Corporate plans are fully funded. Now what?

New era of stability has fund execs pondering how to take advantage

By ROB KOZLOWSKI

U.S. corporate de ned bene t plan executives are mulling over how to take advantage of a new era of funding stability after a second straight year of being fully funded on average, experts said.

The publicly traded U.S. companies with the 100 largest de ned ben-

e t plans can now boast an average funding ratio of 99.9% as of Dec. 31, according to Pensions & Investments’ analysis of the latest 10-K lings.

That’s a slight drop from the average ratio of 100.2% in the P&I analysis a year earlier, but it still represents a level of stability for funding among corporate pension plans not seen in years. While not all the 100 measured plans are fully funded, 49 had funding ratios of 100% or more as of Dec. 31, and 30 plans even have funding ratios of 110% or more. Those are nearly the same numbers as in 2022, when 50 plans were 100%

Active management is needed now, says Man Group’s Grew

‘Unprecedented times,’ political and economic, require custom solutions

By LY DI A TOMKIW

Robyn Grew has helmed the world’s largest publicly listed hedge fund manager, Man Group, for eight months now and contends investors are living in “unprecedented times” that favor active management.

“I think we are in a period of unprecedented geopolitical, geo-economic impact,” Grew said in an exclusive and wide-ranging interview with Pensions & Investments. “I’m not a forecaster, I’m an observer. But ever were that the case in the moment, translating some of the geopolitical events alongside a different market environment alongside things like climate — these are unprecedented times.”

ALL TOGETHER: In times like these, ‘all of the effort and all of the acumen and depth of experience we have across the organization can be put to work,’ says Man Group’s Robyn Grew.

Man Group has changed dramatically from its founding over 200 years ago and grown from its roots

FLEXIBILITY: Jonathan Grabel’s approach has LACERA beating benchmarks.

n A list of the funding

of the 100 largest corporate DB funds appears on Page 17

or more funded and 31 plans were 110% or more funded.

Even among the 51 measured plans that had ratios of under 100% as of Dec. 31, only three plans had ratios below 80% and all were above 70%.

“(The) combination of improved funding and derisked asset allocation has proven to be incredibly powerful,” said Jared Gross, manag-

ing director, head of institutional portfolio strategy at J.P. Morgan Asset Management, in an interview.

The last time corporate pension plan funded status looked this healthy was as of Dec. 31, 2007, when P&I’s analysis showed an average funding ratio of 108.6%. That all came quickly crashing down, however, with the global nancial crisis. Just one year later, the average funding ratio plummeted nearly 30 percentage points to 79.1%.

Now, however, there is new stability, and it began in 2022. Corporate pension plans bene ted mightily

LACERA CIO’s methodical approach pays off

By A RLEEN J A COBIUS

Jonathan Grabel, CIO of the $77 billion Los Angeles County Employees Retirement Association, which just adopted a new asset allocation re ecting the higher interest rate environment, said pension fund ofcials there take a methodical approach, adjusting its targets rather

than making sweeping changes.

But that doesn’t mean that the Pasadena, Calif.-based pension fund is opposed to change.

In the seven years since Grabel joined LACERA from the $16.3 billion New Mexico Public Employees Retirement Association, Santa Fe, where he was CIO, the pension fund has ditched asset class buckets for a

total fund approach, brought private equity co-investments in-house and launched a cash overlay program that has produced a total of about $500 million in gains so far.

In the pension fund’s most recent performance report, it beat its benchmarks in the one-, three-, veand 10-year time periods ended Feb.

from rising interest rates during the year. The average discount rate rose to 5.25% as of Dec. 31, 2022, from 2.88% the year before, which caused liabilities to plummet and offset poor investment performance during the period.

That dramatic rise in discount rates came primarily as a result of the Federal Reserve’s aggressive ght against in ation, that would eventually reach its end point in July when the central bank raised the federal funds rate to a range of 5.25% to 5.5%.

First lawsuit led against duciary rule; more expected Regulation

By BRI A N CROCE

Stakeholders with competing views and interests expected legal challenges against the Department of Labor’s new duciary investment advice rule, and on May 2 the rst such lawsuit was led.

The Federation of Americans for Consumer Choice, which represents annuity and life insurance rms, and ve insurance agents and rms collectively led the lawsuit in U.S. District Court in Tyler, Texas, arguing that the new rule exceeds the Labor Department’s authority and is arbitrary and capricious, in violation of the Administrative Procedure Act.

Stepping back, one side of the debate says the rule, which covers onetime advice such as rollovers to individual retirement accounts or annuity purchases, will better protect retirement investors by expanding the universe of nancial professionals who have to put the investors’ best interests rst, while the other says it will hurt those investors’ ability to get the advice they seek when making crucial nancial decisions.

“Here’s the bottom line: We’re putting this rule in place to ensure that America’s workers can enjoy the retirement that they’ve earned, paycheck by paycheck, year after year,” said Lisa M. Gomez, who leads the

SPECIAL REPORT CORPORATE BALANCE SHEET

CONTINUED ON PAGE 16 SOUND BITE Emerging markets investing in ux Investors are keeping a close eye on election results, while exploring ex-China options in Asia, and looking at options in Vietnam and Turkey. Page 12 COPIA GROUP’S SHUNDRAWN THOMAS: ‘People talk about private credit as a monolith, and that’s not the case .’ Page 4 THE INTERNATIONAL NEWSPAPER OF MONEY MANAGEMENT | MAY 6, 2024 | PIONLINE.COM | $16 AN ISSUE / $350 A YEAR

Money

Management

SEE FIDUCI A R Y ON PAGE 26

RELATED CONTENT

ratios

Pension Funds

SEE L A CER A ON PAGE 24 SEE

CTIVE

PAGE

A

ON

27

Buck Ennis

IN THIS ISSUE

ESG

CalSTRS CIO Christopher Ailman said sustainability is integrated ‘in everything, in every way, in every minute of every day’ at the fund. Page 4

Alternatives

Copia Group’s Shundrawn Thomas, during a P&I LinkedIn Live event, said institutional interest in private credit will continue to grow. Page 4

Defined contribution

The U.K.’s master trusts are ripe for consolidation. We look at the recent Smart Pension-Evolve Pensions deal. Page 6

Special Report: Emerging Markets

Managers are keeping a close eye on this year’s elections in particular, the ones in emerging markets Page 12 Economic growth and governance reforms have Asian markets attracting more investors. Page 12 Vietnam is drawing interest, but investors must make the effort to understand the market. Page 13

Managers are split on whether Turkey remains an investable opportunity amid difficult economic conditions. Page 14

Money Management

BlackRock’s cost to provide security for Larry Fink in 2023 more than doubled from the year before. Page 18

Now online: RiskWatch Q1 RiskWatch takes a look at volatility and correlation in the first quarter. Find it at PIonline.com/riskwatch.

Manager survey closing; OCIO survey prepping

Last call for late responses to Pensions & Investments’ annual survey of the largest money managers . Firms managing U.S. institutional, taxexempt assets are eligible to participate. Results will run June 10. Next up, P&I will distribute the annual investment outsourcing survey with responses due by June 7. Firms serving as outsourced CIOs to institutional asset owners are eligible to participate. Results will run July 15. To request a survey or obtain further information, please contact Anthony Scuderi at ascuderi@pionline.com or 212-210-0140, or visit www.pionline. com/section/surveys

Plan to nd workers’ lost 401(k)s

can’t use

By COURTNEY DEGEN

Congress has tasked the Labor Department with building a lostand-found database to help Americans nd their lost retirement savings. It's off to a rocky start.

The database — mandated by the retirement package SECURE 2.0 passed in late 2022 — will allow savers who lost track of their retirement money to locate their plan administrators, which experts agree is a complex problem in need of a solution.

However, the DOL’s recent proposal for gathering information to build that database is laden with obstacles, industry sources said. The proposal, which the department re-

leased April 15, states that the DOL had planned to use existing data that 401(k) plans regularly submit to the IRS and Social Security Administration, in a ling known as Form 8955SSA.

That ling informs the government about retirement savers who left their employer but still have retirement accounts with them, explained Michael Kreps, principal at Groom Law Group and chair of its retirement services group.

“The challenge with the IRS is … they have a lot of statutory restrictions on what they can do with taxpayer information,” Kreps said, and according to the proposal, the IRS decided it cannot share such data with the Labor Department, citing disclosure and con dentiality restrictions.

