Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

PTCL’s Telenor acquisition: Inside the $400 million merger that reshapes digital competition

The Competition Commission’s conditional approval of PTCL’s acquisition of Telenor Pakistan marks the telecommunications sector’s most consequential consolidation in a decade

By Ahtasam Ahmad

On October 1, 2025, after months of intense scrutiny and stakeholder consultations, the Competition Commission of Pakistan (CCP) delivered its verdict on what may prove to be Pakistan’s most significant telecommunications transaction since the Mobilink-Warid merger of 2016. The conditional approval of Pakistan Telecommunication Company Limited’s (PTCL) Rs108 billion ($400 million) acquisition of Telenor Pakistan didn’t just greenlight a corporate transaction, it fundamentally rewrote the competitive landscape of Pakistan’s digital economy.

The decision transforms a fragmented four-player mobile market, where Jazz commanded 37%, Zong held 26%, Telenor controlled 22%, and Ufone struggled with 14%, into a concentrated three-operator structure. Post-merger, the newly created MergeCo, combining Telenor’s network strength with Ufone’s PTCL backing, will control approximately 35% of Pakistan’s mobile market, creating a near-duopoly with Jazz while potentially squeezing third-placed Zong into an increasingly marginal position.

Yet the CCP’s 147-page order, dense with technical analysis and unprecedented regulatory conditions, tells a far more nuanced story than simple market consolidation. It reveals deep anxieties about vertical integration, infrastructure foreclosure, and the delicate balance between enabling sector sustainability and protecting consumer welfare in an industry simultaneously experiencing explosive data growth and catastrophic revenue decline.

The deal’s unlikely origins

The transaction’s genesis lies not in strategic ambition but strategic retreat. Telenor, the Norwegian telecommunications giant, has been systematically exiting low growth markets, divesting operations in Myanmar, and now Pakistan as part of a global portfolio rationalization. For PTCL, majority-owned by UAE’s e& since 2006, the opportunity represented something more desperate: a chance to salvage its struggling mobile subsidiary Ufone, perpetually trapped in fourth place and bleeding cash. Economics tells the story of distress. Topline Securities’ analysis reveals PTCL acquired Telenor at a remarkable 2.25x EV/ EBITDA multiple, a significant discount to the

estimated 5x fair value for Pakistani telecommunications assets. With Telenor’s balance sheet showing Rs160-170 billion in non-current assets against a purchase price of Rs108 billion, PTCL secured what amounts to a bargain purchase, with the tower portfolio alone valued at approximately the entire consideration.

The International Finance Corporation (IFC), World Bank’s private sector arm, led a $400 million financing consortium including British International Investment, providing seven-year tenor debt. This multilateral development finance involvement signals both commercial opportunity, acquiring distressed assets cheaply, and strategic importance, as Pakistan’s digital infrastructure investment aligns with broader economic development objectives.

The CCP’s exhaustive analysis examined distinct markets where the merger creates overlaps or raises foreclosure concerns, each revealing different competitive dynamics and regulatory anxieties.

The core battlefield

In retail mobile services, the merger’s impact is most visible and contentious.

The CCP’s Herfindahl-Hirschman Index (HHI) analysis, the standard measure

It is a great development provided they are able to strictly follow all the conditions set by CCP. I am concerned that the follow-up, or the supervision part, of CCP may not be as robust as it should be, and with time it may even fade out. However, if that can be managed in letter and spirit, it can result in something very positive for the country

Parvez Iftikhar, senior IT consultant and founding CEO of Pakistan’s Universal Service Fund

of market concentration, shows concerning trends. Revenue-based HHI jumps from 2,994 pre-merger to 3,514 post-merger, an increase of 520 points. Subscriber-based HHI rises even more dramatically, from 2,790 to 3,428, a 638-point increase signaling substantial concentration.

“The Commission concludes that the proposed merger is likely to create a dominant position in the retail mobile telecommunications market, carrying a risk of reducing competition,” the order states bluntly. While noting that dominance itself doesn’t violate competition law, the CCP emphasizes it “increases the risk of future market abuse and collusion.”

The oligopoly mathematics are stark. With only three significant players post-merger, economic theory suggests coordination becomes easier. Jazz and MergeCo together will control 72% of the market, creating dynamics where tacit collusion, aligning pricing and strategies without explicit agreements, becomes more viable. Zong, trapped at 26%, faces the prospect of becoming a perpetual third player unable to challenge the duopoly’s market power.

Yet the CCP also acknowledges countervailing pressures. Mobile Number Portability (MNP), which allows subscribers to switch operators without changing numbers, provides some demand-side constraint. Analysis of 2021-2024 porting data shows peak migration in 2022 with 725,191 portouts across all operators, though activity has since declined. The Commission warns that “without sustained regulatory oversight, operators may adopt practices that could impede portability and erode pro-competitive effects.”

“We hope the MergeCo focuses towards a ServiceCo model like Jazz, where competitive advantage stems from innovative products and services rather than pricing strategies,” states, Kazim Mujtaba, President Jazz Consumer Division.

Vertical integration fears

The Long Distance and International (LDI) market, covering both retail international calling and wholesale international incoming voice services, presents the merger’s most complex competitive concerns. Here, PTCL already dominates with 32.67% retail market share, while Telenor LDI holds a modest 15.61%. The combined entity’s 48.28% share isn’t dramatically concentrated by global standards, but vertical integration with mobile operations creates foreclosure risks.

Wateen Telecom, a major stakeholder opponent, argued forcefully that PTCL’s control over both upstream infrastructure (fiber networks, interconnection points) and downstream mobile operations (MergeCo’s 35% subscriber base) creates both input and customer foreclosure opportunities. “After being merged with Ufone, Telenor Pakistan will get tied to PTCL and will either no longer provide services to other LDI operators or will provide substantially less capacity,” Wateen submitted, warning of competitive exclusion. The CCP found these concerns credible, adding, “PTCL has both the ability and incentive to pursue input foreclosure strategies, resulting in substantial lessening of competition. The Commission also believes PTCL has the ability and incentives to provide LDI services to MergeCo, which may result in total or partial customer foreclosure for other LDI service providers.”

PTCL’s historical conduct amplifies these worries. The Commission notes PTCL has “on quite a few occasions, been accused of engaging in anti-competitive practices,” lending empirical weight to foreclosure theories. With MergeCo’s entire LDI requirements likely met internally by PTCL, competitors like Wateen face losing access to approximately 35% of the potential customer base, an existential threat in an already challenging market.

The duopoly problem

The wholesale IP bandwidth market, providing internet connectivity capacity to retail ISPs and mobile operators, presents perhaps the clearest case of market power concerns. Pakistan Telecommunication Authority’s 2021 Significant Market Power (SMP) determination identified this as a duopoly, with PTCL holding 64.5% and Transworld Associates (TWA) controlling 35.5%.

The Commission’s analysis highlights the market dynamics. “TWA and PTCL have all the means to control their consumers as other operators have no choice but to acquire IP bandwidth services only from these two operators,” PTA observed. With Telenor Pakistan currently sourcing 100% of its IP bandwidth from PTCL since 2019, the merger transforms an arm’slength commercial relationship into internal transfer pricing.

This creates opportunities for preferential treatment. “PTCL may grant preferential treatment to its wholly-owned subsidiary MergeCo by leveraging its control over essential IP bandwidth and fiber network infrastructure,” the CCP warns. “This could take various forms including discounted bandwidth rates, expedited service provisioning, or exclusive access to enhanced network capacities, enabling MergeCo to deliver more competitive retail services than rivals.” Jazz and Zong, dependent on PTCL/TWA for wholesale bandwidth, face asymmetric disadvantages. The merged entity’s vertical integration means MergeCo potentially accesses bandwidth at cost while competitors pay market rates, creating margin differentials that compound over time.

The tower portfolio puzzle

The telecommunications infrastructure market reveals the transaction’s physical dimension. Post-merger, MergeCo will control approximate-

We hope the MergeCo focuses towards a ServiceCo model like Jazz, where competitive advantage stems from innovative products and services rather than pricing strategies

Kazim Mujtaba, President Jazz Consumer Division

ly 17,000-24,000 cell sites (accounts vary between owned and leased sites), representing roughly 44% of Pakistan’s total tower infrastructure. Jazz operates about 15,500 sites (27.9%), while Zong maintains 15,239 (27.4%).

The immediate controversy concerns decommissioning. PTCL plans to reduce overlapping sites from the combined 24,000 to approximately 17,000 towers, optimizing the merged network. However, about 1,200 sites (5% of total) currently host “guest operators”, competitors renting space under infrastructure sharing agreements. Of these, approximately 500 sites (2% of total) face potential decommissioning.

