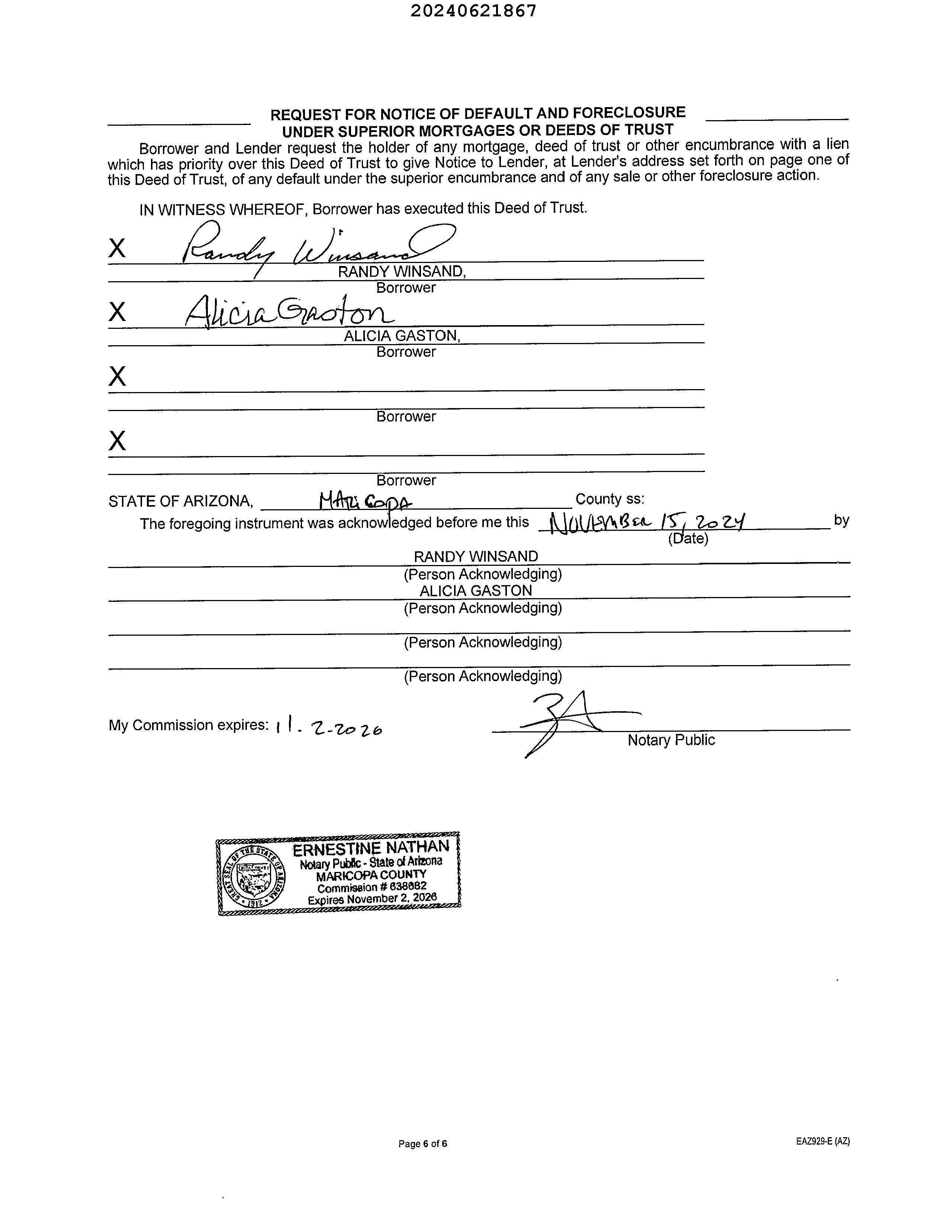

Email-based, real estate fraud schemes are on the rise. One common scenario is altering wiring instructions with the intention of rerouting funds.

Keeping this in mind, First American Title is changing the way we receive payment information. It is imperative that we are familiar with the people in our transactions.

RELYING ON EMAIL ALONE IS NO LONGER AN OPTION.

Fraudsters often use email to send falsified wire instructions to unsuspecting victims. Please warn your buyers and sellers to only follow wire instructions they receive personally from First American Title.

Additionally, we will not accept disbursement instructions for seller or buyer funds via email OR from any third party (attorney, real estate agent, etc).

ALTERNATIVE INSTRUCTIONS?

If your buyer or seller receives alternative wiring instructions that appear to be from First American Title, make sure they contact their escrow officer at a trusted phone number for confirmation.

Know that our wiring instructions do not change so any communication is suspect. Our banking institution is First American Trust.

IN SHORT – wire instructions will not be accepted by email. New wire instructions must be hand-carried or uploaded to the First American Secure Portal.

Thank you for joining First American Title in fostering a secure real estate transaction process. Have questions or concerns? Please contact our office or your escrow officer.

LIMITATION OF LIABILITY FOR INFORMATIONAL REPORTS

IMPORTANT -- PLEASE READ CAREFULLY:

This report is not an insured product or service or a representation of the condition of title to real property. It is not an abstract, legal opinion, opinion of title, title insurance commitment or preliminary report, or any form of Title Insurance or Guaranty. This report is issued exclusively for the benefit of the Applicant therefor and may not be used or relied upon by any other person. This report may not be reproduced in any manner without First Americans prior written consent. First American does not represent or warrant that the information herein is complete or free from error, and the information herein is provided without any warranties of any kind, as-is, and with all faults. As a material part of the consideration given in exchange for the issuance of this report, recipient agrees that First Americans sole liability for any loss or damage caused by an error or omission due to inaccurate information or negligence in preparing this report shall be limited to the fee charged for the report. Recipient accepts this report with this limitation and agrees that First American would not have issued this report but for the limitation of liability described above. First American makes no representation or warranty as to the legality or propriety of recipient's use of the information herein.

