Amid geopolitical turmoil, institutional investors are seeing the appeal of the traditional in ation hedge

y B CHRISTOPHER MARCHANT

Institutional investors are looking for a Midas touch when it comes to their portfolios, with greater recent interest in gold among pension funds.

However, it’s not simply mythological levels of wealth they are seeking. It’s more a matter of valuing the commodity’s well-known role as an in ation hedge

and its role in protecting portfolios against geopolitical turmoil, such as the potential for upcoming volatility associated with the U.S. presidential election in November.

In June, the A$223 billion ($143.2 billion) Future Fund, Melbourne, con rmed plans to add exposure to gold within its portfolio.

The glittering asset was trading at

How large hedge funds are navigating the AI revolution

The boom in generative arti cial intelligence is both new and old for some of the world’s largest hedge funds. Many have had teams focused on machine learning for years, but are now trying new use cases. Pensions & Investments spoke with AQR Capital Management, Balyasyny Asset Management and Man Group about how they are thinking about AI, where AI staff t in their rms, the skill sets they are looking for and how AI is being applied.

Over the past several years, AI has broadly transitioned from the back-of ce technology domain at asset managers, to a focus on “actionable insights that impact the

$2,326 an ounce on July 1 — up 12.5% vs. Jan. 1, when one ounce was priced at $2,068. A June report by the World Gold Council showed that institutional investors are at least interested in getting in on gold’s rally, with at least 85% of North American institutional investors andnancial advisers now having some holding in the product.

Another big investor, the ¥254.7 trillion ($1.58 trillion) Government Pension Investment Fund, Tokyo, in March called for information on asset classes that it does

Defined Contribution

Large-cap funds led changes to 401(k) lineups in a busy year

U.S. corporate plans nearly double the lineup changes in 2023 compared to 2022

y B ROB KOZLOWSKI

Well over 100 U.S. corporate 401(k) plans made changes to their investment option lineups in 2023. That's nearly double the number that disclosed changes the previous year, with 401(k) plans in 2023 saying changes to active domestic large-cap growth equity options dominated.

DISPERSION: Callan’s Greg Ungerman

The number of plans that made changes in 2023 was up signi cantly from the prior year. Pensions & Investments compared 819 corporate 11-Ks led with the Securities and Exchange Commission between May 14 and June 28 with similar lings in 2022. For 2023, slightly less than 15% of 11-K lings showed retirement plans that made at least one investment option change during the year, with the majority affecting individual active equity options, P&I's analysis of recently released 11-K lings showed.

Last year's 847 corporate 11-K lings found that 65 U.S. corporate 401(k) plans, or just under 8%, added or

Amy McGarrity, chief investment of cer of the Colorado Public Employees’ Retirement Association, considers the pension fund’s emphasis on internal money management a signi cant competitive advantage over its peers.McGarrity has a staff of about 60 people across all asset classes, administration and operations who have the responsibility of managing most of its global equities asset class, and the entirety of its xed-income portfolio in active management.

“We believe that is a competitive advantage for Colorado relative to our peers and relative to other state pension plans,” said McGarrity. “Every year we run an estimate of what those cost savings are, and last year was $65 million.”

McGarrity said what has also helped considerably is the strong support of PERA’s board and a compelling compensation package, and what also helps is the attractiveness of the Denver metropolitan area as an appealing place to live.

“I think we have a combination of

Wayne E Wilson/Getty

IN THIS ISSUE

ESG

The EU’s ambitious effort to help investors gain more clarity about their ESG investments is sowing confusion. Page 4

Washington Crypto is emerging as an electoral issue. Some say it’s typical ‘pay-to-play’ Washington politics. Page 6

Money Management

BNP Paribas is in talks to acquire AXA Investment Managers, a deal that would create a $1.64 trillion money manager. Page 6

Special Report:

Artificial Intelligence

Fixed income and equity managers are already reaping the bene ts of generative arti cial intelligence and machine learning.

Page 18

The AI boom is fueling investments in data centers and infrastructure, but raising questions about how much power is needed. Page 19 AI is becoming an important resource in sustainable investing — but its application is also growing as a governance issue. Page 20

RE manager survey in progress

Responses to Pensions & Investments' annual survey of real estate investment managers are due by Aug. 30. Firms managing private real estate assets or REIT securities for U.S. institutional, tax-exempt clients are eligible to participate. Results will run Oct. 7. To request a survey or obtain further information, please contact Anthony Scuderi at ascuderi@ pionline.com or 212-2100140, or visit www.pionline. com/section/surveys

William Blair’s Braming exploring ‘the unobvious’

If active managers are judged on their ability to outperform the crowd and nd alpha while the rest of the herd looks elsewhere, unobvious parts of the market would be a good place to explore.

That's proving to be a good tactic for William Blair Investment Management, the $72.4 billion manager where Global Head Stephanie Braming and her team are nding opportunities — and client interest — in those “unobvious spaces that are adding value” right now, she told Pensions & Investments in an exclusive interview.

Take developed vs. emerging markets in terms of treading the untrodden path for regional allocations. All eyes right now are on developed markets' central bank moves and whether in ation’s new normal will remain above the traditional 2% target. Frontier markets — countries that are too small or not liquid enough to be deemed an emerging market, such as Kazakhstan and Vietnam — are proving to be of interest with consultants, and one of the rm’s “top ideas,” she said.

“In some ways, it’s the unobvious space relative to, like, private credit. And it’s really personally intellectually interesting to me because it’s just so

far out of my own investment experience,” Braming said. The rm’s rst emerging markets debt strategy

Pensions & Investments is accepting entries for the 2025 Eddy Awards, an annual program recognizing plan sponsors and service providers that exhibit best practices in offering investment and nancial education to de ned contribution plan participants.

The deadline for completing the entry in the online system is Sept. 13.

All materials — including participant communications distributed as part of a de ned contribution education campaign — must be included as part of the online entry, via PDFs of printed materials, high-resolution JPEGs or website links. Regardless of whether they were dis-

Netherlands-based rm NN Investment Partners.

Percentage-based formulas disproportionately bene t higher earners, Vanguard says

Even in their generosity, employers can unwittingly be unfair.

That's one of the biggest takeaways from a new Vanguard report that looks at the 401(k) matching contributions that employers typically put into employees' retirement accounts.

Employers labor over the right matching formula, with many choosing to match 50 cents for every dollar employees put into their accounts, up to 6% of their pay.

The popular “50% on 6%” match, however, has some shortcomings in that it rewards higher-paid workers more. Employees making $100,000 who contribute 6% of their pay, or $6,000, to their accounts get an employer match of $3,000. Those making $50,000 can

tributed to participants in print or online, entry materials must be submitted online.

Complete rules and entry forms are available at pionline.com/EddyEnter . Campaigns must have been launched no earlier than Jan. 1, 2023.

Sponsors of plans of all sizes are encouraged to enter, with materials judged against those from their peers based on the number of participants. Record keepers and retirement plan advisers can submit their own generic entries or in conjunction with plan sponsor clients. In the latter instance, both will receive trophies for a winning entry.

Winners of the Eddy Awards will be announced at P&I's annual East Coast De ned Contribution Conference

only get $1,500.

One way to make the employer matching contribution more equitable is to cap the dollar amount. Employers could, for example, cap the match at $2,500, so that all workers — regardless of income — would have a chance at receiving the same maximum employer contribution.

Traditional percentage-based matches, such as 50% on 6%, are “disproportionately owing to top earners,” said Fiona Greig, global head of investor research and policy at the Vanguard Group, summing up the topline nding of Vanguard's report released in May.

If employers want to promote retirement security among their workers as their “North Star,” employers need to start thinking about who needs the match dollars most and how they can channel the money “to move the needle on retirement security to the greatest effect,” she said.

Of the estimated $200 billion that employers contribute to workers’ retirement

March 9-11 in Fort Lauderdale, Fla.

