NAV financing fills gap as GPs look to increase own commitments

AS GENERAL partners (GPs) look to increase the amount of commitments they make to their own funds, private credit funds have started picking up the cheque, offering flexible financing solutions to firms, as well as individuals.

“Managers want to invest more in their funds, show their limited partners (LPs) more conviction, and they may also want to open this up across the broader team, rather than just the three to four people at the top of the house,” said David Wilson partner at 17Capital.

When 17Capital provides such financing it is not usually for the minimum one or two per cent that is stipulated in the Limited Partners Agreements, Wilson said. It is more about helping them to make up to eight per cent or larger GP commitments. He noted that the financing is sometimes

for an individual, a team or the management company’s own balance sheet.

The fund typically uses the GP commitment in a previous fund or a different strategy as collateral, though

sometimes management fees and carried interest can also be included.

17Capital focuses on buyouts and looks for groups that are established and have a good track record. It does not lend to emerging managers

for GP commitments. The average deal size they see is around $200m (£149.5m), but Wilson noted that it can vary quite a bit.

“High performing brand name GPs looking to fuel growth, >> 4

Mid-Market EUROPE

Exploring debt & equity opportunities in the European Mid-Market segment

Pullman London St. Pancras 18 November 2025

info@royalcrescentpublishing.co.uk

EDITORIAL

Suzie Neuwirth Editor-in-Chief suzie@alternativecreditinvestor.com

Aysha Gilmore News Editor aysha@alternativecreditinvestor.com

Selin Bucak Reporter

Laura Purkess Reporter

Jon Yarker Reporter

Ellie Duncan Reporter

PRODUCTION

Tim Parker Art Director

COMMERCIAL

Tehmeena Khan Sales and Marketing Manager tehmeena@alternativecreditinvestor.com

SUBSCRIPTIONS AND DISTRIBUTION tehmeena@alternativecreditinvestor.com

Find our website at www.alternativecreditinvestor.com

Printed by 4-Print Limited ©No part of this publication may be reproduced without written permission from the publishers.

Alternative Credit Investor has been prepared solely for informational purposes, and is not a solicitation of an offer to buy or sell any private debt product, or any other security, product, service or investment. This publication does not purport to contain all relevant information which you may need to take into account before making a decision on any finance or investment matter. The opinions expressed in this publication do not constitute investment advice and independent advice should be sought where appropriate. Neither the information in this publication, nor any opinion contained in this publication constitutes a solicitation or offer to provide any investment advice or service.

Private credit has been front-page news recently, but not for the best reasons.

The collapse of US auto parts supplier First Brands and subprime auto lender Tricolor Holdings left a wide range of lenders exposed, raising questions about the health of the credit market.

However, the specific focus on private credit – and warnings of “cockroaches” and “canaries” from highprofile City figures – is slightly confusing.

The majority of First Brands’ debt was originated in the broadly syndicated loan market, not private credit. In fact, ratings agency KBRA has declared private credit’s exposure as “minimal”. So where is the commentary in the mainstream media warning of a “banking crash” or “banking bubble”?

Everyone I speak to in the industry concedes that default rates will tick up this year. Ultimately, the cycle has to turn at some point, and we’re in challenging macroeconomic times that will undoubtedly impact all facets of the economy and daily life.

But it seems like an overly dramatic leap to conflate a few individual cases of alleged fraud with systemic risk and the demise of a $1.7tn (£1.3tn) sector.

Should all lenders learn from this and take additional measures to identify fraud? Definitely.

Are the Bank of England’s proposed stress tests to assess the health of the industry a good thing? Yes, proof of private credit's resilience will be reassuring to regulators and investors alike.

Large credit losses should of course be scrutinised, but it’s important to strip away the hype from the facts.

Perhaps the actual ‘bubble’ is the fearmongering around the underlying events, and that’s what needs to be popped.

SUZIE NEUWIRTH EDITOR-IN-CHIEF

cont. from page 1

raise financing for initiatives like buying another manager or launching a new strategy, can use this solution,” he added. “As managers raise different strategies it's becoming a more balance sheet intensive business. They could also be looking for capital to seed retail or evergreen products.”

Arcmont has also been financing GP commitments, with

head of NAV financing

Peter Hutton saying that financing at the GPlevel has been “relatively starved of capital” with banks being the only real providers. The only alternative has been dilutive equity capital, he said, which is why lending by private credit firms has been growing.

“GPs have deployed a lot since Covid, and as a result, they haven’t

yet realised the value creation of those assets yet,” he said. “The rise in interest rates hasn’t helped either. Now, they’re back out raising funds.

“Typically, the GP commitment has been one or two per cent. Not only do they often lack the capital to finance that in a larger fundraise, but in an increasingly competitive fundraising environment, LPs are

sometimes asking for more skin in the game – more alignment of interest. When given the option, GPs are electing to increase the size of their commitment to three to four per cent, based on the size and value of their own commitments. They are putting more skin in the game, and this results in much broader incentivisation throughout the team.”

Italy and Spain become hunting ground for direct lending deals

DIRECT lenders are eyeing opportunities in Southern Europe, amid increasing competition in the historically more popular Northern European markets.

Italy’s and Spain’s middle markets in particular are recording strong growth rates, according to industry experts.

While sponsor-backed deals are more common in Northern Europe, lenders need to navigate a world of individually-owned businesses in Southern Europe, which can bring its own challenges but also opportunities.

