The shortage of newly qualified accountants is creating a real talent gap and imbalance in the workforce, according to the latest Reed accountancy and finance salary guide.

Reed’s Alan Myers said this shortage is partly due to disruptions in professional training during the pandemic years, as training contracts were delayed and professionals chose alternative career paths.

It all means there is a surplus of senior professionals, but insufficient entry-level talent to sustain longterm growth. Myers felt that addressing this gap “will require renewed focus on training and development to ensure a robust pipeline of talent for the future”. Firms that prioritise upskilling are more likely to retain their workforce and maintain a competitive edge in the marketplace.

Dr Ian Gregory, CTO at Advancetrack, said that 74% of accounting firms are struggling daily with staff shortages, and 42% of partners are working an additional day every week just to keep their heads above the water. He said the AdvanceTrack

Accounting Talent Index found while three-quarters of firms reported significant staff shortages, some 20% still had no concrete plan to address it.

The real issue, however, is the undergraduate and postgraduate accounting enrolment pipelines.

The Talent Index found that between 2010 and 2023 domestic student enrolments into tertiary accounting programmes declined by an average of 56% across the UK, US (61%), Canada (54%) and Australia (51%).

The Accountancy Talent Index

said: “To call the talent crisis an existential threat is far from a shrill overstatement. Accountants and the accounting profession underpin the trust which sits at the foundation of global capitalism. Without them it is more than possible that the entire system could collapse.”

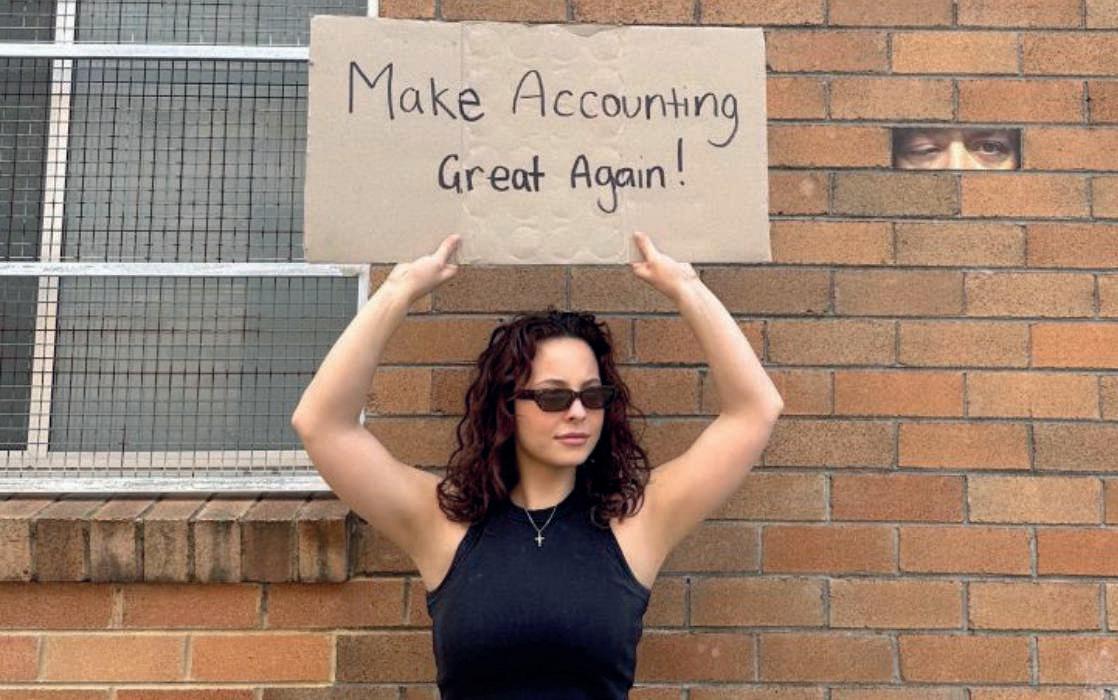

This is a global concern. Joanna Perry (pictured) from Australia recently posted on LinkedIn: “We are facing a massive talent crisis in accounting and nobody is talking about it.”

She feels the reality is we’re

ACCA MARCH EXAM FEEDBACK

The ACCA March exams have finished, so where were the problem papers this time around?

Well, it appears no one liked sitting the tax papers. One in four of those sitting the TX and ATX exams this time around said they had a ‘disaster’, according to the Open Tuition Instant Poll.

One TX sitter described their

exam as ‘just crazy’, another said it was ‘brutal’.

For ATX sitters the exam was ‘quite hard’ and ‘shocking’, all at the same time. What really concerned one sitter was the unusual nature of the exam.

that while the ACCA does not release papers anymore it is almost impossible to work out just how hard papers really are. “I really do think it is time the ACCA released the full papers again,” he ventured.

heading towards a 3.5 million global shortage of accountants in 2025.

This, she stressed, isn’t a staffing problem, it is a business crisis waiting to happen. And, Perry said, it is time to reimagine the entire profession.

She said we need to show young professionals the true scope of modern accounting careers (‘Make Accounting Great Again’).

Perry feels the shortages mean unprecedented opportunities for students. “You won’t just find a job – you will have your pick of roles, industries and work styles.”

As she explained: “The talent crisis in accounting isn't coming – it’s here.” That LinkedIn post already had over 8,000 likes, 879 comments and 748 reports when we saw it.

In the US, former CFO Howard Katzenberg said companies there are raising accountants’ salaries by over 10%. With many struggling to find them he claimed major firms like EY are throwing money at the problem: “EY pledged $1bn to boost salaries,” he said. For him the bottom line is simple: rare skills will equal higher salaries.

AFM and SBR.

At the other end of the scale there were mixed emotions from those sitting the SBL exam, but with an ‘OK’ rating of 63% in the Open Tuition Instant Poll, most sitters thought the exam was ‘alright’. One sitter even said: “I thought it was quite a good paper.”

AA was deemed another ‘easier’ paper this time around.

A leading tutor told PQ magazine

The other papers that student admitted they struggled with were

Check out page 17 for all the feedback.

TAKE YOUR PLACE AT THE FOREFRONT OF ACCOUNTANCY AND FINANCE

IN THIS ISSUE

A note from the Editor

It has been another busy month at PQ Towers. I have been out and about talking all things AI at Northeastern University London’s apprenticeship event, and was billed as a ‘special guest’ at Queen Mary University’s sustainability talk!

Then it was off to our joint roundtable with Rogo to talk all about the growing importance of those ‘soft skills’. You can now watch the roundtable discussion at https://getrogo.com/pqwebinars/.

Then there was a little matter of the PQ magazine awards. We have found a fab venue – Salsa Temple (read more about that on page 4), and we had to deal with over 3,000 entries. In fact they broke our email system, and we have to apologise for that. We received all the entries, but the email system didn’t like being so overworked.

Hopefully, we will see all those shortlisted on awards night, which is 28 April this year. You will need to keep watching our website for a first look at who made that shortlist.

In the news this month we take a look at the ACCA March exams, PwC Israel being fined over exam cheating, and worrying stats about university student’s anxiety and depression.

We have some great features, too. You can read all about the CASSL ball, what will be occurring at Accountex this year and FRC’s Going Concern changes.

Graham Hambly, Editor and Publisher, PQ magazine

4 Bupa anxiety survey

One in 10 university students say they feel ‘constantly anxious’, poll finds

6 PwC exam cheats

PwC Israel sanctioned by US regulator over cheating in internal exams

8 International standards

IASB issues major update to IFRS for SMEs

9 Audit in crisis

Two-thirds of audit professionals want to leave their position in the next year

10 NAO report

Local government finances are becoming unsustainable, says National Audit Office

12 Tech news

Why there’s no functioning finance system at Birmingham City Council

Features, etc

14 Have your say

Where are the stats on diversity when it comes of pass rates?; ACCA needs to sort out exam hall tech issues; and in praise of Mark Foley. Plus our social media round-up

17 ACCA exam feedback

What did those actually sitting the March exams think of them?

18 CIMA spotlight

Why creating the right environment for your CGMA exams is vital

20 New FRC guidance

FRC has provided an ‘explainer’ on its update to going concern reporting

21 ACCA spotlight

Celebrating International Women’s Day

22 A question for Tom Tom Clendon explains how an organisation should account for finance raised via crowdfunding

23 AAT exams

Everything you need to know about tax points, relevant to the level 3 Tax Processes for Business unit

24 You shall go to the ball! CASSL travels back to the ‘Roaring Twenties’ for a night of fun and frolics

25 Study tips

Rob Sowerby believes by keeping it simple you can pass even the hardest accountancy exams

26 An ethical dilemma

When it comes to disclosing personal information, what can (and can’t) you do?