The award categories, in alphabetical order, are:

Conversions: This category recognizes campaigns devoted to explaining the move to a new record keeper. This category also includes consolidation of record keepers by 403(b) plans. All ongoing investment education materials do not have to be included.

Financial wellness: Workplace experts increasingly warn that employees' nancial stress can damage their productivity, health and ability to retire. This category aims to recognize efforts that take a holistic view of employees' nancial wellbeing outside of traditional retirement programs. Those efforts should

include, but are not limited to, education or tools regarding student loans, health savings accounts, emergency savings and debt reduction, and household budgeting. Ongoing investment education: Entries should educate existing employees on the investment options of the plan and how it helps them save and reach their retirement goals, or new employees about investment options of an existing plan. Entries must focus heavily on the investment process. Note: Campaigns aimed at educating participants on the importance of saving in their dened contribution plan for retirement, via their 401(k) plan, for example, can be included in this

came as a result of a team liftout from The Hague,

‘INTELLECTUALLY INTERESTING’: William Blair Investment Management’s Stephanie Braming.

Blue Owl: ‘Golden age’ falls short in describing the private credit boom

$1.7 trillion segment is a sustainable, ‘go-to’ asset class, co-CEO maintains

y B LYDIA TOMKIW

Blue Owl Capital co-CEO Marc Lipschultz doesn’t think it's a golden age for private credit, saying that’s the wrong frame of reference for the booming investment space.

“This paradigm of the golden age is too much about some golden moment … but the de nition of golden moments is there’s something unique and probably not sustainable about why it worked. And then the golden age passes,” Lipschultz said in an interview at Blue Owl’s New York of ce.

“I actually don’t see that analog because we weren’t trying to be the gold miners. I mean to switch metaphors, but probably appropriately, we always talk about being the picks and shovels to the gold miners.” Blue Owl, which was born out of Owl Rock Capital Group and Dyal Capital Partners agreeing to merge

in 2020, manages over $174 billion in assets as of March 31, investing across credit, GP strategic capital and real estate.

Lipschultz sees the purpose of private credit as a “go-to reliable, long-dated solution” for a multitrillion-dollar leverage lending marketplace, with Blue Owl following the three “Ps” of direct lending: predictability, privacy and partnership.

“What we’re trying to do is a steady production of attractive, risk-adjusted returns. And others can mine for gold, and they will have golden eras and dark periods,” he said. “We’re trying to stay in a much steadier band, and that’s been working, and I think will continue to work.”

The rapid growth in the private credit segment in recent years, now estimated by Preqin at $1.7 trillion, has brought questions about potential cracks. Lipschultz said from his seat, “we’re still in a very healthy place” and he doesn’t see cracks, but added, “it doesn’t mean there won’t be someday.” Blue Owl manages $91.3 billion in credit strategies,

‘SUBSTANTIAL

HUBRIS’: Arizona Public Safety’s Mark Steed said a pullback could be coming for managers.

Ohio State Teachers compensation ght spotlights public pension plan pay scales

A ght over compensation at one of Ohio's largest public pension funds has turned a spotlight on other retirement plans' pay packages, and intensi ed scrutiny of how much pensions funds' investment staff are paid.

Some public pension funds are

under increasing criticism from members regarding what they perceive as excessive investment staff compensation. The average annual salary of a CIO at a public pension plan was $277,000, according to the 2022 NCPERS Public Pension Compensation Survey. Including bonuses, the average CIO earned $517,000.

In many cases, however, public pension staff members are paid less compensation than staff at university endowments and private-sector money managers. By far the most visible pension fund that has faced criticism in recent years is the $94.5 billion Ohio State Teachers’ Retirement System,

Arizona Public Safety CIO sees ‘existential crisis’ in private equity

Arizona Public Safety Personnel Retirement System, Phoenix, has bene ted from outsized contributions in recent years that have allowed it to become a liquidity provider in private equity deals. But an existential crisis is afoot in the asset class, which means the pension fund and institutions like it are practicing greater caution in pulling the trigger on deals, said Mark Steed, chief investment of cer.

Steed and the multiemployer retirement

system have been aided in recent years from a massive ongoing project to shore up its funding, working with more than 300 municipal, county and state public safety-related employers whose assets feed the system to increase their contributions.

Arizona PSPRS had hit a low point with a funding ratio of 46.9% as of June 30, 2020, but improved three years later to 66.3%. The funding ratio for this latest scal year is pending the actuarial valuation.

While there is still plenty of work to do,

Lower interest rates may boost fixed income, hurt private credit

PSPRS has experienced a signi cant spike in system assets that made it the fastest-growing U.S. retirement plan in the three years ended Sept. 30, according to Pensions & Investments data.

During a period of signi cant market volatility, the system’s assets grew 81.7% to $19.8 billion as of Sept. 30 from $10.9 billion three years earlier thanks to those outsized contributions. PSPRS now has about $21.3 billion in assets.

A cut in interest rates in September seems to be a foregone conclusion, and chatter has turned to how aggressive an approach the Fed will take. Should longer-term yields continue declining, pension funds’ U.S. xed-income assets will likely bene t. However, private credit funds could see their outsized returns under pressure, since they typically

Fixed allocation: Large pension funds have a signi cant allocation to U.S. xed-income assets. The class made up about 20% of the largest pension plans’ assets, although that’s down from the nearly 25% held in 2019.

Largest U.S. pension funds’ fixed-income allocation

D r opping yields: 2- and 5-year

Tr e a sury yields peaked in October at 5.1 % and 4.9%, respectivel y. They’ve dro p ped si nce due t o economic data, including slowing in ation. The 2-year yi el d s tood at 4%, and the 10-year yield was 3.96%, as of Aug. 7.

U.S. Treasury yields

Locking in yields: U.S. corporate high-yield bonds currently have a 7.71% yield to worst. Although down from nearly 10% at the end of the third quarter of 2022, it’s high compared against the past 10 years. Investment-grade securities, represented by the Bloomberg U.S. Aggregate Bond index, have a 4.51% YTW. The YTW averaged 2.7% from 2014 through 2023.

Yields to worst

Private credit reversal?

North American private credit funds have bene ted from higher short-term interest rates, returning a cumulative 65.9% over the ve years ended March 31. With the Federal Reserve poised to cut rates, though, returns could slow.

North American private credit vs. U.S. corporate high yield

bold climate transparency push hitting snags

say the legal requirements aren’t clear and too many data gaps exist. And key de nitions within the EU Sustainable Finance Taxonomy, which underpins understanding of what can be classi ed as “green,” haven’t been fully decided yet.

Three years in, the European Union’s most ambitious effort to help investors gain more clarity about environmental, social and sustainability characteristics of their investments continues to sow division and confusion.

Investors say they’re inundated with details. Investment managers

There is broad consensus that the launch of the EU’s Sustainable Finance Disclosure Regulation, which aimed to create a common, transparent framework that allowed investors to more easily compare investments — and reduce greenwashing — has been less than optimal.

“SFDR still has to address several de ciencies such as unclear legal

concepts (e.g. de ning exactly what sustainable investment is), low quality data reported by the investable companies or the misuse of SFDR for marketing purposes,” according to Joanna Frontczak, senior impact equity analyst at Swiss investment management rm Vontobel, which had AUM of 206.8 billion Swiss francs ($230 billion) as of Feb. 29.

However, recent joint recommendations by the European Supervisory Authorities have proposed a way forward.

Introduced across the European Union in March 2021, SFDR aimed to let investors know the green and

ESG-related credentials of investment strategies through the introduction of a reporting framework for funds.

As it stands, the technical and detailed approach of SFDR can make it challenging for pension fund clients to understand the signi cance of certain data points, such as the emissions of inorganic pollutants or even a rm’s anti-bribery policies. So much granular information “can lead to more confusion than clarity,” according to Elisabeth Ottawa, head of public policy for Europe at Schroders, a U.K asset management rm with £751 billion ($949 billion) in

AUM as of Dec. 31.