“With over 200,000 founder- or family-

owned businesses across Europe, this segment is less cyclical and far less competitive than the private equity-backed space,” said Josh Shipley, European head of PGIM’s private credit business.

While the UK, French and German markets have a stronger foothold,

sourcing the best deals in newer markets requires a thorough understanding of regional nuances, he explained.

Looking at the European market more broadly, M&A activity has picked up significantly, according to Sophia Alison, EMEA

direct lending portfolio manager at Macquarie Asset Management.

This is particularly visible in highquality companies that have EBITDA of €20m (£17.4m) to €50m, she said.

Still the investment selection process remains more critical than ever.

"The increased competition is driving convergence in pricing and terms across companies of varying quality, with the market now offering up to an extra turn of leverage to weaker companies and less pricing differentiation from stronger ones,” she added.

UK insurers’ uptake of CFOs will take time

UK SOLVENCY II reforms are unlikely to trigger an evolution in insurers’ investment approaches, experts have said.

In June 2024, the Prudential Regulation Authority (PRA) implemented a new matching adjustment mechanism (under UK Solvency II), which reduces insurers’ capital requirements for investing in longer-term, illiquid assets as long as they can demonstrate “highly predictable” cashflows.

Some industry onlookers expected that this would trigger increased investment in structured assets such as collateralised fund obligations (CFOs) – a type of securitisation that is backed by alternative investments, such as private equity, hedge funds, and real estate funds – without facing disproportionate

capital penalties.

However, it appears that this has not materialised yet.

“We have not observed a notable increase in exposure to structured assets, such as CFOs,” said Rishi Sivakumar, a director in the insurance team at Fitch Ratings. He expects progress to be gradual as, so far, only a limited set of new asset types has been put forward.

Robert Cannon, partner in the capital markets group of law firm Cadwalader, agrees. He considers the changes introduced by the UK regulator as “more of an evolution than a revolution”, with material impacts only to become visible “over the next several years”.

There are some constraints that will prevent a speedy uptake of CFOs by insurers.

highly-rated tranches and, where necessary, to structure them to deliver highly predictable cash flows as is required under the new rules. Consequently, shorterdated, lower-rated, or cashflow-uncertain CFO tranches are unlikely to be favoured by insurers.

Cannon notes the reforms primarily benefit life insurers with long term liabilities as matching adjustment is much less relevant for non-life insurers, who typically have much shorter-term liabilities.

He also emphasises that it will take time for insurers to become familiar with determining the overall risk capital charge for such assets and weighing it against the increased yield of these assets.

While UK life insurers are exploring ways to use the additional flexibility under the new matching adjustment mechanism, “we do not anticipate firms materially changing their investment risk profiles,” said Fitch’s Sivakumar.

When UK insurers do consider CFOs, he expects them to focus on the most

To achieve higher predictable cash flows, CFOs are being redrawn to make them more attractive to UK insurers. According to Cannon, common features include extended maturities and fixed repayment schedules, longer reinvestment periods, stronger reserve funds and liquidity facilities, as well as the incorporation of stable asset buckets.

Despite the challenges, some asset managers offering CFO vehicles are already making inroads with insurers. Churchill Asset Management said its recent $750m (£579.4m) CFO, focused on a range of US and European private capital strategies, was particularly well-received by insurance investors.

“We believe the structure’s long duration strongly resonated with insurers and other investors focused on long duration investment grade rated debt, especially as they look to capture attractive yield enhancement,” the firm said.

Private credit looks to fund defence supply chain

DEFENCE spending in Europe has gained a lot of attention this year with private equity firms previously highlighting the growing opportunity to deploy capital. While private credit firms were a little more sceptical at first, the strategy is now gaining traction.

For example, Sienna Investment Managers announced in September that it had raised over €270m (£234m) in commitments for a dedicated strategy targeting small- and medium-sized enterprises (SMEs) and mid-caps in a first close. The fund is targeting up to €1bn by the end of 2026.

Philippe Roca, codirector of Sienna Hephaistos fund, said that a large part of the defence ecosystem is

made up of SMEs that provide parts to the larger corporations and need to increase their production capacity at short notice.

“They already increased their debt during Covid,” he said. “They are now asked to increase their production capacities. So they need further financing following the rearming of Europe and the increase in the backlogs of military equipment manufacturers.”

Sienna is looking across Europe for opportunities, although Roca says that they are seeing a lot of businesses in France in particular.

The fund is getting ready to approve its first investments in the next few weeks.

Although Roca said that there are some

interesting opportunities in drone manufacturers, he is also interested in the supply chain of the defence industry.

Tikehau Capital’s head of private debt Cecile Mayer-Levi, said that there is definitely increased activity in the space driven by private equity firms.

“It used to be a bit in the grey zone and it wasn’t very clear from the bylaws whether you could invest in defence businesses, but there have been changes at the regulator level to make sure that the bylaws of the funds and enviromental, social and governance rules don’t limit investment in this area,” she explained.

Although Tikehau has been investing in this area for some time, it has not launched a dedicated

debt fund like Sienna. Instead, it has decided to keep it as one of its active sectors from its existing pool of assets.

The group has previously lent to aerospace defence subcontractors, such as maintenance operators and economic intelligence providers.

“One of the key concerns of the diligence process is understanding the governmentled contracts,” Mayer-Levi said.

“They are privatelyheld companies but they are all subcontractors for governments, so you need to understand that when it comes to working capital requirements, they often depend on large orders with long payment timelines. They will have a long order book that seems active but there are systematically some deferred orders and that’s very sensitive in that environment.”