27 Risk management

We explain what is meant by risk and risk management in a business scenario

28 Accountex 2025 PQ magazine to partner accountancy’s leading expo, which takes place in London in May

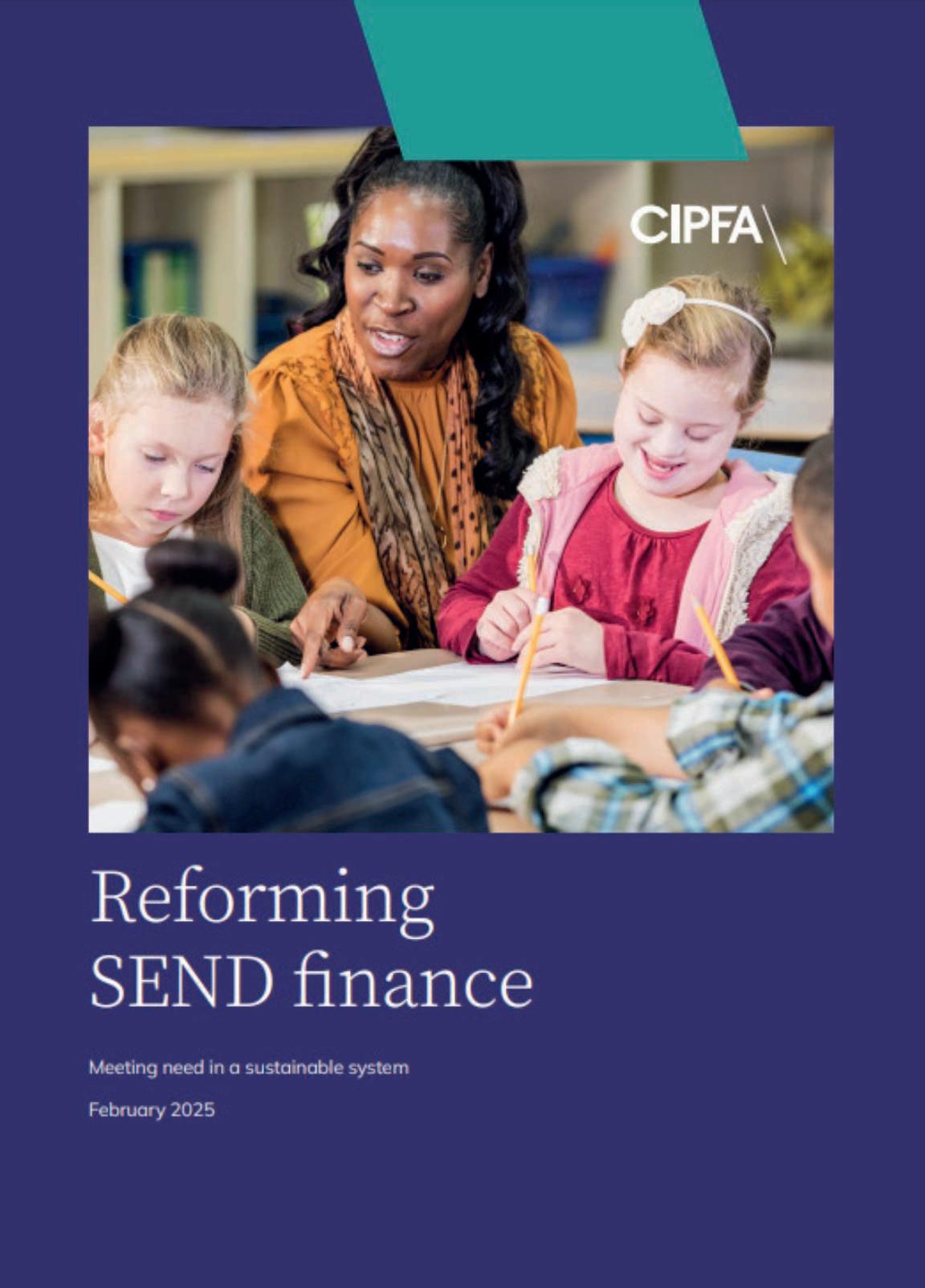

30 CIPFA spotlight

How the institute’s reforms can fix the SEND system, which is reaching crisis point

32 Your career

Four practical tips for overcoming anxiety and succeeding in your job search

33 QuickBooks expo

Software giant uses London Get Connected event to announce major product updates

34 IFA spotlight

The key challenges and opportunities that lie ahead

35 Careers

Guidance and education is lacking when it comes to GenAI, survey finds; more great advice from our Agony Aunt; and PQ’s Book Club review

36 Fun

The lighter side of life – and accountancy

The columnists

Lisa Nelson Why ethics must be a central tenet throughout your career4

Robert Bruce Trump’s ESG stance is leaving US isolated 6

Prem Sikka Who benefits when an individual buys shares? 8

Anna Kate Phelan Exam assessment must reflect evolving tech 10

Hannah MacDonald Advocating for highly ethical workplace cultures 12

LISA NELSON

Why ethics must be central to your career

Ethics isn’t just a theoretical topic in your accountancy qualification: it’s the living, breathing heart of our profession. It is one of few topics in your qualification that will be highly relevant no matter what level of seniority you are, the job role you are in or the stage of your career. It’s tempting to think you will only need to address ethical issues once you’re more senior, but the truth is that ethical decisions are made at every level, every day.

In the Carillion case, the respondents to the case included an assistant audit manager who, at the time of the events, was a part qualified accountant. Ethical responsibility isn’t just for those at the top. Even as a more junior accountant or auditor you have a duty to uphold professional standards. It’s about developing your ability to think independently, to question assumptions and to speak up when something doesn’t feel right. So remember, when studying ethics it isn’t just about memorising rules to pass an exam; it’s about building a strong moral compass. Sometimes doing the right thing means challenging the status quo, even if it’s uncomfortable. Your career in accountancy isn’t just about numbers; it’s about building trust.

Kaplan

CIMA study support

CIMA has reminded its students they are not alone with their CCMA study. Remember, the CGMA Study Support Diagnostic tool offers personalised support services and answers the 10 issues candidates battle with most.

Maybe you are struggling to recall the knowledge, or don’t feel supported and don’t know who to ask for help? Well, CIMA will point you in the right direction.

And if you need more then you can opt to get some one-to-one

Students battling anxiety

One in 10 university students say they feel ‘constantly anxious’ because of exam stress, money concerns and the difficulty of juggling social life and study.

A Bupa poll of 1,000 current and past students found nearly half (43%) were consistently experiencing anxiety during their academic journey. A dread of failing, social integration issues and the daunting pressures surrounding life after graduation all add to that anxiety.

A staggering 55% confessed to having moments where they doubted their educational future and contemplated quitting their

Time to Salsa!

We can finally do the big reveal, and tell you where we are holding the 2025 PQ magazine awards night. This year’s celebration of everything good in accountancy education will be taking place at Salsa Temple, which is located on London’s Embankment, right next to the River Thames.

Our independent judges now have all your entries and will whittle these down to our final

courses. The survey found first and final years were particularly stressful for students, with the second term deemed most

shortlist. If you make the shortlist then you will be invited to our 22nd awards night.

We can reveal that we had a record number of entries this year – they came in in their thousands. Although, sadly, some entrants didn’t read the application process – we needed more than a ‘they are the best’ to get on the shortlist.

difficulty, because that is when the reality of student life hit.

Bupa’s Medical Director, Dr Naveen Puri, said: “Many think students have it easy – and say it is the best time of your life – but it can be a very stressful and worrying time for those who may be feeling anxious about how to deal with their course, manage finances or simply be away from home.”

Coinciding with Bupa’s launch of its new health subscription service, the research emphasises the critical need for students to have accessible mental health and medical care.

We will unveil the full shortlist in next month’s issue, but watch our website because it will appear there first – www.pqmagazine. com

The rise of ‘soft skills’

Having technical skills are vital, but if you don’t have the professional skills you are not going to make it as a professional accountant, explained ICAEW’s Helen Powling at our recent roundtable event.

The ‘Accountants… time to power up your employability skill’ roundtable looked at the rise and rise of the demand for accountants with ‘soft skills’, and ACCA’s Jamie Lyon said developing your networking skills and personal

support, too. Go to https://bit.ly/3QqS0aM

Need the right course?

If you are looking to move quickly from PQ to NQ then you need to choose a top training provider. But which one? Well, you need to check out our Course Finder page at https://tinyurl.com/2ebtwxau

Select who you want to study with and you will see our trusted providers.

We have nine trainers on the AAT

relationship are also key to a successful career.

