11 Google’s AI now available in rupee priced subscriptions in Pakistan

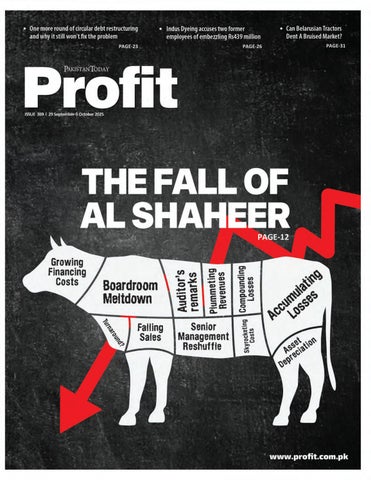

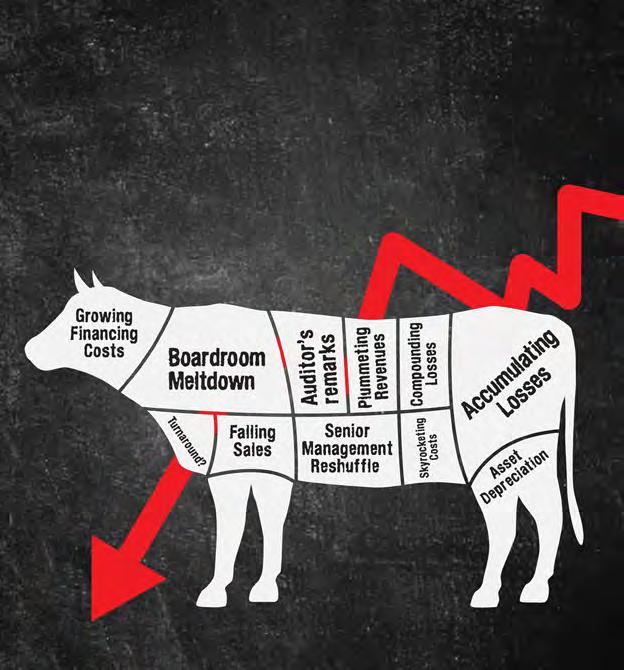

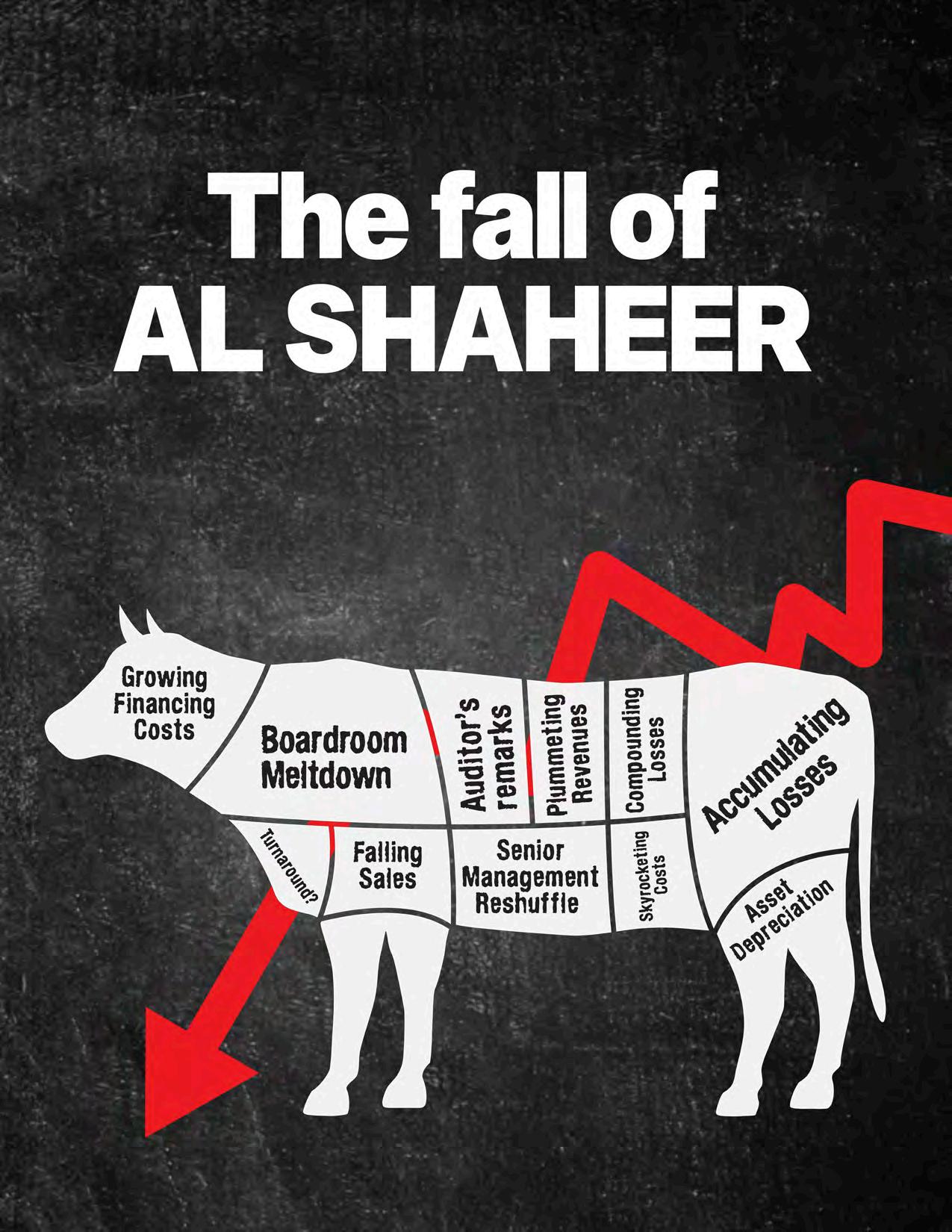

12 The fall of Al Shaheer

18 Sapphire to merge two of its listed textile companies

20 Cement sector profits up 38% in fiscal 2025

22 K-Electric to shut down major portion of power generation capacity

23 Can Pakistan’s rising corp of investment influencers do the trick?

26 Indus Dyeing accuses two former employees of embezzling Rs439 million

29 Pakistan’s high-stakes crypto experiment Maha Shah

31 Can Belarusian Tractors Dent A Bruised Market?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Google’s AI now available in rupee priced subscriptions in Pakistan

The Mountain View-based giant is the only one of the major LLM model players to offer its services directly to Pakistanis in their own currency for premium tiers of service

Profit Report

Google has switched on rupee priced subscriptions for its consumer AI in Pakistan, lowering a long standing payments barrier for millions of users who do not hold international enabled credit cards. The company’s new Google AI Plus plan – part of the Google One family – has been rolled out to Pakistan as one of 40 new markets, with pricing set locally and benefits bundled into a single package. For a market where international recurring card payments often fail, the simple fact that billing happens in rupees could be as important as any headline feature.

Google announced on September 24 that AI Plus is priced at around Rs1,400 per month, with an introductory 50% discount for the first six months. The bundle includes higher limits in the Gemini app, access to Gemini 2.5 Pro, Veo 3 Fast for video generation, integration of Gemini in Gmail/Docs/Sheets, 200GB of Google One storage, and family sharing for up to five members. Google’s official announcement doesn’t fix a single global price – “price varies by country” – but it confirms Pakistan is in the new cohort, which is consistent with the rupee figures reported locally.

The rupee billing sits on top of Google’s existing payments rails in Pakistan, where Google One storage plans have long displayed prices in PKR – evidence that local currency processing is the default rather than the exception in Google’s consumer subscriptions

here. That context matters, because it hints the AI plan should be payable with the same locally issued cards that already work for Google One.

By contrast, most competing premium AI assistants in Pakistan still quote and bill in US dollars. OpenAI’s ChatGPT Plus is $20 per month – and while accessible in Pakistan, many users run into card acceptance issues because their banks block international recurring payments or the processor rejects locally issued cards. Microsoft’s Copilot Pro is likewise $20 per user per month. Anthropic’s Claude Pro launched at $20 (US) or £18 (UK) and, outside supported sterling markets, is generally priced in foreign currency. For Pakistani consumers, that means exposure to FX swings and higher friction at checkout.

The payments hurdle isn’t theoretical. Local guides routinely explain workarounds – from virtual cards to third party gateways –precisely because many domestic cards fail on USD subscriptions and international recurring charges. Those workarounds add cost and complexity; a native PKR checkout does not.

Viewed through a commercial lens, Google has combined three levers that could shift share quickly: (1) rupee pricing (lower friction, no FX anxiety), (2) introductory discounting (which compresses the headline cost gap with free tiers and trials) and (3) bundled value – notably storage and family sharing – that makes the plan feel like more than just a chatbot. In a market where ARPU is sensitive and FX volatility is real, those choices give Google a tangible go to market advantage: the first

premium LLM subscription most Pakistani households can buy and share without juggling foreign cards or rates.

The move also echoes tactics in other price sensitive, high growth markets. In India, for example, Perplexity has pursued distribution through local partnerships – most prominently with Bharti Airtel, which is offering a year of Perplexity Pro at no charge (marketed as ₹17,000 of value) to its 360 million users. That is a different mechanism – carrier bundling rather than local currency billing – but the strategic aim is similar: remove friction at the point of purchase and seed habitual use among mainstream consumers.

