Sazgar’s poised to profit from Pakistanis’ new taste for SUVs

Revenue down at Lucky Core Industries

Revenue up, profits down

As the war continues at TRG, it seems the victor will rule over ashes

There’s a Rs 1.6 trillion shaped hole in the power sector. The race to plug it could be futile

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

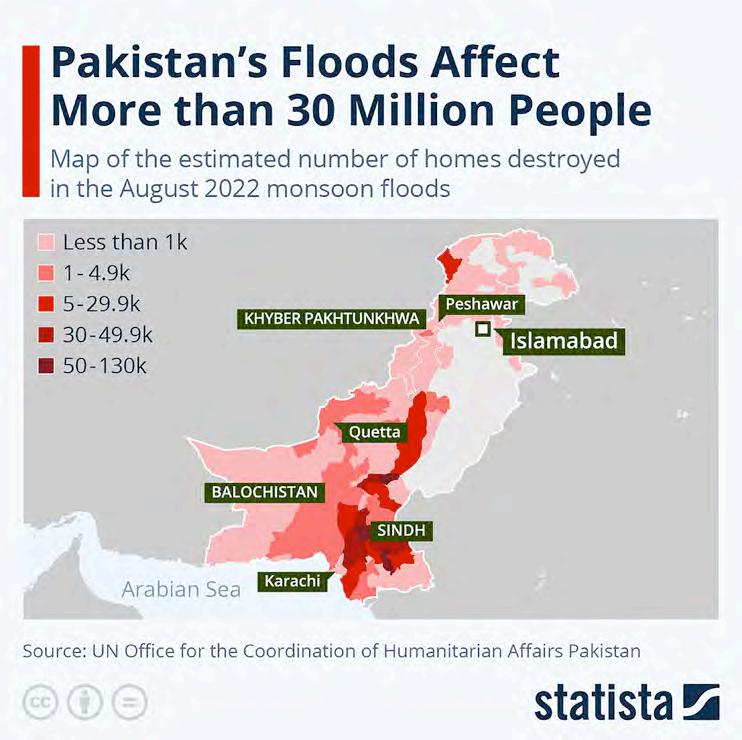

Monsoon death trap

This year’s floods are not an anomaly — they are the new normal

Profit Report

From June to July, at least 234 people died in monsoon related incidents across Pakistan. At least 113 of the casualties were children.

Most of the deaths are caused by roof collapses. The rains come lashing down with such severe violence that water damage can weaken the foundations of homes to a point of collapse. As the rain falls, there are few signs that the roof is at a point of collapse.

In the past few years, the intensity and timeline of the monsoon rains have been changing rapidly. It will only get worse in the days to come. A recent study published in a leading journal called Nature concluded that Pakistan is likely to experience more frequent and severe floods due to extreme rainfall events and human-induced development encro¬aching on floodplains.

It is a problem that may prove to be the most critical for Pakistan in the future.

The monsoon patterns

In Pakistan, the monsoon season isn’t just a weather pattern—it’s a lifeline. For much of the country, nearly 80% of the yearly rainfall comes in a concentrated period from late June to September. This short window is critical for agriculture, which makes up a significant part of Pakistan’s economy. With over 40% of the workforce relying on farming, crops like rice, wheat, and sugarcane thrive or fail based on how much rain falls during these months.

The monsoons are a blessing when they arrive at the right time, filling rivers and reservoirs and giving farmers the water they need to grow crops. However, the delicate balance of nature has been upset by climate change. Take the 2022 floods, for example. Pakistan saw three times the usual rainfall during that year’s monsoon, resulting in catastrophic flooding that killed over 1,700 people and caused $40 billion in damages. Researchers say that human-driven climate change likely intensified the rains by up to 75%, making the floods more severe than they would have been otherwise.

This year, the summer season was followed by flash floods in northern areas, with melting glaciers adding to the chaos. These events only highlighted how vulnerable the country is to extreme weather patterns.

For farmers, this volatility is a nightmare. The crops that were meant to be harvested during one season are often wiped out by unexpected floods, while other parts of the country suffer from droughts. When this happens, food prices soar, and farmers are left to deal with debts they can’t repay.

Pakistan’s economy, especially its agricultural sector, is tied to the monsoon rains. But with the unpredictability of these rains, there’s an increasing risk of floods, crop failures, and economic losses. It’s a reminder that the rain the country once relied on so heavily may not be as reliable as it once was.

A sign of times to come

It was not long ago that Pakistan saw just how damaging an unpredictable monsoon season can be. More than 1700 people were killed in the floods and 79 lakh people

were displaced by the flooding. Nearly 10 lakh people had to move into camps. If we count individuals that suffered loss of crops, livestock, and damage to their homes the direct affectees of the floods come out to over 3.3 crore people — that is nearly 12% of the entire population.

In Sindh, Chief Minister Murad Ali Shah estimated that 90% of all farmers in the province had their entire crops damaged or entirely destroyed. With a similar situation prevailing in both South Punjab and KP, the breadbasket regions of the country were devastated. Outside of Sindh, Balochistan had more than 50,000 houses lost and nearly as many damaged, and more than 700,000 acres of crops worth around $10 million destroyed across the province.

Nearly 70,000 people lost their homes, at least 3200 roads and 149 bridges were destroyed, while upwards of 80,000 livestock animals died in the floods.

In short, climate change resulted in a gargantuan increase in the amount of monsoon

Monsoons 2025

Deaths: 242

Injured: 598

Houses destroyed: 854

Livestock deaths: 208

Rescue operations: 62

rainfall that Sindh and Balochistan received in 2022. The two provinces saw the highest amount of water fall from the skies in living memory, recording 522 and 469 per cent more than the normal downpour this year according to the met department.

And that was one year of extreme destruction. The study mentioned earlier in the story found that the events of 2022 were “a forewarning of elevated future flood risks”. According to the study, the Indus Plain, home to millions, has endured 19 devastating floods between 1950 and 2012. These disasters have swept through an area of 599,459 square kilometers, claiming over 11,000 lives and leaving economic damages surpassing $39 billion. Monsoon rains were a significant contributor to these floods, with nearly half of the events occurring after the 2000s, particularly in the post-monsoon season.

After a prolonged drought, 2022 saw pre-monsoon rainfall spike 111% above the long-term average from 1951 to 2021, leading to a 30% increase in soil moisture in the Indus Basin floodplains. But the monsoon rains that followed, peaking at a staggering 547% above the historical average, exacerbated the crisis. July’s rainfall, recorded at 200mm, was unprecedented, and the combined effect of rain-on-snow and elevated temperatures accelerated snowmelt, compounding the deluge. The streamflow at Sukkur Barrage in August 2022 was 170% higher than the historical norm, creating the perfect storm for catastrophic flooding.

The 2022 disaster was a reminder of the rising risks linked to human activity. The study suggests that anthropogenic changes, such as intensive agriculture along riverbanks, exacerbate riverine flooding. In regions like Larkana, cropland expanded from 37,000 to 47,500 square kilometers over the past two decades, intensifying the vulnerability of already flood-prone areas. Additionally, the effects of accelerated upstream snowmelt and rain-onsnow events added fuel to the fire, making the floods even more severe.

Looking ahead, the study paints a grim

picture of what could come. If current emission trends continue, flooding risks in Pakistan may skyrocket. By the end of the century, extreme rainfall events, particularly five-day deluges, could rise by 58%. The frequency of rainfall totals over 400mm during five-day periods would become more common, pushing vulnerable regions beyond their limits. Single-day rainfall extremes could increase by 44%, further straining the nation’s ability to cope.

The study’s authors, Dr. Ali Mirchi and Dr. Arfan Arshad, warn that while Pakistan cannot tackle global warming alone, it can take significant steps to mitigate future flooding risks. Restoring natural floodplains, improving drainage systems, and shifting development away from riverbanks are essential. Upgrading drainage infrastructure in both urban and rural areas could prevent widespread damage, similar to what occurred during the 2022 floods. The authors emphasize the importance of improving early warning systems, which could save lives and reduce the devastating consequences of future floods.

brunt of this crisis, but South Asia is also in danger. By 2030, nearly 49 million people in the region could be plunged into extreme poverty due to climate change—10 million more than if no climate damage occurred. While South Asia has the potential to eradicate extreme poverty by 2050, high-emission scenarios could still leave 3.4 million people stuck in poverty.

Road to poverty

Climate change is no longer just an environmental issue—it’s becoming an economic crisis, one that’s pushing millions further into poverty. A new World Bank report paints a grim picture: if emissions continue at their current pace, an additional 43 million people could be living in extreme poverty by 2050. And if income inequality continues to rise, that number could soar to 150 million. The most vulnerable? The world’s poorest nations, many of which are already ill-prepared to cope with the escalating climate impacts.

Two scenarios highlight the severity of this threat. The first scenario, called SSP5, envisions a world where the economy grows rapidly through fossil fuels, but no real effort is made to cut emissions. The second, SSP5RCP8.5, takes the effects of climate change into account: dwindling agricultural yields, lost labor productivity, and slower economic growth. The difference? It’s staggering. The report shows that without action, millions more people will be pushed below the poverty line because of income losses driven by climate-induced damage.

Sub-Saharan Africa is set to bear the

For Pakistan, the stakes are especially high. With its vast rural population, weak safety nets, and constant exposure to extreme weather like heatwaves, floods, and crop failures, the country is incredibly vulnerable. Already grappling with widespread poverty, Pakistan could find its progress undone if it doesn’t act fast. Just this summer, devastating rains claimed lives, destroyed homes, and displaced families. Another round of monsoon rains is expected to hit, reminding the country that the climate crisis is ongoing, with no end in sight.

