DEPAUL SENTIMENT REPORT: RETAIL OPPORTUNITIES MAY OR MAY NOT INCLUDE RESIDENTIAL

Segments of the retail sector continue to benefit from a reset that started before the pandemic and then became more critical as centers had to evolve or become extinct.

4 8 10

WHAT DOES IT TAKE TO GET A DEAL DONE? In a year filled with economic and political uncertainty, a number of starts and stops even for space within our own portfolio, and the eventual emergence of retail as the sweetheart product type, there are a handful of observations that David Strusiner of Craig Steven Development Corporation thought would be helpful to explore heading into 2025.

2025 RETAIL INVESTMENT THEMES AND PROGNOSIS: SUBURBAN CHICAGO RETAIL

As we begin a new year in the real estate industry, Charles S. Margosian Jr of Highland Management has his opinions of what 2025 will bring for retail investment in the Chicagoland area.

12

PRESERVING THE PAST WHILE BUILDING A NEW FUTURE: VARSITY THEATER AND BOOKMAN’S ALLEY MIXED-USE DEVELOPMENT POISED FOR SUCCESS IN EVANSTON Some developments just mean more to a community. The former Varsity Theater and Bookman’s Alley adaptive-reuse development in downtown Evanston is an example.

14

THE BOULDER GROUP NETLEASE MARKET REPORT

21

WINTER METRO CHICAGO RETAIL SPACE GUIDE

31

INFLATION? HIGH INTEREST RATES? NOTHING IS SLOWING THE LUXURY RETAIL MARKET Persistent inflation and higher interest rates might be worrying to consumers. But that hasn’t stopped many from making big-ticket retail purchases this year.

The Metro-Chicago Retail Space Guide is published twice a year by the Real Estate Publishing Corporation, 1010 Lake St Suite 210, Oak Park, IL 60301 • 312.933.8559. • www.rejournals.com

Publisher: Mark Menzies • menzies@rejournals.com

DePaul Sentiment Report: Retail Opportunities May or May Not Include Residential

By The Real Estate Center at DePaul University

Segments of the retail sector continue to benefit from a reset that started before the pandemic and then became more critical as centers had to evolve or become extinct.

Common strategies, paths that remain prevalent today, have been adding residential components and focusing attention to experiential elements that broaden the appeal of malls. Further, although not a new strategy, grocery-anchored and need-based centers have remained very

popular investment options, especially as some shakeout occurs in the grocery sector.

“Broadly speaking, retail is in a very good state operationally,” said Adam Tritt, Chief Development Officer, Brookfield Properties. “As far as the overall market, we’ve all been a little constrained by rising interest rates and have seen that impact everywhere.”

Brookfield’s Oakbrook Center is an example of a center that hasn’t needed to add apartments to

reach standard measures of success. According to Tritt, the Center continues to see sales gains and earlier in 2024 surpassed $1 billion in total sales.

