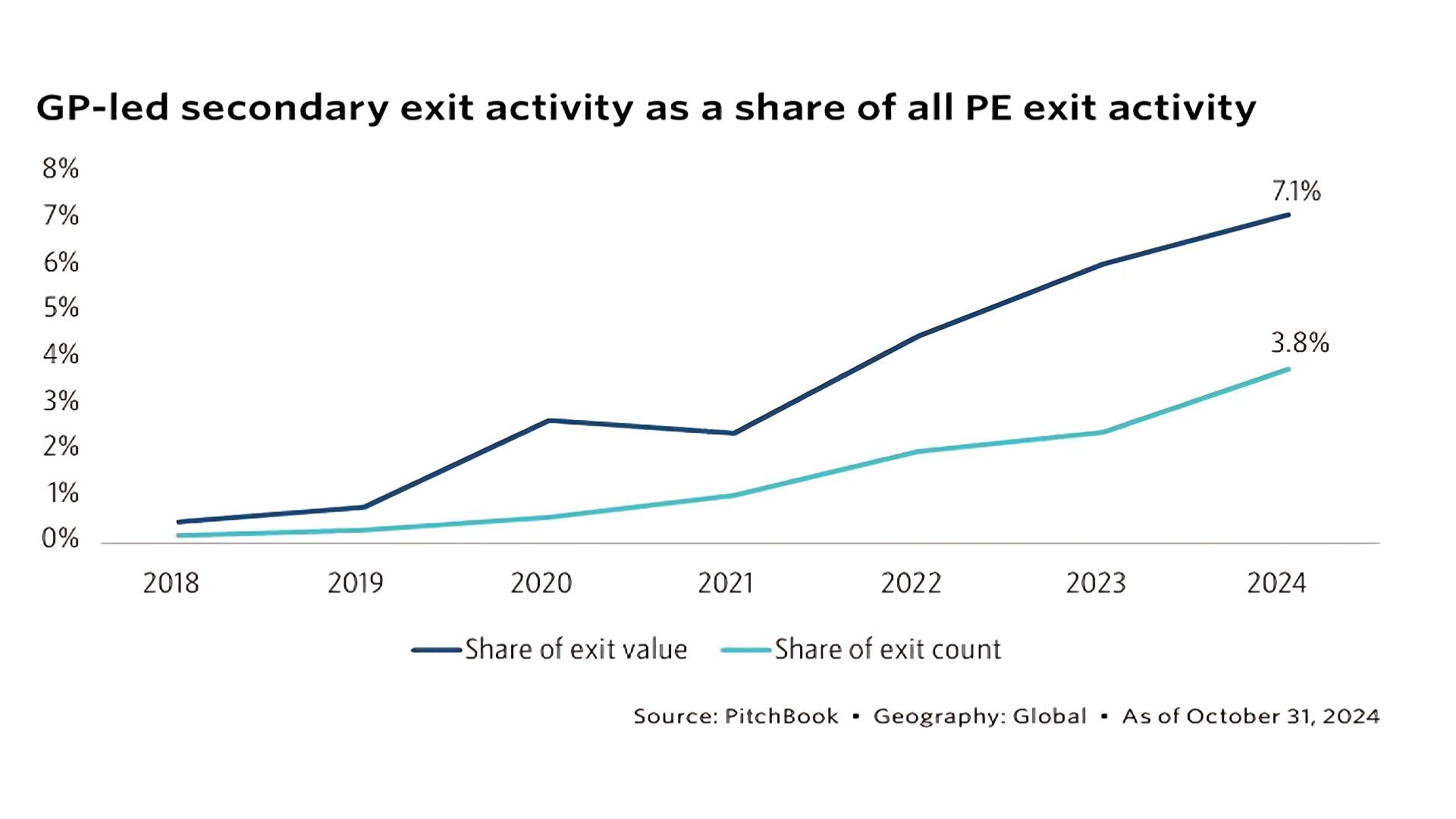

Before I give my final wrap up, let me add one more thing into the mix: the rise of secondary funds. Secondary vehicles, either continuation or LP vehicles are a growing sector of PE and a dynamic and growing part of the alternative space (including providing LPs with much needed liquidity).

Secondary exit activity has increased dramatically since 2021. Of course, this increase coincides with the decrease in platform dispositions and increasing frustration of LPs due to lack of liquidity but as often is the case, the animal spirits of the market corrects for a shortfall. As the chart provided by Pitchbook indicates, GP led secondaries (which is different than LP’s selling their interest to a buyer) has grown dramatically over the last few years (with an average roll/exit of the platform of five years) and according to Pitchbook the entirety of the secondary market will increase 40% from 2022 to 2028 (500bn to 700bn); AND secondaries continue to grab larger share of total exits.

In conclusion, based upon the data that we know, all signs point to clear and bright skies ahead but as Mark Twain once said, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

1 Jefferies has a great piece on the economic outlook of the USA entitled—Trump 2.0.

2 The last bit of this sentence reminds me of something read many years ago written by the great Alan Ableson (https://en.wikipedia.org/wiki/Alan_Abelson) the long time editor of Barrons and writer of its influential column, Up and Down Wall Street: quoting (Anglicized quote—so not an exact French translation) Charles Baudelaire “The greatest trick the Devil ever pulled was convincing the world he didn’t exist”; “The second greatest trick was the US sending worthless dollars to China in exchange for real goods.”

3 For those keeping score at home on the CCI: anything below 100 is negative, at 100 is neutral, and above (or +100) is positive sentiment.

4 https://www.conference-board.org/topics/consumer-confidence/June-US-CCI; the highest number ever achieved was 144.7 in May of 2000.

5 https://www.reuters.com/markets/us/us-small-business-sentiment-nears-3-12year-high-november-2024-12-10/ (visited, 12/10/2024)

6 https://www.investing.com/news/economic-indicators/us-small-businesssentiment-nears-312year-high-in-november-3763272

7 https://www.youtube.com/watch?v=bJuDD93JbOw

8 https://www.realclearpolling.com/polls/state-of-the-union/direction-of-country (visited, 12/10/2024).

9 https://www.youtube.com/watch?v=tJ-LivK4-78&t=17s

10 This is from Jefferies 2025 Economic Outlook report. If you’re interested in reading the entire report please contact Jefferies.

11 https://www.linkedin.com/in/dustinmartelo/

12 https://pitchbook.com/news/reports/q4-2024-pitchbook-analyst-note-gp-ledsecondaries (downloaded, 12/10/2024). Study authored by Nicolas Moura, CFA titled: GP-Led Secondaries, Sizing the market for exits to continuation vehicles

BY PAUL J. MARINO

SADIS

& GOLDBERG

I wrote this a few years ago (who am I kidding—I wrote this 11 years ago—when you get older a few just means a lot) and things changed a lot at Tony’s Barber shop. Because of Covid he began to take appointments and people liked that instead of waiting for an hour or more on a first come first serve basis to get your hair cut. While the reservation system is more convenient, we lose some of the communal appeal of the barbershop; you never knew who you were going to run into and you always knew you’d run into someone that you hadn’t spoken to in a while or someone you never knew. I still see Tony once a month on a Friday and it remains a highlight—he is a true professional and gentlemen.

A friend asked why am I am republishing this story and the answer is because it is an important reminder (especially to me), that no matter what you do, tunnel vision is the best practice and remain semper praesens; focus on and care about what’s in front of you.