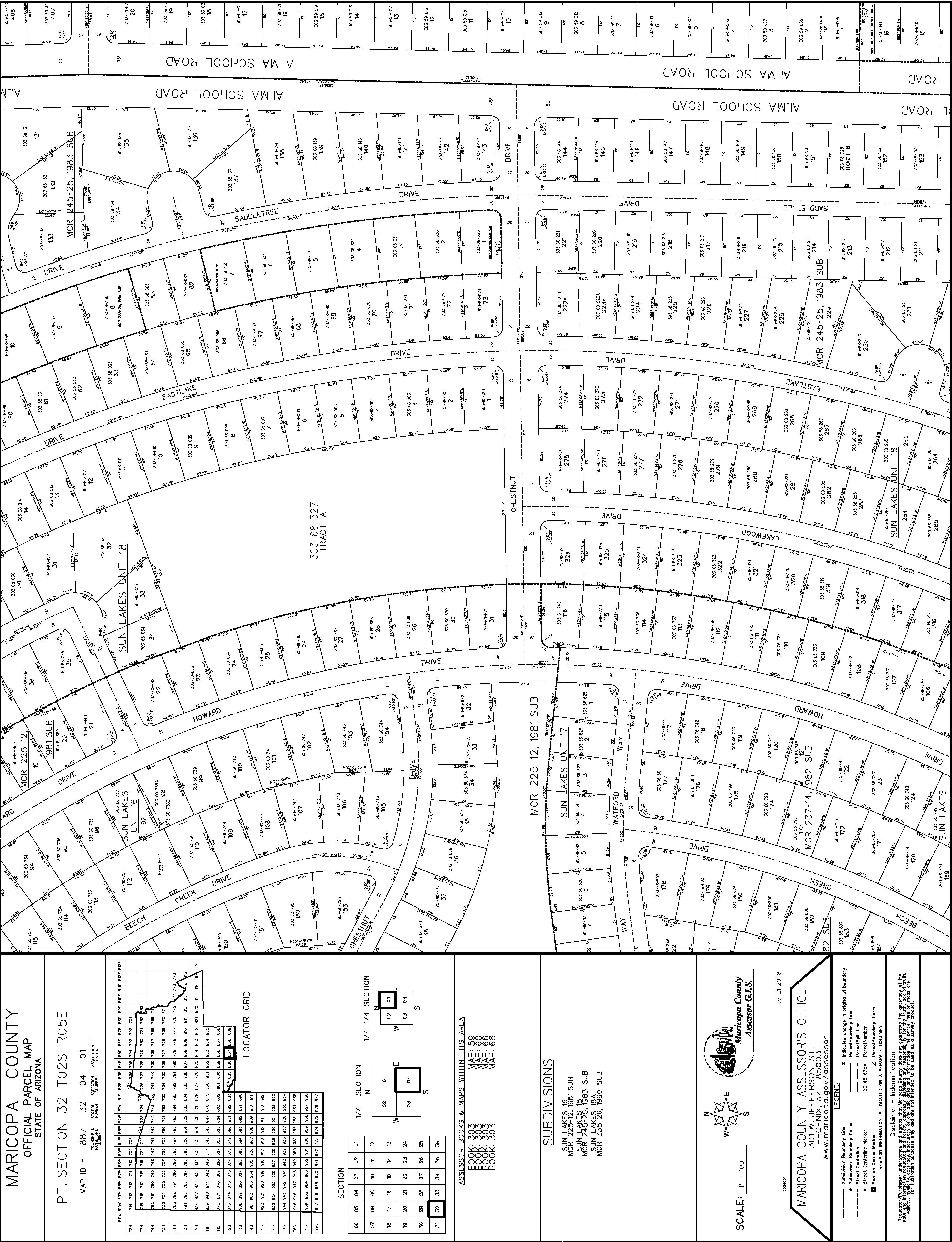

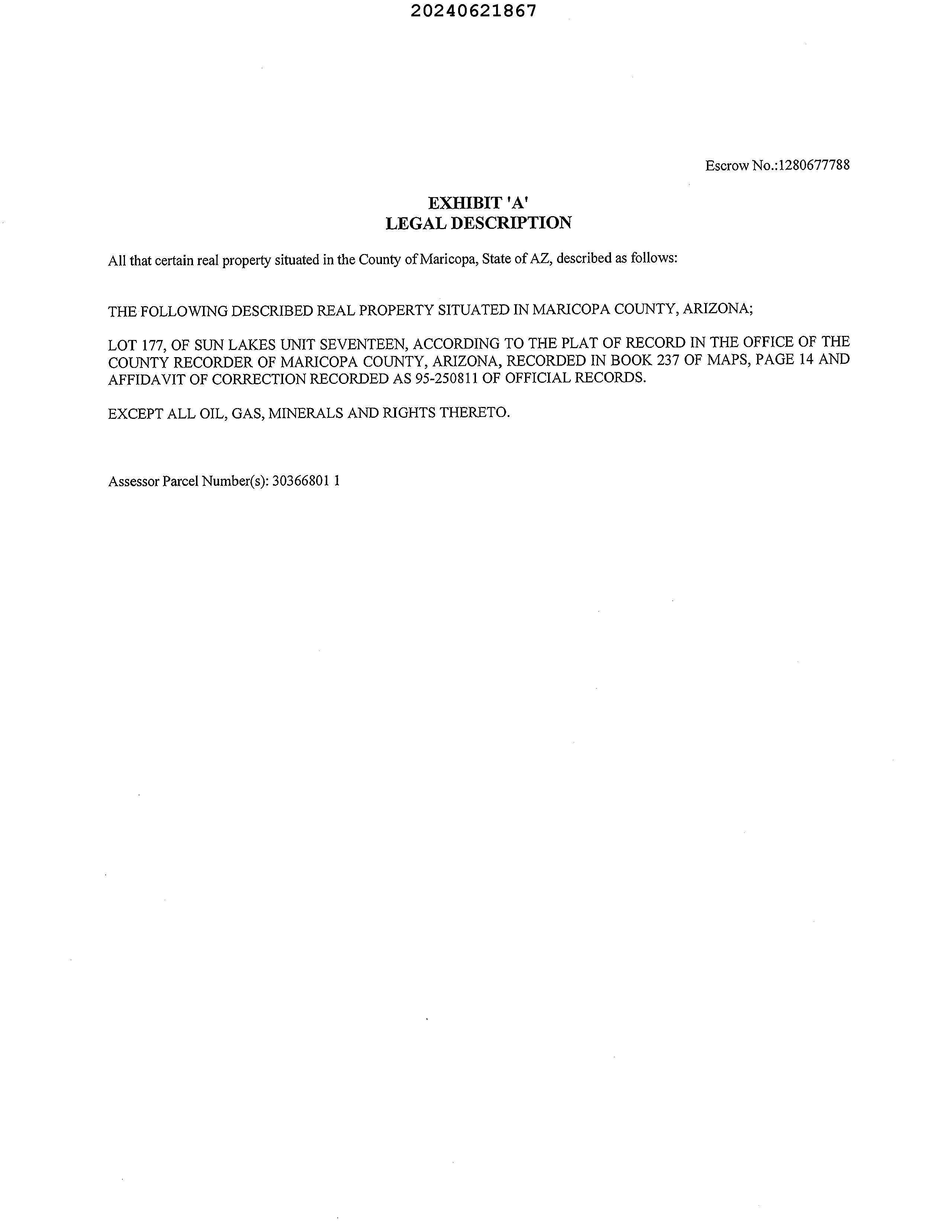

Subject Property

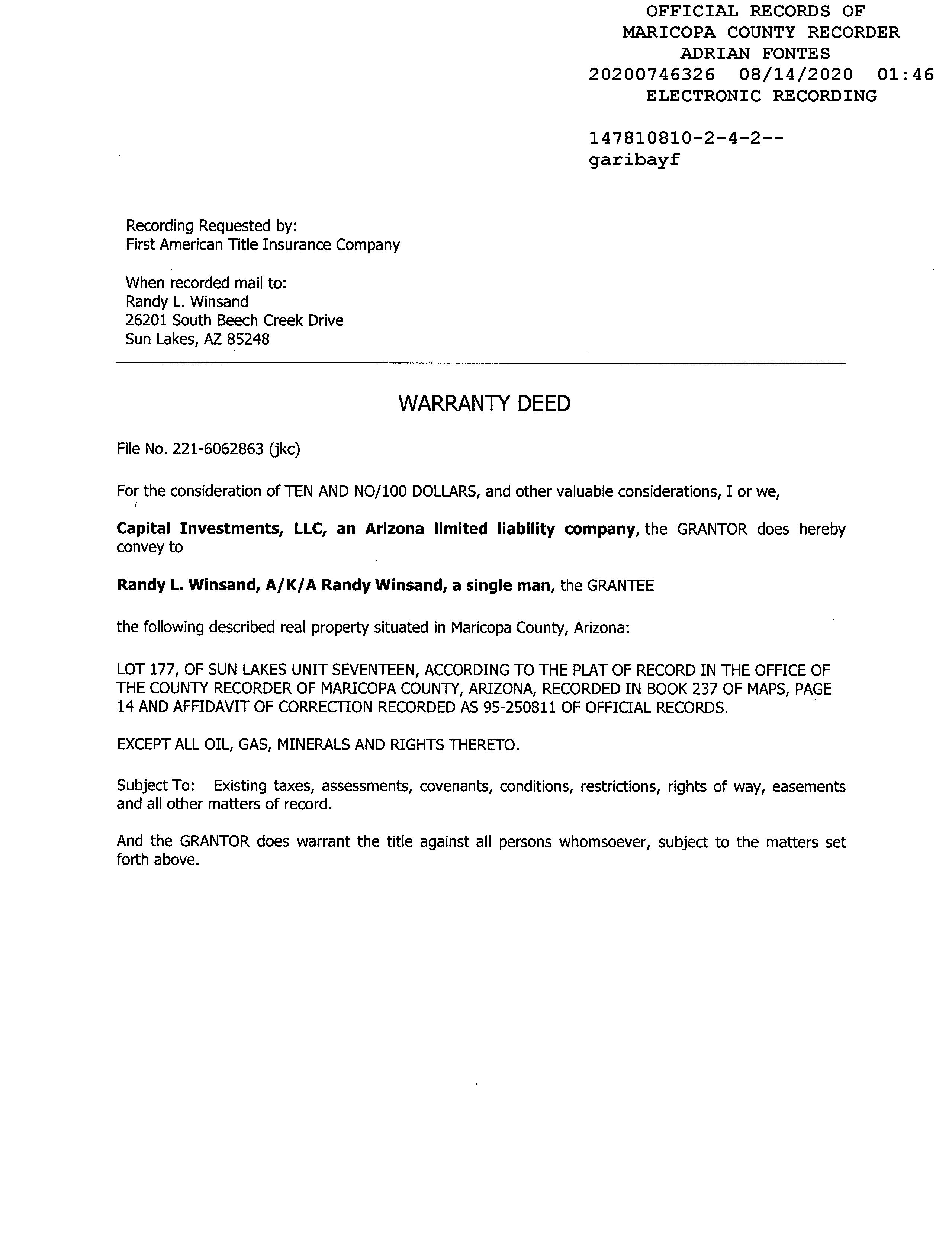

26201 S Beech Creek Dr Sun Lakes AZ 85248 APN: 303-66-801

Disclaimer

This REiSource report is provided "as is" without warranty of any kind, either express or implied, including without limitations any warrantees of merchantability or fitness for a particular purpose. There is no representation of warranty that this information is complete or free from error, and the provider does not assume, and expressly disclaims, any liability to any person or entity for loss or damage caused by errors or omissions in this REiSource report without a title insurance policy.

The information contained in the REiSource report is delivered from your Title Company, who reminds you that you have the right as a consumer to compare fees and serviced levels for Title, Escrow, and all other services associated with property ownership, and to select providers accordingly. Your home is the largest investment you will make in your lifetime and you should demand the very best.

Subject Property : 26201 S Beech Creek Dr Sun Lakes AZ 85248

Owner Information

Owner Name : Winsand Randy L

Mailing Address : 1846 E Delta Ave, Mesa AZ 85204-3645 C043

Owner Occupied Indicator : A

Location Information

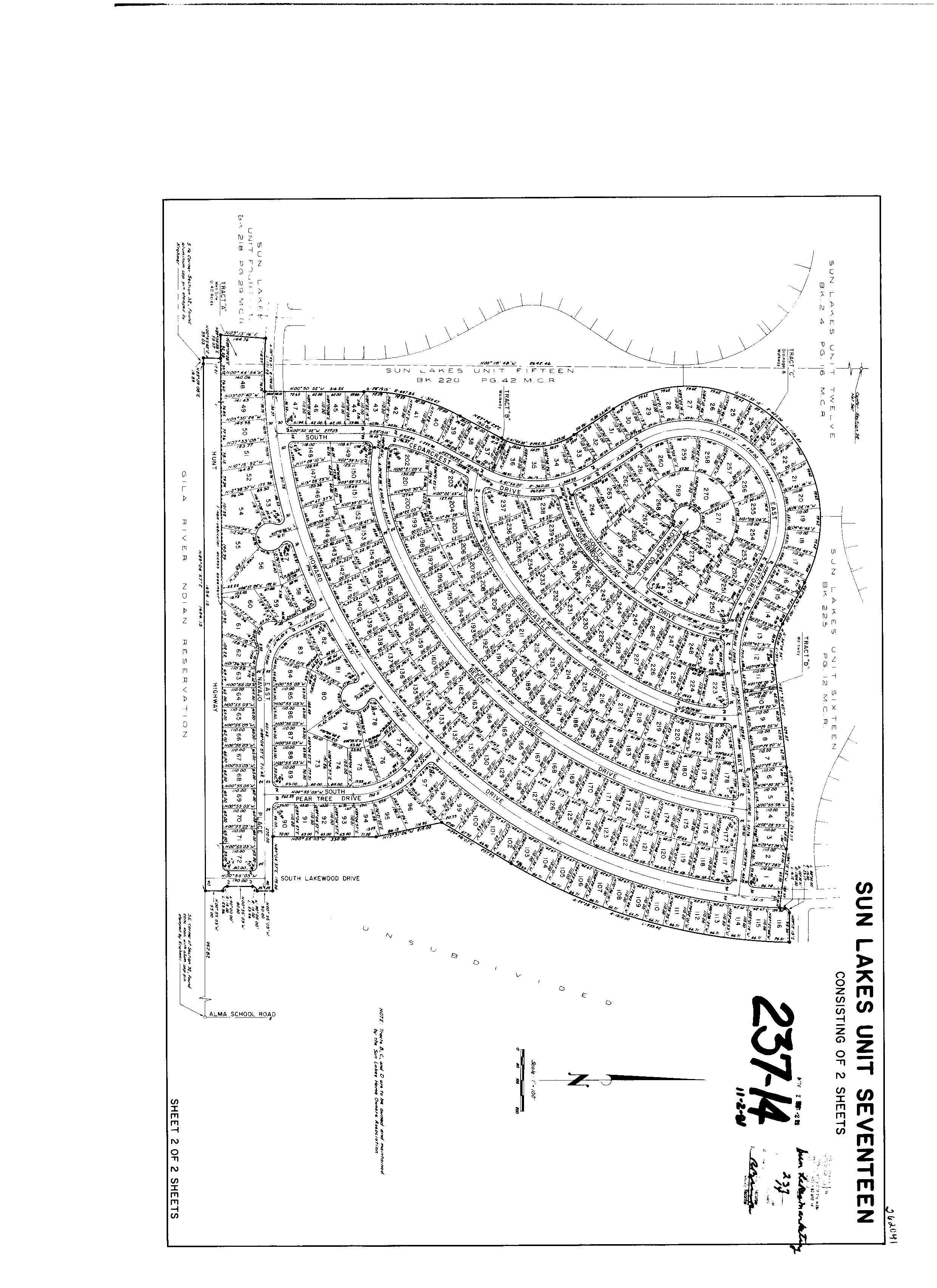

Legal Description : Lot 177 Sun Lakes Unit 17 Mcr 237-14

County : Maricopa, Az

Census Tract / Block : 8175.00 / 2

Township-Range- Sect : 02S-05E-32

Legal Lot : 177

Legal Block : 237

Last Market Sale Information

APN : 303-66-801

Subdivision : Sun Lakes 17

Map Reference : 23714

School District : Chandler 80

Neighbor Code : 02-011

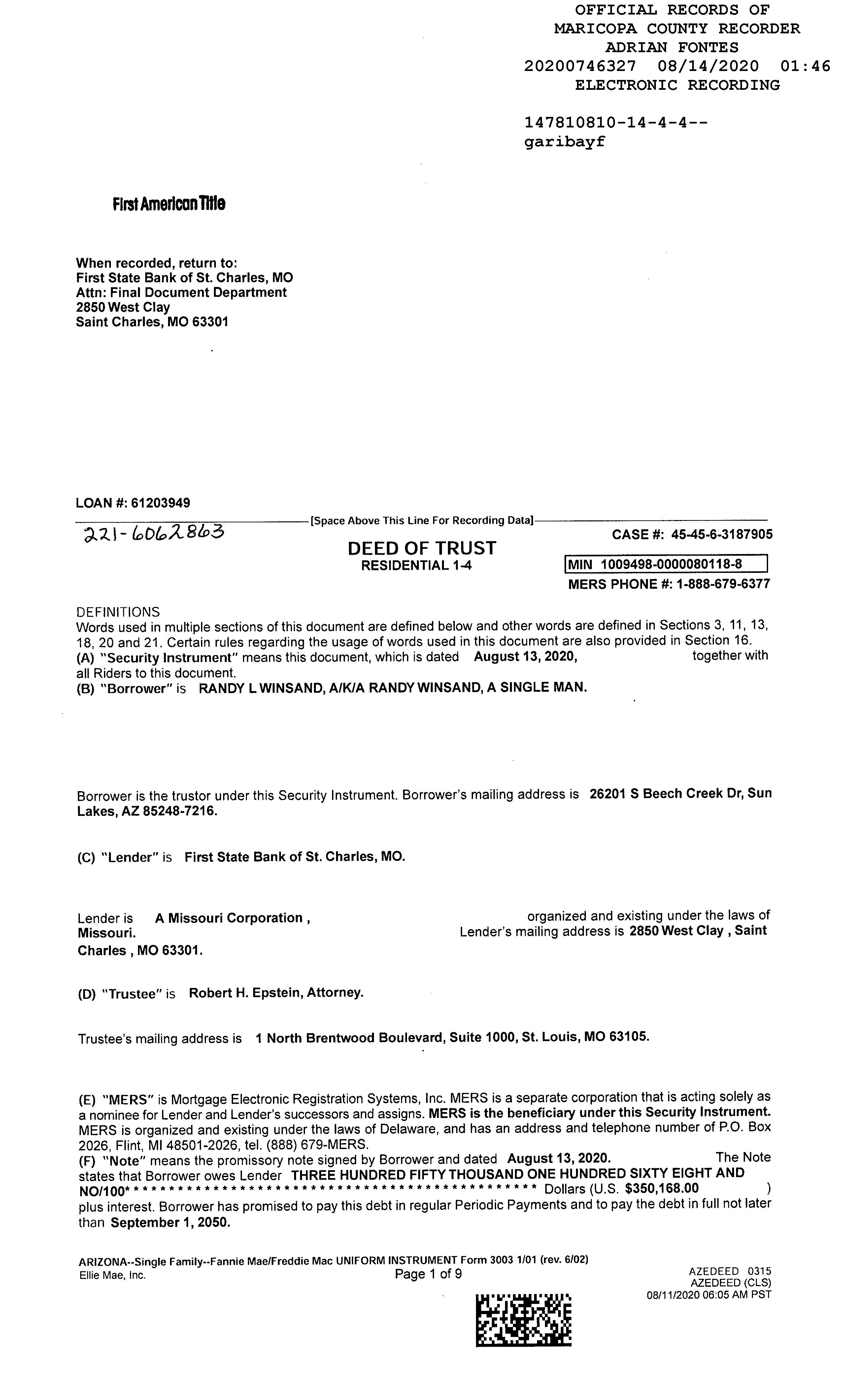

Recording/Sale Date : 08/14/2020 / 07/06/2020 1st Mtg Amount/Type : $350,168 / Va