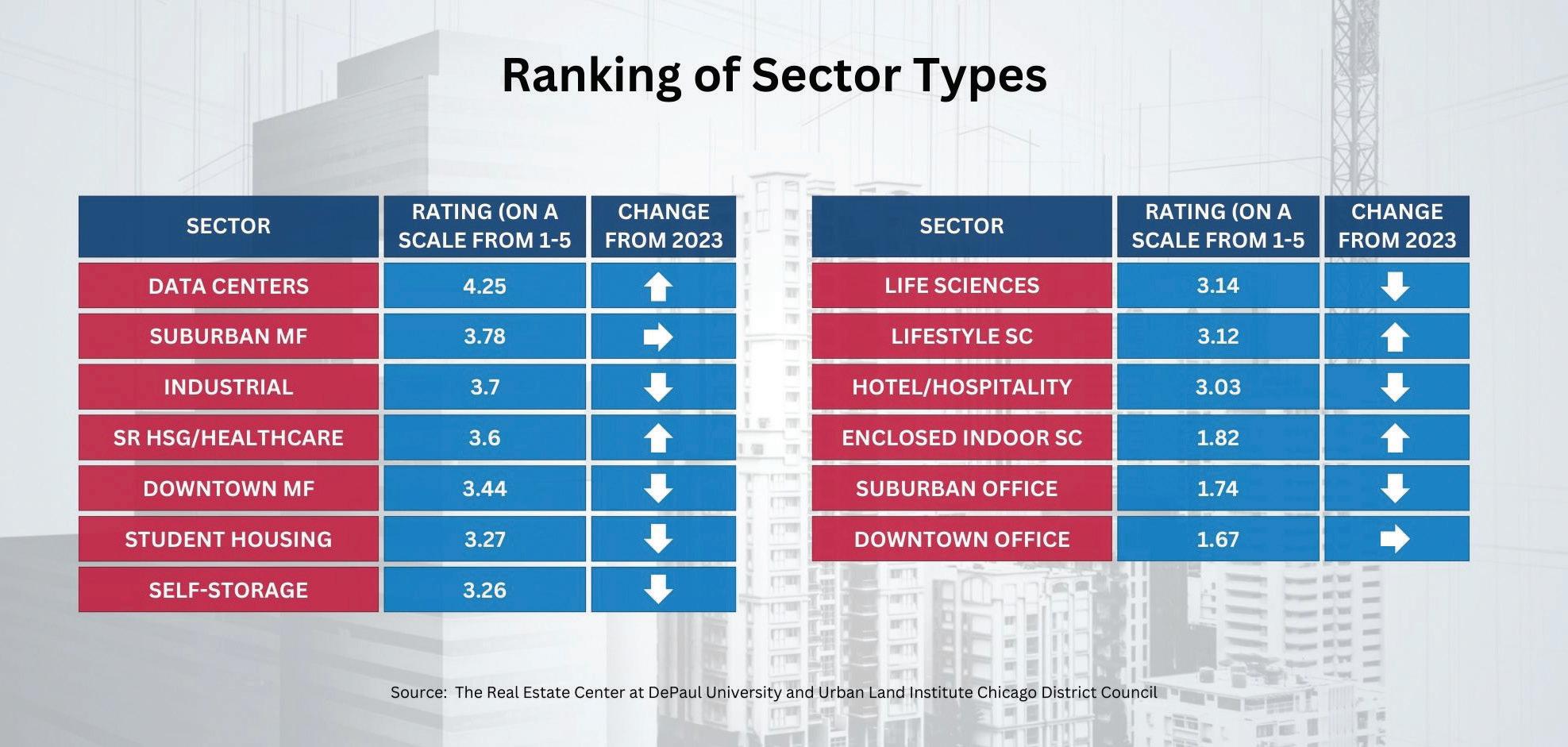

Despite success stories, CRE professionals participating in the DePaul Real Estate Center’s 2024 Sentiment Report, in collaboration with ULI Chicago, ranked retail properties among the weakest property types—better than office but not as good as self-storage—for investment.

Photo by Mike Petrucci on Unsplash.

“Retail is an interesting asset class whether it’s a purely retail or an asset with a strong retail core,” Tritt said. “You must view them as living breathing organisms that need a constant level of care and touch.”

Treating the retail asset as a living, breathing organism and making sure public spaces are being managed to ensure positive experiences emotional connections with visitors are created pays dividends, regardless of the point in a cycle.

“There’s plenty of room to find success as long as you’re committed to caring for that asset and trying to work the best out of it,” he added.

Over the last five years, there have been major retail property redevelopments that added multifamily components to the mix. Vicky Lee, senior vice president of development, Focus, believes there are opportunities in mixed-use development, specifically augmenting existing retail experience with residential uses and new public spaces.

“It depends on the specifics of the market and of the retail center,” Lee said, Some have winning potential while others don’t.”

In 2025, Focus expects to begin construction on 400 apartments at Old Orchard Mall, an iconic mall in Chicago’s northern suburbs. Recently, Old Orchard has undertaken a repositioning of

“There’s plenty of room to find success as long as you’re committed to caring for that asset and trying to work the best out of it.”

the retail space which includes the renovation of the existing Lord and Taylor box, the addition of a Bloomie’s and Louis Vuitton, and more. The addition of a multiphase multifamily community is being led by Focus and is based on the company’s experience redeveloping portions of Fox Valley Mall in Aurora, portions of Hawthorn Mall in Vernon Hills and The Atworth at Mellody Farm, also in Vernon Hills.

According to Lee, all three projects enjoyed strong lease-ups with tenants citing the benefits of an urban environment in a suburban setting.

“Walkability to grocery stores, restaurants, and entertainment are very attractive amenities,” she said.

Yet adding apartments isn’t always the answer and may not be a difference-maker.

Oakbrook Center, for example, doesn’t have multifamily but has mixed-use environment with hotel and office properties on site. Other advantages include having immediate adjacencies to residential communities, research corridors and major expressways and thoroughfares.

“Is multifamily going to be part of some of those success stories? Absolutely,” Tritt said. “Is it a must have? Of course not. If you’re talking a retail property the size of Oakbrook, apartments totaling 300, 600, or 1,000 units is not really going to move the needle.”

While metro area malls have flourished with or without apartments, there have been several prominent malls in the Chicago area, including Stratford Square and Spring Hill Malls, that closed permanently. That points back to the concept for any retail investments that if an asset has been overlooked for an extended period of time, it could face a long road to recovery.

Further, at some point the opportunity runway gets shorter and shorter. One of the most exciting things about this moment in the sector is that most have almost completely abandoned prototypical solutions. The solution for each asset is bespoke to its marketplace: the broad market that supports it economically and the closer-in community that lives with it every day.

“As a developer/owner, that’s super fun because there is no one recipe for success,” Tritt concluded.

The Real Estate Center at DePaul University, in collaboration with Urban Land Institute, Chicago District Council, annually produces a Chicago real estate sentiment report. This piece contains excerpts from the retail and multifamily section of the report. Read the full report.

Image by StockSnap from Pixabay

What does it take to get a deal done?

By David Strusiner, Craig Steven Development Corporation

In a year filled with economic and political uncertainty, a number of starts and stops even for space within our own portfolio, and the eventual emergence of retail as the sweetheart product type, there are a handful of observations that I thought would be helpful to explore heading into 2025.

The Who: How the Players are Evolving

Those of us who have been in the real estate industry for many years are familiar with the various critical participants in every transaction – the owner/seller and the user/buyer and typically the brokers representing each of those parties. In the fall, the US Government and the State of IL increased requirements for real estate licensees that leave most of us scratching

our heads and wondering what exactly we’re supposed to do. Two areas that we’re all trying to understand how to handle are 1) requirement for signed representation agreements prior to showing any property whatsoever, and 2) commission transparency related to cooperative commissions. It is expected the formalization of the agreements between the parties will benefit clients but creating new processes is something each company has to figure out.

