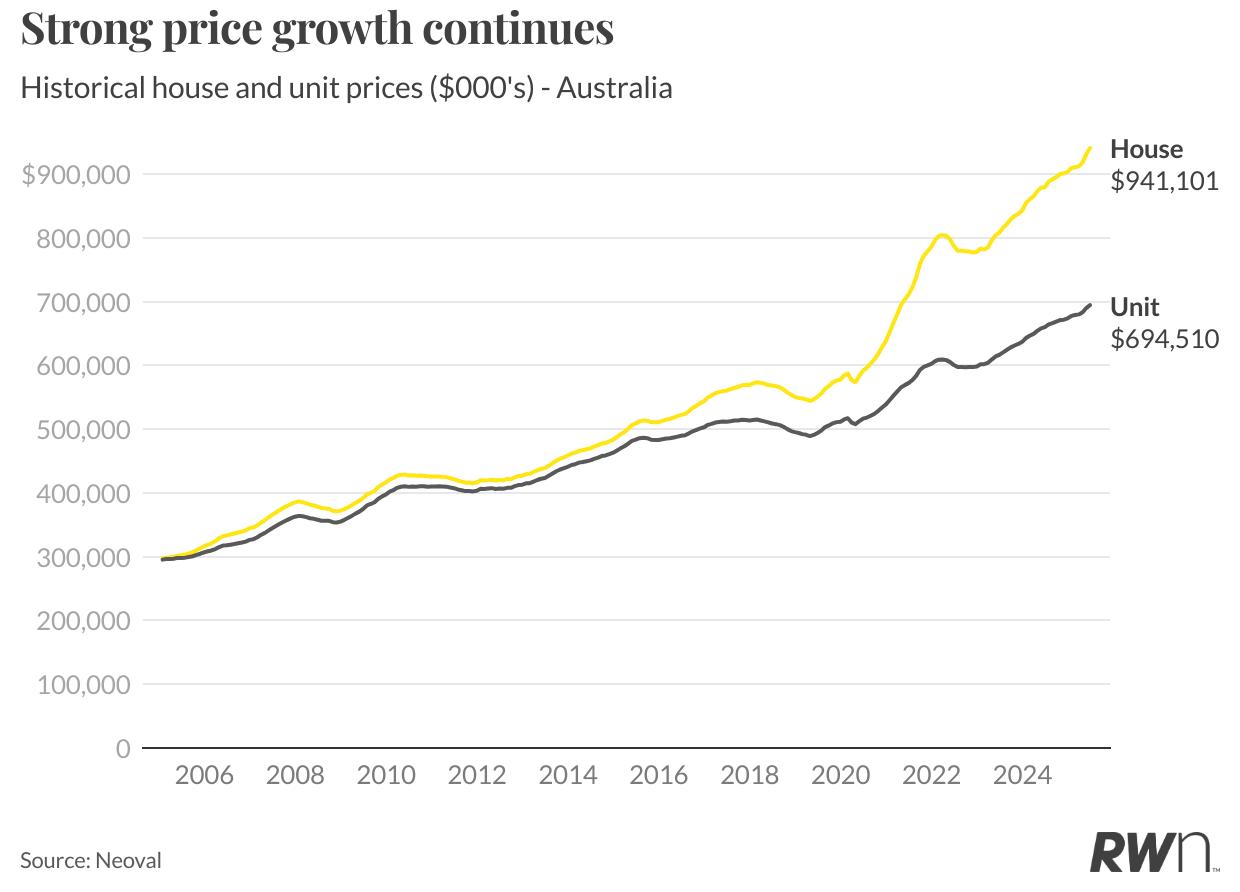

Australian property prices continued their remarkable acceleration through June 2025, with house prices surging 1.0 per cent to reach $941,101, delivering robust annual growth of 7.0 per cent. Unit values advanced 0.6 per cent to $694,510, maintaining steady 5.2 per cent year-on-year appreciation. The momentum reflects the powerful impact of two interest rate cuts this year, with the March quarter inflation result of 2.4 per cent reinforcing market expectations for additional monetary policy easing in the months ahead.

Every major market is now exhibiting monthly growth rates that signal significant momentum building across the nation. Perth’s exceptional 1.3 per cent monthly growth continues to lead the charge, while Brisbane’s surge past $1.05 million demonstrates the broad-based nature of this acceleration phase. This coordinated strengthening appears directly linked to the Reserve Bank’s cutting cycle, with buyers moving decisively ahead of anticipated further rate reductions.