The roundtable went out live,

list, including HTFT Partnership, Ideal Schools, e-Careers, Training Link and Premier Training. We know if you choose any one of these you will get a first-class service and be one step nearer your goal of becoming a qualified accountant.

Back to Basics – our free videos

We have fours videos in our Back to Basics series 2, with more coming soon!

Three-time PQ magazine award winner Tom Clendon has provided

and there was a whole T Level class from Stanmore College watching. You can watch the whole event too, at https://getrogo.com/ pqwebinares/

So big thanks to our panellists: Daniel Cornes, senior business manager at Reed Finance; Hazel Powling, ICAEW Head of Qualifications Development; Jamie Lyon, Head of Skills, Sectors & Technology at ACCA; and Jonathan Barber, Executive Director –UK at the Institute of Financial Accountants.

Read more in next month’s issue.

an eight-minute video looking at IAS 37 and provisions. IAS 37 is a strict about when you can recognise a provision. So, do you know, for instance, the three conditions which must be met? You will after watching Tom – go to https://tinyurl.com/2xx5p4u4

We also have PQ magazine award-winner Will Boardman looking at the VAT control account. With his help you will understand what goes on the credit side and what goes on the debit side, and all in under eight minutes.

Lisa Nelson is Director of Learning at

ROBERT BRUCE

Trump’s ESG stance is leaving US isolated

It is puzzling. The great divide over environmental, social and governance disclosures (ESG) is seen, particularly in the US, as a geographical divide. In the US, where Donald Trump is bullying companies into dropping any mention of ESG measures, it is portrayed as something that effete European countries implement, whereas the good old Trumpian US economy, harking back to the 1950s, should not.

But the truth of the matter, as the isolated and furious US fails to see, is that the divide is not simply US versus Europe. It is the US versus the world. Companies in Asia, where the real economic powerhouses lie, think that ESG issues are common sense. Increasingly, European companies are following suit. The big boys in US asset management, BlackRock amongst them, have decided that despite having supported ESG measures and advocated for them are dropping them, hoping to keep in the good books of an increasingly irrational president.

In Europe this makes no sense. As a result, for example, in February one of the largest UK pension funds pulled £28bn of funds out of giant US asset manager State Street. And it makes even less sense across the largest Asian economies where the importance of ESG measures, particularly in combatting climate change, is seen as common sense. The US is once again being left behind, squabbling amongst itself in its own back yard.

Robert Bruce is an award-winning writer on accountancy for The Times

FRC investigating Woking council

The Financial Reporting Council (FRC) has started an investigation into the conduct of two accountants “in relation to their compliance with governance, reporting regulations and professional standards in respect of Woking Borough Council’s operations and investment activities”.

The FRC’s Executive Counsel will be looking at the financial years ended 31 March 2017 to 31 March

PwC Israel fined over exam cheating

PwC Israel has been sanctioned and fined by the US regulator over widespread cheating in internal audit exams.

The Public Company Accounting Oversight Board (PCAOB) has fined the firm $2.75m after it was found hundreds of individuals were engaged in training exam misconduct. The PCAOB said from 2017 to 2022 the firm failed to detect or prevent extensive, improper sharing of tests for mandatory internal training courses.

PCAOB chair Erica Y. Williams

said: “The PCAOB will not tolerate cheating or other unethical behaviour at PCAOB-registered audit firms, regardless of whether the firm is located in the United States or abroad.

“We will hold firms accountable

A top five online careers magazine is… PQ!

Where do you get your career advice from? Well, it should be one of the top five best career magazines – PQ magazine!

PQ magazine has been placed at number four in FeedSpot’s top 10 career magazines in 2025.

The list is complied from thousands of magazine on the

web and is ranked by relevancy, authority, social media followers and freshness.

Last month we discovered we were number 11 on the FeedSpot list of top

when they put investors at risk by failing to comply with the PCAOB’s quality control standards.”

Since 2021, the PCAOB has sanctioned 10 registered firms for quality control deficiencies related to the inappropriate sharing of answers on internal training exams.

Without admitting or denying the findings in the order concerning the improper answer sharing, PwC Israel agreed to pay a $2.75 million penalty. The firm was censured by the PCAOB, and it is required to review and improve its quality control policies and procedures.

accountancy magazines to read.

PQ magazine editor Graham Hambly said: “Our career advice section on www.pqmagazine.com/ career-advice/ reveals the real working world of accountants. Recent posts have talked about AI, finance staff shortages and cheating employees, among other things.”

Check out the full list at Top 10 Career Magazines in 2025

The OBU BSc deadline looms

ACCA students only have a limited amount of time to complete the BSc (Hons) in Applied Accounting from Oxford Brookes University before the programme closure deadline.

All students and members must submit all

2023. Both individuals are no longer employed by Woking council. This is an Accountancy Scheme investigation, so it covers members of ICAEW, CIMA, CIPFA, ICAI, ACCA, and ICAS.

Book your tickets to Accountex

PQ magazine is again partnering with Accountex, which takes place over two days in May. Accountex is the premier accounting expo and you can register online for your free ticket now.

requirements for the programme by May 2026.

And May 2026 is the final opportunity to register and submit the Research and Analysis Project (RAP). It is

Accountex London have just announced that Charterpath will be an official charity partner. To book your ticket for 14-15 May go to https://tinyurl. com/533s6pb7

AI and professional judgement

Accounting professionals have a vital role to play in supporting their organisations to achieve AI adoption and implementation, according to new research from ACCA.

also the final opportunity for RAP resubmissions for RAPS submitted prior to May 2026. Any individuals who fail the RAP at the May 2026 submission will have one opportunity for resubmission in November 2026. December 2026 sees the closure of the BSc programme. ACCA said: “Anyone registered on the programme who has yet to meet the assessment criteria will no longer be able to achieve the BSc.”

However, according to the report AI Monitor: Risk and responsibility there are a couple of immediate threats for many organisations relate to the significant amounts of investment being committed and either unrealistic expectations or poor judgement concerning the potential impact of integration. ACCA believes success will come through combining traditional financial acumen with new forms of technological oversight to maintain the profession’s fundamental role as arbiters of trust and integrity.

The UK government wants more people to own shares. Do people have the capacity to buy shares? Around 66% of adults have less than £10,000 in savings. Would people gamble that on shares?

Despite incentives, such as taxing capital gains and dividends at lower rates than wages, only 10.8% of UK quote company shares are held by individuals.

Neoliberals claim that wider share ownership will lead to more investment in the economy. That isn’t necessarily so. Shares traded on stock markets are secondary. Individual A buys shares and bonds from B, money is exchanged between A to B, and not a penny goes to the company for investment in productive assets.

Shareholders manage uncertainly by chasing short-term returns. In 1970, major UK firms paid out about £10 of £100 of profits in dividends. By 2015 this hit £70, and the ratio could be higher now. Cash extraction is accompanied by a squeeze on labour and investment.

Stock market pressures are destroying the nation’s seed corn. In 2024, UK listed companies raised £3.4bn from new shares. They paid £86.5bn in dividends. The UK is ranked 28th out of 31 OECD countries for investment in productive assets. Share ownership does not shelter anyone from the ravages of capitalism. They will still face real wage cuts and rocketing bills. To encourage share ownership, governments need to rethink the relationship between capital and society.

Prem Sikka is Emeritus Professor of Accounting at the University of Essex

Tax briefs

Croner-i and KPMG join forces on tax

KPMG and Croner-i have created an alliance on tax content driven by AI.

Under the agreement Croner-i’s tax information will be integrated into KPMG’s information services. This will mean all KPMG’s UK employees will have instant access to the latest tax legislation, case reports, expert analysis and insight enhanced by AI search tools.

Ben Chaplin, MD at Croner-i, said: “Not only is the alliance

IASB issues major update to IFRS for SMEs

The International Standards Board (IASB) has issued a major update to the IFRS for SMEs accounting standard.

The aim of the standard is to balance the needs of lenders and other users of SMEs’ financial statements with the resources available to SMEs.

The standard defines SMEs as entities without public accountability that prepare general purpose financial statements.

Highlights of the update include:

• A revised model for revenue recognition.

• Bringing together the requirements for fair value measurement in a single location.

said: “The update to the IFRS for SMEs Accounting Standard will improve the information provided to users of SMEs’ financial statements while maintaining the simplicity of the Standard.”

• Updating the requirements for business combinations, consolidations, and financial instruments.

IASB chair Andreas Barckow

The changes are effective for annual periods beginning on or after 1 January 2027, with early application permitted.

The IFRS for SMEs Accounting Standard was issued in 2009 to address the global demand for a simplified Accounting Standard for SMEs. This updated version is the third edition of the Standard.

