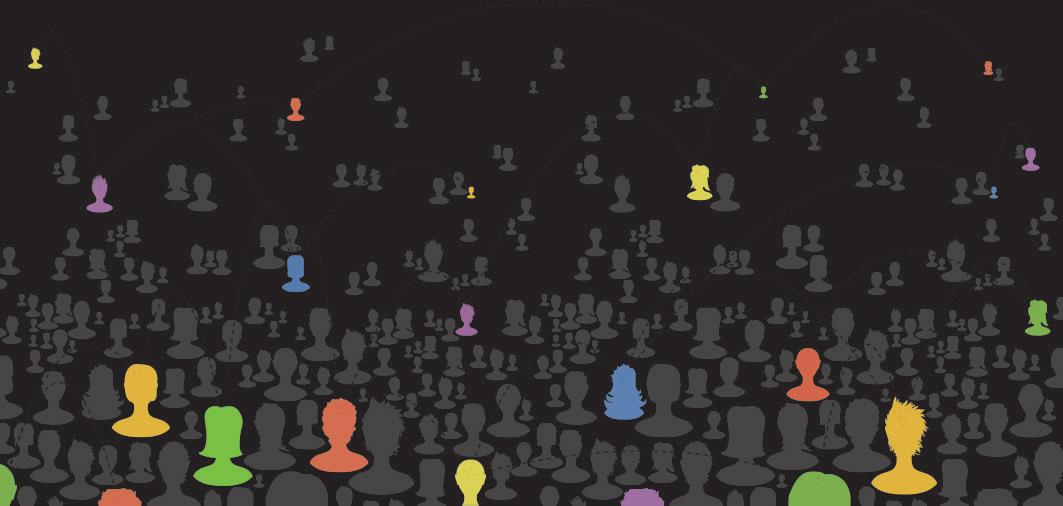

Multimanager hedge funds looking to allocate to external firms in race for talent

y B LYDIA TOMKIW

Hedge funds are always looking for new investments and one is increasingly gaining steam: allocating to other hedge funds.

While investing in other funds is nothing new for the hedge fund industry, the last few years have brought growth in both the number of funds doing so as well as the number of

Washington

external allocations.

External allocation has echoes of the once dominant hedge fund-offunds industry as well as the standalone seeding firms that gave a previous generation of managers their start.

But these days, it is multimanager hedge funds — a sector that has seen immense growth in recent years and

How Harris and Trump compare on taxes, capital gains and the economy

y B BRIAN CROCE

Voters routinely tell pollsters the economy is their most important issue in the 2024 election. And though there are many dividing lines between the two candidates vying for the U.S. presidency, they notably have vastly different economic visions. Regardless of who wins the White House and which parties control the House and Senate, tax policy will be a major discussion point in Washington next year as many of the provisions in the Republican’s 2017 Tax Cut and Jobs Act expire in 2025. Whether those provisions should be extended, amended or be allowed to lapse, and how — if at all — a package should be paid for will be hotly debated.

On the campaign trail, both Vice President Kamala Harris

In this report

■ For a list of the largest hedge funds, see Page 19

■ Hedge funds diving into private credit. Page 18

■ Dmitry Balyasny looks back, and forward. Page 20

■ For the full report, go to PIonline.com/ hedgefunds2024

Pension Funds

U.S. equities drive robust returns for public pensions

Median return of 9.9% makes second straight year of impressive gains

y B ROB KOZLOWSKI

U.S. public pension funds chalked up a second straight year of positive returns for the fiscal year ended June 30, with half posting double-digit numbers despite a somewhat muted bond market and continuing challenges in private markets.

While experts said this was all good news, the dominance of U.S. equities has left them having to convince some public pension fund board members that diversification is still important.

The median return was 9.9% among the 64 pension funds with more than $1 billion in assets whose results had been tracked by Pensions & Investments as of Sept. 16. The median return among plans tracked by P&I the previous fiscal year was 7.6%.

For the most recent fiscal year, every tracked pension fund reported positive returns — with a range

y B PALASH GHOSH

of 5.9% to 14.5% — and those with greater exposure to public equities and lesser exposure to private markets posted the most impressive numbers, continuing a trend from the prior fiscal year. It was even a more impressive year than fiscal year 2023 when pension funds recovered strongly from an anemic fiscal year 2022 that saw negative returns across the board. Returns for the fiscal year ended June 30, 2023, ranged from 2.2% to 11.9%.

A few weeks after the National Football League invited private equity firms to purchase passive stakes in their teams, a very different sport across the pond said it's planning something similar.

While largely unknown in the U.S., cricket is the second most popular sport in the world behind only soccer, boasting at least 2.5 billion fans, according to the World Atlas. That dwarfs the popularity of such U.S. sports as basketball (800 million fans) and baseball (500 million).

Now private equity firms may compete into the medieval sport which is thought to have originated in Britain and is played throughout South Asia, the Caribbean, South

Women execs paying it forward Honorees from the 2024 class of Influential Women in Institutional Investing are dedicated to their mentorship duties.

3

MARKETS LEAD WAY: Wilshire Advisors’ Thomas Toth

IN THIS ISSUE

Alternatives

Canadian pension funds are going big in infrastructure investing. Page 6

In its latest move in private markets, BlackRock has created a new private credit division Page 6

Hedge Funds

Singapore’s GIC and Bridgewater Associates looked at important issues ahead. Page 23

Real Estate

Barings’ John Ockerbloom says buyers and sellers still can’t agree on pricing Page 4

Special Report: Hedge Funds

Hedge funds are diving deeper into private credit. Page 18

Dmitry Balyasny mulls lessons learned over the last 23 years, and what’s ahead. Page 20

Three P&I surveys are now in progress

P&I’s annual survey of investment management consultants is underway with responses due by Oct. 11. Firms providing investment advice and related services to institutional investors are eligible to participate. Results will run Nov. 18.

Responses to P&I’s annual survey of index mangers are due by Sept. 27. Firms managing index strategies, including passive, enhanced, ETFs/ETNs and factor based for U.S. institutional, tax-exempt investors are eligible to participate. Results will run Nov. 4.

P&I is accepting late responses to the annual survey of defined contribution strategies . Firms managing proprietary mutual funds, ETFs or target-date strategies for U.S. institutional, tax-exempt DC plans are eligible to participate. Results will run Oct. 21.

To request a survey or obtain further information, please contact Anthony Scuderi at ascuderi@pionline.com or 212-210-0140, or visit www. pionline.com/section/surveys

New CalPERS CIO talks private markets, returns

The increased allocation was by boosting private equity by 4 percentage points to 17% and private debt by 3 percentage points to 8% at the expense of public equity and public fixed income.

CalPERS officials plan to “gradually increase” the $519.9 billion pension fund’s exposure to private markets to its new 40% target allocation from its actual investment of 30% as of June 30, said Stephen Gilmore, the new CIO, at a Sept. 16 investment committee meeting.

The California Public Employees’ Retirement System, Sacramento, adopted the new allocation in March, four months before Gilmore joined as CIO. The allocation increased private markets exposure to 40% from its former 33% target.

Increasing CalPERS private markets exposure will give the fund a wider range of the investable markets but less liquidity, he said.

Gilmore also said that one of CalPERS’ relative advantage in the private markets is because it had made fewer commitments than its peers.

“And that actually gives us an opportunity to get access to high quality funds and maybe to negotiate better terms and conditions,” he said.

During a presentation, Gilmore spoke about the pension fund’s fiscal year returns which fell below its benchmark for the one, 10 and 20-

year periods ended June 30.

He said that the reason for the underperformance, 9.3% for the year ended June 30 below its 10.3% benchmark, was that private equity was no match for the “very strong performance of the equity market ... where you’ve seen the large cap tech stocks do phenomenally well and you’ll find a lot of our peers and others lag benchmarks because of that.”

Private equity underperformed its public market benchmark in all time periods including the 10 and 20-year periods ending June 30 with a net annualized 11% com-

The retirement savings gap can only be improved by addressing the gaps in access, saving and guaranteed income, said Thasunda Brown Duckett, president and CEO of TIAA, in her closing keynote at the 2024 Influential Women in Institutional Investing Conference in Chicago.