This creates coverage gaps for competitors forced to vacate. While 2% seems minor, these sites often serve strategically important locations. The CCP notes that “procedural complexities” in establishing new sites exacerbate the problem, making it difficult for displaced operators to quickly secure alternative locations.

The regulatory response involves PTA’s Framework for Telecom Infrastructure Sharing (FTIS), issued in October 2023. However, the Commission observes the framework’s “recommendatory nature calls for continuous oversight in the form of enforceable obligations to prevent anti-competitive behavior.”

Real benefits or wishful thinking?

PTCL’s efficiency claims provided the crucial justification for merger approval despite concentration concerns. Under Pakistan’s Competition Act, mergers that substantially lessen competition may still be approved if efficiencies are merger-specific, verifiable, and passed on to consumers, the standard set by European Commission precedents.

The claimed synergies span multiple dimensions, each contributing to projected improvements.

With both entities tower sites merging into a single grid of approximately 17,000 optimized sites promises substantial operational savings. PTCL projects annual cost reductions from decommissioning redundant infrastructure and consolidating spectrum

use. The combined entity will increase data speeds from Ufone’s 12 Mbps and Telenor’s 8 Mbps, eventually reaching parity with Jazz and Zong’s performance, representing a 3-4x improvement.

Telenor’s strength in rural and northern areas combines with Ufone’s urban and southern coverage to create a truly nationwide reach. Population coverage for voice services expands significantly for both customer bases, while data coverage improves through spectrum refarming and site optimization.

Beyond network costs, PTCL identifies multiple efficiency sources including optimized marketing efforts, IT systems and licensing consolidation, employment streamlining, enhanced vendor bargaining power, and spectrum consolidation.

Perhaps most critically for policy objectives, the merger positions MergeCo to participate meaningfully in Pakistan’s planned 2025 NGMS spectrum auction. The consolidated entity’s financial capacity and spectrum holdings make it a credible 5G deployer.

The combined network of physical stores nationwide improves accessibility for both brands’ customers. Spectrum efficiency gains promise better service quality, while consolidated operations enable investment in next-generation services.

Yet the Commission remained skeptical of taking these projections at face value. “While the Applicant’s submissions indicate the proposed transaction could generate significant efficiencies, these are neither assured nor independently verifiable in their current form,” the order states. “In the absence of binding commitments, projected coverage, quality, and capacity improvements remain aspirational and not verifiable for merger clearance purposes.”

PTCL’s conditional approach, investments subject to annual budgets, macroeconomic conditions, regulatory developments, and undefined spectrum auction terms, further undermined credibility.

The materialization of synergies typically requires a multi-year integration period. This window presents a strategic vulnerability: should Jazz, the market leader, intensify its customer acquisition and network expansion efforts, the anticipated benefits of the merger

could be substantially diminished.

The bottom line

For PTCL shareholders, the transaction’s financial logic appears compelling. Topline Securities’ analysis projects incremental earnings per share contribution growing from Rs3.7 in Year 1 to Rs4.9 in Year 3, representing 32% growth as synergies materialize. Starting from an EBITDA base of Rs55 billion, the combined entity should reach Rs60.5 billion in Year 2 and Rs66.6 billion by Year 3, a 21% cumulative EBITDA expansion.

The valuation metrics underscore the bargain nature. At 2.25x EV/EBITDA versus the 5x fair value multiple for Pakistani telecommunications assets, PTCL acquired Telenor at a 55% discount. Using international comparable company analysis, where telecom operators trade at an average 6.67x EV/EBITDA with a 12.25% frontier market discount, suggests PTCL’s fair value per share exceeds Rs65, implying substantial upside from predeal levels.

The bargain purchase gain adds further value. With Telenor Pakistan’s balance sheet showing Rs160-170 billion in non-current assets against the Rs108 billion enterprise value, accounting rules likely require recognizing a sizeable gain, a non-cash boost to reported profitability that improves financial metrics. Infrastructure assets provide tangible value. Telenor’s approximately 7,500 towers, compared to recent comparable transactions like Engro Holdings’ acquisition of Jazz towers at roughly Rs150,000 per tower, suggest the tower portfolio alone approximates the entire purchase consideration. This implies PTCL essentially acquired the operating telecommunications business, subscribers, spectrum rights, brand equity, at minimal or negative valuation, an extraordinary bargain reflecting Telenor’s forced seller position.

However, these rosy projections confront harsh realities documented in the CCP order and broader industry analysis. Pakistan’s telecommunications sector faces structural headwinds: industry revenue declining from $5.0 billion in 2016 to $3.4 billion in 2023

despite data consumption exploding 335%, an unprecedented inverse relationship between demand and revenue. Average revenue per user (ARPU) stands at $0.80 monthly, the world’s lowest, 90% below the global average of $8.00.

The tax and regulatory burden compounds operator distress. Pakistan leads globally with 34.5% total ICT taxation, while spectrum costs consume approximately 20% of operator revenue, double the sustainable 10% international benchmark. These structural factors constrain the extent to which merger efficiencies translate to improved financial performance.

Regulatory armor or paper tiger?

Understanding the approval requires examining the unprecedented 20 conditions the CCP imposed, which collectively represent one of the most comprehensive behavioral remedy package in Pakistani merger control history.

As per the CCP order, PTCL and MergeCo must maintain separate boards and independent management structures, with no overlapping positions. Any individual leaving a position in one entity faces a three-year cooling-off period before assuming board or management roles in the other. This aims to prevent coordination that could enable foreclosure or preferential treatment.

CEOs and senior management must possess demonstrable competence, extensive telecom and digital industry experience, proven turnaround expertise, and “impeccable integrity, honesty and reputation.” These qualifications apply mutatis mutandis to senior management across both entities, with E& required to ensure professional leadership.

Perhaps most significantly, an independent reviewer will be appointed for five years to monitor compliance, audit transactions, and submit quarterly reports to the CCP. The TPR must possess appropriate qualifications and telecom sector experience while maintaining absolute independence, no conflict of interest, remuneration that doesn’t impede effectiveness, and confidentiality obligations.

Cross-subsidization is prohibited unless conducted competitively at arm’s length. All related party transactions must be submitted to the TPR quarterly, with the independent auditor required to explicitly confirm whether transactions were arm’s length and whether substantial price differences existed versus market rates.

The most complex conditions govern interconnection and infrastructure sharing. PTCL and MergeCo must provide equal access to infrastructure capacity for all telecom

operators. All Reference Interconnect Offers (RIO) require PTA approval, with PTCL offering interconnection to all operators per approved RIO. The entities cannot reduce interconnection circuits allocated to other operators without PTA approval, and pricing cannot be used to impede competitor access to MergeCo customers.

PTCL must seek PTA approval for wholesale pricing structures covering IP bandwidth services, LDI services, domestic leased lines, and telecom infrastructure services provided to PTA licensees and associated companies including MergeCo. This direct pricing regulation aims to prevent margin squeeze, charging high wholesale rates while offering low retail prices, that could foreclose competitors.

MergeCo must provide wholesale access to new Mobile Virtual Network Operators (MVNOs), including network access, call origination/termination, international roaming, and portability database access, on commercially fair and reasonable terms. This maintains market contestability even as facilities-based competition decreases from four to three operators.

Post-merger, PTCL and MergeCo must demonstrate claimed efficiencies are passed to consumers through competitive pricing, better services, and infrastructure investments. They must furnish comprehensive verifiable data to the TPR and Commission illustrating how efficiencies benefit consumers, not just shareholders.

Most dramatically, the CCP reserves explicit rights to direct divestiture of assets or business segments if future violations occur. This ultimate enforcement backstop provides regulatory deterrence while acknowledging that behavioral conditions may prove insufficient.

Critics question whether these conditions will prove enforceable. The Commission’s resource constraints, PTCL’s history of challenging regulatory orders in court, and the sheer complexity of monitoring compliance all suggest implementation challenges. The TPR’s effectiveness depends entirely on who is appointed, their actual independence, and whether the CCP vigorously backs their findings.

“It is a great development provided they are able to strictly follow all the conditions set by CCP. I am concerned that the follow-up, or the supervision part, of CCP may not be as robust as it should be, and with time it may even fade out. However, if that can be managed in letter and spirit, it can result in something very positive for the country,” remarked, Parvez Iftikhar, senior IT consultant and founding CEO of Pakistan’s Universal Service Fund.

The road ahead: three scenarios

Pakistan’s telecommunications future post-merger likely follows one of three trajectories, each with distinct implications for competition, investment, and consumer welfare.