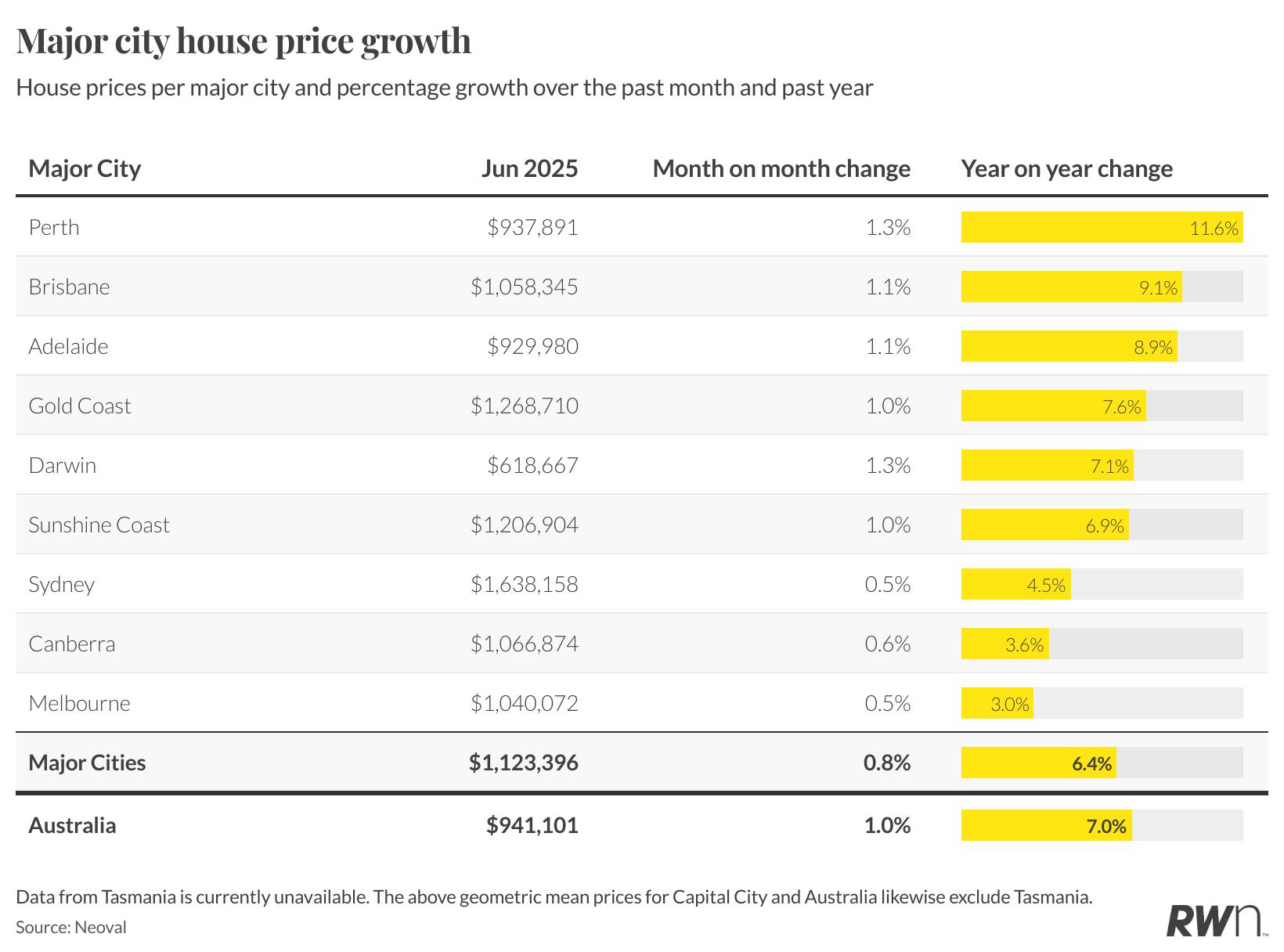

The capital city housing market continued displaying exceptional performance across Australia’s major cities, with Perth maintaining its position as the standout performer. Perth recorded a remarkable 1.3 per cent monthly gain, reaching $937,891 and delivering exceptional 11.6 per cent annual growth, positioning the city firmly on track toward the million-dollar threshold.

Brisbane achieved a significant milestone, surpassing $1.05 million with its median reaching $1,058,345 after a robust 1.1 per cent monthly increase and solid 9.1 per cent annual appreciation. Adelaide demonstrated similar strength with 1.1 per cent monthly growth to $929,980, reflecting 8.9 per cent annual growth and reinforcing its connection to the resource sector boom.

Even the traditionally slower markets showed renewed vigour, with Sydney recording 0.5 per cent monthly growth to $1,638,158, while Melbourne matched this pace to reach $1,040,072. Darwin’s 1.3 per cent monthly surge to $618,667 highlighted the broad-based nature of the current acceleration phase, with every major capital now contributing to national momentum.