Anyone who knows me well knows that I am a creature of habit and a very loyal person. While I haven’t lived in Stamford, CT (my hometown) for about twenty-four years, I continue to go to the same barber, Tony’s Barber Shop, from the time I was about eleven years old. For the last thirty years, Tony has been a virtual trip back in time with its unchanged, beautiful wood paneled walls and its wooden chairs in the waiting area, fixtures that never fail to spark memories of my numerous past visits. Some of my more memorable visits include my crew cut and flat top phase when I was younger (which Tony approved of), and my long hair phase when I was college age (which Tony most certainly and expressly did not approve of). Having my hair cut elsewhere (as I once did in college) was a sin in Tony’s eyes, tantamount to infidelity.

I remember one visit, in particular. One day, when I was about twenty-two, after waiting for one hour to see Tony (Tony doesn’t take appointments), I asked Tony if he ever got nervous because there were so many people waiting in the wooden chairs for a haircut. Tony

responded with a valuable piece of advice he may not even have intended to dispense. He simply said that regardless of whether there were two or twenty people lined up for a haircut, he does not worry, he only concentrates his focus on the person in the chair. While I did not ask him any further questions about his waiting customers, I took this to mean that Tony’s only concern was the customer he was servicing at that moment. Tony approaches the task of his particular skill with laser focus on perfection. And many customers will attest to Tony’s perfect haircuts. In addition, all of his customers, myself included, will also attest to feeling that they had his full and undivided attention. That he took pride in the job he was doing, and that the customer in his old fashion chair was worthy of the same amount of Tony’s care, whether there were no waiting customers or a room full of waiting customers.

Tony taught me to focus on servicing the needs of one client at a time, and to ensure that the service I provide to that client (and each client) is perfect (or as close to perfect as I can get). Thank you, Tony, for teaching me such a valuable lesson.

PAUL MARINO Partner

Sadis & Goldberg

pmarino@sadis.com

Paul Marino is a partner in the Financial Services and Corporate Groups. Paul focuses his practice in matters concerning financial services, corporate law and corporate finance. Paul provides counsel in the areas of private equity funds and mergers and acquisitions for private equity firms and public and private companies and private equity fund and hedge fund formation.

“Drew,what industries are hot right now? Where should I be focusing?”

BY DREW BRANTLEY Frisch Capital Partners

For 28 years Frisch Capital has worked exclusively with Independent Sponsors helping them raise equity and debt for their transactions, and I still get this question at least once every week. To answer – I’d like to break the question down into two parts.

PART 1 – WHERE SHOULD “I” BE FOCUSING?

Before I can answer that – I need to know more about YOU and your group. “What value do you bring to the deal besides just a Letter of Intent (LOI)?”, or asked differently “how does your background relate to the deal?”. This determines directly where you should consider focusing. Every Independent Sponsor has their own unique background, with both successes and lessons learned, that lends them to being the right fit for a deal. This personal history can include everything from finance and M&A experience, operating roles and entrepreneurial experience, industry or operational expertise, turnaround, carveout or special situations experience, and much more. Given this breadth of personal contributions, when we, Frisch Capital, look at how this personal history brings specific (measurable) value to their transaction. This, along with two other metrics are what we base all new business acceptances on.

1. Independent Sponsor Value Add – what value does the Independent Sponsor bring to this

specific transaction. There are a lot of ways that this can manifest itself from C-suite and operating experience, to transaction experience, industry or operational vertical expertise and more. Are they the right ones to execute and grow this business?

2. The Thesis – what is the Independent Sponsors thesis as it relates to the deal. How does their experience and history and or team that they have set up lend to this being executed well?

3. The Deal – does the company, structure, valuation, and transaction itself make sense and does it fall within a realm of what we feel capital providers will be excited about.

In our experience, the more these three things align and make sense the greater the likelihood a capital provider is going to want to finance or invest in the Independent Sponsors deal.

In regards to the “the Independent Sponsor Value Add”, when you look at a company and a deal, you have to think very specifically about how your background and experience fits and/or aligns with the deal. I.e. you have to be able to prove your value as it pertains to that particular transaction. Proving your value can manifest itself in many different forms. As a base you will need very good industry knowledge. You don’t have to have years of operations experience in an industry (though that can be very helpful). You will have to have a depth of industry insight and know-how that truly makes you an expert. We have had clients who are specialists in rollups and M&A integrations, who have had to learn new industries to apply their genius of growth. We always see them asking and answering this question: “how can I become smarter than the average person on a specific industry or company niche?”. Transaction experience, research, talking to people in the industry, industry conferences, articles, deal or transaction experience, are just a

few ways our clients gain expertise or knowledge in an industry that they have not previously worked or transacted in. The best way to learn about an industry is to pick up a phone and start calling companies in the industry and asked questions. It’s amazing what you can learn, and what people will tell you if you just ask questions and listen.

We have found that many of our clients have “rounded out” where they are weak. Especially when a client is taking their expertise (operational, financial) into a new industry, we see great success when they partner or pull in an advisor with deep industry knowledge. This could be operating partners or people with specific operating experience and knowledge in this new industry. Similarly, when we have clients with deep operating industry experience and expertise, they often partner or hire to fill the gaps where they might be lacking (good M&A attorney, financial analyst to run models, buyside investment banker to find more companies to roll up etc.).

In summary, “Where should “I” be focusing?” you must consider and articulate what it is you bring to the transaction, how your background can align with a specific deal, and its projected strong growth. And should you find “holes” in what is needed to be successful, begin the process to fill the gaps with third party advisors, expand your knowledge, or potentially even bring in a partner on a specific deal.

Part 2 – What Industries are HOT right now?

There is a lot of money in the market now and all kinds of niches that capital providers chose to invest in. However, as an Independent Sponsor you must be careful not to fall in love with just “any deal”, but instead fall in love with deals that can get funded!

As we think about working on deals and/or in

specific industries, Frisch Capital always thinks about what the dynamics are, both in structure and in industry that will most likely get more than one group interested in the deal. While it only takes one group to do your deal, many of us have seen capital providers walk away from deals for one reason or another in due diligence. If you only have one capital provider available, then you could be at risk and “up a creek without a paddle”. So what industries, and industry dynamics, are going to get the attention of the most capital providers?

In our opinion we strongly support and encourage our clients to be looking at asset light industrial or business services. This could be blue, grey or white-collar businesses. These businesses are the backbone of the US economy. They are installing, fixing, servicing, maintaining, replacing and restoring, testing, measuring, and monitoring things for companies. These could include anything from infrastructure, IT, healthcare, education, facility services, residential or commercial services, oil and gas, and many more.

Now regardless of the niche, end market, or type of service work the company could be providing, there are three main types of revenue that we see service companies have, one time project-based revenue, reoccurring revenue and more recurring revenue.

When buying a service business, it is important to understand the amount of revenue from each of these three types of revenue.

One time project-based revenue can include installation, implementation, replacement etc. This work is usually a one and done type event with a finite timeline and cost to the project. In many instances this type of revenue can be high margin and very nice revenue. However, you are constantly having to chase more business. With that said, project-based revenue is often the feeder system for the more reoccurring or recurring service work that is steadier and more consistent.

As an example, installing a new HVAC system for an office building is a one-time project, but can lead to a long-term service with a quarterly maintenance contract to maintain the HVAC unit (recurring). Or the unit breaks down and stops working 5 years later, resulting in an emergency service request (reoccurring).

Recurring service revenue is usually revenue that means you are doing work on some type of predetermined frequency and that work is needed, required, or wanted on a frequent basis. Recurring service work often has a contract in place

that can be one or more years, and often renews automatically. Usually this is a lower revenue ticket than the installation or initial project-based work (if there was any) and can sometimes be lower margin than the initial installation work (however this is not always the case). This service work overtime is considered by many capital providers to be more stable and dependable because there is a predetermined frequency, despite it being lower revenue. It is considered stickier than installation work because it is more effort for a client to switch than it is to just stay with their current service provider, as long as you are doing a good job.