Two questions will determine whether Google converts early sign ups into durable share. First, price sustainability: the company says pricing varies by country, and local press highlights a time limited 50% discount; if the plan reverts to the full PKR price too quickly, churn could follow. Second, feature parity: rivals like OpenAI and Microsoft continue to add capabilities to their premium tiers; if Pakistani users perceive gaps in reasoning performance, enterprise interoperability or creative tools, they may keep a free account elsewhere and pay only when must have features arrive. For now, though, Google has an opening: it is the only major LLM provider with a mainstream, rupee priced subscription that ordinary Pakistani cards are likely to accept, and it is pairing that with a bundle families can actually share. In a market where payments friction has held back upgrades, that combination could be decisive. n

The company that practically invented Pakistan’s meat export industry is on life support as its new investors Sunridge work to bring the defunct meat manufacturer back to life

By Zain Naeem

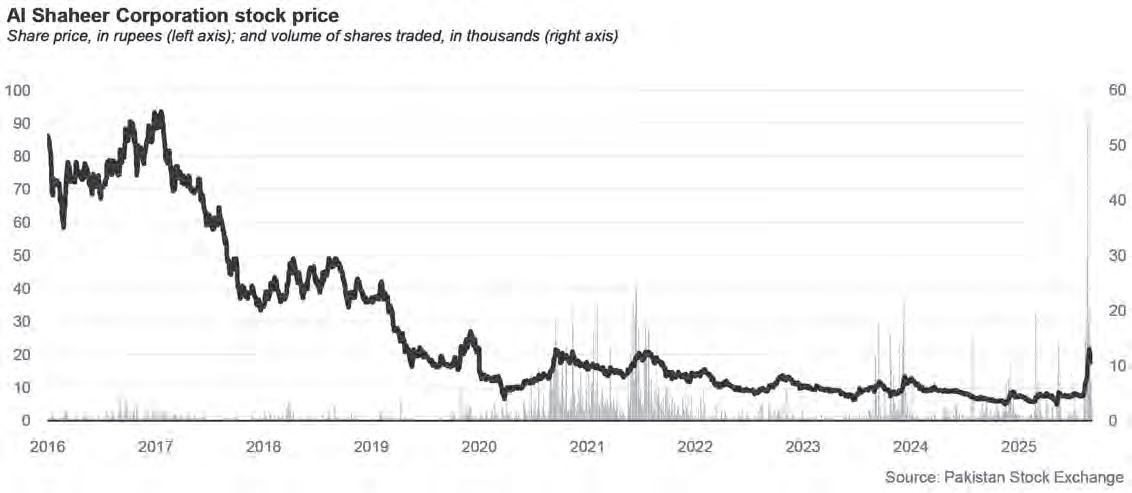

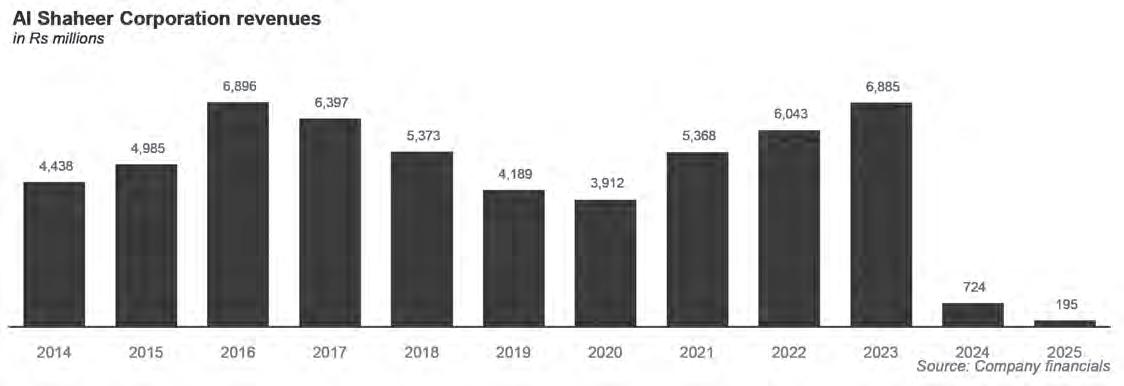

Let’s turn back the clock to 2016. Al Shaheer Corporation has just experienced its best year. Revenues for the company have come to around Rs6.9 billion and earnings per share registered are around Rs3 per share. The market seems to be buoyed by the performance and is valuing the shares at around Rs100. To some it might seem like the stock is being overvalued as it is trading at a multiple of more than 33 times trailing 12 month earnings. However, the company seems to be going strength to strength by registering one great year after another. From 2008 to 2016, the revenues of the company have been on an upward trajectory.

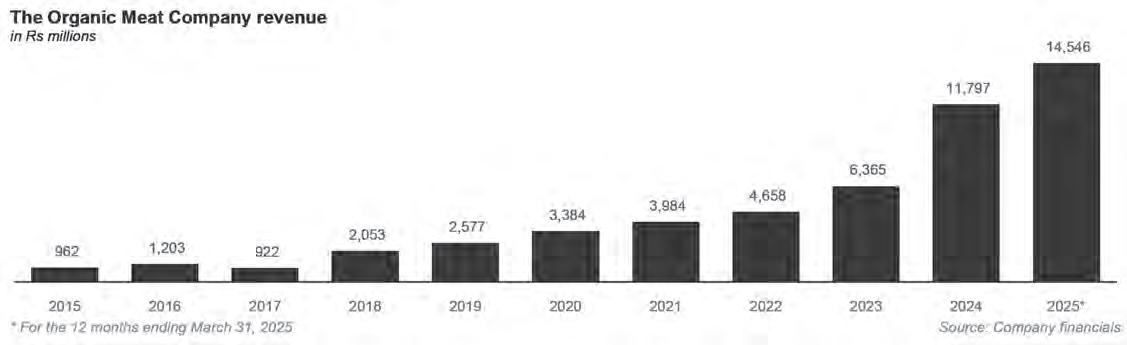

The market is giving a stamp of approval to the stock which was listed at Rs95 per share and it seemed like the company was expected to match the expectations with reality in the near future. Going from a simple partnership in 2008, the company looked to grow by expanding its footprint locally and internationally. To a certain extent, it can be said that Al Shaheer walked so companies like The Organic Meat Company could run. The success of Al Shaheer can be gauged by the fact that it gave out bonus shares in 2015 and 2016 after profitable results.

Ten years on and Al Shaheer is a mere shadow of itself. The company went from one disaster to another and the recent publication of its financial statements show that the downfall is still ongoing. A revolving board room door, losses accumulating over time and auditors passing adverse opinions, it seems like there is still some time before rock

bottom is reached. While companies like The Organic Meat Company reach new heights, Al Shaheer has to deal with its deepening issues before the rot sets in.

The promise that was made in 2016 seems to be dissipating fast. The most recent development has been a dramatic change in the board room and senior management. The baton has now been passed to Sunridge to make the company viable and functional. Sunridge became a substantial shareholder in the company in September of 2023 and is now looking to carry out the necessary changes to turn the company around. Will the gamble pay off for Sunridge and Al Shaheer? All remains to be seen.

The beginnings of Al Shaheer

In 2008, Al Shaheer started out as a partnership. The company was the brain child of Kamran Ahmed Khalili who wanted to turn his business into an international phenomenon. It was small in size but big in ambition. The goal of its original backers was to exploit the opportunity that was present to it to expand their business locally and internationally. The company was going to be involved in distribution, marketing and sale of meat products. The success of the company can be seen from the fact that as early as 2013, the owners were looking to list the company on the stock exchange.

In order to get listed, the company had to disclose its financial performance. As far back as 2014, it was seen that the company was earning revenues in excess of Rs4 billion and there was always a potential that these revenues could be maximised further. The

listing finally took place in 2015 and was carried out to generate funds which could be used to increase the size of operations.

Going from a private limited company to a publicly listed one, the company was looking to increase the exposure of its brand name in the corporate world. This would compliment the fact that the company was becoming a household name as well. The retail footprint of Al Shaheer was growing as it established Meat One which became a brand renowned for selling fresh meat in the market. Slowly, the customer base of the company started to expand into the Middle East as well.

What had started off as a strictly meat business went into a range of ready to cook products. The constant need to improve operations led to the HACCP certification being sought, making sure that the meat being produced was of top quality and free from external contamination. The persistence with quality led to the abattoirs being certified by international bodies for higher quality assurances. Al Shaheer was now producing high quality products which were being bought locally and internationally.

The journey of the company led to establishment of Meat One, Khaas and Al Shaheer farms under the umbrella of Al Shaheer. Meat One and Khaas were associated with providing retail based solutions to clients of all sizes. By 2015, farming business was also set up in order to carry out vertical integration which would allow a consistent source of livestock. The system in place was archaic and the company wanted to gain greater control over a source of high yielding animals who could guarantee quality.

According to its financials, the compa-

ny exported meat worth $45 million in 2015 and there was an expectation that China and Russia could become the next market where Al Shaheet could market itself. The listing would provide a cheap source of financing to the company. The listing was carried out at a price of Rs95 per share and a bonus share of 35% in 2015 and 15% in 2016 shows how well the company was performing during this period.

