Weekly Market Commentary

Week ending 28 June 2024

Week ending 28 June 2024

Week ending 28 June 2024

Welcome to our weekly market update. Our focus is on providing clear, concise insights into stock and bond market movements and the broader economic landscape.

The views expressed here are subject to change without notice and we can’t accept any liability for any loss arising directly or indirectly from any use of it. This is for your information only. It is not a recommendation or advice, if you’re unsure about anything please speak to your financial adviser.

This week’s highlights

• US and Japan equity markets were up: this came after a poor start to the week.

• Increases in inflation globally: came as a surprise in Canada and Australia.

• Japanese Yen weakens: reaching lowest level against the US Dollar for almost 40 years.

This week saw themes of higher volatility in the technology sector, focus on interest rates and Japanese currency challenges. Nvidia extended its losses from the end of last week into Monday, wiping $430 billion over three trading sessions. This contributed to a decline in the S&P 500. However, things recovered over the week with the US and Japan posting positive returns. The US Treasury 10-year yield increased from 4.26% to 4.30%.

Fed speakers reiterated the need for further evidence that inflation was cooling in the US before lowering interest rates. Over the border, Canada saw a surprising increase with year-on-year inflation increasing to 2.9% in May from 2.7% in April. Canada was the first G7 country (a group containing the world’s seven strongest economies) to cut interest rates but this increase in inflation will be a warning to other developed central banks. Australia also saw

higher than expected inflation in May, increasing the probability that the central bank could start raising interest rates again in August. This led to bond yields being higher over the week.

In Japan, low interest rates have continued to weaken the Yen. On Wednesday it fell to its lowest level against the US Dollar since 1986. This broke the level that previously led Japanese authorities to intervene in the currency markets. A weaker Yen boosts Japanese exporters by making their products more competitive. Japanese retail sales data rose for the 26th consecutive month in May. Weaker currency along with ongoing consumer strength meant Japan was one of the best performing markets this week.

Outlook remains consistent with recent weeks. Further evidence of inflation reducing is required before more central banks cut rates. Employment and activity data will also be critical to the evolution of their thinking. The US continues to look strong, but other regions, including the Eurozone, face more challenging conditions.

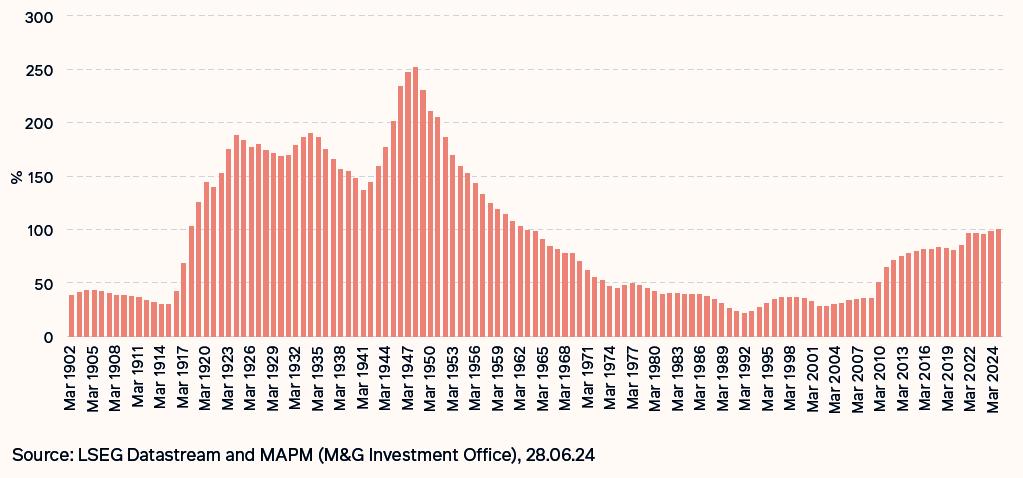

Focus on UK Public Debt as a percentage of Gross Domestic Product (GDP). The latest figures from the Office of National Statistics indicated that UK public debt as a percentage of GDP rose to its highest level since 1961 at 99.8%. Public finances have been impacted by the rise in spending following the COVID-19 pandemic and the Bank of England raising interest rates to a 16-year high. Both Labour and the Conservatives have promised to stick to the UK fiscal rules, meaning public debt as a percentage of GDP will have to fall in the fifth year of office after the election.

The Office of Budget and Responsibility estimates the incoming Chancellor has £8.9 billion of headroom to stay in line. This is the second lowest number any chancellor has had since 2010. This means any large government spending plans would need a significant increase in taxes. However this doesn’t seem likely as both parties have ruled out tax increases. Overall, the amount of spending the next UK government can do appears limited.

It’s clear how quickly outlooks can change across the globe, making it increasingly challenging to predict impact on markets and investments. This is continued evidence that maintaining a well diversified, long-term thinking to your investment approach rather than

reacting to market swings is key. By staying committed to carefully considered plans, investors can navigate through periods of volatility and uncertainty.

Has provided the commentary within this document.

If you have any questions in relation to this document, please discuss them with your financial adviser.. – we look forward to hearing from you.

Principle Financial Services Ltd is an Appointed Representative of New Leaf Distribution Ltd. who are authorised and regulated by the Financial Conduct Authority. Number 460421. 01530 860190

The Springboard Business Centre, Mantle Lane, Coalville, Leicestershire, LE67 3DW

www.principlefinancialservices.co.uk info@principlefinancialservices.co.uk shanefox@principlefinancialservices.co.uk samhagon@principlefinancialservices.co.uk

This guide is for general information and is not intended to address your personal and financial requirements and should not be deemed or treated as constituting financial advice. Nor does this guide constitute tax or legal advice and should not be relied upon as such. Tax treatment of investments and legal advice depends on the individual circumstances of each client and may be subject to change in the future. For further guidance on the matters discussed in this guide please speak to Shane Fox, who is a regulated financial adviser. Our services relate to certain investments whose prices are dependent on fluctuations in the financial markets beyond our control. Investments and the income from them may go down as well as up and you may get back less than the amount invested. Past performance cannot be used as a reliable prediction of future performance.