Great British Railways and the productivity puzzle - RMT report 102025

Great British Railways and the Productivity Puzzle

RMT discussion paper

October 2025

Executive summary

• The British economy has a major and chronic problem with productivity, rooted in chronic underinvestment by the private sector.

• The creation of Great British Railways represents a historic opportunity to contribute to mitigating the weak productivity growth of the UK economy. The rail industry has a significant economic footprint as well as possessing several areas where GBR’s expansion and further investment could help to rebuild high value manufacturing and create more, higher productivity jobs.

• But GBR will be unable to play this role unless two problems are addressed:

1. Firstly, the debate over measuring productivity in the rail industry must move on from crude measures of input and output:

• The current productivity measures used by the Office of Rail and Road (ORR) are deeply flawed and focus debate almost solely on labour costs. This leads to a doom spiral which ends in a perpetual pressure to cut jobs, obscures the real drags on productivity and ignores the social and economic impact of rail as a public service. This process in itself undermines both the productivity of rail and the potential for rail to help raise productivity in the British economy.

• In place of crude input and output models, RMT recommends adopting the Productivity Institute’s approach for measuring public sector productivity, focusing on budgetary efficiency (the productivity by which budgets are transformed into the inputs needed for the organisation), organisational productivity (the way that input resources are transformed into output activities) and effectiveness (the productivity with which output activities contribute to the ultimate socially and economically desired goals).

2. Secondly, Great British Railways must tackle the real issues with productivity which stem from the continuing legacy of Britain’s disastrous privatisation:

• The rail network is cut through with contractual interfaces that create wasteful transaction costs. Alongside the costs of Network Rail’s legacy private sector debt and the rising costs of leasing rolling stock, these contractual interfaces are locking in major inefficiencies in the use of public money and fare revenue and dragging down the overall productivity of the railway. These inefficiencies operate to erode rail productivity, preventing rail from fulfilling its full potential as an engine of economic growth.

• RMT argues that tackling these weaknesses means undertaking a further wave of integration to cut wasteful transaction costs throughout the rail industry. This means action to tackle the position of private rolling stock companies, to protect GBR from the weight of private debt obligations, to insource work across operations and infrastructure renewal and to create new capacity in rolling stock manufacturing and infrastructure enhancement.

• On the basis of greater integration, GBR can create a new centralised fully funded apprentice scheme which will provide industry-wide training aimed at young workers and offer a career path from school leaver to retirement in the rail industry, providing pathways from uniformed, overalled and back-office apprenticeships.

• GBR could also undertake joint work with the unions to create job security and a framework within which future workforce and training needs can be identified, new technologies introduced and through which genuine workforce planning can take place. This would create an environment that could support the accumulation of knowledge and skills and the retention of this knowledge as new technologies are introduced in place of damaging labour-shedding.

3. Finally, RMT argues, the industry needs to see a change in the way the Treasury assesses both investment and operational spending in the rail industry. This requires further relaxing fiscal rules which limit borrowing for greater investment in rail infrastructure and rolling stock, and which press down on operational spending, in addition to reforms to the Green Book’s criteria for assessing rail investment projects.

Introduction: Britain’s productivity problem

Britain has a major and chronic problem with productivity. The root causes of the low productivity in Britain are well understood by economists and lie in chronic underinvestment by the private sector. Academics at the Productivity Institute have calculated that UK workers have 33% less capital per capita than workers in peer group countries. Major British employers prefer to pursue a business model based on low pay, low skill and low investment, responding to a capital environment dominated by shorttermism.1

Tackling these economic problems is a major task for government. In this paper, RMT argues that the creation of Great British Railways represents a historic opportunity to contribute to mitigating the weak productivity growth of the UK economy. The creation of an integrated publicly owned rail company is an important step in the right direction of tackling weaknesses in rail productivity and it creates a significant lever in the wider economy. However, we also show that if GBR is to fulfil this potential, two things must happen:

• The debate over measuring productivity in the rail industry must move on from crude measures of input and output. The current industry productivity measures are deeply flawed and focus debate almost solely on labour costs. This leads to a doom spiral of attempts to cut jobs, obscures the real drags on productivity and ignore the social and economic impact of rail as a public service.

• Great British Railways must tackle the continuing legacy of Britain’s disastrous privatisation by undertaking a further wave of integration to cut wasteful transaction costs that operate to erode productivity and prevent rail from fulfilling its full potential as an engine of growth.

1 The literature on Britain’s chronic under-investment (and its link to short-termist finance) is substantial and well established, but for recent contributions see https://www.productivity.ac.uk/research/the-ukscapital-gap-a-short-fall-in-the-trillions-of-pounds-that-will-take-decades-to-bridge/ ; D. Coyle, B. van Ark, J. Pendrill (2023) The Productivity Agenda. Report No. 001. The Productivity Institute ( https://www.productivity.ac.uk/wp-content/uploads/2023/11/TPI-Agenda-for-Productivity-2023FINAL.pdf,) pp. 26-27; John Van Reenen and Xuyi Yang, Cracking the Productivity Code: An international comparison of UK productivity (June 2024) (https://cep.lse.ac.uk/pubs/download/special/cepsp41.pdf?_gl=1*1amo1yl*_gcl_au*MTY2MjQ0MDE0NS 4xNzU3MDgwMjEw*_ga*NDc2MTgyMzE1LjE3NTcwODAyMTA.*_ga_LWTEVFESYX*czE3NjAxMDA1NjEkbzE kZzEkdDE3NjAxMDA2MTYkajExJGwwJGgw -)