Once the prices are corrected for these bonuses, it can be seen that the stock price stayed above Rs80 long into 2016 when things were looking good for the meat exporter. From 2014 to 2016, the trajectory of the profits remained upwards as the earning per share went from Rs1.3 in 2014 to Rs3 in 2016.

Things start to turn

Even before the financial performance started to suffer, the initial listing price meant that many of the investors felt that they had invested into a stock which was overvalued to say the least. With a price of Rs95 being set, the market was expecting the results to be much better than the ones that had been seen in the past. Even with results improving year on year, there was a huge premium that was being paid to buy a share of Al Shaheer when other stocks were giving a much better return in comparison. Once the trading started, the profits were able to sustain the market price, however, once things took a turn, the price started to suffer the most.

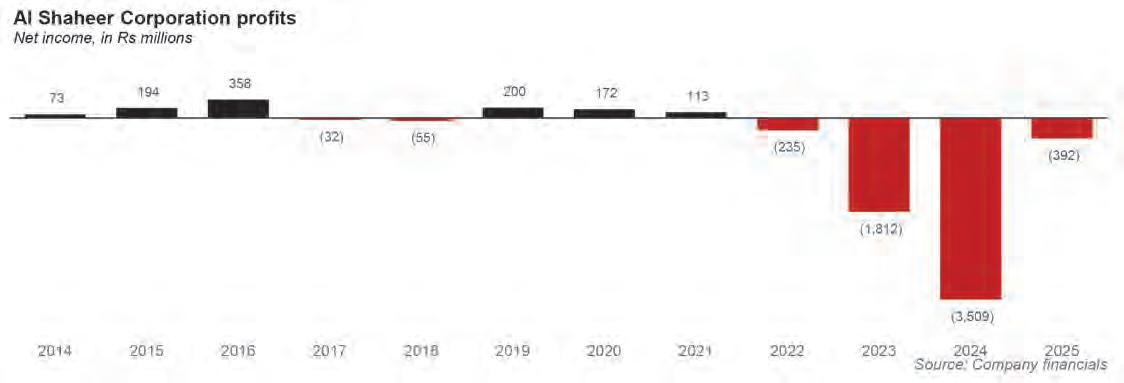

2017 was the year where things started to see a downturn. The revenues were still strong as Al Shaheer was able to make revenues of Rs6.4 billion. As gross profits shrank from Rs1.8 billion to Rs1.5 billion, the operating profit took a serious hit falling from Rs319 million to only Rs43 million. With mounting finance costs and decreasing income from other sources, this was the first time that Al Shaheer saw losses of Rs32 million and loss

per share of Rs0.19. Just a year ago, these had been profits of Rs357 million.

As sales began to fall, this problem became compounded with losses increasing to almost Rs55 million in 2018. The falling gross profits and increasing costs led to losses being suffered consistently. There was a rebound in profits in 2019, 2020 and 2021. Even though sales were falling during this period, Al Shaheer recognized income from other sources which were able to turn losses into profits.

Even when profits were being seen, the real issue at the company was that it was seeing falling gross margins and profits. Once these losses started to grow, the company could not run away from the fact that it was facing a huge crisis. With increasing finance costs and falling profits, the end was inevitable as losses became a mainstay throughout 2022 and 2023. 2023 was such a disastrous year that even in the face of Rs6.8 billion of revenues, the losses recorded were around Rs1.8 billion. These losses had been cushioned by exchange gains that Al Shaheer was able to enjoy due to depreciating rupee, however, the magnitude of losses showed that things were slipping out of Al Shaheer’s hands.

Some of the downturn was attributed to the pandemic which struck in 2020. 80% of the revenues earned by Al Shaheer came from exports. As exports fell in 2020, they only accounted for 45% of its sales which led to lower revenues and higher costs. Another factor for the losses was that the gross margins of the company were shrinking. These had started from 16% in 2015 and were hovering around 9% by 2023. As the direct costs started to increase, less could be retained to cover other expenses.

One of the biggest expenses that had been recognized by Al Shaheer was of Rs1.2 billion which had been in relation to provision for doubtful debts. In the past, around 5% of total debts were considered to be bad against which a provision had been made.

In 2023, the rules around these changed as IFRS 9 mandated for expected credit loss to be realized. Having trade debts of Rs3 billion, around 40% was considered to be the expected credit loss and accordingly a provision was created under the new standards.

The new standards had been introduced to consider any such losses beforehand which meant that the trade debts were considered bad and had to be written off. The writing off of these debts led to losses being realized. It was pretty obvious that on a financial front, the company was losing huge amounts of money. In order to support the company, injection of capital was carried out three times in the form of right share issues to make sure the company had ample working capital which was being wiped out by the losses.

This was the development on the financial front from 2015 to 2023. However, there was something else going on at the company as well which was compounding its issues.

The board room meltdown

When the company had been listed, it had 8 directors which included Kamran Ahmed Khalili, the Chief Executive Officer and the chairman of the board. Khalili was the man who had built the company to what it was. Before setting up the company, Kamran was a member of the Karachi stock exchange and ran Fortune Securities.

The initial board had him with Muhammad Ai Ghulam Muhammad, Noor ur Rahman Abid, M Qaysar Alam, Rukhsana Asghar, Rizwan Jamil, Adeeb Ahmed and Naveed Godil. The board had differing members who had worked at local and international firms and brought their experience and skills to Al Shaheer.

After the most recent elections, the

board had Kamran Ahmed Khalili, Zilay A Nawab, Qaysar Alam, Adeeb Ahmed, Sabeen Fazli Alavi, Zubair Haider and Umair Khalili as its members. The changes seen at the board are mandated as the company changes over time and new members keep getting added to its boards once the older members choose to retire and leave.

These elections were held in November of 2022.

What raised concerns was the fact that from November 2022 to June 2024, the board went through a huge upheaval. During this time, Adeeb Ahmed and Zubair Haider left the board to be replaced by Babar Sultan and Imtiaz Jameel. In December of 2023, the CEO sold 10 million shares while Babar Sultan and Sabeen Fazli also left the board. The new vacancies were filled by Amir Shehzad and Muhammad Altaf. The shares sold by Khalili had been bought by Amir Shehzad.

The company secretary was replaced in January of 2024 while Kamran Khalili and Umer Ahmed Khalili ended up selling 10 million more shares each. Developments started to gain pace as the CEO announced his resignation from the company and the board was asked to choose a new CEO in due time. Both Kamran Khalili and Umer Khalili announced that they would be resigning from the board in February 2024 and were replaced by Muhammad Haris and Muhammad Idrees.

The merry-go-round did not stop as newly appointed directors Muhammad Altaf and Amir Shehzad resigned from the board in February of 2024 just two months after becoming directors. By May, the newly appointed company secretary, Muhammad Tariq Nabeel Jafferi also chose to resign and was replaced by Mubasshar Asif. By June end of 2024, Imtiaz Jaleel, Zillay Nawab and Qaysar Alam had also resigned and there was no announcement on who would replace them.

In October of 2024, the remaining board and the company secretary chose to resign

meaning there was no board member at the company or any person to handle the corporate affairs.

With the board room and financial results in turmoil, the corporate affairs of the company started to suffer as well. The last accounts that had been filed by the company were for June 2023 which were released in November of 2023. Since then, the quarterly accounts for September 2023 were filed in December of 2023. Since then, there has been no such development at the corporate front. There was an attempt to get an extension from the Securities and Exchange Commission of Pakistan to file the results for December 2023 which was rejected.

The company had been fighting on three fronts and losing them all miserably.

Enter Sunridge (Pvt) Limited

While these developments were going on at Al Shaheer, something else was going on in the background. In September of 2023, it was announced that Sunridge (Private) Limited, a wholly owned subsidiary of Unity Foods Limited had acquired 18.4% shares of Al Shaheer. The latest development was that it had bought 37 million shares bringing its holding to 69 million shares in the company. It is difficult to ascertain when the initial investment had started and from whom these shares had been bought. What was obvious was that as soon as the 10% threshold had been crossed, it had to be declared to the market which had been done in September 2023.

Based on the increase in shareholding, the board room started to go through changes that had not been seen in the past. A majority of the board who had been elected started to leave the company and the founders of the company were seen selling their shares and liquidating their investment. By June 2024, only

2 members were part of the board and things were looking bleak in terms of profitability.

Even Sunridge ended up selling 10 million shares that it held in July of 2024 decreasing their investment to only 15.75% of the shareholding. By October, there was no board to talk of and something drastic had to happen. Based on its shareholding being more than 10%, Sunridge asked for fresh elections to be carried out which would allow a new board to be elected. According to Section 133 of Companies Act 2017, Sunridge could call an Extraordinary General Meeting (EOGM) in which they could set the agenda by themselves.

There is a need to understand the perspective of Sunridge at this point. Sunridge had bought shares in Al Shaheer at a time when they thought that the old management had the skills and abilities to bring back the good days back to the company. When this vision did not materialize, they started to see that their investment was losing value. The best course of action available to them was to rationalize its investments and try to manufacture something different.