Consequently, the DOL asked for retirement plan administrators to submit the requested information on

BlackRock, Saudi wealth fund ink compact

Riyadh-based platform aims to invest across asset classes in private, public markets

By SOPHIE BAKER

BlackRock Saudi Arabia intends to establish a Riyadh-based multiasset-class platform investing across public and private markets, with an initial anchor investment of up to $5 billion from the kingdom’s sovereign wealth fund, Public Investment Fund.

The two have signed a memorandum of understanding for the establishment of BlackRock Riyadh Investment Management, a joint statement said. The anchor investment is subject to the achievement of agreed milestones.

A Riyadh-based portfolio management team is expected to manage the assets, with support from BlackRock’s global asset management platform. Recruitment is already underway, with job speci cations already in the market and offers being made for executives to join to set up the operational platform, a BlackRock spokesperson told Pensions & Investments. The investment team will be a combination of existing BlackRock

personnel and new, on-the-ground staff.

In terms of asset classes, the intention is to manage equities and bonds on the public

side, and private debt and infrastructure on the private markets side, the spokesperson

Ohio Teachers dumped by Aon amid board turmoil

By ROB KOZLOWSKI

Ohio State Teachers’ Retirement System, Columbus, has lost Aon as a governance consultant after the rm resigned from the assignment, according to people familiar with the matter.

The $94 billion pension fund’s board recently tilted to a majority of self-proclaimed reformers who want to gut investment staff and move the pension fund to all index funds, citing a desire to restore a permanent 3% costof-living adjustment.

At the April 18 board meeting, Trustee Wade Steen reclaimed his seat after the 10th District Court of Appeals earlier that day ruled that Ohio Gov. Mike DeWine did not have the authority in May 2023 to remove Steen as his appointed investment expert on the STRS board before the completion of his four-year term.

DeWine originally appointed Steen for a term beginning Nov. 25, 2020, and ending on Sept. 27, 2024.

Steen has been vocal in his support of a grassroots movement of retirees and active Ohio teachers angry about reduced or eliminated annual COLAs. After DeWine appointed G. Brent Bishop as Steen’s replacement, Steen led suit in June and stated in his complaint that Bishop “has wrongfully taken and is acting in, the position of the Governor’s appointed ‘investment expert’ to the STRS Board, the public of ce position to which Mr. Steen is legally entitled and from which Mr. Steen has been wrongfully removed.”

Steen’s restoration to the board creates a 6-5 majority in favor of the reformers.

Aon's duciary services practice was retained to implement recommendations by board governance consulting rm Funston Advisory Services, which conducted a ducia-

ry performance audit on the system in May 2022. Recommendations, which Funston said in its report were solely to “improve duciary performance to bene t current and future STRS members and bene ciaries,” included improvements in STRS’ use of committees, including a “revitalization” of investment and audit committees and the creation of a board governance committee.

Aon had already made recommendations on committee structure and made a presentation at the April 18 board meeting on enterprise risk management recommendations, and it had the development of a long-term strategic plan as part of an agenda of future actions. That meeting ended following Steen’s return to the board. Steen halted proceedings at the meeting, citing a desire to take a ceremonial oath of of ce from a retired teacher despite having taken the oath from a STRS of cial

2 | May 6, 2024 Pensions & Investments

snags SEE LOST ON PAGE 20

hits

SEE COMPACT ON PAGE 18 Regulation

Money

Management

Pension Funds

SEE DUMPED ON PAGE 26

VOLUME 52, NUMBER 6 Keith E. Crain , Chairman Mary Kay Crain , Vice Chairman KC Crain President & CEO Chris Crain , Senior Executive Vice President Bob Recchia , Chief Financial Officer G.D. Crain Jr. , Founder (1885-1973) Mrs. G.D. Crain Jr. , Chairman (1911-1996) Published by Crain Communications Inc. Chicago offices 130 E. Randolph St., Suite 3200, 60601 London offices 11 Ironmonger Lane, EC2V 8EY New York offices 685 Third Ave., 10th Floor, 10017 Address all subscription correspondence to Pensions & Investments, 1155 Gratiot Ave., Detroit, M 482072732 or email customerservice@pionline.com. www.pionline.com Entire contents ©2024 Crain Communications Inc. All rights reserved. Pensions & Investments (ISSN 1050-4974) is published monthly in January, February, March, July, August and December, and semimonthly in April, May, June, September, October and November by Crain Communications Inc., 130 E. Randolph St., Suite 3200, Chicago, IL 60601. Periodicals postage paid at Chicago, IL, and at additional mailing offices. POSTMASTER: Send address changes to Pensions & Investments, Circulation Dept., 1155 Gratiot Avenue, Detroit, MI 48207-2912. $350 per year in the U.S. Printed in U.S.A.

DOL database

IRS data as planned, among other challenges

BIRTH ANNOUNCEMENT: BlackRock’s Larry Fink stands with, from left, Yazeed Almubarak, BlackRock Saudi Arabia, and His Excellency Yasir Al-Rumayyan and Yazeed A. Al-Humied, both of Saudi Arabia’s Public Investment Fund, after signing a memorandum of understanding launching BlackRock Riyadh Investment Management.

Money Management

Wilshire Indexes going hard after industry titans

Innovation,

aggressive pricing seen as key to taking share from FTSE Russell, MSCI

DOUGLAS APPELL

Wilshire Indexes, a little over a year since being hived off by consulting and asset management veteran Wilshire Advisors, is counting on a better mousetrap and aggressive pricing to help the benchmark index provider wrest business from entrenched industry leaders at home and abroad, executives say.

“Our goal” is to challenge the dominance of FTSE Russell in the U.S. market and MSCI globally, said Reza Ghassemieh, Wilshire Indexes’ chief benchmark of cer. In the wake of a sharp decline in the number of listed U.S. stocks over the past 25 years, Russell’s use of xed numeric targets to de ne large- and small-cap stocks — with its widely tracked Russell 1000 U.S. large-cap index and Russell 2000 U.S. small-cap index — creates an opening, said Ghassemieh, who joined Wilshire in 2021 following a decade with FTSE in senior roles. Meanwhile, persistent increases in the fees index industry leaders charge clients for using their data could create another opening for Wilshire Indexes, Ghassemieh suggested.

PRICE WAR: Wilshire Indexes’ Reza Ghassemieh said his rm will seek to undercut competitors’ fees, which he says are rising every year.

It’s common for current industry leaders to lift prices by 4% to 5% a year, leaving a client who paid $200,000 in licensing fees a decade before having to pay two or three times that amount today for “exactly the same data,” he said.

In a market where institutional investors and money managers grouse constantly about fees, Ghassemieh says Wilshire Indexes is looking to be a disruptive force, with the intention of being “very commercially competitive.”

For clients using Wilshire Indexes’ U.S. series “in volume,” the company’s fees could be 40% to 50% lower, while offering longer contracts that can give clients con dence the rm won’t come back to them in a year or two looking to extract higher fees for the same data, he said.

By way of example, licensing fee discounts on that scale would slash to $100 million-$120 million from the roughly $245 million that exchange traded fund giant BlackRock paid MSCI in 2023, according to MSCI’s latest annual 10(k) ling. BlackRock, the lone client out

Allspring’s Burke: AI can’t do business relationships

Despite its potential, arti cial intelligence lacks the personal touch so important

By LYDIA TOMKIW

Kate Burke, president of Allspring Global Investments, thinks deep client relationships and customized approaches are critical for asset management — something that arti cial intelligence may not pick up on.

“It is a relationship business. And knowing your client and having those in-person discussions that pull apart the needs of you as an individual or you as a pension ... I don’t know that AI will ever fully pick that up,” she said in an interview with Pensions & Investments

Burke joined Allspring seven months ago after spending 18 years

AI powers hedge funds to strong performance

to asset management

at AllianceBernstein, where she was most recently the chief operating of cer and chief nancial ofcer. As president, she’s focusing on executing the rm’s transformation as an independent asset manager.

She sees a lot of value for AI across the ecosystem of asset management from operations to automating fund performance and agging inconsistencies on the risk side.

“I think it (AI) will drive productivity and insights and will ideally help modernize many of the processes that are inside an asset manager,” she said.

For Burke, a major focus is developing deep client relationships,

Record keepers turn to smaller plans to sustain 2023’s growth

By ROBERT STEYER

Surging stock and bond markets propelled record keepers’ record performance last year, but what can the industry do for an encore?

