Guide to Retirement Income

Principal Sponsor

Principal Sponsor

Despite a succession of minor Budget initiatives, Australia is still a good way off from settling the shape of its retirement incomes regime

The creation of a viable post retirement regime in Australia remains a work in progress.

Despite expressions of intent on the part of the Federal Government and minor initiatives within successive Federal Budgets, the choices available to Australian retirees are almost as limited in 2018 as they were in 2015 and disagreement continues over proposals such as a one-size-fits-all MyPension or MyRetirement approach.

This Money Management Retirement Incomes Guide reflects the reality that the Australian retirement incomes regime represents a work in progress; that translating the relative success of superannuation accumulation to decumulation is proving to be a challenge for both the financial services industry and Government law-makers.

The initiatives announced in the 2017 and 2018 Budgets, particularly the changes to the tax treatment of deferred lifetime annuities (DLAs) have represented a step in the right direction in circumstances where the tax settings have been a perpetual, if largely unintended, obstacle to change but subsequent product development has been at best tentative and limited.

Much of the debate around retirement incomes policy in Australia has centred around the concept of Comprehensive Income Products in Retirement (CIPRs), which a significant section of the financial services industry and some senior officers within the Federal Treasury have sought to translate into a MyPension or MyRetirement offering.

However, the Productivity Commission (PC) and major planning groups such as the Financial Planning Association (FPA) and the Association of Financial Advisers (AFA) have been quick to point out just how diverse the needs of retirees can be and the probability that one size will simply not fit all.

What seems to be generally agreed is that while superannuation funds represent a suitable delivery vehicle for post-retirement products, the diverse needs of individual consumers are such that they will need professional advice in extracting the best from whatever regime is ultimately arrived at.

Mike Taylor Managing Editor

FE Money Management Pty Ltd

Level 10

4 Martin Place, Sydney, 2000

Managing Director: Mika-John Southworth Tel: 0455 553 775 mika-john.southworth @moneymanagement.com.au

Managing Editor/Editorial Director: Mike Taylor Tel: 0438 789 214 mike.taylor@moneymanagement.com.au

Senior Journalist: Nicholas Grove Tel: 0439 076 518 nicholas.grove@moneymanagement.com.au

Associate Editor - Research: Oksana Patron Tel: 0439 137 814 oksana.patron@moneymanagement.com.au

Features Journalist: Hannah Wootton Tel: 0438 957 266 hannah.wootton@moneymanagement. com.au

Journalist: Anastasia Santoreneos Tel: 0438 836 560 anastasia.santoreneos @moneymanagement.com.au

Product Marketing Manager: Dale Henry Tel: 0439 076 518 dale.henry@moneymanagement.com.au

ADVERTISING

Sales Director: Craig Pecar Tel: 0438 905 121 craig.pecar@moneymanagement.com.au

Account Manager: Ben Lloyd Tel: 0438 941 577 ben.lloyd@moneymanagement.com.au

Account Manager: Amy Barnett Tel: 0438 879 685 amy.barnett@financialexpress.net

PRODUCTION

Graphic Design: Henry Blazhevskyi Subscription enquiries: www.moneymanagement.com.au/ subscriptions

Money Management is printed by Bluestar Print, Silverwater NSW. Published fortnightly.

All Money Management material is copyright. Reproduction in whole or in part is not allowed without written permission from the editor. © 2018. Supplied images © 2018 iStock by Getty Images. Opinions expressed in Money Management are not necessarily those of Money Management or FE Money Management Pty Ltd.

Launched 31 years ago, Money Management has firmly established itself as the leading source of news and analysis for Australia’s financial services sector.

In this time, Money Management has rapidly evolved from a B2B newspaper into a respected provider of accredited education and training, research, professional support and advocacy as well as thought leadership in the financial services space.

While it remains the most read print and online publication by financial planners in Australia and is widely recognised as a leading advocate for this profession, Money Management's growing audience is a diverse one that also includes fund managers, accountants, risk advisers and superannuation fund trustees.

Money Management is also the clear publication of choice for finance institutions – both domestic and international – seeking to connect with the high earning and well-educated professionals working in Australia’s financial services sector.

Financial Express is a financial information and communications company founded in the UK in 1996.

It has offices in Australia, India, Hong Kong, and the Czech Republic. It provides data, software, research, and ratings to help asset managers and financial advisers make better investment decisions.

Mike Taylor writes that while the financial services industry agrees on the need for a strong post-retirement incomes framework, there is still significant disagreement on how it should be delivered and whether one size can ever fit all.

For most of the past half-decade there has been discussion within the Australian financial services industry about the possibility of a one-size-fits-all retirement income product – MyPension or MyRetirement.

The concept of MyPension/MyRetirement grew out of the relative success of MySuper, but where a default, ‘no frills’ approach was viewed as adequate in the accumulation phase, particularly for younger superannuation fund members, it has been deemed by some to be wholly inappropriate for people in the retirement ‘draw-down’ phase.

In July, the Productivity Commission’s (PC’s) draft report on Superannuation Efficiency and Competitiveness substantially put paid to the discussions about a MyPension/MyRetirement approach, suggesting that a one-size-fits-all approach would be inappropriate.

The inappropriateness of a one-size-fits-all approach has been argued by planning groups such as the Financial Planning Association (FPA) and the Association of Financial Advisers (AFA) who have pointed to the diversity of circumstances facing retirees, but annuities manufacturers such as Challenger Limited have taken a different view.

Not unlike the FPA and AFA, the PC has argued that the needs of people entering retirement are so diverse and potentially complex that it would be highly inappropriate to seek to foist a one-size-fits-all product on the market.

In doing so, the PC also suggested that the industry had evolved an inverted approach to

the retirement income phase, with people facing needless complexity in the relatively simple accumulation phase while being presented with few options as they positioned to begin drawing down on their accumulated balances.

The PC’s interim report stated the position as follows:

“The irony of the system is that, if anything, products are most complex during accumulation and most simple in retirement — when the converse constellation is needed for most members”.

“In the accumulation phase, most members have fundamentally simple needs: high net returns, low fees, meaningful disclosure by funds and transparent product features. These needs can be well served by ‘no-frills’, low-fee products with a balanced growth asset allocation.”

The PC draft report said many default products had these characteristics, albeit that their insurance offerings were unnecessarily complicated.

“Yet in the choice segment, there has been a proliferation of little used and complex products — over 40,000 in total — which complicates decision making and increases fees without boosting net returns. There are risks that some members who use these products are unwittingly buying a degree of control over their investments at the price of materially lower retirement

Continued on page 10

Continued from page 9

incomes.”

“As members approach retirement age, the potential impact of a year of poor returns on their balance at retirement rises. Life-cycle products - which reduce the share of growth assets in a member’s portfolio as they age - are intended to reduce this sequencing risk,” it said. “But most life-cycle products have a relatively modest impact on sequencing risk, while forgoing the higher returns that come with a larger weighting to growth assets (in some cases, from as early as 30 years of age).”

“While these products will always have a niche in the choice segment, their presence among MySuper products (covering about 30 per cent of MySuper accounts) is questionable and suggests many members are potentially being defaulted into an unsuitable product that sees them bearing

large costs for little benefit,” the PC draft said.

However, it said that, in retirement, members’ needs were no longer as straightforward but then stopped short of suggesting that there was a need for specific new post-retirement products.

“The large diversity of household needs, preferences, incomes and other assets means that no single product can meet the needs of everyone,” it said. “The range of retirement products on offer — including account-based pensions, annuities and new hybrid annuity products — appears sufficient to meet most members’ needs.”

“Annuities in particular offer a way to reduce longevity risk, though many are complex and will not suit many members.”

“A default retirement product (‘MyRetirement’) is not warranted,” the PC draft report said. “The goal of policy should be to remove unjustified

Source: Challenger

obstacles to all products, rather than favouring the take-up of specific products.”

“Policy changes in mid-2017 relating to Comprehensive Income Products for Retirement (CIPRs) were a good step in this direction. One of the underlying problems is that members at all stages find the super system too hard to navigate, and do not know where to turn for help,” it said. “While there is no shortage of information, many find it complex, overwhelming and inconsistent with their needs.”

