18 MCB Funds nearly triples revenue on the back of rising markets

20 Engro steps up lending and direct sales to farmers

22 Pakistani meat to finally be available at Carrefour in Dubai

24 At Hum TV, YouTube is starting to become big business

26 Copper exports from Saindak mine crossed $800 million in 2024

28 Beyond the Loan Rabab Hussain

30 Chenab’s fortunes have not quite changed. Why is its stock price going up?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Habib Bank crosses Rs5 trillion in deposits

Pakistan’s largest bank continues to grow its lead, even as it faces stiff competition from rising star Meezan Bank

Profit Report

Habib Bank Ltd has crossed a symbolic and strategically vital threshold: Rs5 trillion in deposits. By the end of June 2025, management told analysts the balance had climbed to Rs5.2 trillion, up sharply from Rs4.37 trillion at end-2024.

Two details make the feat more than cosmetic. First, the growth is fast – roughly a 19–22% leap in just half a year. Second, the mix improved: current accounts now comprise about 40.5% of the domestic deposit base, with management targeting 42% by year-end – a mix shift that lowers funding costs and hardwires earnings resilience in a falling-rate cycle. The bank attributes the deposit acceleration to “whole-bank” execution rather than a handful of branches, and expects momentum to continue through 2H-2025.

The market backdrop helps, but the bank’s own P&L underscores how deposit depth is feeding through to performance. In

2Q-2025, total revenue rose to about Rs91.6 billion, up 13% year-on-year, led by mark-up income; EPS printed at Rs12.12 (up 24% YoY), and the bank announced a Rs4.5 per share dividend for the quarter, taking 1H-2025 payouts to Rs9 per share. Cost discipline is improving too: the cost-to-income ratio eased to ~49% during the half (domestic business already sub-50%), and management says it wants that trend to hold. Capital remains comfortably above requirements with a CAR near 17.9%.

These datapoints, summarised in the tables and briefing notes shared with analysts, frame the deposit milestone as the financial engine of an improving income statement rather than a vanity metric.

What is powering growth and profitability

The first and most obvious driver is the surge in current accounts. Current account growth was described as the highest ever, with roughly

Rs440 billion added in 1H-2025 alone – moving the CA ratio from 37.3% in December to 40.5% in June. Cheap, sticky funding lowers blended liability costs and protects margins as policy rates move; management is explicit about pushing this mix to ~42% by year-end. A second lever is how the bank has redeployed liquidity. Investments rose to ~Rs4.3 trillion by June, with an emphasis on floating-rate PIBs (about 51%), supplemented by fixed PIBs (22%) and T-bills (18%) – a positioning that preserves carry while keeping duration risk in check as the rate cycle evolves. Only a small portion of the fixed-rate book is due in the next 18 months, limiting reinvestment risk. This portfolio shape is laid out clearly in the corporate-briefing materials.

The cost-to-income ratio has drifted down to the high-40s domestically (55% to 55.2% at the group level), with management reiterating a sub-50% aspiration across the consolidated franchise. That is not just a cost story; it is also about scalability – expanding top-line through better use of an already-built network, technology, and processes.

The infection ratio edged down to ~5.0% by June, with coverage near 90%; 1H2025 also benefitted from lower provisioning as IFRS-9 one-offs rolled off and recoveries improved. That combination – steady asset quality and less P&L drag from credit costs –supports both earnings and capital.

There is improvement in the microfinance arm too: Habib Microfinance Bank swung to a profit of ~Rs1 billion in 1H-2025 versus a loss a year earlier, a helpful catalyst for consolidated numbers and a signal that risk-adjusted pricing and cost control are biting.

Put together, HBL’s profit engine right now is textbook: more and cheaper deposits, earnings-friendly asset mix, contained credit costs, and incremental operating leverage –all underwritten by a strong capital cushion. The bank’s guidance remains deliberately cautious on rates and inflation, but the internal targets on deposit mix and costs suggest it is managing for margin stability even in a normalising rate environment.

A history of Pakistan’s flagship bank

Habib Bank traces its roots to 1941, when the Habib family established the bank in Bombay to serve the trading community of the subcontinent. At Partition in 1947, HBL moved its head office to Karachi and rapidly became the government’s principal banker, financing trade and reconstruction. Throughout the 1950s and 1960s it grew into the country’s largest commercial bank, with a widening international footprint as the diaspora spread out across the Gulf, Africa and the UK.

In 1974, Pakistan nationalised its banking sector. The Habib family, displaced from their flagship, went on to establish Habib Bank AG Zurich internationally and later Bank AL Habib domestically after financial liberalisation, keeping the Habib name present in global and local banking even as HBL itself remained state-owned.

In 2004, the government privatised HBL, with Aga Khan Fund for Economic Development (AKFED) leading the acquisition. The change unleashed heavy investment in governance, risk systems, and technology. Over the past two decades HBL has retained the country’s largest branch network and scaled up digital channels, corporate and investment banking, and payments. The present franchise now spans universal banking in Pakistan – from corporate and SME financing to consumer lending, payments, trade services, wealth management and

agriculture – plus a selective international presence aligned to client needs and remittance corridors.

The Rs5.2 trillion deposit base underlines a bank built on sheer distribution and brand equity, but the current strategy leans as much on quality of deposits as on size. The medium-term playbook is clear in the analyst briefings: expand low-cost current accounts, keep operating costs on a glide-path lower, manage credit risk conservatively, and use the balance sheet to capture carry without overly lengthening duration. In other words: steer a big bank like a big bank – but with sharper mix, tighter costs, and better data.

The competitive heat rises – especially from Meezan Bank

HBL’s scale advantage is real, but competition has never been fiercer. The most conspicuous challenger is Meezan Bank, Pakistan’s leading Islamic bank, which has combined a clear value proposition (Shariah-compliant products), a disciplined branch rollout, and a strong deposit franchise built on current and savings accounts. Its growing market share, especially in retail and lowcost deposits, pressures incumbents to fight harder for both customer experience and pricing.

More broadly, the competitive field now includes other large private banks with sharpened digital offerings, public-sector banks with renewed lending licences, and a swarm of fintechs unbundling payments and micro-savings. As the State Bank pushes interoperability in payments and upgrades the regulatory rails, switching costs for consumers keep falling.

In such an arena, service design matters: onboarding speed, mobile UX, pricing transparency, and bundled ecosystems (bill pay, QR, remittances, investments) are increasingly the battlegrounds where banks win or lose deposits – especially current accounts. HBL’s management clearly understands this, which is why it has emphasised “whole-bank” execution in the CA push and keeps speaking to scalability of infrastructure and digital channels in analyst interactions.

For HBL, then, the defence of a five-trillion-rupee deposit base will hinge on customer intimacy at scale: keeping corporate and SME clients sticky with trade, cash-management and investment services; acquiring retail CASA through salary accounts, everyday payments and savings journeys; and leaning on cross-sell from a re-energised microfinance arm. The bank can still out-gun rivals on distribution, but the long game is about experience as much as reach.

Deposits, GDP and the under-banked opportunity

The milestone also invites a harder look at the Pakistani banking sector. By international standards, Pakistan’s deposit-to-GDP ratio remains low. While definitions vary, industry watchers routinely note that formal savings intermediated by banks lag regional peers – a legacy of informality, cash-intensive commerce, and long bouts of high inflation that keep households wary of holding financial assets for long. That under-penetration is both a constraint and an opportunity. It caps system funding in the short run but leaves huge headroom for first-time savers, pension products, and transactional deposits as digital rails deepen.

The past two years have complicated the picture: monetary policy tightened through 2023-24 to tame inflation, then began easing as price dynamics cooled. In the tightening phase, banks enjoyed fat spreads on government securities; as the cycle normalises, those spreads will compress. The banks best placed to defend margins will be those with cheap deposit mixes, efficient cost bases, and balanced asset-liability profiles – exactly the ingredients HBL is trying to lock in with its CA push, cost glide-path, and floating-rate tilt on investments. The analyst presentations emphasise that management expects SBP to remain cautious, and that while inflation may drift towards ~7% by year-end, monetary decisions will stay data-driven. In such a setting, balance-sheet agility and CASA depth are the decisive moats.

Another structural theme is crowding-out vs. crowding-in. With banks holding large stocks of government paper, the private credit cycle has been muted; HBL’s own advances-to-deposit ratio dropped from ~56% at end-2024 to ~38% in June as liquidity piled up and was parked in sovereigns. Management still guides for a pickup in domestic advances in 2H2025, but concedes full-year loan growth will likely be negative – understandable given corporate deleveraging and a still-elevated cost of capital. The sector’s challenge – and opportunity – over the next two years is to re-engage private credit as rates settle and investment revives.