The report also emphasizes the risks posed by inequality. Even small increases in income inequality could drastically worsen poverty levels. In countries like Pakistan, where inequality is already entrenched, this could make the situation even more dire.

So, what can Pakistan do? The country needs to completely rethink its approach to development. Climate resilience must be at the center of its plans. This means investing in better infrastructure, drought-resistant farming, and stronger social protections for its most vulnerable citizens. If Pakistan fails to take these steps, it could find itself trapped in a cycle where climate change makes people poorer, and poverty makes them even more vulnerable to climate shocks. The clock is ticking, and the time to act is now. n

By Farooq Tirmizi

Picture this world: the United States has completely withdrawn into its shell, which means that the United States Navy no longer patrols the seas, and piracy runs rampant, making international trade very difficult. The total volume of global trade comes crashing down. Pakistan can import and export very little.

What would happen to the country then?

Needless to say, this would be an enormous disruption and would cause a collapse in economic activity. But one thing would not happen: The country would not starve.

Yes, in the absence of fuel imports, we would need to conserve what little fuel existed for the food trucks and the tube wells, so more people would need to move back to their villages to work on the farms since we would probably not have enough for tractors. The country would be vastly poorer than it is today. But the farms and land would produce enough of the basic food we need to ensure that the country would not starve.

This may seem like a baseline thing to say, but the fact remains that most countries in the world cannot say that. The vast majority of humanity – including rising and wealthy nations like China – do not grow enough of their own food and do not have a large enough domestic capacity to do so. If free movement in the world’s shipping lanes – made possible by the United States Navy – were to stop, most of the world would face massive food shortages.

Pakistan would not.

A combination of the blessings of nature and a well-constructed canal system left to us by the British ensures that we can feed ourselves. Without fuel imports, it would be harder, but we could do it and ensure that

we survive and would be alive for whatever comes next.

As the world order changes rapidly and Pax Americana fades into memory, it is important to know our baseline: we can survive a collapse of global trade. A more likely scenario is that global trade will shrink, but not collapse, so it is likely that Pakistan would more than just survive the coming changes in the global political order.

Now let us ask the next question: what would it take for Pakistan to not just survive the shrinking of global trade, but continue to progress? The answer to that – as you may have guessed from the title of this article – is if the country were to become energy independent. Be self-reliant not just for food, but also for energy.

If that were the case, we would still feel the absence of opportunity from shrinking global trade, but the domestic economy would likely have at least a chance of continuing to function and perhaps even continue its growth trajectory.

In this story, we ask the following questions: how far are we from being self-reliant on energy? What do we import, and from where? And what would it take to get from where we are to an increased reliance on domestic energy sources. And what would the implications be for the economy if we were to even come close to energy independence?

What prompted us to even ask these questions was the notion floated by US President Donald Trump that the United States might help Pakistan develop its shale oil and gas reserves, of which there are supposedly quite a lot in the county. What we have found in our analysis of Pakistan’s energy sector is that while an increase in shale hydrocarbon energy is very welcome, Pakistan’s path to energy independence has many other more prominent components that do not rely on the mere statements of the US president.

How far to energy independence?

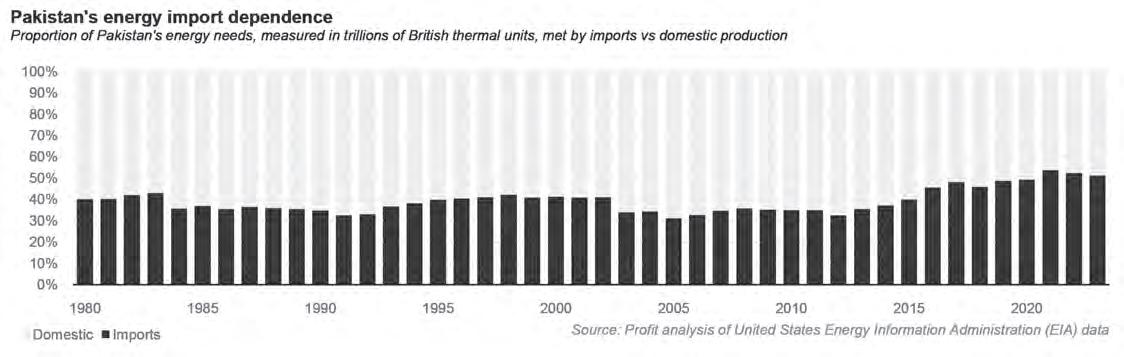

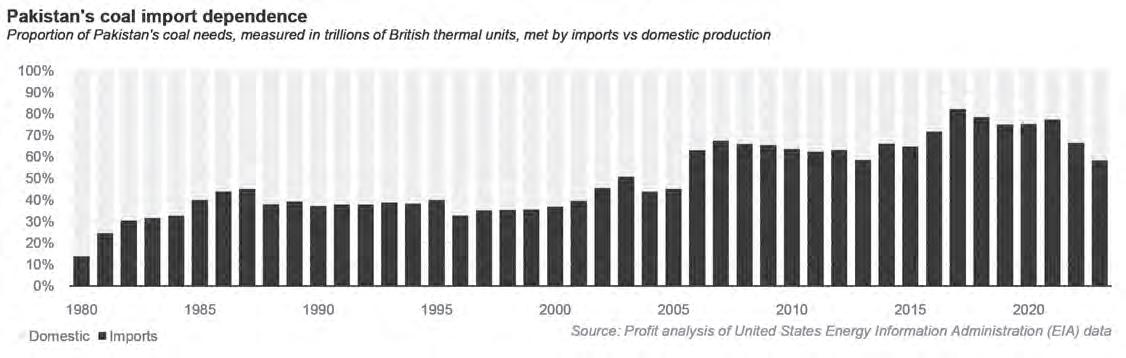

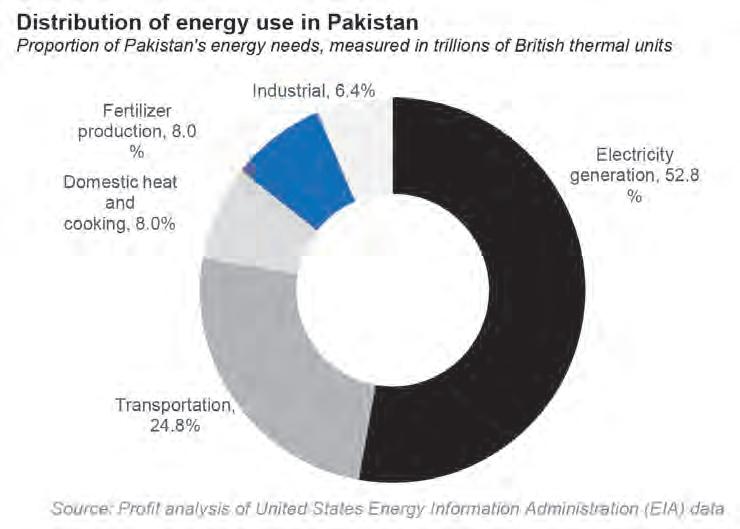

Pakistan relies on imports for approximately 51.2% of its total energy needs – across electricity generation, home cooking and heating needs, and fuel for vehicles and industrial uses – according to data from the United States Energy Information Administration for the year 2023, the latest year for which data is available.

This data is standardized across the various energy sources and converted into trillions of British thermal units (Btu) – a unit of measure that is the imperial equivalent of the joule in that it measures the amount of heat needed to raise the temperature of water. A Btu is the amount of heat it takes to raise the temperature of 1 pound of water by one degree Fahrenheit. One Btu is equal to 1,055 joules.

Why use Btu? Because oil is measured in barrels, natural gas is measured in cubic feet, coal is measured in tons, and that is before we even get to hydroelectricity and nuclear energy. One standard measure of the heat generated by each of these sources of energy allows us to compare across these sources.

The EIA estimates that Pakistan consumed 3,484 trillion Btu in 2023 but produced only 1,701 trillion Btu. That implies imports of 1,783 trillion Btu, or about 51.2% of the country’s energy needs. As recently as 2005, that number was 31.2%, meaning that Pakistan produced more than two-thirds of its energy needs domestically.

Of course, that was back during the Musharraf era when the government started encouraging the use of compressed natural gas (CNG) as a substitute for petrol and diesel imports. It worked for a while – until the country ran out of natural gas because the government did not bother to pay attention to the country’s dwindling natural gas reserves.

That year, however, was a comfortable

one for Pakistan. The increased use in CNG meant that Pakistan’s oil imports were lower than they would have been, despite a massive increase in car usage owing to the unleashing of auto loans on a mass scale for the first time in the country’s history. That year, domestic production was able to cover 25% of the country’s total oil consumption needs.

Since then, oil production has gone up and come back down to approximately the same level they were about 20 years ago. In 2024, domestic oil production in Pakistan averaged about 83,000 barrels per day, marginally lower than the 87,000 barrels per day average produced in 2005.

Consumption, however, has been about 645,000 barrels per day, up much more sharply from the 340,000 barrels per day that were consumed in 2005. About two-thirds of that increase has come from the increase in petrol for cars, which has increased by 8.6 times since 2005. Yes, there are that many more cars being driven that much more in the past two decades.