Sale Price : $338,000

1st Mtg Document # : 746327

Document # : 746326 1st Mtg Term : 30

Deed Type : Warranty Deed

Title Company : First American Title

Lender : First St Bk/st Charles Mo

Seller Name : Capital Investments Llc

Prior Sale Information

Prior Rec/Sale Date : 04/28/2020 / 03/19/2020

Prior Sale Price : $240,000

Prior Doc Number : 363146

Price Per SqFt : $149.76

Prior Deed Type : Warranty Deed

Prior Lender : Private Individual

Prior 1st Mtg Amt/Type : $226,800 / Private Party Customer Name : Jeremiah Stiffler Customer Company Name : First American Prepared On : 04/29/2025

Property Characteristics

Gross Area : 2,257 Garage Capacity : 2

Living Area : 2,257

Total Rooms : 7

Year Built / Eff : 1986

# of Stories : 1

Parking Type : Garage

Property Information

Patio Type : Covered Patio

Roof Material : Concrete Tile Air Cond : Refrigeration

Heat Type : Forced Air Quality : Average

Cooling Type : Forced Air Condition : Average

Exterior wall : Frame Wood Bath Fixtures : 7

Land Use : Sfr Lot Size : 8,028 Water Influence : Corner

Zoning : R1-6 Site Influence : Corner

Lot Acres : 0.18

Tax Information Total Value : $398,500

Use : Single Fam Resurban Subd ( 3 )

Census Tract / block: 8175.00 / 2 Year: 2020

Arizona Schools

PIMA COUNTY

SEARCH PARAMETERS

PARCEL: 303-66-801

PARCEL: 303-66-801 1

OWNER: WINSAND RANDY L & RANDY 2020 746326 08/14/2020

SITUS: 26201 S BEECH CREEK DR SUN LAKES

MAIL: 1846 E DELTA AVE MESA AZ 85204

PLAT: 237 - 14 LOT 177

LEGAL: SUN LAKES UNIT 17 MCR 237-14

CURRENT TAXES INFORMATION THROUGH 04/18/2025

COVERED 1

GARAGE 2

SALES

NO SALES

ADDITIONAL PROPERTY INFORMATION

STANDARD LAND USE: SFR

END SEARCH

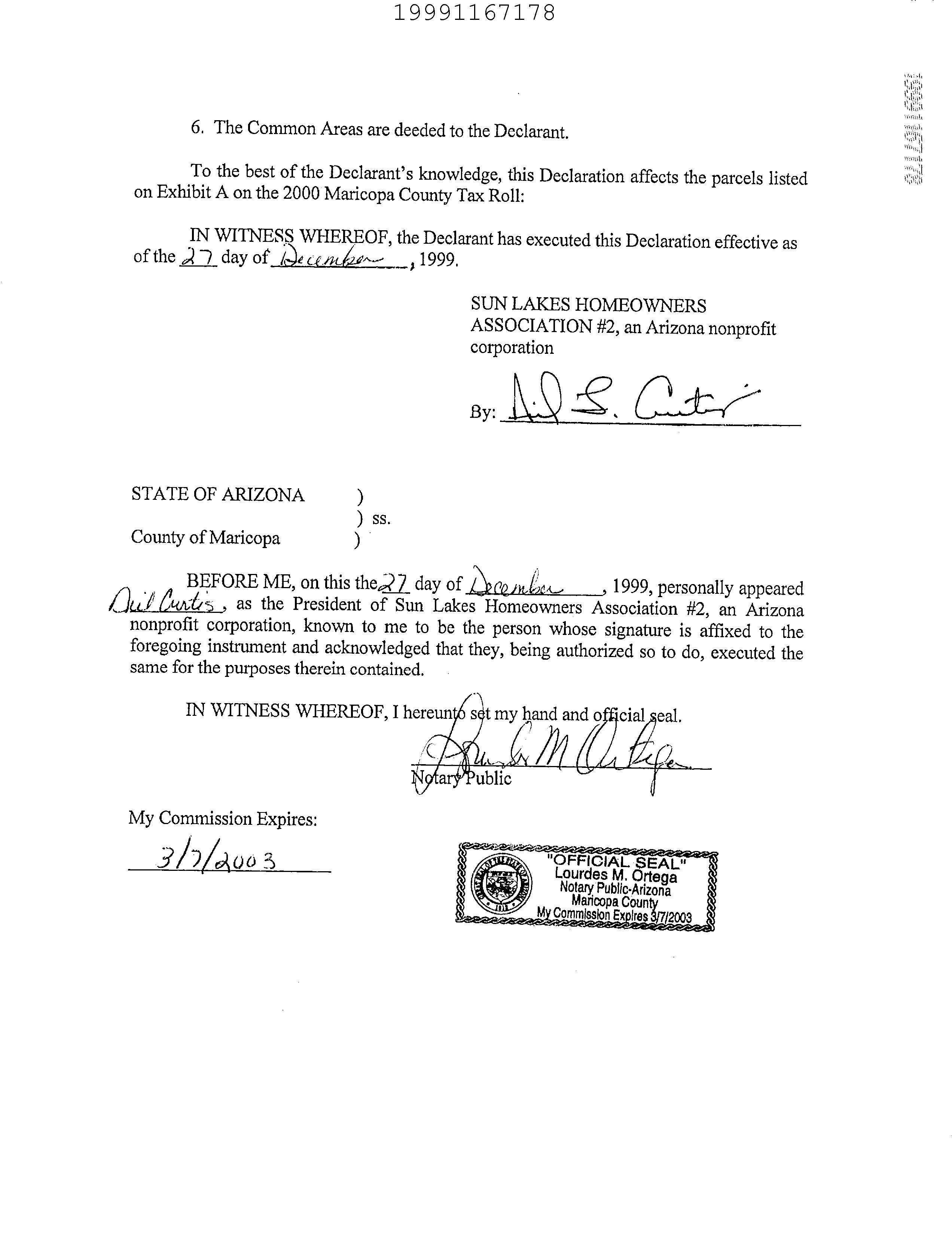

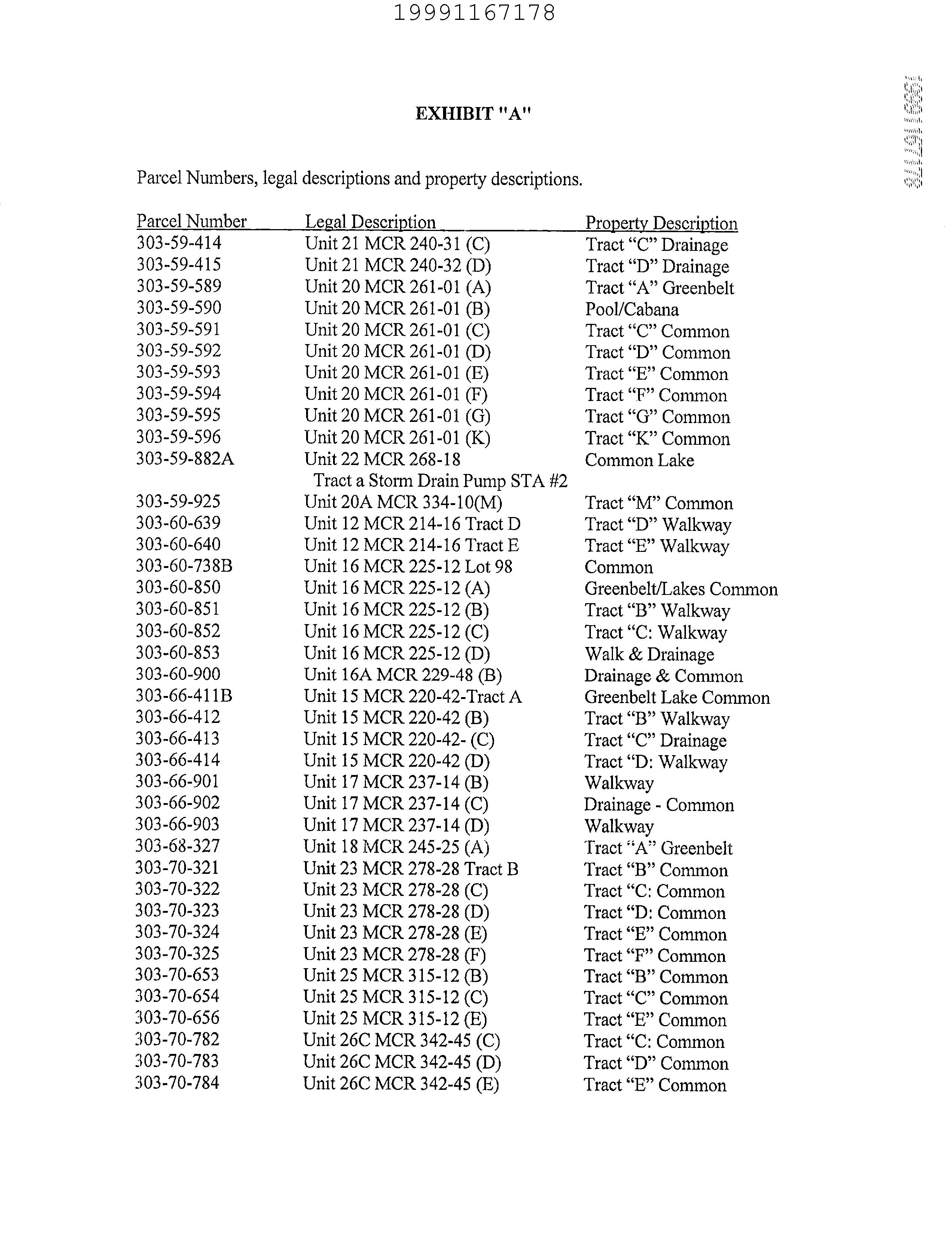

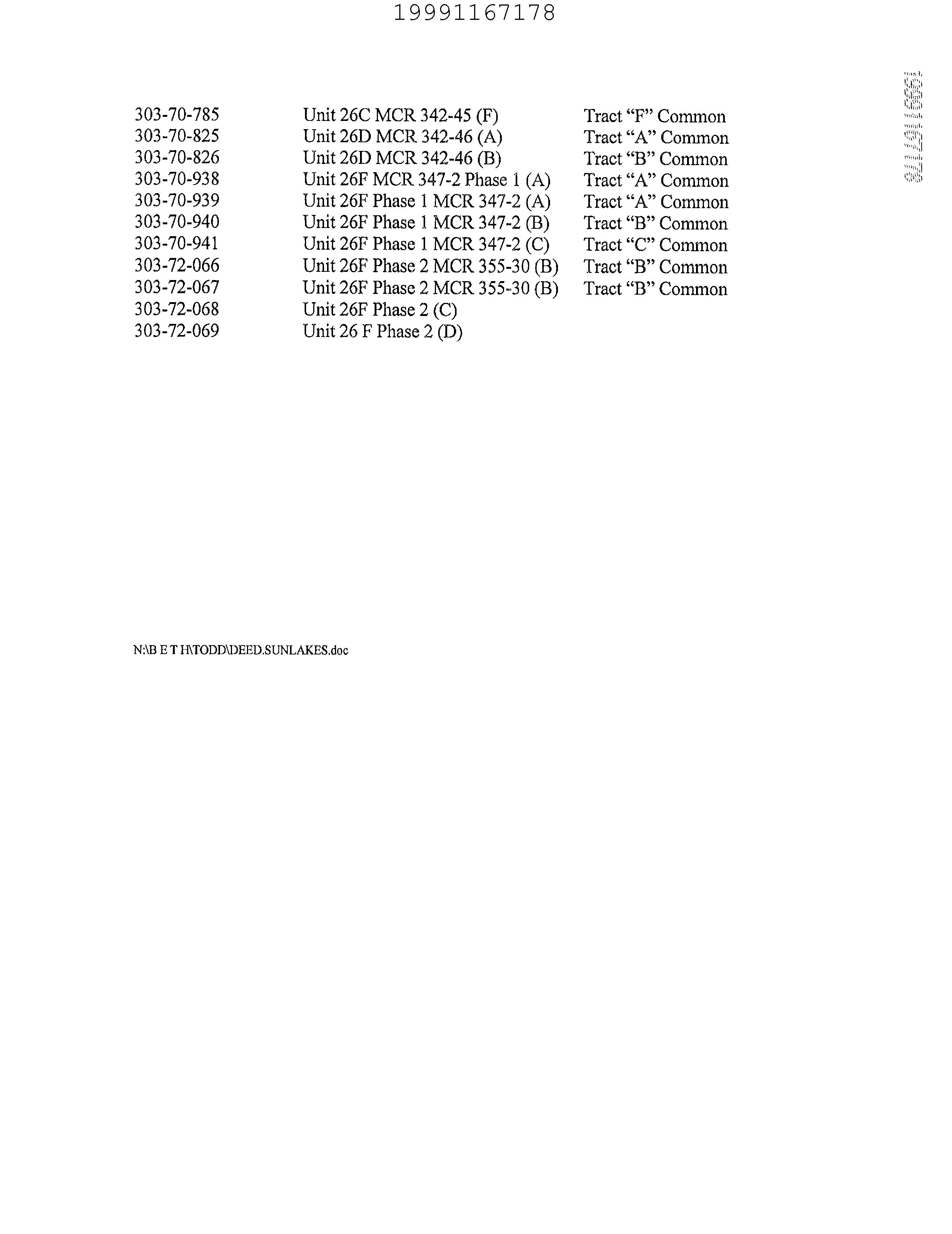

Covenants, Conditions & Restrictions

Thank you for the opportunity to be of service.