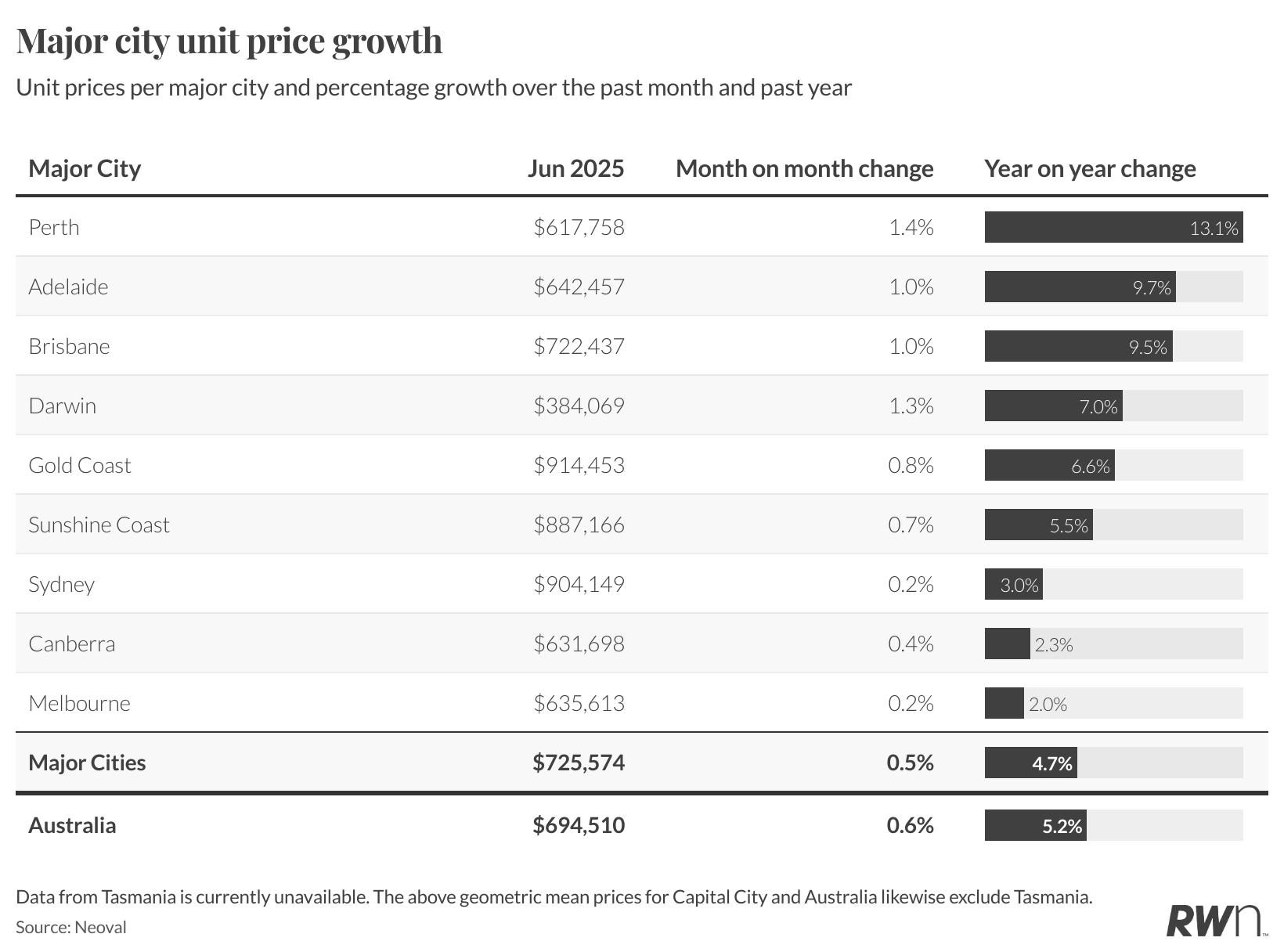

The unit market across major cities demonstrated consistent momentum, with Perth units continuing to lead year-onyear growth at 13.1 per cent despite recording a substantial 1.4 per cent monthly gain to $617,758. This outstanding performance significantly outpaces Perth’s strong house market, suggesting investors and first home buyers are increasingly targeting the more affordable unit sector.

Adelaide and Brisbane units both recorded strong 1.0 per cent monthly growth, reaching $642,457 and $722,437 respectively, with both markets achieving impressive annual growth of 9.7 per cent and 9.5 per cent. Darwin’s unit market posted exceptional 1.3 per cent monthly growth to $384,069, demonstrating 7.0 per cent annual appreciation.

Sydney units moved closer to the million-dollar threshold with 0.2 per cent monthly growth to $904,149, maintaining modest 3.0 per cent annual appreciation. The Gold Coast maintained its premium position at $914,453 with 0.8 per cent monthly growth, while Melbourne continued showing the most subdued performance with just 0.2 per cent monthly growth to $635,613, highlighting the divergent recovery patterns across Australia’s unit markets.

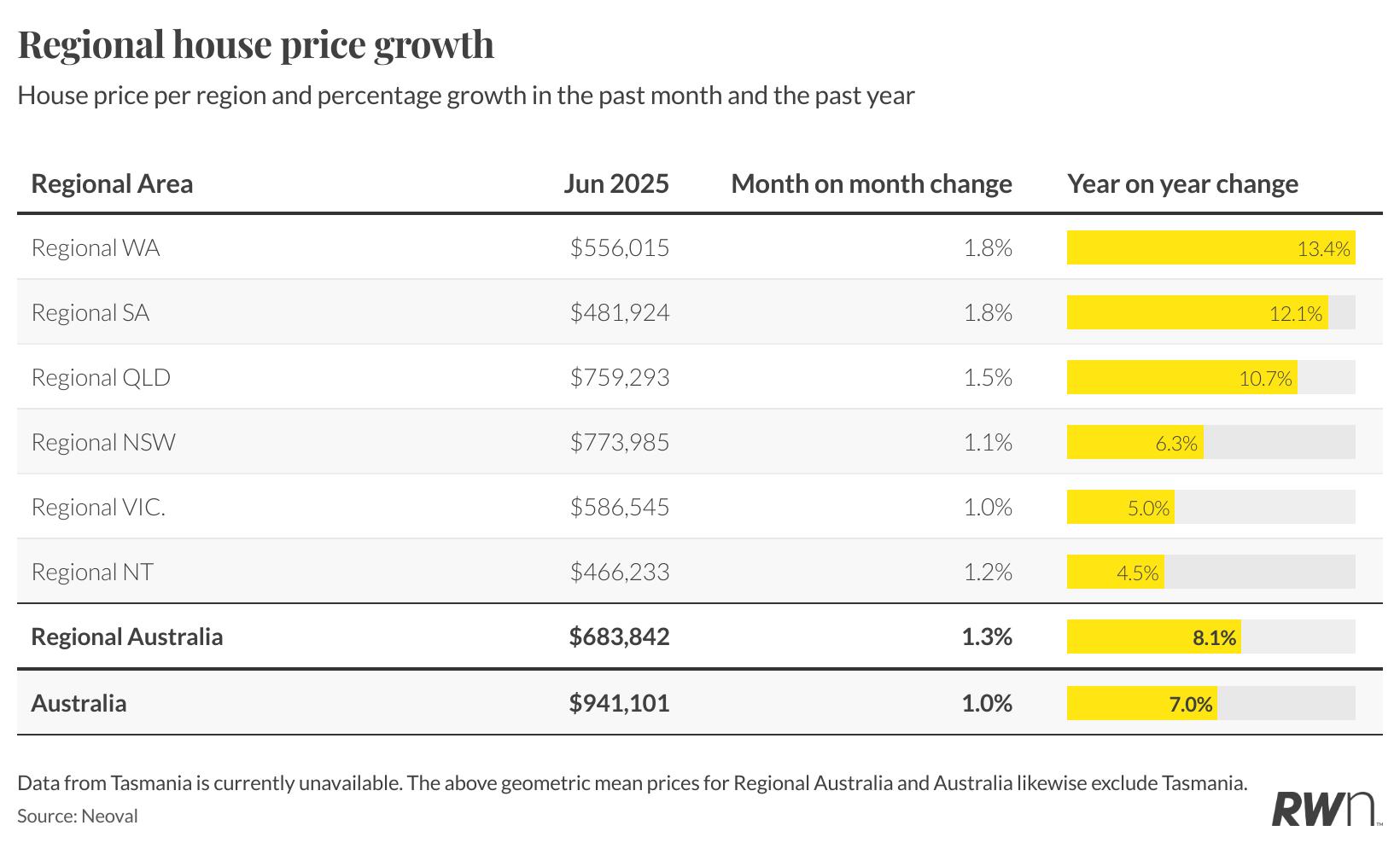

Regional markets continue demonstrating significant variation, with resource-rich states maintaining their leadership positions. Regional Western Australia leads with exceptional 1.8 per cent monthly growth, reaching $556,015 and delivering remarkable 13.4 per cent annual appreciation, driven by the continued strength of both iron ore and expanding lithium operations.

Regional South Australia follows closely with 1.8 per cent monthly growth to $481,924, achieving substantial 12.1 per cent annual growth. The robust performance reflects copper production’s positive impact on local employment and population growth. Regional Queensland maintained strong momentum with 1.5 per cent monthly appreciation to $759,293, supported by ongoing coastal lifestyle demand and population inflows.