The current geopolitical turmoil has prompted many firms in this sector to ramp up their activity. As a result, Mayer-Levi has seen more companies come under stress because they did not have the full financing in place to increase their revenues and order books.

“It’s important to make sure those long-term contracts are secured and not cancelled,” she added.

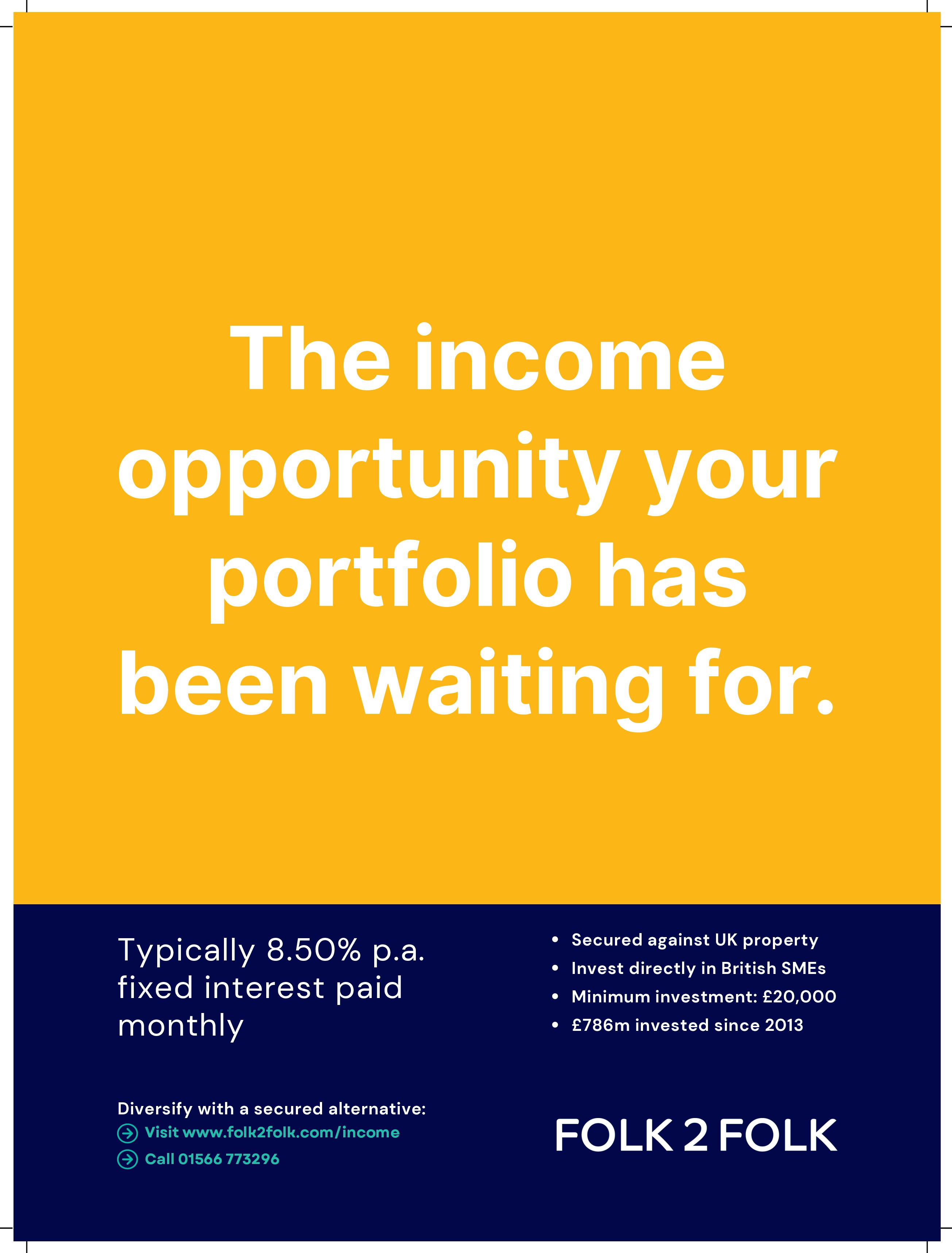

Private credit in practice

As institutional investors and asset managers accelerate their move into private credit and asset-based finance, the practical experience a lender brings in how these models operate in the real economy has never been more important

FOLK2FOLK, the UK’s largest peer-to-peer lender to business, has facilitated over £785m in loans to SMEs since 2013. Every loan is secured against land or property, giving investors tangible assetbacked exposure while providing businesses with an accessible alternative to traditional bank finance.

Kawai Chung, who recently joined as chief executive, believes the platform’s operational record offers a valuable perspective as private credit moves centre stage.

“The growing focus on private credit and asset-based finance is a natural progression of the market,” he says. “But it’s worth remembering there are lenders with many years of practical experience – consistently delivering asset-backed lending that links investors’ capital directly to productive businesses.”

Private credit’s expanding role

Private credit has become one of the most discussed areas in financial markets. Global managers are expanding into assetbased strategies that

seek returns supported by collateral rather than corporate cash flows. At the same time, capital and regulatory requirements continue to limit bank appetites, creating space for experienced non-bank lenders.

“Private credit now spans everything from large corporate direct lending to smaller assetbacked transactions,” notes Chung. “Folk2Folk operates at the practical end of that spectrum, where finance directly supports business activity in the real economy.”

A proven model Folk2Folk’s approach blends property-backed discipline with a humanled credit process. Its interest-only business loans start from £100,000, with terms of up to

five years and typical loan-to-value ratios of around 60 per cent.

