SMART MONEY, STRONG BUSINESS: Navigating Your Finances in 2026

SMART MONEY, STRONG BUSINESS: Navigating Your Finances in 2026

Many aspects of life, from personal decisions to cultural values, are increasingly viewed through an economic lens. While it has been said that everything is political, there are many that would say most decisions we make whether in your personal life or in business is more closely connected to the financial implications of those very decisions. Money plays a central role in our daily life and of course in our businesses as well. Budgeting, saving, investing, considering an expansion, or a strategic purchase impacts short- and long-term business planning.

While political decisions are made through new laws or regulations, viewed as centered in politics, it all has financial consequences, some good, most bad in my opinion. We have recently witnessed how quantitative monetary policy, tariffs, environmental regulations, and other decisions impact the cost of goods and services we rely on every day. It seems it is more important today than ever before as inflation, uncertainty or future outlook in the market guides business leaders at the corporate level that ultimately reaches main street America as well. Financial logic has expanded into domains previously outside of finance, such as healthcare, education, environmental policies, and even personal life decisions.

This issue of In The Know features members that provide services in a variety of financial sectors. Topics covered include banking, investments, human resources, insurance, accounting, real estate and others that provide some insight in a variety of sectors all tied to finance in some way. As you continue to make more financial decisions in your personal and business lives, look to our member businesses to help make those decisions as you navigate a sea of information that continues to grow each day.

As always, thank you for being a part of our organization and thank all who have contributed to this publication. Your knowledge is invaluable and your support very much appreciated.

Wishing you a very happy and prosperous 2026.

Marc A. Baez Chief Executive Officer

• Process Piping

• Pipe Prefabrication

• Plumbing

• Heating/Ventilation/Air-Conditioning

• High Purity Orbital Welding

• Clean Room Pipe Prefabrication

• Institutional Lab Plumbing

• Data Center HVAC

• Design/Build Assist

• BIM/Virtual Design/3-D Drafting

• QA/QC

• Service/Repair/Maintenance

By Curt Schultzberg Vice President & Strategic Market Manager

We’re already a couple of months into the new year, and if you haven’t checked in on your business’s financial readiness for 2026 yet, chances are you’re not alone.

As business owners and top-level executives across the Sullivan County Catskills and the Hudson Valley approach the year with a healthy mix of optimism and caution, now is a good time to pause and reassess your financial readiness. We all want to grow, but it only happens with real planning. And that starts with a solid financial foundation—the thing that keeps your business steady for the long haul.

While every business is different—construction managers juggling multi-year projects, manufac-

turers adapting to new regulations and tariffs, family-run shops preparing the next generation to step in, small IT companies managing cybersecurity threats and compliance regulations—they all face the same fundamental questions: Are we ready for what’s next? How can AI help and what will it cost? Are there gaps that we’re not considering? Are we protecting what we’ve worked so hard to build? These and many other questions are universal and will help guide you toward a thoughtful, holistic readiness plan that can make all the difference.

Here are eight things to consider and understand where your business stands and what to focus on as you move ahead in 2026:

If you offer a retirement plan, re-examine what’s working and what’s not. Plans evolve, costs fluctuate, and employees’ needs change. A review may uncover ways to boost benefits or enhance participation. Consider these questions:

• Does your current plan still meet your workforce’s needs?

• Are administrative fees at market rates?

• Would a different type of plan reduce your costs or improve benefits?

If you don’t offer a plan, it may be more accessible than you think: from SIMPLE IRAs for small teams to 401(k)s with flexible match options, the right plan supports retention, competitiveness, and your own financial future.

2. Review Employee Benefits—and Set a Schedule for “Shopping” Them

Healthcare, disability, and other benefits often automatically renew, but is your company getting the best value? As costs keep going up, regular reviews can reveal new options and opportunities to refresh your benefits package:

• Health insurance coverage and costs

• Dental, vision, disability, and life insurance options

• Whether your renewal cycle gives you enough time to compare plans

3. Review Your Insurance Coverage

Your company may have grown, diversified, or taken on new risks. Your insurance coverage should evolve, too. Check with your agents to ensure that you’re protected and not overpaying for coverage you may not need:

• Fleet insurance for expanding vehicle use

• Insuring leadership positions with key person insurance

• General liability and professional liability coverage

• Property and cyber insurance

4. Enhance Cash Management Tools

Cash flow keeps your business running, especially while you sometimes wait on client payments. Modern cash management tools can make your financial life a whole lot easier and more predictable. Even small gains in efficiency can considerably affect liquidity. Look at:

• Accounts receivable and payable systems

• Automated payment solutions

• Lockbox services

• Sweep accounts for maximizing idle cash

• Fraud prevention tools, including Positive Pay

5. Review Outstanding Loans—and Future Borrowing Needs

Revisit current loan terms, interest rates, collateral, and payment schedules. With interest rates fluctuating, refinancing now might make sense. Meanwhile, thinking ahead may help you secure better terms and align borrowing with your long-term strategy. Consider whether you need:

• Equipment and/or IT infrastructure financing

• Property financing

• Expansion financing

• Seasonal cash flow financing

Whether you’re a sole proprietor, a partnership, an LLC, or a corporation, your business structure affects taxes, liability, and succession. As your company grows, your current setup may no longer fit. Consult your financial and legal advisors to see if a change could offer better protection, tax benefits, or flexibility.

Succession planning often gets delayed because it feels overwhelming, but having a clear plan protects your employees, your customers, and your family. Even a simple framework is better than no plan at all.

• Who steps in if something happens tomorrow?

• Who has authority?

• How are the clients reassured?

If you want your business to transition smoothly or remain in the family, this is an area worth exploring. Many business owners are surprised by how a trust can protect the company’s future. Placing a business in a trust can:

• Avoid probate

• Protect assets

• Maintain privacy

• Support long-term continuity

Financial readiness isn’t about predicting the future; it’s about controlling what you can, preparing for the unexpected, and making wise decisions that protect what you’ve built. With a thoughtful approach and proper guidance, 2026 can bring strength, stability, and new opportunities to your business.

Through Orange Wealth Management (OWM) clients enjoy a holistic and comprehensive suite of wealth management solutions, including Private Banking, Trust Services & Estate Planning, and Investment Services. Our team can help you turn this checklist into a clear, actionable plan tailored to your unique goals. OWM is a division of Orange Bank & Trust, a 130-year-old trusted financial partner dedicated to investing in its communities and reinforcing the economic foundation of the region.

At LeChase, our reputation for integrity, safety and quality has earned us the privilege of building projects – large and small – that continue to shape the future of Sullivan County. Whether a project is in healthcare, K-12, higher education, commercial, manufacturing, hospitality or housing, we are proud to support efforts that make the community an even better place to live, work and learn.

By Nariesha Mortel, Business Banking Senior Relationship Manager, KeyBank

Most small business owners are chief everything officers. Even when outsourcing or hiring to fill needs, their hands run deep in operations, finance, marketing, technology, and sales. Consequently, some meaningful relationships go underdeveloped—including the important relationship between the small business owner and their bank.

It’s not that small business owners don’t value their bank. Most do. Rather, for time-crunched owner-operators, the relationship is transactional. The bank is home to their accounts and the place to deposit and withdraw money. It’s where they turn to access capital and loans. For some, the bank is even a resource for managing cash flow. Yet for many, the bank—and by extension their banker—is not a trusted business advisor. It should be.

There are nearly 4,000 FDIC-insured banks in the U.S. Most offer a range of similar solutions. Even rates and terms tend not to vary dramatically.

So, what differentiates one bank from another? What makes a bank feel more than solely a checking or savings account?

The answer is simple: the relationship. It is a banker understanding the specific demands of a business and being able to provide advice and a tailored solution on a unique problem to achieve a specific outcome that will ultimately help the business run better.

This is especially true when it comes cash management. While small business owners are the wearer of many hats and carry many strong skillsets, deep financial expertise is often not among them.