Duckett said the problems we are trying to solve include the fact that every day 11,000 Americans are reaching their retirement age and yet there’s a $4 trillion retirement savings gap.

“First, we have an access gap,” said Duckett. “Fifty-seven million Americans do not have access to a workplace plan and disproportionately that will be women and people of color.”

“Secondly, we know there is a

savings gap,” she said. “People are not saving enough in accumulation. One of things we can do is continue to ensure that workplace plans offer auto enrollment and auto escalation.”

“Lastly, there’s a guarantee gap in this county,” she said. People are living longer, creating more longevity risk, and Social Security is under pressure. Duckett also mentioned that the last time the U.S. had the level of inflation it has had the past several years, it was the 1970s and at that time, 70% of Americans had access to a pension plan, while today that has plummeted to 12%.

Addressing the gaps will take public and private partnership, she said.

“When it comes to a secure retirement, it’s been one where we as an industry, we have been able

pared to its 11.6% benchmark and net annualized 12.1% vs 13.5% benchmark.

“I expect that (private equity) will recover somewhat over time,” Gilmore said. “We’ve already seen that with the large tech stocks giving up some ground.”

CalPERS is continuing to expand its exposure to active investments with a net $17 billion of new asset deployments across public strategies.

Active management requires patience, said Simiso Nzima, managing investment director, global equity at the investment committee

Sports investing has boomed in the last few years, and one of those leading the charge is Ian Charles, co-founder and co-managing partner of the $10.7 billion Arctos Partners, a firm that raised over $4 billion this year for its now-closed Arctos Sports Partners Fund II.

Pension funds and other institutional investors in the fund included Kentucky Public Pensions Authority, Maryland State Retirement & Pension System, Mutual of Omaha Insurance, Oregon Public Employees Retirement System and University of Texas Investment Management Co., according to P&I and PitchBook data.

Pensions & Investments sat down with Charles for one of his first interviews coming just as the National Football League announced it provisionally will allow certain private equity firms to invest up to 10% in teams’ ownership. Arctos is among those firms, as well as Blackstone, Carlyle

Both candidates vow to protect Social Security, but details are sparse

GOP promises no cuts, while Dems say no to privatization

As the 2024 presidential election gets closer, the candidates have started to hone in on their key issues and campaign promises, one of which is Social Security.

Though they disagree on a variety of topics, both former President Donald Trump and Vice President Kamala Harris have vowed to protect Social Security.

Alicia Munnell, director of the Center for Retirement Research at Boston College, chalked that up to Social Security being “probably the most popular program in the United States.”

Some 87% of Americans agree that Social Security “should remain a priority for our country no matter how bad budget deficits get,” according to a July report from the National Institute on Retirement Security. The report also found that 90% of Democrats, 86% of Republicans and 88% of independents agree with that statement.

However, if Congress doesn’t act, Social Security’s combined trust fund reserves are projected to face depletion in 2035, according to the Social Security Board of Trustees’ annual report.

Social Security has two trust funds: one for retirees and their families, and one for disabled workers and their families. The trust fund for retirees and their families faces a depletion deadline of 2033, at which point the fund's income could only pay 79% of its sched-

After studying economics at what is now Simmons University, Krissy Pelletier “was lucky to work with a great mentor (and) portfolio manager” on the public market side of Wellington Management. She still remembers the words said by Michael Carmen to set the tone going forward on her first day as an administrative assistant.

“He said, ‘Krissy, you didn’t go to Simmons to get this great degree simply to be an administrative assistant. So tell me, what brought you to Wellington? What made you interested? Let’s talk about what I do and how we can work together.’ He wanted to see me succeed. He was interested in what I wanted to be a part of,” Pelletier said. She would leave Wellington in 2006 as a stock-focused research associate, but Carmen, who is still at the $1.25

uled benefits, the report found.

“I actually don't think we're going to get much done (to prevent this) until 2030,” when the deadline is too close to ignore, according to Munnell.

GOP, Democratic platforms

The 2024 Republican platform promises to “fight for and protect Social Security and Medicare with no cuts, including no changes to the retirement age,” but doesn’t specify how

Private DC plan savers relying on equities

it will fund the program to avoid cuts.

According to Munnell, promising to protect Social Security “doesn't really have much meaning without saying how you're going to fund these benefits once the trust fund is exhausted."

The 2024 Democratic platform vows to “reject any effort to privatize Social Security or to cut any of the benefits that the American people have earned,” promising to “strengthen the

Dialing down risk was behind

Nevada PERS’ equity rollback

Short-term Treasuries provide a safe cushion, CIO Edmundson says

Steve Edmundson, the chief investment officer of the Nevada Public Employees' Retirement System, is not one to make big, abrupt moves, but in March he did just that.

The self-effacing CIO recommended that the pension fund's board dial down the portfolio’s allocation to equities a whopping 12 percentage points — to 48% from 60% — and steer the money to shortterm Treasuries instead.

The board approved the recom-

mendation, setting in motion the beginning of what Edmundson describes as Nevada PERS’ most conservative risk posture in the past two decades.

“It makes me feel good because we get to our ultimate end objective, which is to reach our return goals with the least amount of risk possible,” he said in an interview.

The move was not so much about high equity valuations and the possibility of a market downturn, but rather the high-interest-rate environment that Edmundson believes has normalized.

Why, Edmundson reasoned, take on more equity risk than necessary at a time when higher interest rates on U.S. Treasuries can bolster the

Non-governmental defined contributions plans have become increasingly important to participants’ retirement, and stocks have dominated those investments. Nearly three-quarters of plan assets are invested in equities, according to Vanguard’s latest How America Saves report. However, increased equity volatility has resulted in participants shifting from equity funds to fixed income as measured by daily transfers.

DC plan growth: DC assets outside of state/local and the federal governments have grown 163% to $9.95 trillion from the end of 2010 through March 2024. During that period, defined benefit assets increased 14% to $3.25 trillion.

Assets, private DB vs. DC (trillions)

DC allocations: There has been a marked increase in allocations to target-date funds, to 41% of assets last year vs. 23% in 2014. Cash, diversified equity funds and company stock fell over that time; however, total equity allocations still grew.

DC asset-weighted allocation

Younger workers ♥ TDFs: Younger workers have a greater allocation to targetdate funds. Among those under 25, it made up 79% of their allocation, and it was 25% for those 65 and older. The median equity allocation was 88% for those under 25 and 47% for individuals at least 65 years old.

DC asset allocation by age group

Volatility effects: As equity volatility increases, participants tend to move money from equity to fixed income, according to the Alight Solutions 401(k) index. During the first two months of Q3, there were 33 fixed-income days and 11 equity days as the Cboe VIX climbed to an average of 17.2, from 14 the previous quarter. Alight 401(k) index and equity volatility

DIFFERENT PATHS: Presidential candidates Kamala Harris and Donald Trump

Barings’ Ockerbloom on stagnant markets and the best opportunities

John Ockerbloom has had a wild ride. He was promoted to head Barings’ newly combined U.S. and European real estate business earlier this year at a time when higher interest rates and the pandemic ripple effects were shaking up the asset class.

Higher interest rates “created real stagnation in deal ow,” which has yet to free up, Ockerbloom said in his rst interview since assuming the

enhanced role. He now oversees a global team of 197 real estate professionals managing a combined $46 billion in assets under management and assets under advisement. About $4 billion of the total is AUA.

Barings invests across sectors, from core debt to opportunistic real estate and everything in between, Ockerbloom said.

“That was the vision we had when we brought the (real estate equity and debt) businesses together in the

U.S.,” a couple of years ago, he said.

Then in March, Barings quietly brought its U.S. and European real estate equity and debt teams together and promoted Ockerbloom, a managing director, to head of U.S. and European real estate. The combination was “an evolutionary change” for Barings, a subsidiary of MassMutual, he said.