ACCA worried about FRC move on sustainability

ACCA has warned the Financial Reporting Council (FRC) that now is not the time to “row back on UK investor governance commitments on sustainability”.

It appears worried that the FRC’s proposed revised definition of ‘stewardship’ could be interpreted as a scaling back of intent on sustainability.

FRC wants to remove ‘environment’ from the proposed definition, and ACCA’s Mike Suffield (pictured), said: “Climate-related

disclosures continue to mature globally, shifting from tick-box statements to demonstrable action. This is reflected in recent

regulatory developments, such as the International Sustainability Standards Board (ISSB) IFRS S1 and S2.

“In the light of these trends, we are concerned about the message that this proposed change would send to the market.”

Despite this criticism, ACCA stressed it was supportive of the overall proposed updating of the Stewardship Code, and supports FRC’s efforts to bring about a more streamlined approach to reporting.

Hanni Owens wins community award

AAT Hanni Dogan Owens recently picked up a South Gloucestershire Community Award. The 2022 PQ magazine Distance Learning Student of the Year has not rested on her laurels!

She has worked in unpaid volunteer roles for many groups, including Anthony Nolan Leukaemia Research, Southmead Hospital, UWE Beeline Project – and many more. Owens was described as “cheerful no matter

fantastic for the growth of both Croner-i and KPMG, it is also the start of a wider, exciting journey for the ways content will be used in the future. We believe there is currently no other alliance like this in the UK tax market, and the potential for further growth across the industry is compelling.”

HMRC costs are up

An increasingly complex tax system, more people paying tax and investment in staff and IT contributed to HMRC’s costs of

the weather or the work, and happy to give her all to everything she supports”. Her genuine empathy shines through, too.

She told PQ magazine that there are so many great ways to volunteer, not just to maintain your finance skills, but to improve your wellbeing and experience.

She wants to encourage all our readers to check out Reach Volunteering: https://reachvolunterring.org.uk

collecting tax rising by 15% (to £563 million) in real terms between 2019-20 and 2023-24, according to a new National Audit Office (NAO) report.

During this same period, government’s tax yield rose by 16% (to £113 billion) in real terms.

The increase in administrative costs can be attributed to several factors. First, the tax system is becoming increasingly complex, and HMRC has estimated that the combined effect of changes announced between 2022 and 2024

will increase its costs cumulatively by around £875 million over the next few years. None of these changes are expected to reduce costs, although it is anticipated that some of them will increase revenue in the longer term.

Second, the number of people liable to pay income tax has increased from 31.7 million in 2020-21 to 36.2 million in 202324, due to income tax thresholds remaining at the same level since April 2022, and population and employment growth.

Councillor Franklin-Owusu-Antwi presented Hanni Owens with her community award

Students celebrate ADIT exam success

Almost 400 international tax professionals recently celebrated passing exams towards the Chartered Institute of Taxation’s ADIT (Advanced Diploma in International Taxation) qualification.

Online exams took place in December, with 396 students successfully passing at least one exam and 86 achieving ADIT in

full by passing a third ADIT module.

An additional 10 students have attained the ADIT qualification in the past six months, by researching and writing a successful extended essay on an international tax subject of academic interest.

CIOT President Charlotte Barbour (pictured) said:

“May I encourage all our new

Auditors getting itchy feet!

Employers take note – around two-thirds (69%) of audit and governance professionals want to leave their position in the next year.

Research carried out by CareersinAudit.com has discovered the main reason for people looking to move was the lack of promotion and pay rises in their current role.

And the data showed it was experienced professionals who appear to be driving this trend,

with 60% of professionals aged 41 and over planning to move in the next six months, compared with 43% of 26-40-year-olds.

CareersinAudit.com

director Simon Wright said:

“The fact that the majority of professionals in audit and governance industries will be looking for new roles in the near future should be a huge concern for employers across the sectors.

“As with any industry, keeping

graduates to join our popular International Tax Affiliate programme, and to continue your relationship with the CIOT. This offers a valuable way to enhance your professional profile and distinguish yourself in a competitive market. As an ADIT Affiliate, you can connect with a global community of like-minded international tax professionals, as well as gaining access to resources and opportunities for further learning and development.”

employees motivated and happy in their roles is crucial to retaining top talent, and also attracting new people to join.

“Regular one-to-ones and performance reviews, providing clear career progression paths and incentivising employees with additional benefits including work-life-balance and homeworking options, as well as regular pay increases, are just some of the areas that should be implemented to prevent professionals from seeking pastures new.”

New chair for Access Accountancy Access

Accountancy has appointed Mark Pavlides (pictured) as its new chair.

In his new role Pavlides will work with accountancy firms to ensure that everyone has an equal chance of accessing and progressing within accountancy based on merit, not background.

Pavlides is currently ICAEW interim MD, Operations, and he replaces Sharron Gunn who left Access Accountancy in November 2024. He said: “Access Accountancy plays a vital role in ensuring that talented young people, regardless of their background, have a fair chance to build a career in accountancy. There’s still a lot of work to do in improving social mobility in the profession, and I’m looking forward to working with the trustees, signatories and wider stakeholders to drive meaningful progress.”

ANNA KATE PHELAN

Keeping pace with real-world changes

In an industry driven by precision, compliance and evolving regulations, the way we assess accountancy students must keep pace. The shift from paper-based exams to e-assessment is not merely a technological upgrade; it is a fundamental change that enhances learning, efficiency and real-world applicability.

E-assessment for learning includes online quizzes, automated tests and interactive case studies, which can provide immediate feedback. For learners, this means errors can be identified and corrected in real time. In a field where accuracy is paramount, this immediacy significantly improves retention and application of knowledge.

Another key benefit is flexibility. Online assessments allow students and professionals to test their skills anytime, anywhere. This adaptability is particularly relevant in today’s hybrid learning environments, where self-paced study and remote learning are becoming the norm.

From a regulatory standpoint, e-assessments ensure integrity and consistency in marking. Automated grading reduces bias, while built-in security measures, such as remote invigilation and plagiarism detection, uphold examination standards. For professional bodies, this means greater confidence in the certification of accountants.

As accountancy continues its digital transformation, learning and assessment must follow suit. E-assessment not only enhances knowledge retention and accessibility but also ensures that future accountants are equipped with the digital proficiency the profession now demands.

Local authority finances in crisis

Local government finances are becoming unsustainable, due to increasing demand on essential frontline services, the impact of delayed finance reform and the erosion of investment in preventative programmes, says a report from the National Audit Office (NAO).

While funding to local authorities, available through Local Government Finance, increased by 4% between 2015-16 and 2023-24 to £55.7 billion, it was not reflected in funding per person during the same period, which fell by 1%.

Nor has the funding kept pace

with the demand for services to people most in need of support, mainly adult and children’s social care, temporary accommodation and the special educational needs and disabilities (SEND) system, which has increased over and

Class of ’25 anyone?

There is still time (just) for SCS CIMA students to register for the Class of ’25 (season one).

Registration closes on 21 March and CIMA says no late entrants will be able to participate in the programme. Registration closed for MCS on 14 March and 7 March for OCS.

All those signed up receive a structured programme of study and exam support containing

more than 15 hours of support material, including online study guide, recorded webcasts and articles, and dedicated one-to-one support. There is also a dedicated Facebook group, providing PQs with the opportunity to network and learn from their peers. It really is worth signing up. Some 94% of candidates from the Class of ’24 said the programme contributed positively towards

ICAS partners with MoD

Military personnel have the opportunity to enhance their skills and career prospects through a new partnership with the Institute of Chartered Accountants of Scotland (ICAS).

Learning Credits Scheme – an initiative that promotes lifelong learning for armed forces members and veterans.

above population growth. Over half (58%) of the £72.8 billion spent by local government in 2023-24 was on adult and children’s social care. Evidence suggests that when people access services their needs are not being well met.

CIPFA said: “The report recognises the current financial crisis impacting local government, that CIPFA has been calling out for years. We welcome and support the report’s findings that current reforms must be considered holistically, not piecemeal to succeed in the light of current capacity and budget constraints.”

Case Study Success. And, remember, the CIMA’s Class of ’21 won a PQ magazine award.

Check out more and the full terms and conditions at https://tinyurl.com/jd62f4d3

their current function or previous experience.

ICAS CEO, Bruce Cartwright (pictured), said: “It’s vital that military personnel have access to learning opportunities that empower and enable them to pursue new career paths.

The Ministry of Defence (MoD) has officially approved the ICAS Certificate in Accounting and Business (CAB) on its Enhanced

EY facing FRC scrutiny over Post Office audits

The UK’s accounting watchdog has confirmed that it is scrutinising audits that fell outside the scope of the public inquiry into the Post Office Horizon scandal, says news agency Bloomberg.