Regional New South Wales recorded solid 1.1 per cent monthly growth to $773,985, though annual growth remained more modest at 6.3 per cent. Regional Victoria and Northern Territory showed more conservative monthly increases of 1.0 per cent and 1.2 per cent respectively, delivering annual growth of 5.0 per cent and 4.5 per cent. The resource sector’s continued strength provides fundamental support for superior performance in Western Australia and South Australia.

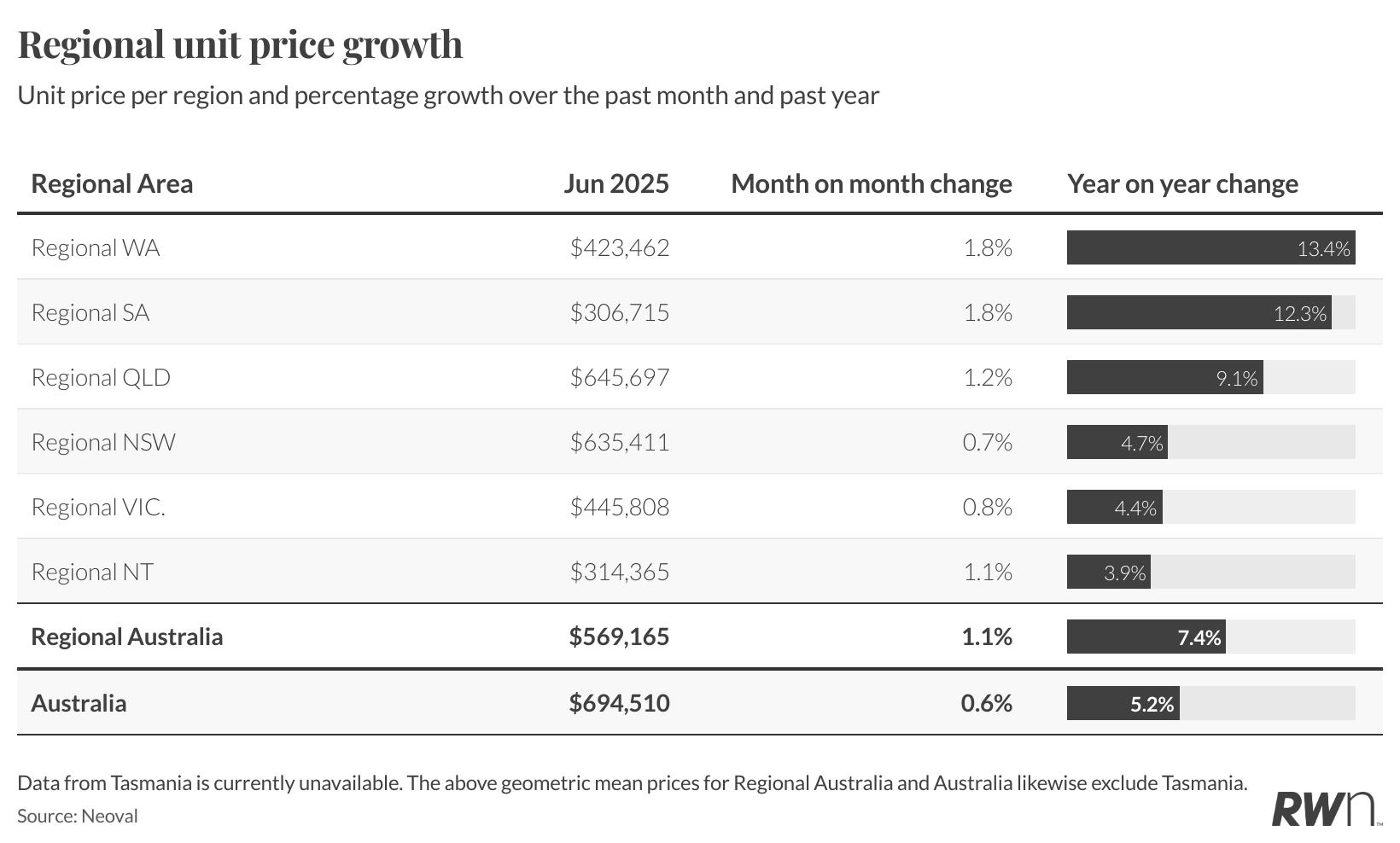

The regional unit market mirrors housing sector trends, with Western Australia and South Australia leading annual growth at exceptional 13.4 per cent and 12.3 per cent respectively. Both regions recorded substantial 1.8 per cent monthly increases, reaching $423,462 and $306,715, continuing their remarkable momentum driven by resource sector strength and relative affordability.

Regional Queensland maintains robust conditions with 1.2 per cent monthly growth to $645,697, achieving strong 9.1 per cent annual appreciation. The performance reflects ongoing demand for coastal lifestyle properties and investment opportunities. Regional New South Wales recorded modest 0.7 per cent monthly growth to $635,411 with more conservative 4.7 per cent annual appreciation.

Regional Victoria and Northern Territory showed limited momentum with 0.8 per cent and 1.1 per cent monthly growth respectively, delivering annual appreciation of 4.4 per cent and 3.9 per cent. Overall, regional Australia’s unit market continues significantly outperforming the national average with 7.4 per cent annual growth, highlighting the ongoing strength in regional markets driven by lifestyle preferences, relative affordability, and resource sector prosperity.