Restrictions indicating a preference, limitation or discrimination based on race, color, religion, sex, handicap, familial status, or national origin are hereby deleted to the extent such restrictions violate 42 USC 3604(c).

This information is furnished without fee and without benefit of a complete title search. No liability is assumed by First American Title. If it is desired that liability be assumed, you may apply for a policy of title insurance with First American Title Insurance Company.

Eagle Policy

Homeowner's Policy of Title Insurance

a One-To-Four Family Residence

OWNER’S INFORMATION SHEET

Your Title Insurance Policy is a legal contract between You and Us.

It applies only to a one-to-four family residence and only if each insured named in Schedule A is a Natural Person. If the Land described in Schedule A of the Policy is not an improved residential lot on which there is located a one-to-four family residence, or if each insured named in Schedule A is not a Natural Person, contact Us immediately.

The Policy insures You against actual loss resulting from certain Covered Risks. These Covered Risks are listed beginning on page 2 of the Policy. The Policy is limited by:

• Provisions of Schedule A

• Exceptions in Schedule B

• Our Duty To Defend Against Legal Actions On Page 3

• Exclusions on page 4

• Conditions on pages 4, 5 and 6.

You should keep the Policy even if You transfer Your Title to the Land. It may protect against claims made against You by someone else after You transfer Your Title.

IF YOU WANT TO MAKE A CLAIM, SEE SECTION 3 UNDER CONDITIONS ON PAGE 4.

The premium for this Policy is paid once. No additional premium is owed for the Policy. This sheet is not Your insurance Policy. It is only a brief outline of some of the important Policy features. The Policy explains in detail Your rights and obligations and Our rights and obligations. Since the Policy--and not this sheet--is the legal document,

If

Eagle Policy

Homeowner's Policy of Title Insurance For a One-To-Four Family Residence

ISSUED BY First American Title Insurance Company

As soon as You Know of anything that might be covered by this Policy, You must notify Us promptly in writing at the address shown in Section 3 of the Conditions.

OWNER’S COVERAGE STATEMENT

This Policy insures You against actual loss, including any costs, attorneys’ fees and expenses provided under this Policy. The loss must result from one or more of the Covered Risks set forth below. This Policy covers only Land that is an improved residential lot on which there is located a one-to-four family residence and only when each insured named in Schedule A is a Natural Person.

Your insurance is effective on the Policy Date. This Policy covers Your actual loss from any risk described under Covered Risks if the event creating the risk exists on the Policy Date or, to the extent expressly stated in Covered Risks, after the Policy Date.

Your insurance is limited by all of the following:

• The Policy Amount

• For Covered Risk 16, 18, 19 and 21, Your Deductible Amount and Our Maximum Dollar Limit of Liability shown in Schedule A

• The Exceptions in Schedule B

• Our Duty To Defend Against Legal Actions

• The Exclusions on page 4

• The Conditions on pages 4, 5 and 6

The Covered Risks are:

1. Someone else owns an interest in Your Title.

COVERED RISKS

2. Someone else has rights affecting Your Title because of leases, contracts, or options.

3. Someone else claims to have rights affecting Your Title because of forgery or impersonation.

4. Someone else has an Easement on the Land.

5. Someone else has a right to limit Your use of the Land.

6. Your Title is defective. Some of these defects are:

a. Someone else’s failure to have authorized a transfer or conveyance of your Title.

b. Someone else’s failure to create a valid document by electronic means.

c. A document upon which Your Title is based is invalid because it was not properly signed, sealed, acknowledged, delivered or recorded.

d. A document upon which Your Title is based was signed using a falsified, expired, or otherwise invalid power of attorney.

e. A document upon which Your Title is based was not properly filed, recorded, or indexed in the Public Records.

f. A defective judicial or administrative proceeding.

7. Any of Covered Risks 1 through 6 occurring after the Policy Date.

8. Someone else has a lien on Your Title, including a:

a. lien of real estate taxes or assessments imposed on Your Title by a governmental authority that are due or payable, but unpaid;

b. Mortgage;

c. judgment, state or federal tax lien;

d. charge by a homeowner’s or condominium association; or

e. lien, occurring before or after the Policy Date, for labor and material furnished before the Policy Date.

9. Someone else has an encumbrance on Your Title.

10. Someone else claims to have rights affecting Your Title because of fraud, duress, incompetency or incapacity.

11. You do not have actual vehicular and pedestrian access to and from the Land, based upon a legal right.

12. You are forced to correct or remove an existing violation of any covenant, condition or restriction affecting the Land, even if the covenant, condition or restriction is excepted in Schedule B. However, You are not covered for any violation that relates to:

a. any obligation to perform maintenance or repair on the Land; or

b. environmental protection of any kind, including hazardous or toxic conditions or substances unless there is a notice recorded in the Public Records, describing any part of the Land, claiming a violation exists. Our liability for this Covered Risk is limited to the extent of the violation stated in that notice.

13. Your Title is lost or taken because of a violation of any covenant, condition or restriction, which occurred before You acquired Your Title, even if the covenant, condition or restriction is excepted in Schedule B.

14. The violation or enforcement of those portions of any law or government regulation concerning:

a. building;

b. zoning;

c. land use;

d. improvements on the Land;

e. land division; or

f. environmental protection,

if there is a notice recorded in the Public Records, describing any part of the Land, claiming a violation exists or declaring the intention to enforce the law or regulation. Our liability for this Covered Risk is limited to the extent of the violation or enforcement stated in that notice.

15. An enforcement action based on the exercise of a governmental police power not covered by Covered Risk 14 if there is a notice recorded in the Public Records, describing any part of the Land, of the enforcement action or intention to bring an enforcement action. Our liability for this Covered Risk is limited to the extent of the enforcement action stated in that notice.

16. Because of an existing violation of a subdivision law or regulation affecting the Land:

a. You are unable to obtain a building permit;

b. You are required to correct or remove the violation; or

c. someone else has a legal right to, and does, refuse to perform a contract to purchase the Land, lease it or make a Mortgage loan on it.

The amount of Your insurance for this Covered Risk is subject to Your Deductible Amount and Our Maximum Dollar Limit of Liability shown in Schedule A.

17. You lose Your Title to any part of the Land because of the right to take the Land by condemning it, if:

a. there is a notice of the exercise of the right recorded in the Public Records and the notice describes any part of the Land; or b. the taking happened before the Policy Date and is binding on You if You bought the Land without Knowing of the taking.

18. You are forced to remove or remedy Your existing structures, or any part of them - other than boundary walls or fences - because any portion was built without obtaining a building permit from the proper government office. The amount of Your insurance for this Covered Risk is subject to Your Deductible Amount and Our Maximum Dollar Limit of Liability shown in Schedule A.

19. You are forced to remove or remedy Your existing structures, or any part of them, because they violate an existing zoning law or zoning regulation. If You are required to remedy any portion of Your existing structures, the amount of Your insurance for this Covered Risk is subject to Your Deductible Amount and Our Maximum Dollar Limit of Liability shown in Schedule A.

20. You cannot use the Land because use as a single-family residence violates an existing zoning law or zoning regulation.

21. You are forced to remove Your existing structures because they encroach onto Your neighbor’s land. If the encroaching structures are boundary walls or fences, the amount of Your insurance for this Covered Risk is subject to Your Deductible Amount and Our Maximum Dollar Limit of Liability shown in Schedule A.

22. Someone else has a legal right to, and does, refuse to perform a contract to purchase the Land, lease it or make a Mortgage loan on it because Your neighbor’s existing structures encroach onto the Land.

23. You are forced to remove Your existing structures which encroach onto an Easement or over a building set-back line, even if the Easement or building set-back line is excepted in Schedule B.

24. Your existing structures are damaged because of the exercise of a right to maintain or use any Easement affecting the Land, even if the Easement is excepted in Schedule B.

25. Your existing improvements (or a replacement or modification made to them after the Policy Date), including lawns, shrubbery or trees, are damaged because of the future exercise of a right to use the surface of the Land for the extraction or development of minerals, water or any other substance, even if those rights are excepted or reserved from the description of the Land or excepted in Schedule B.

26. Someone else tries to enforce a discriminatory covenant, condition or restriction that they claim affects Your Title which is based upon race, color, religion, sex, handicap, familial status, or national origin.

27. A taxing authority assesses supplemental real estate taxes not previously assessed against the Land for any period before the Policy Date because of construction or a change of ownership or use that occurred before the Policy Date.

28. Your neighbor builds any structures after the Policy Date -- other than boundary walls or fences -- which encroach onto the Land.

29. Your Title is unmarketable, which allows someone else to refuse to perform a contract to purchase the Land, lease it or make a Mortgage loan on it.

30. Someone else owns an interest in Your Title because a court order invalidates a prior transfer of the title under federal bankruptcy, state insolvency, or similar creditors’ rights laws.

31. The residence with the address shown in Schedule A is not located on the Land at the Policy Date.

32. The map, if any, attached to this Policy does not show the correct location of the Land according to the Public Records.

OUR DUTY TO DEFEND AGAINST LEGAL ACTIONS

We will defend Your Title in any legal action only as to that part of the action which is based on a Covered Risk and which is not excepted or excluded from coverage in this Policy. We will pay the costs, attorneys’ fees, and expenses We incur in that defense. We will not pay for any part of the legal action which is not based on a Covered Risk or which is excepted or excluded from coverage in this Policy.

We can end Our duty to defend Your Title under section 4 of the Conditions. This Policy is not complete without Schedules A and B.

EXCLUSIONS

In addition to the Exceptions in Schedule B, You are not insured against loss, costs, attorneys' fees, and expenses resulting from:

1. Governmental police power, and the existence or violation of those portions of any law or government regulation concerning:

a. building;

b. zoning;

c. land use;

d. improvements on the Land;

e. land division; and

f. environmental protection.

This Exclusion does not limit the coverage described in Covered Risk 8.a., 14, 15, 16, 18, 19, 20, 23 or 27.

2. The failure of Your existing structures, or any part of them, to be constructed in accordance with applicable building codes. This Exclusion does not limit the coverage described in Covered Risk 14 or 15.

3. The right to take the Land by condemning it. This Exclusion does not limit the coverage described in Covered Risk 17.

4. Risks:

a. that are created, allowed, or agreed to by You, whether or not they are recorded in the Public Records;

b. that are Known to You at the Policy Date, but not to Us, unless they are recorded in the Public Records at the Policy Date;

c. that result in no loss to You; or

d. that first occur after the Policy Date - this does not limit the coverage described in Covered Risk 7, 8.e., 25, 26, 27 or 28.

5. Failure to pay value for Your Title.

6. Lack of a right:

a. to any land outside the area specifically described and referred to in paragraph 3 of Schedule A; and b. in streets, alleys, or waterways that touch the Land.

This Exclusion does not limit the coverage described in Covered Risk 11 or 21.

7. The transfer of the Title of You is invalid as a preferential transfer or as a fraudulent transfer or conveyance under federal bankruptcy, state insolvency, or similar creditors’ rights laws.

CONDITIONS

1. DEFINITIONS

a. Easement - the right of someone else to use the Land for a special purpose.

b. Estate Planning Entity – a legal entity or Trust established by a Natural Person for estate planning.

c. Known - things about which You have actual knowledge. The words “Know” and “Knowing” have the same meaning as Known.

d. Land - the land or condominium unit described in paragraph 3 of Schedule A and any improvements on the Land which are real property.

e. Mortgage - a mortgage, deed of trust, trust deed or other security instrument.

f. Natural Person - a human being, not a commercial or legal organization or entity. Natural Person includes a trustee of a Trust even if the trustee is not a human being.

g. Policy Date - the date and time shown in Schedule A. If the insured named in Schedule A first acquires the interest shown in Schedule A by an instrument recorded in the Public Records later than the date and time shown in Schedule A, the Policy Date is the date and time the instrument is recorded.

h. Public Records - records that give constructive notice of matters affecting Your Title, according to the state statutes where the Land is located.

i. Title - the ownership of Your interest in the Land, as shown in Schedule A.

j. Trust - a living trust established by a Natural Person for estate planning.

k. We/Our/Us - First American Title Insurance Company.

l. You/Your - the insured named in Schedule A and also those identified in Section 2.b. of these Conditions.