This is the time when Sunridge started to carry out large scale changes at the top. After the EOGM was called, the agenda was released which asked for individuals to send in their interest if they wanted to be elected on the board. The meeting to be held on 17th of December would see these elections being conducted which would elect seven directors to the new board. The new board would have one female director, two independent directors and four other directors. After the elections were held, seven directors were elected. These directors were Maria Khurshid, Ammar Junaid, Naeem Ashraf, Muhammad Taha, Mian Muhammad Shahzad Mazhar, Quarulain Asghar and Haris Mansuri.

Among these, Ms. Quratulain Asghar and Haris Mansuri were two individuals who were currently working at Unity which

was the parent company of Sunridge. The remaining were either independent or filled the quota as a female director.

The two individuals who had been elected were senior manager finance and assistant manager payables at Unity when they were elected. As the new board came into place, Quratulain Asghar was chosen as the chairperson of the board while Mubashar Asif became the new company secretary. This was followed by the board committees being constituted and Ghulam Farooq and Farhan Iqbal came in as the new Chief Executive Officer and Chief Financial Officer.

It feels like the earlier two directors who were appointed were placeholders who were made part of the elections to help the board appoint the new CEO and CFO. Once these two were appointed, the elected directors made way for the new senior management.

Ghulam Farooq was the Deputy Chief Executive Officer at Unity and Farhan Iqbal was the head of Finance at Unity.

Sunridge had invested a large amount in Al Shaheer and it could be seen that the company was not being run to its liking. The company had been started by Kamran Khalili in 2008, however, after 15 years, it seemed like Al Shaheer was being run into the ground. When Sunridge made their investment, they saw value within the company which needed to be extracted. As it owned a sixth of the company, the management at Sunridge felt that they could do a better job.

In line with this, they saw the old board leave and started to constitute a board which would be willing to put into action a plan that could help the company recover. From September 2023 to July of 2025, the senior management and the board of directors went through huge changes as Sunridge brought in people it thought could carry out the turnaround.

By this time, Al Shaheer was a company in the non-compliant segment of the stock

market and there was little value that could be seen in terms of positive news for the company. Even if Sunridge wanted to divest their investment, they had to make sure that the company was seen as a profitable investment by the next interested buyer. In order to bring it to that point, changes had to be carried out which allowed it to do so.

Al Shaheer after the changes

The new management had grand designs in their mind relating to where to take the company. The first order of business, after putting together a corporate governance structure, was to fix the non-compliances that existed at the company in relation to its corporate governance issues. There was also a business operations plan which was being formulated to take the company forward.

By July 2025, Al Shaheer saw more directors leaving as Quratulain Asghar, Naeem Ashraf and Muhammad Haris chose to leave the board and Ghulam Farooq, Farhan Iqbal and Imran Younus chose to become the new board members. In this case, two of the independent directors were leaving while Imran Younus came as the only independent director. The same day, another notification came that Mian Muhammad Shehzad Mazhar, Muhammad Taha and Maria Khurshid had also left to be replaced by Tasneem Ashraf, Arshad Shehzad and Adbullah Khan.

Abdullah Khan was made part of the board while he was the Chief Financial Officer at Unity as well.

Four days later, Arshad Shehzad also withdrew his consent to be a director and was replaced by Muhammad Ayub Khan Durrani. Less than a year later, the elected board had only Ammar Junaid while the remaining ones had been replaced by new members. It seems like the revolving door at the board room has persisted as directors keep resigning. Right now, there are three board members at Al

Shaheer who are also linked to Unity which shows that they are able to control the agenda and operations of the company. To some extent, this makes sense as Sunridge would want to drive the agenda of the board in the direction that they deem to be better for the company.

What has happened here is that with an ownership of 16% of the company, the board of directors and senior management has been appointed or brought in which is willing to take a chance and help Al Shaheer get back on its own feet. The board includes 3 individuals who are part of Unity currently while the senior management is also working at Unity simultaneously.

An additional point to note here is that the new management has been able to convince the remaining 84% of the shareholders to go along with the operational plan that the new management has devised and feel that the new direction will end up bearing fruit. Even though Sunridge has a sixth of the shareholding, the remaining shareholders have to be brought on board to carry out such large scale changes at the company and it feels like they have the blessing of the remaining shareholders to do so.

Financial situation

As the new board is appointed, the focus turns to addressing the corporate non-compliances that the company faced. The financial accounts had not been released since September of 2023 and a board meeting was called to review and approve all the accounts from 2023 to June of 2025. The accounts shine a light on the challenge that the new management faces.

In 2024, Al Shaheer saw its revenues plummet from Rs6.8 billion in 2023 to just Rs724 million in 2024. This was a huge fall while the cost of sales only fell from Rs6.3 billion to Rs1.4 billion. This led to the company making a gross loss almost equal to its sales. With another huge write off of trade

debts amounting to Rs1.9 billion, Al Shaheer saw losses of Rs3.5 billion after taxes. This equated to loss per share of Rs9.36 which had been Rs5.53 in 2023. It was evident to see that while sales were falling, the company kept recording more expected credit losses which were accumulating its losses.

Al Shaheer also saw its fixed assets fall due to depreciation and wastage of its property plant and equipment during the year. It wrote off Rs3.6 billion worth of trade debts, loans and inventory as it was looking to clear its balance sheet of assets it did not presume to be of any value. With liabilities not falling with the same magnitude, the accumulated losses went from Rs936 million to Rs4.4 billion in a space of a year. Things were deteriorating fast at the company and the downward slide was still in progress.

Revenues kept falling in 2025 as sales further decreased from Rs724 million to Rs195 million in 2025. The company still saw a high amount of cost of sales which was mainly attributed to the depreciation of its property, plant and equipment. The one bright spot was that many of the expenses were decreasing and no credit losses were realized leading to a net loss of Rs392 million compared to Rs3.5 billion a year ago. The loss per share fell from Rs9.36 per share in 2024 to Rs1.05 in 2025.

On the balance sheet, property kept seeing deterioration as it lost some value. The company was able to extend new loans to suppliers which it could afford to do by using some of its trade payables in order to finance it. As losses kept accumulating, the accumulated losses stood at Rs4.8 billion at the end of the year 2025.

The auditors chime in

With losses accumulating to such a degree, the last thing the management needed was for something adverse to take place and that is exactly what happened. The auditors presented their own views on the status of the company by stating that as

the company was facing financial, operational and regulatory challenges, there were serious concerns that needed to be addressed. The auditors stated that breaches of covenants and terms in relation to financing facilities had occurred as Al Shaheer had defaulted on its short term borrowings. In addition to that, it was facing frozen bank accounts, ongoing legal proceedings and regulatory investigations, non-realization of export receivables and placement on the non-compliance segment at the stock exchange.

In response to this, the board stated that they had started to address the non-compliances of the regulator and the exchange, completed the pending audits and was liaising with parties in order to resolve all the outstanding issues.

In addition to that, the auditors raised concerns over the figures that were being disclosed in the accounts as they felt that many of the items could not be verified and the authenticity of these items was questionable to say the least. Basically what the auditors were saying could be considered a huge shrug on their part for the veracity of the accounts they had been tasked to audit.

So up till now we have seen that the exodus in the board room has been addressed on a temporary basis but the issues still exist as the directors keep resigning on their own accord. The accounts that had not been released have finally seen the light of day, however, their accuracy has a huge asterix next to them. So what about the operations at the company and how they have been restarted?

On 8th of September 2025, the company disclosed to the market that the regulator has removed the caution that had been placed with their bank accounts which shows that their compliance is coming in line. There was an active effort by the company to settle its agreements with financial institutions which was being rescheduled and restructured to help the company for long term operational sustainability. The plant has also become operational after a long hiatus and both its

manufacturing facilities are coming online which will help the company in the future.

While there are good developments taking place, there are still some bad things that have come to light. The Adjudication Court of the State Bank of Pakistan has concluded the proceedings that were ongoing against the company in relation to non-repatriation of its export proceeds. It has been disseminated that the old management at the company was not repatriating the proceeds it was earning back to the country which was being investigated.

The new management was of the opinion that they were not responsible when the repatriation was supposed to be carried out. The Court felt that the responsibility was with the company and its former CEO imposing a penalty of Rs7 million on the company and Rs5 million on the former CEO. The new management has planned to get legal advice on this issue and then take appropriate action in response.

The impact the new management will have can only be judged once the performance of the new financial year starts to come from September 2025. It is evident that there are deep rooted issues present at the company at operational, financial and regulatory levels that need to be addressed before any substantial change can be seen. Revenues need to be restarted, costs need to be addressed and profits need to be earned to allow the company to get back on its feet.

As the new management grapples with these issues, it has to be stressed that the Al Shaheer is suffering through some tough times and a turnaround needs to take place sooner rather than later. With Sunridge now safely residing over the new looking management and board, it needs to show results which can justify its investment and subsequent takeover of Al Shaheer. Even if Sunridge feels that they need to divest from their investment, they need to bring the operational, financial and regulatory affairs into order before they can even think of selling off their investment. n

Sapphire to merge two of its listed textile companies

The textile giant is making the move at a time of considerable stress within its industry

Profit Report

Sapphire Group is combining two of its listed textile vehicles, moving to fold Reliance Cotton Spinning Mills Ltd (RCSML) into Sapphire Fibres Ltd (SFL) through a court sanctioned scheme of arrangement. In coordinated notices to the Pakistan Stock Exchange (PSX), the two companies said their boards have approved a “Scheme of Compromises, Arrangement and Reconstruction” under Sections 279–283 read with Section 285 of the Companies Act, with the Honourable High Court of Sindh to supervise and sanction the process.

