12 minute read

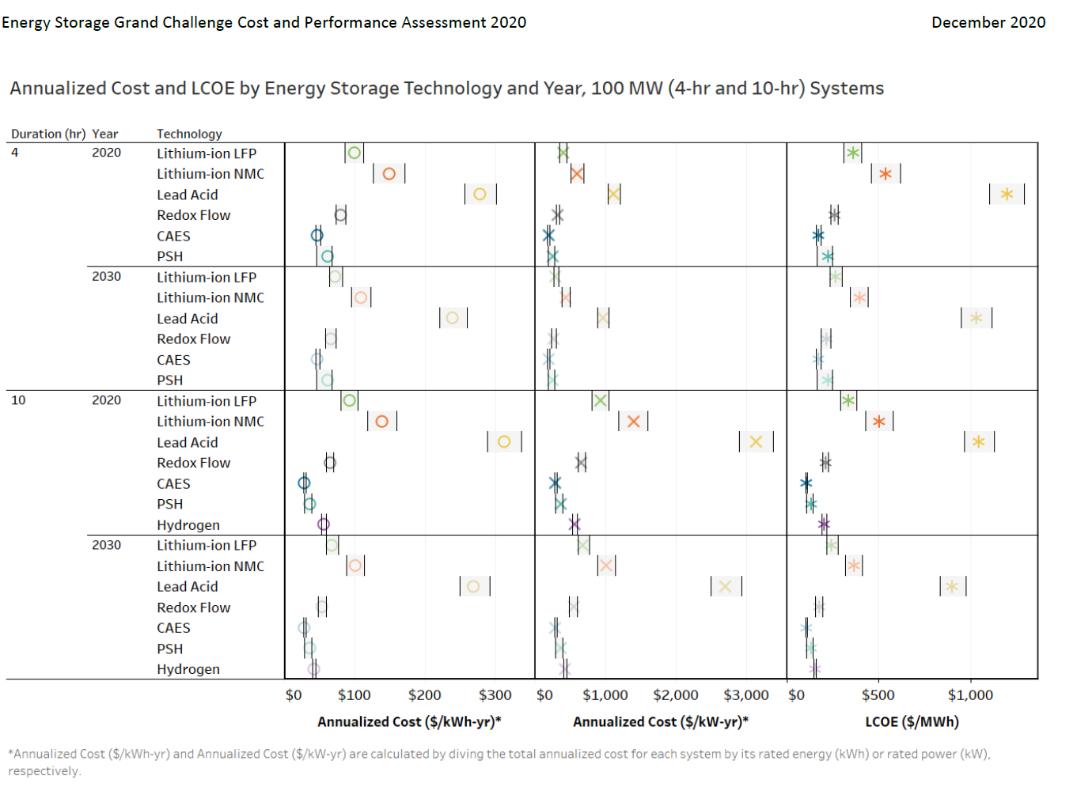

Figure 5.2-1. Annualized Cost and Levelized Cost Comparisons of Energy Storage Technologies

Source: DOE 2020. LCOE – Levelized Cost of Energy

Figure 5.2-1. Annualized Cost and Levelized Cost Comparisons of Energy Storage Technologies

5.3 Investment Tax Credit: Benefits to BESS vs. Pumped Storage

The Inflation Reduction Act of 2022, which went into effect on August 16, 2022, establishes an ITC for stand-alone energy storage, including pumped storage. The Project is expected to qualify for the 6 percent base, the 5x multiplier (bringing the base to 30 percent), the 10 percent bonus for Energy Community, and the 10 percent bonus for domestic content, bringing the total ITC to 50 percent. Since pumped storage costs are more front-loaded versus that of batteries, pumped storage would likely obtain greater benefit from an ITC due to the ITC being applied to more of the Project net present value.

5.4 Energy Value

The cost of charging energy can be assumed to be the same for pumped storage and for BESS. Furthermore, since the differential between peak and off-peak energy value is expected to be relatively low and similar for each technology, the value of Project energy will not be separated from the value of Project capacity. Differences in efficiency will be nominal. While BESS has slightly higher round-trip efficiency than pumped storage, BESS will incur some efficiency degradation through cycling, while pumped storage will not.