Lastly, the system’s capital and risk buffers matter. HBL’s CAR near 17.9% provides comfortable headroom, and the bank’s improved coverage ratio (~90%) offers resilience should credit costs re-accelerate. Sector-wide, the direction of travel is the same: regulators have demanded stronger buffers since 2018, and the biggest banks have complied. The upshot is a sector that can absorb rate volatility and credit shocks better than in previous cycles – provided growth returns to the economy to pull banks away from a narrow dependence on government paper. n

The slow decay of Pakistani Agriculture

PAKISTANI FARMERS ARE USING MORE LAND AND GROWING CROPS MORE AGGRESSIVELY. THE ONLY OUTCOMES HAVE BEEN SHRINKING YIELDS, SMALLER FARMS, AND SLIMMER MARGINS

By Abdullah Niazi

The last time the federal government released any meaningful, consolidated data about Pakistan’s agricultural sector was in 2010. Which is why there was great anticipation when the government announced it was conducting Pakistan’s seventh agricultural census.

What does the census tell us? Over the past 15 years, Pakistani farmers have significantly expanded the amount of land they grow crops on. The rate at which they reuse land in different growing seasons has also increased. All in all there is a clear push from the agriculture sector to try and grow more. It makes sense. Pakistan’s population has grown by 5 crore people since 2010. But the increase in use of land for crops is fast becoming a race against the clock. Put the census data next to crop productivity numbers and it becomes clear that yields for most major crops have decreased.

The census also tells us that the government is terrible at counting. In the case of some crops, such as wheat, the government’s estimates of how much land is being used to cultivate it has been off by as much as 12 million acres. There is also a clear mismatch between the data being reported by the provinces (which is more accurate) and that being reported by the federal government.

All in all it is a story of farmers desperately trying to keep up with demand and failing to find any kind of consistent support. This is the story of Pakistani agriculture since the last census, one crop at a time.

Fragmented landscape

The biggest difference in agriculture from the previous census is how much more land is being used for agriculture. The statistics are actually quite surprising given the increasing trend of a shift away from agriculture and towards real estate development. The shift has been particularly strong in fruit orchards. But the census shows that the total amount of farmland in Pakistan has increased from 52.9 million acres to 59.3 million acres. The additional 6.4 million acres is almost exclusively irrigated land. Non-irrigated (rain-fed) farming saw a sharp decline to 4.9 million acres in 2024, from 8.4 million in 2010, reflecting a shift toward irrigated agriculture nationwide.

Farmers have also been increasing the amount of land they utilize in their farms for cultivation. In 2010, the total cultivated acreage of farms was 81%. This has risen to 89% currently. The obvious indication from this is that farmland has not just increased,

but farmers are trying to use as much of it as possible. That means they are using less space for livestock, for their homes, and for any other facilities on their farmland. One reason for this could also be the changing size of farms in Pakistan.

The average size of a farm in Pakistan in 2024 was 5.1 acres, down from 6.4 acres per farm in 2024. Overall in Pakistan 97.5% of farmers in Pakistan are operating on farms that are smaller than 12.5 acres. {Editor’s note: The provincial data for this is fascinating as well. Sindh, for example, has the largest number of farms that are above 100 acres. In fact, the average size of a farm in Sindh that is over 100 acres is 251 acres, significantly more than in other provinces. But at the same time the percentage of people with farms less than 5 acres is also the highest in Sindh. The other province with the largest farm size disparity is Balochistan, but this provincial distribution will be the subject of a different story.}

What is also interesting to note is that the number of farms have increased as a result of this. Overall, there are 11.7 million farms in Pakistan, up from the 8;2 million farms in the country in 2010. This means that the size of the average farm has not just shrunk because of the new acreage added to the cultivated land, but also because a lot of existing farms have been divided in the process of inheritance. This is a massive problem because in Pakistan the smaller a farm is the less profitable it becomes. Agriculture produce is quite cheap, and farmers often have slim margins. The less land they have the less money they will be able to make.

And then there is another factor. While the overall area under cultivation is 52.7 million acres, the overall cropped area is 82.7 million acres. What does this mean? The area under cultivation refers to the overall amount of land on which any crops are grown. But when the government mentions cropped land they are referring to something in agriculture known as Gross Cropped Area (GSA). In any given year, farmers follow at least two seasons. In Pakistan these are the Rabi and Kharif seasons, each lasting 4-5 months from sowing to harvesting. Farmers might, for example, grow wheat in the Rabi season and rice in the Kharif season. So if a farmer has a farm of 8 acres, he might farm 5 acres of it which would be the total cultivated area. But if he farms the 5 acres once in the Rabi season and once in the Kharif season, then the overall cropped area, or the GSA, will be 10 acres. Essentially it is a measure of how many crops grow on how much land in a given year.

Of course when it comes to actual farm economics, it is never so simple. In reality, farmers need to rest their lands. Sometimes they prefer planting only one big crop such as wheat and using the land for a cover crop

or some vegetables the rest of the year. Other times they rotate different fields that they have, so it is far from true that if wheat is grown on 5 acres then rice will be grown on the same five acres again However farmers are clearly trying to get the most out of the land they have possible.

In 2010 the total cropped area in Pakistan was 67.9 million acres. The total area available on which crops were grown was 42.6 million acres. This gives us a GSA percentage of 159%. In 2024, the total cropped area was 82.7 million acres out of a total available area of 52.7 million acres. That gives it a GSA percentage of 156%.

The values have not changed particularly. Also keep in mind that the 6.4 million acres that have been added since 2010 are new, and fresh land often takes time until it is ready for multiple crop rotations in a year. As such, the overall amount of crop rotation and gross cropping might actually have increased.

Crop by crop

The initial impressions of the census tells a story of a farming community that is trying to keep up with rising demand. The number of farms have increased in Pakistan but the average size of each farm has fallen by 1.3 acres. The fragmentation has resulted in lower margins and poor farm economics. An even bigger challenge is that despite the increasing area on which crops are being grown, the yield is either decreasing or has remained stagnant. In the case of some crops, such as rice and particularly cotton, their acreage has also shrunk as farmers shift towards crops that give them better immediate outcomes and yields.

The state of crop production this year has been abysmal. Back in June, the National Accounts Committee (NAC) released the latest GDP data for Pakistan. Immediately there was attention on the fact that the NAC was indicating Pakistan had a GDP growth rate of 2.68%. This was a revision from the government’s previous GDP growth projections which had predicted GDP growth rate at around 3.6% for 2025.

The problem is even these revised projections from the government of 2.68% are far from accurate. At best, they are naive and hopeful. At worst they are deliberately misleading. In the numbers the government has released, GDP growth in the first three quarters has been 1.37%, 1.53%, and 2.4% respectively. While this indicates an increase in the growth rate with every quarter, it is still well short of the government’s projections of 2.68%. In fact, the average growth for these first three quarters is less than 2%. It was pointed out almost immediately by a number of individuals that the government was

relying on a significantly increased projection of GDP growth in the ongoing fourth quarter being 5.47%

The projection of a sudden tide changing final quarter raises questions. On top of this, there is really very little in the NAC’s report that explains why the government would be this hopeful. Perhaps nothing indicates the dire situation Pakistan’s economy is facing more than the state of the agricultural sector. Overall, the agriculture sector increased by a very meagre 0.56% in this year. This growth is not only partially based on projections, it is also only possible because Pakistan’s livestock sector saw a decent rise of 4.7% with fishing also increasing by 1.7%. What is concerning, however, is that major crops saw huge dips in production. Through a combination of senseless policies, water shortages, and increasing input costs, major crops crashed out and declined by 13.5%.

Wheat

Take the example of Pakistan’s biggest crop. Wheat has remained the undisputed darling of farmers all over the country. What is unfortunate is that farmers are getting less wheat per acre in the past few years, and the federal government seems completely clueless about basic matters such as how much area wheat is actually grown in Pakistan.

In 2024, wheat accounted for 43.3% of the total cropped (GSA) area of 82.7 million hectares. That means wheat was grown on just over 35 million acres. Since wheat is only grown once per season, that means it is grown on 35 million acres out of the total cultivated area of 52.7 million, making it a crop grown on more than half the cultivated land in the country in 2024. Since the survey for the census began in January this year, these are the numbers for 2024-25

According to the federal government, which reported this through the Federal Committee on Agriculture, wheat was being grown on 23 million acres this year — which is significantly less than the 35 million acre figure derived from the census. The FCA’s

When farm sizes are small they reduce the scale of the economy and minimize the prospects of corporate farming. But the overall results of the census are encouraging

Ahsan Iqbal, Minister for Planning and Development

numbers do not make further sense when you look at the crop reporting numbers of the Punjab government, which has reported that farmers in Punjab have planted wheat on 22 million acres alone.