Ockerbloom said Barings is taking a similar research-driven, collaborative approach to investing in Europe, its second-largest real estate business, as it is taking in the U.S.

The combined teams are focusing on how to manage their portfolios “particularly as our market evolves in of ce and other areas” and encounters inevitable challenges, he said.

Among the challenges is the still muted transaction volume, as real estate buyers and sellers, for the most part, cannot settle on price.

Adding to the problem is that the “banks that had been substantial lenders have exited,” Ockerbloom said. “The bank lending market in real estate is really not functional,” which is a favorable trend for a lender, he said.

MassMutual has been in the real estate lending business since 1966. MassMutual’s real estate lending business ultimately was integrated into Barings in 2016 as part of a combination of MassMutual’s boutique investment management businesses under the Barings brand.

As of June 30, Barings had $29 billion in global real estate debt AUM. Many of the transactions that are getting done are at signi cant discounts to the purchase price and discounts to the price expectations they had for those properties two years ago, Ockerbloom said.

While much of the distress is in the of ce sector, there are other areas where sellers are taking discounts. Prices are being cut on some residential and logistics properties because though demand is strong, rental growth is more muted, he said.

Debt coming due

One factor motivating price cuts, much of which is in the troubled ofce sector, is that debt is coming due, which is “calling the question” of whether to keep paying money to continue owning the property, he said.

According to S&P Global Market Intelligence, roughly $950 billion in commercial real estate mortgages are set to mature in 2024, peaking in 2027 at $1.3 trillion.

With mortgages maturing, property owners are not necessarily facing foreclosure. Indeed, banks in particular have been giving borrowers more time to work out their loans, he said.

“The re nance wall is not a wall but a soft barrier that is more exible than people thought,” Ockerbloom said.

Rather, property owners faced with loan maturities will decide whether now is the time to extend the loan and continue to fund the property, or whether the sounder approach is to look at other options including a sale, Ockerbloom said.

CHALLENGES

Public

Private

Canadian funds going big with infrastructure projects

Alternatives Investments in Brazilian water rm and American Tower lead recent moves

B PALASH GHOSH

y

Some Canadian pension funds have recently engaged in large transactions involving infrastructure assets in India and Brazil. Canada Pension Plan Investment Board, Toronto, made a follow-on investment of up to C$532 million ($392 million) in Brazilian water and sanitation company Igua Saneamen-

to. The additional investment will support what is expected to be a period of transformational growth for the company after it was awarded a major concession contract in the Brazilian state of Sergipe, said a Sept. 10 news release.

The Sergipe concession will provide water distribution, and sewage collection and treatment services to 74 municipalities across the northeastern Brazilian state.

CPP Investments, which has C$646.8 billion in assets, rst invested in Igua in 2021 as a platform for further investments in Brazil’s water and sanitation sector and holds —

excluding this additional investment — about 61.4% of the company.

Meanwhile, Data Infrastructure Trust, an infrastructure investment trust sponsored by alternative asset rm Brook eld Asset Management, along with af liates of investors including the C$250.4 billion pension fund British Columbia Investment Management Corp., Victoria, and $770 billion Singaporean sovereign wealth fund GIC acquired 100% of the Indian operations of American Tower for an enterprise value of 182 billion Indian rupees ($2.2 billion).

American Tower is a Boston-based real estate investment trust that

owns, develops and operates wireless and broadcast communications infrastructure across the world.

The transaction involved the buyout of about 76,000 communications sites in India, said a Sept. 12 news release.

This deal marked Brook eld’s third acquisition in the Indian telecommunications industry. In 2022, Brook eld acquired a portfolio of 6,300 indoor business solution sites and small cell phone towers, which advances the rollout of 5G and enables telecom operators to extend their coverage capacity in difcult-to-access and dense areas in

India. In 2020, Brook eld acquired a portfolio of about 175,000 towers from Indian rm Reliance Industrial Investments and Holdings. In India itself, Brook eld has about $29 billion in assets under management across the infrastructure, real estate, renewable power and transition, and private equity sectors.

A BCI spokesperson declined to disclose additional nancial details related to the deal but con rmed that BCI is a “signi cant" minority investor. BCI’s worldwide infrastructure and renewable resources

Investment (LDI) approaches

SOPHIE BAKER

In today’s environment, with many U.S. plans reaching fully funded or overfunded status, reassessing LDI strategies is crucial. Our panel, “Optimizing LDI Strategies to Meet Objectives,” will explore how plan sponsors can better manage ongoing, closed, or frozen plans by tailoring approaches for both return-seeking and liability-hedging portfolios. Key discussion topics:

• Evaluating LDI structure for various stages of the funding cycle.

• Reassessing your glidepath – when is it time for a change?

• Effective risk analysis and portfolio management.

PANEL SPEAKERS:

MODERATOR: Megan Nichols Sr. Partner, Head of Pension Settlement Solutions Aon

David Eichhorn, CFA Chief Executive Officer and Head of Investment Strategies NISA

Mike Jarasitis Pension Strategist Fidelity Investments

Steve Mullin, CFA Head of High-Grade Strategies MetLife Investment Management (MIM)

Shawn Pope, CFA Senior Director of Investments Cox Enterprises

BlackRock has created a new private credit division, a spokesperson con rmed — the latest move by the world’s largest money manager in the area of private markets.

The division, global direct lending, will be led by Stephan Caron, head of European private debt, she said.

The $10.65 trillion money manager runs about $35 billion in direct lending assets, according to Bloomberg.

The move is the latest by the money manager to expand in private markets. In its last quarterly earnings update, for the three months ended June 30, CEO Larry Fink said: “BlackRock is executing on the broadest opportunity set we’ve seen in years, including in private markets, Aladdin and whole portfolio solutions across both ETFs and active.”

In July, BlackRock agreed to acquire U.K.-based private markets data rm Preqin in a $3.2 billion cash deal. The agreement expands its Aladdin technology and data platform capabilities, the rm said at the time, and marked a strategic expansion of the technology business into the private markets data segment. Preqin’s data covers private debt among other private markets asset classes.

The Preqin deal followed the June announcement that BlackRock had agreed to acquire growth and venture debt nancing rm Kreos Capital. At the time, the rm said the deal plugged a gap in the Europe, Middle East and Africa region, and added capabilities in a high-growth part of the private debt market.

The rm has also been adding investment expertise in private credit across the globe, including the appointment of Stephen Allan as head of Australasia private credit in December, a new addition to expand the Asia-Paci c private credit team.

BlackRock said in its 2024 private markets outlook that it sees the potential for the global

Get ready for a groundbreaking panel discussion where

the

and discover what’s

Sandy Blair Chief, Administrator Savings Plus California State Employee 401(k) & 457(b) Plans

Jeb Burns Chief Investment Officer Municipal Employee Retirement System

Vikrant Arya CFA, CAIA MD, Retirement Investing Group TIAA/Nuveen

Matthew Gray Assistant Vice President, Worksite and Middle Markets Allianz Life

Barbara Erickson Retirement Specialist The J. David Gladstone Institutes

Michael Jabs Associate Director, Treasury - Pension The Kraft Heinz Company

Nick Nefouse, CFA MD, Global Head of Retirement SolutionsMulti-Asset Strategies & Solutions (MASS) BlackRock

Daniel Oldroyd CFA, CAIA Portfolio Manager and Head of Target Date Strategies J.P. Morgan

POSITIVE INFLUENCES

P&I celebrates Influential Women program at Nasdaq closing bell

Joined by honorees and guests, Pensions & Investments President and Publisher Nikki Pirrello celebrated the 2024 Influential Women in Institutional Investing at the Nasdaq exchange on Sept. 9.

Pirrello was joined by Veebha Mehta, chief operating officer of Crain Communications, the parent of P&I, interim Editor-in-Chief Julie Tatge and other members of the P&I editorial, sales and conference staff.