5.5 Ancillary Services Value

The Project will be able to provide a wide range of ancillary services, from frequency regulation and voltage support to spinning reserve. Unlike in organized markets such as the California Independent System Operator (CAISO), the value of these services is not quantified in most of the rest of the western region, including Wyoming. Furthermore, the total market for ancillary services is relatively small, particularly for frequency regulation, which has historically been the most lucrative of services in other regions. Therefore, the value of ancillary services provided by the Project—while important—is not a decisive factor in the value of the Project to the region, and Black Canyon does not attempt to quantify it here.

5.6 Costs of Conventional Alternatives

Comparison to conventional peaking resources such as combustion turbines or reciprocating engines would indicate a higher capital cost for the Project than these types of resources on a $/kW basis. For example, PacifiCorp’s 2021 IRP estimates the annual fixed cost for an “F” frame simple-cycle combustion turbine (SCCT) at $73.70/kW-yr in 2025. This, of course, does not include fuel cost and variable O&M. For a reciprocating engine, which is more flexible and efficient than a gas turbine, and thus may represent a better proxy for renewable-paired dispatchable capacity, PacifiCorp IRP’s estimated cost is $1,938/kW, with total annual fixed cost at $152.62/kW-yr.

For a more accurate comparison with these types of resources, the cost of energy (or a per-megawatt hour [MWh]-generated) should be determined along with cost of capacity. The energy used for pumping (the “fuel”) is most likely to be wind over-generation or excess solar energy that is already resulting in “negative pricing” (i.e., cost of energy below zero) in many markets, and which unused, may be subject to curtailment. In fact, there will usually be some net gain in value due to the shift in time of delivery and avoidance of curtailment of renewable resources through utilization for charging. Therefore, the cost of charging/pumping energy that can be assigned to the Project can be assumed to be very low for purposes of estimating total product cost and value.

PacifiCorp’s 2021 IRP calculates the first-year total resource cost of the SCCT at $73.95/ MWh, assuming a 33 percent capacity factor. The estimate for a reciprocating engine, assuming the same capacity factor, is $90.69/MWh. If the Project were operated at its full capacity 365 days a year, it would also have a capacity factor of 33 percent. At a fixed cost of $230/kW-yr and energy value set at zero, the resource cost in $/MWh would be $79.50— higher than that of an SCCT, but considerably lower than that of a reciprocating engine set.

Operating costs for gas-fired generation resources are subject to fuel price variability. They also have shorter useful lives than pumped storage, at 35 and 40 years, respectively, for SCCT and reciprocating engines. More important to the analysis, however, is that their operation emits significant amounts of carbon dioxide. Concern about anthropogenic climate change has made greenhouse gas emissions a major liability and has driven sweeping energy policy changes across the U.S. Accounting for the gas-fired generation resources cost of carbon, let alone the lifespan difference and reduced ability to manage

and make more effective use of renewable sources, effectively renders a lower value option (and potentially a liability or stranded assets at best) compared to the Project.

For the foregoing reasons, gas-fired generation resources no longer represent the benchmark for new utility supply-side options. The transition to low-carbon and no-carbon futures, either though state mandate or as policy chosen by individual utilities, means that utilities are reducing or eliminating the use of fossil-fueled resource additions to meet capacity needs. This shift is being reflected in most utility resource plans.

Instead, energy storage is regarded as essential to utilizing the massive amount of variable and intermittent renewable energy—primarily solar and wind—that is being added to the grid. Conventional peaking resources can be dispatched when those resources are unavailable, but cannot provide the zero-emission, time-shifting capability or flexibility of energy storage.