Consultants and researchers acknowledged the markets’ impact last year boosted assets under administration, but they said record keepers will need more consistent sources of future growth.

They predict more consolidation among record keepers, more educating sponsors to adopt auto enrollment, greater emphasis on keeping participants’ assets in plans and accelerated efforts in pursuing startup and smaller DC plans.

“The M&A game isn’t over,” said Bill Ryan, partner and de ned contribution team leader at NEPC. “I wouldn’t be surprised if three of the top 15 record keepers are acquired in the next 18 months.” He didn’t offer names.

“Organic growth for participants will be modest,” he added. Among the top 15 record keepers by participants in the latest annual Pensions & Investments survey, for example, ve had headcounts that were down or at from the previous survey.

Among record keepers responding to the P&I survey, almost all had higher assets under administration in 2023, but Ryan said he believes this thin-margin business will take its toll on some providers as competition causes a continued whittling of record-keeping fees.

The largest record keepers rebounded ercely last year, producing aggregate assets under administration of $10.79 trillion as of Dec. 31, 2023, up 23.3% from the $8.75 trillion as of Sept. 30, 2022.

The survey compared the 15 months ended Dec. 31 vs. the 12 months ended Sept. 30, 2022. P&I made the change because most client ows occur during the fourth quarter of each calendar year. Comparisons between 2023 and 2022 were affected by Ascensus ($207.3 billion) and BPAS ($12.9 billion), which provided data

SEE GROWTH ON PAGE 23

Arti cial intelligence has grabbed recent headlines, but it’s been used by hedge funds for many years. The Eurekahedge AI Hedge Fund index, showing returns starting in 2010, consists of funds that use AI and machine learning for their trading practices. While recent index returns have lagged the overall Eurekahedge Hedge Fund index, the AI hedge fund index has generated better long-term risk-adjusted returns.

Short-term woes: The Eureka AI Hedge Fund index underperformed the Eureka Hedge Fund index in nine out of the last 15 months through the end of March. The AI index’s average monthly return was 0.7%, compared with 0.9% for the overall hedge fund index. Additionally, AI’s volatility was higher, at 7.1% vs. 5.3%.

Monthly index returns

Better in the long term: Looking at annual returns, AI hedge funds bested overall hedge funds half of the time, in seven of the last 14 years from 2010 through 2023. Year to date, AI hedge funds returned 3.6% in the rst quarter, trailing overall hedge funds by about 140 basis points.

Annual index returns

Sharpe contrast: The AI index returned 10.1% with 6.2% volatility from 2010 and 2023, resulting in a higher Sharpe ratio than the S&P 500, Bloomberg Agg and overall hedge fund indexes. Even omitting 2010’s 54.2% return, the AI index’s 7.1% return (5.3% volatility) bested the overall index (5.5% with 5% volatility). Index risk & return, 2010- ’ 23

Pensions & Investments May 6, 2024 | 3

Defined Contribution

Money

PERSONAL TOUCH: It’s a relationship business, says Allspring President Kate Burke.

Management

| SEE WILSHIRE ON PAGE 24 SEE BURKE ON PAGE 26

Sources: Eurekahedge, Bloomberg Compiled and designed by Larry Rothman and Gregg A. Runburg

-5% -4% -3% -2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% M F J D N O S A J J M A M F J 2023 2024 Eurekahedge AI Hedge Fund index Eurekahedge Hedge Fund index S&P 500 index Bloomberg U.S. Aggregate Bond index -20% -15% -10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40% 2024 2023 2022 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 Eurekahedge AI Hedge Fund index Eurekahedge Hedge Fund index S&P 500 index Bloomberg U.S. Aggregate Bond index 54.2% Bloomberg U.S. Aggregate Bond S&P 500 Eurekahedge Hedge Fund Eurekahedge AI Hedge Fund Annualized return Volatility 10.1% 6.2% 6.0% 5.0% 13.1% 14.8% 2.5% 4.3%

‘Mother Nature is slapping us in the face,’ CalSTRS’ Ailman says

CARYL ANNE FRANCIA By

Amid political backlash and rising interest rates, ESG exchange-traded funds and mutual funds have stopped seeing in ows. Some U.S. red states have enacted or sought to pass laws outlawing ESG considerations in investments, while large asset managers have pulled out of climate-focused initiatives.

But at the California State Teachers’ Retirement System, sustainability is integrated “in everything, in

ension erisking

every way, in every minute of every day,” said Christopher Ailman, CIO of the $331.4 billion West Sacramento-based pension fund.

Despite the anti-ESG backlash unfolding across the U.S., CalSTRS is “still marching ahead because the environment isn’t changing,” he said at an April 16 panel held at the BloombergNEF Summit in New York.

A proponent of investing in the energy transition, Ailman will retire June 30 from the nation’s second-largest public pension fund,

where he has worked since 2000. He will continue to serve as an adviser through the end of 2024.

Ailman has said he will continue to press investors to factor in the risks of climate change into their investment decisions. For now, he’s emphasizing that sustainable investing is “all about long-term thinking,” which is important at CalSTRS, given it provides plan participants money for up to “potentially 60 years.” “I always like to share we have

Alternatives

Private credit is not ‘a monolith,’ according to Copia’s Thomas

ERIN ARVEDLUND By

Private credit is set to grow to $2.8 trillion by 2028 from $1.7 trillion currently, according to data from Preqin, and two portfolio managers in private credit believe there will be increased interest from institutional investors in the asset class.

That's due in part to banks retreating from private credit lending.

“Go back to 2013, and roughly 70% of sponsored middle-market transactions were nanced by banks,” said Shundrawn Thomas, founder and managing parter at the Copia Group, on a Pensions & Investments LinkedIn Live event April 17.

“That’s down 11% last year, so you can appreciate the shift” away from banks to private credit lenders, he said.

"There are more eyes on private credit, but it’s not new. it’s been going on for decades,” said Thomas, who prior to founding Copia in 2022 was president of Northern Trust Asset Management, a global investment manager with $1.3 trillion in assets under management at the time.

Private credit “is now much wider, it’s really just lending,” said Stephanie Rader, global co-head of alternatives capital formation within Goldman Sachs Asset Management, and executive vice president of Goldman Sachs Private Credit Corp.

Despite higher interest rates, “the credit markets have been resilient. Companies have been re nancing, enacting extensions, doing creative solutions with lenders. Defaults have ticked up but that’s been benign. Peak rates are behind us, peak leverage is behind us," Rader said.

Some pension funds have embraced private credit, while others want to wait for a market dislocation or other event to lower prices.

“From my time being an allocator, it’s a very attractive return, coming in cash coupons, principal payments, with less volatility of returns and lower drawdowns," said Thomas. Asset allocators "are saying ‘this has a role in my portfolio.’”

Historically, private credit has

4 | May 6, 2024 Pensions & Investments

ESG

SEE CREDIT ON PAGE 18

*Only asset owners and a limited number of consultants are invited to attend. All registration requests are subject to verification. P&I reserves the right to refuse any registrations not meeting our qualifications. The agenda for the Pension Derisking is not created, written or produced by the editors of Pensions & Investments and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc. Questions? Please contact Kathleen Stevens at kstevens@pionline.com | 843.666.9849. COMPLIMENTARY REGISTRATION AT PIONLINE.COM/PD2024* WELCOME THE 2024 ADVISORY BOARD: LEAD SPONSORS: October 8-9 ATLANTA Stephen Fowler Director Treasury Corning Incorporated Alethea Cababa Senior Manager, Retirement Plans Hearst Corporation Jonathan Glidden Managing DirectorPension Delta Air Lines Laurence Fulton Chief Investment O cer Verizon Michael Kreps Principal Groom Law Konstantinos Grigoriadis Treasury ManagerPension Investments DXC Technology Corp. Megan Nichols Partner, Head of Pension Settlement Solutions Aon Anna McTigue, CFA VP, Head of Public Markets Johnson & Johnson Chantel Sheaks Vice President US Chamber of Commerce Shawn Pope Director of Investments Cox Enterprises Charles Van Vleet Assistant Treasurer/CIO of Pension Investments Textron, Inc. Matthew Stroud Senior DirectorGlobal Pensions Marsh & McLennan GENERAL SPONSORS: ASSOCIATE SPONSOR: MARKETING PARTNER:

PD24-AB House Ad 1 40'.indd 1 5/1/2024 11:00:51 AM

SEE C al STRS ON PAGE 20 Cayce Clifford

IT’S NOT EASY BEING GREEN: CalSTRS’ Christopher Ailman says despite the political backlash, the fund is all-in on sustainability.