Great British Railways: A potential engine of higher productivity

The economic footprint of rail:

The rail industry has a significant economic footprint in the UK economy. Taking just the railway system and the rail supply sector (excluding induced impacts and on-site retail), the Gross Value Added (GVA) contribution of rail exceeds the UK’s legal services sector and the electricity and gas sector. Rail is a comparable size to the food and drink manufacturing industry and telecommunications sectors. According to research by Oxford Economics, the rail sector contributes £41 billion in gross value added (GVA), supports 640,000 jobs, and generates £14.2 billion in tax revenue. The multiplier effect of rail investment is substantial: for every £1 spent on rail, £2.50 is generated elsewhere in the economy.2

The sector is also marked out by its relatively high productivity. The average GVA per job of £68,200 is 38% higher than the UK average of just over £49,500.

It may be far beyond rail to tackle the structural problems in mobilising investment in Britain, but investing in rail would play a role in boosting business confidence. As the Department for Business and Trade’s Invest 2035 document noted:

“Growth-driving sectors [….] require high quality infrastructure and transport connectivity. A resilient, safe, and secure transport network provides access to social and economic opportunity and is fundamental to business investment and location decisions.”3

Polling undertaken by Opinium for the TUC in October 2024 found that 74% of businesses view public transport as important to their success and 65% said that more extensive public transport networks with more frequent services would benefit their businesses. A substantial majority of businesses believe the government should be prioritising public investment in the short-term rather than cutting back.4

In addition, the rail sector has several areas of particularly high productivity activity with the potential to be expanded and create more high productivity jobs.

Train manufacturing:

There is massive potential for Great British Railways to drive the expansion of desperately needed high productivity manufacturing in Britain. Some basis for this already exists. The direct and indirect economic impact of the assembly of rolling stock,

2 Oxford Economics, The economic contribution of UK rail (2021).

3 Department for Business and Trade, 2024. Invest 2035: the UK’s modern industrial strategy

4 Opinium, October 2024 for the TUC. Polling of 501 business leaders and decision makers.

the manufacture of sub-components and maintenance activity in the UK has been estimated at generating £1.8 billion of Gross Value Added to the economy and supporting up to 27,000 jobs. These are high productivity jobs too, with an estimated GVA of £105,000 per employee. This compares well with the average GVA for the manufacturing sector (£65,000) and is more than double the national average. Manufacturing of sub-components is also integrated with the wider UK manufacturing base as many train manufacturing firms supply components to multiple sectors.5

Yet train manufacturing is also a story of chronic fragility, lost opportunities and wasted potential. Rolling stock manufacturing has become restricted to assembly and the manufacture of sub-components, with most components imported. The rolling stock manufacture supply chain is dominated by four non-UK multinationals: Siemens, Hitachi, Alstom and CAF. This leaves Britain’s rolling stock supply chain strategically vulnerable. Without a steady pipeline of orders, these companies can simply close UK plants down, as the recent issues around Alstom ‘s Derby plant and Hitachi’s Newton Aycliffe plant demonstrate. As a senior Alstom Executive put it recently:

“At the end of the day we are a global business…our group is looking at this from a purely portfolio perspective thinking ‘well OK if there is no commitment in the UK we will put our investment somewhere else”.6

The domination of the rolling stock supply chain by these companies also represents a fetter on the development of manufacturing capacity in Britain as they prefer to use their own centralised multinational supply chains.7

Gret British Railways represents an opportunity to address these weaknesses. GBR could use its centralised procurement power to drive investment toward shorter, domestically based supply chains, rewarding manufacturers for buying from UK based component suppliers, using robust social value metrics as advocated by the TUC. But in addition to this, GBR should seek to reduce its dependence on foreign multinationals and rebuild manufacturing capacity directly. This could begin with developing the capacity to manufacture and assemble aluminium bodyshells and aluminium extrusion directly, an area where there is sufficient demand in the rail industry and the wider economy to support strategic, state-led investment.

5 How can the rolling stock supply chain create greater value for the UK? Oxera Report, Prepared for Rail Forum Midlands, August 2021, pp. 10-11, 15.

6 Disjointed rail planning leaves UK train builders facing closure, Philip Georgiadis in Derby and Jennifer Williams in Manchester, Financial Times, APRIL 11 2024

7 How can the rolling stock supply chain create greater value for the UK?, pp. 19-20.

Infrastructure maintenance, renewal and enhancement:

Great British Railways has the potential to drive improved productivity through strategic procurement of goods and the creation of better jobs in both direct employment and the supply chain.

Network Rail’s deal with British Steel to supply 337,000 tons of steel as part of the government’s £2.5 billion steel fund demonstrates the potential power that GBR will have as a procurement body to intervene effectively in the British economy. The fact that NR will still have to seek further contracts with European manufacturers to supply 20% of its needs demonstrates the potential to expand British steel capacity. The recent announcement of EU tariffs on British steel also demonstrates the crucial importance of the home market for British steel.

Last year, Network Rail spent £3.9 million on renewals work in 2023-24, overwhelmingly contracted from a handful of construction giants. Much of this work is delivered using employment that is essentially based on the construction industry’s notoriously low productivity business model.