This discrepancy in data significantly changes what we understand about Pakistan’s wheat yields. Look at it this way. In 2023-24, the total production of wheat in Pakistan was 31.58 million tonnes grown on around 35 million acres. That would give a total yield of 0.92 tonnes per acre. This is significantly less than the earlier estimated range of around 1.3 tonnes per acre based on the FCA’s data.

Compare these yields with 2010. In 2010, wheat accounted for 42% of the total cropped area of 67.9 million acres. This meant wheat was grown on just over 28 million acres. The production for this year was 23.3 million tonnes. This would indicate that the yield for this year was 0.83 tonnes per acre. The yield was lower in 2010 but not by much. And this is compared to 2023-24, a year that saw an above average year in wheat production. Even that slight blip was not to last long. The government gave a low support price under pressure from the IMF. Arguments can be made each way regarding whether a support price is a good idea or not. What is more important is that the current year 2024-25 has seen a dip in the amount of

Rice production

Total area under rice cultivation in 2010 = 9.36 million acres (14% of total)

Total area under rice cultivation in 2024 = 10.6 million acres (12.9% of total)

Total rice production in 2010 = 11.1 million tonnes (1.18 tonnes per acre)

Total rice production in 2024 = 14.7 million tonnes (1.38 tonnes per acre)

area under wheat cultivation. The estimated wheat production is around 28 million tonnes, which would mean the per acre yield is around 0.80 tonnes — less than what it was in 2010.

Clearly farmers are growing more wheat than before for a larger population. They have also seen an improvement in yield here, although this might be a year-to-year difference. If the available data is to be trusted (which it very much should not be – at least not to a fair degree of accuracy) then the yield has been pretty stable in the past five years. However, farm economics have continued to suffer with no introduction of new wheat varieties.

Wheat is the perfect example of what has gone wrong in Pakistan’s agricultural sector in the past 15 years. Farm sizes are decreasing. In Pakistan, the average size of a farm is 5.1 acres now. In the United States, for example, the average size of a farm is 444 acres. The US is an anomaly because they have successfully adopted the corporate farming model. The comparison with Pakistan is simply to illustrate that large farms as the norm is not out of the realm of possibility. The one thing that can be learned from the US is farm mechanisation. The reason their farm size is so large is because a 100 acre farm can easily be managed and run by 2-3 people. It is often small families that run these sprawling establishments because they have the machinery to run them. They have the machinery because banks finance the machinery as well as insure their crops.

Rice

Look at what has happened to the rice crop. Somehow the government’s reported numbers on rice acreage add up (minus some minor discrepancies) with the numbers released in the census. The total area under rice cultivation in 2024 was 10.6 million acres, which makes it 12.9% of the

total cropped area. As a percentage, this is down from 2010 when rice was grown on 9.36 million acres, making it 14% of the total cropped area. Overall the area that is under rice cultivation has not increased by much. Rice has actually seen an improvement in yield. In 2010, the total rice production was 11.1 million tonnes accounting for 1.18 tonnes per acre. In 2024, the total production was 14.7 million tonnes giving an overall yield of 1.38 tonnes per acre.

Even within this sector, however, the increased yields represent an unfortunate shift. The yield has increased because Pakistani farmers have been shifting away from Basmati rice, which dominates the European market and is also very popular in North America. Instead, they have been growing the higher yield Japonica and other small grain varieties that they export to the US. In Pakistan, as far as domestic cooking is concerned, Basmati is exclusively preferred. In the last year alone, however, the export of non-Basmati rice increased by 32% to over 4 million tonnes. From both a food security perspective and an export perspective, Basmati rice is clearly on a downturn. Higher yield but lower quality varieties are behind the increase in yields. Basmati, what Pakistan is famous for and is marketable to the world, has consistently seen a decline in yields and also in areas under yield. Once again there have been no new seed varieties in Basmati for decades.

Cotton

Perhaps nothing represents the dilapidation of Pakistani agriculture more than the woes of cotton in Pakistan. In fact, the fate of cotton has seen a particular decline exactly in the 15 years since the last census was released. For decades, it was the favored crop of millions of farmers, an economic staple that supported the textile mills of Faisalabad and Multan and Karachi. During its golden era, from the 1980s through the early 2000s, cotton was the lifeblood of Pakistan’s largest export industry. In 2008, Pakistan achieved a record output of 15.6 million bales. Farmers grew it with confidence.

Are under cultivation

Total farm size in 2010 = 52.9 million acres

Total farm size in 2024 = 59.3 million acres

Total cultivated area in 2010 = 42.6 million acres

Total cultivated area in 2024 = 52.7 million acres

Total cropped area in 2010 = 67.9 million acres

Total cropped area in 2024 = 82.7 million acres

Mill owners purchased it without hesitation. The system worked.

Then it began to unravel.

The global recession of 2008 was a breaking point. High energy costs, currency depreciation, and an increasingly expensive business environment squeezed Pakistan’s textile industry. Mills began to shut down. From over 450 units in 2009, the number fell to around 400 by 2019. Domestic demand for cotton started to shrink. With fewer buyers, farmers began to question the crop’s viability. Cotton began to lose ground to alternatives like sugarcane and maize.

But the structural flaws in cotton farming itself were just as damaging. Poor quality seed, unchecked pest infestations, lack of investment in research, and insufficient irrigation support made cotton yields increasingly unpredictable. For many farmers, the crop was no longer worth the risk.

As a result, the country has gone from being a proud cotton exporter to one that now imports most of the cotton used in its own textile industry. In the first nine months of the 2024-25 cycle alone, Pakistan imported over 300 million kilograms of cotton yarn and two million bales of raw cotton. The cost to the economy runs into billions of dollars. This is money Pakistan cannot afford to lose.

The numbers from this year’s census are telling. The total area under cotton cultiva -

Cotton production

Total area under cotton cultivation in 2010 = 9.5 million acres (14% of total)

Total area under cotton cultivation in 2024 = 6.5 million acres (7.9% of total)

Total cotton production in 2010 = 9.25 million bales (1.42 bales per acre)

Total cotton production in 2024 = 5.2 million bales (0.8 bales per acre)

tion in 2010 was 9.5 million acres which accounted for around 14% of the total cropped area in the country. In 2024, the total cropped area of cotton in the country was 6.5 million acres according to this year’s census, accounting for 7.9% of the total cropped area. Cotton is being grown on nearly half of it once upon a time. This is very much reflected in the yield as well. In 2010, the yield was 9.25 million bales at 1.42 bales per acre. In 2024, the yield was 5.2 million bales at 0.8 bales per acre.

Shrinking size and ticking time

The census was long awaited. It is not ideal that a country which still proudly wears the agrarian label has not had an agricultural census for 15 years. We are not even considering here the fact that the livestock census that came with it is the first since 2006. There is a lot that the survey leaves to be desired. It has made no record of what the average age of farmers is, or how many people on average work the land per acre. There was no machinery census done either.

The data that was shared shows a farming community desperate to try and keep up, but unable to get the kind of yields required to keep Pakistan food secure. On top of that, the size of farms has been shrinking and the disparity between large and small farm owners has continued to grow. When you look at every crop individually, they appear to be neglected and suffering.

By now Pakistan’s agriculture is a race against time. The government needs to get its act together because up until this point the one thing this country has had going for it is the ability to feed itself. If that also continues to erode the way it has in the past 15 years, Pakistan will be staring down a dark and lonely road. n

MCB Funds nearly triples revenue on the back of rising markets

The significant increase in topline revenue did not come from capital gains, but instead higher fees earned by having a larger base of assets under management

Profit Report

MCB Arif Habib Savings and Investments – now known as MCB Funds – has delivered one of its strongest financial performances in recent memory. For the financial year ended 30 June 2025, the asset manager reported total revenue of Rs4.79 billion, up from Rs1.84 billion a year earlier – an increase of roughly 160%, or “nearly triple” on the year. The step-up was led by management and investment advisory fees, which surged to Rs4.45 billion (FY24: Rs1.61 billion), alongside higher sales-load and related income of Rs259.6 million (FY24: Rs193.7 million). Gains on investments were also positive, though smaller in absolute terms.

The stronger top line filtered through to profits. Profit before tax rose to Rs2.75 billion (FY24: Rs1.27 billion), while profit after tax came in at Rs1.76 billion, up from Rs861 million the prior year. Earnings per share more than doubled to Rs24.42 (FY24: Rs11.96). The board also recommended a final cash dividend of Rs3.5 per share (35%) – on top of an interim dividend of the same amount paid during the year – implying a full-year payout of Rs7.0 per share. On headline numbers, the business is

now solidly back in high-profit territory.