The list and related stories, which published online and in print Sept. 9, honored 60 women who varied in background, experience and their role in the institutional investment industry. P&I also launched the inaugural Rising Stars program, which recognized 40 women for their early impact and influence. The package can be found online at pionline.com/influentialwomen2024

To be considered for IWII recognition, nominees needed to be actively employed in the institutional investing field and have a minimum of seven years of industry experience.

They also were required to demonstrate a measurable effect and results within both their workplace and the industry. Ideal candidates were expected to exhibit a commitment to attracting, retaining, supporting and promoting women within the industry.

P&I held a conference in Chicago on Sept. 12 to recognize the winners. Conference speakers and panels explored leadership, sponsorship, entrepreneurship and closing America’s retirement savings gaps.

CELEBRATION: Honorees, friends and P&I staffers gathered to celebrate the 2024 Influential Women in Institutional Investing program at the closing of the Nasdaq exchange Sept. 9.

Yale Investments

offering a ‘new haven’ for aspiring fund managers

Yale Investments, which manages Yale University's $40.7 billion endowment fund, is rolling out a program to help aspiring asset managers start their own investment funds.

The Prospect Fellowship is an eight-week program where five individuals will have the chance to “hone their investment approaches and receive funding to build their businesses ... while harnessing the resources of Yale Investments and forging deep connections within (Yale Investments') office and network," according to a notice on the New Haven, Conn.-based university's website.

Yale Investments will lend each fellow up to $2 million in working capital to help build up their new funds. Then, each fellow will receive a minimum investment of $25

million at launch with an additional $25 million as a follow-on investment.

In return, Yale will receive capacity rights and pro rata co-investment rights, but will not acquire stakes in the funds or participate in revenue sharing.

Applications for the fellowship — which will take place in the spring of 2025 — are due by Oct. 14. Winners will be selected by the end of 2024.

A program spokesperson said the impetus for the fellowship stems from Yale’s “willingness to back up-and-coming, often unproven investment talent.”

With Prospect, “we hope to offer a new avenue for productive, value-added partnership at the moment when it is most

MISSION

ALIGNED

Janus Henderson to aim 3-year donation at fighting cancer

Now you can preserve capital, maintain liquidity and fight cancer, all in one go.

On Sept. 16, Janus Henderson announced that over the next three years it will donate half of the fees it earns managing the firm’s $400 million government money market fund to the American Cancer Society’s advocacy, research and patient support efforts.

And while no one at present anticipates a return to the days of rock bottom interest rates that forced managers of money market funds to slash fees or eliminate them entirely, Janus Henderson apparently isn’t taking any chances, guaranteeing a minimum donation of $1 million a year over that three-year span.

That gesture is the first fruit of an initiative the firm — with one legacy foot in London and another in Denver — launched earlier this year, called the “Brighter Future Project,” which looks to connect Janus Henderson’s “mission, values, and capabilities to the aspirations of our clients, the communities we serve and our employees.”

A spokeswoman for the firm said the decision to support a health-related cause as the project’s first move reflected the preferences of Janus Henderson employees.

Janus Henderson CEO Ali Dibadj, in a news release, noting the “devastating” financial burden of a cancer diagnosis, said with his firm’s initiative to support the American Cancer Society, Janus Henderson clients can “easily support ACS’ critical work in advocacy, research, and patient support, helping to improve the lives of both cancer patients and their families.”

Karen Knudsen, CEO of the American Cancer Society, in the same news release, said Janus Henderson’s support will help ACS fund critical research and support for cancer patients.

DOUGLAS APPELL

impactful,” the spokesperson added. “Serious candidates will likely have significant investment experience, although we do not favor one particular candidate profile — you may have developed your skills

through life experience, which we find exciting," Yale said in the notice.

A SYSTEMATIC PATH TO TRUE DIVERSIFICATION

In the current market environment, are you relying on private assets to provide uncorrelated exposures that can help protect your total investment portfolio?

That approach may not work, given today’s accelerated market volatility, which tends to impact both public and private markets. Often investors underestimate the degree of diversification in their portfolios because, since the global financial crisis, equity outperformance has created a false sense of confidence, said Philip Seager, head of portfolio management at Capital Fund Management, or CFM, a global quantitative and systematic asset management firm. “Legitimate uncorrelation is rare because so many asset classes and investment strategies are correlated with equity premia.”

Institutional allocators can access true uncorrelation from traditional assets by investing in a combination of zero-correlated, positive-gain strategies that deliver better risk-adjusted returns over the long term, Seager said. These systematic approaches include market-neutral strategies that are simultaneously long and short financial assets, and directional strategies that are long or short for periods, thus averaging to zero through time.

CFM also incorporates systematic hedge strategies alongside its diversifying strategies to increase upside potential when volatility spikes. “Building such products is our breadand-butter business,” Seager said.

A VOLATILE BACKDROP

Today “there is more potential for upcoming market volatility,” he noted, given mixed economic signals and heightened geopolitical tension — from a more polarized political environment in the U.S. and ongoing conflicts overseas. Investors are also contending with the implications of the expected interest rate cutting cycle and the possibility that inflation could reemerge. In addition, the dramatic growth of the Magnificent Seven stocks has increased equity concentration risk, and signaling heightened market volatility, the CBOE Volatility index, or VIX, spiked in August.

While allocators are always paying attention to appropriate diversification, the confluence of market impacts make it more crucial today. “Diversification is more important now than ever before, but when is it not important? Diversification should be at the forefront of every investor’s mind — all the time,” Seager said.

Yet investors often misunderstand the extent to which they’re diversified and the strategies that can provide actual diversification, so they can end up disappointed by the performance of what they think of as diversifiers. “For instance, when volatility spikes, equities go down, but a diversifier could, in equal measure, go up, down or remain unmoved. Many don’t understand that being up when equities are down is a hedge rather than a diversifier,” he said.

OVERESTIMATION

“Equity outperformance over the last 10 to 15 years is a statistical fluke. There’s been a lot of support from monetary policies that have pushed asset prices up,” Seager said. “By its nature, that upward pressure is a fluctuation that is unlikely to continue, and we will see a reversion back to the mean, which is a level of risk-adjusted returns that is lower and more consistent with what we’ve seen historically.”

Also, in the rising-equity environment, many investors dived into private market strategies “that are really just leveraged versions of equities,” said Seager. “People have moved aggressively into the private markets space thinking they would be diversified, but those returns come from the equity premium. You also get some premium from holding an illiquid position, but there’s not much more to it than that.”

“There’s actually a lack of diversification, and portfolios are nowhere near as diversified as people think,” he said.

POOR CORRELATION

Neither do fixed-income instruments always exhibit the diversifying features that they once did. While fixed income was steady for a period after the global financial crisis, mainly because inflation was low, in recent years the Federal Reserve has been tackling an inflationary regime.

Legitimate uncorrelation is rare because so many asset classes and investment strategies are correlated with equity premia.

“It might look like inflation is tamed, but fiscal policies are not helping to get it under control, and as long as we see inflation, real interest rates can be pushed lower, which isn’t good for fixed income, and it’s not good for equities either,” he said.

While the correlation between bonds and equities over the last 20 years has been mostly negative, according to CFM’s research, it is a statistical outlier. “The correlation between bonds and equities has actually been positive through most of history,”1 Seager said.

Therefore, “you do not get diversification or a hedge from bonds, and since the recent rise in inflation, that negative correlation has flipped and become positive. On a forward-looking basis, you get less diversification from a 60/40 portfolio than was previously the case,” he said.

PRAGMATIC PROCESS

CFM takes a practical approach to the use of quantitative strategies that deliver diversification. “We’re not guided by any sort of dogma about what should work. It’s based on trying to maximize risk-adjusted returns on a forward-looking basis by forecasting markets,” Seager said. In certain situations, one data set could forecast the market on a relative-value basis, another could forecast on a directional basis, and some could forecast both.

“We look at a wide set of markets and asset classes, including equity indices, fixed-income instruments and commodities. We do it empirically, and we use what works best in each environment,” he said.

The starting point is forecasting an instrument — including futures, options, credit or a single stock — which presents many

different strategies for the firm to pursue. “The more strategies you have, the better to broaden diversification,” he said.