Speaking of the player evolution, in the time period during and after the COVID-19 pandemic, new firms emerged within the Chicago retail market and brokers switched companies. Colleagues have been moving around within the industry, and it’s likely going to continue.

According to the WSJ on 12/3/2024, “more

Americans are looking to switch jobs than at any point in the past decade.” Finding the right player gets harder when professionals have limited longevity in their roles.

Retail is evolving too. Entertainment retail, including family destinations and dedicated single-purpose sports facilities for cricket, pickleball, and others, has had a lot of media attention. Are we oversaturated? I don’t know. Landlords are quick to capitalize on hot concepts, but it still feels like service, food and traditional fitness remain the most active tenants in the market. Amenities are also evolving, as we are incorporating EV stations at our shopping centers to increase appeal to retailers and shoppers alike.

Image by Phil Reese from Pixabay

The What and the Where: How Deal Awareness is Evolving

Remember how easy it was to put a deal on one platform and everyone would see it there and call you? Or, before that, in a book and everyone had a copy of it? That simplicity is long gone and now every communication channel known to mankind has real estate content that, hopefully, democratizes access to commercial real estate listing information. But let’s be honest: the proliferation of platform just makes the deal person’s job infinitely harder as they need to put out information on each deal on each platform AND make or respond to inquiries on each platform. Want to rent space from Craig Steven Development? You can call me at the office, call my cell, email me directly, email the general line, or message us through Facebook, Instagram, LinkedIn or Twitter. That doesn’t include the many deal platforms where properties are identified, including CoStar, LoopNet, Crexi, Brevitas, and Creco.ai, that many of our brokers are managing as well. I’m sure some tech out there pulls all the queries together to one place but at this point we are all navigating information overload in different ways. I am very grateful for the return to in-person events and individual meetings that keep opportunities top of mind outside of the machine we all create and feed that keeps transactions popping up in front of people on social media.

Do people expect to see vacancies and deals on social media? I think so. Does it “work”? How other companies calculate marketing ROI is their own business, but at Craig Steven Development we are regularly reviewing analytics for our outreach and working with our marketing company to deliver cost-effective and compelling content. That includes potential forays into TikTok or YouTube and increasing video content for specific platforms.

As long as we use marketing as the tool it’s meant to be, and remember it cannot replace sales and relationships, we are all able to maximize this new way of doing business.

The When: How Timelines are Evolving

Improving the space has always been a critical part of the deal timeline and there have been many changes in this arena. The team can range from space planner to architect to interior designer to corporate real estate development manager and goes all the way to… the municipality? Yes, you read that correctly. Getting things turned into the municipality sooner

may be less favorable to shoppers. Landlords often make accommodations to the space and the center, sometimes even relocating other tenants, to ensure fit for the new retailer which only increases the economic impact of a non-rentpaying space tied up in a lease. Regardless of whether the tenant is paying rent prior to opening, they are certainly without income the entire duration of this time. For one shopping center in the southern suburbs, we have 2 tenants who have signed leases but are not open – one 14 months ago and the other 9 months ago. They are still waiting for their permits. They haven’t asked for help, though if they asked we would be more than happy to jump in. Recently, one of our 1,200 sf tenants waited 4 hours at the county Health Department with no resolution of their issue. We were glad they let us know, as we were then able to call and beg the administrator for help. The next day they finally got their permit.

rather than later can make or break your project. As municipalities continue to outsource the processing of zoning and development requests to third parties, it becomes even more critical to make sure your project is buttoned up and in approval format as soon as it’s turned in.

We have discovered a need to adjust our approach. Understanding that there are limited numbers of staff members handling many requests in every governmental department is key. We acknowledge their reality, ensure we have prepared answers to their questions, and intervene to ask for help when we need to –which is increasing in frequency. Moreover, as an industry we should all encourage our tenants to take responsibility to build rapport with the municipalities and incorporate follow-up into their schedules.

Understanding expanded timelines impacts lease negotiations. A recent prospective tenant at a mixed-use building in the north suburbs insisted we provide a firm date for space improvements. This particular point extended the lease negotiation time which in turn delays the overall timeframe for the tenant to get open. And the date we had to provide, given uncertainty with the municipality, was 6 months out.

Permitting delays impact the landlord, the tenant, and the center itself. Co-tenants are impacted when space in the center has dark space for a prolonged period of time, and the center

For multi-site retailers, there can be unrealistic expectations based on prior experience with other municipalities. What we’ve encountered is that timing is variable depending on the specific location. Our recommendation is that tenants expedite the timeline in the beginning, and build in contingencies and extensions whenever possible. Assume no one else is concerned about your timeframe.

The 3 P’s

Three often interchangeable, synonymous terms characterize the only response we can have as professionals to the evolution we are experiencing: patience, perseverance, persistence. Those of us who have devoted our careers to the Chicago retail real estate industry have positioned and repositioned our businesses throughout multiple economic and political cycles. As we move forward into 2025, the most important thing we can do is to stay the course. And, if you are a tenant and you’ve done everything you’re supposed to do, reach out to your landlord. They may be able to help.