The PC’s interim report and its suggestion that the current range of post-retirement products offers consumers a reasonable range of options is likely to further entrench the view that annuities will necessarily continue to sit at the centre of the evolving regime.

That likelihood was also reinforced by the

May Budget in which the Government built on its 2017 efforts based on providing a framework for deferred lifetime annuities.

Given the manner in which the centrality of annuities in the evolving post-retirement environment has boosted the balance sheet of Challenger Limited it is hardly surprising that the company supported the Government’s 2018 Budget announcements, particularly introducing a retirement income covenant to the Superannuation Industry (Supervision) Act requiring super funds to offer Comprehensive Income Products in Retirement (CIPRs).

Challenger also noted the Budget announcement of a new means test for lifetime retirement income stream products, including deferred lifetime annuities (DLAs) – something

Continued on page 12

Source: Australian Life Tables 2010-12 with 25-year mortality improvement factors.

Continued from page 11

which have not been generally available in Australia due to the prevailing tax settings.

The main reason for deferred annuities not being offered in Australia was the fact that they did not attract the same superannuation tax concessions as other retirement investments.

Challenger chose to regard this as an unintended consequence of the tax laws rather than a deliberate Government policy of exclusion.

Hardly surprising, then, was the view of Challenger chief executive, Brian Benari that the changes would encourage retirees to consider a wider range of retirement income products, including deferred lifetime annuities.

Benari noted that fixed term annuities, which represented around 80 per cent of Challenger’s annuity sales, would not be affected by the new rules.

Source: Challenger

Nathan Zahm looks at how careful financial planning prior to retirement can help individuals live in comfort after they stop working.

Retirement is a complex matter. Almost despite the volumes of research on the topic, there are rarely simple answers to the many questions retirees have.

To successfully navigate retirement, detailed planning around goals, risks and financial resources is critical to manage a long retirement, and a lack of sufficient planning makes retirees financially vulnerable to the risks of outliving retirement savings, overreacting to market volatility, holding inappropriate portfolios and being unprepared for unexpected costs.

Ideally, however, our role as financial professionals is to make investing simple and straightforward by taking these tough questions and giving accessible, actionable guidance to our clients.

To that end, perhaps the most popular question we get asked from retirees is, “What product do you recommend for retirement income?”

And while there are of course a lot of dependencies, caveats, and considerations in any financial decision, sometimes there are universal truths that are an important part of providing an accessible, actionable answer regardless of the circumstances.

One of these universal truths is cost. All else being equal, a lower cost product will produce more retirement income than a higher cost product.

Think about that for a second. We spend a ton of time as investment professionals looking for ways to increase retirement income, and one of the easiest ways may have been right in front of our face the whole time.

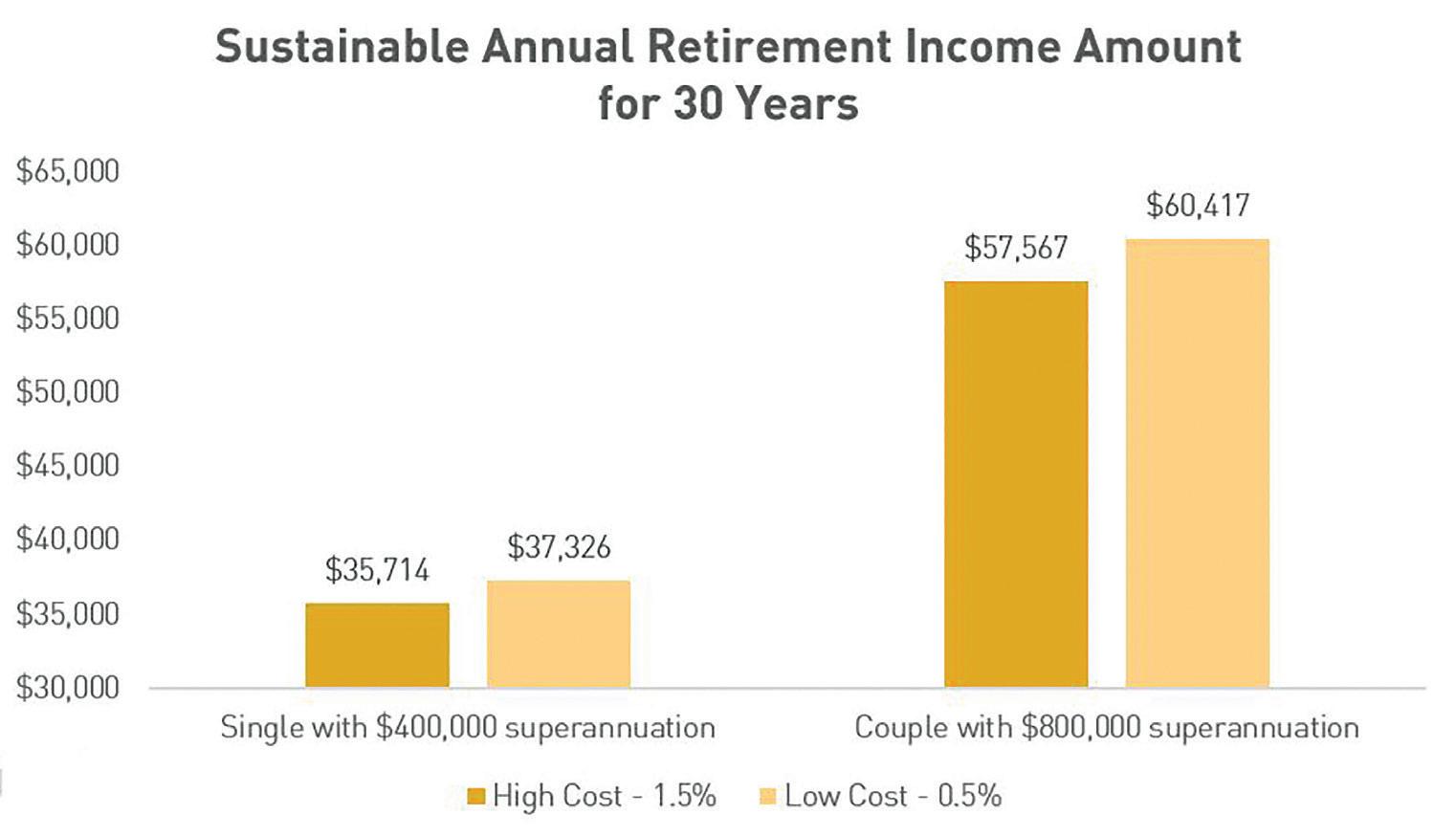

To find the answer we

income from both the age pension and superannuation drawdown, and we look at the amount a retiree can spend in real terms each year for 30 years with 95 per cent certainty, and we compare two cost scenarios. The first assumes that they are invested in a high cost product charging 1.5 per cent, and the second is a lower cost product charging 0.5 per cent. The differences are striking.

For a single retiree with a $400,000 superannuation balance at retirement, they are able to spend over $1,600 (a 4.5 per cent increase) more per year, adding up to more than $48,000 over the course of their 30-year retirement, if they use the lower cost investments. For a couple with

Continued on page 18

Continued from page 17

a combined $800,000 superannuation balance, they are able to spend more than $2,800 (a five per cent increase) more per year, or over $85,000 total, when using lower cost solutions.

Additionally, the importance of fees actually increases with wealth too. Driven by the higher dependence on superannuation to meet income needs, those retiring with superannuation balances over $1,000,000 will find their sustainable annual retirement income increases six per cent to nine per cent when using lower cost products versus higher cost products.

Another candidate for the most popular question from retirees is, “How much do I need to retire?”

Again, there are many complex planning elements that must be considered in answering that question, but our universal truth on the importance of controlling costs to maximise retirement income still holds.