Beneath the headline, the composition of costs changed meaningfully. Administrative expenses climbed to Rs1.30 billion (FY24: Rs778 million), reflecting scale-up and inflation effects, while selling and distribution expenses expanded sharply to Rs1.29 billion (FY24: Rs117 million). In turn, total operating expenses reached Rs2.58 billion versus Rs896 million last year. The company also booked other expenses of Rs62.5 million (down from Rs191 million in FY24). Despite the heavier cost base, stronger fee income and share of profit from associates (up to Rs623 million from Rs532 million) supported the earnings jump. In absolute terms, profitability doubled; in margin terms, however, the surge in distribution spend nudged the net margin lower versus FY24, a reminder that fast growth often comes with higher customer-acquisition and distribution costs.

For shareholders, the picture is straightforward: a much larger revenue base, a doubling of after-tax profit, and a resumed dividend stream that, taken with the interim payout, represents a respectable payout ratio against full-year EPS. Whether FY26 can sustain similar growth will depend on what happens in Pakistan’s capital markets – the fountainhead for management fees – and on

how efficiently the firm can convert scale into durable, high-margin earnings.

The market tailwind: Pakistan’s equities boom

MCB Funds’ results did not occur in a vacuum. They landed at the end of a year in which Pakistan’s equity market was among the best performers globally. The KSE-100 Index finished FY25 near a historic high, with most reputable tallies putting the full-year return between ~56% and ~60% in rupee terms. That is an exceptional follow-through after FY24’s record rally and goes a long way towards explaining why asset-management revenues –which track net asset values and client contributions – swelled so dramatically.

On 30 June 2025, the KSE-100 closed at 125,627, an all-time high reading that capped a year of monetary easing, improving macro expectations under an IMF programme, and a rotation by local investors back into risk assets. Brokerage tallies and media round-ups attribute the outperformance to a combination of lower secondary-market yields, reform progress, and heavy domestic institutional buying – a backdrop tailor-made for mutual funds that

charge fees on growing assets.

Multiple outlets described equities as the best-performing asset class in FY25, outpacing gold and T-Bills; some houses measure the FY25 KSE-100 gain at ~60% and the two-year combined return at ~200%+ – a once-in-a-generation surge that has pulled fee income higher across the asset-management industry. In such cycles, the impact on asset managers is non-linear: rising prices boost AUM; rising AUM increases fee accruals; and strong performance draws new inflows, creating a virtuous loop until the market cools.

From AHI to MCB Funds: a short history of the franchise

The entity investors know today as MCB Funds began life in 2000 as Arif Habib Investments (AHI), founded by the Arif Habib Group. In 2011, AHI merged with MCB Asset Management Company, forming a joint platform that combined a strong retail distribution network through MCB Bank with the capital-markets DNA of the Arif Habib Group. The merged company adopted the name MCB-Arif Habib Savings and Investments Limited.

Subsequent rating reports and company disclosures reiterate that the firm is SECP-regulated, holds the full suite of licences (asset management, investment advisory and pension fund management), and has consistently maintained high AM1 asset-manager ratings from the Pakistan Credit Rating Agency (PACRA). Over the years, MCB Bank’s stake has increased, strengthening the link between the fund house and one of Pakistan’s most profitable banks, while the Arif Habib Group remains an important strategic shareholder. This blend of distribution heft and market expertise has underpinned the firm’s growth and brand positioning.

The strategic logic of the 2011 combination remains relevant in 2025. Bank-anchored asset managers can funnel savings products to a much broader customer base via branch networks and digital channels, while market-savvy sponsors help keep product design, execution and risk management sharp. The latest results suggest the original merger thesis – synergies from scale and distribution – is still paying off.

The industry context: what a bigger market means for AMCs

Pakistan’s asset-management industry has been expanding rapidly, helped by digitisation, money-market product innovation, and a return of risk appe-

tite. Estimates based on MUFAP data place industry AUM in the Rs3.8–4.3 trillion range across 2025, with money-market and income funds dominating, but equity funds gaining share during the market rally. While a single “official” number fluctuates month to month, the trend is unambiguous: the pie is larger, the product shelf is broader, and investor participation is gradually deepening.

As the industry grows, competitive dynamics intensify. Fee rates are under constant pressure globally, and Pakistan is no exception. Asset managers therefore rely on three levers: scale, product mix (including higher-margin strategies such as equity, balanced, and multi-asset funds), and operating efficiency. The FY25 results from MCB Funds hint at all three in action – a larger asset base in buoyant markets; mix benefits from equity NAV appreciation; and the willingness to spend more on distribution to capture flows, which shows up as higher selling expenses but can lock in long-term clients.

Another notable shift is the growing role of pension and Shariah-compliant funds – segments where Pakistani AMCs have an intrinsic advantage. As more Pakistanis look to formal retirement products and as Islamic finance remains mainstream, fund houses with depth in these areas can differentiate on both values and performance. For bank-sponsored AMCs, pension and Islamic products also cross-sell naturally into retail banking franchises.

For the industry, a buoyant PSX is both a blessing and a test. It brings in investors and raises AUM – but also raises the bar for client servicing, compliance, liquidity management, and performance communication. The FY25 experience, where the KSE-100 outperformed every major asset class, is precisely the kind of cycle in which AMCs build franchises –provided they keep service quality high and mis-selling low.

Returning to the FY25 statement, two items stand out as indicators of sustainability.

First, management and investment advisory fees now account for the lion’s share of revenue – a sign that core business health (rather than one-off gains) drove the earnings jump. This is exactly the line item investors want to see expand in a rising-market year, and it did, to Rs4.45 billion. Second, the share of profit from associates (Rs623 million) remains a meaningful contributor – helpful in lifting pre-tax profit, but also a reminder that consolidated earnings include non-operating elements that can swing with market cycles.

On the cost side, the outsized rise in selling and distribution spend tells us the firm leaned into growth – acquiring customers, pushing products, and perhaps incentivising distribution partners. If those gross inflows

remain sticky, the FY25 expense step-up should yield operating leverage in FY26: fee income scales naturally with AUM, while distribution costs may normalise as a percentage of assets.

Cash generation improved too. Net cash from operating activities climbed to Rs1.44 billion (FY24: Rs551 million), giving the company more flexibility on dividends and reinvestment. That cash-flow support, plus a stronger equity base, should keep balance-sheet risk low even if markets wobble.

Through the investor’s lens

For equity investors following the listed asset-management space, FY25 is a case study in how earnings can rerate quickly when markets turn. Put simply: fee businesses are geared to market direction. In downturns, revenues compress and operating leverage runs the wrong way. In upturns, the reverse is true – and faster. With the KSE-100 up roughly ~60% for the year and hitting a record close, it is unsurprising that MCB Funds turned in near-tripled revenue and doubled earnings.

Yet the FY25 P&L also warns against extrapolating one year into infinity. Distribution costs will need to be managed prudently in FY26; and if the market consolidates, fee growth may slow. The dividend – Rs7.0 per share in total for the year – signals confidence, but the company will want to preserve balance-sheet flexibility should volatility return. MCB Funds rode a powerful market tailwind in FY25 and executed aggressively to capture it. Revenues nearly tripled, profit doubled, and cash generation strengthened. The KSE-100’s stellar year amplified AUM and fee accruals, while the firm’s distribution push – visible in higher selling expenses – aimed to convert a cyclical rally into long-term clients. History suggests the franchise is built for such cycles. Born as Arif Habib Investments and reshaped by its 2011 merger with MCB AMC, the company blends a bank’s retail reach with a market group’s capital-markets acumen – a combination that has kept it near the front of Pakistan’s asset-management pack for two decades.

For the industry at large, FY25 was the kind of year that expands the investing public and pulls savings into capital markets – with MUFAP-tracked AUMs scaling up to new highs and equities reclaiming their place as the best-performing asset class. If reforms stick and rates ease further, FY26 could still be constructive. But whether the next year is as euphoric as the last, the lesson of FY25 is clear: when Pakistan’s markets run, asset managers sprint – and MCB Funds just proved it. n

Engro steps up lending and direct sales to farmers

The company’s inventories have been piling up as farmers struggle, so it is stepping up efforts to move further downstream in its own value chain

EProfit Report

ngro Fertilizers has begun to rewrite how it reaches the people who ultimately determine its fortunes: Pakistan’s smallholders and medium-scale cultivators. The company is rolling out direct-to-farmer retail outlets and pairing them with a programme to extend formal-sector credit to growers in partnership with Bank Alfalah. Together, these moves aim to reduce the layers of intermediaries that have long separated Engro from the farm gate – layers that add cost, blunt incentives, obscure demand signals, and often capture a disproportionate share of the margin between factory and field.

On the distribution side, management confirmed that Engro has opened four retail stores – branded “Engro Markaz” – since late 2024, with the explicit goal of ensuring the “smooth supply of products” directly to farmers. The stores augment the traditional dealer network rather than replacing it wholesale, but the strategic intent is clear: build a channel where Engro can set prices transparently, offer agronomic guidance, and tighten feedback loops on demand. The company has also adjusted trade terms and introduced targeted discounts – sometimes as much as Rs150 per bag – to support offtake when market conditions soften.