The key to delivering diversification is the ability to understand the correlations among all the instruments. “We’ve been developing and fine-tuning this process for decades,” he said. CFM has two research groups that work closely together, one for forecasting and the other for portfolio construction. We “combine all of these price forecasts and construct a portfolio that’s as robustly diversified as possible and trades with the lowest execution cost.”

THE ‘BLACK BOX’

One concern that CFM hears from prospective clients is a general mistrust of algorithms versus human input in the investment process. “Algorithms have become ubiquitous in daily life, and advances in data-driven techniques have dramatically improved people’s health, safety and quality of life. Yet in many situations, people fear they will underperform” as an investment process, said Seager.

“Many fear that a systematic process is too ‘black box.’ On the contrary. There is nothing more black box than the human brain, which is prone to biases and demonstrates less repeatability,” he said.

The best investment outcomes, according to Seager, depend on a repeatable, systematic process that reacts in a rulesbased fashion in response to inputs from the market. “Our research process finds systematic patterns that occur and recur, and those patterns are then implemented in an unbiased fashion — even to exploit those inefficiencies in markets that are caused by human biases.”

“Data is becoming ever-more voluminous and available for consumption, and it gives quants a significant advantage over discretionary investors, because their investment decisions are better informed,” he said. Another advantage for a quantitative investor is Large Language Models that bridge the gap between quantitative and discretionary approaches. “We now have algorithms that trawl through mountains of text data to evaluate market sentiment and detect investment signals,” he said.

That said, CFM’s biggest asset is people, Seager said. “We recruit people with science backgrounds alongside those who have financial market experience so we can build algorithms with the right data and get the best outcomes.”

“We’ve been building strategies that are truly uncorrelated with traditional markets and provide genuine diversification since the early ’90s. It’s always the right time to diversify, but today it’s even more important than before.” ■

Sponsored by:

Philip Seager Head of Portfolio Management

(CFM)

OPINION

OTHER VIEWS BOB ELLIOTT

For asset allocators, it’s time to rewrite the playbook on high hedge fund fees

“When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients” — Warren Buffett

Hedge funds are a predominant force in the investment management industry. From the television show “Billions” to the films “Wall Street” and “The Big Short,” they are often portrayed as savvy investment management talent, able to handily outperform over the long term. The narrative that you can share in the success and benefit from their brilliance is compelling. But it often plays out differently in real world applications.

It is not that hedge funds cannot generate alpha. Many do, and it would be irrational as an allocator to ignore their success. The prevailing issue, however, is that allocators often receive diluted benefits from alpha generation due to the burdensome fees they incur. Quite simply, hedge fund managers are benefiting asymmetrically from fees charged to pension funds, endowments and other large investors, in some cases passing along only 41 cents of every $1 made.

How did we get here? While many advancements in the financial sector have helped to drive down fees — think ETFs and mutual funds — hedge funds have endeavored to maintain the classic 2-and-20 model. Some managers may still deliver outsized returns, but their high fee structures can result in the end investor experiencing muted returns.

A less evident aspect to consider is, in some cases, pass-through expenses further erode the returns the client ultimately receives. Some managers have gone as far as to pass through to the end investor expenses for employee salaries, back-office administration and research fees.

A common defense from managers is that these fees support recruiting and retaining the “best and brightest” investment management talent. While this may be true, it does not negate that, even with the impact of elite talent, hedge funds often underperform benchmarks after factoring in the fees.

As the landscape of investment management continues to evolve there is some good news: (1) fees are generally negotiable and (2) innovative products are emerging that empower all investors, regardless of size, with alternatives to the traditional 2-and-20 model.

Why now?

At the end of the day, hedge fund managers survive on fees. And like any business, customers, in this case allocators, have an opportunity to negotiate what they are willing to pay. Multiple factors are now converging to make this the ideal time to challenge the traditional hedge fund fee structure. First, interest rates have reverted to an elevated level after years of being zero bound.

Many existing allocator contracts were signed during the zero-interest years, when less consideration was given to implementing cash hurdles. The cash hurdle effectively allows for incentives to be paid to hedge funds only if and when they outperform cash. If an allocator can earn close to 5% on cash, it seems reasonable to expect that benchmark should be applied when evaluating the alpha generated by a hedge fund. Second, after incorporating fees, many hedge funds’ returns trail the returns of passive index funds. Allocators should instead incur fees on the alpha, meaning returns in excess of market returns, taking into consideration correlation benefits of the strategies implemented by hedge fund managers. Similar to the cash hurdle described above, it is possible to negotiate fees to apply above a

relevant benchmark return stream.

Third, there are an increasing number of alternative investment products that offer access to the return attributes of selective hedge fund strategies but at a lower cost than the 2-and-20. Hedge fund replication, for example, has advanced meaningfully over the past decade, and depending on the strategy, allocators may be able to find index-like products at lower fees, that also offer improved liquidity and better transparency than direct investments in individual hedge funds. Fourth, it has become increasingly difficult for hedge funds to raise capital. This is largely due to (i) a seemingly persistent public equity market, (ii) years of underwhelming performance relative to other investment options, and (iii) significant rotation into private assets.

Bob Elliott is CEO, CIO and co-founder of investment firm Unlimited. He is based in New York.

OTHER VIEWS ZHILEI XU, YANGFAN LI and RENEE YAO

Can modern AI help hedge funds ‘count the cards’?

Machine learning research began over 50 years ago and evolved steadily until the emergence of modern artificial intelligence. Techniques such as principal component analysis, support vector machines, random forests, and even artificial neural networks are all considered traditional ML approaches. Modern AI builds upon these traditional ML methods and leverages increased computational power, enabling it to demonstrate remarkable capabilities across a wide range of applications, from route navigation and protein design to, most notably, the development of advanced conversational models like ChatGPT.

Can AI ‘count the cards’?

Investing is a forecasting business. All investors need to forecast future returns to generate alpha. The stock market is considered random and unpredictable, making forecasting accuracy low due to noise. Can modern AI forecast returns better than humans? We make the analogy that blackjack is like the stock market. The only way to win at blackjack is to “count the cards” because the house has an edge. The market can be thought of as the world’s largest blackjack game, and modern AI can help hedge funds “count the cards” to achieve outperforming returns. Traditional ML often identifies associations in data, which can mistakenly imply causal relationships. For example, we might observe a 100% association between a wet lawn and

rainfall, but traditional ML could erroneously suggest that the wet lawn causes the rain — a clear misinterpretation. Such a model might build confidence in this faulty assumption over successive rainy days. However, on a sunny day when a gardener waters the lawn, traditional ML could wrongly predict rain with high confidence. If investments were made based on that prediction, significant losses could follow — highlighting the limitations of traditional ML in financial decision-making.

While it’s clear that a wet lawn does not cause rain, signals in financial markets are much less straightforward. Modern AI, utilizing advanced nonlinear models and a broader range of input data, can identify leading indicators and uncover genuine causal relationships. In the previous example, modern AI would understand the phenomena of rainfall and a wet lawn, then determine that it is the rainfall that wets the lawn. This capability can help prevent potential losses and turn them into gains.

Essentially, modern AI discovers

the causes behind signals (beyond just association), providing a more reliable basis for identifying investment opportunities. It acts like a noise-canceling system, filtering out misleading correlations and uncovering true causal links. Though even modern AI cannot identify causal relationships with 100% certainty, it offers a slight edge over traditional ML. All that is needed is to “count 1–3 cards” which leads to a 2% edge, similar to a casino’s edge. Hedge funds leverage this edge by making a large number of trades, relying on the law of large numbers to amplify their advantage and generate consistent positive returns. Owning the “math” is the edge every hedge fund strives to achieve.

One strength for hedge funds — sizing

Traditional ML often results in a constant bet size or leverage, as these models cannot predict how much the market will move in their favor. However, what differentiates modern AI is its forward-looking approach, constantly searching for leading

else is out there. Beginning new relationships can provide the opportunity to negotiate new fee structures from the outset.

indicators in the market. This allows the AI to increase its bets when it identifies more alpha opportunities and reduce them when it sees less, just like a card player has to forecast how much to bet on the next hand. Sizing alpha is an under-appreciated component of modern AI and allows an investor to produce a convex/asymmetric payoff — resulting in positive skewness (or convexity), uncommon among hedge funds.