David Strusiner is Vice President and Owner of Craig/Steven Development Corporation. Nearly 30 years ago, David joined the firm founded by his father and uncle to manage retail leasing, increase portfolio occupancy to over 92%, and facilitate tenant retention to over 95%. Since its founding in 1968, Craig/Steven Development Corporation has developed in excess of four million square feet of property, including retail, office, industrial and residential projects. The company’s portfolio is located throughout metropolitan Chicago and other select markets.

David Strusiner

2025 Retail Investment Themes and Prognosis: Suburban Chicago Retail

By Charles S. Margosian Jr, Highland Management

As we begin a new year in the real estate industry, with it comes the inevitable forecasts and opinions of what to expect from real estate investment for the coming year. Given the pending changes in Washington D.C. and the ever-changing retail environment, we at Highland Management too have our opinions of what 2025 will bring for retail investment in the Chicagoland area. I thought this would be a great opportunity to share Highland Management’s outlook for retail in 2025.

• Retail is no longer a “bad” word. For several years leading up to the pandemic, lenders and institutional investors had written retail off as a dying asset class. Many pundits, myself proudly excluded, suggested that the internet and e-commerce would entirely replace bricks and mortar

stores for consumers. However, the pandemic proved that traditional bricks and mortar retail is not dead, and that, once again, demand for retail space can come from a broad spectrum of users. With significant new supply to apartment and industrial markets and office still struggling for occupancy due to work from home policies, retail is suddenly back in the good graces of institutional investors and lenders. This will mean good things for owners of retail shopping centers facing debt maturities, looking to sell and even making new acquisitions, though perhaps increasing competition for those of us trying to acquire or develop new product.

• Demand for Retail Space Will Continue to Be Strong. As we sit approximately 4 years after the height of COVID 19, retail leasing is as strong

as we have seen since before the Great Financial Crisis. Demand for well-located space in the Chicago suburbs is and will remain strong with consumer sentiment rebounding post-election and Fed appearing to have achieved the “soft landing” scenario. Both national retailers and local entrepreneurs continue to show interest in vacancies in our portfolio, and we have very little space available at the end of 2024. In addition to traditional retailers, we have continued to witness that retail space is well suited for service-related businesses, with Med-tail and food users moving strongly into our markets over the past 24-36 months. Chicagoland has had very little meaningful new supply of retail space since 2008, so we remain positive on the prospects for leasing at existing Shopping Centers. We fully

Photo by Ashim D’Silva on Unsplash

expect tight conditions in the suburbs to drive rental rate growth in our portfolio in 2025.

• Chicagoland might be “on sale”. Since the end of the pandemic, Chicago has suffered at the hands of an unrelenting and only partially-earned reputation for being a dangerous place to live that is losing population at a rapid clip. Together with a difficult tax environment and governmental problems, this has provided a meaty target for the mainstream media to attack. As a result, many of the same institutions and lenders that not so long ago said retail would die are extremely cautious and even negative about investment in Chicagoland. When investors and lenders start painting an entire metro with such broad-brush strokes, opportunity for smart and nimble investors inevitably emerges. We think that this has resulted in assets in Chicago being “on sale” (i.e. trading at higher yields) when compared other areas of the country and this will continue present selective acquisition opportunities to investors in all property types in 2025.

• Retail in Chicago Proper Will Come Back. Despite the overwhelming bad press and not insignificant political issues, we think retail in the City of Chicago will survive and begin to show signs of strengthening in 2025. Already, we are seeing reports of long vacant spaces on Michigan Avenue finding takers, and the Fulton Market area continues to be a hot spot. Chicago’s many advantages as a city, including a strong and educated labor market, plentiful access to fresh water and relatively low costs of living will continue to be compelling reasons for corporations to look at Chicago as a hub for growth vs. competing northern coastal cities. We further believe that 2025 will be year of “return to office”, with President Elect Trump’s advisors openly suggesting that the largest employer in the country (the Federal Government) will require employees to return to working from the office full time. As people return to the office, retail in the Loop, the State Street corridor and ultimately on Michigan Avenue will benefit from more foot traffic and begin to return to retailers’ radar screens as desirable locations for new stores.

So What Could Go Wrong … No good investor would ignore the risks and potential downsides to an investment, nor can we rightfully make a forecast without acknowledging the risks that remain to the overall US Economy and Chicagoland in particular. Here are few risks to retail investment we will be watching closely in 2025.

• Returning Inflation. At Highland Management, we believe the threat of reemerging inflation may be the most prescient threat to retail as an investment class While we are optimistic that any national tariff policy will be carefully considered and executed by the incoming administration, the fears of economists around a protectionist economic policy have merit. While the US trade policies with China over the past 8 years did not serve as the trigger for outsized inflation prints in recent memory, the threat and possibility of inflation from new tariffs must be considered. Another bout of higher inflation would serve to dampen the rebounding consumer sentiment and likely force more restrictive monetary policy from the Fed. Both together would deal a big blow to retailers’ sales and demand for retail space.

• Local Political and Tax Risks. Many of the attacks on Chicagoland and Illinois, while overblown in our opinion, are well founded. With the continual budget deficits and threats of further increases to already burdensome property tax rates, Cook County in particular, but Illinois as a whole, is walking a fine line. Political missteps and a lack of willingness on behalf of our leaders to address real budget issues will continue to cast clouds over the local real estate investment climate and impact the willingness for institutional investors and lenders to invest in Chicago.