SFDR currently categorizes funds as Article 6 — which do not integrate any kind of sustainability into the investment process; Article 8 — promoting ESG compliance; and Article 9, which are strategies with investments that speci cally target sustainable outcomes.

An investor shorthand for these three classi cations has been “brown” for Article 6, “light green” for Article 8, and “green” for those most ESG leaning and classi ed as Article 9.

Following SFDR’s introduction, sustainable fund ows do appear to have reacted positively. The proportion of Article 8 and 9 funds as part of the universe of EU funds in scope for SFDR reached 60% in the rst quarter of 2024, up from 33% in the second quarter of 2021, according to data from Morningstar Manager Research.

Soon after its introduction, there became a belief that SFDR, which was created as a disclosure and reporting framework, had become a “de facto labeling regime,” said Stuart Burnside, head of product governance and ESG product at M&G Investments, a U.K. rm with £343.5 billion AUM as of Dec. 31.

“I think SFDR was actually a reasonable and effective instrument, which people have then used to play the wrong tune,” Burnside said.

Perceived problems within SFDR deepened as 2022 drew to a close, when large asset managers such as BlackRock and HSBC Asset Management downgraded Article 9 funds to Article 8, and Article 8 funds to Article 6 as criteria was tightened.

The investment community has been anticipating the key signals to

anticipating it, but there might be more to

Don’t miss our opening keynote, where we’ll cut through the noise and attendees will learn how to stay flexible and navigate the ever-changing markets from a seasoned investment professional. Register now to gain these invaluable insights and position yourself ahead of the (inverted) curve!

The ‘Level 2’ of the regulation’s Regulatory Technical Standards, effective in January 2023, added elements such as requiring investment rms to align their ESG disclosure with the principal adverse indicators reporting framework, which identied ESG risks within an investment strategy, and share detailed information on how to avoid such adverse ESG effects of a fund.

Arthur Carabia, director of ESG policy research at Morningstar Sustainalytics, notes that “as with most EU regulation, enforcement is primarily executed by national regulators, with European Securities and Markets Authority oversight.”

Recent developments

A recent feedback report, published in May and authored by the European Commission and taking views from 324 organizations and individuals with insight into the market, showed ongoing division on how to x SFDR. For example, 56% of respondents believed that the EU should impose standardized disclosure requirements for all nancial products. According to the report, a large majority of respondents also called for these disclosure requirements to be simpli ed and streamlined across the sustainable nance framework.

Following this report, joint recommendations by the European Supervisory Authorities to the European Commission, published in June this year, proposed a way forward. The reported stated that SFDR categories should be simple with clear objective criteria or thresholds to identify which category the product falls into. The ESA encouraged

You are invited to register with 500 euro discount

We are honoured to present our CIO opening panel: POWERING-UP FOR THE NEXT INVESTMENT ENVIRONMENT

Sneak-preview of our speaker faculty:

ANNETTE MOSMAN CEO APG

MICHELLE OSTERMANN CEO PENSION PROTECTION FUND (PPF)

KEVIN BONG Director, Chief Investment Strategist & Head of Singapore ALBERTA INVESTMENT MANAGEMENT CORPORATION (ASIA PACIFIC)

GER JAARSMA Chairman PENSIOENFEDERATIE (FEDERATION OF THE DUTCH PENSION FUNDS)

THOMAS CURRAN Professor of Psychology, Author of the Perfection Trap LONDON SCHOOL OF ECONOMICS

YOU ARE INVITED TO REGISTER SUMMER500WPS Asset owners/Plan Sponsors can apply for a complimentary delegatepass

PEDRO ANTONIO GUAZO ALONSO Representative of the Secretary-General for the investment of the UNJSPF assets UNJSPF

SANYA GOFFE Attorney and Eisenhower Fellow PRESIDENT OF THE PENSION INDUSTRY ASSOCIATION OF JAMAICA (PIAJ)

LAURA CHAPPELL CEO BRUNEL PENSION PARTNERSHIP

AEISHA MASTAGNI Portfolio Manager CALSTRS

CHRISTOPH JUNGE Head of Alternatives VELLIV

Crypto emerges as election issue but opinions vary on why

y B COURTNEY DEGEN

There’s no question that crypto is talked about in the political arena, but opinions vary on why the topic rose to prominence and how it would impact electoral outcomes.

The fact that cryptocurrency made it into the 2024 Republican platform is “a pretty big deal,” according to Sheila Warren, CEO of the Crypto Council for Innovation, a trade group advocating for cryptocurrency.

However, “the reality is this election is just not about crypto or digital assets,” Warren said. "There’s no

question it is an issue … but it is not the issue of this election,” she added.

Warren’s view differs from crypto rms and advocates who insist that voters will base their decision on whether or not a presidential candidate is “pro-crypto,” and the Republican Party seems to be listening.

In its 2024 platform, the GOP pledges that “Republicans will end Democrats’ unlawful and unAmerican crypto crackdown and oppose the creation of a Central Bank Digital Currency. We will defend the right to mine bitcoin, and ensure every American has the right to self-custody of their digital assets, and trans-

act free from government surveillance and control.”

Ripple representatives attended the Republican National Convention, and the company plans to attend the Democratic National Convention as well, with the goal of “education,” and to “spread the messaging of where our smart policies are intersecting with greater kind of American policies,” said Lauren Belive, head of U.S. policy at Ripple, a cryptocurrency rm. Coinbase, another crypto rm, also sent representatives to the RNC, according to reporting from Politico.

Belive contended that this year's

election cycle is a "pivotal" one for the cryptocurrency industry at large.

However, some contend that the crypto industry merely bought its way into the conversation.

“The only reason people are talking about crypto, currently, so much is because of the amount of money they are spending to buy politicians to push their special interest above every other priority of the American people,” said Dennis M. Kelleher, co-founder, president and CEO of Better Markets, a nonpro t that describes itself as a Wall Street and government watchdog.

According to OpenSecrets, both

Coinbase and Ripple are ranked in the top 10 of organizations making the most contributions — including those to candidates, party committees, PACs, 527 organizations and outside groups — in the 2024 election cycle. OpenSecrets tracks contributions “from the organization's employees and members, its PAC and the organization itself, only when it gives to outside groups,” according to its website.

“Despite the industry's rhetoric around this, the shift in position from policymakers in Congress and other parts of Washington is not based on the substance of the industry's policy arguments,” said Mark Hays, senior policy analyst at Americans for Financial Reform, a nonpro t advocating for nancial reform, and Demand Progress, a nonpro t progressive advocacy group.

BNP Paribas Group is in exclusive talks to acquire AXA Investment Managers in a €5.1 billion ($5.6 billion) deal that would create a €1.5 trillion money manager.

Under the deal, which is subject to regulatory approvals, BNP Paribas would also enter into a long-term strategic partnership to provide investment management services to parent company AXA, separate news releases said.

The proposed deal is expected to complete in mid-2025.

BNP Paribas’s money management unit, BNP Paribas Asset Management, had €576 billion in assets under management as of June 30, with €338 billion in institutional AUM. Of its total AUM, €382.8 billion is classi ed as ESG AUM, according to its website. The rm runs strategies across listed and private assets.

AXA IM has about €850 billion in assets under management across equities, xed income and alternatives strategies. The alternatives unit had €184 billion of AUM as of March 31.

AXA’s news release said its intention to exit the money management business emphasizes the group’s strategy to focus on core insurance activities, with CEO Thomas Buberl adding that the group had considered different options to support the future development of AXA IM “in the context of a rapidly consolidating and highly competitive asset management industry.”

“By joining forces with BNP Paribas, AXA IM would become a global asset manager with a wider product offering and a mutual objective to further their leading position in responsible investing,” he said.

BNP Paribas spokesperson could not immediately be reached for comment on the impact on staff.

PE exec’s gift to fuel study on high court

Private equity executive

James A. Kohlberg has donated $30 million to the Brennan Center for Justice at the New York University School of Law to help the center conduct research on Supreme Court reform.