This then begs the question: given the fact that we are clearly consuming more energy than before, where does it all go? And what does the increase in energy consumption tell us about our economy?

Where does Pakistani energy consumption go?

Over half of all of the primary energy consumed in Pakistan goes into electricity generation, about 52.8% to be precise, based on Profit’s analysis of data from the EIA. Transportation accounts for about another quarter, domestic heating and cooking about 8%, fertilizer production another 8%, and then about 6.4% goes into industrial energy needs, the bulk of which are also related to electricity generation.

What is interesting is the degree to which these proportions have changed. Transportation – the fuel that goes into cars, buses, trucks, rickshaws, etc. – has gone from being about oneeighth of total energy use to one quarter in just under two decades., again according to Profit’s analysis of data from the EIA. This doubling of share means that Pakistanis have a lot more vehicles than they once did and are much more likely to be using them than they did a generation ago.

Two things stand out about the above statistics. The first is that the dominant use of energy in Pakistan is electricity generation, so if electricity generation can be moved towards

more domestic sources of fuel, that would have the largest impact on Pakistan’s ability to become energy independent.

And the second is that if Pakistan is also able to somehow reduce its consumption of foreign sources of fuel for transportation, it would effectively be able to have minimal need to import energy.

Both of these are fronts where – through a combination of technology and the Pakistani consumer responding to economic incentives –the need for imported fuels is likely to start dropping soon. On the first front, both solar energy and increased production in the Thar coalfields is resulting in a more domestically oriented national electricity grid. And on the latter front, we have seen the rise of electric and hybrid vehicles that are likely to increase the energy efficiency of Pakistanis’ transportation needs, even as we continue to drive more miles per person per day.

The rise of domestic electricity

Two things are going very right with Pakistan’s electricity sector: power generation is getting reliant on more domestic fuel sources and is getting cleaner.

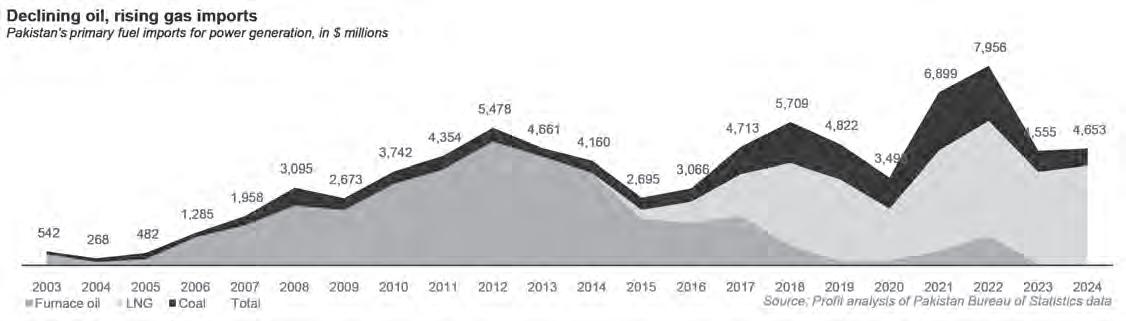

According to Profit’s analysis of NEPRA data, between 2007 and 2017, about one-third of Pakistan’s electricity was generated using furnace oil, nearly all of which was imported. This was a major contributor to Pakistan’s balance of payments problem during that decade: the country needed to import oil just to keep the lights on during a time when – for most of that era – oil prices hovered above $80 per barrel.

Over the past 10 years – since the Nawaz Administration began dramatically altering Pakistan’s electricity generation mix – the country has increased its power generation output by 42%, from 98,655 gigawatt-hours (GWh) in fiscal 2013 to approximately 137,000 GWh in fiscal 2024. The aggregate increase, however, is not the full story.

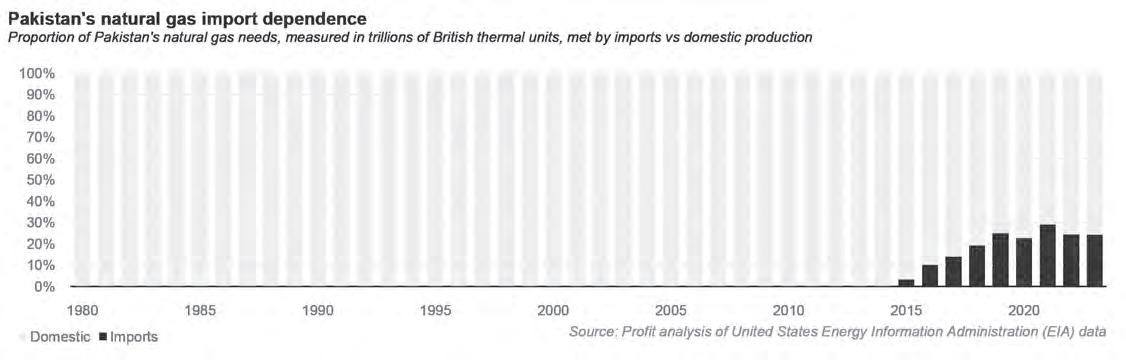

During that time, imported LNG replaced imported oil, and imported coal replaced the decline in natural gas. And when we say replace, we mean that almost literally. Between 2013 and 2023, electricity generation from oil-fired power plants declined by 29,162 GWh, and that generated by LNGfired power plants went up by 29,282 GWh,

an almost exact one-to-one replacement. Power plants run on domestic natural gas saw production decline by 12,942 GWh and replaced almost exactly by an increase of 12,457 GWh in imported coal-fired power production (which itself is now being replaced at least partially by Thar coal).

If those two fuel sources are seen as merely replacements for the previous fuel mix, then about half of the increase in electricity generation – nearly 20,000 out of the 42,000 GWh increase in power generation –has come from nuclear energy.

It does not get much coverage in the press, but Pakistan’s nuclear energy program is a quiet success story. As recently as 2009, Pakistan got less than 2% of its electricity from nuclear energy and now that number is above 17% of the total electricity generated in the country, largely on the back of Chinese-backed nuclear power plants at Chashma, and a substantial increase in the generation capacity at the nuclear power plant in Karachi. So important is nuclear to Pakistan’s increase in electricity generation that the net amount of nuclear energy added to the grid is about equal to the total added

by Thar coal, wind, and the new hydroelectric power plants combined.

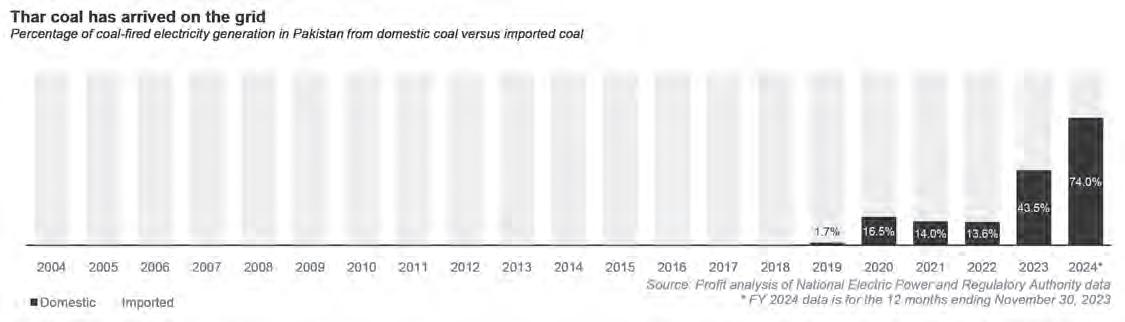

But while nuclear helps explain the ability to increase power generation through domestic means, it is not the only part of the story. The other part is Thar coal, which is increasingly beginning to replace imported coal in Pakistan’s power generation mix, a trend that has become more visible over the past 12 months. December 2022 was the first month when Pakistan generated more electricity from Thar coal than imported coal.

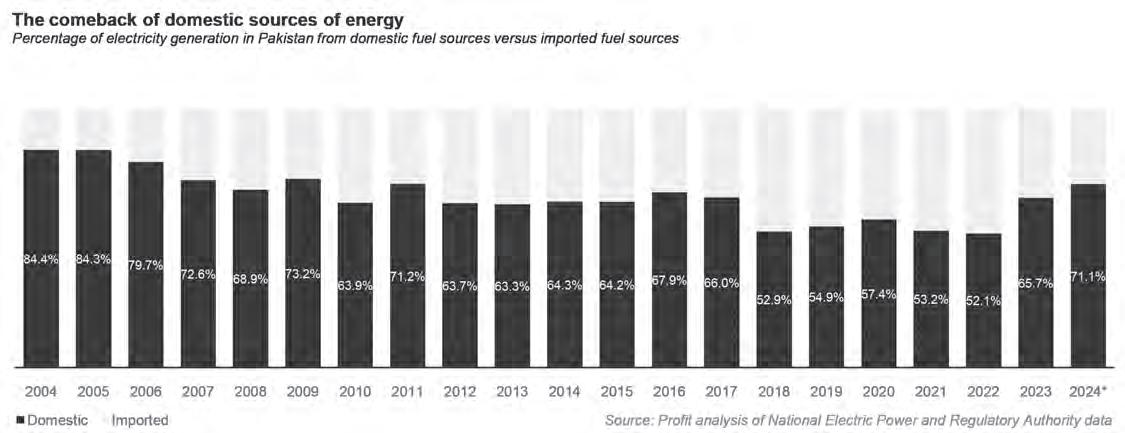

Combine the massive increase in nuclear energy with the additions to hydroelectric power generation, and domestic coal-fired power plants, and Pakistan’s reliance on domestic sources of fuel has gone from 52.1% of electricity in fiscal 2022 to 71.1% in fiscal 2024.