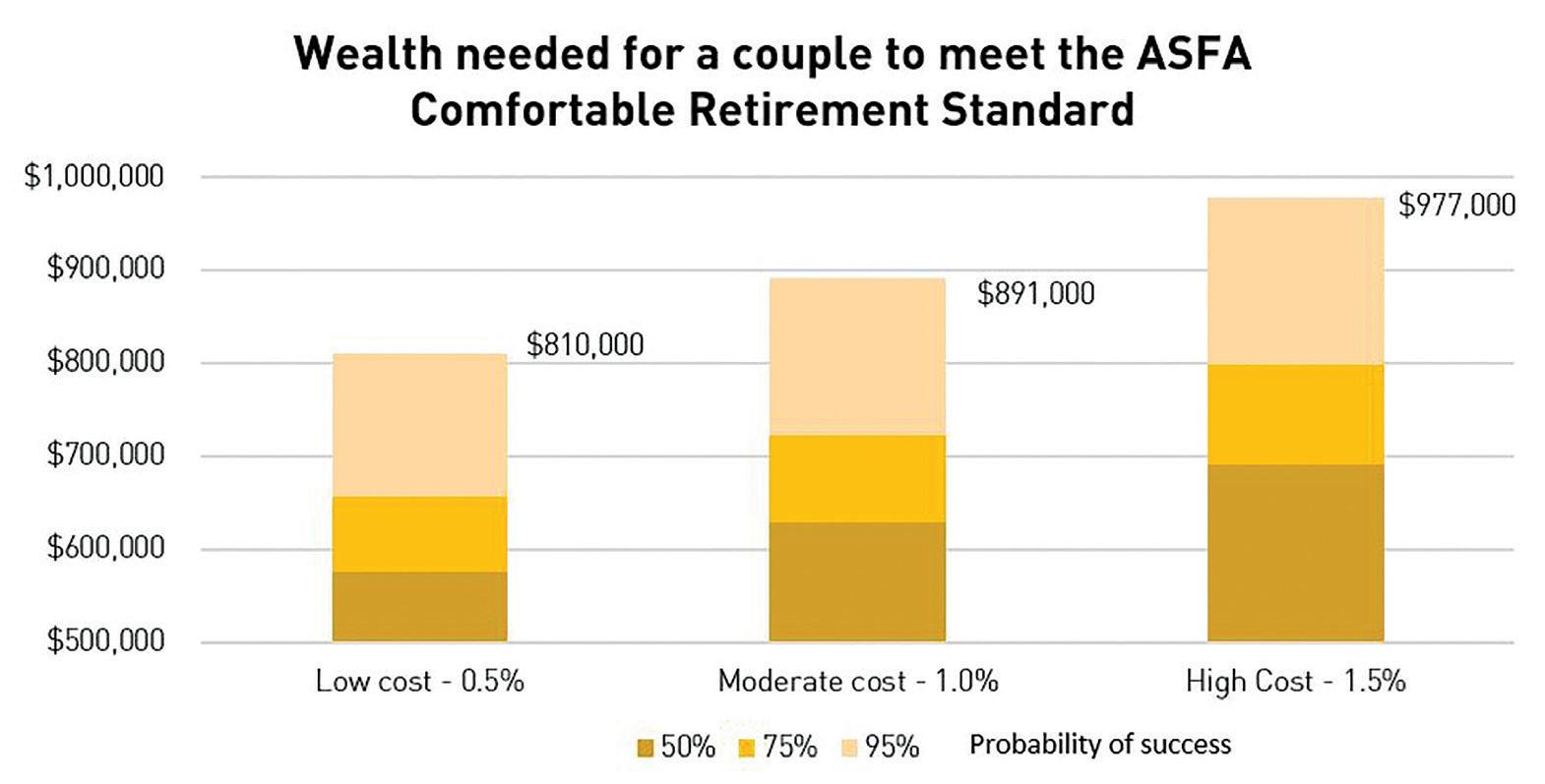

In this case we assume a couple planning for retirement desires to spend the Association of Superannuation Funds of Australia (ASFA) Comfortable Retirement Standard ($60,604 in real terms) for 30 years and would like to see the wealth needed to meet that goal with different probabilities of success.

Again we incorporate both the age pension and superannuation drawdown, and we look at the superannuation balance needed to meet

Source: Vanguard, June 2018 VCMM Simulation

Note for chart one: The income levels shown are based on a constant real spending amount over a 30-year horizon with a 95 per cent probability of success. Retirees are homeowners with a balanced (50 per cent equity/50 per cent bond) portfolio. The model incorporates the age pension as at 20 September 2018 and only considers financial wealth and therefore does not consider assets that would not be deemed to earn an income (i.e. home contents) or additional income (i.e. employment income) which would shift eligibility. The model treats superannuation and non-superannuation assets as one pool of financial assets and therefore we have assumed that any minimum withdrawals from super that exceed the retirement income targeted are reinvested in a non-super account.

this income objective with 50, 75, and 95 per cent probability while paying low (0.5 per cent), moderate (one per cent), or high (1.5 per cent) costs.

Focusing on the 95 per cent probability, we see that roughly for every 50 basis point increase in costs, the couple needs an additional 10 per cent in their superannuation to meet their goal, and comparing the high cost 1.5 per cent scenario to the low cost 0.5 per cent, we can see a difference of $167,000 in wealth needed to meet the same objective.

Now, make no mistake, you will almost certainly need to pay some investment costs for a quality product, and there is more to investing than costs alone, such as the value of quality

financial advice. However, controlling those costs is a guaranteed way to keep more available for retirement income.

Developing a financial plan that can best meet the highly unique circumstances of each retiree is far from simple, and good advice is likely to play an important role for most. But if you’re looking for to deliver accessible, actionable guidance, a good place to start is making sure your clients aren’t paying too much for their investments. It’s one of the few things you can control and a great way to boost your client’s retirement income prospects.

Nathan Zahm is senior investment strategist at Vanguard Investment Strategy Group.

Source: Vanguard, June 2018 VCMM Simulation

Note: The ASFA Comfortable Retirement Standard as at June 2018 is $42,953 per year for a single and $60,604 per year for a couple. We have assumed 0.5 per cent, one per cent, and 1.5 per cent annual investment fees, the retirees are homeowners and a balanced (50 per cent equity/50 per cent bond) portfolio. The model incorporates the age pension as at 20 September 2018 and only considers financial wealth and therefore does not consider assets that would not be deemed to earn an income (i.e. home contents) or additional income (i.e. employment income) which would shift eligibility. The model treats superannuation and non-superannuation assets as one pool of financial assets and therefore we have assumed that any minimum withdrawals from super that exceed what is needed to meet the ASFA retirement standard are reinvested in a non-super account. A non-homeowner would need to consider rental costs in addition to the Retirement Standards.

The task of providing clients with the income they need for a long time, or even a lifetime, is a complex one with many moving parts.

Funding retirement income involves balancing the financial resources a client has available with their expectations of income. It involves choices and priorities. It sometimes also comes down to making some ‘best estimates’ in relation to factors that are simply unknowable –like just how long a client will live in retirement or how investment markets will actually perform over time.

A combination of market and sequencing risk, increasing longevity and unsustainable drawdowns could see many clients outlive their savings in retirement. Without appropriate planning, where a client outlives their savings in retirement they will be dependent on the Age Pension for all of their income needs. And simply, for many clients this just won’t be enough.

There are a range of different philosophies for constructing retirement income streams that will last for a long time, or even a lifetime.

One such retirement income philosophy

involves complementing the income a client will derive in retirement from a structure like an account-based pension (typically with an allocation to a range of growth and defensive assets) with a guaranteed level of income (payable for as long as a client may live and irrespective of how investment markets perform) from a source such as a guaranteed lifetime annuity.

Compiling the ‘right’ combination of different retirement income products can assist a client in improving their retirement income outcomes.