Kohlberg is chairman of Kohlberg & Co., a rm he cofounded in 1987 with this father, the late Jerome Kohlberg Jr. The elder Kohlberg is the “K” in Kohlberg Kravis & Roberts Co., where his son James was a former executive.

James Kohlberg has been chairman of Kohlberg & Co. since 2007.

“We are at a tipping point,” James Kohlberg said in July 23 news release announcing his donation. “Without signi cant reform, the U.S. Supreme Court will remain unchecked, jeopardizing constitutional values and our democracy for generations. I can think of no better institution than the Brennan Center to lead the critical work ahead to hold the Supreme Court accountable.”

The Brennan Center, an independent nonpartisan and policy organization at the law school, was founded in 1995 by former law clerks to Supreme Court Justice William J. Brennan Jr., who served from October 1956 to July 1990.

The donation will create the Kohlberg Center on the U.S. Supreme Court that will, among other things, publish policy reports and research, convene scholars and “advance proposals for Supreme Court reform,” the news release said.

“We will use Jim Kohlberg’s generous gift to deepen the public’s understanding and broaden support for reforming the court,” Michael Waldman, president and CEO of the Brennan Center, said in the news release.

President Joe Biden recently unveiled a series of Supreme Court reform recommendations: setting term limits, suggesting Congress pass a binding ethics code for the justices and advocating a constitutional amendment that eliminates presidential immunity for crimes committed while in of ce.

ROBERT STEYER

TRAINING NEXT GENERATION

Greenwood Project expanding college student program

Nonpro t organization Greenwood Project is expanding its college program for Black and Latino students.

Based in Chicago, the organization was founded in 2016 to train scholars of color in career-tracked skills they will need to succeed in nancial services. Kwesi Smith, formerly a research analyst at corporate partner William Blair & Co., became CEO of Greenwood in July 2023 and has spearheaded an expansion of its training and recruiting efforts.

The organization received an in ux of funding following the murder of George Floyd in the summer of 2020.”Our goal is to grow and scale the organization to train a thousand individuals and transition them into nancial services every year,” Smith told Pensions & Investments. Previously, the program provided high-school juniors and seniors with six weeks of training during the summer, but Smith said they have eliminated

GREEN TRANSITION

that because too few of the students remained in their declared major after entering college.

Instead, the Greenwood Project is expanding its college program. Previously, the project’s college program began with four weeks of training at the beginning of the summer and then a six-week internship with a corporate partner, and now is transforming into an 18-month learning journey, Smith said, beginning with recruiting students in their freshman and sophomore years of college.

“Then they will go through roughly three large learning modules and really get them ready for that speci c internship,” said Smith. Both scholars and corporate partners have requested more on-site time in their internships, and the ability to provide training before the summer will allow scholars to participate in a traditional 10-to-12-week summer internship with corporate part-

Included among over 30 corporate partners are money managers AllianceBernstein, Janus Henderson, Wellington Management and William Blair.

Over 70% of Greenwood Project alumni are currently working in

Investors commit $400 million toward energy transition in emerging markets

Investors including the Caisse de dépôt et placement du Québec and the C$128.6 billion ($97 billion) Ontario Municipal Employees Retirement System, Toronto, have committed to invest an initial $400 million to the emerging markets energy transition under the Emerging Markets Transition Debt initiative.

The debt strategy is managed by investment manager Ninety One, which had £128.6 billion ($164.2 billion) in assets under management as of June.

According to a July 29 news release, the strategy “looks to provide companies in emerging

BANG FOR THEIR BUCK

markets with commercial financing to make critical investments, including in

IEN develops benchmark for measuring investment impact

With various standards around environmental, social and governance factors, endowments and foundations may have dif culty assessing how much impact their investment are having and how that compares with their peers.

To address that, the Intentional Endowments Network has been developing a benchmark to help endowments and foundations with mission-based, sustainable and impact investing mandates see how they stack up.

The Endowment Impact Benchmark is focused on “celebrating progress” being made by institutions, said Georges Dyer, executive director of IEN. The organization designed it to be exible around how endowments “normally operate and do busi-

ness,” regardless of their size, their strategy for deploying capital and ESG metrics they may use, he added.

As a rst step, endowments answer a 32-question assessment focused on process and policy, with 21 of the questions based on data provided by the institutions.

IEN designed the assessment to align around frameworks that endowments may follow, such as the United Nations Principles for Responsible Investment and the Impact Management Project.

The impact veri cation provider BlueMark then scores the responses with a rating and provides feedback to the endowments on areas they can improve in. Institutions can score as high as “platinum” and as low as “bronze.”

low-emission infrastructure and in heavy emitting companies with a credible transition plan — helping

Institutions can score higher based on how “strong commitment to transparency” and how they are “following through on that,” Dyer noted.

IEN is seeking 15 endowments to participate in a second pilot program, and is accepting applications through the end of September.

Results will be published in early 2025.

The rst pilot program for the benchmark was held in 2023, and surveyed ve member institutions of IEN that Dyer said have been “active” around sustainable investing, including the University of California. The Oakland-headquartered, land-grant university system’s $20.7 billion endowment received a “gold” rating according to a report on the pilot’s results, which highlighted the institution’s Sustainable Investing Framework and DEI considerations in investments.

Endowments and foundations “have often wrestled with transparency to their stakeholders around

nancial services, said Smith. There are 200 project alumni before the summer of 2024, of whom about 75 have graduated, he said.

More information can be found on the organization’s website.

reduce carbon emissions and supporting the global energy transition.”

United States Secretary of the Treasury Janet Yellen and South African Finance Minister Enoch Godongwana recently praised efforts to pull institutional capital into emerging markets through the Emerging Markets Transition Debt initiative.

“For many of the investors involved, this initiative represents a significant step forward in expanding their investments in emerging markets. It shows that we are making tangible progress on our ambition to increase private capital mobilization for emerging markets, with hopefully much more progress ahead,” Yellen said at a G20 event in Brazil last month.

their investments,” Dyer said, so IEN sought to design a system that moves them toward “more transparency in a way that ts their constraints — in terms of how they’re governed and what information they can and can’t share.”

He added this benchmarking program can help endowments engage “in more meaningful ways” with their stakeholders, including students who may not “necessarily understand how endowments are managed (and) what their constraints are.” This comes as university students hold protests pertaining to how their institution invests amid the ongoing con ict between Israel and the Palestinian militant group Hamas.

From here, the organization intends on growing engagement with the system, which is also considering a re-evaluation process about every three years for previous participants to assess institutions that may have changed their practices.

CARYL ANNE FRANCIA

ners.

ROB KOZLOWSKI

A LEG UP: Through internships and study, students learn skills to succeed.

CARYL ANNE FRANCIA

‘TIPPING POINT’: James A. Kohlberg ACCOUNTABILITY

OTHER VIEWS HANS STOTER

Why the backlash? Sustainable investing

is simply a better approach to

investing

Responsible investment is under attack. As a responsible investor supporting the transition to sustainable economies, we strive to identify and back environmental, social and governance leaders that can protect and grow client portfolios. We have already seen signs that the global economy is starting to move to a more sustainable and equitable model over the next decade.

Still, some critics simply believe that anything ESG-related is so much greenwashing. Others argue that it is a distraction from the goal of delivering the best possible investment performance. Put differently, that investing in a responsible way limits the opportunity set and thus the potential for nancial returns.

This, in our view, goes to the heart of the backlash. The evidence to support this argument is, however, inconclusive at best.

So why does the backlash, in its various forms, persist?

Souring sentiment toward ESG can be traced back to 2022, when sustainable indexes were negatively impacted by a sectoral bias amid temporarily high energy prices. Oil companies and other energy stocks performed extremely well in the wake of Russia’s invasion of Ukraine, and handed skeptics the ammunition to argue that ESG was a fad whose time had passed.

The subsequent underperformance of the energy sector in 2023 should have blunted that argument, but markets have selective memories. ESG funds have consequently yet to shrug off the stigma of 2022, despite that year’s exceptional nature and the ensuing outperformance of ESG indexes.