RETIREMENT INCOME

REGISTRATION QUESTIONS? Please contact Kathleen Stevens kstevens@pionline.com | 843.666.9849. *Only asset owners and a limited number of consultants are invited to attend. All registration requests are subject to verification. P&I reserves the right to refuse any registrations not meeting our qualifications. The agenda for the Retirement Income Conference is not created, written, or produced by the editors of Pensions & Investments and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc. REGISTER NOW AT PIONLINE.COM/RI2024

Solutions for the Decumulation Phase J. Brian Coleman Vice President, Total Rewards Dawn Food Products Shirley Cheung Senior Director, Global Risk & Investments Comcast NBCUniversal Paul Brown CFA, CAIA Director of Investments Deere & Company Jaime Erickson Director, Retirement Plans (US & Puerto Rico), Corporate HR Abbott Labs Kaye Downey Financial Benefits Manager Meta June 18, CHICAGO June 20, NEW YORK MEET OUR 2024 SPEAKER FACULTY: Natalia Sandoval Associate Director, Retirement Plans and Puerto Rico Health and Welfare Organon Sue Rutherford Associate Director, Retirement Plans & Benefits Finance Northwestern University Chantel Sheaks Vice President Retirement Policy US Chamber of Commerce Ben Roberge Director, Financial & Retirement Programs Unum Diana Winalski Deputy Chief Investment O cer International Paper Company Paul Visconti Sr. Director Total Health & Retirement Programs Avangrid ASSOCIATE SPONSOR: SUPPORTING SPONSOR: MARKETING PARTNER: SPECIAL THANKS TO OUR SPONSORS LEAD SPONSORS: Hugh Penney Senior Advisor Benefits Planning Yale University Dimitra (Demi) Hannon Director, Well Being and Retirement Strategy The Boeing Company Carl Gagnon AVP, Global Financial Wellbeing & Retirement Programs Unum Doug Gardner CEBS, CSPS Director, Corporate Human Resources Seneca Foods Corporation Michael Jabs Associate Director, Pensions The Kraft Heinz Company

SOPHIE BAKER

Consolidation is an often-used term in money management. But right now, it’s also big business in the U.K. for the retirement industry’s master trusts.

Also known as multiemployer retirement plans, the U.K.’s master trust market is only growing as the shift to de ned contribution continues — around 30 plans hold about 75% of trust-based assets in the U.K., equivalent to about £105 billion ($126.6 billion), as of Dec. 31, 2022.

But those 30 master trusts are ripe for consolidation, sources said — and one of the biggest deals in the master trust market last year was Smart Pension's acquisition of

Evolve Pensions.

The U.K. master trust market represents big money already, but with assets owing into DC showing no signs of slowing, it'll only get bigger. The U.K. government estimates that the top 5 master trusts could hold about £300 billion in assets by 2030.

While terms of the deal were not disclosed at the time, Smart Pensions CEO Jamie Fiveash and Evolve Pensions CEO Paul Bannister disclosed the details of the agreement in an

exclusive interview with Pensions & Investments, outlining the work that’s done and what’s still to come.

“We started looking about four

years ago…at the future (of Evolve’s own master trust, Crystal Trust,) how to secure the future for staff, and I couldn’t make it secure,” Bannister said. “I couldn’t do things I wanted to do.”

Conversations with Smart started about three years ago, and it soon became clear that any deal there would be an opportunity — to add tools to the business that Bannister didn’t have time or expertise to do himself, to enable his staff of about 40 people to better their careers, and work on general “things we wanted to do but we couldn’t turn around quick enough.”

Evolve is de nitely the right name for the company, which is not only the parent of the master trust but also provides DC administration, consultancy and secretary services. It’s been through a number of iterations, starting as the JIB Pension Scheme for electrical contractors, morphing into BlueSky Pension Scheme, which transitioned into Crystal in 2020. The BlueSky Pension Scheme and Crystal were two of the rst master trusts to be granted authorization by the Pensions Regulator. Crystal has more than 1,600 employer members and 128,000 participants. The plan has about £870 million in assets.

Then two years ago, Bannister told Jessica Rigby, director of strategy at Evolve, that “now’s the time. We were under more pressure — regulation, (the need to be) building better strategies, better tools — and we couldn’t,” he said. “We were sort of on the edge of standing still — we didn’t have the money, the time,” he added.

And then in January last year, they decided that Smart was the right home. The deal was nalized in June last year, and the rm’s announced in July that Smart would acquire Evolve for an undisclosed amount.

Executives at both businesses are now dealing with the front-end of the integration — systems, interface for employers and other user focuses.

So what else is left to do? The last contributions owed into Evolve for the month of March, and then legacy bank accounts were closed in April. Emails are changing over to Smart, and members and participant communications will be sent out, reminding them of the move. The business will be wound up over the coming months, with the Crystal plan also wound up. August is a big month — the target for the transition of assets to Smart.

It's not just the movement of assets that executives need to be aware of — but the physical movement of people. Evolve is based in Swanley, a town in Kent, England. “We have got to remember we are a local business — most of our staff have only ever worked in Swanley.

into

6 | May 6, 2024 Pensions & Investments

Going

Defined Contribution

master trust consolidation is growing. Here’s how one worked. Evolve needed resources to secure its future, and Smart Pension stepped in SEE CONSOLIDATION ON PAGE 23

U.K.

*Only asset owners and a limited number of consultants are invited to attend. All registration requests are subject to verification. P&I reserves the right to refuse any registrations not meeting our qualifications. The agenda for the Sustainable Returns is not created, written or produced by the editors of Pensions & Investments and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc. Questions? Please contact Kathleen Stevens kstevens@pionline.com | 843.666.984. COMPLIMENTARY REGISTRATION AT PIONLINE.COM/SR2024* 2024 SPEAKERS INCLUDE: GENERAL SPONSORS: Laura Payne Director, Public Markets/ESG Builders Vision David Zellner Chief Investment O cer Wespath Benefits and Investments Adrian Silver Carbon Strategist Carbon Direct Inc. John D. Skjervem Chief Investment O cer Utah Retirement Systems Shaska Chirinos Relationship Manager PRI Rebecca Brown CFP Director, USA Tobacco Free Portfolios Tobacco Free Portfolios Disen Huang Assistant Professor Rutgers Jennifer Koelle Investment O cer –Public Markets Illinois State Board of Investment Sustainable Returns Alpha & Risk Mitigation June 11-12 CHICAGO Ryan Fox Managing Director, Head of Responsible Investing New York Life LEAD SPONSOR: SR24-Spk House Ad 5 40'.indd 1 4/29/2024 2:44:09 PM

By

EVOLUTION OF A DEAL: Conversations between Smart Pensions CEO Jamie Fiveash (left) and Evolve Pensions CEO Paul Bannister began three years before the deal.

THE ENERGY TRANSITION

Sparking Opportunities

Institutional allocators are actively examining investment opportunities across the energy transition value chain, as more companies move to adopt – and improve their progress toward – low carbon goals in the shift toward a net-zero emissions economy. It’s a burgeoning space with expanded usage of renewable energy, advances in technology, more data availability, and global regulatory policy that encourages clean energy and energy security.

This supplement will help asset owners decipher the breadth of energy transition strategies today, from the use of clean technologies in power generation, EVs and renewables, to the clean-energy supply chain and additional sectors leading the way in embracing low carbon and net zero goals. It will highlight current strategies, both listed and private, that investors are pursuing – while also maintaining appropriate riskadjusted return targets.

Panelists will share insights into some current transitionrelated funds and strategies, and they will address challenges such as how investors are positioned for the long investment cycle, valuations, data and measurement issues, and wider economic impacts.