Scenario one might be of a managed decline that sees the merger providing temporary relief, synergies materialize, costs decline, MergeCo survives, but fundamental structural problems remain unaddressed. Revenue continues declining or stagnates, infrastructure investment remains insufficient, and service quality improves marginally but lags regional peers. The 2025 spectrum auction proceeds with “moderately” lower reserve prices; some spectrum sells, but deployment remains limited and urban-focused. By 2028-2030, financial pressures force consideration of further consolidation, potentially reducing the market to two players.

Scenario two might be of a reform catalyst with the merger shocking policymakers into comprehensive reform. Tax rationalization reduces the 34.5% ICT burden to regional norms around 20-25%. Spectrum pricing adopts GSMA recommendations, significantly lower reserve prices, 20-year payment plans with moratoriums, and rupee denomination. Infrastructure sharing policies enable 30-40% cost reductions. These reforms create sustainable telecommunications economics, enabling genuine 5G deployment and narrowing the digital infrastructure gap with regional peers. This scenario requires political will currently absent given Pakistan’s fiscal crisis.

A third scenario might mimic what happened in Bangladesh. The merger proceeded but broader policy failures undermined benefits. The 2025 spectrum auction demands high reserve prices prioritizing government revenue over sector sustainability. Operators bid reluctantly, stretching finances. Spectrum is allocated but deployment stalls, fiber buildout too expensive, device penetration insufficient, business case doesn’t close. “5G” is announced but remains trials indefinitely, like Bangladesh’s three-year deadlock despite successful 2022 spectrum allocation. Operators’ financial positions weaken under spectrum debt service, eventually forcing distress restructuring or bailouts.

Current evidence suggests scenario one as most probable, with elements of scenario three emerging if auction pricing remains unrealistic. The CCP’s conditional approval provides necessary room for consolidation, but cannot substitute for comprehensive policy reform addressing the sector’s structural crisis. n

No, Gul Ahmed is not shutting down exports

A combination of lazy and innumerate financial journalism and the Pakistani penchant for pessimism resulted in people thinking this is a way more significant news story than it actually is

By Farooq Tirmizi

When one of Pakistan’s largest and best known textile exporters announces that it is shutting down apparel exports, one might be tempted to ask why. The country’s financial journalists, LinkedIn influencers, and prolific WhatsApp forwarders, however, are free of such intellectual curiosity. They just assumed: “this is Pakistan, bad things happen here all the time. This must be one of them.”

Shared, bemoaned, moved on.

Except that they did not really understand what happened at all.

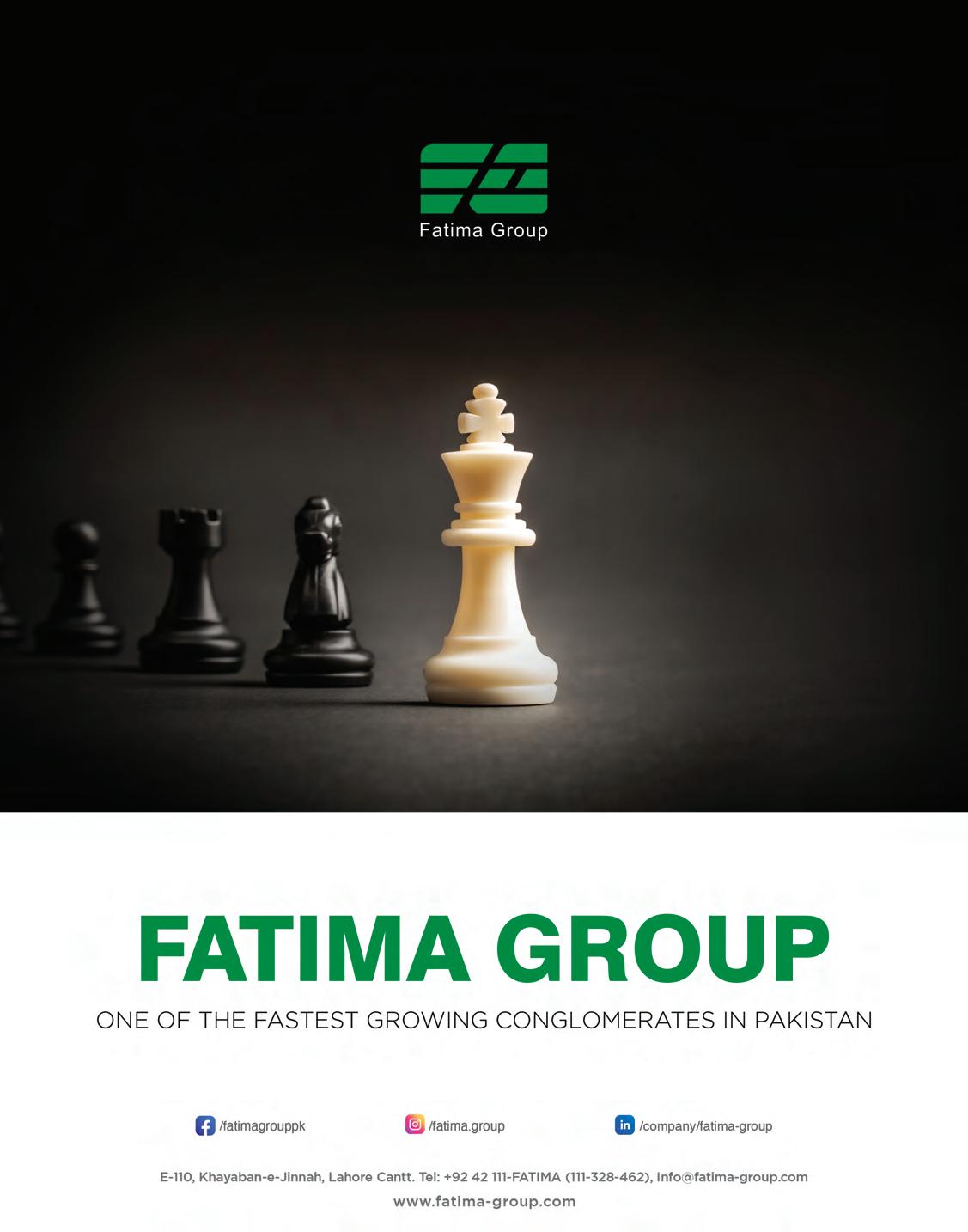

We find ourselves in the unusual position of writing a cover story of our magazine on a topic to highlight that it is not important: no, something as monumental as Gul Ahmed Textile Mills – a company that single-handedly generates half a billion dollars of exports for Pakistan – did not suddenly exit the entire export business because they could not make it work.

They exited one of their smallest product lines from exports, and even that, not for local production, just their export markets.

The reasons they gave – coupled with the fact that the company’s announcement made no effort to quantify the effect of the decision – made it sound like a bigger event than it actually is. In reality, apparel exports account for 7.7% of the company’s total revenue, and are among its lowest margin

earners, with gross margins as low as 9.9% in 2024, the last year for which the segment was broken out separately in Gul Ahmed’s financial statements.

Contrast that with the 35.7% gross margins the company earns on its retail business, which it operates through the Ideas brand of stores, both physical and online.

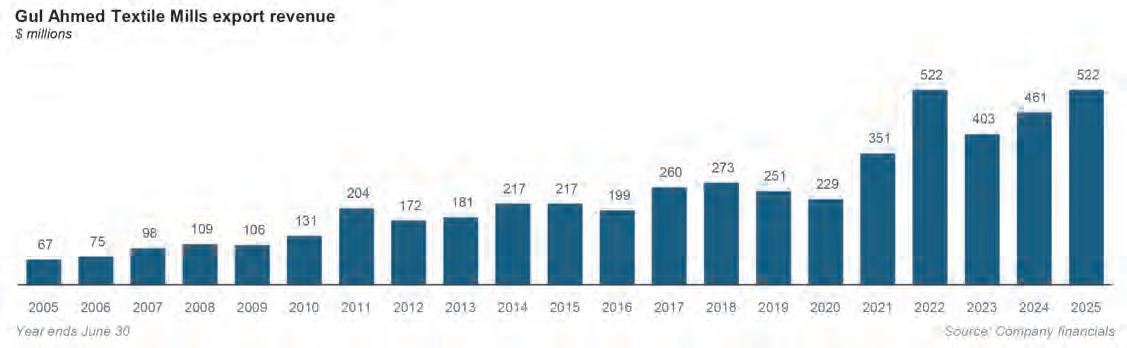

Gul Ahmed is among Pakistan’s largest exporters, having had $522 million worth of export sales for financial year 2025, compared with just $140 million in domestic sales. Announcing that it was giving up the entirety of its export business – obviously not what it actually said – would have been a restructuring of its business of monumental proportions, effectively saying it would get rid of nearly 79% of its revenue. The exit is, instead of a business line that is less than 8% of its revenue, so onetenth less significant.