And all of this is before we even get to the solar energy boom in Pakistan. If the trade data is an accurate representation of reality, at the 2024 prices of solar panels in China – $0.10 per watt, according to consulting firm Wood Mackenzie – having imports worth $2 billion would imply that Pakistan was installing roughly 22,000 megawatts of

solar electricity, which would represent a nearly 42% increase in the country’s electricity generation capacity.

Then we get into the rise of hybrid electric vehicles.

The electric / hybrid SUV comes to Pakistan

Currently, there are only a handful of hybrid vehicles being assembled and/or being sold in Pakistan. These include Toyota Cross, Haval H6, Haval Jolion and the Hyundai Santa Fe. That, however, is about to change as more and more Chinese manufacturers come to Pakistan, including the global electric vehicle powerhouse: BYD.

According to Reuters, “Chinese electric vehicle giant BYD plans to roll out its first car assembled in Pakistan by July or August 2026

to capture growing demand for electric and plug-in hybrid vehicles in the region.

BYD, the world’s top EV maker, has been expanding rapidly outside its home market, where it is in a strong price war. The Pakistan plant addresses rising demand from emerging markets and allows the company to take advantage of incentives offered by the Pakistani government. The plant has been under construction since April near Karachi in a partnership between BYD and Mega Motor Company, a subsidiary of Hub Power Company.

It would initially have the capacity to produce 25,000 units a year on a double shift. The plant will start by assembling imported parts, with some local production of non-electric components. It would initially produce vehicles for the domestic market, with potential to export to right-hand drive countries in the region depending on freight costs and business economics.”

The macroeconomic impact

Here is the punchline of all of this: If Pakistan had been able to halve its energy imports between 2003 and 2024, it would have had a current account surplus in 13 out of those 22 years, instead of just the one calendar year during which it had a current account surplus. If the country eliminated its energy import bill completely (highly improbable), it would have had a current account surplus in 19 of the last 22 years.

In other words, energy independence is the entire ballgame. If Pakistan is able to substantially reduce its dependence on oil and natural gas imports, the current account deficit is substantially reduced, and may cease to be a macroeconomic problem for the country altogether. Think about what that would mean: no more sudden currency shocks that cause massive increases in the price of everything. No more government officials obsessing over the exchange rate rather than trying to correct more substantive macroeconomic imbalances.

The country would look vastly different. Could the shale revolution help with this? Yes, of course. And given Pakistan’s sizeable shale natural gas reserves – 101 trillion cubic feet, according to EIA data – the country should absolutely pursue any offers of assistance by the US government or private sector players to help develop those resources.

But Pakistan is already on its way to becoming more energy independent, and incremental progress on this front is happening mostly due to individual initiative, though a handful of government policies – particularly the ones encouraging energy efficient hybrid and electric cars – appear to be helping.

How long it will take to arrive at that point is difficult to project given the multitude of variables that could influence that trajectory. However, the direction is clearly one of progress. n

JDW’s expansion of its ethanol production

Expansion into auxiliary production should help expand its margins in an otherwise tough year

Profit Report

JDW Sugar Mills Limited (PSX: JDWS) has released its condensed interim accounts for the nine month period ended 30 June 2025, and the numbers underline a challenging year for the country’s largest sugar producer.

Gross revenue fell 4% to Rs97.9 billion (9M FY24: Rs102.0 bn), while net sales after taxes and commissions eased to Rs84.7 bn from Rs89.4 bn – a 5% contraction that management attributes to a sharp correction in domestic sugar prices during the first half of the fiscal year.

As costs rose faster than sales, gross profit halved to Rs9.87 bn (9M FY24: Rs18.10 bn), pulling the gross margin down to 12% from 20 pc. The directors note that molasses realisations have also dipped 25% year on year, squeezing by product economics.

On the bottom line, profit after tax plunged 63% to Rs3.09 bn, translating into earnings per share of Rs53.39 versus Rs144.86 a year earlier.

The results commentary spells out five key drivers behind the earnings decline. First, JDW was forced to sell sugar below cost early in the season to fund working capital needs amid a glut in inventories sector wide. Second, administrative expenses ballooned under double digit inflation. Third, the fair

value gain on the cane crop shrank markedly, dragging “other income” down to Rs1.91 bn from Rs2.94 bn. Fourth, while finance costs did recede by Rs1.14 bn in line with lower policy rates, the saving could not offset the fall in operating profit. Finally, the new 18% levy on sugar exports shaved more than a billion rupees off pre tax earnings.

Despite the earnings slump, the balance sheet size swelled to Rs94 bn (September 2024: Rs70 bn) after the company capitalised its ongoing capital expenditure cycle – most conspicuously the ethanol/distillery project discussed below. Gearing remains manageable: total equity of Rs28.4 bn funds roughly 30% of the asset base, while short term borrowings cover seasonal stockpiles and cane procurement.

Segment

Sugar Power co generation

By products

Main products

Crystalline white sugar

Export of surplus bagasse based electricity (Unit II & III)

Molasses, mud, bagasse

Cash flow optics are mixed. Operating cash flow swung back into the black at Rs9.38 bn on the strength of cane supplier advances and inventory run down, yet a hefty Rs17.1 bn outlay on property, plant and equipment – largely the new ethanol plant – left free cash flow deeply negative. The company bridged the gap through fresh long term finance and a Rs16.6 bn reduction in short term facilities, helped by timely sugar off take.

Notwithstanding the squeeze, directors approved a first interim dividend of Rs20 per share (200 pc) and sounded an upbeat note for the full year, citing firmer sugar prices, lower borrowing costs and the imminent commissioning of the ethanol unit.

JDW’s revenue historically came from three inter locking lines:

Revenue drivers

Ex mill prices, sucrose recovery, crushing volumes

Bagasse calorific value, NEPRA tariff indexation

Spot molasses prices, fertiliser demand

FY25 dynamics

Prices crashed in 1H FY25 but have since rebounded; cane procurement now fully market linked.

Remained profitable thanks to fuel cost pass through, cushioning the sugar downturn.

To hedge commodity swings, JDW has moved decisively into fuel grade ethanol, leveraging the molasses that streams out of its three mills. The greenfield distillery at Pir Ahmedabad, Sadiqabad fired up its burners on 12 July 2025, with trial production running “smoothly” ahead of commercial operation targeted for 1 August 2025. Name plate capacity is a robust 230,000 litres per day, and management says sufficient molasses stocks exist to keep the plant at 100% utilisation until the 2025 26 crushing season starts.

The ethanol will be aimed primarily at the export market, where Pakistani producers currently enjoy duty free access to several Asian blend markets and stable demand from European beverage and industrial buyers.

Given the plant’s scale, analysts reckon ethanol could generate Rs25 30 bn in incremental annual revenue at prevailing FOB prices, potentially restoring JDW’s historical profit trajectory even if sugar margins remain volatile.

The company has also piloted a solar powered tube well financing scheme for its cane growers, hoping to lift field yields and secure quality feedstock – an indirect but strategic move to de risk its raw material supply chain.

JDW was incorporated in May 1990 as a private limited company and went public in August 1991, listing on what is now the Pakistan Stock Exchange. From a single 6,500 tonne per day (TCD) mill at Jamal din Wali (Unit I), the group has expanded into a three mill, 44,500 TCD powerhouse straddling Punjab and Sindh. Key milestones include:

•1998 2002 – Capacity leap: Unit II at Machi Goth and Unit III at Ghotki came on stream, cementing JDW’s status as Pakistan’s largest sugar producer.

•2006 – Co generation diversification: Two high pressure bagasse turbines (80 MW each) enabled the sale of renewable power to the national grid, earning carbon credit income and reducing bagasse disposal costs.

•2014 17 – Vertical integration: Acquisition of Deharki Sugar Mills and investments in corporate cane farms broadened raw material control.

•2023 – Ethanol strategy approved: The board sanctioned a state of the art distillery with daily output of 200,000 230,000 litres, financed through a mix of debt and internally generated cash.(The News International, Mettis Global)

•July 2025 – Trial production starts: The plant lights up, marking JDW’s first step into higher margin bio fuels.

Today, JDW also holds stakes in two captive power subsidiaries (Sadiqabad Power and Ghotki Power) and in Faruki Pulp Mills, underscoring a strategy of adjacent diversification. Its credit profile is strong: VIS Credit Rating reaffirmed an AA /A 1 rating in May 2025,

citing robust cash generation and prudent capital structure.

Management is candid that FY25 has been “a year of reset” as the sugar sector inches towards deregulation. With provincial governments abstaining from setting a support price for cane for the 2024 25 crop, mills – for the first time in decades – paid fully market based rates. JDW argues that full deregulation, including parity between imported and local sugar prices, is critical if mills are to invest in yield enhancing technology and stabilise grower incomes.

In the near term, three swing factors will determine whether JDW’s earnings rebound:

1. Sugar price trajectory – spot rates have firmed since April as inventories cleared, but another supply glut cannot be ruled out if the federal government allows duty free imports.

2. Ethanol ramp up – every 10% increase in utilisation could add roughly

Rs1.5 bn to the top line, according to brokerage estimates.

3. Interest rate path – the State Bank has trimmed its policy rate by a cumulative 11 percentage points over 12 months; each 100 bp cut shaves Rs450 500 million off JDW’s annual finance cost.