Sponsored by:

The content of this supplement and webinar is not created, written or produced by the editors of Pensions & Investments and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc. For information on participating in P&I Custom Content projects, please contact Julie Parten at julie.parten@pionline.com.

pionline.com/energy-transition-report2024 Read all the articles and access exclusive sponsor content online: WEBINAR REGISTRATION: pionline.com/energy-transition-webinar24 FREE WEBINAR Wed, May 8 | 2:00 PM ET PANELISTS: Jennifer Boscardin-Ching Client Portfolio Manager Thematic Equities Pictet Asset Management MODERATOR: Gauri Goyal Senior Director, Content & Programming Pensions & Investments Alicia White Senior Product Manager Morningstar Sustainalytics David Boyce CEO Schroders Greencoat North America ADVERTISING SUPPLEMENT THE ENERGY TRANSITION Sparking Opportunities

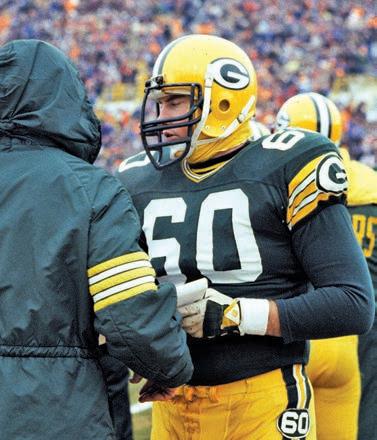

DRIVEN TO DELIVER

Blake Moore’s NFL journey helped shape his asset management career

E. Blake Moore Jr., the president and CEO of Touchstone Investments, has come full circle. He now runs an asset management rm in the town, Cincinnati, where he began his pro football career over four decades ago.

He played in the NFL as an offensive lineman in the early 1980s — four seasons with the Cincinnati Bengals (including a trip to the Super Bowl in 1982) and two more years with the Green Bay Packers before retiring in 1985.

Moore, who would later secure a degree from Harvard Law School before joining the ranks of asset management, said his career on the gridiron helps him in his current role.

“The discipline and rigor required to compete in the high-pressure NFL helped shape my career and leadership style long after football,” he said. “The NFL demands the very best out of each player each week, so as an undrafted free agent rookie at tryouts, I knew I had to deliver above-average effort and results to survive the training

camp cuts and make the roster.”

Moore learned quickly that being “average” in the NFL was never going to be good enough.

“The same applies to the asset management industry, where our clients are relying on us to beat the benchmarks and deliver returns that enable them to meet their nancial goals,” he added. “If all we do is deliver average returns, we should expect our clients to cut us and nd a better-than-average manager.”

Moore indicated that he always saw football as a “fun” endeavor, not as an end in itself.

“I went to a Division III school (College of Wooster in Ohio) without a scholarship and

Real estate managers may have increasing access to physical climate risk data but few know what to do with that information, an issue a new paper by the Urban Land Institute and LaSalle Investment Management aims to address.

According to a LaSalle analysis, 34% of the $850 billion in U.S. commercial real estate tracked by NCREIF Property index in the fourth quarter was located in high and medium-high climate risk zones.

This is ULI and LaSalle’s second joint paper on the topic. Their rst paper, released in 2022, focused on obtaining and interpreting reliable climate data.

“What we learned is there is no perfect data,” said Julie Manning, global head of climate and carbon at LaSalle Investment Management. "In fact, one of the mantras that I said like a broken record to my team is that you need to understand what the data is telling you but also what the data is not telling you.”

The new paper provides a framework for incorporating physical climate risk into real estate underwriting.

The rst step is to make sure the data isn’t wrong, Manning said. “You know the building. You know the location it’s in. Does that (data) make sense to you?” she said.

In one instance, climate risk data agged a risk for ooding because the property was a certain distance from a river, she said. What the data provider didn’t know was that the property was on a hill that was several hundred feet from that river, Manning said.

Once the risks have been accurately identi ed, managers need to analyze the cost of mitigating those risks, the report shows.

And that mitigation is very particular to the property in question, she said. For example, LaSalle has a logistics property in Osaka, Japan, which is a at coastal city where buildings are required to be 3 meters above sea level. Due to the coastal ood risk, LaSalle executives decided to raise the buildings another 1.5 meters and located equipment at higher levels, Manning said.

I didn't start thinking about possibly playing in the NFL until my junior or senior year of college,” he noted. “Even when I started training camp at the Bengals, I was all set up to go to law school out of college and pursue a career in law or business.”

After graduating from Harvard Law in 1989, Moore held various executive roles at a number of major rms, including Allianz Global Investors and UBS Global Asset Management, before taking the top job at Touchstone in 2020.

Moore wouldn’t be surprised if more pro athletes followed in his footsteps.

“An athlete’s competitive drive and desire to win, combined with the discipline to put in the hard work required to succeed, can play well in our business, whether in a sales-oriented position or portfolio management role,” he said.

Touchstone, which manages a number of active mutual funds and ETFs, has about $28.9 billion in assets under management.

STAYING THE COURSE

CalPERS’ Frost vows to keep up the ght against climate change

In announcing Michael Cohen’s appointment as chairman of the steering committee for Climate Action 100+, CalPERS’ CEO Marcie Frost told pension fund board members that his appointment comes at “a crucial time.”

Cohen is the chief operating investment of cer at CalPERS, which in 2017 co-founded Climate Action 100+, a coalition of investors that works with the world’s largest corporate greenhouse gas emitters to take steps to ght climate change.

“Not only are we ghting the existential race against the clock, but we are also, sadly, ghting in some corners a creeping sense of complacency,” Frost said at the pension fund’s April 16 board meeting. “But this is not time to be complacent ... The cause of combating climate change will not move forward on its own.”

This is the second time one of CalPERS’ executives has chaired the group’s steering committee.

The role of steering committee chair rotates every 12 months. Anne Simpson, former head of board governance and sustainability at the $491.4 billion California Public Employees’ Retirement System, Sacramento, served as the group’s

inaugural chair. But instead of expanding the number of high greenhouse gas-emitting companies willing to work to reduce emissions, in recent weeks, in uential investors have decided that they no longer want to be part of a global coalition, Frost said.

In March, four of the 20 largest money managers by assets under management — $4.34 trillion State Street Global Advisors, $3.56 trillion J.P. Morgan Asset Management, $1.86 trillion PIMCO and $1.63 trillion Invesco — left Climate Action 100+, which has more than

compensation trending at U.S. public pension plans?

What are U.S. public pension fund staff earning these days? The National Conference on Public Employee Retirement Systems and CBIZ’s talent and compensation solutions division are teaming up on a compensation survey for U.S. public pension funds to nd out. Both organizations have conducted their own surveys in the past, and the partnership will enable a “uni ed, more robust dataset,” said

Hank Kim, executive director and counsel for NCPERS, in an April 24 news release.

The need for that more robust dataset became clear to NCPERS when its most recent compensation survey showed almost 60% of public pension funds are experiencing signi cant challenges with recruitment and retention, said Kim.

“We hope to increase transparency into compensation and bene ts

700 investors representing about $68 trillion in total assets. The largest money manager in the world, BlackRock, with $10.47 trillion in AUM, shifted its relationship to its international business.

“The constant bombardment of information or political pressure … It has given these investors pause about staying the course and nishing the work,” said Frost. “As our investment team shared with the board last month, we listen to the institutions that recently chose a different path. We can’t speak to their decisions because we see things differently.”

Cohen, she added, serves as steering committee chair at “a pivotal moment” as the group pushes to get consistent information for investors including its effort to create a net-zero benchmark for companies, she said.

“Climate risk can lead to instability for investors, lower returns and higher volatility,” and CalPERS of cials have a duciary duty “to be relentless in examining risk,” Frost said.

“I am honored to be appointed chair of the Steering Committee and eager to help guide the organization through its next phase of investor engagement,” Cohen said in a news release.

ARLEEN JACOBIUS

packages at state and local pension plans to help identify what resources are needed to attract and retain quali ed, high-functioning staff,” said Kim.

The survey will include comprehensive salary and bonus data for more than 80 common positions found at public pension funds. NCPERS plans to distribute the survey in May to the 500 pension funds, sponsors and other stakeholders in its organization.

NCPERS’ 2023 survey provided information on 13 mid- and senior-level staff positions and re ected responses from 176 participants.

ROB KOZLOWSKI

8 | May 6, 2024 Pensions & Investments

ARLEEN

JACOBIUS

REPORTERS NOTEBOOK

PALASH GHOSH

PUTTING IN THE WORK: E. Blake Moore Jr. played in the NFL for six seasons.

LOCATION, LOCATION, LOCATION: To mitigate flooding risks, LaSalle built a logistics warehouse in Osaka, Japan, higher than mandated.

BUILDING CONFIDENCE LaSalle, ULI unveil framework for using climate risk data

E. Blake Moore Jr.

THE SKINNY ON PAY

How’s

Vernon J. Biever/AP

FIGHTING COMPLACENCY: Marcie Frost says CalPERS won’t be swayed by political pressure.