We do not believe this situation will last. It makes little nancial sense to eschew an approach whose aim is to deliver superior investment returns alongside non- nancial outcomes, like mitigating climate change. But it may take several years and a deeper level of appreciation about the direction of travel at a corporate, governmental and regulatory level — ultimately the drivers of the economic case — for ESG to become as accepted as it should be.

If short-term relative performance challenges have proved a headwind for ESG, we should also acknowledge that confusion around the topic has, to some extent, helped fuel the backlash.

What ESG is not about is overzealous responsible investors seeking to achieve their sustainability goals using client money. What it is about in the rst place is having a framework to assess a business and its operating environment across a range of key risk factors. And the evidence shows that, in the medium to long term, businesses that are low on carbon, socially aware and display the best governance practices are likely to outperform their peers and help improve the risk pro le of portfolios.

Seen through this lens, we are convinced that there can’t be any robust active investment process without a solid ESG framework.

After all, when an investor is taking long-term views on companies, they must take into consideration all the risks; not just the business and market risks, but also those around potential litigation, changing consumer trends, and evolving societal attitudes and regulation toward sustainability. These are real risks, and they present real investment opportunities.

A key point here is that corporates are changing their business models themselves. Not only are they becoming more sustainable, but they are also expending signi cant time and resource on improving transparency across a range of issues. Most companies now produce a sustainability report because the way they do business is changing. We are not, as investors, selecting them because they are an “ESG” company, but because they are attractive nancial investments.

Equally, it is important to remember that corporates are not operating in a vacuum. We are in the midst of two epoch-de ning transitions: the technology transition and the energy transition. These will fuel seismic shifts in the way the world economy works, and they are increasingly core to how businesses operate. If an investor is not evaluating all the risks associated with these transitions, how can they be accurately assessing a company’s ability to deliver sustainable shareholder returns?

Arguably, this point has been lost in the commotion around ESG, yet there is no doubt that the different and evolving corporate strategies adopted by asset managers has done little to impart clarity. Approaches to RI vary from highly active and committed to hands-off, with the onus on the client to decide what to do or how to vote. Some groups are increasingly attempting to straddle both camps, depending on the client type or continent where they pitch.

This shifting spectrum has not, in some eyes, helped ESG maintain credibility when consistency is prized in a complicated area. The range of sustainable nance policies that have come into force in several geographies over recent years has further added to the complexity and confusion. It is evident that

more simplicity and comparability are needed in a landscape littered with different metrics, targets and de nitions.

But asset managers could be more transparent, too. Of course, they are free to choose how to engage with different policy frameworks as well as the various investor initiatives that seek to drive change through collective action. They can be more or less of a responsible investor. But they should be clearer about their choices and what approach to RI they offer and why, to allow asset owners and other investors to make informed decisions.

As an active asset manager committed to responsible investing, we would make several observations about the future. First, investment strategies that align with industry efforts to reduce fossil fuel usage in society are simply economically rational. Companies making aggressive cuts to their greenhouse gas emissions have been shown to at least match or outperform their wider benchmarks . Corporate efforts to effect change do not have to come at the expense of shareholder returns.

Second, a huge amount of progress has already been made. Regulation, data, guidelines and benchmarks have evolved to help companies and asset managers make accurate disclosures and well-informed investment decisions. Asset managers can choose to ignore changing market frameworks. But disregarding the transition to net zero is equivalent to forfeiting the impact of the billions that governments are already spending to transform economies, support (or enforce) the decarbonization of high emitters and assist those companies providing solutions necessary to the transition.

Third, we should not pretend that the transition is going to be painless. There is a physical and social cost to it, and that creates problems for governments. The use of renewable energy is rising in many regions as the costs rapidly decline, but the transition will have implications that have not always been acknowledged. More honesty is required.

OTHER VIEWS CHRIS WALVOORD

The typical NAV loan looks something like this: A private equity sponsor looks at their portfolio of equity stakes in highly leveraged companies and says, “I want to spend some more money. None of our companies can afford to borrow any more capital and we have already called all of our LP commitments. How about if we post all the equity in the portfolio against a fund-level loan and then we can do all sorts of things with the money.”

This may be a slightly cynical description of net asset value loans, but this rapidly growing corner of the private credit market certainly warrants some in-depth analysis. First, what motivates a sponsor to take out an NAV loan? They are typically employed by funds that are past their investment period and the GP is likely waiting for their cost cutting, levering up, and other “synergistic improvements” at the portfolio companies to start showing up in the nancial results.

The sponsors need to start working on an exit plan so that they can return capital to their LPs and pay themselves. Private equity is, after all, longer-term capital but, unlike public markets, it is not permanent capital. GPs need to sell their companies and move on in order to collect that carried interest.

But what happens when exits are dif cult? Perhaps a company is struggling to grow into their now much higher cost of debt. Or they need just one more bolt-on acquisition to achieve scale and turn a pro t. Or maybe the LPs are anxious for a return of capital so they can stick to their pacing plan, reinvest in the next vintage fund and not risk getting shut out of the private equity market forever.

These factors create demand for NAV loans when portfolio compa-

Stoter

CONTINUED FROM OPPOSITE PAGE

Finally, progress will take time. While many corporates are making climate commitments and devising and implementing credible plans to meet them, it is unrealistic to expect large investors to move at the same pace. Institutional asset owners cannot transform their overall investment portfolios to meet decarbonization commitments overnight. The practical realities of integration at that scale across asset classes should warrant patience given the challenges involved.

Will ESG still be facing the same backlash in ve years’ time?

We believe the answer is no. As policy prompts greater action and thus ever more investment in reducing carbon emissions, the economics of renewable energy will become increasingly compelling. It is these shifts that ESG is designed to capture to generate better investment performance over the long term. There will be

nies can’t be sold anywhere near where they are marked. While at a very high level these all seem like reasonable justi cations for adding leverage with a NAV loan, adding leverage increases risk, so investors need to dig into the details and think through the scenarios and possible downsides. If the bolt-on acquisition does not quite get that company to scale or they continue to struggle with their debt service coverage ratio after the capital infusion, what then?

Chris

Walvoord is an alternatives investor who was most recently the global head of liquid alternatives research and portfolio management at Aon. He is based in Chicago.

The sponsor will have to source capital from other companies in the portfolio to pay back the loan. This puts more pressure on the rest of the portfolio, the companies that did not get any of the initial loan proceeds. It could result in a debt spiral that sinks the whole fund.

Sponsors do work hard to add value to their portfolio companies, but they are also quite good at extracting value from those companies. The returns that private equity LPs have earned over the past decade bear this out, as well as the fortunes that the GPs have made.

Sponsors will extract value from every corner of the portfolio, one way or another, sometimes engaging in asset transfers, charging the companies for “services,” and other sorts of what is known as “investor on investor violence.”

If things go bad for a NAV loan, who is rst in line to get the value? When the sponsor says to the NAV lender “I can’t pay back that loan,

blips along the way. But many of the doubts expressed about ESG miss the point. It is not about advancing agendas or foregoing returns. In today’s world, sustainable investing is simply a better way of investing.

In a few years’ time ESG will be a redundant acronym. Assessing risk to a business, and therefore an investment, will automatically consider risks from climate change, environmental liabilities, social protection and the ongoing governance of how companies are managed. All of these factors, governed by regulation and market preferences, will constitute mainstream investment decision making. Sustainable investment returns depend on sustainable business models and that is just not about selling product but about positioning companies to prosper as the world becomes more able to quantify non- nancial risks.

This content represents the views of the author. It was submitted and edited under Pensions & Investments guidelines but is not a product of P&I’s editorial team.

you can have the portfolio of equity stakes,” what do you imagine that portfolio will be worth? My guess is close to zero.