Productivity growth in construction lags behind rates of growth in manufacturing and other sectors and construction is weakly capitalised. It is highly fragmented, with a handful of big firms mobilizing a supply chain of smaller ones around projects with the result that procurement bodies are faced with ‘navigating a challenging and opaque marketplace’ As one report noted: “The results are operational failures within firms, including inefficient design, insufficient time spent on implementing the latest thinking on project management and execution, a low-skilled workforce, and underinvestment in the technology and digitization that would help raise productivity”. The report concludes that “the degree of fragmentation has a significant impact on productivity”.8 The same will be true of Network Rail, in both its direct use of contingent labour and its contracting arrangements with the construction sector.

GBR could play a role in raising construction productivity by insourcing its renewals work and delivering it directly, eradicating wasteful interface and transaction costs and enabling the targeting of investment toward the rolling out of new technology at scale and the training and upskilling of the workforce. It could achieve the same in relation to enhancements and ‘megaprojects’ by creating its own in-house enhancements arm, as suggested in the recent Stewart Review of lessons from HS2.9

8 Reinventing construction: A route to higher productivity, McKinsey Consultancy 2017: (https://www.mckinsey.com/~/media/mckinsey/business%20functions/operations/our%20insights/reinv enting%20construction%20through%20a%20productivity%20revolution/mgi-reinventing-construction-aroute-to-higher-productivity-full-report.pdf ) p. 47.

9 See, for example, RMT’s evidence to the Transport Select Committee’s ‘Ending Boom and Bust’ inquiry, (https://committees.parliament.uk/writtenevidence/142909/pdf/ )

In summary, the potential economic power of GBR is clear, but its ability to play this catalysing role in the UK economy will depend on addressing its own weaknesses, and its own productivity issues, both which are rooted in the disastrous legacy of privatisation.

The productivity debate in rail: Moving on from the ORR’s flawed measures

Great British Railways will not be able to play its full potential role without addressing its own productivity issues. In order to do this, however, the nature of those productivity issues must be properly understood. Unfortunately, the debate on productivity in the rail industry, like that of the public sector more widely, is largely motivated by a perceived need to cut public spending. For example, the Office of Rail and Road, the regulatory body tasked with reporting on rail productivity, says:

“Productivity matters. It is a major driver of growth and value – and rail is no different. Expenditure on the operational railway is more than £25 billion per year, with nearly half of this government funded, so even small percentage changes in productivity can make a big difference in value for passengers, freight users and taxpayers.”10

It is also dominated by the use of crude input-output metrics derived from the business sector. As the ORR defines it:

“Productivity is the ratio between the outputs and the resources (inputs used) in a business activity. Productivity increases when more output (or higher quality output) is delivered with the same or fewer resources”.11

In rail, unlike in a business, there is no simple price for the output, so the ORR uses data on trains run and passenger travelling numbers as proxies for prices. Train operators’ productivity is measured against the number of passenger kilometres travelled, while the productivity of Network Rail is measured against the number of train kilometres that are run on the rails. However, there are a series of problems with the ORR’s approach, some of which the ORR are themselves aware of

Obscuring the role of investment and fares policy

The ORR’s analysis necessarily focuses on input costs and obscures the role of investment in stimulating higher productivity. This approach marks a considerable regression in the level of understanding of productivity from the days of British Rail. In 1981, the British Rail Board’s Corporate Plan was at pains to stress that productivity growth could not be driven simply by cutting labour costs:

11 ORR: Report on rail industry productivity March 2025 (https://www.orr.gov.uk/sites/default/files/202503/2025-rail-industry-productivity-report.pdf,) p. 3.

“Investment, which for the most part means renewal of assets in modern for, leads directly to significant productivity improvement. Furthermore, marketing initiatives leaing to increased asset utilitisation also brings about substantial productivity increases”.12

This understanding of the importance of investment to productivity is notably absent from the ORR’s productivity report. Yet it was integral to the discussion of British Rail’s productivity throughout its history as well as to subsequent historical assessments of its performance.13

Artificial separation of train operations and infrastructure productivity measures

The ORR separates out the productivity of infrastructure workers and train operations workers and uses different measures for each. The effect of this is to artificially depress the productivity of infrastructure workers.

The productivity of workers in train operation is measured against the number of passenger kilometres travelled, a measure that is calculated by multiplying the number of passengers on a particular flow by the number of track kilometres between the two required stations. By contrast, infrastructure workers’ productivity is measured against the number of passenger train kilometres travelled – “the actual mileage in kilometres travelled by revenue earning passenger trains on the Network Rail infrastructure.”

Which measure you use is important as it produces very different results. The ORR’s measure of ‘Passenger train kilometres’ measures how many kilometres are travelled by passenger vehicles in scheduled services over the network. The number of trains run and the extent of the track they run over are relatively fixed and grow slowly. By contrast, the number of passenger kilometres travelled by people using the services can grow more rapidly, and tends to do so, particularly in times of economic growth. The ORR measure Network Rail staff’s productivity against a slow-growing metric rather than the one that has grown more rapidly in recent decades. Correspondingly, they measure Train operators’ productivity in terms of passenger kilometres travelled. This has the effect of making them look more productive than Network Rail.