Jayson Carpenter

GLOBAL MACRO PROVIDES ALLSEASON COVERAGE

Even as the U.S. Federal Reserve and other central banks prioritize getting inflation under control, which sets the stage for lower interest rates, institutional investors face no shortage of ongoing global macroeconomic and geopolitical issues that can keep capital markets — and investment portfolios — volatile.

That’s one reason why a global macro strategy can — and should — play a role in institutional portfolios. Not only can it provide juice to a portfolio during periods of market uncertainty, it can also offer a steady anchor to other investment strategies when times are relatively stable. Viewed as such, global macro can be a useful strategy for all types of institutional investors.

“Allocators should consider macro strategies as an important addition to their portfolios,” said Christian Dery, head of macro strategy at Capital Fund Management (CFM), a global quantitative and systematic asset management firm. “First, it can be a consistent source of return and diversification; and second, it can generate insights for other areas of the portfolio exposed to macro risks.”

Those insights are critical, because all asset allocations — equity and bonds, alternatives buckets, real assets — face macro risks.

Global macro seeks to understand specific scenarios — whether economic, political, regulatory or other factors — that will affect financial assets, and it considers all asset classes and geographies to take advantage of those scenarios.

“The opportunity set spans a broad range of liquid asset classes — including foreign exchange, equities, rates, credit and commodities — with the ability to position long or short across the world to construct uncorrelated and diversified strategies,” said Dery.

UNDERSTAND WIDER IMPACTS

“You can think of macro as a strategy that eventually impacts all strategies,” he said. Dery pointed to 2022, when equity long-short strategies underperformed as central banks aggressively ratcheted up interest rates to combat inflation. Many macro investors understand this playbook well and positioned successfully in 2022. Other strategies would have benefitted from a deeper understanding of emerging macro risks.

“For long-term investors with buy-and-hold portfolios, 2022 was a perfect example of macro impacting passiveinvestment portfolios,” he said. “Inflation and the Fed’s appropriate response caused both stocks and bonds to underperform, breaking the flight-to-quality properties of safe bond portfolios.”

“Not paying attention to the macro environment introduces unnecessary tail risk into strategies,” Dery said. Even strategies that appear market neutral will eventually flash macro biases, he added. For that reason, understanding the role that macro strategies can play is “critical” for all types of investors in order to better understand changing economic trends and their impact on markets and portfolios.

SYSTEMATIC FRAMEWORK

The two foremost global macro strategies are systematic and discretionary. It’s important for investors to understand their key differences. Systematic funds follow rules-based strategies, while discretionary funds rely on managers to make day-to-day investment decisions.

The two approaches have generated complementary performance patterns over various market environments, but the systematic approach can provide better comparative returns and broader diversification by leveraging significantly

more data, computing and technology to test ideas and invest in a wider range of instruments and markets.

Another major difference is cost. “Discretionary traders will have competent execution desks,” but as assets under management grow, trades and positions become larger, which can make it more difficult to control transaction costs, he said.

“At CFM, we dedicate significant research and technology resources to understanding transaction costs,” he added. “Investors forget that transaction costs are the largest cost in strategy implementation, higher than fees paid to access strategies. We store a terabyte of tick data daily and have a database of over 250 million executed trades. This information automatically feeds back into our investment processes and improves execution costs on an ongoing basis.”

Because it trades many more instruments globally, a systematic approach achieves significantly more diversity, not only in markets traded but also in the source of ideas.

“Discretionary funds might not be doing this as effectively, leading to performance leakage,” Dery said.

Another key difference is around diversification. Discretionary global macro portfolios tend to be concentrated, making them potentially riskier than a systematic global macro portfolio. And the bigger the discretionary portfolio, the greater the concentration as human risk takers are forced into a narrow set of liquid contracts to express a small number of investment ideas, Dery explained.

“Because it trades many more instruments globally, a systematic approach achieves significantly more diversity, not only in markets traded but also in the source of ideas,” he said.

“There are certain opportunities which are impossible for a human to capitalize on. For example, small, statistically significant opportunities that decay quickly can only be captured with a platform that has achieved a critical technological scale. It turns out that adding up many of these small but statistically significant effects results in high-performing portfolios.”

HUMAN INPUT

Another major factor that sets systematic global macro apart from discretionary is the human factor.

“Our research process is a form of scientific discovery in which numerous ideas are generated and assessed,” Dery said. “The ability to ideate is only limited by the number of researchers and their creativity, the availability of data and our technology stack. Significant investment in these areas has allowed us to achieve scale.”

“A systematic approach is ruthless. It never sleeps, has no emotions and is continuously adapting,” Dery said. “A human trader might get tired or be having a bad day. This can lead to bad decision making and potentially inferior trades. Ultimately, this will leak into performance.”

But that doesn’t mean that every risk can be captured in a model. “The primary function of our market risk group is

Christian Dery Head of Macro Strategy

to identify emerging risks and determine how they will affect our strategies. As a quantitative manager, we rarely override models but in highly uncertain scenarios, we can reduce our overall exposure to an emerging risk.”

THREE-PILLAR FOUNDATION

CFM’s global macro strategy is built on three pillars: research, portfolio construction and execution. The firm uses a quantitative, data-driven approach to identify macro trends and attractive investments related to those trends. The strategy is systematically implemented across a diversified range of financial instruments and asset classes.

The firm not only has a dedicated global macro fund, but it also applies the same scientific approach for its other strategies. The process involves sourcing and analyzing data to create new investment insights and ideas, testing those ideas, validating them and building them into portfolios.

“The research platform allows us to scale and rapidly evaluate insights to determine if they add value to our strategies. The platform determines whether an insight adds new or statistically valid information to our portfolios or not.”

AGILITY ACROSS SCENARIOS

One of the benefits of a global macro approach is the ability to modify positions quickly, including the critical function of being able to identify and react to major economic, geopolitical or policy changes, he said. This is especially true in periods marked by higher levels of uncertainty, when a global macro manager needs to stay agile to assess the pace and flow of data.

Even the most diverse investors — those allocating significantly to hedge funds at one end and those employing buy-and-hold strategies at the other — face ongoing risks that will impact their investment portfolios. That’s where a global macro strategy can make a difference.

“Adaptive statistical approaches are codified into our models and strategies,” Dery said. “This allows us to detect and react to regime changes quickly.”

“We live in a complex world that is continuously changing.” For example, the last few years have featured rising interest rates, elevated inflation and increased geopolitical risks. The investment environment so far in 2024 has been characterized by uncertainty around the timing of central banks’ next moves, improving economic indicators and a raft of geopolitical hotspots.

“Through a combination of insights generated from our strategies and our deep bench of experienced researchers, we strive to stay in front of key macro risks,” he added. “Investors can benefit from these insights as well to help them better understand embedded risks in their own portfolios.”

“Macro strategies can always find interesting investment opportunities irrespective of the environment,” Dery said. ■

This sponsored Investment Insights was not created, written or produced by the editors of Pensions & Investments and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc. For information on participating in P&I Custom Content projects, please contact Julie Parten at julie.parten@pionline.com.

pionline.com/global-macro-cfm24

Sponsored by:

SPONSORED SECTION

Any description or information involving investment process or allocations is provided for illustration purposes only. There can be no assurance that these statements are or will prove to be accurate or complete in any way. This article does not constitute an offer or solicitation to subscribe for any security or interest.

Capital Fund Management

(CFM)

OPINION

VIEWS ANGELO CALVELLO

Deepfakes — the next threat for investors

There’s a short video of Jim Dunn, CEO of Verger Capital Management, talking about arti cial intelligence and investing, at pionline.com/ deepfakes

But Jim never made such a video and he never spoke those words (those come from one of my articles). The video is a deepfake. One of my colleagues took a photo of Jim and a short recording of Jim’s voice and, using open-source technology, in about 15 minutes, cloned Jim’s voice and transformed his picture into a video. (For security reasons, we deliberately chose to make a lower quality deepfake of Jim.)

sexual misconduct.

■ A deepfake of a false corporate earnings report or a non-existent M&A transaction posted on social media leads investment managers to make damaging trades.

■ A scammer creates a deepfake of a partner at a private equity rm and, via a Microsoft Teams call, directs the operations group at a pension fund to wire $25 million to meet a capital call.

hard-to-detect deepfake still requires signicant graphics-editing and audio-dubbing skills and the use of a high-quality graphics processing unit (or GPU).