MAJOR CITY HOUSE PRICES (%CHANGE) | SINCE LAST MONTH

$ GEOMETRIC MEAN PRICE % CHANGE IN PRICE

REGIONAL HOUSE PRICES (%CHANGE) | SINCE LAST MONTH

LISTINGS ACTIVITY

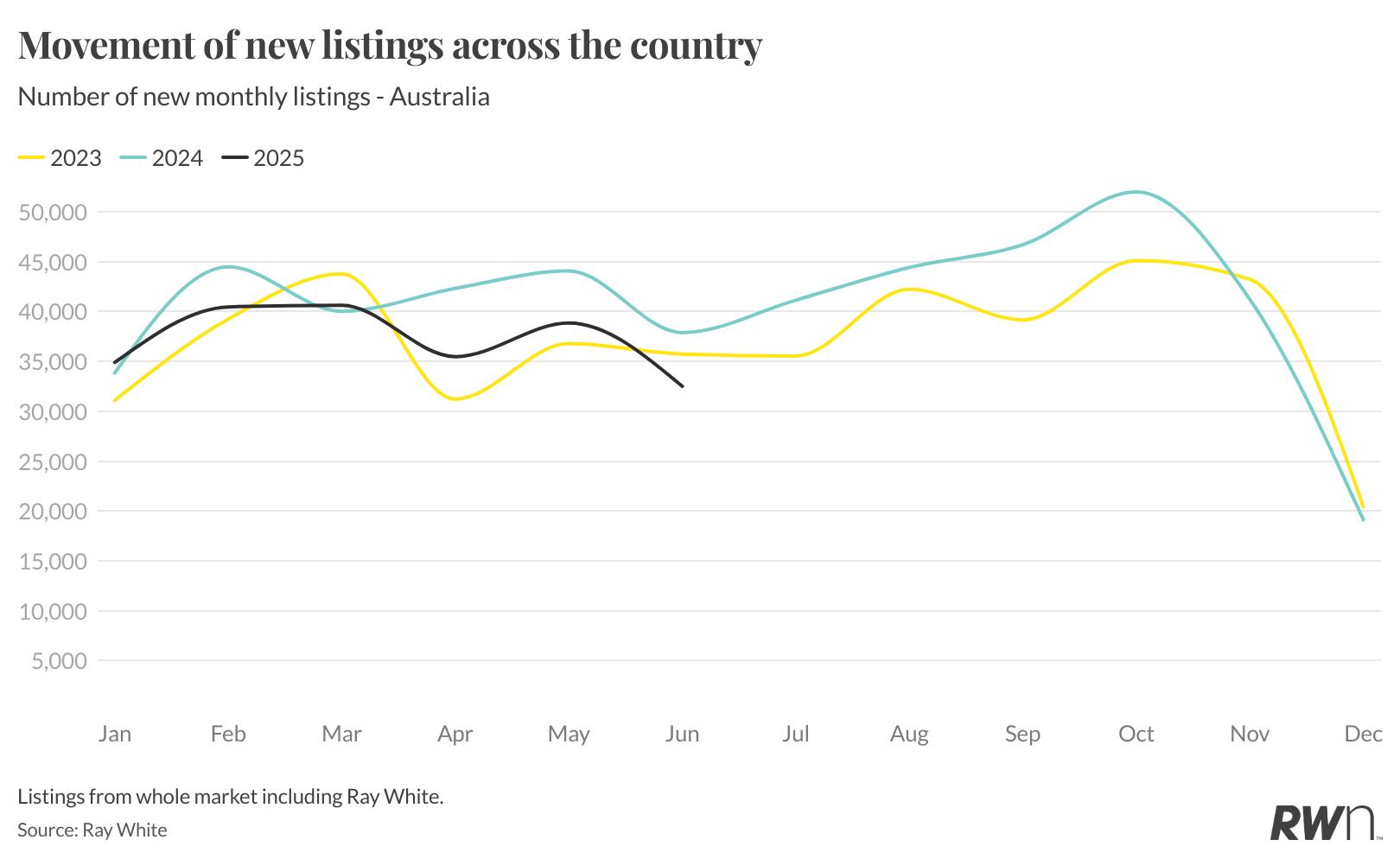

National listing patterns reveal a concerning trajectory through 2025, with June recording 32,494 new listings compared to 37,871 in June 2024 and 35,730 in June 2023. This represents a substantial 14.2 per cent decline from 2024’s stronger performance and a 9.1 per cent reduction from 2023 levels, highlighting the severe supply constraints that have characterised this year.

The annual comparison demonstrates 2025 has consistently tracked below both 2023 and 2024 listing volumes throughout most months, creating the tightest supply conditions in recent years. January through May 2025 recorded particularly weak performance, with monthly shortfalls ranging from 3,000 to 9,000 fewer listings compared to the same periods in 2024.

This persistent shortage represents a dramatic shift from 2024’s robust listing activity, which consistently exceeded 2023 levels through most of the year. The magnitude of 2025’s underperformance suggests structural supply constraints beyond normal seasonal variations, with total listings for the first six months running approximately 25,000 properties below 2024’s pace. This severe shortage of properties coming to market represents the critical factor underpinning current price acceleration across most Australian markets.