2. CONTINUATION OF COVERAGE

a. This Policy insures You forever, even after You no longer have Your Title. You cannot assign this Policy to anyone else.

b. This Policy also insures:

(1) anyone who inherits Your Title because of Your death;

(2) Your spouse who receives Your Title because of dissolution of Your marriage;

(3) the trustee or successor trustee of a Trust or any Estate Planning Entity to whom You transfer Your Title after the Policy Date;

(4) the beneficiaries of Your Trust upon Your death; or

(5) anyone who receives Your Title by a transfer effective on Your death as authorized by law.

c. We may assert against the insureds identified in Section 2.b. any rights and defenses that We have against any previous insured under this Policy.

3. HOW TO MAKE A CLAIM

a. Prompt Notice Of Your Claim

(1) As soon as You Know of anything that might be covered by this Policy, You must notify Us promptly in writing.

(2) Send Your notice to First American Title Insurance Company, Attn: Claims National Intake Center, 1 First American Way, Santa Ana, California 92707. Phone: 888-632-1642. Please include the Policy number shown in Schedule A, and the county and state where the Land is located. Please enclose a copy of Your policy, if available.

(3) If You do not give Us prompt notice, Your coverage will be reduced or ended, but only to the extent Your failure affects Our ability to resolve the claim or defend You.

b. Proof Of Your Loss

(1) We may require You to give Us a written statement signed by You describing Your loss which includes:

(a) the basis of Your claim;

(b) the Covered Risks which resulted in Your loss;

(c) the dollar amount of Your loss; and

(d) the method You used to compute the amount of Your loss.

(2) We may require You to make available to Us records, checks, letters, contracts, insurance policies and other papers which relate to Your claim. We may make copies of these papers.

(3) We may require You to answer questions about Your claim under oath.

(4) If you fail or refuse to give Us a statement of loss, answer Our questions under oath, or make available to Us the papers We request, Your coverage will be reduced or ended, but only to the extent Your failure or refusal affects Our ability to resolve the claim or defend You.

4. OUR CHOICES WHEN WE LEARN OF A CLAIM

a. After We receive Your notice, or otherwise learn, of a claim that is covered by this Policy, Our choices include one or more of the following:

(1) Pay the claim;

(2) Negotiate a settlement;

(3) Bring or defend a legal action related to the claim;

(4) Pay You the amount required by this Policy;

(5) End the coverage of this Policy for the claim by paying You Your actual loss resulting from the Covered Risk, and those costs, attorneys’ fees and expenses incurred up to that time which We are obligated to pay;

(6) End the coverage described in Covered Risk 16, 18, 19 or 21 by paying You the amount of Your insurance then in force for the particular Covered Risk, and those costs, attorneys’ fees and expenses incurred up to that time which We are obligated to pay;

(7) End all coverage of this Policy by paying You the Policy Amount then in force, and those costs, attorneys' fees and expenses incurred up to that time which We are obligated to pay;

(8) Take other appropriate action.

b. When We choose the options in Sections 4.a. (5), (6) or (7), all Our obligations for the claim end, including Our obligation to defend, or continue to defend, any legal action.

c. Even if We do not think that the Policy covers the claim, We may choose one or more of the options above. By doing so, We do not give up any rights.

5. HANDLING A CLAIM OR LEGAL ACTION

a. You must cooperate with Us in handling any claim or legal action and give Us all relevant information.

b. If You fail or refuse to cooperate with Us, Your coverage will be reduced or ended, but only to the extent Your failure or refusal affects Our ability to resolve the claim or defend You.

c. We are required to repay You only for those settlement costs, attorneys' fees and expenses that We approve in advance.

d. We have the right to choose the attorney when We bring or defend a legal action on Your behalf. We can appeal any decision to the highest level. We do not have to pay Your claim until the legal action is finally decided.

e. Whether or not We agree there is coverage, We can bring or defend a legal action, or take other appropriate action under this Policy. By doing so, We do not give up any rights.

6. LIMITATION OF OUR LIABILITY

a. After subtracting Your Deductible Amount if it applies, We will pay no more than the least of:

(1) Your actual loss;

(2) Our Maximum Dollar Limit of Liability then in force for the particular Covered Risk, for claims covered only under Covered Risk 16, 18, 19 or 21; or

(3) the Policy Amount then in force.

and any costs, attorneys’ fees and expenses that We are obligated to pay under this Policy.

b. If We pursue Our rights under Sections 4.a.(3) and 5.e. of these Conditions and are unsuccessful in establishing the Title, as insured:

(1) the Policy Amount then in force will be increased by 10% of the Policy Amount shown in Schedule A, and

(2) You shall have the right to have the actual loss determined on either the date the claim was made by You or the date it is settled and paid.

c. (1) If We remove the cause of the claim with reasonable diligence after receiving notice of it, all Our obligations for the claim end, including any obligation for loss You had while We were removing the cause of the claim.

(2) Regardless of 6.c.(1) above, if You cannot use the Land because of a claim covered by this Policy:

(a) You may rent a reasonably equivalent substitute residence and We will repay You for the actual rent You pay, until the earlier of: (i) the cause of the claim is removed; or (ii) We pay You the amount required by this Policy. If Your claim is covered only under Covered Risk 16, 18, 19 or 21, that payment is the amount of Your insurance then in force for the particular Covered Risk.

(b) We will pay reasonable costs You pay to relocate any personal property You have the right to remove from the Land, including transportation of that personal property for up to twenty-five (25) miles from the Land, and repair of any damage to that personal property because of the relocation. The amount We will pay You under this paragraph is limited to the value of the personal property before You relocate it.

d. All payments We make under this Policy reduce the Policy Amount then in force, except for costs, attorneys' fees and expenses. All payments We make for claims which are covered only under Covered Risk 16, 18, 19 or 21 also reduce Our Maximum Dollar Limit of Liability for the particular Covered Risk, except for costs, attorneys’ fees and expenses.

e. If We issue, or have issued, a Policy to the owner of a Mortgage that is on Your Title and We have not given You any coverage against the Mortgage, then:

(1) We have the right to pay any amount due You under this Policy to the owner of the Mortgage, and any amount paid shall be treated as a payment to You under this Policy, including under Section 4.a. of these Conditions;

(2) Any amount paid to the owner of the Mortgage shall be subtracted from the Policy Amount then in force; and

CONDITIONS (Continued)

(3) If Your claim is covered only under Covered Risk 16, 18, 19 or 21, any amount paid to the owner of the Mortgage shall also be subtracted from Our Maximum Dollar Limit of Liability for the particular Covered Risk.

f. If You do anything to affect any right of recovery You may have against someone else, We can subtract from Our liability the amount by which You reduced the value of that right.

7. TRANSFER OF YOUR RIGHTS TO US

a. When We settle Your claim, We have all the rights and remedies You have against any person or property related to the claim. You must not do anything to affect these rights and remedies. When We ask, You must execute documents to evidence the transfer to Us of these rights and remedies. You must let Us use Your name in enforcing these rights and remedies.

b. We will not be liable to You if We do not pursue these rights and remedies or if We do not recover any amount that might be recoverable.

c. We will pay any money We collect from enforcing these rights and remedies in the following order: (1) to Us for the costs, attorneys’ fees and expenses We paid to enforce these rights and remedies; (2) to You for Your loss that You have not already collected;

(3) to Us for any money We paid out under this Policy on account of Your claim; and (4) to You whatever is left.

d. If You have rights and remedies under contracts (such as indemnities, guaranties, bonds or other policies of insurance) to recover all or part of Your loss, then We have all of those rights and remedies, even if those contracts provide that those obligated have all of Your rights and remedies under this Policy.

8. THIS POLICY IS THE ENTIRE CONTRACT

This Policy, with any endorsements, is the entire contract between You and Us. To determine the meaning of any part of this Policy, You must read the entire Policy and any endorsements. Any changes to this Policy must be agreed to in writing by Us. Any claim You make against Us must be made under this Policy and is subject to its terms.

9. INCREASED POLICY AMOUNT

The Policy Amount then in force will increase by ten percent (10%) of the Policy Amount shown in Schedule A each year for the first five years following the Policy Date shown in Schedule A, up to one hundred fifty percent (150%) of the Policy Amount shown in Schedule A. The increase each year will happen on the anniversary of the Policy Date shown in Schedule A.

10. SEVERABILITY

If any part of this Policy is held to be legally unenforceable, both You and We can still enforce the rest of this Policy.

11. ARBITRATION

a. If permitted in the state where the Land is located, You or We may demand arbitration.

b. The law used in the arbitration is the law of the state where the Land is located.

c. The arbitration shall be under the Title Insurance Arbitration Rules of the American Land Title Association (“Rules”). You can get a copy of the Rules from Us.

d. Except as provided in the Rules, You cannot join or consolidate Your claim or controversy with claims or controversies of other persons.

e. The arbitration shall be binding on both You and Us. The arbitration shall decide any matter in dispute between You and Us.

f. The arbitration award may be entered as a judgment in the proper court.

12. CHOICE OF LAW

The law of the state where the Land is located shall apply to this policy. In Witness Whereof, First American Title Insurance Company has caused its corporate name to be hereunto affixed by its authorized officers as of Date of Policy shown in Schedule A.

(This Policy is valid only when Schedules A and B are attached)

Copyright 2006-2010 American Land Title Association. All rights reserved. The use of this form is restricted to ALTA licensees and ALTA members in good standing as of the date of use. All other uses are prohibited. Reprinted under license from the American Land Title Association.

Eagle Schedule A

Eagle Schedule B

File No.: 246-5734161

EXCEPTIONS

In addition to the Exclusions, You are not insured against loss, costs, attorneys' fees, and expenses resulting from:

1. The right to enter upon said land and prospect for and remove all coal, oil, gas, minerals or other substances, as reserved in the Patent to said land.

2. Any charge upon said land by reason of its inclusion in Ocotillo Water Conservation District.

3. Any charge upon said land by reason of its inclusion in Sun Lakes Homeowners Association #2, Inc. (All assessments due and payable are paid.)