The structure is straightforward: RCSML will merge with and into SFL, and SFL shares will be issued to RCSML’s registered shareholders against a swap ratio to be certified/determined by M/s Shinewing Hameed Chaudhri & Co., Chartered Accountants. Upon effectiveness of the court’s order, RCSML will stand dissolved without winding up. The companies added that the full text of the scheme will be circulated to shareholders and the PSX in due

course as directed by the court.

The pair of disclosures underscores that the merger is contingent on the fulfilment of corporate, regulatory and legal formalities as well as the court’s sanction – standard steps for such transactions. The notices instruct the exchange to inform TREC holders and make clear that shareholder communications will follow once the court issues directions on circulation. While the swap ratio has not yet been published, naming the valuer – Shinewing Hameed Chaudhri & Co. – sets expectations for an independent determination anchored in the two companies’ relative values.

For Sapphire Group, which controls both companies, the logic is familiar: reduce duplication, simplify a fragmented listed footprint, and concentrate scale in a flagship composite textile entity – Sapphire Fibres –better known to local institutions and offshore frontier funds. The legal route chosen (a scheme of arrangement under the Companies Act) allows the parties to address share exchanges, minority protections and post merger housekeeping in one court blessed document rather than via multiple piecemeal steps.

Sapphire is among Pakistan’s most diversified textile families, with a history reaching back to pre Partition trading roots and a modern portfolio spanning yarn, woven and knit fabric, garments, retail, and energy. The group’s textile cornerstone is Sapphire Textile Mills Ltd (STML), while Sapphire Fibres Ltd (SFL) serves as the flagship composite unit in the listed universe.

Over the last two decades, Sapphire has also pushed into power generation, including a 212 MW combined cycle plant at Muridke through Sapphire Electric Company Ltd, and equity in wind assets developed under independent power producer frameworks – part of a broader hedging strategy against Pakistan’s cyclical textiles margins.

On the consumer side, the group has built out the Sapphire Retail brand, adding a high visibility domestic footprint to its otherwise B2B heavy portfolio. The combination – deep manufacturing, retail, and energy – has given the sponsors optionality: integrate fibre to fashion capabilities when market conditions favour value addition, or lean on power assets when domestic costs squeeze milling and

spinning margins.

Sapphire’s corporate geography is spread across Sindh and Punjab, with spinning, weaving, dyeing and garmenting clusters located to optimise access to cotton, labour and logistics. The Abdullah family sits at the centre of governance across the listed entities, an arrangement that has historically facilitated cross company projects (and, at times, prompted calls from investors for rationalisation – exactly what the RCSML–SFL merger now attempts).

RCSML is a focused spinning unit that came online in 1991–92 “under the umbrella of Sapphire Fibres”, and has since specialised in ring spun cotton yarn across a broad range of counts and blends. The company cites a capacity of around 13,000 tonnes per year, with a striking export mix of roughly 85% and the balance sold domestically – an export orientation that amplifies both currency hedge benefits in boom cycles and order book volatility in down cycles. The unit’s site at Ferozewattoan, Sheikhupura – a well worn textile cluster – is geared to produce 6Ne to 80Ne (single and double), plied, slub, mélange and blended yarns, with quality assurance benchmarked to Uster standards.

On the corporate register, RCSML was incorporated on 13 June 1990 as a public limited company and listed on Pakistan’s exchanges thereafter. Disclosure snapshots describe its principal activity simply as the manufacture and sale of yarn, with the business model centred on throughput discipline and cost control – spinners live and die by cotton procurement, energy input prices and working capital turns.

That Sapphire already owns and oversees both RCSML and SFL is baked into the history: Reliance was launched explicitly as a Sapphire satellite to add spinning heft and give the group more flexibility in orders and counts. The merger now proposed essentially reverses that satellite logic – bringing Reliance back into the flagship listed composite.

SFL is a vertically integrated composite – yarn, fabric and garments – and the flagship of Sapphire’s listed textiles. Incorporated on 5 June 1979 as a public company, SFL’s manufacturing footprint sits largely in Punjab – including sites around Raiwind Road (Lahore), Feroze Wattoan/Kharianwala (Sheikhupura) –and has historically encompassed ~99,000 spindles along with multiple fabric and yarn dyeing lines, knitting and stitching capacity. The company is a regular dividend payer and, crucially for investors, has associates/subsidiaries in power – notably Sapphire Electric Company Ltd (212 MW) – which cushions consolidated results when textiles margins tighten.

In investor presentations, SFL positions itself as a “lead player” among composite mills, supplying fabric and garments to marquee buyers in Asia, Europe, Australia and North

America. The organisational design – spinning to garmenting – supports value addition and order book continuity; when yarn markets soften, fabric/garments can carry some of the load, and vice versa. This is precisely the platform into which RCSML will be folded if the court sanctions the scheme.

From a governance perspective, keeping the composite and the power linked associate interests under one listed roof simplifies capital allocation and investor communications. Over time, it could also improve trading liquidity and coverage: the PSX page for SFL shows a steady cadence of financial reporting and distributions, signalling to the market that SFL is the group’s principal listed interface.

The timing of the consolidation is not accidental. Even as export receipts have stabilised and modestly recovered from the post pandemic whiplash – PBS data cited by local media show textile exports up ~7% to about $17.9 billion in FY25 – the operating environment for Pakistani mills remains demanding. Energy and financing costs have been the two dominant headwinds.

On energy, export oriented firms have long argued that the jump from regionally competitive tariffs (~9 cents/kWh in 2021–22) to well above 14 cents/kWh (as per APTMA’s public warnings) eroded competitiveness and forced capacity curtailments in FY23, when textile and apparel exports fell to ~$16.5 billion from ~$19.3 billion the year before. Industry groups have also protested gas tariff hikes and the phased withdrawal of subsidised gas to captive power plants, both of which raise unit costs and complicate planning for mills that invested in co generation over the last decade.

On finance, the policy rate’s climb to 22% through 2023–24 (before easing in 2024–25) turned working capital into a profit and loss event for spinners and weavers. Although rates have since come down to the low teens as inflation cooled, the legacy of elevated borrowing costs still sits in income statements and the caution it has instilled in new investment. In that landscape, simplifying corporate structures and removing duplicated overheads are not just tidy governance exercises – they are survival instincts.

APTMA, the industry’s principal lobby, has repeatedly characterised the FY25 budget and subsequent energy price adjustments as “catastrophic” for liquidity, citing delayed sales tax refunds and thin operating margins. While lobby statements naturally carry advocacy tone, they are a useful barometer of stress –especially for mid tier spinners whose margins swing hard with cotton procurement, energy and financing. Folding RCSML into SFL can therefore be read as both tidying up Sapphire’s listed portfolio and hardening its core against cost volatility.

The merger also fits a broader capital markets logic. Investors typically prefer fewer, larger, and more liquid listed vehicles that present a consolidated story – particularly in sectors where stock specific coverage is thin. A combined SFL RCSML platform could improve free float visibility, index weight, and research coverage, reduce related party complexity, and streamline intragroup transactions (for example, yarn transfers into fabric/garment units), all without diluting the sponsors’ effective control. In Pakistan’s market, where textiles names can be under owned, these details matter to the marginal buyer. (SFL’s consistent disclosures and distribution history – visible on the PSX company page – reinforce that the flagship already carries investor mindshare.)

Finally, consolidation creates scope for operational synergies: harmonised cotton buying across a larger base; coordinated energy procurement and load management; shared maintenance and spares; and aligned sales pipelines where RCSML’s yarn can be internalised into SFL’s fabric and garment streams when market pricing favours downstream conversion. Not all of this will materialise immediately; integration is work. But the architecture – one listed composite housing a former satellite spinner – is set up for it.

From here, the companies will seek directions from the Sindh High Court on circulation of the scheme, convene shareholder meetings as required, and liaise with regulators on approvals. The valuer’s report from Shinewing Hameed Chaudhri & Co. will be the next market moving document: it will specify the swap ratio – how many SFL shares RCSML shareholders receive – and, by implication, the embedded valuation of each business. Because both entities already sit within Sapphire Group’s orbit, governance observers will watch minority safeguards in the scheme: fairness opinions, dissenters’ rights, and post merger disclosure commitments.

For now, however, the direction of travel is clear. Sapphire is consolidating its listed spinning and composite assets into one stronger platform. Given the industry’s recent cost shocks – on energy and finance – that instinct looks less like window dressing and more like fortification. If the court sanctions the scheme and shareholders assent, RCSML will disappear as a separate ticker, and SFL will inherit its assets, people and order book – another chapter in a group history that has repeatedly pivoted to keep scale, costs and capital aligned.