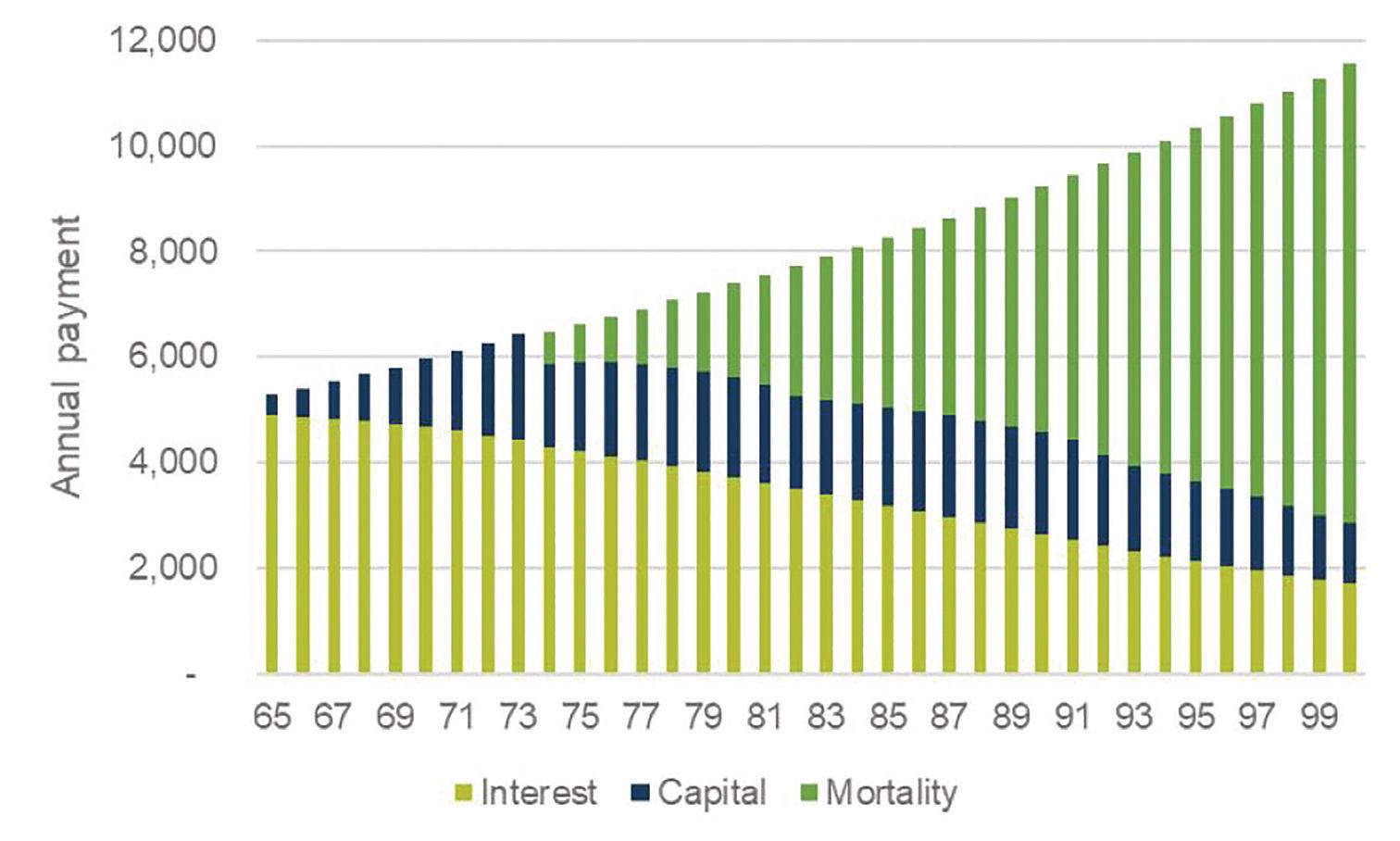

Take, for example, a recently retired 66-year old client couple, Mary and Michael. They own their own home and have no plans for moving any time soon. Mary and Michael have each accumulated $300,000 in retirement savings in their respective superannuation funds. They are comfortable with an allocation of 50% of their portfolio to growth assets. They have $50,000 in joint cash savings and $20,000 of non-financial assets.

Mary and Michael ‘want’ income of $60,604 p.a. (equal to the ASFA ‘comfortable’ level of income at June 2018) for as long as possible to

meet their desired level of retirement lifestyle. However, if this level of income were to runout (where their retirement savings were depleted over time for example) they ‘need’ income of $42,000 p.a. to meet their essential expenses. In this case their $42,000 of income ‘needs’ exceeds the current maximum rate of Age Pension for a couple ($35,916.40 p.a. at 20 September 2018).

Using the Challenger Retirement Illustrator we can model different retirement product allocations for these clients. A projection

of Mary and Michael’s combined retirement income is shown in the chart below.

Account-based pensions only

We see that using an account-based pension only for these clients (shown as the black dotted line) that retirement assets last to age 93. From this point these clients are dependent on income from the Age Pension alone. As highlighted above, this level of income is insufficient for their needs.

There

Source and assumptions: Challenger Retirement Illustrator. Amounts shown are in today's dollars. Investment return sourced from Willis Towers Watson data. Assumes net investment returns (after all fees and charges) of 2.6% p.a. for defensive assets and 6.4% p.a. for growth assets. CPI of 2.5% p.a. Cash and term deposits return 3% p.a. Centrelink rates and thresholds as at 20 September 2018. Challenger Guaranteed (Liquid Lifetime) Annuity, Flexible Income Option illustrated. Full CPI indexation, maximum withdrawal period, nil ASF. Annuity rates effective 21 September 2018.

The Illustrator also allows us to model this scenario over a range of 2,000 possible market scenarios and, in this case, we see that Mary and Michael are only able to meet their income needs (at age 93 which is the point at which there is a 50% chance that one of this couple is still alive) in 40% of these 2,000 modelled scenarios.

Partial allocation of defensive assets to a guaranteed lifetime annuity

However, by allocating in this case 25% of Mary and Michael’s superannuation assets to guaranteed lifetime annuities (while maintaining the initial 50% allocation to growth assets) the projected retirement income outcomes are significantly improved. This partial allocation provides:

• A guaranteed layer of income above the Age Pension, sufficient to meet income ‘needs’ (in fact in 100% of the 2,000 modelled scenarios income needs are metan increase of 60% over the account-based pension only);

• Improved longevity of the account-based pension;

• Increased retirement income over life expectancy and beyond; and

• Increased estate outcomes over various timeframes.

There are many circumstances in which a tailored combination of account-based pension and guaranteed lifetime annuity can significantly improve retirement income outcomes. To see how you can improve retirement outcomes for your clients please contact a Challenger Business Development Manager.

This information is provided by Challenger Life Company Limited ABN 44 072 486 938, AFSL 234670 (Challenger Life). It is intended for advisers only for illustrative purposes, and we have not taken into account any individuals actual financial situation, needs or circumstances. Clients should consider the relevant product disclosure statement and the appropriateness of the product before making any investment decision.

TAL’s Ashton Jones writes that superannuation is, for the most part, succeeding in its objective of preparing Australians for retirement.

Today, Australia’s age pension system is comfortably supported by 4.5 workers per pensioner. But by the time a current 30-year-old retires in 2050, the Department of Treasury forecasts that this rate will fall to just 2.7 workers per pensioner. Needless to say, this has profound implications for future retirees.

The proportion of workers to pensioners (the “Dependency Ratio”) is a bellwether for the structural integrity of our retirement system. In its current state, we can expect three pillars of the Australian retirement system (the age pension, family home and super guarantee) to face major challenges, such as:

1. The age pension becoming less sustainable for future Governments, 2. Home ownership continuing to concentrate towards the older or wealthier, 3. Many super funds’ net cash flow position moving towards negative.

We have shown immense foresight in developing a robust retirement system that is the envy of most comparable countries. To maintain this privileged position, the industry must acknowledge its challenges, and continue to innovate.

Opportunity knocks for super funds –however, supporting 21st century retirees will require new and creative services.

For a start, super funds need to take stock and think deeply about the skills available across staff and partners. Different skills will be required to more closely match investment strategies to members’ retirement needs.

An emerging school of thought revolves around the idea that super funds need to broaden their value propositions beyond mere investment vehicles to full-service retirement concierges –but what does that mean in practice?

For a start, super funds can focus on the wellbeing and living standards of members rather than merely generating investment returns. This should lead to a better quality of life for retiree members, as super funds become a gateway to retirement planning, health and wellbeing services, or even aged care.