Founded in Cornwall, it was established to support entrepreneurs and landowners outside the cities who found themselves underserved by mainstream lenders. Since then, it has expanded nationally, supporting businesses across sectors such as agriculture, leisure and tourism, property development, and manufacturing – industries that underpin regional economies across the UK.

“Asset-based lending can sound abstract,” says Chung. “But at its heart, it’s about understanding the borrower and the asset. For us, it’s grounded in tangible value, where there’s a transparent link between investor capital and productive

enterprise – from a farmer diversifying into agritourism, to a developer regenerating a local site. That’s the kind of lending Folk2Folk knows best.”

Folk2Folk’s lending record through periods of volatility, from Brexit to shifting interest rate cycles, has reinforced the durability of its approach.

“Markets move, but the fundamentals stay the same,” says Chung. “Strong security, sensible loan-tovalues, and transparency. Those are the constants of successful lending.”

As new entrants scale up in private credit, Chung believes the sector’s credibility will increasingly hinge on proven experience rather than ambition.

“Private credit is entering a new phase,” he says. “Its growth and credibility will depend as much on responsibility and experience as on capital. The lenders who’ve lived the realities of asset-backed finance day to day will have an essential role in shaping what comes next.”

This is commercial content, produced in partnership with Folk2Folk.

ALTERNATIVE CREDIT INVESTOR

COO SUMMIT 2026

7-8 May 2026, South Lodge, Sussex, UK

The Alternative Credit Investor COO Summit takes place on 7-8 May 2026 at South Lodge, a luxury hotel accessible from London. This is an exclusive, overnight event for senior operational executives from alternative credit fund managers, for valuable networking and insights in a relaxed environment, held under Chatham House rules.

The Summit will address all the most important topics affecting the sector, including the nuances of AI, the macroeconomic environment and rising liquidity demands. The event will take place from Thursday morning until Friday lunchtime.

If you are a COO/CFO who wishes to attend the event, please email editor-in-chief Suzie Neuwirth at suzie@alternativecreditinvestor.com.

For sponsorship enquiries, please email sales and marketing manager Tehmeena Khan at tehmeena@alternativecreditinvestor.com

ALTERNATIVE CREDIT INVESTOR

CONFERENCE 2026

20 October 2026, The Royal Horseguards Hotel, London

The Alternative Credit Investor Conference takes place on 20 October 2026 at the historic Royal Horseguards Hotel in Central London, bringing together investors, fund managers and service providers to exchange valuable insights, strengthen relationships and forge new connections over a day of panel discussions, speeches and networking sessions.

The conference will cover the full gamut of alternative credit, including direct lending, asset-based finance, real estate debt, infrastructure debt, fund finance, SRTs and CLOs.

Not just another conference

We are publishers as well as event organisers. We have built a community that has regular engagement with our magazine throughout the year. This enables us to attract a high calibre of delegates and speakers to the ACI Conference, including industry experts that are less familiar faces on the conference circuit.

The ACI Conference is backed by content. We will be distributing exclusive content during the conference and producing content from the event itself, extending its value beyond the day. This comprises both print and video footage, which will be distributed via the Alternative Credit Investor magazine and social media channels.

We will be hosting a variety of break-out sessions for COOs, LPs and insurers.

For attendance and sponsorship enquiries, please email sales and marketing manager Tehmeena Khan at tehmeena@alternativecreditinvestor.com

Rethinking default rates: Why time to resolution defines European credit opportunity

Zach Lewy, chief executive and chief investment officer at Arrow Global, explains why measuring defaults alone is insufficient and why resolution timelines hold the real key to unlocking value in European markets.

IN MY PREVIOUS ARTICLE, published in the October edition of Alternative Credit Investor, I discussed how structural shifts and local dynamics are reshaping private credit in Europe. I highlighted the importance of fragmentation, the limitations of relying on short-lived dislocations, and the opportunities presented by smaller local deals. I now turn to a subject where over-reliance can be misleading: default rates.

Default rates are frequently cited as leading indicators of distress. In Europe, they can be misleading. Unlike the United States, where legal processes are fast and standardised, Europe’s jurisdictions vary dramatically in how long it takes to work through troubled assets. Resolution timelines are often extended by procedural complexity, inconsistent enforcement, and regulatory variation.

In some US states, a distressed loan can be resolved in three months. In Europe, the process may take two years, five years, or even decades. At Arrow, we reviewed a bankruptcy claim in Italy that began in 1982 yet

still presented a live investment opportunity 40 years later. These are not exceptions. They are features of a system where resolution is slow, fragmented, and complex.

This reality has two major implications. First, the headline default rate only signals the start of a process. A default does not equate to an immediate investment opportunity. Second, it is the backlog of unresolved positions that matters most. These create a layered inventory of assets in transition that may be far removed from the initial point of stress.

Duration

awareness and the road ahead

We view this lag as an opportunity. Much like a half-life decay process, some dislocated assets resolve quickly, while others take years and require patient capital and specialist restructuring. The key is not to chase volatility but to identify assets that are fundamentally sound yet trapped in legacy structures, misaligned covenants, or outdated business plans.

Our model is built for this environment. With more than 4,500 professionals, regulatory

permissions across eight Western European countries, and over 35 million assets under management, Arrow is structured to operate in markets where friction is high, but value can be unlocked. In total, we manage €125bn (£108.3bn) of assets, giving us both the scale and the operational depth to act decisively when opportunities emerge. In many cases, we are already the incumbent servicer. Borrowers may be paying directly into our accounts, and asset-level data is integrated into our systems. This embedded position allows us to move quickly when opportunities emerge.