Reoccurring revenue is service work that is not on a regularly scheduled basis, but is still service work. Often this could be an emergency call when a system is broken down and not working. For example, an HVAC unit stops working. But there could also be non-emergency service work where there is just not a recurring contract in place. For service companies, this can often be a large component of their service revenue, and sometimes it is hard for a founder owned company to differentiate between recurring and reoccurring revenue given that a scheduled recurring service call can result in additional reoccurring revenue due to additional repairs and work that is uncovered.

When evaluating service companies, it is not uncommon for some service companies to have primarily one time project-based revenue because it is often higher revenue and potentially higher margin. So, when evaluating companies, you would like to see a mix of all types of revenue demonstrating a company’s ability to convert onetime revenue into service work, both long term service contracts or unscheduled service work.

There is not a perfect mix, but in general the more recurring and reoccurring service work the better.

Especially attractive is to see that the amount of recurring and reoccurring service revenue is growing year over year as the company grows.

In summary, “Where should I be focusing?”. You should be focusing on things that align with your background or expertise, or in a niche where you are developing an expertise and have a targeted thesis.

And “What industries are HOT?”, asset light industrial and business service companies is a broad umbrella that a growing number of capital providers are interested in. This has the potential to allow you to have multiple capital providers interested in your deals, not just one.

DREW BRANTLEY Managing Director Frisch Capital Partners

Michael and Grant Kornman, co-founders of Align Collaborate, are transforming the private equity landscape by specializing in equity solutions for independent sponsors. Their innovative approach stems from a decade of firsthand experience in the independent sponsor model. Recognizing the unique challenges faced by these investors, the Kornmans created Align Collaborate to provide a flexible, efficient, and responsive partnership tailored to the specific needs of this growing segment.

Their approach draws on deep industry insight and a commitment to filling gaps left by traditional capital providers. Align Collaborate bridges the strengths of various investor types—private equity funds, family offices, and institutional partners—without their typical drawbacks. This model emphasizes alignment, speed, and strategic

collaboration, offering sponsors a partner who truly understands their world.

By focusing on key business attributes like profitability, demand resilience, and growth potential, the Kornmans ensure their investments are poised for long-term success. Additionally, they remain committed to supporting their partners beyond funding, offering resources to enhance operations, leadership, and scalability.

For an in-depth look at how Align Collaborate is redefining the independent sponsor model, explore the full interview.

BY RONALD J. SYLVESTRI

Private credit involves private lenders lending directly to borrowers rather than through banks or investment banks. Private lenders are non-banks, such as funds, family offices, wealth management platforms or high-net-worth individuals. Borrowers are usually small and mediumsized enterprises (SMEs) with limited access to the public credit markets. Even before the Global Financial Crisis of 2007-2009, some of these SMEs had difficulty obtaining credit from conventional lenders. This is a result of the declining number of banks, additional banking regulations and the small scale of SME transactions for most banks. Because these lenders provide swift and creative solutions to meet their business growth requirements, SMEs have turned to private lenders to meet demand. Private credit investments have the potential to offer attractive, uncorrelated returns with mitigated risk compared to other investments.

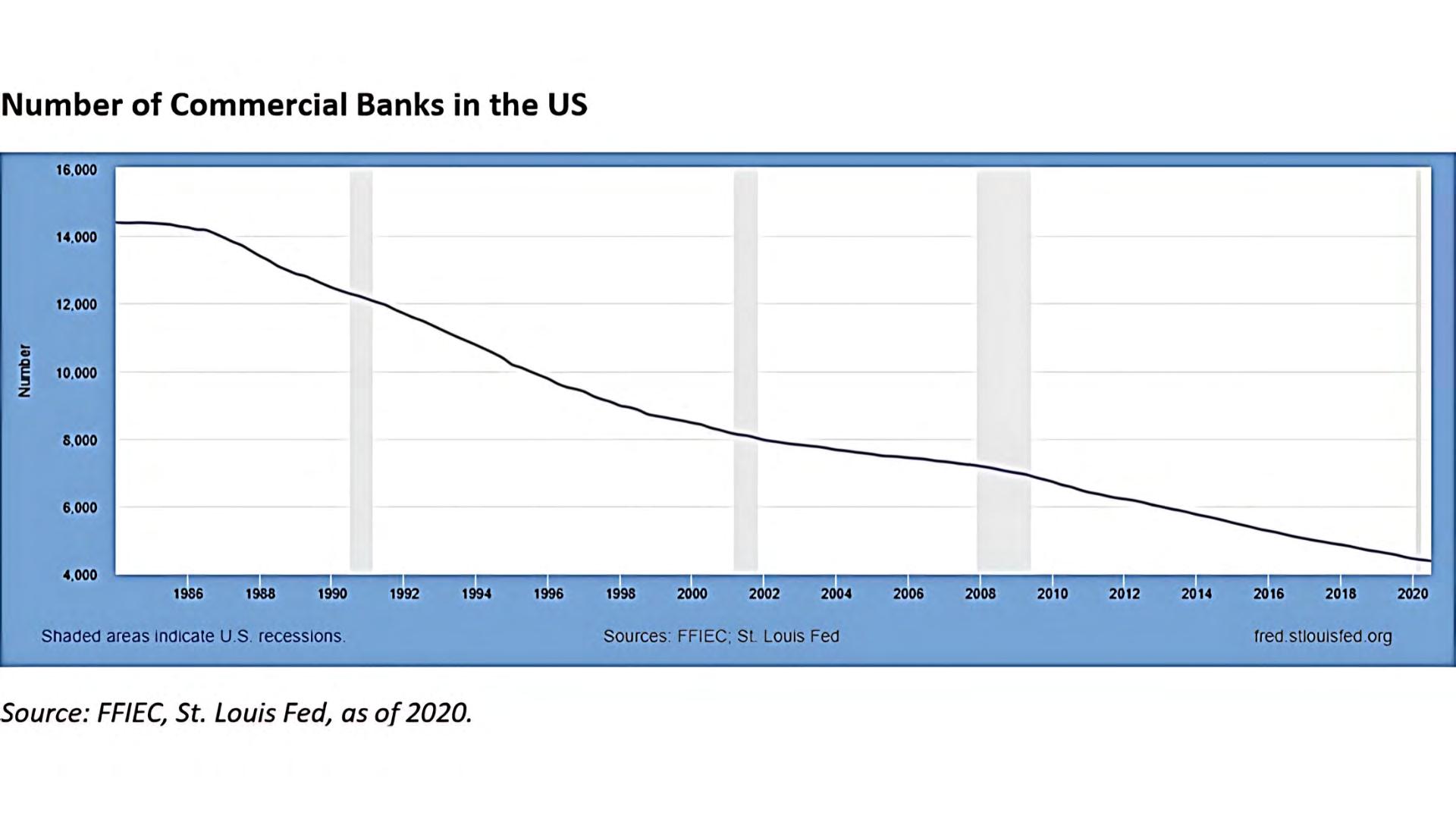

The investment opportunity in private credit is largely fueled by the reduced number of commercial banks and a corresponding decline in

lending to SMEs. The repeal of the Glass- Steagall Act led to a consolidation of commercial banks and their assets. Since 1984, the number of commercial banks in the U.S. has plummeted from 14,400 to just 4,127 by the fourth quarter of 2022, according to the Federal Deposit Insurance Corporation (FDIC).

As a result, SMEs have struggled to secure loans from traditional banks, which now prioritize larger transactions. This gap in financing has created a significant opportunity for private credit lenders. While banks began to shift away from lending to SMEs even before the 2007-2009 financial crisis, the introduction of post-crisis regulatory changes further limited their ability to lend to smaller businesses. These regulations, which include stricter capital ratios and leverage limits, increased the cost of servicing loans, making it less profitable for banks to work with SMEs. Despite the financial strength and growth potential of many SMEs, these regulatory burdens have left a void that private credit lenders are now filling.