Modern AI is also revolutionizing intraday trading by processing vast amounts of real-time data — including price movements, trading volumes, and news sentiment — to uncover patterns and predictive signals that are beyond humans’ ability to process; it can adjust trading strategies on the fly, dynamically altering the sizing of trades based on predicted price movements and volume shifts. This capability enables more precise entry and exit points, optimizing trade execution throughout the day. By continuously adapting to evolving market conditions, modern AI provides a critical edge in capturing short-term market opportunities.

AI’s adoption is challenging but inevitable

First, a manager needs an edge and a time horizon to minimize risk/variance. AI, like any forecast-

ing technology, will have periods of underperformance until skill emerges. While modern AI is undoubtedly a powerful tool, specialized skills are required to effectively apply it to investment; if modern AI is akin to a magic wand, wielding it skillfully involves understanding and innovating intricate “spells.” This is why opinions vary on AI’s potential in investment. Some are able to design models that deliver exceptional results; while others may struggle to outperform traditional methods. The ability to design high-performing AI models is the competitive edge that sets leading hedge funds apart.

Modern AI has already impressed the world with its capabilities in generating text (such as ChatGPT and Gemini), images (like DALL-E), and even videos (such as Sora). We believe AI is poised to revolutionize hedge fund strategies by effectively “counting the cards” and driving exceptional performance. As we stand at the forefront of this unfolding revolution, it is clear that the advantage of modern AI today may not yet be fully apparent, but we are confident that its adoption will be inevitable in the decade ahead. n

This content represents the views of the authors. It was submitted and edited under Pensions & Investments guidelines but is not a product of P&I’s editorial team.

Share Pensions & Investments’ content with your social community

All told, new launches are now less frequent and are being made at smaller size.

Next steps

As an allocator you have an enhanced ability to negotiate the fees you pay. You have likely picked great managers, but now is time to revisit to make sure the economics are equitable and reflective of the emergent competitive landscape. So what can allocators do?

Start by addressing the cash hurdle rate. If an allocator can earn close to 5% on cash, it seems reasonable to expect that benchmark should be applied when evaluating the alpha generated. We are not alone in thinking this. A group of allocators led by the $202 billion Texas Teacher Retirement System in Austin recently raised this point in an open letter to the industry.

Next, improve the alignment of interests by evaluating and challenging pass-through expens-

es related to the manager’s operations. Managers should bear their cost of their operations independently, not dilute the returns the investor achieves. Sometimes these can be difficult to distinguish from valid fund operational expenses, which are important independent control mechanisms (audit, admin, tax, custody, etc.).

Consider employing different firms — how long have you been with your current hedge funds? As with other services, it may make sense to shop around and see what

Finally, initiate an allocation to lower-cost hedge-fund-index replication products. Use it as a benchmark to assess your existing managers and whether the fees they charge are worth it. Take advantage of the liquidity in these products to remain fully invested during transition periods between managers or to increase the overall portfolio liquidity profile.

Ultimately, allocators have the fiduciary responsibility to protect clients’ assets.

Every dollar a manager charges is one less dollar available to the end investor. Hedge funds can play an important role in your portfolio, but teachers and firefighters should not subsidize their operations. Given the competitive landscape and the availability of new replication alternatives, now is the time to push back on high fees.

We're excited to offer the next level of article reprints! A stand-alone HTML digital article that will never be placed behind a subscription paywall. The P&I HTML reprint can be licensed to post to your website, share on social media, used in email correspondence, presentations and so much more.

Select from news articles (print and digital), rankings, opinion pieces, editorials, awards and more.

Contact Laura Picariello at lpicariello@crain.com or 732.723.0569 for pricing and details

Zhilei Xu and Yangfan Li are quantitative researchers and Renee Yao is the chief investment officer at Neo Ivy Capital. They are all based in New York.

Pension risk transfer activity

funding & buyout indexes

ETFs are making a move to the trading oor at NYSE

y B ARI I. WEINBERG

The “Home of ETFs” has put on an addition.

Over the last two years, the New York Stock Exchange, a unit of Intercontinental Exchange, has attracted more than 30 exchange-traded funds to the NYSE oor. Traditionally handling ETFs on its all-electronic Arca exchange, NYSE launched oor listing as an additional venue to attract issuers and products.

Despite higher aggregate listing and maintenance fees for oor treatment, some issuers say that the bene ts are worth the incremental cost.

In November 2022, xed-income specialist PIMCO was the rst asset manager to bring an ETF to NYSE. Switching the $4.8 billion PIMCO Active Bond ETF, or BOND, to the oor meant its trading would include the oversight of a designated market maker, obligated under exchange rules to facilitate opening and closing auctions and incentivized to maintain tighter trading spreads.

Other listing venues — Arca, Nasdaq and Cboe — all have programs and rebates designed to narrow spreads. And many ETF issuers have capital markets desks that can help guide investors on signi cant trades. But as the market has been ooded with new products, particularly actively managed stock and bond ETFs and those employing derivatives in their strategies, more issuers are looking for ways to demonstrate to prospective investors that their ETFs have tight spreads and ample liquidity.

The shift to the oor is part of the evolution of exchange-traded products beyond index funds. U.S. ETP listings now top 3,000, with roughly 60% listed on NYSE properties, and around 20% for both Nasdaq and Cboe. All three have trading and incentive programs designed to improve quoting and tighten spreads, though any adjustments to their rules have to be approved by the U.S. Securities and Exchange Commission.

For PIMCO’s BOND, average daily spreads were cut in half, ranging from 2 and 4 basis points since November 2022, compared to between 6 to 8 basis points for the immediately prior period, according to data provided by FactSet Research Systems. BOND competitors from J.P. Morgan Asset Management and Eaton Vance, a unit of Morgan Stanley, have also moved to the oor.

“A designated market maker can help the order book at size and add tightness to trading,” said Paul Weisbruch, head of ETF issuer services at GTS, which serves as DMM for 23 ETFs, including the entire suite of offerings from Strive Asset Management and TCW Group.

Strive, which has $1.5 billion in assets under management across 12 ETFs, took its products to the oor in January, while TCW, with $1.4 billion across six ETFs, moved in late May. Still, trading spreads in ETFs are also a function of the liquidity of underlying assets. For example, similar products from Strive and TCW that add governance preferences to a basket of the 500 largest U.S. publicly traded stocks, saw only marginal spread improvement, according to FactSet.

NYSE, the ETFs that had transferred to the oor through the second quarter of 2024 had seen average spreads cut to 18 basis points from 41 basis points, mostly experienced by smaller products with limited trading. Opening slippage, the drop in the expected price on market orders on open, fell to 25 basis points from 68 basis points.

“It’s a little bit of back to future,” said Douglas Yones, head of exchange products at NYSE. When ETFs rst listed on the American Stock Exchange in the 1990s, they were guided by specialists. “Now

we’re combining technology with a human element to solve a problem for some ETFs.”

A head-scratcher caveat

For years, ETF trading has come with caveats. “Avoid the open and close. Don’t place market orders,” distributors say. For those investors jumping to ETFs from mutual funds, this conversation was always a head-scratcher. Mutual funds only had one price. So, issuers new to the ETF market would need to either to SEE TRADING ON PAGE 17

Tackling plastic pollution in India

We believe that no company is perfect and as long-term shareholders, engagement, voting and research are key responsibilities for us. We see these as a way to mitigate business risks, protect against potential challenges and improve investment outcomes.

With a history of investment spanning over three decades in India, we are all too aware of the challenges the country faces when it comes to plastic waste and there is no escaping that plastic waste is a significant global environmental problem.

In 2016, we started on a journey to help tackle plastic pollution in India.