• Interest Rates, Interest Rates, Interest Rates. While the Fed has cut short term rates by 75

bps since September and is widely expected to follow with an additional 25 bp cut on December 18th, the benchmark 10 year US Treasury rate has actually risen from a close of 3.84% on September 2, 2024 to the current level of 4.24% on December 10, 2024. Most fixed rate, long term real estate loans are benchmarked in some way against Treasuries, and Treasury rates have remained stubbornly at or near the 4.0% level since mid-2022. We do expect Treasury rates to remain elevated near these levels given the massive US debt issuance required to fund the Federal Deficit. Higher Treasuries will result in some real distress in refinancing markets, especially in deals of the 2020-2021 vintage with record low rates that will be maturing in 2025 and 2026. While this may present acquisition opportunities, it also poses recession risks to the overall economy. While we believe that a major recession is unlikely in 2025, we maintain that there is a risk of a recession. Fittingly, a negative shock to real estate financing markets will push spreads up for new loans on all asset types, and cap rates would follow.

Conclusions

Overall, we remain cautiously optimistic about the general trend in Retail real estate markets, especially in Chicagoland, where we feel that the negative news cycle has had an outsize impact on valuations. We also expect some amount of refinancing induced distress in the real estate markets, and the depth and severity of that distress may very well determine the course of real estate investment in 2025. Should the distress be gradual and manageable, it will present opportunities for investors without disrupting the overall economy. At the same time, there is a risk that the distress levels are broader than is widely believed, and may even be large enough to push the economy into a recession, hence the word “cautiously” before “optimistic” in our 2025 outlook. The one thing that we can always guarantee about predictions, some or many of them will be right and some will be dead wrong, but every year in our business is exciting. We here at Highland Management are wishing everyone in the retail real estate world a successful and exciting 2025!

Charles S. Margosian Jr. joined Highland Management in 2005 in the capacity of acquisition and development manager. Working together with other team members, Charles S. Margosian Jr. is responsible for lease negotiations, property and asset oversight as well as sourcing and financing new acquisition and development opportunities.

Charles S. Margosian

Preserving the past while building a new future: Varsity Theater and Bookman’s Alley mixed-use development poised for success in Evanston

By Dan Rafter, Editor

Some developments just mean more to a community. The former Varsity Theater and Bookman’s Alley adaptive-reuse development in downtown Evanston is an example.

The building at the center of this development once housed Evanston’s beloved Varsity Theater. After redevelopment, the project, spanning 1706 to 1712 Sherman Avenue in downtown Evanston, is now home to a 33-unit multifamily

property, 8,500 square feet of ground-floor retail and two live-work units.

The project will also include the redevelopment of Bookman’s Alley, a space that long held the Bookman’s Alley Bookstore opened by Roger Carlson in 1980. That store closed in 2013.

JLL is handling the initial leasing at the Varsity Theater and Bookman’s Alley. Guzman y Gomez will open a location at the Varsity Theater at 1710 Sherman Ave. as the first retail tenant.

Steven Rogin, owner of the former Varsity Theater, along with his partners, Campbell Coyle, DMA and BVI LLC, have led the redevelopment of the theater and adjacent Bookman’s Alley. The goal was to save as much of the character of the former theater, which opened in 1926 and closed in 1984.

The redevelopment of Bookman’s Alley will include new lighting, public art and outdoor seating to support street-level commercial at the space. The plan is to turn the alley into an

Photo courtesy of Varsity Theater, LLC.

“Between the history of the theater and the institution that Roger Carlson built over time with his bookstore, this is an extremely important spot in Evanston. We hope this new development will continue to be a cherished space for the Evanston community. It has always been a cherished space, and our goal is to build upon the tradition.”

activated community space with entertainment and retail. It’s a trend that many cities are embracing, including Detroit, which has activated several alleyways as part of its downtown rejuvenation.

Rogin said that he and his partners spent long hours crafting a redevelopment plan that would keep the spirit and feel of both the Varsity Theater and Carlson’s bookstore.

“Between the history of the theater and the institution that Roger Carlson built over time with his bookstore, this is an extremely important spot in Evanston,” Rogin said. “We hope this new development will continue to be a cherished space for the Evanston community. It has always been a cherished space, and our goal is to build upon the tradition.”

Rogin said that the Evanston community did not want a new development on this site that did not preserve the theater and bookstore feel. That led Rogin and his partners to focus on an adaptive reuse here.

“The community is interested in maintaining the character of the old structures in Evanston,” Rogin said. “Combine that with the attachment people have to the theater and the bookstore, and an adaptive reuse made the most sense.”

In a statement, Steve Schwartz, JLL senior vice president, said that JLL’s leasing data show that

demand is strong for downtown retail housed in revitalized historic spaces.

“Varsity Theater and Bookman’s Alley presents a unique opportunity for retail businesses in the food, entertainment and retail sectors to provide an unmatched experience serving Evanston and the surrounding communities,” said Schwartz, who represented The Varsity, LLC in its deal with Guzman y Gomez.

Paul Zalmezak, economic development manager with the City of Evanston, said that the Varsity Theater project also fulfills a bigger need in the city: There isn’t enough housing in Evanston to meet the demand for it. The addition of any housing, then, is a positive.

At the same time, the Varsity Theater/Bookman’s Alley project will provide yet another boost to Evanston’s revitalized downtown.