But though it is not as monumental as one of the country’s largest exporters giving up on exporting, it does nonetheless say something interesting about the evolving nature of business in Pakistan, particularly with respect to geographic concentrations within the labour market.

In this story, we will begin with an overview of Gul Ahmed Textile Mills and their current business, examine how they got where they are today, and then look at why they decided to quit apparel exports, particularly given the fact that some of their exporting peers have been able to make exports their core business.

Gul Ahmed: origins and history

The history of the company starts – as with many Pakistani businesses –with a Gujarati trading family. In this case, it begins with Haji Ali Mohammad, a Gujarati cloth and textile trader who started his career the late 1940s by setting up a bottling affiliate for PepsiCo in Karachi. By 1950, Ali Mohammad, in addition to bottling and distributing Pepsi’s products, was also using the same company – Mehran Bottlers –to manufacture and sell his own brand of soft drink, what we now know as Pakola.

Bolstered by his success as a Pepsi bottler, Haji Ali Mohammad started a textile company in 1953 and named it Gul Ahmed Textiles, which is now arguably one of the best known brands in Pakistani clothing. (Mehran Bottlers is no longer part of the same group.) From the outset, the company sought to go beyond the most basic level of manufacturing cotton yarn and created a vertically integrated textile mill.

That meant it could take ginned cotton and convert it into yarn, take that yarn and weave it into cloth, and then dye, process, and stich that cloth into a finished product.

From a very early point in its history, Gul Ahmed wanted its brand name to be known to the Pakistani consumer, even as it made a substantial portion of its income exporting its products under other people’s brand names to other countries. That level of sophistication is

also reflected in the fact that not many trading businesses created incorporated businesses as early as 1953, but Gul Ahmed did. It was one of the first 1,000 companies to be registered in Pakistan after independence.

The company made the decision to go public in 1970, which in hindsight was not ideal timing as the events that would lead up to the 1971 war and Bangladesh’s independence had already begun. And that would then be followed by a left-leaning government suspicious of the profit motive, which effectively meant that for the first decade or so after the company was publicly listed, Pakistan’s capital markets went nowhere.

The company and the group, however, kept on expanding. Throughout the 1980s and 1990s, it kept expanding both its domestic footprint and export network. Its exports were especially helped after the creation of the World Trade Organization in 1995, which allowed Pakistani textile companies to export much more than they had previously been able to due to the pre-WTO quotas that restricted how much each country could export textiles.

The entire 10-year period that coincided with the phased end of the Multifiber Agreement (1995 to 2005) – which was the formal name of the pre-WTO textile export quotas – was one of significant growth for the group. It was during this time, in 2003, that they launched a domestic retail brand called Ideas, meant to offer the rising Pakistani middle class the same quality of goods that the company was exporting outside the country.

In the meantime, as is the case with many Pakistani business families, the family grew big enough that the assets needed to be divided up. Haji Ali Mohammad had two sons, Iqbal and Bashir. Bashir and his children got Gul Ahmed Textile. Iqbal and his offspring got Gul Ahmed Energy. The companies have some dealings with each other, but they are not owned by the same people and are specifically separated as part of a distribution of inheritance.

(This used to not be an important disclaimer to make, but then came the August 2024 drunk driving incident involving a member of the family that owns Gul Ahmed Energy, and it is now necessary in any story about Gul Ahmed Textile to note that the people who own the textile mill are related to, but not the same as, the people who own the energy company.)

What Gul Ahmed sells

Like most textile mills in Pakistan, Gul Ahmed started off as a seller of yarn, though unlikely many others, it kept moving up the value chain. The company still produces yarn to be sold to other textile companies, and has many other product

lines as well, but by far its most important is the line called home textile. What are home textiles? Bedding, blankets, towels, table cloths, curtains, bed sheets, etc. Stuff that is made of cloth, used in the home, but not worn on a person.

This is important to understand because this type of product is different from clothing worn by individuals. Specifically, the nature and amount of stitching involved is different –and generally less complex – than the stitching involved in making apparel worn by people.

But we are getting ahead of ourselves. First, let us understand the process by which textiles are made. Briefly, cotton is grown on farms, picked by farmers either by hand or machine, and then sold to cotton ginning mills. Nearly the entirety of Pakistan’s cotton ginning industry is located in South Punjab. Ginning involves removing the cotton seed from the cotton. It is a labour-intensive, low margin business, so even the owners of cotton gins are not particularly rich people.

That ginned cotton is then bought by textile spinning companies, who use spindles to turn that ginned cotton into cotton yarn. The yarn is then woven into cloth, the cloth is then dyed and printed, and after that comes the stitching phase.

This is, again, is a labour intensive part of the process, but it is a bit further up the value chain, so the margins are a little bit better. And here is where a big strategic decision needs to be made by the person who owns a textile factory.

See, textile spinning, weaving, and dyeing are big mechanical processes where large machines run by semi-skilled labourers and engineers do most of the work.

After that, your ability to go further up the value chain involves how many people you can have in a factory literally just sitting at a sewing machine and sewing up the items you are trying to manufacture. And the margins you will earn at this stage are determined by one decision: do you want to earn higher margins by having people sew smaller, more

complex stitches, or do you accept lower margins, but potentially higher volumes by doing simpler stiches that you can probably churn out faster?

A bedsheet, for example, involves a small number of straight lines that can be stitched very quickly. A pair of jeans, however, involves pockets, zippers, and curved stiches that can be significantly more complex. Your factory would earn a lot more for the jeans, but it will also take longer. The bedsheet could probably be done in seconds by a skilled labourer.

Historically, Gul Ahmed has been the company that chose the simpler product and made its money on the higher volumes. This, of course, is a strategy that has served the company quite well. Over the past 20 years –since 2005, when the textile barriers to trade completely fell away – the company has grown its export revenue from just $67 million in 2005 to $522 million in 2025, which represents an average growth rate of 10.8% per year in USD terms.

But having achieved that scale, Gul Ahmed then tried to invest in expanding its small but significant apparel manufacturing business. And that appears to have been the move that has not quite worked out and is being reversed. Let us take a look at what could be some of the reasons.

Apparel vs home textiles

We have already discussed the different levels of dexterity and time involved in stitching apparel versus home textiles. What is less appreciated is the margin levels between the two. This is best illustrated with an example.

Gul Ahmed Textile Mills has a consolidated revenue of Rs186 billion during the financial year ending June 30, 2025, which translates to approximately $662 million. This is somewhat less, but comparable in scale to Style Textiles (Pvt) Ltd, which earned revenue

of Rs209 billion, or $747 million in 2024, the latest year for which data is available.

But now look at profit margins. Gul Ahmed’s best net profit margin (net income divided by revenue) came in 2022, when it was almost 9%, and more typical years see its net margin at between 3% and 5% of revenue. Style Textiles, meanwhile, routinely has net margins exceeding 20% and in a good year can exceed 25% net margins.

Gul Ahmed’s main product is home textiles. Style’s main product is apparel, particularly sports apparel, for some of the world’s leading brands. The infrastructure at both Gul Ahmed and Style looks quite similar in many ways. But Style is enormously profitable in ways that Gul Ahmed is simply not.

It is natural, then, for Gul Ahmed to see the example of Style – a company that started in 1995 – and think about ways they can emulate its profitability levels, especially given the relative similarity of the infrastructure.

Gul Ahmed has had an apparel business for decades at this point, and Ideas now has lines of apparel products that are comparable in range to Khaadi, arguably the most well developed apparel brand in Pakistan. But producing for the domestic market and the export market are completely different endeavours. In the domestic market, the manufacturer controls when the product is launched, and so if it encounters delays, by virtue of the fact that it controls its own distribution to the customer, it can manage that delay with relatively no real impact.

In the export market, however, the manufacturer does not control the distribution, and is therefore working on somebody else’s timelines, in this case, companies who have expectations that their suppliers can meet very tight deadlines with relatively little warning or notice.

So developing the ability to produce apparel products for export is significantly harder. In theory, Gul Ahmed needed to put together the speed of its home textile export business with the complexity its domestic

business can handle. But that is what created the problems.

But before we dive into those problems, let us first make note of what the market thought was happening, and why it was not the right reading of the situation.

Why Gul Ahmed’s announcement was misinterpreted

Here is what Gul Ahmed said in its statement to shareholders on September 29:

“The Board of Directors of Gul Ahmed Textile Mills Limited, in its meeting held on 29-Sep-2025 has resolved to discontinue the business operations of the Company’s Export Apparel Segment. This decision has been taken following a comprehensive strategic review of the segment’s performance and future outlook.