A number of super funds have begun to factor in the demographic shift through an investment lens, taking sizeable stakes in retirement villages around the country. As members age, this presents a natural synergy for funds to explore – subsidising retirement living arrangements for members could provide more value than the equivalent cash amount.

A similar shift in mindset will be required from insurance in super. People in their late 60s and over have less need for life insurance once mortgages are settled and children have moved

Continued on page 24

Continued from page 23

out. However, retirees still face health risks and need a protection strategy.

Cover for illnesses such as dementia or stroke could be more valuable than the broad insurance cover typically available through super. And if benefits are provided through direct support – such as in-home care – this might be a better member outcome than an equivalent lump sum payment. This benefit model is particularly compelling in light of a North American study showing that 74 per cent of people over 65 suffer from at least one chronic disease, and for retirees facing cognitive decline and a diminishing capacity to make financial decisions.

Super funds must also recognise that members entering retirement face different risks to younger members and have different priorities as a result. Rather than being content to take on risk and watch balances accumulate over decades, older members will require investment strategies that manage sequencing risk (the risk of poor investment performance just prior to retirement) by factoring in their withdrawal behaviour whilst still allowing them to benefit from exposure to growth assets.

Super funds are also increasingly looking at lifetime income products, such as annuities, to provide security to older members with their increasing life expectancies.

This trickle will soon become a flood following the release of the Government’s Retirement Income Covenant Position paper. As currently proposed, all funds will be required to offer a Comprehensive Income Product for Retirement (CIPR) by 1 July 2020. This CIPR must include a component of longevity risk protection that provides a “broadly constant income for

life.” Simple account-based pensions will not be sufficient.

Of course, longevity in product design requires a deep understanding of mortality trends and their influential factors – this is why it is the natural domain of insurers. Understanding these trends could offer ancillary benefits for super funds, including being able to provide more tailored member experiences and bespoke retirement solutions from a menu of different propositions.

Super funds can’t allow their members to face these risks alone and should look to leverage the trust held in them through goals-based advice that helps members to mitigate risks and retire in comfort. Meanwhile, new savings products – outside the super balance with its many access restrictions and contribution limits – could support one-off costs, whether health-related expenses or a welldeserved holiday. If recent investment data is any indication, historically-maligned insurance bonds are beginning a resurgence.

While some of these ideas will undoubtedly fall by the wayside, now is the time for debate –while we still have the luxury! Whatever happens, it seems likely that super funds will naturally move to become the key pillar in Australian retirement over coming decades – particularly as structural changes in our economy challenge the age pension and the very concept of home ownership for many young Australians. While there are many clear challenges for super, I look forward to seeing it evolve to a bold new dynamic.

Ashton Jones is head of investments, retirements and new propositions at TAL.

“Understanding [mortality] trends could offer ancillary benefits for super funds, including being able to provide more tailored member experiences and bespoke retirement solutions from a menu of different propositions.”

- Ashton Jones, TAL

We know clients want advisers to take the time to understand their goals and dreams and offer solutions for achieving them. When we do this well, clients value advice.

Starting with good conversations is important. If, for example, an adviser can clearly explain which investments are supporting their client’s goals – like housing and health care – or how investments may help mitigate the rising cost of living, they’ll truly value your advice.

A traditional way advisers model retirement portfolios for clients is based on the Capital Asset Pricing Model.

The client’s risk appetite is the most important factor determining their Strategic Asset Allocation (SAA). Once the SAA is set, fund managers are selected, and the portfolio is constructed. However, the model is technically complex and often difficult for clients to understand.

Behavioural economics has led to a shift away from the traditional risk profile-based framework towards a more goals-based world of tailored investment portfolios. The focus becomes what’s needed to achieve a client’s goals, bringing more meaning to the conversation and helping clients articulate their risk appetite in terms of tradeoffs between tangible outcomes. The supporting portfolio is then built to manage these outcomes. Outcomes are typically based on the categories of future (legacy), lifestyle, essentials and safety.

This approach to investment choice is led

by a holistic assessment of the client’s needs, objectives and tolerances, as opposed to the existing framework principally driven by the client’s risk profile. The focus is then on whether the investments support the client’s goals and not on whether a chosen fund out-performed its relevant market benchmark.

Put another way, the value advisers provide won’t be linked to whether managers out or underperformed benchmarks. Instead, client goals become central to the conversation – and staying on track, the definition of success.

To help have this discussion, AMP has developed a Retirement Modelling Tool that allows a client’s income and withdrawal needs to be modeled using a combination of, account-based pension, annuity and Centrelink payments that’ll help achieve their goals in delivering consistent income through their retirement.

It works through 300 scenarios and will show the ones that meet the client’s income and withdrawal needs as well as their risk profile. Analysis provided by the tool includes the client’s retirement income, assets and Centrelink payments over 15 or 25 years. The tool can also help in structuring the client’s investments in their account based pension to achieve their goals.

If you'd like to know more about AMP's Retirement Modelling Tool, get in touch with AMP.

account-based pension?

Jim Hennington questions whether growing longevity combined with market risk means that the time for the account-based pension has passed.

Recent research from National Seniors Australia indicates that almost a quarter of seniors aged 75 to 79 have run out of savings. This proportion increases to almost a third for those aged over 80.

A typical household has two or three sources of income in retirement including: the Age Pension, income from superannuation and income from non-super investments. Running out of savings means living solely on the Age Pension, which is $23,598 per annum for singles or $35,573 per annum for couples.

The Age Pension is significantly less than what the Association of Superannuation Funds of Australia (ASFA) deems a ‘modest’ standard of retirement. It covers basic living costs but includes no budget for things like home maintenance, household items, any creature comforts, health insurance, running a car or holidays.

For those wanting a lifestyle that’s higher than the Age Pension, a complex balance needs to be met between how much they spend now and preserving some assets for spending later in life.

Retirement savings ideally should be managed with great care and vigilance. If you spend too much early in retirement you risk running out later in life and becoming a potential burden on family and loved ones. But if you’re too frugal you may not get to enjoy the retirement you saved hard to secure. The balance needs to be ‘just right’.

The superannuation product typically used by retirees to manage the balance between spending and capital preservation is the account-based pension (ABP).

With an ABP your superannuation remains invested in the investment option of your choice and you simply draw down on your account balance for income. The level of income you

take is subject to a minimum percentage of your balance each year. The minimum is four per cent of your balance for people up to age 65 and then steps up at key age bands to peak at 14 per cent for those aged 95 or more.

ABPs, and their predecessor the ‘allocated pension’, were designed around 1992 - with the purpose of providing an income that broadly reflects a CPI-linked lifetime pension up to age 80. However, for many retirees their ABP has not and will not deliver anything like a CPI-linked income for the whole of their lifetime.

As we saw in the GFC in 2008, investment returns over, and above inflation can be very uncertain.