Find out more

This material should not be construed as an offer, invitation, recommendation or inducement to distribute or purchase securities, shares, units or other interests or enter into an investment agreement.

P&I: Is it ‘prime time’ for CLOs today?

PRIME TIME FOR CLOs

For institutional investors looking for diversifi cation strategies, collateralized loan obligations can be a stable option that provides downside protection in an uncertain macro environment. A market that tops $1 trillion, CLOs are floating-rate instruments that sit within the larger structured credit market. They have different tranches, each with its own risk-reward profile, cash flow structure and credit rating. As such, CLOs can fit into different allocation sleeves within an institutional portfolio. CLO managers Barings, Polen Capital and Sycamore Tree Capital Partners dig into current market dynamics and the potential impact of lower rates on the asset class. They unpack what increased CLO issuance means for investors and highlight manager characteristics needed to successfully navigate this market.

“It definitely is prime time for CLOs,” said Adrienne Butler, head of global CLOs at Barings. “We have seen stars align across the industry, both on the issuance side and on the investing side, which makes it a potentially beneficial time to be invested in CLOs.” The firm has seen strong demand for floating-rate products up and down the capital stack, from triple-A rated to equity tranches, she said.

The macro environment, with uncertainty around economic growth and interest rates, is supportive. “Having a diverse pool of assets in a time like this is really important because you don’t have complete visibility on where rates are going to go or on any kind of exogenous shocks or geopolitical events,” Butler said. “Having a highly diverse pool that you can invest in provides you a degree of confidence in what might be a more volatile market.”

CLOs have gained popularity among institutional investors as they have evolved from a niche product to a broadly used fixed-income alternative, according to Jack Yang, co-founder and president of Sycamore Tree Capital Partners. In addition, the user base of the asset class has expanded beyond banks and insurance companies to include, notably, public pension plans, endowments and asset managers.

“We see CLOs gaining utilization in portfolios, similar to how high-yield bonds and bank loans have done previously. This is now a thoroughly researched, $1 trillion market that offers potential return, diversification and hedging benefits versus traditional fixed income,” Yang said. “With asset managers, pension funds and even mutual funds increasingly investing in CLOs, you could over time see the size of the CLO market grow dramatically, even double from where it is today.”

P&I: What’s driving strong CLO deal volume in recent years, and do you expect that to persist?

Lower rates driven by the Federal Reserve’s easy-money policy after the Great Recession and then following the pandemic helped increase interest in CLOs, and refinancing was a major component that benefitted borrowers. But in the subsequent higher-rate environment, the question is whether the factors that drew borrowers and lenders to the CLO market will remain.

“We have seen stars align across the industry, both on the issuance side and on the investing side, which makes it a potentially beneficial time to be invested in CLOs.”

— ADRIENNE BUTLER, BARINGS

Jim Stehli, co-lead of the CLO platform at Polen Capital, pointed out that CLOs have become the largest securitized asset class, another contributor to its use and popularity. “Its size and scale provide investors with a large enough investible universe, across the whole rating spectrum, to consider as part of either a fixed-income allocation or an alternative investment allocation,” he said. “The market size is important, and from a product features perspective, structure is one of the key components of CLOs. The product has been performing well for over 25 years — it’s been tested through various cycles.”

Stehli said that he expects that two components that have emerged relatively recently — tighter credit spreads and relatively calm markets — will keep interest high in CLOs. Through midyear, volumes on broadly syndicated loan CLOs as well as new issue middle market and private credit CLOs are up 80% over last year, he noted. “On top of that, you’ve got a huge refinance and reset cycle happening,” he said. “In both cases, these outcomes are largely driven by tighter credit spreads overall and relatively lower volatility, allowing investors to participate in these deals.”

“With record CLO issuance expected in 2024, we anticipate continued growth in CLO volume due to attractive conditions for both assets and liabilities,” Yang said. Sycamore Tree Capital Partners is seeing investor demand for CLO debt and equity grow as well, with both existing and new investors increasing capital allocations.

The combination of institutional investors’ positive return experience over the last 14 to 15 months and the level of CLOs being called and refinanced is likely to keep volume humming, Butler said. “Even with possible rate cuts on the horizon, there is still demand for floating-rate products right now” with new issue and refinancing activity garnering demand from investors who are receiving repayments of existing exposure to CLOs, she said. “CLOs, in general, offer attractive relative value compared to other fixed-income or floating-rate products, and the market remains an attractive place to invest.”

P&I: What’s your outlook on the current rate cycle, where we may be at the peak on interest rates, and its impact on CLO assets as well as underlying loans by borrowers?

“While we expect the inverted yield curve to normalize, we see rates reverting to levels consistent with long-term historical averages, not the near-zero rates

created by global government interventions since the great financial crisis,” Yang said, adding that Sycamore Tree expects to see base rates of 3% to 4% over the next few years. “We see CLOs having ongoing attractive relative value compared to other corporate and structured credit.”

With the Fed poised to embark on its interest rate cutting cycle, Butler said, lower rates could bode well for the CLO market. “That’s a positive that would lead to lower cost of capital and increased cash flows for the underlying loan issuers in the portfolio,” she said. In addition, “lower rates may very well trigger an upsurge in M&A activity, which could increase loan volume and ultimately help to create additional diversity and growth within the CLO market.” Once base rates are cut to some degree, she noted, that could boost consumer-related sectors, such as retail services.

Even when rates come down, CLOs will likely remain attractive relative to other credit vehicles, such as investment grade and high yield, Stehli said. “Most economists seem to be forecasting a target fed funds rate of 3.5% to 4% by late 2025 into 2026,” he said. “That’s still a far cry from where we were at 0% post-COVID into early 2022. Despite CLOs being floating-rate instruments, there remains an implied risk-free base rate of 3.5% to 4%. Triple-A rated CLOs are still pretty attractive, yielding at 5%-plus, while the entire CLO stack is going to be closer to 6.5% to 7%-plus. We think that’s going to represent an attractive potential return compared with investment grade and high yield overall.”

P&I: Looking ahead, are you concerned about rising corporate defaults and their impact on the CLO market?

For CLO managers, keeping a close eye on defaults is a critical function that’s related to the economic backdrop. “We follow very closely what’s going on in the fundamental economy of the United States,” Yang said. “The bank loan market is a relevant microcosm of the overall economy, so a lot of our call on what happens with defaults is a function of our outlook on the economy.”

default rates, but it’s important to be cautious and committed, and also to be involved in liability-management exercise activity. Having a deep research team with experience in the market, understanding those LME activities and having the market relationships are going to be really important,” Butler said.

P&I: Where do CLOs best fit within an institutional portfolio?

The wide range of institutions active in the CLO market, from insurance companies and pension funds to hedge funds, is a proof point of the asset class’s versatility.

“CLOs can fit into a variety of different portfolios,” Butler said. “How you categorize the asset class depends on where in the capital stack you’re investing. This versatility also speaks to why we’re seeing this as a compelling time for CLOs. Up and down the capital structure, everybody seems to be finding something to meet their needs.”

“Throughout the CLO stack, investors can add spread, even as they’re adding protection to the downside through the CLO structure and diversification through the collateral.”

— JIM STEHLI, POLEN CAPITAL

He added, “Over the next six to 12 months, we’re constructive. We’ve seen defaults moderate and even come down some from the peaks of ’22 and ’23, post COVID, post the Ukraine invasion. However, I would also say there’s been an uptick in out-of-court restructurings to right-size capital structures.” In any scenario, he said, a CLO manager’s goal should be to avoid defaults and minimize risk as much as possible. “It’s impossible for any manager to outright avoid all ratings downgrades and defaults, but the better we are at identifying and designing process and risk management, the better manager we become.”

“CLO managers are paid to be concerned about defaults,” Stehli said. “Historically, managers have focused on creating upper-tier performance compared with a broader leveraged loan index and, ultimately, managing against the downside of that broader loan market. Defaults are a concern, and that’s what managers are paid to be focused on.”