Duration awareness is critical. In jurisdictions where time to resolution is long, the ability to underwrite and manage assets across that timeline becomes a decisive differentiator. Investors who rely solely on reported defaults may miss the broader picture. The real opportunity is defined not by new defaults, but by the backlog of unresolved exposures. This distinction is critical for institutional allocators seeking to balance risk and reward. Technology will also play a part. Artificial intelligence

and blockchain may not yet be transformative, but they hold promise in improving capital velocity; that is the speed at which capital can be deployed, recycled and redeployed, across fragmented jurisdictions. For Europe to close the growth gap with the US and more dynamic markets, transaction speed must increase without undermining regulatory integrity. Better data transparency, standardised servicing, and enhanced underwriting tools could shorten resolution timelines and increase system-wide efficiency.

The contrast with the US is striking. In the US, securitisation and risk transfer enable higher velocity of capital. Europe,

by contrast, has prioritised resilience with higher capital ratios and stricter oversight. This has strengthened stability but constrained velocity. Achieving both safety and speed will be Europe’s next challenge.

Importantly, time to resolution is not just a legal consideration. It is a fundamental variable in investment outcomes. The longer an asset remains unresolved, the greater the operational costs and the heavier the drag on returns. Our integrated model minimises inefficiencies by controlling as much of the servicing, asset management, and restructuring process as possible. This creates stronger margins of safety and more

predictable results for investors. Looking ahead, resolution timelines will become an increasingly important factor in credit underwriting. Investors will need to assess not only creditworthiness and collateral value but also the practical realities of how long assets take to resolve. Those who can incorporate duration risk effectively into their models will have an edge in sourcing and executing transactions that others may avoid.

In addition, it is worth considering the societal and behavioural trends that shape these opportunities. Changes in remote working practices, the reduced relevance of certain office assets, and the increased appeal of Southern European hospitality are examples of how long-term behaviours can interact with resolution timelines. Investors who combine a clear understanding of macroeconomic shifts with the patience required to manage extended resolution timelines will be better placed to capture opportunities that are not immediately obvious but become valuable over time.

At Arrow, we believe that successful investing in this environment demands more than capital. It requires presence, insight, and operational execution. As the credit cycle evolves, we remain focused on identifying resilient assets, managing resolution timelines, and delivering strong risk-adjusted outcomes for our investors. Together with the themes introduced in my October article, this provides a framework for navigating the complexity of European private credit and real estate markets in the years ahead. This is commercial content produced by Arrow Global.

AI IS ALMOST unavoidable in 2025 with constant discussions around how this technology could radically change many elements of financial services. Private credit fund managers are already using and exploring AI, although adoption is in its early stages.

A common theme around AI is its ability to speed up tasks that people will have manually executed before. Some firms are now using the technology to complete previously arduous tasks, thus freeing up their employees’ time for other efforts.

For example, Man Group is actively integrating AI across its investment processes, particularly in private credit through Man US direct lending. There, AI is used in document processing and data extraction through proprietary automations to drive greater efficiency at these stages. As such Putri Pascualy, senior managing director and client portfolio manager for private credit at Man Group, says this has reduced the processing time per document from 15 minutes to just three.

“This significantly saves analyst time and reduces keying errors in daily workflows around credit ratings for private loan securities,” she explains. “Private credit is a very document-heavy business – every

Leveraging AI

AI is predicted to transform private credit, but there is still a long way to go. Jon Yarker explores the technology’s potential.

loan has lots of documents, and every time there's a change in terms, there are more documents. With AI, we can do data scraping which reduces the time we need to analyse all these documents significantly.”

Tech provider Oxane Partners, which works with many private credit firms, explains that AI is a “partner in performance”, acting as a

catalyst for better decision-making.

“We're leveraging AI to automate manual and onerous tasks with a well-defined scope, within clear guardrails and human-in-theloop checkpoints,” says Oxane’s managing director Kanav Kalia. This can include automating workflows around data validation checks, deliverable tracking,

data extraction from financial documents, reporting, and other manually intensive processes.

“The key is having a well-defined scope, breaking complex tasks into smaller chunks that AI can reliably handle, and building in verification points,” he adds. “AI [oversees] the repetitive execution, while teams validate the outputs and remain in charge of decision-making.”

Many private credit firms are at a point of adoption, reviewing already established processes and assessing where AI can be integrated to automate and enhance. Liquidity Capital is coming at this from a different perspective as a private credit firm built on a proprietary AI platform. Co-founder and chief science officer Oron Maymon explains that the firm’s AI and machine learning (ML) systems

screen markets and generate full investment reports after scoring and analysing these. Deals are then structured and stress-tested through hybrid ML engines, and monitored continuously through

analytics to act as a full decisionsupport engine that autonomously assesses borrower health through real-time data feeds, simulates macroeconomic scenarios and recommends portfolio adjustments before risks even surface. We’re very close to achieving this.”

Tomorrow’s AI applications

Private credit firms are clearly sold on the merits of AI and, in an industry that is becoming increasingly competitive, more are looking to this technology as a way of edging out their peers.

At Man Group, the firm is exploring opportunities to automate more of its pipeline through the creation of workflow tools around automation and the centralisation of deal data.