Business bankers can offer advice and expertise around a host of financial challenges that small business owners may not have themselves— including cash flow management, the lifeline of every successful enterprise.

• Streamlined receivables unlock opportunities. When cash comes into the business on time and with consistency, owners can focus on growth instead of worrying about meeting payroll and inventory purchasing. Online mobile and payment acceptance, remote deposit capture, lockbox services, and automated accounts receivable (A/R) management are all helpful tools.

• Efficient payables keep operations running smoothly. Payables aren’t just bills to be paid, they’re a strategic tool for controlling cash flow and

strengthening business relationships. Automated accounts payable (A/P) platforms; commercial credit and virtual cards; ACH and wire payments; and integrated bill pay are all solutions that can help business owners stay organized and optimize on-hand cash.

• Effective cash flow management puts business owners in control. Understanding where money is— and where it’s going—is essential to strong financial management. Cash flow forecasting, real-time account alerts, working capital financing, and dedicated relationship support provide the tools and insights needed to make strategic decisions and take action.

Of course, determining what services and solutions are best for the business isn’t easy. That’s where focused conversation rooted in a strong relationship comes in.

Banks realize differentiation is about more than the products and solutions they offer. Differentiation is about changing the relationship from transactional to consultative.

KeyBank, for example, offers a Certified Cash Flow Advisor Program. The program empowers business owners to navigate their financial operations by providing them with a highly trained advisor who can work with them holistically across the business to help reduce friction, improve efficiency, and identify and act on opportunities for growth.

This advice-driven approach goes beyond traditional banking and offers strategic insights that help owner-operators make informed decisions towards their financial goals. It puts business owners first and product-driven solutions second.

This is as it should be. If business owners view their banks only through the lens of product catalogs to navigate and choose from, banking is just another ball to juggle and hat to wear.

Small business owners are accustomed to facing more challenges than their larger counterparts. Yet what makes them most vulnerable—size and scope— is also their strength. Typically free from red tape and stakeholder interests, they can be nimbler and adapt and innovate faster.

Here are some conversations small businesses should be having with their banks.

• Assessing the health of the business: What are some concerns? How are the payments and cash flow?

• Exploring ways to improve cash flow: Are business operations insulated from supply chain disruption? Can the business pivot to invest in technology to streamline operations?

• Addressing workforce challenges: Banks can offer a platform of benefits and specialized products to attract and retain employees.

Small businesses are the backbone of our economy. As challenges continue to grow, they are no doubt up to meeting them. Still, they deserve more. They deserve collaboration and a relationship that opens doors.

Jonathan Rouis, CPA, Partner

RBT CPAs

2025 was a pivotal year for U.S. tax law, with the One Big Beautiful Bill Act (OBBBA) enacting major changes across the federal tax code. Here are five key considerations businesses should take into account for 2026.

Businesses making new equipment purchases may benefit significantly from changes under the One Big Beautiful Bill Act. The OBBBA both restores 100% bonus depreciation and expands the Section 179 deduction limit, reducing taxes and freeing up capital for businesses that purchase qualifying property.

The Qualified Business Income (QBI) deduction, also known as the 199A deduction, allows eligible taxpayers to deduct up to 20% of their qualified business income. Previously scheduled to expire December 31, 2025, this deduction has been made permanent under the OBBBA. The OBBBA also expands the phase-in thresholds for the deduction and introduces a minimum deduction of $400. These changes benefit owners of pass-through businesses by providing increased certainty for tax planning and by expanding eligibility for the deduction.

Another result of the OBBBA is the restoration of immediate full expensing for domestic research and development costs. Previously required to be amortized over five years, U.S. R&D expenses can now be deducted in the year paid. All businesses that made domestic R&D expenditures between 2022 and 2024 may elect to accelerate the remaining deductions for those expenditures over one or two years. Small businesses averaging $31 million or less in annual gross receipts for the prior three tax periods may elect to apply the change retroactively to tax years beginning after December 31, 2021. Foreign R&D costs continue to require a 15-year amortization.

The OBBBA also introduces new deductions for employees earning qualified overtime pay and tips. These new laws impose additional reporting and compliance requirements on employers. Speak with your CPA to discuss these reporting requirements in more detail.

Owners of pass-through entities in New York should also speak with their CPA about the possibility of opting into the Pass-Through Entity Tax (PTET). The PTET can reduce taxable income by providing a workaround for the federal cap on state and local tax deductions, which has been temporarily increased (for 2025-2029) by the One Big Beautiful Bill Act to $40,000 for most taxpayers, subject to income limitations. PTET elections must be made by March 15.

Recent tax law changes have expanded opportunities for businesses to take advantage of deductions and other benefits, while also presenting new compliance requirements. To make the most of tax-saving opportunities this year and ensure compliance with new regulations, we recommend meeting with a certified public accountant to learn more and review your 2026 tax strategy in depth.

By Christopher Chazin, SVP, Head of Treasury & Trade Products & Services, TD Bank/Commercial Banking

Owners of small and medium size businesses often wear many hats or manage others who do. Sales and marketing, operations, finance, human resources, compliance, the list goes on. But, too often, one important responsibility may get scant attention: fraud prevention and cybersecurity.

In today’s world, a security breach is not a matter of if, but when. According to a recent study, 41% of small businesses suffered cyber-attacks in 2023, up from 38% in 2022 and nearly double the number of 2021 attacks.1 Not only are cyber threats and the resulting fraud increasing in frequency, but they are also becoming more sophisticated with artificial intelligence and automation behind them.

The consequences can be dire in terms of business disruptions, substantial costs, and sullied reputations. Consider these two examples from many thousands of cyber-attacks reported each year:

• A local retail store experienced a data breach where customer payment information was stolen. The store lost customer trust and sales. It had to compensate customers with identity theft protection and invest heavily in cybersecurity measures.

• A small accounting firm fell victim to a ransomware attack that encrypted all their client data. The attackers demanded a hefty ransom, which the firm was forced to pay due to the absence of data backup and recovery plans. The incident caused significant financial strain and damaged their reputation.1

Just as business owners set the tone and culture of their companies, they must do the same for cybersecurity, making vigilance part of their organization’s ethos. Of course, that does not suggest they should handle cybersecurity themselves. They certainly can and should hand off the technical details to a knowledgeable IT person, whether an employee or a consultant, so they can focus on more strategic concerns.

No matter what the approach, it is important for business owners to make cybersecurity a strategic priority. Moreover, they must establish sound security practices to help employees identify fraud attempts and protect vital data.

To help educate your employees, a TD Bank representative can come to your business and present a cybersecurity and fraud prevention curriculum we call TD SAFE - Security Awareness For Everyone. We designed the program to emphasize both the risks of cybersecurity and fraud as well as how to safeguard you and your business against them.

In addition to setting up employee training and awareness programs, business owners should take the following actions and schedule periodic reviews of policies, procedures, and governance to prevent cyber-attacks and financial fraud:

Update your technology safeguards. These include firewalls, anti-virus software, security patches, identity management, and other safe-computing measures. These protections should be audited and assessed at least once a year for vulnerability gaps, which should then be closed.

rigorous financial and banking controls. Consider performing online banking from a dedicated, standalone PC with limited access. Segregate duties so that no single employee is responsible for both recording and processing transactions. Limit who can authorize purchases based on their job role and

the size of their purchase authority. Also, ensure that different people oversee bookkeeping and bank reconciliations. TD Bank can set up Dual Control payment methods that require two or more users to release an ACH batch or wire transfer. This way, a compromised user cannot initiate a fraudulent transaction without another authorized user.

Conduct periodic audits. Engage a trusted, third-party accounting professional to review the company’s financial records at least once a year. Between audits, run unannounced random audits of these records, especially accounts payable for cash disbursements and payments to unknown vendors.