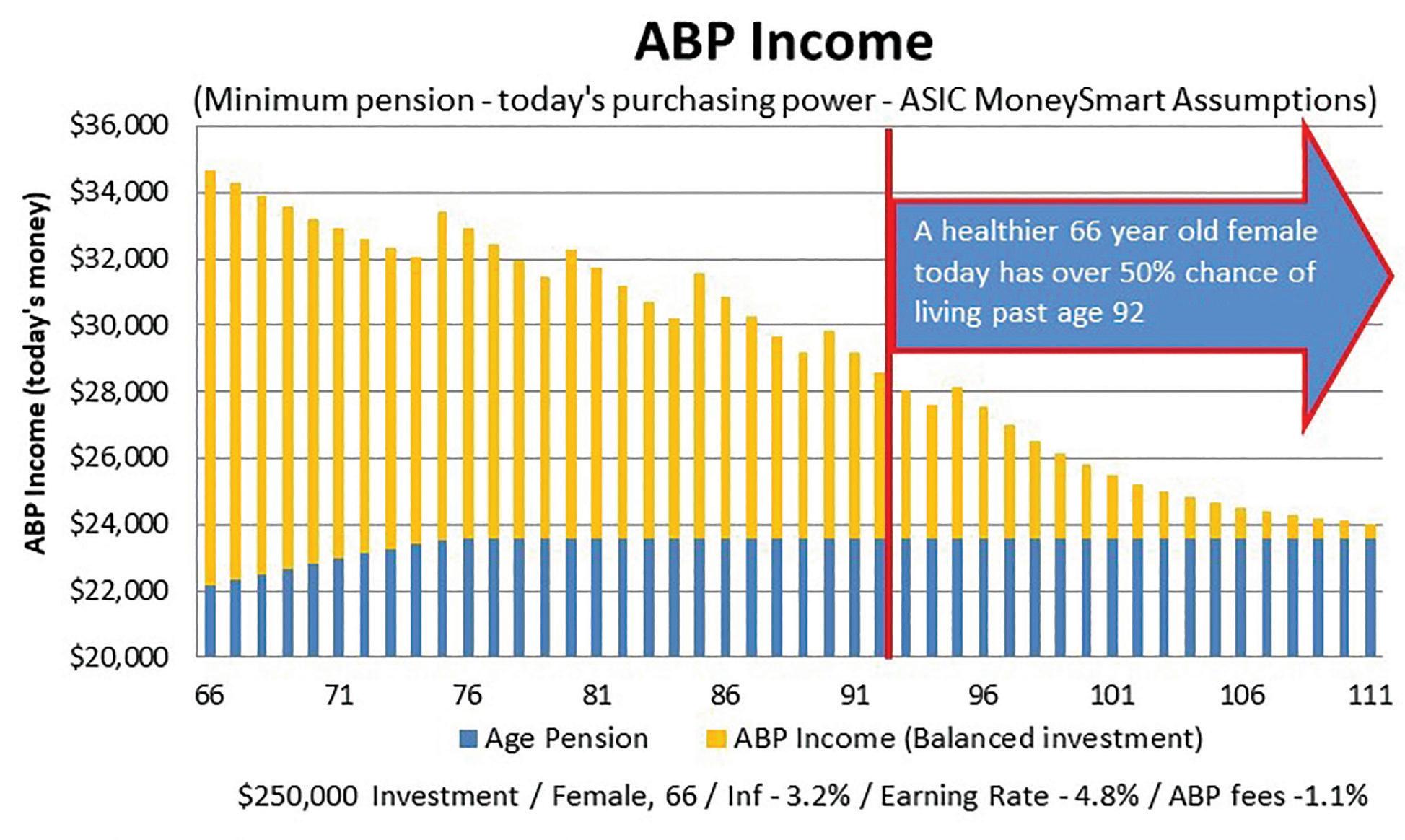

“ABP Income’ chart shows the projected income (in today’s purchasing power) from an ABP invested in a balanced portfolio using the recommended assumptions in ASIC’s MoneySmart retirement calculator. This illustration assumes a rate of return of just 4.8 per cent per annum, less fees of 1.1 per cent per annum and a 3.2 per cent allowance for cost of living increases throughout retirement.

Presumably the Australian Securities and Investments Commission (ASIC) is being conservative to allow for the fact that ABPs carry considerable market risks.

If your actual investment returns are less than the amount you are required to draw, then you’re actually spending your capital. Retirees need to use conservative assumptions in order to have any reasonable degree of confidence that their lifestyle will last for life and their savings won’t run out prematurely.

The assumed starting balance for chart one is $250,000 invested in a balanced portfolio

Continued on page 30

Continued from page 29

at age 66. It assumes the standard minimum percentage is drawn as income each year.

You can see that by age 95, the spending power of the income from the ABP under this scenario has dropped to around one third of what it was at age 66. This is a far cry from the product’s objective when it was designed in 1992 – to provide a CPI-linked pension.

Longevity risk is increasing and this is a problem, particularly given that more and more retirees are living well into their 80s and 90s now.

The world has seen significant advances in medical research, particularly over the past 50 years. With each decade that passes, retirees find their life expectancies increasing further and further.

Recent research has found that the cashflow

projections used by financial advisers aren’t always continued to the end of the Australian Life Tables. If they were then retirees would see how the real income from their ABP reduces at older ages. By not projecting this far into the future many members may be lulled into a false sense of security, particularly if their health status is better than average.

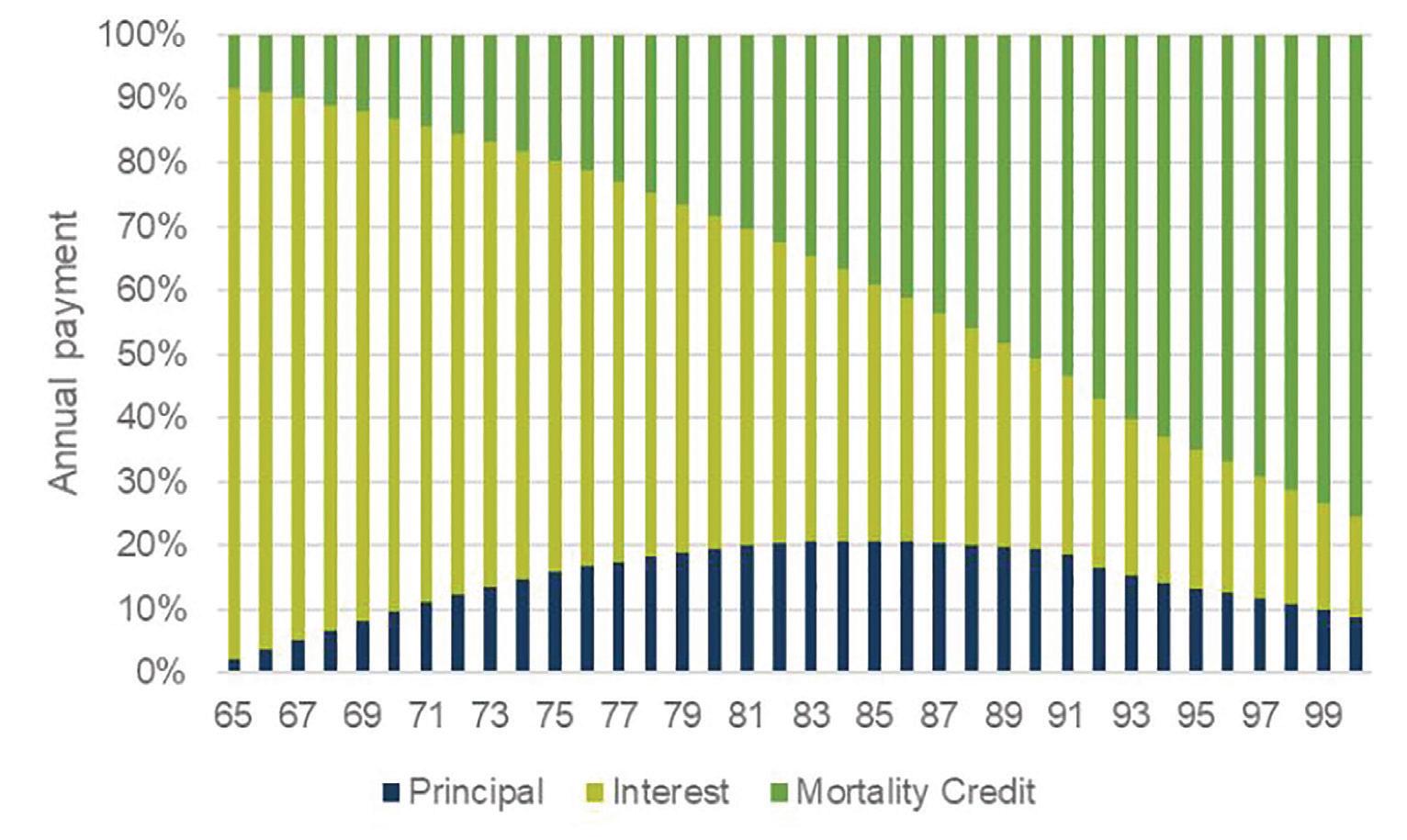

The ABS publish age data on all those who die each year. Looking at older Australians (aged 65 or more), half of those who died in 2016 were age 86 or more. The figure was higher for females with half being over age 88.