“There are significant opportunities in the mid-market space where AI can help us unlock opportunities by allowing firms to work through many more deals,” adds Pascualy. “The smaller the deal, the greater the volume of trades required to put money to work, so there's greater emphasis on processing trades efficiently.”

Meanwhile, John Channing,

“ With AI, we can do data scraping which reduces the time we need to analyse all these documents significantly.”

live data flows and intelligent alerts.

“We see AI transforming private credit from reactive analysis into proactive capital intelligence, where the entire lifecycle, from origination and structuring to monitoring and exit, is continuously optimised,” adds Maymon.

“Our goal is to push AI beyond

chief technology officer at Mount Street, a global loan services and technology provider, sees scope for further AI innovation through the use of model context protocol servers to help standardise large language models and help them connect with external tools, data sources and services.

“This will make up-to-date, business-specific data available in AI tools, rather than just the data in the training set,” says Channing. “We anticipate being able to ‘chat’ with our loan and collateral data and to be able to generate insights through querying, analysing and summarising data through a natural language interface.”

Liquidity Capital is pursuing a similar approach, where Maymon says the ambition is to build an “autonomous private credit” where AI underpins every stage of the process, from sourcing opportunities to managing loans.

“Ultimately, it’s about enhancing human judgement, freeing investment teams to concentrate on the most strategic and highimpact decisions,” he adds.

The pursuit of autonomy AI is playing an increasingly important role in supporting investment teams and questions about its ability to operate with autonomy are inevitable. Could this technology fully usurp the decisionmaking power of a human being?

Many in the industry are unconvinced about this and see the need for maintaining human input as crucial. Benjamin Lamping, chief executive at Reframe Capital, is not an expert in AI but sees several

use cases for it to make investment teams’ lives easier and predicts that it could eventually augment high-value tasks. However, he is pragmatic about its limits.

“Full autonomy is limited: final judgments on management quality, sponsor incentives, or niche risks at this time remain human-led,” says Lamping. “AI functions as an active collaborator,

facilitating analysts’ productivity and insights rather than fully replacing human decision-making.”

Others share this view, anticipating AI and humans to become closely interlinked within investment but with humans remaining involved. Man Group’s Pascualy sees the “future” of private credit hinging on the convergence of human expertise and cutting-

edge technologies like AI.

“Personal relationships and networks will always play a crucial role in deal origination,” she says. “Our part of the business is ‘AIproof’ in that sense – human judgment and relationshipbuilding remain irreplaceable.”

This sentiment is even shared by the providers of the technology itself. Henry Lindemann is cofounder and chief growth officer at Blueflame which provides AI solutions to alternatives sectors including private credit, and he admits there are limits to AI.

“AI is increasingly supporting higher-value investment activities in private credit, complementing rather than replacing human judgment,” says Lindemann. “While AI excels at identifying patterns and suggesting options, final decisions remain in human hands, preserving

the judgment, experience, and relationship management that have been pillars of successful private credit investing.”

credit processes as it develops greater capabilities and ultimately robustness in its decision making,” says Simon Heath, chief operating officer and corporate finance partner at Heligan Group. “It will become a substitute for talent, and this is starting to be experienced at more junior grades with a lower volume of graduate roles across the industry. AI will reduce the requirement for middle management also.”

As well as undermining some roles, AI will change how other functions are viewed. Liquidity’s Maymon sees this evolving to ironically champion two distinct skillsets: “First, those who can work effectively with AI, who think logically and precisely about what they’re asking for, will have an advantage over those who just know how to code.

“[And] second, people with strong interpersonal skills will thrive. As technology streamlines decision-making, human connection becomes even more valuable.”

“ With AI, we can do data scraping which reduces the time we need to analyse all these documents significantly.”

AI may not be set to replace humans completely, but it is starting to influence how private credit firms view talent.

Intensifying competition in private credit is forcing firms to pay out more to attract the best talent, but AI could change how some of these roles are prioritised.

“The landscape is rapidly evolving, and AI will be an increasing component of private

AI will continue to dominate many conversations, especially in an industry like private credit where there is a growing pressure to compete and stand out from the pack. AI is already being actively integrated in many firms’ investment processes, but instead of replacing the ultimate human decision-making function this is highlighting the need to keep this out of AI’s reach.

Bridge the Gap

Don’t accept disconnected data... in Fund and Corporate Services

We’ve fully integrated our market-leading private credit loan reporting and accounting systems to provide you with a single source of truth.

The results? Information on demand, data you can trust and real time decision-making. And with our dedicated team of private credit professionals by your side, you’ll have specialist expertise you can call on every step of the way.

To find out more visit aztec.group/private-credit

The right tech to scale with private credit’s growth

By Kevin Hogan and Todd Werner, Aztec Group

PRIVATE CREDIT IS scaling fast, projected to hit $2.6tn (£1.9tn) by 2029 according to JP Morgan. Fund managers still relying on siloed systems are in for a rude awakening. The future is integrated, automated, and investor-ready. The asset class’s rapid expansion, coupled with increasingly complex strategies to meet borrowers’ needs, means that firms must adapt, and fast. Fund managers can no longer rely on the fragmented data systems that were sufficient for a simpler, lower volume, and less sophisticated industry.

Private credit investors are also becoming more mainstream and include wealth management platforms, pension funds and insurance companies. These institutional LPs are more demanding, having historically been exposed to daily public market trading strategies. Regulatory bodies too are turning their attention to private credit, mandating transparency, and clarity as the asset class expands in size and scope.