If the objective of a merger is to simplify, scale and survive, Sapphire’s latest move ticks all three boxes. In a sector where cost curves have shifted sharply, putting more of the group under a single, better capitalised and better covered listed umbrella may be the most practical hedge of all.

Cement sector profits up 38% in fiscal 2025

A decline in interest costs and the ability to maintain pricing has been critical to boosting a sector that will likely be needed for the reconstruction after this year’s devastating floods.

PProfit Report

akistan’s listed cement makers closed fiscal 2025 with their strongest earnings in years, lifting combined post tax profit by 38% to Rs167.0bn, up from Rs121.4bn a year earlier. Revenue rose 7% to Rs895.5bn, while sector gross margin widened to 30.7% as companies held on to higher retention prices, coal stayed cheaper, and plants leaned more on efficient power sources. Dispatches edged up 2% to 37.4m tonnes, signalling a modest rebound in volumes against a backdrop of firmer pricing. The fourth quarter kept the momentum going: sales increased 5% year on year, and dispatches climbed 4% to 9.3m tonnes

Two causes stand out. First, finance costs fell 34% to Rs46.0bn, reflecting the easing of policy rates and tighter balance sheet management after an unusually expensive borrowing cycle in FY24. Second, other income jumped 33% to Rs36.4bn, boosted by interest and dividend flows that fattened the bottom line. Together with a better gross margin, these helped lift net margin to 18.6% for the year.

Pricing power was visible across both regions. The North averaged Rs1,434 per bag in FY25, up 16%, while the South averaged Rs1,395, up 17%. The note attributes the lift partly to a higher federal excise duty but mainly to stronger retention prices, which more than offset a soft patch in quarter on quarter volumes late in the year. A continued narrowing of the cost base has happened: international coal averaged USD 102 per tonne for the year, down 4.6%, and dipped to $92 in the fourth quarter – tailwinds that flowed straight into margins given coal’s centrality in kiln fuel.

Sector net sales have recovered from the troughs of FY23; gross margins have stair stepped higher over the last four quarters; finance costs have rolled over; and profit after tax has re rated accordingly. In short, FY25 combined a friendlier input cost curve with disciplined pricing and a more forgiving interest rate backdrop.

The recovery was broad, but the dis-

persion in outcomes was striking – shaped by capital structures, fuel strategies, and the mix of export versus domestic sales.

DG Khan Cement (DGKC) delivered the largest percentage swing, with earnings rising almost fifteen times year on year. The turnaround reflects a 56% drop in finance costs as the rate cycle turned, and a 1,110 basis point expansion in gross margin. Volumes helped too: dispatches grew 10% to 5.3m tonnes.

Bestway Cement (BWCL) posted a 73% profit jump to Rs23.9bn, underpinned by a 469 basis point margin uplift to 34.6%. Pricing discipline, flat to lower coal, and a lighter finance cost load did the heavy lifting. Dispatches dipped 2% to 6.8m tonnes, but yield per tonne improved enough to overpower the volume slippage.

Kohat Cement (KOHC) increased earnings 30%, powered by a 19% rise in other income and a 923 basis point improvement in gross margin. Volumes softened 10% to 2.3m tonnes, but margin expansion and income flows offset the drag.

Cherat Cement (CHCC) grew profit 58% as gross margin widened 563 basis points to 36.9%, other income surged, and finance costs fell 57%. Dispatches eased 9% to 2.4m tonnes, yet pricing and costs more than compensated.

Fauji Cement (FCCL) rose 62%, with margin advancing 662 basis points to 35.5%. The note credits higher retention prices, a deliberate tilt towards local coal, and a greater share of in house power generation –all visible in the cost line. Volumes rose 6% to 5.4m tonnes.

Maple Leaf Cement (MLCF) printed 66% consolidated profit growth, off the back of a 5.8 times surge in other income and a 439 basis point margin expansion to 37.1%. Dispatches were essentially flat at 3.9m tonnes.

Pioneer Cement (PIOC) was the outlier on the downside: earnings slipped 6% to Rs4.9bn as gross margin shrank 396 basis points and both other income and revenue fell 25% and 6%, respectively. Its dispatches fell 12% to 2.1m tonnes, compounding the squeeze.

The engine was a 27% rise in other income plus 9% higher revenue; volumes rose 9% to 9.3m tonnes. The research also hints at a potential extra tailwind from the power sector’s circular debt unwind since Lucky has exposure to coal power receivables through an associate; if those cash flows materialise, they could support dividends or de leveraging at the consolidated level.

There has been a clear re rating in profitability: BWCL at Rs23.9bn (+73%), FCCL at Rs13.3bn (+62%), MLCF at Rs11.5bn (+66%), KOHC at Rs11.6bn (+30%), DGKC at Rs8.7bn (a near fifteen fold rebound), CHCC at Rs8.7bn (+58%), PIOC at Rs4.9bn ( 6%), and LUCK at Rs84.5bn on a consolidated basis (+17%).

What explains the divergence? Three choices stand out:

• Fuel mix and self generation. Plants that switched earlier and more aggressively towards local or Afghan coal, and that invested in in house power, saw a bigger step down in their cash cost per tonne. That shows up most clearly in FCCL’s and CHCC’s margin maths.

• Balance sheet posture. High debt names captured the rate relief most visibly (DGKC), while those with cleaner balance sheets enjoyed smoother earnings without the volatility that heavy finance costs bring.

• Pricing versus volumes. Across the board, FY25 rewarded price discipline more than chase the tonnage strategies. Where volumes were flat or even declining, firms that maintained retention pricing still came out ahead as coal eased and finance costs fell.

Analysts expect the profit up cycle to continue in FY26, anchored by three drivers: a recovery in domestic dispatches, further improvement in retention prices, and a cheaper fuel and power mix as more kilns diversify away from imported coal and lock in local or Afghan supply. As the cost base stabilises and the financing environment remains less punitive than the FY24 peak, sector earnings should retain altitude, even before any large scale public sector projects kick in.

One important nuance in the FY26 setup is coal price volatility. FY25 benefited from a down shift to USD 92 per tonne in the

last quarter; if that floor holds, gross margins can stay wide even if bag prices stop climbing. Many producers are also better hedged operationally, with mixed coal baskets and higher waste heat recovery or captive power, which should dull the impact of any short term spikes.

Interest rates are the other swing factor. The sector’s 34% drop in finance cost to Rs46.0bn was a huge earnings lever in FY25. If the easing cycle continues – or even just pauses – financing outflows should remain manageable. The corollary is that other income (which rose 33% to Rs36.4bn) could normalise if deposit yields drift lower; but analysts’ base case is that operating leverage and cost control will more than offset any tapering in treasury gains.

On pricing, the charted series of bag prices shows both regions ending FY25 near the higher end of a four year range. The note assumes incremental rather than explosive price moves in the coming year, with retention supported by supply discipline and cost push elements such as taxes. If dispatch growth does materialise, mix and operating rates could add a second leg to earnings without needing another large price reset.

Analysts flag GWLC, FCCL and MLCF as top picks, citing their fuel strategies, operating execution and earnings momentum. While valuations are not the focus of the sector review, the combination of strong FY25 prints, cleaner balance sheets, and a gentler cost curve sets up a constructive tape for FY26 – barring exogenous shocks.

Another wildcard is the power sector clean up now underway. To the extent that lower system borrowing costs and a more stable grid lower electricity charges or reduce the frequency of costly outages, cement producers could see further relief on the power line of their cost structures. The large circular debt refinancing that lowers financing costs in the power chain and proposes dedicated surcharges for repayment – developments that, while outside the cement sector per se, contribute to a less volatile energy backdrop for heavy industry.

Risks to watch include renewed coal spikes, a sharp rupee move that widens imported input costs, aggressive taxation on construction materials, or a more severe demand down cycle in private housing. But the base case remains upbeat: dispatches normalising, costs contained, and margins resilient.

Even without a mega public works push, Pakistan’s construction economy carries a backlog of repair and reconstruction needs after recent flood seasons that battered roads, bridges, healthcare facilities and housing. Those bills seldom get settled in a

single budget; they get spread over multiple fiscal years, moving from emergency relief to brick and mortar rehabilitation once waters recede and damage assessments are finalised. For cement makers, that sequencing matters: government led works tend to favour bulk supply contracts – cement for roads, culverts, embankments and public buildings – while household rebuilding spreads demand over many smaller retail channels, often with a lag as families arrange financing or compensation.

The sector’s FY25 data already show the supply side is prepared. Plants have rationalised fuel baskets, nudged power self generation higher, and defended retention prices – meaning they enter FY26 with better control over their cost curves. If provincial and federal executing agencies accelerate the pipeline of flood related works – be it resilient road surfacing, embankment fortification, school and clinic reconstruction, or low cost housing – the incremental tonnes could lift plant utilisations without eroding margins. That is particularly true for northern producers situated near the largest public works corridors.

Private rebuilding dynamics are just as important. The experience of past flood cycles suggests rural housing repair can come in waves as cash grants land, remittances arrive, and reconstruction crews become available. Retail demand behaves differently from institutional demand – spiking on weekends, leaning towards smaller bag lots, and sensitive to price moves in steel and aggregates. For the sector, this creates an incentive to keep bag availability smooth and intensify retail distribution in affected districts. With North region bag prices averaging Rs1,434 and South Rs1,395 in FY25, the affordability of a bag relative to household cash flows will shape how quickly private rebuilding converts into steady throughput.