On finance, Engro is leaning on its own corporate relationships and credibility to bring farmers into the formal credit system. During the latest analyst call, management highlighted microcredit through Bank Alfalah as a centrepiece of its farmer-support initiatives, designed to lower the cost of capital and smooth working-capital gaps that routinely keep growers from applying the optimal dose of nutrients at the right time. The logic is simple: if cheaper, predictable financing is available at planting and top-dressing stages, farmers buy closer to agronomic recommendations, yields improve, and the company sells more fertiliser with fewer distressed discounts.

These two moves – retail disintermediation and credit enablement – come at a pivotal moment. After a difficult 2024 for margins and a soft start to 2025 demand, Engro’s second quarter showed renewed operating momentum: net revenue rose 28% year-on-year to Rs50.4 billion, gross margin rebounded to 31% (from 20% in the same period last year), and earnings per share jumped to Rs4.17, enabling a Rs4.25 per share dividend for the quarter. The company’s 2024 full-year revenue had climbed to Rs256.7 billion (up 15% YoY), but full-year gross margin slipped to 28% before improving again in 2QCY25 as operations normalised. Management is explicit that farm economics remain under stress, so the company is meeting the challenge by closing the distance – both physical and financial –between its factories and Pakistan’s farms.

Farmers on the back

foot: weak

yields, cash crunch, and rising stocks

If Engro is changing how it sells and finances fertiliser, it is because farm economics are genuinely strained. Management reiterated on multiple occasions that low crop yields, erratic weather, and the limited pricing power of farmers have depressed offtake relative to historical norms. Even with stable urea pricing and various support initiatives, liquidity constraints at the farm level have persisted, prompting Engro to flex trade terms and roll out the selective discounts noted above.

The numbers tell the story. Despite an impressive 40% year-on-year jump in Engro’s urea sales to 431,000 tonnes in 2QCY25, stocks in the system continued to build. Engro’s own urea inventory rose to 563,000 tonnes by end-June 2025, up from 431,000 tonnes a year earlier, as offtake lagged behind production. Company guidance suggests that – absent exports – the industry’s inventory could stay north of one million tonnes by December 2025; at mid-year, analysts estimated

~1.3 million tonnes of urea were already sitting in warehouses across the country. In the DAP segment, international prices rose 23% yearto-date while domestic prices did not rise as much, compressing local margins and further complicating dealer economics.

The demand headwinds are not merely cyclical. Management flagged changes in regulations on support prices and unpredictable monsoons as structural challenges that could keep offtake subdued in the second half of 2025. This is why the company is simultaneously seeking permission to export some volumes – discussions with relevant authorities are ongoing – even as it tries to stimulate local sales through retail and financing initiatives. The aim is to prevent inventories from becoming a drag on working capital while keeping farmers supplied and engaged.

The cost advantage –and why it does not always reach the farmer

Pakistan’s urea is significantly cheaper than world-market prices. As of the latest briefings, Engro and its peers estimate a local–international price delta of roughly Rs3,600 per bag, meaning domestic urea trades at a ~44% discount to international levels. The gap exists largely because domestic gas feedstock for urea –sourced from state-controlled fields – has historically been priced well below international parity. That policy is deliberate: fertiliser is an input into food security, and the state subsidises it upstream.

But the existence of a cost advantage is not the same as farmers capturing it. In practice, multiple linkages stand between Engro’s plants and the person applying urea on a two-acre plot: primary distributors, sub-dealers, village retailers, informal credit providers who bundle financing with product, and the logistics costs embedded in each hop. In good years, this chain is an efficient allocator of stock; in tough years, it absorbs more margin

and slows down both price transmission and offtake.

That is why Engro is building a direct retail presence. Even a small network of company-owned stores can set reference prices, showcase bundled offers (for instance, pairing urea with DAP or micronutrients at agronomically sensible ratios), and create data visibility on which SKUs are moving where and when. Over time, direct outlets also provide a platform for service layers: soil testing, advisory on application timing, and even input-linked insurance, all of which tend to improve agronomic efficiency and therefore fertiliser use intensity. The early “Engro Markaz” pilots are intended to be laboratories for these ideas; their ultimate success will be measured not only by volumes pushed through store tills but by how much price benefit and agronomic guidance they can deliver to the farm gate.

The gas side of Engro’s cost curve is also in focus. To guard against falling field pressures and depletion risks, the company is advancing a pressure-enhancement facility tied to the Mari field. Phase 1 is near completion; Phase 2 is underway, with orders for compressors placed, and Scope-1 of Phase 1 already completed by early August. Management emphasises that this project does not add nameplate capacity; it simply secures continuity of existing production – which, in a market where off-take is the binding constraint, is exactly the kind of insurance policy shareholders ought to want.

Cheaper money for farmers: using Engro’s balancesheet credibility

For decades, formal banking has underserved Pakistan’s farmers.

Smallholders rarely have the collateral or formal income documentation banks require, while branch networks and risk scoring were built for urban commerce rather than rural seasonality. The vacuum was filled by informal lenders – often the same dealers who supply inputs – at interest rates that would make a credit-card issuer blush. The impact on fertiliser economics is profound: high costs of capital compel farmers to under-apply nutrients, delay purchases, or barter field output against input credit, all of which depress yields and drive boom-bust sales patterns for producers.

Engro’s response is pragmatic. The company is partnering with Bank Alfalah to extend micro- and small-ticket credit to farmers who buy Engro products, bringing them into the formal system at lower rates and with clearer repayment schedules. The

company’s brand and supply-chain data improve underwriting, while purchase and repayment records help build a credit history that can be used well beyond fertiliser. In the near term, better access to liquidity should lift offtake; over time, it nudges Pakistani agriculture towards the working-capital rhythms seen in more formal markets, where input purchases align more closely with the agronomic optimum rather than the cash-onhand constraint.

There is also a risk-management dividend for Engro. The more farmers finance purchases through a bank rather than through trade credit embedded in the distributor chain, the cleaner the company’s receivables and the less pressure there is to offer deep off-invoice discounts to move stock. In seasons of weak demand, that cushion matters. It is no coincidence that management has referred to flexible trade terms and selective discounts as tactical tools; the strategic play is to replace dealer credit with bank credit where feasible, using Engro’s data and distribution to make lenders comfortable.

A brief history of Engro Fertilizers

Engro Fertilizers is the fertiliser arm of the Engro group, itself one of Pakistan’s most diversified industrial conglomerates. The fertiliser business traces its roots to the 1960s and later became part of Engro Corporation after a landmark management buy-out in 1991. As a separately listed entity, Engro Fertilizers Limited (EFERT) today operates one of the country’s major urea complexes, marketing under the widely known “Engro” and “Engro Zarkhez” brands and distributing DAP and other nutrients through a nationwide network.

The company’s financial profile reflects a heavy industrial core with periodic exposure to global commodity cycles and local policy. In CY2024, Engro Fertilizers reported net sales of Rs256.7 billion (up 15% year-on-year) on which it earned EPS of Rs21.16 (up 8% YoY), even as gross margin compressed to 28% due to cost and pricing dynamics. The momentum improved in 2QCY25, where gross margin recovered to 31%, operating profit rose 188% year-on-year, and profit after tax more than tripled from the prior year’s quarter, allowing for a quarterly dividend of Rs4.25 per share. Those results provided breathing room – and the credibility – to pursue structural fixes in distribution and farmer finance.

Strategically, Engro has tended to invest in reliability (gas security, plant efficiency) and brand (farmer loyalty programmes, agronomy support) rather than in headline-grabbing capacity expansions. The current project pipeline, centred on the Mari pressure-enhance-

ment facility, underscores that bias: keep the base humming, protect the low-cost position, and use commercial innovations – like the Engro Markaz and the Bank Alfalah partnership – to unlock growth where the bottlenecks actually are.

What to watch next

Three markers will show whether Engro’s strategy is working:

• Inventory drawdown without margin collapse. The acid test is whether Engro can reduce stocks – its own and system-wide – without resorting to deep discounts. If the Markaz outlets and Bank Alfalah lines do their job, sell-through should rise in kharif and rabi windows without eroding price realisation. Early signs are mixed but improving: Q2CY25 saw margin recovery and share gains, but industry inventory remains elevated.

• Export valve. Management has held discussions with the ministry regarding urea exports as a safety valve. Any approval will depend on a formal demand-supply review; pricing would likely sit near global benchmarks, turning domestic cost advantage into foreign exchange and creating room in warehouses before the next application season.