While TD Bank uses industry-best practices to safeguard your financial information and assets using the latest tools, encryption, and software, you can do a lot to enhance our effectiveness together. By combining our efforts, we can make it hard for cyber criminals to compromise your defenses against intrusions and fraud.

Note that TD Bank will never contact you to obtain personal information or user credentials via e-mail, text or voice call and will never ask you for remote access to your device.

If you are concerned about a fraudulent e-mail, text or call that may have resulted in disclosing confidential information, immediately report the incident by calling TD’s Fraud Resolution Group at 1-800-893-8554. For more information, stop by any TD Bank location or call 1-888-388-0408.

• Architecture

• Mechanical Engineering

• Electrical Engineering

• Plumbing Engineering

• Civil Engineering

• Land Use

• Environmental Services

• Surveying

• Construction Administration www.lanassociates.com

As a professional engineering firm engaged in municipal engineering services for over 35 years, Delaware Engineering D.P.C. has extensive experience in successfully assisting dozens of municipalities in securing hundreds of millions of dollars in low-cost borrowing and grant funds.

With our focus on municipal infrastructure, our in-house grants team is keenly aware of funding agency requirements and the vital role funding plays in helping communities realize infrastructure projects while minimizing impacts to serviced users.

Since 1990, American Electric LLC has been a trusted, family-run electrical contractor based in Lake Huntington, NY. Founded by Michael and Patti Popolillo, the company has grown to include their twin sons Michael and Brian, and a skilled team of 10–20 year-round electricians.

They continue to provide expert electrical solutions for residential, commercial and industrial projects.

Chianis + Anderson Architects, PLLC is an experienced, imaginative, and innovative team of architects and designers who are committed to providing the highest level of customer support for every engagement. Formed in 2001, Chianis + Anderson Architects is a full service Architectural and Interior Design firm. The firm’s leadership consists of Partners Greg A. Chianis, AIA, and Todd J. Anderson, AIA.

Engineering Properties (EP), founded in 2004 by Jay Samuelson, P.E. and Ross Winglovitz, P.E., is a full-service engineering and surveying firm serving the Hudson Valley and Catskills. EP provides site design, land surveying, planning and environmental permitting, construction support, project management, landscape design, and municipal engineering services for residential and commercial developments.

Based in the Hudson Valley and serving clients nationwide, 23 Marketing delivers results-driven solutions tailored to your marketing and communications needs. As a full-service agency, we bring together standout talent across the industry with a roster of expert strategists, data analysts, graphic designers, copywriters, social media specialists, web developers, and public relations professionals to provide cohesive, high-impact support from concept to execution.

With roots in the 1800s, the Inn at Lake Joseph is a historic lakeside bed and breakfast in the New York Catskills, two hours from New York City. Overlooking the lake, it offers 16 distinctive guest rooms, warm hospitality, recreational activities, and a thoughtfully prepared breakfast—continuing a long tradition of charm, history, and peaceful retreat under new owners Rom and Maria.

Yield Group is a full-scale real estate development firm specializing in industrial and townhome developments.

Thank you to these members who are celebrating milestone years with the Partnership! We appreciate your continued support.

AFLAC

Apple Ice

Atlas Security

Foster Supply Hospitality

Capacity Bookkeeping

ELEC 825

Fallsburg Lumber

Here’s Help Staffing

Hudson Valley Home Source

MDS HVAC

Keller Signs/Outdoor Media Corp.

Prestige Energy

Keller Williams

Servpro Team Johnson The Center for Discovery

Keystone Associates Architects, Engineers and Surveyors, LLC

Billig Loughlin and Silver, LLP

By Eric Egeland, CPCU, AU President Capacity Bookkeeping

In today’s competitive and rapidly shifting business environment, financial clarity is no longer optional, it is essential. Yet many small and mid-sized companies do not need, or cannot justify, a full-time Chief Financial Officer. This is where a Fractional CFO provides tremendous value. A Fractional CFO delivers high-level financial strategy, oversight, and discipline on a part-time basis, giving organizations access to executive expertise exactly when and how they need it.

Working with a Fractional CFO is a structured, collaborative process that blends financial analysis with strategic decision-making. While every engagement is customized, the experience generally follows several key phases designed to strengthen the financial health and long-term resilience of the business.

The engagement begins with a deep dive into the company’s operations, culture, and financial history. This immersion phase is essential for building context and establishing a foundation for strong financial decision-making.

A Fractional CFO will meet with the owner or CEO and other key team members to gain insight into how the business operates day to day. Beyond numbers, this includes understanding the organization’s rhythms, internal

processes, challenges, and opportunities. Historical financial data is thoroughly reviewed to identify trends, anomalies, and turning points in the company’s financial journey. This early analysis often reveals important patterns—such as seasonality, margin erosion, or shifts in customer behavior—that may not have been previously recognized.

This phase not only builds clarity but also develops trust, setting the stage for transparent and effective collaboration.

Once the foundational understanding is established, the Fractional CFO conducts a detailed analysis of the company’s financials, systems, and performance drivers. This involves identifying areas where improvements can be made quickly— commonly referred to as “low-hanging fruit.”

Examples include unnecessary expenses, inefficient processes, or rising costs that have gone unnoticed. The CFO also evaluates broader trends such as exponential expense growth or revenue patterns when seasonality is a factor. Each insight is quantified to show its financial impact, giving leadership a clear picture of opportunities for improvement and potential risks that need to be addressed.

This analysis serves as the springboard for strategic goal setting.

Based on immersion and analysis, the Fractional CFO works with leadership to establish a clear set of objectives and goals. These are designed to stabilize the business where needed, unlock growth opportunities, and address emerging threats.

Potential objectives range widely depending on the business’s needs. They may include improving cash flow, restructuring compensation or bonus programs, adjusting headcount strategies, or evaluating alternatives to rising lease expenses. In some cases, goals may focus on diversification to reduce vulnerability from concentrated revenue streams. In others, the priority may be implementing systems or processes that provide better visibility and control.

Objectives are always tied to measurable outcomes, ensuring that both the CFO and the leadership team remain aligned.

While some goals can be executed quickly, others require a mid- or long-term plan. During the planning phase, the Fractional CFO develops structured roadmaps to help the business reach its targets methodically.

These plans may include initiatives such as purchasing real estate, expanding high-potential

profit centers, improving profit margins, launching complementary lines of business, or strengthening operations to weather economic fluctuations. The CFO also evaluates the feasibility of various scenarios, ensuring leadership fully understands each plan’s risks, benefits, timelines, and capital needs.

This phase transforms ideas into actionable, realistic strategies.

A critical element of working with a Fractional CFO is ongoing financial monitoring. The healthiest organizations practice disciplined budgeting and trend analysis—and a Fractional CFO ensures this structure is put in place.

An annual budget is developed that serves as a baseline for accountability. Each month, actual financial results

are compared against budgeted expectations, and trends are evaluated to spot shifts before they become problems. This proactive approach enables leadership to adjust quickly to cash flow challenges, cost surges, or changes in demand. It also ensures steady progress toward long-term goals.

This continuous oversight safeguards the business’s financial health and reinforces operational discipline.

6. Special Projects: Leveraging Expertise when it Matters Most

Beyond routine financial management, a Fractional CFO often leads or supports high-impact projects that require specialized expertise. These may include process improvement initiatives, updates to standard operating procedures, system implementations or integrations, audit preparation, or support solving complex production or operational challenges. This flexibility allows businesses to tap into high-level

financial leadership whenever strategic opportunities or obstacles arise.

In essence, working with a Fractional CFO brings clarity, structure, and strategic focus to a business’s financial landscape. By blending deep analysis, long-term planning, and disciplined oversight, a Fractional CFO becomes a trusted partner—helping the organization grow sustainably, operate more efficiently, and prepare confidently for the future.