In fact, of course, this approach fails to reflect the reality of the railway system and is rooted instead in the artificial fragmentation of the system that accompanied privatisation. In reality, the railway is an integrated whole, regardless of its current legal

12 British Rail, Corporate Plan, 1981-85, cited in NUR submission to review of Railway Finances, 1982, p, 14.

13 In fact, the only reference to investment in the ORR’s March 2025 report is in a section on spending on rolling stock. By comparison, see the discussion of lack of investment in relation to British Rail’s productivity in Terry Gourvish, British Railways, 1948-73: A Business history (Cambridge, 1986), p. 613; British Rail, 1974-97: From Integration to Privatisation (Oxford, 2002), pp. 53-95.

and commercial fragmentation, and it is artificial to only use the measure of train kilometres to assess the productivity of infrastructure workers. If the infrastructure is not functioning properly, it impacts across the entire network and drives down passenger kilometres, as the history of Railtrack shows. The existence of a complex machinery of compensations between the infrastructure company and train operators under Schedule 4 and 8 of the Track Access agreements demonstrates that the whole industry understands this

It is also notable that the British Rail Board never appear to have disaggregated workers in this way in their 50 years of measuring and debating productivity. Nor indeed have subsequent historians of BR The separation of train operation and infrastructure workers for the purposes of measuring productivity is an abstraction that serves to artificially depress the productivity of infrastructure workers. It is a relic of privatisation and should be consigned to the same dustbin.

Cost base abstraction:

The cost base of the train operators is abstracted from the cost base of the infrastructure, even though they are completely interdependent. Again, this has consequences for comparative measures of productivity because Open Access operators, who are artificially sheltered from railway costs appear more productive on these measures.

Hidden staffing figures

The ORR’s calculations are based on inaccurate staffing figures. The figures for the labour input, for example, fail to count outsourced and sub-contracted staff. This distorts the analysis and particularly so, when the ORR uses them to assess the productivity of different parts of the railway. Different parts of the railway use outsourcing and sub-contracting to different degrees. The ORR are aware of this but make no attempt to address it.

Disappearing debt

While it focuses attention on labour productivity, the ORR’s March 2025 report performs an extraordinary sleight of hand in concealing one of the key drags of industry productivity – Network Rail’s debt burden. In its discussion paper of April 2024, the ORR acknowledged the role that Network Rail’s debt played in its productivity problem. The number one listed reason for the industry’s rising costs was identified as ‘financing costs for the rail infrastructure [which] increased by 130 per cent, primarily driven by the rising cost of financing index-linked debt’.14 Yet the same discussion paper then proceeded to conduct analysis while excluding that debt from its industry measures.

14 ORR Discussion paper on rail industry productivity, 04 April 2024, p. 11.

The March 2025 report concealed the debt completely from its substantive discussion, only noting in its methodology section that it has done so because the debt was historic and not under Network Rail’s control. This obscures the fact that the burden of servicing that debt, wherever it falls in accounting terms, reduces the overall funding available to it for investment and operational spending. The combined effect of the ORR’s decisions is to make Network Rail look more efficient than it is at the same time that its analysis focuses unduly on staff costs. Indeed, the commentary on page 4 of the ORR report attributes falling productivity solely to staff costs.15

The need for a change in the measurement of productivity in rail

The issues with the ORR’s productivity measures identified above make them largely unfit for purpose. Some of the issues with measuring productivity are specific to rail as BR’s historian Terry Gourvish noted in his seminal history.16 However, the issues above also stem from a deeper problem with attempts to measure the productivity of public services through a simple input-output model using proxies for prices. As the Productivity Institute have argued, measures like these tend to lock public services into a doom spiral that drives them toward cuts that ultimately erode the real basis of productivity.

“The combination of increased demand for services and rising cost pressures means that public services are under constant funding pressure. This can easily lead to a fatalistic view that cutting budgets is the only viable policy instrument. Policymakers either conclude that the only way to keep expenditure under control is by squeezing more out of remaining resources, or that the only way to meet demand is by spending more without much hope of a productivity gain. In other words, service performance can only be improved by increasing spending, consolidation of operations, reduced quality, or axing ‘non-essential’ functions.”17

This is the net effect of the ORR’s focus on labour productivity. In focusing all attention on staff costs (partly by obscuring other drags on productivity), the ORR helps to drive the industry further toward a crude focus on labour shedding and wage restraint.

What is to be done?

It is essential to move debate on productivity in rail away from crude measures of input and output. Rail is a public service and as the Productivity Institute have argued, public services are complex systems, serving a wide range of stakeholders and beneficiaries, closely interwoven with other sectors of the economy and society. Any attempt to measure their ‘production’ and ‘productivity’ needs to reflect this. Instead of crude input

15 ORR Report on Rail Industry productivity, 18 March 2025, pp, 4, 44.

16 Terry Gourvish, British Rail, 1974-97: From Integration to Privatisation (Oxford, 2002), p. 68.

17 https://www.productivity.ac.uk/wp-content/uploads/2023/11/TPI-Agenda-for-Productivity-2023FINAL.pdf, p. 89.

and output models, they suggest that public sector productivity can be measured in three ways:

1. budgetary efficiency (the productivity by which budgets are transformed into the inputs needed for the organisation);

2. organisational productivity (the way that input resources are transformed into output activities) and

3. effectiveness (the productivity with which output activities contribute to the ultimate socially and economically desired goals).

“In order to increase both efficiency and effectiveness…it is essential to view the public sector as a dynamic interconnected system. It is crucial to underscore the interdependence and feedback loops among the various components of the public sector and its diverse services.” (PS Productivity Review) p. 6 ‘For each public service this public service value chain will look distinct’.18

For public transport, this means that any measurement of its delivery of increased passenger kilometres or increased train kilometres would have to be part of a richer analysis based on measuring the societal and economic impact of effective public transport systems. Rising demand for rail, for example, is a societal good that can be part of mass mode shift toward sustainable transport, as well as a source of higher economic productivity in the wider economy. How effectively rail systems deliver on these goals must be measured as part of any assessment of its productivity. Similarly, an approach like that mapped out above would also mean attending to the organisational productivity of the rail supply chain as a whole and how this enabled or prevented the efficient use of public funding and fare revenue. This would allow a more meaningful assessment of productivity that was not skewed toward simple metrics based on the unit cost of the rail worker.