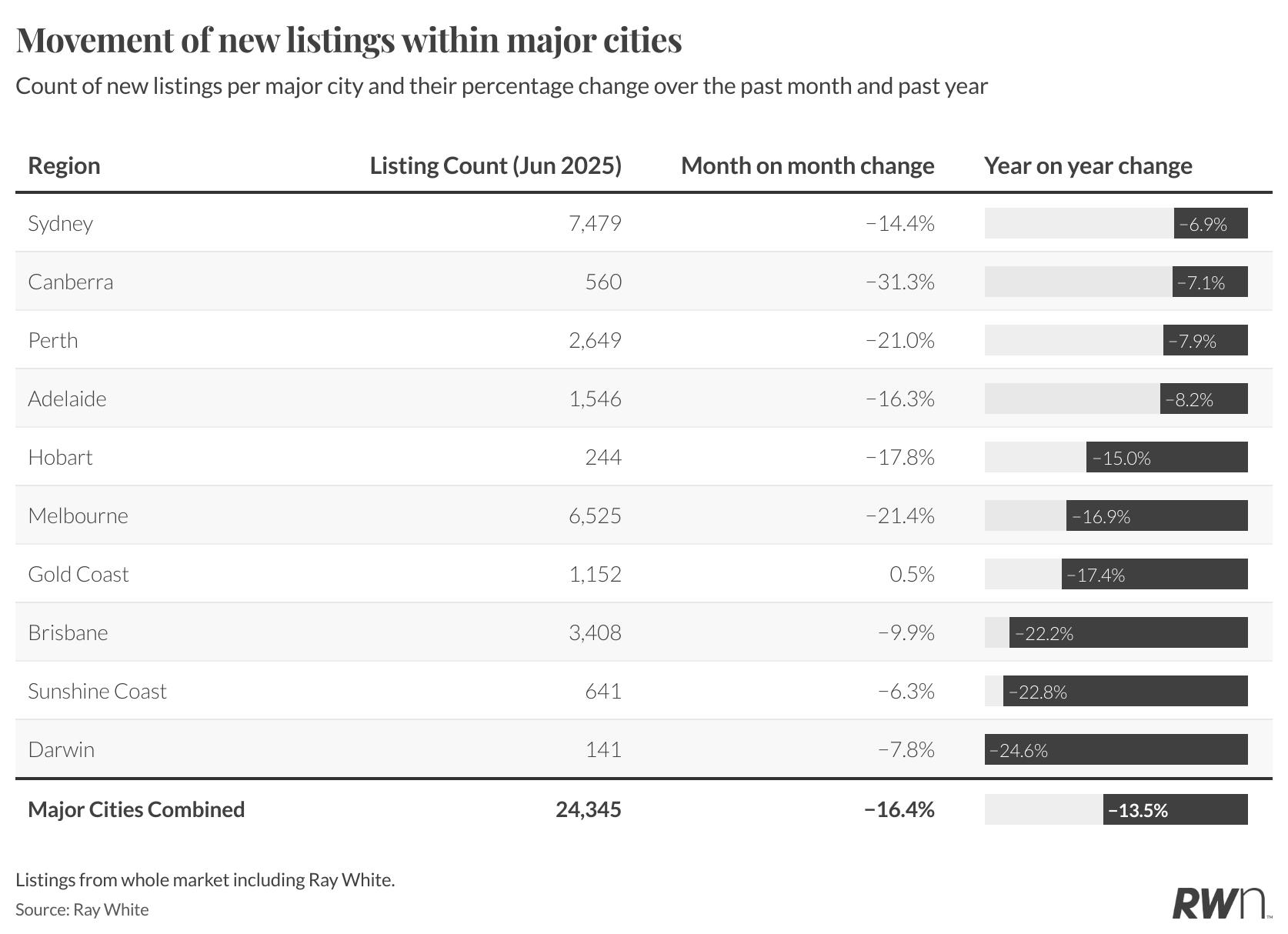

Major cities recorded 24,345 new properties in June, experiencing a significant 16.4 per cent monthly decline and 13.5 per cent annual reduction. Sydney dominated with 7,479 listings but recorded a substantial 14.4 per cent monthly decrease and 6.9 per cent annual decline. Melbourne contributed 6,525 properties with a severe 21.4 per cent monthly drop and 16.9 per cent annual reduction.

Brisbane’s 3,408 listings reflected a 9.9 per cent monthly decline despite a significant 22.2 per cent annual decrease, while Perth’s 2,649 listings showed a 21.0 per cent monthly reduction and 7.9 per cent annual decline. The persistent shortage of available properties in high-growth markets is directly contributing to their continued strong price performance, as buyer demand significantly outstrips available stock.

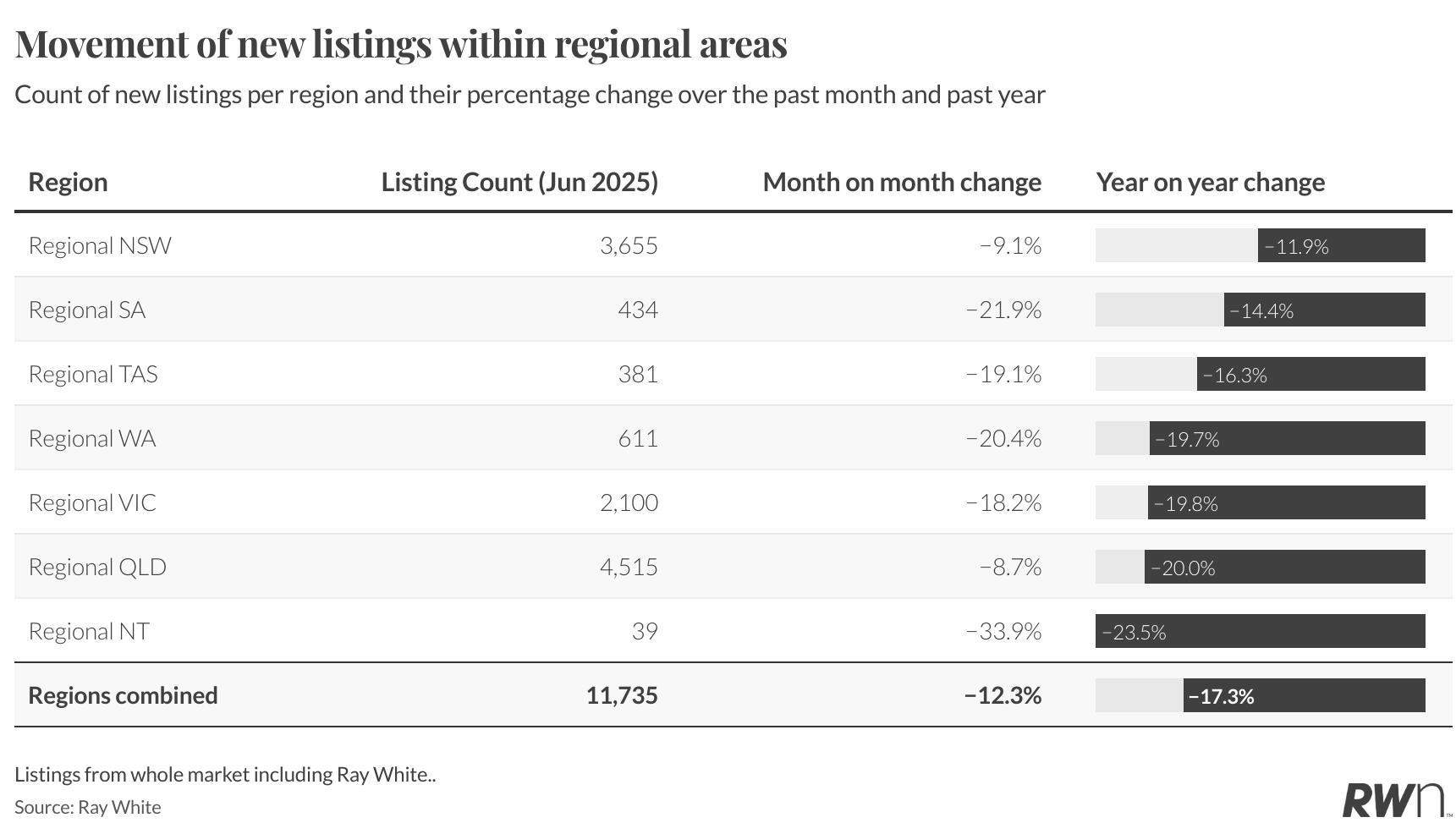

Regional markets posted 11,735 new listings in June, showing a substantial 12.3 per cent monthly decline and concerning 17.3 per cent annual reduction. Regional Queensland led absolute volumes with 4,515 listings but recorded an 8.7 per cent monthly decline and significant 20.0 per cent annual decrease, reflecting tight supply conditions in popular coastal markets.