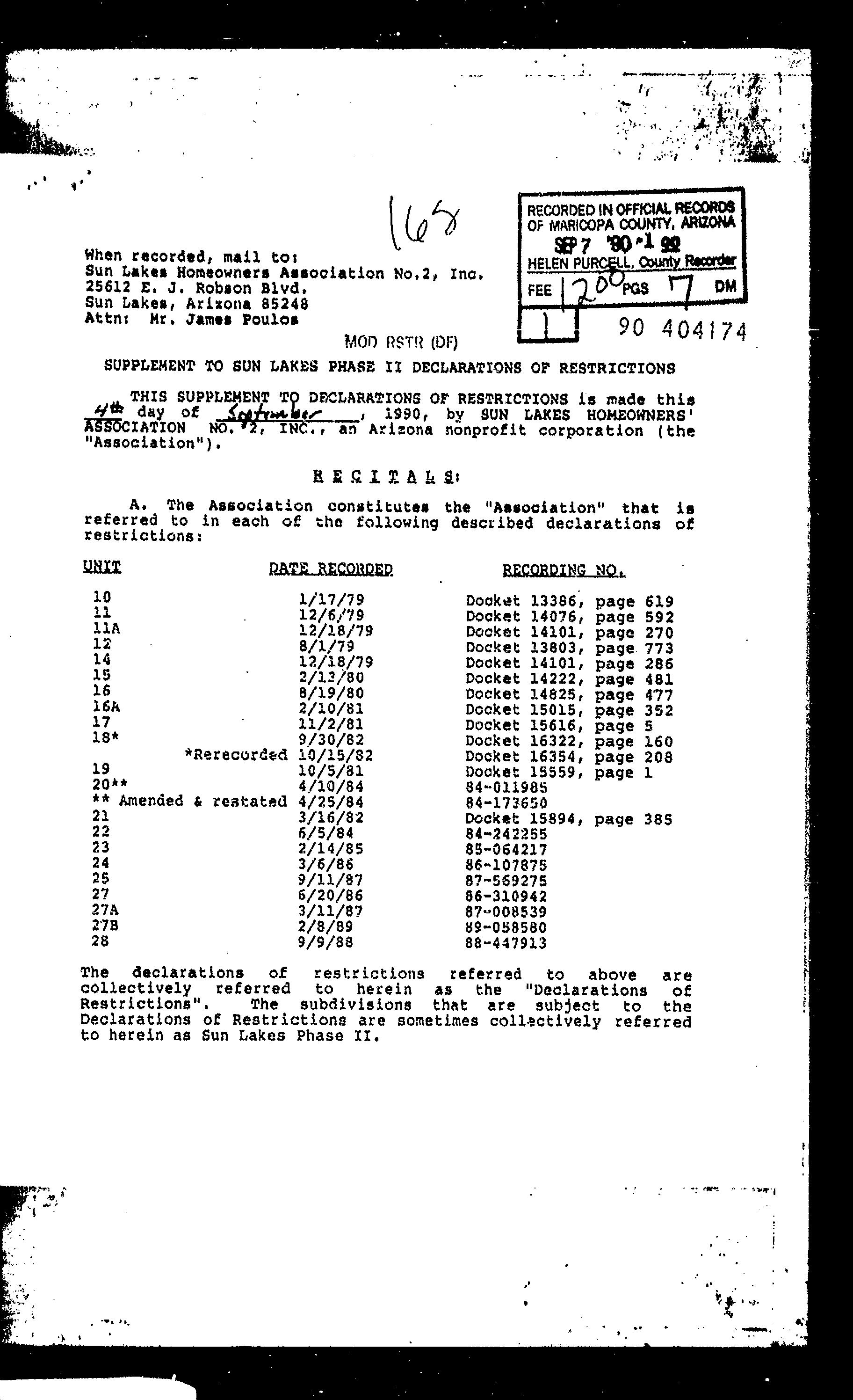

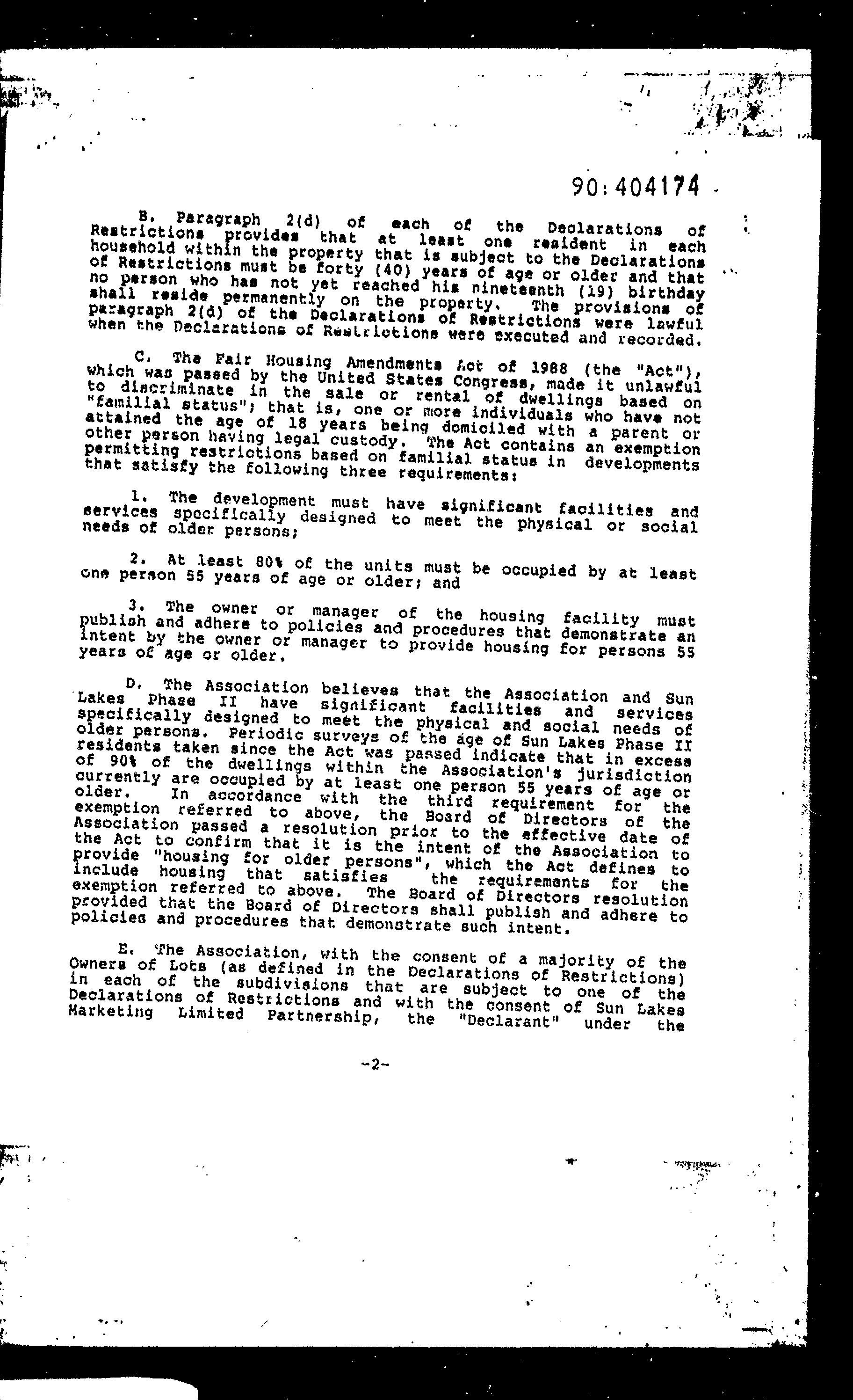

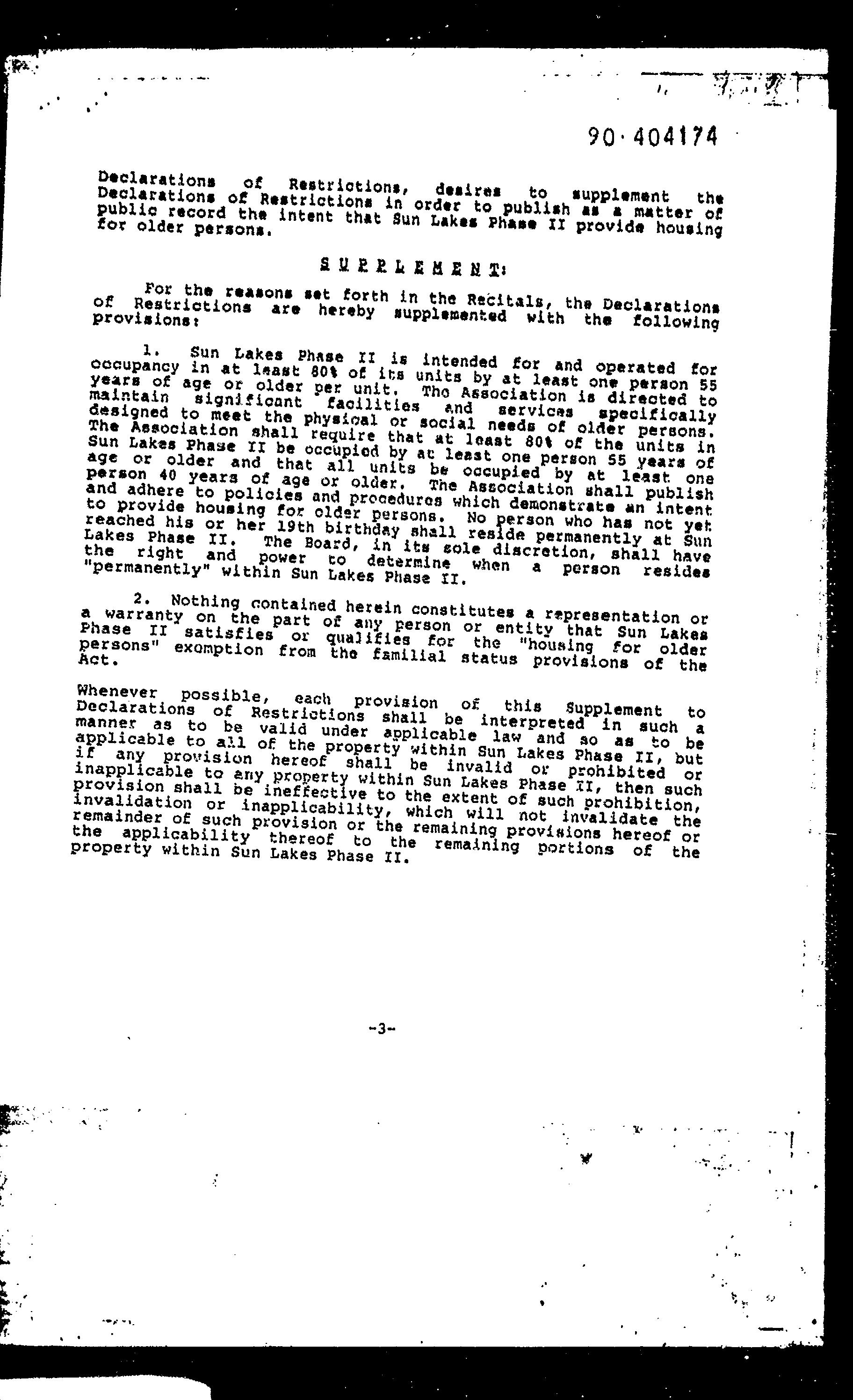

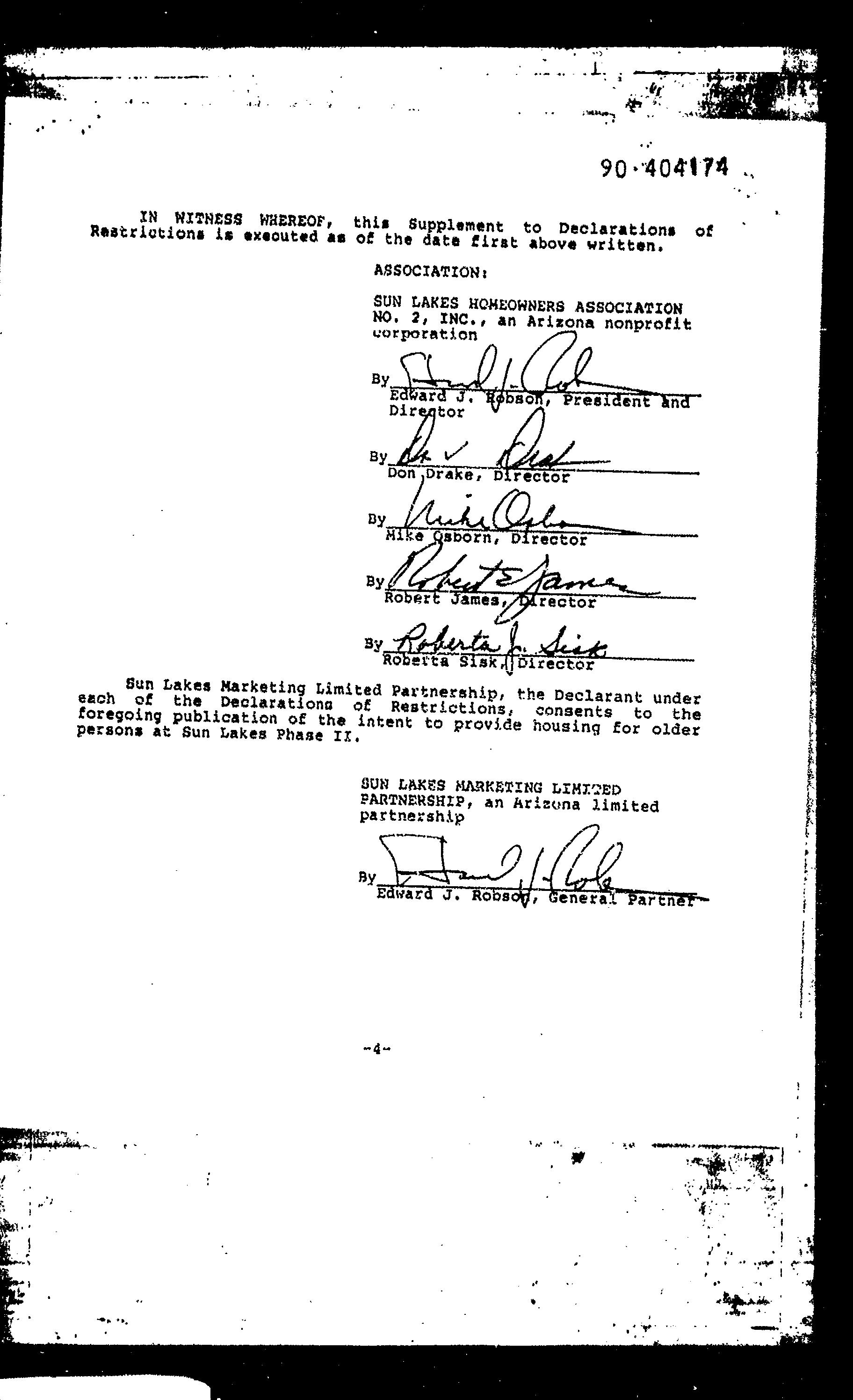

4. Covenants, conditions and restrictions in the document recorded as Docket 15617, Page 5; Supplement recorded as 90-404174, of Official Records, but deleting any covenant, condition or restriction indicating a preference, limitation or discrimination based on race, color, religion, sex, handicap, familial status, or national origin, to the extent such covenants, conditions or restrictions violate Title 42, Section 3604(c), of the United States Codes.