“The conversion of the Varsity Theater in Downtown Evanston couldn’t come at a better time,” Zalmezak said in a written statement. “More people living In downtown means more shoppers and diners. It is terrific to see how this redevelopment strikes a balance between preserving the building’s character and meeting the current and future needs of our community.”

Rogin agrees with this, and is happy to help bring more housing to downtown Evanston.

“You create vitality within a downtown community by bringing in more residential,” he said. “How do you bring more people into downtown beyond the 9-to-5 workday to support the businesses and create vibrancy? By adding more residential.”

Rogin and his partners kept much of the character of the Varsity Theater with their new residential development. The entire fourth floor of the building is exposed to the original infrastructure of the theater. Some of the apartments on the second and third floors feature original ceilings from the theater building.

Contractors are refurbishing some of the cameras from the theater and much of its plaster work. They are retaining the ornamental grates that covered the radiators at the Varsity Theater for use within the project.

The first residential tenants moved into the multifamily residences in August.

“Mixed-use developments like this are very successful today,” Rogin said. “The idea of being able to live, work and play in a single development has always been attractive. Mixed-use developments are especially attractive in communities like Evanston where you have mass transit. And here we also have access to Lake Michigan, Northwestern University, major medical facilities and other cultural institutions. When you bring both residents and businesses together, it creates dynamic space.”

“Cap Rates in the single tenant net lease sector increased for the 10th consecutive quarter.”

Net Lease Market Report

Q3 2024

Market Overview

Cap rates in the single tenant net lease sector increased for the 10th consecutive quarter within all three sectors in the third quarter of 2024. Single tenant cap rates increased to 6.50% (+3 bps) for retail, 7.75% (+8 bps) for office, and 7.15% (+5 bps) for industrial. The persistent upward trend in cap rates can be primarily attributed to sustained high interest rates. Additionally, there is a stagnant supply of net lease properties on the market resulting from limited transaction activity from both private and institutional buyers.

The supply of properties in the single tenant sector continued to rise in the third quarter, increasing by 6% compared to the previous quarter. The supply of net lease properties is expected to grow as tenant expansion plans continue and sellers add supply to the market for reasons including loan and/or lease maturities, tenant concentration issues, etc. The market continues to favor buyers as supply and demand dynamics play out, allowing investors to be more selective and demand higher yields. As developers begin to construct properties at higher yield on cost, the expectation is that cap rates will continue to expand aside from the most sought-after properties, tenants and markets.

Current sellers of net lease properties, whether developers or owners, hope that the recent 50 basis point cut in the federal funds rate will increase transaction velocity and potentially improve pricing in their favor. However, most market participants remain cautious, and do not expect cap rates to compress in the near future unless there are continued rate cuts. Furthermore, it is expected that the 1031 market will need two or three quarters of increased activity in order to absorb supply in the net lease market. It is important to note that historically, interest rate moves do not immediately correlate to net lease cap rates as a lag exists.

Despite a low probability in cap rate compression, the expectation is that the recent federal funds rate cut will assist in spurring transactions. Lower borrowing costs may encourage some buyers who have been sitting on the sidelines to re-enter the market, increasing buyer demand. Investors will continue to monitor the Federal Reserve’s monetary policy and its impact on the capital markets. The potential for further rate cuts in 2024 could gradually improve the transaction velocity and pricing in the net landscape near the mid-point of 2025.