18 D. Coyle, B. van Ark, J. Pendrill (2023) The Productivity Agenda. Report No. 001. The Productivity Institute, pp. 89-91

Tackling the real drags on GBR’s productivity - The dead hand of privatisation

If rail is to be able to play its full potential role in the UK economy, the government must ensure that every pound invested in Great British Railways is spent efficiently and with the aim of making GBR optimally effective. This means it will have to address a series of current inefficiencies that arise from the legacy of privatisation As we show below, the government can achieve this by increasing the integration of the railway and eradicating wasteful transaction costs and rent seeking by the private sector.

Ending the rolling stock racket and dealing with fragmented procurement

The Office of Rail and Road correctly identifies the costs of rolling stock leasing as a major issue for the productivity of the railways. Between 2013 and 2024, rolling stock costs increased by 94%: “Rolling stock costs now make up 27% of operator costs and have a significant impact on our productivity measures’ 19 The procurement of new trains should be a lever for economic growth and raising productivity, but the fragmented and privatised procurement system creates significant drags. Firstly, the presence of rolling stock leasing companies who own the assets creates a structural interest in the system lobbying against the procurement of new trains because it devalues their assets and threatens their profit margins. These companies then seek to recoup supposed risks they take on through ‘hell and high water’ leases that entail rising costs on the railway.

Finally, the dominance of manufacturing by four foreign-based multinationals has led to a series of inefficiencies in the introduction and performance of new trains. The issues arising from attempting to introduce standardized trains onto Britain’s complex inherited infrastructure has led to persistent delays in introducing them from the beginning of the privatisation era to the recent South-Western Railways and Piccadilly Line Underground procurements. Newer trains have also underperformed and demonstrated poor reliability since privatisation.20

19 ORR Report on Rail Industry productivity, 18 March 2025, p. 18.

20 trategic Rail Authority Improving passenger rail services through new trains REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 263 Session 2003-2004: 4 February 2004 (https://www.nao.org.uk/wp-content/uploads/2004/02/0304263.pdf )

Comparison of rolling stock leasing costs and staff costs

2016-24

charges

Source: ORR Data - https://www.orr.gov.uk/sites/default/files/om/toc-benchmarking-report-2012.pdf

What is to be done?

The government can begin to tackle these problems by taking action to control rolling stock leasing costs, including recouping lost revenue through a retrospective profit levy. For example, RMT has calculated that a 25% levy on pre-tax profits measured against a 7-year average would raise £58.5 million each year. A 50% levy would raise £116 million each year. This money could be reinvested into the railway.

Secondly, the government could establish a rolling stock arm – Great British Rolling Stock- financed by government borrowing, which can take over new rolling stock orders and begin replacing the costly leasing system and using it to promote UK manufacturing. Over time this could include expanding into direct rolling stock manufacture, beginning with key components.