To meet these needs, private credit is leaning into technology adoption to better manage:

1. Volume – larger funds mean more transactions and scaling one’s platform is essential to meet demands.

2. Automation – properly harnessed and embedded in daily processes to deliver a competitive edge.

3. Data – real-time data collection and analysis from a single point of truth is a differentiator.

4. Liquidity – robust investor servicing technology to support

evergreen and semiliquid fund structures, designed to attract capital from new sources, including retail investors.

5. Products – advanced waterfall functionality to support complex fund structures, such as rated note feeders, which are used to attract insurance capital seeking exposure to private credit returns with favourable riskbased capital treatment.

6. Transformation – orchestrated management of both internal and clientfacing change is imperative to identify required adjustments and implement them effectively.

As a market-leading administrator, Aztec is adopting industry relevant technology at pace. We are helping our clients to do the same.

A good example of how technology has overhauled the industry is machine reading capabilities. Now high volumes of unstructured data, such as agents notices and client invoices, can be processed to extract the core information, ready it for review, and deliver real-time reports to clients. More specifically for private credit, Aztec’s unique integrated loan and GL model, incorporating expert teams, best-in-class technology, and data management provides comprehensive and timely reports for managers to make investment decisions based on integrated data. Technology solutions like this one provide tailored solutions for

fund accounting, loan administration, and investor communications.

Coupled with a dynamic digital workspace like Aztec Connect and a seamless investor experience like Aztec Invest, which manages investor fundraising and onboarding, it enhances delivery and transparency. This uplifts the overall investor experience. Key to the ongoing adoption and implementation of industry-specific technology is understanding what fund managers need to manage their business more efficiently now, while evolving and scaling processes to take advantage of the rapidly developing opportunities private credit offers. Private credit’s inflexion point for technology adoption is most likely to succeed if delivered through partnerships where clients and providers ensure the systems and processes implemented meet the current needs and future wants of both parties. This disciplined approach to business transformation is best realised through expertly planned change management, which Aztec is adept at as we continue our own successful evolution as a transatlantic, market-leading private markets fund administrator for alternative investments. This is commercial content produced by Aztec Group.

ALTERNATIVE CREDIT AWARDS

14 April 2026, 583 Park Avenue

The Alternative Credit Awards North America, hosted by Alternative Credit Investor, recognise the most influential fund managers and service providers shaping the alternative credit space across the continent.

The Alternative Credit Awards North America are now open for entries until 28 November 2025. The winners will be unveiled on 14 April 2026 at the iconic 583 Park Avenue, NYC.

The Alternative Credit Awards have quickly become the must-attend event of the industry calendar, attract the cream of the sector for a night of celebrations and networking, creating valuable branding and business development opportunities. Access our awards website at aciawards2026northamerica.awardsplatform.com.

For sponsorship enquiries, please email sales and marketing manager Tehmeena Khan at tehmeena@alternativecreditinvestor.com

Central London, November 2026

The Alternative Credit Awards Europe, hosted by Alternative Credit Investor, recognise the most influential fund managers, specialist lenders and service providers shaping the alternative credit space across the continent.

The winners will be unveiled at a glittering ceremony in November 2026 at a prestigious venue in Central London.

The Alternative Credit Awards have quickly become the must-attend event of the industry calendar, attract the cream of the sector for a night of celebrations and networking, creating valuable branding and business development opportunities.

For sponsorship enquiries, please email sales and marketing manager Tehmeena Khan at tehmeena@alternativecreditinvestor.com

Invest from just £500

Helping newcomers navigate P2P lending

An increasing number of investors are flocking towards peer-to-peer lending but there still misconceptions that platforms need to dispel. By Lisa Holmes, head of investor relations, Kuflink

HEADING UP INVESTOR

relations at Kuflink, I speak to a wide range of people every day – some will be quite experienced with investing in general, while others are taking their first steps. Regardless, my team and I often come up against the same kinds of questions so I thought it’d be useful to lay out how I see newcomers navigating peer-to-peer lending (and crucially how we can help).

Getting to grips with the platforms

A lot of people will mostly learn about P2P through the platforms they engage with. It’s important not to just skim read the T&Cs and instead take time to really get familiar with the platform and how they have generated results in the past, as well as how they deal with defaults when they occur. I’d suggest reaching out to the P2P platform directly and asking them questions about how they operate. My team and I make ourselves available for these sorts of calls and it can really make a difference in helping people become familiar with P2P.

It's important investors do their own research, and platforms engage with them on this, as I often see the former turn to review websites. These will often reflect one person’s specific scenario –they’ll have had a bad experience with a platform and just want to vent online about it. Interesting

yes, but not representative of P2P and platforms as a whole!

Investors’ key concerns

My team and I get asked all sorts but the questions will often come down to the worst-case scenarios. What happens to their money if the platform were to wind down? People naturally want to plan ahead and learn about what protections their money could benefit from.

At Kuflink, this is when we spend time explaining all the processes behind the scenes – essentially covering the journey from an initial enquiry to a loan being completed. We explain how the loans are underwritten and detail the thorough checks made by the team throughout our due diligence process.

Battling misconceptions

It’s crucial to understand the process behind P2P, not just how a specific platform works but how this operates

as an investment. Unfortunately, many still compare P2P to savings accounts which are very different. People like to be able to withdraw what they want, whenever they want, from their savings account. P2P does not operate this way and investors need to have that understanding when they are engaging with this platforms. This even extends to defaults. A default is a loan that’s more than 180 days past its contractual payment date but even in that moment the platform can be working closely with parties to resolve the situation. It's a normal part of lending, and that's what people get confused about sometimes with P2P. I tell people not to look at defaults in a negative light necessarily. Instead focus on the recovery outcomes, timeframes and the communications you are being sent by the provider. This is commercial content, produced in partnership with Kuflink.