1. Net Lease Auto Sector

2. Net Lease Casual Dining Sector

3. Net Lease Dollar Store Sector

4. Net Lease Drug Store Sector

5. Net Lease Quick Service Restaurant (QSR) Sector

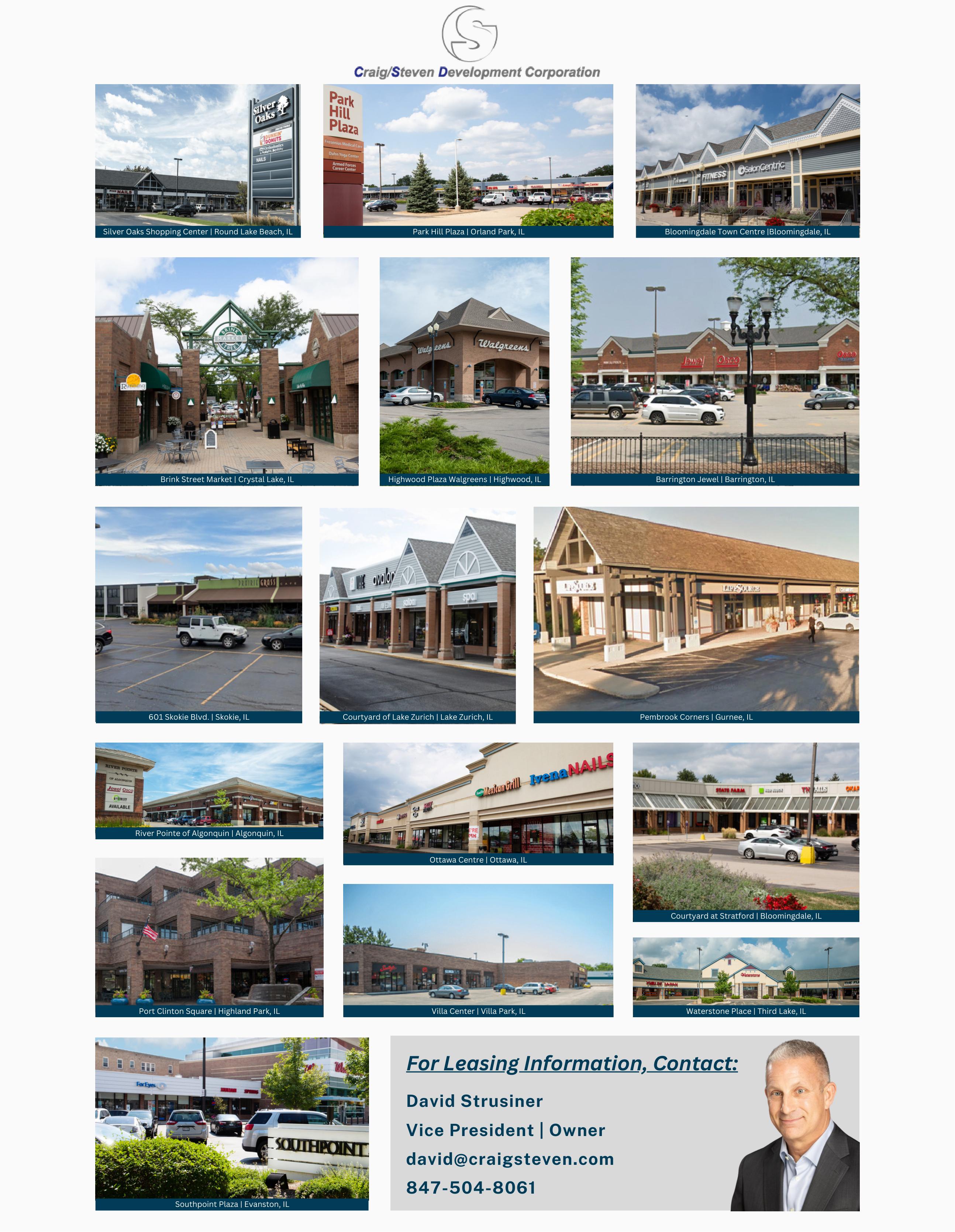

River Pointe of Algonquin Phase I

Algonquin

Bloomingdale Town Centre NEC Lake St & Bloomingdale Road

Year Built/Year Renovated: 1996

Type of Center: Neighborhood No. of Stores: 9

Total Space: 32,246

Total Available Space: 0

Available Minimum: 0

Maximum Contiguous: 0

Anchor Tenants: AccuQuest Hearing Center, Pink Hair Studio, DG Market

Rental Rate: $19.00

Total Passthroughs: $6.88

Bloomingdale Town Centre Phase III

NEC Lake St & Bloomingdale Road

Year Built/Year Renovated: 2005

Type of Center: Neighborhood No. of Stores:

Total Space: 15,000

Total Available Space: 15,000

Available Minimum: 1,200

Maximum Contiguous: 15,000

Anchor Tenants: Future Development

Rental Rate:

Total Passthroughs:

Aurora Restaurant

Year Built/Year Renovated: 2008

Type of Center: Community No. of Stores: 24

Total Space: 14,715

Total Available Space: 6,334

Available Minimum: 1,200

Maximum Contiguous: 6,334

Anchor Tenants: Tropical Smoothie Cafe, Bank of America, Double Yolk Pancake House, Verizon

Anchor Tenants: Apple Store, Ramsay’s Kitchen, Filson, Bluemercury

Rental Rate: Contact Broker

Total Passthroughs Contact Broker

McHenry

Naperville

Lake Zurich

Hoffman

Naper Ridge Plaza

Naper Boulevard & Ridgeland Ave

Year Built/Year Renovated: 2004

Type of Center: Neighborhood No. of Stores: 2

Total Space: 30,000

Total Available Space: 25,000

Available Minimum:

Maximum Contiguous:

Anchor Tenants: Office Depot, Fifth Third Bank

Rental Rate: Negotiable

Total Passthroughs: N/A

Year Built/Year Renovated: 2018

Type of Center: Neighborhood No. of Stores: 10

Total Space: 18,500

Total Available Space: 0

Available Minimum: 0

Maximum Contiguous: 0

Anchor Tenants: Great Clips, Spice Mart

Rental Rate: N/A

Total Passthroughs: N/A

Year Built/Year Renovated: 2016

Type of Center: Neighborhood No. of Stores: 14

Total Space: 24,883

Total Available Space: 2,310

Available Minimum: 2,310

Maximum Contiguous: 2,310

Anchor Tenants: Jewel/Osco

Rental Rate: $42.50

Total Passthroughs: $7.85

Year Built/Year Renovated: 1988

Type of Center: Neighborhood No. of Stores: 30

Total Space: 61,121

Total Available Space: 11,500

Available Minimum: 1,400

Maximum Contiguous: 3,000

Anchor Tenants:Clothes Mentor, Culver’s, Namaste Grocery Store

Rental Rate: $16.00

Total Passthroughs: $8.11

S. Margosian

S. Margosian

Total Space: 10,000

Total Available Space: 10,000

Available Minimum: 3,800

Maximum Contiguous: 10,000

Anchor Tenants: Rental Rate: $18.00-$25.00 Total Passthroughs:

Total Space: 63,446

Total Available Space: 18,851

Available Minimum: 2,500

Maximum Contiguous: 12,000

Anchor Tenants: .AT&T Verizon, Rosati’s Pizza, Game Stop Rental Rate:

Total Passthroughs:

Total Space: 137,000

Total Available Space: 6,559

Available Minimum: 1,475

Maximum Contiguous: 3,589

Anchor

Rental Rate: $20.00

Total Passthroughs: $9.25

Anchor

Rental

Total Passthroughs: Contact Broker

The Shoppes at Stony Creek

Year Built/Year Renovated: 2023

Type of Center: Community No. of Stores: 17

Total Space: 39,393

Total Available Space: 1,200

Available Minimum: 1,200

Maximum Contiguous: 1,200

Anchor Tenants: Jewel/Osco, Ace Hardware

Rental Rate: $25.00

Total Passthroughs: $9.65

Year Built/Year Renovated: To Be Built

Type of Center: Neighborhood No. of Stores: TBD

Total Space: 18,000

Total Available Space: 18,000

Available Minimum: 1,200

Maximum Contiguous: 12,000

Anchor Tenants: Jewel/Osco, McDonald’s, JP Morgan Chase

Rental Rate: Please Call

Year Built/Year Renovated: 2004

Type of Center: Neighborhood No. of Stores: 13

Total Space: 29,748

Total Available Space: 2,561

Available Minimum: 1,169

Maximum Contiguous: 0

Anchor Tenants: Lou Malnati’s, CK Salon, Home of the Sparrow, Aki of Japan

Rental Rate: $12.00-19.00

Total Passthroughs: $5.36

Year Built/Year Renovated: 1985

Type of Center: Neighborhood No. of Stores:

Total Space: 19,553

Total Available Space: 1,200

Available Minimum: 0

Maximum Contiguous: 0

Anchor Tenants: Dollar General, Supercuts, Stella’s

Rental Rate: $16.00

Total Passthroughs: $4.10

Villa Park

Year Built/Year Renovated: 1970/1987

Type of Center: Neighborhood

No. of Stores:

Total Space: 100,000

Total Available Space: 13,685

Available Minimum: 1,500

Maximum Contiguous: 10,000

Anchor Tenants: Jimenez Foods, Mark Drug Medical Supply

Rental Rate:

Total Passthroughs:

Inflation? High interest rates? Nothing is slowing the luxury retail market

By Dan Rafter, Editor

Persistent inflation and higher interest rates might be worrying to consumers.

But that hasn’t stopped many from making big-ticket retail purchases this year. Need proof? JLL says that the U.S. luxury retail sector recorded more than $75 billion in sales last year.

And this year? JLL says that 2024 should be another stellar year for luxury retailers.

Luxury retailers, as the name suggests, are those brands that specialize in high-price items. Think Louis Vuitton, Versace and Dior.

In its 2024 luxury retail report, JLL said that from 2020 to 2023, luxury retail sales in the United States saw a compounded annual growth rate of 8.6%.

The future looks bright for this segment, too. Citing statistics from Statista, JLL predicts that U.S. luxury retail sales will hit $77.3 billion in 2024 before rising to $83.3 billion in 2028.

With numbers like that, it’s not surprising that many luxury retailers saw notable revenue gains last year.

JLL pointed to LVMH, the company behind brands such as Louis Vuitton, Dior, Fendi and Tiffany and Co., which saw $85.483 billion in revenue in 2022. That figure jumped to $95.095 billion last year. The brand also boosted its number of stores to 6,097 in 2023, a increase of 7% from a year earlier.

Richemont, the company behind Cartier, Van Cleef and Piaget, saw its 2023 revenue jump 6% from 2022, hitting $22.755 billion last year. Prada Group revenues jumped 13% to $5.2 billion in 2023.

Of course, some markets are more likely to attract luxury retailers. JLL said that New York City and Los Angeles remain preferred U.S. destinations for such high-end brands. Both markets accounted for a combined 36.9%

of new luxury openings from July of 2023 through the same month this year.

And while headlines consistently state that large indoor malls are struggling – and it’s true that many are – these retail centers remain coveted destinations for luxury brands. These malls must be of the high-end variety, but those that are see a steady stream of new luxury retailers.

According to JLL’s research, malls accounted for nearly half of all new luxury store openings from July of 2023 to July of 2024. Class-A malls also boast higher occupancy rates, with an average vacancy rate of 5.8% in the second quarter of 2024.

Luxury retailers are similar to others when it comes to success today. Those that are thriving are focusing on the omnichannel approach, putting money into both their online presence and physical storefronts. Many luxury brands use their storefronts as ways to entice consumers to later make a purchase at their online store.

Just consider this stat from JLL’s report: E-commerce’s share of total retail sales rose to 16% in the second quarter of this year. That, though, is below the pandemic high of 16.4% in the second quarter of 2020. More than 80% of retail sales, then, still occur in physical stores.

JLL also cites another interesting trend: Because of a lack of desirable retail space, luxury brands are reinvesting in their existing flagships to personalize the in-store experience. For example, retailers are taking advantage of rising consumer travel by partnering with hospitality operators to improve the in-person experience.

JLL points to Louis Vuitton, which will open its first Louis Vuitton hotel in 2026 on the Champs-Elysées in Paris, marking a significant hospitality investment that will offer consumers a personalized travel and retail experience.