The Financial Reporting Council said in an emailed statement it was looking at the work of EY, who audited the Post Office from 1986 to 2018. Bloomberg said the FRC did not say if it was looking at PwC as well.

Although at the time EY said it was co-operating with the public inquiry, in the end the audits related to the scandal were not

The CAB qualification has been designed to develop knowledge and practical experience in key areas of accountancy, business and finance. It has been designed to upskill any individual or team, no matter what

looked at. It has been suggested that scrutiny of the audits was dropped because it would take too long.

Azets buys part of KPMG Sweden

Azets has agreed to acquire part of KPMG’s Sweden business. It is buying the arm which focuses on audit, tax and advisory services for SMEs, along with the audit and audit-related services for municipalities and regions.

A total of 270 new staff members, including 14 equity partners, will join Azets on completion of the deal, doubling the size of its Swedish business to SEK 1 billion (£77 million). The transaction is expected to be completed in summer 2025.

“With no prior business or accountancy knowledge required, our CAB programme caters to all. It not only upskills individuals, but also boosts their confidence, helps them gain credibility in a variety of sectors, and enables them to stand out in a competitive job market.”

This is Azets’ first agreement in the Nordic counties, and underpins its strategy to become a £1 billion turnover business by 2027.

Deloitte UK keeping DEI targets

Deloitte UK has said it will continue with its commitment to diversity target, irrespective of what its US business does.

Deloitte US looks set to scrap diversity, equity, and inclusion (DEI) goals, as the current climate in the United States changes.

Deloitte ‘s Richard Houston told the UK staff the Big 4 firm was “committed to our diversity goals” and “will continue to report annually on our progress on inclusion”.

Anna Kate Phelan is Head of Product at Eintech

HANNAH MACDONALD

Ethics is about all of us

Ethics is embedded in all accountancy qualifications. It’s fundamental that we as accountants uphold public trust in the profession, are dependable business advisors and support the economy to function effectively.

However, there is a known conflict between revenue maximisation and ethical conduct. I’ve seen this conflict manifest in various ways: onboarding clients who don’t align with the values of the organisation, under-resourcing projects to the point where long hours are normalised and quality issues arise, unprofessional behaviour and even discrimination.

At Accountancy Hub, we advocate for highly ethical workplace cultures. We strive for progress across the industry, calling on regulators to take tough action on individuals and organisations who aren’t demonstrating robust ethical principles.

More generally, newspaper articles highlighting poor workplace culture can often allude to ‘bad apples’ who have brought an organisation into disrepute. However, as Alison Taylor points out in her book Higher Ground: How Business Can Do the Right Thing in a Turbulent World, the point of the ‘bad apple’ metaphor is that bad apples spoil the barrel. Toxic behaviour is systemic, endemic, and the responsibility of every leader to root out.

I’m a believer that ethics needs to be more holistically embedded into accountancy training, not as a tickbox, but as a way of living, working and being. Let’s not shy away from the conversation to ensure accountants are at the pinnacle of ethical behaviour.

Hub

QuickBooks’ major product updates

Intuit Quickbooks has revealed a series of updates at its London Get Connected show, designed to help accounting professionals manage and grow their practices. These include advancements in QuickBooks Online, spotlighting readiness for MTD for Income Tax to help customers stay ahead of compliance, and new innovations in QuickBooks Online Advanced specifically designed for small and mid-market businesses. The latest

IT fiasco exposed in new report

Birmingham City Council has been left without a functioning finance system until at least 2026, according to a 66-page report from external auditors Grant Thornton.

The report into the failed Oracle Fusion enterprise resource planning (ERP) implementation at the council said the overall cost to put things right will be £90m in excess of the original budget.

It all means that the council has not had a proper financial management and cash receipts system for more than two years. It has also been unable to produce reliable financial reports and account for income and spending.

The failures in turn contributed to the council’s de facto bankruptcy in 2023.

Grant Thornton said when the decision to go live was taken in April

Fintech investment hits four-year low

Total UK fintech investment dropped to $9.9 billion in 2024, down 27% from $13.6 billion in 2023, according to KPMG’s Pulse of Fintech, a bi-annual report on fintech investment trends.

Geopolitical uncertainty, high levels of inflation and the higher interest rate environment all

contributed to more subdued levels of UK fintech investment, compared with the record highs in 2021. UK fintech investment in 2024 was at its lowest level since 2020 ($7.6 billion).

KPMG’s Hannah Dobson said: “2024 was another tough year for fintech investment, which inevitably has led to

2022 “the level of risk inherent in the Oracle solution was not properly understood. This resulted in the implementation failing at a significant cost to the council, contributing to a breakdown of financial control such that it has been unable to adequately control its finances throughout 2022/23, 2023/24 and into 2024/25.”

It added: “The governance and programme management for the Oracle programme had fundamental weaknesses that were never effectively reminded and were further exposed by high turnover of staff in both senior and operational roles.”

some business failure and some consolidation. It has also sharpened the focus on a path to profit and cost control which positively leads to more sustainable saleable businesses in the longer term.”

UK can be a world leader in AI

The UK can be one of the top three world leaders on artificial intelligence and the government’s AI strategy is a step in the right direction, says Sam Robinson (pictured), AI policy lead and senior researcher at the Social Market Foundation.

Although the UK can’t compete at the same level as the US or China, he believes it

updates to Intuit Assist were also showcased, bringing more of the power of Intuit’s AI platform to UK customers.

For more see page 33

Dext partners with Scope Solutions

Dext has announced a new strategic partnership with Scope Solutions, to bring its automation and financial management capabilities across the UAE, Cyprus and Malta. This follows the successful integration of Dext with

has the talent, universities and the start-ups to succeed. Robinson said perhaps the

Zoho Books, and reflects the increasing demand for advanced bookkeeping solutions across all three markets.

Sabby Gill, CEO of Dext, said: “Partnering with Scope Solutions allows us to better meet the growing demand for digital bookkeeping and compliance solutions across the Middle East and Europe. Following the integration with Zoho Books, this partnership enables us to deliver even greater value by pairing automation-driven tools with local

biggest opportunity for the UK is to establish itself as an AI leader in the public sector. He explained: “The UK is uniquely well placed to demonstrate how AI can improve the productivity and quality of public services, and Technology Secretary Peter Kyle is building a reputation for the UK as the country that is most ready and willing to seize the opportunity.”

expertise to empower firms to save time, drive growth and deliver superior client service.”

FreeAgent and Mimo team up

FreeAgent and global payment solutions company Mimo have unveiled a new partnership that will enable SMEs to manage their payments, cash flows and financing more effectively. Under the partnership FreeAgent will integrate with Mimo’s platform, saving customers time and money.

Hannah Macdonald is the founder of Accountancy

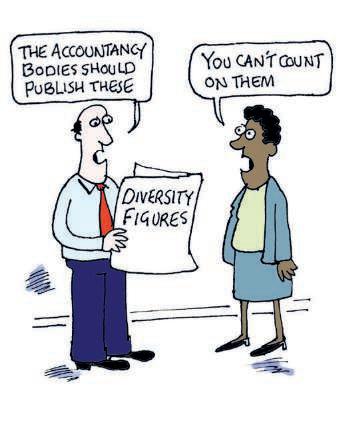

Making diversity work for all

I was shocked to read about the Solicitors Qualifying Examination (SQE) and the diversity pass rates (PQ magazine, March ’25, page 8). White students had a pass rate of 58%, Asian students achieved a 42% pass rate and black trainees only managed a 28% pass rate.

It all seems quite scandalous, but whatever you think of the different pass rates and reason for them, at least they are all out there in the open.

It is interesting that no accountancy body seems to collect similar stats. And the obvious question is why not, if they really believe in equality?

Tech issues persist

I have just sat the March APM exams, and there are still problems with the tech! My computer froze twice and I had to be relocated twice. I wasn’t alone either, as I saw a lot of hands go up in my exam centre.

I do wish the ACCA would come clean about all this, and explain how it all works when things don’t work properly. I understand that things do go wrong and just think if we all know how it works it would take a bit of the stress away. Name and email address supplied The Editor says: I would love to hear from anyone else who had problems in the exam centre this March. We can then take it to ACCA…

Conquering exam fears

Can I say how much I liked Mark Foley’s piece on ‘how to conquer your exam fear’ (PQ magazine, March '25, page 19).

It was nice to read an honest piece that says it is sometimes OK to put off your exams altogether. Many of us are balancing work, family commitments, physical and mental health, all on top of our studies. It really does sometimes get a bit too much. And you should

the Financial Reporting Council collects? Maybe it is something PQ magazine could campaign for to start with.