There is also a resilience angle to post flood demand. Engineers are more frequently specifying higher strength concrete, better drainage designs and flood tolerant materials for roads and public buildings. That can lift cement intensity per kilometre or per structure, even if project counts do not explode. To capture that value, producers will want to push technical sales – demonstrating how particular cement grades perform in high moisture or high chloride settings – and align with contractors bidding for resilience focused programmes.

A final, more subtle, linkage sits in working capital cycles. Public sector works often pay on a delayed schedule; contractors, in turn, manage cash flow by stretching their own payables. In FY24, that environment combined with high interest rates to make

contractor financing painfully expensive –crushing the flow of small projects. FY25’s easing in borrowing costs has begun to defrost that pipeline. If rates remain lower, as the sector hopes, and if PSDP style disbursements flow more predictably, the cement value chain – from clinker to bag to wheelbarrow – should see a healthier cash conversion cycle than it did two years ago. The sector’s own finance cost drop to Rs46.0bn is a reminder of how powerful that lever can be when the macro environment co operates.

Two visuals are worth revisiting. The bag price trend on page 5 captures a multi year climb that steepened during inflationary quarters and then plateaued at a high level through FY25. That plateau, combined with cheaper coal, explains the 30.7% gross margin outcome for the year. The dispatch table on the same page shows how companies with flat or slightly lower tonnes still printed better earnings because every tonne earned more, and cost less to make. This is not a classic volume led up cycle; it is a margin led one.

The quarterly galleries on page 6 add nuance: profit after tax has become less lumpy; gross margins are no longer whipsawing quarter to quarter; and finance costs are clearly trending down. For investors and planners alike, that stability is almost as valuable as the headline growth rate, because it encourages capex planning and maintenance catch up – both prerequisites for meeting any surge in reconstruction orders.

FY25 delivered the sort of earnings combination the cement sector has been chasing since the late pandemic whiplash: firmer pricing, cooler coal, cleaner power, and a lighter debt load. The aggregate numbers – profit up 38% to Rs167.0bn, revenue up 7% to Rs895.5bn, gross margin at 30.7%, finance cost down 34% – tell a story of regained operating control. Under the hood, leaders like DGKC, BWCL, FCCL, MLCF and CHCC show what cost discipline and smarter fuel choices can do; PIOC is the reminder that the cycle is not equally kind to all.

The base case for FY26 is constructive: dispatches recover, retention holds, fuel remains manageable, and rates stay friendlier than in FY24. Add the country’s rebuilding agenda after recent floods and a potential smoothing of the power sector’s finances, and the demand and cost pictures could align more often than they collide. Risks – coal spikes, tax surprises, currency swings – are real. But after a year of margin led repair, the sector looks better placed to supply the next round of roads, bridges and homes than it has since before the last monsoon disaster.

If FY25 was about fixing the economics of a bag, FY26 may be about moving more bags to where they are most needed. n

K-Electric to shut down major portion of power generation capacity

The utility believes it cannot rely on natural gas supply from SSGC and has decided to stop waiting around for it

Profit Report

KElectric (KE) has moved to retire two of its legacy gas engine power plants—Korangi Town Gas Turbine Power Station (KGTPS) and S.I.T.E. Gas Turbine Power Station (SGTPS)—citing years of constrained gas supply and the completion of new capacity and grid links that render the older units surplus. In a disclosure to the Pakistan Stock Exchange, KE said its board, at its 1,259th meeting on 23 September, approved the decommissioning/early retirement of KGTPS and SGTPS and authorised a filing with the National Electric Power Regulatory Authority (NEPRA) to modify the company’s generation licence accordingly (Generation Licence GL/04/2002). The company stressed that the step would not impair its ability to meet demand in Karachi.

The utility’s reasoning traces back to how these plants were added and fuelled. Under a 2009 implementation agreement with the federal government, the two sites—engine based gas plants—were inducted with an explicit commitment for local gas allocations from Sui Southern Gas Company (SSGC). In 2016, KE bolted on small steam turbines at each site to squeeze out extra efficiency. But as domestic gas reserves thinned, pressurised supply became erratic, prompting the Cabinet Committee on Energy in 2018 to direct a shift to RLNG for KE’s fleet, including KGTPS and SGTPS. Even after that pivot, the company says optimal gas at the required pressure remained a persistent challenge—undermining reliable dispatch and the economics of keeping the plants online.

KE’s case for early retirement rests on the system it has built since. Most notably, the utility has commissioned Bin Qasim Power Station III (BQPS III), a 900 MW RLNG plant, and expanded interconnection with the national grid so that KE can now draw more than 2,000 MW when needed. The company has also executed a long term Power Purchase Agency Agreement (PPAA) with the Central Power Purchasing Agency (CPPA G) and an Interconnection Agreement (ICA) with the National Grid Company (NGC), formalising the framework for regular power offtake from the grid. Together, KE argues, these steps remove the reliability value once provided by the older gas engine sites.

The plants in question are modest in size but strategically located. Each site consists of several dozen gas engines and a small steam turbine

that harvests waste heat—an arrangement that originally made sense in a city where distributed generation could help stabilise local feeders. KE’s technical pages describe 32 engines at each location (roughly 3 MW apiece) with a 10 MW steam turbine per site. Put together, the two plants contribute about 215 MW of installed capacity to KE’s own fleet. Measured against KE’s self owned installed capacity of 2,397 MW, retiring KGTPS and SGTPS removes about 9% of the utility’s in house generation. In practice, the loss is more than offset by the 900 MW recently added at BQPS III and by the enhanced ability to import over 2,000 MW from the national grid during peaks. That is why KE says there should be no adverse impact on supply security in its service territory.

At the national level, the scale is smaller still. Pakistan’s installed generation capacity stood at 45,888 MW by mid 2024, according to NEPRA’s State of Industry Report. On that base, a 215 MW retirement is about 0.5% of the country’s total capacity—a rounding error in planning terms, though it matters locally if the retired plants sit near dense load pockets.

KE’s message to consumers and investors is unambiguous: no deterioration in service is expected because the system has already been reshaped around newer, larger and more efficient assets and around firmer grid ties. The company points to three pillars:

• A modern baseload plant. BQPS III delivers 900 MW at better efficiency than the gas engine sites, and its scale materially improves KE’s unit costs when it is dispatched.

• Bigger national grid backbone. Two additional interconnections commissioned in FY25 have lifted KE’s grid draw capability to more than 2,000 MW, giving planners latitude to ramp imports in hot months or during plant maintenance windows. The PPAA with CPPA G and ICA with NGC give a contractual spine to this operating reality.

• Operational simplification. Exiting older engine parks that often ran below their potential due to gas pressure constraints should reduce maintenance overheads and fuel logistics complexity. It also tilts KE’s dispatch towards plants that sit higher on the efficiency ladder or towards imported power when that is cheaper.

There are, of course, trade offs. Engine based plants can be flexible; they start and stop quickly and can anchor local networks. Retiring them places a greater premium on transmission resilience—the ability of KE’s grid to move large blocks of power from BQPS and from nation-

al interconnections to neighbourhoods that once leaned on nearby engines. It also increases exposure to RLNG and national grid availability. KE’s planning documents show these risks are now part of the design: power imports are under longer term agreements and the transmission build out has been geared for higher draw from the national system. The regulatory process is the next milestone. KE will seek NEPRA’s approval via a Licence Proposed Modification, the statutory route to amend a generation licence. That filing will typically include the technical case for retirement, environmental and cost implications, and a demonstration that adequacy standards are still met. Until approved, the plants remain on the books even if their dispatch is curtailed.

Read closely, the timing reflects both supply realities and portfolio optimisation. On supply, KE is blunt: depleting domestic gas reserves and pressure issues made sustained operation of KGTPS and SGTPS increasingly unreliable, even after the switch to RLNG. On the portfolio side, the commissioning of BQPS III and expansion of grid offtake create headroom to rationalise older, less efficient capacity without compromising adequacy. When you can import more than 2,000 MW and you have a 900 MW anchor plant in service, the case for keeping about 215 MW of small engines is weaker—particularly when fuel supply is uncertain.

K Electric’s planned retirement of its KGTPS and SGTPS plants marks the end of a chapter that began when local gas was plentiful and engine based stations offered a nimble way to shore up Karachi’s supply. The context has changed. Gas is tighter, the city’s demand is larger and more variable, and the utility has built a different system architecture—big block generation at Bin Qasim and beefed up interconnections to the national grid. Against that backdrop, retiring about 215 MW of small, gas dependent engines looks less like a retreat and more like a pivot to a different operating model.

The company’s assurance is clear: no adverse impact on Karachi’s supply is expected once NEPRA clears the licence modification, because the new 900 MW plant and 2,000 plus MW grid draw capability have already been in place to take the strain. The national picture supports that claim: the capacity being retired is a sliver of Pakistan’s overall system, and the utility’s replacements are already dispatching. The test, as ever, will be the next summer peak—and whether the “new KE” of big plants and big interconnections keeps the city cool when it counts. n

The data cannot be clearer. There is no better place for the average, salaried, Pakistani to invest than the stock market. Awareness, however, remains elusive. Some young Pakistanis want to change that

By Zain Naeem and Abdullah Niazi

Abdul Rehman Najam appears to be exceedingly normal. He is 33 years old, a clean dresser, and affable. He does not have a natural presence on camera, but he has learned how to look directly at the lens and speak in a slow and deliberate manner. His tenor is always steady.