5. Easements, restrictions, reservations, conditions and set-back lines as set forth on the plat recorded as Book 237 of Maps, Page 14 and Affidavit of Correction recorded as 95-250811, of Official Records, but deleting any covenant, condition or restriction indicating a preference, limitation or discrimination based on race, color, religion, sex, handicap, familial status or national origin to the extent such covenants, conditions or restrictions violate 42 USC 3604(c).

6. Water rights, claims or title to water, whether or not shown by the public records.

Count on First American Title.

Count on us for service.

First American Title’s professionals are proud to provide the title insurance that assures people’s home ownership. Backed by First American Title Insurance Company, your transaction will be expertly completed in accordance with state-specific underwriting standards and state and federal regulatory requirements.

Count on us for stability.

First American Title is the principal subsidiary of First American Financial Corporation, and one of the largest suppliers of title insurance services in the nation. With roots dating back to 1889, we’ve served families for generations.

Count on us for convenience.

First American Title has a direct office or agent near you. We also have an extensive network of offices and agents throughout the United States, and internationally.

Count on us to meet your needs.

First American Financial Corporation offers more than title insurance and escrow services through its subsidiaries. Our subsidiaries also provide property data, title plant records and images, home warranties, property and casualty insurance, and banking, trust and advisory services.

Benefits from a professional REALTOR® .

Before you make the decision to try to sell your home alone, consider the benefits a REALTOR® can provide that you may not be aware of:

Understands market conditions and has access to information not available to the average homeowner.

Can advertise effectively for the best results.

Knows how to price your home realistically, to give you the highest price possible within your time frame.

Is experienced in creating demand for homes and how to show them to advantage.

Knows how to screen potential Buyers and eliminate those who can’t qualify or are looking for bargain-basement prices.

Knows how to go toe-to-toe in negotiations.

Is always “on-call,” answering the phone at all hours, and showing homes evenings and weekends.

Can remain objective when presenting offers and counter-offers on your behalf.

Maintains errors-and-omissions insurance.

Will listen to your needs, respect your opinions and allow you to make your own decisions.

Can help protect your rights, particularly important with the increasingly complicated real estate laws and regulations.

Is experienced with resolving problems to facilitate a successful closing on your home.

For sale by owner.

Many people believe they can save a considerable amount of money by selling their homes themselves. It may seem like a good idea at the time, but while you may be willing to take on the task, are you qualified? The following are some questions to help you realistically assess what’s involved:

Do you have the knowledge, patience, and sales skill needed to sell your home?

If your buyer is aggressive, can you negotiate a successful outcome for yourself?

Do you know how to determine the current market value of your home?

Are you aware of conditions in the marketplace today that affect value and length of time to sell?

Do you know how to determine whether or not a buyer can qualify for a loan?

Are you concerned about having strangers walking through your home?

Do you understand the steps of an escrow and what’s required of you and the buyer?

Are you familiar enough with real estate regulations to prepare a binding sales contract? Counter-offers?

Are you aware that every time you leave your home, you are taking it off the market until you return?

Have you made arrangements with an escrow and title company, home warranty company, pest-control service and lender to assist you with the transaction?

Do you need to hire a real estate attorney? If so, do you know what the cost will be and how much liability they will assume in the transaction?

Only you can determine whether you should attempt to sell your home—probably your largest investment—all alone. Talk with a REALTOR® before you decide. You may find working with a professional is a lot less expensive and much more beneficial than you ever imagined!

Do you know how to advertise effectively and what the costs will be?

Are you aware that prospective buyers and bargain hunters will expect you to lower your cost because there’s no REALTOR® involved?

Do you understand the various types of loans buyers may choose and the advantages and disadvantages for the seller?

Are you prepared to give up your evenings and weekends to show your home to potential Buyers and “just-looking” time wasters?

Key professionals involved in your transaction.

REALTOR®

A REALTOR® is a licensed real estate agent and a member of the National Association of REALTORS®, a real estate trade association. REALTORS® also belong to their state and local Association of REALTORS® .

Real Estate Agent

A real estate agent is licensed by the state to represent parties in the transfer of property. Every REALTOR® is a real estate agent, but not every real estate agent has the professional designation of a REALTORS®

Listing Agent

A key role of the listing agent or broker is to form a legal relationship with the homeowner to sell the property and place the property in the Multiple Listing Service.

Buyer’s Agent

A key role of the buyer’s agent or broker is to work with the buyer to locate a suitable property and negotiate a successful home purchase.

Multiple Listing Service (MLS)

The MLS is a database of properties listed for sale by REALTORS® who are members of the local Association of REALTORS®. Information on an MLS property is available to thousands of REALTORS®

Title Company

These are the people who carry out the title search and examination, work with you to eliminate the title exceptions you are not willing to take subject to, and provide the policy of title insurance regarding title to the real property.

Escrow Officer

An escrow officer leads the facilitation of your escrow, including escrow instructions preparation, document preparation, funds disbursement, and more.

Lenders

A financial institution that provides money to a borrower to purchase real estate, often in the form of a mortgage. Lenders play a vital role in the home buying process by assessing the borrower’s ability to repay the loan and setting the terms of the mortgage.

Inspectors

A licensed professional who evaluates the condition and safety of a property for a buyer or seller. They inspect the property from top to bottom, looking for defects that could be a financial burden or safety risk.

Appraisers

A professional who provides an unbiased estimate of a property’s value.

Preparing your home for sale.

First impressions have a major impact on potential buyers. Try to imagine what a potential buyer will see when they approach your house for the first time and walk through each room. Ask your REALTOR® for advice; they know the marketplace and what helps a home sell. Here are some tips to present your home in a positive manner:

Mow and edge the lawn regularly, and trim the shrubs.

Make your entry inviting: paint your front door and buy a new front door mat.

Paint or replace the mailbox, if needed.

If screens or windows are damaged, replace or repair them.

Repair or replace worn shutters and other exterior trim.

Make sure the front steps are clear and hazard-free. Make sure the doorbell works properly and has a pleasant sound.

Ensure that all exterior lights are working.

Check stucco walls for cracks and discoloration.

Remove any oil and rust stains from the driveway and garage.

Clean and organize the garage, and ensure the door is in good working order.

Shampoo carpeting or replace if worn. Clean tile floors, particularly the caulking.

Brighten the appearance inside by painting walls, cleaning windows and window coverings, and removing sunscreens.

Repair leaky faucets and caulking in bathtubs and showers.

Repair or replace loose knobs on doors and cabinets. If doors stick or squeak, fix them.

Make sure toilet seats look new and are firmly attached.

Repair or replace loud ventilating fans.

Replace worn shower curtains.

Rearrange furniture to make rooms appear larger. If possible, remove and/or store excess furniture, and avoid extension cords in plain view.

Remove clutter throughout the house. Organize and clean out closets.

Clean household appliances and make sure they work properly.

Air conditioners/heaters, evaporative coolers, hot water heater should be clean, working and inspected if necessary. Replace filters.

Check the pool and/or spa equipment and pumps. Make sure all are working properly and that the pool and/or spa are kept clean.

Inspect fences, gates and latches. Repair or replace as needed.

Staging your home for show.

To make the best impression, keep your home clean, neat, uncluttered and in good repair. Please review this list prior to each showing:

Keep everything clean. A messy or dirty home will cause prospective buyers to notice every flaw.

Clear all clutter from counter tops.

Let the light in. Raise shades, open blinds, pull back the curtains and turn on the lights.

Get rid of odors such as tobacco, pets, cooking, etc., but don’t overdo air fresheners or potpourri. Fresh baked bread and cinnamon can make a positive impact.

Send pets away or secure them away from the house, and be sure to clean up after them.

Close the windows to eliminate street noise.

If possible you, your pets, and your children should be gone while your home is being shown.

Clean trash cans and put them out of sight.

If you must be present while your home is shown, keep noise down. Turn off the TV and radio. Soft, instrumental music is fine, but avoid vocals.

Keep the garage door closed and the driveway clear. Park autos and campers away from your home during showings

Hang clean attractive guest towels in the bathrooms.

Check that sink and tub are scrubbed and unstained.

Make beds with attractive spreads. Stash or throw out newspapers, magazines, junk mail.

Terms you should know.

Appraisal

An estimate of value of property resulting from analysis of facts about the property; an opinion of value.

Annual Percentage Rate (APR)

The borrower’s costs of the loan term expressed as a rate. This is not their interest rate.

Beneficiary

The recipient of benefits, often from a deed of trust; usually the lender.

Closing Disclosure (CD)

Closing disclosure form designed to provide disclosures that will be helpful to borrowers in understanding all of the costs of the transaction. This form will be given to the consumer three (3) business days before closing.

Close of Escrow

Generally the date the buyer becomes the legal owner and title insurance becomes effective.

Comparable Sales

Sales that have similar characteristics as the subject real property, used for analysis in the appraisal. Commonly called “comps.”

Consummation

Occurs when the borrower becomes contractually obligated to the creditor on the loan, not, for example, when the borrower becomes contractually obligated to a seller on a real estate transaction. The point in time when a borrower becomes contractually obligated to the creditor on the loan depends on applicable state law. Consummation is not the same as close of escrow or settlement.

Deed of Trust

An instrument used in many states in place of a mortgage.

Deed Restrictions

Limitations in the deed to a parcel of real property that dictate certain uses that may or may not be made of the real property.

Disbursement Date

The date the amounts are to be disbursed to a buyer and seller in a purchase transaction or the date funds are to be paid to the borrower or a third party in a transaction that is not a purchase transaction.

Earnest Money Deposit

Down payment made by a purchaser of real property as evidence of good faith; a deposit or partial payment.

Easement

A right, privilege or interest limited to a specific purpose that one party has in the land of another.

Endorsement

As to a title insurance policy, a rider or attachment forming a part of the insurance policy expanding or limiting coverage.

Hazard Insurance

Real estate insurance protecting against fire, some natural causes, vandalism, etc., Depending upon the policy. Buyer often adds liability insurance and extended coverage for personal property.

Impounds

A trust type of account established by lenders for the accumulation of borrower’s funds to meet periodic payments of taxes, mortgage insurance premiums and/or future insurance policy premiums, required to protect their security.

Legal Description

A description of land recognized by law, based on government surveys, spelling out the exact boundaries of the entire parcel

of land. It should so thoroughly identify a parcel of land that it cannot be confused with any other.

Lien

A form of encumbrance that usually makes a specific parcel of real property the security for the payment of a debt or discharge of an obligation. For example, judgments, taxes, mortgages, deeds of trust.

Loan estimate (LE)

Form designed to provide disclosures that will be helpful to borrowers in understanding the key features, costs and risks of the mortgage loan for which they are applying. Initial disclosure to be given to the borrower three (3) business days after application.

Mortgage

The instrument by which real property is pledged as security for repayment of a loan.

PITI

A payment that includes principal, interest, taxes, and insurance.

Power of Attorney

A written instrument whereby a principal gives authority to an agent. The agent acting under such a grant is sometimes called an “attorney-in-fact.”

Recording

Filing documents affecting real property with the appropriate government agency as a matter of public record.

Settlement Statement

Provides a complete breakdown of costs involved in a real estate transaction.

TRID

Tila-respa integrated disclosures

The life of an escrow.

Chooses a Real Estate Agent

Gets pre-approval letter from Lender and provides to Real Estate Agent.

Makes offer to purchase. Upon acceptance, opens escrow and deposits earnest money.

Finalizes loan application with Lender. Receives a Loan Estimate from Lender.

Completes and returns opening package from First American Title.

Schedules inspections and evaluates findings. Reviews title commitment/preliminary report.

Provides all requested paperwork to Lender (bank statements, tax returns, etc.) All invoices and final approvals should be to the lender no later than 10 days prior to loan consummation.

Lender (or Escrow Officer) prepares CD and delivers to Buyer at least 3 days prior to loan consummation.

Escrow officer or real estate agent contacts the buyer to schedule signing appointment.

Documents are recorded and the keys are delivered!

Accepts Buyer’s offer to purchase.

Completes and returns opening package from First American Title, including information such as forwarding address, payoff lender contact information and loan numbers.

Orders any work for inspections and/or repairs to be done as required by the purchase agreement.

Escrow officer or real estate agent contacts the seller to schedule signing appointment.

Documents are recorded and all proceeds from sale are received.

Upon receipt of order and earnest money deposit, orders title examination.

Requests necessary information from buyers and sellers via opening packages.

Reviews title commitment/ preliminary report.

Upon receipt of opening packages, orders demands for payoffs. Contacts buyer or seller when additional information is required for the title commitment/preliminary report.