Two more decades will pass before those retiring today will reach their mid-80s. By then average life expectancy for a 66-year-old is expected to have increased another two years. Those whose health is better than average (that is, not below average) should anticipate living well beyond these averages.

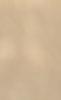

Source: Optimum Pensions

Research being conducted by the Actuaries Institute will show just how much longer healthy Australians are expected to live. These are the retirees without obvious medical problems which will otherwise shorten life expectancies. They live longer than average because the average includes the less healthy retirees.

As an indication, a healthier 65-year-old female today has a 50 per cent chance of dying between age 92 and 110. Taking into account that most retired households have a female member, it’s a fair question to ask – has Australia outlived the ABP?

The 2015 Financial Systems Inquiry recommended legislative changes to allow and incentivise new types of retirement income products to solve this critically important problem for all current and future retirees. This legislation has now passed, and new products are coming onto the market that are designed to maximise retirement income while ensuring that income lasts for life – irrespective of how long the retiree lives. From 1 July 2019, these products will receive highly advantageous treatment under planned Centrelink means testing rules. The options a retiree has for retirement income now include:

1) The ABP – As described above. As you can see the product carries significant risk including the risk of capital running low or savings running out.

(2) A Traditional Lifetime Annuity – For highly risk averse retirees, this product lets you use your super to purchase a guaranteed, fixed annuity income from an insurance company. For example, a $250,000 balance might secure

a lifetime income of $13,500 per annum for a 65-year-old with no spouse. In this scenario the income would increase each year with price inflation but there would be no lump sum benefit upon death. If a death benefit option is chosen, the annuity income would be lower.

(3) A Real Lifetime Pension – This is an investment-linked lifetime income stream that’s guaranteed to last for life but where the payment level is linked to the performance of the professionally-managed investment option you select. It suits retirees with more balanced risk preferences than options (1) or (2). The product allows you to benefit from an exposure to growth assets if you wish but with peace of mind that your income can’t run out later in life. The longevity guarantee is provided by a global reinsurer. It means a 65-year-old can confidently secure an income in retirement that, depending on how long they live, is 20 per cent to 30 per cent higher than the account-based pension minimum (with the same investment choice) – and without the worry of running out of savings if markets perform poorly or they live beyond their life expectancy.

For those impacted by Centrelink means testing, options two and three will also result in a higher Age Pension than option one from 1 July 2019. So, for those retirees wanting a lifestyle that’s higher than the Age Pension there is now a range of options available to deliver the level of financial security they need. This can help retirees proactively enjoy their retirement and remove the fear they only have the option of trying to exist on the available funds an ABP provides.

Jim Hennington is head of innovation for Optimum Pensions and a fellow of the Institute of Actuaries.

The amount of income needed in retirement is both varied and hard to reach. But, as Hannah Wootton finds, there are choices in both structures and investments that providers can make to help members hit their retirement goals.

Australians are living longer but retirement isn’t getting cheaper.

With both the length of time retirement income strategies need to provide for and costs of living increasing, it’s little wonder that Australians aren’t retiring with enough ongoing income secured.

State Street Global Advisors recently found only one in five Australians think all will be well when they retire, with close to 40 per cent of the

workforce thinking they won’t have enough money in retirement.

So how much is needed to retire, why aren’t we hitting it, and what can we do to get there?

While different figures are thrown around as to how much income is needed in retirement, consensus within the industry is that it’s really a case-by-case scenario.

“There’s no single answer, everyone is different,” senior partner at Mercer, David Knox, says.

“It can be impacted by whether you’re in a couple, single, the level of any other savings you have, your health, where your family is located and whether you are a home owner.”

The Association of Superannuation Funds of Australia’s director of research, Ross Clare, says that your expectations of how you will live in retirement are also a factor.

In terms of putting a number on it as reliably as possible, the ASFA Retirement Standard puts the household budget per year for 65-year-olds at $42,764 for singles and $60,264 for couples for a comfortable lifestyle. For those prepared to live more modestly, the Standard is $15,396 and $20,911 less, respectively.

According to Clare, “for the great bulk of the population something around the ASFA comfortable [budget] makes sense”.

Of course, that changes the older you get.

“When we do our numbers in terms of the capital sums you need at retirement, we have people living through until 92 as part of the calculations, and after that we see the active lifestyle as a bit limited, people are off the road, they don’t have a car, but at the same time their healthcare and personal care costs can go up,” Clare says.

ASFA estimates that for those around 85 years old, $40,636 and $56,295 is needed for singles and couples respectively to have a comfortable lifestyle.

General estimations of retirement costs also often don’t factor in that many people want not just income but also capital for any big needs or emergencies.

“The other thing that is worth mentioning,

even when looking at the ASFA retirement standard, is that it assumes that an amount of capital is run down through your retirement. But many retirees … want a rainy-day fund,” Knox says.

This could cover refurbishments, having aides built into the home, cars or health costs that aren’t otherwise covered.

“It’s this idea of wanting a buffer because there’s uncertainty. I’m not sure how long I’m going to live, I don’t know what health costs might arise that aren’t covered by the government or by private health, so I need a buffer. It’s not a bequest or an estate plan, but just a buffer,” Knox says.

“How big should the buffer be? Well it’s an unknown. Again, individual needs and situations impact this.”

Whatever the figure, Australians aren’t securing enough savings to have sufficient income in retirement as we all live longer.

People are also often retiring earlier than expected, meaning that regardless of longevity they may not have enough saved. Investment Trends found that half of retirees say they had to retire earlier than planned, with the top reason being health issues.

According to Clare, only about 20 per cent of people would currently hit the ASFA comfortable Retirement Standard (although that will get up to 50 per cent going forward).

People know they are not entering retirement with enough too. The Investment Trends 2017 Retirement Income Report reports that only 46 per cent of Australians feel prepared for retirement.

Worryingly, insecurity about retirement income is such that State Street Global Advisors

Continued on page 34

Continued from page 33

recently found that almost 50 per cent of Australians anticipate getting a part-time job to make up any shortfall they might have in retirement. Which, of course, begs the question of where they will find these jobs in the current employment market.

So where does the industry go from here?

Superannuation funds, and professionals in the retirement income sector generally, can help by actively providing guidance to consumers.

“Part of the reason why people may feel unprepared for retirement is because many may not know how much they need to retire. Our data shows that there is a relationship between how informed people are about what they need to retire and whether they feel prepared for it,” Investment Trends senior analyst, King Loong Choi, says.

He believes that super funds can play a key role in addressing this. Indeed, Investment Trends found that only 33 per cent of Australians believe they can reach their retirement goals without any professional assistance.

Clare points to income calculators as one means of assisting, as they help people better understand what they will actually need in retirement.

Funds can also guide members in considering what investment approaches best suit them, and companies offering other retirement products such as annuities or income-focused funds can also help.

According to managing director of Optimum Pensions, David Orford, the biggest problem causing insufficient retirement income is that

people simply aren’t saving enough.

State Street Global Advisors’ most recent survey backs this up, finding that the key to solving the problem of not having enough money in retirement is to start saving early.

Orford believes that while products geared toward assisting this weren’t good in the past, they’re improving now. This is especially true for products that specifically address annuity.

Orford says, however, that not enough people know about these options or the importance of saving. Recent legislative changes, for example, make annuities a much more varied and appealing means of securing income regardless of when you live until. Consumers are largely unaware of

this, which is where quality advice and education from providers can assist.

Again, retirement needs’ individual nature comes into play.

“There’s a whole range of things that funds and financial institutions can do to help people, but it still comes down to some individual responsibility,” Clare says.

He points out that the super system has to service pretty much the entire Australian population, making it difficult to tailor it to individuals without them also taking an active role.

“So, you need to do a little bit of homework to ask, well what’s my lifestyle going to be, recognising too that during retirement over 20-30 years, things are not going to be constant. Even expenditure isn’t going to be constant, it’s probably going to reduce gradually,” Knox says.

Australia, of course, already has two core structures in place to help with retirement income. The brunt is borne by the superannuation system, with the Aged Pension theoretically there to provide for those who need it.