Eric Egeland, the CEO of Capacity Bookkeeping, has been providing Fractional CFO services for two decades. Clients include for profit, non-profit, and startups. For more information or a consultation call 845-430-1347 or e-mail eric@capacitybookkeeping.com

In a perfect world, nothing would ever go wrong. Cars wouldn’t crash, homes wouldn’t suffer damage, and businesses wouldn’t face unexpected setbacks. But the real world is unpredictable… and that’s exactly why insurance exists.

Insurance is a financial safety net designed to protect you from losses that could be devastating without proper coverage. A well-built policy doesn’t just meet requirements—it helps ensure your business can survive and thrive even when the unexpected happens.

By Jason Hoffman, President & Owner, J. Hoffman Insurance

Many business owners see insurance as just another expense. But unlike most bills, premiums are an investment in stability. What you pay in coverage is typically only a fraction of what a loss could cost.

• A house fire can cause tens or hundreds of thousands of dollars in damage.

• A car accident can lead to repair costs, medical bills, and liability claims.

• A business interruption or lawsuit can drain resources quickly and even threaten the survival of a business.

Insurance provides certainty in an uncertain world. It’s not about spending more—it’s about making sure you’re protected when it counts.

Insurance isn’t just about reacting to events; it’s part of a long-term financial strategy. With the right coverage, you gain:

• Financial predictability: Know what your protection costs.

• Risk management: Avoid losses that could derail savings or future goals.

• Stability: Recover faster when setbacks occur.

Under-insuring—or assuming old policies still cover today’s risks—can be just as dangerous as having no coverage at all. Common gaps include outdated property valuations, missing business income protection, low liability limits, or no cyber coverage.

The real value of insurance isn’t the policy itself—it’s the confidence it provides. Proper coverage allows you to focus on running your business, caring for your family, or growing your investments without constant worry about “what if.”

If you’re unsure whether your current policies fully protect you, the best next step is a simple, no-obligation risk assessment. It’s a straightforward review that identifies coverage gaps, outdated valuations, and other blind spots—without sales pressure or confusing jargon.

Most business owners say, “I wish someone explained it this way years ago.” One conversation could make the difference between recovering from a challenge and facing a loss you never could.

To schedule your complimentary risk assessment, contact Jason Hoffman at 845-239-4787 or email Jason@jhoffmaninsurance.com.

By John Leigh, CFP® Financial Advisor

If you own a business, you’ve probably spent countless hours thinking about how to grow it, manage daily operations and serve your customers. But have you thought about how you’ll eventually step away from it? While it might seem premature, planning your successful exit from your business is one of the smartest moves you can make as an owner.

The reality is that most business owners have 80% to 90% of their net worth tied up in their companies, according to the Exit Planning Institute. That’s a significant investment that deserves careful planning to protect. Unfortunately, 70% to 80% of businesses put on the market don’t sell, and about half of all business exits are involuntary due to unexpected circumstances like health issues, family emergencies management disputes or economic downturns.

Exit planning is more than preparing for retirement. It’s taking control of your future and ensuring you can transition away from your business when and how you choose. You can start with the end in mind – a proactive approach that can inform your current business decisions and help increase your company’s value and marketability.

Begin by articulating your personal goals for both the transaction and your life afterward. Maybe you want to sell only a portion of your business, stay on as a paid consultant or use the proceeds to start your next venture. Understanding your vision helps shape everything else.

You’ll want to calculate how much money you’ll need to fund your desired retirement lifestyle, accounting for expenses that may be currently covered by the business, like your cellphone, vehicles, travel and health care. Don’t forget about your legacy goals too – what you want to leave for your family or charitable causes.

Getting started requires building a strong professional team. At the center, there should be a financial advisor who can help you through the

planning, execution and post-sale phases. You’ll likely also need a tax professional, legal advisor, commercial banker and business valuation expert. Depending on your exit strategy, you might later add specialists like business brokers, investment bankers or employee stock ownership plan advisors.

Understanding your business’s current value is crucial. It’s a good idea to get a calculation of value at least three to five years before your planned exit. This isn’t as formal or expensive as a qualified appraisal, but it gives you a realistic range of what your business might be worth.

This step may reveal a gap between what you need financially and what your business could sell for. If so, don’t panic. You have several options: work longer, adjust your spending expectations, save more outside the business or focus on increasing your

company’s value. You can boost value by increasing profits through higher market share, new products, better pricing or reduced costs. You can also improve intangible assets like employee expertise, operational systems and customer relationships.

Finally, consider who your successor might be. Selling your interest to family members, business partners or employees often provide more control over timing and lower transaction costs, though they may result in lower sale prices. Selling the business to third parties typically brings higher proceeds but less control over the process.

The key message is simple: it’s never too early to start planning your exit. Whether you’re thinking about stepping away next year or in the next decade, taking proactive steps now puts you in control of your business’s future and your own financial security.

Sullivan County Shines at Our 31st Annual Meeting & Awards Dinner!

Awards were presented to:

Mike Taylor — CEO/Combined Energy Services,

Holiday Mountain Ski Area

Walter A. Rhulen Award

Kevin McLaren — Commercial Banking Market President/

Hudson Valley Credit Union

Distinguished Service Award

Gerald Skoda — Skoda Enterprises

Lifetime Achievement Award

In December, we celebrated the holidays with 90 of our closest friends and members at Solaia Restaurant in Monticello. 11 perfect attendance medals were awarded along with the grand prize of a whiskey flight generously donated by Pollinator Spirits.

According to the Federal Trade Commission (FTC), the number of consumer fraud reports has remained steady the past few years, hovering around 2024’s total of 2.63 million. The percentage of those reports that have included monetary losses, however, has jumped–rising from 27% in 2023 to 38% in 2024.

With that 38% representing $12.8 billion in total fraud losses, it’s clear that fraud’s impact on consumers can be significant. Not surprising, artificial intelligence (AI) has upped the ante, providing new tools for bad actors and making it critical for consumers and financial institutions like Mid-Hudson Valley Federal Credit Union (MHV) to stay vigilant in safeguarding information.

By Charlie Broe VP Asset Protection Mid-Hudson Valley Federal Credit Union

Here’s what to know about AI and its impact on fraud. Spoiler alert: there’s both good and bad news.

AI is a form of technology that allows computers to problem solve, much like humans. It’s particularly good at recognizing patterns from massive amounts of data and making split-second decisions based upon its’ analysis.

The technological concept dates to 1950, when Alan Turing, the British mathematician and computer scientist (and subject of the 2014 film The Imitation Game), proposed the “Turing test,” which gauged a machine’s ability to demonstrate “human level” intelligence.

As AI has developed and advanced, bad actors have increasingly misappropriated the technology to scam consumers. For instance, the majority of phishing emails sent between September 2024, and February 2025 exhibited some use of AI, according to a March 2025 “Phishing Threat Trends Report” from security software provider KnowBe4.

Data from America’s Credit Unions, a trade association dedicated to advancing the industry and members’ interests, identifies phishing, along with two other modalities, as the three most prevalent AI-assisted scams as of mid-2025. Voice clone calls from “family” members in emergencies and fake QR codes and digital wallet requests joined AI-crafted phishing messages on the group’s list.

AI-enabled threats are developing rapidly due to the technology’s ability to mass produce, automate, and create realistic and convincing fraud communications that may seem too well-targeted to each individual consumer to be anything but the real deal.

Mass production and automation are central in this. Bots can deliver messages to every iteration of a phone number–almost like a thief trying to crack the code on a safe. It only takes a few consumers with personal details matching the content of the scam to fall for it to net a huge payday for the scammers.

Because AI-enabled scams are often designed to elicit and leverage your emotions—whether it be panic, love, anger, or something else—MHV’s advice mirrors that of many experts in this field.

Pause to consider the message you’ve received, any emotions that it has brought up and exactly what it’s asking you to do. Are you feeling pressure

to take some form of immediate action? Was the message unexpected?

Disregard phone numbers and hyperlinks in the message. Instead, use a trusted phone number for your financial institution, from a statement or bank card, and reach out directly to verify any claims in the message that you’ve received.