All demands, invoices, and fees must be collected and sent to lender at least 10 days prior to loan consummation.

Coordinates with lender on the preparation of the CD.

Reviews all documents, demands, and instructions and prepares settlement statements and any other required documents.

Schedules signing appointment and informs buyer of funds due at settlement.

Once loan is consummated, sends funding package to lender for review.

Prepares recording instructions and submits docs for recording.

Documents are recorded and funds are disbursed. Issues final settlement statement.

Accepts Buyer’s application and begins the qualification process. Provides Buyer with Loan Estimate.

Orders and reviews title commitment / preliminary report, property appraisal, credit report, employment and funds verification.

Collects information such as title commitment / preliminary report, appraisal, credit report, employment and funds verification. Reviews and requests additional information for final loan approval.

Underwriting reviews loan package for approval.

Coordinates with Escrow Officer on the preparation of the Closing Disclosure, which is delivered to Buyer at least 3 days prior to loan consummation.

Delivers loan documents to escrow.

Upon review of signed loan documents, authorizes loan funding.

The Buyer

The Escrow Officer

Chooses a Real Estate Agent

The Seller

The Lender

Closing Costs: Who Pays Whats

The Escrow Process

What is an escrow?

The escrow is the process of having a neutral party manage the exchange of money for real property. The escrow holder is known as an escrow or settlement officer or agent. The buyer deposits funds and the seller deposits a deed with the escrow holder along with all of the other documents required to remove all "contingencies" (conditions and approvals) in the purchase agreement prior to closing.

How is an escrow opened?

Once a purchase agreement is signed by all necessary parties, the agent representing the party who will pay the fee selects an escrow holder and the buyer's earnest money deposit and contract are submitted to the escrow holder. From this point, the escrow holder will follow the mutual written instructions of the buyer and seller, maintaining a neutral stance to ensure that neither party has an unfair advantage over the other. The escrow holder also follows the instructions of the Buyer's new lender, the seller's existing lender, and both parties' agents. The escrow holder ensures the transparency of the transaction, while carefully maintaining the privacy of the consumers.

Your escrow professional may:

Open escrow and, if instructed to do so, deposit your good faith funds in a separate escrow account.

Order a title search to determine ownership and status of the subject real property.

Issue a preliminary report and begin the process of eliminating the title exceptions you and your lender are not willing to take title subject to.

Request payoff information for the seller’s loans, other liens, homeowner’s association fees, etc.

Coordinate with the buyer’s lender on the preparation of the Closing Disclosure (CD).

Prorate fees, such as real property taxes, per the contract, and prepare the settlement statement.

Set separate appointments allowing the seller and you to sign documents and deposit funds.

Review documents ensuring all conditions and legal requirements are fulfilled; request funds from lender.

When all funds are deposited, record documents with the County Recorder’s Office to transfer the subject real property to you.

After the recordation is confirmed, close escrow and disburse\funds, including seller’s proceeds, loan payoffs, etc.

Prepare and send final documents to all parties involved.

Understanding title insurance.

The title industry and title insurance in brief.

Prior to the development of the title industry in the late 1800s, a home-buyer received a grantor’s warranty, attorney’s title opinion, or abstractor’s certificate as assurance of home ownership. The buyer relied on the financial integrity of the grantor, attorney, or abstractor for protection. Today, home-buyers look primarily to title insurance to provide this protection. Title insurance companies are regulated by state statute. They are required to post financial guarantees to ensure that any claims will be paid in a timely fashion. They also must maintain their own “title plants” which house duplicates of recorded deeds, mortgages, plats, and other pertinent county property records.

What is title insurance?

Title insurance provides coverage for certain losses due to defects in the title that, for the most part, occurred prior to your ownership. Title insurance protects against defects such as prior fraud or forgery that might go undetected until after closing and possibly jeopardize your ownership and investment.

Why is title insurance needed?

Title insurance insures buyers against the risk that they did not acquire marketable title from the seller. It is primarily designed to reduce risk or loss caused by defects in title from the past. A loan policy of title insurance protects the interest of the mortgage lender, while an owner’s policy protects the equity of you, the buyer, for as long as you or your heirs (in certain policies) own the real property.

When is the premium due?

You pay for your owner’s title insurance policy only once, at the close of escrow. Who pays for the owner’s policy and loan policy varies depending on local customs.

5

Compare First American Title’s Eagle Policy® for Owners

Consider This

One escrow transaction could involve more than 20 individuals, including real estate agents, buyers, sellers, attorneys, escrow officer, escrow technician, title officer, loan officer, loan processor, loan underwriter, home inspector, termite inspector, insurance agent, home warranty representative, contractor, roofer, plumber, pool service, and so on. And often, one transaction depends on another.

When you consider the number of people involved, you can imagine the opportunities for delays and mishaps. Your experienced escrow team can’t prevent unforeseen problems from arising; however, they can help smooth out the process.

Closing Your Escrow

What to do before the closing appointment.

Your escrow officer or escrow technician will contact you to schedule your closing appointment and inform you of the funds you need to bring with you. Obtain a cashier’s check for that amount made payable to First American Title. If a wire transfer is necessary, arrange for it in advance with your escrow officer.

First American Title is required by law to have funds deposited before escrow funds can be disbursed. Expect delays if you submit a personal check! If you have questions or anticipate a problem, contact your escrow officer immediately.

Don’t forget your identification.

You will need valid identification with your photo; a driver’s license is preferred. This is necessary so that your identity can be sworn to by a notary public. It’s a routine step, but it’s important for your protection.

What happens next?

During your signing appointment at First American Title, you will sign loan documents for the home you are purchasing and you will present your identification so the documents can be notarized. You will review the settlement statement and give the escrow officer your cashier’s check. (The seller will sign at a separate appointment.)

First American Title will confirm that all contract conditions have been met and ask the lender to “fund the loan.” If the loan documents are satisfactory, the lender will send funds directly to First American Title. When all necessary funds are received we will disperse escrow funds to the seller and other appropriate payees. The signed loan documents will be returned to the lender. We will record the deed at the county recorder’s office. At this time your escrow is closed.

After the Closing

We recommend you keep all records pertaining to your home together in a safe place, including all purchase documents, insurance, maintenance and improvements.

Loan payments and impounds. You should receive a statement from your lender before your first payment is due. If you have not been notified, or if you have questions about your tax and insurance impounds, contact your lender.

Home Warranty Repairs. If you have a home warranty policy, call your home warranty company directly for repairs. Have your policy number available when you call.

Title Insurance Policy. First American Title will deliver your policy and your recorded deed.

Property Taxes. You may not receive a tax statement for the current year on the home you buy; however, it is your obligation to make sure the taxes are paid when due. Check with your mortgage company to find out if taxes are included with your payment. For more information on your property taxes, contact your county treasurer’s office.

Planning Your Move

Six Weeks Before:

Create an inventory sheet of items to move

Research moving options You’ll need to decide if yours is a do-it-yourself move or if you’ll be using a moving company.

Request moving quotes Solicit moving quotes from as many moving companies and movers as possible. There can be a large difference between rates and services within moving companies.

Discard unnecessary items Moving is a great time for ridding yourself of unnecessary items. Have a yard sale or donate unnecessary items to charity.

Packing materials. Gather moving boxes and packing materials for your move.

Contact insurance companies (Life, Health, Fire, Auto) You’ll need to contact your insurance agent to cancel/ transfer your insurance policy. Do not cancel your insurance policy until you have and closed escrow on the sale.

Seek employer benefits If your move is work-related, your employer may provide funding for moving expenses. Your human resources rep should have information on this policy.

Changing Schools If changing schools, contact new school for registration process.

Four Weeks Before:

Contact utility companies Set utility turnoff date, seek refunds and deposits and notify them of your new address.

Obtain your medical records. Contact your doctors, physicians, dentists and other medical specialists who may currently be retaining any of your family’s medical records. obtain these records or make plans for them to be delivered to your new medical facilities.

Note food inventory levels Check your cupboards, refrigerator and freezer to use up as much of your perishable food as possible.

Service small engines for your move by extracting gas and oil from the machines. This will reduce the chance to catch fire during your move.

Protect jewelry and valuables Transfer jewelry and valuables to safety deposit box so they can not be lost or stolen during your move.

Borrowed and rented items Return items which you may have borrowed or rented. Collect items borrowed to others.

One Week Before:

Plan your itinerary Make plans to spend the entire day at the house or at least until the movers are on their way. Someone will need to be around to make decisions. Make plans for kids and pets to be at the sitters for the day.

Change of address Visit USPS for change of address form.

Bank accounts Notify bank of address change. Make sure to have a money order for paying the moving company if you are transferring or closing accounts.

Service automobiles If automobiles will be driven long distances, you’ll want to have them serviced for a troublefree drive.

Cancel services. Notify any remaining service providers (newspapers, lawn services, etc) of your move.

Start packing Begin packing for your new location.

Travel items Set aside items you’ll need while traveling and those needed until your new home is established. Make sure these are not packed in the moving truck!

Scan your furniture. Check furniture for scratches and dents before so you can compare notes with your mover on moving day.

Prepare Floor Plan Prepare floor plan for your new home. This will help avoid confusion for you and your movers.

Moving Day:

Review the house Once the house is empty, check the entire house (closets, the attic, basement, etc) to ensure no items are left or no home issues exist.

Sign the bill of lading Once you are satisfied with the mover’s packing your items into the truck, sign the bill of lading. If possible, accompany your mover while the moving truck is being weighed.

Double check with your mover Make sure your mover has the new address and your contact information should they have any questions during your move.

Vacate your home. Make sure utilities are off, doors and windows are locked and notify your real estate agent you’ve left the property.

Central Arizona Branch Locator

1 Sun City West

623-299-3644

13940 W. Meeker Blvd, #119 Sun City West, AZ 85375 N of Meeker Blvd W of R.H. Johnson

2 The Legends

623-537-1608

20241 N. 67th Ave, #A-2 Glendale, AZ 85308 E side 67th Ave/N of 101

3 Arrowhead

623-487-0404

16165 N. 83rd Ave, #100 Peoria, AZ 85382

SE corner of N 83rd Ave and W Paradise Ln

4 Anthem

623-551-3265

39508 N. Daisy Mountain Dr, #128 Anthem, AZ 85086 NE corner Daisy Mtn Dr/Gavilan Peak Pkwy

5 Tatum Ridge

480-515-4369

11211 N Tatum Blvd, #A150 Phoenix, AZ 85028 N of Shea, E side of Tatum

6 Carefree

480-575-6609

7202 E. Carefree Dr, Bldg 1, #1 Carefree, AZ 85377 NE corner of Tom Darlington/Carefree Dr.

7 Scottsdale Forum

480-551-0480

6263 N. Scottsdale Rd, #110 Scottsdale, AZ 85250 E Side Scottsdale/S of Lincoln

8 Raintree

480-563-9034

8605 E. Raintree Dr, # 130 Scottsdale, AZ 85260 SW corner of E Raintree Dr and N 87th St

9 Chandler Portico

480-777-0051

2121 W. Chandler Blvd., #100 Chandler, AZ 85224 SW Corner Chandler Blvd./Dobson Rd.

10 Gilbert San Tan

480-777-0614

1528 E. Williams Field Rd. #101 Gilbert, AZ 85295 NW corner of Williams Field Rd./Val Vista Rd.

11 Mesa

480-401-3738

1630 S. Stapley Dr, #123 Mesa, AZ 85204 N of Baseline / W of Stapley

12 Gold canyon

480-288-0883

6877 South Kings Ranch Rd, #5 Gold Canyon, AZ 85118 E of 60/South Side Kings Ranch Rd.

Southern Arizona Branch Locator

1 Main Office

6390 E Tanque Verde Rd Tucson, AZ 85715

phone 520-885-1600 / 520-202-2626

2 Broadway

3777 E Broadway, Ste 130 Tucson, AZ 85716

phone 520-747-1644

3 Cambric 1840 E River Road Ste 200 Tucson, AZ 85718

phone 520-577-8707 / 520-529-1944

4 Casa Grande

442 W Kortsen Road, Ste 101 Casa Grande, AZ 85122

phone 520-426-4600

5 Casas Adobes

6760 N Oracle Rd, Ste 100B Tucson, AZ 85704 phone 520-575-1900

6 Green Valley

210 W Continental Road, Ste. 248 Green Valley, AZ 85622 phone 520-625-1095

7 Oro Valley/La Canada 11165 N La Canada Dr, Ste 143 Oro Valley, AZ 85737 phone 520-877-9200

8 Oro Valley/Oracle 8500 N Oracle Rd, Ste 100 Oro Valley, AZ 85704 phone 520-297-2576 | 520-219-6451

9 Houghton

8280 S. Houghton Rd, Ste 130 Tucson, AZ 85747 phone 520-618-7790

10 Skyline

2890 E Skyline Dr, Ste 200 Tucson, AZ 85718 phone 520-529-0506