The Modigliani and Miller theorem tells us that leverage does not create value, it simply changes how the value is divided across stakeholders. We see this clearly when the proceeds of the NAV loan are used to make distributions to the LPs. The end result is that while the LPs do get some capital back, their remaining equity is much riskier due to the increased leverage. The payouts also increase several of the metrics that are commonly used to judge private equity performance such as multiple on invested capital (or MOIC) and IRR. Finally, the distributions can help get over any hurdle rate required to trigger carried interest payments to the GP.

One additional concern for the LPs is the cost of this NAV loan.

Private credit funds have a much higher cost of capital than the banks. If the private equity fund can’t generate a rate of return higher than the cost of the NAV loan with this incremental additional capital, then the loan

will be dilutive to the LPs' returns. The cost of the loan is certain, the return on the incremental capital is uncertain. If the LPs are satis ed with the existing risk-return proposition, then the NAV loan may not be desirable.

We need to ask questions about the lenders’ side of the equation as well. One common argument given by NAV lenders for the attractiveness of the strategy is that the loan-to-value ratios are very low — on the order of 15% to 25%.

But remember that the NAV loan is subordinate to any debt at the company level, so the ratio of this debt to the underlying assets is signi cantly worse. We also have some fairly strong evidence that current PE valuation numbers are at a minimum stale and likely well off the market. Remember that one of the factors driving the demand for these loans is the fact that exits are generally not available at current marks. So the V in our LTV calculation is much smaller than it would rst appear.

The other question worth thinking through is how are the loans repaid? The primary mechanism for generating cash to pay back principal is selling the equity stakes. In this sense the NAV lenders are really just taking on the same risk as the LPs — they get their money back when companies are sold. But the NAV lender has a capped upside with similar downside risk to the LPs.

All of this feels a bit like the

nancial engineering exercises we saw leading up to the great nancial crisis. There was a large increase in leverage on leverage and, as we learned later, the underlying credits were shaky and many collapsed. Both the subprime mortgage market and the CLOsquared transactions are prime examples. Investors failed to appreciate the common risk factors that could, and did impact all of the underlying loans in these “diversied” pools at the same time. The result was an ugly mess that took years to work out.

To be clear, I am not predicting that private markets are going to crash and bring down the nancial system. And within a diversi ed portfolio, there is a place for well-researched private equity and private credit exposure that can earn a liquidity and complexity premium. But borrowing adds risk, especially at the fund level. Investors need to be aware of this added leverage and understand the risks they are taking. They need to convince themselves that the risk-return proposition is still attractive vs. what is available in public markets. And if something does not smell quite right, they need to either keep digging or walk away.

This content represents the views of the author. It was submitted and edited under Pensions & Investments guidelines but is not a product of P&I’s editorial team.

Pension risk transfer activity

Total

Bond ETF innovation mostly steers clear of derivatives

Amid a surge in issuance of equity exchange-traded funds employing derivative-based opportunities and hedges, the xed-income ETF market has been relatively devoid of such offerings around rates and credit.

The paucity is not for lack of liquidity, particularly in listed and over-the-counter derivatives linked to U.S. Treasuries or the federal funds fate, but more likely in the collateral and leverage required to eke out noteworthy gains from markets that tend to move slowly — and then all at once.

Moreover, the fate of past exchange-traded products trying to exploit spread differentials and the yield curve may be the limiting factor to experimentation among the nearly 700 products and $1.7 trillion in assets under management in U.S.-listed xed-income products, said Elisabeth Kashner, vice president and director of global fund analytics at FactSet Research Systems.

Outside of broad-based bond index exposures — from Treasuries, governments, agencies and munis, to investment-grade corporates and high yield, as well as mortgage-backed securities, the rst novel xed-income offerings to take

hold among investors were target-maturity products. From BlackRock and Invesco, these ETFs are built with bonds all maturing at the same time, allowing investors to ladder diversi ed ETFs as they would individual securities.

These products paved the way for a variety of funds that hedge interest rate risk, target duration, or even invest in on-the-run Treasuries — the most recently issued Treasuries. But as the market lls once again with speculation on the depth and timing of changes to the federal funds rate — and, indeed, central bank action around the world — ETF investors have limited opportunities to speculate on rates in the ETF market.

“This may not be such a bad thing,” Kashner said.

Based on her analysis of recent ows and returns, “ETF investors have been quite terrible at using relatively simple tactical tools in the xed-income market,” Kashner said. For example, the iShares 20+ Year Treasury Bond ETF (TLT) “raked in billions in the past three years, despite losing about 11.4% per year during that time.”

Effective duration for TLT was 16.7 years on Aug. 2, according to BlackRock.

“None of this will stop asset managers from innovating and introduc-

ing new products into the market,” Kashner said. “Their mandate is to nd a winning business strategy. Investors' mandate is to grow their capital. It's great when the mandates overlap, and not so great when things don't go to plan.”

Making it work

Among those that have recently found that overlap, F/m Investments offers exposure to on-the-run Treasury bills, notes, and bonds, while making monthly dividend payments. Its US Treasury 3 Month Bill ETF has nearly $4 billion in assets two years after listing. And, over the same period, BondBloxx Investment Management has accumulated $2.3 billion across its eight target-duration Treasury ETFs.

“Having precise duration is a tool to manage risk in the current interest rate environment,” said Joanna Gallegos, co-founder of BondBloxx.

The Municipal Employees’ Retirement System of Michigan, for example, has utilized a handful of BondBloxx products to ne-tune positions in Treasuries, corporates and emerging-market debt, according to its most recent 13F ownership ling with the Securities and Exchange Commission.

“To make an ETF product targeting the yield-curve worthwhile, it would really have to be levered up

beyond a level that’s prudent for a listed open-end fund,” said Harley Bassman, managing partner at Simplify Asset Management. “An ETF using solely feds funds futures might need leverage as high as 40 to 1 to be interesting.”

Simplify, which manages $5.5 billion in ETF assets, has products that include “better beta” exposure to changes in credit and rate levels, as well as equity volatility, among other strategies. “ETF products should be reasonable and perform as advertised … without a trap door,” Bassman said.

Exchange-traded products designed speci cally for scenarios such as a steepening or attening of

the yield curve or the magnitude of in ation or de ation have not employed enough leverage to attract investors, according to Bassman, and have often been challenged by the timing of investor interest or market calls.

Speci cally, FactSet’s Kashner points to the rise and fall of the Quadratic Interest Rate Volatility & Ination Hedge ETF (IVOL), which was designed to target rising rates and in ation. “The ETF attracted billions in investment, only to dramatically underperform TIPS when in ation hit,” Kashner said.

The reality for xed-income ETFs may be that creative thinking trumps overthought products.

PIMCO'S cyclical outlook, published in April, for example, called on investors to be more mindful of diverging markets, particularly on duration and regional rate moves, precisely the scenario that trapped global investors in early August.

And should xed-income investors still want to be whipsawed by speculating on rates and the yield curve, PIMCO’s 25+ Year Zero Coupon U.S. Treasury Index ETF (ZROZ) goes far beyond BlackRock’s TLT by targeting U.S. Treasury principal STRIPS.

Its effective duration as of Aug. 2 was 27.1 years, according to PIMCO.

DELIVERING MULTI-FACETED BENEFITS

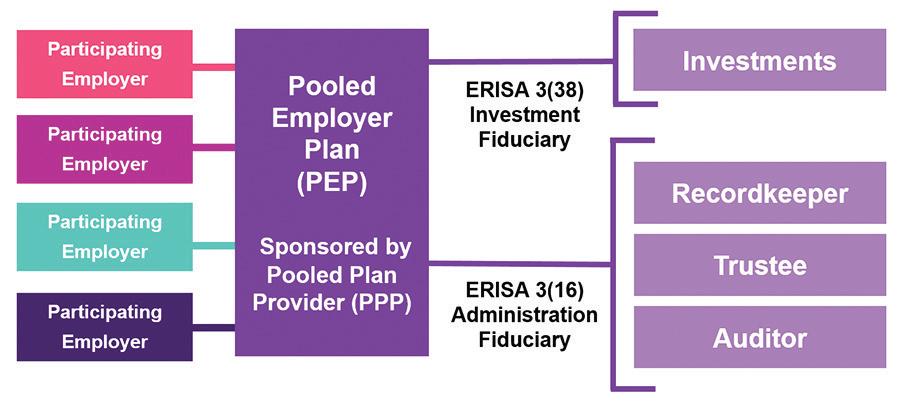

The defined contribution plan has gained prominence as a key benefit for attracting and retaining employees, which has led plan sponsors to reassess how they can optimize e ciently to provide strong retirement benefits for their workforce. Powered by the SECURE Act of 2019 that sought to boost retirement security for working Americans, the pooled employer plan — or PEP, a new type of multiple employer plan that has several unrelated employers and is managed by one pooled plan provider — has emerged to meet that objective.