Demand for smaller private credit loans, typically

ranging from $10 million to $50 million, remains high. Data from the FDIC highlights how regulatory pressures have led to a reduction in small loans issued by banks, opening the door for private lenders to step in and address this underserved market.

While traditional banks shifted their focus from lending to SMEs prior to the Global Financial Crisis of 2007-2009, regulatory changes were implemented that governed banks and resulted in fewer banks’ lending to SMEs. These rules require heightened regulatory scrutiny, with stricter capital ratios and leverage limitations, resulting in high servicing costs for loans and less availability of loans to SMEs. This made it less economical for banks to lend to SMEs, despite a market of strong and growing borrowers; however, this has allowed private credit lenders to step in and address that void. The need for smaller private credit loans ($10-$50 million) is illustrated by the following graph from the FDIC, which shows how the regulatory burden has reduced the

amount of small loans made by banks.

Asset-based lending (ABL) involves loans made against assets pledged as collateral security that can be sold if the borrower defaults. Asset-based lenders generally assess the value of the collateral and make advances (loans) at less than the liquidation value of the collateral. The relationship between the amount of the loan and the liquidation value of the collateral is called the loan-to-value (LTV). The lower the LTV, the greater the protection against borrower default. Asset-based loans have some common characteristics which are:

• Typically, a term loan for liquidity against longerterm assets or a revolving line of credit for working capital requirements.

• Secured by hard or financial assets; underwritten with emphasis on capital preservation and income generation.

• Focus on LTV, rather than underwriting cash flows or enterprise value.

• Provide some tangible asset protection against borrower default.

Cash flow lending involves a loan made to a business that is secured by a company’s expected cash flows. The collateral securing the loan is not typically hard assets, but the equity of the company after other more senior debt obligations have been satisfied. The key financial metric used in assessing the creditworthiness and the amount of the loan to the business is the quality and size of its EBITDA.

• Sourced through private equity sponsors, boutique investment banks, commercial banks, attorneys,

accounting firms, past lending relationships, etc.

• Secured by future cash flows (typically measured by EBITDA)

In addition to asset-based lending and cash flow lending, there are specialty types of Private credit that are tailored to unusual or niche markets.

Examples of these follow.

• Distressed Debt: Involves loans made to companies that are in financial difficulty—either bankrupt or insolvent, or close to it. These lenders use special knowledge about restructuring and the bankruptcy laws to turn a company around outside of bankruptcy or to restructure a company through bankruptcy. Debt provided in this context is structured to have seniority over all other debt (and equity) and to permit effective control over company management. Distressed debt investing affords very high returns—at commensurate high risk.

• Venture Debt: a type of debt financing obtained by early-stage companies and startups. This type of debt financing is typically used as a complementary method to equity financing. Venture debt can be provided by both banks specializing in venture lending and non-bank lenders. Venture debt issuers tend to discount cash flow and tangible assets and focus on intangible assets like patents, etc.

Venture debt is frequently used as an alternative to equity financing instruments like convertible debt or preferred stock. As a debt instrument, venture debt has a higher liquidation priority than equity. Many venture debt deals include warrants which may be exercised to purchase common stock in the borrowing entity. Unlike equity instruments, using debt financing prevents the further dilution of the equity stake of a company’s existing investors,

including its employees.

• Syndicated Loans: these loans involve many lenders, are generally quite large in scale (>$100 million), are often rated and are usually publiclytraded. As such, these loans are priced much lower than private credit. Even if they are originated by a non-bank, syndicated loans are not generally considered private credit.

As the private credit market grows and matures, there are increasing opportunities for investors to add this asset class to their portfolios for

diversification and returns. Investors may access private credit in several ways:

• Private Credit Funds: Accredited investors can invest directly in private credit funds through a specific manager and a specific private credit strategy. Investors need to perform due diligence and consider the track record of the manager, the fund structure, liquidity provisions, the investment process, the third-party service providers and other operational due diligence procedures.

• Interval Funds: These funds are a closed-end fund structure that continuously offer new shares for sale but repurchase existing shares only during specific periods. These structures are registered

1940 Act Funds. Interval funds can invest in private credit investments and funds to create the yield they need to distribute to investors. Interval funds must make periodic repurchase offers of no less than 5% of the outstanding shares at intervals of three, six, nine or twelve months, and must hold enough liquid investments to cover such repurchases.

• Custom Portfolio of Private Credit Funds:

Investors can access an investment platform to create a custom portfolio of investments in a variety of private credit managers. The platform provider sources the investment opportunities, performs the private credit manager due diligence, negotiates capacity, addresses minimum investment thresholds and can create a legal structure that allows for an investment in a pool of private credit managers. The platform provider typically handles all the administration and technology for investors to research funds, build portfolios and creates marketing material.

• Co-investments: Many private credit managers will sell a portion of a specific investment to investors. In this case, the investor is purchasing a specific interest in a specific transaction that will continue to be managed by the investment manager. While this type of investing may limit

RONALD

diversification, investors may be able to create the desired exposure to a specific asset class with its own return characteristics.

As a veteran of Private Credit, Jeff Haas President of SR Alternative Credit, sees a future that will continue to include alternative lenders. The ability for SME’s to access traditional lending has steadily deteriorated over the past 20 years as more and more banks exit the space for regulatory reasons. His opinion is that the regulators identified a mismatch between assets and liabilities at banks (short term deposits versus loans that mature in years) which was a risk that needed to be mitigated. The regulators attempted to address by imposing regulations that made it difficult for banks, especially smaller banks, to engage in SME lending. These SME borrowers are a significant part of the US economy and exactly the borrowers that need financial resources to maintain their companies. Therefore, alternative lenders, who can better match the assets (capital) and liabilities (loans) via fund or company structures, have stepped in to fill the void, private credit is here to stay.

SYLVESTRI

Founder & President

Quail Ridge Asset Management

As president of Quail Ridge Asset Management, Mr. Sylvestri has provided value-added strategic assistance to private equity and other alternative asset managers, and advisory services for small to midsized companies

BY SETH LEBOWITZ

SADIS & GOLDBERG

Imagine the following situation. The founder (or another shareholder) of a privately-held corporation is considering an offer to buy the company’s shares for cash. Negotiations over the price soon show that seller and buyer disagree on the value of the company being sold, with the seller convinced that the company is worth more than the offered price and the buyer reluctant to increase the offer. This gap is proposed to be bridged by agreeing to a contingent increase in the purchase price based on the performance of the company subsequent to closing of the sale (such as income, sales, or another metric or combination thereof). This kind of “earnout” mechanism can allow sellers to benefit from a purchase price that is potentially significantly

higher than they are otherwise being offered and can allow buyers to be confident that any increased price will be justified by post-closing performance.

Under certain conditions, a seller who receives rights to contingent future payments as consideration for the sale of shares in an “installment sale” for federal income tax purposes may defer taxation on a portion of the total gain recognized in such sale until the receipt of future payments in future years. Under the installment method of reporting gains from the sale of property, installment payments received by a seller are made up of three components, each with its own character for tax purposes. The

three components of an installment payment are: (1) return of basis, (2) gain and (3) interest (whether provided for by the contractual terms or imputed by the tax law ). The portion of each installment that represents gain to the seller is taken into account in the year the seller receives that installment. (For the sake of simplicity, the remainder of this discussion will assume that in all cases adequate interest is stated and will not discuss the interest payments further, as the tax accounting rules for interest are a complex topic separate from installment reporting of gains.)