For investors, the story is transitioning from a pure play sugar cyclical to a bio fuels and energy hybrid. If the distillery runs as advertised and export orders materialise, JDW could claw back much of the margin lost in FY25. But sustainable value creation will still hinge on sectoral reform that aligns cane economics with global sugar benchmarks.

For now, the company’s motto of “creating opportunities for the future” seems more than marketing spin: by distilling its own by product into a high value export, JDW is quite literally turning molasses into money – and offering shareholders a new source of sweetness after a decidedly bitter year. n

Sazgar’s poised to profit from Pakistanis’ new taste for SUVs

Company to launch several new models, with its partnership with Chinese automakers continuing to deliver dividends

Profit Report

Sazgar Engineering Works Limited (PSX: SAZEW) has put another powerful year on the odometer. According to a detailed brokerage update released on 28 July 2025, the Lahore based assembler is heading for triple digit top line growth on the back of a sports utility vehicle boom that shows little sign of abating. Analysts at Arif Habib Research expect Sazgar’s revenue to surge to Rs133.4 billion in FY26, up from an estimated Rs90 billion in the year just

ended, before climbing a further 43% to Rs191.6 bn in FY27 as incremental capacity for new Chinese models hits the market. The earnings picture is equally arresting, albeit tempered by an inevitable margin correction once government incentives expire. The brokerage now projects earnings per share of Rs367 for FY26 — implying a hefty net profit of Rs22.2 bn and a sector beating net margin of 16.6 pc. A year later, as the 2021 26 Auto Policy concessions on customs duty and sales tax lapse, that net margin is forecast to settle at roughly 7.6 pc, still solid for an assembler that was loss making barely four

years ago.

Gross profitability tells the same two stage story. FY25’s gross margin is estimated at 30.6 pc, helped by duty free completely knocked down (CKD) kits and a weak rupee that made fully built up imports prohibitively expensive for rivals. The chart on page 3 of the note plots a clear inflection: a high thirties gross margin band in FY24 26 that normalises to the 17% area from FY27 onwards, cushioned by an ambitious localisation drive. Volume momentum is unmistakable. Unit sales of Haval branded SUVs leapt 102% year on year to 10,832 units in FY25 and are projected to reach 12,500 in FY26, even before the expected late FY26 launch of a plug in hybrid (PHEV) variant. The brokerage’s model implies average monthly despatches of nearly 1,100 vehicles — an unheard of number for what was once a niche premium segment.

Higher throughput is feeding cash generation. Management guidance baked into the forecast assumes dividends of Rs92 per share for FY26, equivalent to a 7.4% yield at current market prices and comfortably funded out of operating cash flows, despite a Rs11.5 bn capital expenditure programme for a new energy vehicle (NEV) facility.

In short, Sazgar is steering into a sweet spot: revenue is racing ahead, profitability remains muscular, and the margin compression expected after FY26 looks manageable thanks to localisation and scale economies.

Sazgar’s product mix today bears little resemblance to the auto rickshaws that first made its name. The research note highlights four pillars:

Product line

Haval SUVs

Great Wall “Tank” series

Poer/Canon pick ups

Electric & NEVs

Key models / variants

H6 (1.5T, 2.0T, HEV), Jolion sub compact, forthcoming H6 PHEV

Tank 500 (3 row body on frame 4×4)

Canon ALPHA lifestyle double cab

Haval PHEV, future battery electric variants

The common denominator is a tilt towards higher value, feature rich vehicles that command fatter rupee margins per unit than mass market saloons — and that play to a burgeoning domestic appetite for SUVs equipped with advanced driver assistance systems. Sazgar’s sales mix is already more

than 90% SUV centric by revenue, a ratio that is expected to climb once the brawnier Tank 500 and Canon pick up join the line up. Localisation is the strategic hinge. Sazgar currently imports CKD packs at zero duty under the auto policy, assembling engines, transmissions and body panels on semi automated lines in Lahore. The planned NEV facility will take localisation beyond sheet metal welding into battery packs, wiring harnesses and selected interior trim — reducing foreign exchange exposure and arresting the post FY26 margin squeeze. Management’s internal target, reflected in the brokerage model, is 17% gross margin by FY27 29, four percentage points higher than earlier sell side estimates.

Founded in 1991 as a manufacturer of three wheeler auto rickshaws, Sazgar Engineering earned a reputation for sturdy, fuel efficient vehicles that became an urban transport staple. Export orders from Afghanistan and parts of Africa followed, prompting the company to list on the Karachi Stock Exchange in 2001 to fund capacity expansion. The decisive pivot arrived two decades later. In 2021 Sazgar inked a technical licence and CKD supply agreement with China’s Great Wall Motors, giving it exclusive rights to assemble and market the Haval H6 and Jolion SUVs in Pakistan. A skeletal assembly hall in Lahore’s Sundar Industrial Estate was retooled in under nine months, and the first locally built H6 rolled off the line in mid 2022 — just as pandemic deferred demand and a weak rupee made imported crossovers painfully expensive.

Status

& outlook

Core revenue engine; volumes more than doubled in FY25; PHEV bookings open Aug 2025.

CKD roll out targeted before March 2026; brokerage models 600 units in FY27, adding Rs16 EPS.

Local assembly slated alongside Tank 500; projected 2,400 units in FY27, contributing Rs51 EPS.

Underpinned by an Rs11.5 bn NEV plant; localisation expected to lift post FY26 gross margins to ~17 pc.

By FY24 the SUV venture had eclipsed rickshaw earnings; by FY25 Sazgar had captured what analysts believe is a 46% share of the premium C segment SUV market, edging past Korean incumbents and forcing Japanese assemblers to revisit their model strategies. The company’s board green lit the

Rs11.5 bn NEV plant in late 2024, signalling a definitive break with its low technology origins. The research note projects that, once fully ramped, the facility will lift installed capacity to 30,000 units per annum, up from the current 15,000.

The evolution has not been entirely smooth. Exchange rate volatility inflated CKD costs in 2023, prompting temporary price hikes; and the expiry of tax incentives after June 2026 looms large. Yet the company’s balance sheet — equity of Rs41.7 bn against negligible long term debt — gives it the fire power to absorb shocks and self fund expansion. Return on equity is projected at a head spinning 66.5% in FY26 before normalising in the mid 20s as margins taper.

With the stock trading on just 3.4x FY26 earnings — a steep discount to the sector’s 8.6 × average — analysts argue that Sazgar is ripe for rerating, provided three conditions hold:

1. SUV demand remains resilient. Industry data suggest that the SUV share of Pakistan’s passenger vehicle market has climbed from 7% in 2019 to more than 20% today, driven by aspirational first time buyers and a shift away from sedans. The chart on page 3 of the note projects Haval volumes nudging above 15,000 units by FY30, even on conservative GDP assumptions.

2. Localisation offsets the loss of fiscal incentives. With the NEV plant scheduled to come on stream in mid 2026, the brokerage believes Sazgar can source batteries, seats, wiring looms and infotainment units domestically, shaving 5 6% off its cost of goods basket.

3. Working capital discipline persists. The model assumes a current ratio of 2.4 × in FY27, falling inventories and quick receivables turnover — all hallmarks of the lean operations that helped deliver a 30% net margin in FY25.

For now, the company appears well placed to tap Pakistan’s changing automotive palate. A decade ago, the notion of a locally assembled, fully loaded mid size SUV selling north of Rs8 million would have seemed fanciful. Sazgar has shown that, with the right foreign partner and a nimble cost base, such products can not only sell but dominate. If the localisation gambit pays off, the margin road bump expected after FY26 could prove a mere speed breaker on the company’s journey from rickshaw pioneer to SUV powerhouse.

With new models in the pipeline, hybrid technology on deck and a growing appetite for high riding vehicles among urban professionals, Sazgar looks poised to profit handsomely from Pakistanis’ evolving taste for SUVs — and investors who buckle in now may enjoy a rewarding ride. n

Revenue down at Lucky Core Industries

Slow down across several key products lines hit the company’s top line in a harbinger of what may be affecting the broader economy

LProfit Report

ucky Core Industries Limited (PSX: LCI) reported its results for the financial year ended 30 June 2025, revealing that net revenue edged down 1% year on year to Rs119.9 billion as a cooling soda ash market and soft textile demand offset price revisions in other divisions. Fourth quarter sales fell a steeper 6% YoY to Rs27.9 bn, confirming the down trend that gathered pace in the final months of the year.

Despite the top line slippage, the company protected—and even slightly widened—its profitability. Gross profit rose 2% to Rs27.45 bn, nudging the gross margin up by 50 basis points to 22.9% as manage-

ment pushed through selective price rises and benefitted from lower energy tariffs at its Sheikhupura polyester plant. However, margin expansion could not fully cushion the operating line: higher other expenses and a Rs56 million exchange rate loss trimmed fourth quarter operating leverage.

For the full year profit after tax (PAT) inched up 5% to Rs11.76 bn, translating into earnings per share of Rs25.46. Yet the quarterly view tells a more sobering story: 4Q PAT dropped 12% YoY to Rs2.85 bn, while the net margin for the quarter slipped to 10.2% from 10.9% a year earlier. Declining finance costs ( 38% YoY) provided some relief, but a heavier effective tax rate of 36.9% eroded much of that benefit. The board declared a final cash dividend of Rs6.20 per share, bringing the full

year payout to Rs13.00.