• The estimated annual value of Project power is based on the value of capacity in the expected high-renewable environment, with minimal reliance in valuation on energy costs and ancillary services value that may have traditionally been used to estimate pumped storage annual value. • Given regional decarbonization plans and the transition to renewable resources as the dominant energy supply, dispatchable energy storage options become the benchmark for capacity. Other pumped storage projects have been proposed in the region, but they are in an early stage of planning and Black Canyon cannot speculate on their cost or likelihood of development. Therefore, to establish a benchmark for comparison,

Black Canyon uses BESS—specifically lithium-ion systems—as a benchmark for comparison of the value of Project power. • Based on an equivalent energy storage duration, lithium-ion in 2030 may have a lower cost for an equivalent amount of capacity. However, lithium-ion systems have a lifespan of 10 to 20 years, while pumped storage has a useful life of 100 years. • Based on the storage duration and difference in useful life, the proposed Project would have a total lower cost of power than BESS, and would, in effect, establish the benchmark for capacity value for long-duration (10 hour), long-life storage (and generation) assets in a high-renewables regime. • Assuming an 8 percent carrying charge rate to the estimated total Project capital cost of $3,110/kW, this results in an annual cost of $249/kW-yr, to which fixed O&M of $20/kW-yr is added for a total of $269/kW-yr.

6.0 Cost of Energy Alternatives

Other electric energy alternatives are discussed below.

6.1 Fossil-Based Generation

Coal-fired steam generation provides large-scale baseload energy, serving a different function in an energy supply portfolio than pumped storage. As a major source of greenhouse gas emissions, coal-fired generation in the market region for the Project is being phased out and there are no new plans for new coal-fired capacity additions. Coal is, therefore, not a viable alternative to the Project.

Gas-fired power plants include SCCT, combined-cycle combustion turbines (CCCT), and internal combustion reciprocating engines. Gas-fired generation has provided most of the peaking and intermediate capacity in the western market since the 1990s. CCCT plants are used for intermediate-to-baseload service. SCCTs, including frame turbines and aeroderivatives, are used for peaking power and are lower in initial capital cost than pumped storage. However, similarly to CCCT plants, they are significant sources of greenhouse gas emissions and their inclusion in regional resource plans is being scaled back dramatically. Furthermore, while they can be used to follow variations in solar and wind output, they do not provide the energy storage function that will be critical for integrating large amounts of renewable resources. Gas-fired generation is, therefore, not a viable alternative to the Project.

6.2 Nuclear Power

Nuclear fission power plants have provided baseload energy in many regions of the U.S. since the 1970s and several plants operate in California, Arizona, and Washington. Due to policy changes, safety concerns, or economic factors, the two nuclear plants in California are being or have been retired.

While being carbon-free sources of generation, nuclear power plants using existing technology are large, have a long development timeline, and require significant capital investments. Disposal of nuclear waste is also a significant concern. Wyoming is the largest domestic producer of uranium used for conventional nuclear fission power plants; however, the state does not have any existing fission plants. One small, modular nuclear reactor is currently proposed in Wyoming. The 345 MW Natrium power plant is based on new technology using molten salts as a heat source. Cost estimates for pilot plants such as the Natrium power plant are high and they will need to be operated at a close to baseload capacity factor to keep the cost of energy at a competitive level.

Nuclear generation is a baseload resource and does not provide the flexible energy storage services that will be required to integrate large amounts of renewable energy. This fact, combined with cost, ongoing concerns about waste disposal, and the experimental nature of new nuclear technology options, indicates that nuclear power is not a viable alternative to the Project.

6.3 Renewable Resources

Solar energy, particularly photovoltaic solar (PV solar), is emerging as a dominant new form of electric energy supply across the U.S., particularly in the western U.S. It is one of the lowest cost energy sources available today and entails no greenhouse gas emissions. Solar output is also somewhat predictable, with only cloud cover interrupting normal patterns of generation. However, those normal patterns involve a mid-day output peak, which does not coincide with peak demand, and no generation at all during the night. The result is the well-established “duck curve,” with a steep ramp up needed for generating capacity that aligns with increasing load in the early evening. Since PV solar is not a firm or dispatchable generation alternative, it is not a viable alternative to the Project. In fact, for the reasons given, PV solar is a major driver of the need for energy storage resources like the proposed Project.