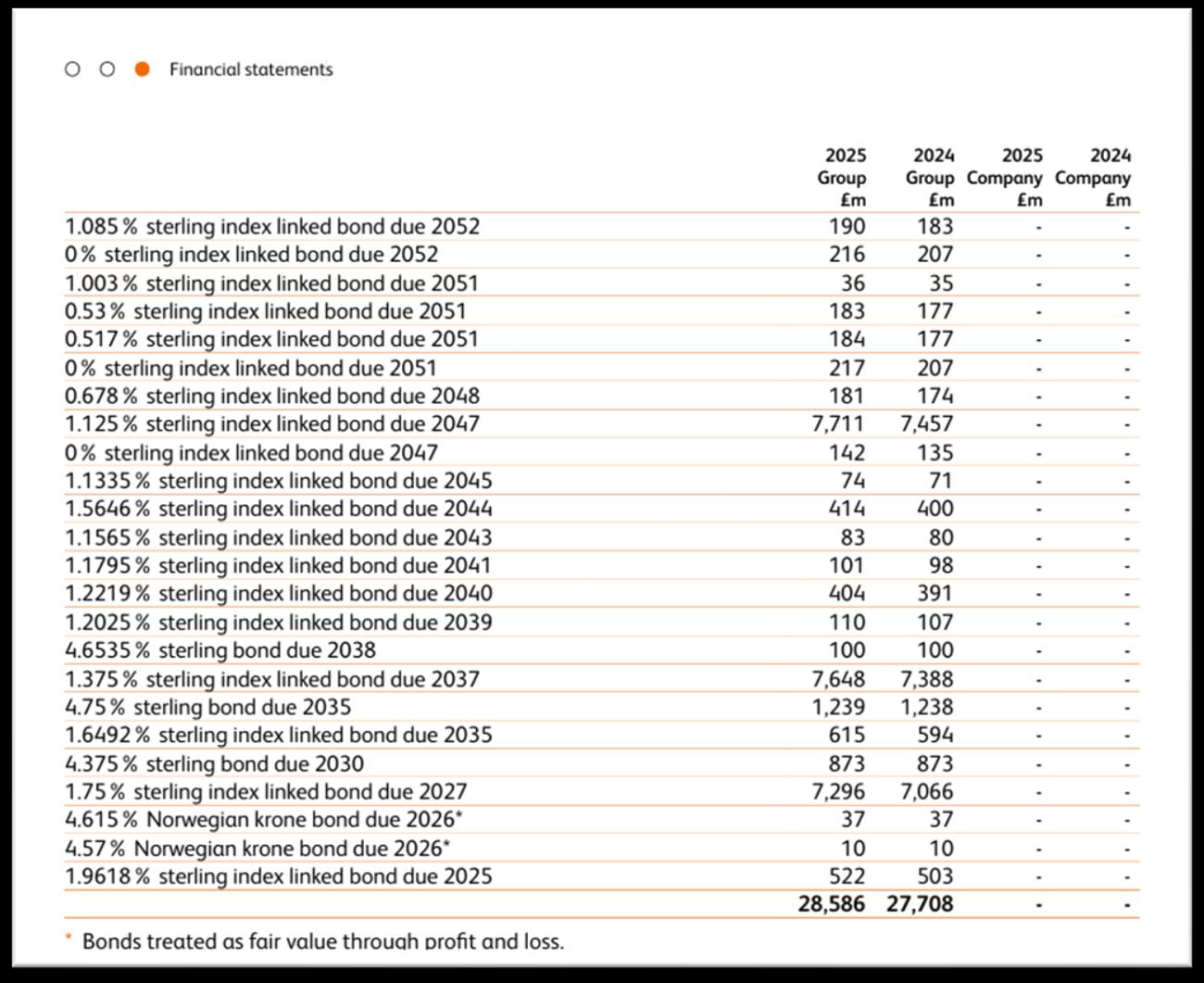

Protecting GBR from the inheritance of Network Rail’s debt:

Like its forebear British Rail, Great British Railways will come into the world saddled with debt obligations to the private sector. Where BR owed £900 million to the former rail companies, GBR will owe tens of billions of pounds to private bond holders as a consequence of a disastrous experiment with ‘off balance sheet’ financing after the collapse of Railtrack.21 As it was at that time a private sector not-for-profit company with the ability to borrow on its own account, Network Rail sold £30 billion in bonds to the markets to finance renewals without burdening the Treasury. Many of these bonds were

21 T. Gourvish, British Railways, 1948-73: Business History (Cambridge, 1986), pp. 27, 650; C. Wolmar, British Railways, British Rail: A New History (London, 2022), pp. 27-28.

index linked to RPI inflation and they all carry an absolute government guarantee to their holders. As the ORR’s April 2024 discussion paper acknowledged, this debt burden is one of the main drags on Network Rail’s productivity:

“financing costs for the rail infrastructure increased by 130% [between 2013 and 2024] driven by the rising cost of financing index-linked debt”

Yet, as we’ve seen, the ORR subsequently omitted this observation from their March 2025 report on productivity and justified this on the grounds that Network Rail has ‘limited control, and which is funded separately from its operations, support, maintenance and renewals expenditure.’ This is beside the point as the costs of financing Network Rail’s legacy of private debt now consume a significant proportion of the funds made available to the railway as a whole and this puts pressure on Network Rail to reduce spending elsewhere in ways that further undermine the basis of real productivity.

What is to be done?

Resolving this situation is complex because of the government guarantee to all existing private bondholders that their coupons and principal will be paid. The DfT has agreed with Network Rail that as each bond expires it will refinance using its own departmental loans. But the costs of the remaining private debt will be a very large drain on railways resources until 2052.22 Unless some action is taken to protect or ringfence GBR’s finances, the nationalised railway will be hamstrung, just as BR was before it, by continuing obligations to private interests dating from an era of failed railway policy.

22 See Appendix 1 for the outstanding private debt obligations.

Changing composition of Railtrack/Network Rail spending 1996-2024

Source: Railtrack and Network Rail Regulatory statements

A wave of insourcing in the outsourced and sub-contracted ‘supply chain’

One of the disastrous legacies of privatisation has been the fragmentation of the integrated railway value chain and its penetration by a host of outsourcing and subcontracting firms. The effect of this wave of outsourcing has been to create a mass of contractual interfaces and transaction costs that lead to cost escalation and inefficiency for both rail infrastructure and operations. For example, Network Rail’s current reliance on outsourcing renewals work creates cost pressures on the Company in several ways:

I. Firstly, the commercial margin on contracts in Network Rail’s supply chain divert much needed resources away from the frontline toward City investors, Subcontractor profits from renewals work can be estimated using data from Network rail’s Regulatory reports. Using the standard industry assumption of 6% margins on these contracts, we can see that contractor profits would have been in the region of £235 million last year and could total as much as £4.8 billion since 1996.

II. Secondly, large, shareholder value companies look to defend or increase their profit margins for dividend payments and share buybacks by passing on inflationary cost pressures to Network Rail.

III. Thirdly, the fragmented supply chain has a lack of resilience to change and the need for flexibility which entails costs on Network Rail. In circumstances where there are changes to funding streams, project planning, specifications, or unforeseen events, contractors faced with delays or changes claim compensation, leading to project cost overruns.