In short, LCI’s FY25 scorecard is a study in contrasts: a leaner cost base and stronger pricing in pharmaceuticals bolstered margins, yet the revenue contraction flags weakening demand in core industrial inputs—most visibly soda ash and polyester. Investors will be watching whether the company can reignite volume growth in FY26 as macro conditions stabilise.

Lucky Core’s portfolio spans five operating verticals, giving the group one of the broadest revenue bases in Pakistan’s chemicals and materials sector:

The diversified mix partly explains why LCI has been able to hold margins in the face of cooling soda ash off take. Management noted in the results call that deregulation of non es-

Soda Ash

Flagship products

Light ash, dense ash, refined sodium bicarbonate

Terylene polyester staple fibre (standard, recycled PET chip, speciality grades)

General chemicals, polyurethanes, speciality additives, masterbatch, crop protection formulations

sential medicine prices lifted pharma margins, counterbalancing weaker polyester spreads.

Dairy, meat and poultry producers

The company traces its roots to 1944, when the Khewra Soda Ash Company set up Pakistan’s first soda ash works in Punjab’s Salt Range. Post Partition, the business came under the aegis of Imperial Chemical Industries (ICI) and was later rolled into ICI Pakistan Limited, which diversified into polyester fibre in 1982 and launched a landmark PTA plant in 1998.

A string of pivotal milestones followed: •2008 – AkzoNobel’s global acquisition of ICI made the Dutch paints giant the ultimate parent.

•2012 – Yunus Brothers Group (YBG) bought a 75.8% stake from AkzoNobel, heralding a shift towards local ownership.

•2016–21 – The group expanded into nutritionals, veterinary health and 100% recycled PET chips.

•August 2022 – Reflecting its widened remit and YBG’s branding, the company adopted the name Lucky Core Industries Limited.

•2024 – Announced a 200,000 tonne soda ash expansion that will lift Khewra capacity to 760,000 tpa, and signed agreements to acquire Pfizer’s Karachi injectable plant.

This arc from a single product chemical pioneer to a diversified industrial player underpins LCI’s long term strategy: leverage Pakistan’s demographic tail winds while hedging against cyclicality in any one segment.

Portfolio boosted by the May 2024 agreement to acquire Pfizer’s Karachi facility and selected brands, broadening sterile capability.

Investing in a green field veterinary medicine plant approved in 2023.

The FY25 numbers underscore a clear message: pricing power can only go so far when volumes soften. With inflation moderating and monetary policy easing, analysts expect an incremental pick up in downstream demand—particularly in flat glass and detergents, which together absorb over half of domestic soda ash consumption. Yet head winds persist: imported soda ash from low cost Chinese producers is capping local price rises, and polyester margins remain hostage to global oil derivative spreads.

Management’s response is three pronged. First, capacity expansions in soda ash aim to lock in scale efficiencies before a new entrant arrives. Second, the Pfizer acquisition should accelerate a pivot into higher margin sterile injectables. Third, digitalisation initiatives in the Chemicals & Agri Sciences business are expected to shave off working capital days. Whether these moves can restore top line momentum will be clearer after the first half FY26 results, but for now investors can take solace in a sturdy balance sheet, a 22.5% return on equity and a dividend yield approaching 4% at current prices.

For a company that has reinvented itself several times over eight decades, the next chapter once again hinges on making the right capital allocation bets—this time in a lower growth, post inflation Pakistan.

Revenue up, profits down at Ghani Glass

Slow down across several key products lines hit the company’s top line in a harbinger of what may be affecting the broader economy

Profit Report

Ghani Glass Limited (PSX: GHGL), the country’s largest listed glass maker, has reported a mixed score card for the year ended 30 June 2024 (FY24). Net revenue advanced 16% year on year to Rs47.8 billion, but that growth failed to translate into the bottom line. Profit after tax declined 17% to Rs6.75 bn, pulling earnings per share down to Rs6.75 from Rs8.10 in FY23.

The culprit was a sharp escalation

in production costs. The company’s cost of sales jumped 22% to Rs34.7 bn, outpacing revenue and compressing the gross margin from 31% to 27 pc. Operating expenses also frayed the cushion: selling and distribution outlays surged 23 pc, while administrative expenses rose 14 pc, together slicing four percentage points off the operating margin, which slipped to 16.7 pc.

Finance charges, though still modest at Rs206 million, ballooned 76% amid higher policy rates and working capital borrowings. Meanwhile a 215% leap in taxation—the company warned it will

enter the full corporate tax regime with an effective rate of 39% from FY26—further hollowed out net profitability.

Quarterly numbers underline the downshift. In 3QFY25 (the three months to March 2025) revenue edged just 1% higher to Rs11.5 bn, yet earnings per share fell 4% to Rs1.65 as the net margin retreated to 14.3 pc. Management attributed the pressure to subdued float glass demand from the still moribund construction sector and the cost of running only one furnace at partial capacity.

Ghani’s board maintained a token dividend of Rs1.00 per share, 46% lower than last year, citing the need to conserve cash for a capital expenditure cycle that includes a new state of the art tableware press scheduled to be commissioned in September 2025.

In summary, FY24 proved that revenue growth is not enough when input costs, energy tariffs and depreciation all rise faster. Until construction demand revives and a second float furnace can be restarted—ear marked for 2027—margins will remain tightly correlated with management’s ability to contain costs and pass on selective price rises.

Although best known for its float glass, Ghani’s product palette is wider and more diversified than many investors realise:

Segment

Float glass

Glass containers

Tableware

Principal products

Clear, tinted and reflective sheets; mirror grade; automotive windscreens

Bottles and vials for pharmaceuticals, beverages, foods and cosmetics

Management said sales volumes are presently exceeding production volumes, forcing it to dip into inventories. That imbalance partly explains why cost of goods escalated faster than revenue: overtime shifts at the single running furnace and outsourced fabrication added incremental cost without the scale economies the idle furnace would provide if demand normalised.

Looking ahead, the imminent arrival of the new tableware press is expected to shift more sales into higher value SKUs. The machine’s promise is two fold: tighter dimensional tolerance, enabling the export of stemware, and reduced glass wastage, cutting cullet ratios by an estimated 3 4 percentage points.

Ghani Glass’s origins date back to the early 1990s, when the Ghani family—already active in trading commodities—took the strategic decision to integrate backwards into glass manufacturing. The company was incorporated in 1992 and listed on the Karachi Stock Exchange (now the Pakistan Stock Exchange) in 1994 with a modest single furnace container glass plant at Lahore.

Key milestones since then include:

• 1999 2001 – Float glass breakthrough: Ghani commissioned Pakistan’s first privately funded float glass line in Sheikhupura,

End use sectors

Building & construction, vehicle assembly, interior décor

Pharma, FMCG, brewery

Household retail, hospitality

Competitive position

Largest domestic capacity; only one furnace active at present while the second lies idle awaiting demand pick up.

Supplies both bulk amber bottles and low alkali type III pharma vials; competes with Tariq Glass and imports from the GCC.

Currently upgrading with “state of the art pressing machines” that management says will boost quality and premium pricing by Q2 FY26.

uous furnace came on stream, raising float capacity to 600 tonnes per day and allowing the company to export sheets to Afghanistan and East Africa.

• 2017 – Foray into tableware: Responding to a rise in middle class discretionary spending, Ghani launched a decorated tableware range under the GB brand, using imported moulds and local silica sand.

• 2023 – Energy retro fit: The group installed waste heat boilers and switched part of its fuel mix from furnace oil to re gasified liquefied natural gas (RLNG), trimming energy intensity by roughly 9 pc.

The expansion drive has vaulted Ghani from a small lot container producer to a Rs43 billion market capitalisation glass conglomerate employing nearly 3,800 people and exporting to more than 15 countries. Yet size brings complexity: raw material logistics, energy sourcing, and carbon footprint compliance all add layers of cost that not every domestic competitor bears.

Management’s own forward guidance is cautious. With the construction sector “yet to begin a meaningful recovery,” the board has postponed the restart of the second float furnace to 2027. In the interim, Ghani will rely on value added tableware and pharma containers to sustain revenue growth, but neither offers the volume leverage of float glass.

Two variables will determine whether FY25 turns out better than FY24:

1. Energy tariffs and fuel mix. The shift to RLNG assisted margins in FY24, but any renewed spike in gas prices would feed straight through to cost of sales. Management has mooted rooftop solar and further waste heat recovery to cap exposure, but those projects remain on the drawing board.

2. Recovery in builders’ demand. Should government incentives for affordable housing finally gain traction, latent demand could justify firing up the spare furnace sooner. That would restore operating leverage, smoothing fixed cost per tonne and potentially re inflating the gross margin above 30 pc.

Heat resistant borosilicate tubes, ampoules, solar glass

Medical devices, solar water heaters

The float glass business remains the revenue anchor but has become margin dilutive because it is energy intensive and strongly linked to the cyclical construction market. By contrast, container glass—particularly pharmaceutical vials—delivers steadier margins and helped soften the blow

Niche but higher margin; leverages know how from container glass chemistry.

breaking the import stranglehold and setting the stage for local sourcing in construction.

• 2006 – Pharmaceutical focus: Seeing the boom in generics, the firm added a dedicated amber vial line, becoming a key supplier to multinationals such as GSK and Abbott.