My worry is that this is too radical a step for the profession. I don’t think I have ever seen a breakdown of the ethnicity of students coming into the profession. Is this something

I always feel the accountancy bodies don’t really provide enough of a breakdown of pass rates, even without taking this next step. I see (again only in PQ magazine) that the ICAEW and AAT have suddenly started to publish European verses Rest of the World pass rates. Why haven’t the other bodies, like mine (the ACCA), followed suit? Is it because they would show massive disparities in pass rates? Name and email address supplied The Editor says: Thanks for the email. Leave it with us and I will ask the question.

Our star letter writer wins a fantastic ‘I love PQ’ mug!

be able to take a step back from it all without feeling guilty.

He stresses the importance of self-care – I also use his personal option of Cadbury’s chocolate bars to keep me going. And will be forever in their debt!

Robert Bruce, Prem Sikka,

I also liked the fact that Foley talks about the concept of ‘peaking’ at exam time. As he says, you have to remember, you don’t need to perform to the best of your ability, just enough to get a pass.

Name and email address supplied

Paul Goodman, a specialist in commercial finance solutions, recently highlighted on LinkedIn what happens when you have the wrong tax policies: “The UK is currently providing a real-world case study of the Laffer Curve – the economic principle that beyond a certain point, higher tax rates can lead to lower overall revenue by discouraging economic activity.

Three recent tax policies seem to demonstrate this:

• North Sea oil and gas taxation: A 78% tax on profits, combined with the removal of key tax allowances, has led to a forecasted collapse in investment. Capital spending in the sector is projected to plummet from £14 billion to £2.3 billion between 2025 and 2029, potentially reducing the UK’s economic value by £13 billion. The unintended consequence? A tax designed to increase government revenue may ultimately reduce it by discouraging investment and economic output.

• National Insurance hike: Labour’s planned increase in employer National Insurance from 13.8% to 15% has reportedly triggered hiring freezes, redundancies and reduced business investment, particularly in retail and hospitality. Businesses now face higher costs per employee, leading many to reconsider expansion. This aligns with the Laffer Curve’s prediction that higher employment taxes may not raise more revenue if they shrink the tax base by making hiring less attractive.

• High income tax rates: Scotland’s 48% top rate and the UK’s 45% additional rate are among the highest in developed economies. While these rates target higher earners to boost revenue, research suggests the UK’s optimal tax rate for maximizing revenue is around 36%.

These cases illustrate a crucial economic reality: raising tax rates doesn’t always raise revenue.”

Advance your career with an award-winning course or apprenticeship

Flexible, inspiring and engaging. Mindful Education courses are expertly designed to bring learning to life and achieve outstanding results.

Discover more mindful-education.co.uk/learners Become an Intermediate Financial Accountant

Unlock you career potential with the IFA

Graduates, recently qualified and part qualified accountants get the support, guidance and recognition you need to set yourself apart in a competitive SME job market with:

• Designatory letters IFA AIPA

• Access to a variety of technical resources

• Relevant CPD webinars and networking meetings

• Financial Accountant, our member magazine

• MyCommunity, our online member space

• A weekly enewsletter covering accounting, finance and business

ACCA March exam feedback

What did those actually sitting the March exams think of them?

Here are some of the comments straight from the horse's mouth

How did the March sitting go? Here's the day-by-day feedback as it happened…

AA

One sitter wondered why there was so much on substantive procedures. “Feel like I was typing the same thing over and over again,” they said.

Another sitter said the exam wasn’t difficult, but due to time management spent too long on risk assessments and too much on questions in section A.

In the Open Tuition Instant Poll, 62% of sitters said the exam was ‘OK’, 22% found it ‘hard’ and just 7% said it was a ‘disaster’.

AAA

For many it felt like the exam wasn’t difficult, one sitter even thought it was “reasonable”. Another said they had “a fair set of questions”. That said, time management was key – let’s hope you didn’t spend too long on the risk question. The lack of sustainability reporting for some (remember, there is more than one paper) was a disappointment, too.

In the Open Tuition Instant Poll some 37% of sitters said the exam was ‘hard’, and 13% had a ‘disaster’.

TX

For one PQ this exam was “just crazy”! How,

they asked, can it all be done in three hours?

Another sitter said the exam was “brutal”. They added: “I was prepared but boy was I wrong, especially those last three questions.”

In the Open Tuition Instant Poll, 26% said the exam was a ‘disaster’ for them, and another 31% said it was ‘hard’. That left 40% saying it was ‘OK’.

SBL

One sitter suggested the paper was “quite good”, and another said it was “alright”.

Mixed emotions from others, but there were few complaints this time around.

Lots of votes in the Open Tuition Instant Poll – over 400! Some 63% of sitters voted the exam ‘OK’, 21% said it was ‘hard’ and 7% had a ‘disaster’.

PM

For many this exam was between OK and hard, with a lot of calculations and some quite tough questions. The target costing question being one of the tricky ones.

One student said they had been studying PM for a year and if they fail this time they were going to quit. A fellow ‘sufferer’ tried to persuade them not to quit and explained it was their ninth attempt.

‘Hard’ came out top in the Open Tuition Instant Poll with 46% of the votes. Another 14%

of sitters had a ‘disaster’ and 38% said the exam was ‘OK’.

APM

“Awful” is all one sitter said about APM this time around. The ABC question threw a few sitters – “I didn’t understand what I was meant to calculate,” said one PQ.

One student explained their computer froze twice during the exam and they had to be relocated both times. There were also a few system issues for other students as well.

In the Open Tuition Instant Poll the exam was deemed ‘OK’ by 47% of sitters. Some 29% found the exam ‘hard’ and another 16% had a ‘disaster’.

ATX

“Quite hard” and “shocked” were two comments post-exam. Many found the exam difficult and left halls disappointed. There was a general feeling that the questions were a little unusual.

One sitter thought there was minimal stuff on IHT, reliefs and share schemes/tax planning.

Another admitted they had mismanaged time badly, which never helps.

Just 29% of sitters in the Open Tuition Instant Poll said this one was ‘OK’, with 44% calling it ‘hard’, and 25% a ‘disaster’.

FR

Sitters thought section A and B were harder than the mocks and past papers. However, section C was the exact opposite and easier than both.

Only 31% of sitters told the Open Tuition Instant Poll that the March exam was ‘OK’. For 45% it was ‘hard’ and for another 17% it was a ‘disaster’.

SBR

People who got the segmental reporting question found it hard.

For one in five sitters (22%) this exam was a ‘disaster’, according to the Open Tuition Instant Poll. For just over a third (36%) it was ‘hard’ and for 39% it was ‘OK’.

FM

We loved the comment from the student who said: “I have no idea what that was.” What that was was lots of theory questions, said another sitter.

The management of receivables and exchange risk hedging in section B also threw some. One PQ said: “I felt prepared but was disappointed the wordy section B question beat me.”

In the Open Tuition Instant Poll some 35% of sitters said the exam was ‘OK’. Another 44% admitted they had found it ‘hard’, and 18% had a ‘disaster’.

AFM

Sitters found the acquisition question hard –one wondered where all the missing pieces of information were. The SWAP question with two counter parties was also deemed tricky.

Voting in the Open Tuition Instant Poll was evenly divided. Some 32% said the exam was ‘OK’, 37% found it ‘hard’ and 25% had a ‘disaster’.

Levelling the exam playing field

Creating the right environment for your CGMA exams is vital, says Nasheen Wuisman – and here’s how you can do it

Embarking on the journey to become a CGMA designation holder with CIMA is both an exciting and rewarding experience. Yet ‘exam day’ are two words that can easily fill you with dread.

Over the past few months I’ve been approached by some of our CGMA candidates asking me to tell them more about the exam day itself. They placed specific emphasis on adjustments that might be possible for them to be able to focus on the exam better.

Succeeding on your CGMA journey does take individual determination and personal resilience. Whilst you put in the necessary question and skill practice from your side for the day to go as smoothly as possible, we also work to provide you with the right support to make your exam day as comfortable as possible and make sure that we’re creating the right exam environment for you.

In this month’s column I’d like to build awareness by talking about how we’re committed to providing the necessary support to help you succeed in your CGMA exams. Our goal is to create a level playing field, allowing each and every one of our candidates to demonstrate their skills and capabilities fully.

How we

can support you

We can offer adjustments as per our special accommodation policy to candidates, allowing those with special educational needs, disabilities or temporary illnesses and injuries equal access to our exams. These include:

• Testing environment: We make adjustments to the testing room at the test centre, such as setting up a specific workstation or providing the candidate with a separate room to sit their exam.