To illustrate the way in which gain is recognized in a situation, such as an earnout, in which the amount and/or timing of the future payments

is not known at the time of the sale, it is helpful first to look at the way gain is recognized in fixed-price installment sales. In a fixed-price installment sale, a proportionate amount of each installment payment is treated as gain, and the remainder of each such installment is treated as a return of capital. The portion of each installment that is treated as gain is determined by multiplying the dollar value of that installment by the “gross profit ratio,” which, subject to certain adjustments (ignored here for the sake of simplicity), means the total amount of taxable gain on the sale (taking into account all installments), divided by the total sales price.

Although the same method of calculation cannot

be applied when the total amount of payments is unknown at the end of the year of sale, the regulations governing contingent payment installment sales provide rules for determining how much of eawch installment is treated as gain and how much as return of basis depending on whether the installment sale calls for (1) a maximum sales price (such as an earnout capped at a maximum dollar amount), (2) no maximum sales price but a determinable period over which contingent payments can be made (such as an earnout that provides for a percentage of the target company’s profits for a stated number of years, but without a maximum dollar amount) and (3) neither a maximum amount nor a fixed time period (which is less common for an earnout). Although the mechanics of these methods is beyond the scope of this discussion, an earnout provision in connection with the sale of stock can usually be handled by the installment method.The

The advice of counsel, including tax counsel, is

crucial in planning, negotiating and documenting the sale of a business, and those terms always need to take into consideration the unique circumstances of the parties and the transaction. But in general terms, what are some of the issues possibly affecting a seller’s tax treatment that a seller should keep in mind when considering and negotiating an earnout provision in the transaction documents?

The inclusion of certain terms with respect to the earnout provision can result in the installment method being inapplicable, and therefore sellers should be aware of this and avoid the inclusion of such terms if they desire installment treatment. For example, in order to be eligible for installment treatment, the obligation to make future payments must be an indebtedness of the purchaser of the property the gain from which is to be reported on the installment method. Therefore, a seller should not accept an agreement in which installment payments are the obligation of a party other than the purchaser. A third-party guarantee

of the purchaser’s obligation, however, will not necessarily preclude installment sale treatment.

If the installment obligation is payable on the demand of the seller, or if the installment obligation is readily tradable, then the seller’s receipt of the obligation will be treated as a payment, rather than a promise to make future installment payments, and deferral of gain from the sale until future installments are received would be precluded. An obligation to make installment payments that is secured directly or indirectly by cash (or cash equivalents) is also treated as a payment rather than a promise to make future installment payments, with similar results –deferral of gain from the sale until future installments are received would be precluded.

The installment sale rules, when the conditions for their application are met, are mandatory unless the seller affirmatively elects out of installment sale treatment. Thus, a seller who wants to report gain

under the installment method should not elect out of the application of these rules. In addition, sellers should consider including a provision in the relevant contracts that requires both the seller and the buyer to report earnout payments as consideration for the sale under the installment method.

Although installment sale treatment allows the deferral of a portion of the gain from the sale to future years in which installments are received, a seller should be aware that in certain circumstances, the tax law imposes an interest charge on the seller’s deemed deferral of taxes resulting from installment reporting. This interest charge is imposed with respect to installment obligations in excess of $150,000 that arose during the taxable year and that remain outstanding as of the close of such taxable year, if the total of all such obligations is in excess of $5 million. Although these conditions reference the year in which such obligations arose, once the interest charge is

imposed with respect to an obligation, the interest charge applies for any future year in which some part of that obligation remains outstanding. If this interest charge applies to a seller utilizing the installment method to report gain from a sale of stock, it could negate the economic benefit to the seller of deferral of gain. Complications arise in the case of a contingent installment obligations (such as how to determine the face amount of an obligation that is wholly contingent), although the IRS considers these obligations to be subject to the interest charge rules, and therefore sellers should consider whether and in what manner these rules would be applied to them in the context of an earnout provision.

A seller who, in addition to receiving an earnout right, also enters into an agreement to perform services for the acquired business post-sale should consider the terms of both the earnout and the services agreement in order to reduce the chances of the IRS arguing that some or all of the amounts received under the earnout should be treated as compensation income, rather than as sale proceeds. The difference between these two treatments can be significant, in terms of tax rates (ordinary income vs. long-term capital gain) as well as the application of employment or selfemployment taxes (applicable to compensation income, but not to proceeds of sale of stock). At the extremes, the difference between the two is clear. Where a seller with an earnout right totally separates from the business, or where an employee with no stock ownership signs an employment contract with compensation linked to company performance post-sale, there is little, if any, room for the IRS to argue for a different tax treatment. However, in certain circumstances it may be less

clear whether some or all of the earnout payments are compensatory (i.e., for services) rather than consideration for the sale of shares. If, for example, a seller agrees to a contract to stay on as CEO of the acquired business under the new ownership, attention should be given to the possible risk of an unfavorable characterization by the IRS. If the CEO’s compensation under the employment agreement is less than would be expected in the case of a CEO without any earnout rights, if the seller’s earnout rights are linked to a requirement to perform or continue performing services, for example, this may call into question whether for tax purposes all or a portion of the earnout payments should be treated as compensation rather than sale proceeds.

As noted above, it is always advisable that a buyer and seller be contractually bound to treat the earnout payments as additional consideration for the sale, and this situation highlights the importance of such an agreement. If, for example, a seller seeks sale treatment on the earnout payments and the buyer reports to the IRS that the payments are compensation (which a buyer might have incentive to do in order to try to make such payments tax deductible), the inconsistency could undermine the seller’s desired treatment, and also could serve to highlight the issue to the tax authorities.

Another consideration that should be taken into account is whether an arrangement intended to be a contingent payment of sale proceeds could be treated instead for tax purposes as a continuing interest (or a newly-acquired interest) in the business being sold. In many, if not most, cases, an earnout right is not likely to be recharacterized as a continuing or newly-acquired interest in

the business, although the possibility should be kept in mind because in certain cases the courts have upheld such characterizations. In the event that an intended earnout representing additional contingent sale proceeds is instead treated as a continuing interest in the business, installment treatment for the sale would be unavailable.

Possibly worse would be the treatment of an earnout as a newly-acquired ownership interest in the purchaser, because in such a case the seller would likely be taxed twice –once on the receipt of the new ownership interest, and again when what are intended to be earnout payments are received.

As a simple example, a seller’s right under an earnout to deeply subordinated (such as being subordinated to trade creditors of the purchaser) payments from the purchaser that are deeply subordinated and that have no maximum dollar

amount and no set termination date could be recharacterized as equity of the purchaser rather than as an installment obligation of the purchaser. Although standard earnout terms do not usually lend themselves to such a characterization, each situation is unique, and the possibility should be kept in mind so it can be avoided if possible.

An earnout right can be a useful tool in structuring the sale of a business, and if attention is given to the terms, can have benefits to the seller from a tax perspective. This article discusses some of the things that a seller should keep in mind, although since each situation is necessarily unique, sellers should be sure to discuss any earnout provision, along with the other terms of the sale, with their tax counsel.ab

1 This discussion assumes an individual shareholder of a privately-held C corporation, who holds the shares as capital assets and has a holding period in the shares of more than one year. However, similar tax principles may be applied to sales of shares of S corporations and of partnership interests, as well as to asset sales, with certain variations for each different situation..

2 The tax law recognizes that whenever some or all of the payments to the seller are deferred, the seller is, economically, compensated for the time value of money during the period of deferral and therefore it treats a portion of each future payment as interest for both the buyer and the seller if the contract does not call for stated interest that results in a yield no less than the “applicable federal rate” published by the IRS for the month in which the sale occurs.

3 This $5 million threshold is determined at the partner level rather than at the partnership level in the case of a partnership that holds installment obligations, and spouses generally are treated as separate persons from one another for this purpose.