• Scale and scope of retail. Four stores are a pilot; the question is whether Engro can scale the format across agro-ecological zones, add advisory and services, and integrate credit and payments in ways that increase farmer stickiness. A small, profitable network with high data yield might beat a sprawling footprint with thin economics. Either way, direct retail is here to stay.

Engro Fertilizers’ latest briefings make one thing explicit: the bottleneck is no longer at the plant. It is in the distribution maze between factory and field, and in the financing gap that forces farmers to under-invest in nutrients when they most need them. The company’s response – open your own tills and bring a bank to the farm – is as old-fashioned as it is modern. Old-fashioned because it harks back to a model where the producer knows the customer by name; modern because it layers data, finance, and advisory on top of bags of urea.

With gross margins recovering in 2QCY25, market share rising, and projects to secure gas on track, the company has bought itself time to let these commercial innovations work. The stakes are larger than one quarter: if Engro can prove that formal credit plus direct retail lift yields and stabilise offtake – even in a challenging year – it will not only protect its own P&L but also shift the structure of Pakistan’s fertiliser market in ways that are better for farmers and, by extension, national food security. That is a story worth watching through the next planting season and beyond. n

Pakistani meat to finally be available at Carrefour in Dubai

The Organic Meat Company has landed the contract to start selling at the selective French retailer’s UAE stores after a decade-long effort

Profit Report

For more than a decade, the founders of The Organic Meat Company Limited (TOMCL) have nurtured a singular ambition: to see their products on the shelves of Carrefour, the French-origin hypermarket giant, in Dubai. It was a goal they talked about in the early days of the business, back in 2010, when they were still proving to themselves and to the market that Pakistan could produce export-grade, halal-certified meat for the most discerning buyers.

That ambition has now been realised. TOMCL has signed a contract to supply meat to one of the largest retail grocery store chains in the United Arab Emirates, operated by Carrefour’s local affiliate, Majid Al Futtaim (MAF). For the company, the deal is not just another line item in its export ledger; it is a symbolic validation of years of strategic positioning in the competitive world of Middle Eastern food retail.

Carrefour stores in the UAE are known for exacting sourcing standards. Securing shelf space there means meeting rigorous benchmarks for quality, traceability, halal certification, and supply chain consistency — all while competing with established suppliers from Australia, New Zealand, and South Ameri-

ca. The TOMCL management believes this contract could open the door to wider regional retail penetration, particularly in other Gulf Cooperation Council (GCC) markets where Carrefour operates.

“This is what they always aimed for,” said one person familiar with the founders’ thinking. “They wanted to make Pakistan’s premium halal meat a regular fixture for Gulf consumers who care about quality and authenticity. Carrefour was always on that list.”

A 15-year journey of growth and discipline

Founded in 2010, The Organic Meat Company positioned itself from day one as an export-oriented, halal-certified meat processor, capable of meeting the most demanding international standards. Based in Karachi, TOMCL built its facilities to comply with certifications recognised across the Middle East, Southeast Asia, and beyond.

The company’s early years were about proving capability – to regulators, and to buyers. In an industry where reputation matters as much as product, TOMCL spent heavily on establishing robust cold chain logistics, traceable sourcing from selected livestock farms, and compliance with hygiene protocols that met or exceeded importing country requirements.

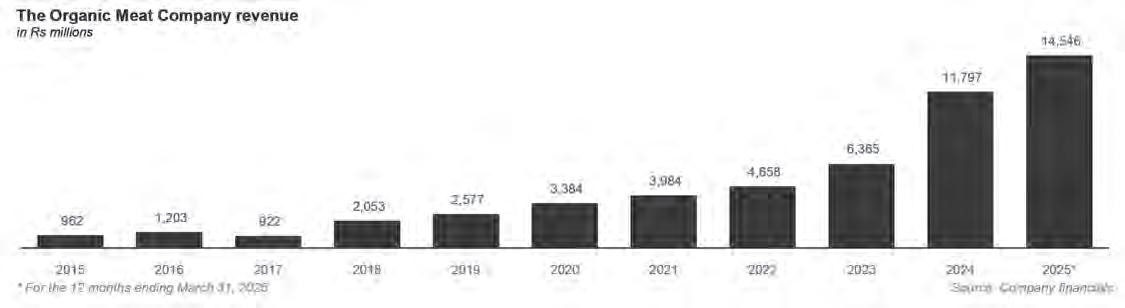

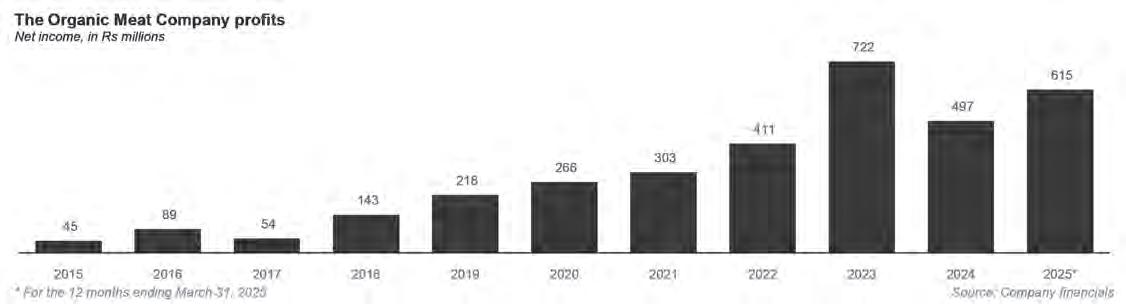

The financials tell the story of steady ex-

pansion: From under Rs1 billion in revenues in 2015, TOMCL is now on track to cross Rs14.5 billion in 2025. Even with occasional dips in net income – such as in 2024 when margins compressed due to expansion costs – the longterm trajectory is upward.

TOMCL’s growth has come from a mix of bulk export contracts to the Middle East, specialty orders to premium hotel and restaurant clients, and more recently, moves into value-added meat products like ready-tocook cuts.

Carrefour in Dubai: the Majid Al Futtaim connection

To understand why this deal is significant, one must understand Carrefour’s position in Dubai’s retail landscape. The French hypermarket brand entered the UAE in 1995 through a regional franchise agreement with Majid Al Futtaim Holding (MAF), the Dubai-based retail, leisure, and real estate conglomerate. Under MAF’s stewardship, Carrefour has grown to dominate the UAE’s grocery market, operating dozens of hypermarkets and supermarkets, both in prime urban locations and inside the region’s largest shopping malls. Carrefour UAE is known for its wide product

range, from local fresh produce to premium imported goods.

It also has a strong brand trust, particularly among the UAE’s diverse expatriate population. And it offers competitive pricing, leveraging scale to keep prices in check.

Its meat aisles typically feature a mix of regional and imported suppliers, with products sourced from Australia, New Zealand, South Africa, India, and occasionally Pakistan, but usually through indirect channels. TOMCL’s direct supply deal means its branded meat products will be part of Carrefour’s official offering, placing them alongside global competition in one of the Middle East’s most scrutinised retail environments.

Pakistan’s meat export ascent

Over the past two decades, Pakistan’s meat export sector has evolved from a small-scale industry to a significant foreign exchange earner. Exports of meat and meat products have risen from under $100 million in the early 2000s to over $500 million annually in recent years. The Gulf states – especially the UAE and Saudi Arabia – have been the mainstay markets.

The drivers behind this growth include its halal advantage. Importing from Pakistan ensures compliance with halal slaughter protocols with a degree of comfort that cannot

be replicated by majority-Catholic Brazil, the global meat export powerhouse. Pakistan also has shorter shipping times to Gulf ports compared to competitors like Australia or Brazil. And it can offer competitive pricing. Lower production costs make Pakistani meat price-competitive, though quality consistency remains a challenge for some exporters.

In this space, TOMCL has distinguished itself as a quality-led exporter, focusing on maintaining standards that appeal to institutional buyers and now — with the Carrefour deal — directly to retail consumers.

The GCC states are among the most food-import-dependent regions in the world. Arid climates, limited arable land, and water scarcity mean that countries like the UAE, Qatar, and Saudi Arabia import 80–90% of their food. Meat, especially beef and mutton, is almost entirely sourced from abroad.

As populations grow and tourism expands, demand for premium meat is rising. The Gulf’s retail and hospitality sectors want reliable suppliers who can offer consistent quality, year-round availability, and halal authenticity.

Pakistan is geographically and culturally well-positioned to fill this role. Its proximity allows for fresher chilled shipments, and its halal certification infrastructure is aligned with GCC requirements. Yet, the sector has historically been hampered by fragmented supply chains, limited processing infrastructure, and inconsistent quality control.

TOMCL’s rise — and its Carrefour breakthrough — suggests that Pakistani exporters can overcome these barriers. If replicated by other firms, it could shift the GCC’s sourcing patterns in favour of Pakistan.