• 2011 – Second float line: A larger, contin -

In the meantime the company’s balance sheet remains healthy—net debt is under 0.4 times EBITDA—but dividend hungry investors will need to accept thinner payouts as cash is channelled into capex. The coming year, therefore, looks set to be another delicate balancing act of cost control, selective price increases and disciplined capital spending.

For now, Ghani Glass has proved that it can still grow the top line in a bleak macro climate. The challenge—which FY24 results lay bare—is to convert that growth into profit at a time when energy, labour and taxation are all moving the wrong way. n

Colgate Palmolive’s sluggish year

Revenue and profits barely grew, as consumers continue to struggle with the after effects of a heavy crisis

Profit Report

Colgate Palmolive (Pakistan)

Ltd (COLG) closed its financial year ended 30 June 2024 with gross revenue of Rs116 billion, up just 2.4% from Rs113 bn a year earlier. Net revenue grew at a slightly gentler clip of 23.8% to Rs113.23 bn as higher sales‐tax incidence and heavier trade promotions diluted some of the top line momentum.

Put together, the year can be characterised as inflation led growth carried by margin recovery, rather than a volume led expansion. That nuance explains why the market greeted the results with only muted enthusiasm: COLG’s share price eked out a 1.8% gain on the announcement day but quickly drifted lower as investors digested the real growth picture.

Colgate Palmolive’s Pakistani portfolio spans four broad buckets:

•Oral care – Flagship Colgate toothpastes (Maximum Cavity Protection, Colgate Total, Optic White, Herbal and Miswak), manual toothbrushes (360°, SlimSoft, Premier/Classic lines) and recently relaunched mouth wash variants.

•Personal care (hair & skin) – Palmolive

Naturals shampoos (Healthy & Smooth, Anti Dandruff, Silky Straight, Intensive Moisture) and bar soaps, plus niche lines such as Palmolive Aloe Vera with Chamomile.

•Antibacterial hygiene – Protex bar soaps and liquid hand wash introduced during the Covid 19 surge and now positioned against Lifebuoy and Safeguard.

•Home care / fabric & surface care – Detergent powders and specialist additives (Brite Machine Wash, Bonus Active), dish care stalwarts Lemon Max bar and liquid and the value washing powder Express Power.

The oral care franchise remains the margin powerhouse, contributing an estimated 55% of operating profit on only one third of turnover, thanks to premium positioning and limited local competition in the higher priced sensitivity and whitening sub segments. In contrast, the laundry and dish care businesses are volume engines but carry lower margins because of commoditised price points and volatility in palm oil and soda ash inputs.

The company’s roots date back to 5 December 1977, when it was incorporated as National Detergents Ltd to manufacture and market Bonus laundry powder under licence from Unilever trained entrepreneurs in the Lakson Group. A pivotal moment came on

28 March 1990, when a Participation Agreement with Colgate Palmolive Company, USA brought international branding, technology transfer and a 30% foreign equity stake; the firm was renamed Colgate Palmolive (Pakistan) Ltd and listed on the then Karachi Stock Exchange soon thereafter.

Throughout the 1990s the business diversified into oral care with the launch of Colgate toothpaste (1992) and into dish care with Lemon Max paste, while the 2000s saw backward integration: a sulphonation plant for detergent intermediates and high speed tube filling lines for toothpaste. By FY14 the company had crossed the Rs30 bn sales mark and, despite periodic currency crises, kept capital expenditure self funded — an approach that shielded margins during bouts of rupee depreciation.

Today COLG operates two integrated sites in Karachi (Port Qasim and SITE) and a networked distribution footprint that reaches 200,000 retail outlets, placing it among the top five fast moving consumer goods (FMCG) players by market capitalisation on the Pakistan Stock Exchange.

For investors the central question is whether Colgate’s FY24 performance marks the end of a cyclical rebound or the begin-

ning of sustained volume recovery. Pakistan’s consumer price inflation has descended from a near 40% peak in May 2023 to single digits after steep monetary tightening and an IMF mandated fiscal squeeze. Yet real wages have not kept pace, leaving urban consumers highly price sensitive.

That backdrop has two implications:

1. Pricing power is fading. Colgate rode successive price rises between FY22 and FY24 to protect margins, but competitive intensity is rising as local rivals such as Hilal in toothpastes and FMCG upstarts in detergents undercut headline prices by 10–15%. Any further price moves risk eroding share.

2. Input cost tailwinds may reverse. Softening global palm oil and petroleum prices underpinned the margin recovery in FY24; however, international futures have rallied 18% since March 2025, and the rupee’s fragile equilibrium could wobble once the IMF programme winds down. A cost resurgence without commensurate pricing latitude would compress margins rapidly.

Management therefore confronts a familiar FMCG dilemma: stimulate volume growth through innovation and distribution width while defending profit pools. A probable playbook involves:

•Pack size engineering – pushing Rs10–20 sachets of Palmolive shampoo to capture down traders;

•Local sourcing – increasing the proportion of locally blown PET bottles and laminated tubes to hedge currency swings;

•Ad spend optimisation – reallocating bud‐gets from traditional TV to digital platforms where cost per reach is lower and shopper data more granular.

From a macro prudential standpoint, staples companies like Colgate serve as bell‐wethers of consumer health. Their perfor‐mance in FY24 underscores two realities: the elasticity of essential categories is not infinite, and even dominant brands must adapt when inflation outpaces incomes. While headline profits soared, the underlying growth engine — consumer volume — sputtered, hence the apt description of a “sluggish” year.

With inflation projected to stabilise near the State Bank’s 5–7% target range in FY26, analysts expect mid single digit real revenue growth for Colgate provided the company can reignite volumes through affordability plays and incremental innovations (e.g., enzyme based detergents, natural ingredient tooth‐paste). Yet execution risk is non trivial: failure to broaden the consumer base could see the margin gains of FY24 unwind swiftly. For now, the market will watch the first quarter FY25 update — due in late October — for ev‐idence that Colgate’s smile can widen beyond price‐led gains.

The solar glut is starting to have downstream impact, including on battery sales, which are driven in large part by the need for electricity storage during intermittency.

Profit Report

Exide Pakistan Limited (PSX: EXIDE) has posted a disappointing set of full year numbers for the 12 months ended 31 March 2025, under‐scoring how bruising price wars in the battery market are eroding both its top line and profitability.

Net sales slid 7% year on year to Rs23.9 billion, reversing the modest growth achieved in the previous two years. The pain was even more acute in the fourth quarter, where revenue tumbled 22% to Rs5.23 bn as Exide was forced to trim selling prices to match new, largely unlisted rivals.

The price cuts, coupled with volatile raw material costs, squeezed gross profit by 20% to Rs3.87 bn for the year, pushing the gross margin down from 19% to 16%. The margin compression was starker in 4Q, falling to just 12%, its lowest point in five years.

Operating profit shrank 41% to Rs1.89 bn, while profit after tax plummeted 51% to Rs614 million, leaving a wafer thin net margin of 3% versus 5% last year. Earn‐ings per share halved to Rs79.09, although the board maintained a dividend of Rs10 per share, signalling some confidence in cash flows.

A glance at the cost structure explains the pressure. Lead, which makes up roughly 65% of a conventional lead acid battery’s bill of materials, is sourced locally but benchmarked to London Metal Exchange prices. Domestic refiners raised quotes during FY25 to offset rupee deprecia‐tion and higher energy tariffs, narrowing Exide’s scope to defend margins through cost savings. The company has historically imported lead when domestic prices spike,

yet seaport congestion and elevated freight costs meant that option offered scant relief this year.

Selling and distribution expenses rose a hefty 20 pc, reflecting aggressive promo‐tional spending to hold shelf space against tax light grey market entrants. Administra‐tive expenses also ticked up on account of higher utility charges and an inflationary wage round. Conversely, finance costs de‐clined 15% as Exide pared back short term borrowings, but the saving was insufficient to offset the profit slide.

Management conceded during its post results briefing that the industry is “in the midst of a ferocious price reset” and hinted at a forthcoming rethink of channel incen‐tives. Analysts nevertheless warn that an‐other year of sub 20% gross margins would threaten dividend sustainability, especially if raw material volatility continues.

Exide’s product menu is wider than casual observers may realise, spanning both established lead acid formats and nascent lithium solutions:

Versatility is a double edged sword. Auto batteries can be repurposed for UPS or solar installations, yet Exide cautions that doing so “often leads to premature failure and warranty claims” because cycling re‐quirements differ. Still, in a pinch customers choose the cheapest watt hour available, amplifying the firm’s exposure to razor thin pricing in replacement markets.

Few industrial names in Pakistan boast a lineage as long as Exide’s. Incorpo‐rated in 1953 as a private limited company in partnership with the United Kingdom’s Chloride Group PLC, the venture brought modern battery technology to a young nation facing chronic power shortages. The firm listed on the Karachi Stock Exchange (now the Pakistan Stock Exchange) in 1982,

gradually indigenising key processes such as lead oxide milling, plate casting and polypropylene container moulding.

Throughout the 1990s Exide invested in maintenance free (MF) battery lines and expanded its Karachi manufacturing complex, securing eight Top 25 Companies awards from the bourse. The 2000s saw the launch of tall plate and tubular batteries tailored for UPS systems, a market that mushroomed alongside urban load shedding. In recent years, management has courted the telecom and renewable energy sectors, betting that the energy transition will spawn demand for stationary storage.