Regional New South Wales followed with 3,655 listings, experiencing a 9.1 per cent monthly decline and 11.9 per cent annual reduction. Regional Victoria contributed 2,100 listings with an 18.2 per cent monthly drop and 19.8 per cent annual decrease. Regional Western Australia posted 611 listings, down 20.4 per cent monthly and 19.7 per cent annually, highlighting extremely tight supply conditions in resource-rich markets.

The Northern Territory showed the most dramatic monthly decline at 33.9 per cent, though from a modest base of 39 listings, with annual figures down 23.5 per cent. This widespread reduction in regional listing volumes across all markets underscores the severe supply constraints supporting current price acceleration trajectories nationwide.

AUCTION INSIGHTS

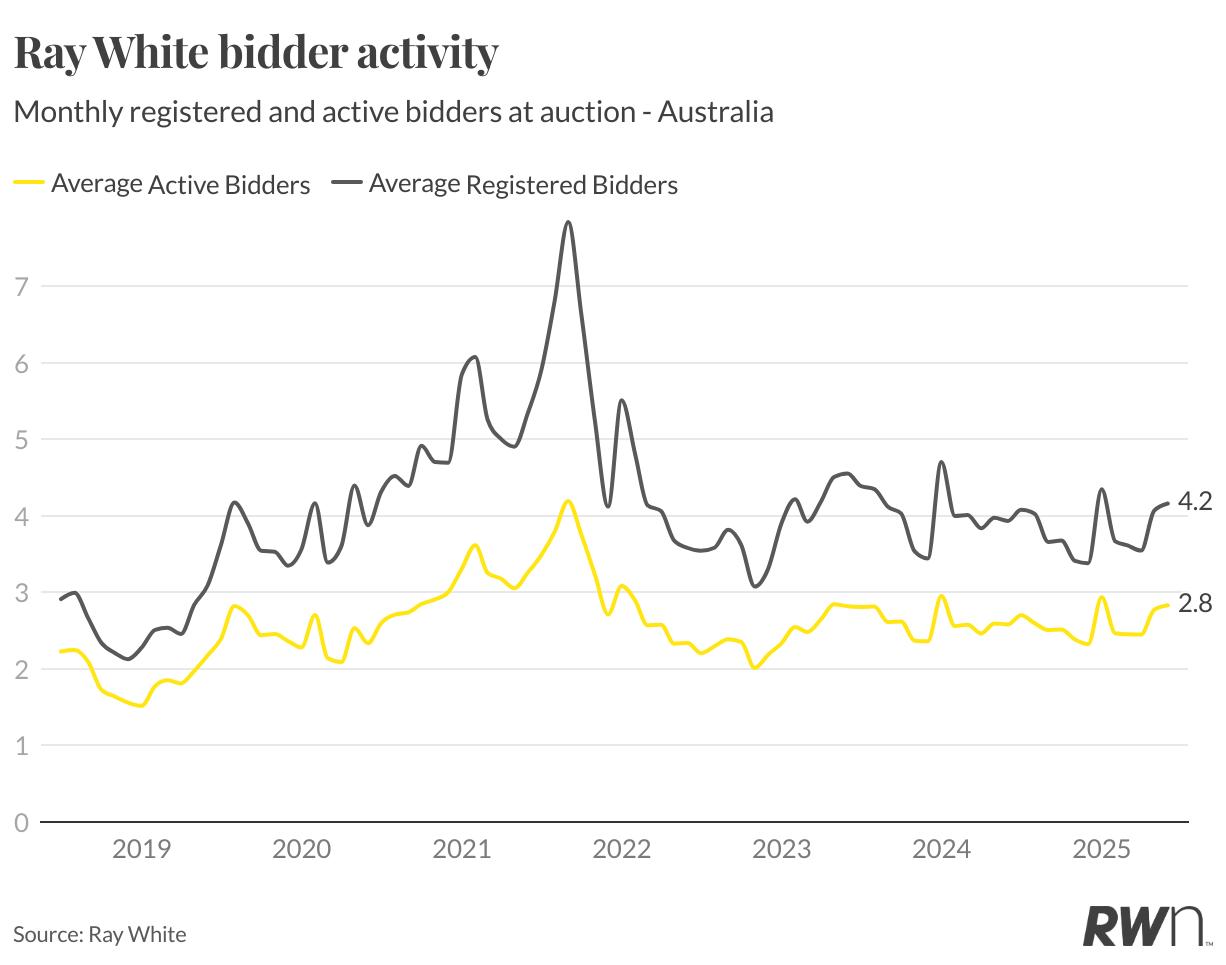

Bidder participation at Ray White auctions maintained steady levels in June, with registered bidders averaging 4.2 per property and active bidders at 2.8 per auction. These figures represent consistent engagement patterns established through 2025, with approximately 67 per cent of registered participants actively competing in the bidding process.

The stability in bidder numbers, despite increasingly challenging affordability conditions, demonstrates serious buyer intent and sustained competitive pressure at individual sales. While participation levels remain below the pandemicera peaks of 2021, current figures reflect a market where genuine buyers are competing decisively for available stock, supporting ongoing price growth momentum.

The ratio of active to registered bidders indicates strong buyer commitment, with most participants who attend auctions genuinely engaged in the purchasing process. This sustained level of competition, combined with severely constrained listing volumes, continues to create the market dynamics necessary for robust clearance rates and ongoing price appreciation across most markets.

Ray White auction clearance rates demonstrated exceptional strength in June, reaching approximately 72.0 per cent, marking a significant improvement from recent months and substantially outperforming both 2023 and 2024 levels for the corresponding period. This performance represents one of the strongest clearance rates recorded this year, reflecting the powerful combination of limited property supply and strengthened buyer confidence.