The Export Apparel Segment, being highly labor-intensive, has faced sustained margin pressures due to a combination of internal and external factors. Persistent challenges include intense regional competition, a stronger exchange rate, recent government policy changes (such as the increase in advance turnover tax), rising costs of nominated fabrics, and elevated energy tariffs. Collectively, these factors have significantly undermined the segment’s cost structure and profitability, resulting in continued operational losses.

The strategic closure is expected to positively impact the Company by reducing ongoing losses, lowering borrowing levels, and improving cash flow management. This step will strengthen the Company’s overall financial position and enable greater focus on sustainable growth in its other business areas.

It is clarified that this decision relates solely to the Export Apparel Segment. The Company will continue its operations in other principal segments, including Home Textiles, Spinning, and Weaving, which remain integral

to the Company’s long-term growth strategy.”

Note where the word export appears: only next to the name of the business line being shut down. All of the other business lines, including home textiles which is its core export business, do not use the word export in their description. This makes it feel like exports as a whole are shutting down, even though that is not the case.

This is how the market reacted to it as well. There were the usual textile lobby crybabies who talked about this as symbolic of the sector’s difficulties.

But even market participants who should have been a bit more careful in their reading of the notice. AKD textile analyst Usama R Gurmani, for example, was quoted in The Express Tribune as talking about the company’s ability to pivot towards its profitable retail segment, which obviously is not what is happening. The retail expansion is independent of the pivot away from garments and continued focus on home textiles in its export markets.

The labour market explanation

What Gul Ahmed is saying with this move is that even the higher prices each clothing product commands was insufficient to compensate for the longer duration it took its employees to produce the products, thus leading it to think that the investment in the apparel business line was unlikely to pay off.

Part of what could explain the divergence in export performance is simply where the labour is located. Punjab has many more smaller apparel export units than Karachi, and even though Karachi has a few well-established apparel export manufacturers, the city’s labour market offers a lot more opportunities to skilled labourers in the apparel industry compared to Punjab.

If you are an apparel manufacturing labourer in Punjab, the majority of oppor-

tunities before you are in other factories doing the same thing, and employers tend to have relatively similar salary levels, so while labourers can and do switch, the motivation to do so is a bit lower than it is in Karachi, and creates a more significant upward trend in wage pressure.

Gul Ahmed alluded to this being a major factor by having labour intensity appear in the first sentence of its explanation. You need not just a small number of highly skilled labourers, but a very large number of them, and then you need them to stay with you as you invest in their growth and hope that you can earn a return from that investment in the skills of your employees.

Karachi has a smaller number of such employees available in the labour market, and they are more likely to switch jobs than in Punjab. Punjab also benefits from its cities having a generally larger pool of labourers from rural areas and smaller towns moving into the bigger industrial centers around the Lahore, Faisalabad, and Gujranwala metropolitan areas.

Could the problem be solved with training one’s own labour supply? This is an approach that many textile companies already undertake, including in Karachi, but Gul Ahmed ultimately decided that the scale of effort needed to make this is a bigger proportion of its business was simply not worth the effort. Ultimately, the improved cash flows and increased available capacity of its labour force could potentially be more profitably deployed towards its core business of home textile exports.

This may well be the right decision in the short term, but a longer term strategy to cross $1 billion in textile exports cannot come from something as simple and low margin as home textiles. Gul Ahmed will need to invest in a more versatile production capability, which means being able to have its labour force produce higher quality – and higher complexity goods – in a rapid enough fashion so that the company can generate enough cash flows to continue investing in its business. n

KE’s power struggle comes to an end with Saudis on top and SIFC backing

After months of legal wrangling, the government has brokered a truce in K-Electric’s ownership saga, with Sheheryar Chishty ceding control to Saudi investors, ending one of Pakistan’s most convoluted corporate standoffs.

By Abdullah Niazi

It took a decade of stalled deals, diplomatic nudges, and bruised egos, but the government has finally managed to untangle one of Pakistan’s longest-running corporate knots. The ownership dispute over K-Electric—the country’s

only vertically integrated power utility—has been settled.

According to a report by The Express Tribune, Pakistani investor Sheheryar Chishty has agreed to step aside and hand over his controlling stake in K-Electric’s parent company, KES Power Ltd, to Saudi prince Mansour Bin Mohammed Al Saud.

The deal marks what officials describe

as the largest Saudi investment yet in Pakistan’s power sector. It also points towards the growing importance of Saudi investors in Pakistan and the government’s willingness to make room for them where necessary.

According to Tribune’s report, the deal was achieved with mediation from the Special Investment Facilitation Council (SIFC) and behind-the-scenes diplomacy that reportedly

involved Prime Minister Shehbaz Sharif’s own outreach to Riyadh.

The agreement ends a bitter ownership battle that had spilled into courtrooms and cabinet meetings. Saudi investors have been involved in KE in some capacity or the other for more than 20 years now. They first got involved in the company when the Musharraf Administration made the decision to privatize KE in 2005. Saudi and Kuwaiti shareholders have had stakes in KES Power since then, but when Mr Chishty entered the scene in 2022, they viewed it as a coup. His purchase of Abraaj Group’s old stake through his investment vehicle, AsiaPak Investments, has been hotly contested since then.

The Saudis have consistently demanded answers about his source of funds and pressed the Pakistani government to intervene. It is this persistence that seems to have paid off. For a company as politically sensitive as K-Electric, that resolution means more than just a change in shareholders. It may finally provide the clarity that foreign investors have demanded for nearly a decade. More importantly, it might be a significant success for the SIFC — the organisation created to make the lives of foreign investors easier.

A tangled legacy

To understand how Pakistan’s largest city came to rely on a company perpetually caught between investors and governments, one has to go back in time. K-Electric began life in 1913 as the Karachi Electric Supply Company (KESC). It was nationalized in 1952 and eventually privatized under Pervez Musharraf’s government in 2005, when 66.4 percent of its shares were sold to a consortium led by Saudi Arabia’s Al-Jomaih Holding Company and Kuwait’s National Industries Group.

The early years after privatization were difficult. By 2008, the Saudi-Kuwaiti consortium brought in Dubai-based private-equity giant Abraaj Group to engineer a turnaround. Abraaj’s founder, Arif Naqvi, invested more than $390 million into the company, injecting both capital and corporate discipline. Over the next eight years, Abraaj poured nearly $1 billion into generation and transmission upgrades, cutting losses and modernizing what had long been an aging, unreliable grid.

By 2016, Abraaj had transformed K-Electric into a company worth buying. Shanghai Electric Power, a state-owned Chinese firm, agreed to purchase the controlling stake for $1.77 billion. It would have been one of the largest foreign acquisitions in Pakistan’s history.

But what should have been a crowning moment for both Abraaj and Pakistan’s privatization drive quickly devolved into a

bureaucratic nightmare. Approvals stalled. Regulatory agencies hesitated. Governments changed—five prime ministers in nine years— and no one could, or would, push the transaction through. Abraaj, meanwhile, continued to push and lobby for the sale. Despite Arif Naqvi’s personal connections and efforts, the sale continued to be stalled. KE had been an example of a successful corporate turnaround of a nationalised company that had been languishing for many decades. Now that it was time for the architects of this revival to reap the benefits, they were being told to wait.

Very quickly, the Shanghai Electric deal became a symbol of Pakistan’s inability to close. Despite repeated assurances and renewed applications, the Chinese suitor faced endless red tape.

Then came the fall.

In 2019, more than three years after the deal had first been struck with Shanghai Electric, Arif Naqvi and Abraaj were wrapped up in a global scandal of corruption and bankruptcy. Naqvi was accused of defrauding his clients and found himself in serious legal trouble. He was arrested and was set to stand trial. Meanwhile, Abraaj’s assets were stranded. One of these assets was KE. Naqvi had been desperate to sell KE because the proceeds from that might have allowed him to somehow evade his clients ire if he had successfully been able to use the funds from

the sale to Shanghai to get them their money back. At the very least it would have given him more time.

The Shanghai sale, which had already been on life support, was now dead in its tracks until the dust from the Abraaj collapse settled. Shanghai Electric lingered for years, still sending polite reminders to Pakistan’s ministries that its offer stood. But by 2023, the Chinese firm had had enough. Last month, it officially terminated the bid, citing Pakistan’s shifting business environment and unfulfilled conditions.

In a statement that was blunt by diplomatic standards, Shanghai Electric said it was “no longer aligned with the company’s international development direction” and needed to protect shareholder interests.

It was the full stop on a saga that had begun with promise and ended in frustration.

For Pakistan’s investment community, the message was uncomfortable. Even as the government created the SIFC to fast-track foreign projects and woo investors, here was a flagship example of how difficult that could be. This needed repairing. It is why when President Zardari visited China, he made it a point to visit the headquarters of Shanghai Electric and assure them that his government would find a path for Shanghai and other foreign investors.