“PEPs represent an extension of the existing DC outsourcing spectrum, enabling employers to outsource the plan sponsor role. This allows companies to focus on their core business while ensuring their employees receive high-quality retirement benefits managed by experts,” said Chris West, managing director, DC strategy leader and head of the U.S. LifeSight® PEP Pooled Employer Plan at WTW. “With DC plans on the rise globally and $3 trillion in pooled DC plans worldwide,1 the availability of PEPs is a significant step forward in the retirement landscape,” she added.

Because it’s a pooled employer plan, the first question that we get is, ‘Can I still design the plan features the way I want?’ The answer is, ‘Yes.’

- David Eisenreich

“The benefits of pooled retirement plan models appeal to many employers. However, access to these models has historically been limited,” said Deborah Rubin, vice president and managing director for pooled plan sales at Transamerica. “As Congress explored solutions to the growing retirement savings gap, broadening access to pooled models became an attractive way to expand coverage for participants while providing employers with many benefits that they seek.”

Valued benefit

HOW IT WORKS

PEPs can effectively address several challenges that employers are facing as they aim to strengthen their DC plans.

Plans also face regulatory uncertainty and complexity, all of which create added burdens. “Employers struggle to provide customized and comprehensive benefits because it takes a lot of work and comes with legal and compliance risks. This makes it harder for them to ensure better retirement outcomes for their employees,” Eisenreich said. He also noted that there are various cost management challenges, including plan administration, record keeping, compliance, fiduciary oversight, and fees for plan investments.

Engaging participants with plan communication and education is critical to retirement preparedness, but this too can be expensive, Eisenreich said. “Participants often don’t have time and feel ill-equipped to make informed decisions around retirement savings. Providing the required educational support to help and engage them can be costly and resource intensive for employers.”

Comparative advantages

“Employers are looking for a retirement solution that is simple, reduces their dayto-day fiduciary and administrative burden, and is cost e ective,” said Stanley Kim, director and pooled plan practice leader at Transamerica, which is a record keeper for single employer DC plans as well as multiple employer plans like PEPs, including the PEP o ered by WTW. For many plans, both small and large, that solution is to join a PEP as a participating employer, he said.

WHAT ARE THE BENEFITS OF PEPS ?

In the 2024 WTW Global Benefits Attitudes Survey, two-thirds of employees said their employer’s retirement plan is more important to them now than ever before. In fact, 55% said it is an important reason for choosing to remain with their employer.2 Even as DC plan sponsors recognize this heightened need for retirement security, they continue to face numerous challenges in delivering a robust retirement plan, said David Eisenreich, managing director and head of retirement, North America, at WTW. The good news is that they can consider an expanding range of DC solutions that now includes PEPs to solve many of these challenges.

Source: Transamerica

In addition to its collective buying power, which typically reduces overall plan costs for each participating employer, the PEP model provides several advantages over stand-alone plans. “A PEP allows DC plans to reduce their liability by outsourcing much of the fiduciary responsibility as well as audit responsibility, with a PEP itself subject to a single audit, which often saves the participating employers money,” Kim said.

The PEP model eases plans’ administrative burdens, said Rubin. “The PEP is structured specifically to do that. The service providers do a lot of the heavy lifting for the plan sponsor.”

• The PEP sponsor is known as the Pooled Plan Provider (PPP) and generally serves as the plan administrator and fiduciary

• “Adopting employers” elect to join the PEP

• These plans are defined contribution (DC) plans

• At any time, adopting employers are easily integrated into the plan hosted by the sponsor and tracked on the Transamerica platform

PEPs expand access to retirement plans for all workers by allowing employers from unrelated industries to join a pooled plan arrangement. Benefits to the adopting employers include increased administrative e ciencies, reduced fiduciary risk, and potential cost savings. ADOPTING

Employee communications is another specialized area that is managed by the pooled plan provider, or PPP, along with the record keeper. “As it pertains to employee engagement, participation and data, each participating employer in the PEP gets the data and services they need, as they would in a single employer plan. Plans don’t lose anything,” Rubin said. In fact, the PEP could provide enhanced communications, education and engagement tools that plan sponsors may not have the resources to provide in a single plan.

• Large plan filers benefit from reduced audit costs, which are distributed among the plan’s adopting employers

A more robust investment menu is another key reason that employers are turning to PEPs, said West. “They may not have access to a sophisticated fund lineup with the lowest fees. In a PEP, participating employers are able to take advantage of scale and can provide better risk-adjusted return potential to their employees, while also transferring their fiduciary risk and lowering fees.”

By joining the PEP, adopting employers can focus on running their business and meeting the needs of their employees. Benefits include:

Employers are looking for a retirement solution that is simple, reduces their dayto-day fi duciary and administrative burden, and is cost e ective.”

- Stanley Kim Transamerica

Dispelling myths

Several myths and misunderstandings about PEPs persist among plan sponsors. Many think PEPs are too new, appropriate only for small plans, or have a one-sizefits-all approach.

Eisenreich said of LifeSight, “Because it’s a pooled employer plan, the first question that we get is, ‘Can I still design the plan features the way I want?’ The answer is, ‘Yes.’ That question jumps out due to a misconception or lack of understanding” of PEPs.

As the PEP provider industry has grown, some plan sponsors may have evaluated some options that don’t, in fact, provide any flexibility in design, Kim said. It has led to the misconception that for all pooled plans, “the employer is restricted in plan design options.” The restrictions are not inherent to the structure, but rather they stem from the constraints of service providers, he said.

Employers should evaluate the specifics of each PEP, along with the track record and capabilities of all organizations involved in managing the PEP, including the record keeper, Kim advised. Transamerica, which has 20 years of experience in the pooled plan market, has technology specifically designed to support these types of plans.

What’s flexible

Plan sponsors who consider joining a PEP need to understand which aspects of the model are pooled and the features that are not, which in turn allow for some flexibility.

Largely the administrative or back-o ce functions are pooled. Eisenreich said, “If you have 10 single employer plans, that means 10 audits need to be done. If you put those same 10 employers into a PEP, things are no longer replicated 10 times — they’re done once.”

But the PEP model can also provide flexibility in some of the design and investment features that are unique and important to each specific employer. At WTW, “we’re not pooling design elements and our investment lineup uses an open architecture approach,” Eisenreich noted, which allows the participating employers to customize these features.

WTW’s LifeSight PEP combines flexibility with e ciency in its approach to overall 401(k) administration, West said. “It has flexibility in areas that materially impact the employer’s value proposition, such as eligibility, types of employer contributions, allocation formulas, automated features and investing.” In addition, the transition process from a single plan to WTW’s pooled plan is relatively seamless as well, she noted. “The flexibility of the LifeSight PEP allows employers to adopt it with little or no change from their current core plan design. We’re keeping what matters most to them and to their employees.”

UNDERSTANDING THE PEP STRUCTURE

An explanation of eligibility, features and plan sponsor responsibilities.

The SECURE Act in 2019 created pooled employer plans for 401(k) plans, and SECURE 2.0 in 2022 expanded the eligibility of PEPs to 403(b) plans o ered by non-profits and educational institutions. Smaller plans that are more resource constrained were the early adopters. Today, interest has widened to include DC plans of all sizes pursuing the PEP solution.