And know that MHV, and the credit union industry more broadly, are fighting to not only maintain, but to enhance, the safety and security of your accounts. As alluded to earlier, AI has made tools possible that fight fraud. As an example, a signature on a check can be compared to thousands of previous versions, thereby helping any anomalies be flagged.

Every day, financial institutions are creating more of these tools, with consumer safety and security in mind. The main oversight entity for credit unions is the National Credit Union Administration, which is an independent federal agency that “insures deposits at federally insured credit unions, protects the members who own credit unions, and charters and regulates federal credit unions.” The agency also developed an

Artificial Intelligence Compliance Plan to, among other things, foster public trust in the federal use of AI.

Additional safeguards exist for consumers, including parts of the Uniform Commercial Code–a set of state laws–that dictates that consumers be made whole as a result of fraudulent transactions that they didn’t initiate.

With updated statistics on fraud as released by the FTC, our hope is that our clients, along with all Americans, see AI as a tool with the power to simplify aspects of life rather than an instrument of destruction and havoc. By pausing and verifying emotionally charged messages and trusting the innovators leveraging AI for good within the credit union industry, there is no need to panic over specific messages or AI’s emergence.

By Cathy Parlapiano, President — Here’s Help Staffing & Recruiting

The talent gap is not just a workforce problem; it’s a financial one. Every unfilled seat cost business money, and every hiring misstep costs even more.

That’s why more companies across Sullivan County and the Hudson Valley are leaning on staffing and recruiting firms to protect their bottom line while securing qualified talent.

Where staffing & recruiting firms eliminate unnecessary spending

Whether you need contract support or a critical full-time hire, a professional recruiting partner absorbs the most expensive and time-consuming parts of hiring.

STOP paying for:

• Advertising and job posting fees.

• Sorting through unqualified applicants.

• Phone screens, skills assessments, and reference checks.

• Payroll taxes, unemployment, workers’ comp, PTO (for contract roles).

• Replacement costs when a new hire does not work out — many firms provide guarantees.

START paying for:

• The right candidate — not the search

• Proven experience, credentials, and culture fit

• Results and productivity instead of a high-risk hiring process

Why direct hire recruiting is financially smarter than it seems.

Some companies hesitate to use recruiters for direct hire roles because of the fee — but the numbers tell a different story:

• A vacancy costs far more than a recruiting fee.

• A bad hire can cost up to 2x the salary.

• High-quality recruiting reduces turnover and increases retention.

• Leaders keep their attention on strategy, revenue, and customers — not resumes.

A contract & direct hire recruiting partner turns talent acquisition from a cost burden into a strategic investment that protects cash flow, limits risk and keeps businesses growing with confidence.

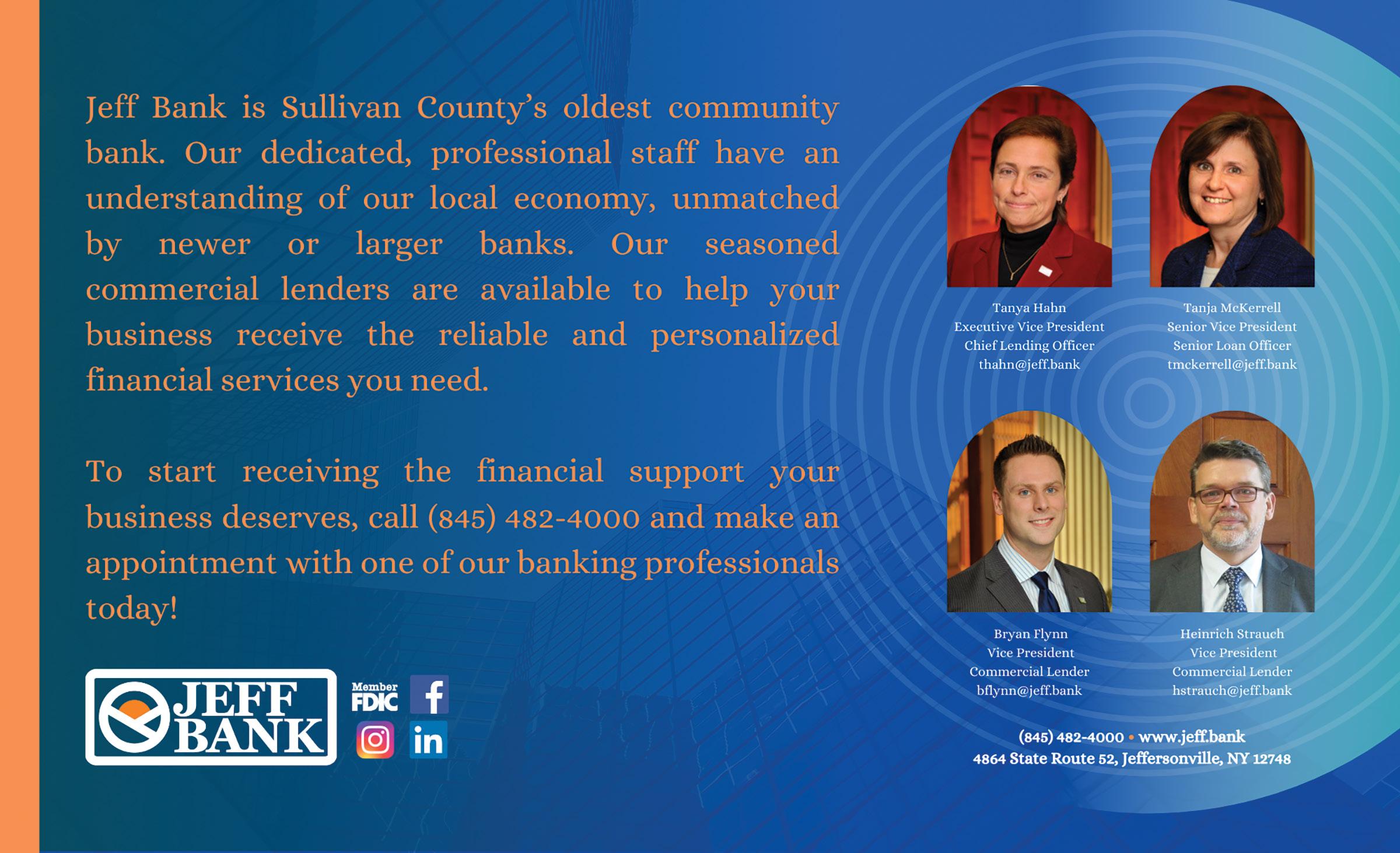

By Bryan Flynn & Heinrich Strauch, Jeff Bank

That quote in the headline comes from Alexander Graham Bell, and he probably knew a thing or two about the process of securing funding as he started the Bell Telephone Company and AT&T. Here are some tips for business owners when applying for commercial financing from a bank. Some questions that a lender is likely to ask you.

What is the purpose of the loan, and how will the funds be used?

That’s usually how the conversation starts. We want to understand what you’re borrowing the money for and how it will benefit your business. The more specific, the better. A lender will also want to make sure that the right product is used (e.g. long-term loans for long-term investments, loans that do not exceed the life expectancy of financed equipment, etc.)

SOME EXAMPLES:

Real Estate Acquisitions: you plan to buy and/or renovate a property for your business operation, or to generate rental income.

Equipment Purchase: you want to replace and upgrade the machinery, vehicles, or technology used for production or service delivery.

Working Capital: your business has short-term cash flow needs to cover seasonal slowdowns, inventory build-up, or payroll.

Business Expansion/Acquisition: you plan to open a new location or even acquire another company.

How will the loan be repaid?

This is a core question for lenders — we need to believe that your business has a reliable and predictable cash flow to cover the loan payments. In most cases that will be the business’ operating income, or rental income generated from the newly purchased property. As a “Plan B”, a lender will also look for secondary repayment sources, such as the income of personal or corporate guarantors.