But the assurances were not enough.

CEO of Trident Energy Pvt Ltd, Habil Ahmed Khan, and K-Electric CEO Moonis Abdullah Alvi sign an MoU to establish hybrid solar and wind power plants, as Sindh Chief Minister Syed Murad Ali Shah and Prince Mansour bin Mohammad bin Saad Al Saud, Chairman of the Saudi-Pak Joint Business Council, look on during a ceremony at the CM House on Thursday.

This was a clear governance failure at a time when the government has been heavily pushing foreign investment. They needed a clear win, but there was a small problem. While this entire saga was unfolding, someone else had quietly bought out Abraaj’s position in KE.

Enter Sheheryar Chishty

After Abraaj’s implosion, its ownership in K-Electric fell into the hands of liquidators managing a Cayman Islands-based fund known as the Infrastructure & Growth Capital Fund L.P. In 2022, Sheheryar Chishty, through his company AsiaPak Investments, purchased Abraaj’s share in KES Power via a special-purpose vehicle registered in the British Virgin Islands.

Chishty already had a presence in Pakistan’s infrastructure landscape, with holdings in Daewoo Pakistan and the Thar Coal-1 project. Buying into K-Electric was a high-stakes move, framed as both a vote of confidence in Pakistan and a business gamble.

But the acquisition was immediately met with resistance from K-Electric’s existing Gulf shareholders. They refused to recognize him as a legitimate partner, citing the absence of board elections that would reflect his stake. The resulting deadlock left Karachi’s main power supplier in limbo, with no clear leadership or strategic direction.

This publication has covered the entire saga every step of the way, chronicling how K-Electric, once considered a model for privatization, had become emblematic of state paralysis and corporate drift. As we noted then, governance issues were compounded by managerial controversies and slipping bill recovery rates, while the company failed to keep up with the rise of solar energy among residential users.

At the same time, Chishty was fighting a brutal legal battle to try and get control of the company, and eventually get his seats on the board so he could take the helm of KE. Unfortunately for Chishty, the old guard investors were not prepared to let go.

A government under pressure

By mid-2025, the ownership dispute had escalated into a diplomatic irritant. Saudi and Kuwaiti investors reportedly raised the issue directly with Pakistani officials, expressing frustration over regulatory obstacles and demanding that the matter be resolved.

Sources quoted by Tribune said the Saudis were particularly concerned about

Chishty’s acquisition, questioning the origin of funds and viewing his actions as a hostile takeover attempt.

The matter reached Riyadh during Prime Minister Shehbaz Sharif’s visit earlier this year. Soon after, the SIFC was tasked with finding a solution acceptable to all parties. The result was the deal signed in Karachi: Chishty’s exit, and Prince Mansour Bin Mohammed Al Saud’s entry as the new majority stakeholder in KES Power. To cement this, an MoU was signed between the CEOs of Trident Energy Pvt Ltd KE to establish hybrid solar and wind power plants.

Standing behind the two CEOs were Chief Minister of Sindh Murad Ali Shah and Prince Mansour bin Mohammad bin Saad Al Saud — who is also the Chairman of the Saudi-Pak Joint Business Council.

For the government, this outcome ticks several boxes. It makes long-standing Gulf partners happy, secures new Saudi investment, and restores a semblance of order to an essential utility. For Chishty, it marks the end of a turbulent two-year chapter and what can be considered a successful exit, even if a quick-out-the-door approach was not the one he initially entered the scene with.

What comes next

Saudi investors have been part of K-Electric’s story since privatization, but their role has mostly been passive.

For nearly two decades, Al-Jomaih Power Limited and Kuwait’s National Industries Group have held large stakes in KES Power, yet they have struggled to assert managerial control or reap consistent dividends.

Now, with a member of the Saudi royal family taking direct interest, that dynamic may change. The signing ceremony in Karachi was not just a formality. It was attended by senior officials, business leaders, and members of the Saudi delegation led by Prince Mansour Bin Mohammed Bin Saad Al Saud, who also chairs the Saudi-Pakistan Joint Business Council.

The prince outlined the Kingdom’s intent to deepen investments in Pakistan’s energy, mining, and tourism sectors. The message was clear: Riyadh sees K-Electric not as a legacy asset but as a gateway to broader economic integration with Pakistan.

For Pakistan’s policymakers, eager to attract capital under the SIFC framework, that message could not come at a better time.

The immediate effect of this settlement is a long-awaited resolution to uncertainty. With Saudi ownership consolidated, the company finally has a clear chain of command. That alone could unlock stalled decisions on tariffs, investments, and management appointments.

Still, the challenges facing K-Electric remain formidable. Its financial performance has deteriorated, bill recoveries are slipping, and the company has yet to adapt fully to the shift toward rooftop solar power. Corporate governance controversies have also tarnished its image.

This publication has previously examined these issues in detail, pointing to a management culture slow to respond to technological change and an ownership structure that blurred accountability.

For now, the focus returns to the boardroom. The company’s spokesperson told media persons that K-Electric has not yet received official communication from shareholders regarding the change, a reminder that even resolved disputes take time to translate into operational reality.

The broader signal

In diplomatic circles, the K-Electric agreement is being read as a test case for Pakistan’s investment diplomacy. After the fiasco of the Shanghai Electric withdrawal, Islamabad has been eager to project stability and reliability. The SIFC’s role in brokering the Saudi deal allows the government to claim a tangible success story.

But the episode also serves as a cautionary tale. The original Shanghai Electric bid was worth nearly $1.8 billion—a figure that dwarfs most foreign investments Pakistan receives annually. Losing it because of bureaucratic inertia was a costly mistake.

Now, the country has a second chance. Riyadh’s willingness to step in suggests confidence, but that confidence is conditional. The government will be expected to ensure regulatory predictability and efficient decision-making if it hopes to avoid another decade of paralysis.

For K-Electric’s employees and consumers, the headlines may not change much in the short term. Power shortages, billing disputes, and infrastructure gaps remain part of daily life in Karachi. But behind the scenes, a major shift has occurred.

The company that once symbolized Pakistan’s flirtation with global private equity is now poised to become the centerpiece of Saudi-Pakistani business cooperation. The investors who waited nearly twenty years for dividends are finally back in charge.

As one chapter closes, another begins—this time under the green and white of Pakistan and the deep green of Saudi Arabia. Whether this partnership can deliver the stability and performance that Karachi desperately needs remains to be seen.

What is certain is that the city’s electricity supplier, once again, sits at the intersection of politics, power, and profit. n

Sardar

Ahsan Rasheed Khan OPINION

Can our economic policymakers find a way to wargame?

For four decades, Pakistan has largely planned with spreadsheets, intuition, and press conferences. What we have not done at least not at scale is simulate policies before launch and then monitor whether promised results actually arrived. We built “monitoring cells” without monitoring systems. The result is short-term firefighting, long-term drift, and a data pipeline that too often fails the very ministries tasked with steering the economy. What I call “press conference economics”.

The price of flying blind

When a tariff is tweaked or a sales tax is nudged by 1%, the shock ripples through prices (CPI), jobs, exports, provincial revenues, and household welfare. Countries that treat the economy as a system run those “whatifs” through integrated models before acting, we usually don’t. Insiders at planning commission, Ministry of Finance will recognize the culture: ad-hoc “quick looks,” post-hoc justifications, and what one senior official described to me as “jhatka” fixes shocks meant to show action

The writer is an NDU alumni, Stanford GSB Lead 26, Sales Director at Oracle & a digital health innovator

rather than deliver measurable outcomes(a bureaucratic colloquialism not a method).

Meanwhile, the data itself hasn’t helped. The finance minister recently criticized the Pakistan Bureau of Statistics (PBS) for forcing policy to rely on outdated indicators concerns widely reported in the press. In parallel, the IMF has asked Pakistan to explain roughly $11 billion in trade-data discrepancies between two government systems over the last two fiscal years exactly the kind of problem a governed data fabric would surface and resolve faster. Dr. Aneel Salman’s “The Price of Statistical Silence” underscores the same point: inconsistent systems create large statistical gaps that corrode trust.

The same simulation logic

Our defence institutions have used computer-assisted war games for decades to rehearse decisions under uncertainty. Pakistan’s National War Gaming Centre (NDU) supports war games and operations planning, the U.S. Naval War College has institutionalized wargaming since 1887 and runs 50+ gaming events annually. The method is identical to what economic policy needs. Policymakers need to define objectives, generate scenarios, simulate moves and countermoves, observe outcomes, then update plans based on evidence not gut feel.

If wargaming helps armies avoid costly mistakes before battle, why wouldn’t we wargame our economy before rolling out a tariff, subsidy, or tax reform.