Yet the historical advantage of scale and brand equity is now under threat. Dozens of small scale assemblers operating on the periphery of the formal tax net are chipping away at Exide’s share by offering batteries 10–15% cheaper. The stakes are high: the firm employs over 1,600 workers and supports a supply chain of plastic moulders, lead recyclers and logistics providers. If profitability continues to erode, capital expenditure on lithium ion localisation could be deferred, placing Exide behind the technology curve just as electric mobility gains traction.

To understand why price competition has intensified, one must look beyond the battery factory gates to Pakistan’s rooftops. A surge in residential and commercial solar installations since 2023 has unleashed a wave of demand for storage solutions, but it has also flooded the market with cheaper imported alternatives.

•Solar panel imports more than doubled in 1H 2024, creating what industry insiders dub a “panel glut” that spilt over into related equipment, including lead acid and lithium batteries.

Product family

Automotive starter batteries (12V SLI, MF, heavy duty)

Tubular and tall plate batteries

Valve regulated lead–acid (VRLA) / AGM batteries

Industrial batteries & traction cells

Lithium ion batteries (imported for now)

•Weak regulation allowed containers of off spec Chinese batteries, originally destined for African markets, to be re routed to Port Qasim, undercutting domestic assemblers by up to 20 pc. Retail surveys in April 2025 recorded “massive” price drops in both tubular and lithium batteries, with tubular units falling from Rs70,000 to Rs55,000 within weeks.

•The fall in hardware prices has fuelled yet more rooftop uptake: the World Economic Forum notes that Pakistan’s “unstable electricity grid has driven a boom in private adoption of solar power”, further altering demand patterns for grid electricity and storage.

Paradoxically, while overall battery volumes have risen, value destruction is rife

End use segments

Passenger cars, trucks, tractors, motorcycles

Un interruptible power supply (UPS), home inverters, small scale solar storage

Telecom towers, data centres

Forklifts, locomotives, forklifts

Electric 2 wheelers, solar hybrid inverters

Competitive dynamics

Margins under siege from low cost local brands; volumes subdued as national vehicle assembly hovers below 300,000 units per annum (auto contributes <5% of sales).

Main revenue driver but highly price elastic; substitution risk from Chinese VRLA imports.

Sticky B2B contracts but slower roll outs of 5G towers curbed demand.

Niche but higher margin; order flow lumpy.

Pilot volumes; Exide plans local assembly “once commercial viability is proven”, likely post 2026.

because most of the incremental demand is met by lower priced imports or tax advantaged informal producers. Exide, as a compliant listed entity, bears the full weight of sales tax, corporate income tax and environmental levies, limiting its ability to match the rock bottom prices flashing across Lahore’s Hall Road and Karachi’s Jodia Bazaar.

The macro backdrop adds another twist. With net metering cutting household electricity bills, the national grid is witnessing a gradual dip in peak demand. A recent report by the Institute for Energy Economics & Financial Analysis projects that widespread adoption of battery energy storage systems could shave grid demand by up to 8.4% in the medium term, reducing the urgency for large scale battery replacement in telecom and industrial backup systems.

Exide’s management believes that pivoting to lithium cells and capitalising on the nascent electric vehicle wave will rejuvenate growth. Yet that transition requires heavy upfront investment in cell assembly, battery management systems and safety certification — expenditure that current margins cannot comfortably fund. Until price discipline returns to the lead acid segment, Exide may have to tread water through cost optimisation and selective outsourcing of lead to cheaper foreign smelters.

For investors, the FY25 scorecard is a stark reminder that brand heritage offers limited shelter when global commodity cycles and policy fuelled energy transitions collide. Exide’s next act will hinge on whether it can turn the very forces undermining its legacy business — cheaper solar and changing energy economics — into catalysts for a new generation of higher value storage products. n

CONSUMER GOODS

As the war continues at TRG, it seems the victor will rule over ashes

In the battle of the giants, the biggest losers are the investors in the company

By Zain Naeem

The searing heat of Karachi. The humidity only makes it worse. A man stands looking at the gigantic screen where the share prices are being displayed outside the stock exchange. He can walk into the air conditioned lobby but he does not have the strength or the motivation to do so. His eyes are transfixed on the price of TRG as it keeps plummeting.

He feels like he has been hoodwinked by the market but the tragedy is that he has fallen prey to two giants who are crushing the pawns that come in their path. He holds in his hand

his latest portfolio of his investments. As the sweat drips from his arms, the paper is becoming as worthless as the investments that are printed on it. As the two sides wage their war, the ones who have lost the most are investors who were sold a castle of sand and glass. The castle that is coming down crumbling in front of their eyes.

The rise before the fall

TRG used to be the darling of many at the market in its past. Only four years ago, the company was considered to be an amazing investment. The share price was hovering around Rs 182 and it

seemed like the company could do no wrong. The volume of shares being traded was one of the highest in the exchange and the financial results backed the market confidence as the company had just announced a cash dividend of Rs 4.4 at the end of its third quarter.

The dividend was supported by the fact that the company had just earned Rs 47.4 per share at the end of its financial year and then gave out another cash dividend of Rs 4.4 per share at the end of its first quarter for the next year.

The prospects of the company made it a favourite for many of the brokerage houses who could not stop showering praises. TRG was considered one of the rising stars in the technology sector as it was growing at a fast

pace in comparison to its competitors.

The engine driving the growth of the company was Zia Chishti. Chishti had a background in investment banking before he decided to invent Invisalign braces and founded Afinit. Afiniti had started off as a calling centre before it started to pioneer AI in order to increase efficiency of its call centre operations.

TRG was structured in such a way which meant that Chishti was able to control Afiniti by having its shareholding held by TRG Pakistan. TRG Pakistan was established way back in 2002 in order to act as a holding company which oversaw several investments being carried out under it. It was expected that the party was going to continue long into the future as there was confidence in the man and his golden touch. Until finally the music stopped.

The fall from grace

Just like the rise was meteoric, the fall seemed to be just as spectacular. In November of 2021, allegations surfaced against Chishti accusing him of a sexual assault against an employee. Seeing the damage to his reputation and impact on the company, Chishti stepped down from Afiniti and then TRG. The fall was complete when he was booted out of the board of directors as well when elections were held in January of 2022.

This should have been an end of the whole ordeal as the new company could be managed and run by a new board of directors who could navigate the choppy waters and bring the company on the other side unscathed. But Chishti was not going to take this lying down. What started after this was a war that continues to this day as the two sides are involved in a tug of war to gain control of the company totally and completely.

Staging a comeback

As Zia stepped down, he started his efforts to do all that he could to wrest back control from the new board of directors. As he was battling the allegations in court, he could not do anything overtly in order to keep the spotlight away from him. His first move was to try to buy shares of TRG from the market in conjunction with JS Group which would constitute a hostile takeover. Zia already had a huge amount of shareholding in his own account and he wanted to join together with the JS Group in order to stay below the radar while accumulating more shares.

The management at TRG saw what was happening and approached the courts to stop JS Group from buying more shares. The rationale used was that JS Group was an associate company and had to disclose when they bought additional shares of TRG which they had not done. The lawsuit also alleged that the

JS Group in conjunction with Chishti had 34% of the shareholding when they should have made a public offer that they did not do.

The court sided with the management and barred JS Group from buying any additional shares and also stopped them from exercising any voting rights that they had that exceeded the 30% threshold. The court also stopped Chishti from setting up third party interest with his own and his wife’s shareholding which would facilitate a hostile takeover as well.

As the courts had gotten involved, there was also a move to malign the reputation of the board of directors by carrying out alleged social media campaigns. TRG Pakistan started to bat away these claims with regular notices being sent to the exchange stating that these allegations were baseless. Seeing most of his efforts failing, Chishti then took out an ad in the newspapers against the company alleging that directors were involved in malpractises and were destroying the company and its value.

One claim that was made in the ad was that Afiniti and Ibex were two investments of TRG Pakistan which were not being managed well and were losing value. Rather than focusing on the company, TRG Pakistan was using its own funds to buy shares through an opaque subsidiary by the name of Greentree Holdings Limited. By doing so, the board of directors at TRG were looking to mop extra shares available in the market and consolidate its own holdings against Chishti and his attempts to takeover.

The claim held some weight as Greentree held only 1 share at the end of June 2021 which increased to 156 million shares or 28.54 percent of the company’s shareholding in a span of 2 years.

In reply to the ad, the management did not contend the claim that was being made against Greentree Holdings but did say that Chishti coming back to the company would damage the value and brand of the company. The allegations being made against Chishti seemed to be far more damaging in the current climate and the best course of action was for the management to stay and improve the situation at the company.

The most recent developments

By the end of December 2024, the war became hot again as both sides started to strengthen their defences. On one hand, Greentree Holdings issued a public offer where they were willing to buy 35.1% additional shares of the company which would take their total shareholding to 63.64%. The move was mandated by the fact that TRG Pakistan had to hold elections which are stipulated by laws and regulations to be carried out within 3 years from the last ones. As the last

ones had been held in January 2022, the next elections had to be carried out by January of 2025.

The greater the shareholding that was held, the more power there would be to elect a board of directors. By having more than 60% of the shares, Greentree would be able to elect a majority of directors on the board.

While the two sides fought with each other, the losses started to pile up. By now, TRG Pakistan was solely a shell of a company with most of its investments residing in Afiniti. In the Financial Year 2023-2024, TRG saw its losses piling up. At September end, loss per share stood at Rs 15.7 which increased to Rs 19.4 by December end, Rs 30.7 by March end and Rs 56.6 by the end of the year.