Why this deal matters beyond TOMCL

The Carrefour contract is a milestone not only for TOMCL but also for Pakistan’s broader food export ambitions. If a Pakistani meat processor can compete successfully in one of the most demanding retail environments in the Gulf, it signals to other industries — from dairy to fresh produce — that the market is open to high-quality Pakistani goods.

Moreover, in an era when Pakistan’s economy is in urgent need of foreign exchange, diversifying and upgrading export profiles is critical. Moving from bulk commodity exports to branded, shelf-ready products is a step towards higher margins and stronger market positioning.

For TOMCL, the road ahead will involve not just maintaining Carrefour’s confidence, but also using the deal as a platform to enter other high-profile retail chains in the region. For Pakistan, the hope is that this is not a one-off success story, but the start of a broader push into the premium segments of the Gulf’s food market. n

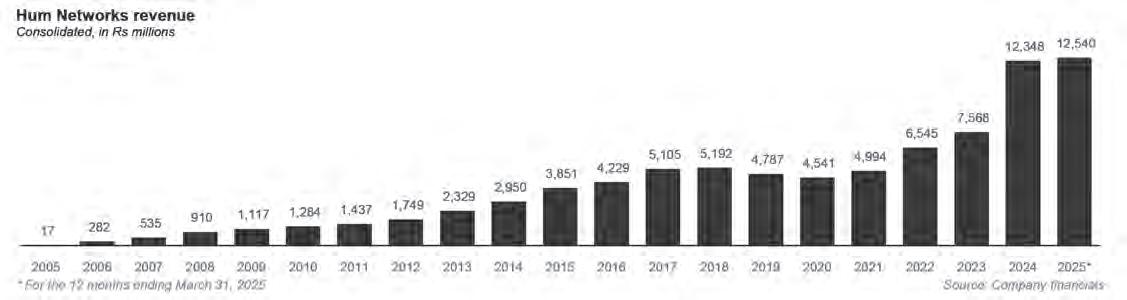

At Hum TV, YouTube is starting to become big business

Revenue from the digital platform accounts for nearly a quarter of the company’s core business, and has been growing faster than traditional advertising

Profit Report

For much of its 20-year history, Hum Network Ltd (HUMNL) has been best known as a conventional broadcaster, producing award-winning Urdu drama serials, running some of the country’s most recognisable entertainment and lifestyle channels, and thriving on advertising revenue. But in recent years, a quiet shift has been taking place in its income streams: digital revenue, particularly from YouTube, has gone from a marginal earner to a significant contributor to the group’s financial health.

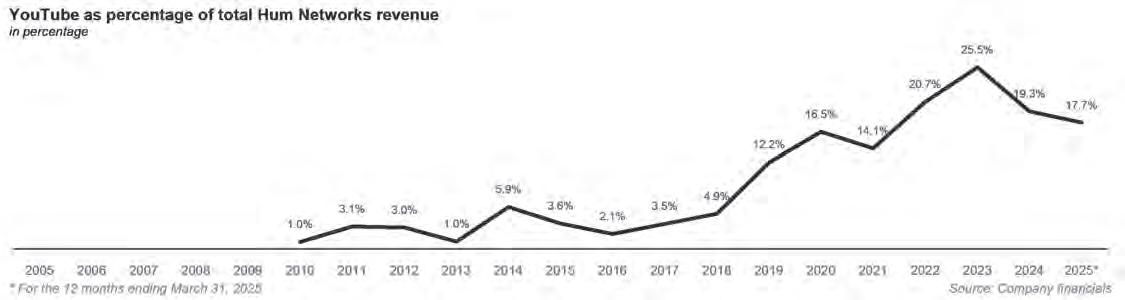

By the end of the financial year ending June 30, 2024, digital revenue and subscription income – which is how the company describes its revenue from YouTube and other digital platforms – accounted for 18% of Hum Networks’ total revenue. That is a remarkable climb from the days when online earnings were little more than a footnote in the accounts.

The company’s official YouTube channel has amassed over 51 million subscribers and 46 billion views, making it the third-largest creator in Pakistan by subscriber count. The revenue line has followed that surge: subscription income has grown at a 10-year compound annual growth rate of 30%, reaching Rs2.2 billion as of the 12 months ending March 31, 2025, the latest period for which data is available.

Yet, the current fiscal year tells a more nuanced story. While digital revenues are still robust, YouTube’s share of total revenue dipped, not because the platform’s earnings fell, but because the revenue pie got much bigger in a different segment.

In 2024, Hum Networks completed the acquisition of Ten Sports, a live sports broadcaster with contracts for events such as the ICC Champions Trophy and Pakistan Super League. Sports broadcasting has little overlap with YouTube monetisation, so its inclusion naturally diluted the digital proportion of total turnover.

Even so, management and analysts see YouTube as central to HUMNL’s future. In an age of shifting viewing habits, where younger audiences spend more time streaming than watching scheduled broadcasts, the digital revenue stream offers scalability, global reach, and recurring income from reruns of timeless dramas.

From a single channel to a media empire

HUMNL’s present-day footprint would have been hard to imagine when Sultana Siddiqui and Duraid Qureshi founded the network in 2004. At the time, Pakistani private broadcasting was still in its growth phase, with only a handful of channels commanding mass

audiences.

The launch of Hum TV in 2005 marked the start of the company’s ascent. It quickly carved out a distinctive identity with high-quality drama serials, often tackling social issues in a way that appealed to both domestic viewers and the Pakistani diaspora abroad. The formula worked: shows such as Humsafar and Zindagi Gulzar Hai became cultural phenomena, cementing Hum TV’s reputation as a hub for emotionally resonant storytelling.

The group expanded steadily:

• Hum Masala (2006) tapped into the booming interest in culinary programming.

• Hum Sitaray (2013) diversified entertainment offerings.

• Hum Films (2014) brought the company into cinema production and distribution.

• Hum News (2018) positioned it in the competitive news broadcasting space.

• Ten Sports (acquired 2023) gave HUMNL a sports broadcasting arm with international rights.

Throughout, the network maintained vertical integration — creating, producing, and broadcasting in-house, ensuring control over content and costs.

Over the past 15 years, net sales have grown from Rs2.95 billion in 2014 to Rs12.35 billion in 2024, a compound growth rate of 15%. Profit after tax rose at an even faster 18% CAGR over the same period.

The content playbook

If there is one thread that runs through HUMNL’s content strategy, it is a focus on premium Urdu-language programming with broad appeal. That means flagship dramas that have a reputation for being well-scripted, high-production-value serials that resonate across demographics. These not only drive prime-time ratings but also enjoy long-tail success on YouTube, where episodes continue to draw millions of views years after airing.

It includes lifestyle programming such as cooking shows on Hum Masala, morning shows, and fashion-related content that cater to a loyal audience segment.

Hum News has positioned itself as a moderate, issues-focused news channel, though it faces stiff competition from larger incumbents.

And while still a smaller part of the business, Hum Films has produced and distributed titles that complement the network’s brand identity.

The formula balances mass-market appeal with brand consistency, ensuring that content travels well internationally. HUMNL’s drama library has been syndicated to audiences in the Middle East, Europe, and North America, often via streaming platforms.

The global trend, and Pakistan’s digital catch-up

The global content industry has been in a state of flux for more than a decade, driven by the rise of streaming and on-demand viewing. In markets like the United States, traditional cable subscriptions have been declining for years, with younger audiences gravitating to platforms like Netflix, YouTube, and TikTok. Advertising dollars are following eyeballs: digital ad spend is growing while traditional TV ad revenues stagnate or shrink.

Pakistan is not immune to this shift, though the pace has been slower due to infra-

structural constraints and the enduring popularity of terrestrial and satellite TV. However, the direction of travel is clear. Digital distribution is becoming increasingly important, not just for reaching younger domestic viewers, but for monetising the vast overseas diaspora that consumes Urdu-language content online.

For HUMNL, YouTube is the tip of the spear in this transformation. Unlike traditional broadcasting, digital platforms offer granular audience data, algorithmic content promotion, and the ability to monetise archives at minimal additional cost. A hit drama from 2016 can still generate revenue today through mid-roll ads, without the need for costly re-airing.

Analysts note that this “evergreen content” monetisation is particularly attractive in markets like Pakistan, where production costs are lower relative to global peers, yet audience engagement can rival or surpass that of larger economies.

The missing OTT piece, and a new arrival

Despite the global trend, Pakistan still lacks a strong local OTT platform to rival Netflix, Amazon Prime, or Disney+. Several 0 attempts have been made, but most have struggled with content licensing costs, payment infrastructure, and scale. As a result, YouTube remains the dominant digital distribution channel for Pakistani broadcasters, including HUMNL.