There are plenty of examples that Pakistan can borrow from. To understand how secure data backbones

are developed, for example, there is the UK’s Integrated Data Service and New Zealand’s Integrated Data Infrastructure which securely link tax, trade, labour and other datasets for cross-government analysis.

The OECD’s METRO (CGE) traces shocks through sectors and value chains exactly the “import => CPI/jobs/exports” linkage Pakistan needs. Even pedagogy related to this is mature. Business schools like Stanford GSB & MIT use management flight simulators (e.g., MIT Sloan’s Platform Wars) so leaders can practice strategy in complex systems the same mindset we need in public policy.

The stack Pakistan actually needs

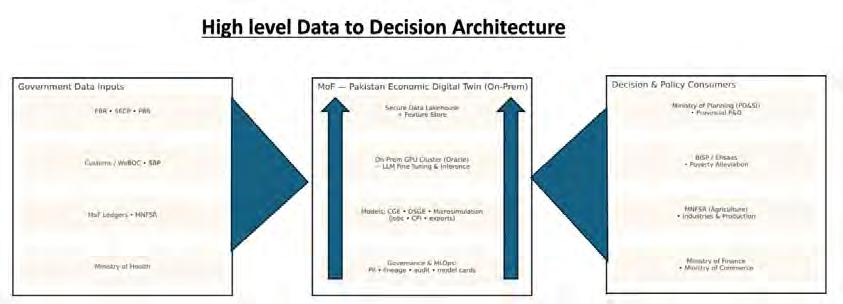

Roughly speaking, Pakistan’s economic planning needs the development of four distinct steps.

1. Live data fabric (governed): automated feeds from FBR, Customs/WeBOC, SECP, SBP, PBS, MoF ledgers, Health, MNFSR into a trusted environment with lineage, access controls, and audit. One “economic truth” analysts across ministries can query (and challenge).

2. Models at three layers:

l Macro (CGE/DSGE): quantify sector/ province impacts of tariffs, subsidies, energy price paths, exchange-rate scenarios.

l Micro (tax-benefit, labour): show distributional effects and improve BISP/Ehsaas targeting.

l LLM + retrieval: assistants that retrieve from governed data (no hallucinations), call the models, and return cited answers in Urdu/ English.

3. Decision workbench: what-if consoles where MoF, Planning, line ministries and provinces move policy sliders and see CPI, GVA, jobs, exports change before announcements.

4. Monitoring & ROI by design: tag every rupee in PSDP/ADP to ex-ante projections and ex-post outcomes, with drift alerts and public scorecards.

The PBS collecting data is not enough

The Pakistan Bureau of Statistics is essential in all of this. But what we must remember is that collection of data does not guarantee data based decision making. The real goal should not just be to collect data. Timeliness, validation and integration across agencies are vital. A digital twin forces the hard parts metadata, versioning, reconciliation, and a single source of truth so ministers see one dashboard, not five conflicting spreadsheets.

The frameworks already existed: input-output tables, macroeconometric models,

early CGE. Had we institutionalized simulation in the 1980s, we would have learned faster, avoided tariff whiplash, and targeted subsidies with more precision. Instead, we staffed monitoring teams without monitoring systems reporting activities, not ROI. In my Stanford coursework, simulations like Platform Wars highlighted dynamic complexity and how small policy changes compound over time. Pakistan’s policymaking still repeats precisely those errors.

The road ahead

So what comes next? Well, Pakistan’s policymakers can begin by following a pragmatic approach that phases in these changes over a period of a year to a year and a half. These phases could look something like this:

l Phase 1 Data & governance: Connect Customs/WeBOC, FBR, SECP, SBP, PBS, MoF into a secure lakehouse, publish a data dictionary and quality KPIs.

l Phase 2 Models & LLMs: Deploy a

baseline CGE calibrated to Pakistan tables i.e. plug in tax-benefit microsim, add an LLM that answers with retrieved, cited facts and can call the models. Computers can be on local, onprem GPUs (e.g., Oracle or equivalent NVIDIA providers) and hosted in a shared government-approved facility (e.g., upcoming Sky47 or Jazz Digital Park) to meet residency needs. (Disclosure: I work at Oracle and vendor names are illustrative, not endorsements).

l Phase 3 Policy pilots: Run three scenarios (e.g., fertilizer tariff relief, electricity price path, export-rebate redesign) and publish ex-ante vs. ex-post scorecards.

l Phase 4 Institutionalize: Embed model stewardship, code reviews, annual re-calibration, require simulation memos in ECNEC/ CDWP/PDWP submissions.

If we keep doing press-conference economics, we’ll keep getting press-conference results. If we build the simulation habit, we’ll finally have a policy with memory and a way to learn from it. n

As inflation slows, Security Papers’ revenues move at slower pace

The producer of banknotes in the country saw revenues climb 8% in fiscal year

Profit Report

Security Papers Limited (SEPL), the country’s specialist maker of banknote paper and other high-security substrates, closed fiscal year 2025 with an 8% rise in net sales and modest growth in earnings, underscoring both the company’s defensiveness and its growing exposure to Pakistan’s gradual shift away from cash. The manufacturer reported earnings per share of Rs25.72 for FY25, up slightly from Rs25.12 a year earlier, with fourth-quarter EPS at Rs7.14 versus Rs6.85 in the same period last year. Operating profit for the year rose 8% to Rs1,702 million as gross margins held steady at 28%.

The topline grew from Rs7,312 million to Rs7,871 million as the State’s demand for banknote paper and related security-grade products remained steady after two years of currency in circulation expanding rapidly during high inflation. But the cadence is clearly slower now. With headline inflation easing from last year’s peaks, the central driver of physical-cash demand – household and retail cash balances chasing rising prices – has cooled. For a company whose principal customer is the State’s banknote printing apparatus and whose revenues ultimately re-

flect the economy’s reliance on cash, this slow down matters.

SEPL’s business model has long been a mirror to how Pakistan pays, saves and transacts. When inflation is raging, currency in circulation tends to expand faster, banks load ATMs more frequently, and wear-andtear retires notes sooner – each of which pulls forward demand for fresh banknote paper. When inflation slows and digital alternatives – RTP rails, QR wallets, and card acceptance – chip away at cash’s share of transactions, that pull moderates. FY25’s results capture the inflection: growth, but at a reduced speed, and profitability that relies more on disciplined operations than on extraordinary volume. That is not to say demand has vanished. SEPL still produced roughly 3,500 tonnes of banknote paper in FY25, and management has signalled that FY26 will be a “transition year” during which inventory is run down as the company upgrades production. The centrepiece is a Rs3.4 billion capital investment to modernise Paper Machine-2 (PM-2) – a project already mobilised with a 15% advance from internal cash – so that future output can embed enhanced security features demanded by its principal client.

SEPL’s FY25 income statement reads like that of a disciplined, utility-adjacent

2025

supplier: steady revenue, tightly managed costs, and a small decline in dividend per share to Rs11.5 from Rs12.5 to conserve cash for capex. Net sales rose 8% year on year to Rs7,871 million; cost of sales grew at the same 8% pace to Rs5,667 million; and gross profit improved to Rs2,204 million, maintaining the 28% gross margin seen last year. Operating profit advanced in lockstep to Rs1,702 million, while EBITDA rose 9% to Rs1,956 million on higher depreciation associated with ongoing asset renewal. Fourth-quarter dynamics were similar: revenue up 2% to Rs2,045 million and operating profit up 7% to Rs483 million as the product mix skewed slightly richer, nudging quarterly gross margin to 30%.

The more consequential development sits off the P&L: the supply contract with Pakistan Security Printing Corporation (PSPC) – historically priced to deliver a 28% margin – concluded in June. Pricing is under renegotiation “in accordance with prevailing industry benchmarks”. Depending on where the parties land, the margin structure that has anchored SEPL’s economics could shift up or down a few percentage points – material for a business with a single dominant buyer and a narrow product set.

Against this backdrop, Pakistan’s payment mix is changing. The company’s

ability to make money is fundamentally tied to the lifecycle of physical cash: notes must be issued, handled, and eventually replaced. Lower inflation reduces churn; better banknote substrates lengthen circulating life; and every incremental digital transaction is one less note handled. None of this spells immediate obsolescence for banknote paper – cash remains deeply embedded in retail and informal trade –but it does cap the growth rate. FY25’s slower revenue expansion is an early data point for that thesis.

Security Papers Limited is a purpose-built enterprise: it exists to supply the sovereign (via PSPC) with secure paper for currency and other sensitive instruments. Over decades, the firm has built process know-how in fibre selection, watermarking, embedded threads, and surface treatments that deter counterfeiting and extend note life. The company is listed on the Pakistan Stock Exchange and treated by investors as a defensive industry: demand is anchored in sovereign operations, volumes track macro variables like inflation and currency in circulation, and pricing is shaped by negotiated contracts rather than purely by spot competition.