SETH LEBOWITZ Partner, Sadis & Goldberg slebowitz@sadis.com

Seth Lebowitz is a partner in the firm’s Tax group. Seth advises clients on the tax-efficient planning and execution of a broad range of transactions, with a particular focus on the formation, operation and investing activities of private equity and hedge funds. Seth has experience with:

• Domestic and international tax issues relating to fund structuring

• Joint ventures and partnerships

• Corporate and real estate investing

• Lending Securities trading

• Distressed investing

• Financial products

BY MARK SINATRA AspenHR

In a value-creation landscape where organic growth is stalling, roll-up strategies are gaining momentum. By acquiring and integrating smaller companies into a unified entity, CEOs and private equity funds can drive accelerated value creation. However, beneath the allure of rapid growth lies a critical challenge: managing human resources effectively. From payroll integration to employee benefits harmonization, HR plays a pivotal role in ensuring the success of roll-ups and resulting value creation.

This article explores the considerations, potential

pitfalls, and best practices involved in navigating the HR aspects of roll-up strategies, offering a roadmap for seamless transitions.

Before embarking on a roll-up strategy, it’s crucial to evaluate the target company’s HR infrastructure, roles, and policies. This evaluation helps identify areas of alignment and divergence between the acquirer and the target. Questions to consider

include how many HR team members the target company has and what their roles are, whether there are overlaps with the acquiring company, and whether the target company has documented policies on PTO, performance reviews, or paid leaves. It is also essential to assess how these policies compare with the acquirer’s policies. Understanding who manages HR and whether key functions are outsourced or internally handled will help streamline future integration.

Common pitfalls to avoid include restarting employee tenure, which can disrupt earned benefits like PTO, inconsistent compensation for employees with similar roles, overlapping job titles without clear standardization, and implementing rapid changes to policies without thoughtful change management.

Smooth payroll operations are fundamental to maintain employee trust and morale during acquisition transitions. Evaluating the existing payroll and HR technology systems of the target company is a vital step. This includes understanding what payroll system is currently used, how it aligns with the acquirer’s system, how frequently employees are paid, and how time and pay changes are tracked. Additionally, it is important to determine whether other HR tools, such as applicant tracking systems or performance management software, are in place and if they integrate effectively.

systems, while the HR information system should feature security compliance, 360-degree feedback tools, and advanced analytics. Streamlining all systems will simplify operations and enhance scalability.

It is important to have one system-of-record that houses payroll and employee information across all companies in one place. Otherwise, updating multiple systems is time-intensive and poses risk.

Potential pitfalls of not planning properly postacquisition include missing payroll due to misaligned pay periods and overlooking payroll tax account setups in multiple states.

Transitioning employee benefits is often one of the most complex aspects of roll-ups. Conducting a thorough benefit gap analysis and harmonization process ensures a smooth transition. This involves comparing the benefit offerings of both companies to identify disparities in health plans, employer contributions, and 401(k) options, as well as evaluating the implications of new health plans, network providers, and changes in 401(k) contributions or vesting schedules.

Common challenges include overlooking network coverage or prescription drug compatibility in new health plans and increasing employees’ out-ofpocket costs due to lower employer contributions.

to ensure employees get credit for any dollars paid towards a deductible if they switch plans prior to the renewal date.

A structured approach is key to managing transitions effectively. The process begins with understanding the target company’s offerings and identifying opportunities for alignment. Next, a deep analysis is conducted to evaluate the costs and implications of changes. Engaging leadership and creating a transparent, multi-channel communication strategy is critical. Finally, changes are executed on a structured timeline with clear ownership and ongoing communication.

Effective planning and communication is crucial to mitigating employee concerns and fostering a positive transition. Ample notice should be provided, along with a clear timeline for changes. Messaging should be employee-centric, explaining the rationale behind changes. Multiple communication

To ensure success, the payroll system should integrate with accounting and time reporting

It is critical to plan well in advance and merge benefit plans to align with one of the plan’s renewal dates so as to minimize disruption. It is very important

MARK SINATRA CEO

methods, such as in-person meetings, emails, and videos, should be employed to ensure everyone is informed. Lastly, it is important to pro-actively engage leaders at the target company to get their feedback on any proposed changes well in advance.

Roll-up strategies offer significant growth potential but require careful planning and execution, particularly in HR. By evaluating infrastructure, harmonizing benefits, and adopting a structured change management approach, companies can mitigate risks and pave the way for successful integration. A thoughtful communication strategy ensures that employees remain engaged and supported throughout the process—ultimately setting the stage for long-term success.

AspenHR is a white-glove PEO provider that specializes in helping PE-backed companies in navigating acquisitions with expert HR support, payroll, large group benefits and HR technology. For more information, visit www.aspenhr.com or contact us at sales@aspenhr.com.

Mark Sinatra is the CEO of Aspen HR, where he leads the strategic direction and growth of the company. Prior to Aspen HR, Mark was CEO of Staff One HR, where he led the company through a period of substantial growth highlighted by achieving the Inc. 5000 list of fastest-growing companies for four years in a row, and culminating in Staff One HR’s sale to its largest privately-held competitor, Oasis Outsourcing, in December 2017

BY ROBERT GEITZ & GREG JACOBS

Capital Dimensions

What is risk? Risk is a threat to success. Just as there are many varieties of success, there are many categories of risk. Importantly, the idea of “risk” means different things to different people.

Risk management is a full-time job for any financial institution or investment entity. Based on our lengthy prior experiences at big financial institutions and investment businesses, in client-facing businesses we have seen institutional risk managers focus on two broad objectives: 1) Protecting the business from regulatory constraints, lawsuits, and/or threats to its reputation, and 2) Modeling and measuring the chances that a proprietary capital business will lose money. In other words: 1) What are the threats to the business’s good name and ongoing ability to operate – and what steps need to be taken to protect the institution in those respects? and 2) How much money can the business lose if a key variable – sometimes market volatility, sometimes a downside market move –changes outside of expectations?

We have much respect for the practice of institutional risk management. We have worked closely with a number of exceptional risk managers, and recognize their critical roles in financial businesses and investment businesses.

Private market participants – including family offices, entrepreneurs and private businesses, among others – share certain risk management objectives with large public institutions. But, because of the heterogeneity of these private businesses, the spectrum of private risks, concerns and preferences is much broader. Risk concerns can span the range from threats to capital to interest rate exposure to sensitivity about generational asset transfer to counterparty trustworthiness.

Individuals tend to be the key owners and decisionmakers at private endeavors – in contrast to larger-scale public enterprises with multi-layered management structures, multiple signoffs and committee oversight. As they mature, private enterprises can encounter ‘new’ or uncustomary risks that fall outside the experience of the business owners that have been dedicated to creating businesses and assets of value.

We recognize that successful businesspeople, successful entrepreneurs, successful investors don’t need help in managing their holdings. By definition, the product of their work speaks for

itself. But many parties tend to encounter matters that require expertise and experience outside of what they regularly apply to their investments and businesses.

Examples of such situations include, but are not limited to:

• Circumstances or structures with elevated complexity

• Scale/growth scenarios, and business adaptations

We recognize that specialization is required to resolve complex situations. The dynamic marketplace is full of surprises – for good and for ill. History instructs us that certain risks can take you by surprise, and that critical risk factors, when misunderstood or unskillfully harnessed, can lead to potential outcomes:

• That keep a business leader awake at night, or

• That can lead to regret over choices not made earlier.

We also recognize that not every risk can be hedged, or should be hedged. In practical terms, decision-makers can recognize that markets are not designed to be safe. After reviewing objectives, and the spectrum of threats to realizing those objectives, it can make sense to accept certain risks. Of course, risk tolerance is relative – this will vary from business to business, and from business leader to business leader.