The improvement in clearance rates coincides directly with the interest rate cutting cycle, which appears to be supporting purchaser confidence and competitive tension at auctions. The June result positions 2025 performance well above historical averages, indicating a market responding positively to improved financing conditions and expectations of further monetary policy easing.

This strengthening trend suggests the auction market has found renewed momentum following the initial rate cuts, with buyers demonstrating increased commitment to securing properties amid ongoing supply constraints. The trajectory indicates auction performance may continue strengthening through the remainder of 2025, particularly as further interest rate reductions materialise and buyer capacity improves across most market segments.

Ray White Group’s sales performance in June reached $7.4 billion, representing a seasonal decline from peak autumn levels but maintaining elevated baselines established through 2025’s strong opening months. The figure reflects both continued price appreciation and steady transaction volumes across most markets, particularly in the high-growth cities of Perth, Adelaide, and Brisbane.

The June result aligns with typical seasonal patterns as the market transitions into the traditionally quieter winter months, yet remains substantially above corresponding periods in previous years. Despite some seasonal moderation in transaction volumes, the sustained price growth across all major markets has supported overall sales values, demonstrating the underlying strength of current market conditions.

With interest rates now firmly in their cutting cycle and further reductions anticipated before year-end, this momentum appears well-positioned to continue through the traditionally quieter winter period ahead. The substantial improvement since January highlights growing market confidence following the first interest rate reductions in over three years, with expectations of additional monetary policy easing providing continued support for sales activity.

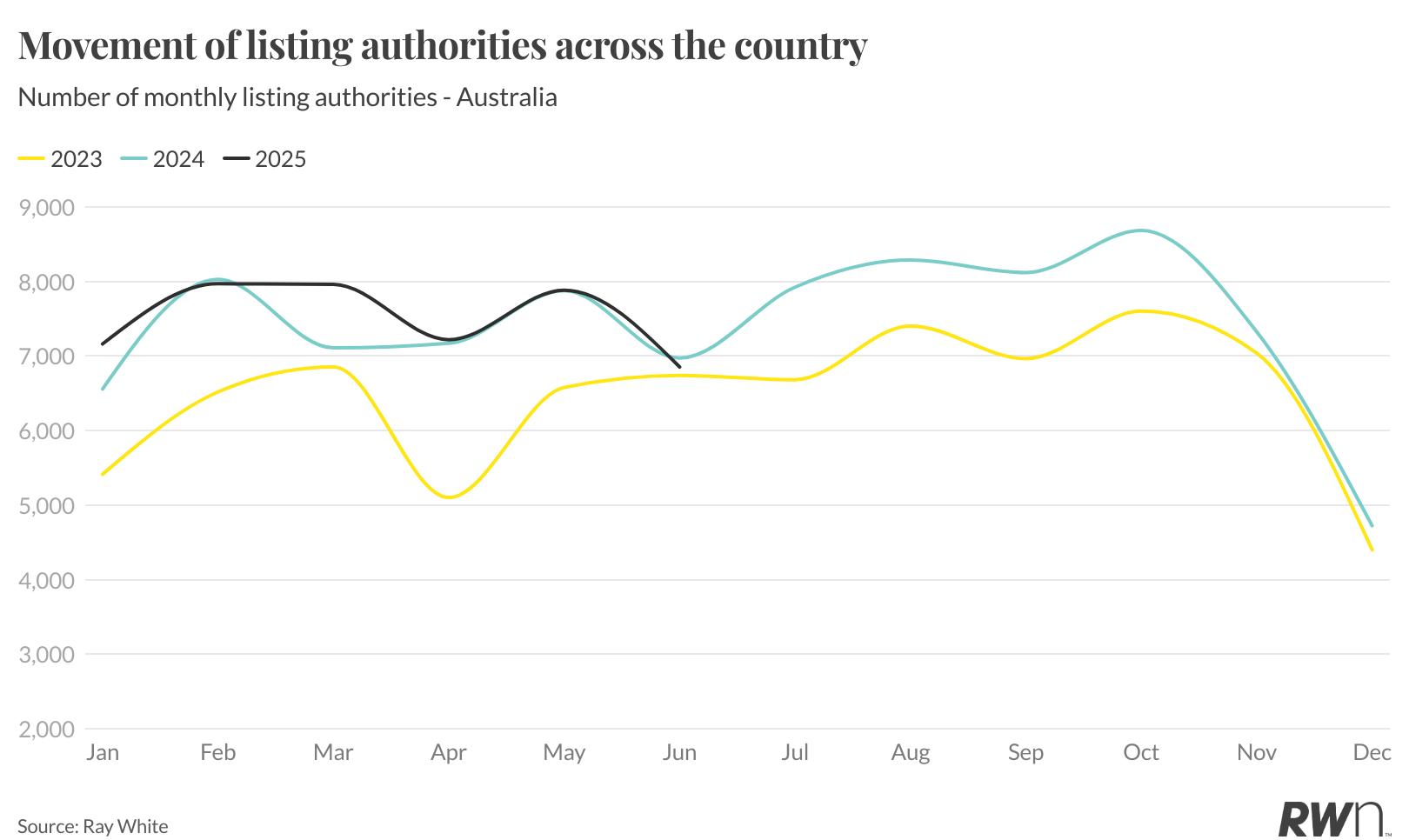

Ray White listing authorities provide crucial forward-looking insight into market supply trends, representing properties signed for sale but not yet marketed. June data shows 6,853 authorities compared to 6,972 in June 2024 and 6,741 in June 2023, indicating modest supply levels ahead but tracking marginally below 2024’s stronger performance.

The annual comparison reveals 2025 has generally maintained similar levels to previous years, though consistently running slightly behind 2024’s robust figures throughout most months. The first half of 2025 shows authority levels ranging from 6,853 to 7,969, compared to 2024’s stronger range of 6,972 to 8,289, suggesting more cautious vendor sentiment this year.

While listing authorities remain relatively stable compared to the dramatic decline in actual listings, the modest shortfall versus 2024 indicates vendors may be exercising greater caution before committing to market their properties. This suggests any increase in spring listing activity may be more measured than in previous years, maintaining support for ongoing price growth momentum as the fundamental supply-demand imbalance persists across most markets.