• Extended time and supervised rest breaks: We grant a candidate extra time to complete their exam and ensure that they’ve scheduled rest breaks during the exam.

• Assistive technology: We offer tools such as screen readers, speech-to-text software, or specialised keyboards to aid candidates with reading and writing tasks.

• Alternative formats: We offer exam materials in different formats such as large print, or

adjusted contrast or font to accommodate a range of needs.

How to apply

If you think that you’d benefit from some reasonable adjustments to be made, please fill in our dedicated online application form. After completing the form, you’ll need to send any supporting medical documentation to special. accommodations@aicpa-cima.com

When to apply

You can apply for reasonable adjustments at any time, but we strongly recommend:

• Doing so, as soon as possible after diagnosis by a healthcare professional. Applying early will allow you to be able to focus on your learning, confident that your requirements are in place when exam day arrives.

• Being sure to apply before scheduling an exam. We process applications within seven working days of receiving your documentation. Remember to allow sufficient time between booking your exam and exam day to allow the test centre to set up reasonable adjustments on your behalf.

We’ll keep the adjustment in place until you complete your studies with us, meaning that you

only need to apply once. If your needs change or a new adjustment needs to be put in place, you will just need to send us updated medical documentation. If you have a temporary illness or injury, the reasonable adjustment will be in place for a pre-defined period.

Where to sit your exam

When making the decision as to where to sit your exam, it’s worth bearing in mind that due to the remote nature of online exams, it isn’t possible to provide the full range of adjustments away from a test centre. Make sure to check our guidance to help you make the best possible decision to suit your needs.

Planning for your exam day

It’s important that you build in planning for the big day as early as possible and not leave it to the last minute. Here are my top tips:

• Find out as much as possible about how the exam day works in a test centre and online, knowing what it involves will help you to visualise the day early and reduce stress.

• Decide what works best for you and whether you might benefit from some adjustments. Complete your application for special accommodations early so that you have one less thing to do as the exam gets closer.

• Plan your travel to a test centre, make sure to give yourself plenty of time and have a back-up plan in case of strikes, disruptions, bad weather – or if things just don’t go to plan that day.

• Try to plan the day before your exam if possible and make sure that you’re not working late in the night. If you have a young family, try to get support so that you can get a decent night’s sleep. Poor sleep can have a huge impact on your exam performance on the day.

• Clear your head – complete focus is key, but it can be hard as we must juggle so many responsibilities in our professional and personal lives. I’d still advise you to give it a go to see how your performance improves when you do.

Finally, do your best on the day, no one can ask any more of you. Always remember that we’re here to support you. Contact us early to make sure we know how we can help you.

• Nasheen Wuisman, Senior Manager – Global Academic Progression at AICPA & CIMA, together as the Association of International Certified Professional Accountants

Going concern explained

FRC has provided an ‘explainer’ on its update to going concern reporting. Here it is…

On 25 February 2025, the FRC issued an updated ‘Guidance on the Going Concern Basis of Accounting and Related Reporting, including Solvency and Liquidity Risks’, to help directors of UK companies demonstrate the assessments underlying their going concern conclusions and increase confidence from all stakeholders.

The guidance is intended for all UK companies except small companies and micro entities. It brings together the requirements or provisions of company law, accounting standards, auditing standards, listing rules, the UK Corporate Governance Code and other regulation relating to reporting on the going concern basis of accounting and solvency and liquidity risks.

statements.

• Disclose principal risks and uncertainties, which may include risks that might impact solvency and liquidity, within their strategic report.

So what has actually changed:

• Its scope includes companies that apply the UK Corporate Governance Code.

• It reflects changes in accounting and auditing standards.

• It provides additional guidance on overarching disclosure requirements that may apply.

Enhanced understanding of requirements

The guidance encourages directors to take a broader view, over a longer term, of the risks and uncertainties:

uncertainties to which the company is exposed –and to its financial and liquidity position.

Areas of focus

The guidance outlines several key considerations for the effective reporting for the going concern assessment, including that directors should:

• Assess the appropriateness of adopting the going concern basis when preparing financial statements.

• Consider any material uncertainties to be disclosed in the financial statements (this assessment should consider all available information about the company’s future).

• Consider whether additional disclosures may be necessary, including disclosures about any significant judgements made and to provide a true and fair view. All disclosures should be clear and company-specific.

Disclosures related to solvency/liquidity risks

Companies must identify and disclose principal risks and uncertainties in their strategic reports, which may include solvency and liquidity risks.

The non-mandatory guidance serves as a proportionate and practical guide to assist directors with the application of the applicable legal and regulatory requirements to:

• Encourage assessment and disclosures related to the going concern basis of accounting and any material uncertainties in their financial

• It acknowledges that companies have risk management processes in place that underpin the assessment, and that the level of analysis applied depends on the size, complexity, and particular circumstances of the company.

• It acknowledges that the amount of information disclosed should be proportionate to the

The guidance encourages directors to consider both financial and non-financial factors that could impact the company's operations and financial health. When assessing these risks, directors should evaluate their likelihood and potential impact, ensuring that disclosures are tailored to the specific circumstances of the company.

You can read the full guidance at https://tinyurl.com/2s7tx8dc

Gender equality

To celebrate International Woman’s Day 2025, Daniella Di Marco spoke to Melanie Proffitt about how ACCA is connecting its newly elected all-female Council leadership team with future members

Daniella: Melanie, what motivated you to pursue a career accountancy?

Melanie: Well, with a surname like Proffitt there was a little amount of nominative determination there! Maths was my strongest subject in school – I had an amazing maths teacher that inspired me to do the best I can. I’ve always loved solving problems and puzzles and who doesn’t like a good jigsaw? I feel like that’s what we do – we pull all the pieces together and create a picture for the organisation.

Daniella: What would you say the key milestones in your career have been and how did you navigate them?

Melanie: The first one was becoming an ACCA member. When you reflect on your career, some of the really nice milestones are when you see people like yourself grow and develop, so I feel like I’m leaving a little trail of Daniellas behind me! I’m trying to inspire people to go on my journey, become ACCA members, silence that inner critic and take on the bigger challenges. Because we’ve got just as much capability as the men in the world – and you can see that rising when you look at the statistics in terms of getting representation.

Daniella: Have you noticed many changes throughout the years? If so what are they?

Melanie: There’s been a lot going on in UK legislation – we’ve got gender pay reporting. That doesn’t mean to say we’ve solved the problem! But at least we’re starting to report on it and look at it. I do think the pandemic had a part to play in accelerating flexible working – the ability to work different hours and work from home. And we’ve seen things like parental leave being shared between couples, so I think we’ve seen a lot of changes but there’s still a lot to do. But talking about it on International Women’s Day is the start – shining a light on metrics of what organisations are doing.

Daniella: What specific actions do you think are needed to accelerate gender equality within the workplace?

Melanie: I think it’s a bit of mindset really. Businesses need to really look at their own internal policies and the way that they work. There are so many different things around training people, but equally in recruitment – like bias, unconscious bias, blind recruiting where you don’t see the name of the individual. There are lots of things that businesses can do to try to encourage that. We definitely have equal pay – that is a legal requirement in the UK in terms of job roles. We shouldn’t be looking necessarily to legislation and government requirements. I think it should come from businesses.

It's good to call out the consumer in this, too. Businesses will be sustainable and will thrive if they adopt these sorts of more ethical, inclusive policies and procedures and values and live by them. Lots of positive changes but lots to do – we’re going in the right direction!

Melanie: So Daniella, what does the future hold for you? What does your career path look like and how are you going to get there?

Daniella: First, passing my ACCA exams! Now that I’ve started with ACCA I’ve moved job roles, moved from practice to industry and I’m excited. I feel that nothing’s holding me back, nothing is stopping me – and I’ve got a great role model! ACCA is a wellknown qualification, and I could go anywhere. Melanie: What I always say to students starting out is remain curious. Keep asking why. Keep wanting to understand more and learn more.

• #IWD was celebrated on Saturday 8 March 2025

Watch the international conversation as Ayla Majid, Datuk Zaiton Mohd Hassan and Melanie engage in meaningful discussions with Saman, Sharifah and Daniella, future members from Pakistan, Malaysia and the UK respectively. You can watch the full film here

Daniella Di Marco, ACCA student and assistant accountant at Farncombe Estate in Broadway, Worcestershire

Melanie Proffitt, deputy president of ACCA and Farncombe Estate CFO

A question for Tom

Tom Clendon explains how an organisation should account for monies raised via crowdfunding

Question

What is crowdfunding and how do you account for the cash received?