Lenders will use financial analysis of both past performance (three years of tax returns, year-to-date internal numbers) and projections for 12-24 months to determine if and how the requested loan fits into your financial picture.

How is the loan going to be secured?

This question is really about risk management for a lender and part of being prepared for the situation when a borrower cannot meet the loan obligations any longer and other sources of loan repayment must be considered. This can be real estate, equipment or vehicles, inventory or account receivables, or even liquid investments. The conversation about collateral also involves loan-to-value considerations as banks limit their lending to certain percentages of collateral value to anticipate discounts if a collateral needs to be liquidated.

What type of business do you operate, and who are the owners and principals?

This is about legal responsibility (e.g. who is the bank contracting with for the loan) as well as control (who makes decisions) and experience & skills (who are the key people in the business). A lender will want to see the organizational documents and understand who owns and controls a business (including potential silent partners), as well as gain insight into the qualifications of key personnel.

Which financial documents should you have ready for a loan application?

This depends on the loan amount as well as the type of business - larger loans will require more extensive financials, and start-up businesses usually don’t have several years of financial history available. For most applications, the most recent three years of tax returns and interim financials (year-to-date) will be needed, and personal tax returns and personal financial statements for personal guarantors. A lender will also want to see a debt schedule for existing loans to learn about what’s outstanding and how those loans are being serviced.

For start-ups, a business plan with financial projections will be needed to outline your vision for the business, including numbers that should demonstrate its economic viability.

Yes, it does - not in the sense of a number by itself but as an insight into your credit history. How have you dealt with loan obligations in the past, were there any issues in the past and what were the reasons for those? Nobody’s perfect but lenders do look for responsibility in how you manage your financial obligations.

A lender will try to learn as much about you and your business as they can - what’s your motivation and experience? How do you see your business operating in its market and region? What are your thoughts about competition? What were past challenges and how is your outlook? Do you have contingency plans if conditions change? This is about making a lender comfortable with yourself as the borrower, to believe that what you set out to achieve has a sound basis in reality.

Ultimately, a bank’s decision to approve a loan application (and lend you their depositors’ money) is a vote of confidence in you and your business. Being prepared by having documents together and being able to make your case is the first step in what every lender hopes to become a long-term relationship and profitable partnership.

When you’re starting up, there are plenty of apps, programs, and consultants available that can help with putting together business plans. But it is important that you remain in charge of that process and that the final product is something you believe you will achieve. The Small Business Administration (www.sba.gov) is usually a good start for free resources.

By Filiberto Nieves, Vice President, Commercial Loan Officer, Walden Savings Bank

Choosing where your business operates is one of the most strategic decisions you will make. The right space can improve customer access, enhance operational efficiency, elevate your brand, and create financial value. The wrong space can limit growth or increase costs. At Walden Savings Bank, we work with business owners every day as they evaluate this choice. Whether they are leasing their first storefront, purchasing a property, or financing new construction. Here are key considerations to help guide your planning.

Leasing commercial space is often the easiest path for startups, entrepreneurs, and businesses in transition. Rent typically requires less upfront capital than purchasing or building, allowing owners

to direct cash toward hiring, technology, marketing, or expansion.

Renting makes sense when:

• Your space needs may change over time

• You are testing a new market or location

• You want flexibility to expand or relocate

However, leasing also comes with limitations. You build no equity in the property, rent can increase at renewal, and space modifications may require landlord approval. Depending on your lease, you may also be responsible for taxes, utilities, or maintenance. For businesses planning to maintain a presence for 10 years or more, renting can cost more over time without offering long-term financial return

Purchasing a commercial property can be a strong strategic move for businesses operating in stable or growing markets. Ownership provides predictability and allows you to build equity as the property appreciates.

Buying can benefit businesses that:

• Want to stabilize occupancy costs

• Plan to stay in the same location long term

• Prioritize building financial assets

Ownership offers full control of the space, so you can upgrade, reconfigure, or expand without waiting for approvals. Real estate can also strengthen your balance sheet and become a tool for future borrowing or retirement planning.

At the same time, purchasing is a long-term commitment. You’ll need to plan for closing costs, maintenance needs, and capital improvements. Our Commercial Lending team at Walden Savings Bank regularly helps businesses compare leasing versus buying to determine when ownership makes the most sense financially and operationally.

Constructing a new space offers the highest level of customization. For specialized industries such as medical, manufacturing, food service, or technology, building a facility ensures the layout and systems are designed around how your business operates.

Businesses choose to build when they:

• Require unique workflow or infrastructure

• Need room for future expansion

• Want a facility that reflects their brand and customer experience

A new build allows you to incorporate energy efficiency, modern design, and scalable systems. However, projects typically take 12–24 months and require financial capacity, patience, and strong planning. That’s where

having an experienced local banking partner matters, one who understands regional permitting, contractor cycles, and construction financing structures.

There is no one-size-fits-all answer. The best option depends on your current needs, long-term strategy, cash flow, and local market dynamics.

A general guide:

• Rent if you want flexibility or are exploring a market.

• Buy if you have stable operations and want to build equity.

• Build if you need customization and are planning for sustained growth.

Business owners should also evaluate financing options, tax considerations, real estate availability, and their 5to 10-year strategy. Consulting with a banker, CPA, and real estate professional can provide valuable insight into how each choice impacts finances and growth.

For more than 150 years, Walden Savings Bank has supported local businesses through every phase of growth, from first locations to expansion facilities, multi-property portfolios, and ground-up construction. Our Commercial Lending team takes a consultative approach, helping owners weigh costs, compare financing scenarios, and structure loans that align with their goals.

Whether you’re renting, buying, or building, your real estate decision is ultimately a growth decision. With the right strategy, your space can support your vision, strengthen your financial position, and help your business thrive in the communities we proudly serve. To discuss financing options or get guidance on your next move, connect with our Commercial Lending team today!

You know what keeps us up at night? Cash flow. When is money actually coming in? When is it going out? And will there be enough left over to finally invest in growth?

Markets don’t wait for us to catch up. Costs fluctuate, customers pay whenever they feel like it, and traditional financial planning tools weren’t built for this kind of constant change. We used to think that’s just how business worked: you dealt with uncertainty, made your best guess, and hoped for the best.

But here’s what we’re learning: AI-powered budgeting is making a real difference for SMBs. We’re talking about automating forecasts, using current data, and spotting trends before they hit. At Meeting Tree Computer, we’re watching this technology give business owners accurate, timely insights that genuinely reduce uncertainty and help them make decisions faster and with more confidence.

Most of us are still budgeting the old way: spreadsheets, assumptions based on last year’s numbers, and one annual update if we’re lucky. By the time we finish entering everything, those numbers are already obsolete.

By Monique Duci Meeting Tree Computer

Here’s where AI budgeting changes everything. Instead of stale data, AI automatically pulls current information from your accounting software and sales systems. Your forecasts stay current because they adjust as the numbers you enter change. You start spotting financial risks or opportunities early enough to take action. It’s proactive rather than reactive, allowing you to plan smarter and avoid surprises.

Now, this isn’t about replacing your financial expertise or gut instinct. That instinct matters. What AI does is give you insights to back up those instincts and make decisions more quickly.

Cash flow forecasting is where AI really shines. AI eliminates anxiety by constantly monitoring revenue patterns: peak seasons versus slower periods. It tracks recurring expenses, notices when costs creep up, and watches customer payment patterns so you can see who’s consistently late. It reminds you of subscription renewals, vendor invoices, all of it.

But what we really love is scenario testing. You can ask AI questions like: “What happens if I give everyone a 6% raise?” “Can we afford new equipment if Q2 sales soften?” “How many months of runway do we have if our biggest client delays payment by 60 days?” Having clear visibility into future cash conditions means you can act early, time investments more effectively, build reserves when needed, and support steady growth rather than lurching from crisis to crisis.