• In 2024-25, the ORR’s assessment of Network Rail’s financial performance noted that it had underperformed by £228 million in the first year of the Control Period. The primary reason was ‘rising costs of renewals projects, which contributed £255 million to overall underperformance in Year 1. These cost increases were associated with access constraints, resulting in longer delivery times and associated compensation payments. Additionally, funding challenges and inflationary pressures led to reprioritisation of work across the regions, causing additional cost when projects were paused or cancelled’ 23 The biggest component of efficiency savings made by Network Rail in 2023-24 was ‘more efficiently managing contracts’. This alone accounted for 25% of all savings achieved, indicating that this is where the flexibility and slack is. 24

• Detailed accounting of performance against cost targets for various headings of expenditure in Network Rail’s regulatory accounts show that a consistent theme has been the rising costs associated with the use of contractors in renewals, maintenance and enhancements work. In Civils projects for example, ‘higher inflation levels impacting materials and contractor prices, reflecting some of the rising prices across the economy as a whole.’25 In Electrical Power and Plant projects, late changes in scope, higher than anticipated supply chain prices and retendering of jobs due to unacceptable performance from contractors all resulted in higher costs. ‘26 In Network Rail’s analysis of its track maintenance costs, it was noted that ‘Expenses are higher than the previous year arising from additional work undertaken on the network and from greater than inflation materials and contractor costs increases’.27 Similarly with enhancements, Network Rail’s analysis of Great Western Mainline electrification project notes that ‘The financial underperformance this control period resulted from programme delays,

23 https://www.orr.gov.uk/media/27118/download p. 28

24 https://www.orr.gov.uk/media/27118/download p. 24

25 https://www.networkrail.co.uk/wp-content/uploads/2016/11/Network-Rail-Regulatory-FinancialStatements-2024.pdf, p. 116

26 https://www.networkrail.co.uk/wp-content/uploads/2016/11/Network-Rail-Regulatory-FinancialStatements-2024.pdf, p. 139

various costs pressures to close out the programme and substantiation of disputed costs’. 28

In summary, even as it comes together, the new publicly owned railway is still cut through with contractual interfaces that create wasteful transaction costs: between rolling stock companies and DFT Operator, between publicly owned train operators and outsourcing companies, between Network Rail and its sub-contractors; between rolling stock companies and train manufacturers. Alongside the costs of Network Rail’s legacy private sector debt and the rising costs of leasing rolling stock, these contractual interfaces are locking in inefficiency in the use of public money and fare revenue and dragging down the overall productivity of the railway.

What is to be done?

The government can tackle this by beginning a wave of insourcing across train operations and infrastructure to eradicate wasteful transaction costs and profiteering. Great British Railways should be mandated to establish with the recognized unions, working groups across train operations and infrastructure to identify priority target contracts and services to insource. This should involve taking over renewals work directly and building up an enhancements arm to undertake more enhancements work and especially to directly oversee megaprojects. [cite Stewart review]

The government understands the case for greater integration and indeed its own impact assessment as part of the Passenger Rail Services (Public Ownership) Act made this case. In addition to removing profiteering from rail, public ownership, the government said, would lead to “reduced administration costs (for example, from reduced costs associated with managing commercial contracts and administering competitions).” The assessment also noted that “by removing the commercially-driven focus on individual operators’ profit, it increases scope for decisions to be made with reference to optimising for the whole rail system, rather than individual commercial interests. There may be additional benefits from economies of scale.”29 While this was aimed at the Train operating companies, exactly the same logic applies to the whole of GBR and its inherited contractual maze.

Enabling the accumulation and retention of knowledge and skills

As well as saddling the rail industry with a dense mesh of contractual interfaces, privatisation operated to erode one of the main sources of productivity of staff: experience and the accumulation of skill. Academic research into knowledge management in large organisations indicates that an under-appreciated source of innovation in such organisations is the ‘long-run historical accumulation of ‘tacit

28 https://www.networkrail.co.uk/wp-content/uploads/2016/11/Network-Rail-Regulatory-FinancialStatements-2024.pdf, p. 150

knowledge’. Workers with security of employment learn, accumulate system knowledge and work out collectively how to problem solve in their workplaces. In addition, security of employment creates a better environment for critical feedback, whereas ‘hire and fire’ relations creates conformism and autocratic management. Workers with greater job security are also more likely to cooperate with managers on labour saving innovations.

Privatisation drove a coach and horses through this knowledge system at British Rail. Firstly, the industry saw a haemorrhaging of skills and tacit knowledge in maintenance functions. As one study put it, ‘draconian job cuts were imposed on all levels of workers within the industry. These workers frequently possessed skills and tacit knowledge of the industry, which were consequently lost when they were sacked.’ The damage created by privatisation went beyond the aggregate loss of skills. As we saw above, the culture of sub-contracting and outsourcing put in place structures that actively worked to erode knowledge accumulation and sharing. As one study noted in 2004:

“…one of the most devastating consequences of the privatisation process was the fragmentation and loss of industry knowledge. Running a railway – making decisions about investment, timetabling, safety, workforce deployment –requires an intimate acquaintance with changing infrastructure conditions, technological possibilities and service requirements throughout the network, that in the case of British Rail was held collectively by its workforce and managers and brought to bear upon decision-making through systems of cooperation and communication at all levels of the industry. This organisational knowledge base, never wholly centralised and much of it effectively tacit, was dissipated with the breakup of the industry. Many highly skilled engineers who knew things about the railway network that no one else did lost their jobs; some hired that knowledge back to the industry as private consultants. Habits of information sharing and freely given advice were interrupted by the requirements of commercial confidentiality. Hard-won accumulations of local and specialised knowledge were lost in the shift to an increasingly casualised and individualized workforce.”30

The fragmentation and contractual relations that still structure large parts of the industry lead to a relentless focus on driving operational cost out, focused invariably on labour costs. This creates a series of interrelated effects: preventing investment in workforce training; promoting churn and loss of knowledge; multiplying contractual interfaces that generate waste and duplication; eroding trust and breaching of the psychological contract between employers and employees. These in turn foster

30 Bart Cole, Christine Cooper, Deskilling in the 21st century: The case of rail privatisation, Critical Perspectives on Accounting, Volume 17, Issue 5, 2006, Pages 601-625; Jean Shaoul, Renaissance delayed? New Labour and the Railways (Catalyst, 2004), p. 19.

demotivation and presenteeism, which leads to wasteful expansions of HR and contract management spending to manage low trust employment relations.