PEPs versus MEPs

For plan sponsors considering this model, it’s important to clarify how PEPs are di erent from traditional multiple employer plans, or MEPs, which require the participating employers to have some commonality in the same industry or business. “PEPs, unlike MEPs, don’t have a common nexus rule, making it a clear path forward for unrelated entities that can join and obtain the benefits that traditional MEPs provided,” said Rubin at Transamerica.

PEPs also avoid the burden of MEPs under the “one bad apple” rule, which penalizes all participating employers for the compliance failures of one. Instead, under a PEP, the participating employers are protected from the failures of any single employer in the plan. “Eliminating the bad apple rule opened up pooled plan options to unrelated employers without that added level of concern,” Rubin said.

PEPs are structurally distinct from MEPs too. They designate a pooled plan provider, or PPP, as the sponsor of the PEP with the individual plans referred to as participating employers. The PPP is the plan’s fiduciary and has oversight of investments, administrative duties and monitoring the other third-party providers. With MEPs, the plan sponsor is typically the industry association or professional organization of the participating employers.

“The PPP is the sponsor, the plan administrator, the named fiduciary, and it is the entity responsible for performing all the administrative duties. The PPP is also required to register with the Treasury and Department of Labor, said Transamerica’s Kim. Further, the PPP is responsible for hiring and monitoring all the PEP’s service providers.

Distinct from group plans

Five common PEP misconceptions

Kim pointed out that the administrative approach for PEPs is di erent from other aggregation programs, including group plan solutions, or GPS. These are unrelated

As

it pertains to employee engagement, participation and data, employers in a PEP get access to their analytics and annual reviews at the specific participating employer level.

- Deborah Rubin Transamerica

1.

PEPs are new and unproven

Pooled delivery of DC plans has been around in the U.S. for decades – recent legislation simply expands access to unrelated employers.

2. PEPs are only for small plans

While small plans may benefit the most from increased scale, PEPs can provide less effort, risk mitigation, improved participant outcomes and lower costs regardless of plan size.

3. 4.

PEPs don’t benefit employees

Lower fees can directly increase retirement balances for employees. In addition, employees may gain access to design features, innovative investments, an enhanced user experience, and more.

PEPs are one size fits all

Flexibility varies significantly from one PEP to another. LifeSight allows each employer to set the plan design that is right for them.

5.

PEPs are difficult to monitor

LifeSight offers a simple, transparent service model and fees. In addition, we provide periodic information to assist employers in their fiduciary monitoring role.

Source: WTW

CASE STUDY: THE LIFESIGHT PEP

How can a PEP deliver e ective operation and administration of the pooled model while also providing employers with a solution that improves retirement outcomes for their plan population? WTW’s LifeSight PEP leverages the firm’s deep experience and capabilities in administering global DC pooled plan solutions totaling over $30 billion in assets and covering more than 500,000 participants and 1,000 clients.3

Institutional focus

As Eisenreich said, “With LifeSight, we focused on maintaining flexibility in the areas that materially impact employers, namely the cost and the alignment to their total rewards approach. Where employers want control, we’re giving them control, and in others, we’re relieving them of burdensome tasks.” The LifeSight PEP provides plans of all sizes access to the institutional scale, features, oversight policies, and governance model used by the most sophisticated DC plans.

“The LifeSight PEP brings e ciency to 401(k) plan administration without requiring a one-size-fits-all approach,” added WTW’s West. Participating employers can determine their preferences for eligibility, types of employer contributions, allocation formulas, automated features and investing. But, if they so choose, they can access WTW’s recommended plan design that includes suggested employee deferral rates.

Transamerica’s Kim underscored the LifeSight PEPs unique approach to delivering flexibility. “This PEP is for an employer looking for all the same benefits of a single employer plan with the maximum allowance of fiduciary and administrative outsourcing. It is designed for the sophisticated plan sponsor that has complexity to their plan and doesn’t want to be put into a particular box.”

Governance is also critical in a pooled plan structure, given that employers are outsourcing so many fiduciary responsibilities. “A strong governance and compliance model is the foundation of the LifeSight PEP,” West said. “Our in-house structure ensures coordination and accountability, which reduces the risk of oversight gaps, and ensures consistent compliance across all of the required plan activities.” The LifeSight PEP has a dedicated compliance leader who closely tracks regulatory changes in coordination with WTW’s Research and Innovation Center.

Ease of transition is another key aspect when selecting a pooled plan. Eisenreich said, “Guiding employers through change is in our DNA. We routinely lead clients through transitions of DC plan, pension plan and health and benefit plan strategy, delivery and employee experience with ease and confidence.” West added, “Our approach makes moving to the LifeSight PEP straightforward. We coordinate directly with a plan sponsor’s existing vendors and payroll to lessen the burden on the plan sponsor.”

PEPs represent an extension of the existing DC outsourcing spectrum, enabling employers to outsource the plan sponsor role.

- Chris West WTW

entities that, for pricing reasons, share common service providers, including an administrator, record keeper or investment manager. However, each large plan filer in a GPS is required to have an audit performed, and each employer is responsible for filling out the DOL’s annual Form 5500. In a PEP, the PPP files a single Form 5500 and coordinates the PEP’s audit.

DC plan sponsors should evaluate all the di erent types of aggregation programs to understand their subtle di erences and comparative advantages — a service that Transamerica provides, he added. The PEP provides the highest level of fiduciary outsourcing among these programs.5

How to evaluate a PPP

When selecting a PEP, sponsors need to assess the PPP and the service providers involved, including their track records, reputations and capabilities.

WTW’s deep expertise across the DC

Employee experience and outcomes

The LifeSight PEP is designed to meet the needs of plan participants on several fronts, starting with WTW’s proprietary employee experience platform that delivers a modern, digital user experience. It is also designed to support employees when it comes to retirement readiness. “It is important that employees are engaged in a way that inspires them to use the tools and resources o ered to them to take appropriate actions,” Eisenreich said.

In addition, employers can use WTW’s analytics to evaluate employee behaviors and help improve participant outcomes. “The LifeSight PEP o ers quarterly interactive insights to identify areas of financial vulnerability. When you identify vulnerability, you can manage it,” he said. This continuous view of data and insights, likely exceeding what many sponsors get from their individual plans, is crucial. “Our ability to segment this data allows us to help plan sponsors identify areas of improvement and curate actions for the most e ective use of their time and budget.”

Investment structure

The LifeSight PEP’s investment structure utilizes custom (“white label”) core funds and custom target date funds, which allow WTW to integrate the top investment research insights where it can be most impactful to participant outcomes. The investment menu also has a range of investment options tailored to di ering risk appetites and retirement goals. “Individuals should have access to funds that really meet their individual risk tolerance and preference,” West said.

The investment menu is designed to meet the needs of the three main types of participant profiles: “do it for me,” “help me do it” and “do it myself.” The investment choices correspond to the di erent profiles: a target-date fund, which is the default option; a core lineup, including a managed account option (WTW’s solution is LifeSight Advice); and a brokerage window. The menu can also accommodate a company stock fund, if o ered by the employer.

Fees are kept low, in part because WTW is able to leverage its outsourced chief investment o cer, or OCIO, platform with $162 billion in global AUM.⁴ In fact, as West noted, WTW played a significant role in originating the DC industry’s first target-date fund.

With LifeSight, Eisenreich said WTW has continued its tradition of DC plan innovation, building on its own expertise and that of its partners. “Our solution includes investment advisory, fiduciary expertise, employee communications and engagement, defined contribution plan design, strategy and compliance. We’re operating the plan e ciently, e ectively and accurately.”

landscape has drawn sponsors to its LifeSight PEP, West said. “We’ve provided retirement consulting services for more than 140 years. The U.S. LifeSight PEP expands on our capabilities, supporting clients through administration, co-fiduciary services, plan design, data and analytics, investment advisory and delegated solution and vendor management.” WTW manages over $30 billion in assets of pooled DC plans globally, which includes pooled plans in the U.K. and Europe.6