The Aged Pension isn’t enough alone – as Clare observes, compared to overseas equivalents it’s pretty ordinary in terms of the retirement income it provides. As a percentage of GDP the Government contributes far less than some international counterparts and both Clare and Knox agree that it enables only a very modest lifestyle.

So it’s the super system then, that must bear the brunt of improving retirement income levels.

“The compulsory system will do quite a bit of the heavy lifting and that will be the base for improving retirement outcomes in the future, and

already the more recently retired are retiring with a lot more than people ten or twenty years before, so the SG is a good start,” Clare says.

He also says the current SG level isn’t enough, joining the cries for it to be raised to 12 per cent. Acknowledging that “we won’t get there for some time”, he says in the meantime, people should make voluntary contributions.

He suggested salary sacrificing or making personal tax-deductible contributions, or even making non-concessional contributions if a person’s concessional cap is fully used, should their financial circumstances allow.

Then there are structures outside the compulsory ones that can help raise retirement income.

Knox points to the development of Comprehensive Income Products for Retirement (CIPR) as a possible remedy to the issues posed by longevity and the need for post-work income.

“They aren’t one-size-fits-all, but it’s a starting point for people to think about what suits them,” he says.

“My hunch is many individuals will say, okay the trustees have recommended this, I’ll just take that, and I can tweak it if I need to. So, I think it will be a nudge that will lead to further discussion.”

Again, in designing the CIPR, trustees will have to look at the average member.

“[The fund] may have a lot of members in the maritime industry, which is different to lots of members who are Qantas pilots, or members who work in the retail sector. Members will then have to work from there, recognising that this is not a one-size-fits-all [solution] and if you have poor health or a big mortgage debt or whatever, your conditions will be different,” Knox says.

Continued from page 35

Knox believes that having more longevityfocused products on the market will also improve retirement income prospects. It means that people will feel more comfortable using more of their retirement savings held through other means when they’re a bit earlier in their retirement, as they would be less concerned about longevity.

Orford points to annuities as one such product. While this is a market Challenger has traditionally dominated in Australia, legislative changes mean that new providers, such as Orford’s Optimum Pensions, can now make a play.

They have been used well in other countries, such as Canada and Switzerland, to provide steady income throughout retirement while mitigating the risk of unexpected longevity leaving you high and dry.

A benefit of the Australian retirement income system, Knox says, is that it can offer a blend of products that provide both access to capital and income. The issue with many European countries’ approaches comparatively is they may compel a product such as annuities but offer no flexibility.

“With a blend, we end up with a system that is better than most countries. It’s just about getting that blend right,” he says.

Regardless of the product, understanding the risks to the underlying capital that generates the income is key to improving the quality of the income produced.

“The issue going forward [for retirement income] is lower total return ... While we’re still getting income technically in payouts, that’s not

the return,” Wheelhouse Partners managing director, Alastair Macleod, says.

With shares very expensive at the moment, hitting a peak that is second only to during the tech bubble, Macleod warns that traditional investments mightn’t cut it for investors of retirement income-focused products.

“If you had a strategy that was generating consistently high income and the capital base wasn’t being eroded, then that’s a good, sustainable source of real return. But we’re still in a low interest rate world, so there aren’t many places that you can generate that,” he says.

“[Schroders] are expecting 1.6 per cent real returns the next seven years for the S&P 500. So if they’re right then, that makes [it] pretty hard to maintain your retirement nest egg if you also need to withdraw five per cent a year to live on. Hence the need for a source of real return, or real income, as opposed to hoping shares will go up.

“Investors need to look for different solutions than what they’ve been doing in the past.”

To improve the value and consistency of retirement income delivered going forward, Macleod says that those investing may need to look at alternative strategies such as private equities or real assets.

“I think that diversifying your source of income, whether it’s from Australian shares, which can benefit from franking credits, or strategies like [Wheelhouse Partners’], which are derivatives-based, or high dividend paying shares offshore, or even in having some annuities as part of the mix, it’s really spreading that risk of retirement income to a variety of sources so that you really get some diversification built into your portfolio.

Anastasia Santoreneos writes that the pre-retiree market might be a honeypot for financial planners, given Investment Trends’ data on misconceptions around retirement income.

Investment Trends’ Retirement Planner report highlights that two-thirds of Australians don’t believe they’ll be able to reach their retirement goals without professional help, exposing a niche market for planners and advisers.

Senior analyst at Investment Trends, King Loong Choi, pointed to a number of figures that highlighted a large misconception among those who haven’t retired yet about how much income they actually needed for retirement.

For example, the Investment Trends Retirement Income report found that pre-retirees thought they needed almost $500,000 to retire, but actual retirees reported they’ve retired with just $300,000.

As well, pre-retirees thought they would get an average monthly income of $2,800, but need $3,300 to retire, while actual retirees report they’ve lived on $2,200 per month.

Choi said only 42 per cent of pre-retirees felt they were well-informed about what they actually needed for retirement, and only onethird felt they could reach their retirement goals without any advice.

“That’s two-thirds of those that haven’t reached retirement yet, that are unsure or do not feel they can reach retirement without any professional help,” he says.

According to the Investment Trends

Retirement Planning report, 84 per cent of preretirees would look to a financial planner for that professional help, and they generally sought access to advice, access to a longevity protection product, and access to a product that can guarantee income for the rest of their life in retirement.

Choi said the pre-retiree market was a key segment for planners given the demand for advice and product knowledge.

When looking at products, planners’ note that the use of annuities has grown significantly in recent years, jumping from 27 per cent in 2012 to 43 per cent in 2017, with expectations to hit 59 per cent next year.

Planners note they primarily recommend annuities for the Centrelink and social security protection they provide as well as the protection against longevity risks.

MyNorth is AMP’s flagship platform and offers a full wrap service to help advisers build their clients’ investment, super and retirement portfolios with over 430 managed funds, managed portfolios, shares, and cash options.

MyNorth has over $38 billion in assets under management and is one of Australia’s fastest growing super and investment platforms. It was also awarded Chant West’s 2017 Advised Product of the Year Award. AMP is committed to keeping MyNorth competitive and contemporary to help your clients confidently reach their retirement goals.

See the advertisement in this guide for more details in the disclaimer.

amp.com.au/mynorth

33 Alfred Street SYDNEY NSW 2000

T: 1800 667 841

Australian Unity is a health, wealth and living organisation providing products and services designed to help people thrive. We have provided healthcare, financial, retirement and living services, for over one million Australians.

Our Wealth platform provides customer-centred solutions that support peace of mind, financial security and help people navigate confidently through lifes’ stages. It includes Australian Unity’s financial planning, investments, life & superannuation, trustee services and property capabilities.

w: australianunity.com.au/wealth p: 1800 649 033

e: investments@australianunity.com.au

Challenger is focused on providing customers with financial security for retirement. We do this by providing customers in the savings (or accumulation) phase with investment strategies exhibiting consistently superior performance, and providing customers in the spending (or retirement) phase with safe and reliable income streams.

As Australia’s largest annuity provider, we provide reliable guaranteed1 incomes to over 60,000 Australian retirees. Annuity products appeal to retirees as they provide security and certainty of guaranteed income in retirement, whilst protecting against market and inflation risks. Our lifetime annuities also protect retirees from the risk of running out of money late in life.

1The word ‘guaranteed’ means payments are guaranteed by Challenger Life Company from the assets of its relevant statutory fund.

At Sunsuper, we know as a financial adviser that you can change people’s lives for the better, and we’re here to help you do that. Talk to us today about partnering with a super fund that has: Dedicated adviser services:

• Ability to request an initial and ongoing adviser fee payments for advice services provided.

• Access to client details 24/7 through our secure Adviser Online portal.

• Indefinite third-party authorities. As well as:

• Industry-leading super and retirement products.

• Lonsec and Morningstar product ratings.

• Wide range of investment options and solid investment performance.

Call us on 13 11 84 or contact the Retail Advice Distribution team at rad@sunsuper.com.au to find out more about partnering with Sunsuper.