If the organisation of the industry works to hold productivity down, the situation is compounded by the terms of the productivity debate promoted by the ORR, as we saw above. In focusing all attention on staff costs, the ORR helps to drive the industry further toward a crude focus on labour shedding, wage restraint, short termism and a continuation of the ‘low road’ labour market practices that dominate much of the industry. The end result is the structural low productivity characteristic of the deregulated, outsourced and sub-contracted parts of the industry and the emergence of the kind of skills gaps identified by the recent National Skills Academy for Rail (NSAR) reports. Similarly, the terms of the debate focus discussions of new technology solely on their potential for labour shedding.

What is to be done?

In addition to the wave of integration argued for above, RMT agrees with the recommendation of the NSAR on the need for cross-industry workforce planning. The creation of GBR is a massive opportunity to take a cross-industry strategic view of what workforce and what skills will be needed to deliver rail’s full potential, not just in terms of improved industry productivity but in terms of delivering what rail is for. Neither a full strategic view nor a workforce plan can be delivered by the fragmented industry we have today.31 Greater integration of the rail industry and the expansion of GBR’s directly owned workforce across more functions will enhance its ability to take a strategic view and deliver meaningful change.

GBR can create a new centralised fully funded apprentice scheme which will provide industry-wide training aimed at young workers and offer a career path from school leaver to retirement in the rail industry, providing pathways from uniformed, overalled and back-office apprenticeships. It can also specify, accredit and monitor apprenticeships within the supply chain, in consultation with unions.

GBR could undertake joint work with the unions to create job security and a framework within which future workforce and training needs can be identified, new technologies introduced and through which genuine workforce planning can take place. This would extend beyond agreements on no compulsory redundancies, for example to the kind of embracing workforce agreements that British Rail and the unions negotiated in the form of Promotion, Transfer, Redundancy and Resettlement (PTR&R). Such a framework would create an environment that could support the accumulation of knowledge and skills and the retention of this knowledge as new technologies are introduced in place of damaging labour-shedding.

31 Even collating the data on which the NSAR report conducts its analysis relies on conducting a survey of rail employers.

Changing the Treasury view of rail spending

Great British Railways needs to see a change in the way the Treasury assesses both investment and operational spending in the rail industry. At the highest level, RMT supports the case for further relaxing fiscal rules which limit borrowing for greater investment in rail infrastructure and rolling stock, and which press down on operational spending. Government accounting rules dictate that spending on enhancing the employment conditions of staff, including insourcing, more training and upskilling, are all to be seen as increased operational spending. Yet as the Productivity Institute have argued, from another perspective this is investment in one of the public sector’s key assets – a form of ‘capital deepening’ and it is vital to delivering enhanced productivity in public services including rail.

As the TUC have argued, the Green Book appraisal system used by government to assess the business case and ultimately funding for new transport schemes requires significant reform.32 “The current system is heavily biased against public transport schemes and towards road schemes. The high importance given to time savings of a few minutes for millions of motorists combined with over-estimated forecasts of traffic growth, translate into enormous ‘benefits’ which generally account for the vast majority of predicted monetised benefits from road schemes. By contrast, the assigned ‘cost’ of carbon emissions is severely underestimated (even with recent increases) and costs of carbon emissions in future years are heavily discounted”. 33 This bias means that environmentally damaging road projects that increase carbon emissions continue to get approved while public transport projects struggle to demonstrate a business case. Broader public policy goals achieved by public transport are also generally underestimated or ignored, so that investment in public transport to regenerate deprived areas is rare in the UK, unlike many European countries where social goals are given much higher priority.34

Summary:

GBR has huge potential to be a key governmental lever for generating higher productivity in the UK economy. It cannot substitute for deeper structural action to tackle UK business under-investment, but it can play a role in mitigating the effects of the UK’s

32 Gov.uk, ‘The Green book 2022’, https://www.gov.uk/government/publications/the-green-bookappraisal-and-evaluation-in-central-government/the-green-book-2020, 2022

33 Metz D. (2008) The Myth of Travel Time Saving Transport Reviews 28, 3, pp.321-336; Metz D. (2014) Travel demand: the basics. Local Transport Today, 643, March/April 2014; Marsden G. et al. ‘All Change? The future of travel demand and the implications for policy and planning’, May 2018. The First Report of the Commission on Travel Demand; and Goodwin P. (2018) ‘How should we use the road traffic forecasts in practice?’ Local Transport Today, 12 October 2018; TUC, ‘Public transport fit for the climate emergency’, 2023.

34 TUC, ‘Public transport fit for the climate emergency’, 2023

‘low road’ approach to investment and employment. However, its ability to play this role in an efficient and effective way will be limited by the disastrous legacy of privatisation. This legacy can be tackled by action to

• change the terms of debate around productivity in rail so that they recognize its true role as a public service in a complex society and economy, and to

• pursue greater integration across the span of GBR’s activities, bringing swathes of rail’s fragmented ‘supply chain’ into its direct operations and eradicating wasteful transaction costs and creating employment security to underpin a new generation of rail careers that support the accumulation and retention of skills and knowledge.