In conceptual terms, the general idea of risk can be divided into passive risk and active risk.

Active risks: “Taking or avoiding risks is considered to be an active decision: Chief executives decide to invest in moon-shot research and development projects, portfolio managers pick assets destined to outperform, and laypeople buy total permanent disability insurance.” (Source: “Active and Passive Risk Taking;” Universität Innsbruck; König-Kerstin, Lohse, and Merkel, 2021)

Passive risks refer to “a wide range of situations of economic relevance in which a change in risk exposure is not a consequence of an active decision, but rather the result of inaction. Not making the necessary investments to stay competitive, not rebalancing portfolios, and not buying insurance clearly affect the risk exposure of companies and individuals, yet are the result of abstaining from taking an action. Future outcomes from these decisions become the result of passive risk-taking.” (König-Kerstin, Lohse, and Merkel)

Without sounding preachy, we believe that it is sensible and prudent to identity and assess the spectrum of risks – active and passive – and to address the following:

• Set a priority for risk acceptance: Which risk will hurt the most if the risk occurs? Which risk will hurt the second-most? Etc.

• Whether and how to tolerate the risk

• The cost for mitigating the risk

• Decide whether the cost of risk mitigation is worth the potential benefit

• Act accordingly

• Monitor exposures and costs on an ongoing basis

Academic economists classify “systematic” risks as risks that are intrinsic to the market. These are also referred to as undiversifiable risk, volatility risk, or market risk. These contrast to risks that apply to specific businesses or exposures.

Examples of systematic risks include the following:

• Interest Rates

• Political Regime Changes

• Policy Changes

• Geopolitical Events

Many, but not all, systematic risks can be hedged – with options or other derivatives. Hedges come with costs and counterparty exposures. The cost of the hedge, the credit quality of the counterparty, and the terms and conditions of the hedge contract all need to be analyzed and assessed before a hedge is implemented.

The costs of certain risks – risks that may be overlooked or risks that may have been ignored – can compound. Think of the compound consequences of failing to seek medical attention for an apparent change in one’s physical being –which, when overlooked, can get worse without treatment. At an extreme, a physical change that isn’t addressed by a medical specialist can have mortal consequences. We think you need to take care of your health – with the counsel and advice of your physician. By the same token, we think you

need to seek the counsel and advice of a specialist on potential risks to your business and your assets.

One example of this syndrome could consist of a foregone decision to purchase an interest rate cap on a large floating rate debt obligation that would result in increases in interest expenses in a risingrate scenario. Another example could relate to an investment portfolio with a concentrated exposure to a single asset or asset category. If unexpected news arises about the category – in this example, a single property type – such a portfolio concentration can result in meaningful drawdowns. Consider the wealth destruction imposed upon office properties by the Pandemic and resulting work-from-home behavior patterns. After experiencing these events in 2023, is it possible that that a real estate investor with a portfolio concentrated in Class A CBD office properties might wish that he had lightened up at 2018 office property valuations?

Certain investors and businesses may undertake regular self-examinations of potentially unaddressed risks. On the other hand, the presence of a skilled, experienced advisor to identify and analyze risks that may be overlooked can result in peace of mind, and elevated security.

The dynamic evolution of society continues to introduce new risks – which may also result in opportunities – on an ongoing basis.

• Technology Innovation (latest example: Artificial Intelligence) – resulting in new methodologies and new products, destroying old methodologies and old products

• Inflation

• Escalating Energy Prices (demand-drivers

include AI requirements for power)

• Accelerating Productivity (resulting in competition for specialized Labor)

While only the parties with a crystal ball know exactly what the future holds, we think it makes sense to pay attention to the changes in a dynamic marketplace.

Certainly, the stock market has dramatically elevated the value of businesses and product manufacturers focused on Artificial Intelligence. As well, professional investors in real estate have focused on building and acquiring industrial space to contain the data centers used to contain the development and production of AI.

But only recently has it become evident that the real estate investment component represents an incomplete picture of the requirement for the AI “factory.” Access to power may be more important than the real estate per se. “Data centers are no longer a real estate business. They are actually a power-first business,” [the leader of KKR’s digitalinfrastructure investments] said. “The status quo is no longer acceptable in solving this.” (Source: “Wall Street Giants Bet on AI and Power,” The Wall Street Journal, October 31, 2024). A year ago, the critical connection between AI data centers and access to power was evident to only a few parties.

It is easy to recognize that different parties can be subject to differing risk preferences and differing desires to endure uncertainty, to put capital at risk,

to pursue opportunities or to let them pass by.

A twenty-three year-old recent college graduate, with small assets and high aspirations, tends to have a willingness to accept higher future uncertainty and higher personal risk than does a sixty-three year-old successful businessperson who is approaching retirement and who owns a home and a portfolio of assets and business interests.

A thinly capitalized private startup business has a higher appetite for risk and uncertainty than a wellestablished public company focused on a single product line.

Respective desires to increase risk, and to decrease risk, can inspire trades between parties with varying risk preferences. But businesses and investments tend to incorporate complex structures, multiasset portfolios (with differing risk qualities), and multiple owners (with differing objectives).

Here is a simple example. The Baupost Group is an investment manager in business for more than 40 years. The firm maintains the objective “to thoughtfully invest, protect, and compound the wealth [of clients and the firm’s principals] over multiple generations.” (Source: Website of The Baupost Group, L.L.C.) In the past, the firm has made sophisticated investments that have included companies and assets in distress –seemingly higher-risk investments (although the firm also seeks to preserve a “margin of safety” in its investments.) It is worth noting that, in the past, when presented with choices for portfolio allocations to low-risk investments, the firm did not invest in bank CDs or money market funds. In the past, the firm chose to invest solely in US Treasury bills as its cash proxies, even though the yields

were lower – explicitly accepting a return penalty in order to elevate the security of its cash equivalents.

In this respect, we think it makes sense to assess risk in multiple dimensions.

We seek to undertake a deliberative process in analyzing risk in a business, in a portfolio, in a development plan. The process takes the following steps: Identify Critical Risks

• Assess current conditions

• Assess assumption

• Employ baseline models for exits

Establish Priority Matrix of Critical Risks – noting the following:

• Commonsense Factor: Experience and judgment frequently outweigh numeric analyses

• Risks can correlate, and can diversify: Compounding or Dampening factors

• Apply risk/rewards standards of client

A consistent process is important. Standards for analysis and decision-making should be objective and well-considered. But we also recognize that life, and markets, can be complicated.

In the recent past we undertook a client engagement for a family with extensive holdings in real estate. This family is one of the country’s leading private owners of their chosen property type. Their portfolio has experienced meaningful growth over the past decade; market conditions have enabled

them to make very large additions to the portfolio in recent years. A meaningful proportion of their assets have been financed with floating rate debt provided by a number of banks.

This growth, and the success of their business, have resulted in certain management challenges, which the family is addressing. This family sought our counsel on managing their (at the time, rising) interest costs.

A large investment bank had proposed incorporating a complicated multi-element structural tool to “hedge” uncertainties in the cost of the family’s floating rate debt. We have practical experience with analogous hedging/ investing structures, and were abundantly familiar with the difference between the family’s potential upside and downside outcomes. We analyzed the complicated tool, and provided the family with practical insights into the structure’s mechanics –and defined its costs and risks.

The relationship managers at the bank, who would receive a commission on a sale of the tool, were anxious for the family to use it – which is to say, for the family to pay for it. When we discussed the tool with the bank’s proprietary trading desk, who would serve as the family’s counterparty on the use of the tool, it became clear that this trading desk was indifferent to the family’s circumstances – all the trading desk cared about was the bank’s profit margin.