Wind energy is the other leading source of carbon-free energy seeing widespread deployment today. Where the wind resource is of high quality, the cost of wind energy is very low. Wind energy viability is particularly high in Wyoming, possessing high average annual wind speeds of 6.5 meters per second or higher at 80 meters above ground surface in over half of the State by area (Tetra Tech 2021). Therefore, Wyoming is likely to export wind energy production to other states. Furthermore, like PV solar, wind energy is not dispatchable, and it has a much lower ability than solar to predictably match demand. Like solar, therefore, the use of wind energy, particularly in Wyoming, is a major driver of the need for energy storage resources like the proposed Project.

Wyoming’s geothermal resources are used for direct heating applications, mainly in Yellowstone National Park and Hot Springs State Park, and do not have adequate resources for commercial electricity generation (State of Wyoming Geological Survey 2015). However, the economics of geothermal power require that it operates as a baseload facility. Geothermal resources are site specific and require significant lead times and development risk. More generally, the cost of geothermal generation is depressing its inclusion in most resource plans. For these reasons, and since geothermal generation is generally baseload in nature and not able to provide the energy storage services needed for integrating other renewable resources, geothermal is not a viable generation alternative to the Project.

Conventional hydroelectric power has provided relatively firm, carbon-free energy in parts of the western U.S., specifically the Pacific Northwest, California, and Colorado, for many decades. Wyoming currently has 21 dams that generate power, most of which are owned and operated by the Federal government. Across a wider region, there is some potential for new, small hydropower additions to non-powered dams, but there are no plans for major hydropower projects akin to those developed in other parts of the west in earlier generations. Due to the limited potential of future large hydropower developments, openloop pumped storage developments serve as opportunities to better utilize existing hydropower developments in Wyoming.

The lack of viable development opportunities for new major hydroelectric power sources in the western region, along with the other reasons given here, mean that conventional hydroelectric power is not a viable generation alternative to the Project.

6.4 Other Pumped Storage

The viability of pumped storage projects requires a relatively rare combination of factors to be present, including suitable topography and geology, land availability, a source of fill water, an acceptable level of environmental impact, correct sizing for the market, and interconnection options. No major pumped storage projects have been constructed in the U.S. since 1995, and relatively few proposed pumped storage projects advance to development and receiving a FERC license. There are only three pumped storage projects in the Western Electricity Coordinating Council region that recently have received a FERC license: Eagle Mountain in California, Swan Lake North in Oregon, and Gordon Butte in Montana. Construction has not commenced at any of these projects.

Within the State of Wyoming, there are currently three preliminary permits pending or recently granted for other proposed pumped storage projects: P-15244, P-15247, and P-15253. Two involve closed-loop concepts and one is an off-stream (open loop) concept similar in concept to the Project. Each of these projects has a proposed generation capacity of 500 MW. Recently, a Notice of Decision Not to Proceed was filed for a 400 MW, closed-loop concept in Wyoming under P-14853 due to landownership and access issues. Pumped storage projects at the preliminary permit stage are considered speculative and, as of the time of this writing, none of these concepts have advanced beyond this phase.

Based on both their early stage of development and smaller project sizes, it is Black Canyon’s estimation that no pumped storage projects are currently proposed in Wyoming with an equivalent or superior level of viability as that represented by the Project.

6.5 Other Energy Storage Technologies

BESS are seeing increasing deployment, primarily in the form of lithium-ion batteries paired with PV solar. The cost of batteries has fallen significantly over the past several years and costs are forecasted to continue to decline. Standalone battery projects are being constructed at the scale of hundreds of MW, and projects of 1 gigawatt have been proposed. These systems generally have storage durations of 2 to 4 hours.

Like pumped storage projects, BESS represent dispatchable capacity that helps to integrate carbon-free renewable resources and will thus see significant deployment across the market. Compared with pumped storage, BESS have the advantage of shorter development times, modularity, and flexibility of location. However, BESS have substantial disadvantages compared to the Project:

• Higher cost at longer durations of storage (duration will be increasingly important as renewable energy penetration increases);

• Significantly shorter useful life (10 to 20 years, depending on cycling);

• Degradation of storage capacity and efficiency through use (resulting in a higher fixed

O&M cost for augmentation);

• Environmental impacts from mining of battery materials and the lack of methods for recycling spent battery cells;