That may soon change. Industry insiders say a new domestic OTT platform is preparing to launch, backed by a consortium of media and technology investors. If it succeeds, it could offer Pakistani content producers a more controlled, potentially higher-margin distribution outlet — though building an audience to rival YouTube’s scale will be a formidable challenge.

For HUMNL, an OTT platform could be both an opportunity and a risk. On one hand, it would give the company a venue to monetise premium content directly, possibly

via subscriptions or pay-per-view. On the other, it would require competing with its own YouTube strategy, where the audience is already vast and the monetisation model well understood.

The promise of digital revenue is not without its vulnerabilities. HUMNL’s YouTube performance took a hit in mid-2025 when heightened Pakistan–India tensions coincided with a sharp drop in viewership from India, historically a major audience base for the network’s Urdu dramas. Subscriber growth slowed dramatically during that period, underlining the geopolitical exposure of cross-border digital traffic.

There’s also platform risk: YouTube’s algorithms and monetisation rules are beyond HUMNL’s control. Changes in ad policies, recommendation systems, or revenue splits could impact earnings. And while digital ad spend is growing, it can be volatile, subject to broader economic cycles.

Finally, HUMNL still relies heavily on advertising, which made up 61% of revenue in 2024, and the company is exposed to shifts in corporate and government ad budgets.

Looking ahead

Hum Networks’ trajectory over the past two decades has been one of consistent growth, strategic expansion, and brand-building. The addition of Ten Sports diversifies its portfolio, potentially boosting overall revenue and viewership, even if it dilutes YouTube’s percentage share in the short term.

Longer-term, the company’s fortunes will hinge on how well it navigates the ongoing shift from linear broadcasting to digital distribution. YouTube has already proven it can be more than just a side hustle for a Pakistani media company. It is becoming a core pillar of the business. The challenge will be to grow that pillar without undermining the other parts of the house.

For Hum, YouTube is not just the future. It is already here. The question is how big they can make it before the market changes again. n

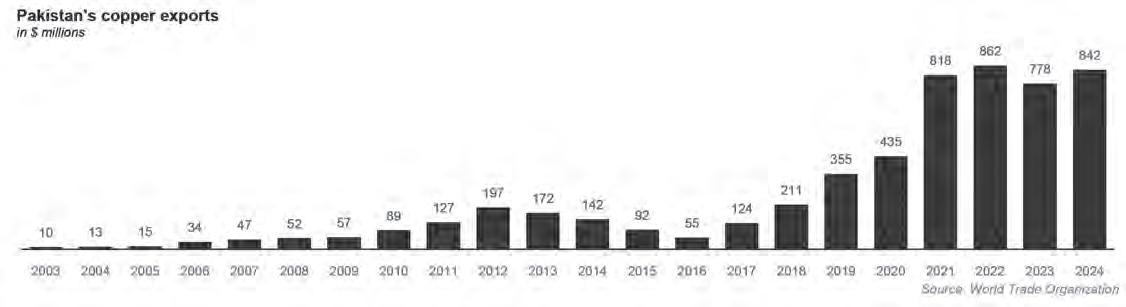

Copper exports from Saindak mine crossed $800 million in 2024

Once a political hot potato, the mine is finally earning Pakistan a meaningful amount of export revenue, with China being the only buyer

PProfit Report

akistan’s copper exports, driven almost entirely by the Saindak mine in Balochistan, crossed the $800 million mark in calendar year 2024, a record high for the project and one of the strongest performances in its chequered history.

Newly compiled trade data shows that copper exports surged to $842 million last year, up from $777 million the year before. That figure caps a remarkable two-decade journey from just $14.6 million in 2005, as the mine’s annual output has grown from tentative beginnings into a central – if still underappreciated – part of Pakistan’s mineral export profile.

Yet despite the political heat surrounding Saindak when the mining lease was first awarded to Chinese operators in the early 2000s, few Pakistanis outside industry and

policy circles have paid attention to how much money it has actually been generating. The project has operated largely outside public scrutiny, its financial flows governed by opaque contracts and periodic extensions negotiated behind closed doors.

A look at the numbers reveals a slow but steady climb in export value during its first decade under Chinese management, followed by sharper rises in the late 2010s and early 2020s as global copper prices surged and production stabilised. By 2021, exports had already crossed the half-billion-dollar threshold; three years later, the $800 million milestone was passed.

A mine that nearly never was

The Saindak Copper–Gold Project, located in the remote Chagai District of Balochistan near the Iranian border, was discovered in the early

1970s through geological surveys conducted with foreign assistance, including the Geological Survey of Pakistan and United Nations agencies. It was hailed as one of Pakistan’s most promising mineral finds: a deposit with commercially significant concentrations of copper, gold, and silver.

But the road from discovery to production was anything but smooth.

Several attempts to develop the mine in the 1980s and early 1990s fell victim to financial constraints, technical difficulties, and the vagaries of global commodity markets. The state-owned Saindak Metals Ltd (SML) oversaw initial development, but Pakistan lacked both the capital and the technical expertise to build and operate the necessary concentrator plant and supporting infrastructure.

By the mid-1990s, with copper prices in the doldrums and domestic fiscal space limited, the government sought foreign help. In 1995, the government was even able to begin

trial production. However, with low copper prices making operations unviable, the project was mothballed in 1996, and the mine lay idle for years.

In 2001, the Metallurgical Corporation of China Ltd. (MCC), a Chinese state-owned enterprise, stepped in with an offer: it would finance and construct the mine and processing plant in exchange for the right to operate it under a lease agreement. With a reported investment of around $350 million, the concentrator was completed and trial production began.

In 2002 – after repeated delays, shifting political winds, and renewed Chinese interest – the MCC began operations under a 10-year lease, marking the true commercial start of the Saindak mine.

Production profile and reserves

The Saindak deposit is not world-class in size, but it is significant by Pakistani standards. Geological estimates put proven and probable reserves at around 412 million tonnes of ore with an average copper grade of 0.5%, alongside small but valuable quantities of gold and silver.

The plant, designed and built by MCC, has the capacity to process 12,500 tonnes of ore per day, producing a copper–gold concentrate that is shipped directly overseas for smelting and refining. Output has fluctuated depending on ore quality and operational efficiency.

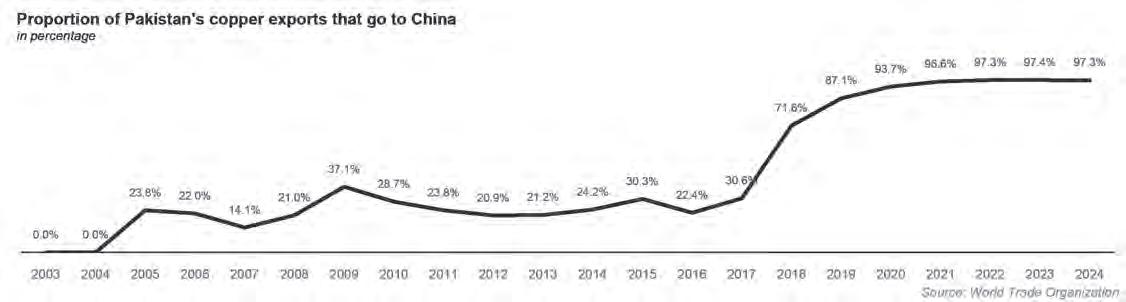

Because the concentrate is exported rather than refined domestically, Pakistan’s export statistics reflect the gross sales value of the semi-processed product, most of which leaves the port of Karachi for China.

China’s hand, and its appetite for resources

China’s role in reviving Saindak cannot be overstated. The project’s resurrection in 2002 came against the backdrop of China’s accelerat -

ing industrialisation and its consequent hunger for mineral resources. MCC’s investment in Saindak mirrored similar deals Beijing was striking across Asia, Africa, and Latin America: providing capital, equipment, and operational expertise in exchange for longterm access to raw materials.

For China, Saindak’s copper output is a modest contribution to its massive import needs – the country accounts for more than half of global copper consumption – but it fits into a broader pattern of securing diversified supply sources close to home. The mine’s location, less than 400 kilometres from the Chinese border at the Khunjerab Pass (albeit across challenging terrain), adds a strategic dimension, though in practice the concentrate travels by sea.

Trade data makes the relationship stark: nearly 100% of Pakistan’s copper concentrate exports go to China. This dependency means that Saindak’s fortunes are tied not just to global copper prices but to Chinese demand and the stability of the Pakistan–China economic relationship.

The Reko Diq question

If Saindak has been Pakistan’s modest but steady copper–gold workhorse, the nearby Reko Diq deposit is its sleeping giant. Located about 50 kilometres from Saindak, Reko Diq is one of the world’s largest undeveloped copper–gold resources, with an estimated 5.9 billion tonnes of ore grading 0.41% copper and 0.22 grams per tonne of gold.