While the company’s early history is bound up with the State’s need to localise banknote supply, its modern arc has been one of gradual integration and periodic technology refreshes. PM-2’s planned upgrade is of a piece with that approach: a step-change in capability to meet the latest security spec, rather than an expansion in nameplate tonnage for its own sake. Management’s indication that FY26 will be used to “reduce inventory” reinforces the view that SEPL is prioritising mix and specification over sheer output tonnage, aligning manufacturing with client roadmaps for future note series and anti-counterfeit features.

SEPL’s portfolio centres on high-security paper, most critically banknote paper destined for PSPC. The hallmark is not the fibre alone but the multi-layered security embedded during papermaking: watermarks, security threads, windowed features, and chemical markers that perform under machine and manual verification. The PM-2 upgrade is explicitly targeted at enabling “enhanced security features” in future runs – a requirement now common in the global banknote industry as central banks fight increasingly sophisticated counterfeiting techniques.

The company reports only a limited requirement for cotton comber and sources most of it through imports, insulating it from domestic cotton shocks – including the recent flood-related disruptions in local supply. This raw-material posture reduces one of the classic volatility channels in Pakistani paper and textile manufacturing, where local cotton crop variability often whipsaws margins.

SEPL produced around 3,500 tonnes of banknote paper in FY25. The plant’s nearterm emphasis is on upgrading PM-2 and running down inventories in FY26 to smooth the transition. The capex – Rs3.4 billion – has been approved by shareholders and partly advanced from internal cash, signalling both balance-sheet capacity and urgency. For a niche, single-buyer supplier, this is a strategic investment: it preserves SEPL’s position as a qualified source for the next generation of Pakistani banknotes, where feature-sets (e.g., denser threads, optically variable elements, durable coatings) demand precise process control at high yields.

SEPL’s anchor relationship is with PSPC. The FY25 note that the legacy “28% margin” contract ended in June, and that new pricing will align with industry benchmarks, is the single most important commercial update this year. It suggests a pivot from administratively stable margins to potentially more market-referenced pricing, which could narrow or widen spreads depending on raw-material indices, energy costs, and peer benchmarks in comparable economies.

FY25’s Rs7,871 million net sales represent an 8% increase over Rs7,312 million in FY24. At face value, that is simply growth. Stripped to drivers, however, the number likely reflects a combination of (i) residual note-replacement demand after two inflationary years, (ii) modest price effect from input pass-throughs, and (iii) normalisation of production following earlier supply chain tightness. The 2% year-on-year growth in the fourth quarter implies momentum softened into year-end as inflation – and with it, currency-in-circulation-linked demand – receded.

Gross margin held at 28% for the full year, with a more favourable 30% print in 4QFY25. The steadiness suggests SEPL executed well on raw-material sourcing and energy cost control. Depreciation rose 13% to Rs254 million, consistent with recent capital works; EBITDA margin ticked up, with EBITDA reaching Rs1,956 million (up 9%). These are robust numbers for a manufacturer in a high-energy-cost country and owe much to the contractual nature of pricing and the limited competition in SEPL’s niche.

PSPC pricing. The previous framework yielded a 28% margin; if the new benchmarked pricing were to tighten, SEPL would need to defend unit economics through yield improvements and lower waste, or through mix that favours higher-spec banknote series. Conversely, if inflation’s long-term trend down supports fewer note issues per year, the pricing formula may need to preserve margin on lower volumes to sustain domestic capability. Either way, the FY26 “transition year” suggests the company is engineering its

production plan and inventory to that negotiation timeline.

On raw materials, management notes only a “limited requirement for cotton comber”, largely imported, and therefore not materially affected by flood-hit domestic cotton supply in 2025. This is a meaningful insulation from a classic Pakistan risk factor and helps explain the margin stability this year despite agricultural shocks. Energy remains a separate, non-trivial cost driver, but the steady gross margin implies either reasonable passthroughs or efficiency offsets.

SEPL’s near-term priorities are clear: complete the PM-2 upgrade on time and on budget; manage the PSPC renegotiation to a sustainable benchmarked price; and use FY26 to recalibrate inventories and product mix for a next-generation banknote specification. Each of these is within management’s control. The less controllable variable is the payments landscape. Pakistan remains a cashheavy economy by international standards, but digitisation is compounding: real-time rails broaden acceptance; government-to-person payments digitalise; and retail QR adoption expands. As this continues, the lifecycle demand for banknotes grows more slowly than nominal GDP. SEPL’s response – investing in higher-security, longer-life note paper and running a lean balance sheet – aims to protect margins even if total note-paper tonnage plateaus.

There are also hedges the company could consider over time. Globally, security-paper makers have diversified into passports, identity documents, tax stamps, and certificates. The skills are transferable: embedded features, substrate chemistry, and precision process control. SEPL’s disclosure for FY25 does not detail such expansions, but the PM-2 upgrade is a platform on which adjacent products could, in principle, be developed if domestic demand or policy opens space. For now, however, the business remains tightly focused on Pakistan’s banknote paper requirements.

FY25 shows a franchise in good operational health, modestly growing revenues in a slower-inflation environment, and maintaining enviable margins while stepping up investment for the next security-feature cycle. The stock’s appeal to investors rests on three pillars: (i) visibility of sovereign-linked demand; (ii) low leverage and strong cash generation; and (iii) a credible capex plan tied to clear client specifications rather than speculative capacity. The key watch-items for FY26 will be the PSPC pricing outcome, progress on PM2, and evidence that SEPL is successfully managing a cash-lite future – by extracting more value per tonne through enhanced features and by keeping the cost base disciplined as volumes normalise. Of all three, FY25 provides reasons for cautious confidence. n

Hubco reaffirms 2026 date for BYD assembly in Pakistan

The energy company is reinventing itself as an electrical vehicle manufacturer, even as its legacy energy contracts struggle

Profit Report

The Hub Power Company Limited (Hubco) has doubled down on its plan to assemble BYD vehicles in Pakistan by late 2026, and is building the charging backbone to make those cars usable on long-distance routes. In a management briefing with investors, the company confirmed the completely knocked-down (CKD) plant is slated to come online in the fourth quarter of fiscal 2026 and disclosed it has already spent about $10 million, with debt drawdowns in place and equity provisioned internally. At the same time, Hubco is laying out an electric-vehicle charging network along highways every 100 kilometres, to be co-owned with fuel retailers, even as it wrestles with regulatory and receivables issues that continue to dog its legacy power portfolio.

The push into electric mobility marks a sharp strategic turn for Pakistan’s largest independent power producer. But it is also a hedge. As power offtake contracts face tariff true-ups, late-payment disputes and policy overhangs, the economics of auto assembly –especially if supported by pro-EV taxation and rising consumer interest – offer a new earnings stream. The company says initial reaction to BYD’s Shark model has been “very encouraging”, a signal that it intends to marry brand equity with local manufacturing and after-sales reach when the factory starts to roll.

Hubco’s auto strategy is not just about putting a logo on a bonnet; it is about assembling vehicles and removing the “range anxiety” barrier that keeps many Pakistani buyers on the fence.

Management reiterated that the BYD CKD facility is targeted for commissioning in the fourth quarter of FY26. The company has already incurred roughly $10 million of capital expenditure and has $90 million in debt drawn, with about $30 million in equity to be funded from internal cash generation. The heavier equipment outlays will follow once letters of credit open for the engineering, procurement and construction (EPC) contract. In other words, the build-out is funded and

sequenced, not just aspirational.

The early market response to BYD’s Shark has been “very encouraging”, according to the company, which is critical in a market where consumers weigh brand novelty against concerns over resale and service. Positive reception gives Hubco and BYD the confidence to tool the plant for meaningful volumes rather than a token presence.

On the policy side, the company notes that sales tax on EV CKD and CBU (completely built-up) units is 1%, a generous concession that improves pricing headroom at launch. For a new entrant, keeping showroom prices tight without sacrificing margins is vital; a low indirect tax wedge helps.

Hubco is also working on electric-vehicle charging stations (EVCS) to make intercity travel viable. The plan is simple and pragmatic: partner with OMCs (oil marketing companies), co-own the charging sites through HUBC Green, and split profits 50:50. The initial capital expenditure is modest – about Rs400 million – and focused on safety and reliability rather than bells and whistles. The company is prioritising chargers at 100-kilome-

tre intervals along highways and motorways, accepts that utilisation will be low at first, and expects it to build gradually as vehicles enter the parc. This is the right order of operations: seed the network, then scale as cars arrive.