AI tools also analyze industry shifts, customer buying behavior, labor and supply chain issues, competitive pricing, and demand patterns. These are all the external factors that impact us, but that we don’t always have time to track. This intelligence lets SMBs respond faster to market changes and stay ahead of the curve.

Now here’s something critical: security. When you’re feeding sensitive financial data into any AI platform, you’re creating potential vulnerabilities. We’ve seen businesses rush into free AI tools without thinking through the implications, and that’s a mistake. Free platforms often lack robust data protection, and some use your data to train their models, meaning your financial information could end up anywhere.

That’s why we always recommend paid, enterprise-grade platforms over free alternatives. Yes, they cost more, but they come with proper encryption, compliance certifications, and contractual data protection guarantees. When evaluating tools, check for SOC 2 compliance, GDPR readiness, and clear data ownership policies. Ask: Where is your data stored? Who has access? How is it encrypted? Can the vendor use your data for other purposes?

continued...

Just as important as choosing the right platform is training your team. Employees need to understand what constitutes private information and why it matters. One careless copy-and-paste of customer data or financial records into the wrong tool can create serious liability.

This is why implementing clear acceptable-use policies is essential. These policies should specify which platforms are approved, what data can be shared, and what’s strictly off-limits. Make sure everyone knows the rules before they start using AI tools. A well-informed team is your best protection against costly mistakes.

Adopting new technology can feel overwhelming, especially when it comes to budget tools. After all, we’re talking about the financial heart of your business. But implementation doesn’t have to be complicated. Modern budgeting platforms scale as your business

grows. You don’t need an enterprise-level budget to benefit from this automation. Many tools are designed specifically for companies of our size.

So start small. Pick one budgeting or forecasting process to automate first. Make sure your existing data is clean, because accuracy starts at the source. And bring your financial and IT team into the conversation early. Their buy-in makes everything work better.

AI (budgeting) isn’t a passing trend, the technology is becoming the baseline for competitive, future-focused organizations.

If this article sparks a question, a “could this help us?” moment, or if you’re curious about using automation, AI, or smarter technology in your business, Meeting Tree Computer is here to help. Reach out — no pressure. We’re here to talk through options.

Call us at 845-237-2117 or email info@meetingtreecomputer.com. Let us help you focus on what actually makes a difference.

Michael Zalkin, Chair

James Bates, Vice Chair

John Brust, Treasurer

Steven Vegliante, Secretary

Jerry Dunlavey

Eric Egeland

Karen Fisher

Amanda Gesztesi

Anthony Griffith

George Kinne

Kevin McLaren

Scott Perry

Kelly Pressler

Bobbi Scroggin

Gary Silver

Fred Stabbert

Norm Sutherland

Our next issue is scheduled for publication in May, and there is a considerable discount if you purchase an ad now for the following four issues. Contact Jen Cassaro at cassaro.jen@scpartnership.com today to find out how to reserve your spot in our Spring issue.

When I asked a group of professionals what “wellness” at work meant to them, the answers ranged from “My company does flu shots every year” to “I think we did yoga once.” While these are pieces of the puzzle, workplace wellness is much more than occasional perks—it’s a strategic investment that impacts health, productivity, and your bottom line.

By Marisa Gee Assured Partners

Effective wellness programs support employees across four key pillars:

Physical Wellness: Fitness programs, preventive care, nutrition, and healthy habits.

Emotional Wellness: Mental health resources, stress management, and resilience training.

Financial Wellness: Budgeting tools, retirement planning, and debt management education.

Social Wellness: Building community, teamwork, and a sense of belonging.

Together, these pillars help reduce chronic disease risk, improve engagement, and lower healthcare costs.

Meet Jim—a dedicated employee, father, and husband. Stress and financial strain lead him to unhealthy coping habits: poor sleep, skipped workouts, and increased alcohol use. He’s overweight, on medication for high blood pressure and cholesterol, and sometimes skips doses to save money. Eventually, depression sets in.

According to WELCOA, most healthcare costs treat preventable chronic conditions. Wellness programs cost about $500 per employee per year, yet studies show an average $3.27 return for every dollar invested through reduced healthcare costs and absenteeism.

• Absenteeism:

$1,685 per employee annually; indirect costs push this to $2,945.

• Presenteeism:**

$4,000–$6,000 per employee annually, or 7–9% of payroll.

(**Presenteeism is defined as being physically present at work but not fully productive due to health issues, stress, or other personal challenges.

The cost of ignoring Jim’s health?

• Heart attack hospitalization: $20,000–$40,000

• Stroke rehab: $30,000–$60,000

• Disability claim: $50,000–$100,000 annually

• Lost productivity: 3–6 months out of work

For Jim, the personal toll is immeasurable. For his employer, it’s a preventable financial risk. Proactive wellness programs could have changed this trajectory. ROI

$3.27 per dollar invested

UR Medicine Employee Wellness: $1,224 cost savings per participant and a $4.90 ROI per dollar spent.

SoFi + Wellhub: Flexible wellness benefits boosted engagement to 30%, improving retention.

WorkWell NYC: City-wide wellness strategy improved productivity and morale, with ROI estimates of $3.15 in productivity savings for every $1 invested.

Wellness isn’t a perk—it’s a strategic imperative. Investing in employee well-being delivers measurable returns in healthcare savings, productivity, and talent retention. For mid-sized companies, the math is clear:

• Program Cost: $300 per employee/year

• Expected Savings: $275,000 for 500 employees

• ROI: 83%—and often much higher with comprehensive programs.

Want to Learn More? Marisa Gee specializes in helping organizations contain costs without sacrificing care. With deep experience across carriers, voluntary benefits, and client management, she delivers tailored solutions for employers throughout the Hudson Valley and beyond. For more information about wellness plans and Employee Benefit options, please contact Marisa at marisa.gee@assuredpartners.com.

Meg Thompson Strategic Architecture Manager CCI System Inc.

Finding ways to boost property value without costly investments is a challenge every owner faces. Amenities like pools and fitness centers have long been standard, but the next level of differentiation comes from something less visible and far more impactful: reliable communication connectivity. Properties that deliver dependable services, such as property wide Wi-Fi, create a better experience for tenants and guests, leading to stronger retention and higher returns.

For residential properties, reliable connectivity is no longer optional, it is an expectation. As work models shift from in-office to hybrid and remote, tenants depend on fast, dependable service for business and expect the same for entertainment, gaming, and smart home devices. Poor internet leads to frustration and lower renter retention. When connectivity fails, remote

work and streaming suffer, creating a negative impression that impacts occupancy rates and erodes property value.

Property owners have an opportunity to differentiate by delivering enterprise-grade connectivity directly to tenants, the same level of service trusted by hospitals and Fortune 500 companies. This elevates managed Wi-Fi from a basic utility to a premium amenity that attracts and retains residents. Beyond convenience, it signals a commitment to modern living standards and positions the property as forward-thinking.

Managed wireless solutions for multi-dwelling units (MDUs) simplify operations for property owners. Instead of managing multiple service providers, owners can offer consistent, high-quality connectivity across the property with centralized oversight. Features such as proactive network monitoring, secure device segregation, and 24/7 support reduce operational headaches while improving tenant satisfaction. For owners, this translates into stronger leasing appeal, higher net operating income through amenity-based pricing, and a competitive edge in markets where connectivity is a deciding factor.

Hotels and resorts face similar challenges. Resort guests expect strong, secure connectivity from the moment they arrive. The hospitality wireless market was valued at $2.17 billion in 2024 and is projected to reach $6.31 billion by 2033. This growth is driven by demand for cloud-managed networks, connected devices, and enhanced guest experiences.

For hospitality operators, connectivity is a competitive advantage, especially in a market with sparse cellular

coverage and limited access to high-speed internet service. Deploying infrastructure that supports phone upgrades, first-time installations, and in-room wireless on a single platform simplifies operations and reduces maintenance costs. Outsourcing management ensures reliability and allows staff to focus on guest service. These improvements lead to better reviews, repeat bookings, and lower operating costs.