A deepfake is a video, recording or photo the subject never actually participated in, and while Jim gave us permission to create this deepfake, bad actors use deepfakes to create non-consensual pornography of celebrities and ordinary woman and unauthorized political messages.

Deepfakes have the potential to be particularly concerning for allocators and investment managers, as malefactors could use deepfakes to commit various nancial crimes or tarnish a rm’s reputation.

For example:

■ A disgruntled former employee uses voice cloning technology to create a deepfake of a portfolio manager’s voice and calls a trading desk to place unauthorized trades that adversely impact his former employer’s fund’s performance.

■ A PM reacts to a deepfake of a Federal Reserve governor making plausible but false statements about the Fed’s view of in ation and interest rates posted on social media.

■ A bad actor posts a deepfake video of the CEO of a publicly traded asset manager in which the CEO announces his resignation because of accusations of embezzlement and

This last example is derived from a stark real-world example. In late 2023, a scammer used a deepfake to pose as the chief nancial of cer of a multinational rm to trick a nance worker into paying out $25 million. CNN reports that “The elaborate scam saw the worker duped into attending a video call with what he thought were several other members of staff, but all of whom were, in fact, deepfake recreations. … Believing everyone else on the call was real, the worker agreed to remit a total of HK$200 million Hong Kong dollars — about $25.6 million.”

Deepfakes are created by using deep learning technologies (hence the “deep” in “deepfake”), often generative adversarial networks (or GANs). Yet, despite the complexity of the underlying technologies, almost anyone can manipulate videos, audio and images to create deepfakes without the need for extensive programming skills. Free web-based deepfake applications and opensource frameworks like DeepFaceLab make it easy and relatively inexpensive to create deepfakes. (Some platforms are free, while others charge as little as $20 for a simple deepfake and $80 for a more complex deepfake.) However, creating a convincing and

This easy access and advancement in technology will lead to a tsunami of deepfakes, especially in 2024, a “super election year,” with closely watched elections in the United States, Mexico, India and Indonesia. Security experts, like FBI Director Christopher Wray, warn that deepfakes and other AI-generated content intended to sow misand disinformation will intensify because the generative AI makes it easy for “both more and less sophisticated foreign adversaries to engage in malign in uence while making foreign in uence efforts by players both old and new, more realistic and more dif cult to detect.”

Beyond 2024, the International Data Center Authority cites experts who estimate that “as much as 90% of content on the internet may be AI-generated by 2026.” In addition to deepfake technologies, “we're seeing that people are using AI to generate garbage on literally everything, in every format, for the revenue that advertising brings. As AI gets better this content will become harder to distinguish from legitimate content, which will cause problems when people are looking for factual information,” writes data scientist Joel Therrien in response to “Inside the World of TikTok Spammers and the AI Tools That Enable Them.” This ood of garbage content will have

consequences

profound

for investment rms 10 | May 6, 2024 Pensions & Investments

TO CONTACT A P&I STAFFER Unless otherwise noted above, email us at firstinitiallastname@pionline.com or find phone numbers at pionline.com/staff KC Crain CEO Nikki Pirrello President & publisher Jennifer Ablan Editor-in-chief/chief content of cer JENNIFER.ABLAN@PIONLINE.COM Julie Tatge Executive editor Erin Arvedlund Managing editor ERIN.ARVEDLUND@PIONLINE.COM Kevin Olsen Enterprise editor Gennady Kolker Audience development editor GENNADY.KOLKER@PIONLINE.COM John Fuller News editor JOHN.FULLER@PIONLINE.COM Sophie Baker International news editor Meaghan Offerman Associate editor MEAGHAN.OFFERMAN@PIONLINE.COM Colette Jordan Chief copy editor Ann Acum Editorial operations associate ANN.ACUM@PIONLINE.COM Caryl Anne Francia Editorial intern CARYL.FRANCIA@PIONLINE.COM Abigail Parrott Editorial intern ABIGAIL.PARROTT@PIONLINE.COM REPORTERS Douglas Appell Money management Hazel Bradford International Margarida Correia De ned contribution Brian Croce Washington Courtney Degen Washington COURTNEY.DEGEN@PIONLINE.COM Palash Ghosh General assignment PALASH.GHOSH@PIONLINE.COM Arleen Jacobius Private equity/real estate Natalie Koh International NATALIE.KOH@PIONLINE.COM Rob Kozlowski General assignment Christopher Marchant International CHRISTOPHER.MARCHANT@PIONLINE.COM Kathie O’Donnell ETFs KATHIE.ODONNELL@PIONLINE.COM Robert Steyer De ned contribution Lydia Tomkiw Hedge funds LYDIA.TOMKIW@PIONLINE.COM ART Gregg A. Runburg Art director DATA/RESEARCH Aaron M. Cunningham Director of research and analytics Larry Rothman Data editor LARRY.ROTHMAN@PIONLINE.COM Anthony Scuderi Directory manager Julie Parten Senior VP-commercial operations JULIE.PARTEN@PIONLINE.COM Mike Palazuk VP-product MICHAEL.PALAZUK@ PIONLINE.COM SALES Lauren DeRiggi Digital specialist/account manager LAUREN.DERIGGI@PIONLINE.COM Judy Kelly New York JUDY.KELLY@PIONLINE.COM Annika Mueller Midwest ANNIKA.MUELLER@PIONLINE.COM Kimberly Jackson Director of conference sales Andy Jenkins Account manager, conferences ANDY.JENKINS@PIONLINE.COM Ed Gorman EMEA +44-(0)20-3823-9891 Thomas Markley Account executive THOMAS.MARKLEY@PIONLINE.COM Stacey George Manager of sales operations STACEY.GEORGE@PIONLINE.COM CUSTOM CONTENT/CONFERENCES/ MARKETING/CLIENT SERVICE Gauri Goyal Senior director, content and programming Diane Pastore Director of conference programming Tammy Scholtes Director of conference programming Joshua Scott Director of conference programming JOSHUA.SCOTT@PIONLINE.COM Howard Moore Associate editor, content solutions HOWARD.MOORE@PIONLINE.COM Corina Lewis Associate project director Sarah Tumolo Senior conference and events manager SARAH.TUMOLO@PIONLINE.COM Mirjam Guldemond Conference manager, WorldPensionSummit +31-6-2333-2464 Assel Chanlatte Conference marketing manager Andy Jang Conference & events coordinator Alison Rivas Marketing & events specialist Kathleen Stevens Investor relations director Erin Northrop Associate marketing manager ERIN.NORTHROP@PIONLINE.COM Todd Van Luling Digital project specialist TODD.VANLULING@PIONLINE.COM Tetyana Saucedo Digital campaign manager Nicole Callaghan Digital campaign specialist NICOLE.CALLAGHAN@PIONLINE.COM SUBSCRIPTIONS/SITE LICENSES Keith Arends Senior account executive KEITH.ARENDS@PIONLINE.COM Costa Kensington Account executive COSTA.KENSINGTON@PIONLINE.COM Erin Smith Sales manager, site licenses Jack Follansbee Account executive, site licenses JOHN.FOLLANSBEE@PIONLINE.COM REPRINTS Laura Picariello Sales manager 732-723-0569 LPICARIELLO@CRAIN.COM ADVERTISING PRODUCTION Sam Abdalla Media services manager (313) 446-0400 SABDALLAH@CRAIN.COM Subscription information - single copy sales: 877-812-1586

Angelo

is co-founder of alternative money management rm Rosetta Analytics. He is based in Chicago.

The International Data Center Authority cites experts who estimate that ‘as much as 90% of content on the internet may be AIgenerated by 2026.’ SEE CALVELLO ON OPPOSITE PAGE Gary Waters/The iSpot

Calvello

OTHER

OTHER VIEWS CHARLES E.F. MILLARD

Target-date funds should give private equity a ‘secondary’ thought

Participants in 401(k) plans are generally long-term investors.

Yet, most 401(k)s have no investment in an excellent long-term asset class: private equity — more specically, secondary private equity.

Today the vast majority of 401(k) and other de ned contribution participants are in target-date funds. Target-date funds take the selection of speci c asset categories out of individuals' hands and put it in the hands of the professional investor — the provider of the target-date fund. Target-date funds also take upon themselves the responsibility to derisk the portfolio as the participants near retirement age They do so by gradually decreasing exposure to higher risk securities and gliding the portfolio into lower risk investments.

Charles E.F. Millard is the former director of the U.S. Pension Bene t Guaranty Corp. He is a senior adviser for Ares Management, based in New York.