Where is the ‘Private Credit+’ technology infrastructure?

Private Credit+ is a $45tn total addressable market opportunity, but the systems currently supporting this market, retrofitted from private equity or capital markets, cobbled together through M&A, or scattered across disconnected point solutions, are fundamentally inadequate. The current landscape isn't just operationally inefficient; it's preventing firms from scaling. Kanav Kalia, managing director at Oxane Partners, makes the case for why the industry doesn’t just need tools, but needs purpose-built technology infrastructure.

PRIVATE CREDIT HAS expanded far beyond corporate direct lending into a much broader opportunity set, which we are calling Private Credit+. In our recent whitepaper, we outline that the total addressable market opportunity for all Private Credit+ strategies stands at a staggering $45tn (£33.6tn). We’ve all seen the sector rapidly expand and this now covers multiple asset classes such as asset-based finance, direct lending, commercial real estate finance, infrastructure finance, fund finance and securitised products – with each day, innovation in this competitive space is opening new opportunities for investors. We are now looking at unparalleled scale and complexity issues. Investment firms must now master new challenges around multi-asset strategies, crossexposure, aggregate risk and diverse reporting requirements. Legacy systems will struggle to keep up, meaning significant investment and overhauls are required in order to capitalise on this $45tn opportunity.

Why the current digital infrastructure is broken

Much of the Private Credit+ world

is currently operating on legacy platforms originally built for private equity or capital market strategies and then retrofitted for Private Credit+ through add-ons and workarounds. These platforms don’t cater to asset class nuances and provide limited flexibility and coverage for the breadth of Private Credit+ asset classes. They are temporary solutions at best. The M&A route hasn’t solved the problem either. With money flowing into the space, we’ve seen providers acquire and combine solutions that look good on paper. Big deals will always appear impressive and signal ambition, but these come with inherent integration challenges and often don’t provide full functionality for the depth and breadth of needs of Private Credit+ strategies.

Beyond these, other solutions have emerged. Point solutions have filled some gaps, offering specialised tools for specific workflows like valuations and monitoring, or focusing on individual asset classes. Unfortunately, they are limited in scope and private credit firms collecting these then risk having a cluttered tech stack. This can also end up creating silos and a lot of overhead for managing

different workflows. Some firms have pursued in-house technology solutions, building custom platforms tailored to their needs. This approach requires significant time, investment, and product development expertise that most firms simply don't have.

How this infrastructure gap plays out in daily operations

Let's trace how capital flows through Private Credit+. Investors – pension funds, insurers, sovereign wealth funds, high-net-worth individuals, individual investors in some cases – commit capital to private credit funds. GPs and investment firms then effectively become the capital providers and often leverage this capital with bank financing. They lend to borrowers across the spectrum: middle market companies, sponsors, originators and more. So, we have four key participants in the capital layer – investors providing equity, GPs orchestrating deployment, banks providing leverage, borrowers receiving capital. That's the easy part. Now overlay the operational layer that actually makes Private Credit+ function. Every loan requires multiple counterparties – agents, collateral administrators, servicers,

trustees – managing everything from borrower communication, waterfall calculations, payments, borrowing bases, compliance to reporting. Each asset class adds its own specialists: real estate needs valuers and property managers, infrastructure requires project monitors and technical advisors, asset-based finance involves specialists across areas from consumer loans to art financing. Each counterparty needs and provides specific information to function: borrower financials, market data, valuations, legal documentation and more. A single loan might involve 10 different parties exchanging data through dozens of channels. Multiply that across hundreds of loans, and you have thousands of information streams with no central infrastructure. The resulting information chaos is staggering.

Infrastructure purpose-built for Private Credit+ What Private Credit+ needs is a fundamental infrastructure transformation. While capital

wants to flow at highway speeds, it's constrained by manual processes, fragmented systems, and information chaos. The solution isn't about adding more tools, it's about building a digital expressway that can handle the speed and scale of Private Credit+.

A digital expressway would connect all participants – investors, GPs, lenders, borrowers, and operational counterparties – on unified digital rails. Instead of information crawling through email chains and Excel files, a digital expressway would enable seamless information flow. Instead of each firm struggling to build their own escape routes, the industry would benefit from shared, scalable infrastructure. This digital expressway must handle the sophistication of Private Credit+: the nuances of each asset class, complex deal structures, multi-currency facilities, and more. It would transform operational chaos into competitive advantage, turning information from a burden into a strategic asset.

At Oxane Partners, we’ve seen

firsthand what it takes to support Private Credit+ at scale. Managing over $800bn of Private Credit+ AUM for some of the top banks and private credit firms, we understand that incremental improvements won't suffice. The industry needs a fundamental leap forward. It requires building from first principles, which is why we created Oxane Panorama, the digital expressway that eliminates friction between parties and enables sophisticated strategies at scale. It’s not just software, but the infrastructure needed to simplify, digitalise, and transform how Private Credit+ is managed. We are bringing together data, workflows, and all stakeholders onto a unified platform that eliminates friction, enhances transparency, and enables smarter decisions. The market is ready. The infrastructure must follow. And we’re building it, for the scale and complexity that a $45tn opportunity demands. This is commercial content, produced in partnership with Oxane Partners.