Tom’s answer

Traditionally, when companies wanted funding they would either go to a bank to borrow or issue equity via the stock market. The internet has facilitated the disintermediation of raising finance. This simply means that companies can raise finance (get funding) direct from investors (the crowd). So crowdfunding is the funding of a new start-up or project by collecting cash from a variety of individuals or entities (the crowd.)

So how do you account for monies received from crowdfunding?

There is no specific accounting standard that deals with the accounting of cash received from a crowdfunding operation. And it is this that potentially makes it a current issue to be examined at SBR. Clearly when cash is received the asset of bank will be debited. But where to credit? Before reaching any conclusion, it will be necessary to properly understand the true nature of the terms of the crowdfunding. What does the crowd get in return? Do they have a right to their

money back? Are they now a part owner of the business? Has the business sold them something in return? These are the key issues to resolve.

Crowdfunding could be debt

If the monies that have been received have to be repaid, then there is a present obligation and a liability is recognised. This financial liability and would be initially recognised at the fair value less issue costs; that is at the net proceeds of issue. IFRS 9 Financial Instruments applies. The default accounting treatment for such financial

instruments is amortised cost. The profit and loss account will be charged with an effective rate of interest on the debt.

Crowdfunding could be equity

If the monies that have been received represent a payment in return for an ownership interest; then an equity instrument has been issued. Again, the relevant standard to apply is IFRS 9 Financial Instruments. Such an issue of equity shares is also initially recognised at fair value less issue costs – that is the net proceeds of issue.

Crowd funding could be revenue

It is possible that the monies have been received because the company is making a sale. In return the crowd are getting a product or service. If that is the substance of the crowdfunding arrangement, then IFRS15 Revenue from Contracts with Customers applies. Revenue will be recognised when the performance obligations are fulfilled and control passes, and before that arises the monies received will be accounted for as a deferred income – a liability.

Conclusion

It will always be necessary to understand the terms that underpin any monies received through crowdfunding so that the accounting treatment is a faithful representation.

• Tom Clendon is an online lecturer for SBR. Contact him on WhatsApp on 07725 350793 or via www.tomclendon.co.uk

On point

Nick Craggs explains everything you need to know about tax points, relevant to the level 3 Tax Processes for Business unit

Alittle-known fact about me is that I used to be a farmer. In fact, I have a degree in it. But a career tilling the soil and feeding calves didn’t work out, and the next thing you know you are wearing a suit, on an ACA training contract, and find yourself on a stock count on New Year’s Eve.

I also love a bit of tax. The problem with tax though is that it keeps changing, and so do the exams. AAT have just started to assess the 2024 Finance act, so I thought I would write this month about an aspect of tax that doesn’t change, which is tax points in the Tax Processes for Business unit.

Anyway, my first job was as a bookkeeper for famers. I knew a bit about farming, and not too much about bookkeeping. One of the earlier tests of my career was from a farmer in Northumberland. He had bought some fertiliser, and as all readers of PQ magazine know, fertiliser isn’t cheap. So there was a lot of VAT on it, and the farmer wanted to claim it back, as you can imagine. However, the problem was the invoice was dated 3 March 2025, but I was preparing the February 2025 VAT return. As an accountant, I stood up for my fundamental principle of integrity, and told him he would need to wait

for the next VAT return before he could claim it back.

Sounds simple – just stick by the date on the invoice, right?

Well, as with most things to do with VAT, it isn’t so simple. The date on the invoice isn’t always the tax point. The tax point is the date which dictates when we can claim back, or have to pay over, the VAT.

If the fertiliser was delivered to the farm on 3 February 2025, this would be the tax point, as the delivery is before the invoice date. This is known as the basic tax point. As ever, it isn’t as straight forward as that. If the invoice is dated within 14 days of the basic tax point, this would override the basic tax point, and the invoice date would be used. So, if the fertiliser was delivered on 25 February 2025, the farmer still couldn’t have his VAT, as the tax point would still be 3 March 2025 as it is within 14 days of delivery.

The farmer could have got around the invoice being dated after his VAT quarter by actually paying for the fertiliser up front. If cash is paid before delivery or the invoice date, the date of the payment will always be the tax point. However, many of the tight farmers I know wouldn’t do this, as they would rather claim the

VAT back, and then pay the invoice later – much later!

We have a tax point which could be the delivery date, could be the invoice date, or it could be the date that the goods were paid for. But wait, it gets more complicated!

What happens if the farmer pays a deposit on his nice shiny tractor up front? In this case there would be two tax points. There will be the date of the payment of the deposit, then the next tax point will be dependent on delivery date, invoice date or the payment of the balance.

Let us look at an example.

Giles is going to buy a brand new tractor for £72,000. He has agreed to pay a deposit of £12,000 on 4 June. This is a tax point as he paid cash over, so the VAT on this will be £12,000 /120% x 20% (or you can just use the VAT fraction of 1/6th), which is £2,000.

He then takes delivery of his new tractor on 25 June. He then receives the invoice for the balance, which is £60,000, on 3 July. He then begrudgingly pays the invoice in November, because that is what farmers do.

His VAT return quarter ends in June, and obviously he wants to claim back £12,000 of VAT from HMRC as soon as possible. Within his VAT return quarter he has made a payment of £12,000 and taken delivery of his new tractor, which is the basic tax point.

However, Giles’s problem is that his machinery dealer has issued an invoice within 14 days of the basic tax point, so the basic tax point is overridden and the actual tax point is 3 July, outside of his VAT return, so he can only claim £2,000 of VAT this quarter. The rest of the VAT will have to wait until the next VAT return before he can claim it back.

• Nick Craggs, AAT distance learning director, First Intuition

Having a ball

CASSL’s 1920s themed ball was a roaring success. Oliver Sighe reports on the night’s events

Guests were transported back to the glitz and glamour of the 1920s at our muchanticipated themed ball. Held at the Chartered Account Hall in Moorgate, the event was a dazzling spectacle of vintage elegance and live music, and also included keynote speeches from Bank of England CFO Afua Kyei and ICAEW President Malcom Bacchus.

Attendees embraced the spirit of the era, donning flapper dresses, feathered headbands, sharp tuxedos and dapper bow ties. The venue itself was transformed into a Gatsby-esque paradise, complete with art deco table décor, soft candlelight and an ambiance reminiscent

of a speakeasy straight from the Prohibition era.

The evening kicked off with a champagne reception, setting the tone for the sophisticated yet lively night ahead. Current CASSL Chair, Aydin Bolton, opened the night with his speech. Guests were then treated to an exquisite threecourse meal. Malcolm Bacchus spoke about his career, and how becoming a chartered accountant has led him to work across many different industries. Afua then took to the stage in a very motivating light, talking about her career and how she’s always pushed for more.

The evening raised over £1,000 for our charity

sponsor, Urban Synergy. Leila Thomas from the charity also took to the stage for a speech about its activities. Urban Synergy is a charity giving young people opportunities in finance through mentoring and empowerment. Further to this, they help companies to be more diverse and give back to younger people.

No 1920s ball would be complete without a dance floor filled with Charleston moves and lively swing dancing. Professional dancers took to the floor to give a dazzling performance before leading an energetic dance lesson, encouraging guests to try the iconic steps of the era.

The night concluded with a grand prize draw, rewarding the best-dressed guest, and raffle.

A huge thank you to everyone who attended and made the night such a roaring success. Your enthusiasm and effort truly brought the magic of the 1920s to life. We can’t wait to do it all again next year – until then, keep dancing, keep celebrating, and keep the spirit of the Jazz Age alive!

• Oliver Sighe is vice chair of CASSL

Keep it simple

Rob Sowerby believes by keeping it simple you can succeed in passing even the hardest accountancy exams

Keep study simple is the name of my company for good reason. I have been teaching for a long time and the longer I stand in front of students the more I am convinced that what we learn in the professional exams is simple.

As I am wont of saying to my poor students, it is not rocket science. The key as a tutor is making it appear simple to the student. That can sometimes be difficult to achieve and it is very easy for a poor tutor to hide behind the veil of the subject.

In my view, the role of the tutor is to simplify everything, to make clear that which is potentially confusing. A definition has to be short, lacking in jargon and easy to apply, explain and replicate by the student. For example, cutting out the detail, debt factoring is the outsourcing of credit control – a simple way of looking at the issue, but one which can be detailed into debt collection, financing and credit insurance issues.

I teach a very wide range of subjects, from introductory level to the highest level and

across many disciplines, as long as it is not tax or audit! I believe that it gives me a far better perspective on the individual subject when I teach it. My natural home is teaching management accounting and financial management. For anyone who knows, these subjects are based on logic and simple theoretical ideas. In order to apply the theory may require complex computations, but the fundamentals to success are understanding why you are doing those computations and what you are trying to achieve.