He is what you would call a “finance bro” — which means he is young, educated, smart, works in the world of finance and loves to talk about it. The term finance bro is a loaded one. It comes with cultural implications. Most people see them as loud, obnoxious, and confusing. The use of jargon, aggressive attitude, and cockiness is often associated with these young men. Their club exists because they know the secrets of the world. They know how money works and other lesser mortals working in unworldly professions such as marketing, medicine, education, HR (what to speak of the scoundrels of the press) simply have not achieved their level of enlightenment.

The exclusivity keeps the illusion. That is the magic trick. But as Abdul Rehman Najam knows, it isn’t particularly difficult to get an understanding of how the markets work. And unlike most finance bros he has the patience and passion to teach the average person the basic ins and outs of how to become an investor. In fact, he plans to make a living out of doing

exactly this.

Starting off by posting regularly on social media about investing, Abdul Rehman noticed there was a demand for financial education. People would reach out to him to ask how it all worked. Starting with meet and greet sessions at cafes in Lahore, he has now created a financial advisory company called ARN Financials which he says has over Rs 5 billion in assets under management. His entire mission has been based on one core goal: getting more people to invest in the stock market as an investment.

His ideas are by no means revolutionary. He believes in value investing and introducing people to the financial markets. It is basic advice that others have given before including this publication. Invest in the stock market. Do not buy that plot. Your friend’s brilliant business idea might not be so brilliant so maybe don’t put all your hard earned savings into it. But somehow Abdul Rehman is a leading light in a crop of young people talking about financial advice and investing on the internet.

Just look at some of the others. There is Laeeq Ahmed, whose financial advisory company has a YouTube account with nearly 200,000 subscribers and over 10 million views on his long-form videos about any topic related to investment and personal finance under the sun — from whether or not to buy a car, how to open an account on the PSX, and even explainers titled “What is a Mutual Fund?” Another good example is Mashal Khan, the

actress turned investor who has left the world of showbiz behind because she got addicted to investing. She now makes videos and podcasts about her journey and invites people to see what investing is all about. “Your favourite Capitalist” reads her Instagram bio, Combined, her two accounts on Instagram have over 1.5 million followers.

These are only a few of the prominent “investment influencers” that are becoming popular in Pakistan. Their existence is both an invitation and a guide for people that might want to become a part of Pakistan’s many stock market investors. Their target audience is really the big fish. There are plenty of financial advisors and brokerage houses out there doing that. Their goal is to get the average person whose savings are probably in a bank account collecting interest (or possibly just depreciating away) and get them to invest a little bit every month. At least that is where all of them started. But why are they kicking off now?

The best time to invest is today

The Pakistan Stock Exchange has been going through a moment. In December last year, the KSE-100 Index crossed 100,000 for the first time. This is the benchmark index that seeks to measure total returns of a representative sample of stocks on the Pakistan Stock Exchange. As this publication pointed out back

then as well, it is generally not a good idea to read too much into the day-to-day movements of the stock index, even when it reaches such momentous psychological levels, but one thing can be said with certainty: the optimists are right to believe in the upward trajectory of the Pakistani economy, and the Pakistani capital markets provide a strong mechanism for middle class Pakistanis to generate wealth for themselves and their families through the capital markets.

Back then, Profit’ own coverage of this momentous event came in these words:

“There is now 33 years of data – roughly a whole generation’s worth – that demonstrates the value of investing in Pakistani stocks. During those 33 years, the country has seen unstable democracy, military coups, war in Afghanistan, refugee crises, dozens of International Monetary Fund (IMF) bailouts, and several cycles of extreme economic upheaval. The market has had several hard crashes, and several euphoric rises.

Is the market volatile? Yes. But now we know how it reacts to just about anything this country can throw at it, and so fewer and fewer of the sceptics reasons for not investing in Pakistani stocks make sense with each passing year. In any given year, is there a very high likelihood that your investment in Pakistani stocks will lose money? Yes. Is there now a reasonable expectation that if you do not panic sell during the market’s crashes, the next bull run will more than make up for your losses? Also, yes.”

In this story, Profit charted the investment trajectory of a young college educated professional that started his career and investing in the stock market in 1991. It took this hypothetical individual through the treacherous twists and turns of the Pakistani economy and assumed one thing: this individual was regularly investing small amounts of savings in the stock market every month. If this person started in 1991, over the course of 34 years he was better off and more wealthy through these investments. In this experiment, he had invested Rs 40 lakh in principal investments and his portfolio stood at a value of Rs 5.1 crores at a point when he still has 10 years to retire. At this point, he can take this money out during a good run for the market and invest it in something safer like government bonds and receive a steady passive income for the rest of his life.

The details are in our original story but what matters is that the stock market is a good place to make small investments over a long period of time. It is now a method that is tried and tested, and that is the information our investment influencers are bringing to the table. Nothing big or fancy or complex. In fact, for a lot of these influencers, they cannot give direct advice since you need a licence for that. Which is why they often create hypothetical

My style was never about chasing quick trades. I connected with the idea of buying great businesses and holding them for the long term

Abdul Rehman Najam, founder

ARN

Financials

scenarios (like Profit did in this earlier story) to explain the benefits of investing in stocks. It is essentially an invitation for people that might not know about this and a guide for people that might be interested but don’t know where to start.

A product of the times

It is interesting that Abdul Rehman Najam was born in 1992 —- a year after the hypothetical man we discussed above. He did his undergraduate degree in economics from the University of Warwick in 2015 after growing up in Karachi. He returned to join the family business but by 2019 he wanted more.

This was the first time that he decided to delve deeper into the financial markets. Having an educational background, he dedicated his life to a deeper exploration of how investment worked. Rehman’s formal financial education came from Youtube videos of Berkshire Hathaway. He started to study the Annual General Meetings of Berkshire Hathaway which were headed by Warren Buffet. Other than these videos, he also dived into books on value investing and studied the case studies of companies involved in value investing. His life’s mantra became the principles followed by Buffet himself. Understand the business, ignore the market noise and let the growth compound over the long term. For a newbie in the market, the first plan of action is to carry out day trades to make a quick profit and exit and enter the market in a span of days. Rehman flipped the script and started to have a long term view. “My style was never about chasing quick trades. I connected with the idea of buying great businesses and holding them for the long term,” he recalls.

The grind might have been slow but it proved to be fruitful. As his investing principle started to gather momentum, Abdul Rehman knew that he had proved his philosophy to be true and correct. Rather than following the price, he followed his fundamentals which proved to be correct in the long run.

Becoming the advisor

The pivot worked well for Abdul Rehman Najam. Over time he saw his investments flourish and he got deeper and deeper into the markets. As he grew, he started talking to people around him. That is one thing about Abdul Rehman Najam anyone that speaks to him will notice: he earnestly wants to talk about things and share ideas. But he found not a lot of people were of the same school of thought as him.

Local investors were carrying out superficial and barely scratching the surface in terms of fundamentals based investing. There was a common misconception that the markets were rigged and that it was better to make a quick profit rather than give the time and effort that was needed to carry out such investment. Seeing his formula working out so well, Rehman felt that he was sitting on a contrary idea.

As Rehman proved the efficacy of his approach, there was a hunger to develop a deeper understanding of the market. Rehman founded ARN Financial Advisors which aimed to broaden the understanding and application of value investing. The company looks to provide advisory and educate the investors while also carrying out research on its own behalf.

The motto of the company is “Invest in what you fully understand.” It is a principle he lives by. After all, shareholders are part owners of the company and they should act in that manner. “Their profit is your profit. The stock market is simply the price tag of Pakistan’s best businesses,” Rehman says.

His courses started to get a positive response. He began in a very earnest way. In 2023, he posted that he would host a get together of people interested in investing at Gloria Jeans in DHA Phase 6 Lahore. The response was more than what he expected. People were interested and engaged. Since then, his courses have started to integrate masterclasses, media appearances and one-on-one advisory services which help the new investors in applying the principles of value investing.

One of the biggest advantages of value

investing and consistent investing is the fact that earnings start to compound over a period of time. In case of short term investing, an investor only looks towards seeing his investment grow for a short time horizon. Compounding is able to see how an investment can grow if it is stuck with. At the end of 2016, the KSE 100 index was trading at 30,000 points. Today, it has grown 5 times. An investor who would have invested 10 years back with Rs 100 would have seen their investment grow to Rs 500. Go back further to 2005 and the index was trading at 10,000. It shows a growth of 15 times in a space of 20 years.

This is the idea which has also been foreign to local investors. They want to trade regularly on a daily basis and double their investment in a short period of time. Rehman has been able to instill the fact that seeing their investment in the long term perspective will see their investment grow further. “Wealth creation in Pakistan is not a fantasy. It has already happened — the only missing link is investor discipline,” he says.