However, lower rates should bode well for defaults, as they could ease the burden on companies that might be feeling the strain of higher rates. “If we’re at a point where you’ve got many companies that are performing relatively well even in today’s higher rate environment, one would expect that if rates fall from here, that outcome should result in a more constructive backdrop for CLO managers,” Stehli said.

While Barings’ team is seeing default rates leveling off, that doesn’t mean they are any less focused on them. “We’re not overly concerned about a spike in

It depends on the institutional allocator’s portfolio goals, said Stehli.

Since CLO bonds offer a floating rate with a defined reinvestment period and a maturity date along with quarterly coupon payments, “it’s logical to consider including CLO debt in a fixed-income portfolio,” Stehli said. “Meanwhile, CLO equity, in particular, tends to be less liquid, and with a target return of, say, mid-teens, coupled with a more illiquid nature, Polen Capital believes that it’s also desirable to include an allocation to CLO equity as part of an alternative investments portfolio.”

“CLOs have the potential to improve the risk-adjusted returns of portfolios, given low correlation to many asset classes,” Yang said. “Fit varies based on the part of the CLO where the allocator is investing. Floating rate, triple-A through single-A CLO bonds add attractive yield and diversification to core-plus portfolios focused on income and capital preservation. CLO mezzanine debt and equity are being included in return-seeking portfolios, such as opportunistic credit, and in private-market allocations as a complement to direct lending and private equity.”

P&I: Which tranches or ratings should investors focus on to meet their portfolio objectives for yield and diversification?

“Throughout the CLO stack, investors can add spread, even as they’re adding protection to the downside through the CLO structure and diversification through the collateral,” Stehli said.

“By defi nition, CLOs off er diversifi cation on an underlying pool of leveraged loans. Regardless of which tranche you’re looking at — triple A, double B, equity — investors are receiving the benefit of diversification and, therefore, that element of downside protection,” he explained.

“CLOs also offer a pickup in spread to investment grade and high yield,” with 6% to 7% yields on single-A to triple-A rated CLOs attracting U.S. institutional investors, as well as Japanese banks, while the CLO exchange-traded fund market is also drawing the interest of retail investors, he said.

“It depends on what your investment objectives are,” Butler said. “What we’re seeing is that tranches from both top-tier and second-tier managers, as well as across the capital stack, are trading close to par today,” she said. “And the spread basis between the various profi les of deals and tranches have compressed, meaning that differences between managers, between styles, between subordination levels are starting to compress because of the demand. So as

an investor, you want to be very picky with and lean toward high quality investing and liquidity.”

Yang added that one of the key benefits of CLOs for institutional investors is that they can offer a wide range of options from the standpoint of risk, return and liquidity. “Depending upon their objectives, investors can choose how they gain exposure to an actively managed, diversified portfolio of senior secured, fl oating-rate loans with the benefit of stable, long-term, non-markto-market leverage,” he said. For example, triple-A rated CLO bonds can be a good complement to core fixed income while CLO mezzanine debt and equity can be used to deliver income and total return.

P&I: What is your outlook on CLO spreads/ yield against public fixed income and private credit for this year and next?

“CLOs have the potential to improve the risk-adjusted returns of portfolios, given low correlation to many asset classes. Fit varies based on the part of the CLO where the allocator is investing.”

“We remain constructive on 2024 for spreads, as rates remain high and credit spreads, in general, are tight but not necessarily at all-time tight levels,” Stehli said. “We are constructive on CLO triple-A’s, given the large demand for a performing floating-rate bond from U.S. and global banks. Our view is that an investment in triple-A rated CLOs provides a fair return with significant downside protection.”

— JACK YANG, SYCAMORE TREE CAPITAL PARTNERS

Yang pointed to the return potential. “CLO bonds generally provide higher returns than comparably rated corporate bonds due to complexity premiums, despite their attractive performance and protections,” he explained. “The relative value of CLO bonds is likely to continue to be attractive versus conventional fixed income in the year ahead, given they’re priced off of the short end of the yield curve with floating-rate spreads.”

Whether spreads tighten or widen, CLOs look attractive with redeeming qualities in either situation, Butler said. “We’re in a pretty good spot right now in terms of liability pricing relative to prior years,” she said. “We’ve got decent visibility into the asset class with a stronger forward pipeline over the next several weeks. Defaults have stabilized. We expect to see more new-issue loan activity, and that creates a more diverse pool of assets to draw from. So, ultimately, we think CLOs should be a solid investment over the next few years.”

P&I: What are some characteristics of a CLO asset manager that are key to delivering consistent long-term performance?

Track record is critical. “Research shows that top-quartile managers have historically delivered significant relative outperformance,” Yang said. “Our battle-tested experience across credit and market cycles has taught us that disciplined focus on capital preservation supports consistent, long-term performance.”

In addition to a manager’s performance track record, institutional investors

should know whether a manager has successfully navigated different market cycles. “A rising tide lifts all boats,” Yang said, “but it’s market volatility that really tests a manager’s skill and also creates opportunity — the most opportunity, in fact, for the managers to differentiate themselves and create value for their investors.”

“We think that the most important litmus test of evaluating a manager is their performance, particularly during volatile markets,” Yang said.

“The No. 1 takeaway is making sure you have a focus on quality research,” Butler said.

“Having a deep and experienced research team is key. There’s no amount of spread that can make up for a high level of defaults. You want to make sure that you’re buying the right credits and minimizing defaults.”

Beyond that, she added, a CLO manager must have specialized teams that are experienced in structuring and legal review.

“As a manager, we tend to be more conservative in our approach to managing assets and credit quality,” Butler said. “We’re never going to stretch for spread. We’re always going to make sure that our credit quality is top of mind.”

It comes down to process, said Stehli, which can translate into performance. “We believe in protecting against the downside and not overreaching,” he said. “CLO portfolios that are thoughtfully constructed on day one and are underwritten throughout the CLO lifecycle tend to perform better. We prefer a balanced portfolio construction process that provides for a healthy level of diversification.”

P&I: What’s an underappreciated fact about recent — or historical — performance of CLOs that’s interesting?

While CLOs have been around for decades, their qualities of diversifi cation, return generation and resilience are still sometimes a positive revelation to even experienced institutional investors. “The long-term, stable leverage of CLOs creates stability and optionality for investors, yet some allocators are surprised that the highest-returning CLOs, ever, were issued in 2007, right before the global financial crisis,” Yang pointed out.

In addition, investors may not know that in more than 14,000 rated classes of CLOs, just about 20 have defaulted, Stehli said. “All those defaults were in the 2020 era, and all were double-B or single-B rated, so nothing at the triple-A, double-A, single-A or triple-B level.”

Butler added, “Not only have there been no defaults in the triple-A part of the stack, but as of June 2024, S&P reported that no triple-A tranches were even downgraded over nine straight years — which further emphasizes the investment’s stability.” ■

Trading

build up an ETF capital markets desk or work with a third-party platform to support those investor conversations.

“This solution outsources some of the capital markets desk,” Yones said.

That was de nitely the case for Sound Income Strategies, which moved its two ETFs to the oor on June 21.

“We were getting investor feedback that trading spreads had to improve before larger brokerage plat-

Second private credit ETF ling lands within days of Apollo’s

The starting gun has of cially red in the race to launch the rst private credit exchange-traded fund.

An application for the BondBloxx Private Credit CLO ETF landed with regulators on Sept. 12, lings show. Subject to regulatory approval, the proposed fund would invest at least 80% of its assets in collateralized loan obligations, which will be backed by a pool of loans made to private companies.

The BondBloxx ling lands just two days after Apollo Global Management Inc. and State Street Corp. submitted plans for a fund that will include private credit. Demand from retail investors for private securities has boomed alongside the industry itself, with private markets now worth more than $13 trillion. That has investment giants such as BlackRock and Invesco looking for avenues to provide such exposure — a quest that will “absolutely” generate many more ETF lings, according to Todd Sohn of Strategas.

“The ‘private label’ marketing war has commenced,” said Sohn, ETF strategist at Strategas. “Some of the exposures will be attractive, interesting solutions. Others will probably be gimmicky.”