Charles E.F. Millard is the former director of the U.S. Pension Bene t Guaranty Corp. He is a senior adviser for Ares Management, based in New York.

One would think that such professionals would make appropriate use of a long-term investment like private equity, especially secondary private equity — which provides easier allocation of capital and broader exposure than typical private equity. Few do so. But they should.

Private equity offers exposure to large swaths of the economy that, by using exclusively public equity, most target-date funds are currently missing. They principally focus on index-level exposure to equities for their return-seeking assets. Usually, this is an allocation to a passive index like the S&P 500 or to an active manager that is meant to

that use data scraped from the web as inputs to their investment processes.

Allocators, managers, and the public should expect little protection from regulators, law enforcement, social media companies or technology companies.

Regulatory and policy frameworks are still evolving, making enforcement a challenge. For example, in the U.S., there currently are no federal laws that prohibit the sharing or creation of deepfakes (some states do have such laws, but they are generally limited in scope), and the European Union’s comprehensive AI Act regulates deepfakes through transparency obligations rather than an outright ban. (This source provides updated information on these jurisdictions and their deepfake-related regulations.)

Social media platforms have policies prohibiting the posting of deepfakes that are “signi cantly and deceptively altered, manipulated, or fabricated,” but enforcement of such prohibitions is neither straightforward nor rigorous. (In the U.S., such enforcement likely could lead to First Amendment challenges.) AI startups and big tech

match or beat the index. This is ne as far as it goes. That kind of breadth provides diversi cation and exposure to a large part of the economy. But, by focusing only on publicly traded companies, target-date funds do not get exposure to enough of the economy.

Fewer than 5% of U.S. companies with 100 or more employees are public companies. This is increasingly the case in recent years, as companies are staying private longer than they used to. In fact, there are about half as many publicly traded companies in the U.S. today as there were 30 years ago. In addition, an index like the S&P is market-cap weighted, so the largest companies have outsized allocations. Today the 10 largest companies in the S&P represent over 30% of the value of the index, even though the index contains 500 companies.

Private markets are increasingly markets that nance mature enterprises, building businesses and creating value through organic growth and operational excellence. They have become important pieces of the economic pie, and they drive fundamental economic growth. Additionally, nancial economists have long argued that private equity managers have access to value-creation tools that public market managers lack. They can change or augment management teams, improve governance structures and use capital markets in a more exible way. Investors who are not exposed to private

companies are building technologies to safeguard against the dissemination of deepfakes, but such technologies offer scant protection. Meta, for example, has created a means for placing watermarks (hidden or visible information about the origin of the content) on images to indicate it is generated by AI, yet researchers were able to remove the watermarks in two seconds. Other tech rms are creating deepfake detection programs, some of which are using biological signals (e.g., imperfections in the natural changes in skin color that arise from the ow of blood through the face or phoneme-viseme mismatches) or forensic techniques that model facial expressions and movements that typify an individual’s speaking pattern,” but there are limitations to these systems and these advancements “drive the increased quality of deepfake videos. GANs can catch up relatively easily; by updating the discriminator to evade the detector, the learning capacity based on feedback loops of those GANs will work to produce a deepfake that can fool the detector.”

This leaves allocators and investment managers on their own to develop deepfake survival skills.

The consensus among security experts like Stu Sjouwerman, the founder of KnowBe4, a rm providing security awareness

equity cannot access those tools.

But private equity poses certain challenges for a target-date fund. Investing in a few private equity funds does not provide the kind of breadth in the economy that the target-date fund needs. And most private equity investments require managing capital calls and dealing with the "J-curve." This means private equity investments usually go down on a mark-to-market basis in the early years.

Private equity offers exposure to large swaths of the economy that, by using exclusively public equity, most target-date funds are currently missing .

This is where secondary private equity comes in. Secondary private equity offerings normally include thousands of companies, rather than only the dozens that might be in an individual private equity fund. This offers the breadth and diversi cation that is a necessary hallmark of target-date-fund investing.

At least as important: Secondaries mitigate the J-curve. With secondaries, capital calls have typically already been made, so an investment does not get marked down by the requirement of additional investments.

An additional bene t of secondaries is

training, is for organizations to “train employees on the basics of deepfakes: what they entail, how they’re created, how they are used for malicious purposes, how they can damage the business, and how employees can help. Security teams must also run phishing and deepfake simulations so that employees build an instinct to recognize them. Employees must learn to evaluate lip movements, accents, background jitters, alignment issues, or unusual timing, and report any signs of suspicious activities.” (MIT’s Affective Computing group offers human-centric guidelines to identify deepfakes and other forms of engineered digital content.)

Because allocators and managers depend on third parties (custodians, fund administrators, brokers, etc.) to provide critical services, their due diligence process should include a rigorous assessment of the vendors’ digital security policy and procedures. Until there are stringent regulations and enforcement or a technological silver bullet, allocators’ and investment managers’ best defense against deepfakes— and all malicious AI-generated content — is the aphorism, “Never trust but always verify.”

that, unlike private equity funds (where the investor is betting that the private equity fund investor will invest well in companies that are typically unknown at the time of commitment), in secondaries, the portfolio companies are already known, and the secondary investors can underwrite the companies in the portfolio that they are buying.

One nal point regarding private equity and DC plans: If it is good enough for the DB plan, it should be available in the DC plan. De ned bene t pension plans have been investors in private equity for decades, and their returns show it.

Georgetown University's Center for Retirement Initiatives published a paper in 2023 that showed a substantial difference in the returns of DB plans using private equity compared with DC plans.

But the bene ciary of the private equity investment by the DB plan is not the pension recipient; it is the corporate plan sponsor itself. The pension recipient will receive the same de ned bene t regardless of the returns of the investments of the plan. The plan sponsor, on the other hand, can mitigate risk or enhance returns through the use of private equity. This has the potential — and the purpose — of helping the plan sponsor manage its contributions to the DB plan.

If the corporate plan sponsor can reap the bene ts of private equity investing, the DC participant should be able to as well. n

This content represents the views of the author. It was submitted and edited under Pensions & Investments guidelines but is not a product of P&I’s editorial team.

Share Pensions & Investments’ content with your social community

We're excited to o er the next level of article reprints! A stand-alone HTML digital article that will never be placed behind a subscription paywall. The P&I HTML reprint can be licensed to post to your website, share on social media, used in email correspondence, presentations and so much more.

Select from news articles (print and digital), rankings, opinion pieces, editorials, awards and more.

Contact Laura Picariello at lpicariello@crain.com or 732.723.0569 for pricing and details

Pensions & Investments May 6, 2024 | 11

n

of the author. It was submitted and edited under Pensions & Investments guidelines but is not a product of P&I’s editorial team.

This content represents the views

Calvello CONTINUED FROM OPPOSITE PAGE

OPINION P&I HTML

Reprints

EMERGING MARKETS

Managers keeping close eye on bumper crop of elections

In addition to the U.S. presidential contest, pivotal votes are taking place in India, Mexico and more

By CHRISTOPHER MARCHANT

In a year that is unprecedented in terms of its number of national elections — with roughly half of the world’s adult population due to go to the polls by the end of 2024 — money managers are keeping a close eye on results and the effect of those votes on emerging markets in particular.

Managers said they will be watching for the potential impact of votes in Mexico, India and South Africa on emerging markets assets, adding that, in order to preserve returns, thenancial sector may need to both appreciate long-term risk and understand what immediate turbulence can be caused by national elections.

But by far, the dominant viewpoint that emerged during money manager interviews is that the most signi cant election this year for emerging markets is not happening among developing countries at all: rather, they’re most closely watching the U.S. presidential contest between incumbent Joe Biden and challenger Donald Trump, slated for November.

“The market is probably cheering” for a Biden re-election, said Thierry Larose, a portfolio manager in the emerging markets bonds team at Vontobel Asset Management, which has CHF 103.3 billion ($113 billion) in assets under management. The last few years under Biden’s tenure have been “relatively friendly” for emerging markets assets, while the expectation is that the policy platform would be more “predictable” than a return of Trump to the White House, Larose said.

However, in the four years of the Trump administration, the MSCI World Markets index only showed a fall in annual performance in one year, dropping 14.57% in 2018, a year before the emergence of the COVID-19 global pandemic. In the three full years of the Biden administration, two have shown annual performance declines in the same index (-2.54% in 2021, and -20.09% in 2022).