Two things became clear: 1) no one at the bank had a fiduciary responsibility to our client – no party at the bank placed our client’s interests first – and, hence, 2) our client’s interests and the interests of

the bank were not aligned. It was also clear that the complicated tool really didn’t facilitate our client’s objectives. Not the best circumstances for an expensive “hedge.” We shared these perspectives with the family, who decided to address the matter differently.

More than once, we have been contacted by clients saying, “Hey, I have a decision to make in the very near future. Can you help me think about this in a hurry?” or “Hey, I have a problem that I need to resolve as soon as possible.” The client suspects, but doesn’t know, that a painful risk may be pending – a financial loss (“How bad can it get?”), a prospective new endeavor with an uncertain outcome (“What is the downside?”) or a possible change in the market landscape (“If this happens, what should I do? How should I prepare?”) Market uncertainty presents ongoing challenges to owners of businesses and assets.

The sense of urgency that results from timesensitivity can supplant a comprehensive review. Frequently, the speed of market change can mean that a decision-maker needs to make choices with

ROBERT GEITZ Managing Principal Capital Dimensions rgeitz@capdimen.com

incomplete information to guide his judgment.

What qualities can support such choices? Experience. Pattern recognition. Conservative values. And, we would like to think, a trusted advisor.

So, what is the point of paying attention to explicit risks, and potential risks? Every business owner, investor, entrepreneur wants to protect what they have built. As we observed at the beginning, risk is a threat to success. We have noticed that risks arise at every stage of life, every stage of businessbuilding, every stage of investment management. Experience tells us that business owners, entrepreneurs and investors, need to pay constant attention to threats to their assets and livelihoods.

What is the point? To preserve what you have built, and to enable what you stand to build in the future.

Capital Dimensions LLC provides advisory solutions to family offices, entrepreneurs and investors. We focus on matters that require expertise and experience beyond what our clients regularly apply to their investments and businesses –recognizing that specialization is required to resolve complex situations.

Capital Dimensions LLC provides advisory solutions to businesses, investors and market participants – with a core focus on critical risk factors that affect capital structures and capital investments. Critical risks can reside outside and inside client assets and businesses, and can meaningfully influence performance and investment returns.

Principal

STEVE BRADY

Partner and Market Leader

Withum

PRACTICE AREAS

Mergers & Acquisitions

Transaction Advisory

EDUCATION

University of Wisconsin-Madison

Bachelor of Business

Administration (BBA), Accounting and Finance

LICENSES & CERTIFIFATIONS

Certified Public Accountant

State of Illinois

Steve is a Partner and Market Leader for Withum’s Transaction Advisory practice. He is a licensed certified public accountant in the state of Illinois and specializes in mergers & acquisitions and transaction advisory, advising clients to realize value from middle-market transactions across multiple sectors. Steve has extensive expertise in buy-side and sell-side due diligence, merger integration and other advisory services for mergers and acquisitions, debt offerings, carve-outs and other transactions.

Steve has been a Transaction Advisory Practice leader in global and national firms for over 16 years, served as a chief financial officer of a middle-market diversified mechanical contractor and specialty manufacturer and a start-up medical device company, and audit partner for a global firm.

Steve previously led a wide variety of crossborder and domestic projects for private equity firms and their portfolio companies, family offices, and strategic acquirers including closelyheld middle-market companies and global organizations, investment banks, mezzanine lenders and financial institutions.

BY STEVE BRADY Partner

and Market Leader

Withum & MICHAEL RITCHIE

Senior Manager, Transaction Advisory Withum

Throughout 2023 and into 2024, the M&A middle market has continued to be bogged down by headwinds from uncertainties in the interest rate changes, the economic environment and political policies. The down M&A market has been further driven by sellers holding out for the lofty multiples of 2020 and 2021, and buyers reigning in their leverage looking for valuebased deals of high-quality companies. Active buyers have been using additional tools to reduce their exposure and while achieving a transactable outcome for sellers.

One significant tool that we have seen being increasingly prevalent during this period are earnouts. Earnouts allow the gap in valuations to be bridged between buyers and sellers allowing sellers to achieve the multiples they desire while protecting the buyers from downside risks and reducing the amount of capital needed at closing.

Let us take a deep dive into the latest trends in earnouts and the implications that come with them.

First, as a refresher, an earnout is a contractual provision where the seller of a business receives additional value for the transaction if the business meets specified financial targets post-closing. Earnouts have a wide range of variations ranging from payments being based on revenue, EBITDA, customer retention, or margins. They are typically paid out from one year up to five years with the intent to reward sellers for maintaining or increasing company performance.

Earnouts are experiencing a resurgence in these challenging times and began to take more of a foothold during the COVID-19 pandemic when there was so much uncertainty about how the economy would impact a business’s performance over the ensuing years. There were several industries, such as communications, technology, telehealth, and medical supplies that saw massive gains in earnings that owners tried to capitalize on as they sold, while other industries such as live entertainment and travel took a temporary hit before rebounding. During this time buyers were unsure what the impact would be in the long-term but with the significant supply of capital and attractive interest rates at the time, there was still a significant appetite for transactions. At this juncture earnouts were able to come into the fold to act as protection for the buyers and provide upside for the sellers.

This trend in earnouts continued to gain momentum

and is now a frequently used mechanism to bridge gaps in valuations between buyers and sellers. However, while this may sound like a win-win scenario this is not without its own drawbacks. Here are some of the drawbacks that could arise from using earnouts:

If not clearly defined and understood by both parties earnout calculations may lead to significant disputes and potentially litigation on how they are calculated.

We have seen several instances where there has been a dispute over an earnout agreement that is not clear, where the buyer’s interpretation of the agreement was not in concert with the seller, and when the seller did not understand how the calculations were being performed. Generally, in these instances the seller did not have experienced advisors supporting them throughout the process of determining the mechanism for an earnout. Often times, their local tax preparer who was not aware of the nuances involved in the M&A process assisted them. Having the right advisors on your side when selling a business is vital to the success of a transaction and each different advisor, whether it be an investment banker, M&A attorney, or M&A financial advisor, brings a lot of value and has the experience to provide the necessary support and look for pitfalls in an earnout calculation.

One of the essential factors to consider as you enter into an earnout agreement is the level of control of the operations and accounting function the seller will have after the transaction. For example, if there is a change in revenue methodology to go from a cash basis to an accrual or Generally Accepted Accounting Principles (GAAP) basis with no clear earnout calculation impact defined in the

purchase agreement then this shift could have a significant impact on an earnout calculation. Also, when reporting on an accrual basis, if earnouts are step increases or all or nothing earnouts versus a percentage of milestones achieved, the buyer could hold back revenues or increase expenses claiming that the financials are GAAP compliant. From an operational standpoint, decisions can be made which are detrimental to the results which measure the earnout, most commonly top line revenue growth or profitability.

2. Lofty Milestone Targets: We have also seen in several instances where earnouts are calculated on forecasted numbers. While lofty aspirations for growth may look appealing to a buyer, they could cause an earnout to be reduced or not achieved at all. However, there have been many court rulings in recent years, such as Fortis Advisors LLC v. Johnson & Johnson (“Johnson & Johnson”) and Shareholder Representative Services LLC v. Alexion Pharmaceuticals Inc., highlighting the risks of using earnouts and requiring the buyers to put their best foot forward to achieve these goals.

Depending upon their role after the deal closes, the seller may likely lose control of important operational decisions which limits their ability to influence the performance of the business. One example could be that the buyer needs to make significant investments in operations resulting in inflated expenses and thus reducing EBITDA. Another example could be that revenue is decreased as the buyer has a change in their customer or product approach or eliminates certain loss leaders or low margin products. We have also seen where these decisions lead to inventory write