Whether in housing or hospitality, the case for investing in connectivity is clear. It improves the experience for tenants and guests, strengthens retention, and creates new revenue opportunities. For developers and investors, it adds measurable value to the property. For unions, electricians, and builders, it opens doors to projects that meet modern expectations. Modernized networks meet today’s connectivity standards and compliance requirements but also ensure properties can handle the growing demands of streaming, remote work, and smart technologies, making connectivity a cornerstone of future-ready development.

Properties equipped with dependable connectivity attract and keep tenants, command higher rents, and deliver better returns. In a competitive market, that advantage matters.

As Sullivan County continues to grow, addressing gaps in dependable connectivity is an opportunity for new development. Builders, architects, and developers who plan around modern connectivity position themselves ahead of the curve. Investors who prioritize these upgrades secure stronger long-term gains. The future belongs to properties that deliver the connected experience tenants and guests expect.

CCI Systems, Inc. is an employee-owned leader in broadband and telecommunications solutions. For over 60 years, CCI has delivered innovative, end-to-end services: consulting, engineering, construction management, and network sustainability, across wireline, wireless, energy, and municipal sectors. With a team of 1,200+ experts and a nationwide footprint, CCI empowers communities and enterprises to expand connectivity and future-proof networks.

Advance Testing, a longtime trusted provider of construction materials testing and quality assurance services, has announced a major milestone in its growth: on October 31, 2025, the firm officially joined SOCOTEC, a globally recognized expert in buildings and infrastructure.

The strategic acquisition positions Advance Testing to significantly expand its capabilities while continuing to deliver the rigorous, reliable service its clients and partners have relied on for more than 40 years. As part of SOCOTEC, Advance Testing now has access to a nationwide network of 25 accredited laboratories and a deep bench of technical expertise spanning building performance and compliance, construction materials testing, forensic engineering, geotechnical services, environmental health and safety, project advisory and risk management, and digital and AI-assisted compliance services.

SOCOTEC’s global reach further strengthens Advance Testing’s ability to support complex projects. The organization employs more than 13,000 professionals worldwide, including over 1,700 experts across more than 40 offices in the United States, providing expanded resources and support for clients from coast to coast.

While the partnership enhances the scope and scale of services available, Advance Testing emphasized that continuity remains a priority. Clients will continue working with the same leadership team, project staff, and office contacts, with no changes to locations, phone numbers, billing, or contractual arrangements. The company’s long-standing commitment to service excellence and to the communities it serves also remains unchanged.

Together, Advance Testing and SOCOTEC are advancing quality, performance, and resilience across America’s built environment—delivering trusted expertise “from the ground up” and reinforcing the vital role industry members play in strengthening regional and national infrastructure.

After more than four decades of leadership and service, James P. “Jimmy” Smith, Jr., founder of Advance Testing, is stepping into a well-earned retirement, leaving behind a remarkable legacy in the construction materials testing and inspection industry.

Jimmy founded Advance Testing in 1984 and spent 42 years guiding the firm with strategic vision, deep market knowledge, and a steadfast commitment to client service. Under his leadership, Advance Testing grew into a trusted name in the region, known not only for technical expertise but also for its role in supporting a stronger, safer, and more resilient built environment.

Equally notable has been Jimmy’s longstanding dedication to the community. For decades, he has been an active member of the Sullivan County Partnership for Economic Development, while also participating in and supporting numerous community organizations, philanthropic efforts, and nonprofit initiatives throughout the region. His willingness to serve—often in board and leadership roles—reflects a deep belief in giving back and investing time, talent, and resources to strengthen the places where he lived and worked.

As Advance Testing looks ahead to the future as part of SOCOTEC, the foundation Jimmy built remains central to the company’s continued growth and success.

Patrick Kiernan has taken on the role of President moving forward. Patrick’s email is pkiernan@advancetesting.com and he can be reached at 845-496-1600 ext. 211.

The Partnership proudly recognizes Jimmy Smith for his extraordinary professional achievements, his generosity, and his commitment to community, and wishes him continued success and fulfillment in retirement.

By Michelle Rider, CPA, Esq.

The importance of integrating your business succession plan and personal estate planning cannot be overstated, yet many small business owners spend so much time worrying about their businesses that they fail to do the proper planning when the time comes for them to exit and move onto their next chapter. In fact, making and implementing a comprehensive business succession and estate plan can sometimes be so time-consuming, emotionally fraught, and overwhelming, that many business owners procrastinate which can lead to unintended consequences and occasionally disastrous results.

A thoughtful integrated business succession and estate plan should take the following into consideration:

1. Who are the likely successors to own the business? Are they family members, or does a sale to a third party make the most sense?

2. When should you start the process of finding a successor or buyer? Is the business ready for the due diligence process if you will be looking for an outside buyer? Are you financially ready to give up the income stream?

3. Does the business owner (and spouse) wish to equalize their children’s inheritance? Are there sufficient assets outside of the business to equalize those who will not step into the business, or will you force your children in the business to be partners with their siblings? Have you provided a buy-sell arrangement for the children involved to buy out the uninvolved ones? It may make sense to gift or sell a portion of the business to the children during lifetime and bind everyone to a shareholders’ agreement to allow for smoother transition.

4. Should the children coming into the business consider a prenuptial agreement?

5. How much have you thought about what you’re going to do with all your free time after you exit the business? This can sometimes be the most difficultbut frequently overlooked issue for an exiting owner.

6. Has your attorney prepared your estate planning documents to work in tandem with the business succession plan? It is critical for these legal instruments to be integrated and should include practical considerations such as appointing officers of the small business

who can attend to the operation of the business in the event of the owner’s death without having to wait for probate and considering the appointment of different agents with powers of attorney for personal vs. business matters.

As a small business owner myself, I know how hard it is to take the time to do this important planning when “duty calls” but cannot stress enough the importance of scheduling dedicated time to discuss and consider these important issues with your trusted advisors and setting deadlines for yourself to complete the process.

For more than 50 years, business owners across the Hudson Valley have trusted us to protect what they’ve built and help them grow.

With a new name and the same steady counsel, MAHON RIDER McKAY is ready for your next chapter—offering legal support for every stage of your financial life—personal and professional. Let us help you move forward with confidence.

From Long Island City, NY to Honesdale, PA — they’re not just from Sullivan County! Each issue, we’ll be calling out members from all over the map.

1 E-J Electric Installation Co. EJ1899.com

718-786-9400

46-41 Vernon Blvd Long Island City, NY 11101

2 EverGreen Meadow Academy evergreenmeadowacademy.org

833-346-4968 PO Box 64

Cochecton, NY 12726

3 Fidelis Care fideliscare.org

518-530-9097

25 British American Blvd Latham, NY 12110

4 Formaggio Italian Cheese Specialties formaggiocheese.com

845-436-4200

250 Hilldale Rd Hurleyville, NY 12747

5 Garigliano Law Offices, LLP

845-796-1010

449 Broadway Monticello, NY 12701

6 Gastronome Packaging 80 Brooks Rd Ferndale, NY 12734

7 Kevin’s Restaurant

845-283-4975

249 Rock Hill Dr Rock Hill, NY 12775

8 Livingston Legacy Holdings livingstonlegacyholdings.com

9 NGS Construction

845-557-8245

10 Niki Jones nikijones.com

845-856-1266

39 Front St Port Jervis, NY 12771

11 Platform Industries platformindustries.com

570-499-3902

134 Crestmont Dr Honsedale, PA 18431

12 Pollinator Spirits pollinatorspirits.com 914-850-1248

244 Delaware Lake Rd Long Eddy, NY 12760

13 RWE Clean Energy rwecleanenergy.com

100 Summit Lake Dr Suite 200 Valhalla, NY 10595

14 VGF Management vgfmanagement.com 845-500-7498

574 State Route 416 Montgomery, NY 12549